EVOLVING CONSUMER PREFERENCES – Challenging Opportunities

Key Issues Affecting the U.S. Light Vehicle Market

George M. MaglianoDirector of Automotive Industry Research, Americas

Detroit, 6 October 2005

Copyright ® 2005 Global Insight, Inc. 22005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

Despite Katrina, economy remains robustThe job market has turned aroundOil prices remain major risk in the environmentWhile FED raises interest rates aggressively, overall increase is modestDemographic underpinning to market is solidGeneration mix provides opportunities and threatsPayback for July and ending of employee deals already factored into last month’s forecastImpact of Katrina and higher oil and gasoline prices costs market @ 100,000 to 200,000 units moreInventory rose modestly in August, but is still in line

Economic and Market Overview

Copyright ® 2005 Global Insight, Inc. 32005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

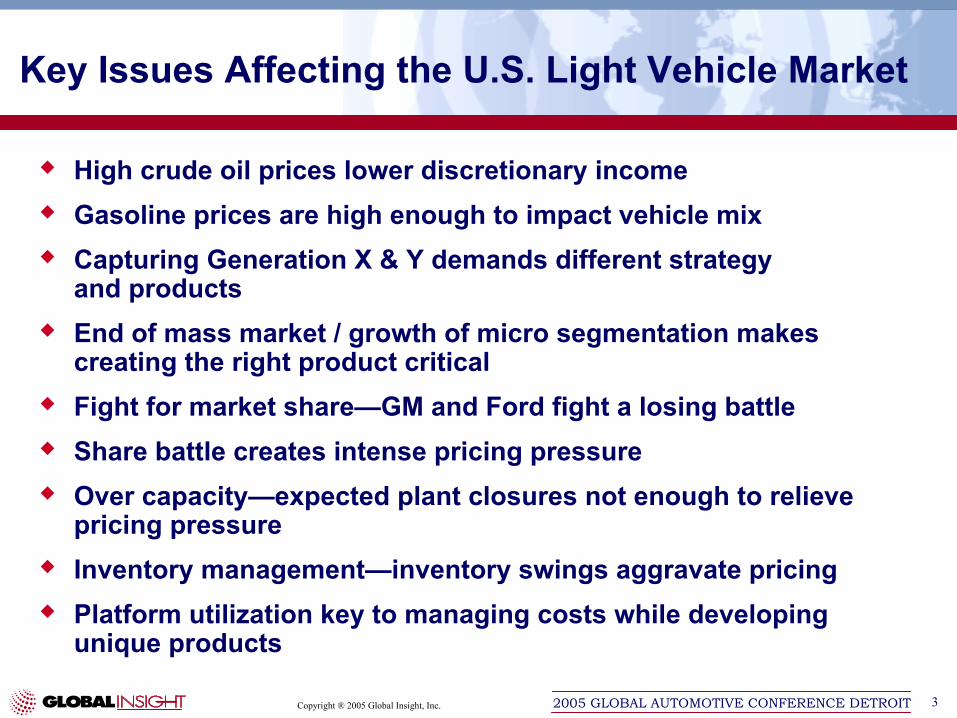

Key Issues Affecting the U.S. Light Vehicle Market

High crude oil prices lower discretionary incomeGasoline prices are high enough to impact vehicle mixCapturing Generation X & Y demands different strategy and productsEnd of mass market / growth of micro segmentation makes creating the right product criticalFight for market share—GM and Ford fight a losing battleShare battle creates intense pricing pressure Over capacity—expected plant closures not enough to relieve pricing pressure Inventory management—inventory swings aggravate pricingPlatform utilization key to managing costs while developing unique products

Copyright ® 2005 Global Insight, Inc. 42005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

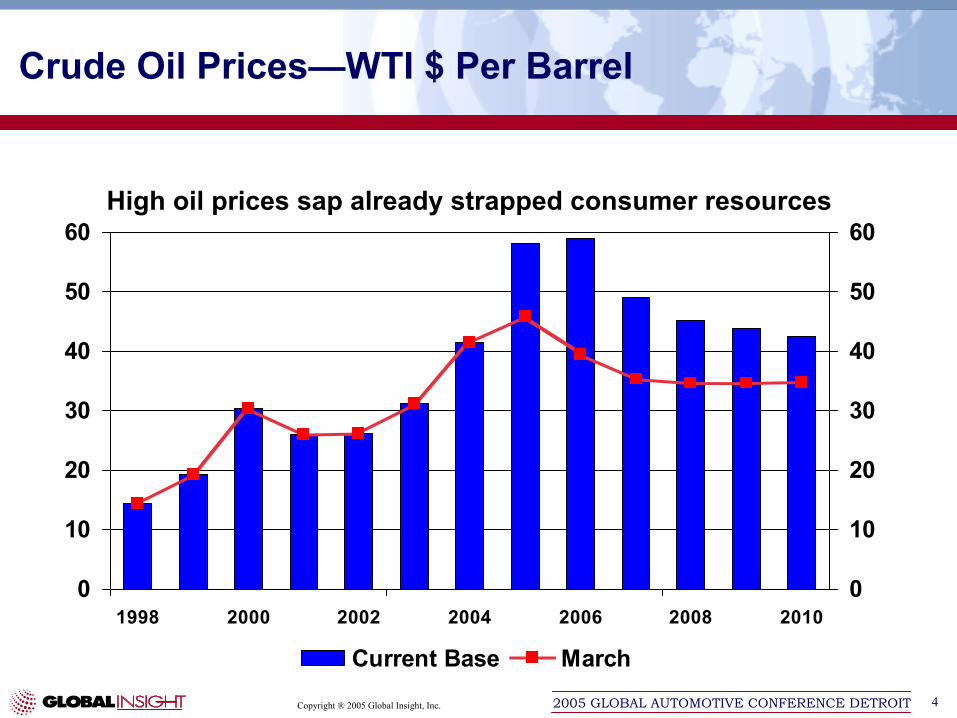

Crude Oil Prices—WTI $ Per Barrel

0

10

20

30

40

50

60

1998 2000 2002 2004 2006 2008 20100

10

20

30

40

50

60

Current Base March

High oil prices sap already strapped consumer resources

Copyright ® 2005 Global Insight, Inc. 52005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

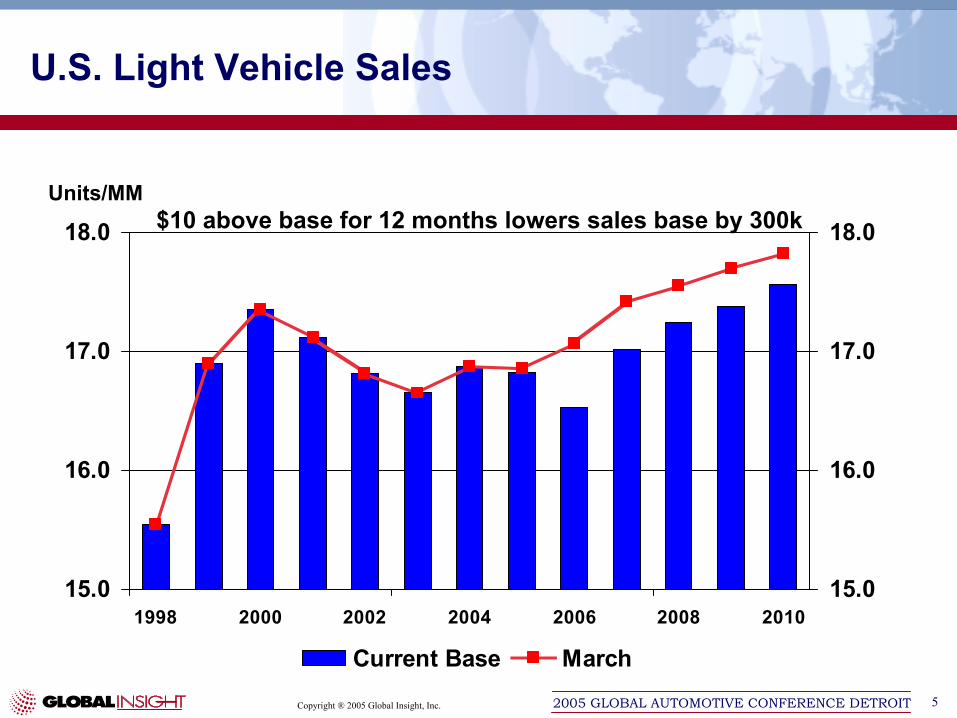

U.S. Light Vehicle Sales

15.0

16.0

17.0

18.0

1998 2000 2002 2004 2006 2008 201015.0

16.0

17.0

18.0

Current Base March

Units/MM$10 above base for 12 months lowers sales base by 300k

Copyright ® 2005 Global Insight, Inc. 62005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

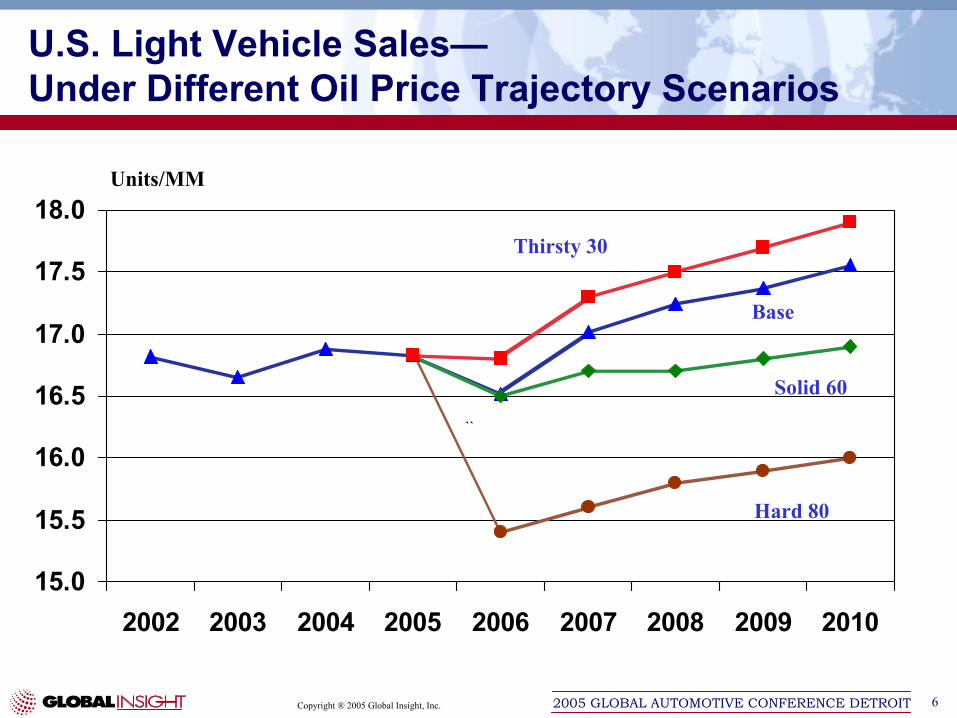

U.S. Light Vehicle Sales—Under Different Oil Price Trajectory Scenarios

15.0

15.5

16.0

16.5

17.0

17.5

18.0

2002 2003 2004 2005 2006 2007 2008 2009 2010

``

Hard 80

Thirsty 30

Solid 60

Base

Units/MM

Copyright ® 2005 Global Insight, Inc. 72005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

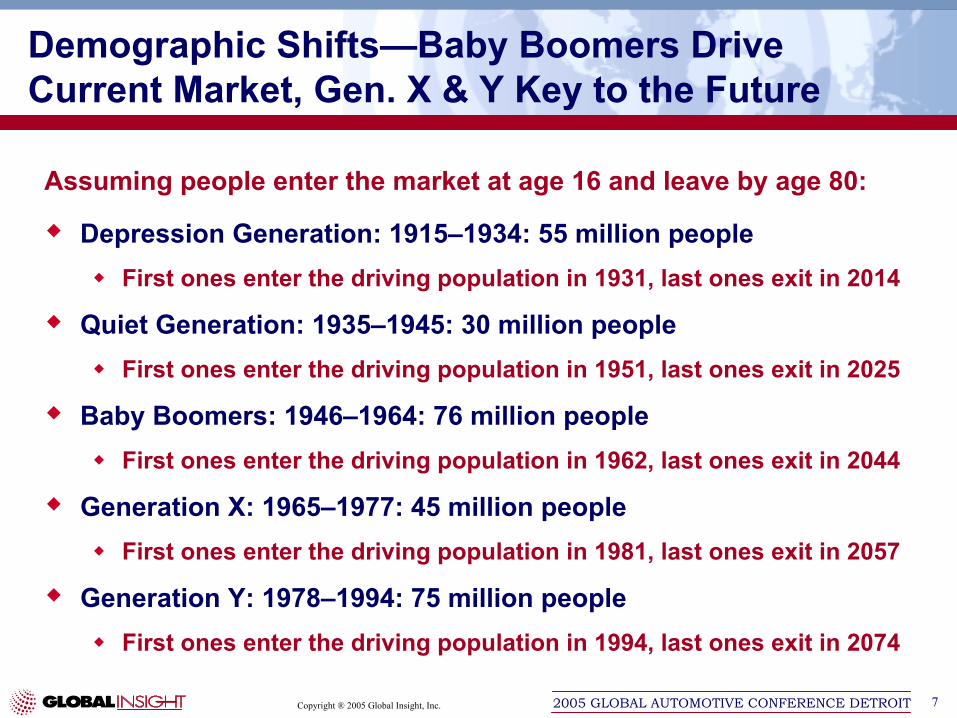

Assuming people enter the market at age 16 and leave by age 80:

Depression Generation: 1915–1934: 55 million peopleFirst ones enter the driving population in 1931, last ones exit in 2014

Quiet Generation: 1935–1945: 30 million peopleFirst ones enter the driving population in 1951, last ones exit in 2025

Baby Boomers: 1946–1964: 76 million peopleFirst ones enter the driving population in 1962, last ones exit in 2044

Generation X: 1965–1977: 45 million peopleFirst ones enter the driving population in 1981, last ones exit in 2057

Generation Y: 1978–1994: 75 million peopleFirst ones enter the driving population in 1994, last ones exit in 2074

Demographic Shifts—Baby Boomers Drive Current Market, Gen. X & Y Key to the Future

Copyright ® 2005 Global Insight, Inc. 82005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

37

39

41

43

45

47

49

1989 1991 1993 1995 1997 1999 2001 2003 2005

CNW Marketing - Months

(Years)

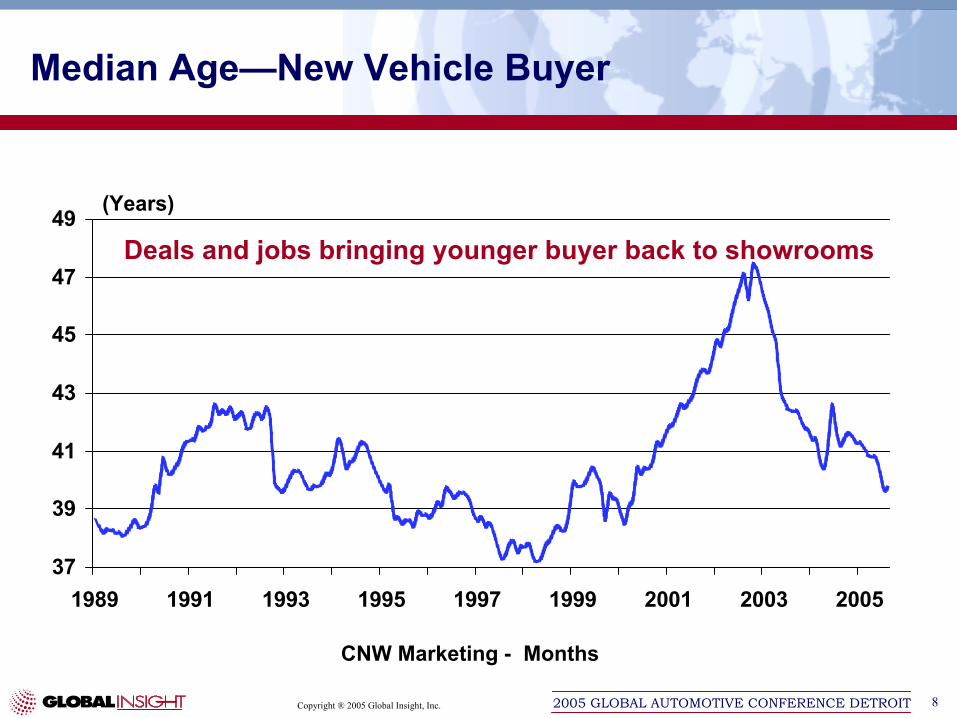

Median Age—New Vehicle Buyer

Deals and jobs bringing younger buyer back to showrooms

Copyright ® 2005 Global Insight, Inc. 92005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

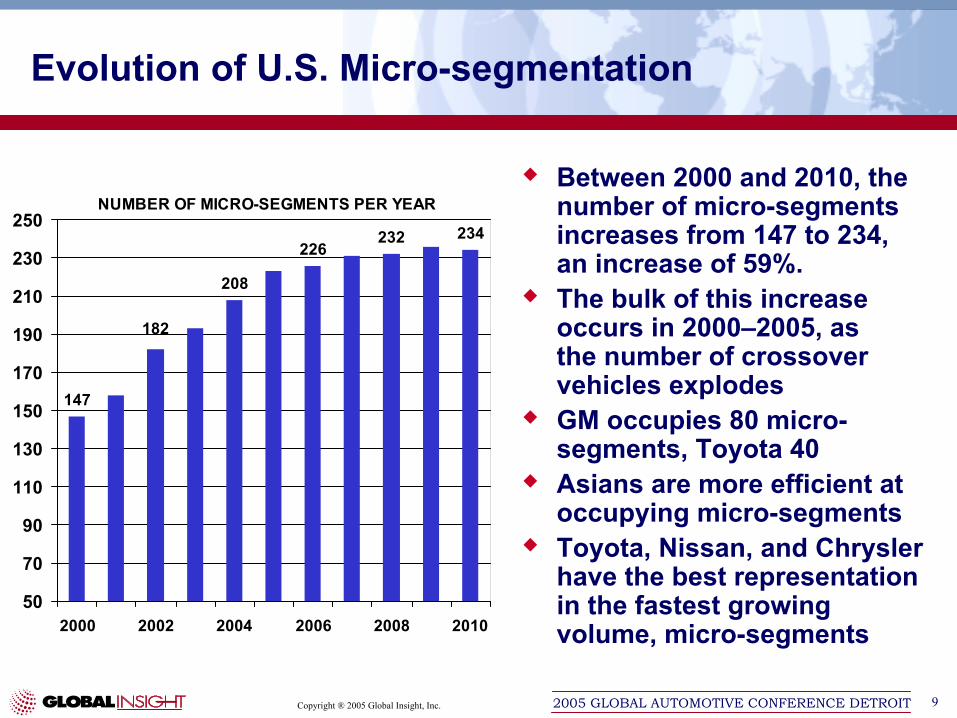

NUMBER OF MICRO-SEGMENTS PER YEAR

147

208

226232 234

182

50

70

90

110

130

150

170

190

210

230

250

2000 2002 2004 2006 2008 2010

Evolution of U.S. Micro-segmentation

Between 2000 and 2010, the number of micro-segments increases from 147 to 234, an increase of 59%. The bulk of this increase occurs in 2000–2005, as the number of crossover vehicles explodesGM occupies 80 micro-segments, Toyota 40Asians are more efficient at occupying micro-segmentsToyota, Nissan, and Chrysler have the best representation in the fastest growing volume, micro-segments

Copyright ® 2005 Global Insight, Inc. 102005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

2.0

3.0

4.0

5.0

6.0

7.0

2000 2002 2004 2006 2008 201010%

15%

20%

25%

30%

35%

40%

Volume - L Market Share - R

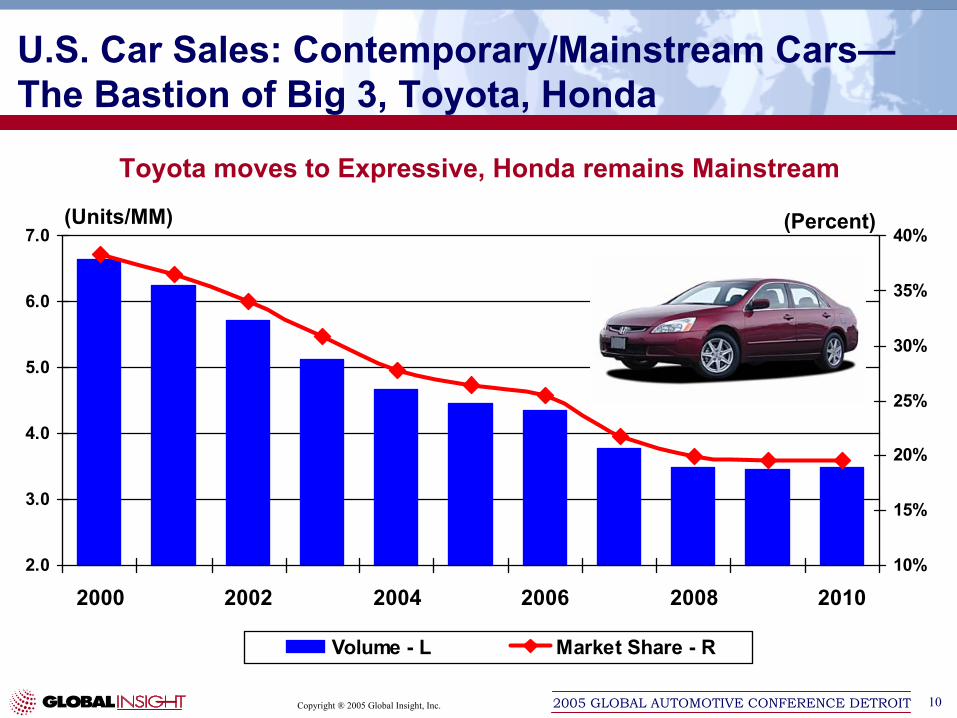

(Units/MM) (Percent)

U.S. Car Sales: Contemporary/Mainstream Cars—The Bastion of Big 3, Toyota, Honda

Toyota moves to Expressive, Honda remains Mainstream

Copyright ® 2005 Global Insight, Inc. 112005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.400

2003 2005 2007 20090.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Volume - L Market Share - R

(Units/MM) (Percent)

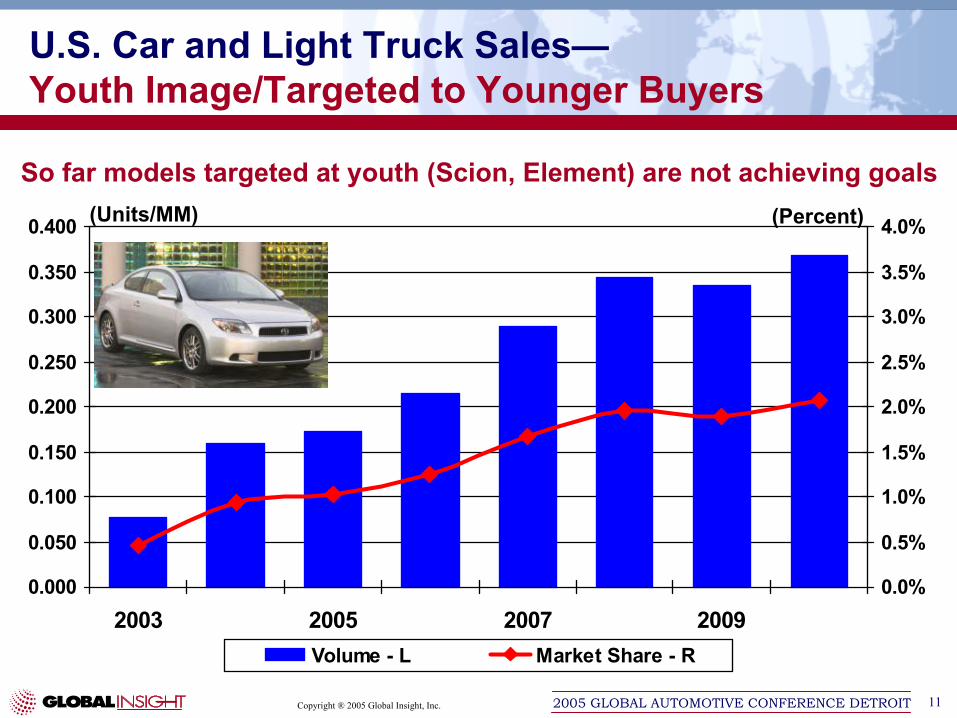

U.S. Car and Light Truck Sales—Youth Image/Targeted to Younger Buyers

So far models targeted at youth (Scion, Element) are not achieving goals

Copyright ® 2005 Global Insight, Inc. 122005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

0.0

1.0

2.0

3.0

4.0

5.0

2000 2002 2004 2006 2008 20100%

5%

10%

15%

20%

25%

30%

Volume - L Market Share - R

(Units/MM) (Percent)

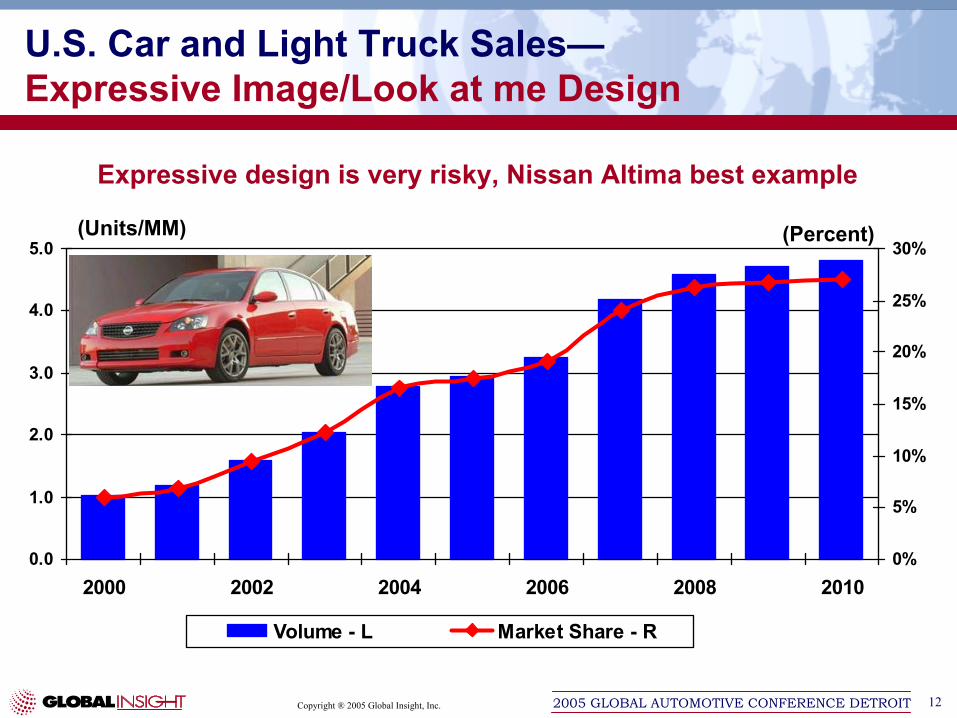

U.S. Car and Light Truck Sales—Expressive Image/Look at me Design

Expressive design is very risky, Nissan Altima best example

Copyright ® 2005 Global Insight, Inc. 132005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

8.5

9.5

10.5

11.5

12.5

13.5

14.5

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05

Months

(Units in millions)

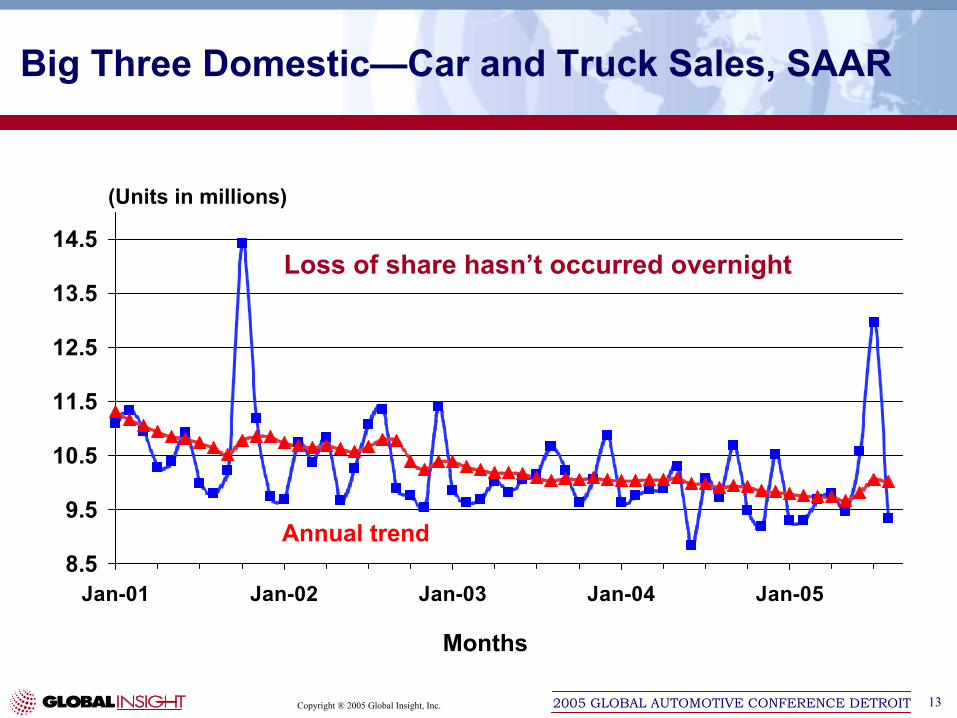

Big Three Domestic—Car and Truck Sales, SAAR

Annual trend

Loss of share hasn’t occurred overnight

Copyright ® 2005 Global Insight, Inc. 142005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

6.0

6.5

7.0

7.5

8.0

Dec-00 Dec-01 Dec-02 Dec-03 Dec-04

Months

(Units in millions)

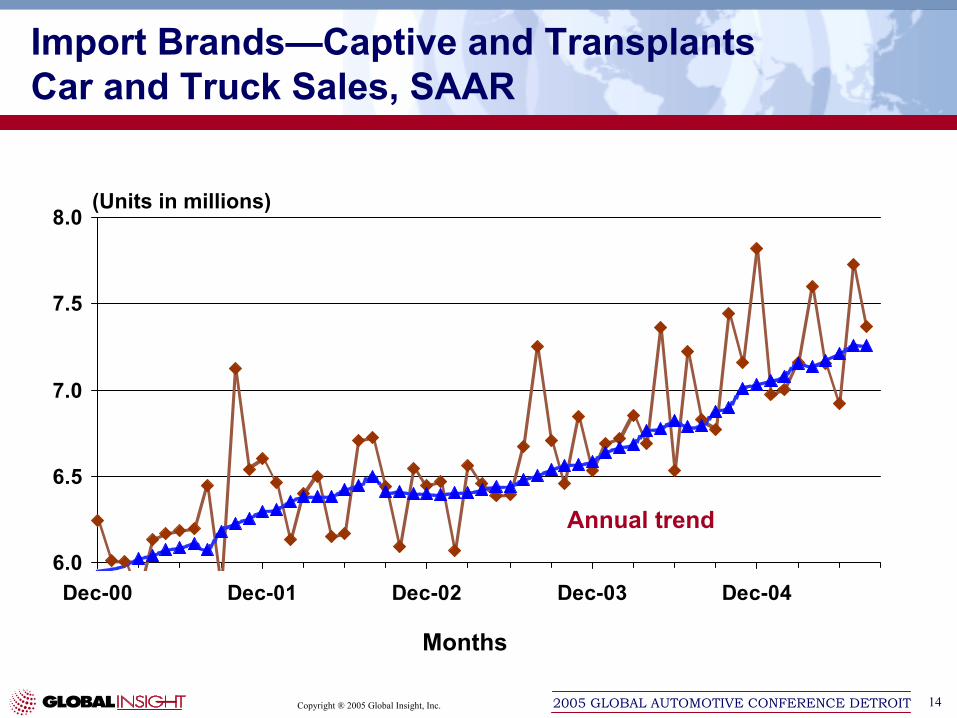

Import Brands—Captive and TransplantsCar and Truck Sales, SAAR

Annual trend

Copyright ® 2005 Global Insight, Inc. 152005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

55

60

65

70

75

80

2001 2002 2003 2004 2005

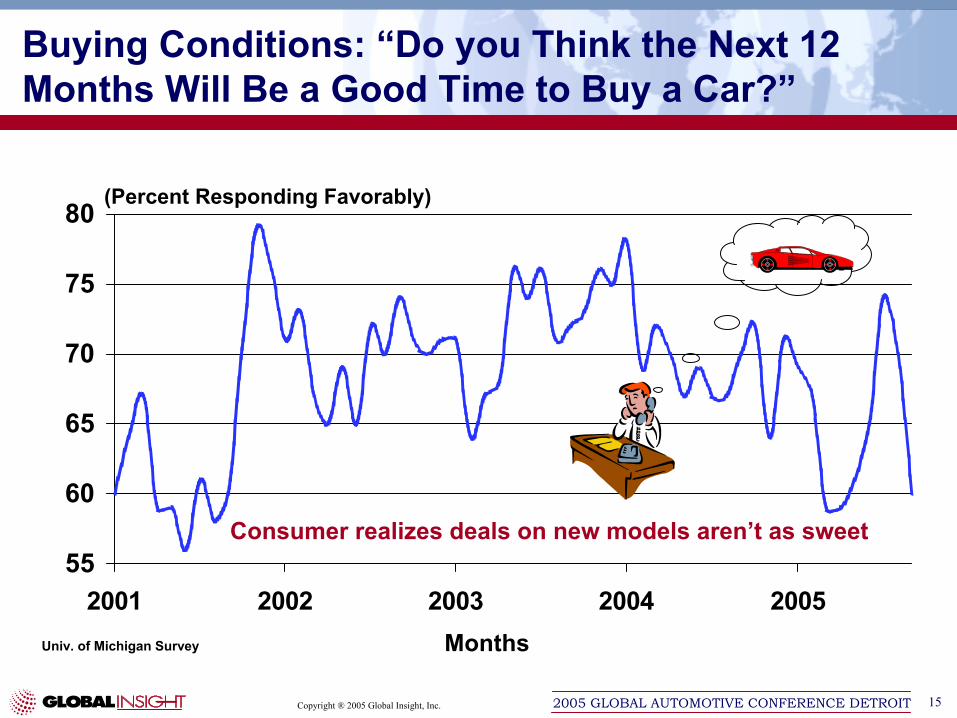

(Percent Responding Favorably)

Univ. of Michigan Survey Months

Buying Conditions: “Do you Think the Next 12 Months Will Be a Good Time to Buy a Car?”

Consumer realizes deals on new models aren’t as sweet

Copyright ® 2005 Global Insight, Inc. 162005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

10

12

14

16

18

20

1999 2000 2001 2002 2003 2004 2005

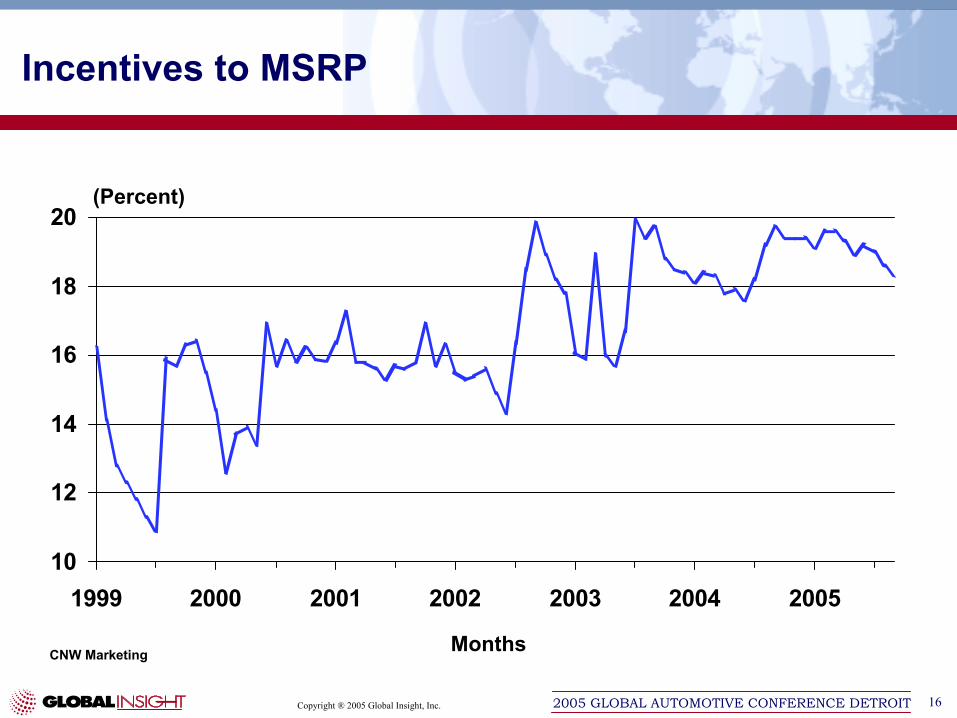

(Percent)

CNW Marketing Months

Incentives to MSRP

Copyright ® 2005 Global Insight, Inc. 172005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

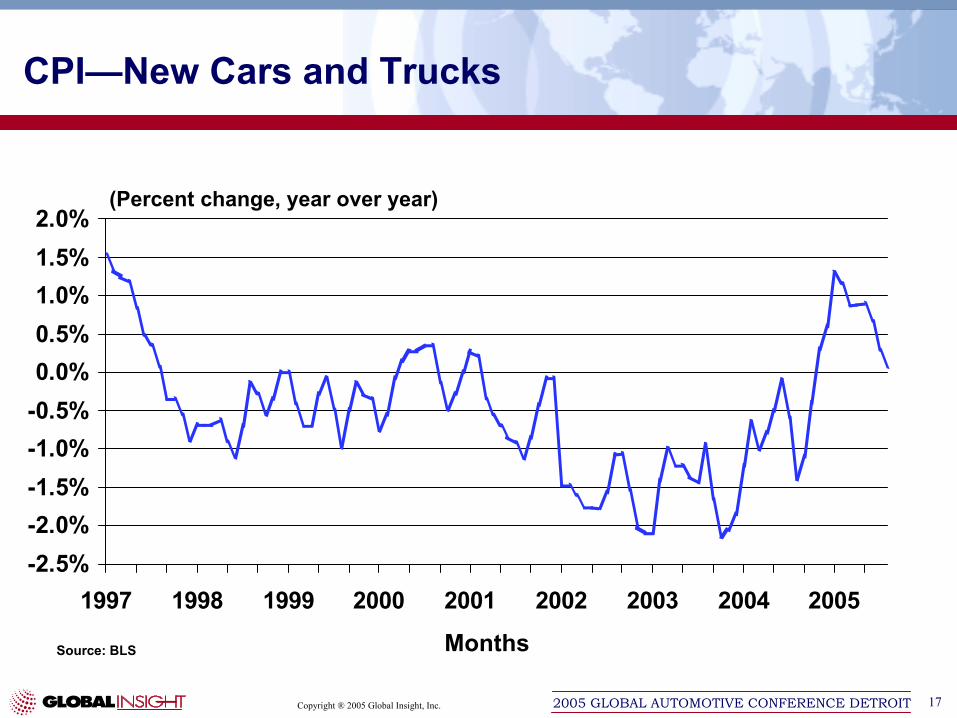

-2.5%-2.0%-1.5%-1.0%-0.5%0.0%0.5%1.0%1.5%2.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005

(Percent change, year over year)

Source: BLS Months

CPI—New Cars and Trucks

Copyright ® 2005 Global Insight, Inc. 182005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1998 1999 2000 2001 2002 2003 2004 2005

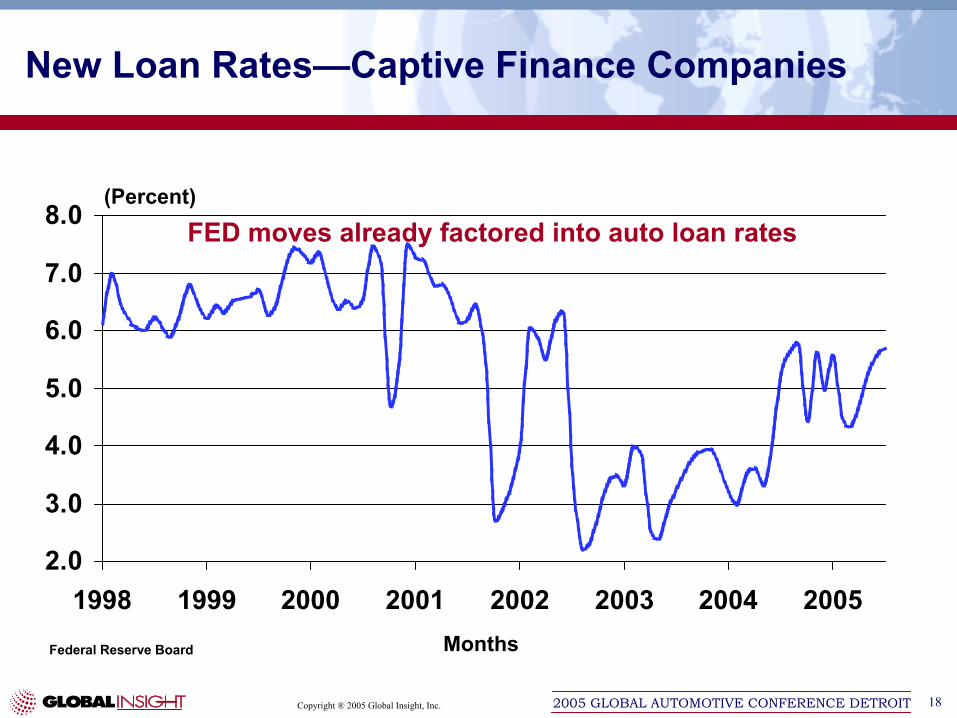

(Percent)

MonthsFederal Reserve Board

New Loan Rates—Captive Finance Companies

FED moves already factored into auto loan rates

Copyright ® 2005 Global Insight, Inc. 192005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

50005500

600065007000

75008000

850090009500

1000010500

'97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '1015000

15500

16000

16500

17000

17500

18000

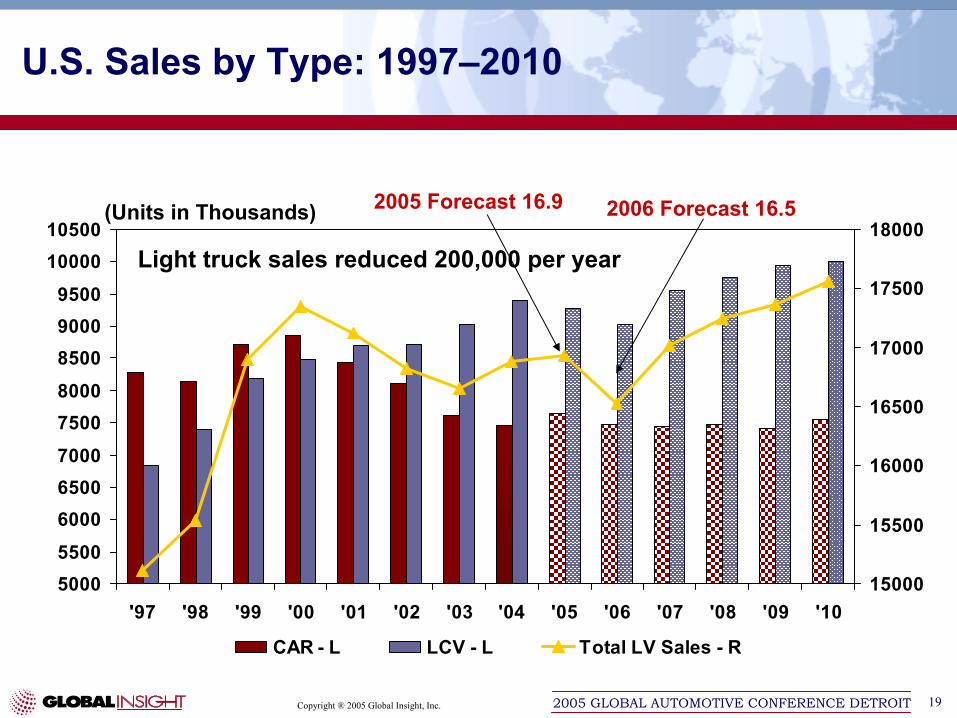

CAR - L LCV - L Total LV Sales - R

(Units in Thousands)

U.S. Sales by Type: 1997–2010

2005 Forecast 16.9 2006 Forecast 16.5

Light truck sales reduced 200,000 per year

Copyright ® 2005 Global Insight, Inc. 202005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

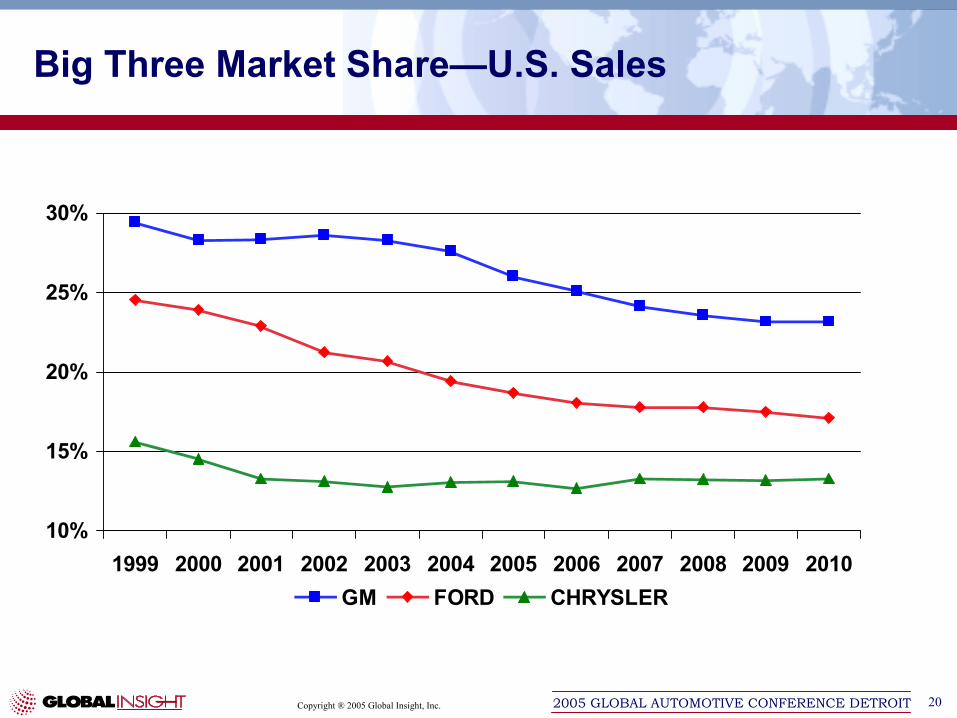

Big Three Market Share—U.S. Sales

10%

15%

20%

25%

30%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010GM FORD CHRYSLER

Copyright ® 2005 Global Insight, Inc. 212005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

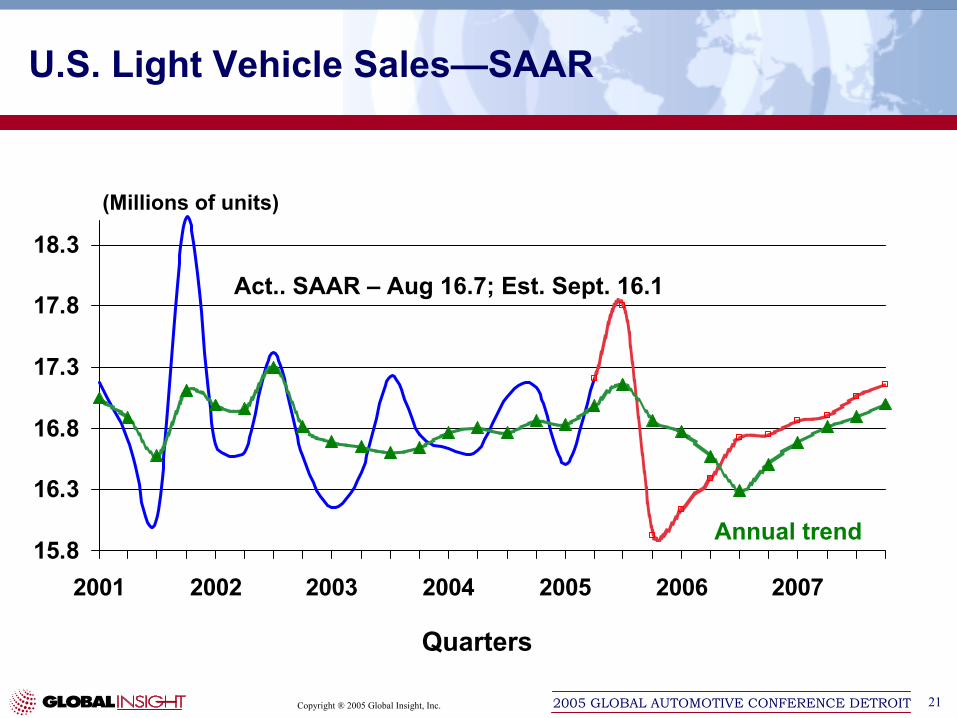

U.S. Light Vehicle Sales—SAAR

15.8

16.3

16.8

17.3

17.8

18.3

2001 2002 2003 2004 2005 2006 2007

(Millions of units)

Quarters

Act.. SAAR – Aug 16.7; Est. Sept. 16.1

Annual trend

Copyright ® 2005 Global Insight, Inc. 222005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

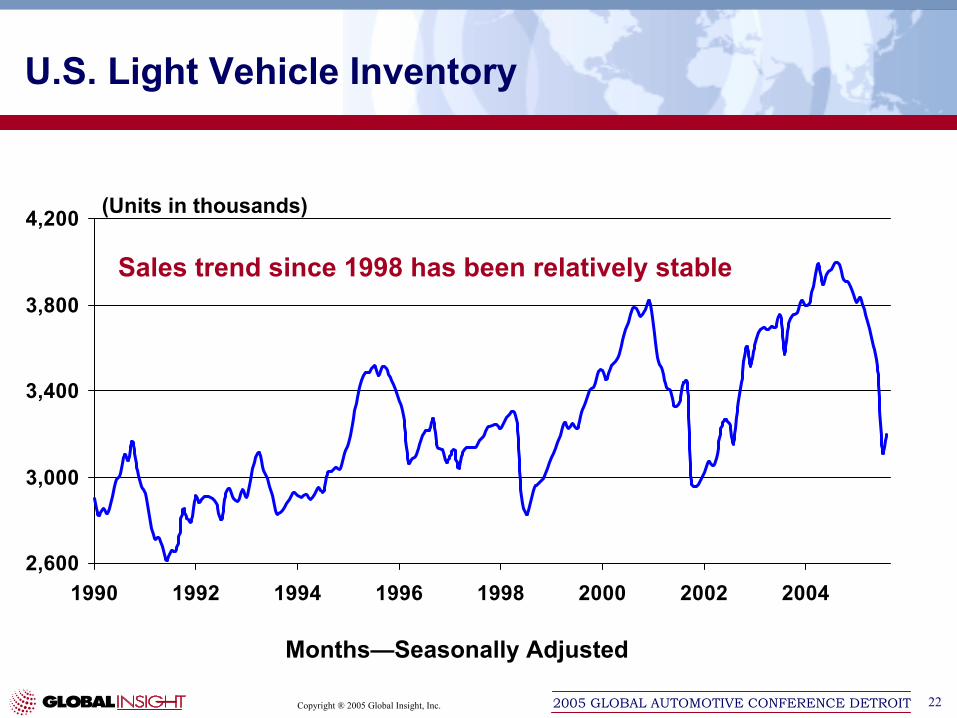

U.S. Light Vehicle Inventory

2,600

3,000

3,400

3,800

4,200

1990 1992 1994 1996 1998 2000 2002 2004

Months—Seasonally Adjusted

(Units in thousands)

Sales trend since 1998 has been relatively stable

Copyright ® 2005 Global Insight, Inc. 232005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

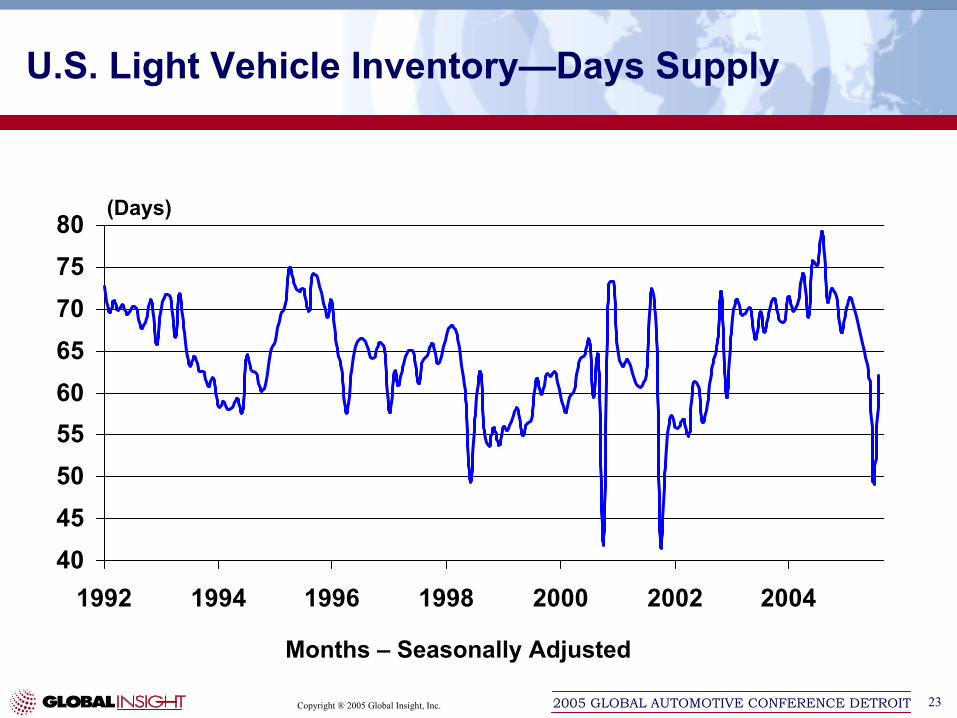

U.S. Light Vehicle Inventory—Days Supply

404550556065707580

1992 1994 1996 1998 2000 2002 2004

(Days)

Months – Seasonally Adjusted

Copyright ® 2005 Global Insight, Inc. 242005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

15.0

15.5

16.0

16.5

17.0

17.5

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

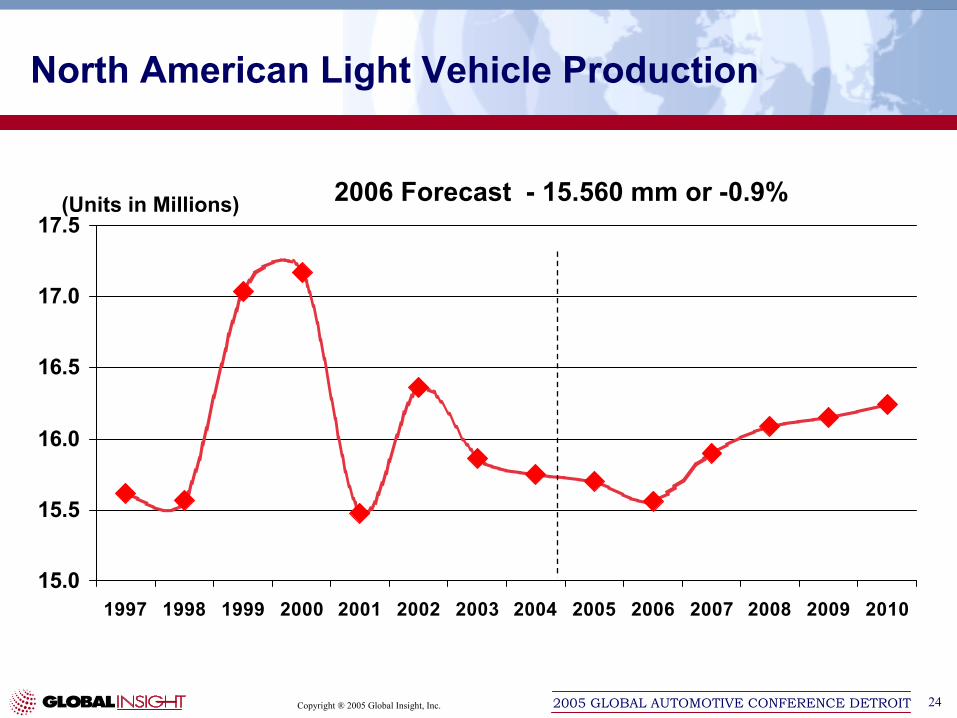

North American Light Vehicle Production

(Units in Millions) 2006 Forecast - 15.560 mm or -0.9%

Copyright ® 2005 Global Insight, Inc. 252005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

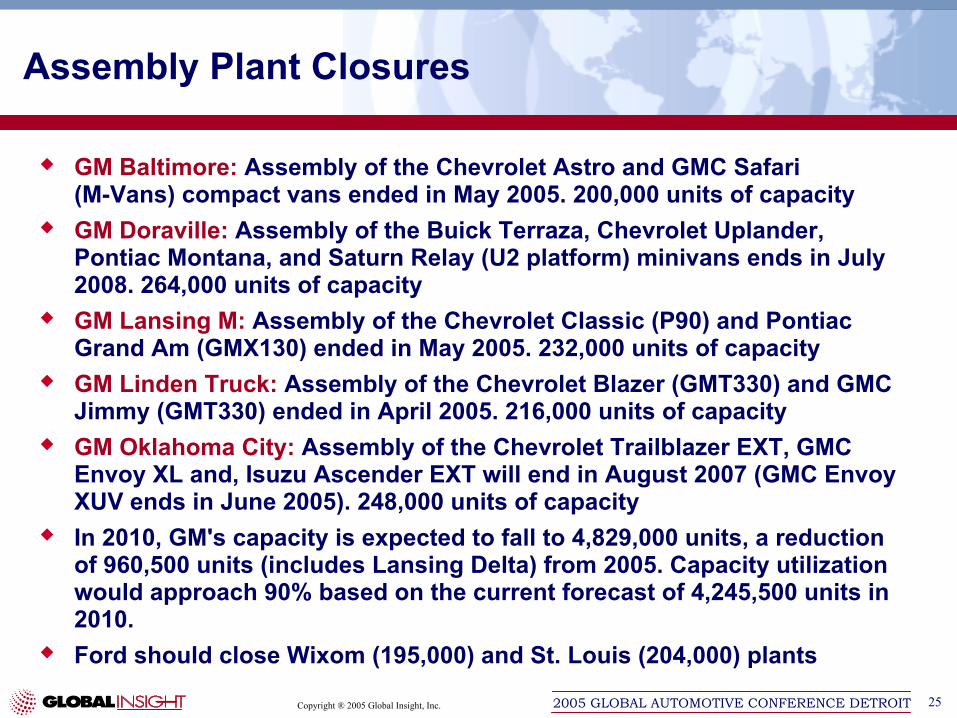

Assembly Plant Closures

GM Baltimore: Assembly of the Chevrolet Astro and GMC Safari (M-Vans) compact vans ended in May 2005. 200,000 units of capacityGM Doraville: Assembly of the Buick Terraza, Chevrolet Uplander, Pontiac Montana, and Saturn Relay (U2 platform) minivans ends in July 2008. 264,000 units of capacityGM Lansing M: Assembly of the Chevrolet Classic (P90) and Pontiac Grand Am (GMX130) ended in May 2005. 232,000 units of capacityGM Linden Truck: Assembly of the Chevrolet Blazer (GMT330) and GMC Jimmy (GMT330) ended in April 2005. 216,000 units of capacityGM Oklahoma City: Assembly of the Chevrolet Trailblazer EXT, GMC Envoy XL and, Isuzu Ascender EXT will end in August 2007 (GMC Envoy XUV ends in June 2005). 248,000 units of capacityIn 2010, GM's capacity is expected to fall to 4,829,000 units, a reduction of 960,500 units (includes Lansing Delta) from 2005. Capacity utilization would approach 90% based on the current forecast of 4,245,500 units in 2010.Ford should close Wixom (195,000) and St. Louis (204,000) plants

Copyright ® 2005 Global Insight, Inc. 262005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

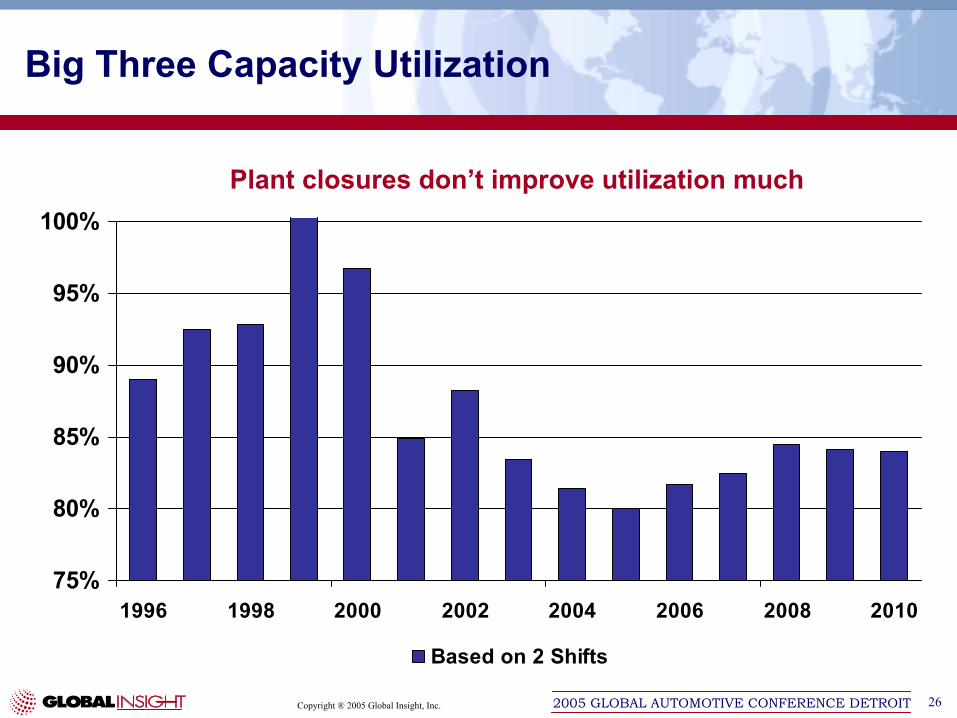

Big Three Capacity Utilization

75%

80%

85%

90%

95%

100%

1996 1998 2000 2002 2004 2006 2008 2010

Based on 2 Shifts

Plant closures don’t improve utilization much

Copyright ® 2005 Global Insight, Inc. 272005 GLOBAL AUTOMOTIVE CONFERENCE DETROIT

Employee price deals will make shift to value pricing difficultPricing on new models not aggressive enoughKatrina has made the environment that much tougher and the risk factor has risen as wellSpike in gasoline prices causes short-term disruptionsLonger term demographics and consumer tastes support and shape the marketProduct, capacity, and inventory have to be aligned to market share in order to relieve pricing pressure

Conclusion

George M. MaglianoDirector of Automotive Industry Research, Americas

E-mail: [email protected]

Tel: +1 212 884 9509