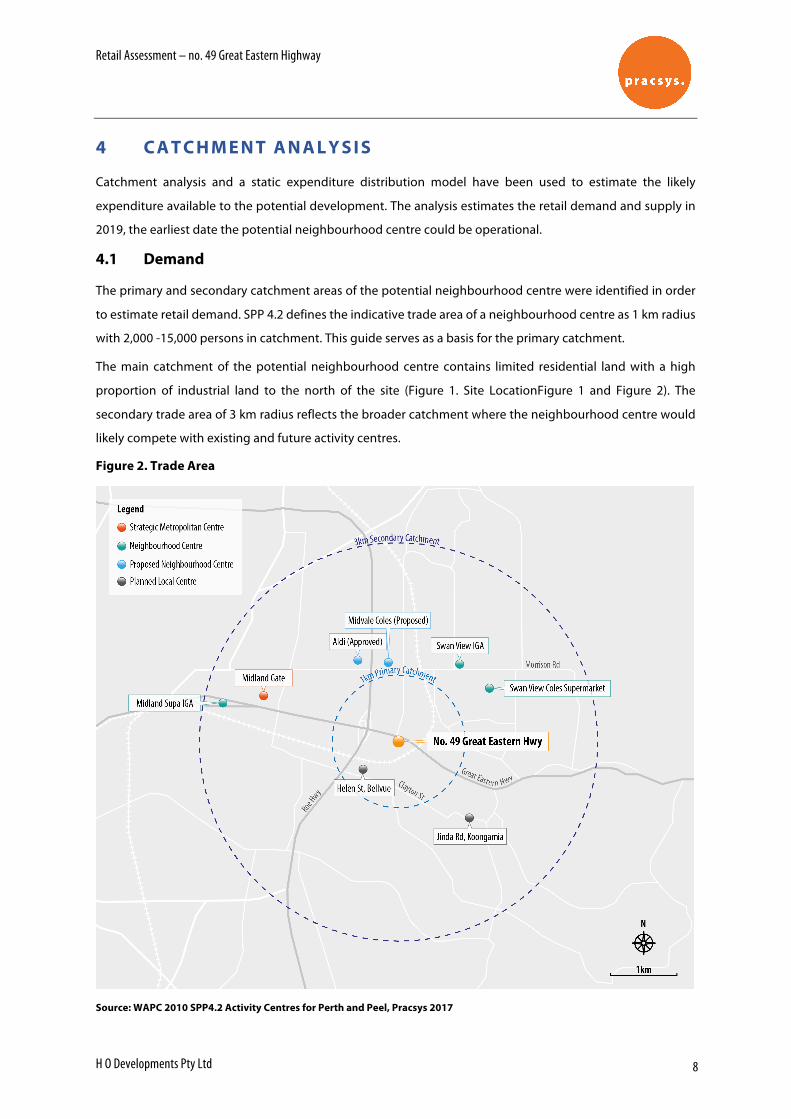

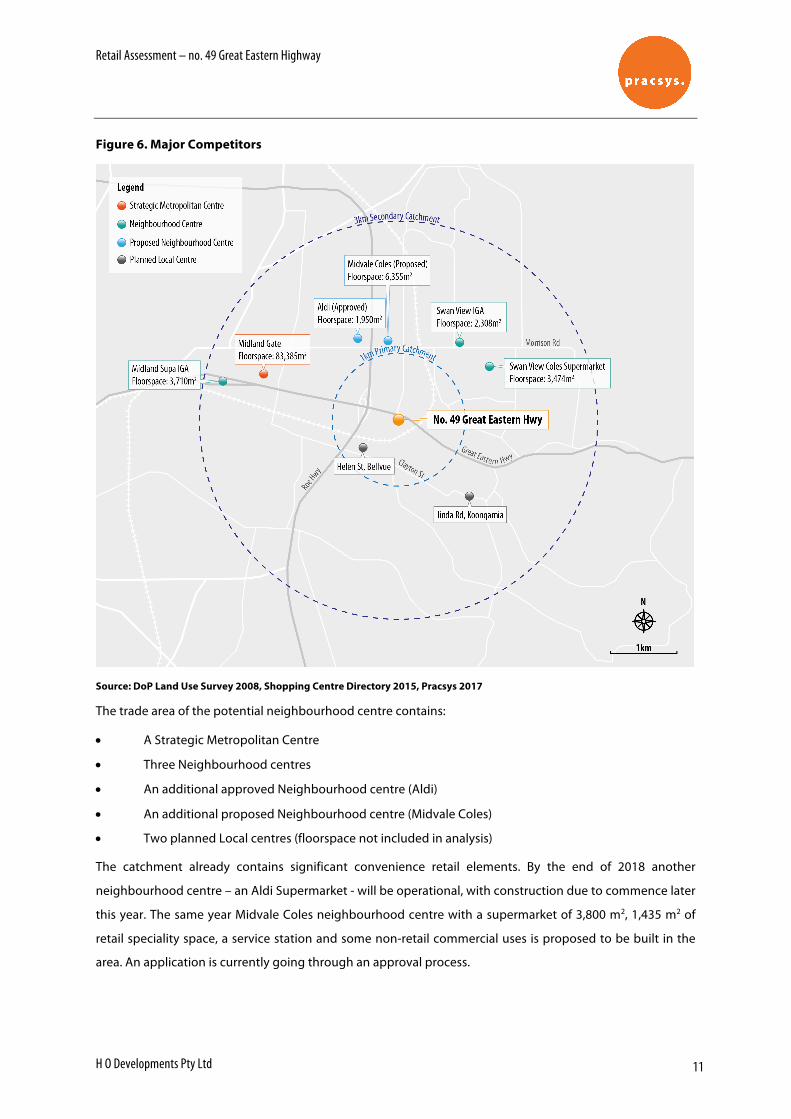

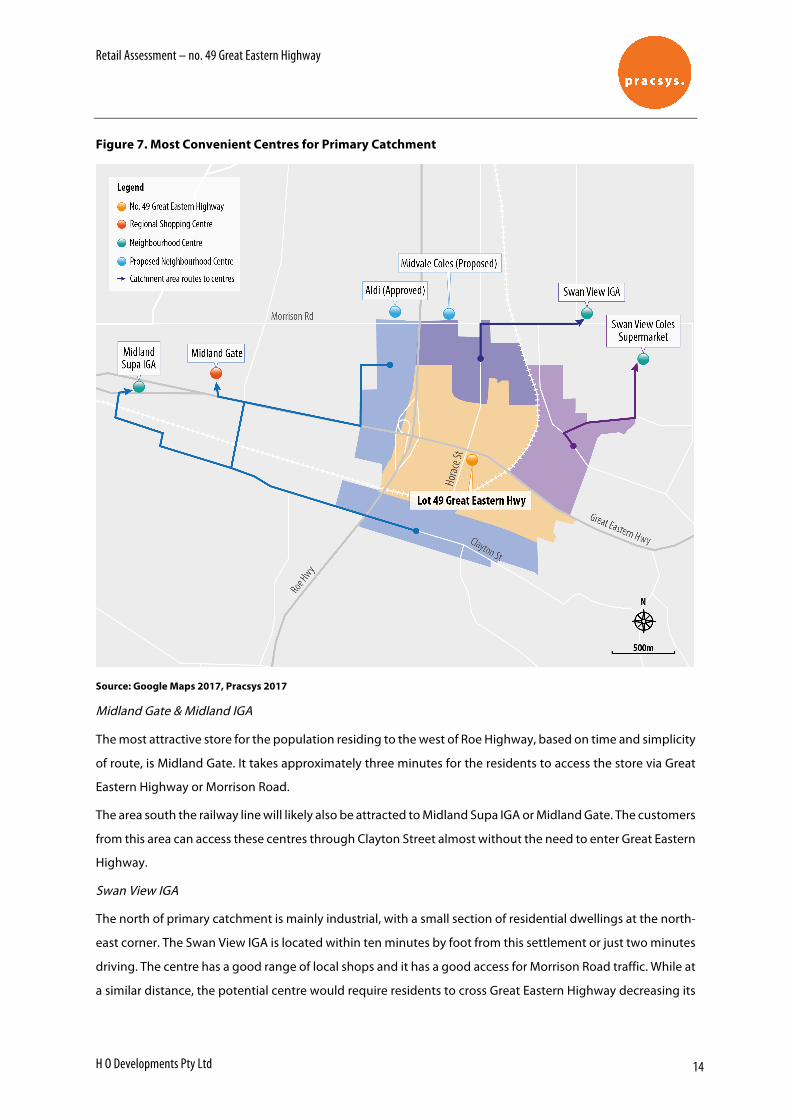

Retail Assessment – no. 49 Great Eastern Highway H O Developments Pty Ltd 8 4 CATCHMENT ANALYSIS Catchment analysis and a static expenditure distribution model have been used to estimate the likely expenditure available to the potential development. The analysis estimates the retail demand and supply in 2019, the earliest date the potential neighbourhood centre could be operational. 4.1 Demand The primary and secondary catchment areas of the potential neighbourhood centre were identified in order to estimate retail demand. SPP 4.2 defines the indicative trade area of a neighbourhood centre as 1 km radius with 2,000 -15,000 persons in catchment. This guide serves as a basis for the primary catchment. The main catchment of the potential neighbourhood centre contains limited residential land with a high proportion of industrial land to the north of the site (Figure 1. Site LocationFigure 1 and Figure 2). The secondary trade area of 3 km radius reflects the broader catchment where the neighbourhood centre would likely compete with existing and future activity centres. Figure 2. Trade Area Source: WAPC 2010 SPP4.2 Activity Centres for Perth and Peel, Pracsys 2017

Transcript

Retail Assessment – no. 49 Great Eastern Highway

H O Developments Pty Ltd 8

4 C A T C H M E N T A N A L Y S I S

Catchment analysis and a static expenditure distribution model have been used to estimate the likely

expenditure available to the potential development. The analysis estimates the retail demand and supply in

2019, the earliest date the potential neighbourhood centre could be operational.

4.1 Demand

The primary and secondary catchment areas of the potential neighbourhood centre were identified in order

to estimate retail demand. SPP 4.2 defines the indicative trade area of a neighbourhood centre as 1 km radius

with 2,000 -15,000 persons in catchment. This guide serves as a basis for the primary catchment.

The main catchment of the potential neighbourhood centre contains limited residential land with a high

proportion of industrial land to the north of the site (Figure 1. Site LocationFigure 1 and Figure 2). The

secondary trade area of 3 km radius reflects the broader catchment where the neighbourhood centre would

likely compete with existing and future activity centres.

Figure 2. Trade Area

Source: WAPC 2010 SPP4.2 Activity Centres for Perth and Peel, Pracsys 2017

Retail Assessment – no. 49 Great Eastern Highway

H O Developments Pty Ltd 9

4.2 Dwellings

ABS Census 2011 data was used to estimate the number of dwellings in the catchment. Dwelling growth to

2019 was estimated based on WA Tomorrow Band C projections (Figure 3).

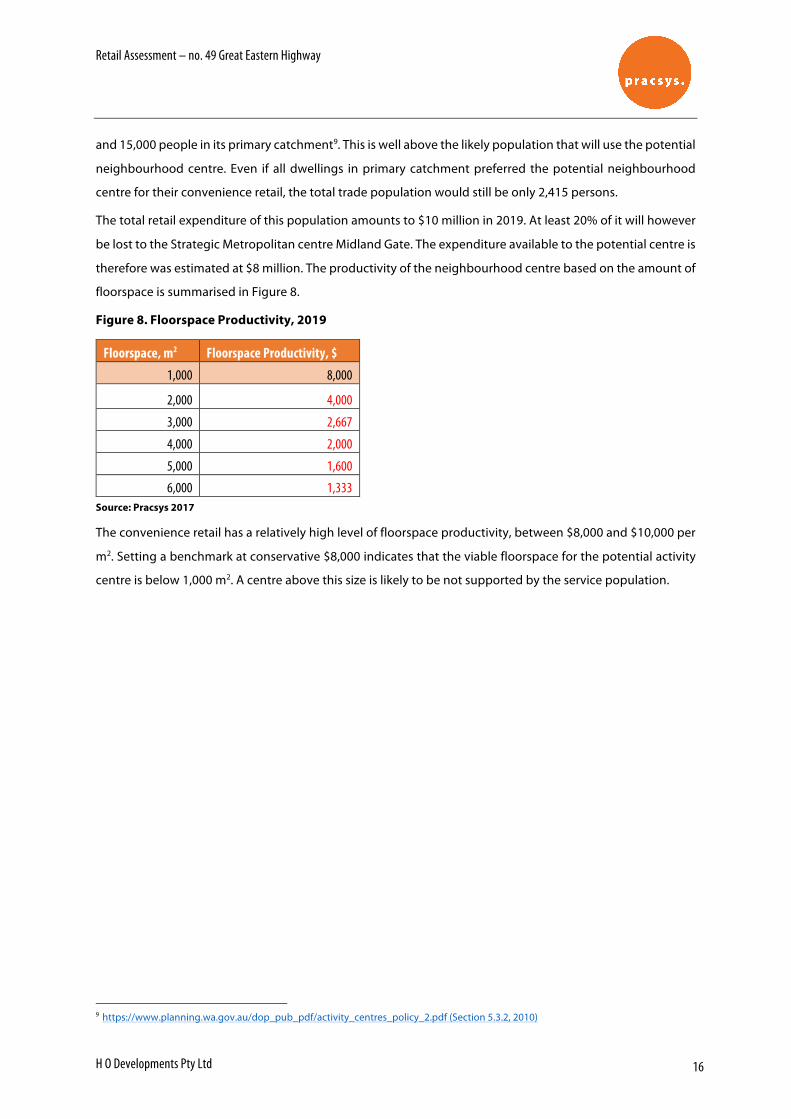

Figure 3. Catchment Area Dwellings, 2019

Source: WA Tomorrow 2015, ABS 201, Pracsys 2017

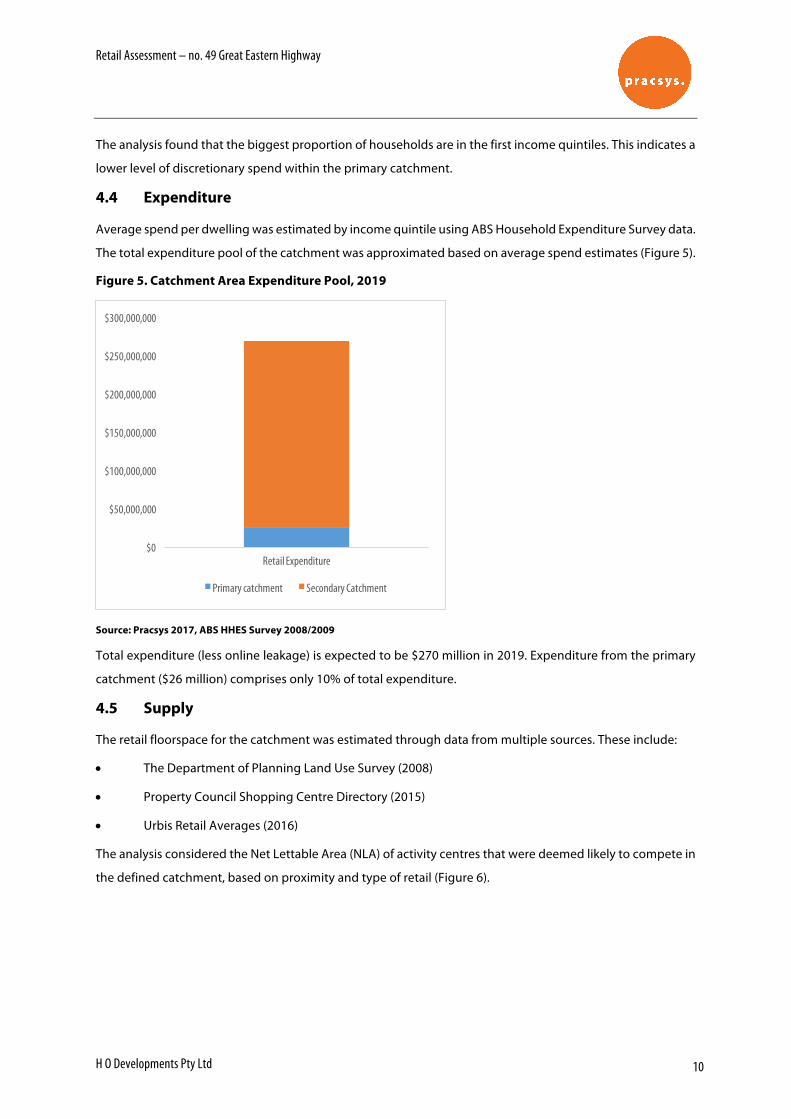

4.3 Catchment Income Profile

ABS Census 2011 data was used to estimate the distribution of income level per dwelling in primary and

secondary catchments (Figure 4).

Figure 4. Catchment Area Population Weekly Income Profile

From a centre design and ongoing management perspective, there are certain economic principles that can

be implemented to ensure that a place is as user-friendly as possible to maximise the number and length of

visits. A successful place must understand what its user groups need and want and provide an environment

that both attracts and retains people.

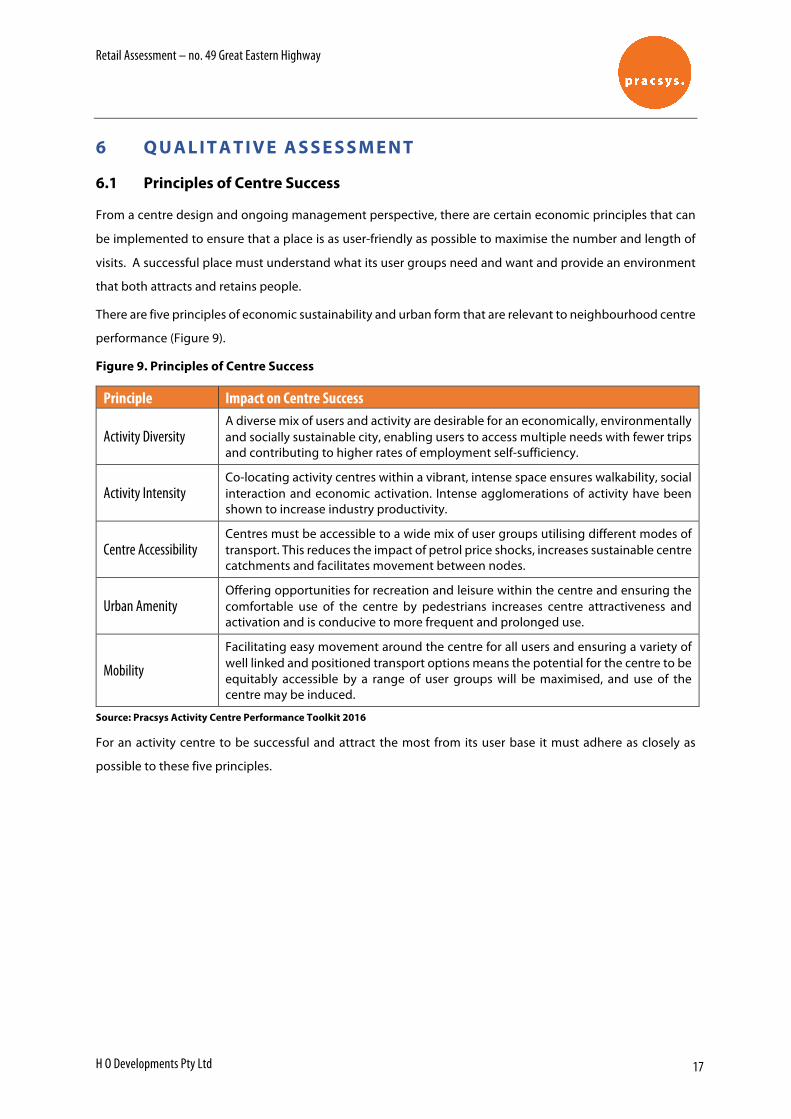

There are five principles of economic sustainability and urban form that are relevant to neighbourhood centre

performance (Figure 9).

Figure 9. Principles of Centre Success

Principle Impact on Centre Success

Activity Diversity A diverse mix of users and activity are desirable for an economically, environmentally and socially sustainable city, enabling users to access multiple needs with fewer trips and contributing to higher rates of employment self-sufficiency.

Activity Intensity Co-locating activity centres within a vibrant, intense space ensures walkability, social interaction and economic activation. Intense agglomerations of activity have been shown to increase industry productivity.

Centre Accessibility Centres must be accessible to a wide mix of user groups utilising different modes of transport. This reduces the impact of petrol price shocks, increases sustainable centre catchments and facilitates movement between nodes.

Urban Amenity Offering opportunities for recreation and leisure within the centre and ensuring the comfortable use of the centre by pedestrians increases centre attractiveness and activation and is conducive to more frequent and prolonged use.

Mobility

Facilitating easy movement around the centre for all users and ensuring a variety of well linked and positioned transport options means the potential for the centre to be equitably accessible by a range of user groups will be maximised, and use of the centre may be induced.

Source: Pracsys Activity Centre Performance Toolkit 2016

For an activity centre to be successful and attract the most from its user base it must adhere as closely as

possible to these five principles.

Retail Assessment – no. 49 Great Eastern Highway

H O Developments Pty Ltd 18

6.2 Multi-criteria Analysis

A multi-criteria analysis has been designed to rank the performance of the potential neighbourhood centre

against the principles of centre success. The analysis is summarised in Figure 10.

Figure 10.Multi-criteria Analysis

Principle Potential Neighbourhood Centre

Activity Diversity

A neighbourhood centre generally provides for daily and weekly household shopping needs and a small range of convenience services. A diverse mix of users are desirable for a sustainable centre.

The tenancy mix of the potential centre is unknown, however due to the restricted amount of floorspace available (after the parking requirements of 4 bays per 100m2 of floorspace are satisfied) and site location, it is unlikely that the centre will be able to offer a wide range of speciality shops.

Score 2/5

Activity Intensity

The site is located in a predominantly industrial area with a limited number of residential dwellings. The primary catchment area in 2019 is expected to have an estimated dwelling per gross hectare ratio of 3:1. Successful neighbourhood centres should be located within an intense residential development and directly linked to its service population.

Score 1/5

Centre Accessibility

The site is located on a major road, Great Eastern Highway, and is separated from its catchment to the south by the railway and to the west by Roe Highway. The site has a limited access from Great Eastern Highway eastbound. Walkable catchment is particularly important for a neighbourhood centre. The node between Great Eastern Highway and the railway is the only segment of population which can safely and easily access the neighbourhood centre by foot. The population to the north of the site will have to walk a great distance through an industrial area and across a busy road to access the centre. The catchment to the south of the site would have to walk around the railway to find an access point to the site.

Score 1/5

Urban Amenity The site is exposed to continuing noise emission from the Great Eastern Highway and provides limited opportunity for comfortable use of the centre by pedestrians. These factors will decrease the centre’s attractiveness.

Score 1/5

Mobility

Despite being located on the arterial road, it does not provide a wide range of transport options. It is inconvenient for the eastbound traffic to access the centre due to the busy road conditions. Regarding public transport, there is a bus stop across from the site. There is only a bus route along Great Eastern Highway, which implies that it doesn’t improve the access to the centre from the south and north of the site. Walkability has been discussed in Centre accessibility principle.

Score 2/5

Average Score 7/25

Source: Pracsys 2017

Retail Assessment – no. 49 Great Eastern Highway

H O Developments Pty Ltd 19

The multi-criteria analysis highlights a low feasibility of potential centre success. As shown, the site’s location

and characteristics significantly limit the potential neighbourhood centre’s ability to attract and retain a

sufficient user catchment. It is, therefore, evident that the potential centre is unlikely to be a positive addition

to a local activity centre network.

Retail Assessment – no. 49 Great Eastern Highway

H O Developments Pty Ltd 20

7 C O N C L U S I O N

The purpose of the analysis was to explore the feasibility and sustainability of the potential activity centre

located at no. 49 Great Eastern Highway.

The analysis identified the following factors:

• Previous local centres had not been successful at the same site

• There is a limited number of residential dwellings in the primary catchment as the area to the north

and the west of the site is predominantly industrial

• There is a lower level of discretionary spend within the primary catchment as most dwellings earn

below $600 a week

• A large proportion of the expenditure is already captured by Midland Gate (a Strategic Metropolitan

centre) and existing neighbourhood centres. Additionally, floorspace expansions, to be completed in

2018, have already been accepted for Midland Gate and an Aldi in the proposed centre’s primary

catchment, further reducing the potential expenditure available to the potential centre

A multi-criteria analysis was used to assess the potential centre against activity centre principles including

diversity, intensity, accessibility, urban amenity and mobility. The arguments include:

• The potential centre is exposed to the small number of residential dwellings

• The site is safely and conveniently accessible by foot only to a small proportion of population located

in the node between Great Eastern Highway and the railway

• The site is exposed to a continuing noise emission from the Great Eastern Highway and provides a

limited opportunity for a comfortable use of the centre by pedestrians

• Despite sites location on the arterial road, it does not provide a wide range of transport and walking

options

The analysis found that the No. 49 Great Eastern Highway development is not likely to be viable as a

neighbourhood centre. Modelling results indicated the potential upper bound of viable floorspace in 2019 is

approximately 1,000 m2, equivalent to a local centre in size. The assessment of the site against activity centre

principles concluded that a neighbourhood centre located at the site is unlikely to be successful and would

not be a positive addition to the activity centre network in the area. It is recommended that the proposed site

is not developed as a neighbourhood centre.

31 March 2017 Our Ref: 17058

Leon Van der Linde Manager Strategic Planning City of Swan By email: [email protected]

Dear Leon,

Re: Bellevue East Neighbourhood Centre Advice

The Bellevue East Land Use Study (BELUS) provides a framework for the future use and development of land in Bellevue East. BELUS was adopted by Council in August 2013 and identified land for the consolidation of a Neighbourhood Centre (referred to as the Horace Street NC) at the intersection of Great Eastern Highway and Horace Street.

H O Developments Pty Ltd own land at 49 Great Eastern Highway and are proposing the development of a service station. The proposal is currently subject to an application to the Metro East JDAP, and the City of Swan are concerned the proposal will limit the ability for a Neighbourhood Centre to be developed in Bellevue East.

In support of the proposal, information has been provided by the City of Swan which includes the following:

A letter from Moharich & More describing the statutory and policy framework

A report by Urbis that provides further information on the proposal and examples of where retail centres are co-located with service stations

A Retail Assessment prepared by Pracsys assessing the demand for a Neighbourhood Centre at the subject site.

Essential Economics recently prepared the draft City of Swan Local Commercial Activity Centre Strategy (LCACS). The draft LCACS identifies potential for either a Local Centre or a Neighbourhood Centre in Bellevue East (referred to as Horace Street in the LCACS). We are currently reviewing submissions on the Strategy received during the public exhibition period.

With regard to Bellevue East and the proposed service station, the City has requested the following advice:

A review of the economic components of the proposal (including Pracsys report)

Analysis of whether a Neighbourhood or Local Centre could be supported at the site

Views on the implications of the proposed service station on the future opportunities for either a Local or Neighbourhood Centre.

This letter provides a high level analysis of the future opportunities for a centre at Bellevue East and includes the following information:

Overview of the subject site and proposed development

Review of the Pracsys report

Overview of considerations for the development of Local and Neighbourhood Centres

A high-level retail demand assessment

Discussion of the implications associated with the proposed service station.

1 Subject Site and Proposed Developments

BELUS identified the opportunity for a Neighbourhood Centre on land located at the intersection of Great Eastern Highway and Horace Street. This site, shown in Figure 1, contains land to the south of Great Eastern Highway, and to the east and west of Horace Street. In total, 10,370m2 of land has been identified for the future use as a Neighbourhood Centre, including the following:

7,075m2 of land to the east of Horace Street

3,295m2 of land to the west of Horace Street in two separate parcels.

The site currently contains a variety of retail and commercial uses, including the following retail uses:

Lunch bar

Indian restaurant

Thirsty Camel bottle-shop

Chinese Restaurant.

In addition, a number of non-retail commercial businesses are also located on the site and these include a TAB, printing shop, pools and pumps, and forklift stores.

3

H O Developments are proposing the development of a service station on land at 49 Great Eastern Highway, which is situated on land to the east of Horace Street identified for a Neighbourhood Centre in BELUS. The site of the proposed service station is shown in Figure 1.

Figure 1: BELUS Neighbourhood Centre and Proposed Service Station Site

Produced by Essential Economics using MapInfo, StreetPro and Nearmap

2 Review of Pracsys Report

Pracsys were engaged by H O Developments Pty Ltd to investigate the viability of a neighbourhood centre at 49 Great Eastern Highway. In particular, the Pracsys analysis sought

4

to identify the size of a neighbourhood centre that could be supported at the site. Their report provided the following information:

A review of relevant policies, including State Planning Policy 4.2 (SPP 4.2), City of Swan Commercial Centres Strategy (2004), the draft Local Commercial and Activity Centres Strategy (2016), and the BELUS.

Analysis of the potential catchment of a neighbourhood centre

Review of the network of competing centres

Analysis of the likely expenditure

Assessment of the ‘local activation potential’.

The Pracsys report concluded that a neighbourhood centre would not be viable, and that a local centre comprising approximately 1,000m2 retail floorspace and achieving average sales of $8,000/m2 is the more likely outcome.

We have reviewed the Pracsys report and make the following comments:

1 Clarification on commentary relating to the draft LCACS: Pracsys correctly state that the draft LCACS identifies the potential for a Neighbourhood or a Local Centre. However, Pracsys’ commentary implies the draft LCACS specifically makes comments relating to the potential for alternative uses at the Horace Street NC, including a petrol station.

For the purpose of clarification, the draft LCACS states the following in relation to Local Centres, not the Horace Street centre specifically:

“…it is acknowledged that local centres have been subject to an increasingly competitive environment, with many centres struggling to attract the required investment to remain commercially viable. In cases where the retention of a commercially viable local centre is no longer a realistic opportunity, these centres may be considered for an alternative use.” (p45, draft LCACS)

In addition, the draft LCACS does not make any acknowledgement of the potential for a convenience store attached to a petrol station at the Horace Street centre (that is not to say potential does not exist for such a development).

2 Confusion between the Primary Catchments used in the analysis: The Pracsys report appears to adopt two different catchments. The first catchment is based on a 1km (Primary Catchment) and 3km (Secondary Catchment) radii from the subject site and references SPP 4.2 as the basis for using these catchments. According to the Pracsys report, the 1km (Primary Catchment) will accommodate 1,047 dwellings in 2019 or a population of approximately 2,500 people (assuming an average household size of 2.4 persons) who will have a retail expenditure of approximately $26 million in 2019.

5

However, it appears the retail analysis is based on an alternative Primary Catchment derived using drive-time analysis. According to Pracsys, this alternative catchment will accommodate only 850 residents in 2019 and retail spending of $10 million. While we prefer to use catchments which take into consideration the level of access to a centre and location of competing centres, we believe a centre at the Subject Site would capture trade from a slightly different trade area (our trade area is identified later in this Letter). We also believe that trade areas overlap and this reflects the real-world practise of residents having a choice of centres.

3 Methodology used for assessing retail development potential: In order to undertake a detailed review of the retail demand assessment, further clarity is required regarding which catchments are used. However, we note that the Pracsys analysis does not take into consideration the following:

- Potential for a centre to capture trade from beyond either of its identified catchments. This is an important consideration for the site in view of its location on the Great Eastern Highway (attracting passing trade) and proximity to a major employment area (attracting the expenditures of non-residents).

- The potential for a supermarket to be attracted to the site. As supermarkets typically act as anchor tenants for neighbourhood centres, the viability of a supermarket should be assessed when assessing the overall potential for a neighbourhood centre.

- Potential for non-retail uses that would typically locate in a neighbourhood centre.

3 Considerations for the Development of a Local or Neighbourhood Centre at Bellevue East

While the land identified for the Horace Street NC fronting the Great Eastern Highway is currently zoned Highway Service, the presence of a number of convenience stores indicates the locality is currently serving a role a ‘quasi’ Local Centre.

The future opportunities for a viable and well-functioning activity centre at Bellevue East, whether it is a Local Centre or a Neighbourhood Centre, are influenced by a variety of factors. A brief overview of these considerations is provided below.

Competition

Residents in Bellevue and the surrounding areas are served by the following centres which contain neighbourhood level retail facilities:

Midland Gate is the main shopping location in the Midland Strategic Metropolitan Centre (SMC). Midland is a regional-level shopping centre providing a wide variety of convenience and comparison shopping.

6

Swan View is a Neighbourhood Centre located 1.6km to the north-east. The centre is anchored by a Coles supermarket.

Darling Ridge is a small neighbourhood centre located 1.5km to the north-east anchored by an IGA.

Helena Valley Shopping Centre is a Neighbourhood Centre located 2.2km to the south and is anchored by an IGA supermarket.

In addition, proposals exist for a Neighbourhood Centre on Morrison Road and an ALDI supermarket in another location on Morrison Road. The draft City of Swan LCACS identifies the potential for a new Neighbourhood Centre in this locality.

Exposure to Great Eastern Highway

The Great Eastern Highway is a major transport route connecting the eastern parts of metropolitan Perth to regional areas further to the east and north. Future retailers at a centre in Bellevue will be able to capture a share of their turnover from the high level of passing traffic.

Accessibility to the Site

Access to the site will be via the Great Eastern Highway and Horace Street. A signalised intersection at Horace Street/Great Eastern Highway will enable access to the centre from the north via Farrell Road.

Constraints Limiting its Trade Area

A number of physical and perceived constraints may limit the geographic areas of a trade area for a centre at Bellevue. These constraints include:

Railway line to the south, limiting vehicle access. It is noted that a pedestrian walkway is provided at the end of Bellevue Road.

Great Eastern Highway is a six-lane separated highway at the intersection of Horace Street; this can be seen as a perceived constraint for potential customers travelling westward along the Great Eastern Highway.

Roe Highway limits the extent to which a trade area would extent to the west.

The major employment area to the north limits the extent of a residential catchment to the north.

7

Employment Areas

According to 2011 ABS Census of Population and Housing data, almost 1,700 jobs are provided in the major employment areas situated to the immediate north of the Great Eastern Highway. Potential exists for a centre in Bellevue to capture a share of retail spending from these workers. (Note that 2016 Census data not yet available).

Potential for Increased Residential Density

BELUS identifies potential for a significant increase in residential densities. For instance, areas surrounding the planned Neighbourhood Centre are nominated to be zoned R60. The proposed R60 areas are currently zoned R40 and accommodate 40 dwellings. Under the proposed R60 zone they could potentially accommodate a total of approximately 175 dwellings, or a net increase of 135 dwellings.

The development of a well-functioning centre, either Local or a Neighbourhood Centre, will be an important component of creating a level of amenity that would be required to attract investment into medium-density housing in the area. When planning for a centre in the BELUS area, consideration of the potential residential outcome arising from the implementation of BELUS should to be considered.

Capacity of Land Planned for the BELUS Neighbourhood Centre

The site identified for the Horace Street Neighbourhood Centre accounts for a total of 10,370m2 of land (or approximately 1.0ha). In our experience in planning for single-level neighbourhood centres throughout Australia, it is prudent to plan for floorspace equivalent to approximately 1/3 of the land area. The eventual floorspace will depend on site-specific requirements.

On this basis, land identified for the Horace Street centre could accommodate approximately 3,500m2 of floorspace.

4 Retail Assessment

A high-level assessment of the potential for a Neighbourhood Centre at Horace Street is provided below which takes into consideration aspects discussed previously in this Letter, along with the following:

A trade area to be served by a neighbourhood centre