Indian Institute of Management, Ahmedabad

Stabilization Scenarios and Implications for India

P.R. Shukla

WORKSHOP on Greenhouse Gas Stabilization ScenariosJanuary 22-23, 2004, Tsukuba, Japan

Stabilization Scenarios and Implications for India

Integrated Economy-Energy-Environment Modeling System for India

Stabilization Scenarios and Implications for India

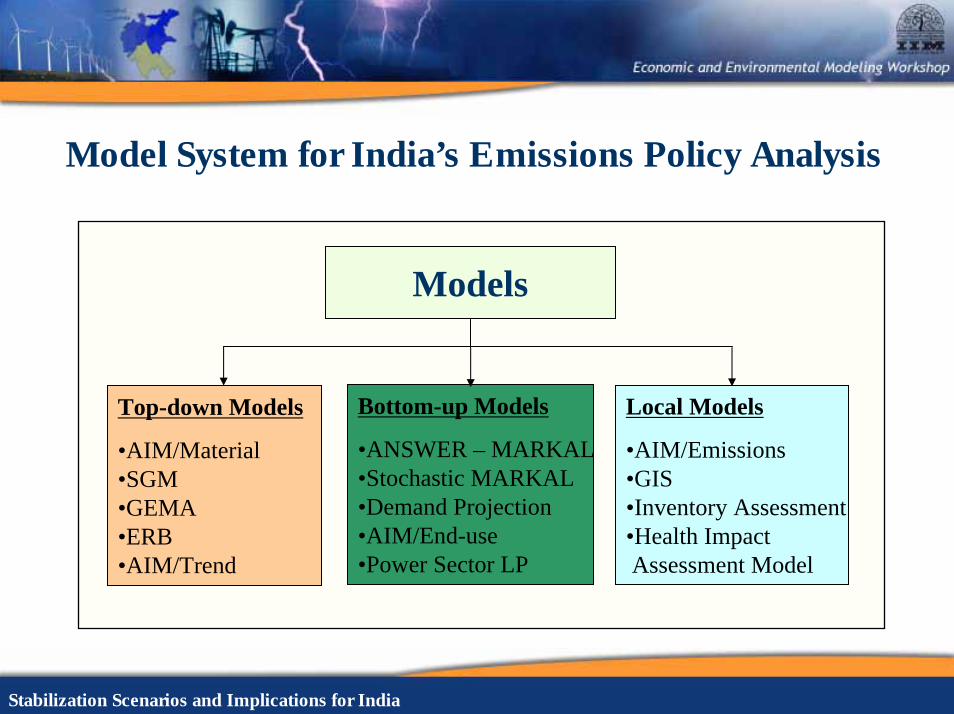

Model System for India’s Emissions Policy Analysis

Models

Top-down Models

•AIM/Material•SGM•GEMA•ERB•AIM/Trend

Local Models

•AIM/Emissions•GIS •Inventory Assessment•Health Impact Assessment Model

Bottom-up Models

•ANSWER – MARKAL•Stochastic MARKAL•Demand Projection•AIM/End-use•Power Sector LP

Stabilization Scenarios and Implications for India

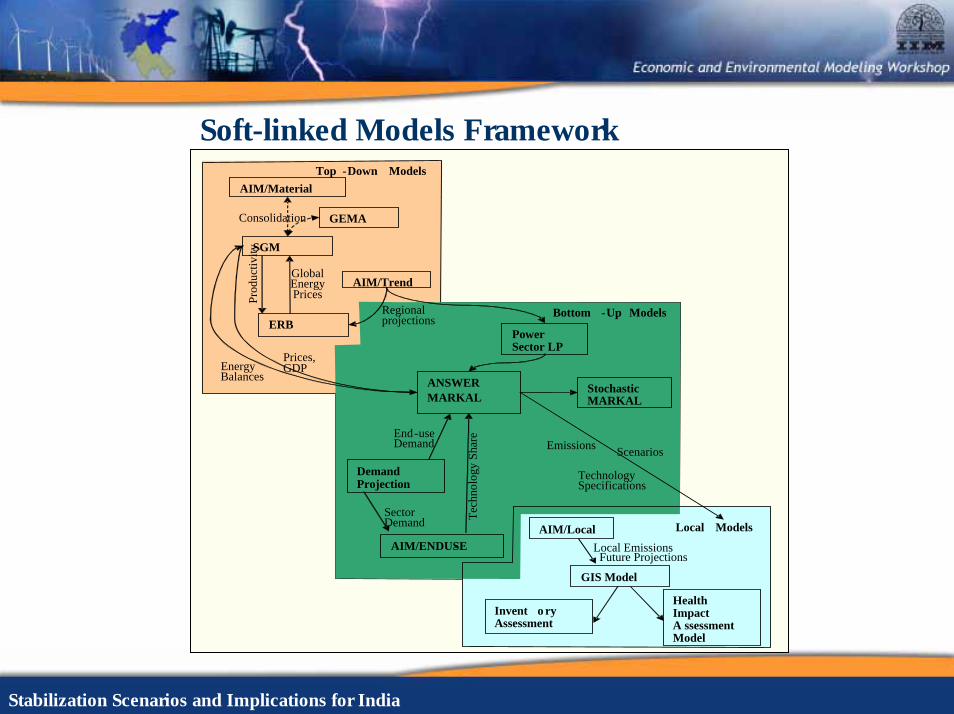

Soft-linked Models Framework

ERB

SGM

AIM/Material

AIM/Trend

Invent o ry Assessment

Health Impact A ssessment Model

GIS Model

Prod

uctiv

ity

Global Energy Prices

Regional projections

Power Sector LP

Demand Projection

AIM/ENDUSE-

ANSWER MARKAL

Stochastic MARKAL

AIM/Local

Bottom -Up Models

Energy Balances

SectorDemand

End-use Demand

Tech

nolo

gy S

hare

ScenariosEmissions

Consolidation

Prices, GDP

Local Models

Top -Down Models

GEMA

Local EmissionsFuture Projections

Technology Specifications

Stabilization Scenarios and Implications for India

Medium-Term National Scenarios (for Emissions Projections)

Stabilization Scenarios and Implications for India

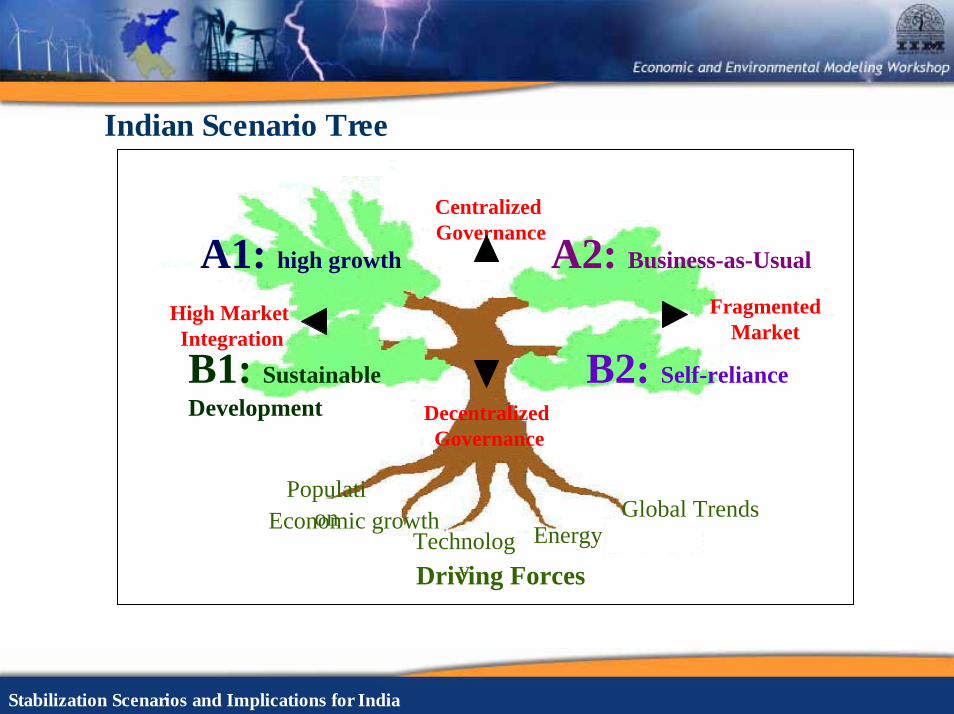

Indian Scenario Tree

Centralized Governance

Decentralized Governance

FragmentedMarket

High Market Integration

A2: Business-as-Usual

B1: Sustainable Development

B2: Self-reliance

PopulationEconomic growth

Technology

EnergyGlobal Trends

Driving Forces

A1: high growth

Stabilization Scenarios and Implications for India

Indian Scenarios

Fragmented

IA1

China

IA2

Pre-reform(Mixed Economy Model)IB1

Sustainable Development

IB2

Self Reliance Model

Cen

tral

izat

ion

Dec

e ntr

ali z

atio

nMarket integration

Gov

erna

nce

Integrated

Stabilization Scenarios and Implications for India

Governance

Decentralization

Demand-side orientation

Competition

Regional development

Rural focus

Distributed utilities

Medium/high population

Low/medium GDP growth

Centralization

Supply-side orientation

State Monopoly

Top-down development

Central planning/ policies

Focused Industries

Low/medium population

Medium/high GDP Growth

Stabilization Scenarios and Implications for India

Market Integration

High integration

High-medium growth

Low tariffs

Technology transfer

External investment

Globalization/ competition

Low integration

Low-medium growth

High tariffs

Indigenous technology

Self reliance model

Fragmanted market

Stabilization Scenarios and Implications for India

India: Population Projection

High

Medium

Low

1000

1100

1200

1300

1400

1500

2001 2011 2021 2031

Years

Pop

ulat

ion

(Mill

ion)

Stabilization Scenarios and Implications for India

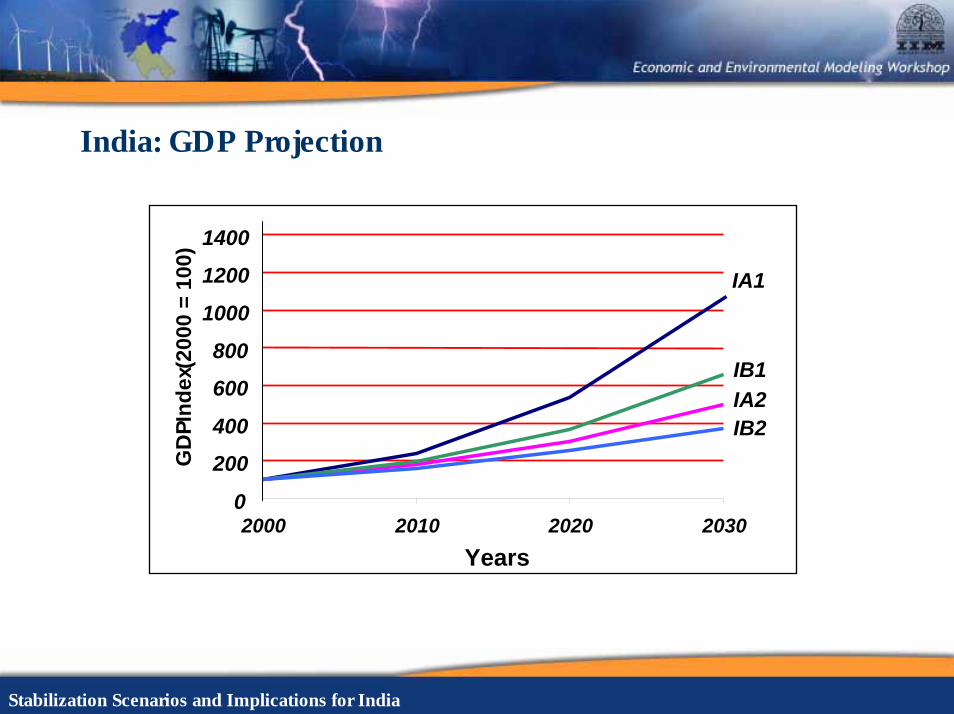

India: GDP Projection

0

200

400

600

800

1000

1200

1400

2000 2010 2020 2030Years

GD

P Ind

ex(2

000

= 10

0)

IA1

IB1IA2IB2

Stabilization Scenarios and Implications for India

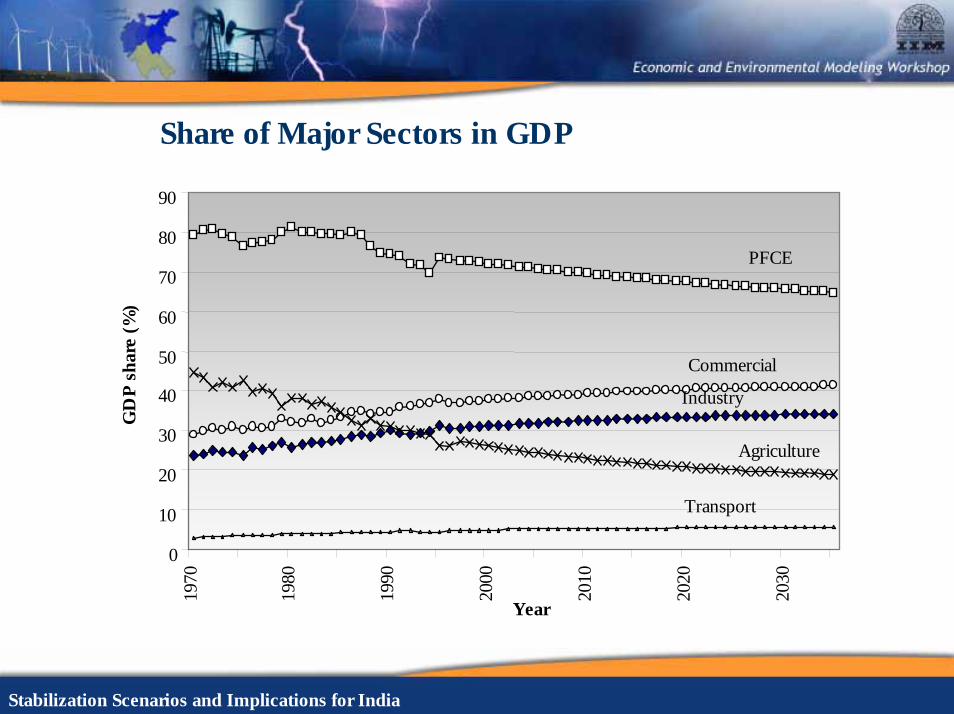

Share of Major Sectors in GDP

0

10

20

30

40

50

60

70

80

9019

70

1980

1990

2000

2010

2020

2030

Year

GD

P s

har

e (%

)

Industry

Commercial

Transport

Agriculture

PFCE

Stabilization Scenarios and Implications for India

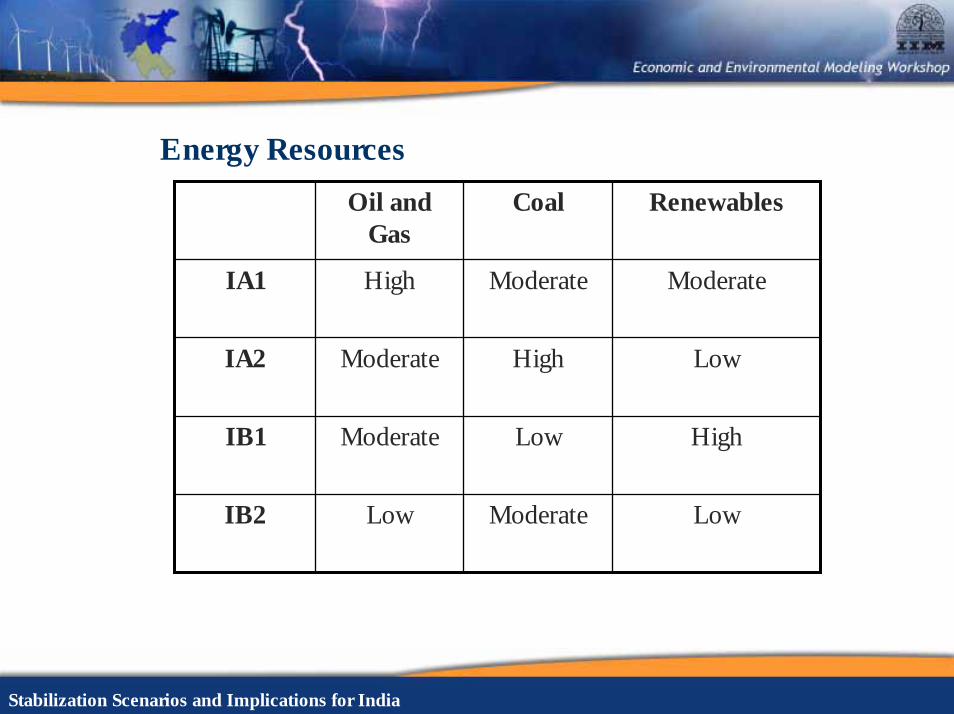

Energy Resources

Oil and Gas

Coal Renewables

IA1 High Moderate Moderate

IA2 Moderate High Low

IB1 Moderate Low High

IB2 Low Moderate Low

Stabilization Scenarios and Implications for India

National Development Goals

1) Economic Security

2) Energy Security

3) Environment Security

4) Water Security

5) Food Security

6) Health Security

Stabilization Scenarios and Implications for India

Future Energy and Emissions Projections for Scenarios

Stabilization Scenarios and Implications for India

Integrated Bottom-Up Modeling System

Long-term Supply & Demand Technology-Mix, Fuel-Mix, Emission, Cost

Energy Sector Optimization Model ( MARKet ALlocation )

Long -Term Demand

Projection ModelTechnology Shares

End -use

Transport Agriculture Residential CommercialIndustry

Urban Rural Steel

Cement

Aluminum

Sugar

Chlor -Alkali PaperBrickTextiles Fertilizer Others

End -use Sub -Sector Models ( Asia -Pacific Integrated Model/ENDUSE)

Road Rail

Ship Air

Demands

Stabilization Scenarios and Implications for India

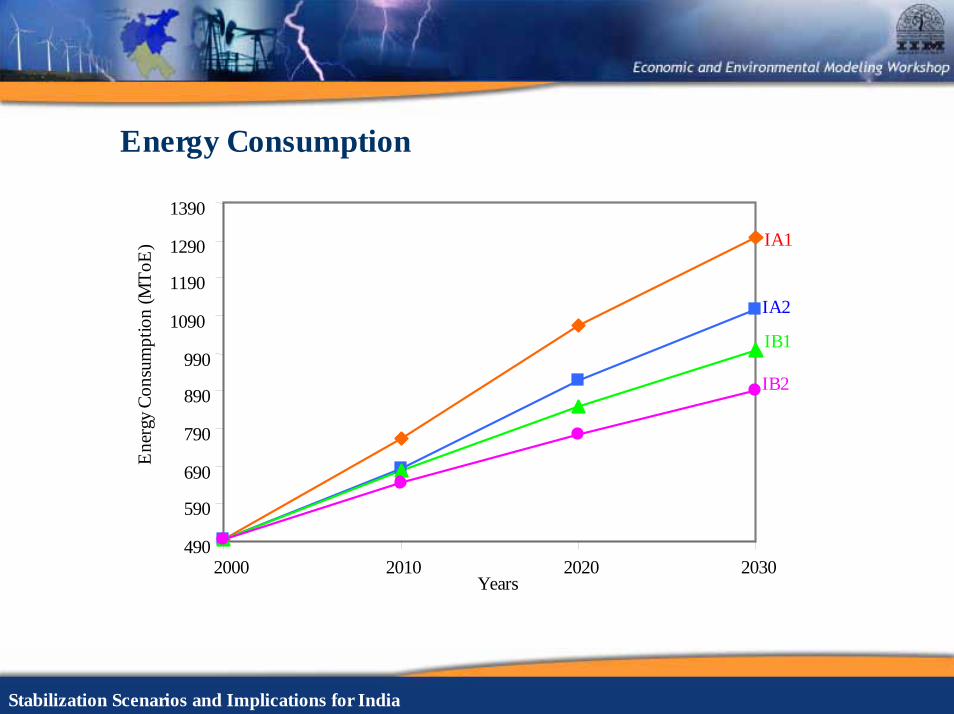

Energy Consumption

Years

490

590

690

790

890

990

1090

1190

1290

1390

2000 2010 2020 2030

Ene

rgy

Cons

umpt

ion

(MTo

E) IA1

IA2

IB1

IB2

Stabilization Scenarios and Implications for India

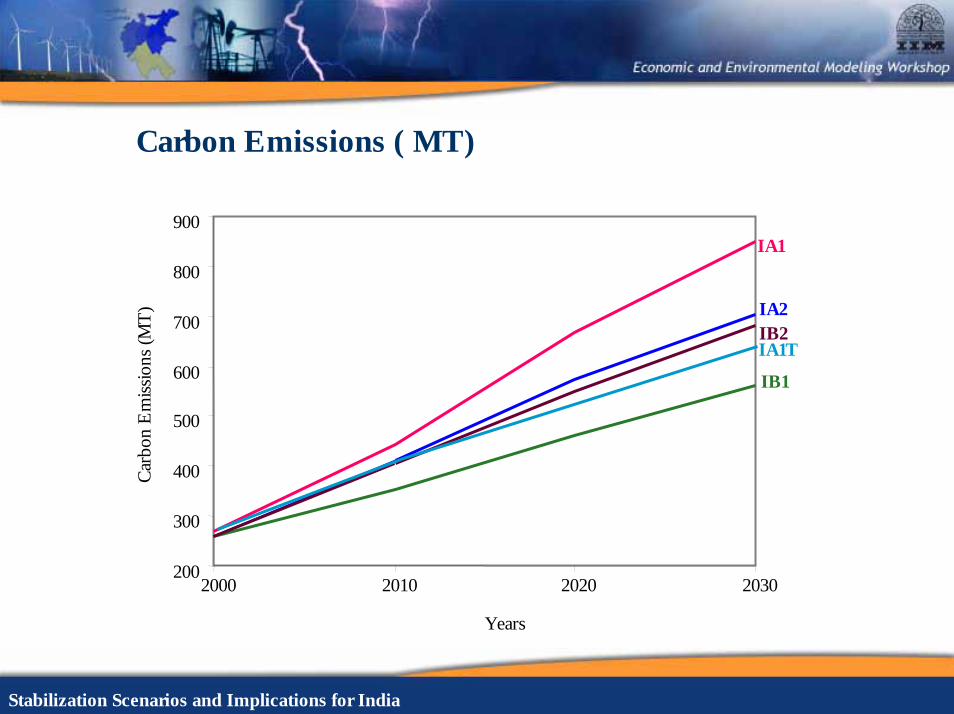

Carbon Emissions ( MT)

200

300

400

500

600

700

800

900

2000 2010 2020 2030

Carb

on E

miss

ions

(MT)

IA1

IA2

IB1

IB2IA1T

Years

Stabilization Scenarios and Implications for India

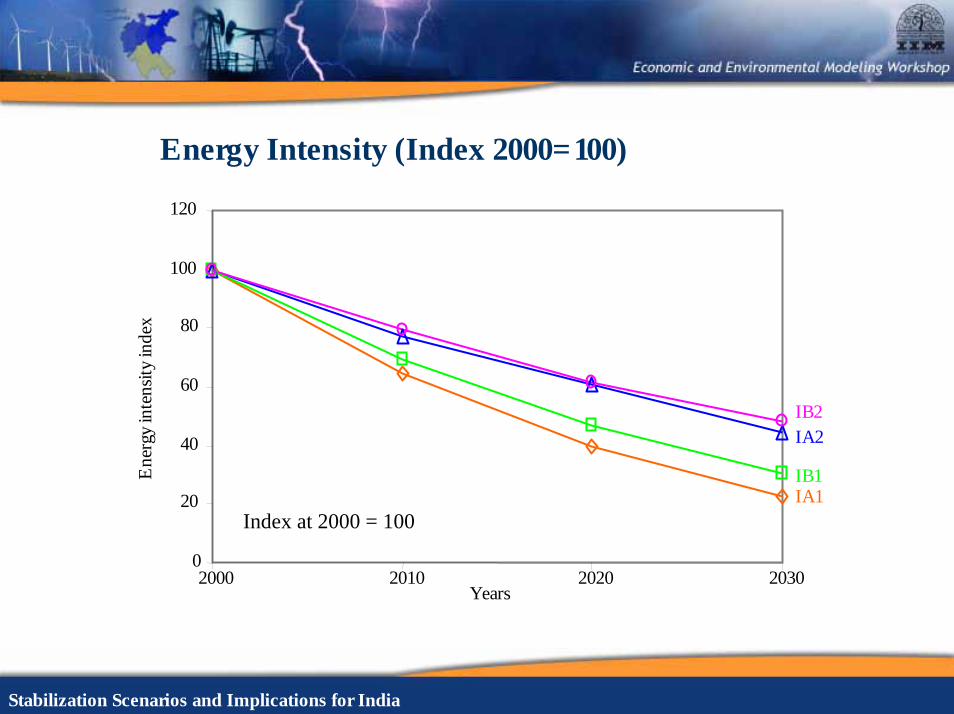

Energy Intensity (Index 2000=100)

0

20

40

60

80

100

120

2000 2010 2020 2030Years

Ene

rgy

inte

nsity

inde

x

IA1

IA2

IB1

IB2

Index at 2000 = 100

Stabilization Scenarios and Implications for India

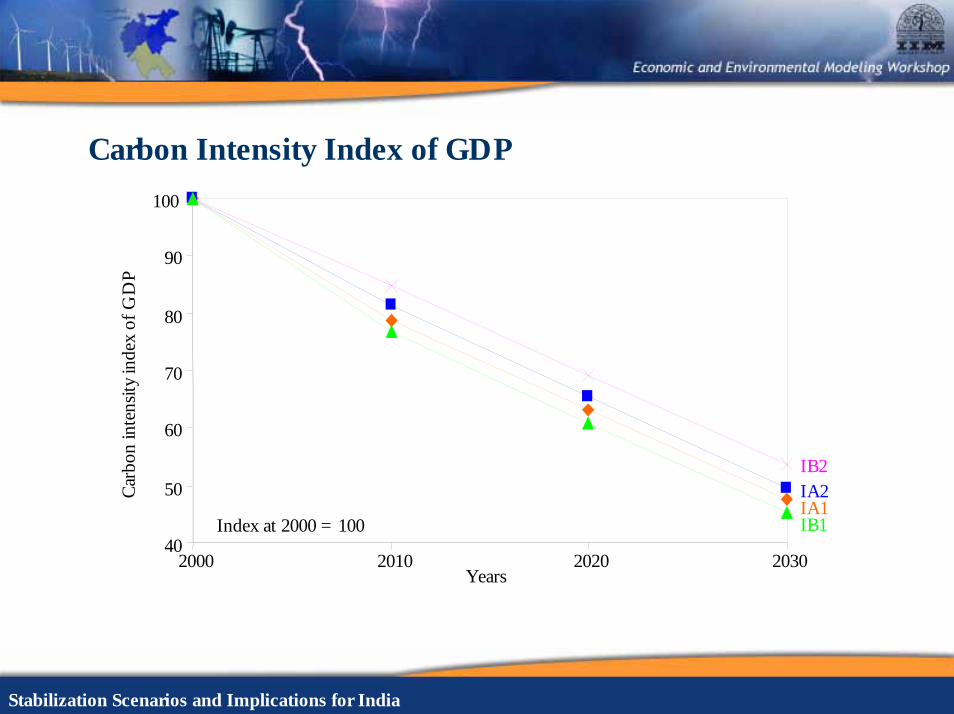

Carbon Intensity Index of GDP

40

50

60

70

80

90

100

2000 2010 2020 2030Years

Carb

on in

tens

ity in

dex

of G

DP

IA1IA2

IB1

IB2

Index at 2000 = 100

Stabilization Scenarios and Implications for India

Per Capita Carbon Emissions (kgC/person)

250

300

350

400

450

500

550

600

650

700

2000 2010 2020 2030Years

Per

Cap

ita

Em

issi

ons

IA1

IA2

IB1

IB2

Stabilization Scenarios and Implications for India

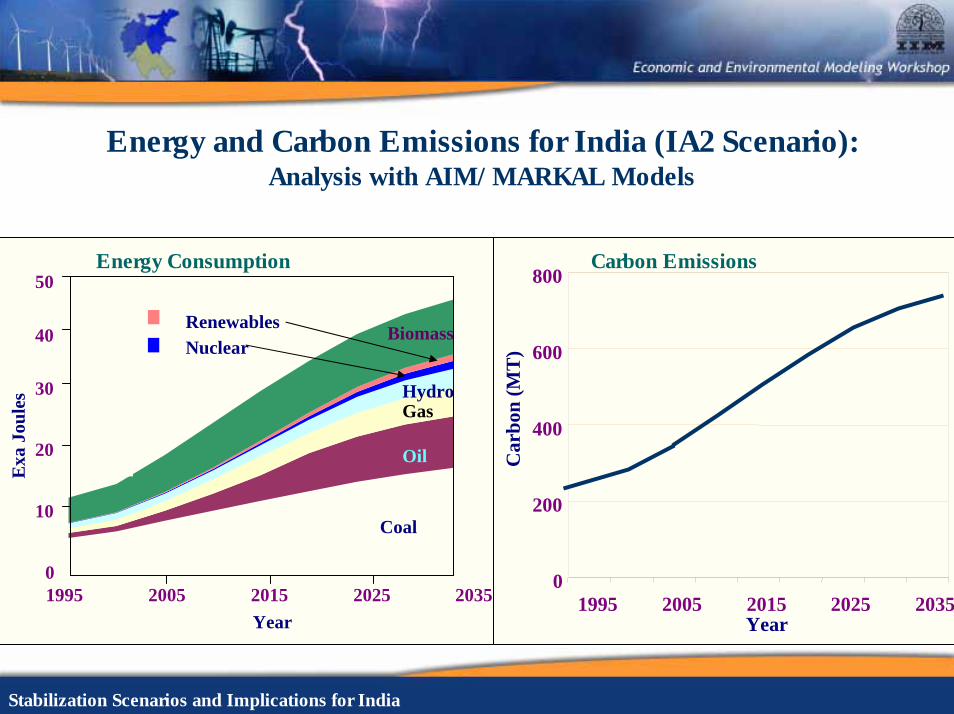

Energy and Carbon Emissions for India (IA2 Scenario): Analysis with AIM/MARKAL Models

0

200

400

600

800

1995 2005 2015 2025 2035Year

Car

bon

(MT

)

0

10

20

30

40

50

1995 2005 2015 2025 2035Year

Exa

Joul

es

Coal

Oil

GasHydro

NuclearRenewables Biomass

Carbon EmissionsEnergy Consumption

Stabilization Scenarios and Implications for India

Energy, Carbon, Electricity and GDP(IA2 Scenario)

0

2

4

6

8

10

12

14

16

18

20

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Energy Carbon Electricity GDP

Past Trends

Future Projections

Stabilization Scenarios and Implications for India

GDP intensities of Energy, Electricity and Carbon(IA2 Scenario)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Electricity

CarbonEnergy

Past Trends Future Projections

Stabilization Scenarios and Implications for India

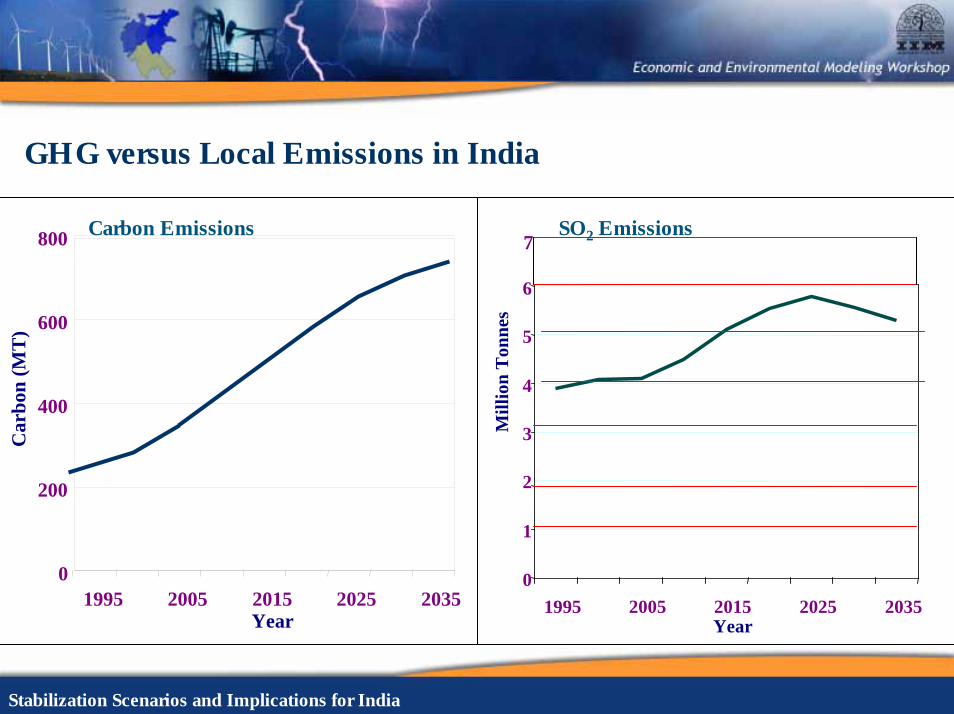

GHG versus Local Emissions in India

0

200

400

600

800

1995 2005 2015 2025 2035Year

Car

bon

(MT

)

Year

Mill

ion

Ton

nes

0

1

2

3

4

5

6

1995 2005 2015 2025 2035

7Carbon Emissions SO2 Emissions

Stabilization Scenarios and Implications for India

Implications of Medium Term Mitigation

Assessment for IA2 Scenario for 2000-2030 Period

Stabilization Scenarios and Implications for India

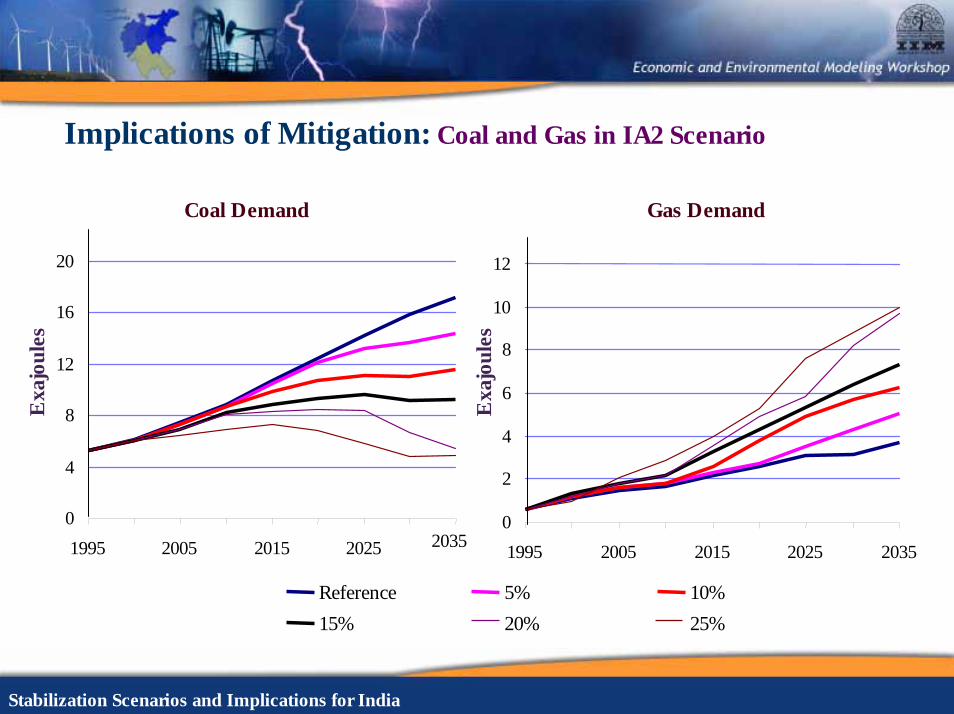

Implications of Mitigation: Coal and Gas in IA2 Scenario

Coal Demand

0

4

8

12

16

20

1995 2005 2015 2025 2035

Exa

jou

les

Reference15%

Gas Demand

0

2

4

6

8

10

12

1995 2005 2015 2025 2035

Exa

jou

les

5% 10%20% 25%

Stabilization Scenarios and Implications for India

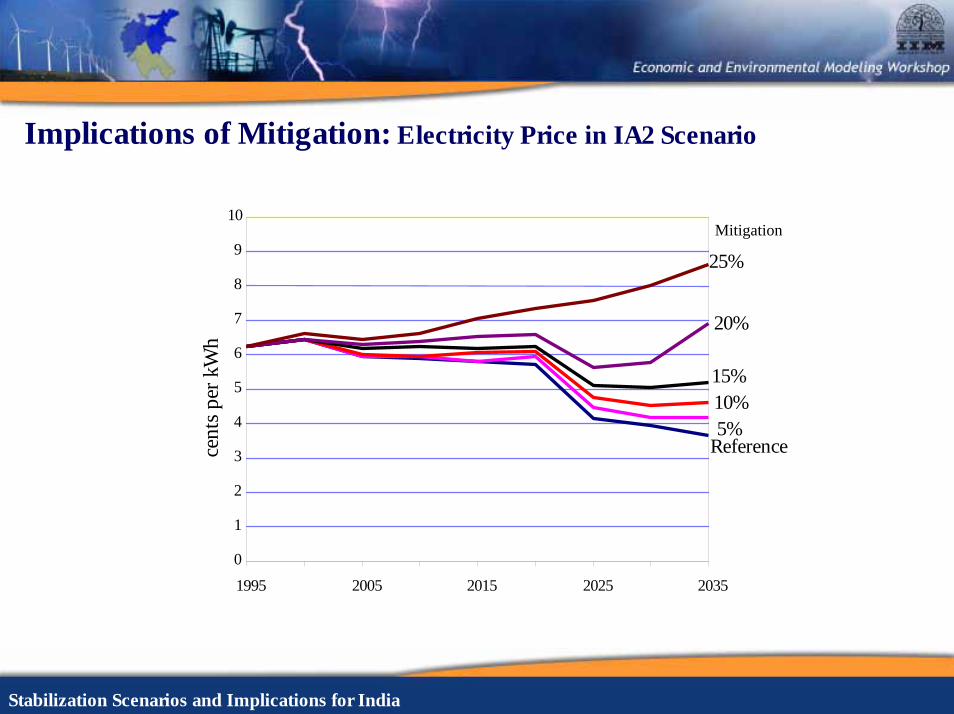

Implications of Mitigation: Electricity Price in IA2 Scenario

0

1

2

3

4

5

6

7

8

9

10

1995 2005 2015 2025 2035

cent

s per

kW

h

Reference5%10%15%

20%

25%

Mitigation

Stabilization Scenarios and Implications for India

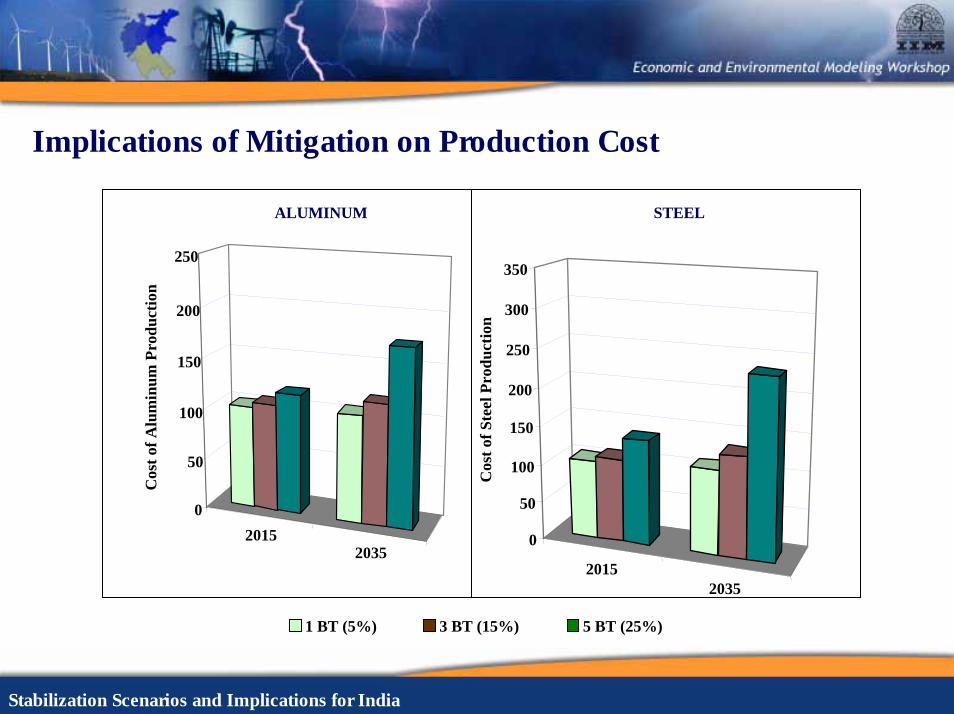

Implications of Mitigation on Production Cost

20152035

0

50

100

150

200

250

Cos

t of A

lum

inum

Pro

duct

ion

ALUMINUM

20152035

0

50

100

150

200

250

300

350

Cos

t of S

teel

Pro

duct

ion

STEEL

1 BT (5%) 3 BT (15%) 5 BT (25%)

Stabilization Scenarios and Implications for India

Carbon Mitigation Supply Curve: (2005-2035)

0

10

20

30

40

50

60

1 2 3 4 5 6 7Carbon abatement (billion ton)

Cos

t ($/

Ton

of C

arbo

n)6 billion tons of mitigation below $25/ ton of carbon

Stabilization Scenarios and Implications for India

Implications of Stabilization Regimes

Assessment for IA2 Scenario for 2000-2100 Period

Stabilization Scenarios and Implications for India

Primary Energy Projections (IA2 Scenario)

21000

20

40

60

80

100

1995 2010 2025 2040 2055 2070 2085Years

Exa

Joul

es

Coal

Liquid

GasNuclear

Hydro

Renewables

Imports

Energy Security Concern

Stabilization Scenarios and Implications for India

Carbon Emission Projections (IA2 Scenario)

0

300

600

900

1200

1500

1800

Milli

on T

onne

s

1995 2010 2025 2040 2055 2070 2085 2100

Power Agriculture Residential&Commercial Industry Transport

208

1655

Stabilization Scenarios and Implications for India

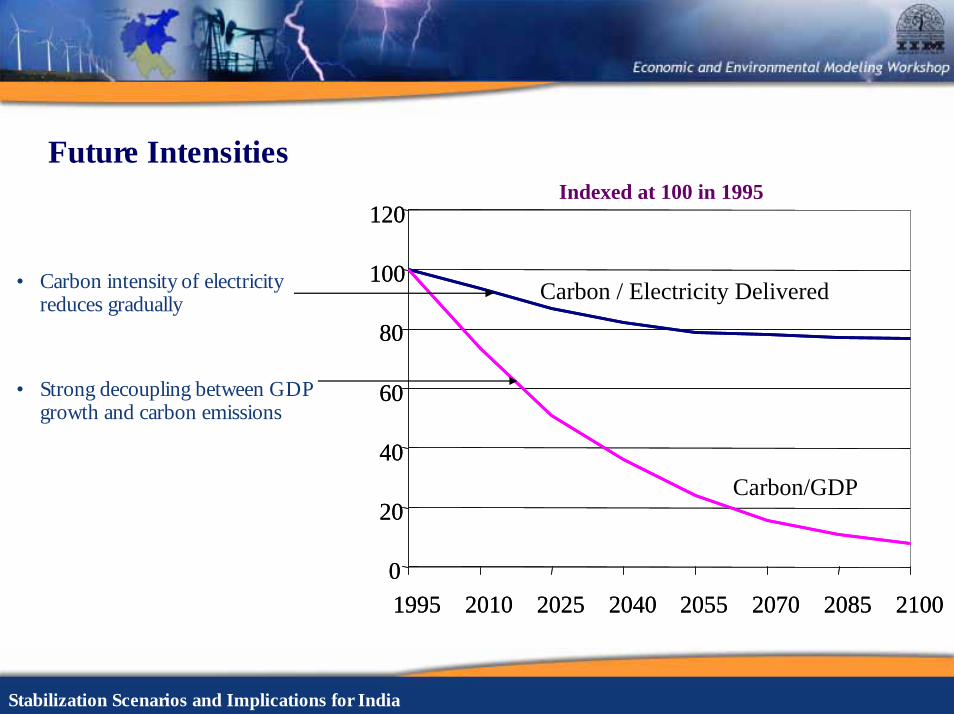

Future Intensities

• Carbon intensity of electricity reduces gradually

• Strong decoupling between GDP growth and carbon emissions

0

20

40

60

80

100

120

1995 2010 2025 2040 2055 2070 2085 21000

20

40

60

80

100

120

1995 2010 2025 2040 2055 2070 2085 2100

Carbon / Electricity Delivered

Carbon/GDP

Indexed at 100 in 1995

Stabilization Scenarios and Implications for India

Carbon Emission Constraints

0

300

600

900

1200

1500

1800

1995 2010 2025 2040 2055 2070 2085 2100

Mill

ion

Ton

550 ppmv

650 ppmv

Base

Stabilization Scenarios and Implications for India

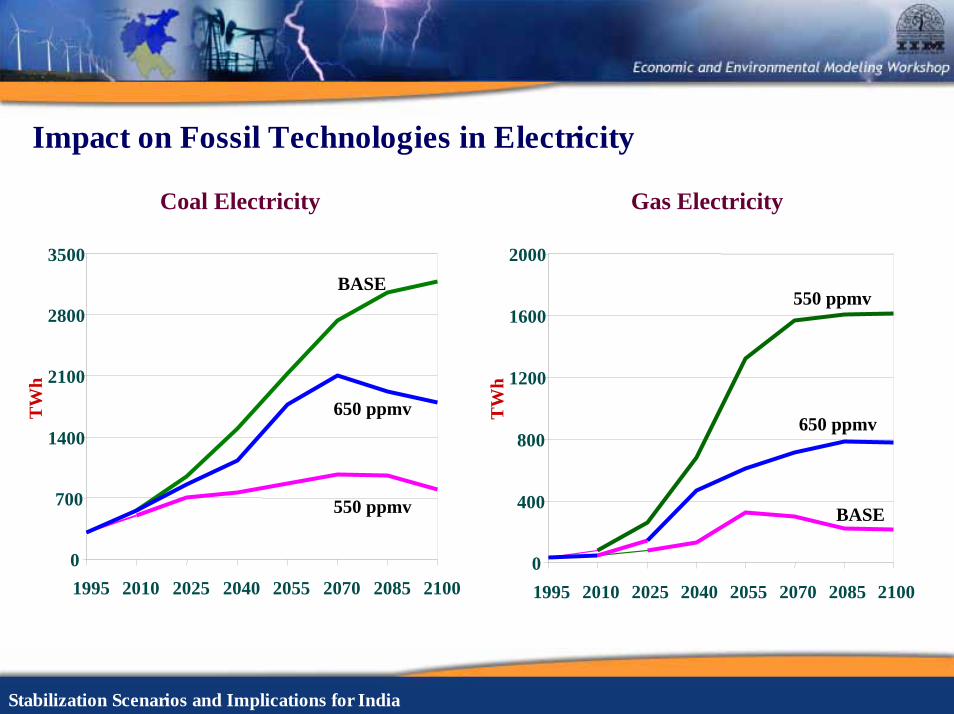

Impact on Fossil Technologies in Electricity

0

700

1400

2100

2800

3500

1995 2010 2025 2040 2055 2070 2085 2100

TW

h

BASE

550 ppmv

650 ppmv

Coal Electricity

0

400

800

1200

1600

2000

1995 2010 2025 2040 2055 2070 2085 2100

TW

h

550 ppmv

650 ppmv

Gas Electricity

BASE

Stabilization Scenarios and Implications for India

Impact on New and Renewable Technologies

0

100

200

300

400

500

2070 2085 2100

TW

h

BASE

550 ppmv

650 ppmv

Nuclear Fusion

0

150

300

450

600

750

1995 2010 2025 2040 2055 2070 2085 2100

TW

h

BASE

550 ppmv

650 ppmv

Renewable Technologies

Stabilization Scenarios and Implications for India

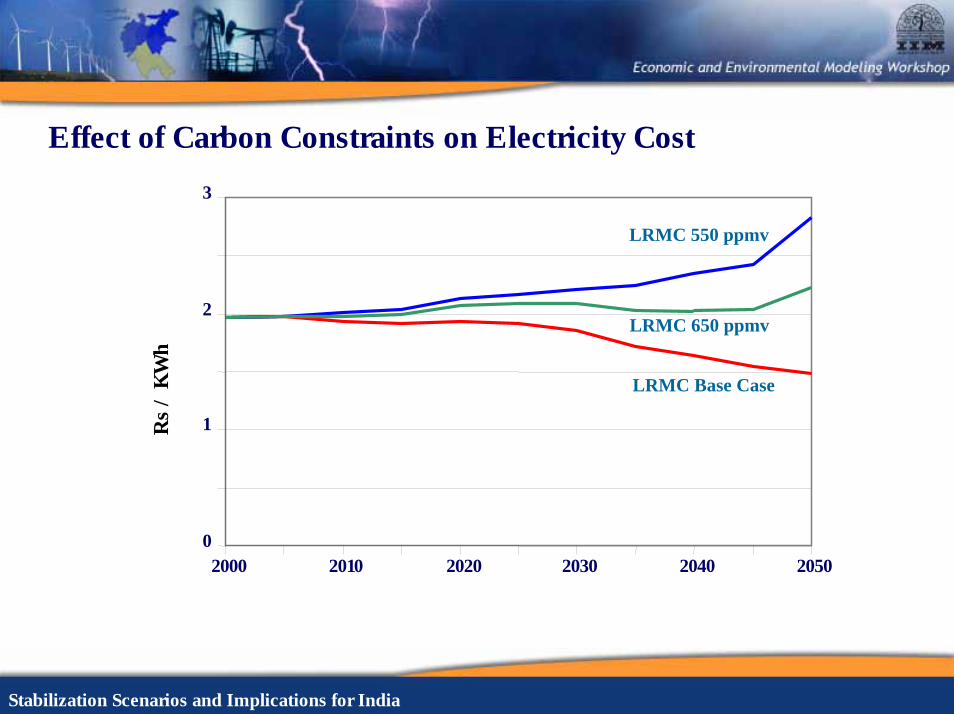

Effect of Carbon Constraints on Electricity Cost

0

1

2

3

2000 2010 2020 2030 2040 2050

Rs

/ K

Wh

LRMC Base Case

LRMC 550 ppmv

LRMC 650 ppmv

Stabilization Scenarios and Implications for India

South-Asia Regional Cooperation: Implications for Stabilization

Stabilization Scenarios and Implications for India

Regional Energy Market Development

Stabilization Scenarios and Implications for India

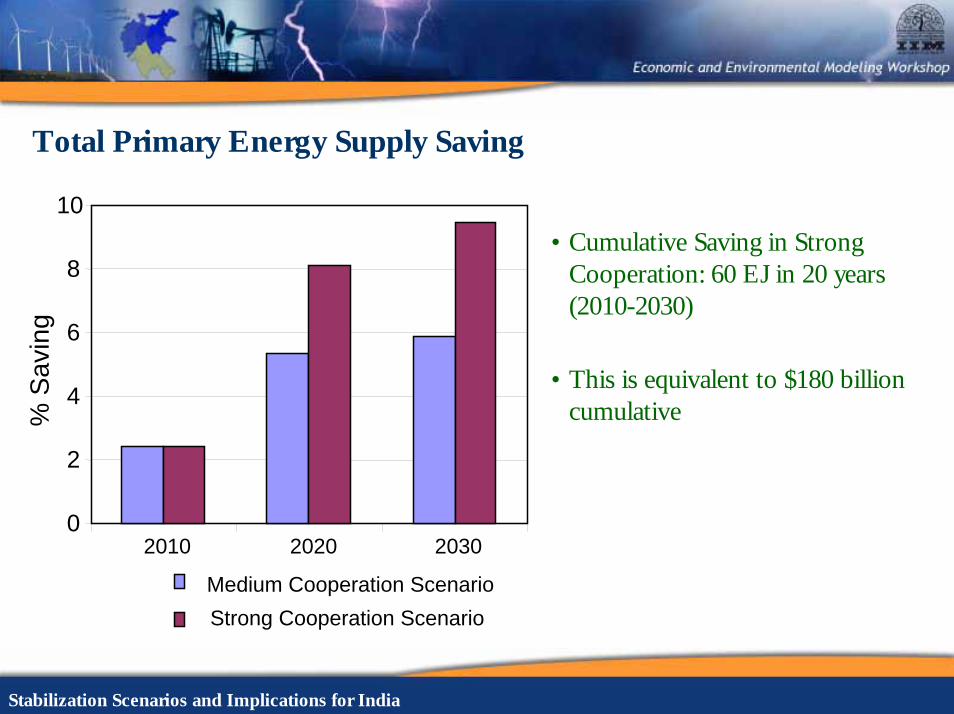

Total Primary Energy Supply Saving

• Cumulative Saving in Strong Cooperation: 60 EJ in 20 years (2010-2030)

• This is equivalent to $180 billion cumulative

0

2

4

6

8

10

2010 2020 2030

% S

avin

g

Medium Cooperation ScenarioStrong Cooperation Scenario

Stabilization Scenarios and Implications for India

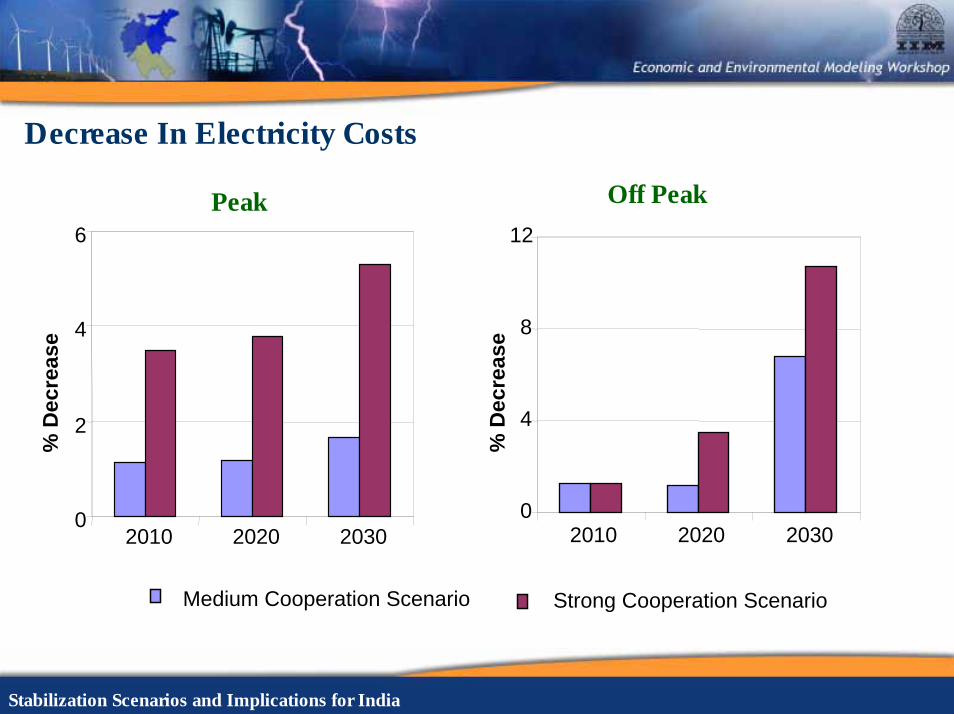

Decrease In Electricity Costs

0

2

4

6

2010 2020 2030

% D

ecre

ase

0

4

8

12

2010 2020 2030

Off PeakPeak

% D

ecre

ase

Medium Cooperation Scenario Strong Cooperation Scenario

Stabilization Scenarios and Implications for India

Benefits from South-Asia Energy Cooperation (2010-2030)

Benefit (Saving)

$ Billion % of Region's GDP

Energy (Direct Benefits)

Energy 60 Exa Joule 180 0.48 Investment in Energy Supply Technologies

72 0.19

Investment in Energy Demand Technologies

69 0.18

Environment (Indirect Benefits) Carbon 1.4 Billion Ton 28 0.08 Sulfur Dioxide (SO2) 50 Million Ton 10 0.03

Total Direct and Indirect Benefits 359 0.98 Spillover Benefits

Water 16 GW additional hydro capacity Flood Control From additional dams Competitiveness Reduced unit energy/electricity cost

Stabilization Scenarios and Implications for India

Stabilization and Technological Change

Stabilization Scenarios and Implications for India

Technological Change in India to Stabilize CO2 at 550 ppmv

0

500

1000

1500

2000

2500

1990 2005 2020 2035 2050 2065 2080 2095

Carbon CaptureEnergy EfficiencyW indSolarBiomassHydroNuclearGasOilIndia 550 ppmv emission

Reference Case Emissions

400

800

1200

2000

1600

550 PPMV

Stabilization Scenarios and Implications for India

Stabilization: Policy Issues and Concerns

• UNFCCC Article 2 definition (Balancing costs and benefits)

• Emissions Rights Regime

• Indigenous Coal

• Competitiveness

• Structural changes in the economy (autonomous and policy driven)

• Implications for Developmental Goals

Stabilization Scenarios and Implications for India

Stabilization: Policy Actions

• Technology Portfolio

• “Fair” Allocation of Emissions Rights

• Linking Development and Climate Change

• Obtaining Multiple Dividends (Designing Pathways)