Correcting Accounting Errors

Mastering Correction of Accounting Errors

American Institute of Professional Bookkeepers

© American Institute of Professional Bookkeepers, 2010

No accrual or deferral was recorded (or was recorded for the wrong amount)

For example, revenue was recognized before it was earned.The decimal point was put in the wrong place (for example, 1,000 should be 100)

Correcting Accounting Errors

An account was credited when it should have been debited (or vice versa)

Types of Accounting Errors Omission Accrual or Deferral

Error Classification Error Arithmetic Error Use of an Incorrect

Accounting Principle Use of an Improper

Estimate Transposition Error Slide Error Posting Error

Two digits were reversed (for example, 739 was recorded as 379)

An event was never recorded

For example, depreciation expense was computed using the wrong useful life

Incorrect addition, multiplication, etc.

An amount was posted to the wrong account within a category (e.g., the bill for rent was posted to Insurance Expense)

Correcting Accounting Errors

When Accounting Errors Are FoundAccounting errors are usually discovered during: The monthly bank reconciliation Preparation of the trial balance Reviews of end-of-period adjustments Routine internal audits Year-end audits by external auditors

Correcting Accounting Errors

The Bank ReconciliationCash is the lifeblood of a business Even profitable companies can fail

without adequate cash management Cash can easily be hidden or moved, making it

an attractive target for theft

Correcting Accounting Errors

The Bank ReconciliationOne important control on cash is the monthly bank reconciliationThe bank reconciliation accounts for the difference between the balance on the bank statement and the balance in the company general ledger Cash account(s)Therefore, to be most effective, the bank reconciliation should be done by an employee who neither has custody of nor keeps records of cash

Correcting Accounting Errors

Items on the company‘s books are not on the current bank statement Outstanding checks Deposits in transit Book errors

The Cash account balance and bank statement balance often differ because:

Company checks that have not cleared the bank

Company bank deposits not yet credited to its account

Cash v. Bank Balance Differences

Customer checks returned for insufficient funds (“bounced” checks)

Items on the current bank statement are not yet on the company’s books Bank service charges Collections of notes Nonsufficient funds

(NSF) checks Bank errors

Recent bank fees and charges

Customer loans recently repaid (with interest) directly to the bank

The Cash account balance and bank statement balance often differ because:

Cash v. Bank Balance Differences

Correcting Accounting Errors

The goal: Make these two balances equal

Bank Reconciliation: Example 1

Balance per books, 8/31 Balance per bank, 8/31

Corrected book bal., 8/31 Corrected bank bal., 8/31

XYZ CorpBank Reconciliation

August 20X9

x,xxx x,xxx

x,xxx x,xxx

Reconcile:Items on the bank statement

not (yet) recorded bythe company

Reconcile:Items on the company’s

books not on the current bank statement

Reconcile:Items on the bank statement

not (yet) recorded bythe company

Add to book balance:Collection of note xxxInterest on note xxx

Deduct:NSF check xxxBank service charge xxx

Reconcile:Items on the company’s

books not on the current bank statement

Add to bank balance:Deposits in transit xxx

Deduct:Outstanding checks xxx

Correcting Accounting Errors

Bank Reconciliation: Example 1

Balance per books, 8/31 Balance per bank, 8/31

Corrected book bal., 8/31 Corrected bank bal., 8/31

XYZ CorpBank Reconciliation

August 20X9

x,xxx x,xxx

x,xxx x,xxx

Correcting Accounting Errors

Bank Reconciliation: Example 2As of 11/30, Gym-Bo’s ledger Cash account balance is $16,150 and its bank statement balance is $33,520Two checks, totaling $9,810, are outstanding.A night deposit of $12,150 from the 30th is not on the current bank statement.The bank charged Gym-Bo’s account for a check written by another company for $160.The bank statement shows collection of a $20,000 note receivable plus $900 interest.The bank statement shows an NSF check for $1,000 and a bank service charge for the check of $30.

Bank

Bank

Bank

Book

Book

Correcting Accounting Errors

Bank error 160

Deduct:NSF check 1,000Bank service charge 30

Bank Reconciliation: Example 2

Balance per books 11/30 Balance per bank 11/30

Corrected book bal., 11/30 Corrected bank bal., 11/30

Gym-BoBank Reconciliation

November 20X9

16,150 33,520

36,020 36,020

Add to book balance:Collection of note 20,000Interest on note 900

Deduct:Outstanding checks 9,810

Add to bank balance:Deposits in transit 12,150

Correcting Accounting Errors

Deduct:NSF check 1,000Bank service charge 30

Bank Reconciliation: Example 2

Balance per books 11/30

Corrected book bal., 11/30

Gym-BoBank Reconciliation

November 20X9

16,150

36,020

Add to book balance:Collection of note 20,000Interest on note 900

Book items to be reconciled require journal entries to adjust the current Cash account balance of $16,150 to the reconciled balance of $36,020

Correcting Accounting Errors

Deduct:NSF check 1,000Bank service charge 30

Bank Reconciliation: Example 2

Balance per books 11/30

Corrected book bal., 11/30

Gym-BoBank Reconciliation

November 20X9

16,150

36,020

Add to book balance:Collection of note 20,000Interest on note 900

Cash 20,900Notes Rec. 20,000Interest Revenue 900

Accts Rec. 1,000Cash 1,000

Misc. Expense 30Cash 30

Correcting Accounting Errors

To find errors in the unadjusted trial balance, follow these steps:1. Check that all account balances have been correctly transferred to the trial balance•Scan account balances to see if they are in the correct column (Dr v. Cr)•Make sure that every account with a balance was transferred to the trial balance•Verify that the balance listed in the debit or credit column matches the one in the account

Finding Errors in a Trial Balance

Correcting Accounting Errors

Account Dr CrCash 577Prepaid Assets 48Accounts Receivable 699Accounts Payable 702 Salaries Payable 254R. Smith Capital 566Sales 4,001Cost of Goods Sold 1,287 Salaries Expense 1,179Rent Expense 637Utilities Expense 344Interest Expense 200Tax Expense 552

Example

Accounts Payable is a

liability account

(normal credit balance)

Correcting Accounting Errors

To find errors in the unadjusted trial balance, follow these steps:1. Check that all account balances were correctly transferred2. Total the debits and credits. If the totals are not equal, take these steps:

a. Check for a doubling error

Finding Errors in a Trial Balance

Correcting Accounting Errors

Account Dr CrCash 577Prepaid Assets 48Accounts Receivable 699Accounts Payable 702 Salaries Payable 254R. Smith Capital 566Sales 4,001Cost of Good Sold 1,287 Salaries Expense 1,179Rent Expense 637Utilities Expense 344Interest Expense 200Tax Expense 552Total

Example

4,8216,225

Calculate the difference

between the two totals and

divide by 2

= 1,404 / 2 = 702

Look for this amount in the trial balance

Correcting Accounting Errors

Account Dr CrCash 577Prepaid Assets 48Accounts Receivable 699Accounts Payable 702 Salaries Payable 254R. Smith Capital 566Sales 4,001Cost of Sales 1,287 Salaries Expense 1,179Rent Expense 637Utilities Expense 344Interest Expense 200Tax Expense 552Total

Example

4,8216,2255,5235,523

After the correction is made, the totals should be equal

Correcting Accounting Errors

Finding Errors in a Trial BalanceTo find errors in the unadjusted trial balance, follow these steps:1. Check that all account balances were correctly transferred2. Total the debits and credits. If the totals are not equal, take these steps:

a. Check for a doubling errorb. Check for a slide or transposition error

Correcting Accounting Errors

ExampleAccount Dr CrCash 577Prepaid Assets 48Accounts Receivable 7,990Accounts Payable 702 Salaries Payable 354R. Smith Capital 566Sales 4,011Cost of Goods Sold 1,287 Salaries Expense 1,179Rent Expense 637Utilities Expense 344Interest Expense 210Tax Expense 552

12,824 5,633

Calculate the difference

between the two totals and

divide by 9

= 7,191 / 9 = 799

Look for the same total with an extra 0 at the end

Correcting Accounting Errors

ExampleAccount Dr CrCash 577Prepaid Assets 48Accounts Receivable 799Accounts Payable 702 Salaries Payable 354R. Smith Capital 566Sales 4,011Cost of Goods Sold 1,287 Salaries Expense 1,179Rent Expense 637Utilities Expense 344Interest Expense 210Tax Expense 552

12,824 5,6335,633

After correcting the error, make sure the totals are now equal

Correcting Accounting Errors

Transposition ErrorsA transposition error occurs when two digits have been reversed. For example: 123 is recorded as 213 7,912 is recoded as 9,712 476 is recorded as 467

Correcting Accounting Errors

ExampleAccount Dr CrCash 757Prepaid Assets 48Accounts Receivable 699Accounts Payable 702 Salaries Payable 254R. Smith Capital 566Sales 4,011Cost of Goods Sold 1,287 Salaries Expense 1,179Rent Expense 637Utilities Expense 344Interest Expense 210Tax Expense 552

5,713 5,533

Calculate the difference

between the totals and divide by 9

= 180 / 9 = 20

When the difference

between the totals is

divisible by 9, there may be a transposition

error

Correcting Accounting Errors

Transposition ErrorsTo find an amount that has been

transposed: Find the difference between total debits and

total credits and add 1 to the first digit Example: You find a difference between the totals of

180. The first digit is 1. Add 1 and you get 2.

Find account balances with that difference between the first and second digits Example: Look for account balances where the

difference between the first and second digits is 2

Correcting Accounting Errors

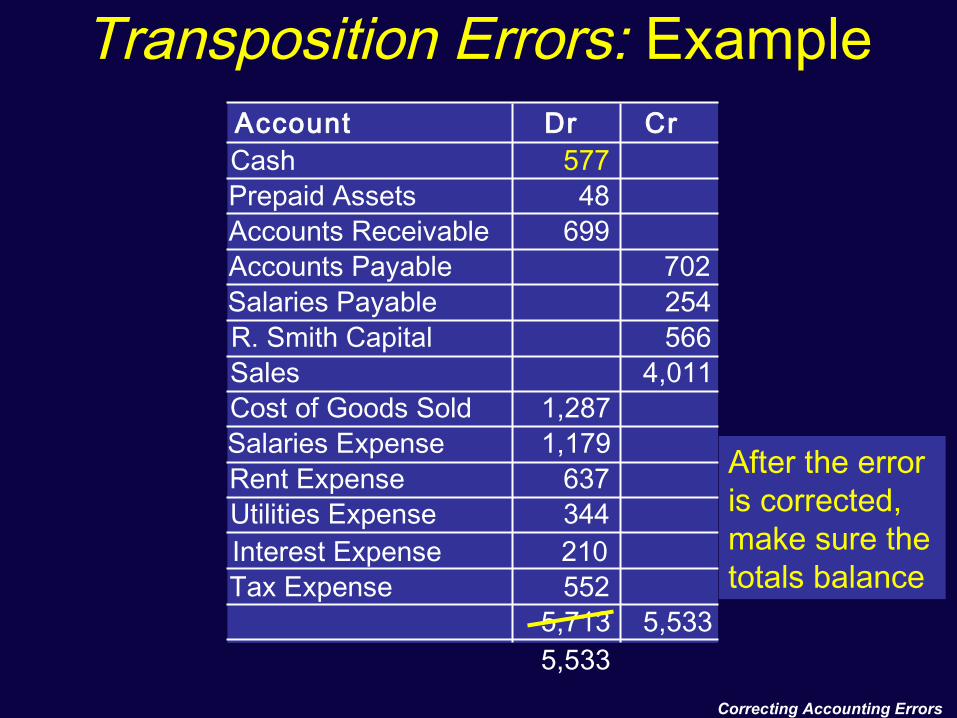

Transposition Errors: ExampleAccount Dr CrCash 757Prepaid Assets 48Accounts Receivable 699Accounts Payable 702 Salaries Payable 254R. Smith Capital 566Sales 4,011Cost of Goods Sold 1,287 Salaries Expense 1,179Rent Expense 637Utilities Expense 344Interest Expense 210Tax Expense 552

5,713 5,533

To the first digit of the difference add 1 1 + 1 = 2

Now look for a difference of this amount between the first and second digits

= 180

Correcting Accounting Errors

Transposition Errors: ExampleAccount Dr CrCash 577Prepaid Assets 48Accounts Receivable 699Accounts Payable 702 Salaries Payable 254R. Smith Capital 566Sales 4,011Cost of Goods Sold 1,287 Salaries Expense 1,179Rent Expense 637Utilities Expense 344Interest Expense 210Tax Expense 552

5,713 5,5335,533

After the error is corrected, make sure the totals balance

Correcting Accounting Errors

Finding Errors in a Trial BalanceTo find errors in the unadjusted trial balance, follow these steps:1.Check that all account balances have been correctly transferred to the trial balance2.Total debits and credits—if not equal, look for a doubling, slide or transposition error.3. Examine journal entries and postings

a. Verify that JEs were posted correctly to the ledger accounts

b. Review JEs for obvious errors—you may need to examine source documents

Correcting Accounting Errors

Accrual ErrorsRecall from Mastering Adjusting Entries that an accrual is an expense incurred or revenue earned before cash flowsAt the end of the period, an adjusting entry is recorded to accrue revenues (and receivables)—and expenses (and payables)

The adjusting entry to accrue revenue is:____ Receivable

____ Revenue

The adjusting entry to accrue expenses is:____ Expense

____ Payable

Correcting Accounting Errors

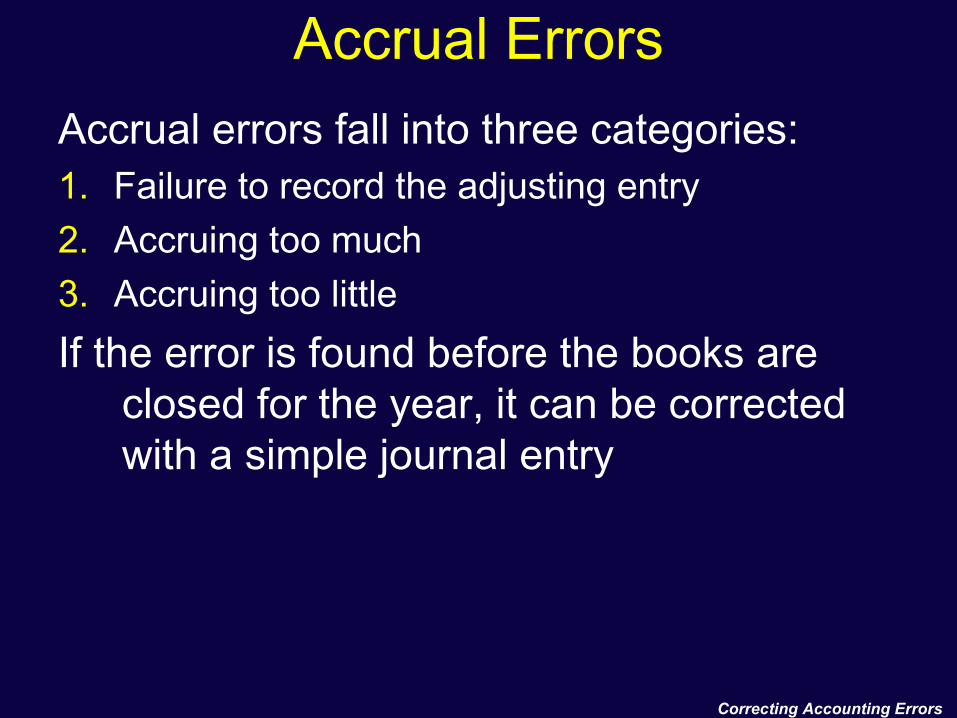

Accrual ErrorsAccrual errors fall into three categories:1. Failure to record the adjusting entry2. Accruing too much3. Accruing too littleIf the error is found before the books are

closed for the year, it can be corrected with a simple journal entry

Correcting Accounting Errors

Accrued Revenue ErrorsReview: The adjusting entry to accrue revenue is:

____ Receivable xxx ____ Revenue xxx

Error:Failure to record the adjusting entry

Correction:Record the adjusting entry

____ Receivable xxx ____ Revenue xxx

Correcting Accounting Errors

Accrued Revenue ErrorsReview: The adjusting entry to accrue revenue is:

____ Receivable xxx____ Revenue xxx

Error:Too much revenue was accrued

Record an adjusting entry with the accounts reversed. The amount must reduce the revenue account to the correct balance.

Correction:

____ Receivable xxx ____ Revenue xxx

Correcting Accounting Errors

Too little revenue was accrued

Accrued Revenue ErrorsReview: The adjusting entry to accrue revenue is:

____ Receivable xxx ____ Revenue xxx

Record an adjusting entry that increases the revenue account to the correct balance

Error:

Correction:

____ Receivable xxx ____ Revenue xxx

Correcting Accounting Errors

Accrued Revenue ErrorsExampleAdviceCo is doing a $30,000 consulting job and will be paid upon completion. At year end, 30% of the job has been completed.

The year-end AJE should be:Accts. Receivable

Consulting Rev. 9,000

9,000

If no AJE was recorded, the correction is simply to record it:

Accts. Receivable Consulting Rev. (a) failed to record an AJE

Correct the error if AdviceCo:9,000

9,000

Correcting Accounting Errors

Accrued Revenue Errors

The year-end AJE should be:Accts. Receivable

Consulting Rev. 9,000

9,000

But AdviceCo recorded:Accts. Receivable

Consulting Rev.

(b) accrued 40% (instead of 30%) of $30,000

(a) failed to record an AJECorrect the error if AdviceCo:

12,00012,000

Accts. Receivable Consulting Rev.

3,0003,000

The correcting journal entry is:

ExampleAdviceCo is doing a $30,000 consulting job and will be paid upon completion. At year end, 30% of the job has been completed.

Correcting Accounting Errors

Accrued Revenue Errors

The year-end AJE should be:Accts. Receivable

Consulting Rev. 9,000

9,000

But AdviceCo recorded:Accts. Receivable

Consulting Rev.

(c) accrued 20% (instead of 30%) $30,000

(b) accrued 40% (instead of 30%) of $30,000

(a) failed to record an AJECorrect the error if AdviceCo:

6,0006,000

The correcting journal entry is:Accts. Receivable

Consulting Rev. 3,000

3,000

ExampleAdviceCo is doing a $30,000 consulting job and will be paid upon completion. At year end, 30% of the job has been completed.

Correcting Accounting Errors

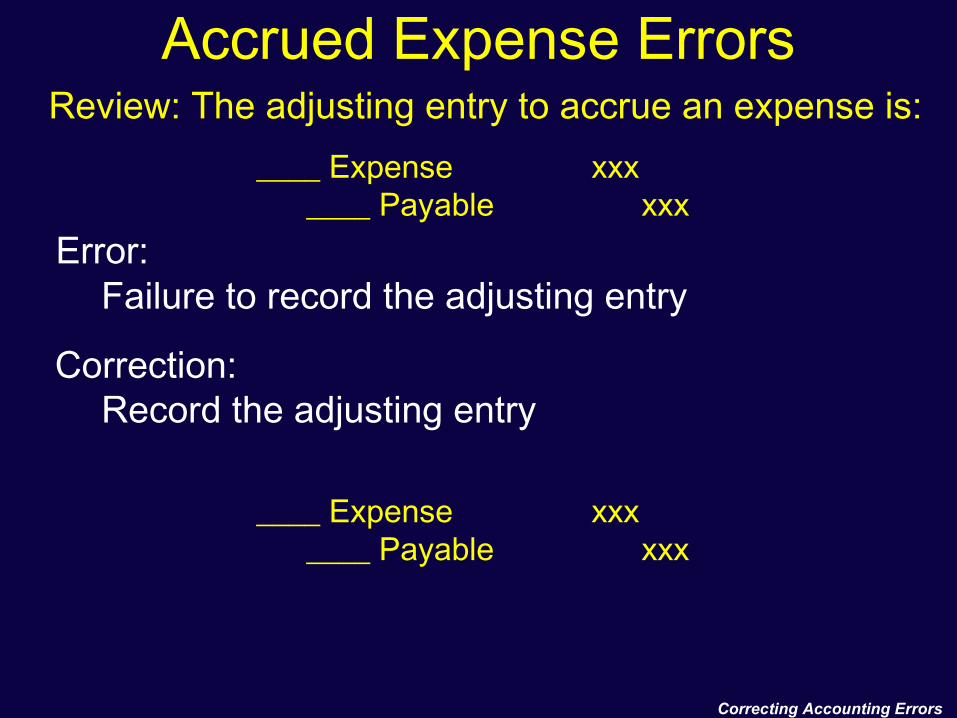

Accrued Expense ErrorsReview: The adjusting entry to accrue an expense is:

____ Expense xxx____ Payable xxx

Error:Failure to record the adjusting entry

Correction:Record the adjusting entry

____ Expense xxx____ Payable xxx

Correcting Accounting Errors

Accrued Expense ErrorsReview: The adjusting entry to accrue an expense is:

____ Expense xxx ____ Payable xxx

Error:Too much expense was accrued

Record an adjusting entry that reduces the expense account to the correct balance

Correction:

____ Expense xxx____ Payable xxx

Correcting Accounting Errors

Too little expense was accrued

Accrued Expense ErrorsReview: The adjusting entry to accrue an expense is:

____ Expense xxx ____ Payable xxx

Record an adjusting entry that increases the expense account to the correct balance

Error:

Correction:

____ Expense xxx____ Payable xxx

Correcting Accounting Errors

Accrued Expense ErrorsExampleClarkCo takes a $50,000 loan at an annual interest rate of 12%. Interest is paid twice a year on 2/1 and 8/1. The last payment was on 8/1 this year.

The year-end AJE should be:Interest Exp.

Interest Payable 2,500

2,500

If ClarkCo failed to record an AJE, the correction is simply to record it:

(a) failed to record an AJECorrect the error if ClarkCo:

Interest Exp. Interest Payable

2,5002,500

Correcting Accounting Errors

Interest Payable

Accrued Expense Errors

The year-end AJE should be:

But ClarkCo recorded the following entry:

Therefore, the correcting entry is:

Interest Exp. Interest Payable

2,5002,500

Interest Exp. Interest Payable

3,0003,000

Interest Exp. 500

500

(b) accrued 6 (instead of 5) months’ interest

(a) failed to record an AJE

ExampleClarkCo takes a $50,000 loan at an annual interest rate of 12%. Interest is paid twice a year on 2/1 and 8/1. The last payment was on 8/1 this year.

Correct the error if ClarkCo:

Correcting Accounting Errors

Accrued Expense Errors

The year-end AJE should be:

But ClarkCo recorded the following entry:

Therefore, the correcting entry is:

Interest Exp. Interest Payable

2,5002,500

Interest Exp. Interest Payable

1,5001,500

Interest Exp. Interest Payable

1,0001,000(c) accrued 3 (instead of 5)

months’ interest

(b) accrued 6 (instead of 5) months’ interest

(a) failed to record an AJE

ExampleClarkCo takes a $50,000 loan at an annual interest rate of 12%. Interest is paid twice a year on 2/1 and 8/1. The last payment was on 8/1 this year.

Correct the error if ClarkCo:

Correcting Accounting Errors

Deferred Expense ErrorsRecall from Mastering Adjusting Entries that a deferred expense is a prepaid expense.The original entry may have an included an asset account—or an expense account:

Thus, the adjusting entry was either:

Prepaid Exp. xxxCash

xxx

Expense xxxCash xxx

Expense xxxPrepaid Exp. xxx

Prepaid Exp. xxxExpense xxx

Correcting Accounting Errors

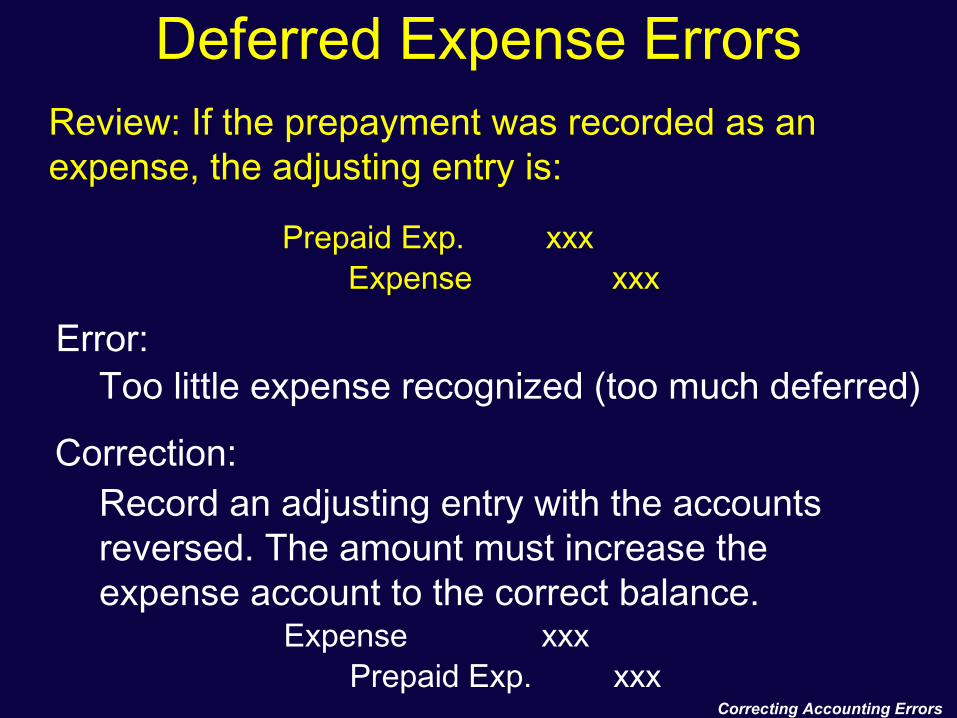

Deferred Expense ErrorsReview: If the prepayment was recorded as an asset (prepaid expense), the adjusting entry is:

Error:Failure to record the adjusting entry

Correction:Record the adjusting entry

Expense xxxPrepaid Exp. xxx

Expense xxxPrepaid Exp. xxx

Correcting Accounting Errors

Deferred Expense ErrorsReview: If the prepayment was recorded as an asset (prepaid expense), the adjusting entry is:

Too much expense was recognized

Record an adjusting entry with the accounts reversed. The amount must reduce the expense account to the correct balance.

Error:

Correction:

Expense xxxPrepaid Exp. xxx

Prepaid Exp. xxxExpense xxx

Correcting Accounting Errors

Too little expense was recognized

Deferred Expense ErrorsReview: If the prepayment was recorded as an asset (prepaid expense), the adjusting entry is:

Record an adjusting entry that increases the expense account to the correct balance

Error:

Correction:

Expense xxxPrepaid Exp. xxx

Expense xxxPrepaid Exp. xxx

Correcting Accounting Errors

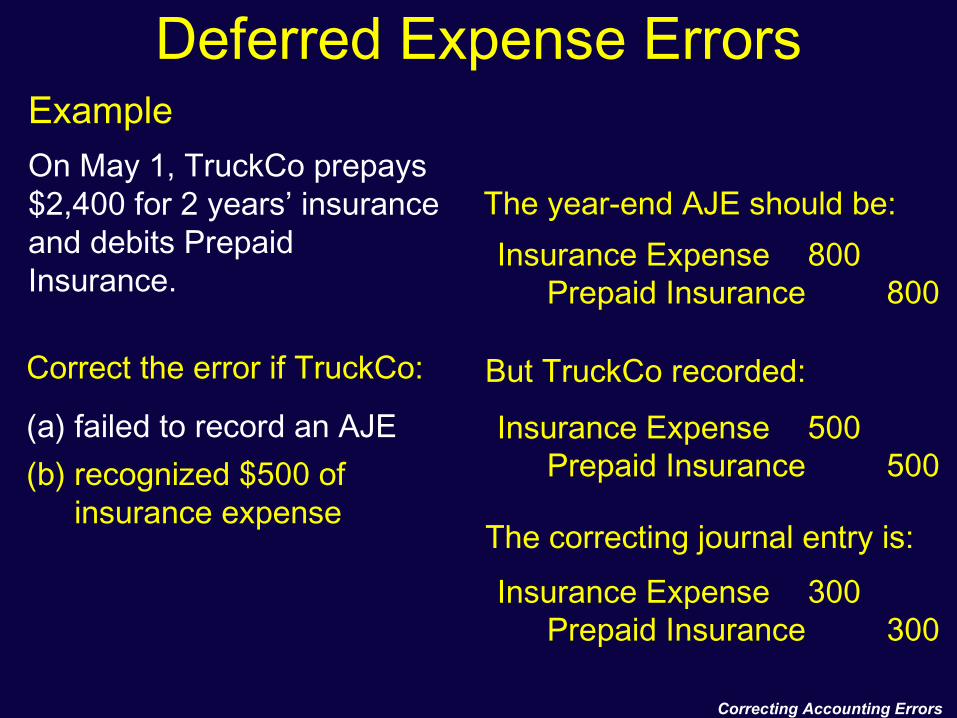

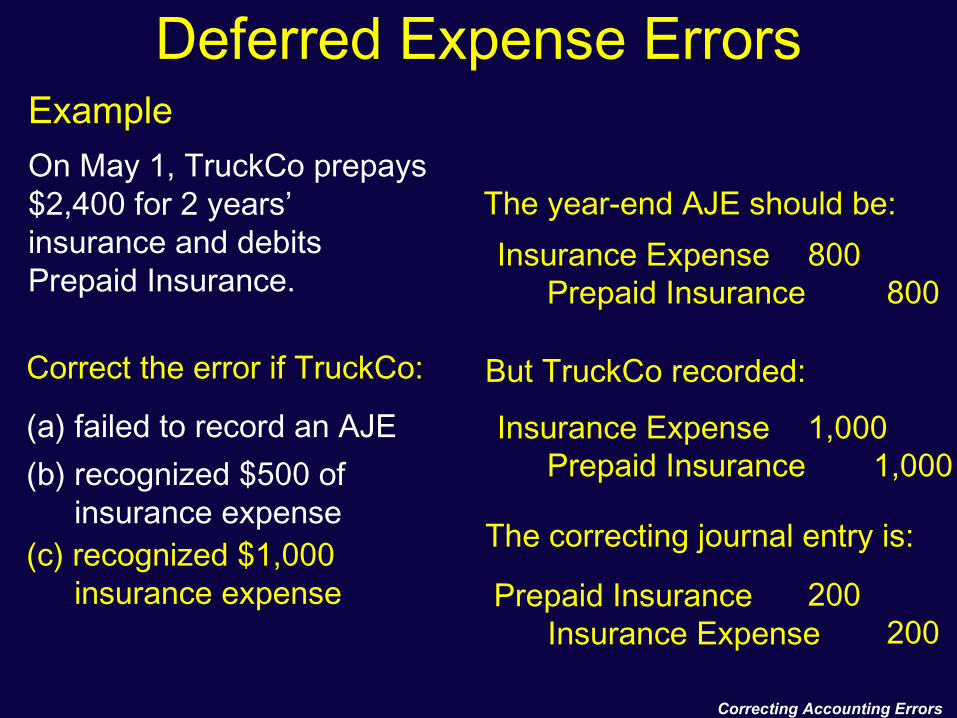

Deferred Expense Errors

The year-end AJE should be:Insurance Expense

Prepaid Insurance800

800

If no AJE was recorded, the correction is simply to record it:Insurance Expense

Prepaid Insurance800

800

ExampleOn May 1, TruckCo prepays $2,400 for 2 years’ insurance and debits Prepaid Insurance.

(a) failed to record an AJE.

Correct the error if TruckCo:

Correcting Accounting Errors

Deferred Expense Errors

The year-end AJE should be:Insurance Expense

Prepaid Insurance800

800

But TruckCo recorded:

(b) recognized $500 of insurance expense

(a) failed to record an AJE Insurance Expense Prepaid Insurance

500500

The correcting journal entry is:

Insurance Expense Prepaid Insurance

300300

Correct the error if TruckCo:

ExampleOn May 1, TruckCo prepays $2,400 for 2 years’ insurance and debits Prepaid Insurance.

Correcting Accounting Errors

Deferred Expense Errors

The year-end AJE should be:Insurance Expense

Prepaid Insurance800

800

(c) recognized $1,000 insurance expense

(b) recognized $500 of insurance expense

(a) failed to record an AJE Insurance Expense Prepaid Insurance

1,0001,000

Insurance Expense Prepaid Insurance 200

200

But TruckCo recorded:

The correcting journal entry is:

ExampleOn May 1, TruckCo prepays $2,400 for 2 years’ insurance and debits Prepaid Insurance.

Correct the error if TruckCo:

Correcting Accounting Errors

Deferred Expense ErrorsReview: If the prepayment was recorded as an expense, the adjusting entry is:

Error:Failure to record the AJE

Correction:Record the AJE:

Expense xxxPrepaid Exp. xxx

Expense xxxPrepaid Exp. xxx

Correcting Accounting Errors

Too much expense recognized (too little deferred)

Deferred Expense Errors

Record an adjusting entry that reduces the expense account to the correct balance

Error:

Correction:

Expense xxxPrepaid Exp. xxx

Review: If the prepayment was recorded as an expense, the adjusting entry is:

Expense xxxPrepaid Exp. xxx

Correcting Accounting Errors

Deferred Expense ErrorsReview: If the prepayment was recorded as an expense, the adjusting entry is:

Record an adjusting entry with the accounts reversed. The amount must increase the expense account to the correct balance.

Error:

Correction:

Too little expense recognized (too much deferred)

Prepaid Exp. xxxExpense xxx

Expense xxxPrepaid Exp. xxx

Correcting Accounting Errors

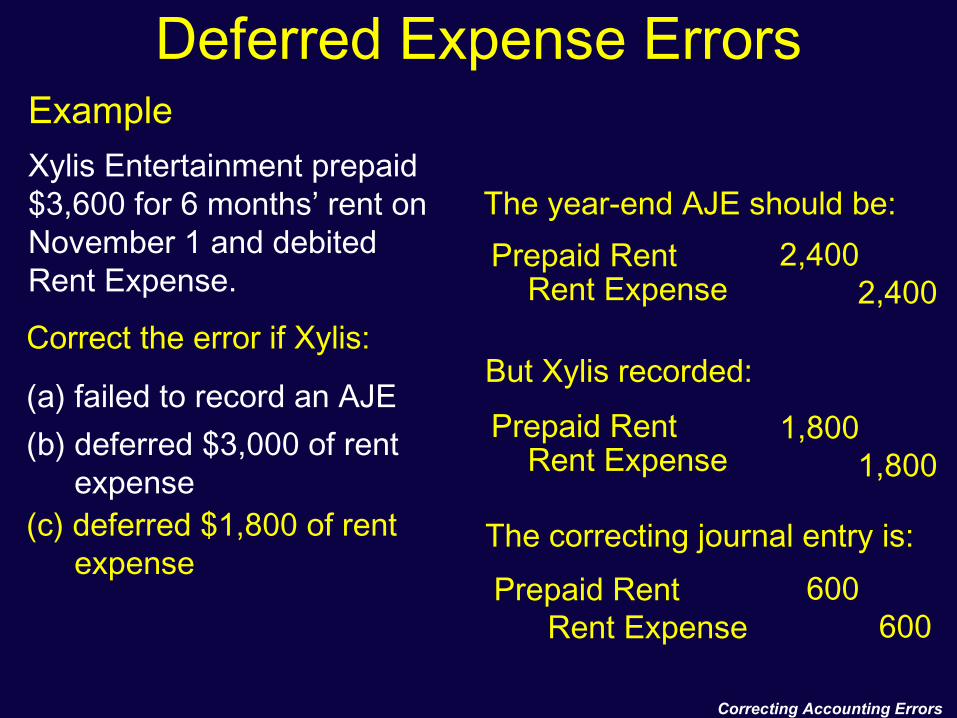

Deferred Expense ErrorsExampleXylis Entertainment prepaid $3,600 for 6 months’ rent on November 1 and debited Rent Expense.

The year-end AJE should be:

Rent Expense Prepaid Rent

2,400

If Xylis failed to record an AJE, the correction is simply to record it:

(a) failed to record an AJE

Correct the error if Xylis:

Rent Expense Prepaid Rent 2,400

2,400

2,400

Correcting Accounting Errors

Deferred Expense Errors

The year-end AJE should be:

But Xylis recorded:

(b) deferred $3,000 of rent expense

(a) failed to record an AJE

Correct the error if Xylis:

3,0003,000

The correcting journal entry is:

Rent Expense Prepaid Rent

600600

Rent Expense Prepaid Rent

2,400

Rent Expense Prepaid Rent

ExampleXylis Entertainment prepaid $3,600 for 6 months’ rent on November 1 and debited Rent Expense.

2,400

Correcting Accounting Errors

Deferred Expense Errors

The year-end AJE should be:

But Xylis recorded:

(c) deferred $1,800 of rent expense

(b) deferred $3,000 of rent expense

(a) failed to record an AJE1,800

1,800

Rent Expense Prepaid Rent 600

600

Rent Expense Prepaid Rent 2,400

Rent Expense Prepaid Rent

Correct the error if Xylis:

The correcting journal entry is:

ExampleXylis Entertainment prepaid $3,600 for 6 months’ rent on November 1 and debited Rent Expense. 2,400

Correcting Accounting Errors

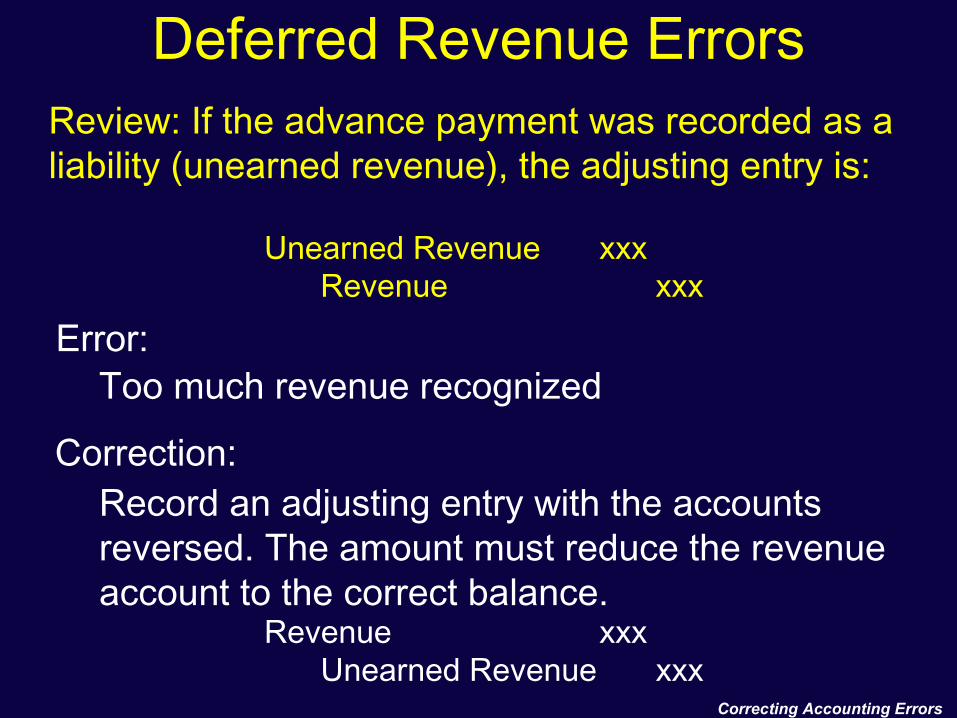

Deferred Revenue ErrorsReview: If the advance payment was recorded as a liability (unearned revenue), the adjusting entry is:

Error:Failure to record the AJE

Correction:Record the AJE

Unearned Revenue xxxRevenue xxx

Unearned Revenue xxxRevenue xxx

Correcting Accounting Errors

Deferred Revenue Errors

Too much revenue recognized

Record an adjusting entry with the accounts reversed. The amount must reduce the revenue account to the correct balance.

Error:

Correction:

Review: If the advance payment was recorded as a liability (unearned revenue), the adjusting entry is:

Unearned Revenue xxxRevenue xxx

Revenue xxxUnearned Revenue xxx

Correcting Accounting Errors

Too little revenue recognized

Deferred Revenue Errors

Record an adjusting entry that increases the revenue account to the correct balance

Error:

Correction:

Review: If the advance payment was recorded as a liability (unearned revenue), the adjusting entry is:

Unearned Revenue xxxRevenue xxx

Unearned Revenue xxxRevenue xxx

Correcting Accounting Errors

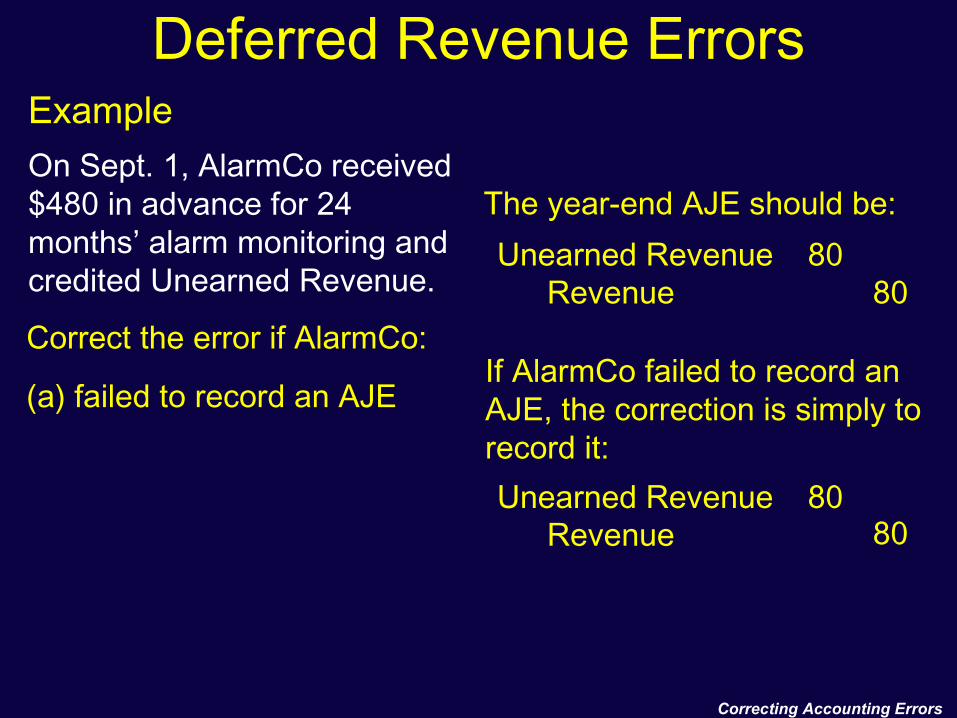

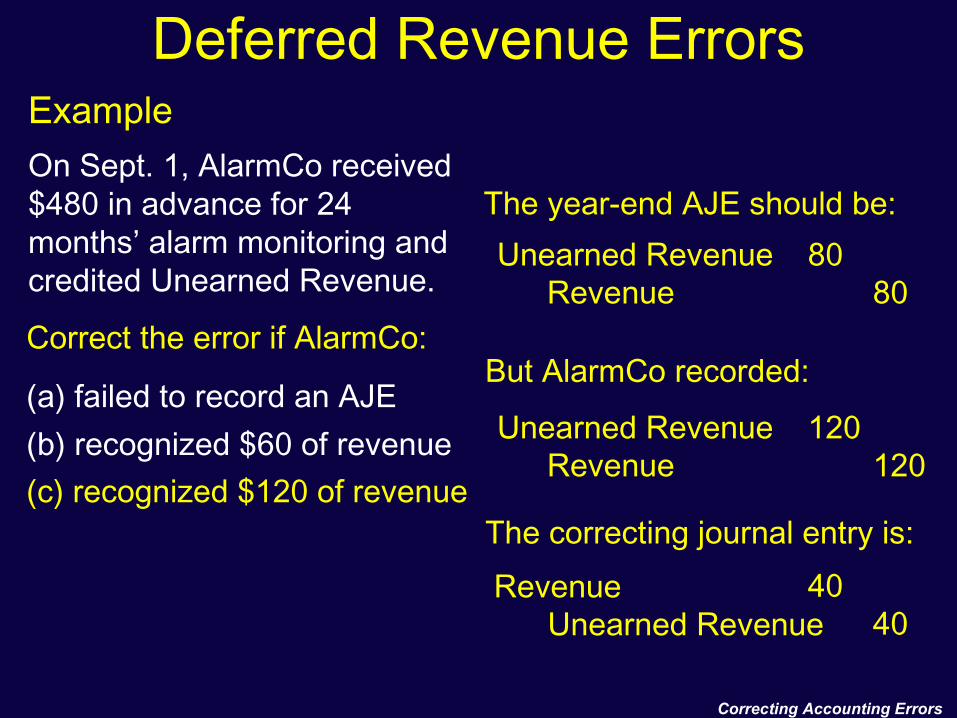

Deferred Revenue ErrorsExampleOn Sept. 1, AlarmCo received $480 in advance for 24 months’ alarm monitoring and credited Unearned Revenue.

The year-end AJE should be:Unearned Revenue

Revenue80

80

If AlarmCo failed to record an AJE, the correction is simply to record it:

(a) failed to record an AJE

Correct the error if AlarmCo:

Unearned RevenueRevenue

8080

Correcting Accounting Errors

Deferred Revenue Errors

But AlarmCo recorded:

Unearned RevenueRevenue

6060

The correcting journal entry is:Unearned Revenue

Revenue20

20

The year-end AJE should be:Unearned Revenue

Revenue80

80

(b) recognized $60 of revenue(a) failed to record an AJE

Correct the error if AlarmCo:

ExampleOn Sept. 1, AlarmCo received $480 in advance for 24 months’ alarm monitoring and credited Unearned Revenue.

Correcting Accounting Errors

Deferred Revenue Errors

But AlarmCo recorded:

Unearned RevenueRevenue

120120

The correcting journal entry is:

Unearned RevenueRevenue 40

40

The year-end AJE should be:Unearned Revenue

Revenue80

80

(c) recognized $120 of revenue(b) recognized $60 of revenue(a) failed to record an AJE

Correct the error if AlarmCo:

ExampleOn Sept. 1, AlarmCo received $480 in advance for 24 months’ alarm monitoring and credited Unearned Revenue.

Correcting Accounting Errors

Deferred Revenue ErrorsReview: If the advance payment was recorded as revenue, the adjusting entry is:

Error:Failure to record the AJE

Correction:Record the AJE

Revenue xxxUnearned Revenue xxx

Revenue xxxUnearned Revenue xxx

Correcting Accounting Errors

Too much revenue recognized

Deferred Revenue Errors

Record an adjusting entry that reduces the revenue account to the correct balance

Error:

Correction:

Revenue xxxUnearned Revenue xxx

Review: If the advance payment was recorded as revenue, the adjusting entry is:

Revenue xxxUnearned Revenue xxx

Correcting Accounting Errors

Deferred Revenue Errors

Too little revenue recognized (too much deferred)

Record an adjusting entry with the accounts reversed. The amount must increase the revenue account to the correct balance.

Error:

Correction:

Review: If the advance payment was recorded as revenue, the adjusting entry is:

Revenue xxxUnearned Revenue xxx

Unearned Revenue xxxRevenue xxx

Correcting Accounting Errors

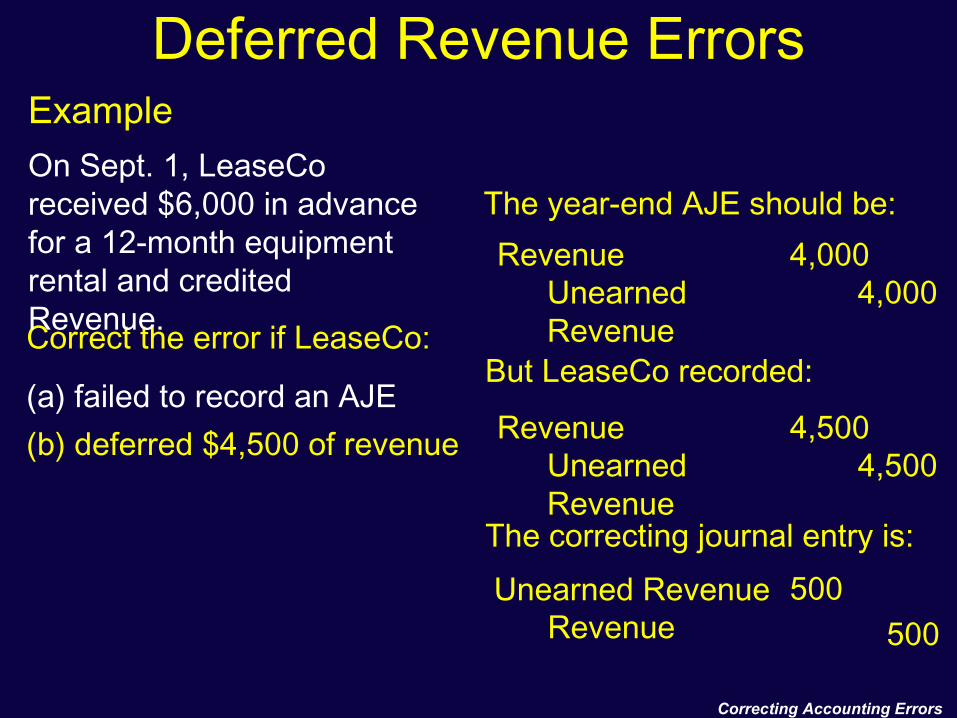

Deferred Revenue ErrorsExampleOn Sept. 1, LeaseCo received $6,000 in advance for a 12-month equipment rental and credited Revenue.

The year-end AJE should be:Revenue

Unearned Revenue

4,0004,000

If LeaseCo failed to record an AJE, the correction is simply to record it:

(a) failed to record an AJE

Correct the error if LeaseCo:

RevenueUnearned Revenue

4,0004,000

Correcting Accounting Errors

Deferred Revenue Errors

But LeaseCo recorded:

RevenueUnearned Revenue

4,5004,500

The correcting journal entry is:

RevenueUnearned Revenue 500

500

The year-end AJE should be:Revenue

Unearned Revenue

4,0004,000

(b) deferred $4,500 of revenue(a) failed to record an AJE

Correct the error if LeaseCo:

ExampleOn Sept. 1, LeaseCo received $6,000 in advance for a 12-month equipment rental and credited Revenue.

Correcting Accounting Errors

Deferred Revenue Errors

RevenueUnearned Rev.

1,5001,500

RevenueUnearned Rev.

2,5002,500

The year-end AJE should be:Revenue

Unearned Revenue

4,0004,000

(a) failed to record an AJE

(c) deferred $1,800 of revenue(b) deferred $3,600 of revenue

But LeaseCo recorded:

The correcting journal entry is:

Correct the error if LeaseCo:

ExampleOn Sept. 1, LeaseCo received $6,000 in advance for a 12-month equipment rental and credited Revenue.