(Lecture notes for the Week 2 Second Session, Wednesday, 2/19/14) Introductory Pricing/Marketing Workshop for Grains, On-Line

Review

Breakeven Basis

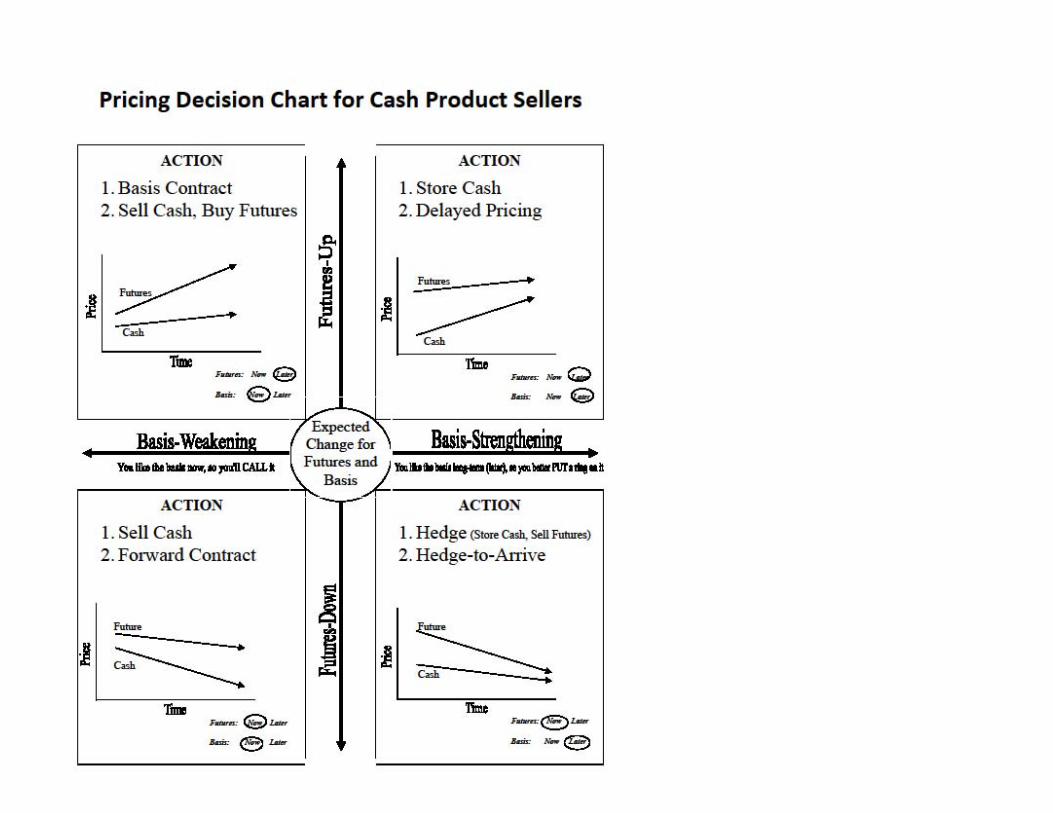

First four pricing tools

Continue with

With three more pricing tools

New

Begin Commodity Options

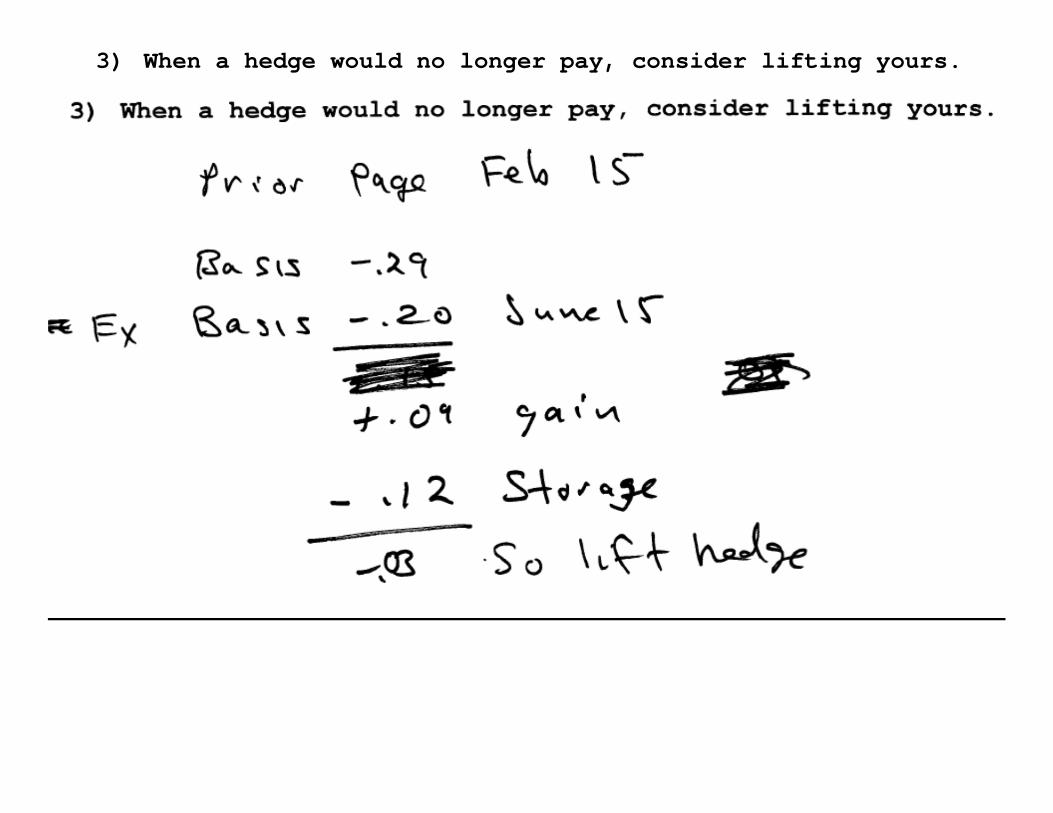

Breakeven Basis, when do you lift a Hedge?

Break-Even Basis Line helps us answer two questions.

1) Should we hedge? a. Basis needs to be weaker than the B-E Basis Line to consider hedging.

2) When to get out of/lift the hedge? a. When basis strengthens to B-E Basis, consider lifting hedge.

3) When a hedge would no longer pay, consider lifting yours.

3) When a hedge would no longer pay, consider lifting yours.

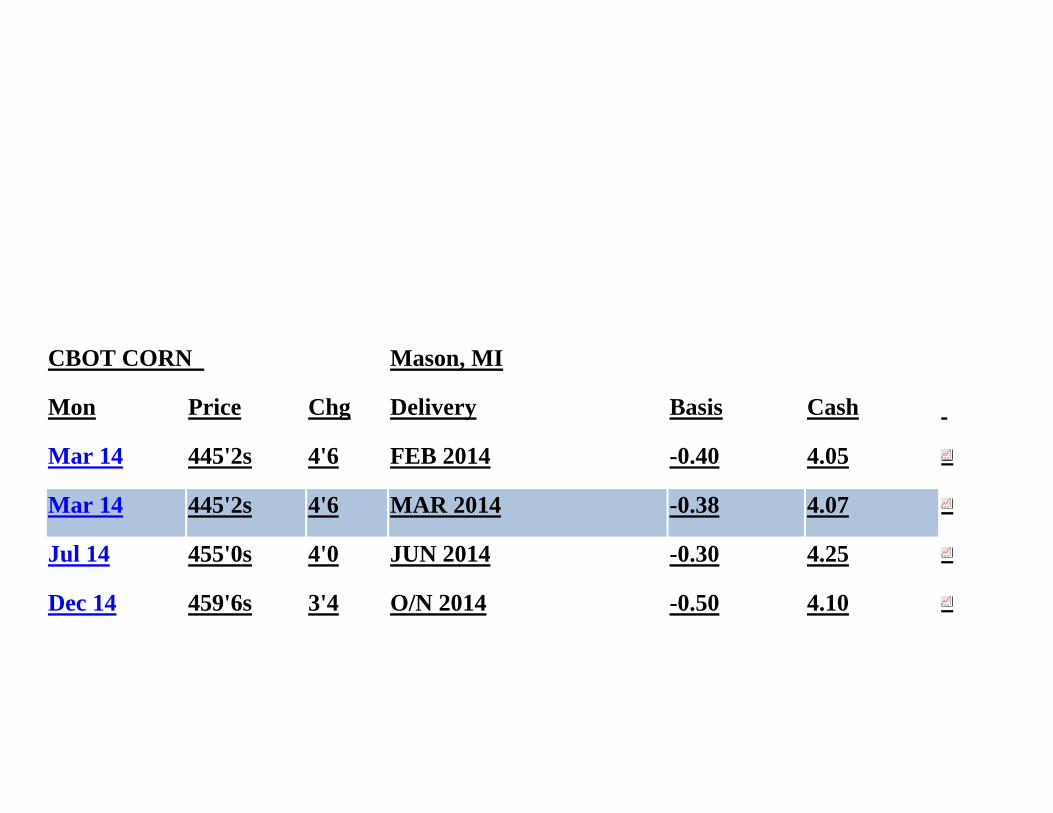

CBOT CORN Mason, MI

Mon Price Chg Delivery Basis Cash

Mar 14 445'2s 4'6 FEB 2014 -0.40 4.05

Mar 14 445'2s 4'6 MAR 2014 -0.38 4.07

Jul 14 455'0s 4'0 JUN 2014 -0.30 4.25

Dec 14 459'6s 3'4 O/N 2014 -0.50 4.10

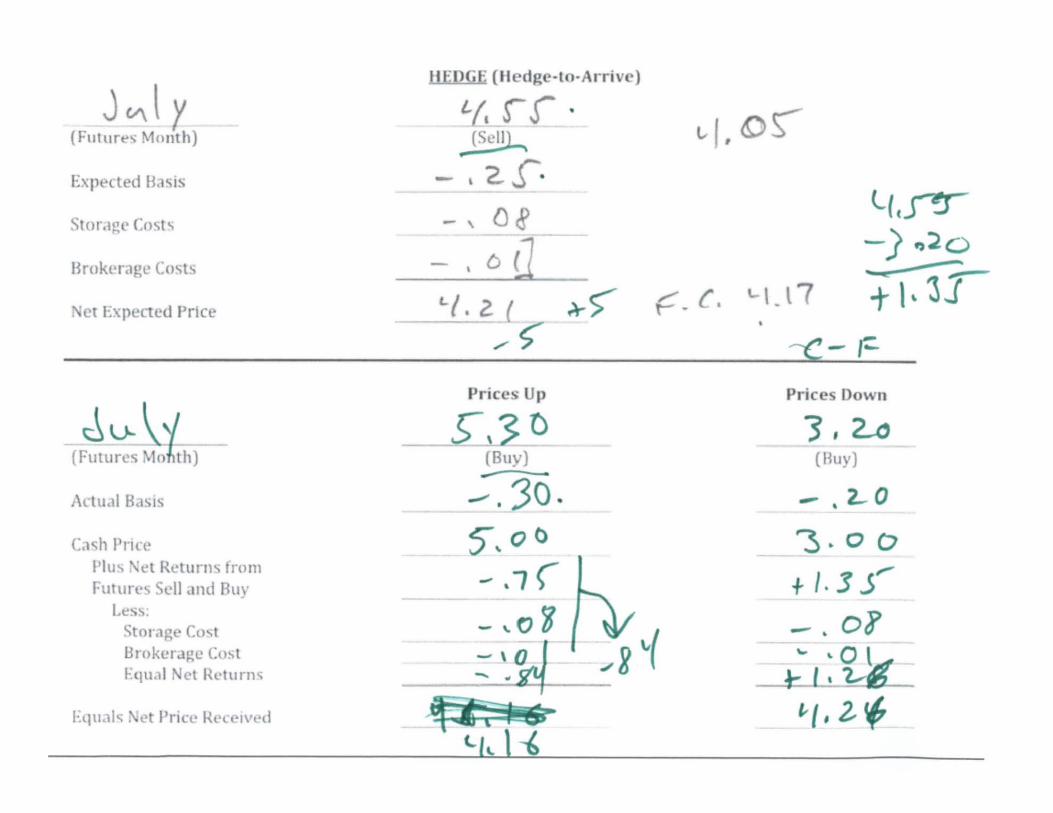

HEDGE(Hedge‐to‐Arrive)

PricesUp

PricesDown

(FuturesMonth) (Buy) (Buy)ActualBasis

CashPrice PlusNetReturnsfromFuturesSellandBuy

Less: StorageCost BrokerageCost EqualNetReturns EqualsNetPriceReceived

(FuturesMonth) (Sell)ExpectedBasis

StorageCosts

BrokerageCosts

NetExpectedPrice

BASIS CONTRACT (Futures Month) (Price) Less: Cash Price

(Deliver Cash) Basis Contract ____________

Prices Up Prices Down (Futures Month) (Price) (Price) Less: Basis Contract Equals Net Price Received

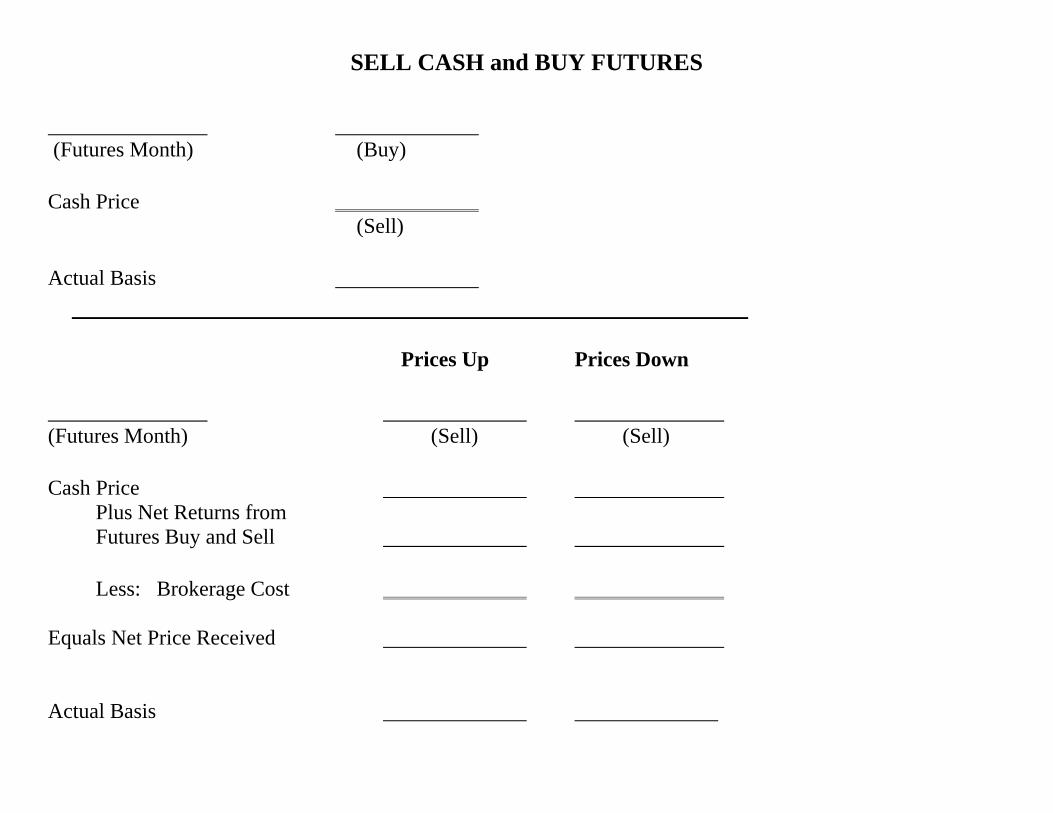

SELL CASH and BUY FUTURES

SELL CASH and BUY FUTURES (Futures Month) (Buy) Cash Price

(Sell) Actual Basis

Prices Up Prices Down (Futures Month) (Sell) (Sell)

Cash Price Plus Net Returns from

Futures Buy and Sell

Less: Brokerage Cost Equals Net Price Received Actual Basis

Problem, the basis is predictable, prices are generally not

I

· .

INSURANCE

Substitution of a small but

certain loss (insurance premium)

for the possibility of. a large .

uncertain loss.

""

/'

, .' t t, '

....\.~.

'.

COMMODITY OPTIONS

MARKET

Market in which producers may

purchase the "opportunity" but 'not thei= / ...j r_ "'}'\. 1...--1- ('-...., r ...", '.

"obligation" to· sell' or buy a C6mmed·~

,at a certain price.

"

l ) I \

ww

00

--

a:a:

a.a.

(J)C

'C

'Z

Zt-

--

~~~.

W...I

>~

...I:::)

~"

a:w

£D.<C

(J)':E

)

~~

C'

~C'

0Z

·Z

---\

.3=-

a:a:

:::)t-

:::)(J)

(J)Z

Z- ~

-~

~~.

I.I

_...~, ..

Want rigl't,t to sell corn for S3.00/bu.

Purchase right in options market by a remium

If price when ready to

sell is above S3.00

- sell for higher price

.If price is below $3.00

- "collect on policy"

.. (I I J

I'. . I J

-0'

_0

.CALL OPTION .

--A contract that gives the holder the °

right to b\.lY_at a specifiedprice_. .. " ..-". .

° "To call- from them"o

- !I \

-/ ) ). \ -I

)

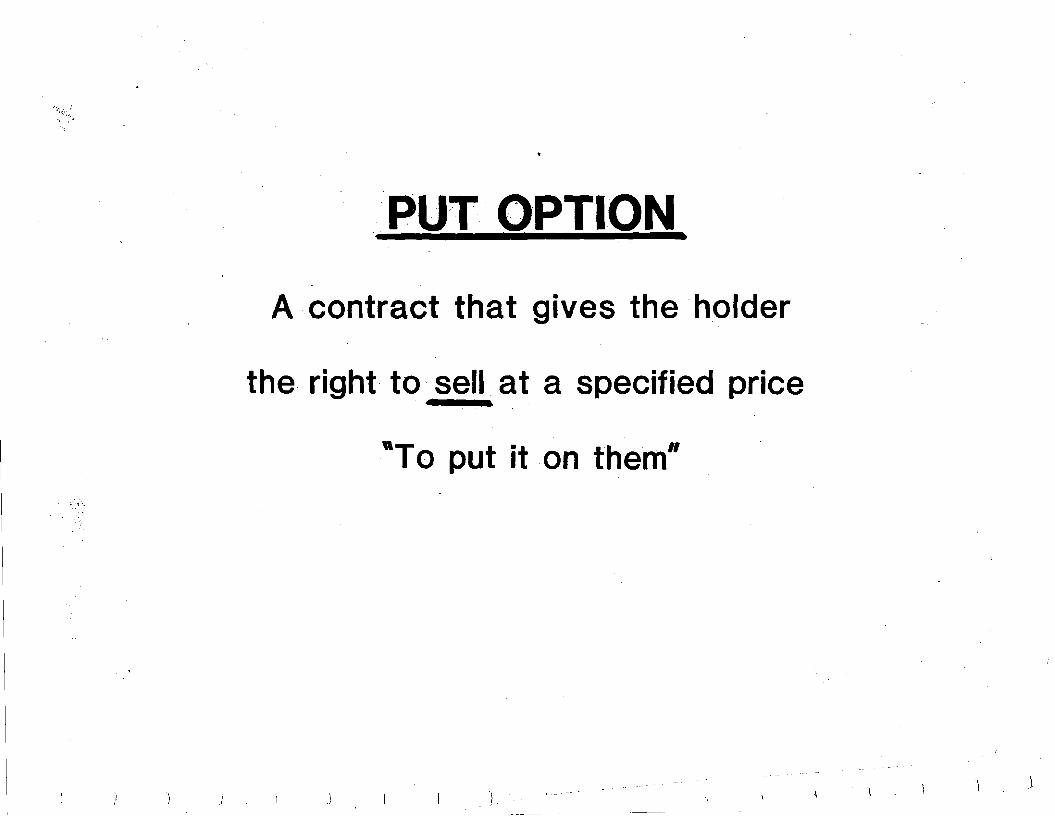

PUT·' OPTION

A contract that gives the ·holder

the· right to sell at a specified price

"T0 put it on them"

t ." \1 \

z0-t-

t-o.en

0a::

zw

-<C:c

Wt-

t->-----

CO>-

::Ja::0

COD

]W0

c.

C:c

wZ

...I~.

>-0

0w

z>

-:I:0

z1-..........,

en0

C.

a:()

i

W

i~

0,

a.en

i"i

t-i

__

-.

W:c

:c(!'

t--cc·

..~

00

.W

IJ:

..J:

I-S2

(J)a:

..JW

I..J

:e

wI-

z(J

)·oo

-I-

Co:c

zW

::«a:

..~«Z

(!'t-

OC

oZ,

(J)Z

a:~

(Jw

~

a..z

wQ

:el-

I-a..o

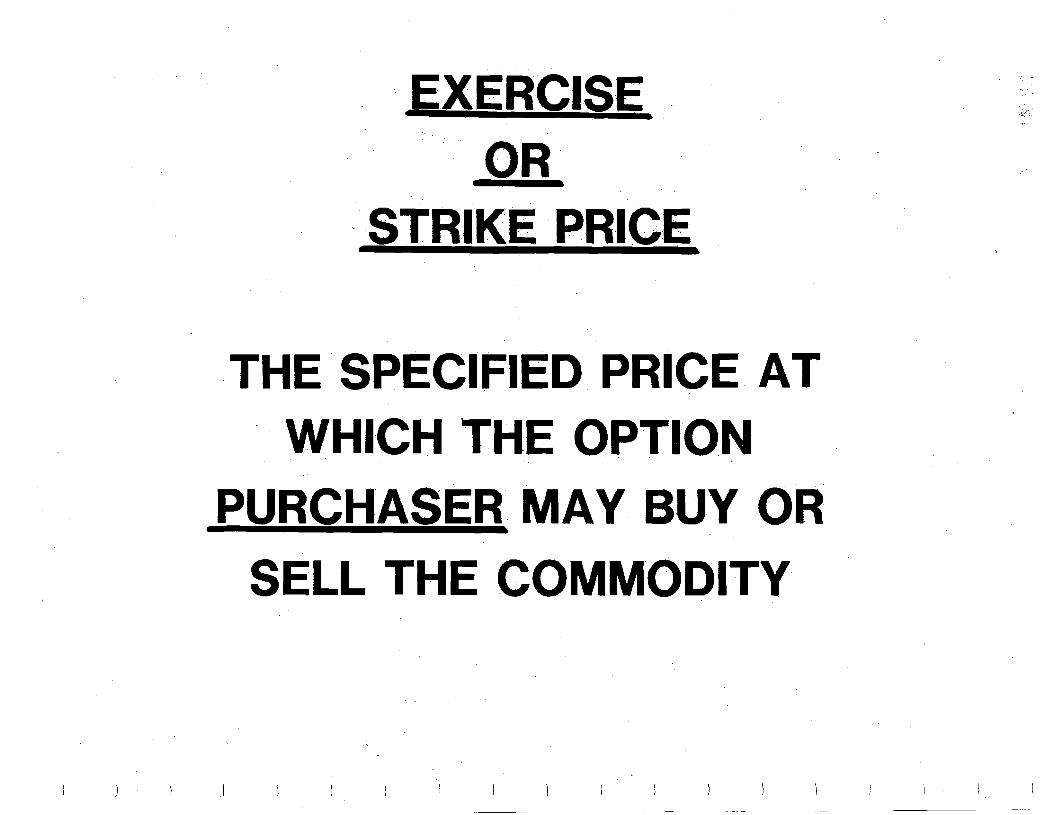

·EXERCISE .... OR

-STRIKE PRICE .

·THE .SPECIFIED PRICE AT

- WHICH THE OPTION

PURCHASER MAY BUY OR

SELL THE COMMODITY

'A':::,'

) ) \ I I \ I I j i ~ I I I I ) I

enw>

t%:

W1

-..::)

:r:.-C

'l-

I-e

·z::)

l-e

-U

.~

>0

..I<C

:Ez

t%:

ew

en~

I-0

e-

0z

>..I

<C::)

.1-<C

cc-

0e

wl-

e-

::E:Z

enI-

~0

>:E

0:r:D

.e0

UJ::J:'I-

Z::J:

Qo

I-

D.

::J:0

3=wz

::I:0

'1-

D.

LL':::J

0W

(J)I-

Ic

(::J:

CCJ'-

Wa:

::J:'I-

:E'

::),-':EW1:1:'0

.Zo-,I-0

.o

w::)'•

..Jz·.<C

0>

-I-~

WO

~w

I:I:::J:~I-W

LL::J:0

.I-

LLoW~

o~

_W

1:1:0

o.Z

w<

C::J:I:I:I-~

Ii'

Z1

--

,0~

WW

LL

::J:L

LI

WZ-

.FAC'TORS AFFE~CTING, . .

.PREMIUMS·

- DIFFERENCE BETWEEN THE STRIKE.. . ..

t~· - PRICE OF THE OPTION AND THE PRICE.. . .

·0F THE UNDERLYING COMMODITY

- LENGTH.OF TIME TO EXPIRATION

\ I I ) I J J I

INTRINSIC VALUE .

.'1'

,,;..if

., \

f/'

i

i::~",

.i1i

"POSITIVE" DIFFERENCE BETWEEN

STRIKE PRICE AND UNDERLYING

COMMODITY PRICE

FOR A PUT - STRIKE PRICE EXCEEDS

- FUTURES PRICE

FOR A CALL - STRIKE PRICE BELOW

FUTURES PRICE/

/

~'. ,itT'

.~

:....... ,~. f·

/I

\

JlJ".11'3: ' ~.' .. l~'\. !".

" i~;~,

"~~

i~~~~).,.l I !

":i7rl,

-

•"?

-,W

W,;

::)::)

..J..J

c:ec:e

w>

>a:

0~

0c:e

>••

--

1-'W

enw

en-

InZ

ZZ

<CI

-0

-_.

:J:0

~a:

a:I

>:E

l-t-

l-I-

wI

WI

·zZ

-i

enz

'>J:

c-

-~:;

.-;

:J:...---

Z-

0W

0<C

I-0

:E>

en•

z-

,.<C

U.

'I-W

'0W

a.:J:

:J:>

0~

I-<C

,.::::)

Z:J:

0- ~

'I!'I!

""F i-4~i;-;'i,~~!f,~P'(, ;:".

:j..

TIME· VALUEi

J

PORTION OF OPTION pREMIUM

RESULTING FROM LENGTH OF.TIME TO EXPIRATION

USl»LLY T~ME VALUE DECREASES;.'~~~'

. WITH LENGTH OF TIME UNTILEXPIRATION,

!

1· I .1 . I I i I

z«IwenU.

U.

o

Wt

l-e:(Z

Co

--

::lI-

0Z

a.-

0o

...Ji=

C'

0CiS

ZI-

0i=

cc0

enw

..z-

cx

a:0

w0

i=z

.z0

e:(

-0

,

:Jb

.~.w

e:(I

ena:

ol-

1-.

Zo()

'"

"':'J."

.~.

MONEY FLOWSHolding a soybean $7.00 putpurchasec

for a $0. 15 premium

OFFSETCurrent futures price is $6.50 .

Sell option at a $0.60 premium

.RESULT

Offset premium received

- Original premium paid

Net returns

l.L-;\

$0.60

....0.15

$0.45",·t',:

zo-~0-oZc:ewen-o£

tW><W

ol-I-o«ccIZoozo-I--a..oz<CI-ccW>ZoooI--

Iw·

~0:

«~UJ

W-cc::>I::>LLWJ:-

I--Z-Zo-I--enoa..<C

,~

;.~.

MONEY.·FLOWS.

.Holding a soybean $7.00 put purchased

for a $0.15 premium

. . '. . .

.Current futures price' is $,6.50

Receive a short ·(sell) futures market

.position at $7.00". . "<. ~ ".

\ .\.<>...... .. . . . - .

~. '1"

" " ~::

Buy futures at $6.50 '>

RESULT

Futures gain

- Original premium paid .

Net· Returns

$0"··'. ijlDji

, ~O~1~&J·

'$0::35."'.