UBS conferenceLennart Persson, CFO

Net sales of SEK 91bn* 37,000 employees Sales in more than 100 countries Leading global hygiene company #1 or #2 positions in close to 80 countries Strong brands;

TEN and Tork are leading global billion-euro brands for Incontinence care and AFH tissue

Europe’s largest private forest owner Europe’s second-largest sawmill company Several of the world’s most prestigious

sustainability awards2 November 2012

SCA Group

* 2011 sales adjusted for closed transactions

November 2012

Divestment of the Packaging business, excluding the two kraftliner mills Acquisition of Georgia-Pacific’s European tissue operations Acquisitions in emerging markets

Everbeauty in Asia Pro Descart in Brazil San Saglik and Komili(50%) in Turkey

Joint venture in Australia/New Zealand Divestment of Aylesford Newsprint Efficiency program Leadership and culture

Transforming SCA

3

SCA Group9 months 2012 sales and EBIT by Business Area

November 2012

Forest Products

Tissue

Personal Care

48%

22%30%

Sales by Business Area

Forest Products

Tissue

Personal Care

49%

16%35%

EBIT by Business Area

4

5

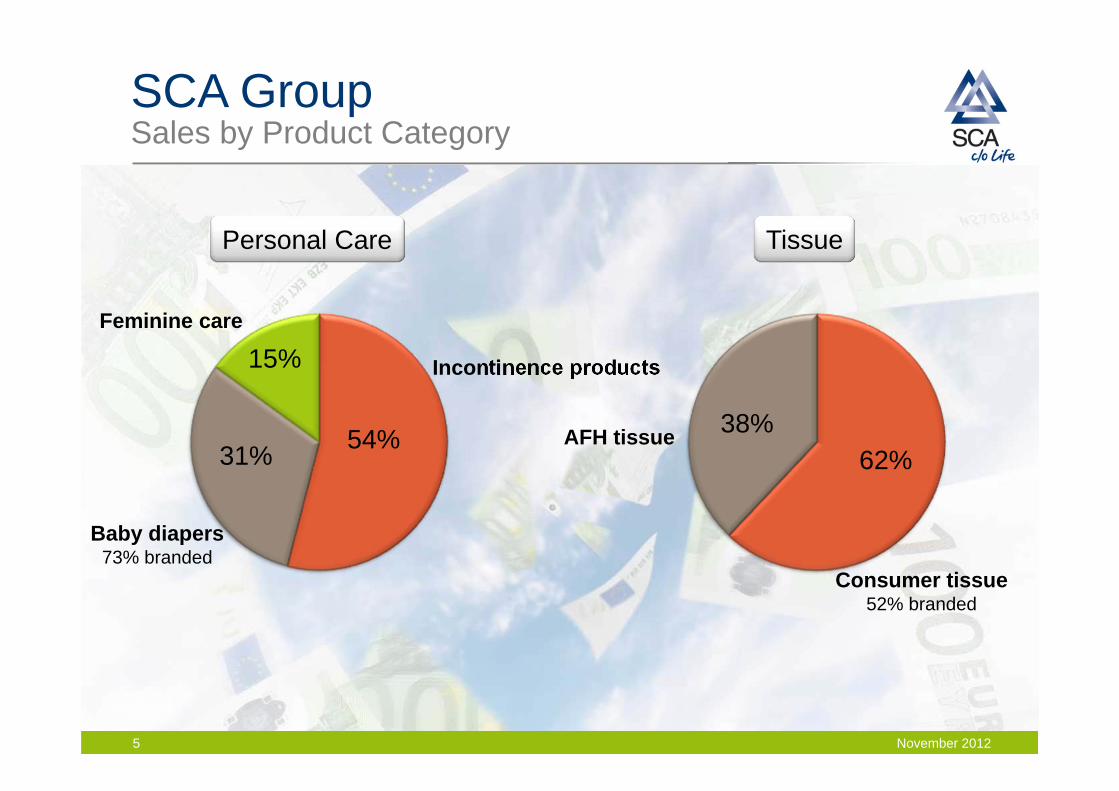

SCA GroupSales by Product Category

November 2012

Feminine care

Baby diapers73% branded

Incontinence products

31%

15%

54%

Personal Care

AFH tissue

Consumer tissue52% branded

38%62%

Tissue

6

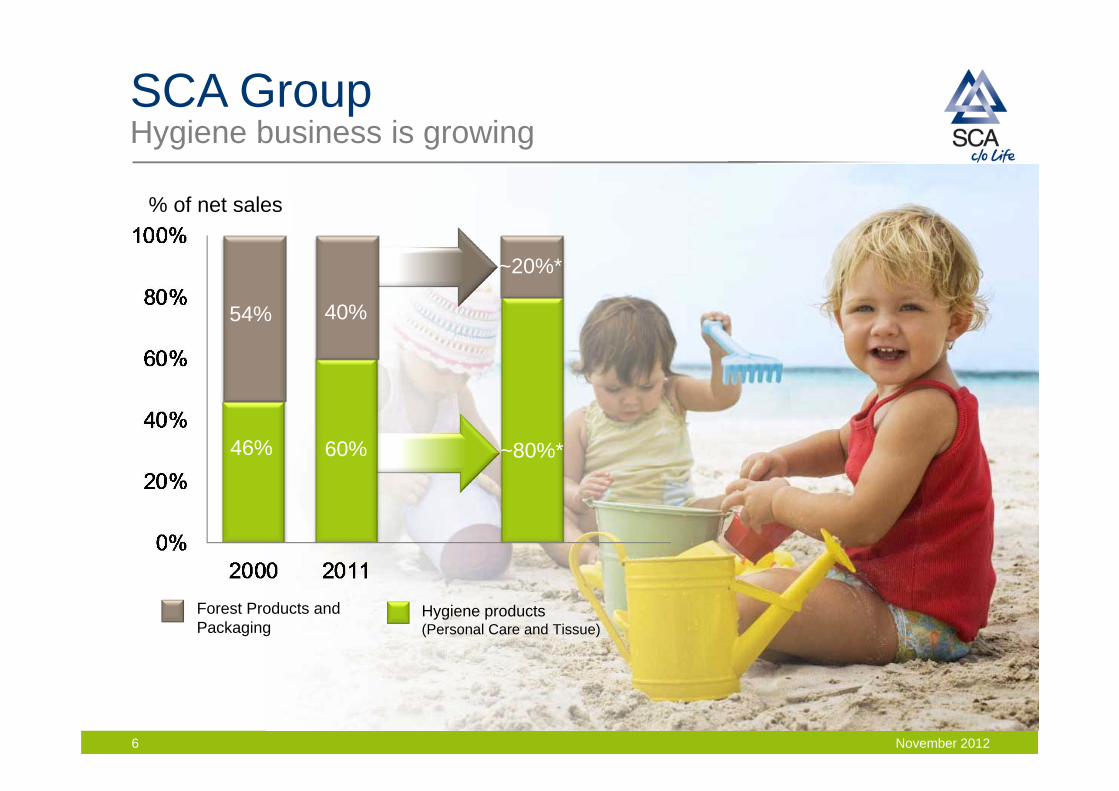

46% 60%

40%54%

~20%*

~80%*

SCA GroupHygiene business is growing

% of net sales

Forest Products and Packaging

Hygiene products(Personal Care and Tissue)

November 2012

Leading Market positions Globally and regionally

North America

Incontinence products:AFH tissue:

23

Mexico

Incontinence products: 1

Feminine care: 1

Consumer tissue 2

AFH tissue: 3

Baby diapers: 3

Colombia

Incontinence products: 1

Feminine care: 1

Tissue: 1

Baby diapers 2

Nordic region

Incontinence products: 1

Baby diapers: 1

AFH tissue: 1

Consumer tissue: 2

Feminine care 2

Europe

Tissue: 1

Incontinence products 1

Baby diapers: 3

Feminine care 3

Private forest owners: 1

Solid-wood products: 2

Asia

Incontinence products: 1Globally

Incontinence products: 1

AFH tissue: 1

Consumer tissue: 2

November 2012

Value market positions

7

November 2012

SCA Group’s Priorities

SUSTAINABILITY

EFFICIENCY INNOVATION GROWTH

8

November 2012

EfficiencyRestructuring program in baby diapers

in Europe completed2011 Efficiency program

Annual cost saving: EUR 80m Higher machine efficiency and reduced CAPEX

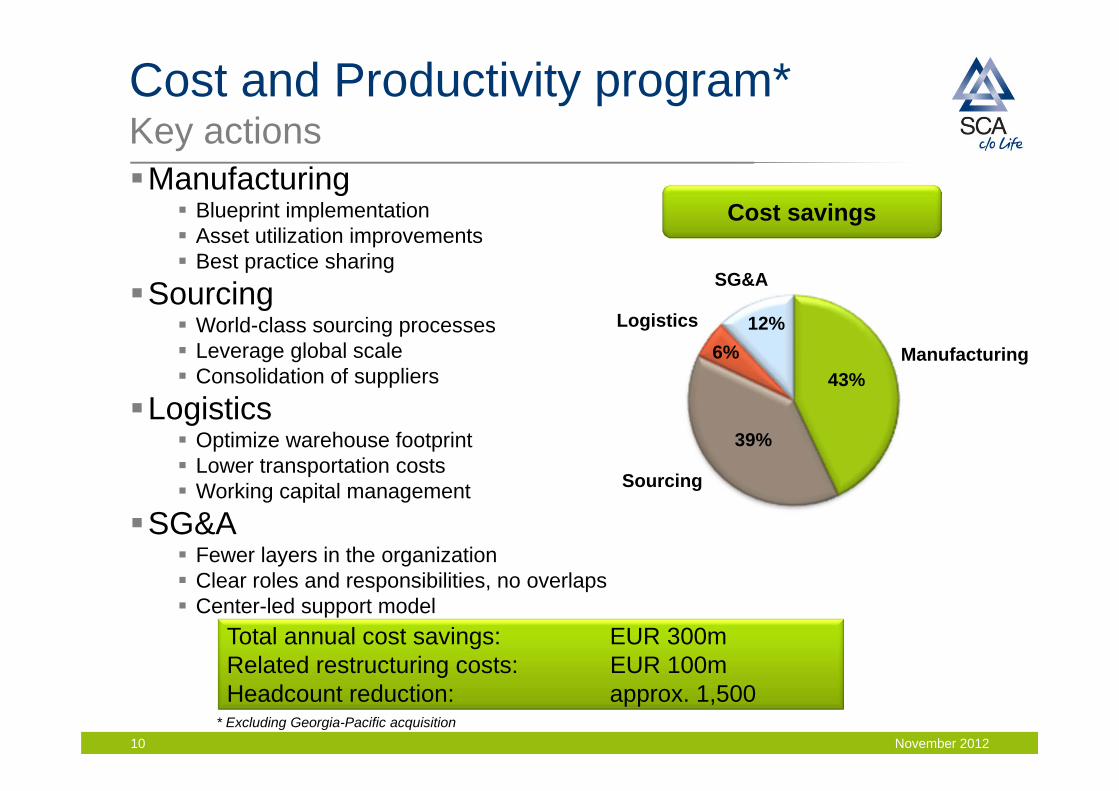

Cost and productivity program Annual cost saving: EUR 300m

Georgia-Pacific synergies Annual cost saving: EUR 125m

Energy efficiency program Annual cost saving: EUR 70m

Efficiency improvements in Forest Products Investments in upgrades and new capacity9

November 2012

Total annual cost savings: EUR 300mRelated restructuring costs: EUR 100mHeadcount reduction: approx. 1,500

Manufacturing

Sourcing

Logistics 12%

43%6%

39%

SG&A

Manufacturing Blueprint implementation Asset utilization improvements Best practice sharing

Sourcing World-class sourcing processes Leverage global scale Consolidation of suppliers

Logistics Optimize warehouse footprint Lower transportation costs Working capital management

SG&A Fewer layers in the organization Clear roles and responsibilities, no overlaps Center-led support model

Cost savings

* Excluding Georgia-Pacific acquisition

Cost and Productivity program*Key actions

10

November 201211

Georgia-Pacific AcquisitionStrengthens our no.1 position

Perfect strategic fit

Substantial synergies

Strengthens our geographic presence in Europe

Strong innovation portfolio

Strengthens our branded portfolio

Georgia-Pacific AcquisitionSynergies

Cost synergies

Supply chainSales and Marketing

Support and overhead

25%

60%15%

Supply chain synergies Manufacturing excellence and best

practice Footprint optimization Scale effects raw materials Logistics optimization

Sales and Marketing S&M organization consolidation

A&P efficiencySupport and overhead

Consolidation of support functions

November 2012

Cost synergies

Total annual cost synergies: EUR 125mRelated restructuring costs: EUR 130m

12

Meet changing demands and requirements

Create long-term, profitable differentiation

Strengthen market positions

Build stronger brands

Drive growth

November 2012

Innovation drives Profitable growthStrengthens market positions and profitability

13

November 2012

Global population growth

An aging population

Increased market penetration

Higher disposable income

Customers and consumers demand more comfort and sustainability

Market DriversGood growth opportunities

14

November 2012

2010 2017

Personal CareTissue

Global Hygiene Products MarketIncreased penetration and aging and growing population

15

November 2012

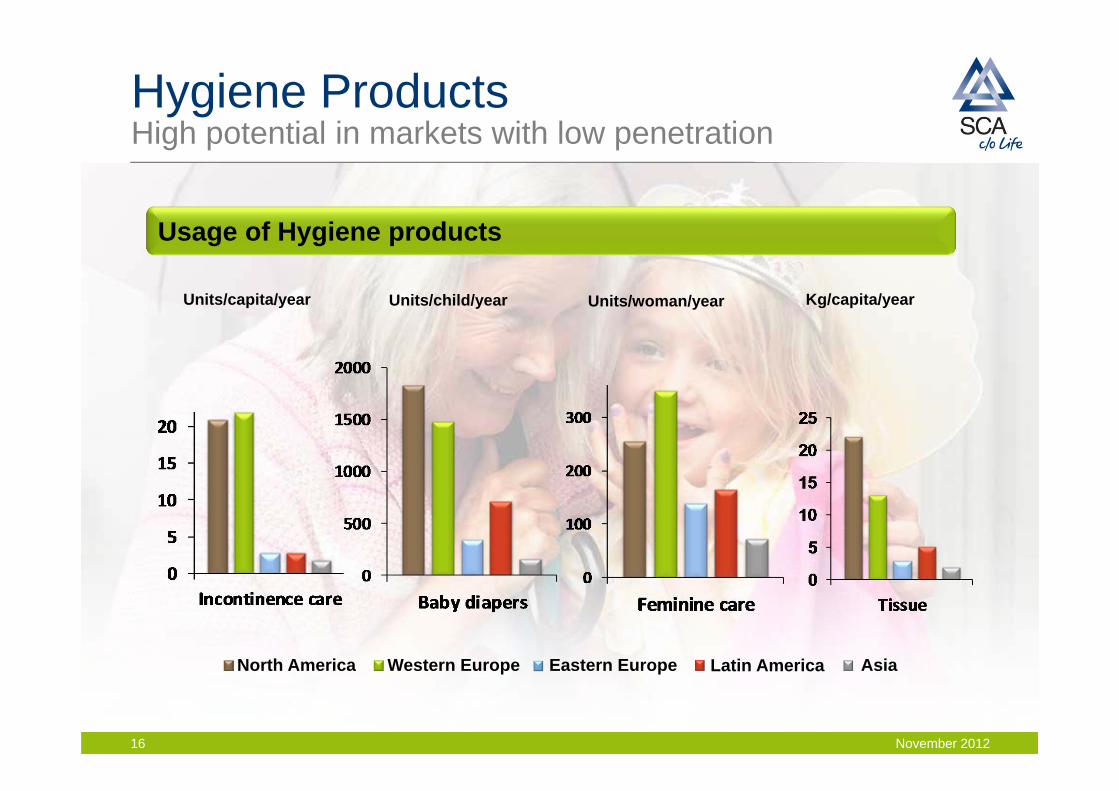

Western Europe Eastern Europe Latin America AsiaNorth America

Usage of Hygiene products

Units/capita/year Units/child/year Units/woman/year Kg/capita/year

Hygiene ProductsHigh potential in markets with low penetration

16

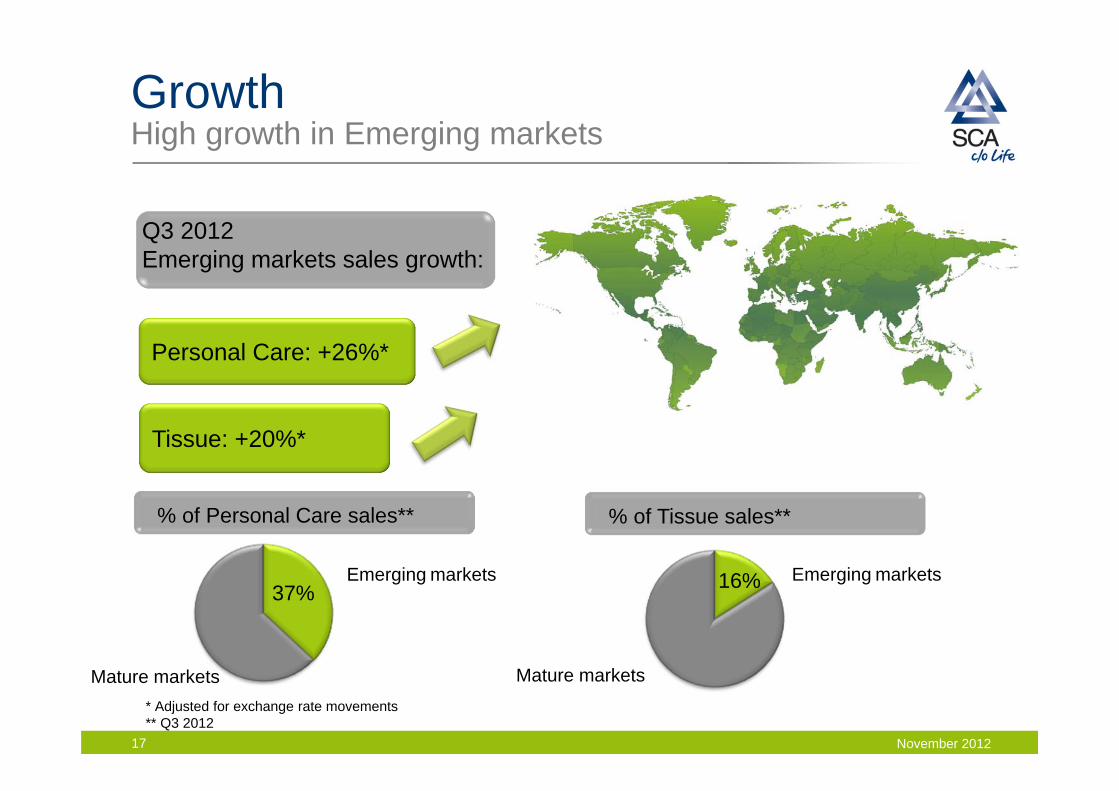

37%

Mature markets

Emerging markets

% of Personal Care sales**

Q3 2012 Emerging markets sales growth:

Personal Care: +26%*

Tissue: +20%*

GrowthHigh growth in Emerging markets

* Adjusted for exchange rate movements** Q3 2012

16%

Mature markets

% of Tissue sales**

Emerging markets

November 201217

Mature markets Improve profitability Increased cash flow

generation Strengthen market

positions Category expansion

Established emerging markets Profitable growth Strengthen market

positions Category expansion

SCA’s Market Priority

Not-present emerging markets Selected entry

November 201218

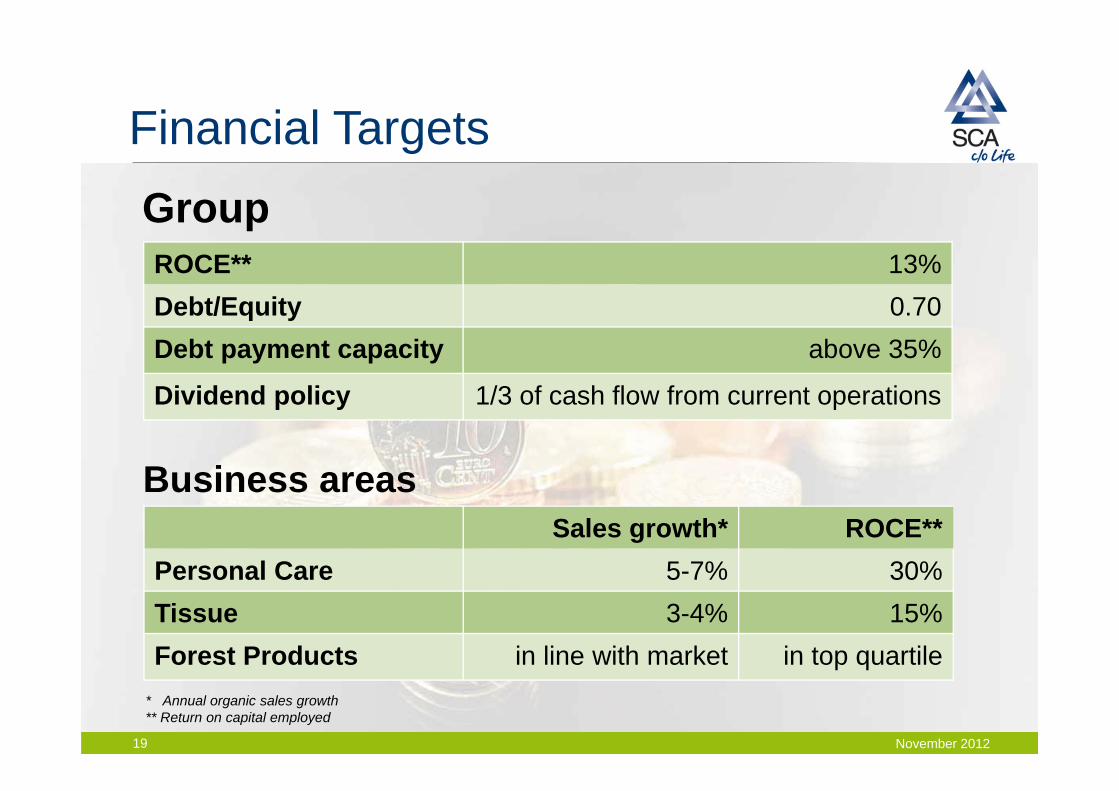

Financial Targets

November 2012

* Annual organic sales growth** Return on capital employed

Sales growth* ROCE**Personal Care 5-7% 30%Tissue 3-4% 15%Forest Products in line with market in top quartile

Group

Business areas

ROCE** 13%Debt/Equity 0.70Debt payment capacity above 35%

Dividend policy 1/3 of cash flow from current operations

19

Johan Karlsson, VP Investor RelationsTel: +46 8 788 51 30

Louise Tjeder, Director Investor RelationsTel: +46 8 788 51 62

IR Contacts:

Email: [email protected] Website: www.sca.com