Key trends and outlook for the fluorspar marketDr. Oliver Rhode

2

▪ Introduction of XENOPS Chemicals

▪ Global facts and figures

▪ Focus on China – trade statistics and future trends

▪ Pricing and outlook

▪ “European” supply alternative

Agenda

3

Our core business

Customer specific sourcing of critical raw materials for Life-Science industries

4

Our key success factorNetwork of local senior experts with international experience

5

▪ Introduction of XENOPS Chemicals

▪ Global facts and figures

▪ Focus on China – trade statistics and future trends

▪ Pricing and outlook

▪ “European” supply alternative

Agenda

6

Fluorspar conference 2019Hot topics to be discussed

▪ China: reduced exports, consuming market hub

▪ Emergence of new sources: Africa, Canada, Mongolia

▪ Squeeze on mineral supply for global markets; recession alleviates this

▪ “Acidspar spot prices on record high”

▪ “Ever-tightening supply”

7

Fluorspar conference 2009Look 10 years back – any lessons learned?

▪ China: reduced exports, consuming market hub

▪ Emergence of new sources: Africa, Canada, Mongolia

▪ Squeeze on mineral supply for global markets; recession alleviates this

▪ “Acidspar spot prices on record high”

▪ “Ever-tightening supply”

8

Presentations at Fluorspar 2009”Interesting times for fluorspar – here to stay”

▪ “An overview of the acidspar supply/demand balance”

▪ “Trends in aluminium & steel – implications for fluorspar”

▪ “Case study of Sephaku’s Dinokeng Fluorspar Project”

▪ “Newfoundland project - in production in three years”

▪ “Fluorspar production status & developments in Mongolia”

▪ “Trade protectionism & the likely impact of the WTO challenge by the EU & USA”

9

Fluorspar production in 2018China and Mexico were the dominating producers

China61%

Mexico19%

South Africa4%

Mongolia4%

Vietnam4%

Spain3%

Others5% Others include:

▪ Morocco▪ Germany▪ Thailand▪ UK▪ Canada▪ Iran▪ Pakistan▪ Brazil▪ Argentina

Global production of fluorspar in 20186 mtons

10

Global production of fluorspar in 20186 mtons

Fluorspar production in 2018Constant ratio of metspar and acidspar over the years

40% Metspar (CaF2 <97%)= 2.4 Mio. tons

60% Acidspar (CaF2 >97%)= 3.6 Mio. tons

11

35% = 1.26 Mio. tonsfor aluminum trifluoride

via hydrofluoric acid

60% = 2.16 Mio. tonsfor fluorocarbons

via hydrofluoric acid

Acidspar consumption in 2018Production of hydrofluoric acid was the biggest segment

5% = 0.18 Mio. tonsfor fluxes, glassmaking,

welding rods

Global production of acidspar in 20183.6 mtons

12

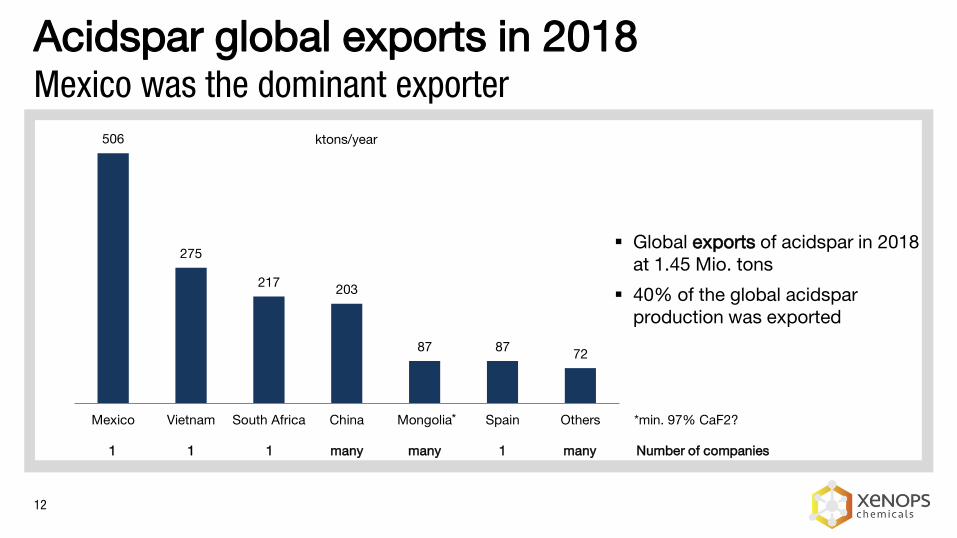

Acidspar global exports in 2018Mexico was the dominant exporter

506

275

217203

87 8772

Mexico Vietnam South Africa China Mongolia Spain Others

ktons/year

▪ Global exports of acidspar in 2018 at 1.45 Mio. tons

▪ 40% of the global acidsparproduction was exported

* *min. 97% CaF2?

1 many1 1 many 1 many Number of companies

13

▪ Global imports of acidspar in 2018 at 1.44 Mio. tons

Acidspar global imports in 2018The main importers were USA, Italy, India and Germany

374

216201

158

86 86 8672

58

101

USA Italy India Germany UAE China Japan Canada Tunisia Others

ktons/year

* *Netherlands 87 ktons

14

Metspar global exports in 2018Mongolia and Mexico were the dominant exporters

ktons/year

▪ Global exports of metspar in 2018 at 1.40 Mio. tons

▪ Nearly 60% of the global metsparproduction was exported

462

378

196

7056

4228 28

140

Mongolia Mexico China Italy Morocco Thailand Iran Pakistan Others

15

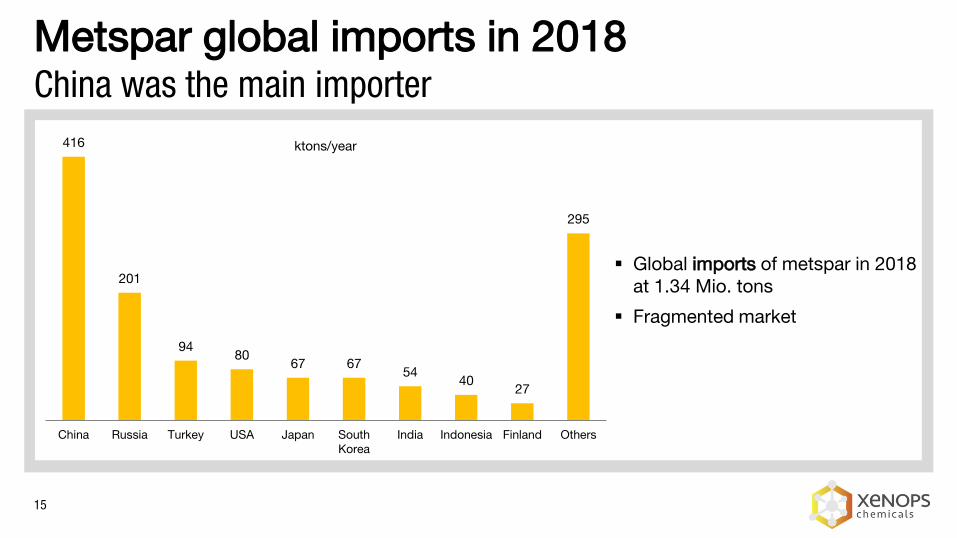

▪ Global imports of metspar in 2018 at 1.34 Mio. tons

▪ Fragmented market

Metspar global imports in 2018China was the main importer

ktons/year416

201

9480

67 6754

4027

295

China Russia Turkey USA Japan SouthKorea

India Indonesia Finland Others

16

What is this?

17

Rebranding of Mexichem“We’re no longer Mexi, and we are no longer Chem”

Union Trademark 018090396Application under examination Application day: Jul. 4, 2019

Union Trademark 018105541 Application published Application day: Aug. 8, 2019

“… To quote Max Planck, the renowned physicist: “When you change the way you look at things, the things you look at change.”

So in order to change as a company, we’re changing how we look at things. Our ImpactMark will be updated every year with our performance. Its three loops indicate the past three years. As we do better, the lines will progress outward...”

18

Rebranding of MexichemThe ImpactMark®

Radar Chart-illustrative example-

19

Rebranding of MexichemMexichem Fluor becomes Koura

Mexichen reporting structure: 3 business groups

Mexichem Fluor Business Group sales 2018▪ 837 Mio.USD▪ + 23% compared to 2017▪ 12% of Mexichem sales

Mexichem Fluor Business Group EBITDA 2018▪ 362 Mio.USD▪ + 40% compared to 2017▪ EBITDA margin of 43%▪ 26% of Mexichem EBITDA

20

▪ Introduction of XENOPS Chemicals

▪ Global facts and figures

▪ Focus on China – trade statistics and future trends

▪ Pricing and outlook

▪ “European” supply alternative

Agenda

21

China’s impact on the fluorine value chainWhy is China so important for the global fluorochemical industry?

▪ Largest producer & consumer of acidspar in the world

▪ Largest producer & consumer of hydrofluoric acid in the world

▪ Largest producer & consumer of fluorocarbons in the world

▪ Largest producer & consumer of aluminum trifluoride in the world

22

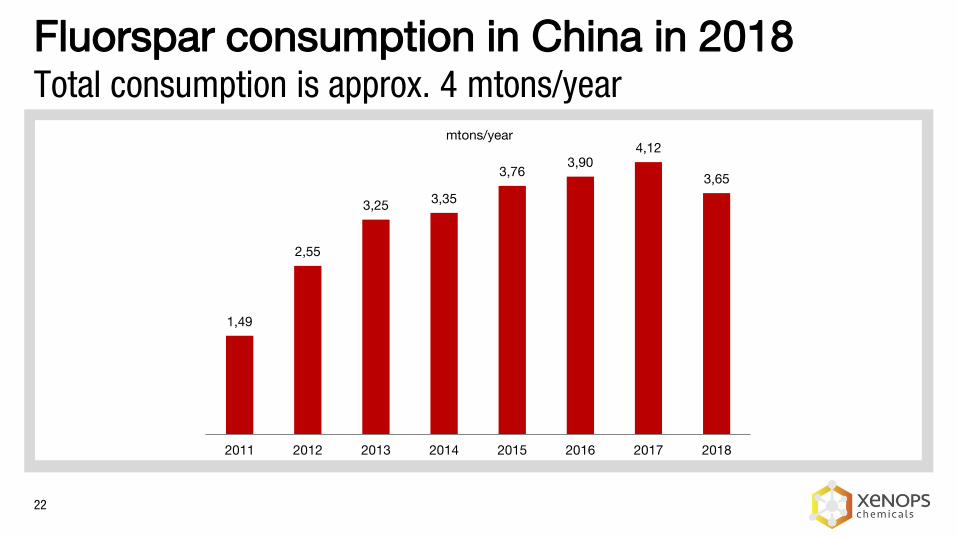

Fluorspar consumption in China in 2018Total consumption is approx. 4 mtons/year

1,49

2,55

3,25 3,35

3,763,90

4,12

3,65

2011 2012 2013 2014 2015 2016 2017 2018

mtons/year

23

Fluorspar consumption in China in 2018China became a net-importer of fluorspar last year

Import Export Trade balance

500

1.000

1.500

(500)

(1.000)

(1.500)

ktons/year

Trade flows in 2018:

▪ Total imports: 511 ktons

▪ Total exports: 403 ktons

▪ Net-import: 108 ktons

24

Chinese acidspar trade in 2018China is a net-exporter of acidspar

Total acidspar exports: 202 ktons Total acidspar imports: 91 ktons

30.633

21.89819.944

9.378

6.954

2.10538

Mexico South Africa Myanmar Vietnam Mongolia Morocco Others

57.379

50.896

39.279

23.076

17.300

10.350

3.668

India Japan Netherlands Germany SouthKorea

Canada Others

Exports in tons Imports in tons

25

Chinese metspar trade in 2018Import volume is more than twice as much as export volume

Total metspar exports: 201 ktons Total metspar imports: 420 ktons

340.089

49.11615.949 6.912 5.910 881 443 225

Exports in tons Imports in tons

46.451

36.99333.879

25.976

18.957

13.214

4.454 4.124 3.008 2.933 2.210

8.670

26

Chinese fluorspar trade in 2018The annual update…

▪ China exported same amounts of acidspar and metspar in 2018

▪ China imported 4,6 times more metspar than acidspar in 2018

▪ China is a net-importer of metspar, but not a net-importer of acidspar yet

[ktons] Acidspar Metspar Total

Exports 202 201 403

Imports 91 420 511

Balance +111 -219 108

27

Chinese acidspar trade in 2019/1-6More imports from Myanmar

Total acidspar exports: 98 ktons Total acidspar imports: 32 ktons

16.327

7.257

4.551

3.126

Myanmar Mongolia Mexico Others

Imports in tons34.847

19.957

16.574

9.187

5.381 4.436 4.5542.560

Exports in tons

28

Chinese metspar trade 2019/1-6Mongolia continues to be the major origin of metspar imports

Total metspar exports: 90 ktons Total metspar imports: 199 ktons

Imports in tons

173.831

8.190 4.913 3.831 2.852 1.575 1.217 2.364

Exports in tons

31.071

17.117

12.61910.510

8.819

4.380 5.192

29

World fluorspar reserves in 2018The Chinese “dilemma”

Mexico21%

China13%

South Africa13%

Mongolia7%

Vietnam2%

Spain2%

Others42%

▪ China consumes approx. 67% (4 mtons) of the global fluorspar production

▪ China has only 13% (40 mtons*) of the global fluorspar reserves

310mtons

*Chinese sources indicate a proven reserve of 242 mtons

30

China’s strategy to secure fluorspar supplyCharacteristics of Chinese fluorspar deposits

(1)Resource-rich, but low-level of explorationAs of 2018, China has 250 million tons of fluorite, the real development value is about 100 million tons, the basic reserves is about 45 million tons(2)Concentration of depositsFluorite deposits are distributed in 27 provinces, but mainly concentrated in Inner Mongolia, Zhejiang, Jiangxi, Fujian, Hunan provinces(3)More single-type fluorite deposits than associated depositsBy the end of 2011, there were 701 single-type fluorite mines (57.2% of the total resources), and 42 associated fluorite mines (42.8%).(4)Single-type fluorite: less rich oreAverage CaF2 grade of single fluorite ore is 35% to 40%, grades greater than 65% accounts for 20%, CaF2 grade greater than 80% less than 10%.(5)Low content of CaF2 in the associated fluorite mine The content is below 26%, mainly in Hunan and Yunnan. Mainly tungsten, tin, lead and zinc ore, iron associated with fluorite ore, low utilization.(6)Ratio of exploitation and reserve is lower than the international averageChina's fluorite resources are rich, accounting for about 14% of the global reserves, but China's fluorite production is as high as 60% of the world, the storage ratio is unbalanced.

31

China’s strategy to secure fluorspar supplyWhat might China consider to secure the fluorine value chain?

▪ January 2019: the National Geological Survey Work Conference was held in Beijing: „… Global demand for fluorspar will continue to increase substantially, which will stimulate geological exploration… The surrounding countries Mongolia and Thailand are also the preferred target areas for geological exploration cooperation…“

▪ Investments in foreign countries to secure raw material supply

▪ Pakistan, Thailand, Myanmar and Zambia are new countries for fluorspar production, reflecting that these countries are currently hotspots for fluorspar investments

32

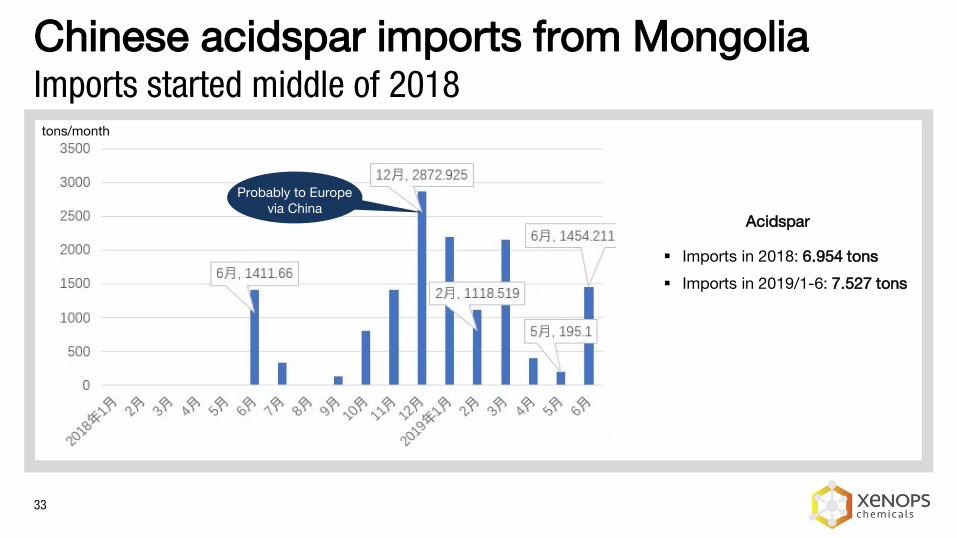

Chinese fluorspar imports from MongoliaOnly minor imports of “real” acidspar

tons/year

“Alternative facts” for 2018:

▪ Imports of acidspar: 87 ktons

▪ Imports of metspar: 287 ktons

▪ Mongolian trade data: total acidspar exports 165 ktons

0 6.954 7.527

131.451

340.089

173.831

2017 2018 2019/1-6

Imports of acidspar

Imports of metspar

33

Chinese acidspar imports from MongoliaImports started middle of 2018

▪ Imports in 2018: 6.954 tons

▪ Imports in 2019/1-6: 7.527 tons

tons/month

Probably to Europevia China

Acidspar

34

Chinese metspar imports from MongoliaSeasonal effects are clearly visible

▪ Imports in 2018: 340.089 tons

▪ Imports in 2019/1-6: 173.831 tons

tons/month

Metspar

35

Chinese fluorspar imports from MongoliaWhy is so much more metspar than acidspar imported?

▪ Most of the “acidspar” has a CaF2 content lower than 97% → metspar (HS 252921)

▪ Imports into China are subject to taxes and duties:

▪ Value added tax: 17% → 16% (May 2018) → 13% (April 2019)▪ Consumption tax: nil▪ Custom duties: MFN duty rate is 3%

→ metspar at 1,5% (Asia Pacific Trade Agreement)

▪ Metspar can be everything with a CaF2 content lower than 97%: powder, lumps, briquettes, ore etc.

▪ We believe a significant volume of the imported metspar is used (directly or after further enrichment) for HF-production in China

36

Mongolian fluorspar exportsIs Mongolia the “new China” for fluorspar exports out of Asia?

▪ Mongolia's fluorite production rebounded in 2018 and 2019

▪ China is the largest export market for Mongolian fluorspar, followed by Russia

▪ The Mongolian government believes that mining investment is the main driving force for the country's economic growth

▪ In the past decade, the political situation has changed frequently, which has complicated the domestic investment environment, and resource nationalism has also risen in recent years

▪ Even in the case of political instability, Mongolia and China still maintain a positive cooperative relationship and are committed to maintaining close political and economic ties

37

Mongolian fluorspar exportsIs Mongolia the “new China” for fluorspar exports out of Asia?

Resource of fluorspar

Favorable mining policy & support by authorities

Currently approx. 20 fluorspar processing plants in operation – more projects to come

Quality: most of current production is not “real” acidspar

Infrastructure: lack of reliable railway system

Climate: seasonal production / transportation due to cold winters

Russia and China: huge markets in the backyard – no need to export to other countries,

prices in China probably highest in the world

-

+

+

-

-

+

-

38

New Mongolian fluorspar projectsIs Mongolia the “new China” for fluorspar exports out of Asia?

▪ The Mineral Resources and Petroleum Authority announced that five new fluorspar projects with approved feasibility study will be launched in 2019

▪ Two projects will be in Dornogovi Province, others in Dundgovi, Sukhbaatar and Khentii provinces

▪ The Association of Mongolian Fluorspar Miners proposed exporting fluorspar through a general terminal

▪ The Mandal-Ovoo fluorite deposit hasn’t been mined despite completing its feasibility three years ago

▪ Berk Uhl JSC recently discontinued its operations at the Delgerkhaan deposit due to issues caused by lack of infrastructure

39

Status of Chinese fluorsparChinese fluorspar is “disconnected” from global markets

▪ China’s role in the global fluorspar market changed significantly

▪ China became a net-importer of metspar, and a net-exporter of acidspar of just 100 ktons/year

▪ Can you still get a 98% CaF2 quality, with SiO2 < 1% and CaCO3 < 1% from China?

▪ Chinese fluorspar doesn’t have a major impact on global markets anymore

▪ Mongolia won’t continue China’s previous role being the leading exporter to global markets

“China is losing its fluorspar advantage slowly”- Chinese fluorspar trader -

40

▪ Introduction of XENOPS Chemicals

▪ Global facts and figures

▪ Focus on China – trade statistics and future trends

▪ Pricing and outlook

▪ “European” supply alternative

Agenda

41

Pricing setting of fluorsparWhat is the mechanism considering China’s new role?

Highest price in 2019 – until today: 665 $/dmt CIF Europe for 90% CaF2

1,000 $/dmtfor acidspar ?

42

Price setting of fluorsparPricing of acidspar in China

▪ There are only a few large-scale fluorite mining enterprises, for example:

▪ Jinshi Resources Group Co., Ltd.▪ Zhejiang Wuyi Shenlong Flotation Co., Ltd.▪ Sinochem Blue Sky Group Co., Ltd.▪ Inner Mongolia Huasheng Fluorite Mining Co., Ltd.

▪ China implemented a weekly price determination

▪ Fluorite commodity index → how reliable?

▪ Due to the changed role of Chinese fluorspar for global markets, China can’t be the reference for price setting anymore

43

Price setting of fluorsparWho has the power to determine prices?

▪ A price setter is a company (or organization) that's powerful enough to set the market price that they can charge customers with

▪ The greater the market share that company has, the more market power in setting prices it has

▪ Factors: product differentiation (quality), low-cost production, volume, place and condition of the market

44

OutlookSupply & Demand balance

Supply

▪ Overall, the fluorspar market remains tight, even when the new producers are running at nameplate capacity next year

▪ There are new projects, but it is not clear when they will start commercial production

▪ Plan B: sell to China

Demand

▪ Biggest threat: trade war & Brexit → global recession

45

OutlookThe transatlantic cheese war

▪ The US is allowed to impose punitive tariffs on imports of $7.5 billion for Airbus' illegal subsidies

▪ On October 18, the surcharges came into force: 10 percent on aircraft, 25 percent on agricultural and industrial goods

▪ The transatlantic aviation-subsidy war, which has lasted 15 years, is far from over

▪ Next, the WTO will determine the extent to which the EU may impose tariffs on America for its aid to Boeing

▪ The fact that the Trump administration made its first victory is simply because the Europeans did complain later

▪ Brussels has a retaliatory list for US products worth $12 billion in the drawer

"I always liked American wines rather than French - even if I do not drink wine. I just like what

they look like"

46

▪ Introduction of XENOPS Chemicals

▪ Global facts and figures

▪ Focus on China – trade statistics and future trends

▪ Pricing and outlook

▪ “European” supply alternative

Agenda

47

Opportunity to fill the supply gapChina situation favors developments of sources outside of China

▪ The trend of increasing fluorspar consumption within China, combined with less domestic production favor development of fluorspar sources outside of China

▪ However, it takes 10 years or more to put a new fluorspar mine into operation

▪ Recent loss in global acidspar output approximately at 800 ktons/year; demand for acidspar is expected to be at 2.5% CAGR until 2025

▪ The tight fluorspar supply situation in China is exacerbated by the later-than-scheduled arrival of new supply from Canada and South Africa

▪ In this tight supply situation, we are pleased to introduce a new alternative source for acidspar, especially for customers in Europe and the Mediterranean

48

New acidspar source for European marketsGujarat Fluorochemicals subsidiary to expand in Morocco

▪ GFL GM Fluorspar SA, a subsidiary of Gujarat Fluorochemicals Ltd., India, is to expand production capacity of acidspar at its Taourirt operation in Morocco

▪ The mine and beneficiation plant have been operational since 2018 with a capacity of 40.000 tpa acidspar, which is now planned to be increased to 60.000 tpa, expected to be complete by Q2 2020

49

New acidspar source for European marketsGujarat Fluorochemicals subsidiary to expand in Morocco

▪ Strategic location of the mine in the north-east of Morocco

▪ Distance of only 95km north to the port of Nador

▪ Max. seven days shipping time to the main ports in Europe

▪ Supply will be targeted primarily, but not only to customers in Europe and the Mediterranean

▪ Second biggest “European” acidsparproducer after Spain

50

New acidspar source for European marketsGujarat Fluorochemicals subsidiary to expand in Morocco

▪ The acidspar has very low content of arsenic, iron and phosphorous

▪ Quality fully approved by customers

▪ Regular shipments to customers

51

New acidspar source for European marketsGujarat Fluorochemicals subsidiary to expand in Morocco

▪ GFL, part of the multi-billion INOX Group of Companies, is India’s largest poly-tetrafluoroethylene (PTFE) producer with hi-tech state of the art technology plants at Dahej, Gujarat

▪ GFL has appointed XENOPS Chemicals, Germany, as marketing and sales agent

52