37

© 2012 Copyrights © Yole Developpement SA. All rights reserved. 3DIC & TSV interconnects business update Semicon Moscow presentation. Infineon Micron Synopsys VTI CEA LETI Xilinx

© 2012

Copyrights © Yole Developpement SA. All rights reserved.

3DIC & TSV interconnects

business update

Semicon Moscow presentation.

Infineon

Micron Synopsys VTI

CEA LETI

Xilinx

© 2012 • 2

Copyrights © Yole Developpement SA. All rights reserved.

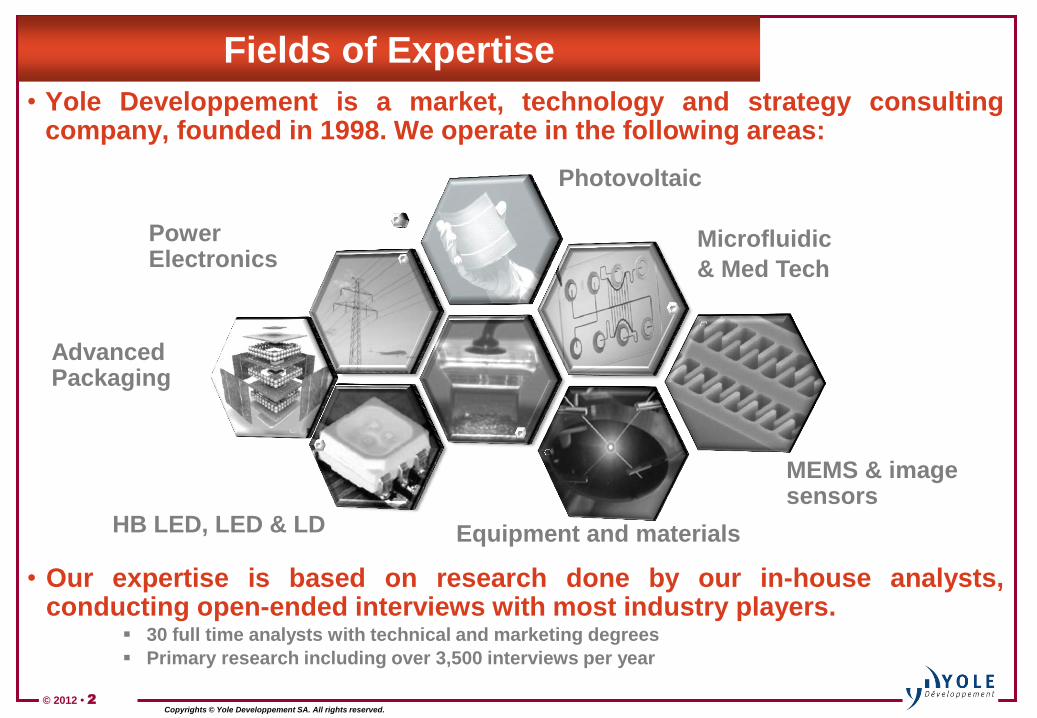

Fields of Expertise

• Yole Developpement is a market, technology and strategy consulting company, founded in 1998. We operate in the following areas:

• Our expertise is based on research done by our in-house analysts, conducting open-ended interviews with most industry players.

30 full time analysts with technical and marketing degrees

Primary research including over 3,500 interviews per year

MEMS & image sensors

Photovoltaic

Advanced Packaging

Microfluidic

& Med Tech

Power Electronics

HB LED, LED & LD Equipment and materials

© 2012 • 3

Copyrights © Yole Developpement SA. All rights reserved.

Mission Statement: Knowledge-Based Company

• Help our customers develop their business through specific

analysis, reports & services providing: Accurate market data, market segmentation and marketing analysis

Technology evaluation; cost estimates and COO analysis

Patent portfolio analysis, licensing strategy and implementation

Identification of strategic development opportunities for companies and business units

Support for M&A, due diligence, and identifying new investors

Advertising opportunities in YOLE magazines, webcasts and specific events

• You get operational results from Yole analysis and actions

© 2012 • 4

Copyrights © Yole Developpement SA. All rights reserved.

4 Business Models

• Custom Analysis: Largest part of Yole activities

Covered by NDA agreement

A few days to several months of work, depending on objectives

• Published Reports: An average of 40 reports published every year

Available individually or through Annual Subscription Program

Market and technology reports, Patent analysis, Reverse Engineering/Costing reports and Reverse Costing tools

• i-Micronews Media: Newsletters and webcasts on 3D, MEMS, Power electronics, LED and imaging

Advertising services providing access to our 45 000+ subscribers to be visible and diffuse information on your company and products

• Yole Finance services:

M&A (buying and selling)

Due diligence

Fund-raising services

© 2012 • 5

Copyrights © Yole Developpement SA. All rights reserved.

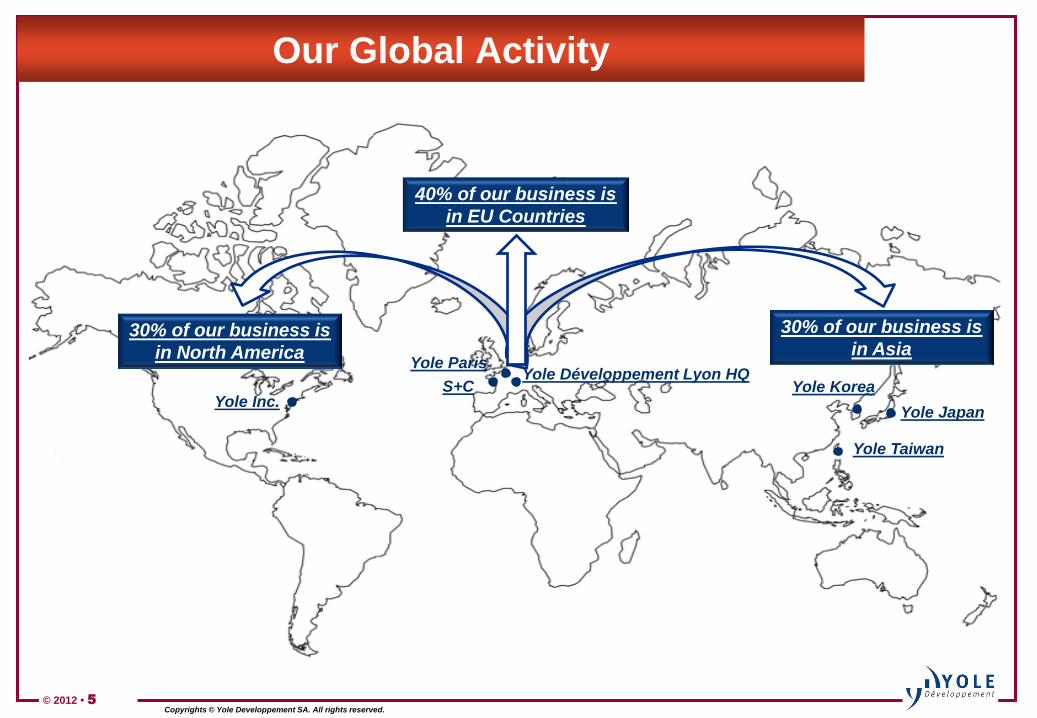

Our Global Activity

Yole Inc.

Yole Paris

Yole Japan

30% of our business is

in North America

30% of our business is

in Asia

40% of our business is

in EU Countries

Yole Korea Yole Développement Lyon HQ

Yole Taiwan

S+C

© 2012 • 6

Copyrights © Yole Developpement SA. All rights reserved.

Some of Our Customers

Financial investors

& industry advocates

R&D Organizations

Suppliers (equipment,

wafers, materials)

Component

manufacturers

Integrators, system

suppliers & end users

© 2012 • 7

Copyrights © Yole Développement SA. All rights reserved.

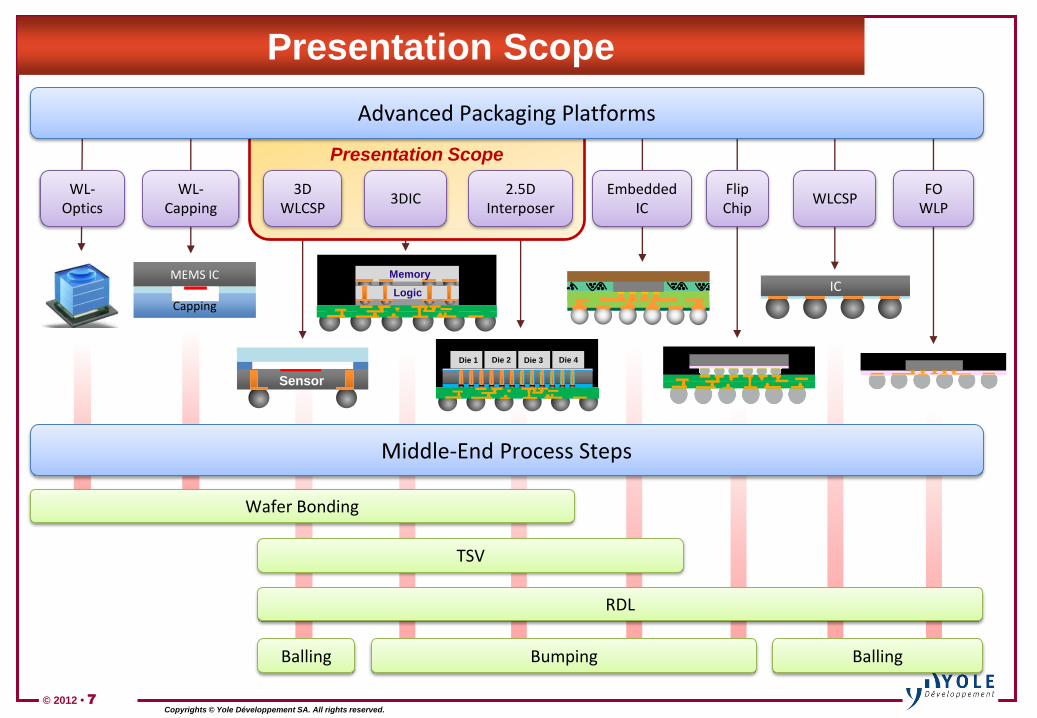

Presentation Scope

Advanced Packaging Platforms

RDL

Bumping Balling

Wafer Bonding

TSV

WL-Optics

WL-Capping

2.5D Interposer

3DIC

Balling

WLCSP FO

WLP Embedded

IC Flip Chip

MEMS IC

Capping

IC

Sensor

Memory

Logic

3D WLCSP

Die 1 Die 2 Die 3 Die 4

Middle-End Process Steps

Presentation Scope

© 2012 • 8

Copyrights © Yole Developpement SA. All rights reserved.

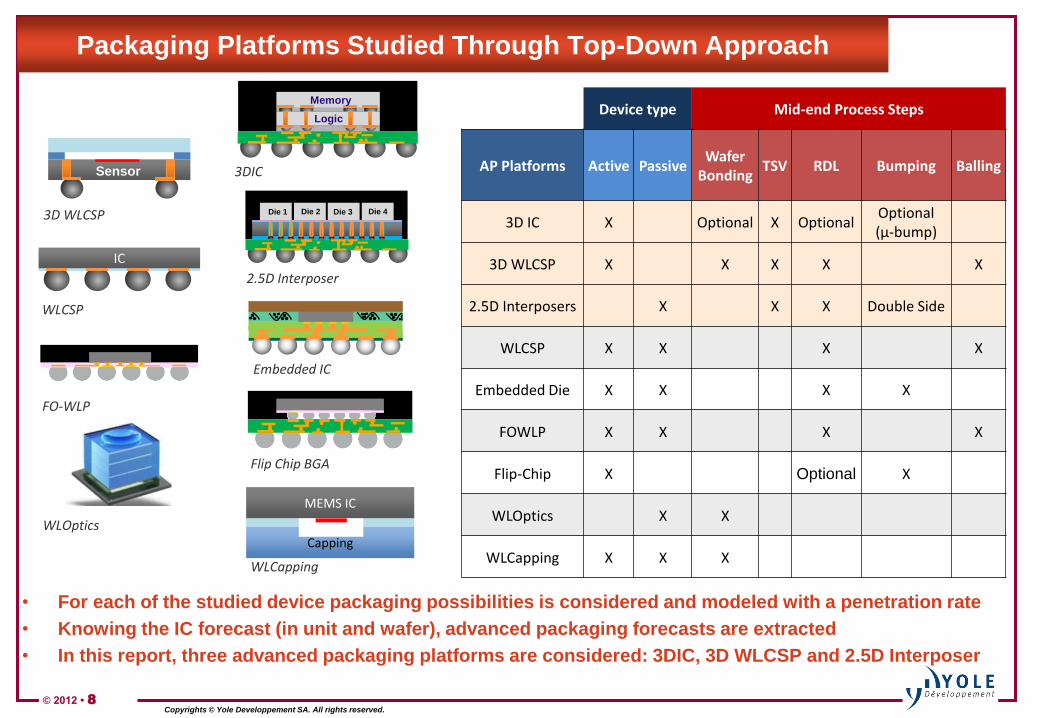

Packaging Platforms Studied Through Top-Down Approach

• For each of the studied device packaging possibilities is considered and modeled with a penetration rate

• Knowing the IC forecast (in unit and wafer), advanced packaging forecasts are extracted

• In this report, three advanced packaging platforms are considered: 3DIC, 3D WLCSP and 2.5D Interposer

Device type Mid-end Process Steps

AP Platforms Active Passive Wafer

Bonding TSV RDL Bumping Balling

3D IC X Optional X Optional Optional (µ-bump)

3D WLCSP X X X X X

2.5D Interposers X X X Double Side

WLCSP X X X X

Embedded Die X X X X

FOWLP X X X X

Flip-Chip X Optional X

WLOptics X X

WLCapping X X X

MEMS IC

Capping

IC

Sensor 3DIC

3D WLCSP

WLCSP

FO-WLP

WLOptics

2.5D Interposer

Embedded IC

Flip Chip BGA

WLCapping

Memory

Logic

Die 1 Die 2 Die 3 Die 4

© 2012 • 9

Copyrights © Yole Développement SA. All rights reserved.

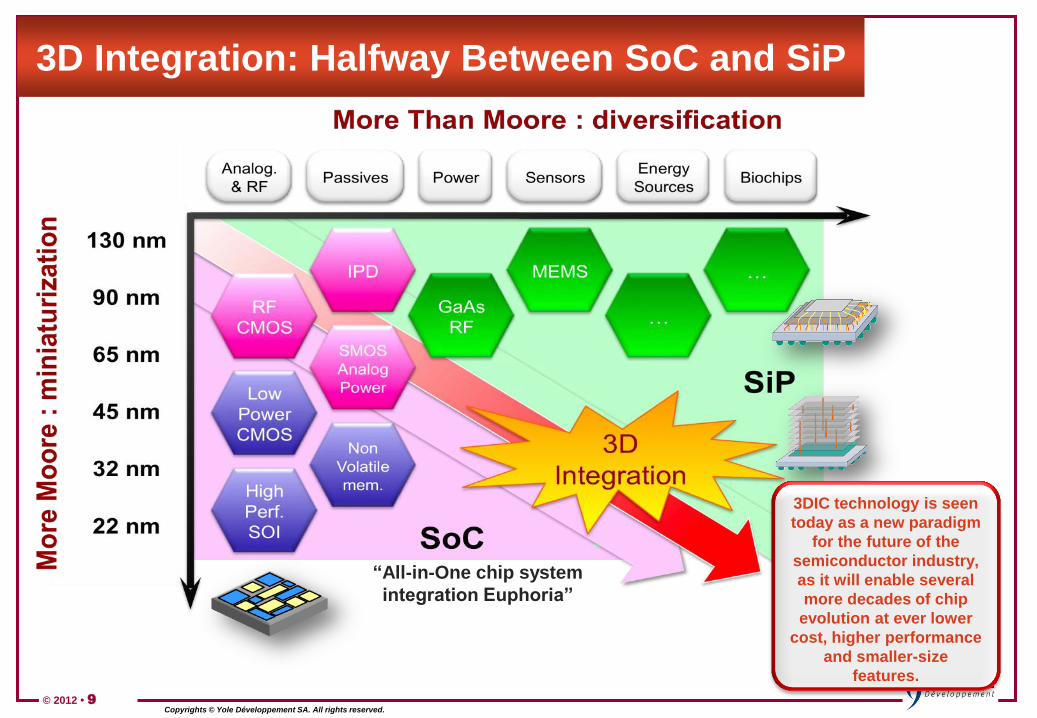

3D Integration: Halfway Between SoC and SiP

“All-in-One chip system

integration Euphoria”

3DIC technology is seen

today as a new paradigm

for the future of the

semiconductor industry,

as it will enable several

more decades of chip

evolution at ever lower

cost, higher performance

and smaller-size

features.

© 2012 • 10

Copyrights © Yole Développement SA. All rights reserved.

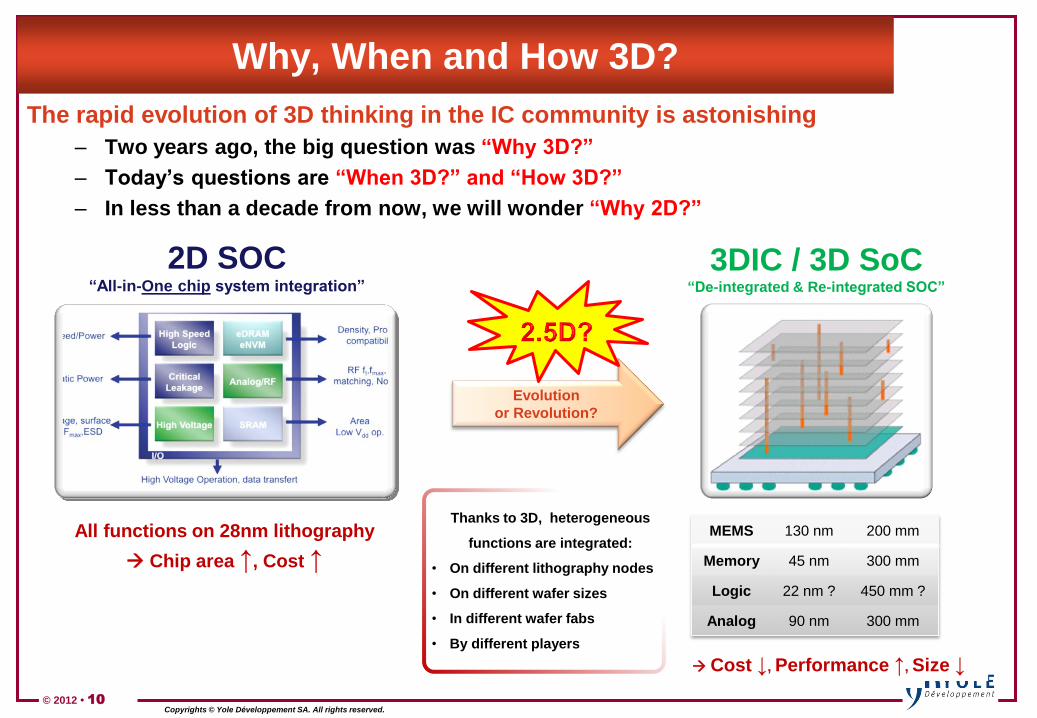

Why, When and How 3D?

The rapid evolution of 3D thinking in the IC community is astonishing

– Two years ago, the big question was “Why 3D?”

– Today‟s questions are “When 3D?” and “How 3D?”

– In less than a decade from now, we will wonder “Why 2D?”

Evolution

or Revolution?

3DIC / 3D SoC “De-integrated & Re-integrated SOC”

2D SOC “All-in-One chip system integration”

All functions on 28nm lithography

Chip area ↑, Cost ↑

MEMS 130 nm 200 mm

Memory 45 nm 300 mm

Logic 22 nm ? 450 mm ?

Analog 90 nm 300 mm

Thanks to 3D, heterogeneous

functions are integrated:

• On different lithography nodes

• On different wafer sizes

• In different wafer fabs

• By different players

Cost ↓, Performance ↑, Size ↓

© 2012 • 11

Copyrights © Yole Développement SA. All rights reserved.

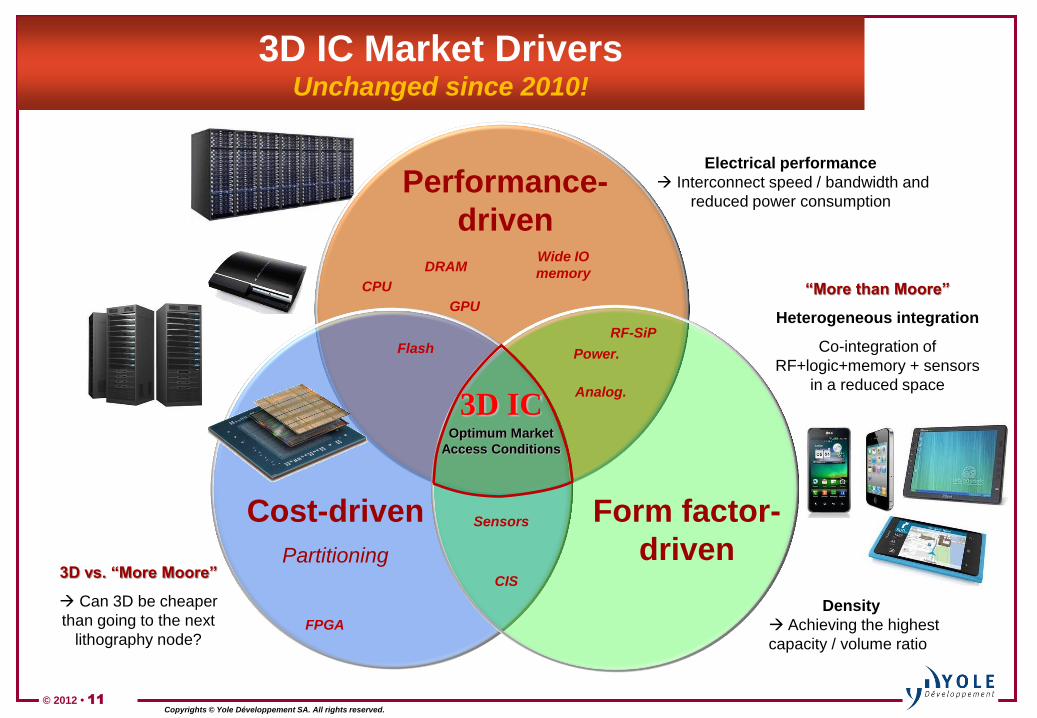

“More than Moore”

Heterogeneous integration

Co-integration of

RF+logic+memory + sensors

in a reduced space

Density

Achieving the highest

capacity / volume ratio

Form factor-

driven

Performance-

driven

3D IC Optimum Market

Access Conditions

Wide IO

memory

CIS

DRAM

RF-SiP

Electrical performance

Interconnect speed / bandwidth and

reduced power consumption

3D vs. “More Moore”

Can 3D be cheaper

than going to the next

lithography node?

Flash

Cost-driven

Partitioning

Sensors

3D IC Market Drivers Unchanged since 2010!

CPU

GPU

Power.

Analog.

FPGA

© 2012

Copyrights © Yole Developpement SA. All rights reserved.

3DIC & TSV Market Forecast Top-Down Analysis

© 2012 • 13

Copyrights © Yole Developpement SA. All rights reserved.

-

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

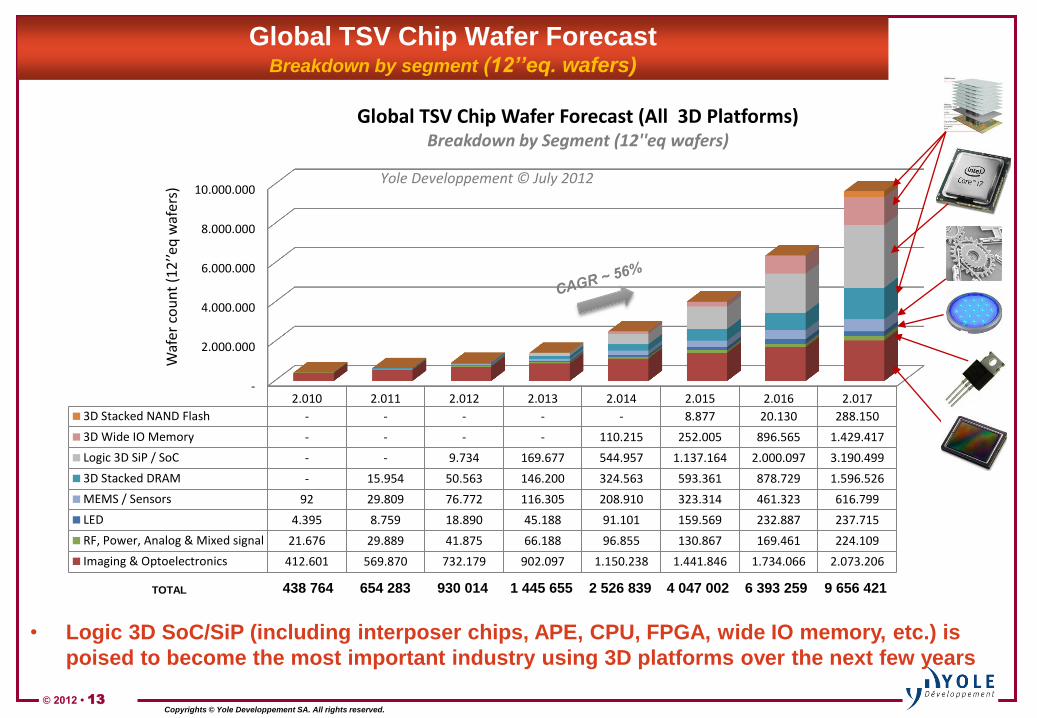

2.010 2.011 2.012 2.013 2.014 2.015 2.016 2.017

3D Stacked NAND Flash - - - - - 8.877 20.130 288.150

3D Wide IO Memory - - - - 110.215 252.005 896.565 1.429.417

Logic 3D SiP / SoC - - 9.734 169.677 544.957 1.137.164 2.000.097 3.190.499

3D Stacked DRAM - 15.954 50.563 146.200 324.563 593.361 878.729 1.596.526

MEMS / Sensors 92 29.809 76.772 116.305 208.910 323.314 461.323 616.799

LED 4.395 8.759 18.890 45.188 91.101 159.569 232.887 237.715

RF, Power, Analog & Mixed signal 21.676 29.889 41.875 66.188 96.855 130.867 169.461 224.109

Imaging & Optoelectronics 412.601 569.870 732.179 902.097 1.150.238 1.441.846 1.734.066 2.073.206

Waf

er c

ou

nt

(12

’’eq

waf

ers)

Global TSV Chip Wafer Forecast (All 3D Platforms) Breakdown by Segment (12''eq wafers)

Yole Developpement © July 2012

Global TSV Chip Wafer Forecast Breakdown by segment (12’’eq. wafers)

• Logic 3D SoC/SiP (including interposer chips, APE, CPU, FPGA, wide IO memory, etc.) is

poised to become the most important industry using 3D platforms over the next few years

TOTAL 438 764 654 283 930 014 1 445 655 2 526 839 4 047 002 6 393 259 9 656 421

© 2012 • 14

Copyrights © Yole Développement SA. All rights reserved.

0

20

40

60

80

100

120

140

Rev

enu

es (

M$

)

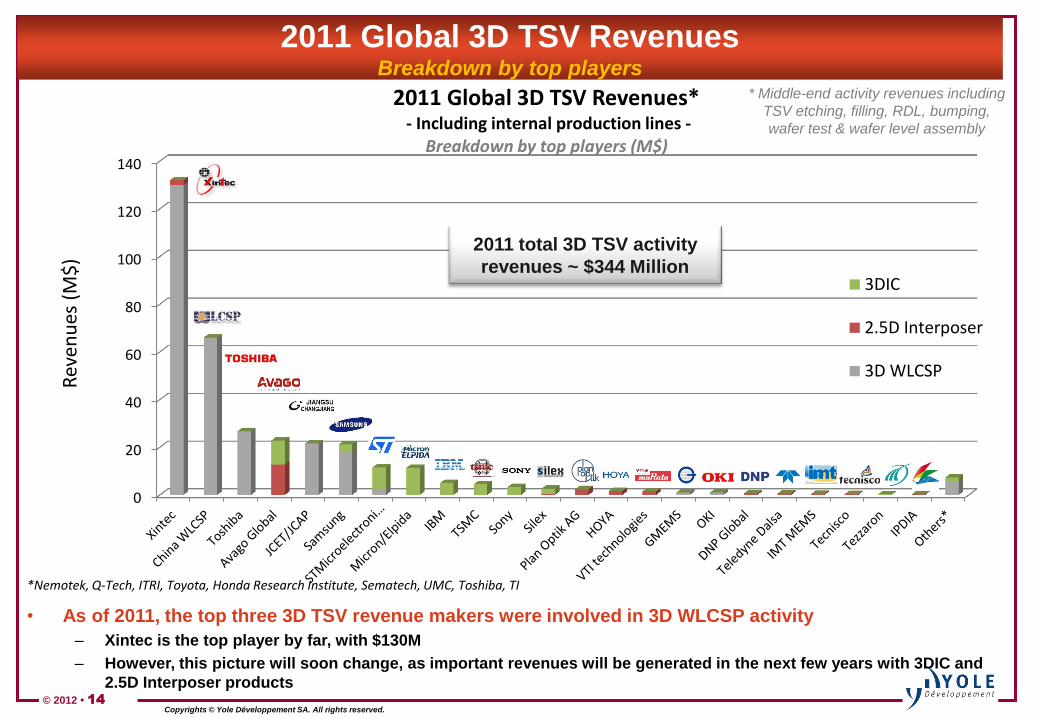

2011 Global 3D TSV Revenues* - Including internal production lines -

Breakdown by top players (M$)

3DIC

2.5D Interposer

3D WLCSP

*Nemotek, Q-Tech, ITRI, Toyota, Honda Research Institute, Sematech, UMC, Toshiba, TI

2011 Global 3D TSV Revenues Breakdown by top players

• As of 2011, the top three 3D TSV revenue makers were involved in 3D WLCSP activity

– Xintec is the top player by far, with $130M

– However, this picture will soon change, as important revenues will be generated in the next few years with 3DIC and

2.5D Interposer products

* Middle-end activity revenues including

TSV etching, filling, RDL, bumping,

wafer test & wafer level assembly

2011 total 3D TSV activity

revenues ~ $344 Million

© 2012 • 15

Copyrights © Yole Developpement SA. All rights reserved.

3D WLCSP: the Most Mature 3D TSV Platform

• 3D WLCSP is the preferred solution today for the efficient assembly of small-size optoelectronic

chips, like CMOS image sensors. It is also the most mature 3D TSV platform at the moment, as we

estimate the market to be ~ $272M in 2011 for the “middle-end” processing factories serving this

specific market

Xintec $130,0M

48%

China WLCSP $66,0M

24%

Toshiba $26,7M

10%

JCAP $21.6M

8%

Samsung $18,2M

7%

STMicroelectronics $2,3M

1% Others* $5,3M

2%

2011 3D WLCSP Platform Middle-End Revenues* Including internal production lines

Breakdown by top players (M$)

Yole Developpement © July 2012

* Middle -end activity revenues including TSV

etching, filling, RDL, bumping, wafer test & wafer level assembly

Total =

$272M

*Others = Oki, G-MEMS,

Nemotek, Q-Tech

© 2012 • 16

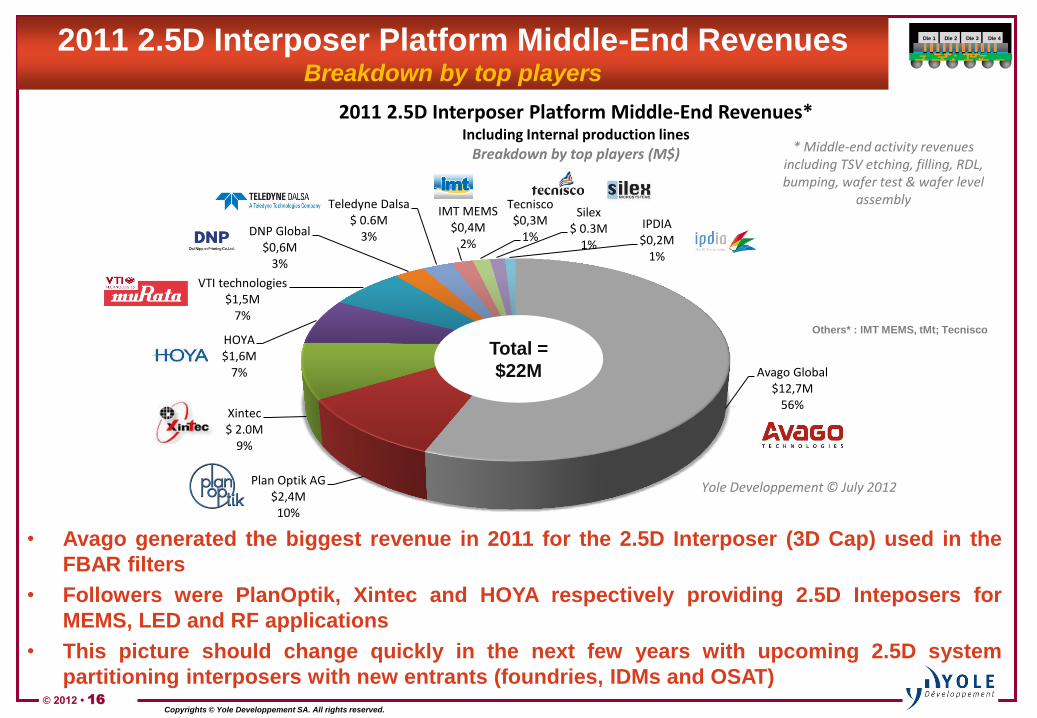

Copyrights © Yole Developpement SA. All rights reserved.

• Avago generated the biggest revenue in 2011 for the 2.5D Interposer (3D Cap) used in the

FBAR filters

• Followers were PlanOptik, Xintec and HOYA respectively providing 2.5D Inteposers for

MEMS, LED and RF applications

• This picture should change quickly in the next few years with upcoming 2.5D system

partitioning interposers with new entrants (foundries, IDMs and OSAT)

Avago Global $12,7M

56%

Plan Optik AG $2,4M 10%

Xintec $ 2.0M

9%

HOYA $1,6M

7%

VTI technologies $1,5M

7%

DNP Global $0,6M

3%

Teledyne Dalsa $ 0.6M

3%

IMT MEMS $0,4M

2%

Tecnisco $0,3M

1%

Silex $ 0.3M

1%

IPDIA $0,2M

1%

2011 2.5D Interposer Platform Middle-End Revenues* Including Internal production lines

Breakdown by top players (M$)

Yole Developpement © July 2012

* Middle-end activity revenues including TSV etching, filling, RDL, bumping, wafer test & wafer level

assembly

2011 2.5D Interposer Platform Middle-End Revenues Breakdown by top players

Total =

$22M

Others* : IMT MEMS, tMt; Tecnisco

Die 1 Die 2 Die 3 Die 4

© 2012 • 17

Copyrights © Yole Développement SA. All rights reserved.

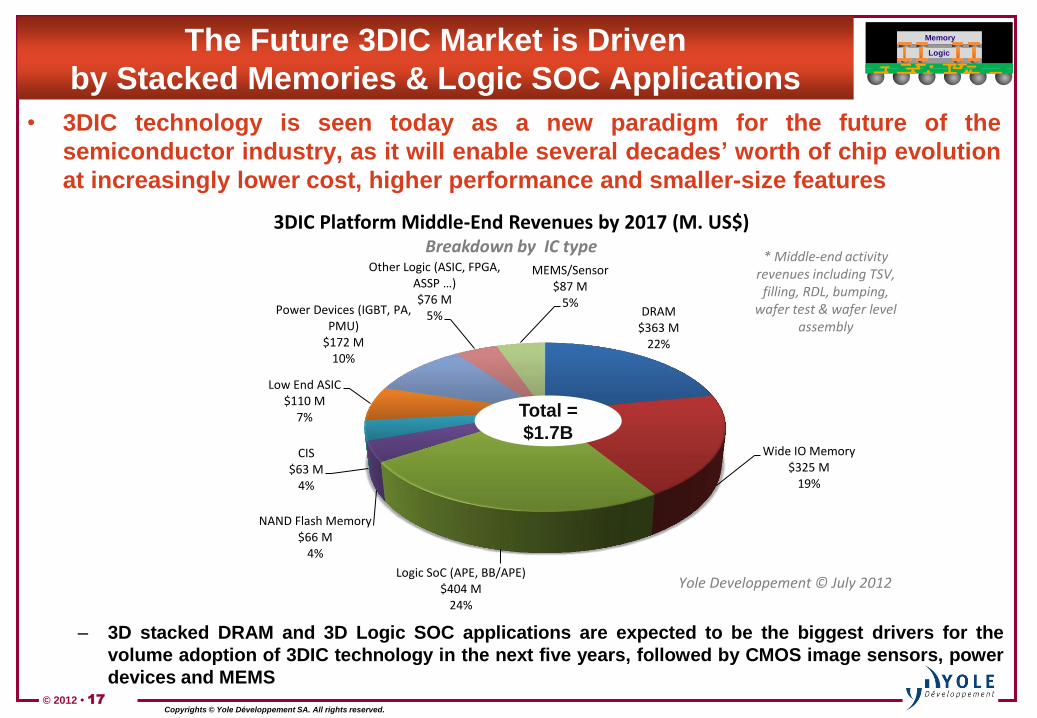

The Future 3DIC Market is Driven

by Stacked Memories & Logic SOC Applications

• 3DIC technology is seen today as a new paradigm for the future of the

semiconductor industry, as it will enable several decades‟ worth of chip evolution

at increasingly lower cost, higher performance and smaller-size features

– 3D stacked DRAM and 3D Logic SOC applications are expected to be the biggest drivers for the

volume adoption of 3DIC technology in the next five years, followed by CMOS image sensors, power

devices and MEMS

DRAM $363 M

22%

Wide IO Memory $325 M

19%

Logic SoC (APE, BB/APE) $404 M

24%

NAND Flash Memory $66 M

4%

CIS $63 M

4%

Low End ASIC $110 M

7%

Power Devices (IGBT, PA, PMU)

$172 M 10%

Other Logic (ASIC, FPGA, ASSP …) $76 M

5%

MEMS/Sensor $87 M

5%

3DIC Platform Middle-End Revenues by 2017 (M. US$) Breakdown by IC type

* Middle-end activity revenues including TSV, filling, RDL, bumping,

wafer test & wafer level assembly

Yole Developpement © July 2012

Total =

$1.7B

Memory

Logic

© 2012

Copyrights © Yole Developpement SA. All rights reserved.

Infrastructure

&

Supply Chain Analysis

© 2012 • 19

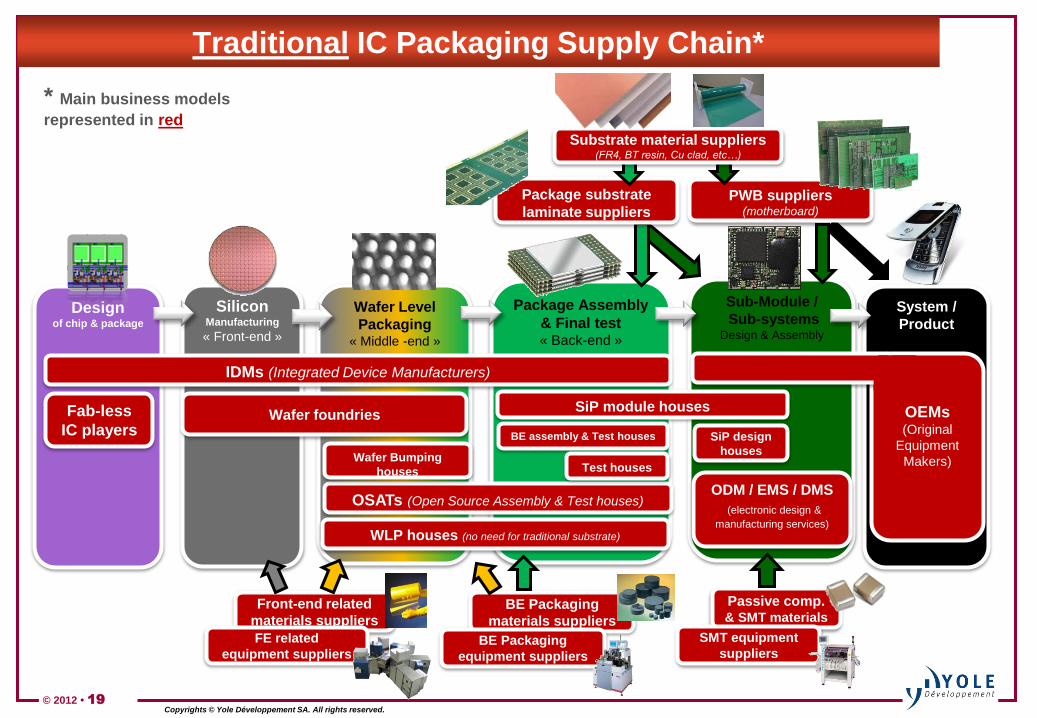

Copyrights © Yole Développement SA. All rights reserved.

Traditional IC Packaging Supply Chain*

System /

Product

Sub-Module /

Sub-systems Design & Assembly

Design of chip & package

Wafer Level

Packaging « Middle -end »

Silicon Manufacturing

« Front-end »

Package Assembly

& Final test « Back-end »

Front-end related

materials suppliers

OEMs (Original

Equipment

Makers)

FE related

equipment suppliers

BE Packaging

materials suppliers

BE Packaging

equipment suppliers

Fab-less

IC players

IDMs (Integrated Device Manufacturers)

Wafer foundries

OSATs (Open Source Assembly & Test houses)

Wafer Bumping

houses

BE assembly & Test houses

PWB suppliers (motherboard)

ODM / EMS / DMS

(electronic design &

manufacturing services)

SiP module houses

Passive comp. & SMT materials

SMT equipment

suppliers

SiP design

houses

Test houses

Package substrate

laminate suppliers

Substrate material suppliers (FR4, BT resin, Cu clad, etc…)

* Main business models

represented in red

WLP houses (no need for traditional substrate)

© 2012 • 20

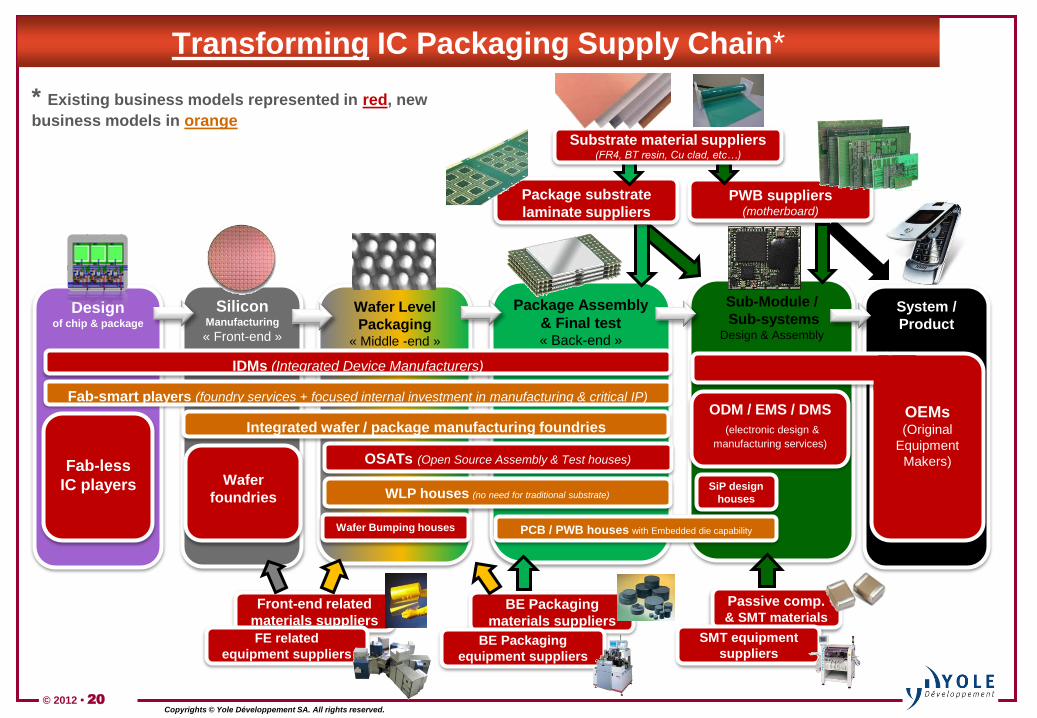

Copyrights © Yole Développement SA. All rights reserved.

Transforming IC Packaging Supply Chain*

System /

Product

Sub-Module /

Sub-systems Design & Assembly

Design of chip & package

Wafer Level

Packaging « Middle -end »

Silicon Manufacturing

« Front-end »

Package Assembly

& Final test « Back-end »

Front-end related

materials suppliers

OEMs (Original

Equipment

Makers)

FE related

equipment suppliers

BE Packaging

materials suppliers

BE Packaging

equipment suppliers

Fab-less

IC players

IDMs (Integrated Device Manufacturers)

Integrated wafer / package manufacturing foundries

OSATs (Open Source Assembly & Test houses)

WLP houses (no need for traditional substrate)

PWB suppliers (motherboard)

ODM / EMS / DMS

(electronic design &

manufacturing services)

Passive comp. & SMT materials

SMT equipment

suppliers

SiP design

houses

Package substrate

laminate suppliers

Substrate material suppliers (FR4, BT resin, Cu clad, etc…)

* Existing business models represented in red, new

business models in orange

Wafer

foundries

Fab-smart players (foundry services + focused internal investment in manufacturing & critical IP)

Wafer Bumping houses PCB / PWB houses with Embedded die capability

© 2012 • 21

Copyrights © Yole Développement SA. All rights reserved.

Global 3DIC / TSV Activity Worldwide

© 2012

Copyrights © Yole Developpement SA. All rights reserved.

3D IC & TSV

Market Focus

© 2012 • 23

Copyrights © Yole Développement SA. All rights reserved.

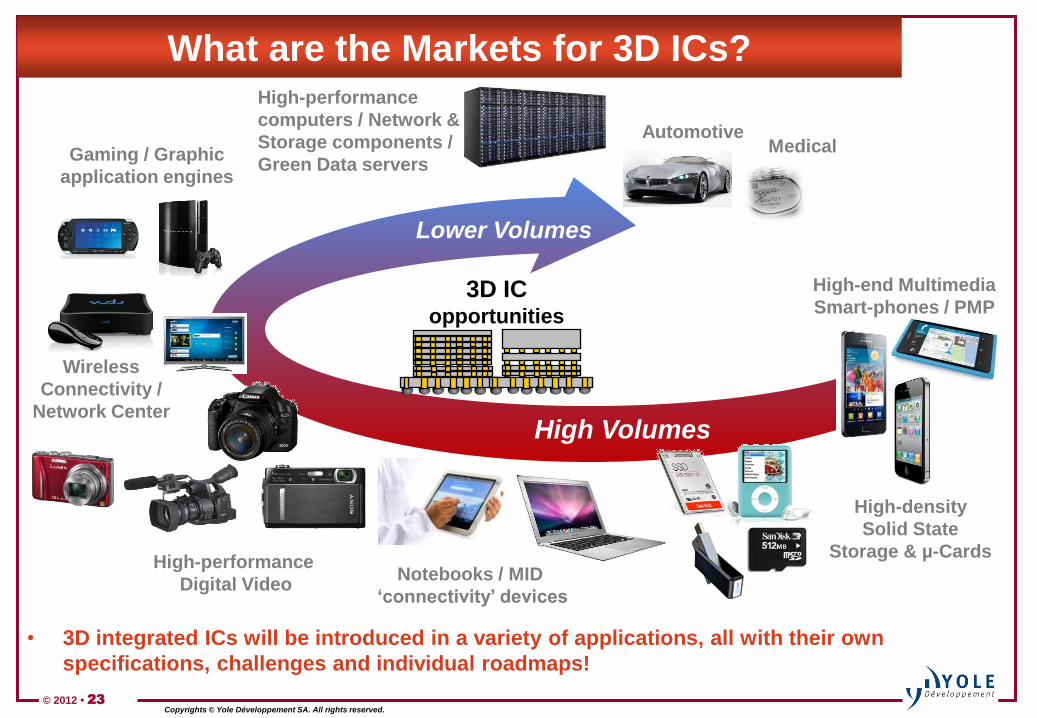

What are the Markets for 3D ICs?

• 3D integrated ICs will be introduced in a variety of applications, all with their own

specifications, challenges and individual roadmaps!

High Volumes

Lower Volumes

3D IC opportunities

High-end Multimedia

Smart-phones / PMP

High-density

Solid State

Storage & µ-Cards

Notebooks / MID

„connectivity‟ devices

Gaming / Graphic

application engines

High-performance

computers / Network &

Storage components /

Green Data servers

High-performance

Digital Video

Wireless

Connectivity /

Network Center

Automotive Medical

© 2012 • 24

Copyrights © Yole Développement SA. All rights reserved.

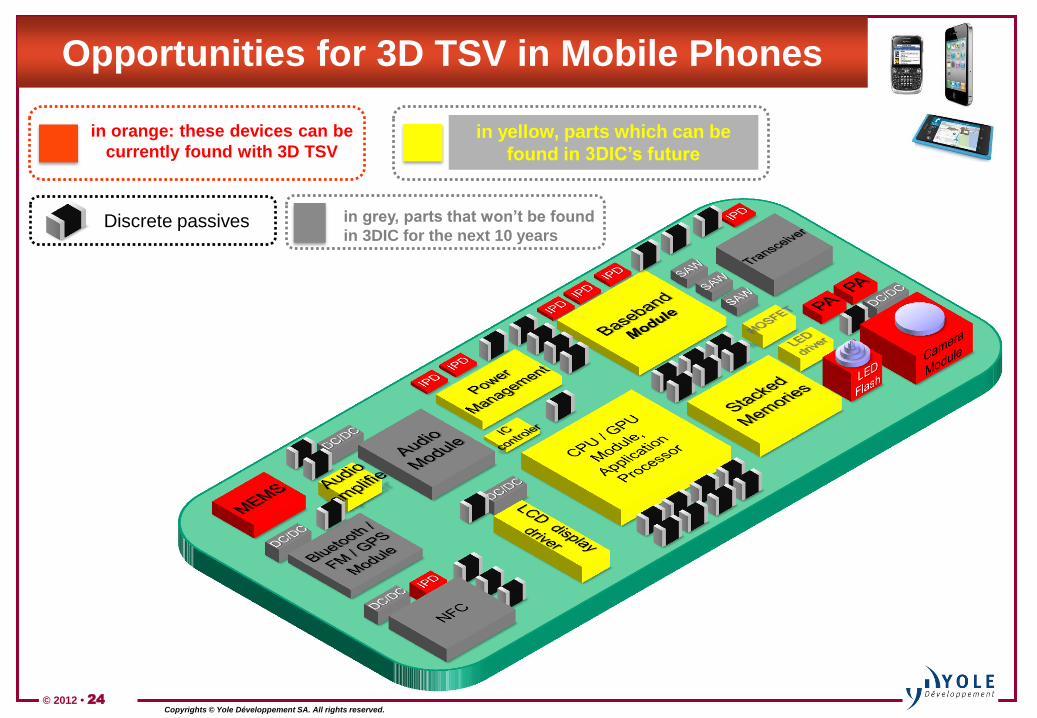

Opportunities for 3D TSV in Mobile Phones

in orange: these devices can be

currently found with 3D TSV in yellow, parts which can be

found in 3DIC‟s future

Discrete passives in grey, parts that won‟t be found

in 3DIC for the next 10 years

© 2012 • 25

Copyrights © Yole Développement SA. All rights reserved.

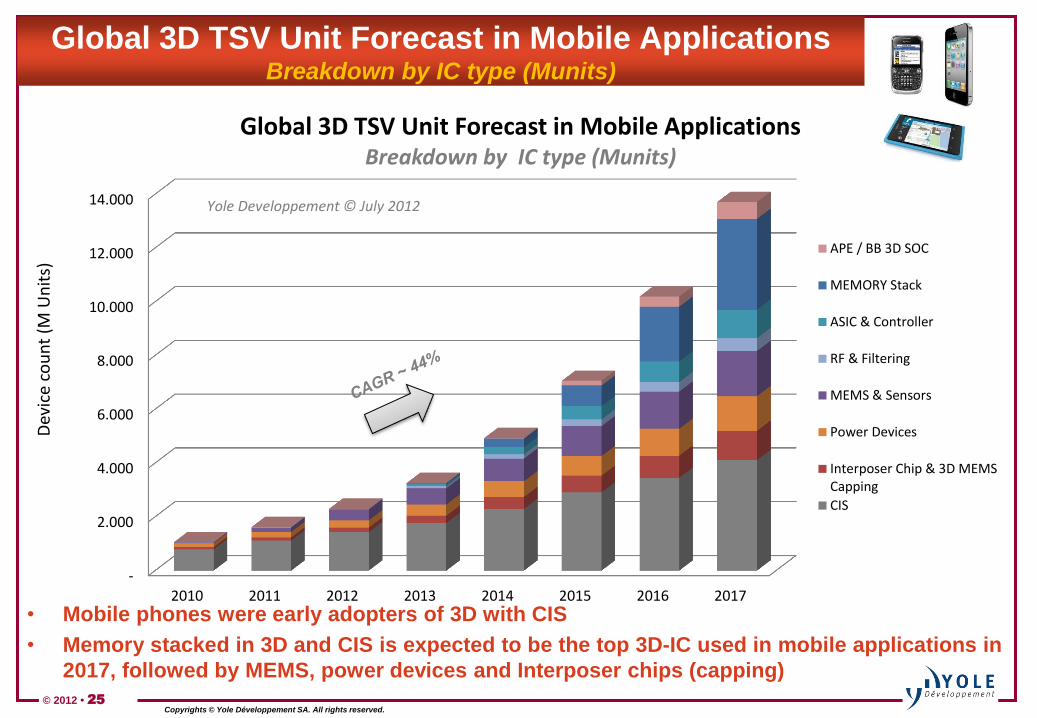

Global 3D TSV Unit Forecast in Mobile Applications Breakdown by IC type (Munits)

• Mobile phones were early adopters of 3D with CIS

• Memory stacked in 3D and CIS is expected to be the top 3D-IC used in mobile applications in

2017, followed by MEMS, power devices and Interposer chips (capping)

-

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2010 2011 2012 2013 2014 2015 2016 2017

Dev

ice

cou

nt

(M U

nit

s)

Global 3D TSV Unit Forecast in Mobile Applications Breakdown by IC type (Munits)

APE / BB 3D SOC

MEMORY Stack

ASIC & Controller

RF & Filtering

MEMS & Sensors

Power Devices

Interposer Chip & 3D MEMSCapping

CIS

Yole Developpement © July 2012

© 2012 • 26

Copyrights © Yole Développement SA. All rights reserved.

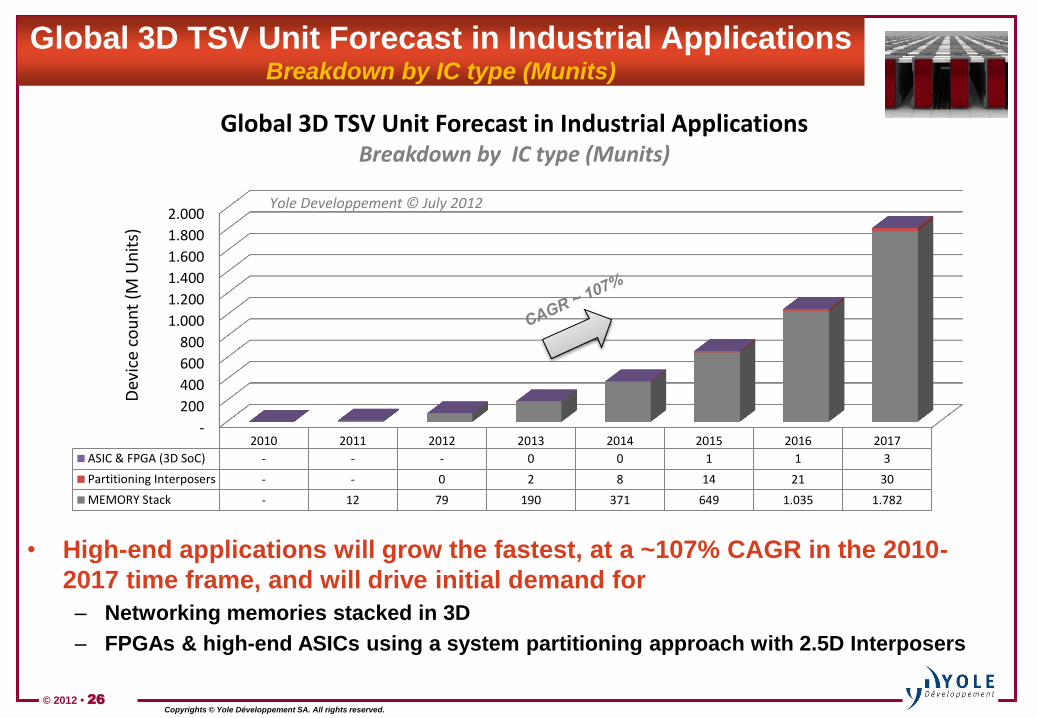

Global 3D TSV Unit Forecast in Industrial Applications Breakdown by IC type (Munits)

• High-end applications will grow the fastest, at a ~107% CAGR in the 2010-

2017 time frame, and will drive initial demand for

– Networking memories stacked in 3D

– FPGAs & high-end ASICs using a system partitioning approach with 2.5D Interposers

-

200

400

600

800

1.000

1.200

1.400

1.600

1.800

2.000

2010 2011 2012 2013 2014 2015 2016 2017

ASIC & FPGA (3D SoC) - - - 0 0 1 1 3

Partitioning Interposers - - 0 2 8 14 21 30

MEMORY Stack - 12 79 190 371 649 1.035 1.782

Dev

ice

cou

nt

(M U

nit

s)

Global 3D TSV Unit Forecast in Industrial Applications Breakdown by IC type (Munits)

Yole Developpement © July 2012

© 2012

Copyrights © Yole Développement SA. All rights reserved.

3D IC & TSV

Application Focus

© 2012 • 28

Copyrights © Yole Développement SA. All rights reserved.

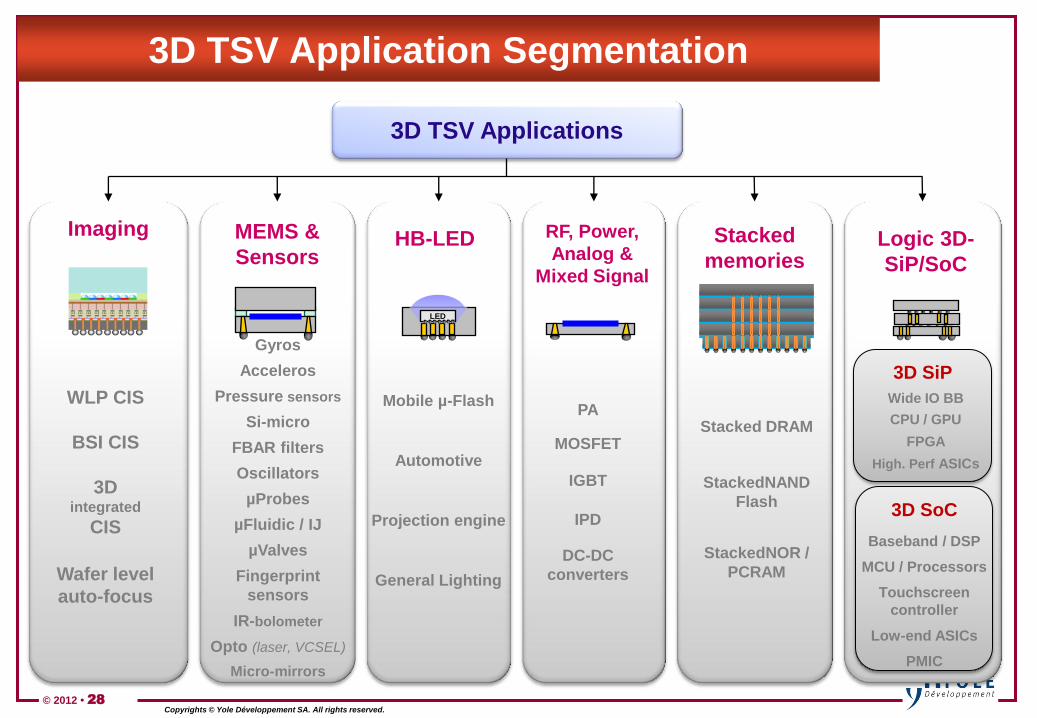

3D TSV Application Segmentation

Imaging

LED

MEMS &

Sensors HB-LED Stacked

memories

RF, Power,

Analog &

Mixed Signal

Logic 3D-

SiP/SoC

3D TSV Applications

WLP CIS

BSI CIS

Wafer level

auto-focus

3D integrated

CIS

Gyros

Acceleros

Pressure sensors

Si-micro

FBAR filters

Oscillators

µProbes

µFluidic / IJ

µValves

Fingerprint

sensors

Micro-mirrors

IR-bolometer

Opto (laser, VCSEL)

Mobile µ-Flash

Automotive

General Lighting

Projection engine

PA

MOSFET

IGBT

IPD

DC-DC

converters

Stacked DRAM

StackedNAND

Flash

StackedNOR /

PCRAM

3D SoC

Baseband / DSP

MCU / Processors

Touchscreen

controller

Low-end ASICs

PMIC

3D SiP

Wide IO BB

CPU / GPU

FPGA

High. Perf ASICs

© 2012 • 29

Copyrights © Yole Développement SA. All rights reserved.

PA

Capping IPD Sapphire or

Silicon 3D IPD MOSFET

IGBT & Power MOSFET Power GaN

2012 2014 2016 2018

CIS DSP SOC CIS

BSI CIS

DSP + mem DSP

mem

CIS

SOC CIS

SOC CIS

2010

SOC CIS

2011 2013 2015 2017 2019

3D

WLCSP

FSI

BSI

< 2009 2009

MEMS

ASIC MEMS

Capping

MEMS

ASIC Analog/RF

MEMS Logic

MEMS

Capping

FBAR

Capping

DDR3 stack Hybrid Memory Cube

NAND Flash stack Wide IO stack

LED

Driver

LED

Driver

LED LED

LED LED LED IPD

FPGA FPGA FPGA FPGA

Analog Digital RF Mem. Analog

Digital

ASIC MEMS

Analog

Digital

RF

Mem.

Wide IO FPGA

Wide IO APE

Wide IO

APE

CPU

DDR3 stack

GPU DDR3

Logic

Logic

Logic 3D

SiP/SoC

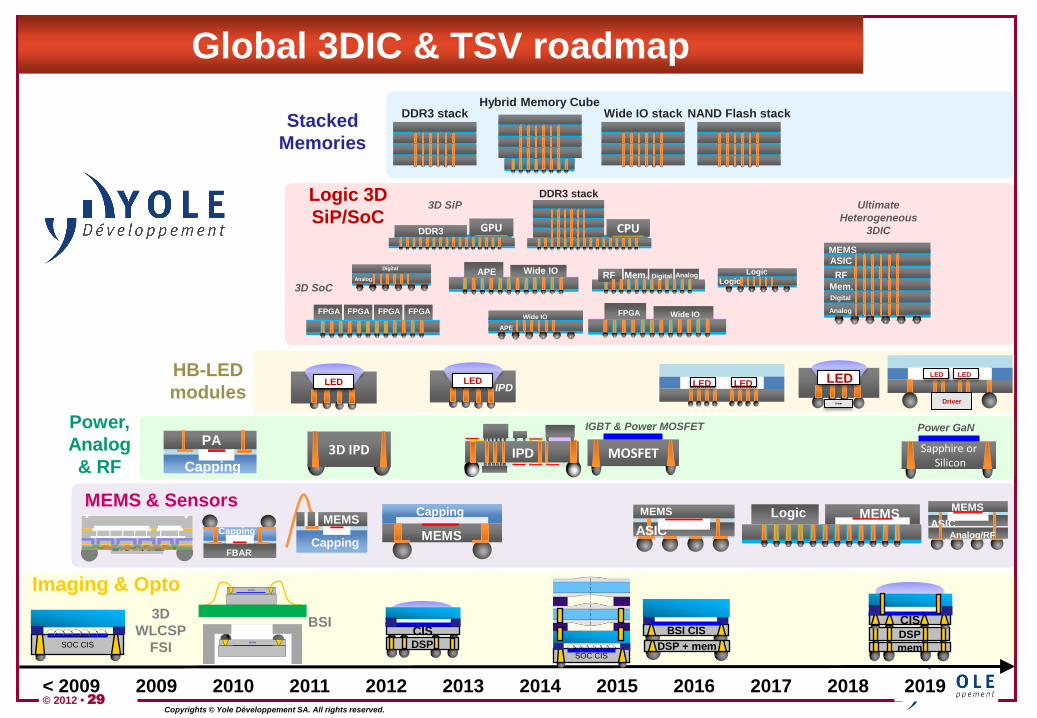

Global 3DIC & TSV roadmap

MEMS & Sensors

Imaging & Opto

Power,

Analog

& RF

Stacked

Memories

HB-LED

modules

3D SoC

3D SiP Ultimate

Heterogeneous

3DIC

© 2012 • 30

Copyrights © Yole Développement SA. All rights reserved.

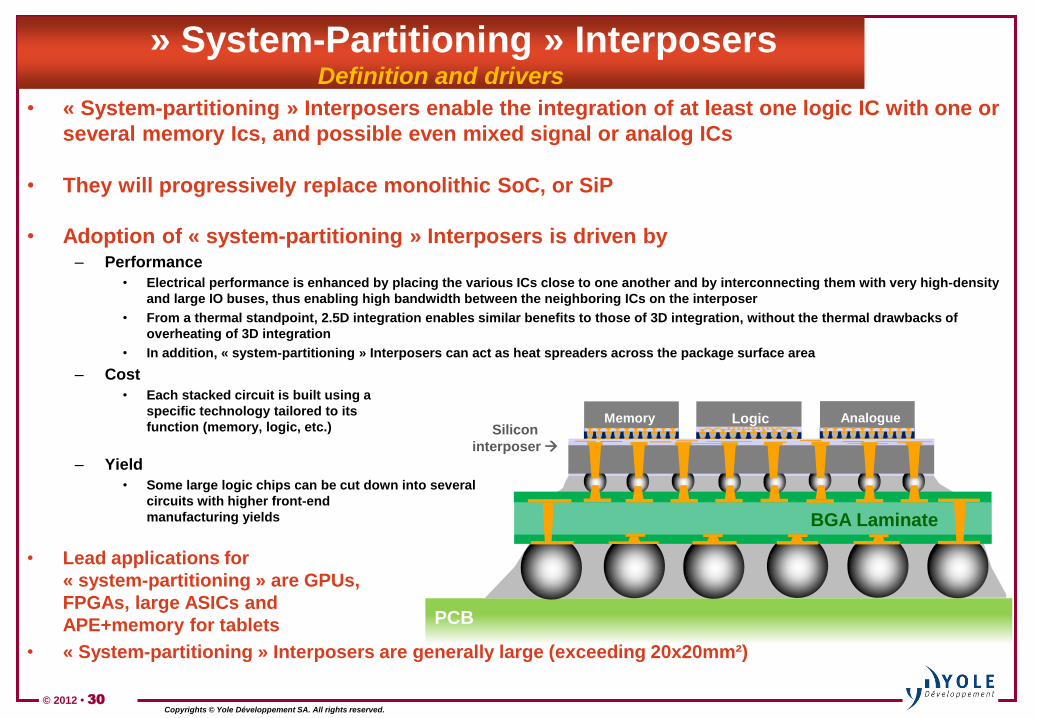

» System-Partitioning » Interposers Definition and drivers

• « System-partitioning » Interposers enable the integration of at least one logic IC with one or

several memory Ics, and possible even mixed signal or analog ICs

• They will progressively replace monolithic SoC, or SiP

• Adoption of « system-partitioning » Interposers is driven by – Performance

• Electrical performance is enhanced by placing the various ICs close to one another and by interconnecting them with very high-density

and large IO buses, thus enabling high bandwidth between the neighboring ICs on the interposer

• From a thermal standpoint, 2.5D integration enables similar benefits to those of 3D integration, without the thermal drawbacks of

overheating of 3D integration

• In addition, « system-partitioning » Interposers can act as heat spreaders across the package surface area

– Cost

• Each stacked circuit is built using a

specific technology tailored to its

function (memory, logic, etc.)

– Yield

• Some large logic chips can be cut down into several

circuits with higher front-end

manufacturing yields

• Lead applications for

« system-partitioning » are GPUs,

FPGAs, large ASICs and

APE+memory for tablets

• « System-partitioning » Interposers are generally large (exceeding 20x20mm²)

PCB

Memory Logic Analogue Silicon

interposer

BGA Laminate

© 2012 • 31

Copyrights © Yole Développement SA. All rights reserved.

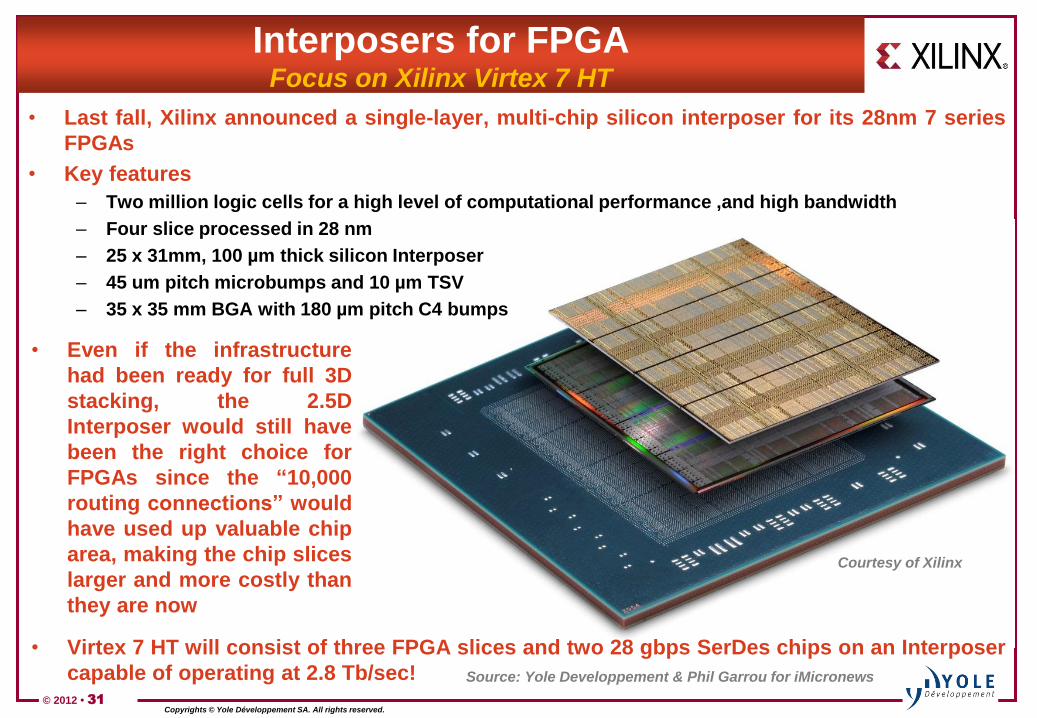

Interposers for FPGA Focus on Xilinx Virtex 7 HT

• Last fall, Xilinx announced a single-layer, multi-chip silicon interposer for its 28nm 7 series

FPGAs

• Key features

– Two million logic cells for a high level of computational performance ,and high bandwidth

– Four slice processed in 28 nm

– 25 x 31mm, 100 µm thick silicon Interposer

– 45 um pitch microbumps and 10 µm TSV

– 35 x 35 mm BGA with 180 µm pitch C4 bumps

• Even if the infrastructure

had been ready for full 3D

stacking, the 2.5D

Interposer would still have

been the right choice for

FPGAs since the “10,000

routing connections” would

have used up valuable chip

area, making the chip slices

larger and more costly than

they are now

• Virtex 7 HT will consist of three FPGA slices and two 28 gbps SerDes chips on an Interposer

capable of operating at 2.8 Tb/sec!

Source: Yole Developpement & Phil Garrou for iMicronews

Courtesy of Xilinx

© 2012 • 32

Copyrights © Yole Développement SA. All rights reserved.

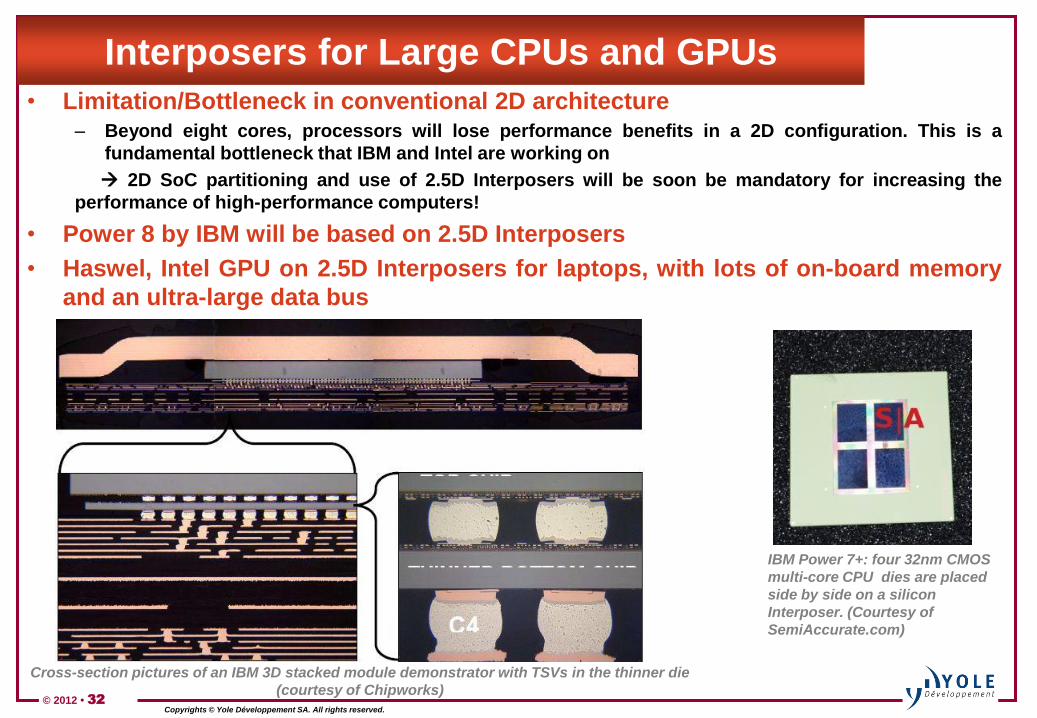

Interposers for Large CPUs and GPUs

• Limitation/Bottleneck in conventional 2D architecture – Beyond eight cores, processors will lose performance benefits in a 2D configuration. This is a

fundamental bottleneck that IBM and Intel are working on

2D SoC partitioning and use of 2.5D Interposers will be soon be mandatory for increasing the

performance of high-performance computers!

• Power 8 by IBM will be based on 2.5D Interposers

• Haswel, Intel GPU on 2.5D Interposers for laptops, with lots of on-board memory

and an ultra-large data bus

IBM Power 7+: four 32nm CMOS

multi-core CPU dies are placed

side by side on a silicon

Interposer. (Courtesy of

SemiAccurate.com)

Cross-section pictures of an IBM 3D stacked module demonstrator with TSVs in the thinner die

(courtesy of Chipworks)

© 2012 • 33

Copyrights © Yole Développement SA. All rights reserved.

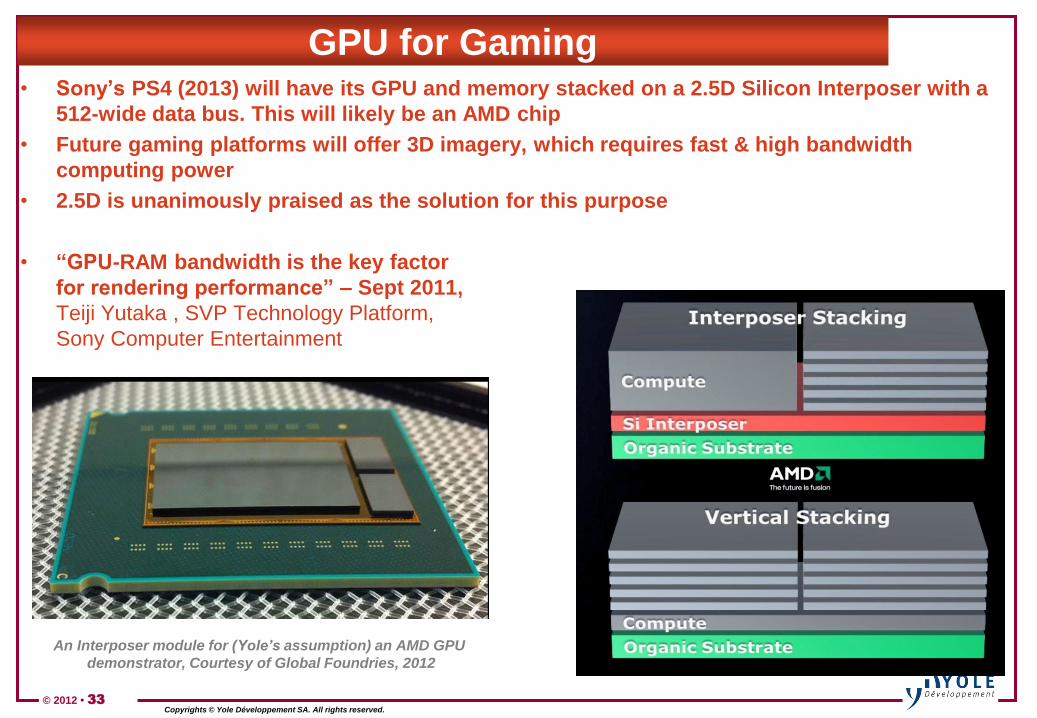

GPU for Gaming • Sony‟s PS4 (2013) will have its GPU and memory stacked on a 2.5D Silicon Interposer with a

512-wide data bus. This will likely be an AMD chip

• Future gaming platforms will offer 3D imagery, which requires fast & high bandwidth

computing power

• 2.5D is unanimously praised as the solution for this purpose

• “GPU-RAM bandwidth is the key factor

for rendering performance” – Sept 2011,

Teiji Yutaka , SVP Technology Platform,

Sony Computer Entertainment

An Interposer module for (Yole’s assumption) an AMD GPU

demonstrator, Courtesy of Global Foundries, 2012

© 2012 • 34

Copyrights © Yole Développement SA. All rights reserved.

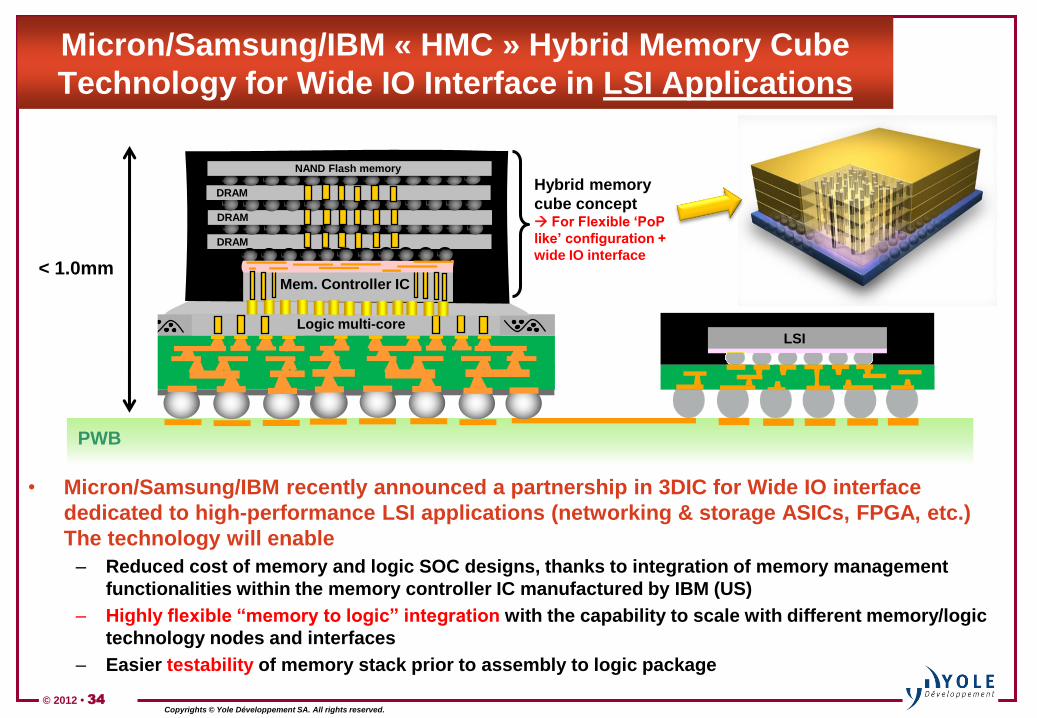

Micron/Samsung/IBM « HMC » Hybrid Memory Cube

Technology for Wide IO Interface in LSI Applications

• Micron/Samsung/IBM recently announced a partnership in 3DIC for Wide IO interface

dedicated to high-performance LSI applications (networking & storage ASICs, FPGA, etc.)

The technology will enable

– Reduced cost of memory and logic SOC designs, thanks to integration of memory management

functionalities within the memory controller IC manufactured by IBM (US)

– Highly flexible “memory to logic” integration with the capability to scale with different memory/logic

technology nodes and interfaces

– Easier testability of memory stack prior to assembly to logic package

LSI

PWB

Logic multi-core

< 1.0mm

DRAM

NAND Flash memory

DRAM

DRAM

Mem. Controller IC

Hybrid memory

cube concept For Flexible „PoP

like‟ configuration +

wide IO interface

© 2012

Copyrights © Yole Developpement SA. All rights reserved.

Conclusions &

Perspectives

© 2012 • 36

Copyrights © Yole Developpement SA. All rights reserved.

Main Conclusions and Perspectives

• 3DIC technology is considered today as a new paradigm for the future of the semiconductor

industry!

– 3DIC will enable several more decades of chip evolution at ever lower cost, higher performance and

smaller-size features

• 3D stacked DRAM and 3D Logic SOC applications are expected to be the biggest drivers for

the volume adoption of 3DIC technology in the next five years, followed by CMOS image

sensors, power devices and MEMS

– Today, the market is driven by high-end applications using 2.5D partitioning Interposers

– Large-die FPGAs and ASICs are on the way to being commercialized for industrial applications, and

are also expected to grow in the near future in the gaming and smart TV markets

• 2013 will likely be the key turning point for the first true implementation of 3DIC technology

in significant volume, driven by the commercialization of hybrid memory cubes

• In terms of value, the 3D TSV market will reach $40B in 2017, growing more than 10 times

faster than the global semiconductor industry!

– Looking closer at the Interposer industry -- as of 2017, Yole expects 2.5D Interposer revenues to

attain 14% of the packaging substrate market value

– 3D WLCSP is the preferred solution today for the efficient assembly of small-size optoelectronic

chips like CMOS image sensors. It is also the most mature 3D TSV platform at the moment, as we

estimate the market to be ~ $270M in 2011 for the “middle-end” processing factories serving this

specific market

© 2012 • 37

Copyrights © Yole Developpement SA. All rights reserved.

Find Out More…

About our company: www.yole.fr

About these markets: www.i-micronews.com