Type of document: Procedure Code: < > Title: Procedure Governing Transactions with Related Parties Edition/Revision: V1R0

1/23

PROCEDURE GOVERNING

TRANSACTIONS WITH RELATED PARTIES

Approved by the Board of Directors on November 11, 2010

2

CONTENTS

1. Reference Statutes and Principles............................................................................3

2. Scope of Implementation ...........................................................................................3

3. Definitions ..................................................................................................................3

3.1 Designation of Related Parties ..............................................................................4 3.2 Designation of Transactions with Related Parties ...............................................5

4. Adoption of the Procedure – General Criteria.............................................................5

5. Composition of the Committee Responsible for Reviewing Transactions with Related Parties and Committee Activities .......................................................................6

5.1 Composition of the Committee...................................................................................6 5.2 Role of the Committee.................................................................................................7

6. Transactions with Related Parties ............................................................................8

6.1 Highly Material Transactions ......................................................................................8 6.1.1 Definitions ...............................................................................................................8 6.1.2 Handling of Highly Material Transactions ................................................................8 6.1.3 Transactions Falling Within the Purview of the Shareholders’ Meeting............10 6.1.4 Amendments to the Bylaws Concerning Whitewash Transactions and Urgent Cases, Including Also Those Arising When a Business Is in Crisis Mode.....................11

6.2 Less Material Transactions ..................................................................................11 6.2.1 Definition ...............................................................................................................11 6.2.2 Handling of Less Material Transactions ................................................................11

6.3 Transactions of Not Material Amount .................................................................12 6.4 Atypical or Unusual Transactions .......................................................................12 6.5 Transactions Executed Through Subsidiaries ...................................................12

7. Framework Resolutions ...........................................................................................13

8. Waiver Availability Instances and Options.............................................................13

9. Public Disclosure of Transactions With Related Parties..........................................17

10. Controls Monitoring the Procedure’s Implementation ..........................................17

11. Updates to and Implementation of the Procedure .................................................18

12. Closing and Transitional Provisions.......................................................................18

13. Annexes.....................................................................................................................18

13.1 Materiality Thresholds for Transactions with Related Parties.............................19 13.2 Annex 3 to the Regulation: “Designation of Highly Material Transactions with Related Parties” ...............................................................................................................20 13.3 Affidavit Form ..........................................................................................................22

3

1. Reference Statutes and Principles This procedure (hereinafter referred to as the “Procedure”) is being adopted to comply with the

requirements of Article 2391-bis of the Italian Civil Code, of Articles 113-ter, 114, 115 and 154-ter

of Legislative Decree No. 58 of February 24, 1998, and of the Regulation setting forth provisions

concerning transactions with related parties enacted by the Consob with Resolution No. 17221 of

March 12, 2010, as amended by Resolution No. 17389 of June 23, 2010 (hereinafter referred to as

the “Regulation”). Lastly, the Procedure takes into account the recommendations of Consob

Communication No. DEM/10078683 of September 24, 2010 (hereinafter referred to as the “Consob

Communication”).

2. Scope of Implementation Transactions with related parties are particularly relevant with regard to three main issues: the

identification of the counterparties, the handling process and the transparency of disclosures.

With this in mind, this document sets forth the principles that Parmalat SpA (hereinafter referred to

as “Parmalat”) shall abide by in order to ensure the fairness and transparency of transactions with

related parties that it executes directly or through its subsidiaries.

3. Definitions

Pursuant to the regulations currently in effect, it is important to define and identify the intended

meaning of such expressions as related parties and transactions with related parties.

In analyzing any relationship with a related party, attention must be paid to the substance of the

relationship and not merely to its legal form.

4

3.1 Designation of Related Parties Parmalat’s related parties are the parties defined as such in Annex 1 to the Regulation governing

transactions with related parties.(1)

More specifically, Parmalat considers a party to be a related party if the party in question:

a) directly or indirectly, through subsidiaries, nominees, third parties or otherwise:

i) controls Parmalat, is controlled by it or is under joint control;

ii) holds an equity interest in Parmalat that enables it to exercise a significant influence(2)

over Parmalat;

iii) exercises control over Parmalat jointly with other parties;

b) is an affiliated company of Parmalat;

c) is a joint venture in which Parmalat is an investor;

d) is one of Parmalat’s Directors or Statutory Auditors;

e) is one of Parmalat’s General Managers (identified as Direttori Generali in Italian);

f) is an executive with strategic responsibilities of Parmalat or its controlling company;

g) is a member of the immediate family of one of the parties listed in letters (a) or (d) or (e) or (f);

h) is an entity over which one of the parties listed in letters (d) or (e) or (f) or (g) exercises

control, joint control or a significant influence or in which one of the abovementioned parties

holds, directly or indirectly, a significant equity interest;

i) is a supplemental, collective or individual, Italian or foreign, pension fund established for the

benefit of Parmalat’s employees or employees of any other entity related to Parmalat.(3)

The parties designated by Parmalat as related parties shall be organized in a list and entered into

a special database that Parmalat shall maintain based on the available evidence (direct related

parties, based on the equity interest relationships and the role performed within the organization)

and affidavits provided by related parties. Parmalat shall approve a special operating protocol

concerning how the database is operated and accessed.

(1) The Extraordinary Commissioner of Parmalat SpA is not a related party, because he is not listed among the parties mentioned in Annex 1 to the regulation. (2) Significant influence shall be understood to mean the power to play a part in determining the financial and operating policies of an entity without controlling it. Significant influence may be achieved through the direct or indirect possession of 20% (10% for publicly traded companies) or more of the shares conveying the right to vote at the shareholders’ meeting of the investee company, or through an equity interest of a different percentage, by virtue of provisions of the Bylaws or shareholders’ agreements. (3) For the purposes of this Procedure, only funds established or promoted by the Company or funds over which the Company can exercise influence are relevant.

5

3.2 Designation of Transactions with Related Parties

The expression transaction with a related party shall be understood to mean any transfer of

resources, services or obligations between related parties, whether consideration is stipulated or not.

More specifically, transactions with related parties include commercial transactions involving the

exchange both of goods and services, financial transactions and transactions involving non-current

assets.

Moreover, transactions with related parties include:

- mergers, demergers through absorption or straight non-proportional demergers,

when executed with related parties;

- any decision involving the award of compensation and economic benefits, in any

form, to members of administration and control bodies and to executives with

strategic responsibilities;

- any collateral or guarantees provided by Parmalat for the benefit or in the interest of

related parties.

4. Adoption of the Procedure – General Criteria Consistent with the principles set forth in the Regulation, the Board of Directors is adopting this

Procedure to ensure that transactions with related parties are transparent and substantively and

procedurally fair.

This Procedure was reviewed in advance by the Internal Control and Corporate Governance

Committee (hereinafter referred to as the “Committee”), consistent with the decision by Parmalat’s

Board of Directors to designate this Committee as the “Committee Comprised Exclusively of

Independent Directors,” which makes it responsible for performing the role required by the

Regulation. Pursuant to Article 148, Section 3, of the Italian Uniform Financial Code and as

required by Corporate Governance Code of Borsa Italiana (Section 3.C.1), the Committee is

comprised of three Independent Directors.

Parmalat’s Board of Directors approved this Procedure on November 11, 2010, as required by the

Consob Regulation.

The Committee shall render an opinion on any amendment to this Procedure before the

amendment is submitted to the Board of Directors for approval.

Moreover, the Chief Executive Officer shall submit to the Board of Directors and the Board of

Statutory Auditors a quarterly report detailing transactions executed with related parties.

6

This Procedure and any amendments to the Procedure shall be made available to the public on the

Company website (www.parmalat.com), without prejudice to the disclosure obligation, which may

be provided by reference to the abovementioned website, applicable to the Annual Report on

Operations pursuant to Article 2391-bis of the Italian Civil Code.

The Chief Executive Officer shall be responsible for adequately disseminating this document within

the Group, particularly with regard to the parties referred to in Section 3.1, Letters d), e) and f),

above.

5. Composition of the Committee Responsible for Reviewing Transactions with Related Parties and Committee Activities 5.1 Composition of the Committee

The Board of Directors designated the Internal Control and Corporate Governance Committee as

the Committee responsible for reviewing transactions with related parties, in view of the fact that all

of its members meet the independence requirements pursuant to Article 148, Section Three, of the

Italian Uniform Financial Code and consistent with the criteria of the Corporate Governance Code

of Borsa Italiana. If a circumstance should occur in which a Committee member were to:

(i) cease to qualify as independent;

(ii) cease to be in office;

(iii) hold an interest with regard to the approval of a transaction with a related party reviewed by the

Committee;

the Committee member in question shall be replaced by the Chairman or (if necessary) by the

most senior member of the Nominating and Compensation Committee, which is also comprised

exclusively of Directors that meet the same independence requirements.

This designation is being made by virtue of the fact that all of the members of the Nominating and

Compensation Committee qualify as independent pursuant to the Regulation.

7

5.2 Role of the Committee

Without prejudice to the jurisdictional attributions set forth in the Regulation and the exclusive

deliberative jurisdiction of the Board of Directors, the Committee shall be allowed to participate in

the negotiations and in the information gathering phase for highly material transactions(1) by

providing it with a complete and timely flow of information and through its right to request

information and make recommendations to the delegated management bodies and the parties

responsible for carrying out the negotiations or the information gathering process. The Board of

Directors shall approve the transaction, after receiving from the Committee a detailed favorable

opinion as to the Company’s interest in executing the transaction and about the transaction’s

suitability and the substantive fairness of the transaction’s terms.

In order for an opinion to qualify as “favorable,” it must express an approval of the transaction in its

entirety. Consequently, an opinion shall be deemed to be a “negative opinion” even if the negative

assessment does not apply to the transaction as a whole. Conversely, a conditional positive

opinion could be deemed to be “favorable” pursuant to the Regulation, provided that the conditions

raised in the opinion are indeed satisfied. In such cases, evidence of compliance with the relevant

conditions shall be provided in the reports on the execution of transactions that must be submitted

to the administration and control bodies.

The Board of Directors may approve highly material transactions despite a negative opinion by the

Independent Directors, provided that, Pursuant to Article 2364, Section 1, Number 5), of the Italian

Civil Code, the execution of the transaction is authorized by the shareholders’ meeting, in a

resolution approved in accordance with the provisions of Article 11, Section 3, of the Regulation,

and that a special provision of the Bylaws allows it(2). Consequently, absent an applicable

provision of the Bylaws, a negative opinion by the Committee Comprised of Independent Directors

will make it impossible to approve a highly material transaction with a related party.

On the other hand, in the case of less material transactions, the Committee is required to render a

detailed opinion, which, however, shall not be binding.

In both cases the Committee’s opinion shall be submitted to the members of the Board of Directors at

least two days before the date of the Board meeting scheduled to deliberate on the transaction. This

document shall set forth in explicit terms whether the Committee supports or rejects the transaction.

If the terms of the transaction are defined as equivalent to market or standard terms, objective

evidence thereof shall be provided the transaction’s supporting documents.

(1) As described in detail in Section 6.1 below. (2 ) The so-called “whitewash” mechanism.

8

If a transaction does not qualify for the exemptions referred to below in Section 8, Letter a),

“Resolutions concerning the compensation1 of Directors and executives serving in special

capacities and managers with strategic responsibilities,” only in this specific case, the Board of

Directors shall designate the Nominating and Compensation Committee as the Committee with

jurisdiction over reviewing the compensation referred to in the abovementioned Section, pursuant

to this Procedure.

6. Transactions with Related Parties 6.1 Highly Material Transactions

6.1.1 Definitions

“Highly material transactions” are transactions that exceed the thresholds set forth in the table

provided in Annex 13.1 to this Procedure and, in any case, transactions in which at least one of the

quantitative materiality indices, computed in accordance with the provisions of Annex 3 to the

Regulation (see Annex 13.2 to this Procedure), as applicable to a specific transaction, exceeds the

threshold set forth therein.

Cumulable transactions, i.e., homogeneous transactions or transactions executed carry out the

same project, which individually do not qualify as highly material transactions but, when viewed

cumulatively, exceed the thresholds set forth in Annex 13.1 to this Procedure, are also defined as

highly material transactions.

6.1.2 Handling of Highly Material Transactions

When highly material transactions are at stake, the Committee shall be allowed to participate in

the information gathering phase and in the negotiations by providing it with a complete and timely

flow of information. The Committee shall have the right to request information and make

recommendations to the delegated management bodies and the parties responsible for carrying

out the negotiations or the information gathering process. The Board of Directors shall proceed

with approving the transaction only after the Committee renders a detailed favorable opinion as to

Parmalat’s interest in executing the transaction and about the suitability and fairness of the

transaction’s terms. Any Director who may have an interest in the transaction, whether direct, 1 Please note that, pursuant to the Consob Communication, the compensation amounts in question are evaluated on an individual basis to determine whether they qualify as highly material or less material. Information about determining the materiality thresholds is provided in Annex 3 to the Regulation.

9

contingent or indirect, shall promptly inform the Board of Directors in detail about the existence of

such interest.

As part of the process of rendering an opinion concerning the execution of a transaction, the

Committee may also seek the support of independent experts of its own choosing, at the Company’s

expense. In principle, there is no requirement that the experts chosen by the Committee be different

from the experts that the Company may have appointed. Therefore, this provision of the Regulation

shall be deemed to have been complied with, even if the members of the Committee are allowed to

designate in advance the experts that the Company may appoint when executing the transaction,

provided that the terms of the engagement specifically require that the experts also and specifically

assist the Independent Directors in the performance of the tasks assigned to them pursuant to the

procedures for transactions with related parties. This specific requirement shall apply regardless of

the type of transaction reviewed by the Independent Directors.

When selecting the experts, the Committee shall choose persons with an established reputation of

professionalism and competency with regard to the subject matter covered by the consulting

assignment and, in all cases, parties that are not in a conflict of interest with regard to the

transaction. The opinion rendered by the experts shall be published on the Parmalat website.

The Committee may also rely on the support of the Administration, Finance and Control

Department or of Internal Auditing in the information gathering phase, or of the Human Resources

Department Corporate for transactions involving the award of compensation and economic benefits

to members of administration and control bodies and to executives with strategic responsibilities.

For this purpose, the parties in charge of the transaction shall promptly prepare a dossier that shall

then be promptly sent to the Committee and the Board of Directors, providing, as a minimum, the

following information:

1. The main features of the transaction (price, execution conditions, payment terms, etc.).

2. The economic justification for executing the transaction.

3. An overview of the transaction’s impact on the income statement, balance sheet and

financial position.

4. The method used to determine the transaction’s consideration and an assessment of the

consideration’s fairness, based on market values for similar transactions. If the economic terms

of the transaction are found to be consistent with market or standard terms, a statement to that

effect shall be provided, together with a listing of objective benchmarks.

5. Whether experts were used for valuation purposes and, in the affirmative, an explanation of

the methods used to determine the consideration’s fairness and a description of any issues

raised by the experts with regard to the transaction in question.

10

The same information, insofar as applicable, shall be included in the dossiers for transaction

involving compensation arrangements.

The Administration, Finance and Control Department and/or Internal Auditing Corporate are

responsible for checking the abovementioned information for completeness, except for issues related

to compensation arrangements, which fall under the jurisdiction of the Human Resources Department.

The opinions rendered by the Committee shall be recorded in the minutes of its meetings.

6.1.3 Transactions Falling Within the Purview of the Shareholders’ Meeting

In urgent cases, including also those arising when a business is in crisis mode, and provided the

Bylaws expressly allow it, transactions with related parties may be executed waiving the

requirement to comply with the provisions of Article 11, Sections 1, 2 and 3, of the Regulation,(1)

provided that the following conditions, as set forth in the Regulation, are satisfied:

a) The proposed transaction must fall within the scope of the powers awarded to the Chief

Executive Officer or the Executive Committee and the Chairman of the Board of Directors

or Managing Board has been informed of the reasons for urgent handling prior to the

transaction’s execution.

b) Without prejudice to their effectiveness, transactions of this type shall be the subject of a

non-binding resolution approved by the first shareholders’ meeting held after a transaction’s

execution.

c) The corporate governance body convening the shareholders’ meeting shall prepare a

report providing an adequate justification for the urgent handling. The Oversight Board shall

provide an independent assessment whether or not urgent handling is justified.

d) The report and assessment referred to in letter c) above shall be made available to the

public, at least 21 days before the scheduled date of the shareholders’ meeting, at the

Company’s head office and with the methods listed in the Issuers’ Regulations. These

documents may be included in an Information Memorandum, when one is required by the

Regulation for highly material transactions.

e) On the day following the date of the shareholders’ meeting, the Company shall make

available to the public, with the methods listed in the Issuers’ Regulations, information

about the outcome of the vote, specifically listing the total number of votes cast by

shareholders who are not related parties.

11

6.1.4 Amendments to the Bylaws Concerning Whitewash Transactions and Urgent Cases, Including Also Those Arising When a Business Is in Crisis Mode

As of the date of approval of this Procedure, the rules set forth in this Procedure do not require the

adoption of any amendment to the Bylaws because, thus far, the option of executing a highly

material transaction by virtue of an authorization by the shareholders’ meeting, even though it was

the subject of an unfavorable opinion by the Independent Directors, is not available, nor does the

Company plan to avail itself of the waiver referred to in Section 6.1.3 above.

6.2 Less Material Transactions 6.2.1 Definition

“Less material transactions” are the transactions with related parties identified as such in the table

provided in Annex 13.1 to this Procedure.

6.2.2 Handling of Less Material Transactions

In the case of less material transactions, the Committee shall render a detailed but non-binding

opinion as to the Company’s interest in executing the transaction and about the suitability and

substantive fairness of the transaction’s terms. The Committee’s opinions shall be recorded in the

minutes of the Committee’s meetings. The Committee and the Board of Directors shall receive

adequate and complete information about the transaction five and three days before their

meetings, respectively. If the transaction’s terms are found to be consistent with market or

standard terms, the supporting document shall contain a listing of objective benchmarks.

As part of the process of rendering an opinion concerning the execution of a transaction, the

Committee may also seek the support of independent experts of its own choosing, at the Company’s

expense. In such cases, when selecting the experts, the Committee shall choose persons with an

established reputation of professionalism and competency with regard to the subject matter covered

by the consulting assignment and, in all cases, parties that are not in a conflict of interest with regard

to the transaction. The opinion rendered by the experts shall be published on the Parmalat website.

When transactions are approved despite a negative opinion by the Independent Directors,

Parmalat, acting pursuant to the Regulation, shall make available to the public, within 15 days from

the end of each quarter in the reporting year, a document listing the name of the counterparty, the

12

subject of the transaction, the consideration involved and the reasons why it did not concur with the

Committee’s negative opinion. 6.3 Transactions of Not Material Amount

Transactions of not material amount are transactions with related parties other than highly

material and less material transactions, to which this Procedure is not applicable, except for the

periodic disclosures that must be provided in the interim reports on operations and the annual

report on operations pursuant to Article 5, Section 8, of the Regulation.

6.4 Atypical or Unusual Transactions Atypical or unusual transactions with related parties are transactions that qualify as such

pursuant to Consob Communication No. 1025564 of April 6, 2001, i.e., transactions that, because

of their materiality/relevance, nature of the counterparties, subject of the transaction (as it relates to

the regular course of business), method used to determine the transfer price and timing of

execution (close the end of the reporting year), could be questionable with regard to:

- the accuracy/completeness of the information in the financial statements;

- the existence of a conflict of interest;

- safeguarding the Company’s assets;

- protecting minority shareholders.

Extraordinary transactions (mergers, demergers, tender offers, share capital increases and/or

reductions, conveyances) do not automatically constitute atypical transactions.

The reports provided to the Committee and the Board of Directors shall specify, for each type of

transaction with related parties, whether the transaction is atypical or unusual.

6.5 Transactions Executed Through Subsidiaries

Pursuant to Article 114, Section 5 of the Italian Uniform Financial Code, transactions executed by

subsidiaries with related parties of Parmalat under the circumstances described above

(specifically: individual and cumulative size) shall always be included among those subject to the

disclosure requirements set forth in Article 5 of the Regulation and Article 114, Section 5, of the

Italian Uniform Financial Code.

With regard to substantive and procedural fairness, Parmalat, acting pursuant to Article 4, Section

1, Letter d), of the Regulation, shall apply the provisions of this document to transactions executed

13

by subsidiaries with related parties of Parmalat when the transactions are also reviewed and

approved by Parmalat, consistent with the guidelines of the Consob Communication and, if

appropriate, reserves the right to describe in a special protocol exclusively the implementation of

the provisions of this paragraph.

7. Framework Resolutions Pursuant to Article 12 of the Regulation, Parmalat may adopt framework resolutions applicable to a

series of homogeneous transactions with certain categories of related parties. Framework

resolutions are admissible only if:

a) transactions are sufficiently identified, indicating, as a minimum, the projected maximum

amount of the transactions planned for the reporting period and a justification for the terms

of the transactions;

b) the transactions reflect the characteristics and the amounts set forth in Items “E” and “G” of

the table provided in Annex 13.1;

c) the transactions have a maximum duration if 12 months;

d) The Chief Executive Officer or the person responsible for executing the transaction

provides a comprehensive report, at least once every three months, about the

implementation of the framework resolutions.

8. Waiver Availability Instances and Options This Procedure shall not apply to resolutions approved by the shareholders’ meeting, pursuant to

Article 2389, Section One, of the Italian Civil Code, concerning compensation payable to Directors

and members of the Executive Committee or to resolutions concerning the compensation of

Directors serving in special capacities the amount of which is included in the total compensation

approved by the shareholders’ meeting pursuant to Article 2389, Section Three, of the Civil Code.

Moreover, this Procedure shall not apply to the following transaction categories:

a) Resolutions concerning the compensation of Directors and executives serving in special

capacities, different from those referred to in Article 13, Section 1, of the Regulation, and

managers with strategic responsibilities(1), provided that, pursuant to the Regulation:

(1) These are individuals who, directly or indirectly, have the power and responsibility to plan, manage and control the Company’s activities. Pursuant to Annex 1 to the Regulation, they also include Company Directors, with or without executive authority.

14

- the Company adopted a compensation policy;(1)

- a committee comprised exclusively of non-executive Directors, the majority of whom

were independent, played a role in defining the compensation policy;

- a report explaining the compensation policy was submitted to the shareholders’

meeting for approval or asking for a consultative vote;

- the compensation provided is consistent with the abovementioned policy.

b) Compensation plans based on financial instruments approved by the shareholders’ meeting

(stock option plans), pursuant to Article 114-bis of the Italian Uniform Financial Code and

transaction executed to implement them;

c) Transactions executed in the ordinary course of business on terms consistent with market

or standard terms, it being understood that these are routine transactions executed on

terms comparable to those usually applied in transactions of similar nature, amount or risk

with non-related parties, or transactions based on regulated rates or government controlled

prices or transactions with counterparties with whom the Company is required by law to

stipulate a specific consideration. More specifically, in order to determine whether a

transaction is executed as part of its regular operating activities or related financial

activities, the Company shall take into account the following elements:

The subject of a transaction. The fact that the subject of a transaction is extraneous

to the Company’s regular activities is an anomaly indicator signaling that the

transaction may not be part of the Company’s ordinary activities.

The recurrence of a type of transaction within the Company’s activities. The regular

repetition of a transaction by the Company is a significant indicator that the

transaction is part of the Company’s ordinary activities, unless other indicators point

in the opposite direction.

The size of the transaction. A transaction that is part of the Company’s operating

activities may not qualify as a transaction executed in the ordinary course of

business if it is of unusually large size. However, it must be noted that the waiver in

question is also applicable to highly material transactions: the distinguishing factor is

whether the amount of a transaction is significantly larger than the amounts that

usually characterize similar transactions executed by the Company.

(1) Please note that by Law No. 96 of June 4, 2010, published on June 25, 2010 in Issue No. 146 of the Official Gazette, authority was delegated to the government to enact, within six months from the effective date of the delegation law, a legislative decree implementing European Commission Recommendations No. 2004/913/EC and No. 2009/385/EC concerning the compensation of Directors of publicly traded companies.

15

The contractual terms and conditions, including the characteristics of the consideration.

As a rule, transactions that involve non-cash consideration are not deemed to be part of

the ordinary course of business, even when the consideration is the subject of an

appraisal by an independent expert. Likewise, contract clause that are inconsistent with

customary contractual uses and practices could represent a significant indicator that a

transaction is not executed in the ordinary course of business.

The type of counterparty. Transactions subjectively qualified as transactions with

related parties may include a subset of transactions that do not qualify as

transactions carried out in the ordinary course of the operating activities (or related

financial activities) because they are executed with counterparties that present

characteristics that are anomalous for the type of transaction in question.

The significance of the elements described above shall be assessed with special emphasis on

the timing of a transaction’s approval and execution. Specifically, when evaluating the indicators

showing whether or not a transaction is executed in the course of the Company’s operating

activities and related financial activities, it is important to keep in mind that an unordinary

indicator can have greater weight, in making such a determination, if a transaction is approved

near the end of the reporting year of a publicly traded company or its related party.

In determining whether a transaction qualifies as an “ordinary transaction,” the type of

activity carried out by the company executing the transaction must be taken into account.

Therefore, when a transaction is executed by a subsidiary of a publicly traded company, the

subsidiary’s activity (or one of the activities carried out in the ordinary course of business)

shall be the relevant activity.

The Company’s Department handling the transaction shall be responsible for verifying

compliance with the foregoing provisions and shall make available economic and financial

data showing that the transaction’s terms are consistent with standard terms.

Ordinary transactions with regard to which the relevant Company Department can produce

a plurality of offers, including offers from non-related parties, may be exempted.

Transactions executed in the ordinary course of business (the following non-exhaustive list

being provided by way of example) include:

- sales and/or disposals of raw materials, semifinished goods and finished products;

- service activities, such as, for example, copacking arrangements.

Transactions settled on terms and conditions and/or with methods that are significantly

different from those existing in the market and/or the conditions usually applied to

transaction with parties that qualify as related parties shall not be deemed to be

16

transactions executed in the ordinary course of business. Transactions involving amounts

greater than 50 million euros and commitments lasting longer than 12 months are included

in this category.

d) Intra-Group transactions(1). Transactions with companies that are not residents of Italy and

directly or indirectly control Parmalat, are controlled by it or are controlled by the same

company that controls Parmalat, based on current tax laws, are valued as follows:

- based on the fair value of the assets sold;

- based on the value of the services provided;

- based on the value of the goods and services received, if the result is an increase in

income.

Fair value shall be understood to be the average price or consideration charged for goods and

services of the same kind, or of a similar type, under conditions of free competition and at the

same salable stage, at the time and place where the good and services were purchased or

supplied or, otherwise, at the most closely comparable time and place.

Insofar as possible, fair value shall be determined based on the price lists or rates of the party

supplying the goods or services or, when these are unavailable, the official lists of average

prices and other price lists of the Chambers of Commerce and fees for professional services,

less customary discounts.

e) Urgent transactions, including those arising when a business is in crisis mode, (when the

waiver is permissible pursuant to the Bylaws) that do not fall within the purview of the

shareholders’ meeting or must be approved by it, when the conditions referred to in the

Regulation are applicable.

Lastly, the Regulation’s provisions, the provisions of Article 5 notwithstanding, shall not apply to

transactions executed in accordance with instructions issued by the regulatory authorities to

promote stability or based on instructions issued by the Group’s Parent Company to implement

instructions issued by the regulatory authorities to bolster the Group’s stability.

(1 ) Intra-Group transaction shall be understood to mean transactions with subsidiaries. The percentage of control that triggers the waiver of the obligation to implement this Procedure is an equity interest equal the ownership of 95% or more of a subsidiary’s share capital. Please note that, pursuant to the Consob Communication of September 24, 2010 (Item 21), the mere sharing of one or more Directors or executives with strategic responsibilities by the Company and its subsidiaries (and, more so, its affiliated companies) does not, in of itself, give rise to interests significant enough to exclude the waiver option.

17

9. Public Disclosure of Transactions With Related Parties When it executes highly material transactions, Parmalat shall prepare an information

memorandum that, pursuant to the provisions of Annex 4 to the Regulation, provides specific

information, such as:

• the transaction’s features, method of implementation, terms and conditions;

• the identification of the related party with whom the transaction is executed;

• an indication of the transaction’s economic justification and the benefit that the Company

expects from the transaction;

• the other information listed in the abovementioned Annex.

The information memorandum shall be made available to the public at the Company’s head

office, within seven days from the date when the transaction is approved by the relevant

governance body (in cases involving the shareholders’ meeting’s jurisdiction or approval, within

seven days from the date when the motion submitted to the shareholders’ meeting is

approved), and shall be published on the Company website, together with any opinions

provided by members of the Board of Directors, Independent Directors, Statutory Auditors and

independent experts. Concurrently with their publication, Parmalat shall transmit these

documents and opinions to the Consob.

In addition, the following information must be disclosed in the interim report on operations and the

annual report on operations:

- information about highly material transactions executed during the reporting period;

- information about other individual transactions with related parties executed during the

reporting period that had a material impact on the Company’s balance sheet or income

statement during the reporting period;

- information about any changes or developments affecting transactions with related parties

described in the latest annual report that had a material impact on the Company’s balance

sheet or income statement during the reporting period.

10. Controls Monitoring the Procedure’s Implementation Parmalat undertakes to carry out all preventive and subsequent controls that may be necessary to

monitor the correct implementation of this Procedure. The results of these control activities shall be

reported periodically to the Committee.

18

11. Updates to and Implementation of the Procedure

The rules governing updates to and the implementation of this Procedures are set forth in the

operational protocols, which shall be updated at least once every three years.

12. Closing and Transitional Provisions

This Procedure, which has been published on the Company website, shall be implemented, by

means of special, merely operational protocols, effective as of January 1, 2011.

13. Annexes

The following annexes are appended to this Procedure:

1. A table showing the materiality thresholds applicable to transactions with related parties

(Annex 13.1);

2. Annex 3 to the Regulation: “Designation of Highly Material Transactions with Related

Parties (Annex 13.2);

3. Affidavit form (Annex 13.3).

19

13.1 Materiality Thresholds for Transactions with Related Parties

The table below shows the materiality thresholds applicable to transactions with related parties:

Types of related partieshighly material less material of not material amount

Individuals

From 250,000 eruos

to100 million euros

Less than 250,000 euros

Legal entities

From 500,000 euros

to100 million euros

Less than 500,000 euros

Larger than 100 million euros

Transactions

Thresholds Applicable to Transactions with Related Parties

20

13.2 Annex 3 to the Regulation: “Designation of Highly Material Transactions with Related Parties” 1. Internal procedures shall establish quantitative criteria to identify “highly material transactions,” which shall include, as a minimum, the types of transactions listed below. 1.1. Transactions in which at least one of the following materiality indices, applicable depending on each specific transaction, exceeds the 5% threshold: a) Consideration materiality index: It is the ratio of the transaction’s consideration to the company’s shareholder’s equity, taken from the most recent published balance sheet (consolidated balance sheet, if available) or, for a publicly traded company, its market capitalization, if larger, computed at the closing on the last stock market trading day in the reporting period covered by the most recent published periodic accounting document (annual or semiannual financial report or interim report on operations). For banks, it is the ratio of the transaction’s consideration to total capital taken from the most recent published balance sheet (consolidated balance sheet, if available). If the transaction’s financial terms are specified, the transaction’s consideration is equal to: i) for cash components, the amount paid to/by the contractual counterparty; ii) for components consisting of financial instruments, their fair value, determined on the transaction date in accordance with the international accounting principle adopted with (EC) Regulation No. 1606/2002; iii) for financing transactions or transactions involving the provision of guarantees, the maximum disbursable amount. If the transaction’s financial terms are predicated in whole or in part on quantities that are not yet known, the transaction’s consideration is the maximum amount receivable or payable pursuant to the transaction’s stipulations. b) Asset materiality index: It is the ratio of the total assets of the entity subject of the transaction to the company’s total assets. The data used must be taken from the company’s most recent published balance sheet (consolidated balance sheet, if prepared). When possible, similar data must be used to determine the total assets of the entity subject of the transaction. For transactions involving the acquisition or disposal of equity investments that have an impact on the scope of consolidation, the numerator amount is equal to the total assets of the investee company, irrespective of the percentage of share capital that is being disposed of. For transactions involving the acquisition or disposal of equity investments that have no impact on the scope of consolidation, the numerator amount is equal to i) for acquisitions, the transaction’s consideration, plus any liabilities of the acquired company assumed by the acquirer; ii) for sales, the consideration received for the sold assets. For transactions involving the purchase or sale of other assets (different from the acquisition of an equity investment), the numerator amount is equal to: i) for acquisitions, the consideration paid or the carrying amount attributed to the acquired assets, whichever is greater; ii) for sales, the carrying amount of the assets. c) Liability materiality index: It is the ratio of the total liabilities of the acquired entity to the company’s total assets. The data used must be taken from the company’s most recent published

21

balance sheet (consolidated balance sheet, if prepared). When possible, similar data must be used to determine the total liabilities of the acquired company or business operations. 1.2. Transactions with a publicly traded controlling company or with parties related to it that, in turn, are related to the companies, when at least one of the materiality indices referred to in Section 1.1 above exceeds the 2.5% threshold. 1.3. Companies shall determine whether they should establish materiality thresholds that are lower than those set forth in Sections 1.1 and 1.2 above for transactions that could have an impact on the operating independence of an issuers (e.g., sales of intangible assets, such as trademarks or patents). 1.4. In the case of multiple cumulative transactions, pursuant to Article 5, Section 2, companies shall determine, first of all, the materiality of each transaction, based on the index or indices set forth in Section 1.1 above that are applicable. To determine whether the thresholds set forth in Sections 1.2, 1.2 and 1.3 above are being exceeded, the results attributable to each index shall be added together. 2. If a transaction or multiple cumulated transactions, pursuant to Article 5, Section 2, qualify as “highly material transactions” based on the indices set forth in Section 1 above and such a finding is patently unjustified in view of special circumstances, the Consob, acting upon a request by the company, may provide alternative methods to compute the abovementioned indices. For this purpose, the company, prior to completing the transaction’s negotiations, shall communicate to the Consob the transaction’s main characteristics and the specific circumstances upon which its request is based.

22

13.3 Affidavit Form Parmalat S.p.A.

Via delle Nazioni Unite, 4 43044 Collecchio (PR)

Affidavit Provided Pursuant to the Consob Regulation Concerning Transactions with Related

Parties and the Procedure Governing Transactions with Related Parties Approved by the Board of Directors on November 11, 2010

With regard to the requirements of Annex 1 of the Consob Regulation concerning transactions with related parties and in implementation of the provisions of Section 3.11 of the Procedure governing transactions with related parties, I, the undersigned ………………………………………........, in my capacity as ……………………………….. of Parmalat S.p.A., hereby disclose, under my personal responsibility, the names of the members of my immediate family ad of the entity referred to in Letter h) of the abovementioned Section 3.1.

First and last name Place and date of birth Family relationship

1 Abstract from Section 3.1 “Designation of Related Parties.” The following abstract of Section 3.1 of the Procedure Governing Transactions with Related Parties is provided for the purposes of this affidavit: “The following parties qualify as Parmalat’s related parties: (d) any Parmalat Director or Statutory Auditor; (e) any Parmalat General Manager (identified as Direttore Generale in Italian); (f) any executive with strategic responsibilities of Parmalat or its controlling company; (g) any member of the immediate family of one of the parties listed in letters (a) or (d) or (e) or (f), specifically including his/her spouse, if not legally separated, live-in partner and children or dependents; (h) an entity over which one of the parties listed in letters (d) or (e) or (f) or (g) exercises control, joint control or a significant influence or in which one of the abovementioned parties holds, directly or indirectly, a significant equity interest. The parties designated by Parmalat as related parties shall be organized in a list and entered into a special database that Parmalat shall maintain based on the available evidence (direct related parties, based on the equity interest relationships and the role performed within the organization) and affidavits provided by related parties. Parmalat shall approve a special operating protocol concerning how the database is operated and accessed.”

23

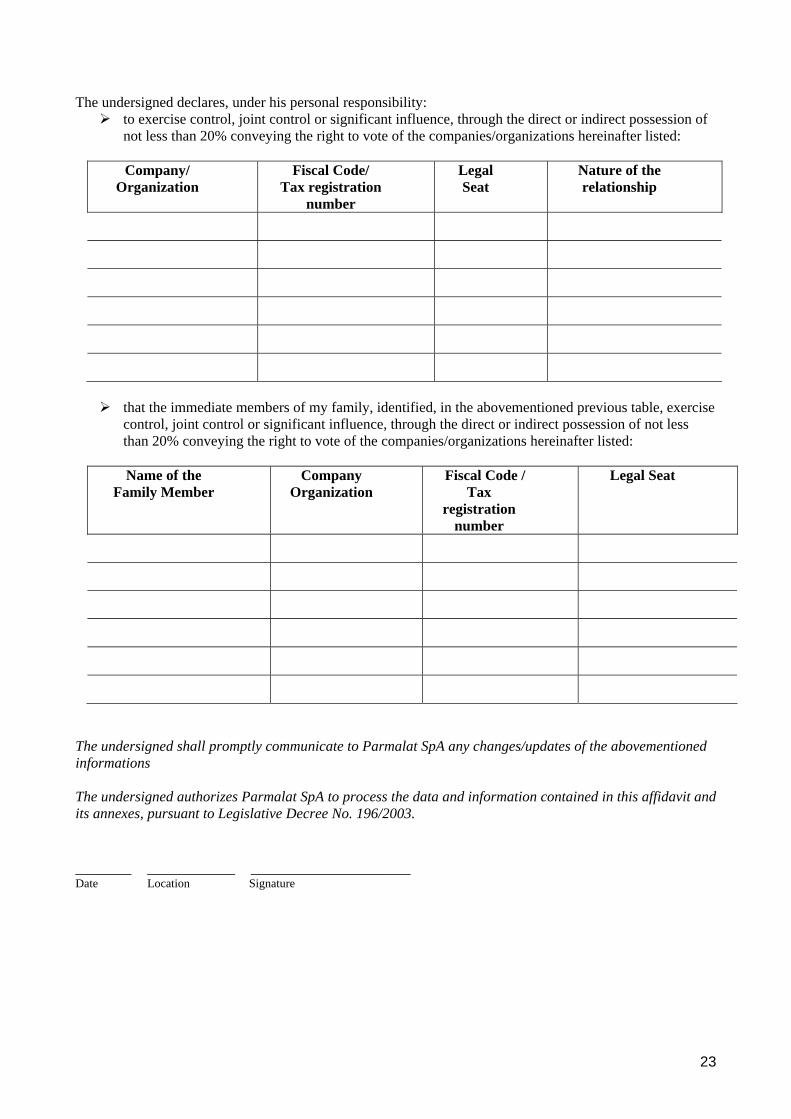

The undersigned declares, under his personal responsibility: to exercise control, joint control or significant influence, through the direct or indirect possession of

not less than 20% conveying the right to vote of the companies/organizations hereinafter listed:

Company/ Organization

Fiscal Code/ Tax registration

number

Legal Seat

Nature of the relationship

that the immediate members of my family, identified, in the abovementioned previous table, exercise

control, joint control or significant influence, through the direct or indirect possession of not less than 20% conveying the right to vote of the companies/organizations hereinafter listed:

Name of the

Family Member Company

Organization Fiscal Code /

Tax registration

number

Legal Seat

The undersigned shall promptly communicate to Parmalat SpA any changes/updates of the abovementioned informations The undersigned authorizes Parmalat SpA to process the data and information contained in this affidavit and its annexes, pursuant to Legislative Decree No. 196/2003. _______ ___________ ____________________ Date Location Signature