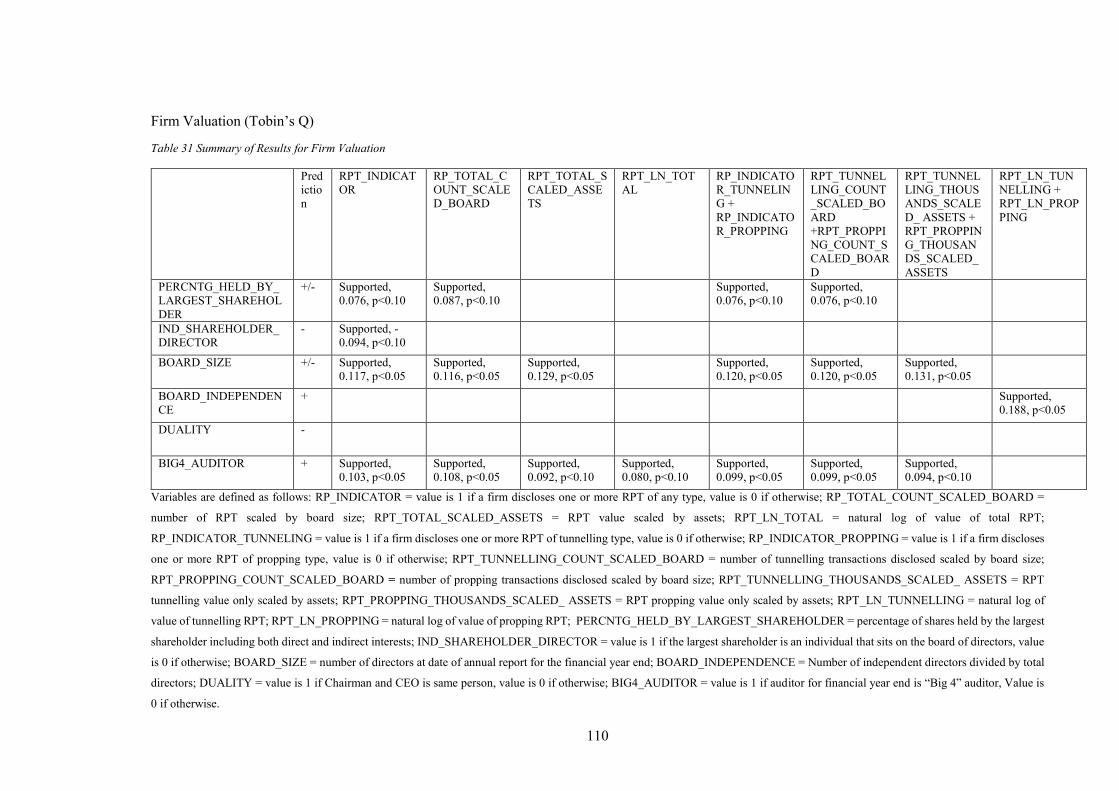

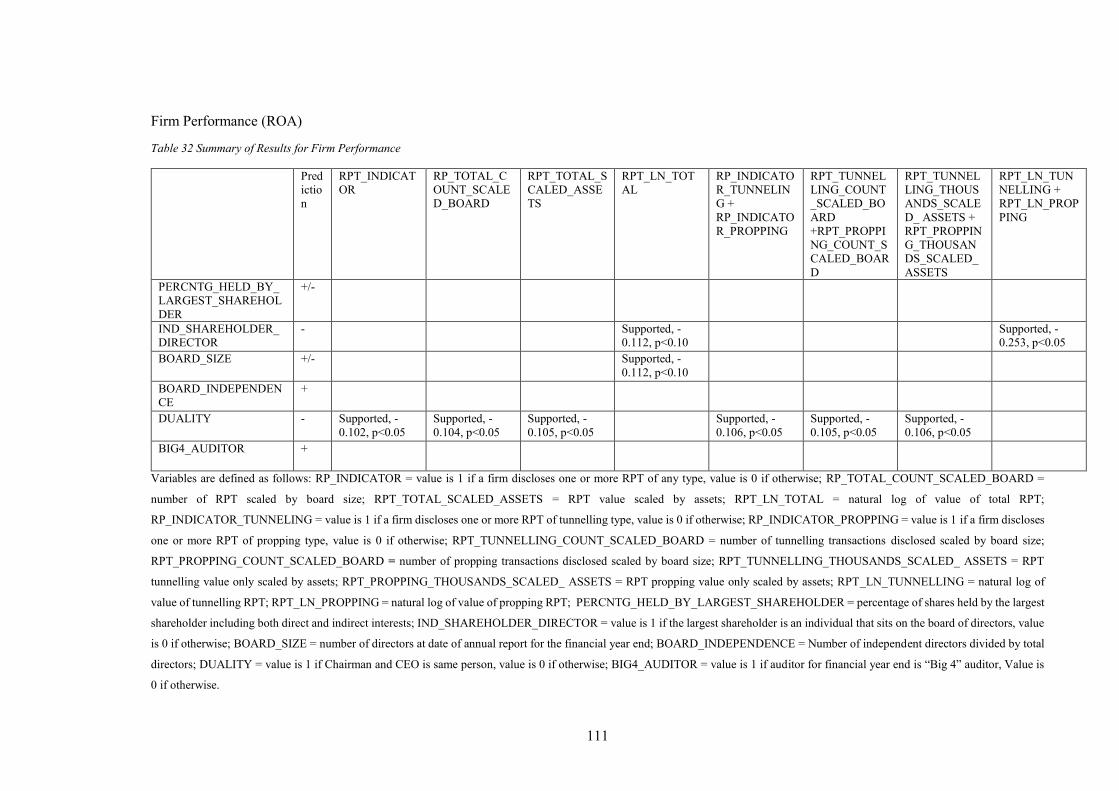

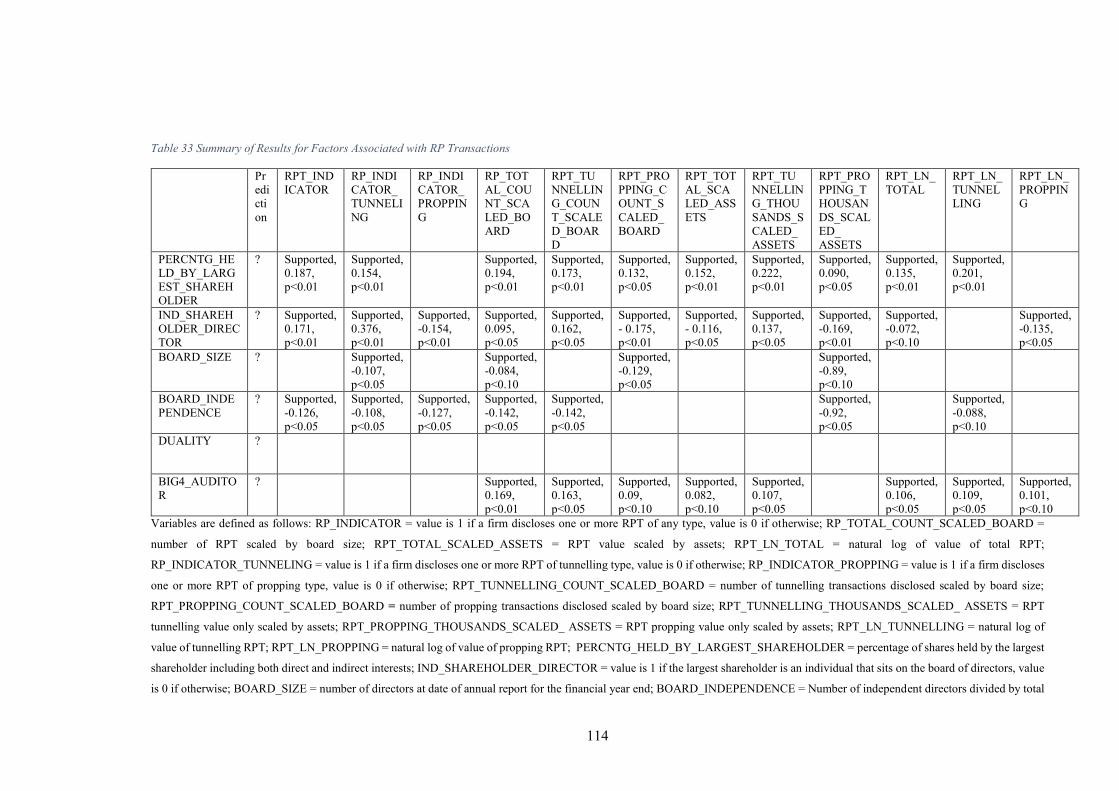

The Impact of Related Party Transactions on Performance and Valuation of Malaysian Listed Firms: Testing the Influence of

Corporate Governance

Victor Gan

A Thesis Submitted for the Degree of

Master of Commerce

Faculty of Business and Design

Swinburne University of Technology

April 2017

ii

Abstract

This study examines the impact of related party (RP) transactions on the performance and

valuation of Malaysian listed firms. It also investigates the influence that corporate governance

has on this relationship. This study uses a sample of 187 firms listed in Malaysia over the period

of 2012 to 2014 for 531 firm-year observations. This study measures RP transactions using

magnitude, number of transactions, and ratios. RP transactions are further broken down into

tunnelling and propping type transactions for further testing. Performance and valuation are

proxied by return on assets (ROA) and Tobin’s Q respectively. Corporate governance is measured

by indicators of both internal mechanisms (board of directors) and external mechanisms

(ownership concentration, audit quality).

This study finds empirical evidence that tunnelling RP transactions have a significant negative

association with firm valuation. At the same time, propping RP transactions have a significant

positive impact on firm valuation. This finding suggests that tunnelling RP transactions represent

expropriation of shareholder wealth and are discounted by investors accordingly, whereas

propping RP transactions are efficient transactions that benefit the firm. This finding is robust

after controlling for leverage, firm size, and stock exchange index membership.

Consistent with prior studies, this evidence confirms that investors in Malaysian firms perceive

tunnelling RP transactions negatively as self-dealing resulting. This supports the conflict of

interest view that tunnelling RP transactions are a front for extraction of private benefits from the

firm resulting in a valuation discount. At the same time, evidence is presented in support of RP

transactions as efficient transactions that can benefit firms operating in imperfect markets.

iii

Declaration

This thesis contains no material which has been accepted for the award to me of any other degree

or diploma, except where due reference is made in the text of the thesis. To the best of my

knowledge this thesis contains no material previously published or written by another person

except where due reference is made in the text of the thesis.

Victor Gan

Faculty of Business and Design

Swinburne University of Technology

6 April 2017

iv

Acknowledgment

It has been through the counsel of many that this thesis is complete. I wish to record my thanks

to my supervisors for their guidance and advice, to my parents and sister for their patience and

understanding, and most of all to the LORD God from whom all knowledge and wisdom flows.

v

List of Tables

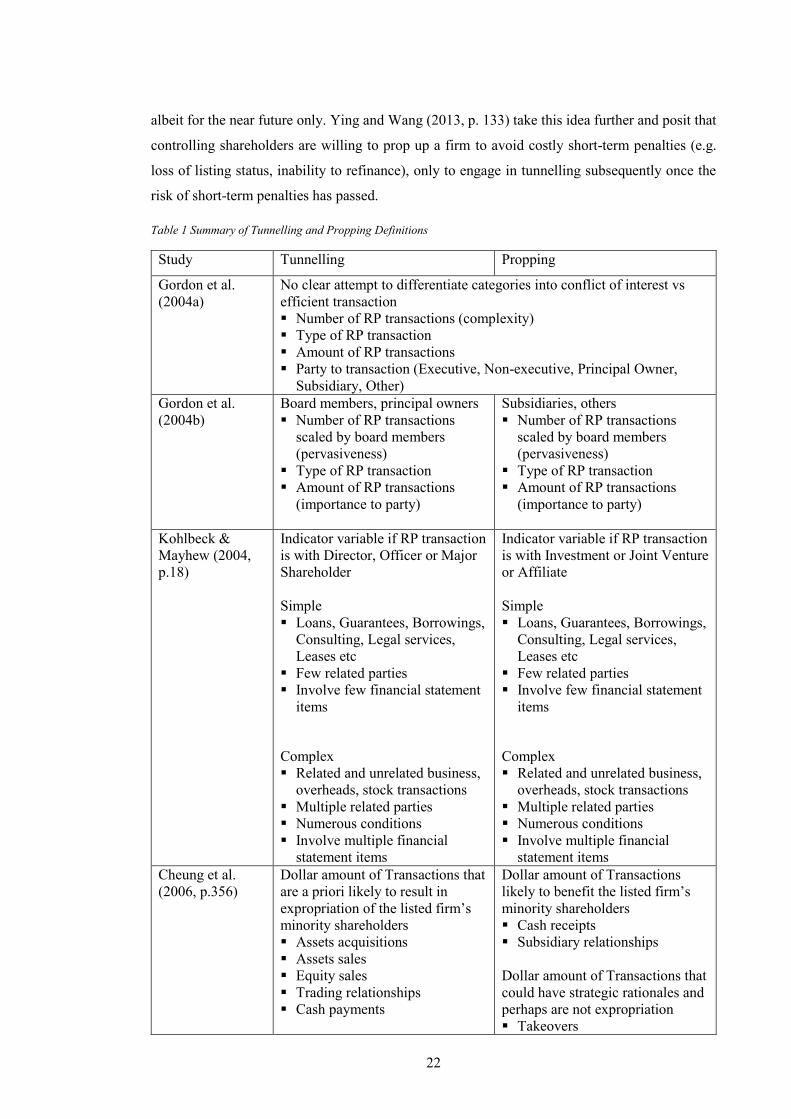

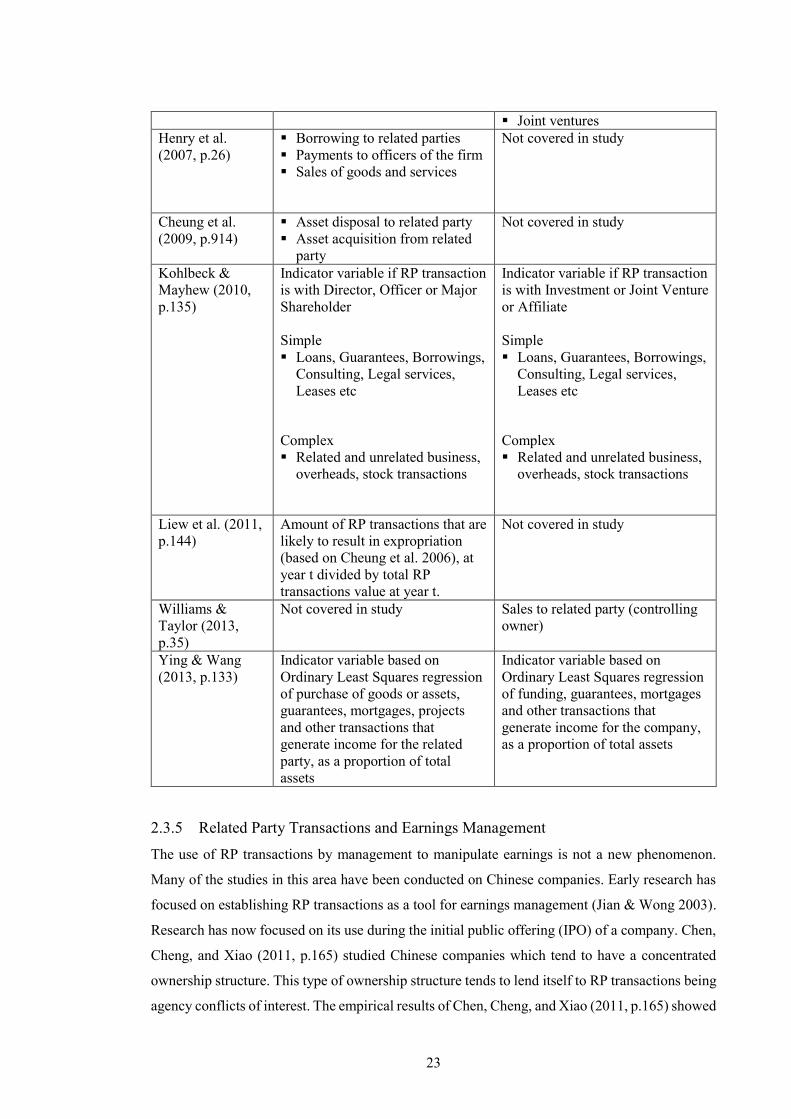

Table 1 Summary of Tunnelling and Propping Definitions ........................................................ 22

Table 2 Malaysian Corporate Governance Research .................................................................. 38

Table 3 RP Transactions and Risks to Firm Valuation ............................................................... 44

Table 4 Definitions of Shareholder Identity ............................................................................... 47

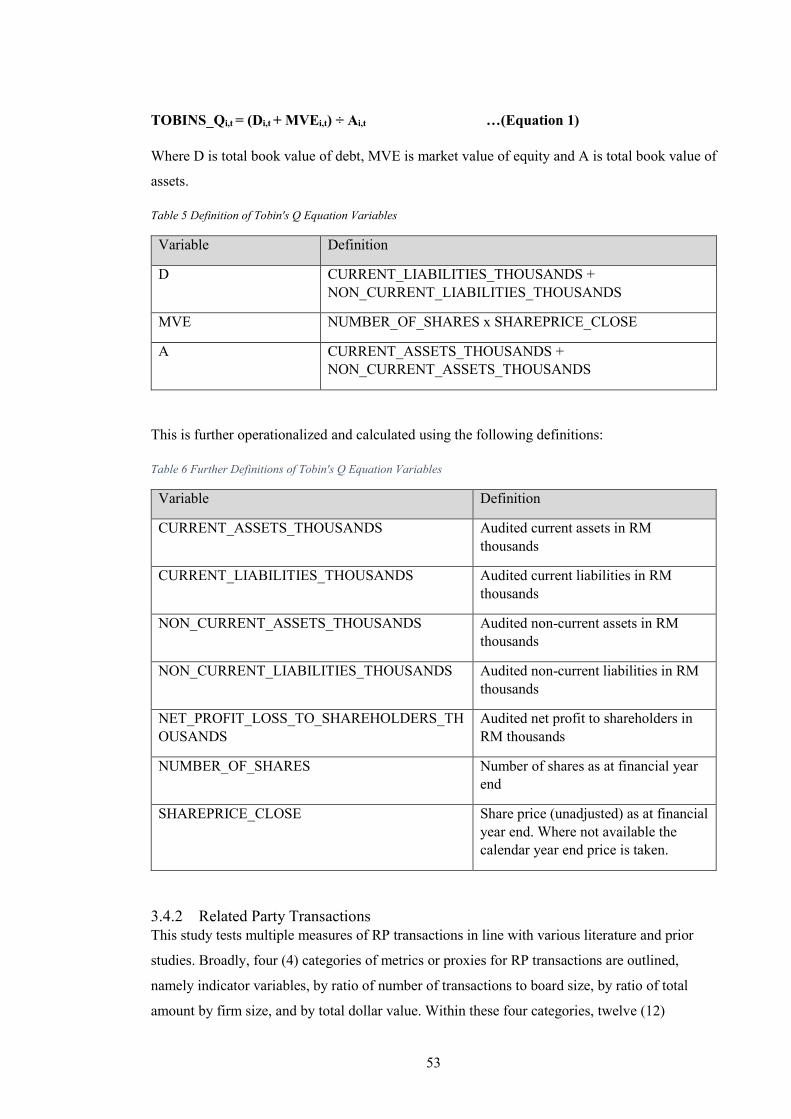

Table 5 Definition of Tobin's Q Equation Variables .................................................................. 53

Table 6 Further Definitions of Tobin's Q Equation Variables .................................................... 53

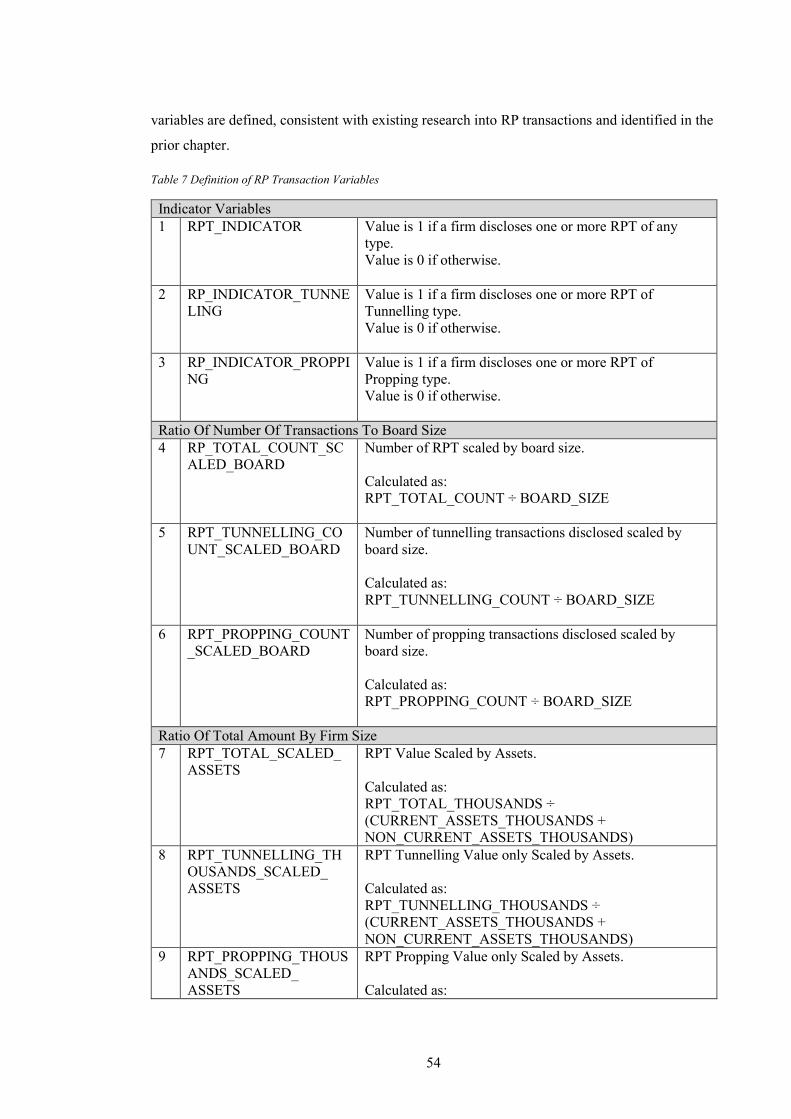

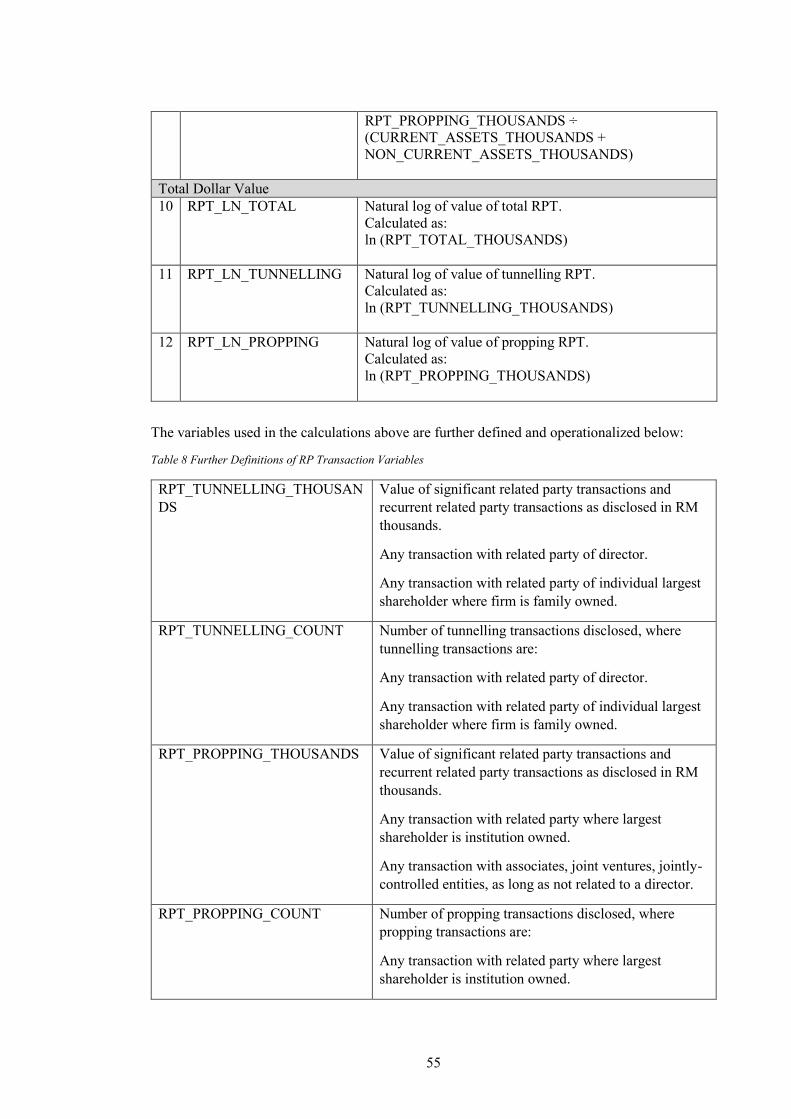

Table 7 Definition of RP Transaction Variables ......................................................................... 54

Table 8 Further Definitions of RP Transaction Variables .......................................................... 55

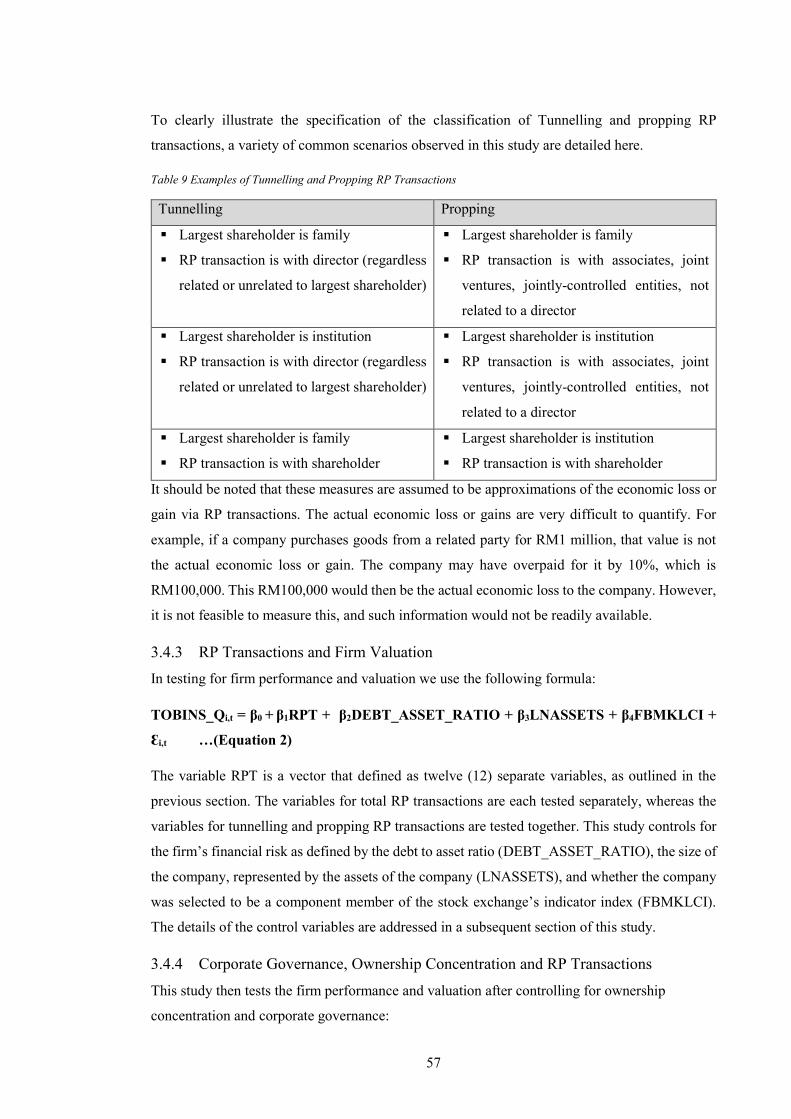

Table 9 Examples of Tunnelling and Propping RP Transactions ............................................... 57

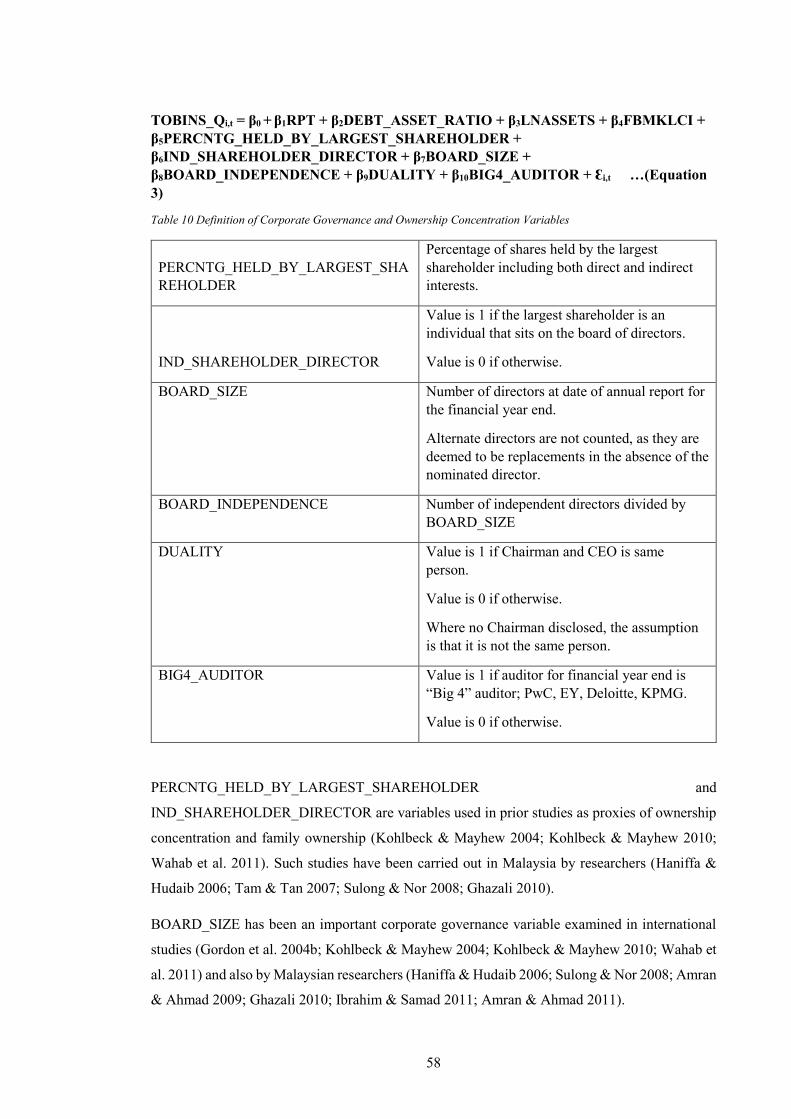

Table 10 Definition of Corporate Governance and Ownership Concentration Variables .......... 58

Table 11 Definition of Return on Assets .................................................................................... 59

Table 12 Defintion of Control Variables .................................................................................... 60

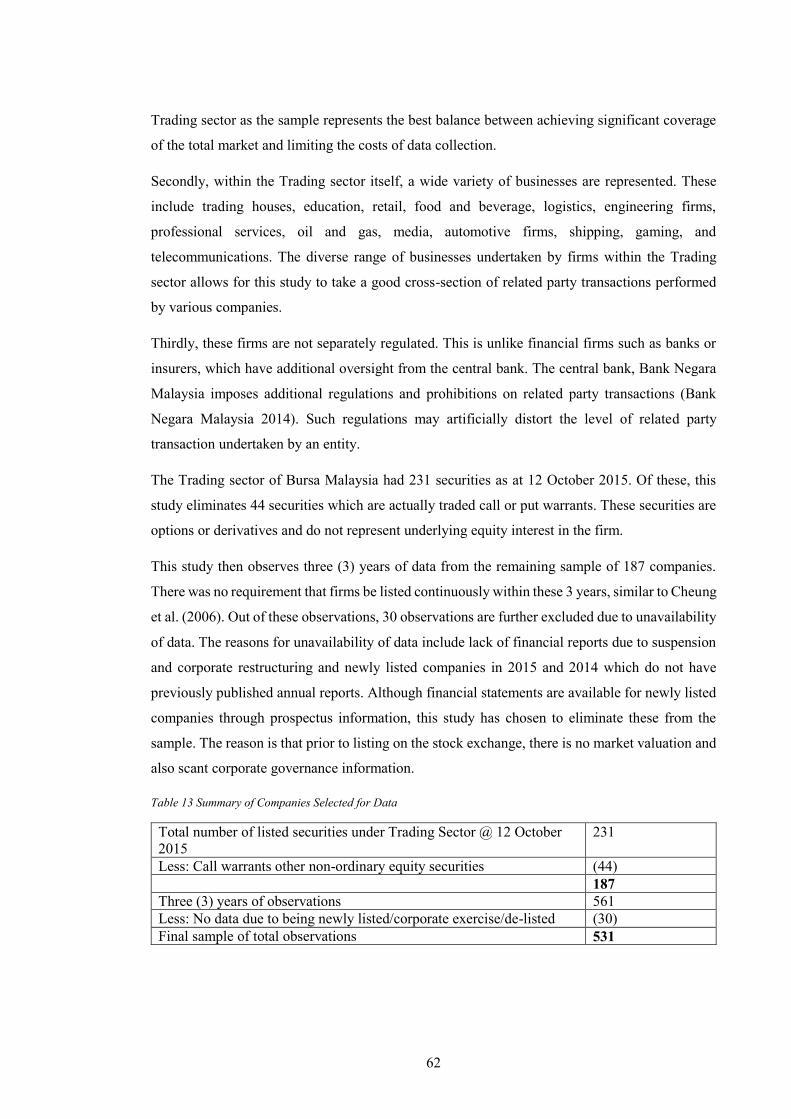

Table 13 Summary of Companies Selected for Data .................................................................. 62

Table 14 Descriptive Statistics for All Variables ........................................................................ 65

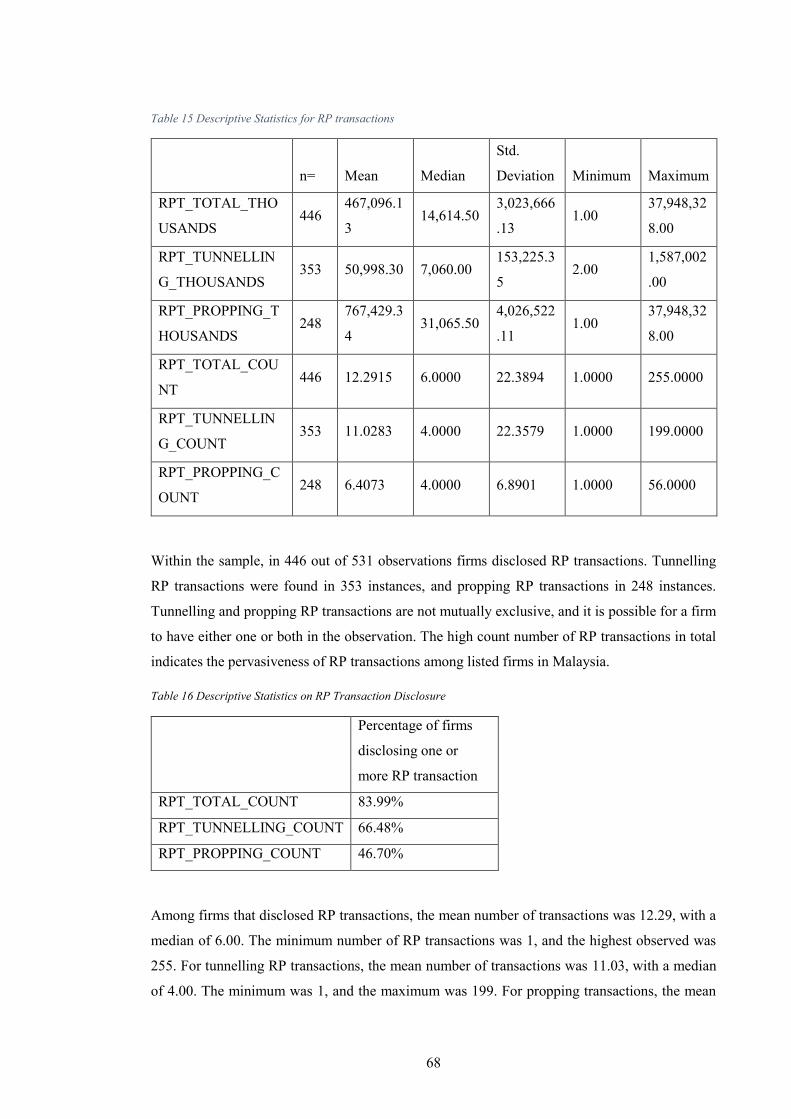

Table 15 Descriptive Statistics for RP transactions .................................................................... 68

Table 16 Descriptive Statistics on RP Transaction Disclosure ................................................... 68

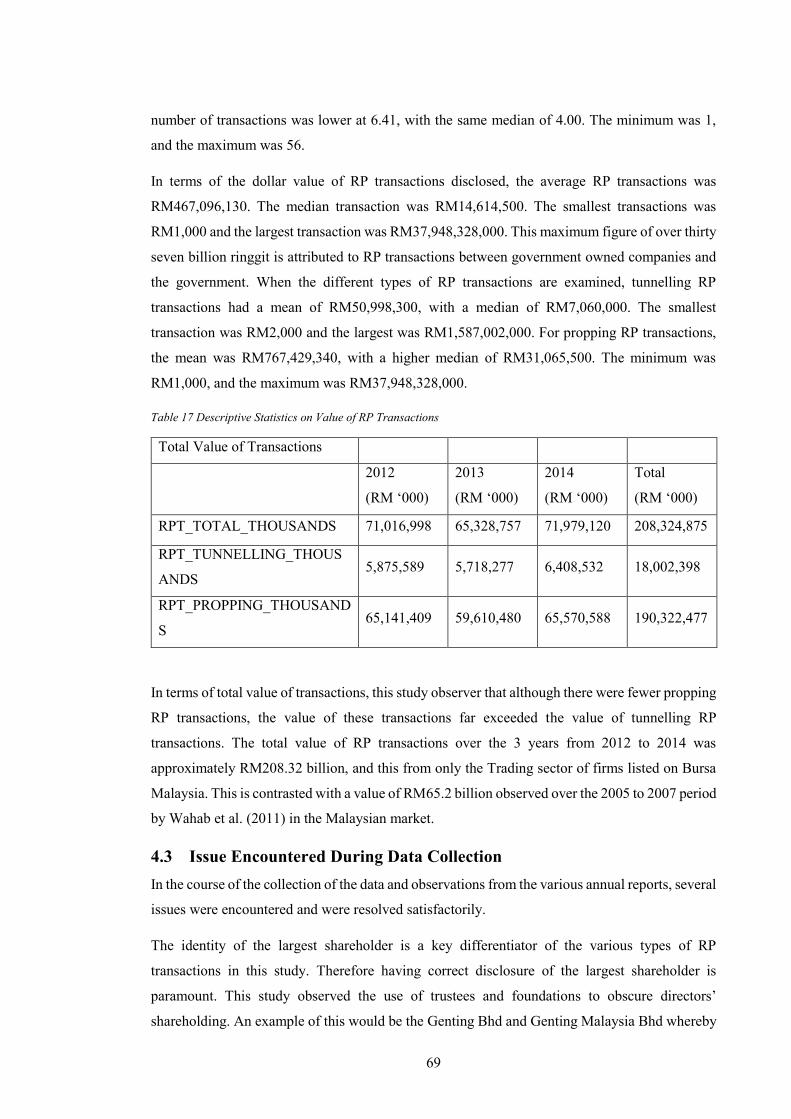

Table 17 Descriptive Statistics on Value of RP Transactions ..................................................... 69

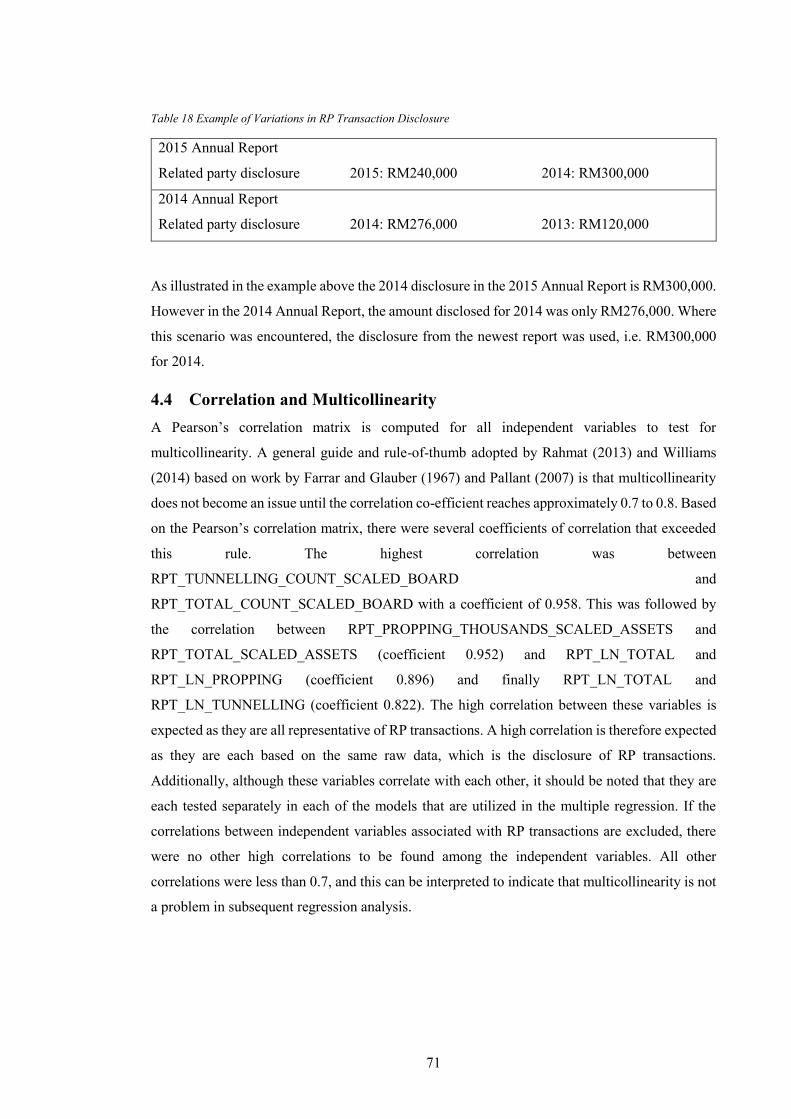

Table 18 Example of Variations in RP Transaction Disclosure ................................................. 71

Table 19 Pearson's Correlation Matrix ....................................................................................... 72

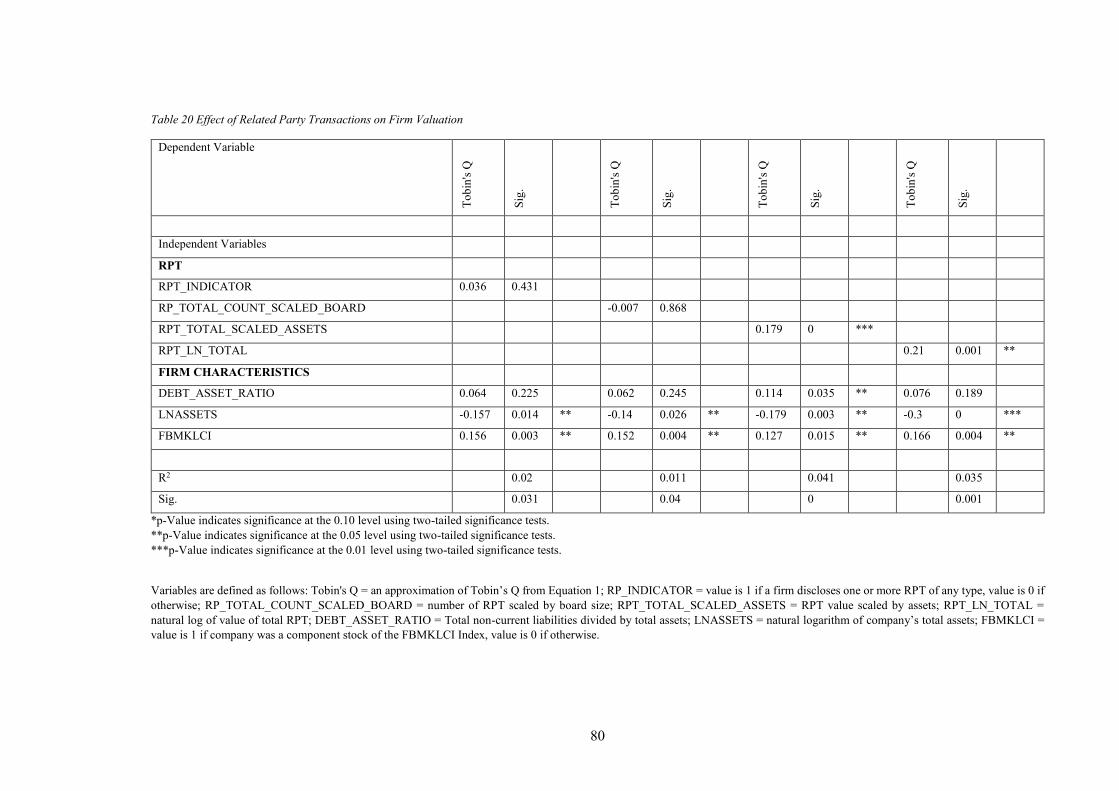

Table 20 Effect of Related Party Transactions on Firm Valuation ............................................. 80

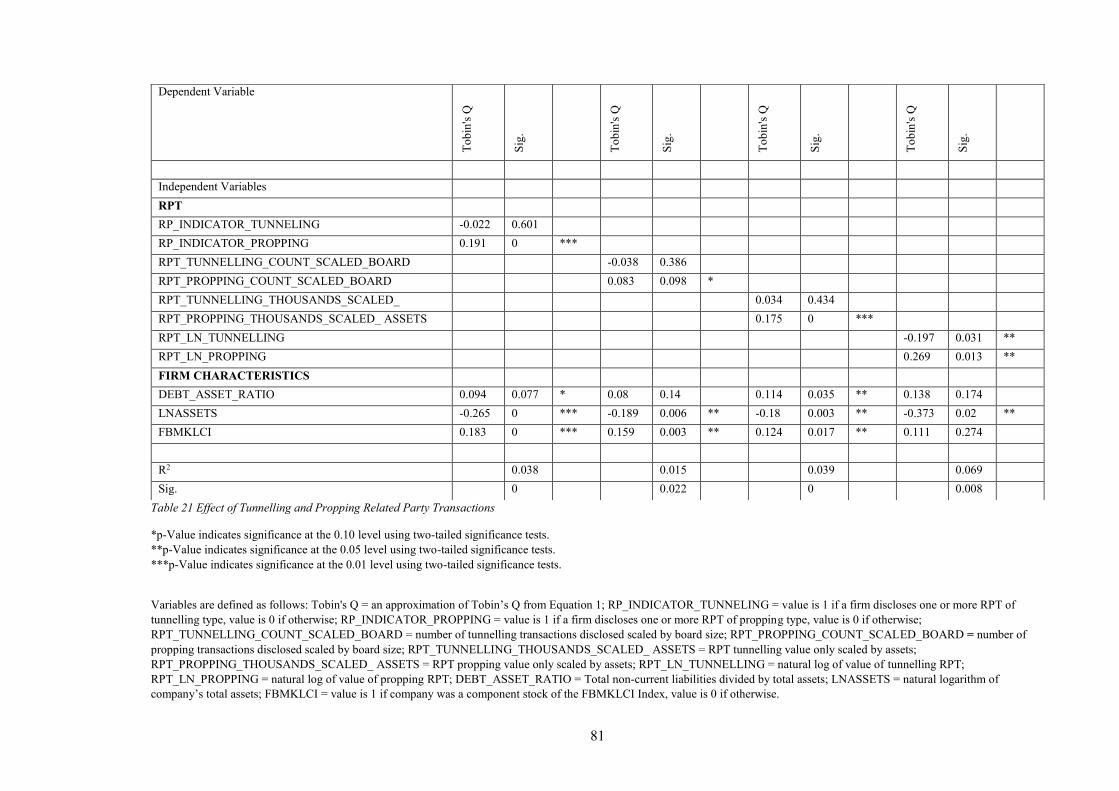

Table 21 Effect of Tunnelling and Propping Related Party Transactions................................... 81

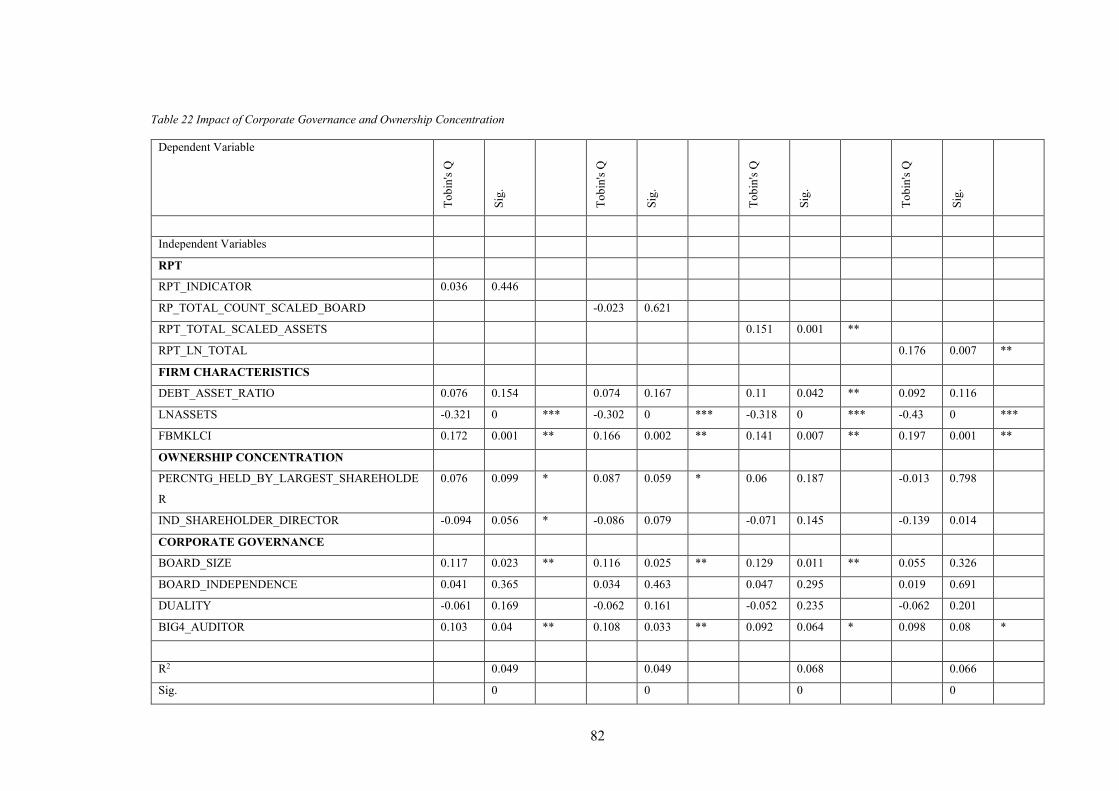

Table 22 Impact of Corporate Governance and Ownership Concentration ................................ 82

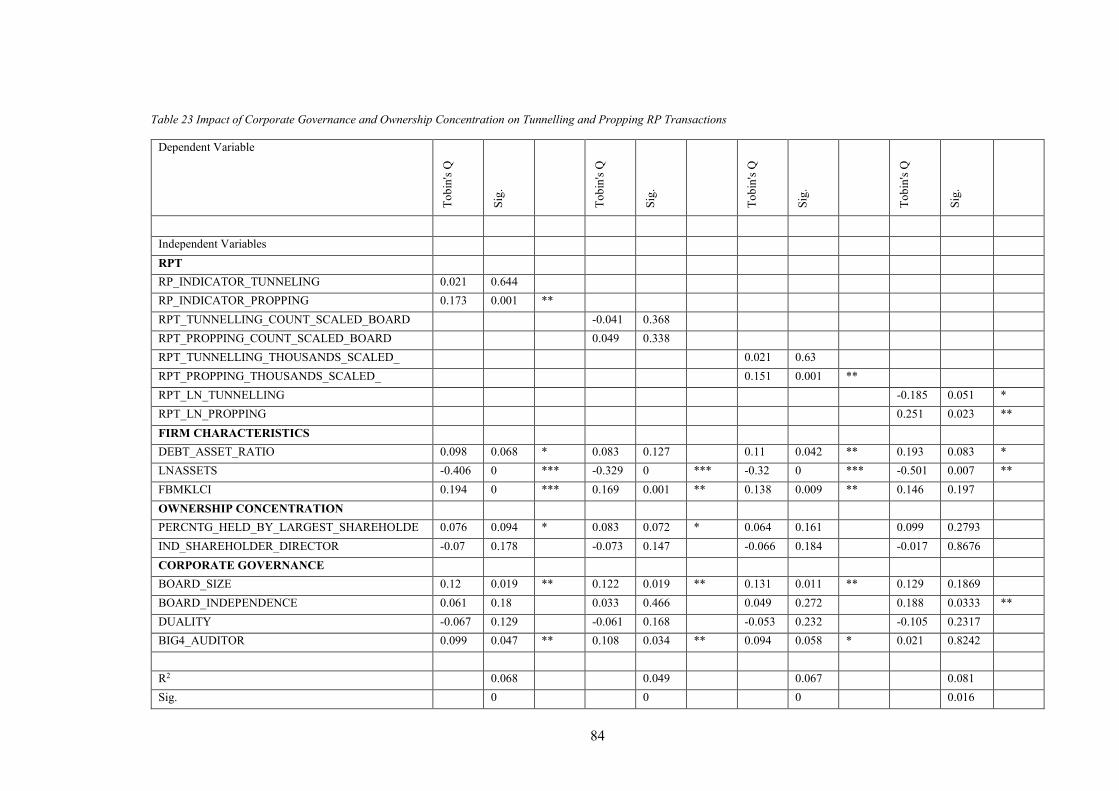

Table 23 Impact of Corporate Governance and Ownership Concentration on Tunnelling and

Propping RP Transactions ........................................................................................................... 84

Table 24 Effect of Related Party Transactions on Firm Performance ........................................ 89

Table 25 Effect of Tunnelling and Propping Related Party Transactions on Firm Performance 90

Table 26 Impact of Ownership Concentration and Corporate Governance ................................ 91

Table 27Impact of Ownership Concentration and Corporate Governance on Tunnelling and

Propping RP Transactions ........................................................................................................... 93

Table 28 Factors Associated with RP Transactions .................................................................... 99

Table 29 Summary of Results for Effect of Related Party Transactions on Firm Valuation and

Performance .............................................................................................................................. 103

Table 30 Summary of Results for Effect of Tunnelling and Propping Related Party Transactions

.................................................................................................................................................. 104

Table 31 Summary of Results for Firm Valuation .................................................................... 110

vi

Table 32 Summary of Results for Firm Performance ............................................................... 111

Table 33 Summary of Results for Factors Associated with RP Transactions ........................... 114

Table 34 Summary of Duality Trend ........................................................................................ 132

vii

Table of Contents 1 Introduction ............................................................................................. 1

1.1 Research Motivations .................................................................................................... 1

1.2 Problem Statement ........................................................................................................ 1

1.3 Research Question ........................................................................................................ 2

1.4 Research Objectives ...................................................................................................... 2

1.5 Significance of Contributions to Topic ......................................................................... 3

1.6 Assumptions and Limitations........................................................................................ 3

1.7 Structure of the Thesis .................................................................................................. 4

1.8 Summary ....................................................................................................................... 5

2 Literature Review ................................................................................... 6

2.1 Introduction ................................................................................................................... 6

2.2 The Role of Corporate Governance .............................................................................. 6

2.2.1 Introduction ........................................................................................................... 6

2.2.2 Development of Corporate Governance................................................................ 7

2.2.3 Related Party Transactions and Corporate Governance ........................................ 8

2.2.4 Internal and External Mechanisms of Corporate Governance .............................. 9

2.3 Related Party Transactions and Theoretical Framework ............................................ 13

2.3.1 RP Transactions: Efficient Transactions or Conflict of Interest? ....................... 13

2.3.2 Agency Theory and Conflict of Interest .............................................................. 13

2.3.3 Transaction Cost Economics and Efficient Transactions .................................... 17

2.3.4 RP Transactions as Source of Tunnelling or Propping ....................................... 19

2.3.5 Related Party Transactions and Earnings Management ...................................... 23

2.3.6 Factors Associated With Related Party Transactions ......................................... 24

2.4 Regulatory Background and Disclosure of Related Party Transactions ..................... 26

2.4.1 Accounting Standards and Market Listing Rules ................................................ 27

2.4.2 Companies Act 1965 and 2007 Amendment ...................................................... 28

2.4.3 Related Party Transactions and Disclosure ......................................................... 28

2.4.4 The Malaysian Political Economy ...................................................................... 29

2.4.5 Corporate Governance in Malaysia ..................................................................... 31

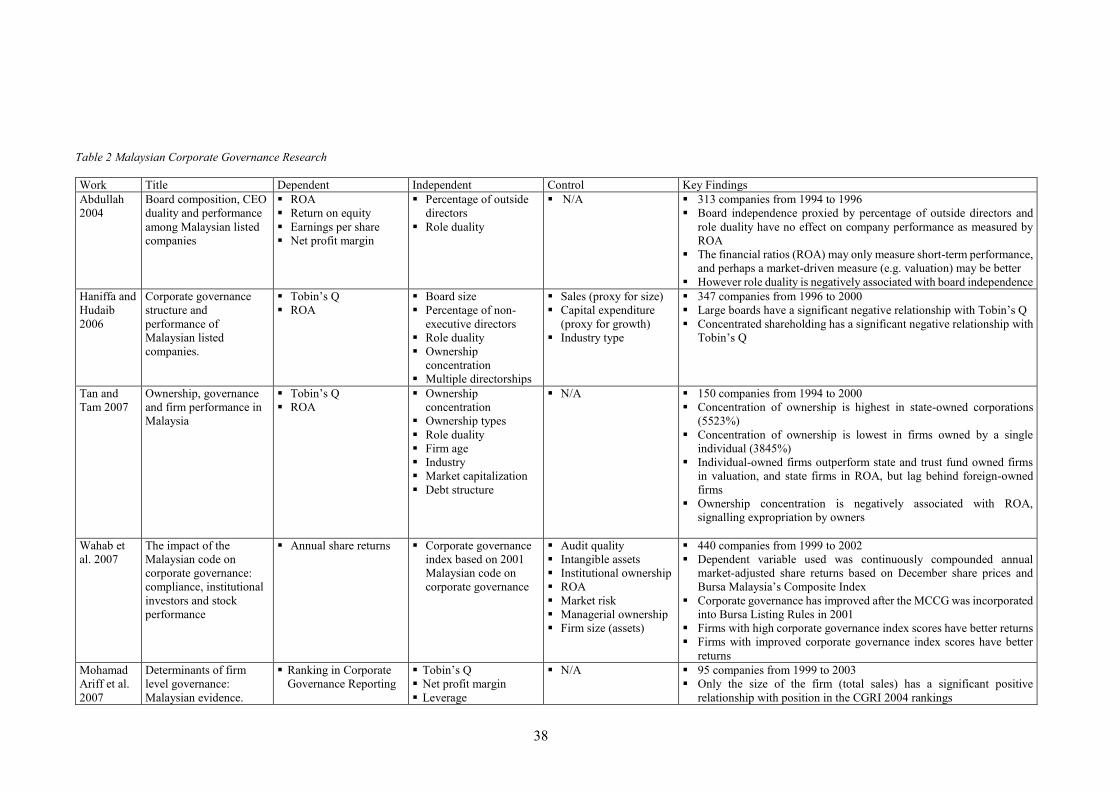

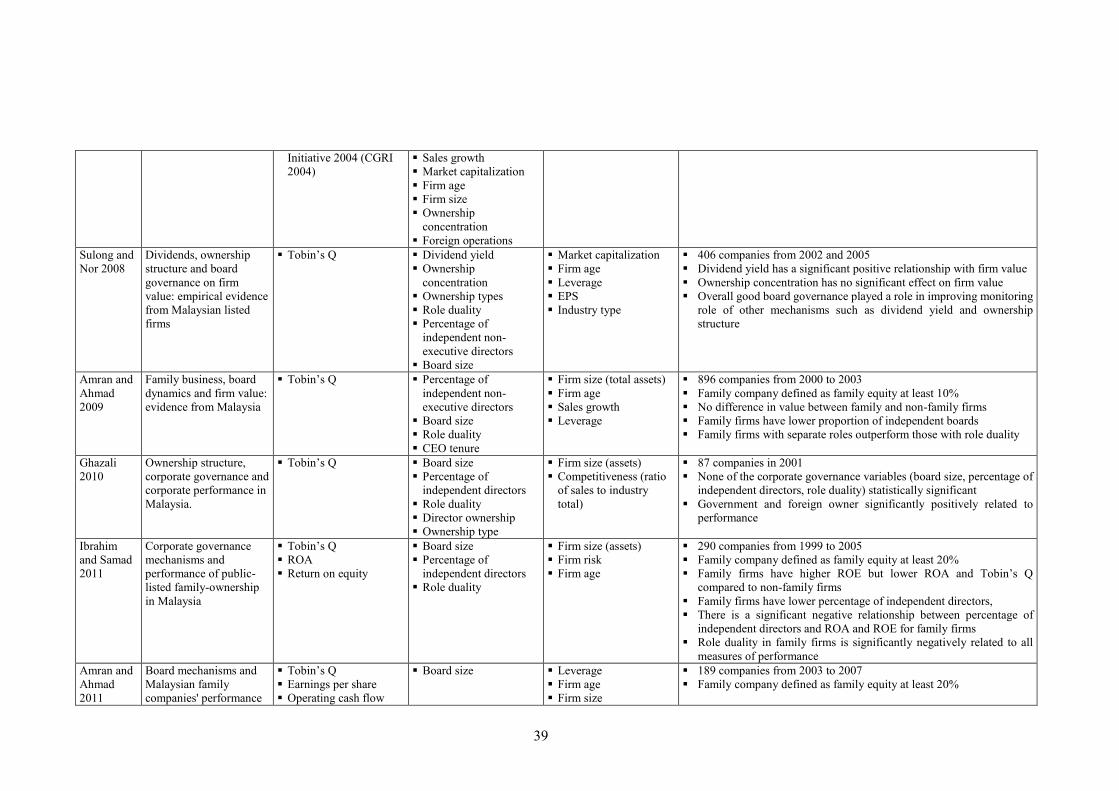

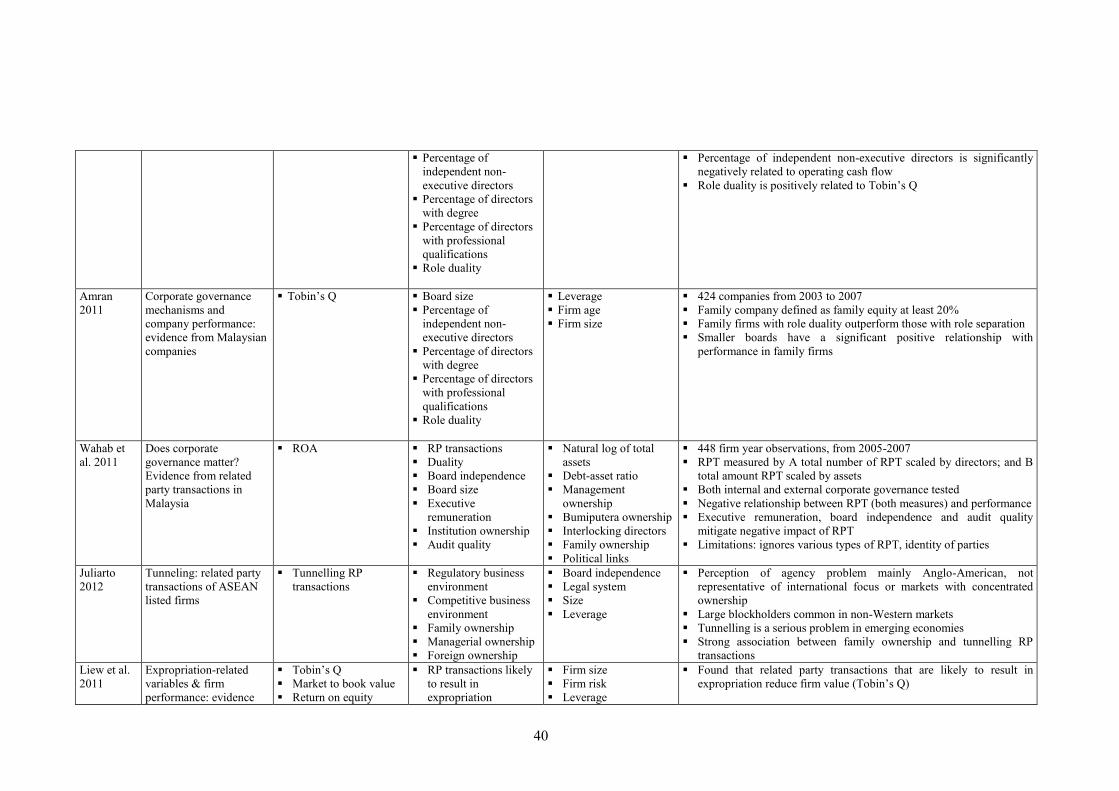

2.5 Review of Existing Empirical Evidence ..................................................................... 32

2.5.1 Review of Studies on Firm Valuation ................................................................. 32

2.5.2 Review of Malaysian Corporate Governance Studies......................................... 33

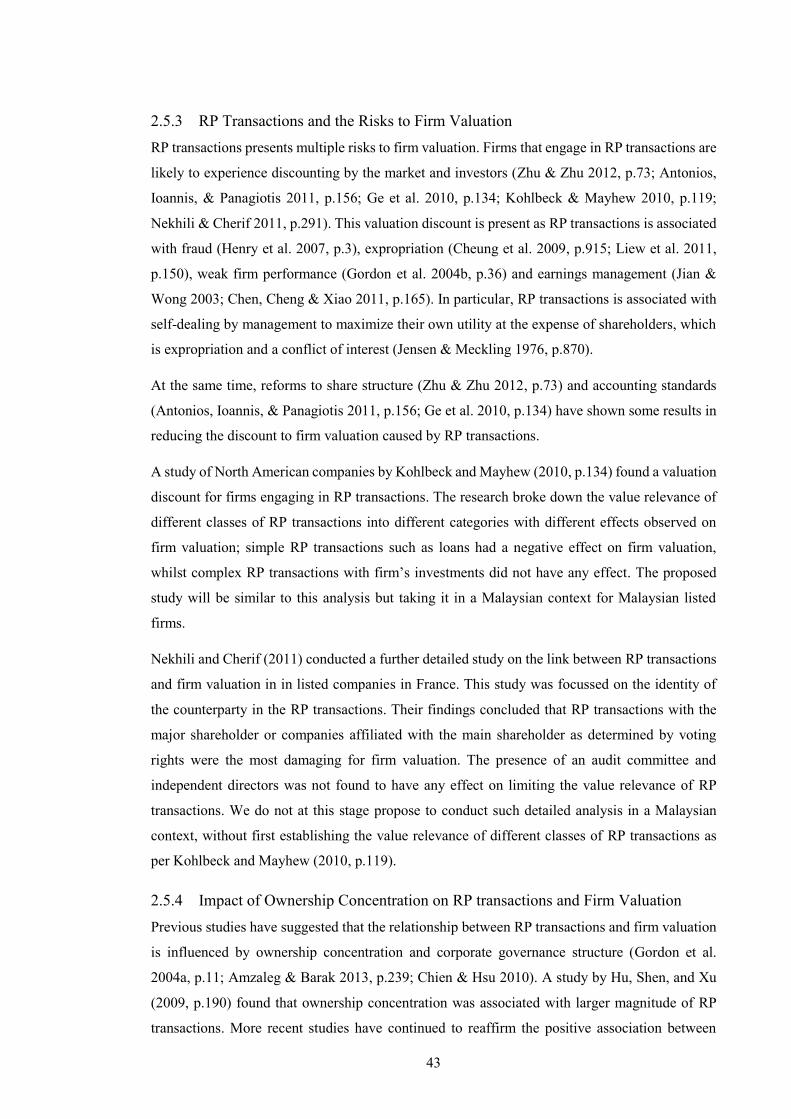

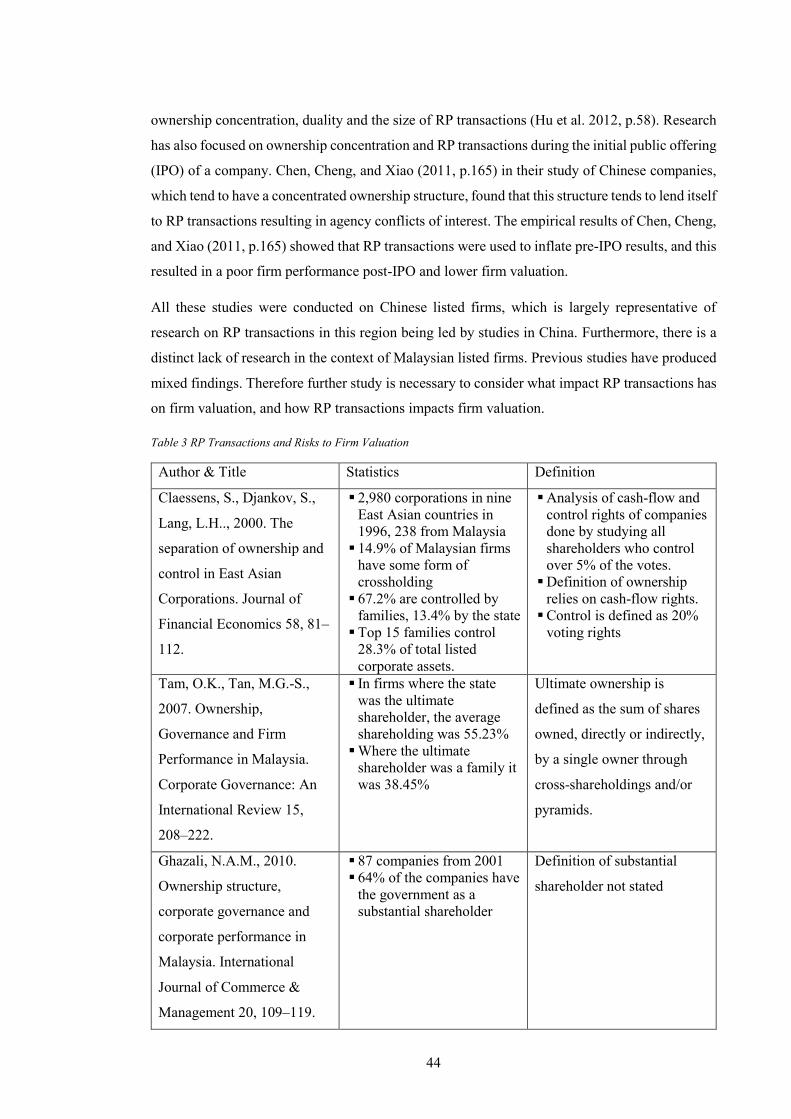

2.5.3 RP Transactions and the Risks to Firm Valuation .............................................. 43

2.5.4 Impact of Ownership Concentration on RP transactions and Firm Valuation .... 43

2.6 Development of Hypotheses ....................................................................................... 45

viii

2.6.1 Related Party Transactions and Association with Firm Performance and Valuation ............................................................................................................................. 45

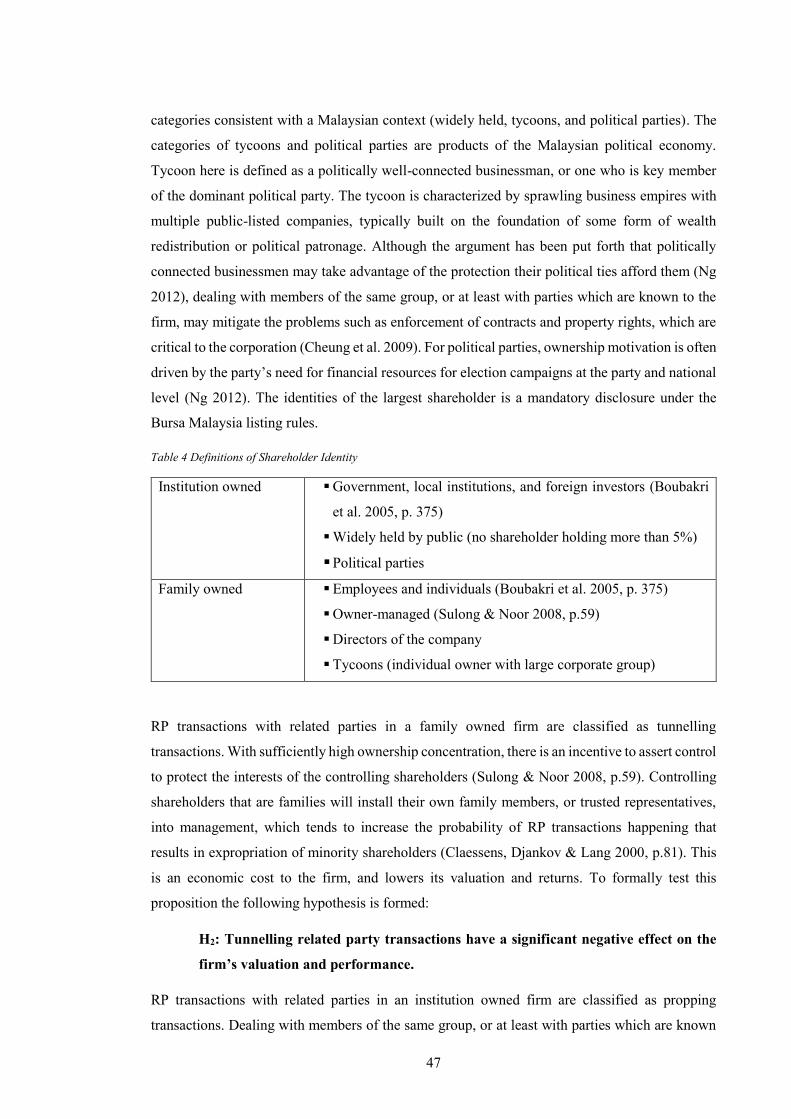

2.6.2 Effects of Different Types of Related Party Transactions .................................. 46

2.6.3 The Impact of Ownership Concentration and Corporate Governance ................ 48

2.6.4 Factors Associated with Related Party Transactions .......................................... 48

2.7 Summary ..................................................................................................................... 49

3 Research Design ................................................................................... 50

3.1 Introduction ................................................................................................................. 50

3.2 Research Philosophy ................................................................................................... 50

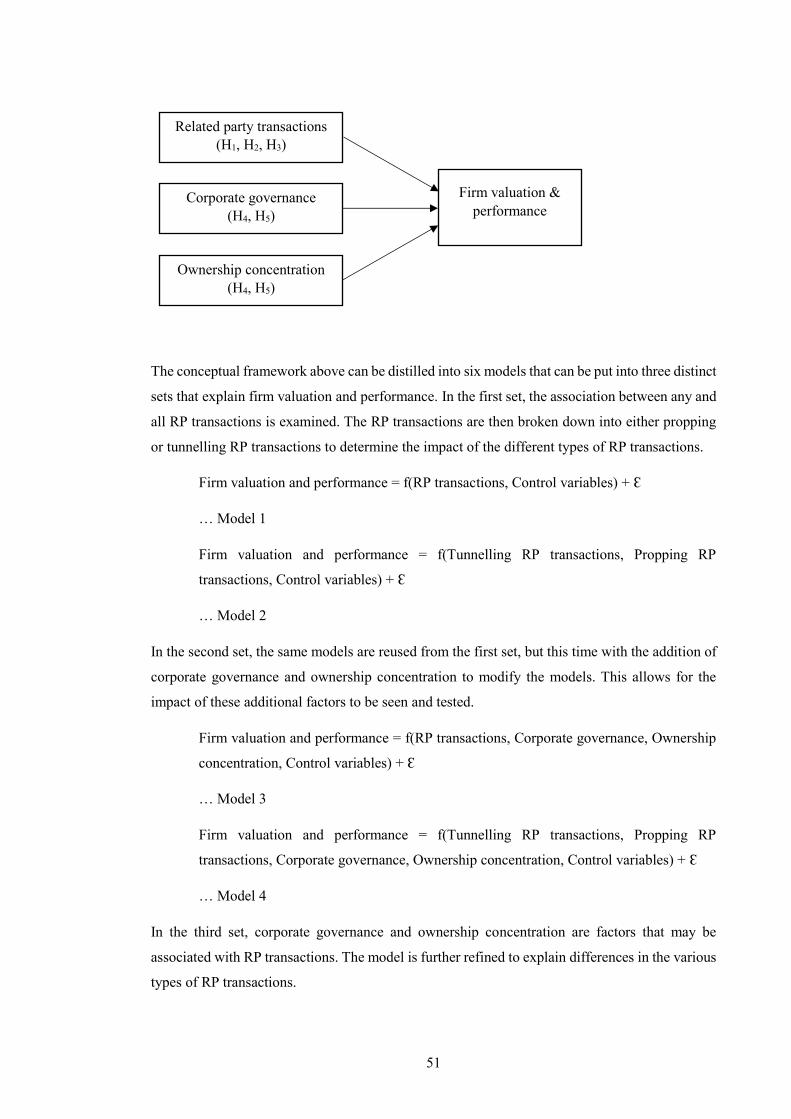

3.3 Theoretical Framework ............................................................................................... 50

3.4 Model Specification and Operationalization of Variables .......................................... 52

3.4.1 Tobin’s Q ............................................................................................................ 52

3.4.2 Related Party Transactions .................................................................................. 53

3.4.3 RP Transactions and Firm Valuation .................................................................. 57

3.4.4 Corporate Governance, Ownership Concentration and RP Transactions ........... 57

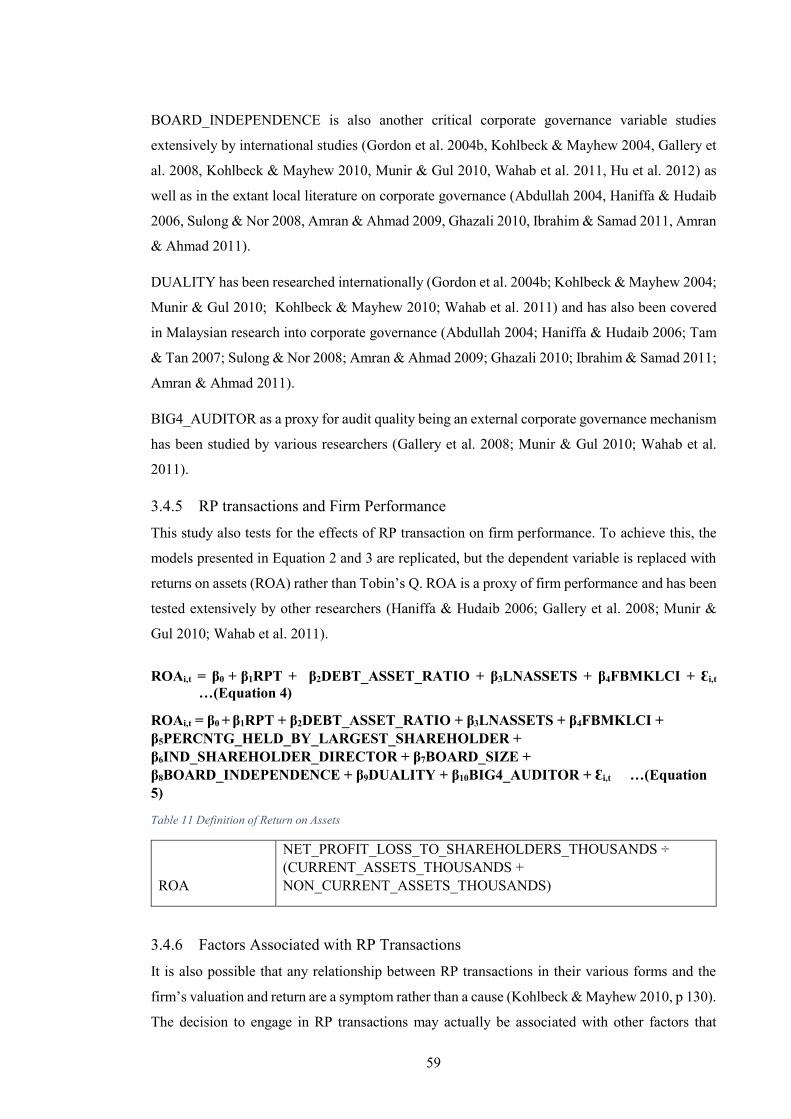

3.4.5 RP transactions and Firm Performance ............................................................... 59

3.4.6 Factors Associated with RP Transactions ........................................................... 59

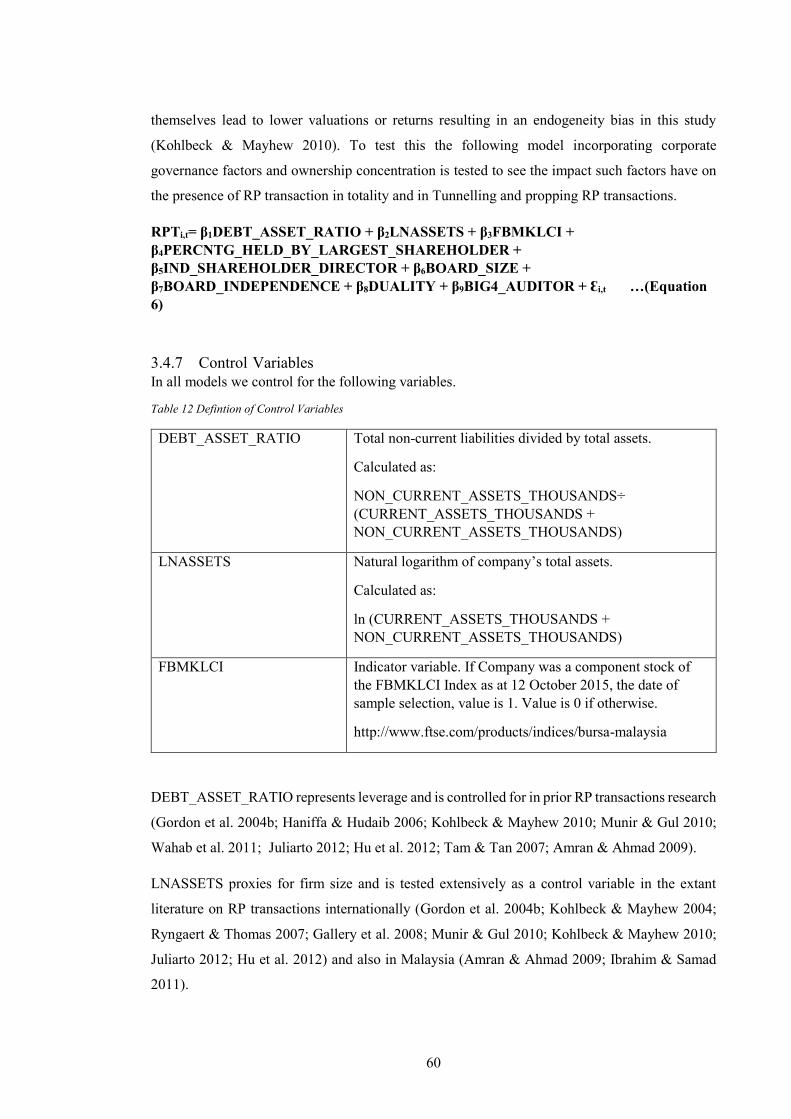

3.4.7 Control Variables ................................................................................................ 60

3.5 Secondary Data and Quantitative Methods ................................................................. 61

3.6 Sample Selection ......................................................................................................... 61

3.7 Data Source ................................................................................................................. 63

3.8 Summary ..................................................................................................................... 64

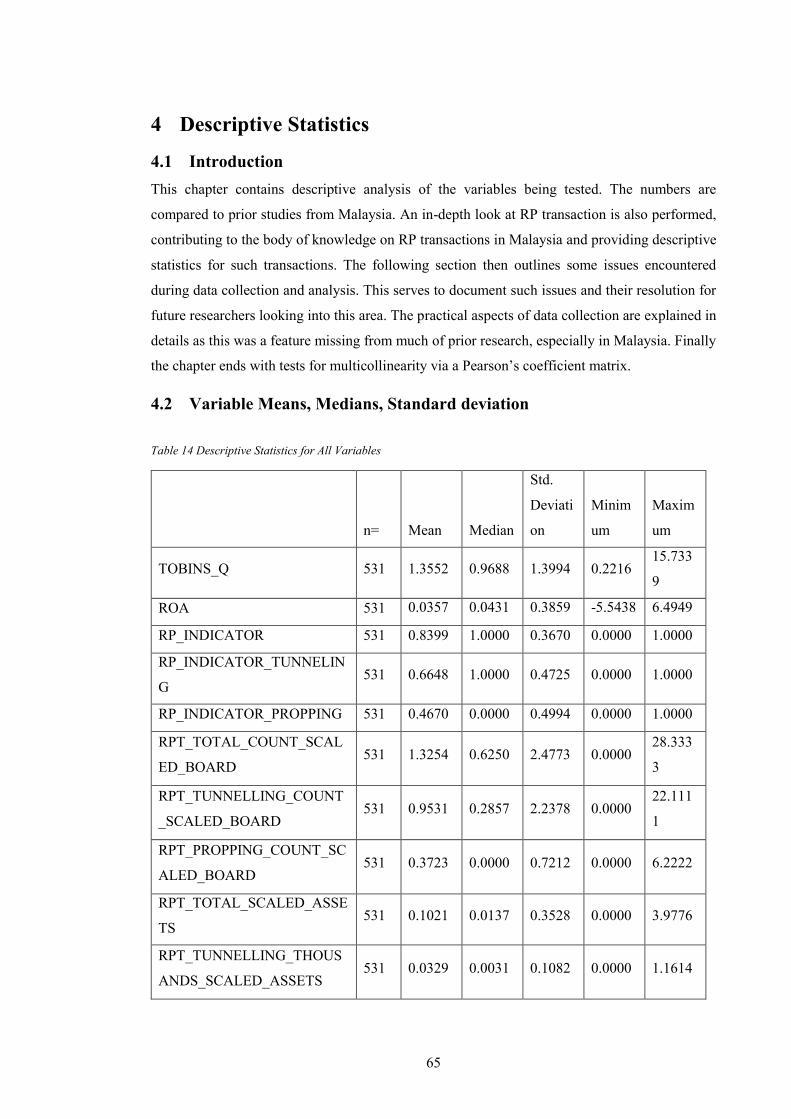

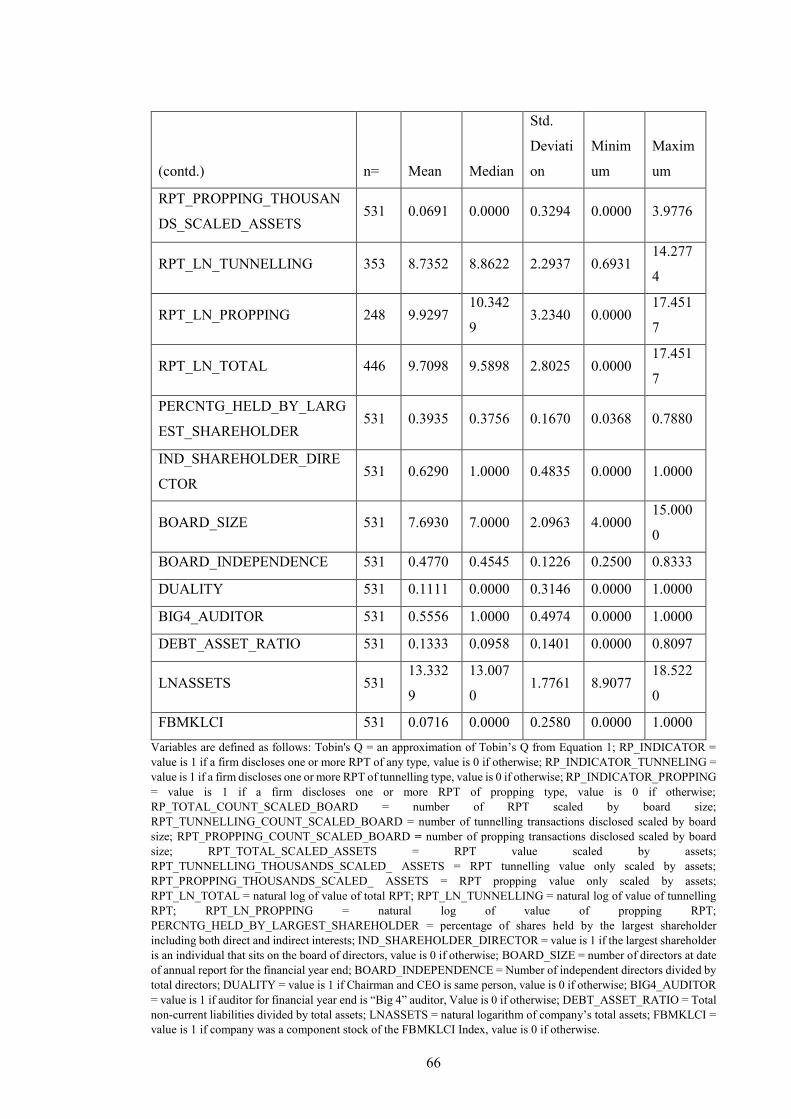

4 Descriptive Statistics ............................................................................ 65

4.1 Introduction ................................................................................................................. 65

4.2 Variable Means, Medians, Standard deviation ........................................................... 65

4.3 Issue Encountered During Data Collection ................................................................. 69

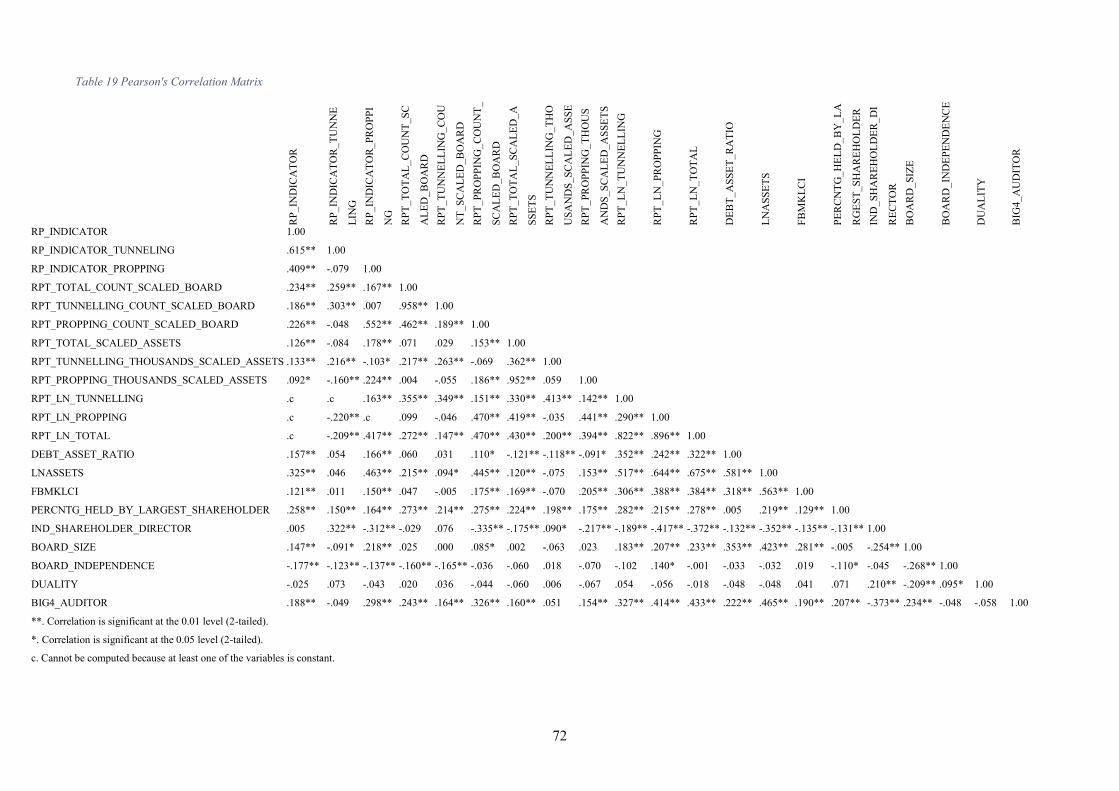

4.4 Correlation and Multicollinearity ................................................................................ 71

5 Empirical Results .................................................................................. 74

5.1 Introduction ................................................................................................................. 74

5.2 RP Transactions and Firm Valuation .......................................................................... 75

5.2.1 Effect of Related Party Transactions on Firm Valuation .................................... 75

5.2.2 Effect of Tunnelling and Propping Related Party Transactions .......................... 76

5.2.3 Impact of Corporate Governance and Ownership Concentration ....................... 77

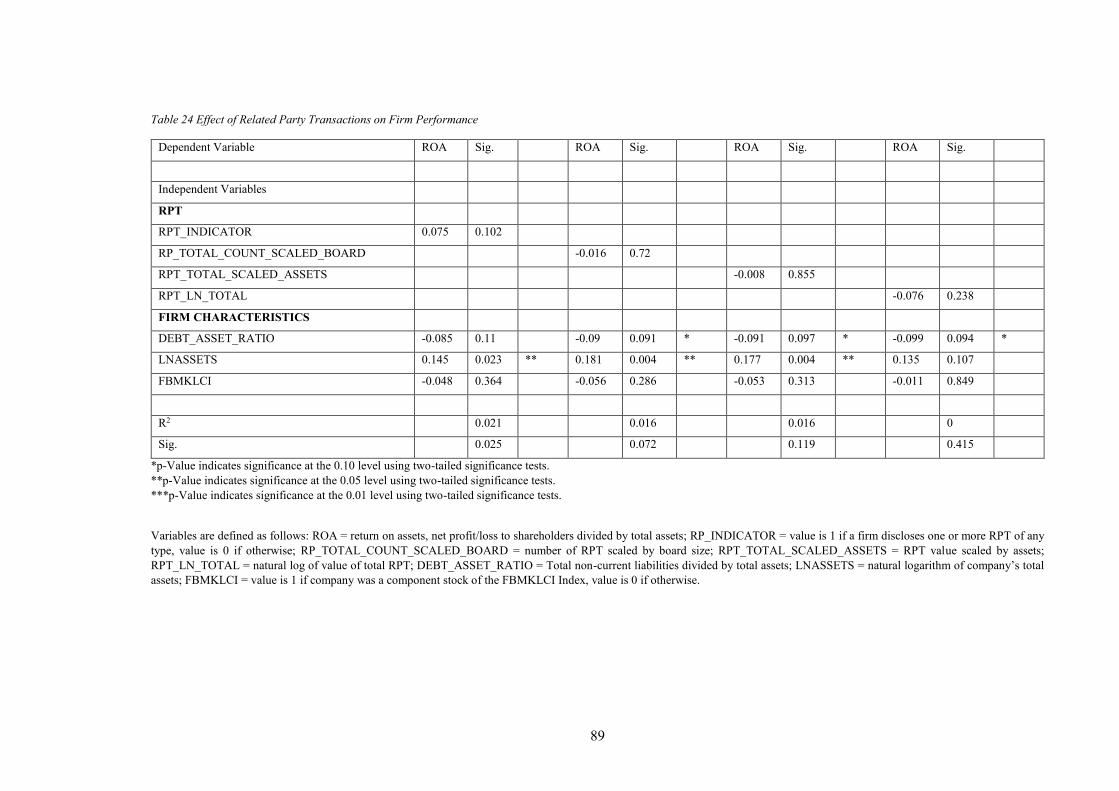

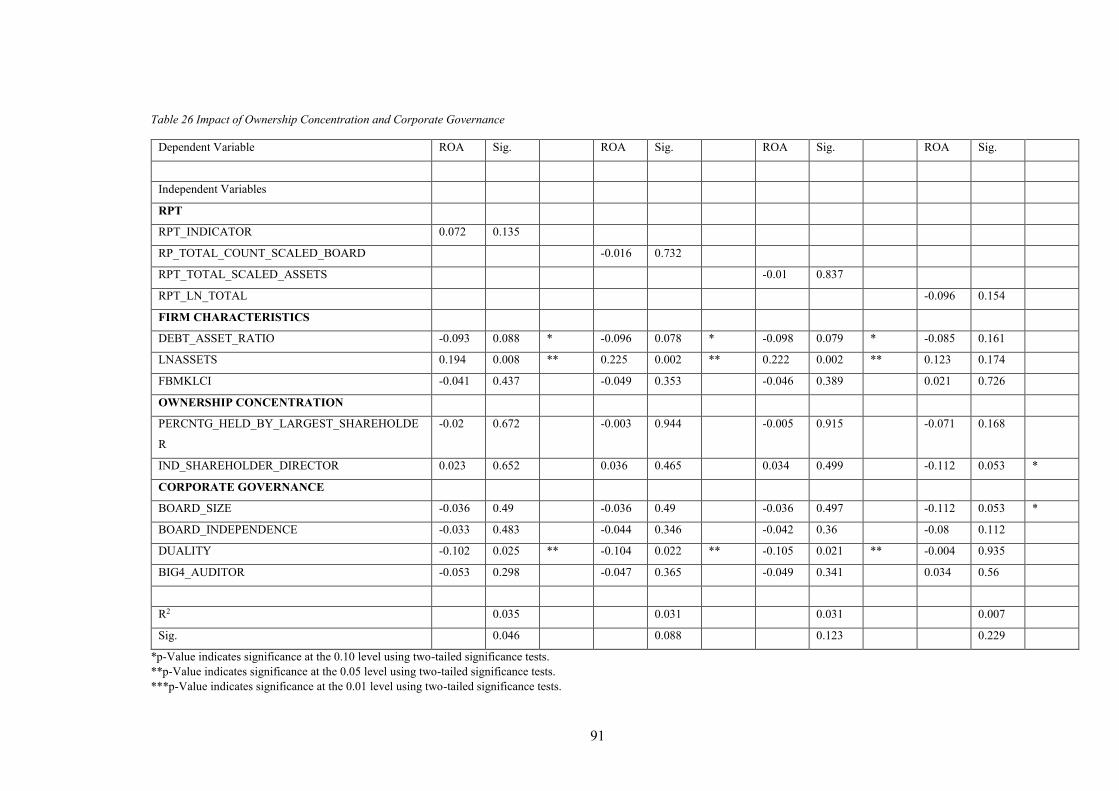

5.3 RP Transactions and Firm Performance ..................................................................... 86

5.3.1 Effect of Related Party Transactions on Firm Performance ............................... 86

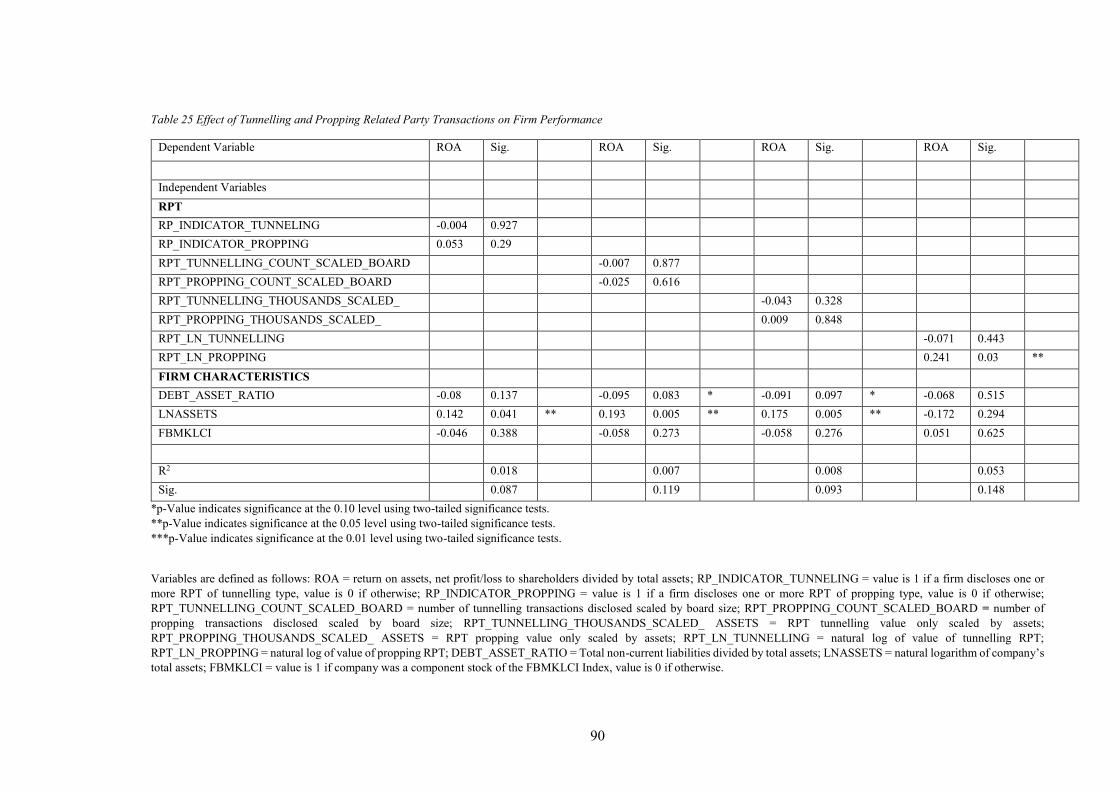

5.3.2 Effect of Tunnelling and Propping Related Party Transactions .......................... 86

5.3.3 Impact of Ownership Concentration and Corporate Governance ....................... 87

ix

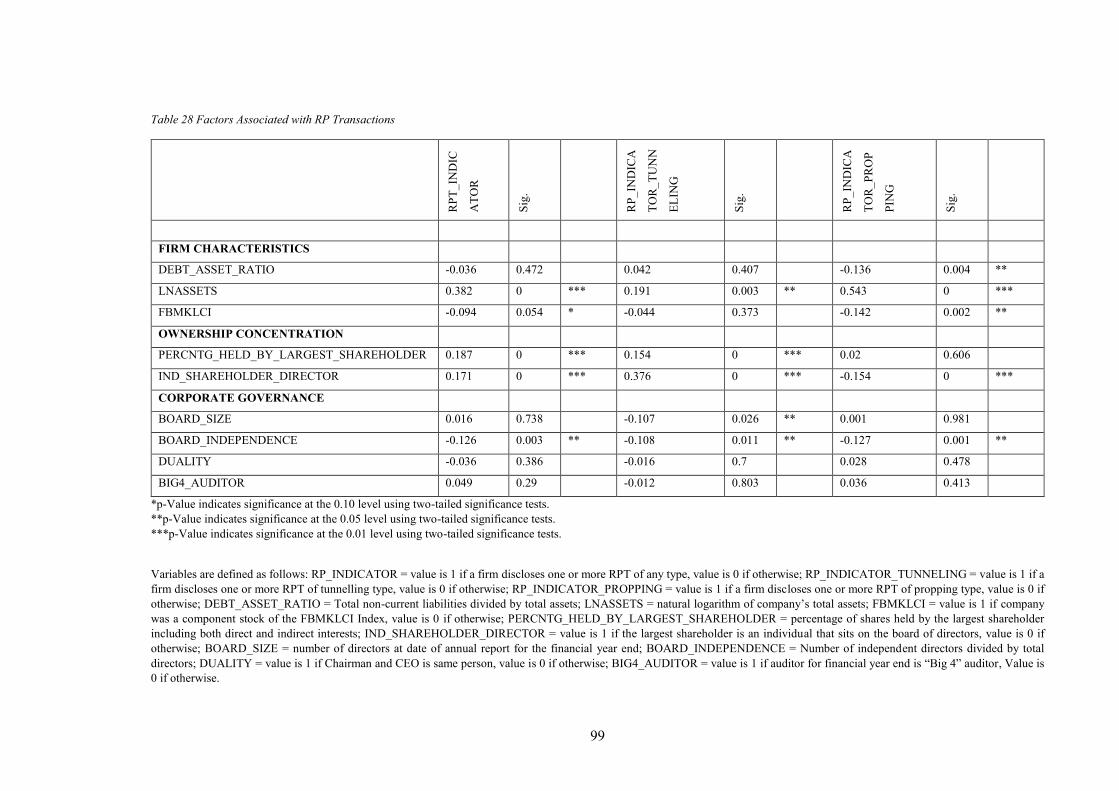

5.4 Factors Associated with RP Transactions ................................................................... 95

5.4.1 RP Indicator Variables ........................................................................................ 95

5.4.2 Ratio of Number of RP Transactions to Board Size ........................................... 96

5.4.3 Ratio to Total Value of RP Transactions to Firm Size ........................................ 97

5.4.4 Total Dollar Value of RP Transactions ............................................................... 98

5.5 Discussion of Results ................................................................................................ 103

5.5.1 Effect of Related Party Transactions on Firm Valuation and Performance ...... 103

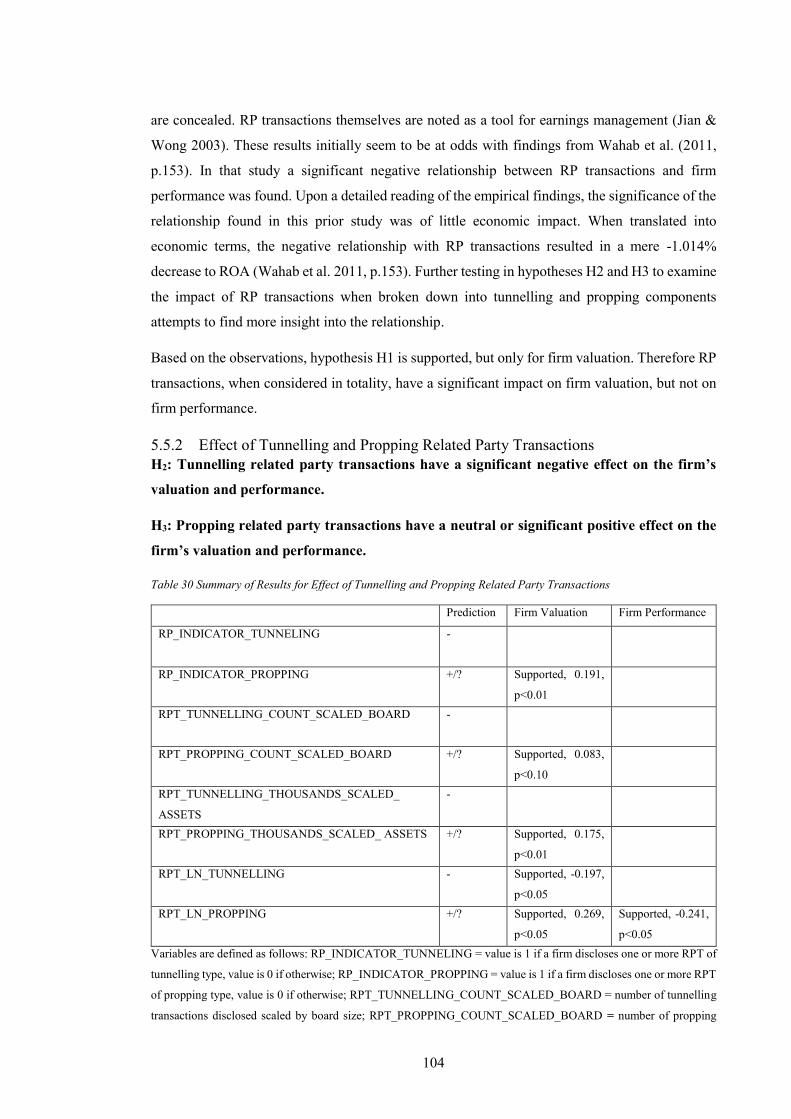

5.5.2 Effect of Tunnelling and Propping Related Party Transactions ........................ 104

5.5.3 Impact of Corporate Governance and Ownership Concentration ..................... 106

5.5.4 Factors Associated with RP Transactions ......................................................... 112

6 Conclusion .......................................................................................... 116

6.1 Summary of Thesis ................................................................................................... 116

6.2 Summary of Results .................................................................................................. 117

6.3 Implications of Study ................................................................................................ 118

6.3.1 Extending Existing Theory ............................................................................... 118

6.3.2 Extending Existing Malaysian Corporate Governance Research ..................... 122

6.3.3 Investors and Public Stakeholders .................................................................... 128

6.3.4 Regulators and Standard-setters ........................................................................ 128

6.4 Limitation of Study ................................................................................................... 130

6.5 Future Research Direction ........................................................................................ 131

6.6 Conclusion ................................................................................................................ 132

7 References ........................................................................................... 133

1

1 Introduction

1.1 Research Motivations Malaysia is a leading capital market in the region. According to the Securities Commission

Malaysia’s annual report, in 2014, the Malaysian capital markets’ size was RM2.76 trillion. Initial

public offerings and other debt instruments raised RM91.9 billion during the year, and Malaysia

also has the largest unit trust industry in Southeast Asia with RM343 billion in assets under

management (Securities Commission Malaysia 2015). In line with the government’s vision to

build a strong capital market and attract investors, there is a need for continual study to understand

how to build a strong regulatory and governance system. At the same time, the close ties between

businesses and politics Malaysia represents a unique institutional and governance setting to be

studied. This is characterized by the involvement of the government and political parties via

policies to redistribute wealth along ethnic lines, which has influenced the development of

business structures and governance in Malaysia (Munir & Gul 2010).

Related party (RP) transactions are a key area of study in corporate governance and related topics

such as accounting disclosure, investor protection and fraud. In one study comprising 448 firms

over the period from 2005 to 2007, there were 4,044 RP transactions valued at RM65.2 billion by

listed companies in Malaysia (Wahab et al. 2011, p.146). Such volumes and magnitude of RP

transactions reflects its acceptance but also highlights the problems it can bring. RP transactions

in Malaysia in the past have been singled out as abusive and as mechanisms for expropriation of

wealth (Wahab et al. 2011, p.132). At the same time, RP transactions may actually have economic

benefits to the firm and its stakeholders. In addition, while regulation, restrictions and guidelines

are being formulated to constrain RP transactions, it must be noted that no country has totally

banned RP transactions (Djankov et al. 2008, p.431).

Within the current literature on RP transactions in other countries, there is no conclusive

knowledge on the nature of the relationship between RP transactions and firm valuation and

performance. There is also a distinct lack of studies on RP transactions in Malaysia. The majority

of studies on RP transactions in this region focus on companies listed in China (Chen et al. 2011;

Chen et al. 2012; Ge et al. 2012; Hu & Li 2010; Lo et al. 2010).

1.2 Problem Statement The need for research into RP transactions is important as Malaysia is a rapidly emerging

economy. Each country has its own unique national character, and each corporation has its own

unique background, environment and business objectives. The variances in corporate governance

practice across the world make it almost impossible to define the term (Aguilera & Jackson 2003).

Thus what is desirable from a corporate governance perspective in one scenario may not be so in

2

another (Haniffa & Hudaib 2006, p.1035). Differences in each country’s legal system will afford

varying levels of investor protection (Demirgüç-Kunt & Maksimovic 2002). Corporate

governance or other alternative governance mechanisms such as ownership concentration may

evolve to cope with legal gaps in investor protection (La Porta et al. 1996). Corporate governance

can also develop based on previous governance and ownership structures, in a path dependent

fashion (Bebchuk & Roe 1999; Licht et al. 2001). Malaysia’s policy of ethnic based wealth

redistribution over the last 40 years via the New Economic Policy (NEP) is a key source of path

dependence in determining current governance practices. At the same time, these governance

practices need to be considered within the social context in which they occur, in that they develop

embedded within an existing social context (Gomez-Mejia & Wiseman 2005; Huse 2005).

Although Malaysia is a leader in the region in the development of a comprehensive system of

corporate governance, significant issues still remain in the areas of expropriation of minority

shareholders (Tam & Tan 2007, p.220). Firstly, without a proper understanding of RP transactions

and its impact on firm valuation and performance, it will be difficult to build a framework for

further development of the Malaysian capital market. This could risk the Malaysian capital

markets losing out regionally to more dynamic centres. Secondly, this is an opportunity for

Malaysia to develop even further as a regional capital market of choice with the right regulatory

stance, armed with a better understanding of the impact of RP transactions.

1.3 Research Question The complex interplay between RP transactions, firm valuation and performance, and corporate

governance gives rise to specific research questions in a Malaysian context:

Research Question 1: What is the relationship between RP transactions and firm valuation and

performance of Malaysian listed firms?

Research Question 2: What is the relationship between RP transactions, corporate governance and

ownership concentration on firm valuation and performance?

Research Question 3 What is the relationship between corporate governance and ownership

concentration and RP transactions?

1.4 Research Objectives More specifically, the research objectives of this study can be expressed as follows:

Research Objective 1 (RO1): To determine the effects of RP transactions on firm valuation and

performance of Malaysian listed companies.

Research Objective 2 (RO2): To determine the effects of RP transactions, corporate governance

and ownership concentration on firm valuation and performance.

3

Research Objective 3 (RO3): To determine the association between corporate governance and

ownership concentration on RP transactions.

1.5 Significance of Contributions to Topic Firstly, the majority of studies on RP transactions in this region focus on companies listed in

China (Chen et al 2011; Chen et al. 2012; Ge et al. 2012; Hu & Li 2010; Lo et al. 2010). Although

current research into the area of RP transactions is limited, its effects can be widely felt.

Secondly this study extends the usefulness of agency theory and efficient transactions in

understanding the underlying nature of RP transactions. This investigation into the relationship

between ownership concentration, governance structure and RP transactions can establish

principles and characteristics of a strong governance system. Additionally, corporate governance

and ownership concentration is seen to be a moderating factor in the effect of RP transactions.

The effect of corporate governance to constrain RP transactions has been documented by previous

researchers (Gordon et al. 2004b, p.36; Wahab et al. 2011, p.158), but no prior study has

investigated the effect of ownership concentration on this relationship. This study is also unique

in the use of multiple indicators of RP transactions that have been previously developed by

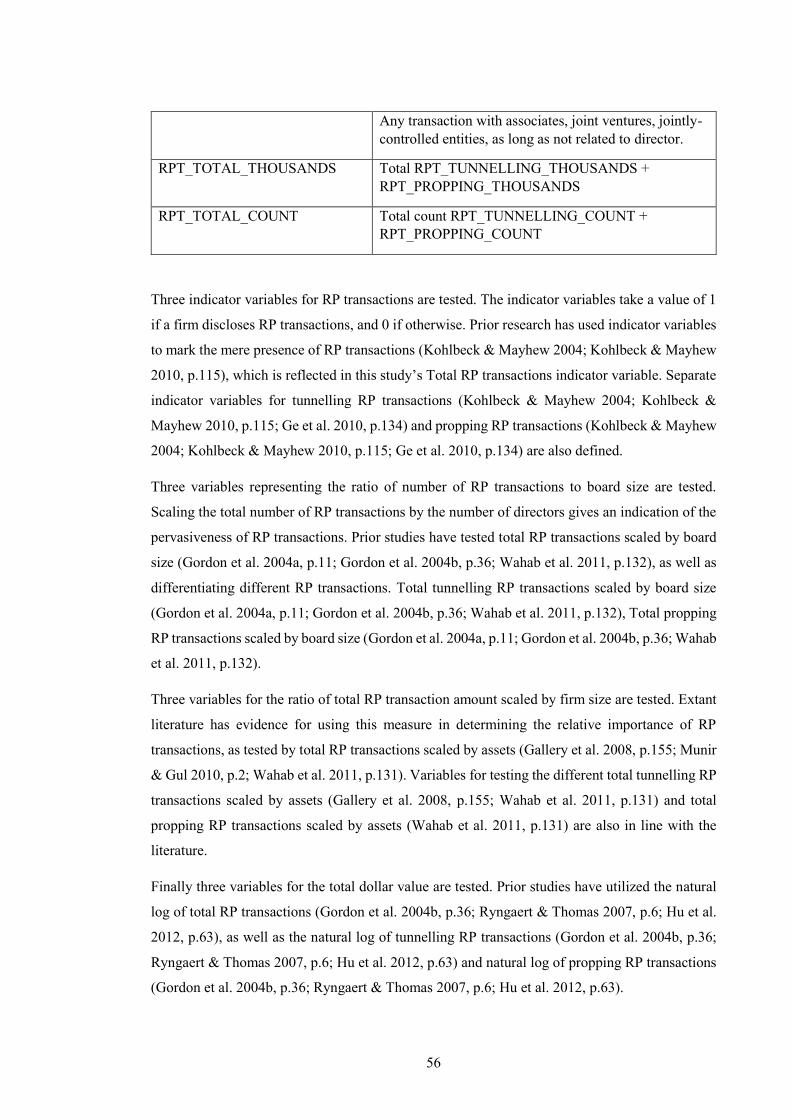

researchers. Briefly, four (4) categories of variables representing RP transactions are identified.

They are namely indicator variables, ratio of number of transactions to board size, ratio of total

amount by firm size, and by total dollar value. Within these four categories, twelve (12) variables

are defined, consistent with existing research into RP transactions and prior work by various

researchers (Gordon et al. 2004a, p.11; Gordon et al. 2004b, p.24; Kohlbeck & Mayhew 2004,

p.10; Ryngaert & Thomas 2007, p.11; Gallery et al. 2008, p.155; Kohlbeck & Mayhew 2010,

p.121; Ge et al. 2010, p.137; Munir & Gul 2010, p.13; Wahab et al. 2011, p.140; Hu et al. 2012,

p.63). Specific details of each variable are presented in later chapters on the operationalization of

variables.

Thirdly this study present empirical evidence that confirms prior studies but in a Malaysian

context. By shedding light on this area, it is hoped that governance standards can be raised and

help the capital market attract both foreign and local investors. It will also serve to inform the

perspectives of all stakeholders, in particular investors and regulators, to give a clearer and more

accurate picture on RP transactions. By doing so, Malaysia is one step nearer to becoming a

developed nation and a leading capital market in the region.

1.6 Assumptions and Limitations Firstly the research is limited to the effects of RP transactions on Malaysian listed firms in the

Trading sector. The Trading sector of Bursa Malaysia was selected over other sectors as it has the

largest market capitalization by far when compared to any other sector. The selection of the

Trading sector as the sample represents the best balance between achieving significant coverage

4

of the total market and limiting the costs of data collection. Within the Trading sector itself, a

wide variety of businesses are represented. The diverse range of businesses undertaken by firms

within the Trading sector allows for this study to take a good cross-section of related party

transactions performed by various companies. Additionally, firms within the Trading sector are

not separately regulated. This is unlike financial firms such as banks or insurers, which have

additional oversight from the central bank. The central bank, Bank Negara Malaysia imposes

additional regulations and prohibitions on related party transactions (Bank Negara Malaysia

2014). Such regulations may artificially distort the level of related party transaction undertaken

by an entity.

The limiting of the sample to only the Trading sector is a restrictive factor in that the results may

not be extrapolated to be representative of Malaysian listed firms, or Malaysian firms as a whole,

which are beyond the scope of this study. However, the findings may of this study are empirical

evidence that may lead to informed perspectives on RP transactions and their effects.

Secondly, the study assumes that all publicly available information is accurate. This is a limitation

as many times there are specific mechanisms and schemes to conceal information for various

reasons. In particular, due to the nature of RP transactions, concealment of such transactions in

the context of its usage as a tool for expropriation should be expected. This study assumes RP

transactions are the reported and disclosed RP transactions. Yet it is not unlikely that there are

unreported RP transactions amongst the various transactions carried out by firms. Similarly,

information about corporate governance is taken at face value, but this does not negate the fact

that there are hidden directors or undisclosed levels of ownership (Juliarto 2012, p.69). However

the study is not able to take this into account and it is assumed that publicly available information

is representative of the variables being measured.

Thirdly, although it is expected that RP transactions, and in particular tunnelling RP transactions,

will have a negative relationship with firm valuation, there is a possibility that the entire

Malaysian market as a whole is discounted due to RP transactions (Cheung et al. 2006, p.384).

Despite the limitations and assumptions outlined above, this study presents empirical evidence

that can give further insight into RP transactions and corporate governance.

1.7 Structure of the Thesis The remainder of the thesis is divided as follows. Chapter 2 lays out the theoretical framework,

current regulatory requirements, review of existing studies, and development of hypotheses. In

Chapter 3, based on the hypotheses, the research design is explained and operationalization of

variables is listed. Chapter 4 has the descriptive statistics based on the sample data collected.

5

Chapter 5 discusses the results of the empirical testing. Chapter 6 concludes this thesis as well as

outlining potential direction of any future research.

1.8 Summary This section introduces the problem statement and motivations for this study, as well as the

research questions and research objectives. The significance of the contributions of this study to

the topic are also outlined. Finally major assumptions and limitations of this study are explained.

6

2 Literature Review

2.1 Introduction The purpose of this chapter is to review existing literature on RP transactions, reasons for this

study, and to develop the hypotheses for testing. This chapter contains 5 sections. In the first

section, the role and significance of corporate governance is examined. The concept of corporate

governance itself, and traditional theories such as agency theory and transaction cost economics

are considered. Both internal and external corporate governance mechanisms are also looked at.

The second section examines the nature of RP transactions within the theoretical framework

developed by other researchers. In particular, agency theory and transaction cost economics are

used in building up the case for this study. In the following section, a detailed elaboration of the

Malaysian context of RP transactions from the viewpoint of legislation and regulator-issued

guidance is dealt with. Key aspects of the Malaysian political economy are also covered. The

fourth section reviews existing studies and their results regarding RP transactions, corporate

governance and firm valuation and performance. Finally, based on the arguments of the preceding

chapters, and underpinned by the theoretical framework in place, the necessary hypotheses are

developed and outlined.

2.2 The Role of Corporate Governance

2.2.1 Introduction The issue of asymmetric information is the primary driver that necessitates the existence of

corporate governance in the structure of a firm (Gordon 2004b, p.1). Corporate governance can

be defined in many ways. The Organisation for Economic Co-operation and Development

(OECD) gives a broad definition (OECD 2004, p.11):

Corporate governance involves a set of relationships between a company’s management,

its board, its shareholders and other stakeholders. Corporate governance also provides

the structure through which the objectives of the company are set, and the means of

attaining those objectives and monitoring performance are determined.

This view is representative of the state and understanding of corporate governance in the large

majority of developed countries, in particular in those under the Anglo-American legal and

economic environment (Shleifer & Vishny 1997, p.737). The definition given by the OECD is

reflective of the external and internal structures and mechanisms, by which a company may attain

its objectives and monitor its performance (Mallin 2013, p.15). The need for these structures and

mechanisms would not exists if external providers of finance and other stakeholders had perfect

information on the management of a firm. The external parties would be able to monitor, reward,

7

and penalize the behaviour of the managers, thereby preventing any self-dealing or expropriation

of the firm (Gordon 2004b).

A much narrower definition of corporate governance is given by Shleifer and Vishny (1997,

p.737):

Corporate governance deals with the ways in which suppliers of finance to corporations

assure themselves of getting a return on their investment. How do the suppliers of finance

get managers to return some of the profits to them? How do they make sure that managers

do not steal the capital they supply or invest it in bad projects? How do suppliers of

finance control managers?

This view is a very practical one, and deals exclusively with the potential for management to

expropriate from the company, at the expense of the shareholders. It is only concerned with how

investors will obtain a return from managers on the capital they have sunk in to a firm. This

interpretation of corporate governance assumes separation of ownership and control and frames

the governance structure from an agency problem perspective. However, it fails to bring up the

potential conflicts of interest that may exist if the management is also a principal shareholder.

This type of conflict is typically referred to principal-principal conflict (Shleifer & Vishny 1997,

p.737; La Porta et al. 1999, p.471; Cheung et al. 2006, p.343). It involves the expropriation by the

major shareholder against the minority shareholders. Additionally, other parties such as

debtholders would not be covered by this definition.

2.2.2 Development of Corporate Governance Agency theory and the separation of ownership and control underpinned the early development

of corporate governance (Smith 1904, Berle & Means 1932, Jensen & Meckling 1976, Fama &

Jensen 1983). Management could not be expected to utilise capital within the company provided

by external investors as diligently as if that same capital had been provided by themselves (Smith

1904). Early corporation law development was largely done with the intent on preventing outright

expropriation by the management of a firm. This was evident in the 18th to 19th centuries in

Britain as well as Europe (Shleifer & Vishny 1997, p.741). Consequently, courts and corporation

law have in the past set the tone and laid down the rules by which the duties, rights and

responsibilities of management were defined (La Porta et al. 1996).

A key feature of the agency problem espoused by the separation of ownership and management

model of Berle & Means (1932), Jensen & Meckling (1976), and Fama & Jensen (1983) is the

that the conflict is between management and a wide shareholding base. In recent years this view

of the agency theory that assumes diffused shareholding to be a given has increasingly been

viewed as a Western and Anglo-American take on corporate governance (Juliarto 2013, p.2). A

wide shareholding base is primarily a feature of major Western capital markets and is not

8

representative of the shareholding structures in other parts of the world, for example in Africa,

Asia, the Middle East and South America. In these markets researchers have found that ownership

is more concentrated, and controlling shareholders have higher stakes in the companies they own

(La Porta et al. 1999, p.471; Claessens et al. 2000, p.81; Faccio et al. 2001, p.54; Claessens et al.

2002, p.2741; Young et al. 2008, p.196).

In emerging and developing markets, the focus of corporate governance shifts from mitigating

principal-agent conflicts to restraining principal-principal conflicts (La Porta et al. 1999, p.471).

This becomes an issue that is more pressing in view of the fact that many emerging markets do

not have adequate corporate governance systems and the necessary legal recourse in place for the

protection of minority shareholders (La Porta et al. 1999, p.471; Liu & Lu 2007, p.881). This

problem is further exacerbated by the high ownership concentration that is a feature of listed

companies in many of these markets (Claessens et al. 2000, p.81). In Asia, much research has

been conducted, particularly in China. The issues faced are exemplary of the complexity of

managing the different interests in a country with a developing capital market, high ownership

concentration, and relatively weak corporate governance (Jian & Wong 2003; Chen et al. 2009,

p.285; Hu et al. 2009, p.190; Hwang et al. 2013, p.292). Listed firms in such an environment

typically have a large controlling shareholder. This shareholder would have the ability to select,

monitor and control management. This give power to the controlling shareholder to expropriate

funds that should be used for the benefit of all investors (Huyghebaert & Wang 2012, p.308).

2.2.3 Related Party Transactions and Corporate Governance

Gordon (2004b, p.35) finds that corporate governance and external monitors such as lenders are

associated with a reduced dollar amount of RP transactions in the United States. In Malaysia

Wahab et al. (2011, p. 158) found that RP transactions are linked to a reduction in firm return on

assets. In the same study the authors find that external monitoring such as a big-four auditor and

the level of board independence have a moderating effect on the performance-reducing impact of

RP transactions. The study however did not differentiate between different types of RP

transactions, and only concentrated on the effect on asset return rather than firm valuation. This

is consistent with the Kohlbeck and Mayhew’s (2004, p. 20) study which also found that higher

levels of board independence were associated with less RP transactions. Other governance

mechanisms such as the presence of audit committees were also found to affect the level of RP

transactions disclosed by a company (Cheung et al. 2009, p. 924).

Studies on internal and external governance measures to protect minority investors from the

majority have also been conducted. As the gap between the major shareholders’ control rights and

cash flow rights increases, so does the level of RP transactions that a firm engages in

(Huyghebaert & Wang 2012, p.308). In this particular study, it was also found that state-owned

9

firms were associated with more RP transactions, possibly to subsidise other financially weak

state-owned firms. Corporate governance mechanisms such as the board of directors and

independent directors were unable to limit this relationship.

The concept of ex ante and ex post RP transactions has also been examined. Ex ante refers to RP

transactions entered into when the counterparty is already a related party. Ex post refers to RP

transactions initiated before the counterparty becomes a related party and the effects on firm

valuation and performance. An examination of small to medium-sized American firms finds no

relationship between RP transactions and firm performance or valuation in general. However

when RP transactions are differentiated between ex ante and ex post, there is a significant

difference (Ryngaert & Thomas 2012, p.845). In particular, ex post transactions have a negative

relationship with firm performance and value, and in fact are associated with future financial

distress in firms. Ex ante transactions show no such relationship.

An examination of the key issues regarding regulation of RP transactions is the focus of a paper

by Trivun et al. (2012, p.15). They conclude that approval and disclosure of such transactions, as

well as holding board members and the controlling shareholder responsible if the firm suffers

economic losses due to the RP transactions, are key issues. This is further enhanced by having a

clear definition of RP transactions and an effective enforcement regime.

2.2.4 Internal and External Mechanisms of Corporate Governance The established view of research into corporate governance generally divides governance

mechanisms into two broad categories, namely internal and external mechanisms. Internal

mechanisms comprise primarily the board of directors, as well as ownership structure (e.g.

ownership concentration and large blockholders) (Shleifer & Vishny 1997, p.737; Boubakri et al.

2005, p.369; Jiang & Peng 2011, p.15; Huyghebaert & Wang 2012, p.308). External mechanisms

would include the regulatory and legal environmental, institutional development, leverage and

the takeover markets (Shleifer & Vishny 1997, p.737; Claessens & Fan 2002, p.71; Boubakri et

al. 2005, p.369; Wahab et al. 2011, p.131; Huyghebaert & Wang 2012, p.308).

The primary pillar of modern corporate governance in the firm is the board of directors. The board

is the pinnacle of the systems put in place to monitor, reward and penalize management of the

company (Fama & Jensen 1983, Jensen 1993, p.831). The board also serves as the first line of

defence against issues that may escalate into the crisis stage. Unfortunately few boards have

served this internal control mechanism effectively over the past few decades (Jensen 1993, p.831).

There is some evidence that research is progressing in understanding the complexities behind

board effectiveness. It is presumed that if the board is effective, the value of the firm will increase

(Amran 2004, p.48).

10

Board size is a factor that can contribute to elevating the board’s effectiveness (Jensen 1993,

p.865). It is argued that the larger the board, the less effective it becomes. Coordination between

members and going through processes with a large number of members outweighs the benefits

from having more individuals to draw on (Jensen 1993, p.865). This also makes it easier for

management to influence or manipulate. Empirical findings in the United States (Yermack 1996,

p.185), Europe (Eisenberg et al. 1998, p.35), Singapore and Malaysia (Mak & Kusnadi 2005,

p.301) support this view. In each of the previous studies, the researchers found that larger board

sizes were negatively related to firm value. This is consistent with prior research in organizational

behaviour that finds small groups being more effective than larger groups in decision making

(Mak & Kusnadi 2005, p.391). Additionally the risk of a large board being captured and

controlled by the CEO or management is higher than that of a small board (Jensen 1993, p.831).

From a practical stand, a large board consumes more in terms of remuneration, which is a direct

usage and drain on firm resources (Mak & Kusnadi 2005, p.391). Finally, a large board may be a

symptom of a predisposition of the existing board to add directors rather than replace them. This

causes an expansion in board size over time. The issue that arises is that the underlying reason for

such addition rather than replacement could be the board culture which avoids conflict and is

content to merely rubber-stamp decisions (Jensen 1993, p.831; Mak & Kusnadi 2005, p.391). At

the same time, larger boards may contribute to an increased access to resources, as well as a wider

range of experience which reduces risk to the firm (Haniffa & Hudaib 2006, p.1038). This

enhances corporate governance, as a variety of skills, experiences, knowledge and expertise can

be had with a larger board (Ghazali 2010, p. 112). A larger board also may have increased

capability to monitor management as the number of directors increases (Sulong & Noor 2008, p.

62). Board size is therefore an important corporate governance variable that must be taken into

account.

In the latest iteration of the Malaysian Code on Corporate Governance (MCCG), the code

recommends having a board composed of a majority of independent directors if the chairman is

not an independent director (Securities Commission Malaysia 2013). Board independence is

important in ensuring an effective control environment for management (Fama & Jensen 1983).

Independent directors have incentive to develop their reputation as experts on decision making,

and to be seen as watchdogs, with the main purpose of taking care of shareholder interests (Fama

1980, Fama & Jensen 1983). It is argued then that a larger proportion of independent directors on

the board ensures better monitoring and alignment of shareholder interest as the independent

directors wish to maintain their reputation as experts in decision control (Fama & Jensen 1983).

They have no economic interest in the firm and do not participate in day to day operations, and

are therefore able to provide objective assessments of the decision making process at the board

level (Rahmat 2013, p. 73). At the same time, arguments have been put forth on opposing

11

perspectives on board independence. Independent directors, by virtue of their lack of day to day

involvement, have limited time commitment to the company (Amran 2004, p.51) Additionally

they normally will not have shares in the firm, thus contributing to a lack of incentive to perform

a monitoring function (Amran 2004, p.51). Generally, the evidence supports higher board

independence as having a positive impact on firm valuation and performance, and this is reflected

in policy makers’ choices in mandating board independence via codes such as the MCCG.

Duality refers to the practice whereby the CEO and Chairman of the board are one and the same

person (Rahmat 2013, p.67). It is a widely accepted practice that is prone to be subject to conflicts

of interest if performed by the same individual (Jensen 1993, p.866). The function of the chairman

is to monitor and evaluate the CEO. Therefore if the CEO were to assume the position of chairman

also, it would be difficult in practice to achieve the function of chairman performed in an

independent manner (Jensen 1993, p.866). This also creates an atmosphere at the board level that

lacks independence and is characterized by conflict of interest (Amran 2004, p.52). Such an

environment can reduce the role of independent directors to mere rubber stampers, and not able

to protect the interests of shareholders (Amran 2004, p. 53). In the context of a market with

concentrated ownership, a controlling shareholder can dominate management by ensuring that the

chairman and CEO are both the same appointed individual. This can contribute to principal-

principal conflict that results in expropriation of minority shareholders (Jensen 1993, p.866).

Duality reduces the check and balance that should exist between the two positions of chairman

and CEO, and enable self-dealing behaviour to be unchecked (Rahmat 2013, p.67).

Ownership structure can act as both an internal corporate governance mechanism and also a

source of agency conflict (Shleifer & Vishny 1997, p.737; Gordon et al. 2004b, p.36; Boubakri et

al. 2005, p.377). Ownership concentration refers to the ownership of large blocks of shares by

investors, as opposed to diffused shareholding where many investors own many small blocks of

shares (Shleifer & Vishny 1997, p.754). It is easier for a single shareholder or a small number of

shareholders to act together to maintain their interests by monitoring, rewarding and penalizing

management as they have the necessary incentive to protect their investments (Shleifer & Vishny

1997, p.754). The large shareholder has the most to gain from any effort expended in watching

over management (Gordon et al. 2004b, p.36). This can be contrasted to the scenario of diffused

ownership, whereby no single small shareholder will want to act, as this will lead to a marginal

benefit for that individual while benefitting the remaining shareholders for free (free rider

problem) (Shleifer & Vishny 1997, p.756). At the same time, ownership concentration can have

its own costs to the remaining shareholders. A large controlling shareholder can also more easily

control management by appointing key posts and engage expropriation of minority shareholders

(Shleifer & Vishny 1997, p.758; Claessens et al. 2000, p.81).

12

Two major aspects of ownership structure have been researched. They are the level of ownership

concentration, and the identity of the owners (Boubakri et al. 2005, p.376; Juliarto 2012, p.29).

The identity of owners may be generally categorized as follows: government, local institutions,

foreign investors, employees and individuals (Boubakri et al. 2005, p. 375). This study groups

these into 2 even broader categories, namely institutions (government, local institutions, and

foreign investors) and families (employees and individuals). The identity of the shareholder in a

concentrated ownership situation can have very different impacts. For example having an

institution as a controlling owner may lead to better monitoring and oversight of management,

whereas having a family as a large shareholder tends to lead to higher rates of expropriation of

minority shareholders (Ismail & Sinnadurai 2012, p.255; Juliarto 2012, p.30). These issues arise

as large shareholders represent their own interests, which may or may not be the same as the

interests of the minority shareholders (Shleifer & Vishny 1997, p.758).

Family ownership in particular is an aspect that is common among Asian firms (Claessens & Fan

2002, p.71). Typically the family will have a controlling stake in the firm, or the firm will be part

of a larger group controlled by the family (Juliarto 2012, p.31). On one hand family ownership

may assist to align the interests of the shareholders with management (Jensen & Meckling 1976,

p.305; Fama & Jensen 1983). On the other hand, the risk of expropriation of minority shareholders

is also increased (Faccio et al. 2001, p.54).

Audit quality can serve as an effective external governance measure. The role of the independent

auditor is increasing users’ confidence in financial statements by expressing an opinion as to their

fairness of presentation and reliability of reported figures (Rahmat 2013, p.75). The Companies

Act 1965 requires auditors to be independent and have the right to address the shareholders in a

general meeting, thus fulfilling the public role of a public accountant (Wahab et al. 2011, p.198).

Although there is a general requirement for financial statements to be audited, the quality of the

auditor may vary. A more reputable auditor is likely to be more effective in preventing financial

statement misreporting and self-dealing activities as they have more of reputation to protect

(Wahab et al. 2007, p.108). At the same time, a more credible auditor might be appointed by a

company that has a propensity for more self-dealing to enhance the legitimacy of their

transactions and to play a certification role (Wahab et al. 2011, p.198; Gordon et al. 2007, p.83;

Fan & Wong 2005, p.35). The auditor in each of these situations would play the role of an external

corporate governance mechanism. In a large number of studies, audit quality is proxied by the

usage of Big 4 or Tier 1 public accounting firms (Rahmat 2013, p.75; Wahab et al. 2011, p.198;

Chien & Hsu 2010; Gordon et al. 2007, p.81). A criticism of using this metric is the obvious

involvement of the former top tier public accounting firm, Arthur Andersen & Co.’s implication

in the Enron scandal of 2001 (Rahmat 2013, p.76). This reinforces the notion that a firm with

shady RP transactions might seek to legitimise those same transactions by having them signed off

13

by a reputable auditing firm (Gordon et al. 2007, p.93; Wahab et al. 2011, p.143). At the same

time, having a strong and independent external monitor, outside of the board of directors, can be

an effective mechanism in countering the negative effects of RP transactions (Rahmat 2013, p.76;

Gordon et al. 2007, p.93).

Leverage can also act as a corporate governance mechanism (Jensen & Meckling 1976, p.40).

External creditors are concerned with the ability of the firm to repay borrowings, and will

therefore ensure management or controlling shareholders do not expropriate firm resources. They

have the necessary incentives to monitor firms and their management to ensure sufficient funds

for debt repayment (Gordon et al. 2004b, p.36).

2.3 Related Party Transactions and Theoretical Framework

2.3.1 RP Transactions: Efficient Transactions or Conflict of Interest? Related party transactions are transactions between the firm and a party that is related either as a

subsidiary, associate, principal owners, officers or directors (Gordon et al. 2007, p.83). There are

two primary views on RP transactions in the extant literature which result in either positive or

negative effects on investors and minority shareholders. Gordon et al. (2004a, 2004b) and

Kohlbeck and Mayhew (2004) were among the earliest to identify these two opposing

perspectives on RP transactions. Prior to this it had been perceived that RP transactions would

only constitute conflicts of interest that were detrimental to shareholders. However, based on

rational economic arguments, it was hypothesized that it was possible to view RP transactions in

two contrasting ways. One view is that RP transactions are conflicts of interest and are negative

for firm performance and valuation, and the other view is that RP transactions are efficient

transactions that benefit firm performance and valuation. These two views are also known as the

conflict of interest hypothesis, and the efficient transactions hypothesis.

Under the conflict of interest hypothesis, RP transactions were a breach of the agent’s

responsibility. This responsibility could take the form of management’s duties to shareholders, or

the monitoring function of the board of directors (Gordon et al. 2004a, p.4, 2004b, p.11). The

alternative efficient transactions hypothesis states that RP transactions are the most economically

efficient method for the company to carry out certain dealings. In the next section, we examine

the detailed theoretical frameworks underpinning these two contrasting views on RP transactions.

2.3.2 Agency Theory and Conflict of Interest

Related party transactions have emerged as a form of self-dealing with the potential for a

multitude of negative consequences. The basis of determining the negative impact of RP

transactions has its roots in agency theory (Gordon et al. 2004a, p.4; Kohlbeck & Mayhew 2004,

p.3; Cheung et al. 2006, p.346).

14

The modern firm is characterized by separation of ownership and management. Agency theory

explains the nature of the separation of ownership and management in a firm. This has been

developed by Berle and Means (1932), and further refined for the modern corporation by Jensen

& Meckling (1976). Subsequent work in this area led to development of contracting theories of

the firm (Fama 1980; Fama & Jensen 1983). However much of this development was done in

Western or Anglo-American economies where there is a high dispersion of ownership. In

emerging economies such as Malaysia, concentrated ownership is the norm. Research in a

Malaysian context, with concentrated ownership, is limited.

The majority of research in corporate governance is based on agency theory. Principal-agent

conflict arises between shareholders (principal) and management (agents). Management is

assumed to have different objectives from shareholders, many of which are to benefit themselves.

Mechanisms such as the board of directors are governance measures put in place to ensure that

management acts in the interest of shareholders. These measures represent agency contracting

costs, which are put into place at the expense of the shareholders, to align management’s

objectives to that of shareholders.

The Great Depression-era book ‘The Modern Corporation and Private Property’ was among the

earliest works on the basis of agency theory and modern corporate governance. Published in 1932,

it examined the evolution of the corporation that had resulted in the separation of ownership and

management. It also looked at the implications for the corporation and its shareholders. Written

by Adolf Berle and Gardiner Means, the key idea was this: once an investment had been made in

a corporation by shareholders, they were distanced legally from the property (investment) they

had put into the corporation. Legal title now rested with the corporation. It is noted that the

shareholders own the corporation; in fact in many instances now and in the past, they were also

the management. However, through the changing roles and delegation of power in a corporation,

management in a modern corporation is often surrendered to a controlling group other than the

shareholders (Berle & Means 1932, p. 334).

Berle and Means (1932 p. 336) state that “All powers granted to management and control are

powers in trust”, but the question arises as to how to ensure that those powers are not abused.

Courts and corporation law have in the past laid down the rules by which the statement above is

enforced (La Porta et al. 1996, p. 12). In the working paper entitled ‘Law and Finance’, the authors

study the legal rights attached to shares (La Porta et al. 1996). These legal rights are the means

by which shareholders ensure their investment is protected and a return can be obtained from it.

Shareholder rights such as voting rights, calling for general meetings, obtaining relevant

information and protection of minority shareholders are all meant to protect the investments of

shareholders. As seen in the previous section on the Malaysian Companies Act, there has been an

15

effort to regulate RP transactions in Malaysia through various amendments to the Act. This is an

overall theme of whether there is sufficient legislation and regulation to protect shareholders,

investors and the general public from fraud in RP transactions in Malaysia.

Another issue to consider is the type of abuse that may occur. The most obvious is outright

expropriation. As Adam Smith (1904 p. 439) writes in his book entitled ‘The Wealth of Nations’,

managers of companies in which the capital is not their own will not have the same ‘anxious

vigilance’ of a company managed by the capital providers. Consequently, a significant amount of

early corporation law development was focused on preventing outright theft by the controlling

group of management. This was evident in the 18th to 19th centuries in Britain as well as Europe

(Shleifer & Vishny 1997, p. 742).

However, mere legal protection for investors is insufficient. Rigid rules do not put the interests of

the investors, the management or the corporation in good stead. Due to the endless variety in the

nature of business that could be carried out by a corporation, it is not practical for the courts to

determine the commercial merits of transactions carried out by a corporation. Take for example

the United States, which is the most litigious society in the world (Rubin 2010). Even in this

country, courts refuse to engage in meddling with the day-to-day affairs of a corporation, quoting

the now universal ‘business judgement rule’ (Shleifer & Vishny 1997, p. 741). It is also not in

commercial interests to have shareholders running the corporation through voting on every

transaction (OECD 1999, p.12). In Malaysia, the development of regulation is an ongoing process

to bring it in line with global best practices (Chan 2010, p.3). This needs to be balanced with

effective enforcement, which has been lacking in the past (La Porta et al. 1996, p.6). A study on

the impact of RP transactions and factors associated with it will aid both the development of

regulation and effectiveness of enforcement in Malaysia.

Jensen and Meckling (1976, p.58), in their paper on the theory of the firm, developed the

formalized view of the agency problem using financial economics. Contracting within the agency

relationship is between the shareholders (principal) and management (agent). Due to the

separation of ownership and control, the problem of ensuring that funds or capital are not wasted,

and that a return is assured, arises as a concern for shareholders.

Related party transactions can be seen as a conflict of interest between the agents and principals

in the agency relationship within a corporation. The incentive to expropriate varies with cash flow

rights (Jensen & Meckling 1976, p.64). Cash flow rights refer to ownership via shareholding. In

a widely held corporation, this indicates that management’s self-dealing is a maximization of their

own utility at the expense of the other shareholders. Jensen & Meckling (1976, p.58) further

expound that there will be differences in the decisions made by the agent relative to the best

interests of the principal. The key assumption here is that both the principal and agent are utility

16

maximizers. It would then be expected that the agent may not act in a manner that is optimal from

the perspective of the principal. The opportunism of the agent may variously result in misuse of

power, overconsumption of perquisites, adverse risk-taking, and information asymmetry (Mallin

2013, p.15).

This has led to the view of the firm as a nexus of contracts, with each contract interconnected to

the other, balancing out the various incentives and costs to the principal and agent. The sets of

contracts act together to discipline the individual members of in a firm and the firm as a whole to

be aligned to the interests of the principal. The monitoring function of a board of directors that

brings independence and oversight to the firm is also theorized (Fama 1980, p.293; Fama &

Jensen 1983, p.14).

A more common issue in emerging markets is the problem of principal-principal conflict. High

ownership concentration is a common feature of firms in this region, including Malaysia. La Porta

et al. (1999, p.471) concluded that higher ownership concentration increases the power that major

shareholders have to expropriate the minority. In a closely held corporation (i.e. concentration of

ownership) this would indicate maximization of the principal shareholders’ utility ahead of the

other minority shareholders. Principal-principal conflict arises when there is concentrated

shareholding. Here there is conflict between two principals – the major shareholder and the

minority one. The effect of this conflict is the major shareholder expropriating the minority one.

Management may act to benefit the major shareholder, but at the expense of the minority

shareholders. Governance mechanisms such as the board of directors may be overridden by the

major shareholder. This is because the major shareholder has the ability to appoint the board.

Research on both principal-agent and principal-principal conflict is categorized as self-dealing.

Earlier studies have focused on issues such as managements spending on perquisites (Djankov et

al. 2008, p.430). This has progressed to studies on the private benefits of control by which insiders

enrich themselves. Several researchers have variously examined excessive compensation, transfer

pricing, appropriation of corporate opportunities, self-serving financial transactions, preferential

placement of equity, personal loans to directors or management and outright expropriation of the

firm’s assets (Shleifer & Vishny 1997, p.737). The common link and the emerging focus of self-

dealing is however on related party transaction, and their impact on the firm and implication in

self-dealing. Related party transactions, more than any other method, represent a key enabler of

management opportunism and an avenue for both principal-agent and principal-principal conflict.

Gordon et al. (2004a, p.4, 2004b, p.11) explores the idea of RP transactions as being a conflict of

interest by the agent through the lens of agency theory. The related party transaction would reflect

neglect of the agent’s responsibility to the principal, and subversion of the monitoring function of

the board of directors. The researchers also highlight the role that RP transactions played in the

17

multitude of corporate scandals that had emerged in the wake of Enron in 2001. As a result, the

view of RP transactions was a fulfilment of the very concerns raised of an agent not acting in the

interests of the principal. The researchers put forth this view of RP transactions to be known as

the conflict of interest hypothesis.

Kohlbeck & Mayhew (2004, p.6) further build on the prior work by Gordon et al. (2004a, 2004b)

using agency theory to differentiate between various classes of RP transactions. In particular they

conclude that simple RP transactions might be the results of self-dealing by management, whereas

more complex RP transactions are consistent with efficient contracting to align interests of the

principal and agent.

Delving into the specific mechanics of self-dealing and RP transactions, Cheung et al. (2006)

examined actual transactions of listed firms in Hong Kong. Their work shows clear demarcation

in terms of the impact of different types of RP transactions on firm valuation by the market. Of

particular note is the consistency of the result with predictions by agency theory as to which

transactions would be value-destroying. Cheung et al. (2009) continue further to compare RP

transactions versus their arm’s length equivalents to show clearly the mechanisms used by agents

(majority shareholders, in an environment of concentrated ownership) to expropriate from the

minority shareholders.

2.3.3 Transaction Cost Economics and Efficient Transactions An alternative view of RP transactions as efficient transactions was proposed by Gordon et al.

(2004a, p.4, 2004b, p.11) and is known as the efficient transactions hypothesis. This is based off

the work of Coase (1937) and Williamson (1988) on the topic of transaction cost economics.

Transaction cost economics takes the position that the firm is a governance structure for the

efficient conduct of economic affairs. This can be contrasted to the agency theory view that sees

a firm as a nexus of contracts (Mallin 2013, p.16). In the efficient transactions hypothesis, RP

transactions actually help the corporation. The transactions are not viewed as detrimental to the

interests of shareholders, but rather serve to efficiently deliver economic benefits to a firm

(Ryngaert & Thomas 2007, p.6). The RP transactions are posited as an efficient contracting

mechanism.

The firm derives economic benefits from performing certain transactions internally rather than

with external parties (Mallin 2013, p.16). This is consistent with the theory of transaction cost

economics. In the context of this study on RP transactions, conducting transactions internally

would refer to contracting with related parties, as they would be considered internal by virtue of

not being at arm’s length. Williamson (1984, p.28) builds the case for an internal capital market

within the firm. The outcome of such a market would be for the firm to undertake internal

transactions (or, in the case of this study, RP transactions) up to the point where it is more efficient

18

for external transactions to be performed. Another way to phrase this is that a firm should engage

in RP transactions so long as the benefits continue to outweigh its costs. This view of RP

transactions being a form of internal dealings that offer advantages over arm’s length or external

dealings is in line with the theory of transaction cost economics (Pizzo 2013, p.309). The firm

must derive certain benefits from RP transactions to justify the transaction being entered into by

the firm.

Various benefits of RP transactions as efficient transactions have been theorized and would

include lower transaction costs, improving capital allocation, obtaining better returns on assets,

and providing to solutions to overcoming problems impairing production (Pizzo 2013, p.317;

Wahab et al. 2011, p.133; Jian & Wong 2010, p.74). By engaging a related party, information

asymmetry is reduced. For example confidential information does not need to be shared with an

external party (Gordon et al. 2004a, p.4, 2004b, p.17). There would be greater co-ordination of

actions, faster feedback loops, and better insights (Ryngaert & Thomas 2007, p.6). Related party

transaction between related parties assumes that both parties would have sufficient information

on each other. This depth of information might then enable transaction which would not be

otherwise possible at arm’s length. (Pizzo 2013, p.309).

It is also possible that RP transactions could be a substitute or complement to management

compensation (Pizzo 2013, p.309; Kohlbeck & Mayhew 2004, p.6). Related party transactions

may form part of a formal or informal agreement on compensation. The transactions with the

related party could serve as an alternative to cash-based compensation for management. The RP

transactions could also be a more liquid form of compensation for management when they are

remunerated largely in stock options, which tend to be less liquid (Kohlbeck & Mayhew 2004,

p.6).

The related party may also have certain skills or abilities which are not easy to find in the market,

and by engaging them the corporation has saved time and search costs (Kohlbeck & Mayhew

2010, p.119). This could be exemplified by a service provider with comprehensive knowledge of

the firm. Obtaining the services from a related party who already possesses this knowledge will

be more efficient than hiring an external party that is not privy to this information. There is less

information asymmetry and therefore a lower transactional cost. Moreover, the relationship with

the related party providing the service will also be enhanced (Gordon et al. 2004b, p.11). It is also

conceivable that management may prefer working with a known and trusted party, for example

family members, which in turn may enhance the performance of both management and the

contracting party. This benefits the shareholders through better effectiveness and efficiency

(Gordon et al. 2004a, p.4).

19

Another argument in favour of the efficient transactions hypothesis is the inefficient state of

markets in developing economies (Khanna & Palepu 1997). From an institutional context,

markets that are less developed will have imperfect financial, labour and product markets. These

inefficiencies increase the business risk for a firm. It would then make sense for a firm in such a

setting to deal with related parties to be assured of better access to capital, financing, business

development opportunities and economies of scale (Pizzo 2013, p.309; Khanna & Palepu 1997).

Dealing with members of the same group, or at least with parties which are known to the firm,

may mitigate the problems such as enforcement of contracts and property rights, which are critical

to the corporation (Cheung et al. 2009, p.915; Khanna & Palepu 1997). This occurs more

frequently in firms found in East Asia due to the high level of ownership concentration. The

shareholders may hold blocks either through individuals, families, or governments. Typically,

controlling shareholders will install their own family members, or trusted representatives, into

management, which tends to increase the probability of RP transactions happening (Claessens,

Djankov & Lang 2000, p.2741).

It has also been argued that the amount and quantum of RP transactions is small and immaterial

to the firm. The RP transactions may be large in relation to the related party but sufficiently small

so as to be immaterial to the firm. For example, a director may influence a contract worth RM10

million to be awarded to a related party. The sum of RM10 million may very significant from the

view of the personal net worth of the director. However, if the firm has billions of dollars in sales,

this sum of RM10 million will be almost inconsequential. This argument is consistent with the

view that RP transactions do not negatively impact the firm (Gordon et al. 2004a, p.19; Wahab et

al 2011, p.133).

Furthermore, although there are varying levels of restrictions on RP transactions around the world,

no nation has completely outlawed them (Djankov et al. 2008, p.430). This lends credence to the

efficient transactions hypothesis of RP transactions that they can be in some ways beneficial to

the firm. An efficient transaction yields benefits to the firm and its shareholders, and does not act

against their interests.

2.3.4 RP Transactions as Source of Tunnelling or Propping This study considers the two alternative views of RP transactions, which are the conflict of interest

view and efficient transactions hypothesis. These two alternative views suggest that there are

variations in the in different types of RP transactions undertaken by the company (Kohlbeck &

Mayhew 2004, p.6). In examining whether the RP transactions has a positive or negative impact

on the company, the actual nature of the transactions should be looked at.

Gordon et al. (2004a, p.4) was an early study looking into the various types of RP transactions in

the United States. The authors merely classified the transactions examined, offered descriptive

20

statistics and suggested possible implications of the various types of transactions. Agreements

related to employment and indemnification agreements were left out in the study as these were

deemed to be clearly compensation for executives. Gordon et al. (2004a, p.8) also established a

measure of the complexity of a company’s RP transactions. This is achieved by looking at the

number of parties and the number of types of transactions, with a higher number for either

indicating increased complexity. Increased complexity in RP transactions would be a sign of

potential conflicts of interest and bypass of monitoring mechanisms in the firm.

Gordon et al. (2004b, p.32) continue from their earlier work to investigate the effect of corporate

governance on RP transactions, as well as the effect of RP transactions on firm value. They find

evidence generally of conflict of interest, and a restraining effect of strong corporate governance

on RP transactions. In particular, the identity of the related party involved in the transactions

impacted the effect on firm value.

Kohlbeck & Mayhew (2004, p.14) apply a categorization system to RP transactions. The two

categories they defined were simple and complex. Simple transactions are typically very clear in

purpose and involve few financial statement items. Complex transactions involve multiple parties

and impact the financial statements in more subtle ways. The study found that stronger board

independence lowered the probability of RP transactions. Moreover the study suggested that both

the conflict of interest perspective and efficient transactions hypothesis could be supported

depending on the type of RP transaction. There was evidence that complex RP transaction would