44

KAPLAN PUBLISHING 1 QUESTIONS

KAPLAN PU BL ISHING 1

QUESTIONS

PAPER F6 : TAXAT IO N (FA 2009 )

2 KAPLAN PU BL ISH INGH

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 3

INCOME TAX AND NATIONAL INSURANCE

INCOME TAX BASICS

1 DARRYL AND NICHOLE

(a) Darryl, an advertising executive, and his wife Nichole, an IT consultant, have one son. Having made a large gain on the sale of a property when they got married, they have acquired a considerable number of investments. They now require assistance in preparing their taxation returns for 2009/10 and have listed out their income and expenditure:

Darryl £

Salary 45,500

Premium Bond winnings 5,000

Interest received on National Savings Certificate 300

Nichole

Salary 48,000

ISA account − dividends received 350

− interest received 125

Dividend received on Virgin plc shares 2,250

Interest received on 2009 10% Treasury Stock 2012 (Gross) 2,000

Gift Aid payment to Dogs Trust 1,000

In addition they received interest of £4,400 on a joint building society account.

Required: Calculate the income tax liabilities for Darryl and Nichole for 2009/10, showing the income tax liability. (15 marks)

(b) Darryl’s father, Mr Ancient, is 65. His income for 2009/10 comprised the following.

£ State retirement pension 6,226

Pension from former employer 14,355

Building society interest received 3,348

National lottery winnings 10,000

Required:

Calculate the income tax liability of Mr Ancient for 2009/10. (5 marks) (Total 20 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

4 KAPLAN PU BL ISH INGH

2 EMPLOYED OR SELF-EMPLOYED

Required:

Briefly discuss the criteria to be considered when deciding whether an individual is ‘employed’ or ‘self-employed’. (11 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 5

INCOME FROM EMPLOYMENT

3 KYRIA LAMPARD

Kyria Lampard was 43 on 30 September 2009. She is the managing director of Roberts Ltd, a family owned company.

Kyria received a salary of £44,000 for the year ended 5 April 2010 (tax deducted under PAYE £8,505) and is provided with a petrol driven car by the company (list price in 2002 £29,143) for which she is required to pay the company £400 per month in respect of her private use. She travelled 12,000 miles on business during 2009/10 and is provided with all fuel for business and private use by the company. The car omits 204 g/km of CO2.

On 1 July 2009, Kyria purchased the company’s video camera. It had cost £750 two years ago and was now worth £250 when she purchased it. Kyria paid £45 for it. It had never been used by Kyria for private purposes until 1 July 2009.

She paid premiums into a personal pension plan of £8,500 in 2009/10.

Kyria has let out unfurnished property for several years and due to extensive repair expenditure sustained a property income loss of £2,000 for 2009/10. She also has a house let as furnished holiday accommodation. This house was let for 43 weeks during 2009/10 and the net rental income was £17,000. Kyria also wishes to claim capital allowances of £5,000 for 2009/10 on plant and machinery used for the purposes of maintaining the furnished holiday property.

She received UK company dividends of £4,500 and building society interest of £4,200 (net) during 2009/10.

She has paid £4,100 as payment on account of her liability for 2009/10.

Required:

Calculate Kyria’s income tax payable for 2009/10 and state the normal due date for payment of any balance payable. (15 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

6 KAPLAN PU BL ISH INGH

4 RITA

Rita, who is a fashion designer for Daring Designs Limited, was re-located from London to Manchester on 6 April 2009. Her annual salary is £50,000.

She was immediately provided with a house with an annual value of £4,100 for which her employer paid an annual rent of £3,500. Rita was re-imbursed relevant re-location expenditure of £12,000.

Daring Designs Limited provided ancillary services for the house in 2009/10 as follows:

£ Electricity 700Gas 1,200Water 500Council tax 1,300Property repairs 3,500

The house had been furnished by Daring Designs Limited prior to Rita’s occupation at a cost of £30,000. On 6 October 2009 Rita bought all of the furniture from Daring Designs Limited for £20,000 when its market value was £25,000.

On 6 April 2009 Rita was provided with a laptop computer, which cost £1,500 for her personal use.

Daring Designs Limited had made a loan to Rita in 2007 of £10,000 at a rate of interest of 3%. The loan is not being used for a ‘qualifying purpose’. No part of the loan has been repaid. Assume the official rate is 4.75%.

Rita was provided with a 1800cc company car. It had a list price of £18,500 when new in August 2006 and has a carbon dioxide emission rating of 207 g/km. Daring Designs Limited paid for the petrol for all the mileage done by Rita until 5 December 2009.

On 5 December 2009, the company discontinued the company car scheme and sold the car to Rita for £5,000, its market value at that date. Her mileage from 6 April 2009 to 5 December 2009 was 20,000 of which 13,000 was on business.

Required:

Calculate the total amount chargeable to income tax as employment income on Rita for the year 2009/10. (11 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 7

INCOME FROM SELF EMPLOYMENT

5 WILLIAM OAKLEY

The following items have been charged against profit in the accounts of William Oakley, a shoe manufacturer, for the year ended 31 March 2010.

(1) In Repairs and Renewals an amount of £2,000 was included for the fitting of security bars over the factory windows as a precaution against theft.

(2) A loan of £100 to a former employee was written off.

(3) Gifts of ‘Oakley’ calendars in December 2009 costing £12 each.

(4) Incidental costs incurred in obtaining a bank loan, £350.

(5) A donation of five pairs of running shoes, costing a total of £200, when sponsoring a local charity raising money by organising a marathon.

(6) A lease rental of £4,000 per annum on a car with CO2 emissions of 180 grams per kilometre provided for a senior employee.

(7) Registering a patent for a new shoe design, £1,275.

(8) A parking fine of £100 incurred by an employee on a business trip to Manchester.

(9) Payment of £6,000 relocation expenses to a new employee.

(10) In Repairs and Renewals an amount of £2,000 to re-condition a second-hand stitching machine bought for £10,000. The repairs were necessary before the machine could be used in the business.

(11) Cost of a course in computer skills, costing £350, for William himself who had no previous computer experience.

Required: State how you would deal with each of the items when preparing the tax adjusted trading profit computation for the year ended 31 March 2010.

You should give a brief explanation for your treatment of each item. (11 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

8 KAPLAN PU BL ISH INGH

6 SEAN

Sean began his car repair business from a rented workshop on 1 May 2009. His trading profits, as adjusted for taxation, are expected to be:

£ Period to 30.9.10 91,742 Year ended 30.9.11 61,922 Year ended 30.9.12 25,419

Additions and sales were: £ 1.5.09

Additions of plant machinery 83,000

1.6.10

Car (no private use) with CO2 emissions of 143 grams per kilometre

11,000

1.11.10 Sale proceeds from plant and machinery (original cost £10000)

6,000

1.12.10 Additions of equipment 26,500

Required:

(a) Calculate the assessable amounts for the years 2009/10 to 2012/13 inclusive (7 marks)

(b) Calculate the ‘overlap’ profits. (1 mark)

(Total: 8 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 9

INCOME TAX – EMPLOYMENT AND SELF EMPLOYMENT

7 OLGA

On 1 May 2009 Olga, who is 26 years old, commenced in business working in the evenings as a self-employed musician. Her profits, as adjusted for income tax but before capital allowances, are estimated to be:

£1.5.09 – 30.6.10 (14 months) 26,250 1.7.10 – 30.6.11 (12 months) 40,065

Olga purchased recording equipment costing £3,000 on 17 October 2009 and £4800 on 30 November 2010. None of the assets are to be treated as ‘short-life’ assets. Olga used her car with CO2 emissions of 150 grams per kilometre, which was valued at £5,000 on 1 May 2009, in the business and estimated that 30% of her total mileage was for business purposes.

During the day Olga worked as a hairdresser and in 2009/10 earned a salary of £16,000, from which PAYE of £1,905 was deducted. She was in an occupational pension scheme into which she paid 6% of her salary. In 2009/10 Olga received bank interest of £100 (net).

In 2006 Olga’s employer lent her £50,000 to purchase her house which is her main residence. Interest was paid at 2% and there was no other loan on the property.

Required:

(a) Calculate Olga’s trading income assessments for the years 2009/10, 2010/11 and 2011/12. (8 marks)

(b) Calculate Olga’s ‘overlap’ profits. (1 mark)

(c) Calculate the income tax payable by Olga for 2009/10. (7 marks)

Assume the 2009/10 rates and allowances continue in the future and assume that the official rate of interest is 4.75%.

(Total: 16 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

10 KAPLAN PU BL ISH INGH

8 MR KAIKOURA

Mr Kaikoura began trading as a financial consultant on 1 September 2008 preparing accounts to 30 June annually. His recent tax adjusted trading profits are:

£ Period to 30 June 2009 39,400Year to 30 June 2010 47,800

Mr Kaikoura receives £4,140 of dividends each year from United Kingdom resident companies. He has no other source of income.

Mrs Kaikoura is a senior employee of Picton Ltd. She earns £35,000 per annum and is paid a bonus in May each year following the Directors’ Board meeting in March. Mrs Kaikoura received a bonus of £8,500 in 2009 and £9,000 in 2010. She pays 5% of her salary into the company’s registered occupational pension scheme.

Picton Ltd provides Mrs Kaikoura with a 3,300cc car which had a list price when new in January 2008 of £25,500. The car has a carbon dioxide emission rating of 257 g/km. Mrs Kaikoura contributed £6,000 towards the cost of the car.

In 2009/10 Mrs Kaikoura drove 11,000 miles of which 80% were private. Picton Ltd pays for all of the running costs of the car including all of the petrol used by Mrs Kaikoura. Mrs Kaikoura pays £50 per month towards the cost of the petrol used by her for private purposes.

Mrs Kaikoura purchased a wide-screen digital television from Picton Ltd on 30 June 2009 for £250. The television, which cost Picton Ltd £2,200 on 1 January 2008, has always been on loan to Mrs Kaikoura. It was worth £600 on 30 June 2009.

On 1 August 2009 Picton Ltd made a loan to Mrs Kaikoura of £25,000 which she used to build a swimming pool at her house. Interest is charged on the loan at 1% per annum payable monthly in arrears and the loan is due to be repaid in 2012.

Mrs Kaikoura paid PAYE of £12,000 and received bank interest of £442 in 2009/10.

The official rate of interest in 2009/10 is 4.75%.

Required:

(a) Calculate the income tax payable by Mr Kaikoura for 2009/10 and state the overlap profits arising on the commencement of the business. (9 marks)

(b) Calculate the income tax payable by Mrs Kaikoura for 2009/10. (16 marks)

(Total: 25 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 11

9 CHALK AND CHEESE

Alice Chalk and Zara Cheese, aged 37, are twin sisters. Although having the same levels of earned and investment income, they are surprised that their total income tax and NIC liabilities for 2009/10 are not the same.

The following information is available for 2009/10:

Alice Chalk

(1) Alice is employed by Tesbury plc as a manager in one of the company’s nationwide chain of retail grocery shops. She is paid a gross annual salary of £43,000.

(2) Throughout 2009/10 Alice was provided with an 1800cc petrol powered motor car which has a list price of £14,600. Alice made a capital contribution of £2,000 towards the cost of the motor car when it was first provided. The official CO2 emission rate for the motor car is 197 grams per kilometre. Tesbury plc paid for all of the motor car’s running costs of £5,400 during 2009/10, including petrol used for private journeys.

(3) Tesbury plc has provided Alice with living accommodation since 2008. The property was purchased in 2004 for £105,000, and was valued at £120,000 when first provided to Alice. It has an annual value of £3,895, and Tesbury plc pays for the annual running costs of £3,200.

(4) Alice contributes 6% of her gross salary of £43,000 into Tesbury plc’s HM Revenue & Customs registered occupational pension scheme.

(5) During 2009/10 Alice received building society interest of £1,800 (net).

Zara Cheese

(1) Zara is self-employed running a retail grocery shop. Her profit and loss account for the year ended 5 April 2010 is as follows: £ £

Gross profit 123,105 Depreciation 12,425 Motor expenses (note 2) 5,400 Property expenses (note 3) 9,600 Other expenses (all allowable) 52,680 ––––––– (80,105) ––––––– Net profit 43,000 –––––––

(2) During the year ended 5 April 2010 Zara drove a total of 12,000 miles, of which 3,000 were for private journeys. Zara’s motor car originally cost £12,600, and at 6 April 2009 had a tax written down value of £9,600. She does not own any other assets that qualify for capital allowances.

(3) Zara purchased her grocery shop in 2002 for £105,000. She lives in a flat that is situated above the shop, and one-third of the total property expenses of £9,600 relate to this flat.

(4) Zara contributed £2,800 (gross) into a personal pension scheme during 2009/10.

(5) During 2009/10 Zara received dividends of £1,800 (net).

PAPER F6 : TAXAT IO N (FA 2009 )

12 KAPLAN PU BL ISH INGH

Required:

(i) Calculate Alice’s liability to income tax and Class 1 NIC for 2009/10. (11 marks)

(ii) Calculate Zara’s liability to income tax, Class 2 NIC and Class 4 NIC for 2009/10. (10 marks)

(Total: 21 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 13

RELIEF FOR TRADING LOSSES

10 SIMON

Simon began trading on 1 January 2007. He prepares accounts to 31 December annually, with results as follows:

Trading profit/(loss) £

Year ended 31 December 2007 Loss (12,000) Year ended 31 December 2008 Loss (4,000) Year ended 31 December 2009 Profit 8,000 Year ended 31 December 2010 Profit (estimated) 11,500

Details of the amounts of other income for the years 2003/04 to 2006/07 were as follows:

Salary from employment Gross interest received £ £ 2003/04 10,000 200 2004/05 13,200 800 2005/06 9,800 1,300 2006/07 3,300 200 From 1 January 2007 the business is Simon's only source of income.

Simon wishes to obtain relief for his initial trading losses as soon as possible.

Required:

(a) Calculate the trading income assessments for 2006/07 to 2010/11 assuming all losses are carried forward and offset under s83 ITA 2007. (7 marks)

(b) Show how the losses incurred in the first two years of trading are to be relieved so as to provide relief as early as possible. (9 marks)

(c) If a trading loss were to arise in tax year 2009/10 for a continuing business, explain the loss reliefs available to a taxpayer. (4 marks)

(Total: 20 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

14 KAPLAN PU BL ISH INGH

11 MR TAPAWERA

Mr Tapawera transferred his business to Atapo Ltd on 31 March 2010 wholly in exchange for shares. He is now the Managing Director of Atapo Ltd and is paid a salary of £18,000 per annum.

The tax adjusted trading profits/(loss) of the business up to cessation have been:

£ Year to 31 March 2007 8,000 Year to 31 March 2008 11,000 Year to 31 March 2009 9,000 Year to 31 March 2010 (7,000)

There are unrelieved overlap profits of £3,700.

In January 2010 Mr Tapawera sold an investment property which he had inherited on the death of his grandfather in March 2007. The chargeable gain on the property was £56,300.

Mr Tapawera’s only other source of income is bank interest received of £1,840 each year. He had been unable to find a tenant for the investment property and had therefore received no rental income.

Required:

(a) Explain the relief that is available when a business is transferred to a company whereby accumulated trading losses of the business can be offset against income derived from the company and state the conditions which must be satisfied. (4 marks)

(b) Explain the implications of Mr Tapawera making a terminal loss claim. You are not required to produce detailed calculations. (4 marks)

(c) Explain the other reliefs available to Mr Tapawera in respect of the loss made in the year ended 31 March 2010. You are not required to produce detailed calculations.

(4 marks)

(d) Explain, with reasons, the relief which Mr Tapawera should claim in respect of the loss of the year ended 31 March 2010. (3 marks)

(Total: 15 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 15

PARTNERSHIPS

12 DOMINIC AND JUSTIN

Dominic and Justin commenced in partnership on 1 July 2007 and decided to produce their accounts to 30 June annually. On 1 January 2009, Simon joined the partnership. The partnership’s accounts show the following adjusted trading profits:

£ Year ended 30 June 2008 10,000Year ended 30 June 2009 13,500Year ended 30 June 2010 18,000

Required: Show the amounts assessable on the individual partners for all the years affected by the above information, assuming that profits are shared equally.

State the amount of overlap relief for each partner. (11 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

16 KAPLAN PU BL ISH INGH

13 CHARLIE, JULIETTE AND MIKE

Charlie, Juliette and Mike are interior design consultants and have been in partnership since 1 October 1997 trading as CJM Designs. They prepare annual accounts to 30 September.

Details of their profit-sharing arrangements, which were changed on 31 March 2009 are:

to 31 March 2009

from 1 April 2009

Interest on fixed capital 5% 4% Partner’s annual salary Charlie £6,000 None Profit-sharing ratio Charlie 1/5 Charlie 1/3 Juliette 2/5 Juliette 1/3 Mike 2/5 Mike 1/3

Fixed capital accounts have remained unchanged since 1997 and are:

£ Charlie 12,000Juliette 16,000Mike 18,000

In the year ended 30 September 2009 the partnership sustained its first ever trading loss, as adjusted for income tax, of £40,000. All partners have sufficient other income to absorb any trading losses and wish to utilise their share of the loss in this manner rather than carry it forward.

Required:

Calculate the amount of each partner’s share of the trading loss sustained in the year to 30 September 2009. (8 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 17

PENSIONS AND NIC FOR EMPLOYEES

14 INGRID

Ingrid, who is not contracted out of the state second pension scheme, receives an annual salary of £44,600 and is also provided with a company car by her employer. Until 5 November 2009 she had a 1700cc petrol-engined car which had been first registered on 1 August 2006 with a list price of £11,000 and a CO2 rating of 212 gms/km. On 6 November 2009 the car was exchanged for a new 2200cc diesel-engined car with a list price of £16,500 and a CO2 rating of 226 gms/km. Ingrid was provided with fuel for both cars for both business and private motoring. Required: Calculate the National Insurance contributions payable by Ingrid and her employer for the year 2009/10. (11 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

18 KAPLAN PU BL ISH INGH

15 FREDA

Freda has the following income in 2009/10. £ Trading income 80,000 Employment income (part time) 10,000 Interest income (gross) 500 Property business income 50,000

She has not previously made any provision for retirement and in 2009/10 she decided to contribute the maximum contribution into a personal pension scheme for which she would obtain tax relief.

Required:

(a) Calculate the amount of the pension contribution that Freda paid into her personal pension scheme in 2009/10. (8 marks)

(b) Calculate Freda’s income tax liability for 2009/10. (5 marks) (Total: 13 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 19

SELF-ASSESSMENT AND PAYE

16 RETURNS AND PAYMENTS

Required: (a) State the latest date by which the taxpayer should submit his 2009/10 income tax

return if:

(i) he wishes to submit a paper return;

(ii) he wishes to submit an electronic return. (2 marks)

(b) State:

(i) the normal dates of payment of income tax for a taxpayer with income received gross in respect of the tax year 2009/10;

(ii) how the amounts of these payments are arrived at. (5 marks)

(c) State:

(i) the fixed penalties for late submission of tax returns and when they apply;

(ii) the circumstances under which the penalties will be reduced;

(iii) the further penalties which may be imposed when HM Revenue & Customs believes that the fixed penalties will not result in the submission of the return.

(iv) the penalties due for the submission of an incorrect return

(v) the regime of HMRC information and inspection powers.

(8 marks)

(Total: 15 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

20 KAPLAN PU BL ISH INGH

17 VERA OLD

Vera Old has been a self-employed antiques dealer since 1999. Her tax liabilities for 2008/09 and 2009/10 are as follows:

2008/09 2009/10 £ £

Income tax liability 8,240 4,770 Tax suffered at source (810) (640) –––––– –––––– Income tax payable 7,430 4,130 Class 4 national insurance contributions 1,660 1,230 –––––– –––––– 9,090 5,360 Capital gains tax liability 1,820 700 –––––– –––––– 10,910 6,060 –––––– ––––––

Required:

(a) Assuming that Vera does not make a claim to reduce the payments on account, prepare a schedule of her payments on account and balancing payment or repayment for 2009/10.

Your answer should show the relevant due dates of each payment/repayment. (3 marks)

(b) (i) Advise Vera of the claim that she should make to reduce her payments on account for 2009/10. (2 marks)

(ii) State the implications if Vera were to instead make a claim to reduce her payments on account for 2009/10 to nil. (2 marks)

(c) Advise Vera of the latest date by which her self-assessment tax return for 2009/10 should be submitted, and the implications if it is submitted three months late. (3 marks)

(d) (i) Assuming that her self-assessment tax return for 2009/10 is submitted on 15 December 2010, state the date by which HM Revenue & Customs will have to notify Vera if it intends to enquire into the return, and the possible reasons why such an enquiry would be made. (3 marks)

(ii) State the circumstances in which HM Revenue & Customs would be entitled to raise a discovery assessment in respect of Vera’s self-assessment tax return for 2009/10, and the time limit for making such an assessment. (2 marks)

(Total: 15 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 21

18 PAYE

Required: Describe the PAYE (Pay As You Earn) system of tax collection and briefly explain its operation. Your explanation should include a short description of the end of tax year procedures and a brief account of the action taken when a taxpayer changes jobs. (11 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

22 KAPLAN PU BL ISH INGH

CHARGEABLE GAINS

19 SARAH

Sarah made the following disposals in 2009/10.

(a) On 9 June 2009 she sold an antique organ for £13,000. She had bought it in October 1989 for £8,000.

(b) On 5 September 2009 she sold a painting at an auction. The painting cost £7,500 in November 1990 and the sale proceeds received were £5800 from which Sarah had to pay £60 auctioneer’s fees

(c) On 1 March 2010 she sold a car, which she had bought in February 1984 for £3,000. By the time she sold it, it had become a collector’s item and Sarah managed to obtain proceeds of £9,000, out of which she paid £450 in auctioneer’s fees.

(d) On 5 December 2009 she sold part of her interest in a piece of investment land for £30,000. The original land cost £10,000 in August 1987. The market value of the remaining land at the date of sale was £40,000.

(e) She sold her principal private residence during the year realising a gain of £50,000. The residence was acquired in 2002 and has been used throughout her period of ownership 20% for business use.

Sarah has capital losses brought forward from 2007/08 of £1,420

Required:

Calculate Sarah’s capital gains tax payable for 2009/10 and state the due date for payment.

. (12 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 23

20 COLUMBUS AND MARCO

(a) Columbus sold one of his factories on 30 April 2009 for £900,000. The factory had been purchased in September 1983 for £300,000. In March 2010 Columbus purchased another factory for £700,000 and claimed rollover relief on the gain on the factory sold in April 2009.

Required: Calculate the chargeable gain on the sale of the first factory, the amount of any

rollover relief available and the base cost of the second factory.

Assume Entrepreneurs’ relief is not available. (5 marks)

(b) Marco who has a dry-cleaning business, purchased a building for business use in June 1983 for £50,000. In September 2009 he sold the building for £150,000. Marco had purchased a replacement building to carry on his business in December 2008 for £130,000.

Marco claimed any available reliefs. (5 marks)

Required: Calculate the chargeable gain arising on the sale of the first building, how much of the

gain can be rolled over and the base cost of the replacement building.

(Total: 10 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

24 KAPLAN PU BL ISH INGH

21 NUI LEE

For the purposes of this question you should assume that today’s date is 15 March 2010. Nui Lee has been in business as a sole trader since 1 January 1995. On 5 April 2010 she is going to sell her business for £300,000 to an unconnected person. The following information is available: (1) Nui has tax adjusted trading profits of £65,800 for the year ended 31 December 2009,

and will have profits of £29,700 for the period from 1 January to 5 April 2010. These figures are before taking account of capital allowances.

(2) The tax written down value of the general pool at 1 January 2009 is £45,600. (3) Nui has unused overlap profits brought forward of £5,900. (4) The sale proceeds figure of £300,000 is made up as follows:

£ Goodwill 60,000 Freehold property 165,000 Plant and machinery 30,000 Net current assets 45,000 ––––––– 300,000 –––––––

The goodwill has been built up since 1 January 1995, and has a nil cost. The freehold property cost £110,000 on 10 August 2008. All items of plant and machinery have qualified for capital allowances, and are being sold for less than original cost.

(5) Nui and the purchaser of her business are both registered for VAT. (6) Nui understands that it may be beneficial to postpone the sale of her business by one

day until 6 April 2010. A postponement would not alter the sale proceeds figure of £300,000, and the tax adjusted trading profit of £29,700 would remain unchanged for the period from 1 January to 6 April 2010.

Required:

(a) Calculate Nui’s trading income assessment for 2009/10. You should prepare separate capital allowance computations for each period of account. (5 marks)

(b) Calculate the chargeable gains that Nui will be assessed on for 2009/10. You should ignore the annual exemption. (4 marks)

(c) Explain the VAT implications arising from the sale of Nui’s business. (3 marks) (d) Briefly advise Nui of the income tax and CGT implications of postponing the sale of

her business until 6 April 2010. (3 marks) (Total: 15 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 25

22 OSKAR BARNACK

(a) On 31 July 2009, his 46th birthday, Oskar Barnack gifted his 10% ordinary shareholding in European Traders Ltd to his daughter, Felicity. Oskar does not work for the company, and never has.

The agreed market value of the shares on 31 July 2009 was £550,000. Oskar inherited the shares on 1 August 1995 at a valuation of £125,000. Oskar and Felicity elected to hold over the gain.

The market values of the assets of the company at 31 July 2009 were: £ Land and buildings 700,000Shares held as an investment 200,000Stock 160,000Bank and cash balances 25,000Government securities 220,000

Required: Calculate Oskar’s chargeable gain for 2009/10 before the annual exemption, and the

base cost of the shares acquired by Felicity.

Note that Entrepreneurs’ relief is not available. (6 marks)

(b) Walter purchased his business premises in October 1985 for £10,000. In May 2006 he gave them to his son Darren when the value was £50,000. The appropriate joint election for gift relief was made. On 12 April 2009 Darren sold the premises for £200,000. The disposal is not part of the disposal of the entire business.

Required: Calculate the chargeable gain assessable on Darren for 2009/10, before the annual

exemption. (5 marks)

(c) Ada sold a necklace for £25,000 on 1 March 2010. The necklace had been given to her by her husband on 6 April 2008 when its market value was £20,000. Ada’s husband had purchased the necklace for £8,000 on 1 June 1999.

Required: Calculate the chargeable gain assessable on Ada for 2009/10, before the annual

exemption. (5 marks)

(Total: 15 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

26 KAPLAN PU BL ISH INGH

CORPORATION TAX

CORPORATION TAX BASICS AND ADMINISTRATION

23 UNFORGETTABLE UNITS LTD

Unforgettable Units Limited is a UK resident company which manufactures self-assembly furniture. It has no associated companies and has always prepared accounts to 31 March.

In the year ended 31 March 2010 the company’s profit was £802,000 which was arrived at after charging and crediting the following items:

Expenditure: £ Patent royalties (gross) (note 1) 58,000Legal expenses (note 2) 10,000Impaired debts (note 3) 42,000 Income: Loan note interest (note 4) 64,000Bank interest (note 5) 5,000Dividend (note 6) 10,000

Notes:

(1) Patent royalties payable (gross amounts)

£ 30 November 2009 paid 20,00028 February 2010 paid 25,00031 March 2010 accrued 13,000 58,000

The payments were made three monthly in arrears without deduction of income tax. The royalties are paid for a trading purpose in respect of rights commencing on 1 September 2009.

(2) Legal expenses incurred were:

Fine for not fitting saws with protective guards £10,000 (3) Impaired debts account

£ £ Trading debts written off in year 20,000 Allowance for trade

debtors at 1.4.09 97,000 Loan to former employee written off 3,000

Recovery of trading debt previously written off 11,000

Allowance for trade debtors at 31.3.10 127,000

Profit and Loss Account 42,000

150,000 150,000

(4) Loan note interest receivable

£ £ 1.4.09 b/f 25,000 30.4.09 received 29,000Profit and Loss Account 64,000 31.10.09 received 32,000 31.3.10 c/f 28,000 89,000 89,000

The interest was non-trading income.

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 27

(5) Bank interest

The £5,000 was credited to the company’s bank account on 31 March 2010.

(6) Dividends received

On 1 July 2009 Unforgettable Units Limited received a dividend from another UK company of £10,000. This amount represents the actual amount received without any adjustment for tax credits.

(7) Plant and Machinery

On 1 April 2009 the tax written down value of the plant pool was £100,000.

New machinery, which is not to be treated either as a ‘short-life’ asset, costing £35,000 was purchased on 31 August 2009. On 1 October 2009 a car was sold for £2,000 which formed part of the general pool and replaced with one costing £13,000 (CO2 emissions of 170 grams per kilometre).

Required:

Calculate the corporation tax liability of Unforgettable Units Limited for the year ended 31 March 2009.

You should give reasons for your treatment of the legal expenses in Note 2.

Note: All apportionments should be made in months. (28 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

28 KAPLAN PU BL ISH INGH

24 UNSEEN ULTRASONICS LTD

Unseen Ultrasonics Ltd is a UK resident company which manufactures accessories for telecommunication systems. It has no associated companies. The company’s results for the year ended 31 March 2010 were as follows:

£ Trading profits (as adjusted for taxation but before capital allowances) (note 1) 2,300,000 Dividends received from overseas companies (note 2) 60,000 Bank interest receivable 1,500 Chargeable gains 25,000 Loan note interest received (gross amount) 80,000 Gift Aid payment to a national charity 5,000

The loan note interest received is the same as the amount credited in the accounts on an accruals basis.

The company has traded in a purpose-built unit since 1 January 1998. The total cost of the unit was made up as follows:

On 1 April 2009 the tax written down values of plant and machinery were: £ General pool 190,000 Short-life asset 4,000

The short-life asset was purchased on 1 December 2004 and sold on 31 October 2009 for £9,000. On 1 November 2009 a new car (with CO2 emissions of 150 g/km) costing £18,000 was purchased for the managing director. The car previously used by him had cost £10,000 in July 2007 and was sold for £8,000. A new precision engineering machine was purchased on 1 August 2009 for £112,500 Notes (1) In arriving at the adjusted trading profit an adjustment had been made for small

capital additions acquired in April and May 2009 totalling £8,750 which the company had written off as repairs but which have been added back for tax purposes.

(2) The company had received the following dividend from an overseas company in which it owned 15% of the share capital.

31 May 2009 £60,000

(3) On 1 April 2009 the company had capital losses brought forward of £30,000.

(4) On 1 April 2009 the company had trading losses brought forward of £567,750.

(5) The Gift Aid payment was made in March 2010.

Required: Calculate the corporation tax liability for the year ended 31 March 2010 and state how any unrelieved amounts are to be dealt with. (16 marks)

£ Freehold land 50,000 Manufacturing area 240,000 Canteen 30,000 Design office 90,000 General office 130,000 __________ 540,000 __________

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 29

25 UNBEATABLE UNDERCARRIAGES LTD

Unbeatable Undercarriages Ltd is a UK resident company which has been trading for many years and manufactures aircraft components. It has no associated companies. The company had always prepared accounts to 31 March but decided to change its accounting date to 31 December.

The company’s results for the nine months ended 31 December 2009 are as follows: £ Trading profits (as adjusted for taxation but before capital allowances and loan interest) 1,200,000 Payment to a national charity (gross amount) (notes 4 and 7) 5,000 Loan interest payable on trade loan (gross amount) (notes 5 and 7) 10,000 Bank interest receivable (note 6) 7,000 Dividends received from UK companies 56,250

Notes

(1) On 1 April 2009 the tax written down values of plant and machinery were: £ General pool 105,000Short-life asset (purchased 1.6.06) 4,000

On 1 August 2009 a car which had cost £10,000, and so was part of the general pool,

was sold for £7,000 and replaced by one costing £14,000 with CO2 emissions of 180 g/km. The short-life asset was sold on 1 July 2009 for £1,920.

(2) The company had purchased a warehouse on 1 July 2001 for £200,000 (including land of £20,000). On 31 May 2009 the warehouse was sold for £397,200 (including land of £30,000). An indexation factor of 0.249 applies. The company did not replace the warehouse.

(3) On 1 April 2009 the company had trading losses brought forward of £300,000.

(4) The payment to charity was made on 1 June 2009.

(5) Included in the figure of £10,000 for loan interest payable is a closing accrual of £2,000. The £8,000 was paid on 1 July 2009. The loan was taken out in 2009.

(6) Included in the figure of £7,000 for bank interest receivable is a closing accrual of £2,440. The £4,560 was received on 30 September 2009. The bank account was opened in 2009.

(7) The gross amount of loan interest payable is shown. The payment to charity was made gross and is relievable under the Gift Aid rules.

Required: Calculate the corporation tax liability for the accounting period to 31 December 2009.

(17 marks)

Note: All apportionments may be made to the nearest month.

PAPER F6 : TAXAT IO N (FA 2009 )

30 KAPLAN PU BL ISH INGH

26 UNFORESEEN UPSETS LTD

Unforeseen Upsets Limited (UUL) is a UK resident company which has been manufacturing lifeboats for many years. It has no associated companies. The company has previously prepared its accounts to 31 March but has now changed its accounting date to 30 June.

The company’s results for the 15 month period to 30 June 2010 are as follows:

£ Trading profits (as adjusted for taxation but before capital allowances) 1,125,000 Bank interest receivable (Note 3) 20,000 Loan note interest receivable (Note 4) 17,500 Chargeable gain (Notes 5 and 6) 30,000 Dividends received from UK companies (Note 7) 36,300

Notes

(1) Capital allowances – Plant and Machinery

On 1 April 2009 the tax written-down value of plant and machinery was £142,000:

Sales during the accounting period were: £ 31.10.09 3 cars (originally forming part of the general pool) 15,000 31.12.09 Plant and machinery 12,000

Additions during the accounting period were:

1.9.09 1 car (CO2 emissions of 190 g/km) 14,000 1.11.09 3 cars (£8,000 each) (CO2 emissions of 130 g/km) 24,000 28.2.10 Plant and machinery 92,000 31.5.10 Plant and machinery 12,000

(2) On 1 April 2009 the company had trading losses brought forward of £609,200.

(3) Bank interest receivable £ 30.6.09 received 3,000 30.9.09 received 4,000 31.12.09 received 5,000 31.3.10 received 6,000 30.6.10 received 2,000 ––––– 20,000 –––––

(4) Loan note interest receivable £ 30.6.09 received 3,500 31.12.09 received 7,000 30.6.10 received 7,000 ––––– 17,500 ––––– (a) The loan was made on 1 April 2009.

(b) Interest of £3,500 was accrued at 31 March 2010.

(c) The interest was non-trading income.

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 31

(5) Chargeable gain

The chargeable gain was realised on 1 October 2009.

(6) On 1 April 2009 the company had capital losses brought forward of £50,000.

(7) Dividends received £ 31.5.09 18,000 31.10.09 12,000 31.5.10 6,300 –––––– 36,300 ––––––

Required:

(a) Calculate the corporation tax liabilities for the 15-month period of account and state the due dates for payment and the filing date. (18 marks)

(b) State what unrelieved amounts are carried forward at 30 June 2010. (1 mark)

(Total: 19 marks)

Note: All apportionments should be made to the nearest month.

Assume that the FY2009 rates continue in the future.

PAPER F6 : TAXAT IO N (FA 2009 )

32 KAPLAN PU BL ISH INGH

RELIEF FOR TRADING LOSSES

27 UNCUT UNDERGROWTH LTD

Uncut Undergrowth Limited is a UK resident company which has been manufacturing garden machinery since 1990. It has no associated companies and is wholly owned by Mr and Mrs Weed.

The company results are summarised as follows:

Year ended 31.12.06 31.12.07 31.12.08 31.12.09 31.12.10 (forecast) £ £ £ £ £

Trading Profit/(Loss) 100,000 30,000 (35,000) (362,500) 87,000Loan interest received – – 15,000 22,000 –Bank interest received 20,000 – – – 10,000Property business income – 20,000 – – –Chargeable gains – – – 30,000 –Gift Aid payments (gross amount)

1,000 1,000 1,000 1,000 1,000

Notes (1) On 1 January 2006 there were no trading losses brought forward but £40,000 of

capital losses were available. (2) Non-trade loan interest was received on the following dates:

£ 31.12.08 15,000 31.12.09 22,000

(3) Gift Aid payments were made on the following dates: £ 31.12.06 1,000 31.12.07 1,000 31.12.08 1,000 31.12.09 1,000 31.12.10 (forecast) 1,000

Required:

(a) Calculate the profits chargeable to corporation tax for all years in the question after giving maximum relief at the earliest time for the trading losses sustained and any other reliefs (10 marks)

(b) Show any balances carried forward (5 marks)

(Total: 15 marks) Note: All apportionments may be made to the nearest month.

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 33

28 SPACIOUS LTD

Spacious Ltd is a UK resident company that commenced trading on 1 July 2008 as a manufacturer of engineering equipment. The company’s summarised profit and loss account for the year ended 31 March 2010 is as follows: £ £ Gross profit 113,640 Operating expenses

Impaired debts (Note 1) 12,460 Depreciation 54,690 Patent royalties (Note 2) 6,800 Professional fees (Note 3) 22,500 Repairs and renewals (Note 4) 27,700 Other expenses (Note 5) 149,490

––––––– (273,640) –––––––Operating loss (160,000) Profit from sale of fixed assets

Disposal of office building (Note 6) 54,400 Income from investments Bank interest (Note 7) 7,000

––––––– (98,600) Interest payable (Note 8) (23,000) –––––––Loss before taxation (121,600) –––––––

Note 1 Impaired debts Impaired debts are as follows: £

Trade debts written off 8,490 Increase in allowance for trade debtors 3,970

–––––– 12,460 ––––––Note 2 Patent royalties

Patent royalties of £2,900 were paid on 30 September 2009, with a further £3,900 being paid on 31 March 2010.

These relate to the year ended 31 March 2010.

Note 3 Professional fees

Professional fees are as follows: £

Accountancy and audit fee 6,100 Legal fees in connection with the issue of share capital 6,200 Legal fees in connection with the issue of loan notes (see Note 8) 7,000 Legal fees in connection with the defence of the company’s internet domain name

2,300

Legal fees in connection with a court action for not complying with health and safety legislation

900

––––––22,500

––––––

PAPER F6 : TAXAT IO N (FA 2009 )

34 KAPLAN PU BL ISH INGH

Note 4 Repairs and renewals

The figure of £27,700 for repairs includes £9,700 for constructing a new wall around the company’s premises and £5,400 for replacing the roof of a warehouse because it was in a bad state of repair.

Note 5 Other expenses

Other expenses include £1,800 for entertaining customers, £600 for entertaining employees and a donation of £1,000 made to a national charity under the Gift Aid scheme.

Note 6 Disposal of office building

The profit of £54,400 is in respect of a freehold office building that was sold on 30 June 2009 for £380,000. The indexed cost of the building on 30 June 2009 was £345,400. The building has always been used by Spacious Ltd for trading purposes. The company has claimed to roll over the gain arising on the office building against the cost of a new factory that was purchased on 1 July 2009 for £360,000 (see Note 9). The new factory is used 100% for trading purposes by Spacious Ltd.

Note 7 Bank interest received

The bank interest was received on 31 March 2010. The bank deposits are held for non-trading purposes.

Note 8 Interest payable

Spacious Ltd raised a loan note on 1 October 2009, and this was used for trading purposes. Interest of £23,000 in respect of the first six months of the loan was paid on 31 March 2010.

Note 9 Industrial building

Spacious Ltd purchased a new factory from a builder on 1 July 2009 for £360,000 and this was immediately brought into use. The figure of £360,000 includes £135,000 for land, £61,500 for general offices and £54,000 for a drawing office.

Note 10 Long-life asset

On 1 September 2009 Spacious Ltd installed a new overhead crane, costing £110,000, in the new factory. The crane is a long-life asset.

Note 11 Plant and machinery

On 1 April 2009 the tax written down values of plant and machinery were as follows:

£ General pool 28,400 Expensive motor car 14,800 The following transactions took place during the year ended 31 March 2010:

Cost/(Proceeds) £

10 April 2009 Purchased equipment 26,300 17 May 2009 Purchased a computer 3,100 18 May 2009 Purchased computer software 800 5 February 2010 Sold the expensive motor car (9,800) 5 February 2010 Purchased a motor car 13,600 20 March 2010 Sold a lorry (17,600) 31 March 2010 Purchased a motor car 9,400

The lorry sold on 20 March 2010 for £17,600 originally cost £18,200. The motor car purchased on 5 February 2010 has CO2 emissions of 175 g/km and the motor car purchased on 31 March 2010 for £9,400 has CO2 emissions of 145 g/km. It is used by the sales manager, and 20% of the mileage is for private journeys.

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 35

Note 12 Other information

Spacious Ltd has no associated companies.

The company’s results for the nine-month period ended 31 March 2009 were as follows:

£ Trading profit 183,200 Interest income 5,200 Capital loss (4,900) Donation to charity – Gift Aid (800)

Spacious Ltd’s profits chargeable to corporation tax for the year ended 31 March 2011 are expected to be £575,000, of which £550,000 represents trading profit.

Required:

(a) Calculate Spacious Ltd’s trading loss for the year ended 31 March 2010.

Your answer should commence with the loss before taxation figure of £121,600.

You should assume that the company claims the maximum available capital allowances. (20 marks)

(b) Assuming that Spacious Ltd claims relief for its trading loss against total profits under s393A ICTA 1988, calculate the company’s profits chargeable to corporation tax for the nine-month period ended 31 March 2009 and the year ended 31 March 2010. (7 marks)

(c) Explain why it would probably have been beneficial for Spacious Ltd to have carried its trading loss forward under s393(1) ICTA 1988, rather than making the claim against total profits under s393A ICTA 1988. (3 marks)

(Total: 30 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

36 KAPLAN PU BL ISH INGH

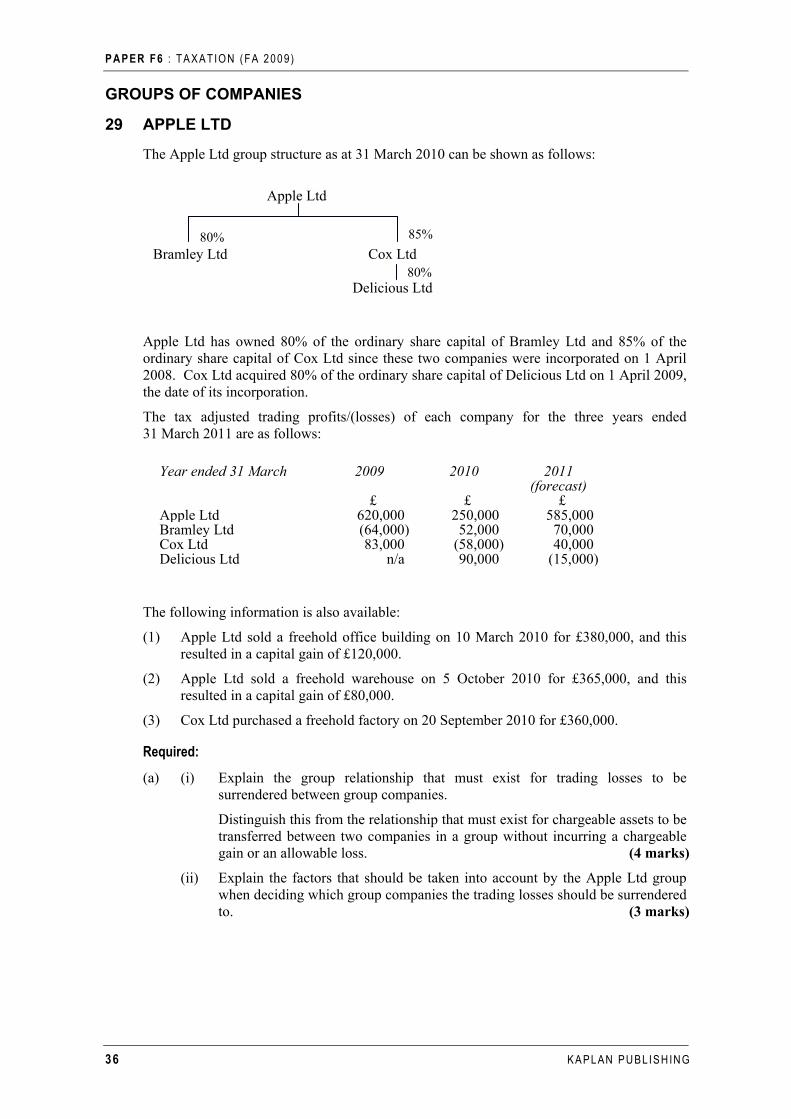

80% 85%

80%

GROUPS OF COMPANIES

29 APPLE LTD

The Apple Ltd group structure as at 31 March 2010 can be shown as follows: Apple Ltd

Bramley Ltd Cox Ltd Delicious Ltd

Apple Ltd has owned 80% of the ordinary share capital of Bramley Ltd and 85% of the ordinary share capital of Cox Ltd since these two companies were incorporated on 1 April 2008. Cox Ltd acquired 80% of the ordinary share capital of Delicious Ltd on 1 April 2009, the date of its incorporation.

The tax adjusted trading profits/(losses) of each company for the three years ended 31 March 2011 are as follows:

Year ended 31 March 2009 2010 2011 (forecast) £ £ £ Apple Ltd 620,000 250,000 585,000 Bramley Ltd (64,000) 52,000 70,000 Cox Ltd 83,000 (58,000) 40,000 Delicious Ltd n/a 90,000 (15,000)

The following information is also available:

(1) Apple Ltd sold a freehold office building on 10 March 2010 for £380,000, and this resulted in a capital gain of £120,000.

(2) Apple Ltd sold a freehold warehouse on 5 October 2010 for £365,000, and this resulted in a capital gain of £80,000.

(3) Cox Ltd purchased a freehold factory on 20 September 2010 for £360,000.

Required:

(a) (i) Explain the group relationship that must exist for trading losses to be surrendered between group companies.

Distinguish this from the relationship that must exist for chargeable assets to be transferred between two companies in a group without incurring a chargeable gain or an allowable loss. (4 marks)

(ii) Explain the factors that should be taken into account by the Apple Ltd group when deciding which group companies the trading losses should be surrendered to. (3 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 37

(b) (i) Calculate the profits chargeable to corporation tax for each of the companies in the Apple Ltd group for each of the three years concerned assuming that reliefs are claimed as efficiently as possible.

Ignore the possibility of claiming for a deemed transfer of assets between group companies prior to a sale to a third party. (8 marks)

(ii) Give an explanation of why you have chosen the reliefs as applied above in (b)(i). (4 marks)

(Total: 19 marks)

Assume that the FY2009 corporation tax rates continue in the future.

PAPER F6 : TAXAT IO N (FA 2009 )

38 KAPLAN PU BL ISH INGH

30 TAHUNA LTD

(a) Tahuna Ltd commenced to trade as a manufacturer of outside furniture on 1 June 2009.

In the seven months ended 31 December 2009 Tahuna Ltd made an adjusted trading profit of £235,000, before capital allowances and before accounting for the following:

(1) On 1 May 2009 Tahuna Ltd incurred legal fees on setting up the company of £500

(2) On 15 May 2009 the company paid £1,200 to an advertising company in respect of a market research report that they had prepared for the company.

The following information is also relevant to the company’s results for the seven month period:

Note 1 – Capital additions and disposals

During the period Tahuna Ltd had the following additions and disposals:

Additions £ 1 May 2009 Car (CO2 emissions are 180 g/km) 20,000 2 May 2009 Car (CO2 emissions are 130 g/km) 10,000 1 June 2009 Plant and machinery 50,000 Disposals 1 December 2009 Plant (sold for less than cost) 5,000

Private use of each of the cars by directors of the company was 25%.

Note 2 – Purchase of factory

Tahuna Ltd acquired a new factory on 1 June 2009 for £250,000 which it brought into industrial use immediately. The cost of the new factory may be analysed as follows:

£ Land 25,000 Land preparation 5,000 Professional fees 7,000 Air conditioning system 8,000 Drawing office 10,000 Administration area 35,000 Factory 160,000 ––––––– 250,000 ––––––– Note 3 – Other income and expenditure

(1) Tahuna Ltd received bank interest of £6,000 on 30 November 2009. Interest receivable at 31 December 2009 was £500.

(2) From 1 June 2009 the company rented out an office building that it owned as an investment property for £1,500 per month, payable quarterly in advance. Interest payable for the seven month period in respect of a loan taken out to acquire the property was £4,000. It also incurred redecorating costs of £2,000 and other allowable costs of £800 during the period.

Required:

Calculate Tahuna Ltd’s profits chargeable to corporation tax for the seven months to 31 December 2009. (10 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 39

(b) Hakatere Ltd is a manufacturing company which prepares accounts to 31 March. Its profits chargeable to corporation tax in the last few years have been approximately £1,700,000 per annum. It is about to start a new venture which will generate further profits of £200,000 per annum.

Required: Advise Hakatere Ltd, with the aid of supporting calculations and with the objective of minimising corporation tax, whether the new venture should be operated by the company itself or by a new subsidiary formed specifically for the purpose. (6 marks)

(c) Kaniere Ltd is a trading company which, after a number of profitable years, has recently made a small loss due to economic changes which have affected its markets. It anticipates that it will continue to make losses for a number of years and is considering acquiring 50% or more of Ikamatua Ltd, a profitable company.

Required:

Explain whether trading losses and capital losses of Kaniere Ltd can be utilised by Ikamatua Ltd.

You should consider both brought forward losses and current year losses. (6 marks)

(d) Tinwald Ltd has owned 100% of Mayfield Ltd and Peel Ltd for a number of years.

During the year ended 31 March 2010, Peel Ltd made a tax adjusted trading loss of £70,000 and a capital gain of £28,000. The profits chargeable to corporation tax of Tinwald Ltd and Mayfield Ltd in the same period were £620,000 and £140,000.

Required:

State concisely the manner in which the loss of Peel Ltd should be used. (3 marks) (Total: 25 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

40 KAPLAN PU BL ISH INGH

VALUE ADDED TAX

31 OCTAVIUS

You are provided with the following information relating to Octavius for the quarter ended 31 March 2010: (1) The VAT-exclusive management accounts:

£ £ Sales 16,500 Sales returns (1,100) –––––– 15,400 Purchases 9,600 Purchases returns (300) ––––– 9,300 Impaired debts written off 1,500 Other expenses 2,400 ––––– (13,200) –––––– Profit 2,200 ––––––

(2) The sales and other expenses are all standard rated for VAT.

(3) The purchases are all deductible for VAT.

(4) The sales and purchases returns are all evidenced by credit notes issued and received.

(5) The impaired debts were written off in March 2010. Payment for the original sales was due by December 2009.

(6) A sales invoice for £3,000 excluding VAT had been omitted in error from the VAT return for the quarter to 31 December 2009.

(7) Included in the expenses figure is the cost of both business and private petrol for Octavius’s car which had CO2 emissions of 200 g/km. The quarterly car fuel charge (VAT exclusive) is £300.

Required:

(a) Complete the VAT account for the three-month period ended 31 March 2010, showing how much VAT is payable. The ‘cash accounting’ scheme is not being used.

(7 marks)

(b) State when is the VAT shown by (a) above is payable. (1 mark)

(Total: 8 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 41

32 REGISTRATION MATTERS

Required: (a) State when a trader should notify HM Revenue & Customs that he is required to

register for VAT and from what date registration is effective (4 marks) (b) State two advantages and two disadvantages of registering for VAT voluntarily, i.e.

when annual turnover is below the annual registration threshold. (4 marks) (Total: 8 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

42 KAPLAN PU BL ISH INGH

33 TAX POINT

Required: State:

(a) how the basic VAT tax point is normally determined (2 marks)

(b) how the basic VAT tax point can be varied (3 marks)

(c) the importance of the VAT tax point (4 marks)

(d) how the VAT tax point is determined for goods supplied on a sale or return basis (1 mark)

(e) how the VAT tax point is determined for continuous supplies of services. (1 mark)

(Total: 11 marks)

LECTURER RESOURCE PACK – QUESTIO NS

KAPLAN PU BL ISHING 43

34 VAT SUPPLIES

Required:

(a) Contrast the VAT treatment of traders making:

(i) only zero rated supplies

(ii) only exempt supplies. (2 marks)

(b) VAT input tax on three categories of expenditure is not normally recoverable even if the supplies are fully taxable. State these three categories. (3 marks)

(c) State how a cash discount offered to customers is treated for VAT purposes.

(2 marks)

(Total: 7 marks)

PAPER F6 : TAXAT IO N (FA 2009 )

44 KAPLAN PU BL ISH INGH

35 TARDY LTD

Tardy Ltd registered for value added tax (VAT) on 1 July 2007. The company’s VAT returns have been submitted as follows: Quarter ended VAT paid/

(refunded) £

Submitted

30 September 2007 18,600 One month late 31 December 2007 32,200 One month late 31 March 2008 8,800 On time 30 June 2008 3,400 Two months late 30 September 2008 (6,500) One month late 31 December 2008 42,100 On time 31 March 2009 (2,900) On time 30 June 2009 3,900 On time 30 September 2009 18,800 On time 31 December 2009 57,300 Two months late 31 March 2010 9,600 On time

Tardy Ltd always pays any VAT that is due at the same time that the related return is submitted.

During May 2010 Tardy Ltd discovered that a number of errors had been made when completing its VAT return for the quarter ended 31 March 2010. As a result of these errors the company will have to make an additional payment of VAT to HM Revenue & Customs.

On 30 June 2010 Tardy Ltd is to write off three irrecoverable debts. The debts (inclusive of VAT) are for £8,225, £3,525 and £2,350, and are in respect of sales invoices dated 30 September 2009, 15 December 2009 and 15 January 2010 respectively. Tardy Ltd allows two months’ credit to all of its customers before payment is due.

Required:

(a) State, giving appropriate reasons, the default surcharge consequences arising from Tardy Ltd’s submission of its VAT returns for the quarter ended 30 September 2007 to the quarter ended 31 December 2009 inclusive. (8 marks)

(b) Explain how Tardy Ltd can voluntarily disclose the errors relating to the VAT return for the quarter ended 31 March 2010, and state whether default interest will be due, if:

(i) the net errors in total are less than the deminimus level;

(ii) the net errors in total are more than the deminimus level. (3 marks)

(c) (i) State the conditions that must be met in order to claim VAT bad debt relief. (2 marks)

(ii) Advise Tardy Ltd of the amount of bad debt relief that can be claimed in its VAT return for the quarter ended 30 June 2010. (2 marks)

(Total: 15 marks)