0

Second Quarter of Fiscal Year Ending March 2016

Briefing on Financial Results

October 22, 2015

Ricoh Leasing Company, Ltd.

1

1. Performance Overview (Second Quarter of Fiscal Year

Ending March 2016)

Performance Overview

2

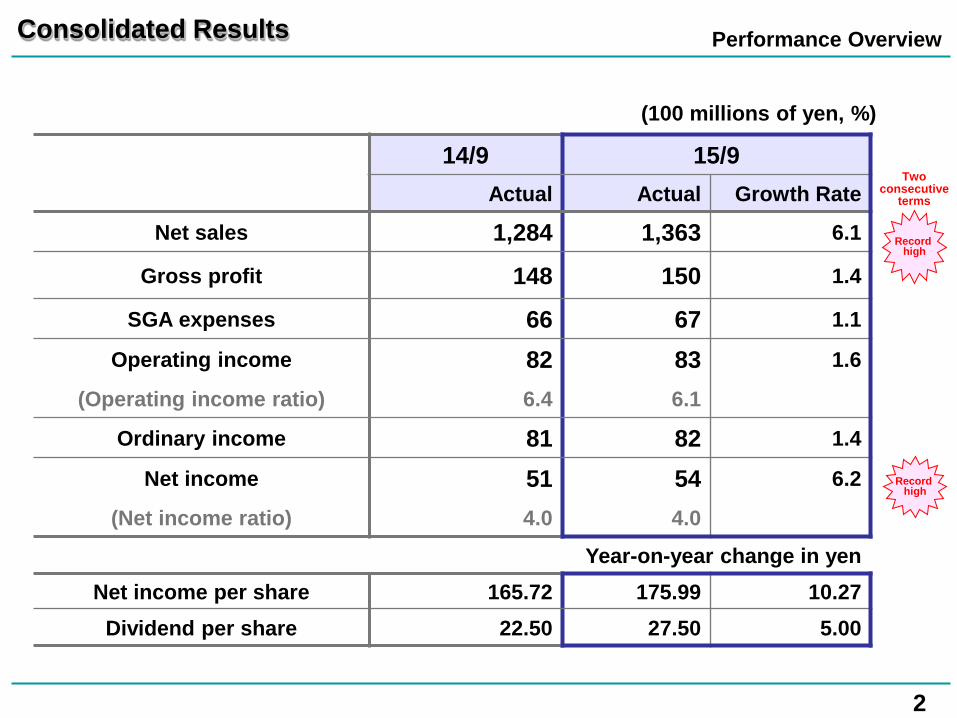

14/9 15/9 Actual Actual Growth Rate

Net sales 1,284 1,363 6.1

Gross profit 148 150 1.4

SGA expenses 66 67 1.1

Operating income 82 83 1.6

(Operating income ratio) 6.4 6.1

Ordinary income 81 82 1.4

Net income 51 54 6.2

(Net income ratio) 4.0 4.0

Year-on-year change in yen Net income per share 165.72 175.99 10.27

Dividend per share 22.50 27.50 5.00

Consolidated Results

(100 millions of yen, %)

Record high

Record high

Two consecutive

terms

Performance Overview

3

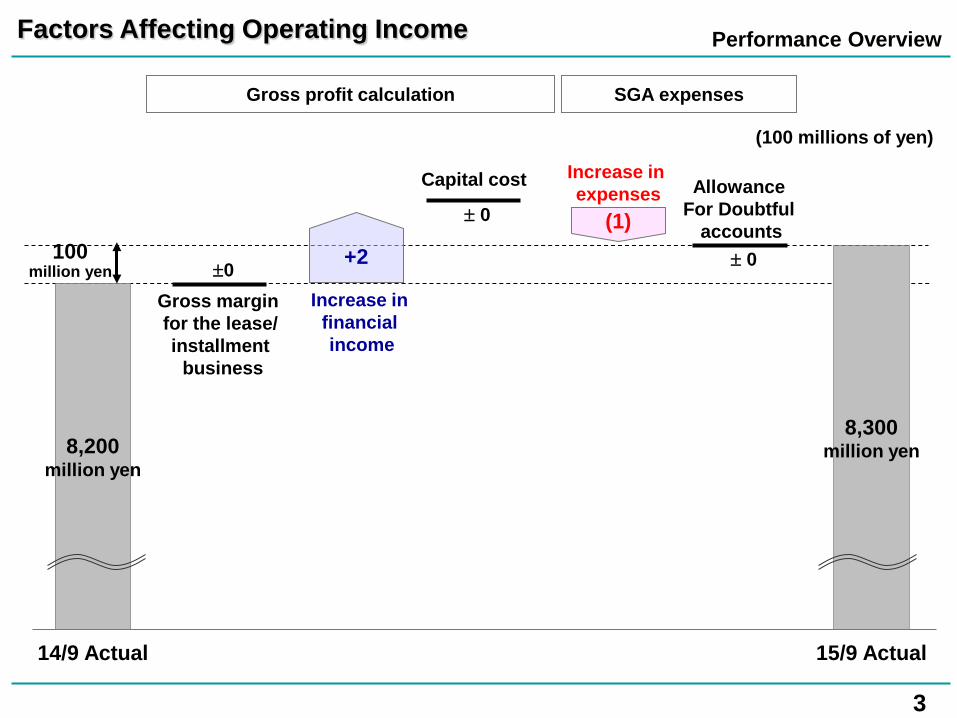

Factors Affecting Operating Income

(100 millions of yen)

8,200 million yen

15/9 Actual

8,300 million yen

14/9 Actual

100 million yen

Gross profit calculation SGA expenses

+2

Increase in financial income

Increase in expenses

(1)

Capital cost

± 0

Gross margin for the lease/ installment business

±0

Allowance For Doubtful

accounts ± 0

Performance Overview

4

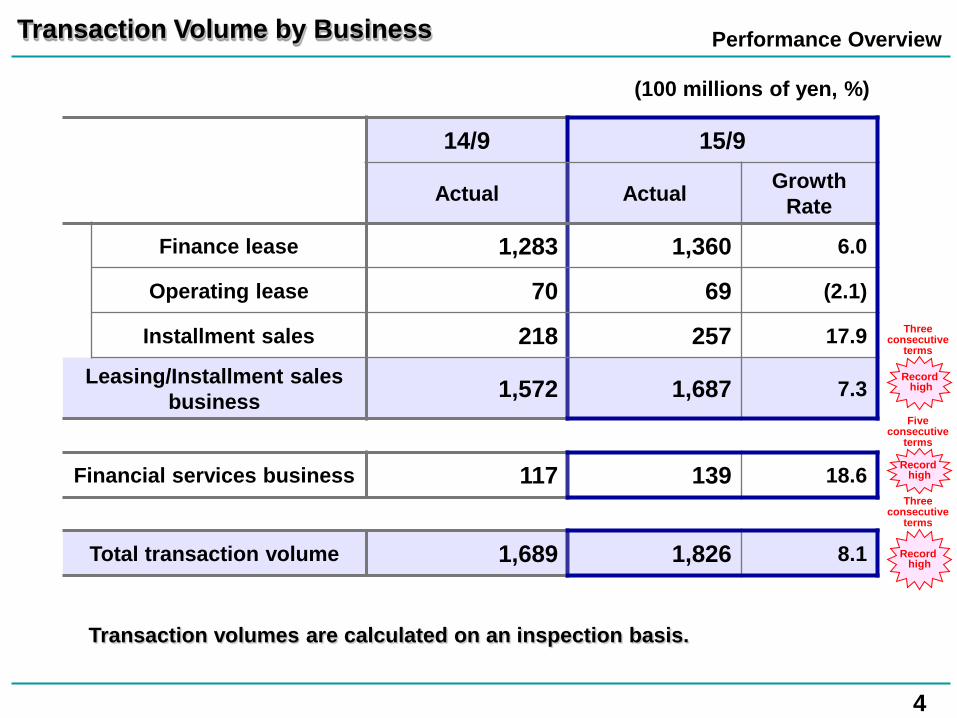

Transaction Volume by Business

(100 millions of yen, %)

Transaction volumes are calculated on an inspection basis.

14/9 15/9

Actual Actual Growth Rate

Finance lease 1,283 1,360 6.0

Operating lease 70 69 (2.1)

Installment sales 218 257 17.9

Leasing/Installment sales business 1,572 1,687 7.3

Financial services business 117 139 18.6

Total transaction volume 1,689 1,826 8.1

Record high

Record high

Record high

Three consecutive

terms

Five consecutive

terms

Three consecutive

terms

Performance Overview

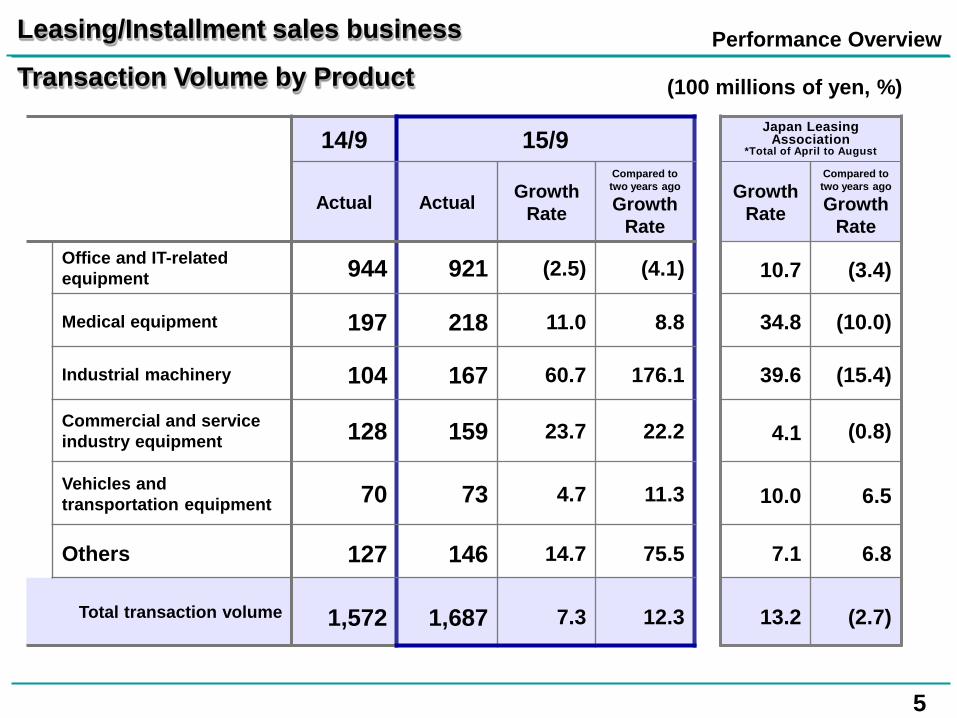

5

(100 millions of yen, %)

Leasing/Installment sales business

Transaction Volume by Product

14/9 15/9 Japan Leasing

Association *Total of April to August

Actual Actual Growth Rate

Compared to two years ago

Growth Rate

Growth Rate

Compared to two years ago

Growth Rate

Office and IT-related equipment 944 921 (2.5) (4.1) 10.7 (3.4)

Medical equipment 197 218 11.0 8.8 34.8 (10.0)

Industrial machinery 104 167 60.7 176.1 39.6 (15.4)

Commercial and service industry equipment 128 159 23.7 22.2 4.1 (0.8)

Vehicles and transportation equipment 70 73 4.7 11.3 10.0 6.5

Others 127 146 14.7 75.5 7.1 6.8

Total transaction volume 1,572 1,687 7.3 12.3 13.2 (2.7)

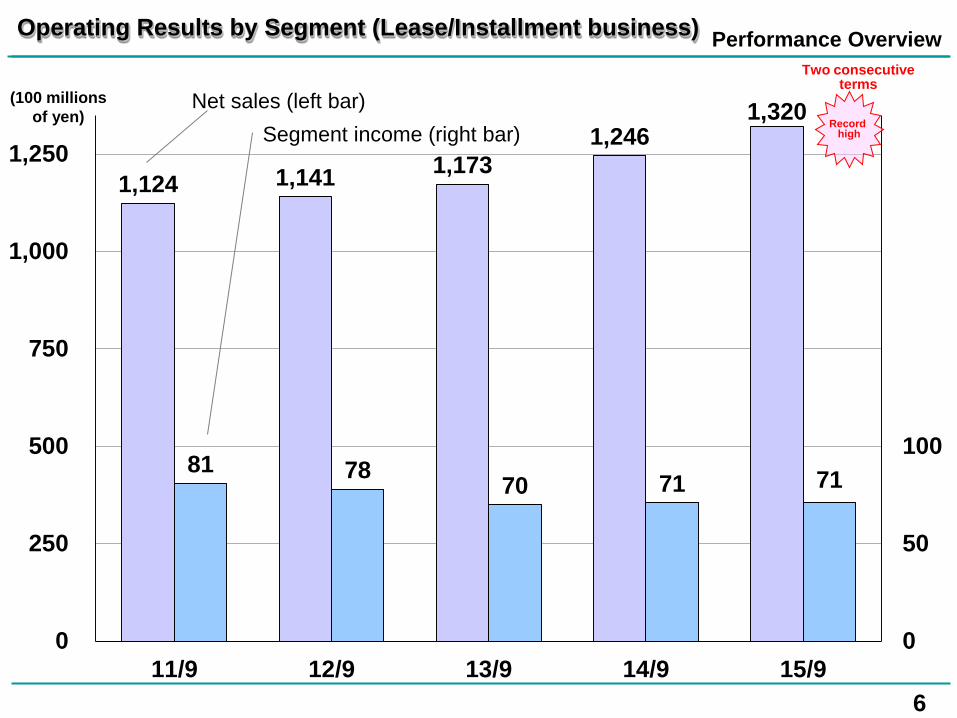

Performance Overview

6

1,124 1,141 1,173 1,246

1,320

81 78 70 71 71

0

50

100

150

200

250

0

250

500

750

1,000

1,250

11/9 12/9 13/9 14/9 15/9

Operating Results by Segment (Lease/Installment business)

(100 millions of yen)

Net sales (left bar) Segment income (right bar)

Record high

Two consecutive terms

Performance Overview

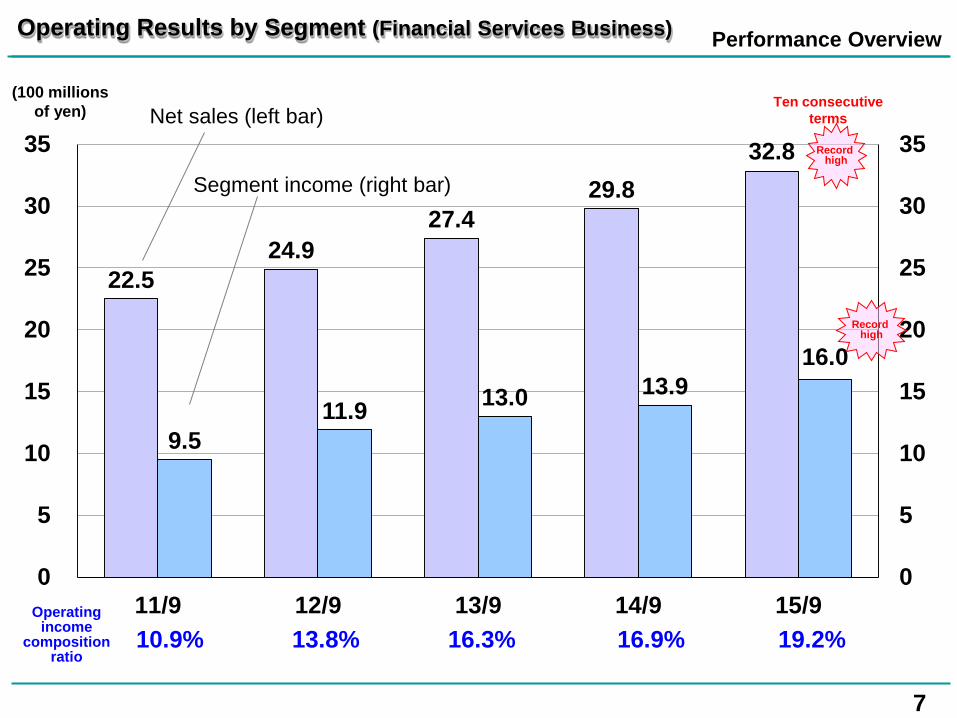

22.5 24.9

27.4 29.8

32.8

9.5 11.9 13.0 13.9

16.0

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

11/9 12/9 13/9 14/9 15/9

7

Operating Results by Segment (Financial Services Business)

Net sales (left bar) (100 millions

of yen)

Operating income

composition ratio

10.9% 13.8% 16.3% 16.9% 19.2%

Record high

Segment income (right bar)

Record high

Ten consecutive terms

Performance Overview

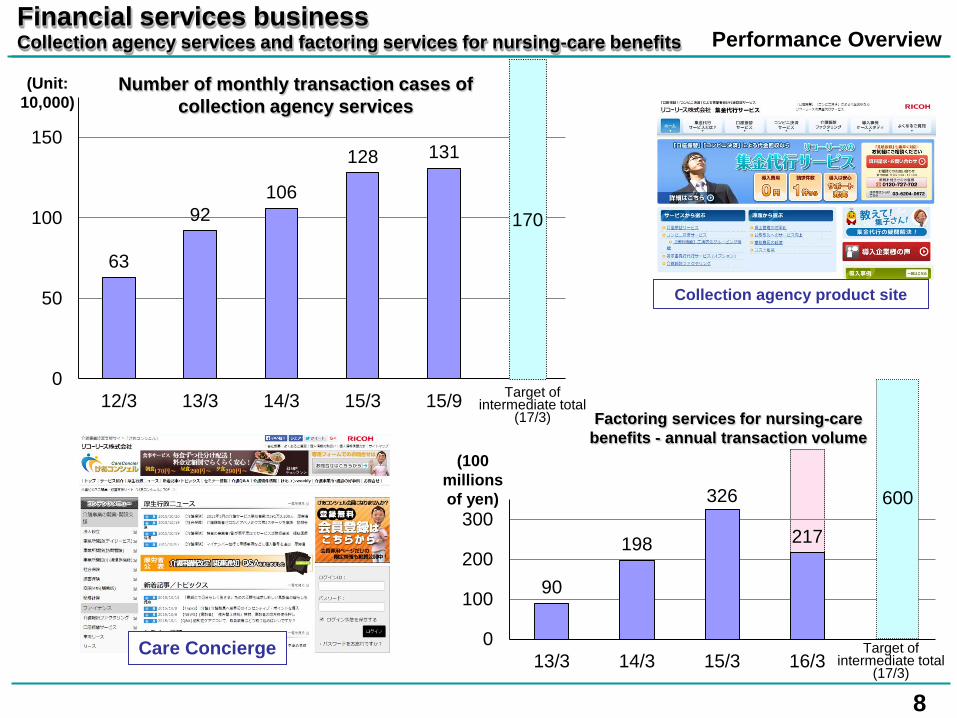

63

92 106

128 131

0

50

100

150

12/3 13/3 14/3 15/3 15/9

8

Financial services business Collection agency services and factoring services for nursing-care benefits

Number of monthly transaction cases of collection agency services

Factoring services for nursing-care benefits - annual transaction volume

Collection agency product site

(Unit: 10,000)

Target of intermediate total

(17/3)

90

198

326

217

0

100

200

300

13/3 14/3 15/3 16/3

600

170

(100 millions of yen)

Care Concierge Target of intermediate total

(17/3)

Performance Overview

9

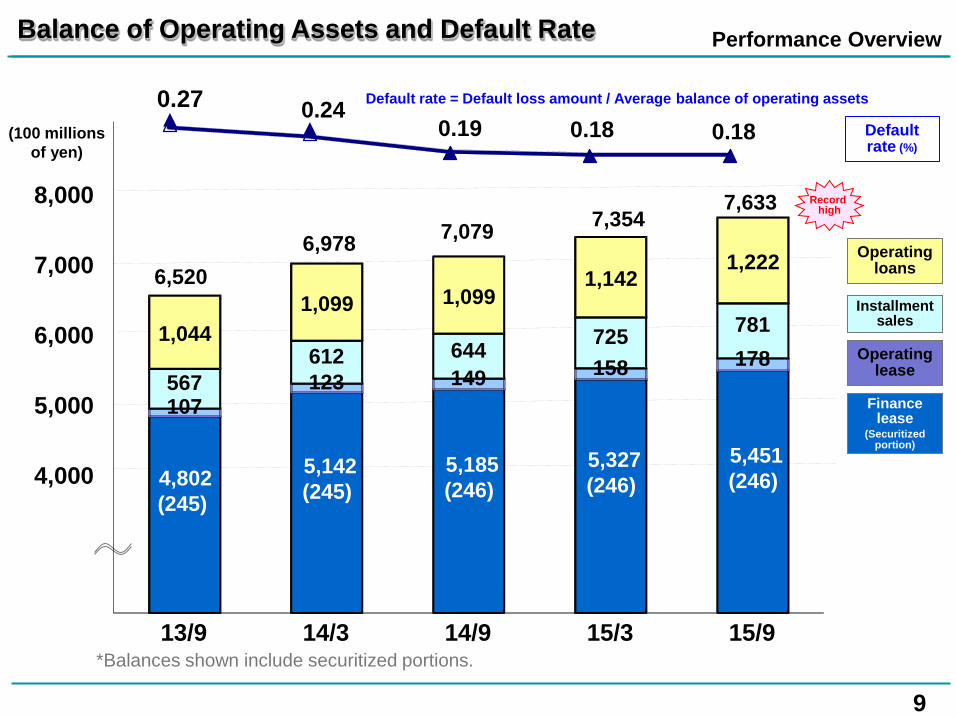

Balance of Operating Assets and Default Rate

Finance lease

(Securitized portion)

Operating loans

Installment sales

Operating lease

*Balances shown include securitized portions.

7,079 7,354

6,520

Default rate = Default loss amount / Average balance of operating assets

Default rate (%)

6,978

7,633

(100 millions of yen)

Record high

4,802 (245)

5,142 (245)

5,185 (246)

5,327 (246)

5,451 (246)

107 123 149 158 178

567 612 644 725 781 1,044

1,099 1,099 1,142

1,222

4,000

5,000

6,000

7,000

8,000

13/9 14/3 14/9 15/3 15/9

0.27 0.24 0.19 0.18 0.18

Performance Overview

10

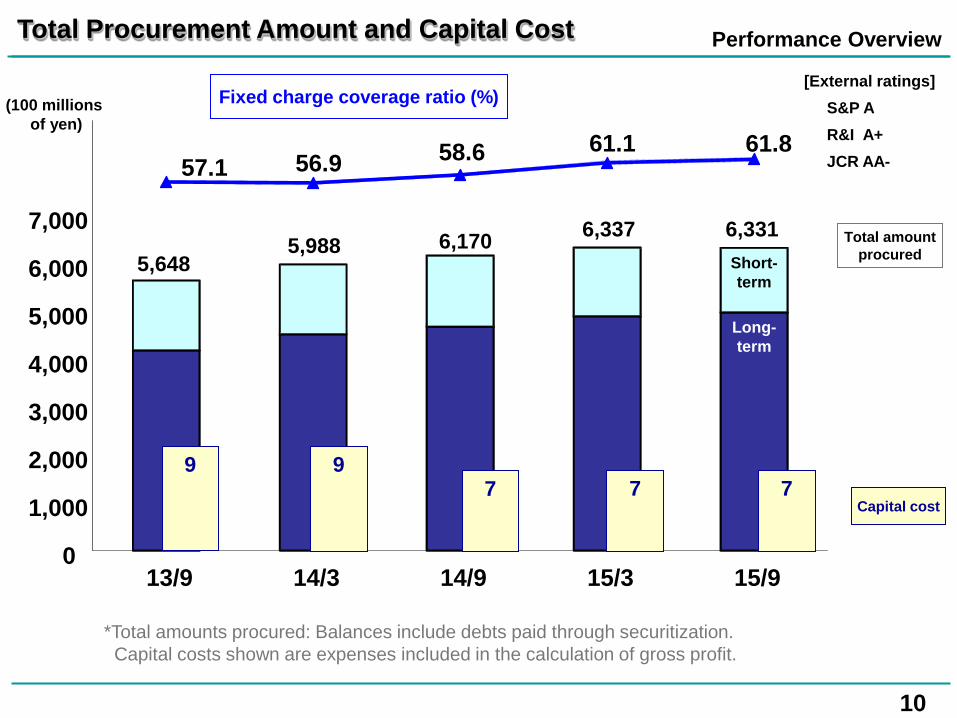

Total Procurement Amount and Capital Cost

[External ratings] S&P A R&I A+ JCR AA-

Fixed charge coverage ratio (%)

Capital cost

Total amount procured

*Total amounts procured: Balances include debts paid through securitization. Capital costs shown are expenses included in the calculation of gross profit.

Long-term

Short-term

57.1 56.9 58.6 61.1 61.8

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

13/9 14/3 14/9 15/3 15/9

9 7

9 7 7

5,648 5,988 6,170 6,337 6,331

(100 millions of yen)

Performance Overview

11

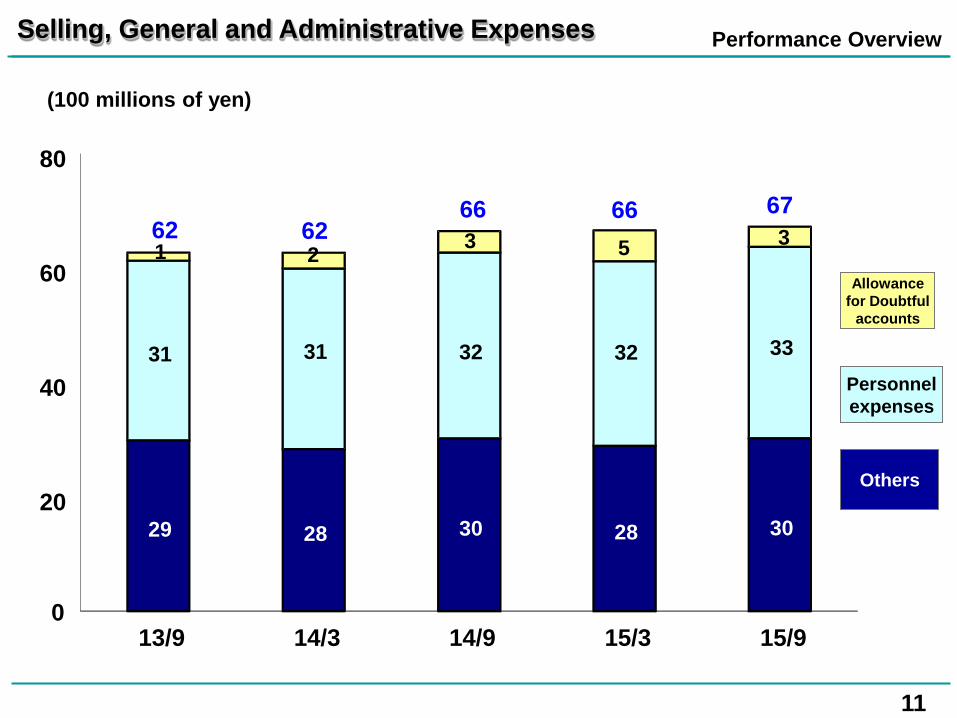

Selling, General and Administrative Expenses

Allowance for Doubtful

accounts

Personnel expenses

Others

(100 millions of yen)

66 66 62 62

67

29 28 30 28 30

31 31 32 32 33

1 2 3 5 3

20

40

60

80

13/9 14/3 14/9 15/3 15/9 0

12

2. Financial Forecast (Fiscal Year Ending March 2016)

Financial Forecast

13

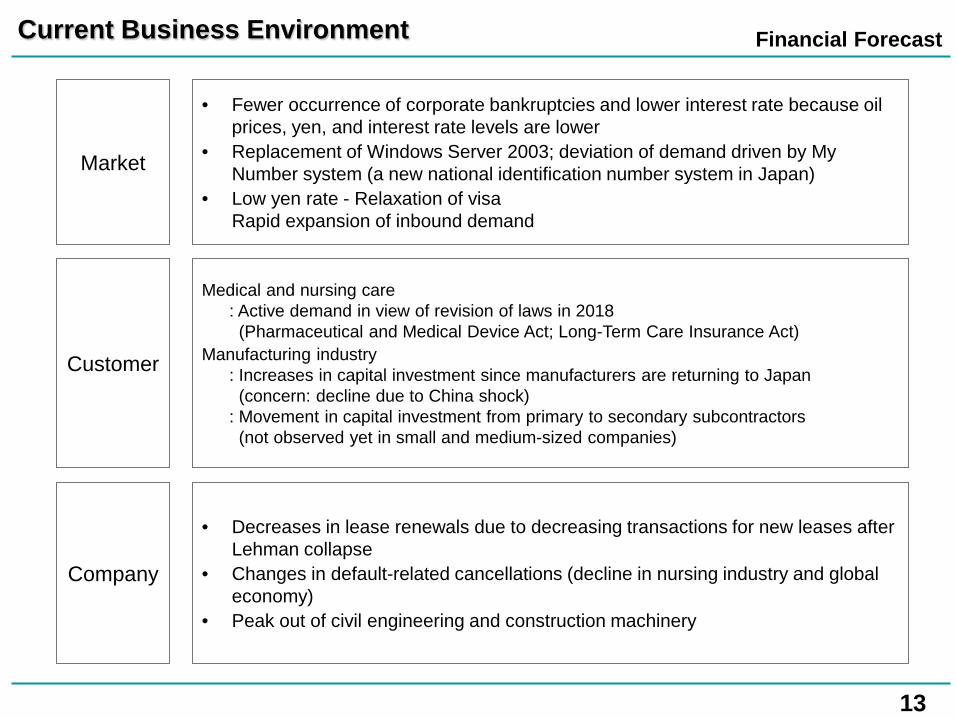

Current Business Environment

• Fewer occurrence of corporate bankruptcies and lower interest rate because oil prices, yen, and interest rate levels are lower

• Replacement of Windows Server 2003; deviation of demand driven by My Number system (a new national identification number system in Japan)

• Low yen rate - Relaxation of visa Rapid expansion of inbound demand

Market

• Decreases in lease renewals due to decreasing transactions for new leases after Lehman collapse

• Changes in default-related cancellations (decline in nursing industry and global economy)

• Peak out of civil engineering and construction machinery

Company

Medical and nursing care : Active demand in view of revision of laws in 2018 (Pharmaceutical and Medical Device Act; Long-Term Care Insurance Act)

Manufacturing industry : Increases in capital investment since manufacturers are returning to Japan (concern: decline due to China shock) : Movement in capital investment from primary to secondary subcontractors (not observed yet in small and medium-sized companies)

Customer

Financial Forecast

14

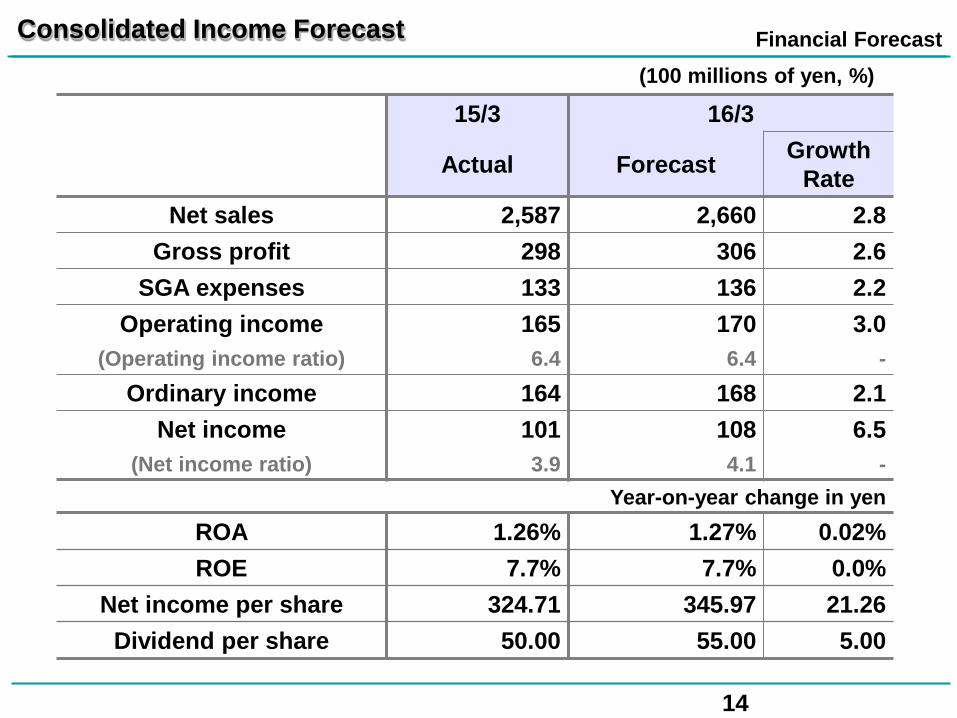

Consolidated Income Forecast (100 millions of yen, %)

15/3 16/3

Actual Forecast Growth Rate

Net sales 2,587 2,660 2.8 Gross profit 298 306 2.6

SGA expenses 133 136 2.2 Operating income 165 170 3.0

(Operating income ratio) 6.4 6.4 - Ordinary income 164 168 2.1

Net income 101 108 6.5 (Net income ratio) 3.9 4.1 -

Year-on-year change in yen ROA 1.26% 1.27% 0.02% ROE 7.7% 7.7% 0.0%

Net income per share 324.71 345.97 21.26 Dividend per share 50.00 55.00 5.00

Financial Forecast

15

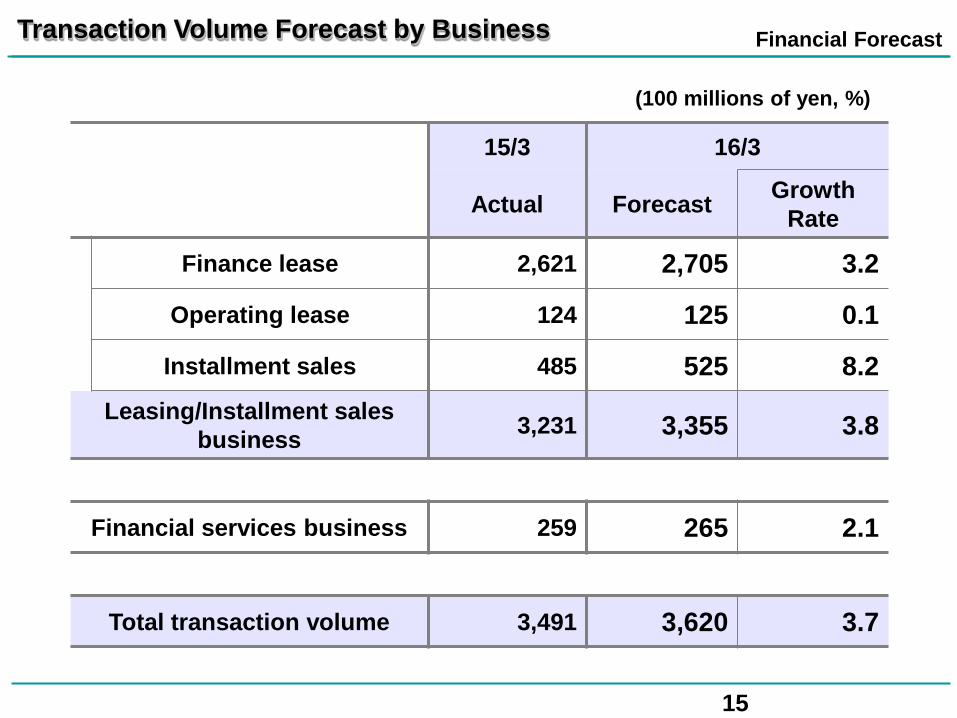

Transaction Volume Forecast by Business

(100 millions of yen, %)

15/3 16/3

Actual Forecast Growth Rate

Finance lease 2,621 2,705 3.2

Operating lease 124 125 0.1

Installment sales 485 525 8.2 Leasing/Installment sales

business 3,231 3,355 3.8

Financial services business 259 265 2.1

Total transaction volume 3,491 3,620 3.7

Financial Forecast

16

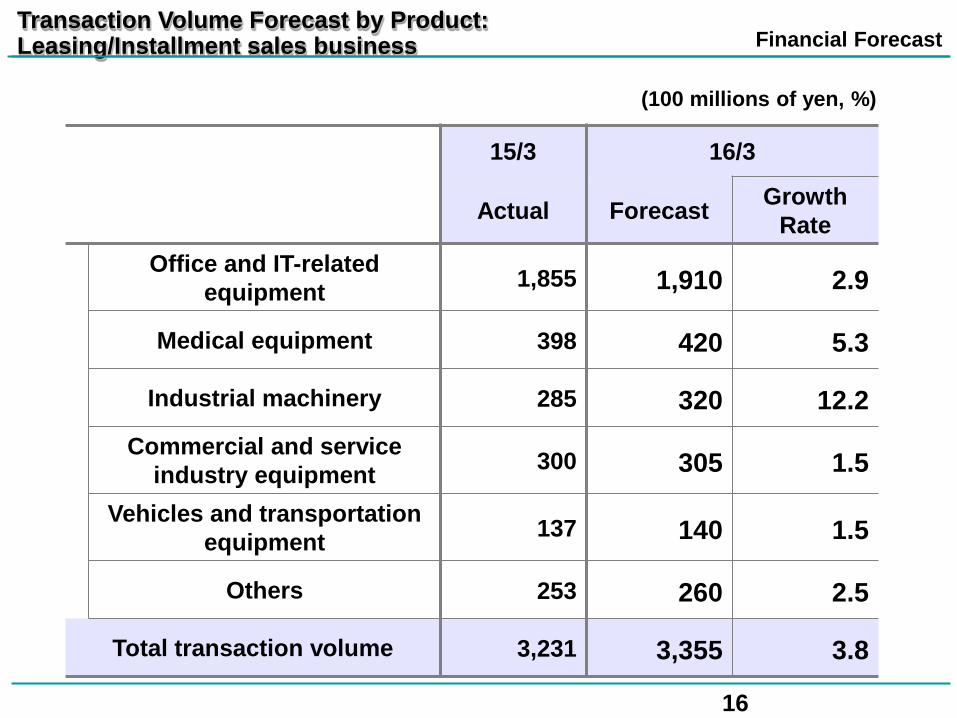

Transaction Volume Forecast by Product: Leasing/Installment sales business

(100 millions of yen, %)

15/3 16/3

Actual Forecast Growth Rate

Office and IT-related equipment 1,855 1,910 2.9

Medical equipment 398 420 5.3

Industrial machinery 285 320 12.2 Commercial and service

industry equipment 300 305 1.5

Vehicles and transportation equipment 137 140 1.5

Others 253 260 2.5

Total transaction volume 3,231 3,355 3.8

Financial Forecast

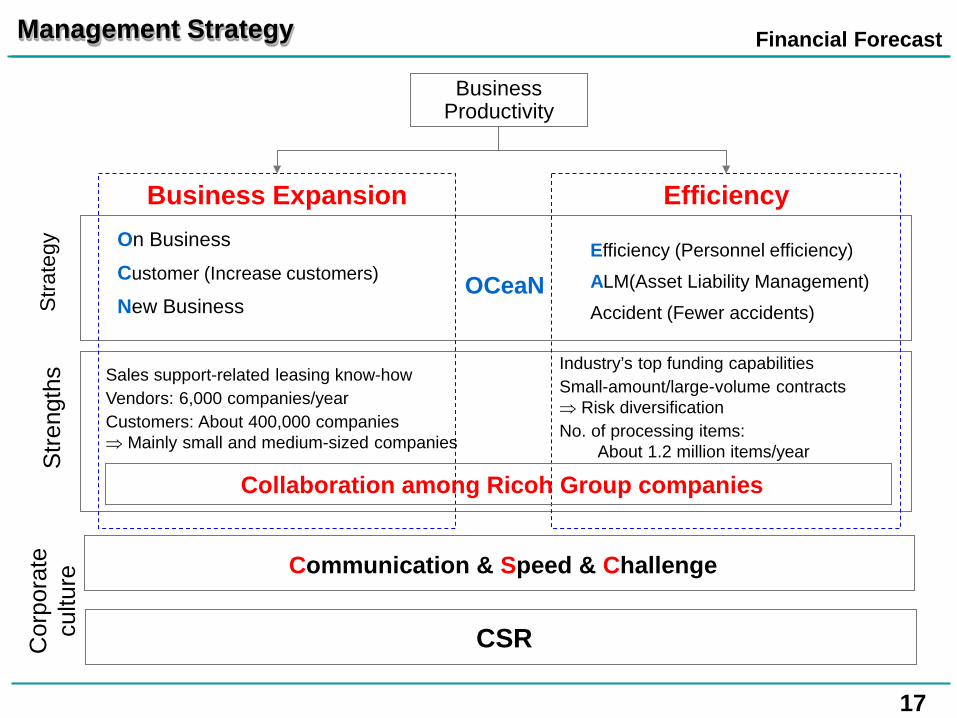

17

Management Strategy

Business Expansion Efficiency

Business Productivity

On Business

Customer (Increase customers)

New Business

Efficiency (Personnel efficiency)

ALM(Asset Liability Management)

Accident (Fewer accidents)

Sales support-related leasing know-how Vendors: 6,000 companies/year Customers: About 400,000 companies ⇒ Mainly small and medium-sized companies

Industry’s top funding capabilities Small-amount/large-volume contracts ⇒ Risk diversification No. of processing items:

About 1.2 million items/year

OCeaN

Stra

tegy

S

treng

ths

Collaboration among Ricoh Group companies

Communication & Speed & Challenge

CSR Cor

pora

te

cultu

re

Financial Forecast

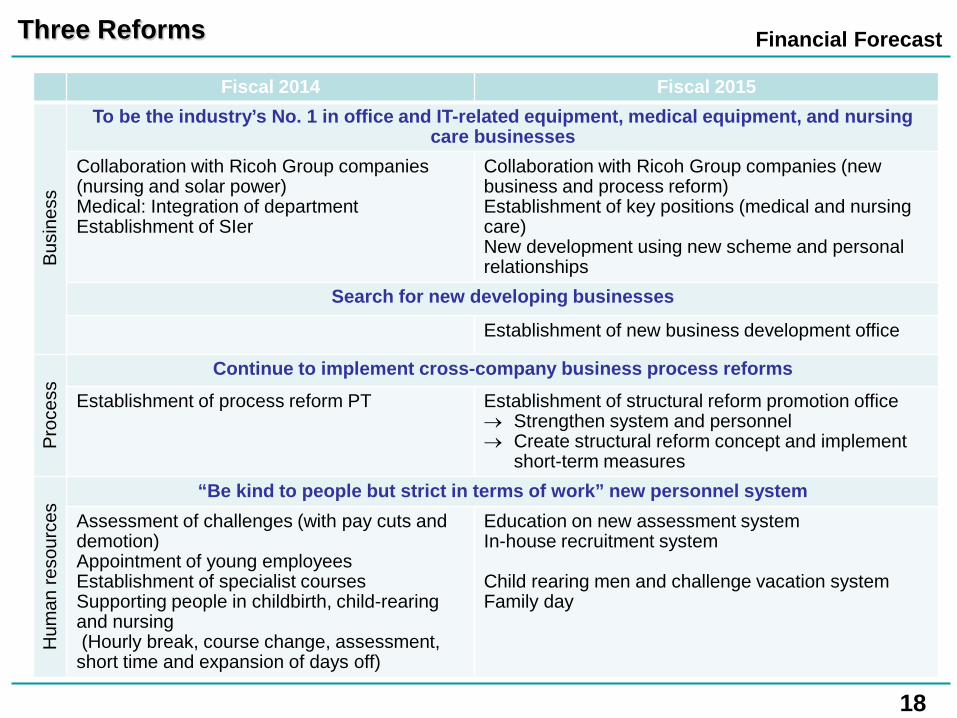

18

Fiscal 2014 Fiscal 2015

Bus

ines

s

To be the industry’s No. 1 in office and IT-related equipment, medical equipment, and nursing care businesses

Collaboration with Ricoh Group companies (nursing and solar power) Medical: Integration of department Establishment of SIer

Collaboration with Ricoh Group companies (new business and process reform) Establishment of key positions (medical and nursing care) New development using new scheme and personal relationships

Search for new developing businesses

Establishment of new business development office

Pro

cess

Continue to implement cross-company business process reforms Establishment of process reform PT Establishment of structural reform promotion office

→ Strengthen system and personnel → Create structural reform concept and implement

short-term measures

Hum

an re

sour

ces

“Be kind to people but strict in terms of work” new personnel system Assessment of challenges (with pay cuts and demotion) Appointment of young employees Establishment of specialist courses Supporting people in childbirth, child-rearing and nursing (Hourly break, course change, assessment, short time and expansion of days off)

Education on new assessment system In-house recruitment system Child rearing men and challenge vacation system Family day

Three Reforms

Financial Forecast

19

Final Summary

OCeaN Strategy

New

20

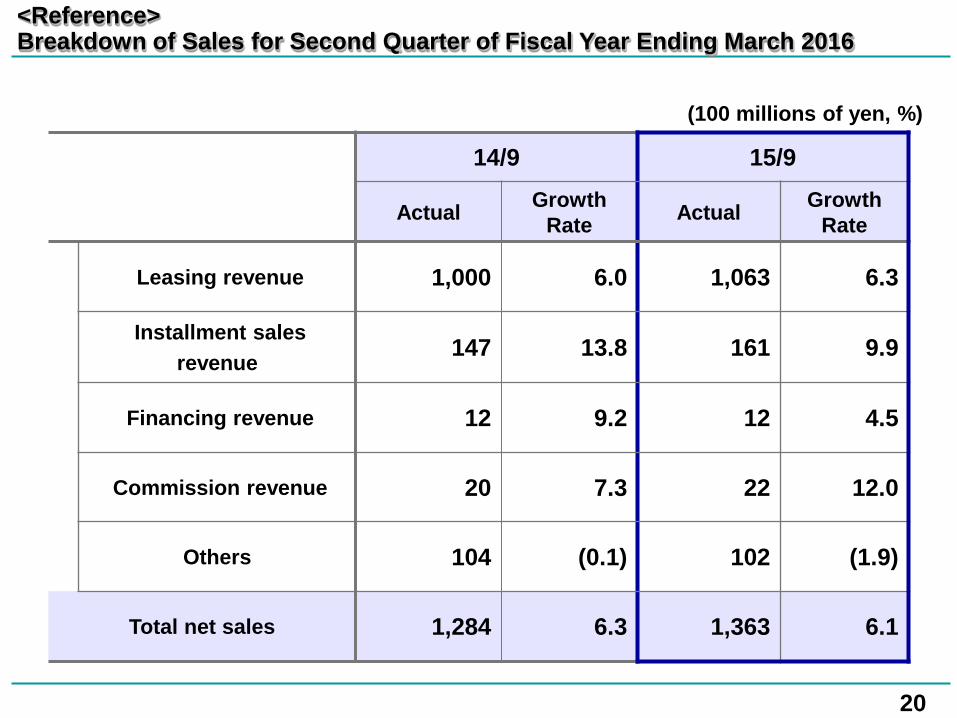

(100 millions of yen, %)

14/9 15/9

Actual Growth Rate Actual Growth

Rate

Leasing revenue 1,000 6.0 1,063 6.3

Installment sales revenue 147 13.8 161 9.9

Financing revenue 12 9.2 12 4.5

Commission revenue 20 7.3 22 12.0

Others 104 (0.1) 102 (1.9)

Total net sales 1,284 6.3 1,363 6.1

<Reference> Breakdown of Sales for Second Quarter of Fiscal Year Ending March 2016

21

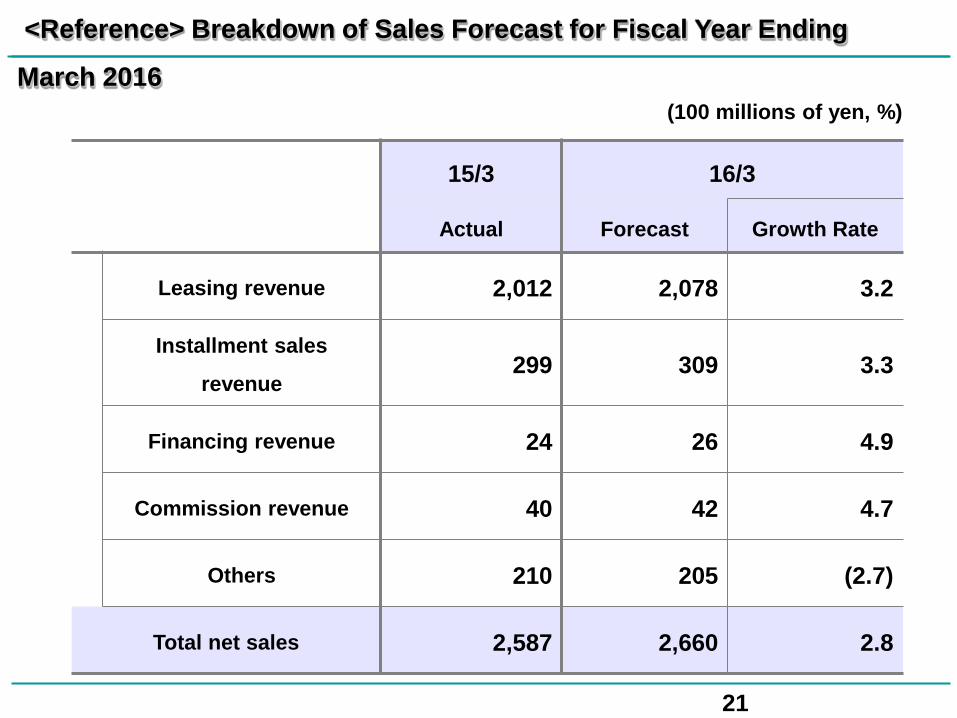

<Reference> Breakdown of Sales Forecast for Fiscal Year Ending

March 2016 (100 millions of yen, %)

15/3 16/3

Actual Forecast Growth Rate

Leasing revenue 2,012 2,078 3.2

Installment sales

revenue 299 309 3.3

Financing revenue 24 26 4.9

Commission revenue 40 42 4.7

Others 210 205 (2.7)

Total net sales 2,587 2,660 2.8

22

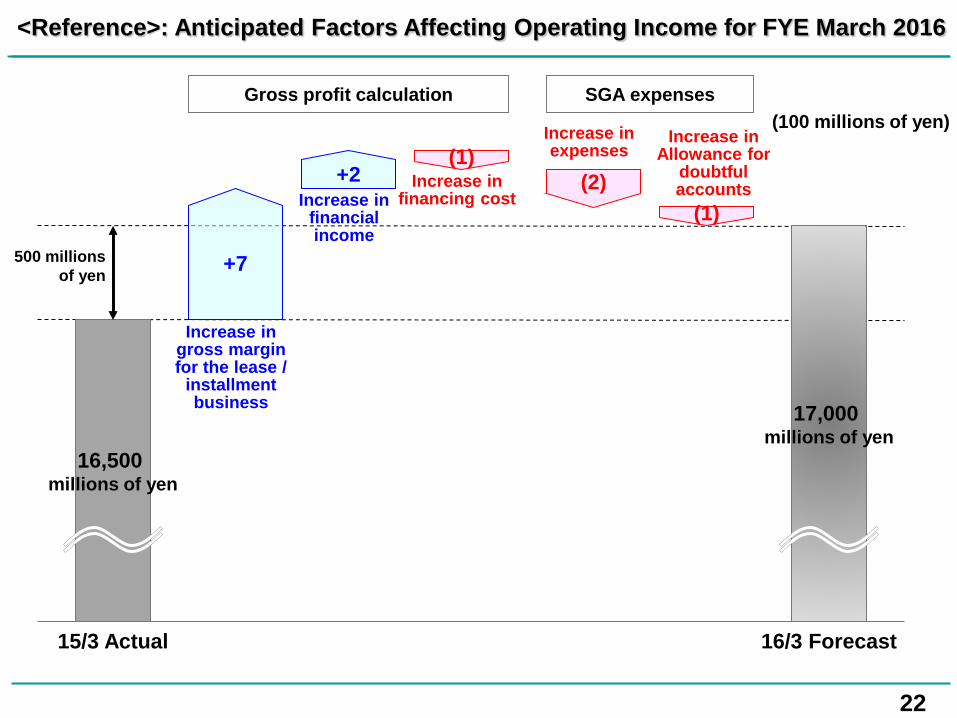

<Reference>: Anticipated Factors Affecting Operating Income for FYE March 2016

(100 millions of yen)

17,000 millions of yen

16/3 Forecast

16,500 millions of yen

500 millions of yen

Gross profit calculation SGA expenses

Increase in Allowance for

doubtful accounts

15/3 Actual

(1)

+2 Increase in

financial income

Increase in gross margin for the lease /

installment business

Increase in financing cost

Increase in expenses

(2)

+7

(1)

Performance Overview

23

Forward-looking statements including earnings forecasts contained in this document are based on certain assumptions deemed to be rational in light of the information available to the Company at the time of preparing the document, and are not intended to be guarantees of future performance. Actual results may differ significantly from plans and forecasts due to a variety of factors.

Reliability for

the Future Ricoh Leasing Company, Ltd.

Ricoh Leasing Company, Ltd.