Top 8 Mobile Finance Trends 2015

What will Apple Pay mean for the financial institutions? Who are the

mobile innovators and disruptors of the financial industry? How will

banks tackle mobile security threats in 2015? What’s the regulatory

impact of new mobile technology such as wearables? How do

financial institutions stay on top of mobile technology with an

accelerated pace of innovation? How much longer will employees

of financial firms be tied to a desktop? We’ve asked customers and

partners, spoken to industry experts and made our own conclusions

and predictions to help financial organisations succeed in mobile

in 2015.

1. Customer First and User ExperienceThe main topics and focus when speaking to financial institutions is

still regulatory challenges, cost reduction pressures, cyber security

threats and reduced footfall to retail branches. Customers, whether

they are consumers or businesses, always seem to be far down the

priority list. Controllers, business analysts, lawyers and software

engineers create and shape new products with limited or no

involvement of the customers.

When we recently showed a video to the CMO of a bank of the

painstaking steps that a customer had to go through to sign up for

an online account he stopped us in the middle and said, “This is

enough. We have to do something now.”

What this means for you

In the past banks have been pretty well protected from competition

except a few success stories of Internet only banks. This is no more.

With money going digital, branch offices becoming obsolete, start-ups

disrupting loans, forex, payments and credit cards, traditional banks

are facing real threats and challengers can grasp the opportunity.

Forget about Mobile First if you don’t like buzzwords and put the

Customer First in your business. Give product managers and business

managers real power to lead and develop products and customers

experiences that put the Customer First. Tell the other departments

that their goal is to support and not to obstruct this effort. Ask yourself

about the honesty in having customers sign several pages of terms

and conditions that they will never read. Start now!

Forget about ‘Mobile First’ if you don’t like buzzwords

2. Use Start-ups and Disruptors as InspirationFollowing on the Customer First trends, many of the start-ups in

the fintech industry are now offering services that are directly in

competition with the banks and not just provided to the banks. Recent

success stories include Prosper and Lending Club in the loan space,

Simple for improved banking, Mint (previously known as Check) for

financial planning, TransferWise disrupting forex and Venmo in person-

to-person transfers. Some get acquired while others continue to

disrupt as independent companies.

What this means for you

The financial industry is slower than most other industry due to the

complexity, regulation and security requirements. Use this to your

advantage to beat or leverage the start-ups before they disrupt your

business or help your competitors get an advantage. Several of the

trends outlined in this presentation can leverage the core ideas, or

potentially technology, of these start-ups.

Here are some of the start-ups that we believe have potential of

disrupting or helping financial institutions disrupt the financial space

in 2015 and beyond:

Lenddo Using social media to score and underwrite small loans over

a mostly mobile platform

Ferratum Mobile/online only banking in Europe (Disclaimer: DMI client)

Bionym Heartbeat authentication that can be used as an alternative

or complement to passwords, secure ID devices and more to

improve banking security

MyMobileSecurity Personal security services and tools for bank

customers

Pindrop Pattern recognition to detect fraud

Personetics Making personalised real-time recommendations to

customers and bank retail staff based on big data

Use this to beat the start-ups before they disrupt your business

3. Omni-Channel BankingImagine if you could start completing an application for a new credit

card from your mobile, continue from the tablet at home and when

in need call customer service and have them help you fill out the

blanks. Customers today expect their service providers to keep all

data in one place and provide services based on this. However, the

real experience is very different. Most registrations are still based

on old fashion PDF printouts that have to be mailed to the bank. In

fact, most banking processes are 20 years or older and were never

designed for the web or mobile.

What this means for you

Design services and user experiences that work the same way

independent of channel and/or device. Ask customers what they

do on the move, what they do at work or at home with access to a

desktop/laptop, when they want to speak to customer service over

the phone or in a retail branch and design your services based on

this. Challenge and rethink processes and find ways to avoid barriers

to entry such as tedious and annoying forms, 5 min videos that

customers have to watch and papers, papers and more papers.

Take the opportunity to redesign some of your core banking

processes if they cannot support the user experience that customers

expect and want.

Take the opportunity to redesign processes to give your customers what they expect and want

4. Banks Turning Into a Digital MarketplaceIn the past the bank branch office provided the opportunity for

banks to sell everything from bank accounts, mortgages, forex and

credit cards to pension plans, mutual fund savings and insurance.

Now online and mobile banking have completely taken over. The

smaller screen of mobile devices and quick bites of consumption

(e.g. checking balance) means that the services recommended

need to be relevant and spot on.

What this means for you

Use the power of data to provide your customers with the services

they want or need. If a customer is traveling a lot, offer them a travel

insurance tailored for them; if a millennial has too much cash in their

account, provide them with a first introduction to long-term savings,

etc. Banks have amazing data at their hands although usage is

restricted. Use it to serve your customers, because they expect it.

Use data to serve your customers

5. Help Protect Your CustomersAll the cyber security threats, hacks and data intrusions are causing

concerns among customers. Is it safe to use my bank application

over an open Wi-Fi network? Can other apps access the banking

data on my phone? Can I use a device that is not my own to

complete a personal banking transaction? Customers have no idea

and the number of threats and media focus on this keeps increasing.

The biggest barrier to customers signing up and using mobile

banking is still security concerns.

What this means for you

This is an opportunity for banks and not a threat. Be the bank

that offers customers the assurance that it’s safe and help your

customers stay safe. Provide them with the tools necessary to use

the mobile safely on public Wi-Fi-networks, monitor for viruses and

Trojan horse apps, understand the access rights of each application

and tell them what third-party apps are safe to use.

Be the bank that helps your customers stay safe

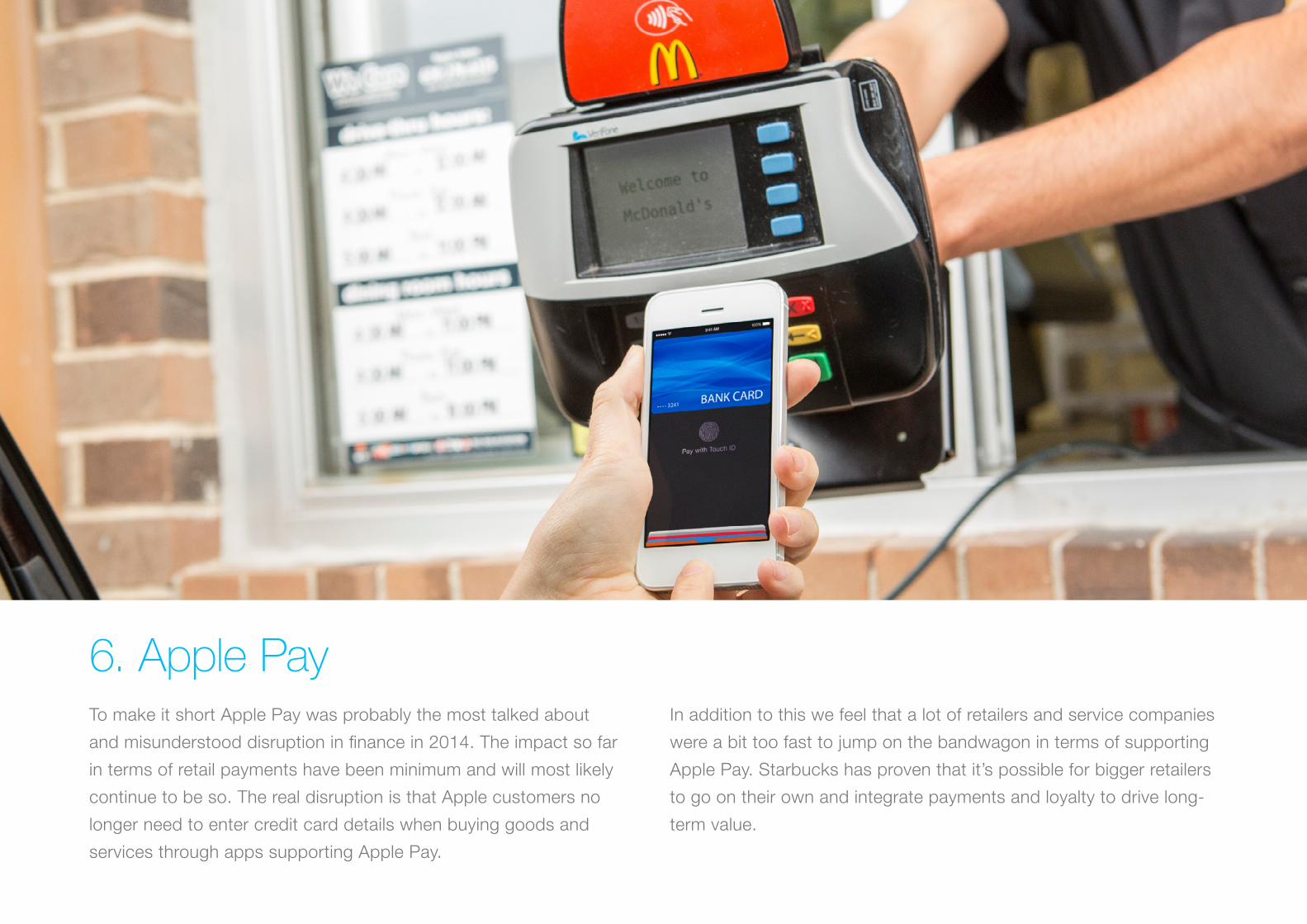

6. Apple PayTo make it short Apple Pay was probably the most talked about

and misunderstood disruption in finance in 2014. The impact so far

in terms of retail payments have been minimum and will most likely

continue to be so. The real disruption is that Apple customers no

longer need to enter credit card details when buying goods and

services through apps supporting Apple Pay.

In addition to this we feel that a lot of retailers and service companies

were a bit too fast to jump on the bandwagon in terms of supporting

Apple Pay. Starbucks has proven that it’s possible for bigger retailers

to go on their own and integrate payments and loyalty to drive long-

term value.

What this means for you

We love Apple Pay but make sure that you evaluate Apple Pay

from a customer value perspective and the long-term impact on

your business. How important is the data that Apple captures and

doesn’t share with you? Could you get customers to sign up

directly with credit cards and other payment mechanisms with

a small incentive and will this offer create greater value for your

business in the long- term?

Evaluate Apple Pay from a customer value perspective

7. The Office is Going MobileBanks are typically the biggest property occupants in any downtown

area and especially in the financial centers. Most financial services

require a great share of the customer facing process and all of the

administration work to be carried out in a bank office. This means

that financial services sales staff frequently spends a day per week

or more in the office when they would prefer to spend their time with

customers. In addition to this, banks occupy prime real estate, which

is a big expense. What if it was possible to mobilise the office for

banks? We think it is.

What this means for you

Most financial institutions have regulatory, security and process

requirements that make it difficult for bank staff to work from home, in

the field or on-site with customers. And you’re already at risk anyway.

According to a recent survey by Ovum, 62% of those employees

who use their own devices at work do not have a corporate IT policy

governing that behaviour. Challenge these restrictions and start

redesigning your services for a mobile only world.

Start redesigning your services for a mobile only world

8. Customers Want Access to Everything On The GoBank CIOs frequently tells us that their corporate and institutional

customers don’t need or want mobile services because they spend

all day in an office with desktops. According to a recent study by

Mobile trading, DARTs (Daily Average Revenue Trades) have been

steadily increasing since 2012, with 13% of all trades being placed

on a mobile device in 2014. This is of course the average for

trading and generally not corporate trades. However behaviour is

changing with almost 50% of all work applications accessed from

mobile devices (Ovum multi-market BYOD survey) and the work

environment for corporate banking and customers is also changing.

What this means for you

Customers expect mobility and flexibility whether they are individuals

or employees of a hedge fund. The role of the office is changing, work

life and personal life is becoming less and less distinct and customers

expect to be able to access information and services whenever and

wherever they are. This may be challenging and the organisations that

solve this challenge first will be the winners of tomorrow.

The organisations that solve this challenge first will be the winners of tomorrow.

Fighting for a world full of mobile solutions since 2005

web www.goldengekko.comemail [email protected]