For info about the proprietary technology used in comScore products, refer to http://comscore.com/About_comScore/Patents 2015 Holiday Commerce Trends Through Green Monday Dec.14 December 18, 2015 Gian Fulgoni Co-Founder & Chairman Emeritus, comScore, Inc. Andrew Lipsman VP Marketing & Insights, comScore, Inc.

Transcript

For info about the proprietary technology used in comScore products, refer to http://comscore.com/About_comScore/Patents

2015 Holiday Commerce Trends Through Green Monday Dec.14 December 18, 2015

Gian Fulgoni Co-Founder & Chairman Emeritus, comScore, Inc.

By Q3 2015, Total Digital Commerce had grown to account for about 1 in every 7 discretionary dollars spent by consumers

*Note: e-Commerce share is shown as a percent of DOC’s Total Retail Sales excluding Food Service & Drinking, Food & Bev. Stores, Motor Vehicles & Parts, Gasoline Stations and Health & Personal Care Stores.

Desktop & Mobile Digital Commerce Share of Corresponding Consumer Spending*

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

16%

Digital Commerce Share (desktop + mobile)

e-Commerce Share (desktop)

11.6% (Q3 ‘14)

11.0% Q3 ‘15

13.1% Q3 ‘15 Digital’s share of consumer spending peaks in Q1 and Q4

Q1 ‘15 saw a 14.7% share, the highest ever

10.3% (Q3 ‘14)

Source: comScore e-Commerce / m-Commerce & U.S. Department of Commerce (DOC) for Retail

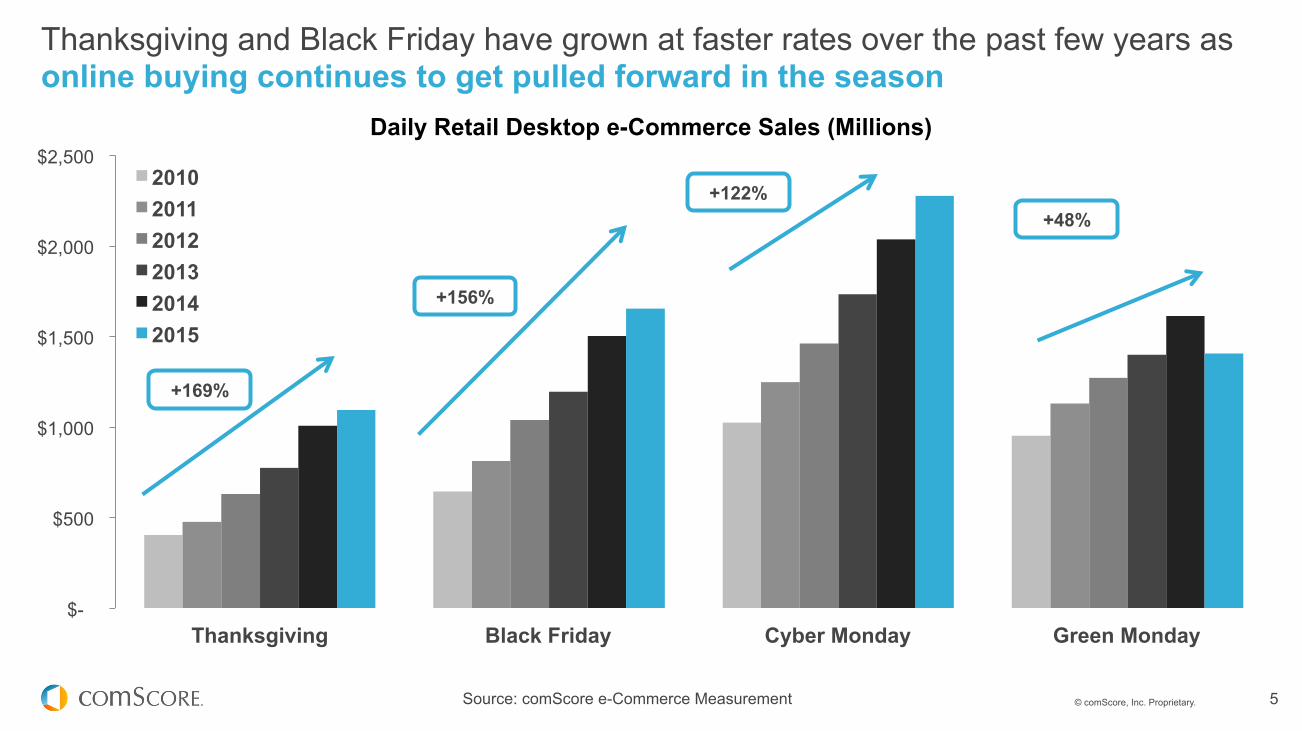

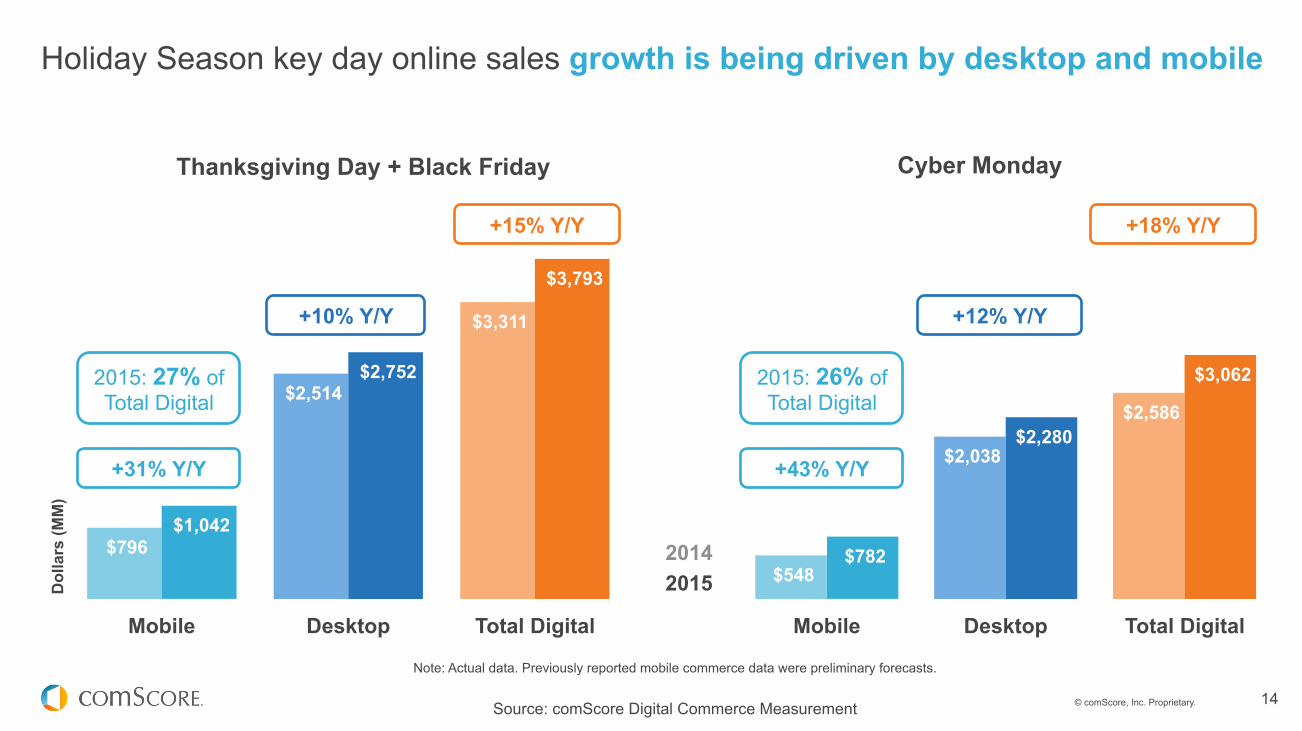

Every weekday since Thanksgiving has exceeded $1 Billion in online spend; Cyber Monday became the highest desktop spending day ever at $2.3B, +11.9% Y/Y

Holiday 2015 U.S. Desktop e-Commerce Spending by Day

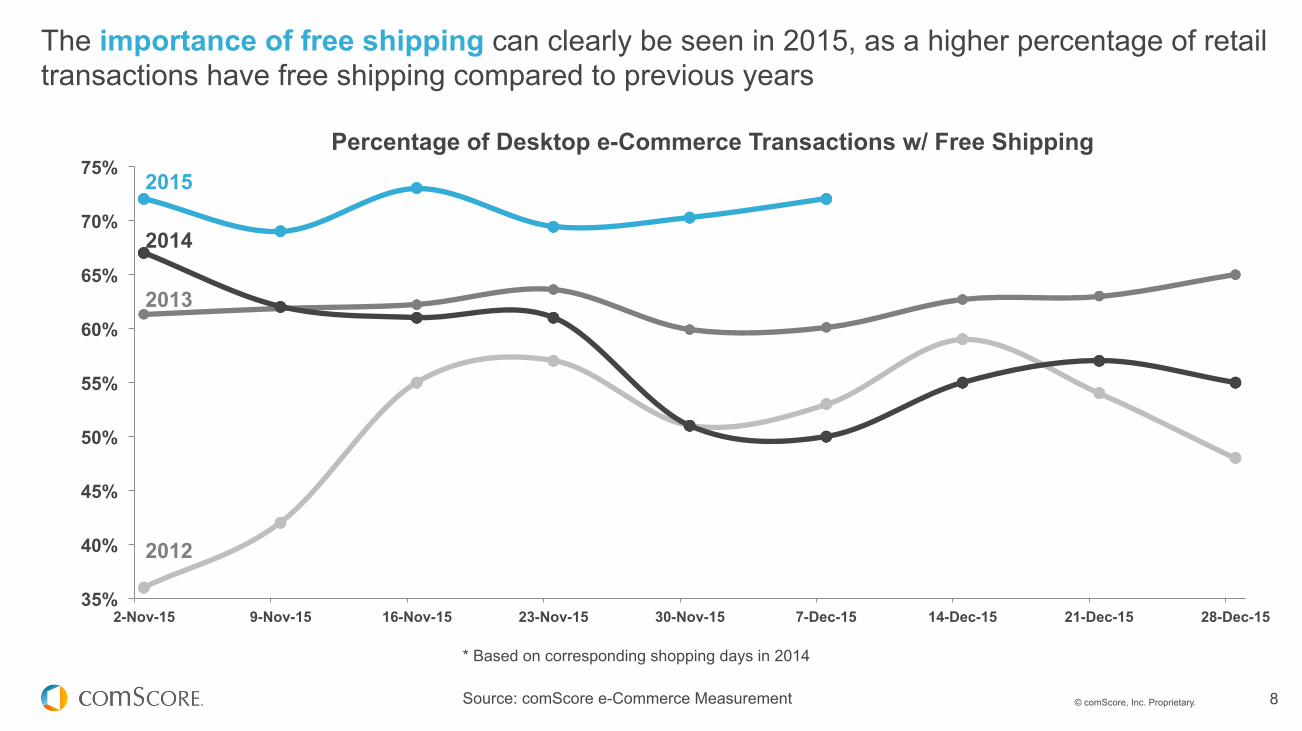

The importance of free shipping can clearly be seen in 2015, as a higher percentage of retail transactions have free shipping compared to previous years

Percentage of Desktop e-Commerce Transactions w/ Free Shipping

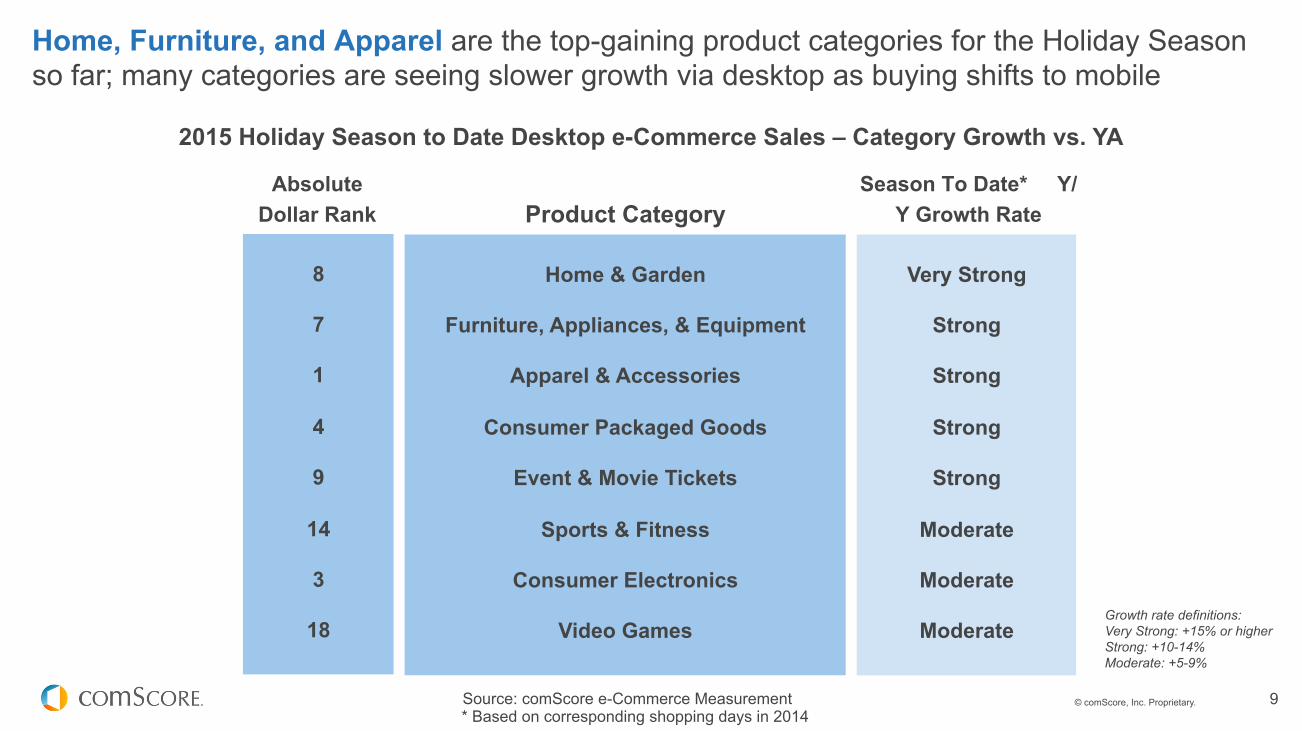

Home, Furniture, and Apparel are the top-gaining product categories for the Holiday Season so far; many categories are seeing slower growth via desktop as buying shifts to mobile

8

7

1

4

9

14

3

18

Home & Garden

Furniture, Appliances, & Equipment

Apparel & Accessories

Consumer Packaged Goods

Event & Movie Tickets

Sports & Fitness

Consumer Electronics

Video Games

Very Strong

Strong

Strong

Strong

Strong

Moderate

Moderate

Moderate Growth rate definitions: Very Strong: +15% or higher Strong: +10-14% Moderate: +5-9%

2015 Holiday Season to Date Desktop e-Commerce Sales – Category Growth vs. YA

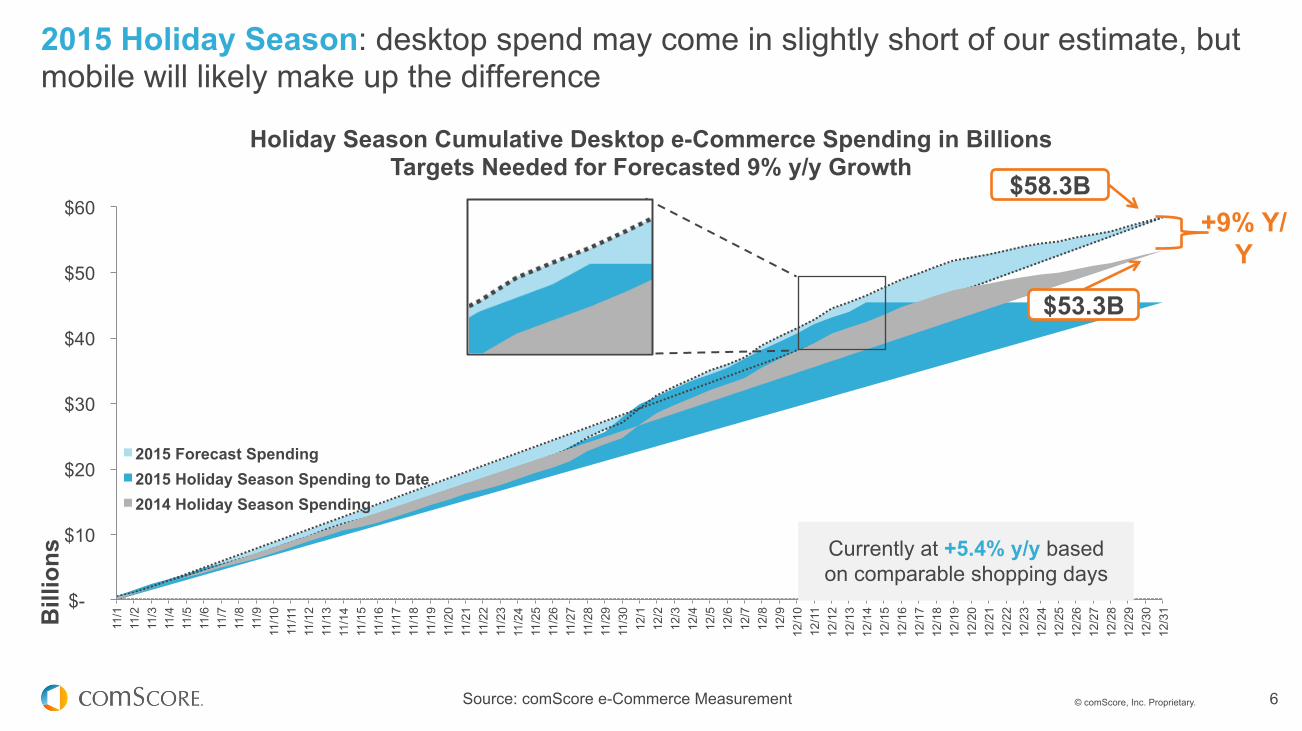

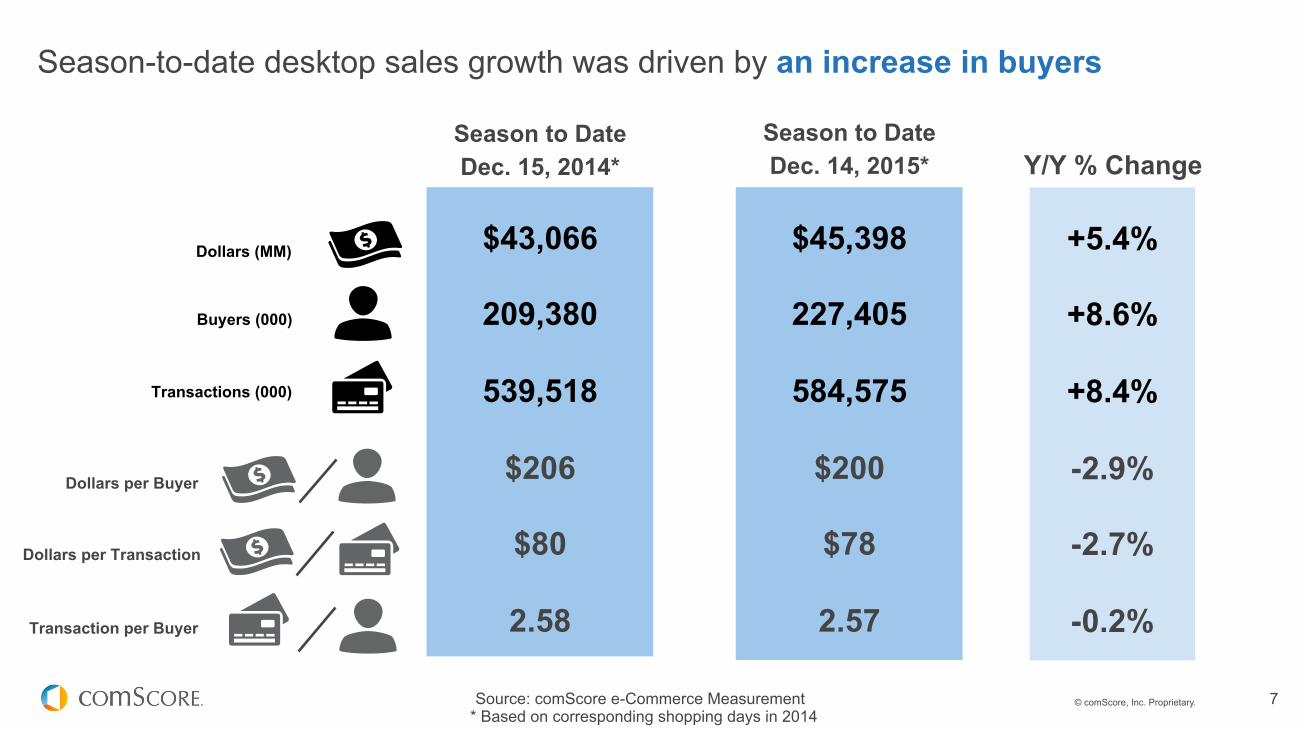

Desktop sales were light so far this season (+5%), but 1 extra day vs. YA and the strength of Green Week will likely push us closer to forecast Mobile is having a larger share of digital dollars than expected this season, but mobile is more important to shopping than buying

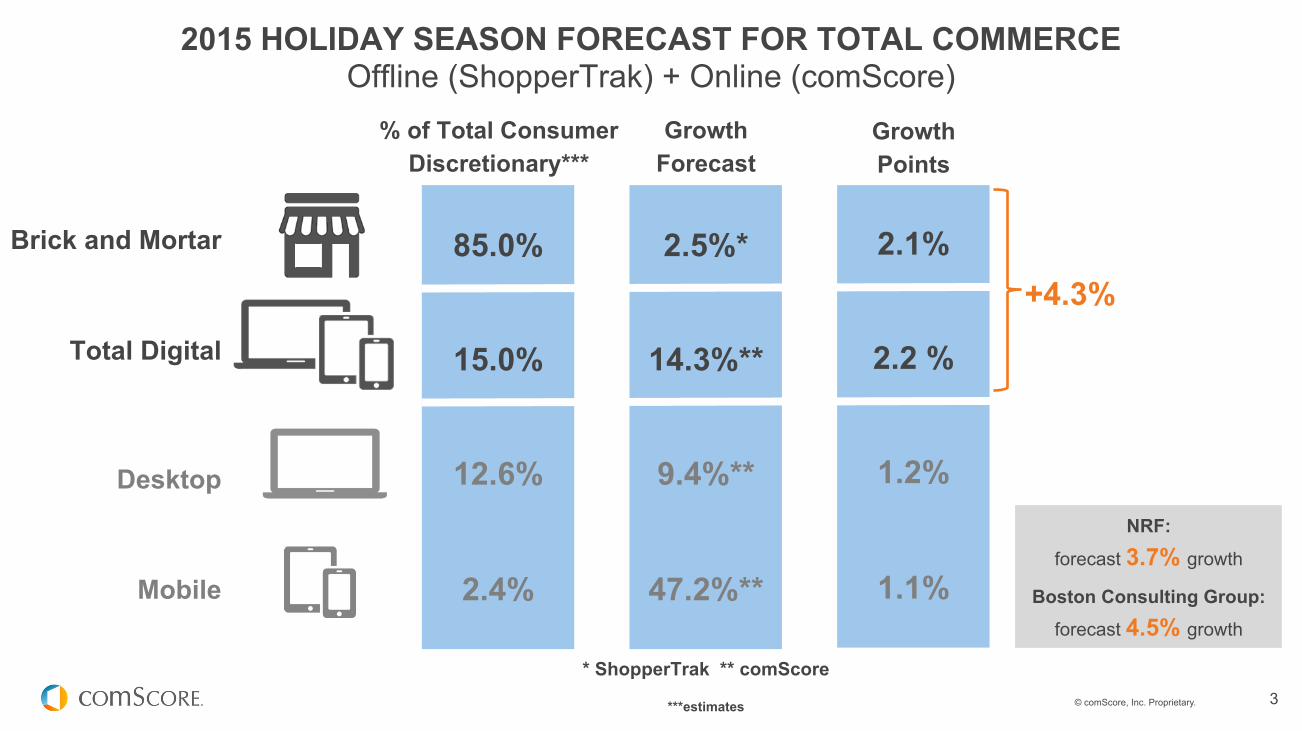

1 comScore Forecast Holiday 2015: $70 B +14% Total Digital $ +9% Desktop $ +47% Mobile $

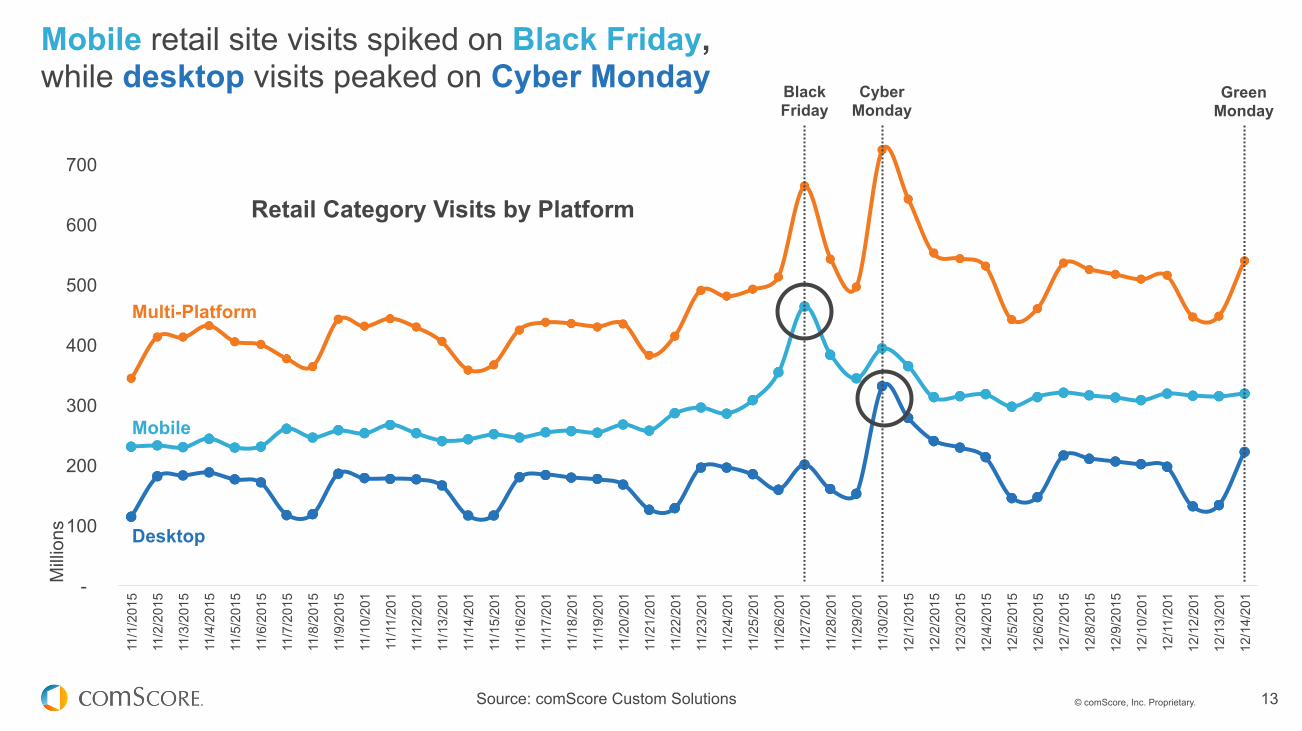

M-Commerce sales were up strongly Y/Y on TG, Black Fri. and Cyber Mon., accounting for nearly 30% of digital commerce sales Mobile retail visits peaked on Black Friday, while desktop visitation remains largely significant on Cyber Monday

2 TG through Cyber Monday online sales exhibited strength, while offline sales declined -10% Y/Y

Free shipping day on Friday this week will promote desktop sales growth as we approach Christmas week With the surge of online traffic and buying this holiday season, it is essential for retailers to make sure their sites and apps can keep up

3 Green Monday kicked off a week that’s likely going to bolster desktop growth rates for the season

For info about the proprietary technology used in comScore products, refer to http://comscore.com/About_comScore/Patents

Beginning in August 2015, eBay no longer included traffic from PayPal’s media property. This change resulted in a significant decline in eBay’s unique visitors, which does not reflect the performance of eBay’s branded sites/apps.

A significant percentage of top retailers’ audiences are accessing via mobile browser, while the majority of mobile time spent is via retailers’ apps

Selected Leading Retailers: U.S. Total Mobile Unique Visitors – Browser vs. App

137M 72M

68M 55M

52M 37M

23M 23M 21M 17M

28%

39%

23%

99%

35%

86%

66%

26%

42%

45%

72%

61%

77%

<1%

65%

14%

34%

74%

58%

55%

Browser App

% of Time Spent Browser vs. App

Apple Sites

Source: comScore Mobile Metrix, U.S., November 2015

![[Conference];[Comscore statistic]](https://static.documents.pub/doc/80x56/554c187eb4c905e7568b4ea3/conferencecomscore-statistic.jpg)