Powering through the storm

Danie Mouton

Carbon Manager, Growth

Exxaro Resources Ltd

South African Coal Exports Conference 2009

Cape Town

5 February 2009

2

Sunday Times, 25 January 2009

3

• Introduction to Exxaro

• World economic crisis – Severity and impact

• World economic crisis – All doom and gloom?

• Coal – Blown away or riding the storm?

• Conclusion

Agenda

4Introduction to Exxaro

COALthe fourth largest coal producer in South Africa MINERAL SANDSone of the world's top three producers of zircon and chlorinatable TiO2 slag

BASE METALS AND INDUSTRIAL MINERALSthe only zinc producer in South Africa

IRON ORE20% holding in Sishen Iron Ore Company

Our commodities At a glance…

One of the largest South African based diversified resources company

An ALSI Top 40 company, listed on the JSE

Over 9 000 employees

Revenue: R5.8bn* (±US$ 0.8bn)

Net operating profit: R806m* (±US$107m)

Operations in South Africa, Australia, Namibia and China

53% BEE ownership

* H1 2008 (6 months) results

5

The world economic crisis – severity and impact

6

Source: Global Insight

World crisis – GDP growth

-4

-2

0

2

4

6

8

10

Ja

n-7

1

Ja

n-7

3

Ja

n-7

5

Ja

n-7

7

Ja

n-7

9

Ja

n-8

1

Ja

n-8

3

Ja

n-8

5

Ja

n-8

7

Ja

n-8

9

Ja

n-9

1

Ja

n-9

3

Ja

n-9

5

Ja

n-9

7

Ja

n-9

9

Ja

n-0

1

Ja

n-0

3

Ja

n-0

5

Ja

n-0

7

Ja

n-0

9

Ja

n-1

1

Gro

wth

Ra

te (

% C

ha

ng

e)

World USA Western Europe Japan

Oil crisis Oil crisisStock market

crashAsian crisis

Dotcom bubbleburst

September 11

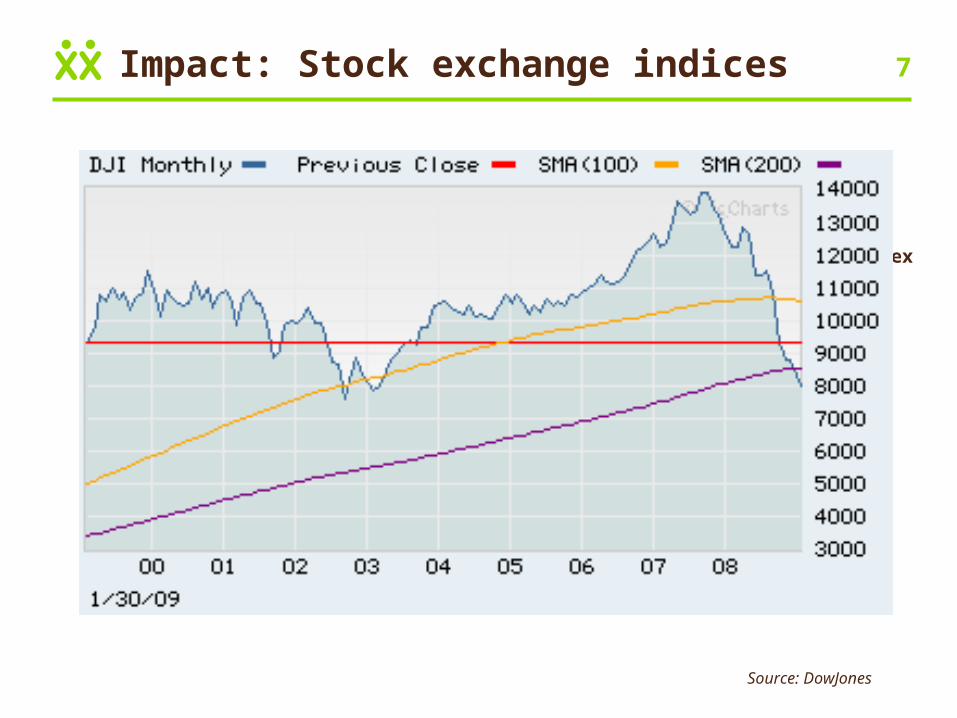

7Impact: Stock exchange indices

Source: DowJones

JSE Industrial Index Dow Jones Industrial Index

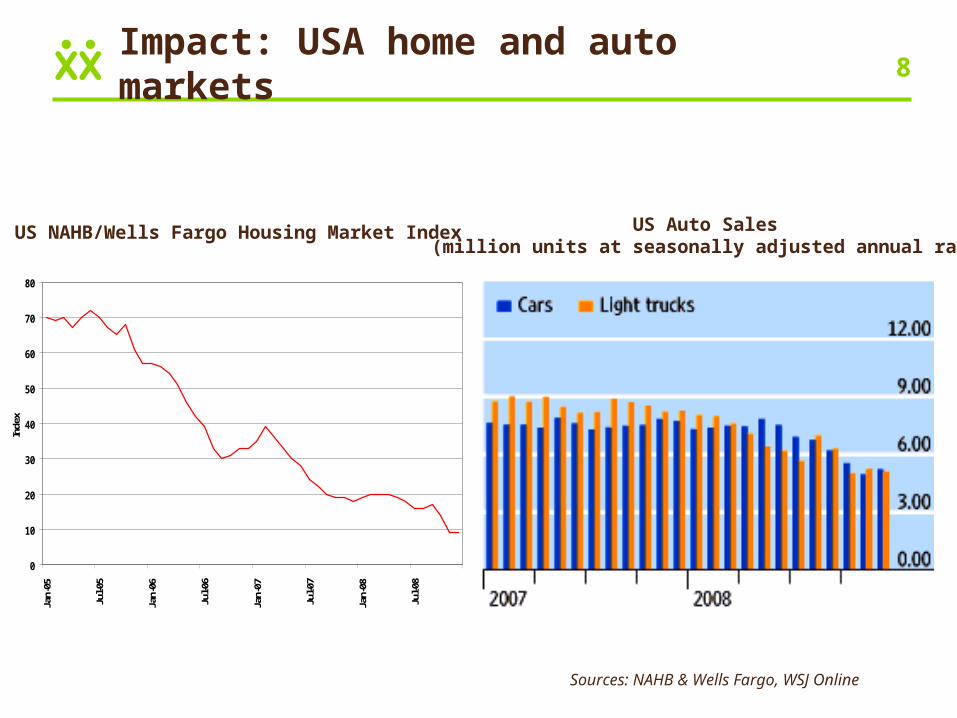

8Impact: USA home and auto markets

Sources: NAHB & Wells Fargo, WSJ Online

US NAHB/Wells Fargo Housing Market Index US Auto Sales (million units at seasonally adjusted annual rate)

0

10

20

30

40

50

60

70

80

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Inde

x

9Impact: Commodity prices

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000Ja

n-0

0A

pr-

00Ju

l-00

Oct

-00

Jan

-01

Ap

r-01

Jul-

01O

ct-0

1Ja

n-0

2A

pr-

02Ju

l-02

Oct

-02

Jan

-03

Ap

r-03

Jul-

03O

ct-0

3Ja

n-0

4A

pr-

04Ju

l-04

Oct

-04

Jan

-05

Ap

r-05

Jul-

05O

ct-0

5Ja

n-0

6A

pr-

06Ju

l-06

Oct

-06

Jan

-07

Ap

r-07

Jul-

07O

ct-0

7Ja

n-0

8A

pr-

08Ju

l-08

Oct

-08

Cu

& Z

n P

rice

s (U

S$/

t)

0

20

40

60

80

100

120

140

160

180

Co

al &

Oil

Pri

ces

((U

S$/

t &

US

$/b

bl)

Copper Zinc Brent Crude RBCT Steam CoalSource: I-Net

10

The world economic crisis – all doom and gloom?

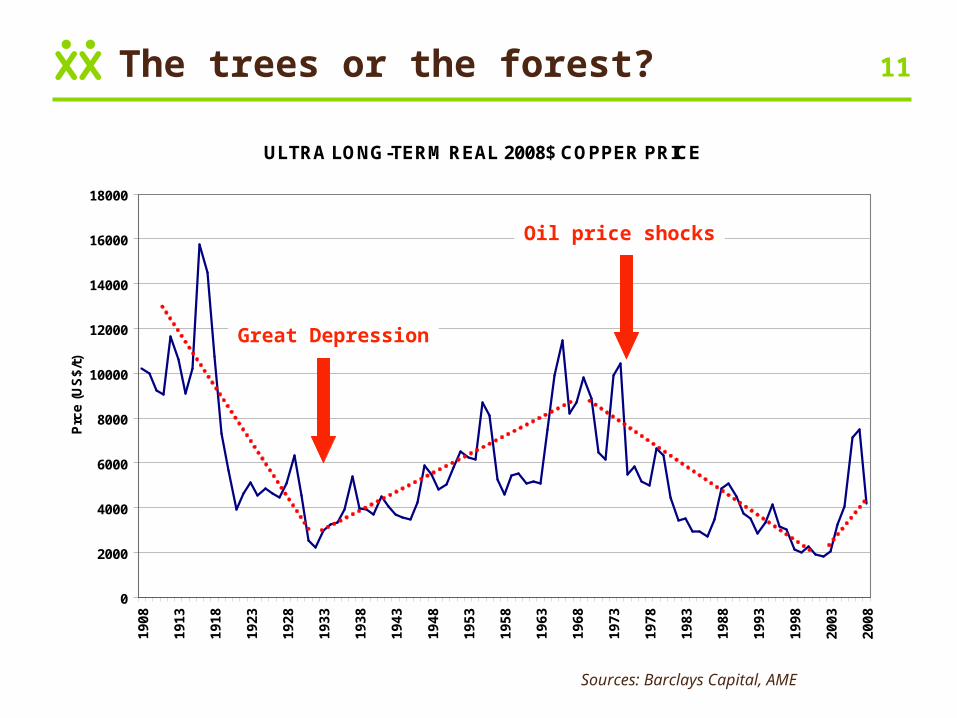

11The trees or the forest?

Sources: Barclays Capital, AME

ULTRA LONG-TERM REAL 2008$ COPPER PRICE

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

19

08

19

13

19

18

19

23

19

28

19

33

19

38

19

43

19

48

19

53

19

58

19

63

19

68

19

73

19

78

19

83

19

88

19

93

19

98

20

03

20

08

Prc

e (

US

$/t

)

Great Depression

Oil price shocks

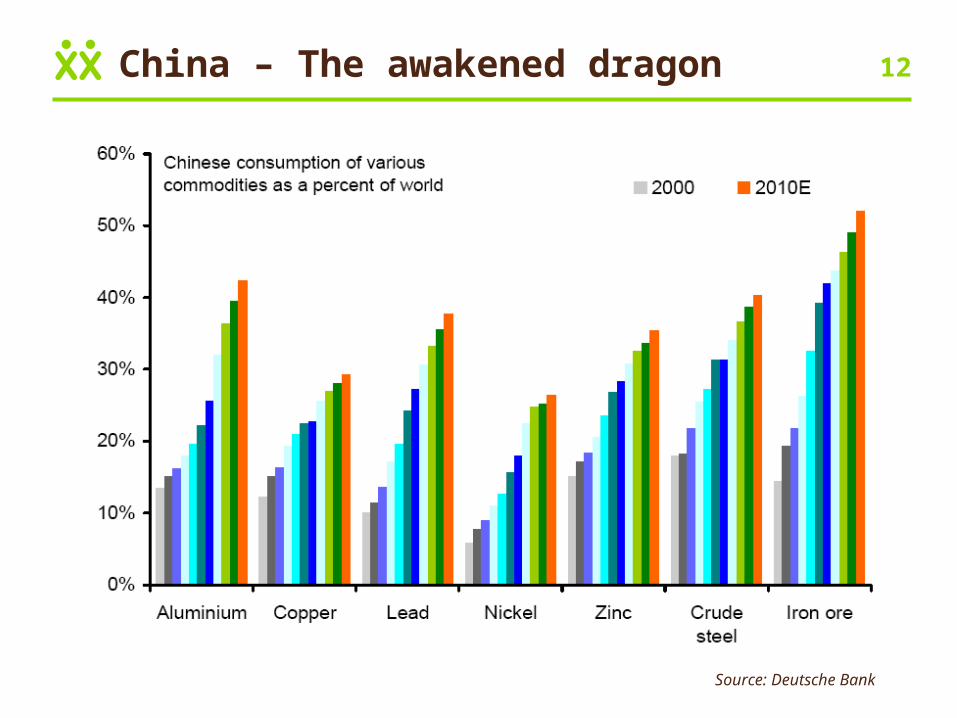

12China – The awakened dragon

Source: Deutsche Bank

13

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

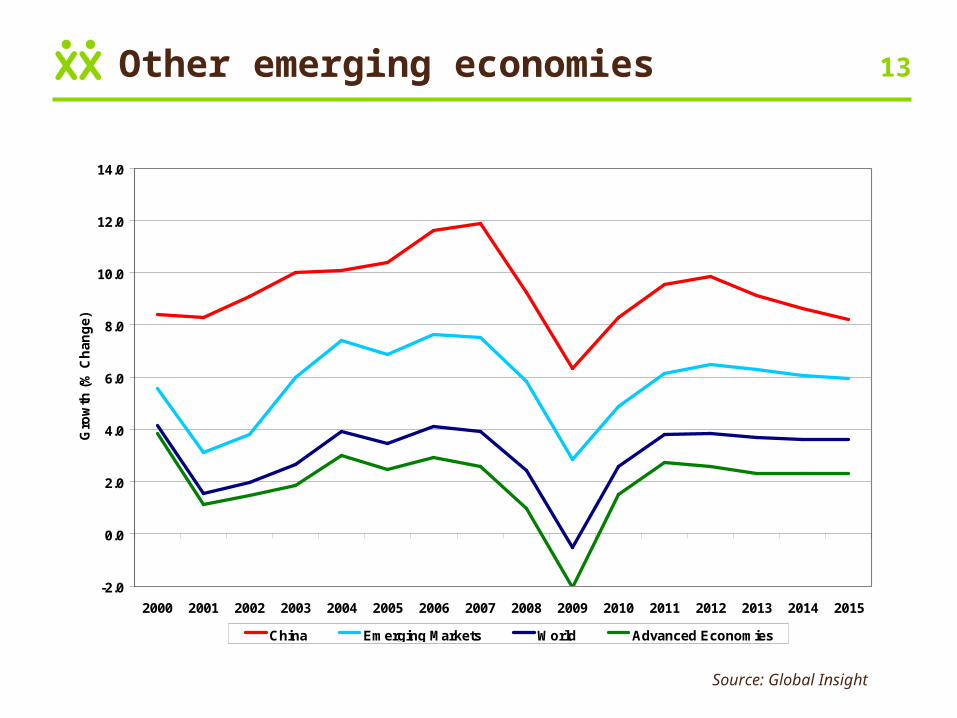

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Gro

wth

(%

Ch

an

ge

)

China Emerging Markets World Advanced Economies

Source: Global Insight

Other emerging economies

14

Sources: Citigroup, Barclays Capital, Brook Hunt, Deutsche Bank, JB Were, Macquarie, Standard Bank

0

20

40

60

80

100

120

140

160

2008 2009 2010 2011 2012

Ind

ex (

2008

= 1

00)

Zinc Rutile Zircon Steam Coal Iron Ore Fines Hard Coking Coal

Real LT Prices

$1680/t

$500/t

$712/t

$66/t

USc74/mtu

$115/t

Commodity prices – recovery?

15

Source: I-Net

4

5

6

7

8

9

10

11

12

13

Ja

n-0

0

Ma

y-0

0

Se

p-0

0

Ja

n-0

1

Ma

y-0

1

Se

p-0

1

Ja

n-0

2

Ma

y-0

2

Se

p-0

2

Ja

n-0

3

Ma

y-0

3

Se

p-0

3

Ja

n-0

4

Ma

y-0

4

Se

p-0

4

Ja

n-0

5

Ma

y-0

5

Se

p-0

5

Ja

n-0

6

Ma

y-0

6

Se

p-0

6

Ja

n-0

7

Ma

y-0

7

Se

p-0

7

Ja

n-0

8

Ma

y-0

8

Se

p-0

8

Ja

n-0

9

Ex

ch

an

ge

Ra

teExchange rate – protection?

16The glass is half full!

• Lower energy costs (oil price)

• Rational filtering of asset quality

• Slow-down of capex escalation

• Greater willingness and incentive to form synergistic alliances

• Diversification potential (some assets are cheap now…)

• Skills retention

17

Coal – Blown away or riding the storm?

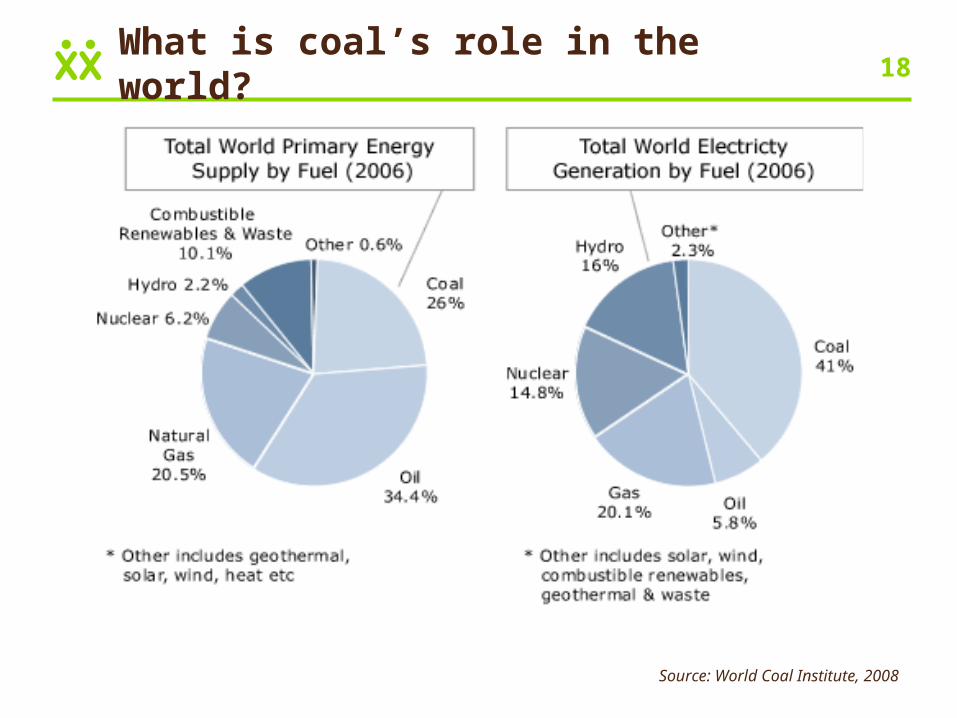

18What is coal’s role in the world?

Source: World Coal Institute, 2008

19Does coal have a future role to play?

Source: IEA, 2006

• Fossil fuels remain dominant source of energy – 83% of the overall increase in energy demand

• Coal sees the biggest increase in demand in absolute terms (59% by 2030), while non-hydro

renewables grow fastest, but from a small base

20Is there enough coal?

21

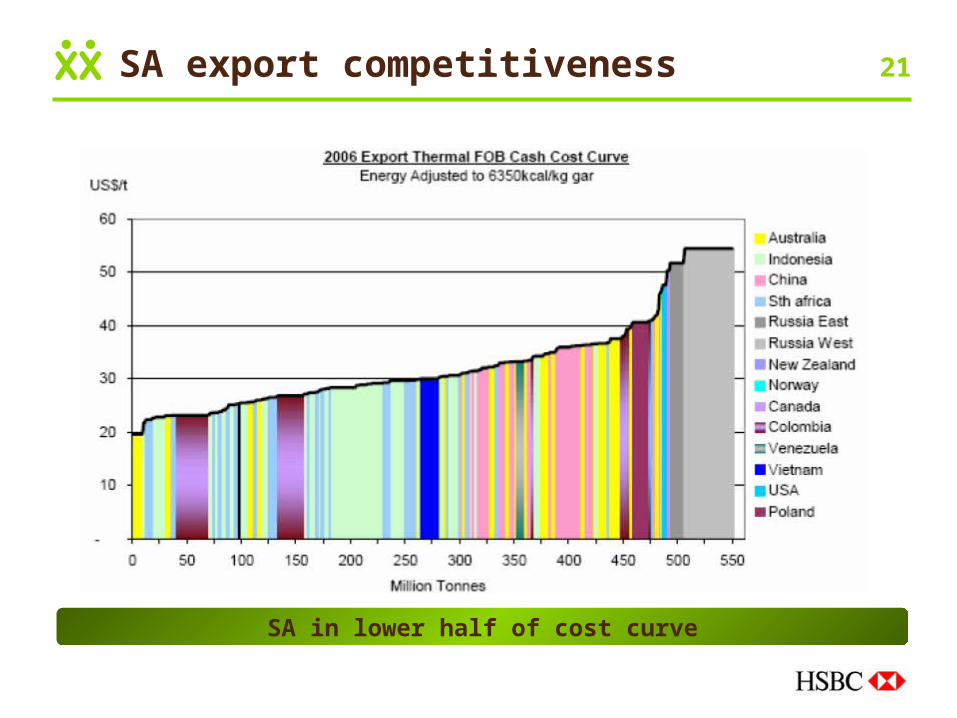

SA in lower half of cost curve

SA export competitiveness

22Logistics is the key

MineralResource

LogisticsMarket

Products

MineralReserve

MineralDeposit/Rights

Losses

Losses

Losses

Losses

Conversion through Technology

Mining Beneficiation

Losses

ROM

Losses

Losses

Losses

Typical

OC Mine10%

losses

3 to 5%

dilution

6% to slimes

85% organic eff

3%losses

Due to Quality

variation

60 to 120%

Of Costs

20%margin

Loss due

To over/under

spec

At least 45% of value destruction across value chain

Source: Exxaro company analysis

23It’s time to work together

In order to have reached its annual capacity target of 76Mtpa during 2008,

producers would have had to produce, TFR would have had to rail, and

RBCT would have had to ship an average of 6.3Mtpm during the year.

Source: Barlow Jonker, 2009

24

Conclusion

25Power through the storm – together

• Cost discipline

• Improve efficiencies

• Spend cash wisely

• Create alliances

• Minimise value losses across value chain – exploit synergies

• Collectively develop logistical solutions for the coal business

BUSINESS AS IT USUALLY SHOULD BE

26Final thought

“As the credit crunch threatens to become a global

downturn, corporate leaders have a choice: pull in

their horns and ride out the storm or look for

opportunities to pick up bargain-basement assets

that will help them grow and create future value for

shareholders. If past is prologue, more will follow

the first course – which is a mistake.”

M&A strategies in a down market

The McKinsey Quarterly, September 2008

27

THANK YOU