107

New Horizons for China Petrochemical Industry March 25 th 2019

New Horizons for China Petrochemical Industry

������ ����� �� � � � ���� � � ����������� ������

�������� �March 25th 2019

CONTENTS 1

2

3

B : C : C : A B FA C: B :

4

FF : / B

: : : :

:

B E :

&

E :

E G E

&

: C & &&

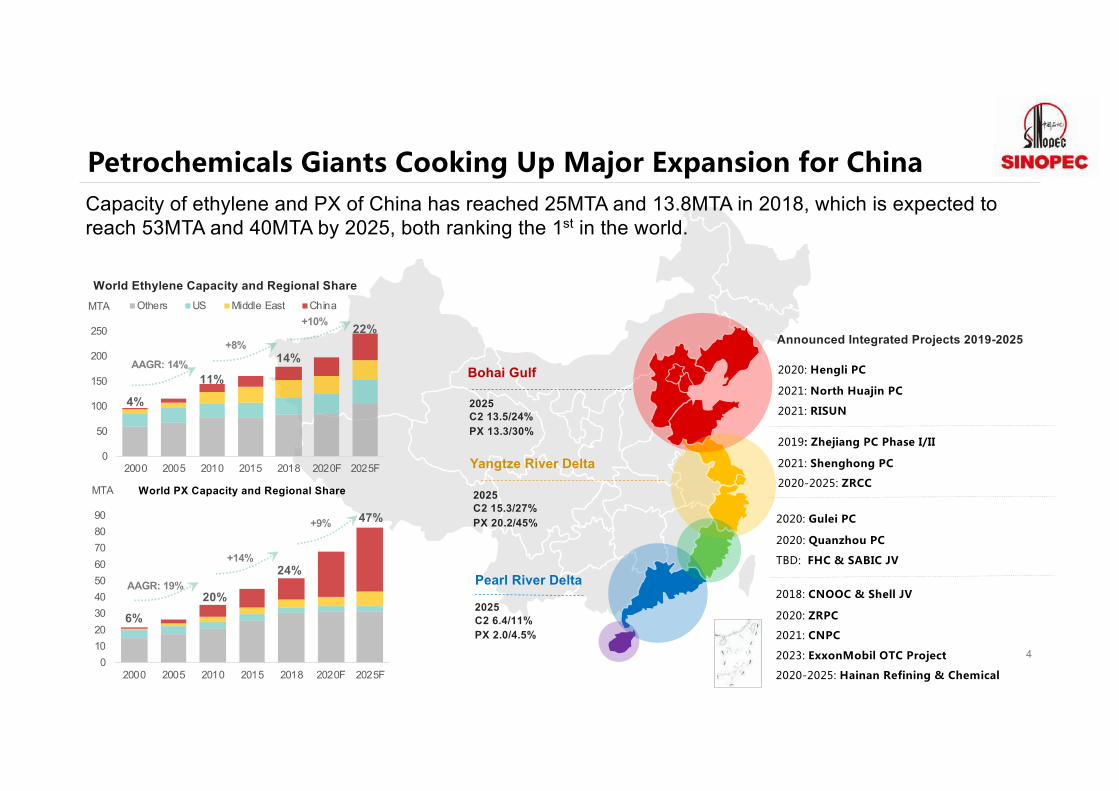

Bohai Gulf

Yangtze River Delta

Pearl River Delta

Announced Integrated Projects 2019-2025

2025C2 13.5/24%PX 13.3/30%

2025C2 15.3/27%PX 20.2/45%

2025C2 6.4/11%PX 2.0/4.5%

4%

11%14%

22%

0

50

100

150

200

250

2000 2005 2010 2015 2018 2020F 2025F

MTA Others US Middle East China

Capacity of ethylene and PX of China has reached 25MTA and 13.8MTA in 2018, which is expected to reach 53MTA and 40MTA by 2025, both ranking the 1st in the world.

+10%

AAGR: 14%

+8%

World Ethylene Capacity and Regional Share

6%20%

24%

47%

0102030405060708090

2000 2005 2010 2015 2018 2020F 2025F

MTA

AAGR: 19%

+14%

+9%

World PX Capacity and Regional Share

5

China alone contributes 50-70% of the new capacity during another two round of expansion in 2019 and 2023.

Average Annual New Capacity of Basic Petrochemicals

1996-2000 2007-2009 2012-2013 2018-2019 2021-2025Note: Basic chemicals including ethylene, propylene, butadiene, benzene, toluene, PX and methanol

MTA14

3021

1525

MTA

MTA

MTAMTA

11%

45%69%

55%

44%

China Middle East US Others

7

China still holds the largest share of world petrochemicals demand, which is expected to maintain a high growth after the recent booming period. Demand of synthetic resin, fiber and rubber is expected reach 135MTA, 60MTA and 3.2MTA respectively by 2025.

16%

30%

38%

40%

0

50

100

150

200

250

300

350

2000 2010 2019F 2025F

MTA

Others Middle East US China

AAGR 11%

7%

6%

Share and Growth of Synthetic Resin Demand

30%

63%

71%

74%

0

10

20

30

40

50

60

70

80

90

2000 2010 2019F 2025F

MTA

Others Middle East US China

Share and Growth of Synthetic Fiber Demand

14%

6.5%

5.5%

10%22%

25%

27%

0

2

4

6

8

10

12

2000 2010 2019F 2025F

MTA

Others Middle East US China

9.7%

4.5%

3.8%

Share and Growth of Synthetic Rubber Demand

8

World petrochemicals demand are recovering from years before, growth of which outruns the world GDP. China, as a key driver, is expects to hold 1% higher than the world average demand growth by 2025.

AAGR of World Synthetic Resin, Fiber and Rubber Demand

3.9%2011-2014 2015-2016

4.0%2017-2019 2020-2025

5.1% 4.2%2.6%2007-2010

5.1%4.8%5.2%

6.0%

8.0%China

World Avg.

China per capita consumption of petrochemicals is catching up with Japan and Europe in the coming years. But 43kg(in equivalent ethylene) still has a long way to go compared with South Korea(89-90kg) and U.S.(70-80kg).

9Consumption per capita of Equivalent Ethylene vs GDP per capita from 1990-2025

0

10

20

30

40

50

60

70

80

90

100

0 10000 20000 30000 40000 50000 60000 70000 80000

Kg per person

GDP per capita, $

China

South Korea

US

Japan

Europe2018

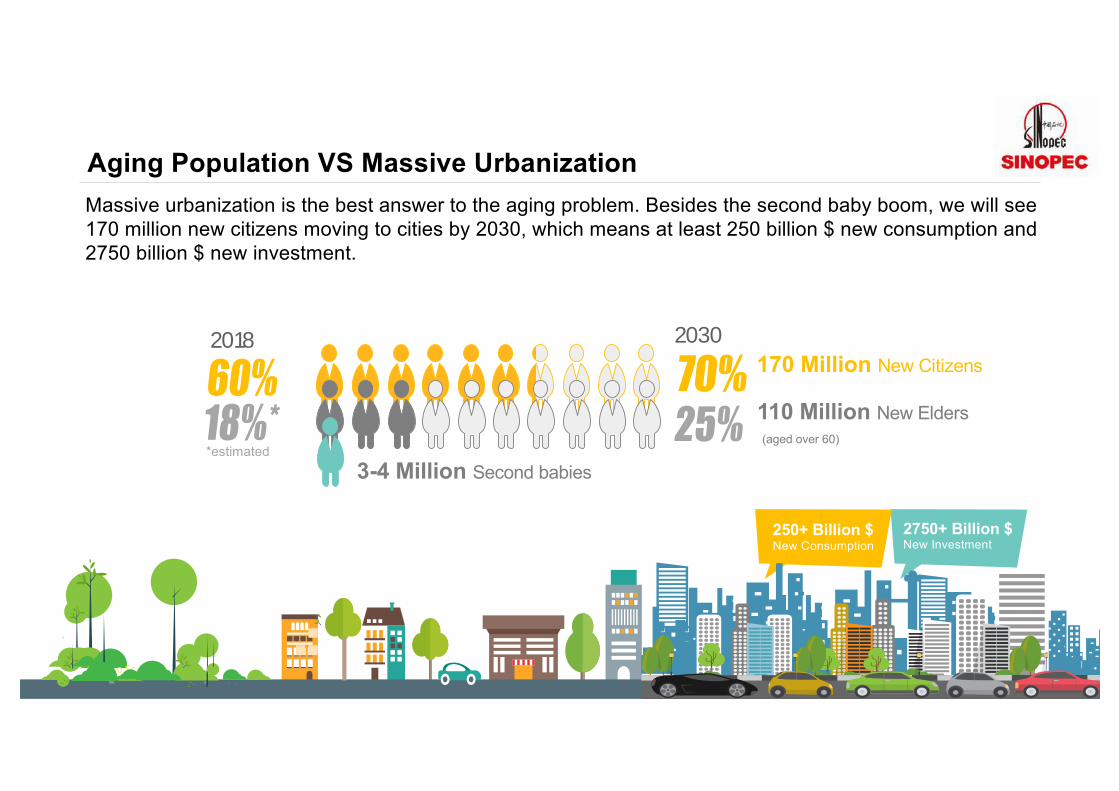

Aging Population VS Massive Urbanization

10

Massive urbanization is the best answer to the aging problem. Besides the second baby boom, we will see 170 million new citizens moving to cities by 2030, which means at least 250 billion $ new consumption and 2750 billion $ new investment.

250+ Billion $ New Consumption

2750+ Billion $ New Investment

2018 2030170 Million New Citizens

110 Million New Elders(aged over 60)

3-4 Million Second babies*estimated

Explosive Growth of E-commerce Boosting the Polymers Demand

11

Billions of online orders and catering services are creating a whole new area for polymers consumption,which is growing by 20-30% each year and increasing the demand of polyolefins by 1-2%.

50Billion

Packages

250-300KTPE/PP

50-60KTPE/PP

20% 20-30%8 BillionOrders

更多行业精品报告,登陆东西智库(dx2025.com)下载

New Demand from Environmental Protection Business

12

Recycling rate of China has been much higher than the average of the world, which makes it harder to getsignificantly improved in years, together with waste plastics import ban, increased the virgin PE demand by0.7-1.0 million ton. While air-pollution control regulation has driven the natural gas pipeline demand by 10%.

-

0

3000

6000

9000

2015 2016 2017 2018 2019

KT

New Polymers Replacement Waste Ethyl Polymers ImportWaste Ethyl Polymers Production

AAGR: -12%

0

100

200

300

400

500

2017 2018 2019

KT

New Consumption from Fuel Changing PolicyPE Consumption for Pipeline

- - - -

AAGR: 10.3%

- -

EU30%

China25%

World18%

U.S.9%

Sources: Roland Geyer, Jenna R. Jambeck, Kara Lavender Law

2015 2020 2025 2030

65

99

145

12%

10%

8.9%Billion $

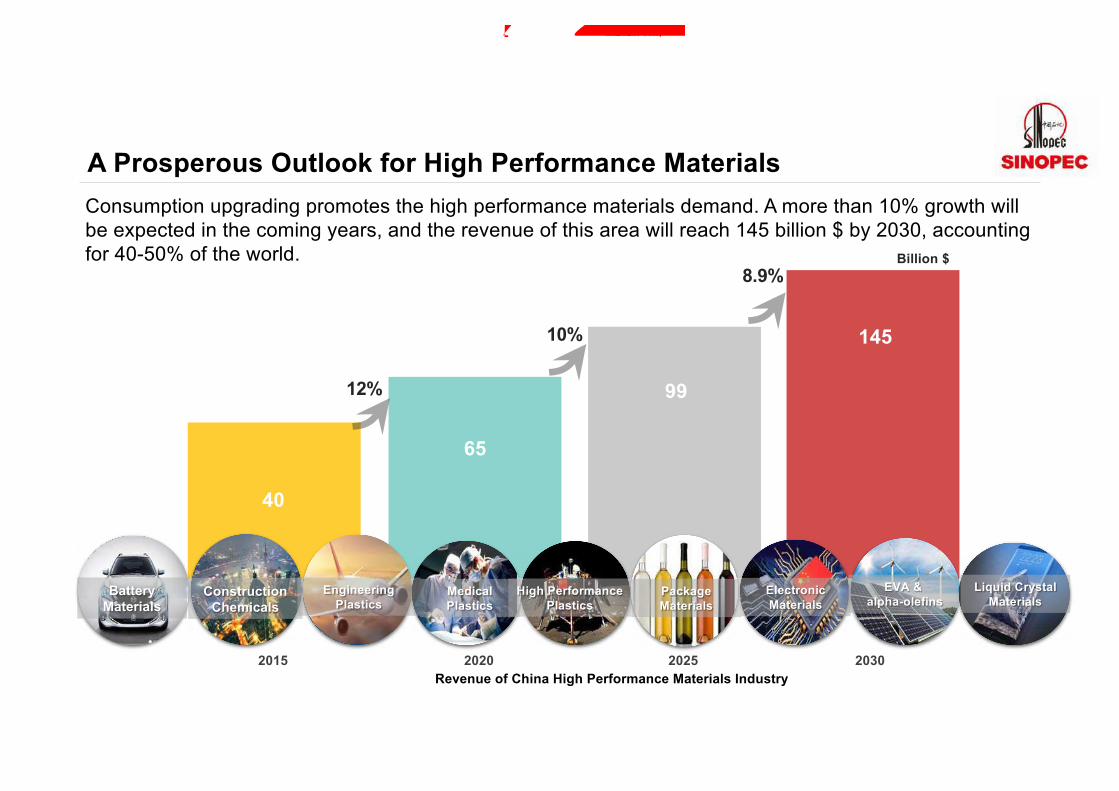

A Prosperous Outlook for High Performance MaterialsConsumption upgrading promotes the high performance materials demand. A more than 10% growth will be expected in the coming years, and the revenue of this area will reach 145 billion $ by 2030, accounting for 40-50% of the world.

40

BatteryMaterials

ConstructionChemicals

EngineeringPlastics

MedicalPlastics

PackageMaterials

ElectronicMaterials

EVA &alpha-olefins

Liquid CrystalMaterials

High PerformancePlastics

Revenue of China High Performance Materials Industry

更多行业精品报告,登陆东西智库(dx2025.com)下载

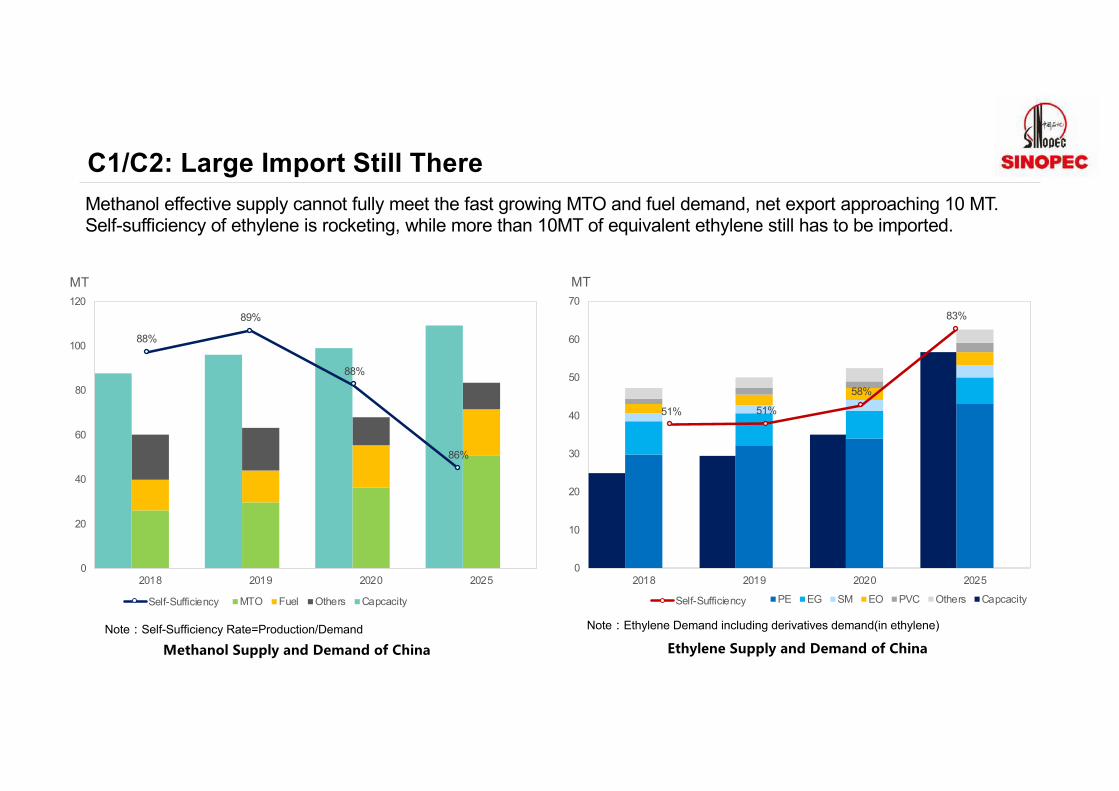

C1/C2: Large Import Still ThereMethanol effective supply cannot fully meet the fast growing MTO and fuel demand, net export approaching 10 MT.Self-sufficiency of ethylene is rocketing, while more than 10MT of equivalent ethylene still has to be imported.

Note�Self-Sufficiency Rate=Production/Demand

0

20

40

60

80

100

120

2018 2019 2020 2025

MT

MTO Fuel Others Capcacity

88%

89%

88%

86%

Self-Sufficiency

0

10

20

30

40

50

60

70

2018 2019 2020 2025

MT

PE EG SM EO PVC Others Capcacity

Note�Ethylene Demand including derivatives demand(in ethylene)

51% 51%

58%

83%

Self-Sufficiency

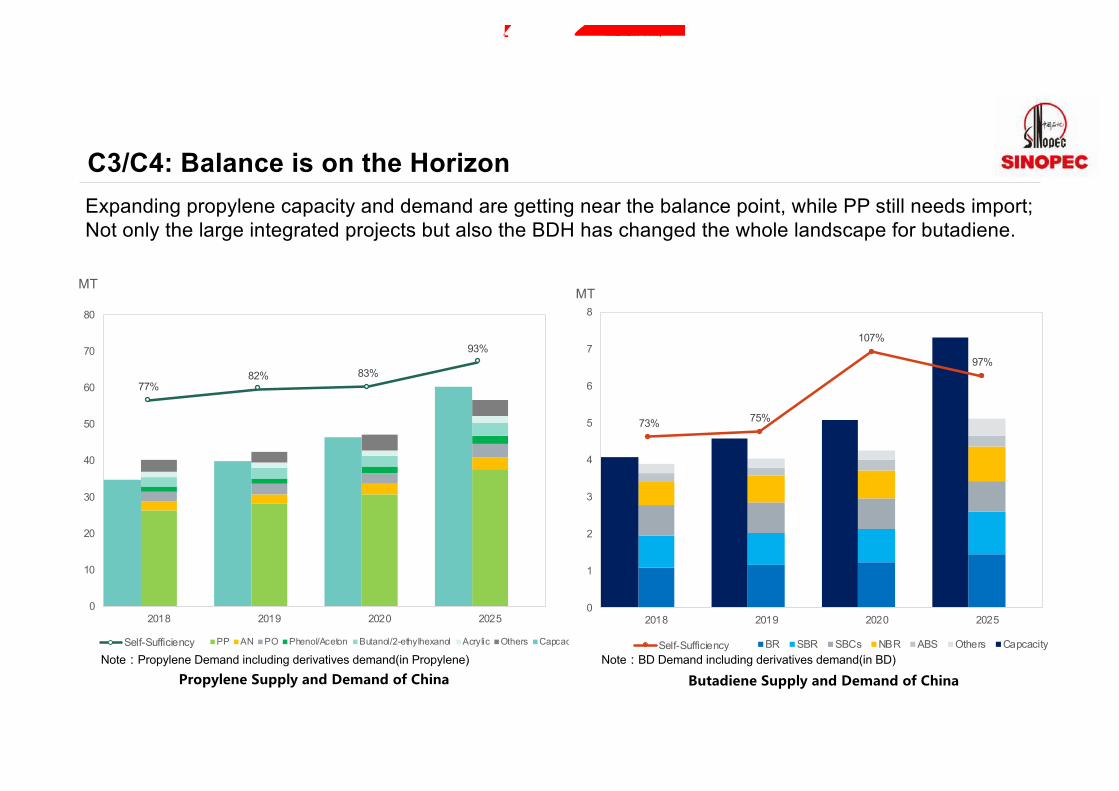

C3/C4: Balance is on the Horizon

0

10

20

30

40

50

60

70

80

2018 2019 2020 2025

MT

PP AN PO Phenol/Aceton Butanol/2-ethylhexanol Acrylic Others Capcacity

77%82% 83%

93%

Self-Sufficiency

Expanding propylene capacity and demand are getting near the balance point, while PP still needs import;Not only the large integrated projects but also the BDH has changed the whole landscape for butadiene.

0

1

2

3

4

5

6

7

8

2018 2019 2020 2025

MT

BR SBR SBCs NBR ABS Others Capcacity

73% 75%

107%

97%

Self-Sufficiency

Note�BD Demand including derivatives demand(in BD)Note�Propylene Demand including derivatives demand(in Propylene)

更多行业精品报告,登陆东西智库(dx2025.com)下载

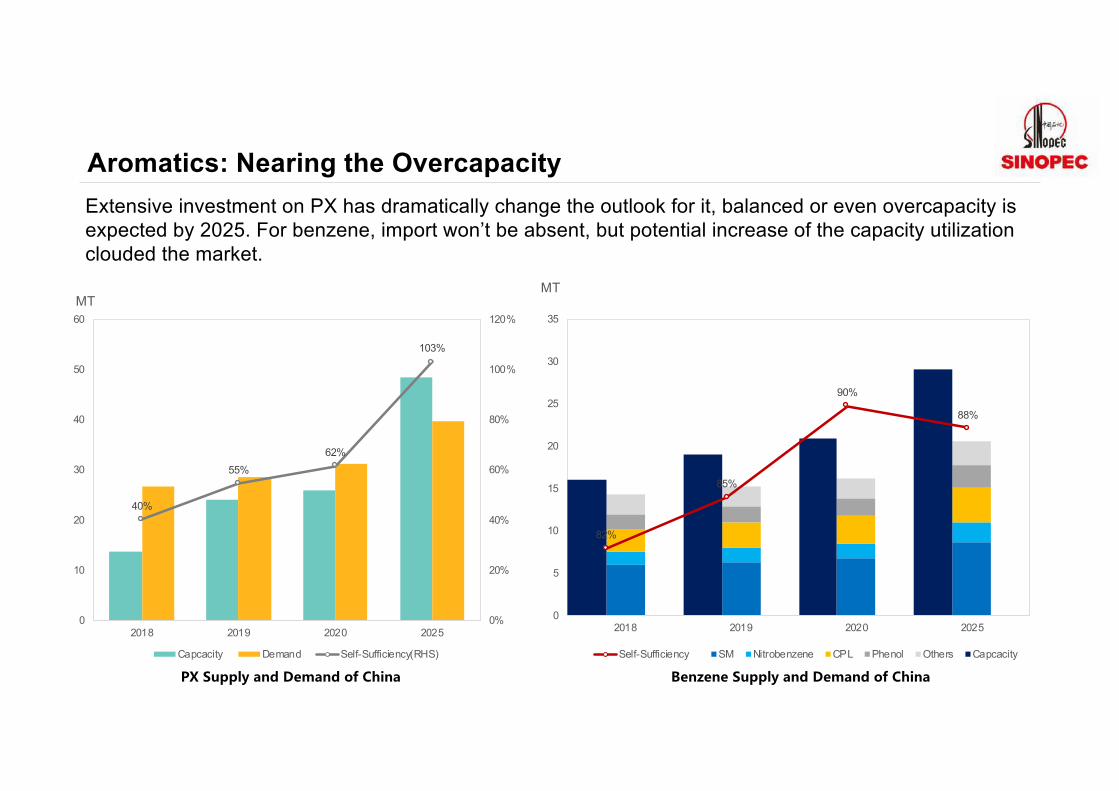

Aromatics: Nearing the OvercapacityExtensive investment on PX has dramatically change the outlook for it, balanced or even overcapacity is expected by 2025. For benzene, import won’t be absent, but potential increase of the capacity utilization clouded the market.

40%

55%62%

103%

0%

20%

40%

60%

80%

100%

120%

0

10

20

30

40

50

60

2018 2019 2020 2025

MT

Capcacity Demand Self-Sufficiency(RHS)

0

5

10

15

20

25

30

35

2018 2019 2020 2025

MT

SM Nitrobenzene CPL Phenol Others Capcacity

82%

85%

90%

88%

Self-Sufficiency

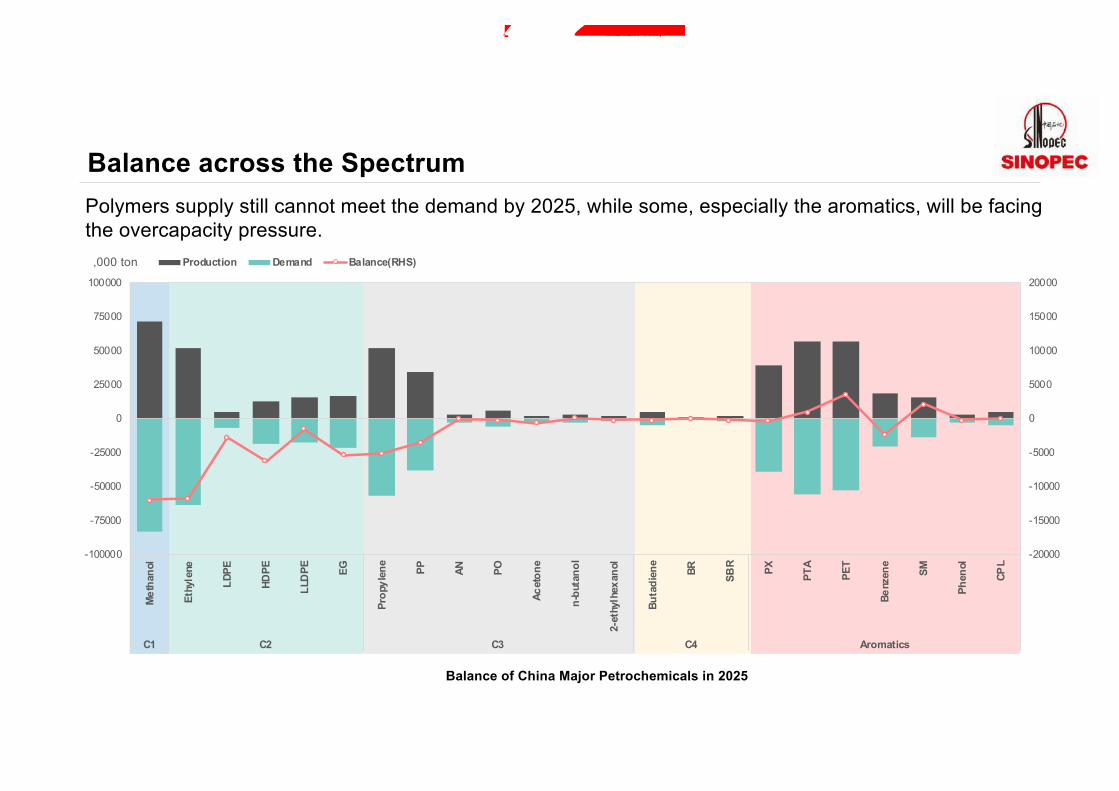

Balance across the SpectrumPolymers supply still cannot meet the demand by 2025, while some, especially the aromatics, will be facing the overcapacity pressure.

Balance of China Major Petrochemicals in 2025

-20000

-15000

-10000

-5000

0

5000

10000

15000

20000

-100000

-75000

-50000

-25000

0

25000

50000

75000

100000

Met

hano

l

Ethy

lene

LDPE

HDPE

LLD

PE EG

Prop

ylen

e

PP AN PO

Acet

one

n-bu

tano

l

2-et

hylh

exan

ol

Buta

dien

e

BR SBR PX PTA

PET

Benz

ene

SM

Phen

ol

CPL

C1 C2 C3 C4 Aromatics

,000 ton Production Demand Balance(RHS)

更多行业精品报告,登陆东西智库(dx2025.com)下载

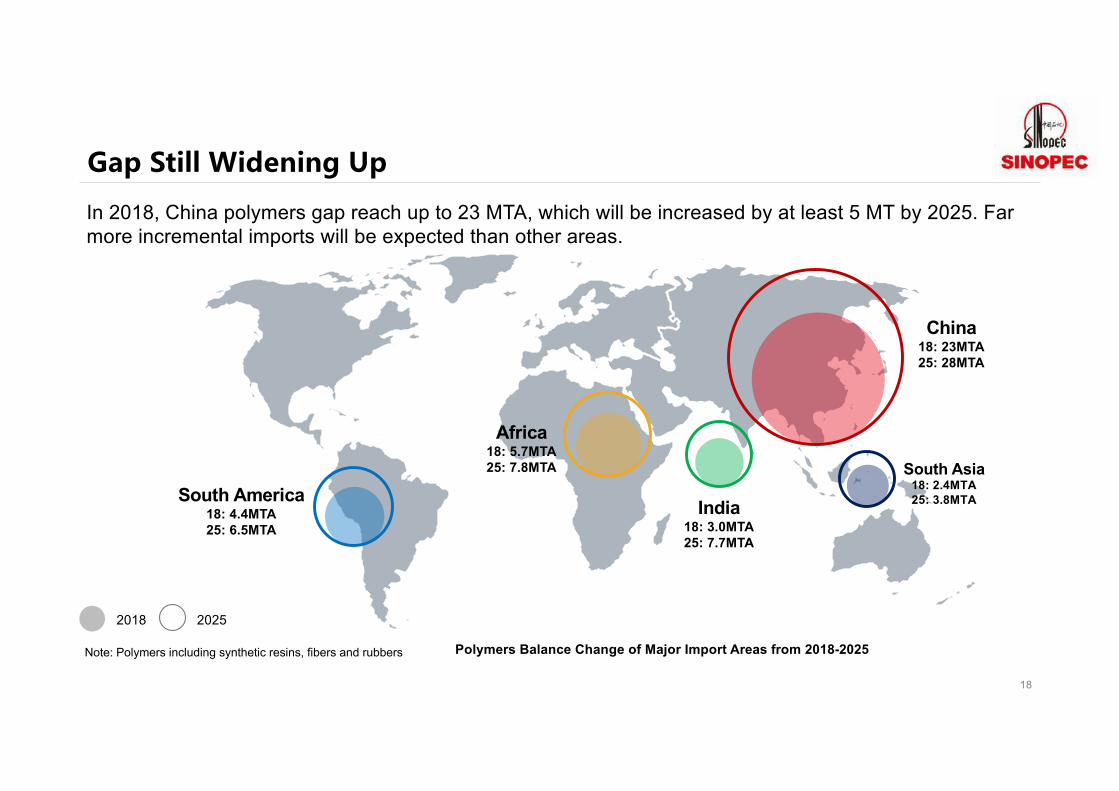

China18: 23MTA25: 28MTA

India18: 3.0MTA25: 7.7MTA

In 2018, China polymers gap reach up to 23 MTA, which will be increased by at least 5 MT by 2025. Far more incremental imports will be expected than other areas.

18

Polymers Balance Change of Major Import Areas from 2018-2025

Africa18: 5.7MTA25: 7.8MTA

South America18: 4.4MTA25: 6.5MTA

South Asia18: 2.4MTA25: 3.8MTA

2018 2025

Note: Polymers including synthetic resins, fibers and rubbers

更多行业精品报告,登陆东西智库(dx2025.com)下载

A Further Opening-up Market

20

A series of measures are implemented to reduce the market access barrier, which has attracted not only the domestic private investors but also the foreign investors, like Saudi Aramco, SABIC to join the game.

9%

11%

Private Investors

25%

Foreign Investors

13%

Ethylene Capacity Share 2018(inner circle) and 2025

Ethylene

26%

7%

Private Investors

50%

Foreign Investors

7%

PX Capacity Share 2018(inner circle) and 2025

PX

Remove restrictions on wholly foreign funded petrochemical companies

Remove restrictions on crude oil import of private companies

Introduce mixed ownership to SOEs

Implement negative list for market access

Cut items requiring government review by 30%

Cut taxes and administrative fees Lower the VAT from 17% to 13%

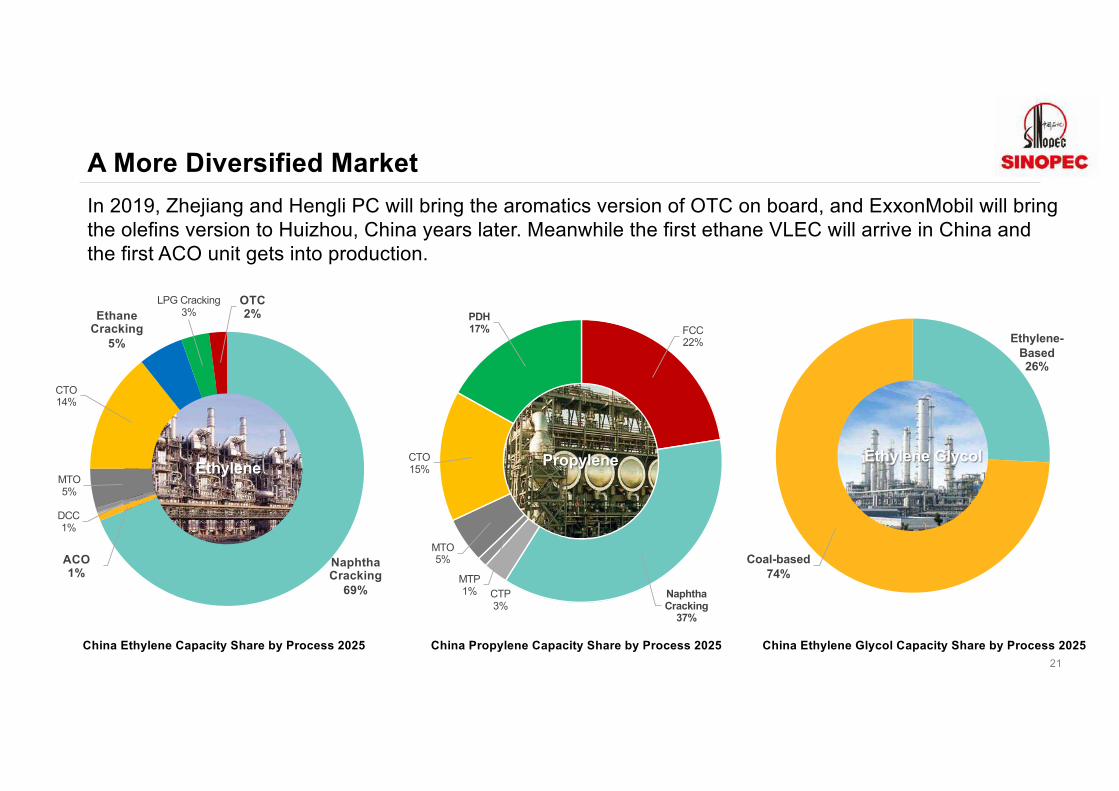

A More Diversified Market

21

In 2019, Zhejiang and Hengli PC will bring the aromatics version of OTC on board, and ExxonMobil will bring the olefins version to Huizhou, China years later. Meanwhile the first ethane VLEC will arrive in China and the first ACO unit gets into production.

China Ethylene Capacity Share by Process 2025 China Propylene Capacity Share by Process 2025

Ethylene-Based26%

Coal-based74%

Ethylene Glycol

China Ethylene Glycol Capacity Share by Process 2025

Naphtha Cracking

69%

ACO1%

DCC1%

MTO5%

CTO14%

Ethane Cracking

5%

LPG Cracking3%

OTC2%

Ethylene

FCC22%

Naphtha Cracking

37%

CTP3%

MTP1%

MTO5%

CTO15%

PDH17%

Propylene

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-200

-150

-100

-50

0

50

100

150

200

250

300

350

2000 2005 2010 2015 2020 2025 2030

Margin Index Self-sufficiency Index

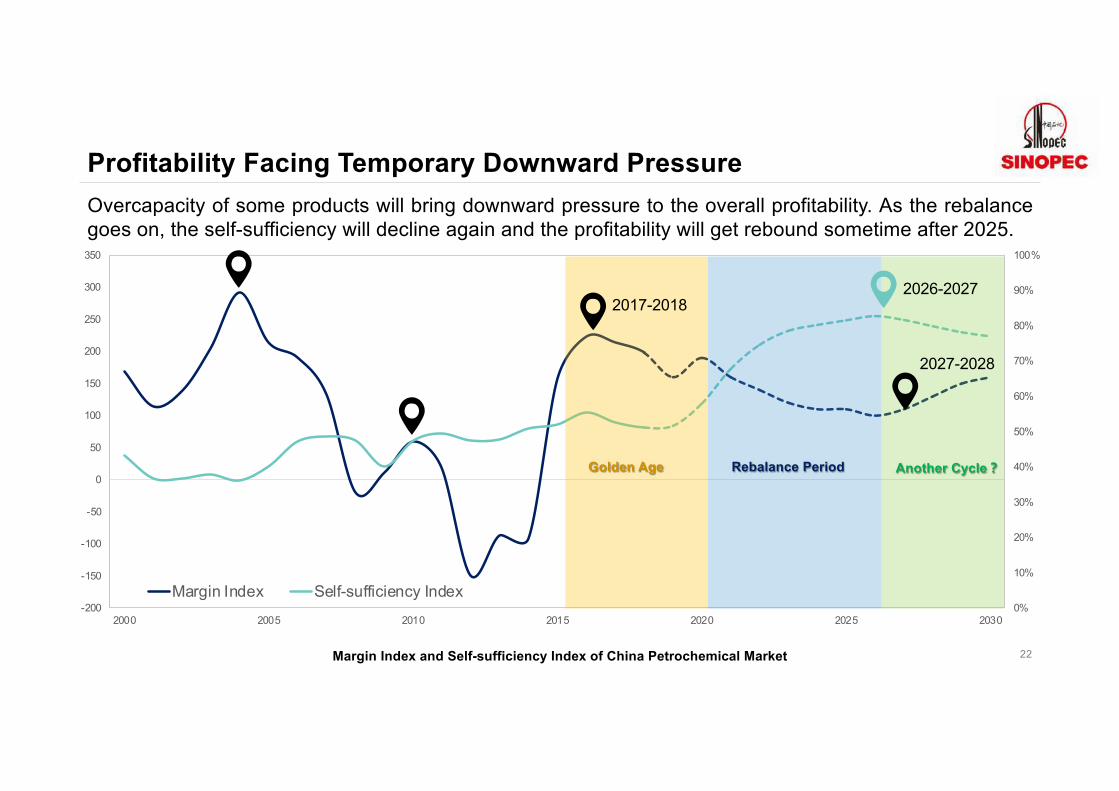

Profitability Facing Temporary Downward Pressure

22

Overcapacity of some products will bring downward pressure to the overall profitability. As the rebalance

goes on, the self-sufficiency will decline again and the profitability will get rebound sometime after 2025.

Margin Index and Self-sufficiency Index of China Petrochemical Market

2026-2027

2027-2028

2017-2018

Rebalance PeriodGolden Age Another Cycle�

Consolidation on the Way

23

Stricter environment regulations and fierce competition are forcing the disadvantages out of the games.Rapid decreasing small companies/units and climbing concentration ratio indicate the on-going consolidation.

concentration

ratio+27%

-18%

201525200

201624500

201723300 2018

21300

Numbers of enterprises above designated size

Takeaways

24

• As the largest producer and consumer, China petrochemical market to maintain a steady annualdemand growth of 6-7% and a capacity growth of 9-10% before 2025.

• Opportunities are emerging from massive urbanization, consumption upgrading, infrastructureconstruction, e-commerce, environmental protection business and further opening up.

• China will take more imports from the Middle East and U.S., as the polymers gap of China will bewidening up by 5 million tons by 2025.

• Steady economy and huge demand will help the market to get rebalanced quickly. And a rebound isexpected sometime after 2025.

Q&A

China Refining Industry Outlook

and Oil Demand Peak

March 25, 2019Xiaoming KE

CONTENTS 1

In the future: oil demand growth shifting from fuel-driven to petrochemical feedstock-driven

3 Transformation and upgrading of refining industry in China under a new round of investment

2

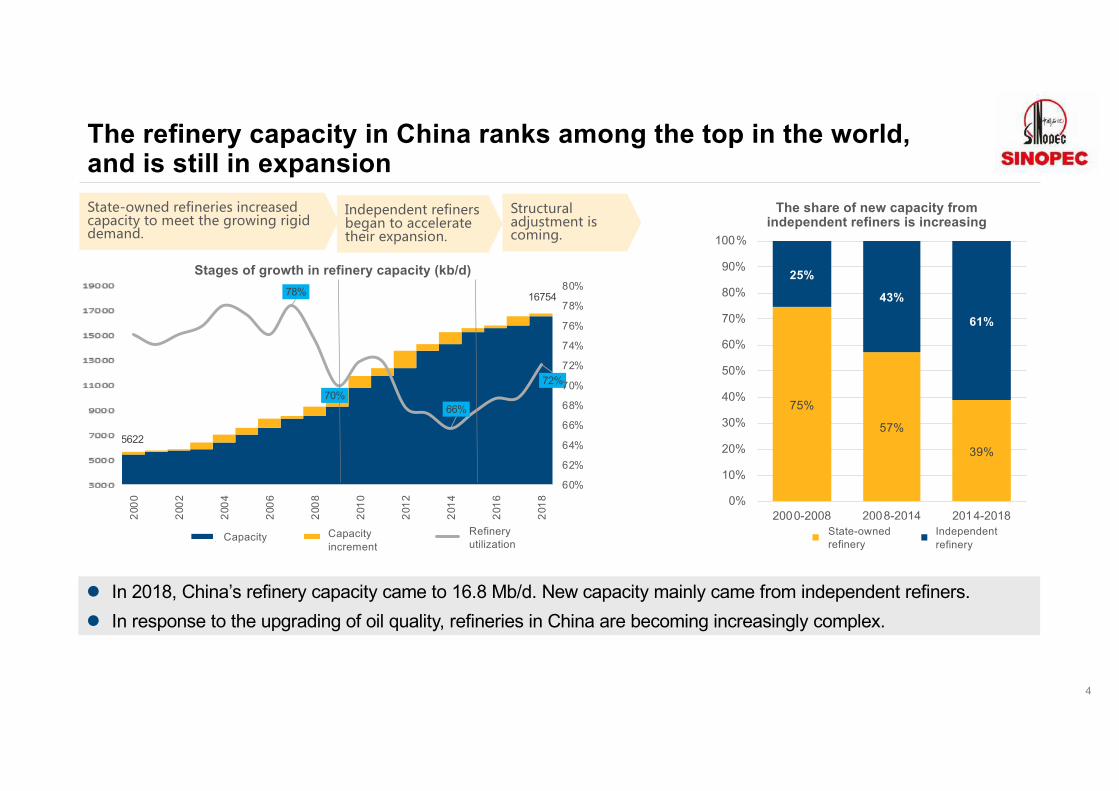

The refining industry in China ranking among the top in the world

The refining industry in China ranking among the top in the world

The refinery capacity in China ranks among the top in the world, and is still in expansion

4

-. - -

.-. - -

l In 2018, China’s refinery capacity came to 16.8 Mb/d. New capacity mainly came from independent refiners.l In response to the upgrading of oil quality, refineries in China are becoming increasingly complex.

75%

57%

39%

25%

43%

61%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000-2008 2008-2014 2014-2018

The share of new capacity from independent refiners is increasing

State-owned refinery

5622

1675478%

70%66%

72%

60%

62%

64%

66%

68%

70%

72%

74%

76%

78%

80%

15000

25000

35000

45000

55000

65000

75000

85000

95000

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Stages of growth in refinery capacity (kb/d)

Capacity Capacity increment

Refinery utilization

Independent refinery

The increasing crude oil processing meets domestic demand

5

l By 2018, China’s refining throughput was 12.1 Mb/d, and the dependency on imported crude oil came to 70.8%.l Since the release of imported oil quotas in 2015, the growth rate of refining throughput has risen from 4.1% to 5.4%.

l The utilization rate of independent refineries increased from 30% in 2014 to 60% in 2018, and the share ofimported crude oil in processing feedstock increased from 21% to 71%.

%

The crude oil processing volume is rising (million b/d)

3 15 0 2

AAGR 8.3%AAGR 8.1%

AAGR 4.3%

AAGR 5.8%

crude oil processing volume

Dependency on imported crude

21% 24%

45%58%

71%

55% 58%

49%37%

25%

0%

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

10 0%

2014 2015 2016 2017 2018

The bottleneck of crude oil for independent refineries is eliminated (10,000 tons)

4 3 3Imported crude Domestic crude Other sources

Urgent issue: large numbers of refineries with small average capacity

6

l By 2018, the average refinery capacity in China was only 87 Kb/d, which is only half of the global average level.l Excluding the outdated capacity of less than 40kb/d, the average utilization rate could be around 82% in 2018.

54

70

49

15

4

0 100 200 300 400 500 600 700

�40

40-100

100-200

200-400

≥400

Number of refineries

2018 China refinery capacity distribution(1,000 b/d)

18,133 16,754

6,217 5,002

3,484 87

0

50

100

150

200

250

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

�� �� �� �� �

The top 5 oil refining countries (1,000 b/d)

Total capacity Average refinery capacity

U.S. China Russia India Japan

In the future: Oil demand growth shifting from fuel-driven to petrochemical feedstock-driven

8

Outlook for demand-The key driver for China oil demand is shifting from fuel to petrochemical feedstockThe rough picture:l The future oil consumption will peak due to factors such as economy, population, fuel economy and EV deployment.

l Compared with the relative rigid demand of jet fuel and petrochemical feedstock, gasoline and diesel are more

likely to be replaced.

l There is still uncertainty about vehicle fuel economy improvement and the development of electric vehicles.

12.4

14.5

12.0

10

11

12

13

14

15

16

17

18

2018

�

��

��

��

���

����

�

2025-2

030

�

��

��

��

���

����

�

2050

�

The factors affecting oil demand are changing (million b/d)

20

18

Alte

rnativ

e

s Alte

rnativ

e

sTra

nsport

Petro

chem

ical

Avia

tion

Fuel e

fficie

ncy

EV

20

25

-

20

30

EV

Fuel e

fficie

ncy

Avia

tion

Petro

chem

ical

Tra

nsport

20

50

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Demand for oil and oil products (million b/d)

� � � ��� � -�

Chemical light oil: 3.7Around 2050

Diesel: 3.5Around 2015

Gasoline: 3.2Around 2025

Kerosene:1.8Around 2045

Oil: 14.5

Light

chemical oil

Oil (right

axis)

Gasoline Diesel Jet fuel

Driver shifting--Fuel-oriented oil consumption in China is decreasing

9

l China's oil demand reached 12.4 million b/d in 2018. What’s more, the oil consumption structure has changed or is about to change.

l Instead of transportation fuel, petrochemical feedstock will become the major refining product by 2050.

37%53% 51% 47%

35%

9%

15% 16% 25%36%

26%

12% 11%8% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

The trend of oil consumption structure in China

G NO ITransport Industry Daily useTransport

0: : 120 2 5 2 . 1 2 20 0 2 0 2. 252 .1 . 021 .42 :3 1 . C. :

: 12 : 22 52 4 : 4 12 . 1 3: 0 : 5 4 . 1 1.2E : 0: : 0 2. 4

Transportation ,52 4 : 5 0. : 2 5 1 : 2 52 4 : 5 :3 :

0: :

: 2 0 . 25 0 2 : 2 5 2 1 : 2. . 21 . 1 3 2 20: : 2 4 : 21

, . 2 :12 05. 42 . 1 52 12 2 : 2 :3- .002 2 . 2Petrochemi

calAgriculture Constructio

nOthers

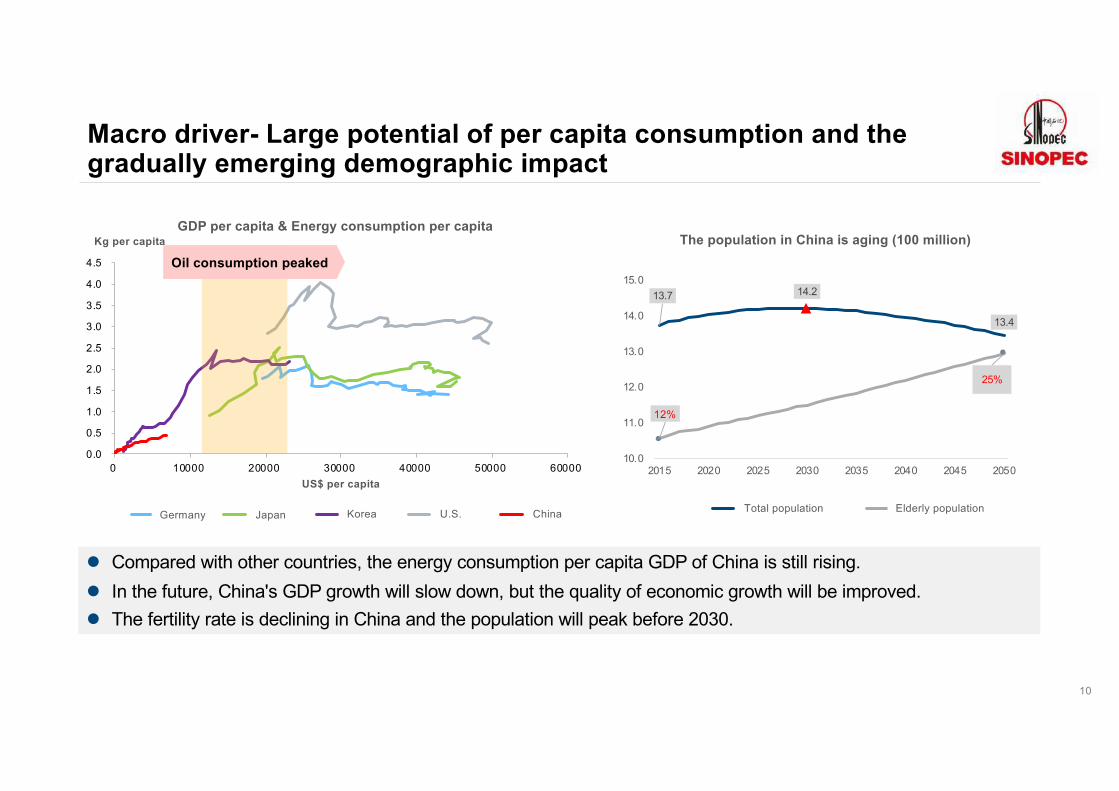

Macro driver- Large potential of per capita consumption and the gradually emerging demographic impact

10

l Compared with other countries, the energy consumption per capita GDP of China is still rising.l In the future, China's GDP growth will slow down, but the quality of economic growth will be improved. l The fertility rate is declining in China and the population will peak before 2030.

13.7 14.2

13.4

12%

25%

10.0

11.0

12.0

13.0

14.0

15.0

2015 2020 2025 2030 2035 2040 2045 2050

The population in China is aging (100 million)

��� ����-�Total population

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0 10000 20000 30000 40000 50000 60000

Kg per capita

US$ per capita

GDP per capita & Energy consumption per capita

�� � �� ��

Oil consumption peaked

Germany Japan Korea U.S. China Elderly population

The population densityPeople/km2 6000-8000 100-500 4-35

300

(livable)

Natural resources Extremely

scarce

Rich in coal

Lack of oilRich in oil & gas

Rich in coal

Lack of oil

Proportion of fuel tax 60%-80% 40%-70% 10%-20% 40%

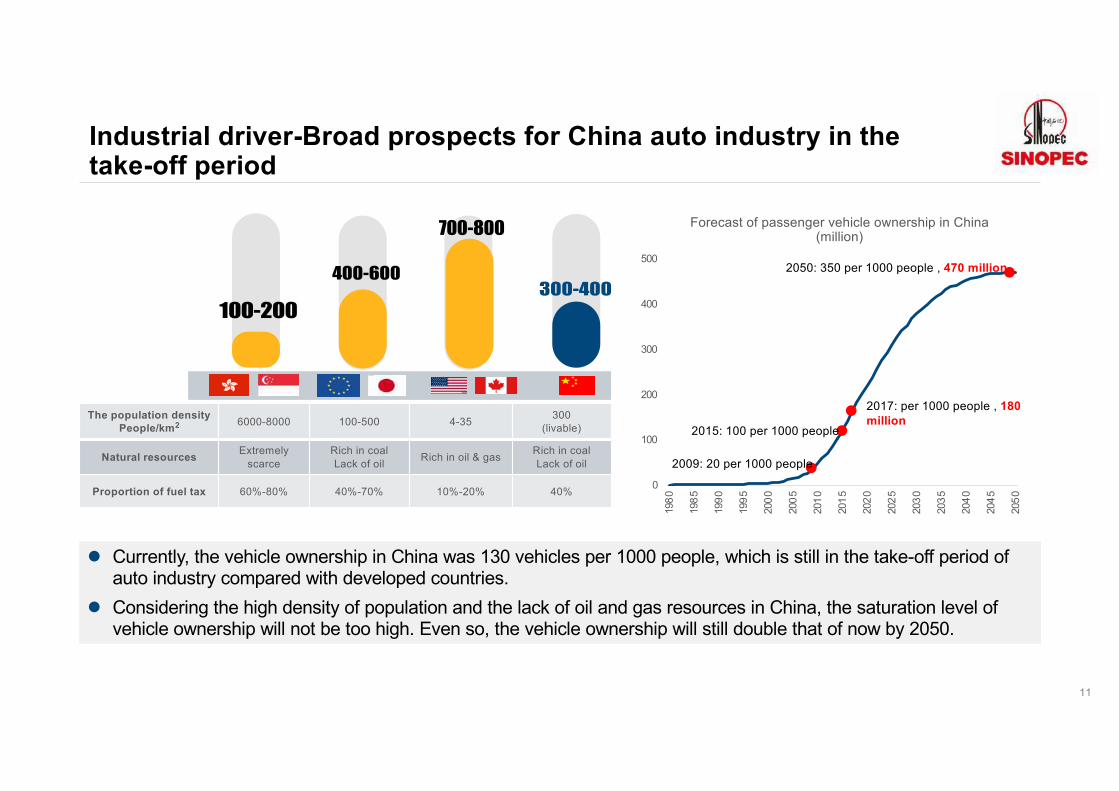

Industrial driver-Broad prospects for China auto industry in the take-off period

l Currently, the vehicle ownership in China was 130 vehicles per 1000 people, which is still in the take-off period of

auto industry compared with developed countries.

l Considering the high density of population and the lack of oil and gas resources in China, the saturation level of

vehicle ownership will not be too high. Even so, the vehicle ownership will still double that of now by 2050.

0

100

200

300

400

500

198

0

198

5

199

0

199

5

200

0

200

5

201

0

201

5

202

0

202

5

203

0

203

5

204

0

204

5

205

0

Forecast of passenger vehicle ownership in China

(million)

2009: 20 per 1000 people

2015: 100 per 1000 people

2017: per 1000 people , 180 million

2050: 350 per 1000 people , 470 million

11

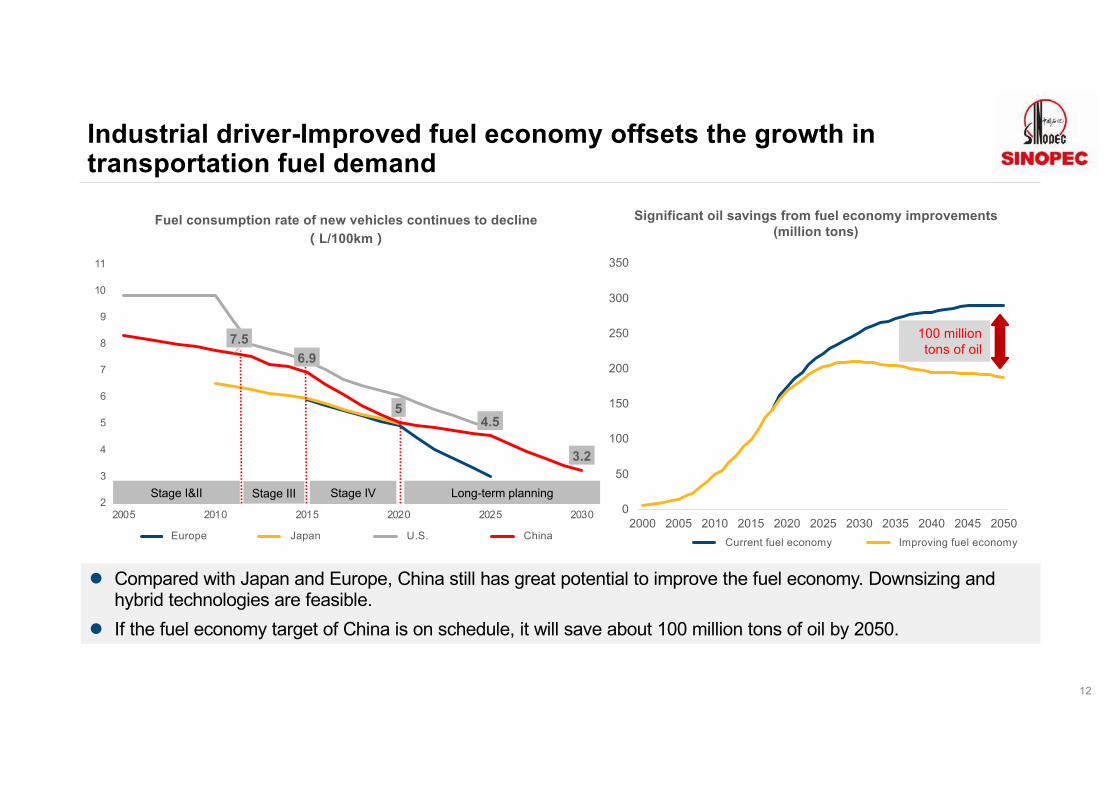

Industrial driver-Improved fuel economy offsets the growth in transportation fuel demand

12

7.56.9

54.5

3.2

2

3

4

5

6

7

8

9

10

11

2005 2010 2015 2020 2025 2030

Fuel consumption rate of new vehicles continues to decline�L/100km�

� �� �� �� Europe

Stage I&II Stage III Stage IV Long-term planning

l Compared with Japan and Europe, China still has great potential to improve the fuel economy. Downsizing and hybrid technologies are feasible.

l If the fuel economy target of China is on schedule, it will save about 100 million tons of oil by 2050.

0

50

100

150

200

250

300

350

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

����� ����

100 million tons of oil

Improving fuel economy

Significant oil savings from fuel economy improvements (million tons)

Japan U.S. ChinaCurrent fuel economy

Alternative driver-Diversity of oil alternatives

13

l Currently, natural gas and coal-to-liquid, coal-to-olefin are the main oil substitutes. l After 2025, electric vehicles will replace natural gas as the first alternative.

NG36%

EV7%

Biofuel9%

Methanol1%

Coal-to-oil12%

Coal chemical industry

35%

2018

NG12%

EV58%

Biofuel7%

Coal-to oil3%

Coal chemical industry20%

2050

4%

9%

16%

25%

34%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

5000

10000

15000

20000

25000

30000

35000

2015 2020 2030 2040 2050

The consumption of oil alternatives is increasing �kb/d�

��� ���� ��� ��

�� ��� ���� ��

48

1320

282

4360

6260

The share in oil consumption

NG EV Biofuel Methanol

Coal-to-chemicals

Coal-to-oil

14

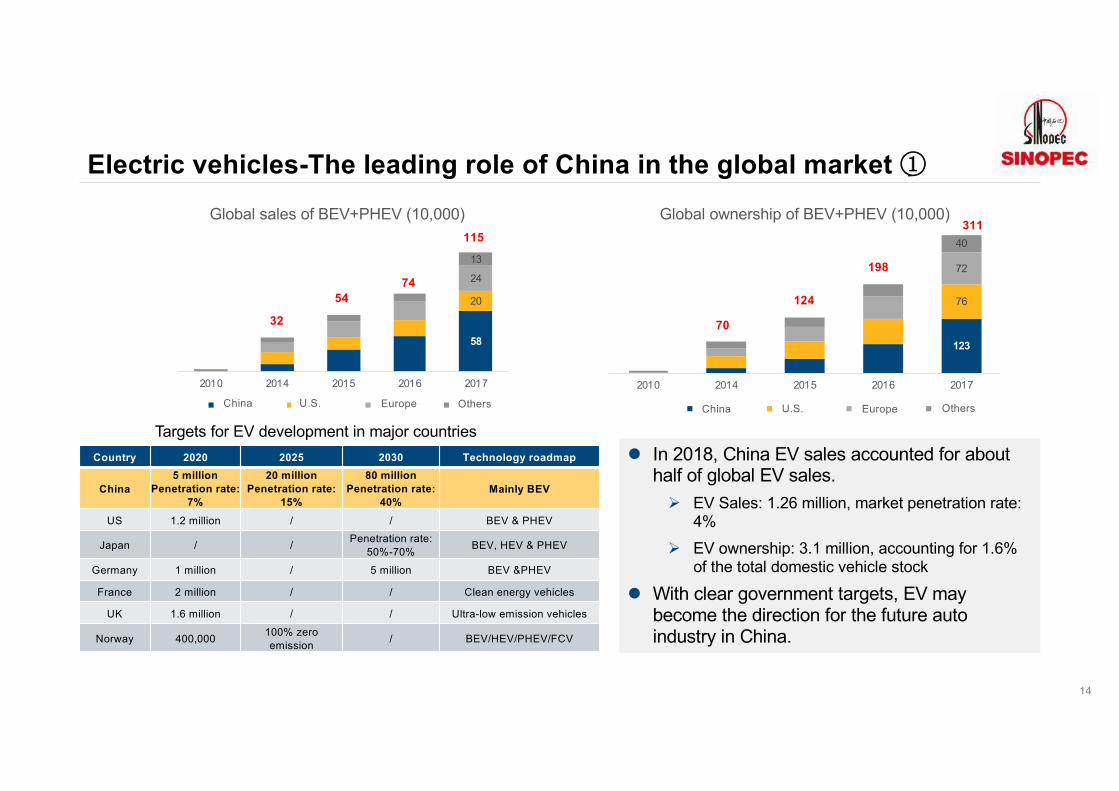

Electric vehicles-The leading role of China in the global market �

Targets for EV development in major countriesl In 2018, China EV sales accounted for about

half of global EV sales.Ø EV Sales: 1.26 million, market penetration rate:

4%Ø EV ownership: 3.1 million, accounting for 1.6%

of the total domestic vehicle stock

l With clear government targets, EV may become the direction for the future auto industry in China.

Country 2020 2025 2030 Technology roadmap

China5 million

Penetration rate: 7%

20 millionPenetration rate:

15%

80 millionPenetration rate:

40%Mainly BEV

US 1.2 million / / BEV & PHEV

Japan / / Penetration rate: 50%-70% BEV, HEV & PHEV

Germany 1 million / 5 million BEV &PHEV

France 2 million / / Clean energy vehicles

UK 1.6 million / / Ultra-low emission vehicles

Norway 400,000 100% zeroemission / BEV/HEV/PHEV/FCV

58

20

24

13

2010 2014 2015 2016 2017

Global sales of BEV+PHEV (10,000)

�� �� �� ��

115

7454

32

OthersChina U.S. Europe

123

76

72

40

2010 2014 2015 2016 2017

Global ownership of BEV+PHEV (10,000)

�� �� �� ��

311

198

124

70

China U.S. Europe Others

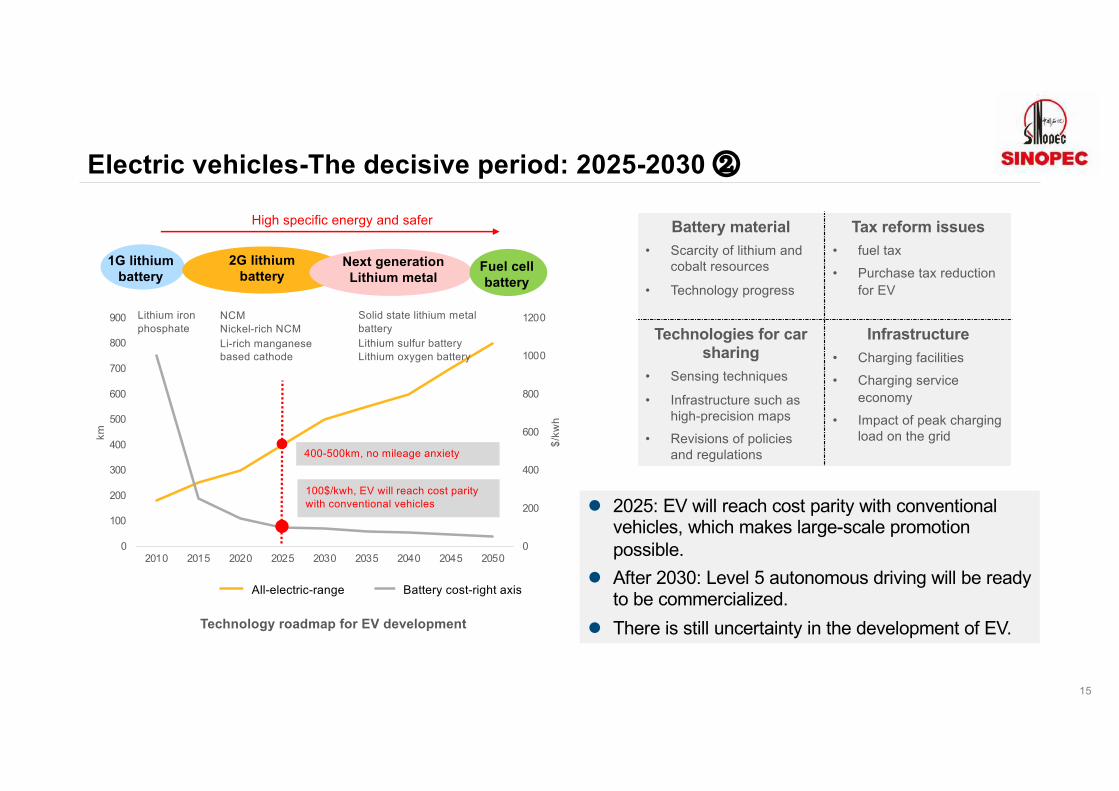

Electric vehicles-The decisive period: 2025-2030 �

15

l 2025: EV will reach cost parity with conventional vehicles, which makes large-scale promotion possible.

l After 2030: Level 5 autonomous driving will be ready to be commercialized.

l There is still uncertainty in the development of EV.

Battery material• Scarcity of lithium and

cobalt resources

• Technology progress

Tax reform issues• fuel tax• Purchase tax reduction

for EV

Technologies for car sharing

• Sensing techniques

• Infrastructure such as high-precision maps

• Revisions of policies and regulations

Infrastructure• Charging facilities• Charging service

economy• Impact of peak charging

load on the grid

Technology roadmap for EV development

0

200

400

600

800

1000

1200

0

100

200

300

400

500

600

700

800

900

2010 2015 2020 2025 2030 2035 2040 2045 2050$/

kwh

km

��� ����-�

1G lithium battery

2G lithium battery

Next generationLithium metal

Fuel cell battery

Lithium iron phosphate

NCMNickel-rich NCMLi-rich manganese based cathode

Solid state lithium metal batteryLithium sulfur batteryLithium oxygen battery

400-500km, no mileage anxiety

100$/kwh, EV will reach cost parity with conventional vehicles

High specific energy and safer

All-electric-range Battery cost-right axis

Industrial driver-Significant growth of oil demand in petrochemical industry

Naphtha84%

CPP/DCC

2%

MTO5% CTO

9%

����

Naphtha61%

Coal-based Naphtha1%

CPP/DCC1%

MTO7%

CTO22%

Ethane5%

LPG2%

Acetylene1%

����

l In the future, with the improvement of living standards, auto, home appliances, textiles and real estate industries in China will continue to develop. Significant growth is expected in ethylene and PX consumption.

l Despite the diversification trend, Ethylene feedstock will still be dominated by petroleum-based feedstock.

3761

5230

7000

77008000

1997

2605

34433793 3800

10

1010

2010

3010

4010

5010

6010

7010

8010

9010

2015 2020 2030 2040 2050

Ethylene and PX demand (10,000 tons)

������� ��PX���

Changes in feedstock structure for ethylene

ethylene equivalent consumption

PX equivalent consumption

13

Transformation and upgrading of refining industry in China under a new round of investment

18

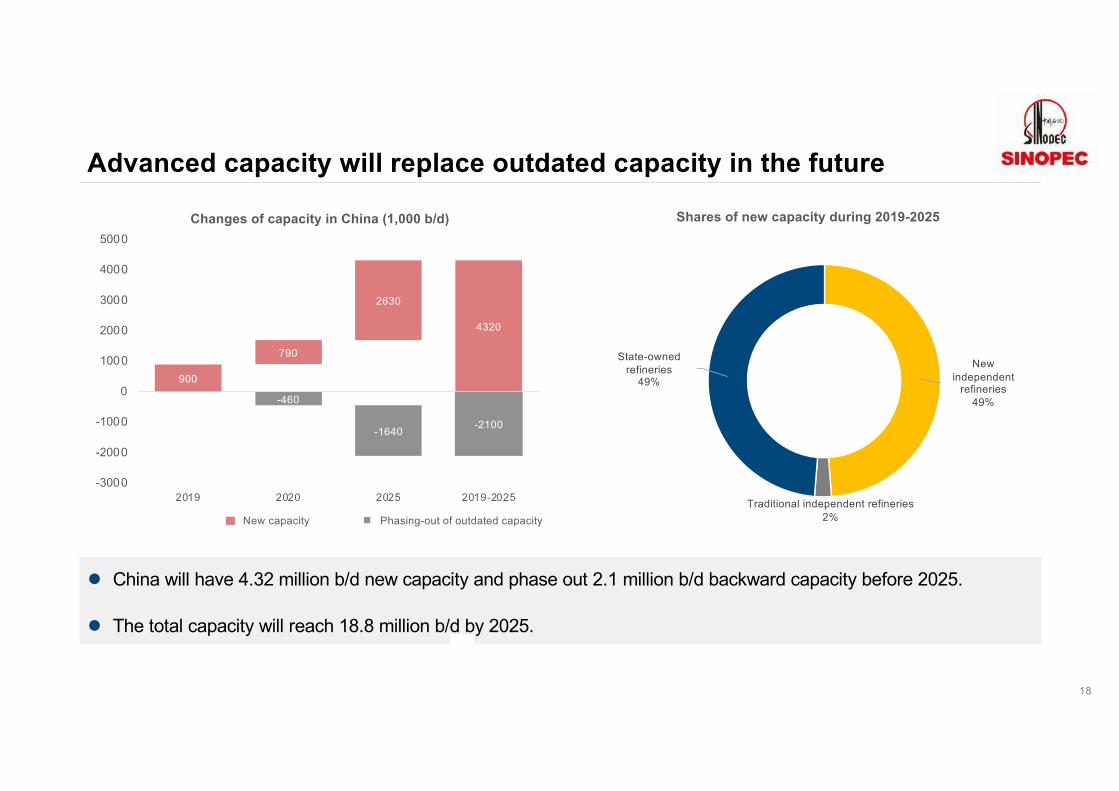

Advanced capacity will replace outdated capacity in the future

l China will have 4.32 million b/d new capacity and phase out 2.1 million b/d backward capacity before 2025.

l The total capacity will reach 18.8 million b/d by 2025.

New independent

refineries49%

Traditional independent refineries2%

State-owned refineries

49%

Shares of new capacity during 2019-2025

900

4320

790

2630

-460

-2100-1640

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

2019 2020 2025 2019-2025

Changes of capacity in China (1,000 b/d)

���� ����New capacity Phasing-out of outdated capacity

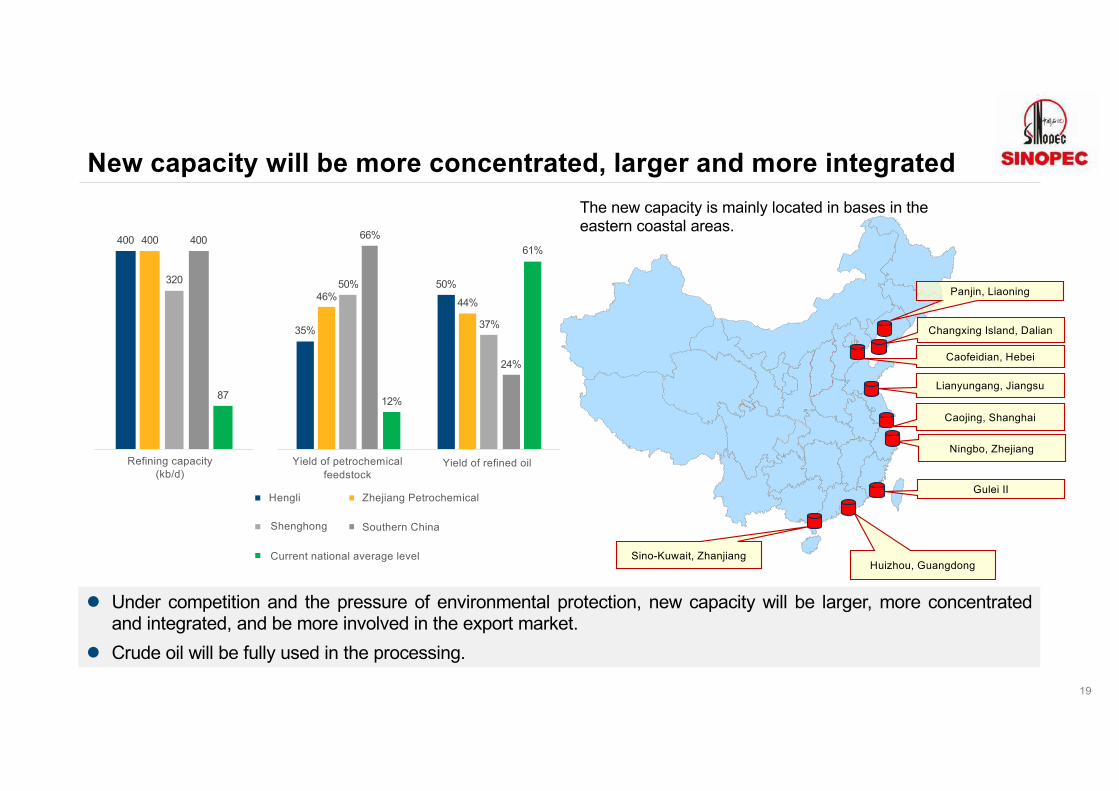

New capacity will be more concentrated, larger and more integrated

19

The new capacity is mainly located in bases in the eastern coastal areas.

l Under competition and the pressure of environmental protection, new capacity will be larger, more concentratedand integrated, and be more involved in the export market.

l Crude oil will be fully used in the processing.

400 400

320

400

87

�������/��

35%

50%46% 44%

50%

37%

66%

24%

12%

61%

����� �����

�� ��

�� �*

�����

Hengli Zhejiang Petrochemical

Southern China

Huizhou, Guangdong

Gulei II

Ningbo, Zhejiang

Lianyungang, Jiangsu

Changxing Island, Dalian

Panjin, Liaoning

Sino-Kuwait, Zhanjiang

Caojing, Shanghai

Caofeidian, Hebei

Shenghong

Current national average level

Refining capacity(kb/d)

Yield of petrochemical feedstock

Yield of refined oil

19

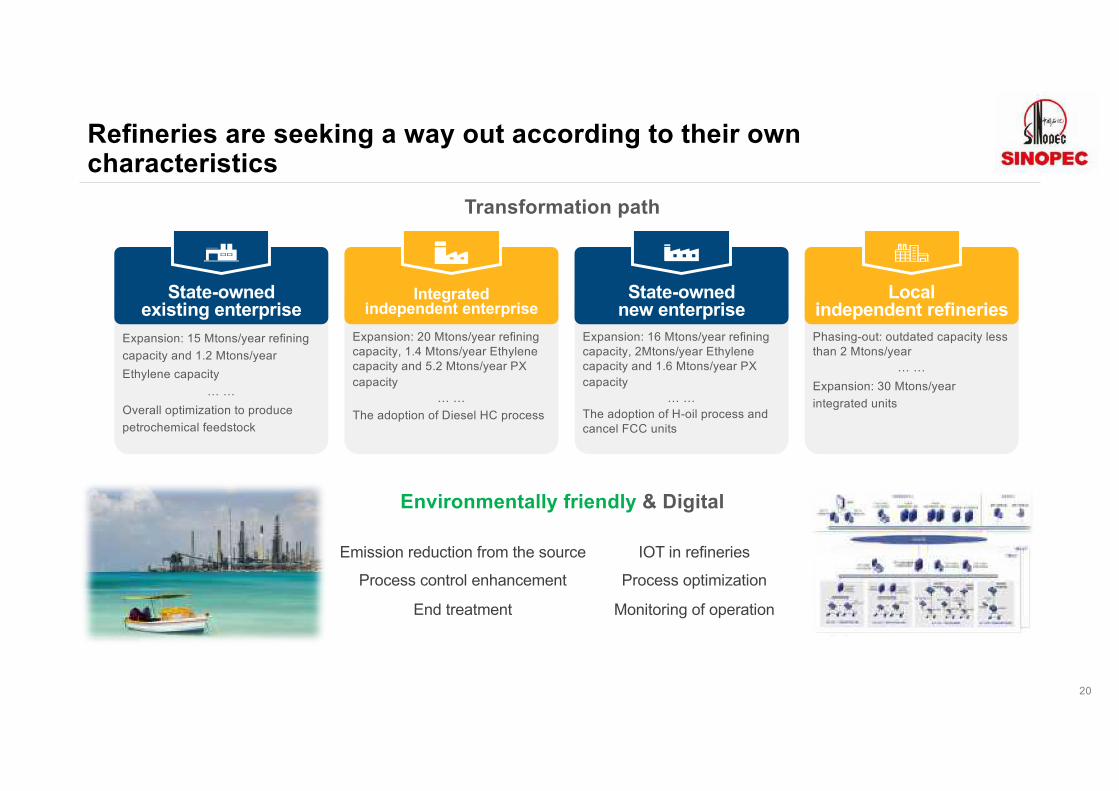

Refineries are seeking a way out according to their own characteristics

Expansion: 15 Mtons/year refining capacity and 1.2 Mtons/year Ethylene capacity

… …Overall optimization to produce petrochemical feedstock

State-owned existing enterprise

Expansion: 20 Mtons/year refining capacity, 1.4 Mtons/year Ethylene capacity and 5.2 Mtons/year PX capacity

… …The adoption of Diesel HC process

Integratedindependent enterprise

Expansion: 16 Mtons/year refining capacity, 2Mtons/year Ethylene capacity and 1.6 Mtons/year PX capacity

… …The adoption of H-oil process and cancel FCC units

State-owned new enterprise

Phasing-out: outdated capacity less than 2 Mtons/year

… …Expansion: 30 Mtons/year integrated units

Localindependent refineries

Transformation path

Emission reduction from the source

Process control enhancement

End treatment

IOT in refineries

Process optimization

Monitoring of operation

Environmentally friendly & Digital

20

21

Increasing influence of China in the Asia-Pacific refined oil export market

l In 2018, China's refined oil exports increased by 1.9 times compared with 2010 and became the fourth largest exporter in the Asia-Pacific region. (Top 3: Korea, Japan and India)

l Due to the low yield of refined oil in new capacity, the net export of refined oil will not increase much by 2020-2025.l In the future, large refineries in coastal areas will target both domestic and international markets.

6%

7% 8%

10% 10%

11% 11%

0%

2%

4%

6%

8%

10%

12%

-200

0

200

400

600

800

1000

2005 2010 2015 2016 2017 2018 2019 2020 2025

Outlook for China's refined oil import and export (kb/d)

�

��

���������-�

Import

Export

The share of import & export in Asia-Pacific market (right axis)

A more opening-up refining market in China welcomes cooperation in various fields

Investments overseas

• Yanbu Aramco Sinopec

refinery put into operation in

Saudi Arabia

• The “Belt and Road Initiative”

boosts oil and gas cooperation

among countries along the

route

Domestic refining

• PDVSA-CNPC Jieyang refinery is

under construction.

• Saudi Aramco joins Huajin

Petrochemical and Zhejiang

Petrochemical.

• BASF plans to build an integrated

petrochemical base in Guangdong

Retail market

• BP will build 1,000 gas stations in

China

• Saudi Aramco plans to enter the

retail market in Zhejiang

Charging service

• Tesla has built supercharging

stations in 27 provinces and cities.

• Shell‘s first charging station was put

into operation in Tianjin in September,

2018.

• In January 2019, BP's first

supercharging station was put into

operation in Shanghai

Oil import quotas for

independent refineries

Crude oil import

refined oil exports will

become ordinary

Refined oil export

Relax market access and

scrap limits on foreign

holdings

Refined oil sales

Coming soon……

Refined oil pricing mechanism reform

22

Thank you

China’s Energy Transition and

Development Path

Report series of China energy and petrochemical industry

Zuoxian LuoMarch 20th 2019

CONTENTS

1. Evolution of China's Energy Supply and Demand Structure

2. Coal Demand and Development Trend

3. Oil Demand and Development Trend

Gas Demand and Development Trend

Non-fossil Energy Demand and Development Trend

4.

5.

Future Energy Demand and International Cooperation6.

Evolution on China's Energy

Supply and Demand

Energy production and consumption have maintained growth and energy self-sufficiency has declined

• Energy consumption grew; Supply stable;

• Self-sufficiency rate :

111.8% (1985) to 98.2% (1992), 93.7% (2000) and 79% (2018).

• Domestic oil and gas production is stable.

• Growth of oil and gas consumption replaces coal.

• 2018, coal consumption dropped to 59%, 10 % lower than in 2000.

4

39

Coal Oil Gas

R/Preserve reserve R/Preserve

36.75.5 trillion cubic m³18.33.5 billion tons138.8 billion tons

R/P

5

Industrialization

2018: proportion of tertiary

industry 51.6%

2030:60.3%

2018:1.40 billion

2029:1.44 billion, peak

Population Urbanization Economic Growth

2018:60%

2030:70%

2018:GDP growth 6.9%

2030:GDP growth 5%

China Key economic development indexes estimated

6

Oil

Gas

Coal

Non-fossil

2.2% VS 2018

7% VS 2018

9% VS 2018

11% VS 2018

Targets for 2030 within the framework of China's energy revolution

Total Energy Demand: 4.2billion toeGreenhouse gas per unit of GDP: reduces 60%-65% than 2005

Terminal energy consumption : electricity increases to 30%

2020/2030,energy demand : below 5/6 billion tce

(3.5/4.2 billion toe).

Energy consumption revolution

Added energy is mainly from clean energy

Energy supply revolution

Overseas cooperation;one belt one road energy corridor

International cooperation

Energy-saving technologies; smart energy technologies

Technology revolution

• Effective and competitive energy market system;

• Market-oriented pricing mechanism;

• Energy legal system.

Energy system revolution

Coal Demand and Development Trend

0

5

10

15

20

25

30

35

40

45

Coal consumption, production and imports(100 million tons)

consumption production import

8

• Consumption increased

• Imports increased

1990-

2005

2005-

2013

2013-

Three stages of China's coal

consumption since 1990

• Steady development;

• Production exceeded consumption

• Self-sufficiency

• Energy conservation

• Emission reduction

• Energy structure transition

• Cutting the backward capacity

• Encourage the import of high-quality coal

2005, difference between consumption and

production expand, coal imports accelerated.

2013, coal consumption and

imports peaking at the same time.

Since 2005, China's dependence ratio on foreign coal remained between 6% and 7.5%. The external dependence ratio of 2018 is 7.3%.

Coal consumption reached its peak on 2013

Consumption:2.4 billion tons

Production : 2.3 billion tons

Consumption:4.2 billion tons

Imports : 0.3 billion tons

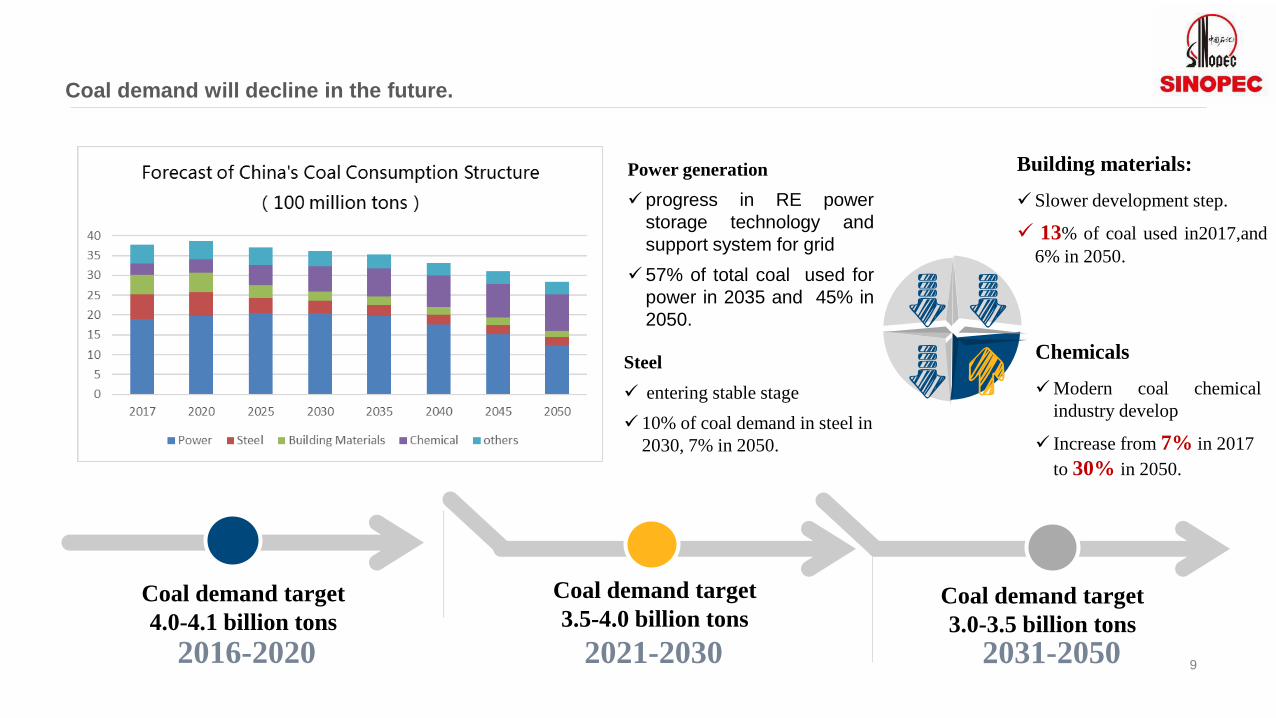

Coal demand target

4.0-4.1 billion tons

Coal demand target

3.5-4.0 billion tons

2016-2020 2021-2030 2031-2050

Coal demand will decline in the future.

Power generation

✓ progress in RE power

storage technology and

support system for grid

✓ 57% of total coal used for

power in 2035 and 45% in

2050.

Steel

✓ entering stable stage

✓ 10% of coal demand in steel in

2030, 7% in 2050.

Building materials:

✓ Slower development step.

✓ 13% of coal used in2017,and

6% in 2050.

Chemicals

✓Modern coal chemical

industry develop

✓ Increase from 7% in 2017

to 30% in 2050.

Coal demand target

3.0-3.5 billion tons

9

10

Optimization of coal industry is to mainly promote construction of integrated base

International cooperation in science and

technology promote base construction

Around 2020, the output of 14 large coal bases will be 3.7 billion tons, accounting for

more than 95% of the total coal production.

Coal production Coal clean

energy base

Coal power Chemical production

Coal to oil (gas)

Power grid

transmissionPipeline

transportation

Land

transportation

Olefins, etc.

Base construction:

coal production, chemical conversion,

electricity, building materials integrated

Oil Demand and Development Trend

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

0

10000

20000

30000

40000

50000

60000

70000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

China oil demand, supply and foreign dependence ratio

(10 thousand tons)

production consumption foreign dependence ratio

12

Domestic production decrease and refining capacity increase led to external dependence ratio rise

Oil

price

down

2016

199 million tons

2017

192million tons

2018

190million tons

Refining

capacity

growth

2017 2018

Net increase of 18 million

tons

Refining capacity

reached 770 million tons

Net increase of 22

million tons

Refining capacity

reached 830 million tons

64800

19000

70.7%

China oil demand, supply and foreign dependence ratio(10 thousand tons)

0

1000

2000

3000

4000

5000

6000

7000

Oil imports by major countries(10 thousand tons)

Imports in 2000 Imports in 2017

13

Importing country in 2000

New importing countries in 2017

• 2000: 30 importing countries, covering the Middle East, Africa, Europe/former Soviet Union, the Americas and the Asia-

Pacific region. The import volume was led by the Middle East, nearly 38 million tons, far exceeding other regions.

• 2017: 43 importing countries, 13 of which were added and mainly from Africa, America and Europe. Most of the new

imports came from the Middle East and Europe, with Saudi Arabia increase more than 45 million tons.

China has more oil trade partners in the world

2017 imports of

52 million tons

2000 imports of

16 million tons

14

The oil demand will reach its peak with over 700 million tons around 2027.

China’s population:

1.44 billion

Energy efficiency :

the world's advanced level

Urbanization level:

70%

Number of electric :

50-80 million ; 1/4 of the total.

Data sources: EDRI

Aviation kerosene: Driven by annual growth

rate of passenger turnover.

Gasoline: replaced by electrification; a decade of

growth

Diesel: replaced by gas in urban buses,

and truck transportation.

709million tons

By 2030:

15

Resource

Unconve-

ntionalsOutput

Resource

Conversion

Rate

✓Rich in petroleum

✓35% proven, and has

potential

✓ Resource conversion rate is

Low

✓ Improving recovery and

conversion rate through

technological progress

✓ Shale oil and oil sands

are rich.

✓The State Key Laboratory

of Shale Oil has been set

up .

✓Diversified investors

✓Oil production will have

space for growth

Domestic supply: widen E&P fields and EOR technologies

Natural Gas Demand and Development Trend

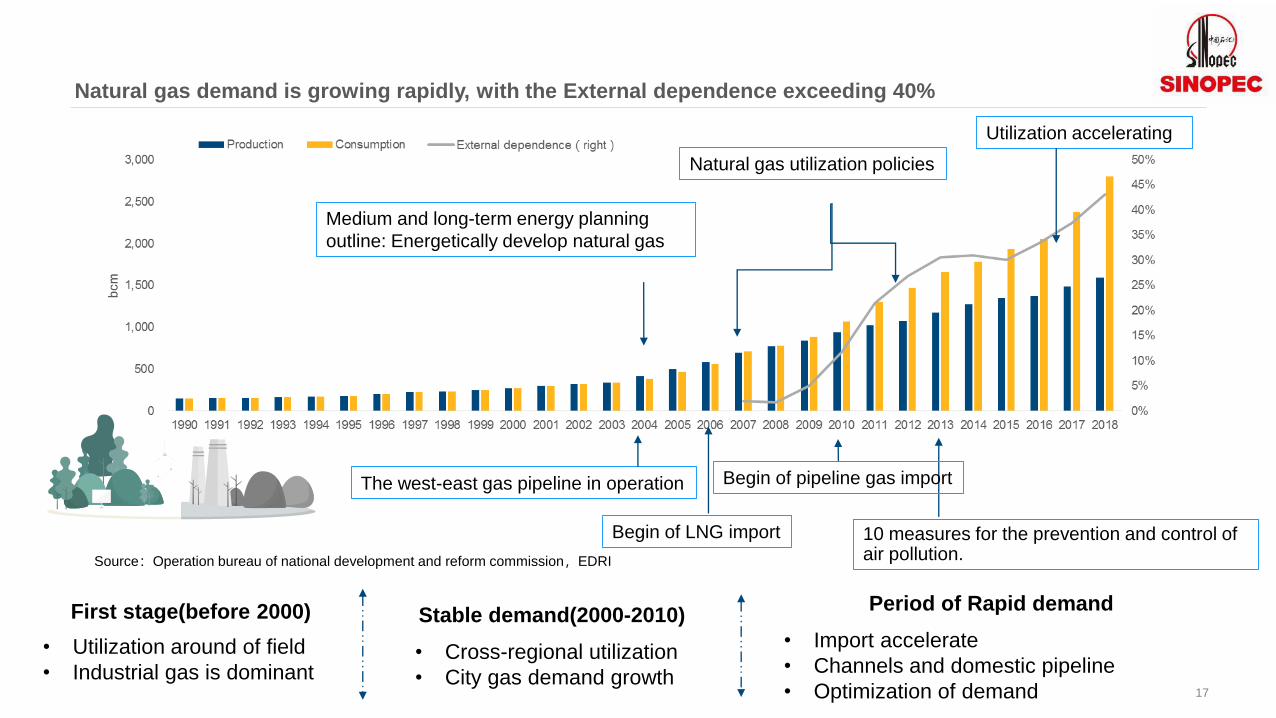

Source:Operation bureau of national development and reform commission,EDRI

Natural gas demand is growing rapidly, with the External dependence exceeding 40%

17

The west-east gas pipeline in operation

Natural gas utilization policies

Medium and long-term energy planning

outline: Energetically develop natural gas

First stage(before 2000)

• Utilization around of field

• Industrial gas is dominant

Stable demand(2000-2010)

• Cross-regional utilization

• City gas demand growth

Begin of LNG import

Begin of pipeline gas import

Period of Rapid demand

• Import accelerate

• Channels and domestic pipeline

• Optimization of demand

10 measures for the prevention and control of air pollution.

Utilization accelerating

18

Diversified imports, more gas trade partners, quick LNG import growth

✓2006-2007,85% came from long-

term contracts in Australia

✓The rest from spot contracts in Oman,

Algeria and Nigeria.

Middle EastOman

Qatar

Yemen

Asia PacificIndonesia

Malaysia

Australia

Papua New Guinea

Europe

Belgium

U.K.

France

Netherland

Norway

RussiaAmericaPeru

Trinidad and

Tobago Canada

U.S.A.

Africa

Algeria

Angola

Cameroon

Egypt

Equatorial guinea

Nigeria

Map of LNG and pipeline gas import of China

Exporters in 2012 Imported from Yemen only in 2012

✓2012, mainly from Qatar, Australia,

Indonesia, Malaysia, Yemen and Russia.

Australia24%

Qatar34%

Malaysia13%

Indonesia

16%

Russia3%Yemen

4%others

6%

China’s LNG import structure in 2012

✓ China has imported LNG from more than 20 countries in 2018.

New exporters in 2018

Russia

Countries and regions of pipeline gas import

Myanmar

Central Asia

Australia, 44%

Qatar, 17%

Malaysia, 11%

Indonesia, 9%

Papua New Guinea, 5%

U.S.A., 4%

others, 11%

China’s LNG import structure in 2018

2018

2030

2040

2050

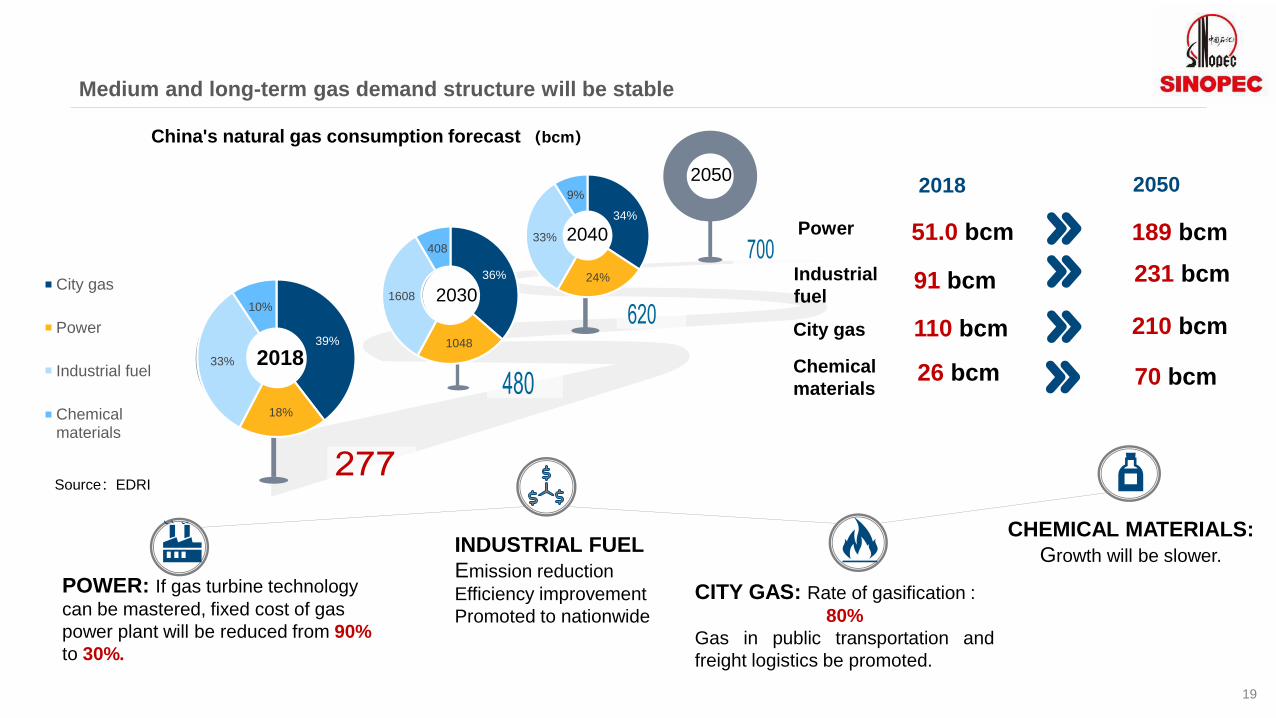

Source:EDRI

China's natural gas consumption forecast (bcm)

Power 51.0 bcm

Industrial

fuel

City gas

Chemical

materials

91 bcm

110 bcm

26 bcm

189 bcm

231 bcm

210 bcm

70 bcm

20502018

POWER: If gas turbine technology

can be mastered, fixed cost of gas

power plant will be reduced from 90%

to 30%.

INDUSTRIAL FUEL

Emission reduction

Efficiency improvement

Promoted to nationwide

CITY GAS: Rate of gasification :

80%

Gas in public transportation and

freight logistics be promoted.

CHEMICAL MATERIALS:

Growth will be slower.

34%

24%

33%

9%

39%

18%

33%

10%

City gas

Power

Industrial fuel

Chemicalmaterials

36%

1048

1608

408

19

Medium and long-term gas demand structure will be stable

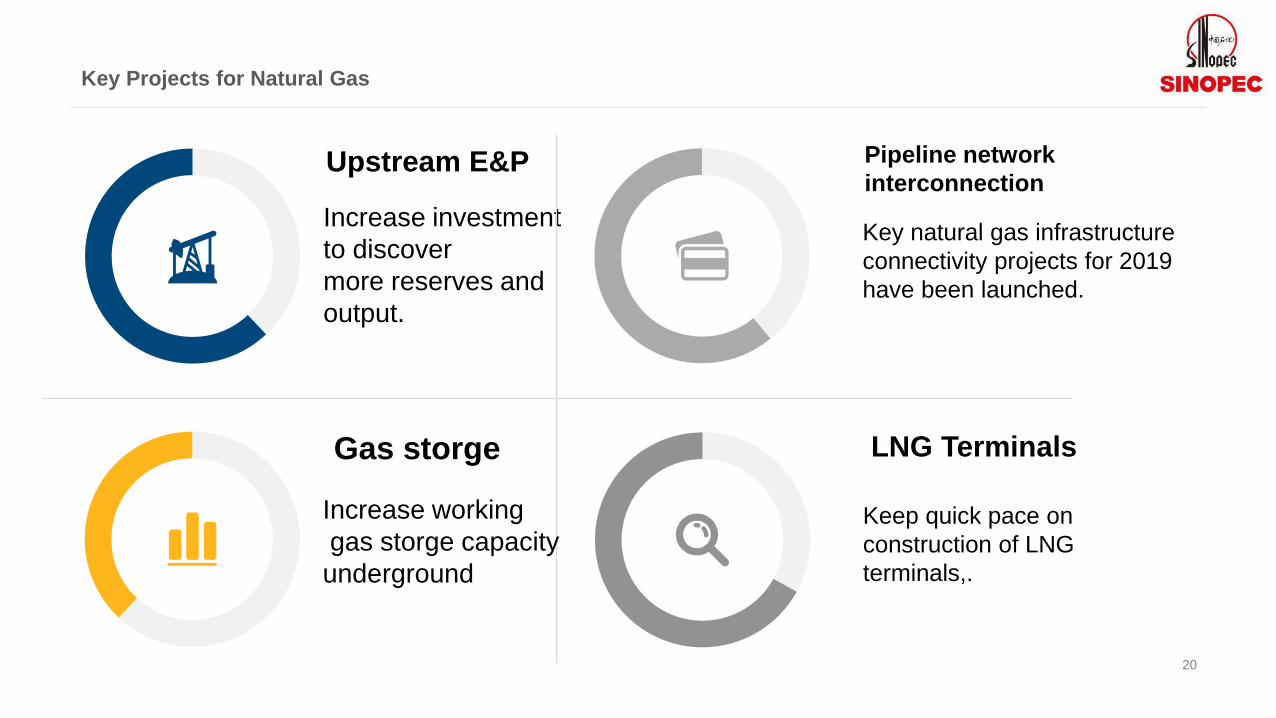

20

Upstream E&P

Increase investment

to discover

more reserves and

output.

Key Projects for Natural Gas

Gas storge

Increase working

gas storge capacity

underground

Pipeline network

interconnection

Key natural gas infrastructure

connectivity projects for 2019

have been launched.

LNG Terminals

Keep quick pace on

construction of LNG

terminals,.

Non-fossil Energy Demand and Development Trend

22

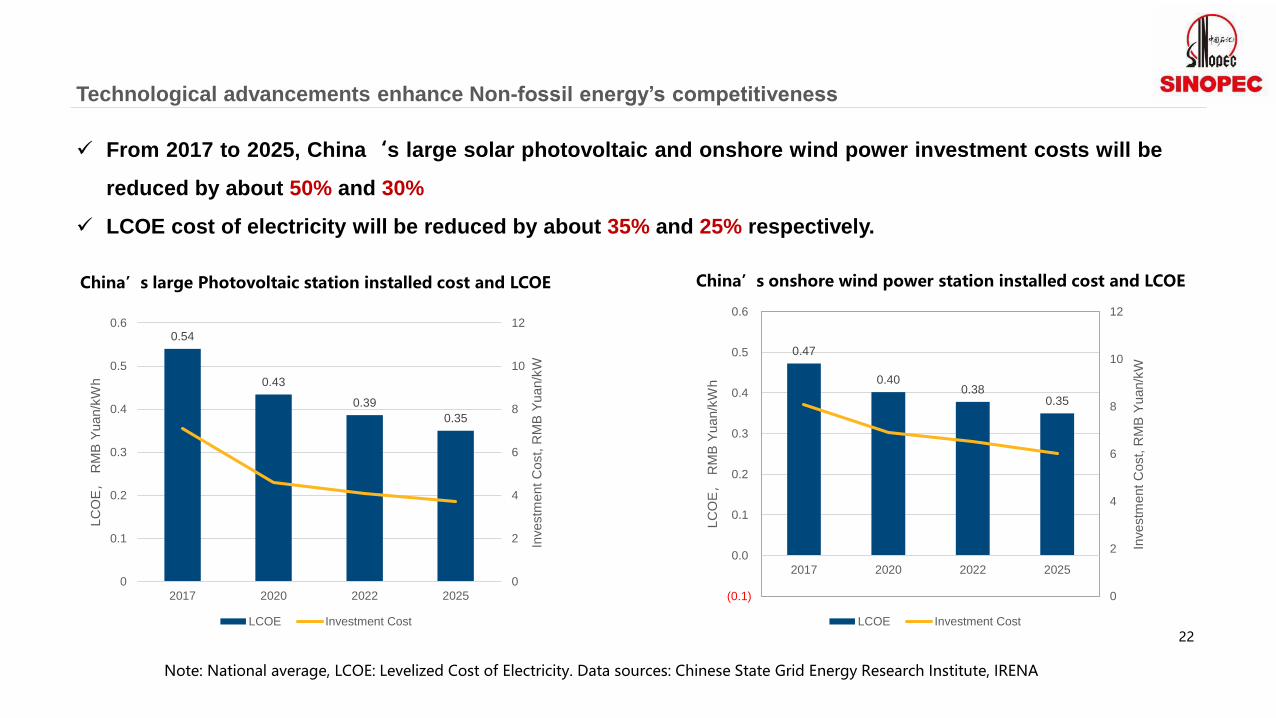

Technological advancements enhance Non-fossil energy’s competitiveness

✓ From 2017 to 2025, China‘s large solar photovoltaic and onshore wind power investment costs will be

reduced by about 50% and 30%

✓ LCOE cost of electricity will be reduced by about 35% and 25% respectively.

Note: National average, LCOE: Levelized Cost of Electricity. Data sources: Chinese State Grid Energy Research Institute, IRENA

China’s large Photovoltaic station installed cost and LCOE China’s onshore wind power station installed cost and LCOE

0.54

0.43

0.39

0.35

0

2

4

6

8

10

12

0

0.1

0.2

0.3

0.4

0.5

0.6

2017 2020 2022 2025

Investm

ent

Cost, R

MB

Yuan/k

W

LC

OE

,R

MB

Yuan/k

Wh

LCOE Investment Cost

0.47

0.400.38

0.35

0

2

4

6

8

10

12

(0.1)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

2017 2020 2022 2025

Investm

ent

Cost, R

MB

Yuan/k

W

LC

OE

,R

MB

Yuan/k

Wh

LCOE Investment Cost

23

Non-fossil energy: China’s electricity generation capacity will keep fast growing

• 2018, China’s non-Fossil energy cumulative installed power capacity is 780 GW, 40% of the total installed

power capacity, generating 2200 TWh of electricity, 30% of total electricity generation.

• 2050, China’s non-Fossil energy cumulative installed power capacity will be over 2800 GW, generating

7300 TWh of electricity.

0

500

1000

1500

2000

2500

3000

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Cum

ula

tive insta

lled

pow

er

capacity,

GW

Hydro power Wind Bio-power Solar PV CSP others Nuclear power

0

1000

2000

3000

4000

5000

6000

7000

8000

200

5

201

0

201

5

202

0

202

5

203

0

203

5

204

0

204

5

205

0

Ele

ctr

icity g

enera

tion,

TW

h

Hydro power Wind Bio-power Solar power others Nuclear power

China's Non-fossil energy cumulative installed power capacity China's Non-fossil energy electricity generation

Energy Demand & International

Cooperation Outlook

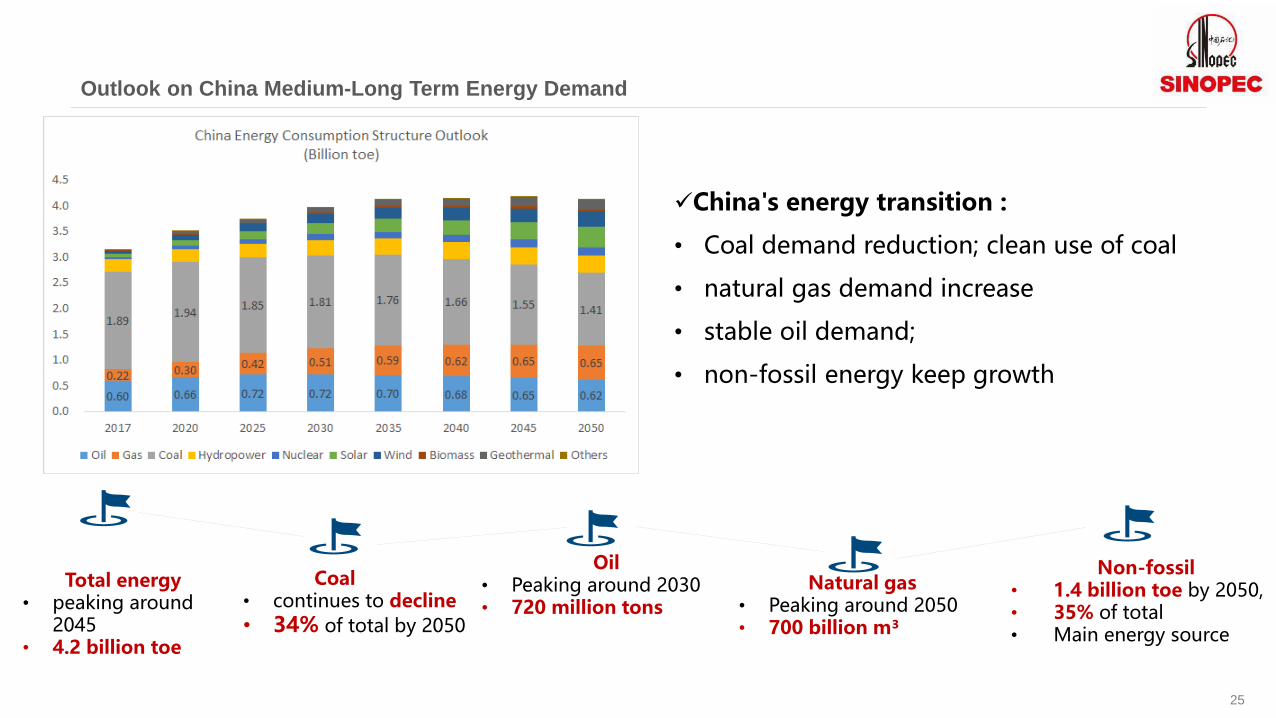

Outlook on China Medium-Long Term Energy Demand

Non-fossil • 1.4 billion toe by 2050,• 35% of total• Main energy source

✓China's energy transition :

• Coal demand reduction; clean use of coal

• natural gas demand increase

• stable oil demand;

• non-fossil energy keep growth

Total energy• peaking around

2045• 4.2 billion toe

Coal• continues to decline

• 34% of total by 2050

Oil• Peaking around 2030• 720 million tons

Natural gas • Peaking around 2050• 700 billion m³

25

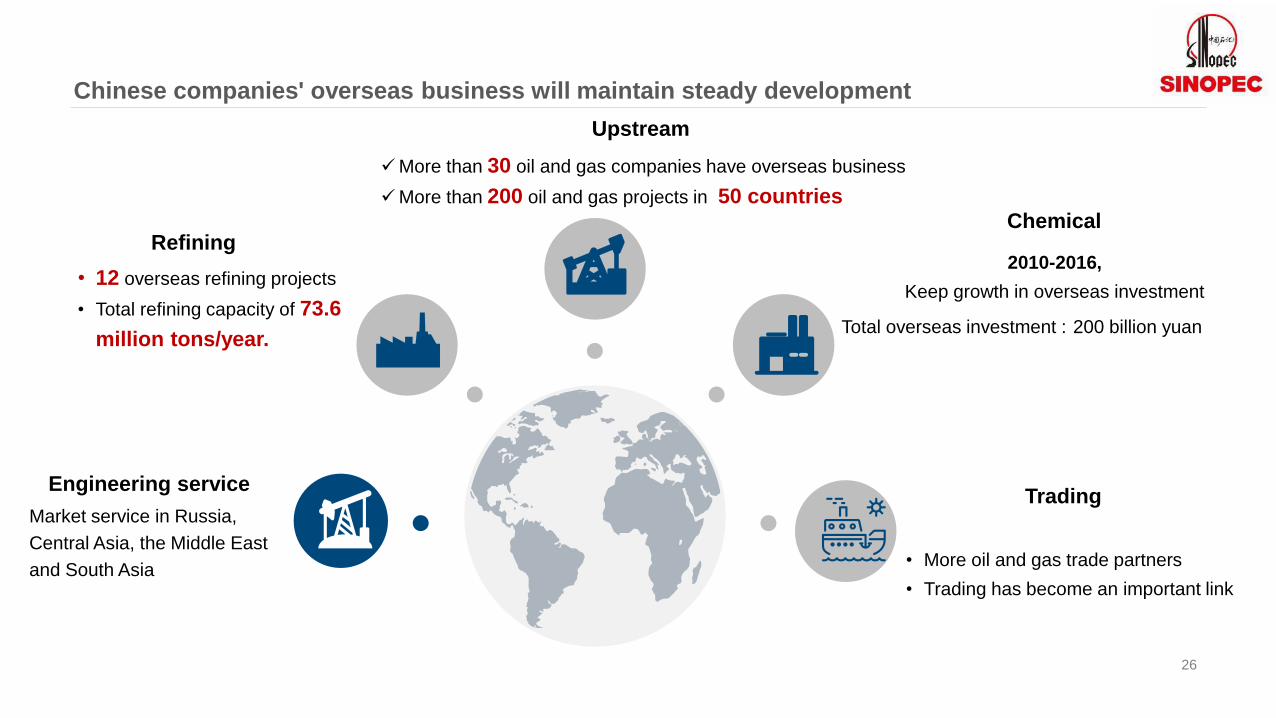

26

Refining

• 12 overseas refining projects

• Total refining capacity of 73.6

million tons/year.

Chemical

2010-2016,

Keep growth in overseas investment

Total overseas investment : 200 billion yuan

Trading

• More oil and gas trade partners

• Trading has become an important link

Engineering service

Market service in Russia,

Central Asia, the Middle East

and South Asia

Upstream

✓More than 30 oil and gas companies have overseas business

✓More than 200 oil and gas projects in 50 countries

Chinese companies' overseas business will maintain steady development

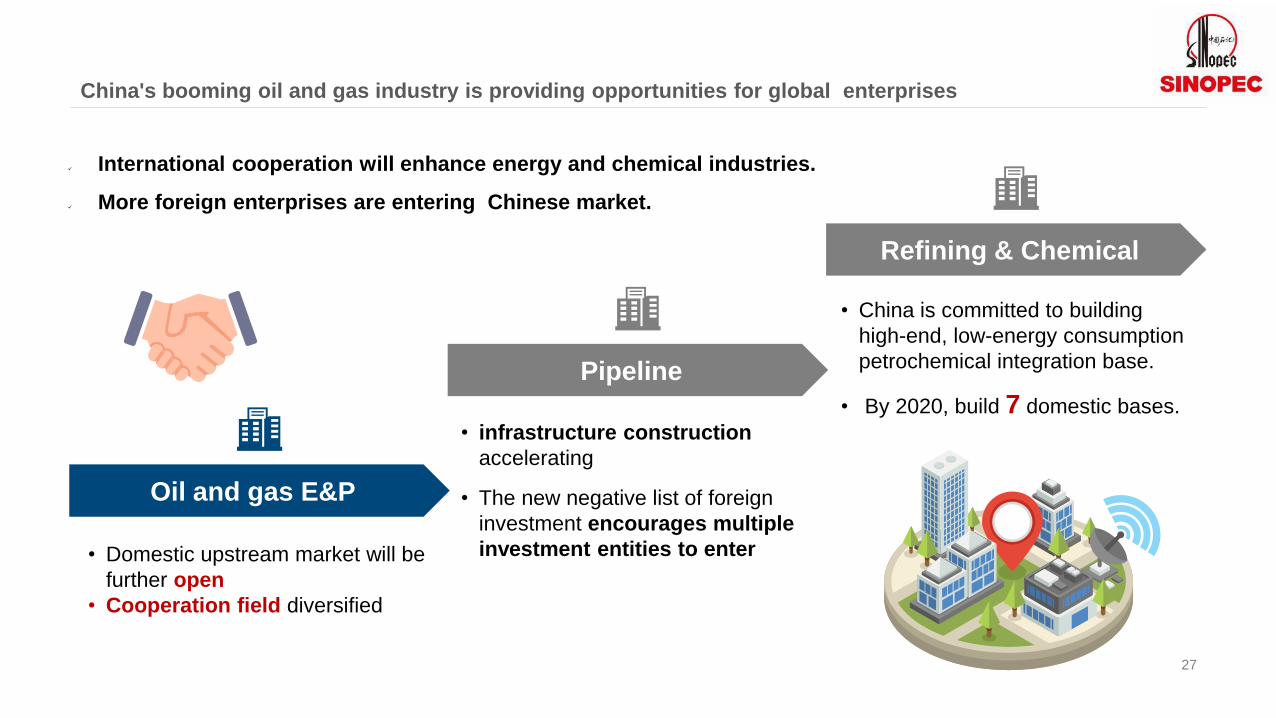

27

Oil and gas E&P

• Domestic upstream market will be

further open

• Cooperation field diversified

Pipeline

• infrastructure construction

accelerating

• The new negative list of foreign

investment encourages multiple

investment entities to enter

Refining & Chemical

• China is committed to building

high-end, low-energy consumption

petrochemical integration base.

• By 2020, build 7 domestic bases.

✓ International cooperation will enhance energy and chemical industries.

✓ More foreign enterprises are entering Chinese market.

China's booming oil and gas industry is providing opportunities for global enterprises

Q&A

Review and Prospect of China’sEnergy and Petrochemical Industry

������ ����� �� � � � ���� � � ����������� ������

���� ��March 25th 2019

The release of 2019 Annual Report of China Energy and Petrochemical Industry

2

Industrial Chains

Refinery�C2�C3C4�PX�C6

6

Parts3 ProductsCrude oil, natural gas, refined oil, ethylene, propylene, ethylene glycol, butadiene rubber, acrylic ……

Over 40

F Economy ForecastF Market AnalysisF Insights on Hot Events

Modules3

F EnergyF Refinery IndustryF Chemical Industry

Main content of the 2019 report

3

Review 2018

Prospect 2019Pattern of Supply and Demand

&Trend of Price

Demand & Supply & Price

How many�

How much� How to change� How to impact�Impacts of Hot Events

International Market China Market

CONTENTS 1 The Development of China Energy and PetrochemicalIndustry over the Past 40 Years

2 The New Pattern of Long-term Development of Energy and Petrochemical Industry in China

3 Market Prediction for 2019

The Development of China Energy and Petrochemical Industry in the Past 40 Years

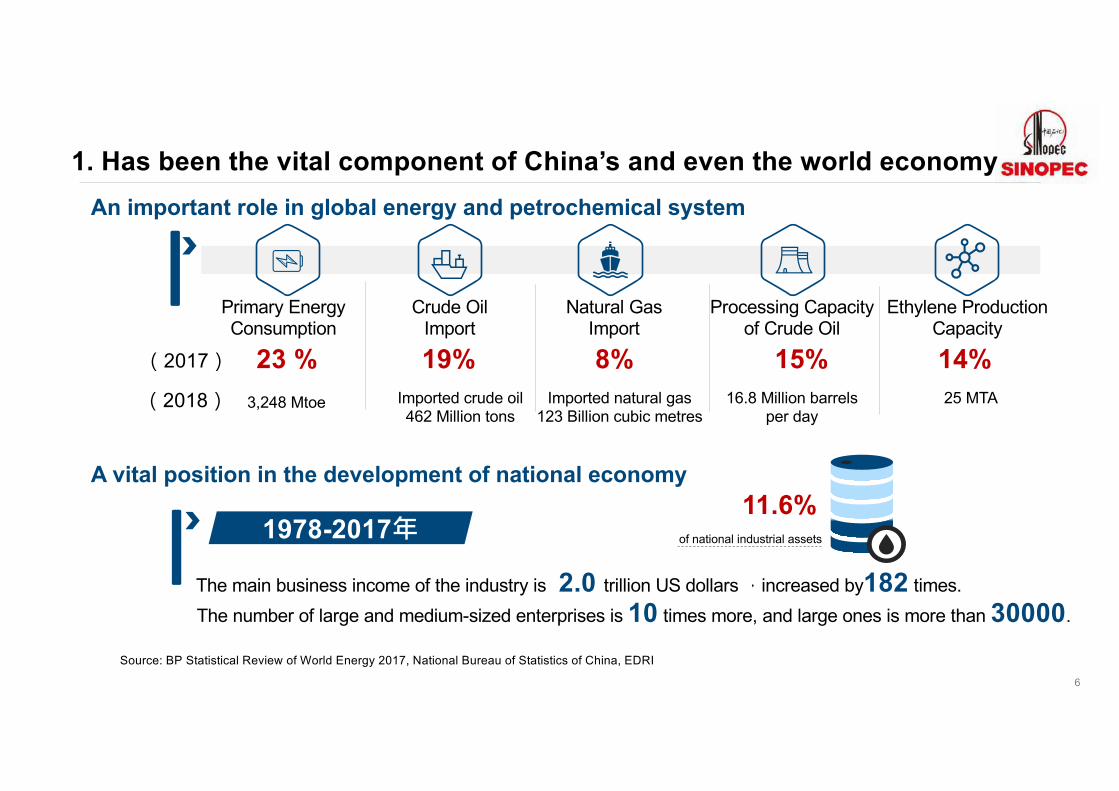

1. Has been the vital component of China’s and even the world economy

6

Crude Oil Import

Imported crude oil462 Million tons

Primary Energy Consumption

16.8 Million barrelsper day

Processing Capacityof Crude Oil

An important role in global energy and petrochemical system

1978-2017�

The main business income of the industry is 2.0 trillion US dollars �increased by182 times.

A vital position in the development of national economy

3,248 Mtoe

The number of large and medium-sized enterprises is 10 times more, and large ones is more than 30000.

11.6%of national industrial assets

19%23 % 8% 15% 14%

Natural GasImport

Imported natural gas 123 Billion cubic metres

Ethylene Production Capacity

25 MTA�2018�

�2017�

Source: BP Statistical Review of World Energy 2017, National Bureau of Statistics of China, EDRI

7

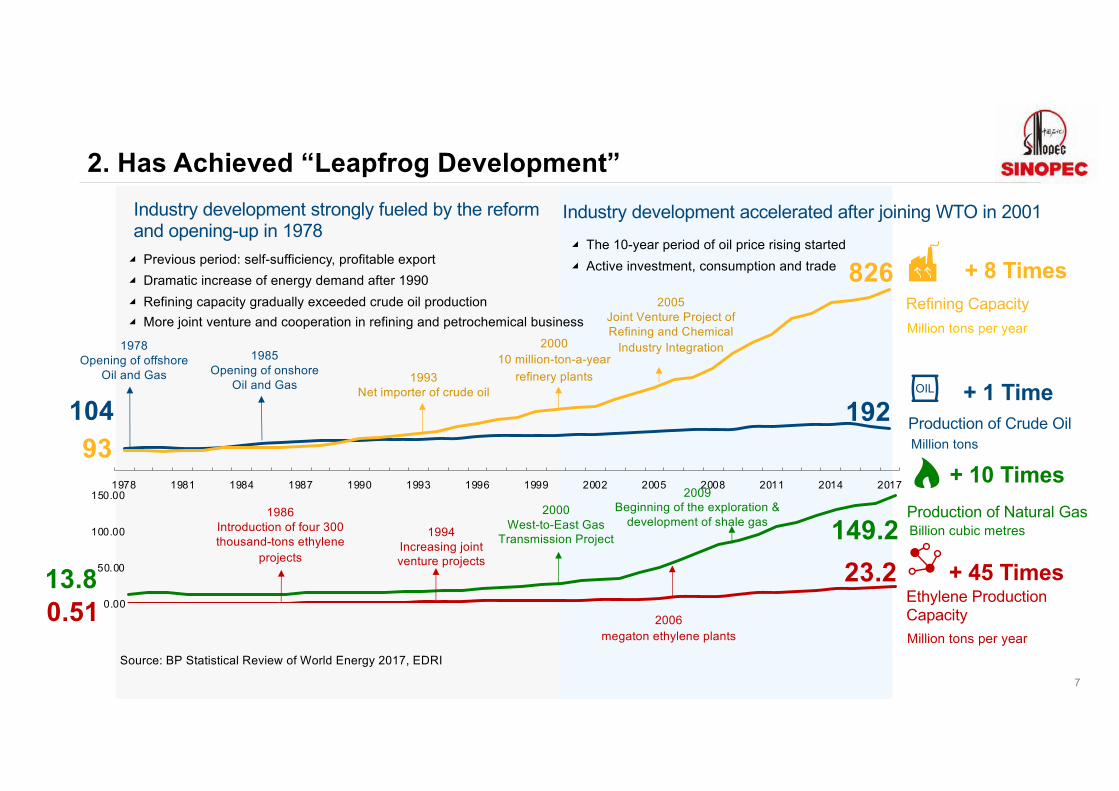

Source: BP Statistical Review of World Energy 2017, EDRI

Industry development accelerated after joining WTO in 2001Industry development strongly fueled by the reform

and opening-up in 1978

1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014 2017

0.00

50.00

100.00

150.00

Ethylene Production

Capacity

Production of Natural Gas

Refining Capacity

Production of Crude Oil

Million tons

Million tons per year

93

826 + 8 Times

192104+ 1 Time

23.20.51

+ 45 Times

Million tons per year

149.2 Billion cubic metres

+ 10 Times

13.8

1993

Net importer of crude oil

1978

Opening of offshore

Oil and Gas

2000

10 million-ton-a-year

refinery plants

2005

Joint Venture Project of

Refining and Chemical

Industry Integration

2006

megaton ethylene plants

1985

Opening of onshore

Oil and Gas

1986

Introduction of four 300

thousand-tons ethylene

projects

1994

Increasing joint

venture projects

2000

West-to-East Gas

Transmission Project

2009

Beginning of the exploration &

development of shale gas

� Previous period: self-sufficiency, profitable export

� Dramatic increase of energy demand after 1990

� Refining capacity gradually exceeded crude oil production

� More joint venture and cooperation in refining and petrochemical business

� The 10-year period of oil price rising started

� Active investment, consumption and trade

2. Has Achieved “Leapfrog Development”

Upgrading Stage�2013~Now�

Mutual Integration Stage�1999-2012�

Go Abroad Stage�1992-1998�

Preliminary Exploration Stage �1978-1991�

Overview of overseas business of Chinese oil companies

u Overseas investment enterprises �

u Overseas Oil and Gas Projects �

2017

210 34

Upgrading internationalenergy cooperation system

3. Opening and cooperation helps be in line with the global industry system

8

Started to “going global”

Focused on “bringing in”�

Combined “bringing in” and “going global”

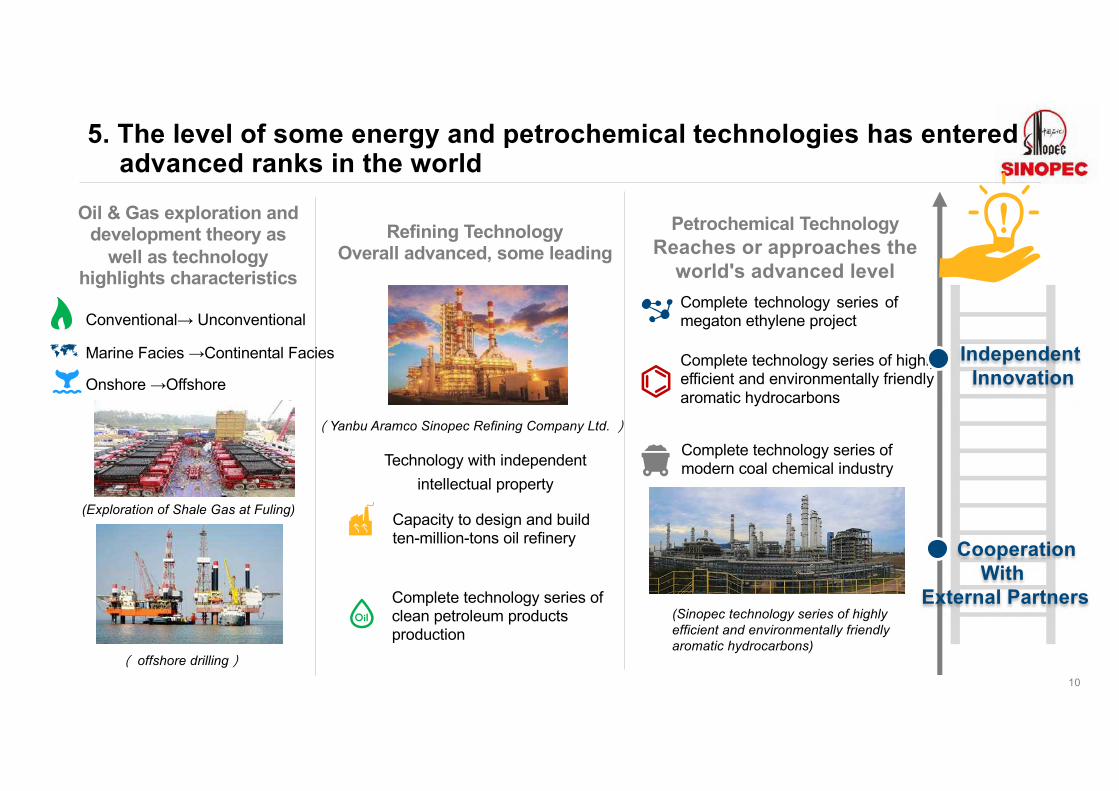

4. A number of petroleum and petrochemical international enterprises have emerged

9

4 3 87 5 8 28 33 9

5 4 93 1 6 10 11 3

69 70 >500 4 5 14 15 3

Refining TechnologyOverall advanced, some leading

Oil & Gas exploration and development theory as

well as technology highlights characteristics

Petrochemical TechnologyReaches or approaches the

world's advanced level

Complete technology series of modern coal chemical industry

Complete technology series ofmegaton ethylene project

Complete technology series of highly efficient and environmentally friendly aromatic hydrocarbons

(Sinopec technology series of highly efficient and environmentally friendly aromatic hydrocarbons)

Onshore →Offshore

Marine Facies →Continental Facies

Conventional→ Unconventional

5. The level of some energy and petrochemical technologies has entered advanced ranks in the world

Cooperation With

External Partners

IndependentInnovation

10

� offshore drilling�

(Exploration of Shale Gas at Fuling)

Technology with independent intellectual property

Capacity to design and build ten-million-tons oil refinery

Complete technology series of clean petroleum products production

�Yanbu Aramco Sinopec Refining Company Ltd. �

The New Pattern of long-term Development of Energy and Petrochemical Industry in China

Hig

h-qu

ality

Dev

elop

men

t In the past 40 years, petroleum and petrochemical industry emphasized on satisfying

Clothing Food Housing Transportation

Past——Meet the Demand of Basic Necessities of Life

Future——Meet the Requirement of High-quality DevelopmentIn the future, petroleum and petrochemical industry emphasized on satisfying

quality and efficiency requirement

More SustainableMore IntelligentCleaner Higher-end

New Development

New Drivers

12

quantity and speed requirement

13

2018

13.6 15.423.3

44.3

96.9

2020 2025 20502035

1.41 1.42 1.41

1.361.44

2029Population�Billion�

GDP�current trillion dollar�

9.9 12 19 36 83GDP Per Capita�thousand dollar�

1.40

• China will be able to maintain GDP growth rate at 6-6.5% by 2025. Also, the population willcontinue to grow and is expected to reach peak at 1.44 billion in 2029.

• China’s Per Capita GDP will increase significantly. Compared to 2018, it will double in2025, triple in 2035, and seven times in 2050.

1. Steadily growing economy in China will constantly provide a sustained impetus for industrial growth

6.5%5.8%

5.0%

4.0%

Source�The State Information Center�Development Research Center of the State Council�EDRI

0

10

20

30

40

50

60

70

80

90

100

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

The 1st New Driver: New urbanization and the rural vitalization strategy will inspire the potential of China's economic and industrial development

Source�UN, National Bureau of Statistics of China, EDRI

60% in 2018

ChinaUS

World70% in 2030

831 Million Urban Population1,018 Million Urban Population

• The rural vitalization strategy will break the urban-rural dual structure and drive economic growth strongly.

• By the free flow of factors , the integration of urban and rural industries could be promoted, level of

urbanization could be raised, the synergy of urban development and rural revitalization could be achieved.

) ( ) % ) ' % % ) % %

14

80% in 2050

The 2nd New Driver: The rising middle class has become a strong driver of consumption growth and industrial upgrading

• Urban residents' consumption is upgrading along the path from necessary

consumption to improved consumption to high-end consumption.

Source�National Bureau of Statistics of China

30.1

8.46.1

23.3

12.5 10.8

6.12.7

28.6

7.2 6.2

22.8

13.611.6

7.3

2.7

3.5

1.1

6.9

8.8

4.77.9 9.0 9.6

Food, Cigarette andLiquor

C lothing Daily necessities andService

Residential Transportation,Communication

Education, Culture andEntertainment

Health Care Other Supplies andServices

% of Consumption Expenditure in 2013 % of Consumption Expenditure in 2017 Growth Rate in 2017

Consumption Upgrade -- - - -

Consumption Expenditure Structure of Urban Residents (%)

One Hundred Million in 2015

Three Hundred and Fifty Million in 2030

Middle Class

15

Northeast China-Eastern InnerMongolia Economic Zone

�Belt and Road�

Yangtze River Economic Belt

Beijing-Tianjin-Hebei Economic Circle &

Xiong'an New Area

Hainan Pilot Free Trade Zone

GDP�%�: Midwest + Northeast

2017 35%2050 40%

GDP�%��East + South

2017 51%2050 46%

The 3rd New Driver: The coordinated regional development strategy will provide a broader space for industrial further expansion

16

Guangdong-Hong Kong-Macao Greater Bay Area

Boosted GDP by more than $7.5

trillion

17

The 4th New Driver: Technological revolution will foster new growth and promote the upgrading of traditional petroleum and petrochemical industries

Emerging IndustryDeveloping and Growing

New Business Model

Clean Energy, Advanced Polymer Materials, High Performance Materials, etc

A New Generation of Information and Technology IndustryBig Data, Cloud Computing, High-end Software, etc

New Energy, New Materials

New Energy VehicleElectric Vehicles, Fuel Cell Vehicle, etc

Traditional IndustryTransforming and Upgrading

Traditional ManufacturingPromoting the In-depth Integration of the Internet, Big Data, Artificial Intelligence with the Real Economy

Building a clean, low-carbon, safe andefficient modern energy system

Energy Industry

Chemical IndustryProduct Upgrading, Resource Conservation and Clean Production

�Internet Plus�, Block chain , Sharing Economy, Modern Supply Chain, etc.

l China will substantially ease market access, strengthen intellectual property rights protection, and

take the initiative to expand imports.

Bringing In

Opening-up of Manufacturing

Open to developed countries

Opening-up of coastal areas

Multilateral opening-up �WTO�

Going Global

Opening-up of Services

Open to developing countries

Opening-up of inland areas

Regional opening-up (free trade zone)

LOREM

18

The 5th New Driver: More comprehensive opening-up in China will create a more favorable industrial investment environment

China will never close but open its door even wider.

ëOutdated production capacity will be largely eliminated to make room for the

development of advanced clean production capacity and green production.

ëEnvironmental costs of companies will be increased significantly.

ëThe development space of urban enterprises will be limited.

Environmental protection costs have accelerated the industry reshuffle, further enhanced the industry concentration.

19

Environmental Protection Policy

The 6th New Driver: The requirement of green development will lead traditional industries to explore new development paths

Air

Water Soil

Long-term Mechanism

TAX

EnvironmentalProtection Tax

Pollutant Discharge Permits

0

5

10

15

20

25

2000 2010 2016 2020 2025 2030 2035 2040

Ene

rgy

Con

sum

ptio

n P

er U

nit G

DP

�kB

tu/$�

�� �� �� �

China’s energy intensity descends most quickly Will reach the peak of carbon emissions before the world does

2000-2017 2026-2035

6.5%

2%

2035-2050

0.7%

5%

0.1%

4%

10%

8%

2017-2025

China's energy consumption has been decoupled from GDP growth

21.6 22.224

28.531.5

33.8 34.5 36 36.7 36.9 36.8 36.3 35.5

2.3 3 3.46.1

8.1 9.3 9.5 9.9 9.8 9.5 8.9 8.1 7.2

1990 2000 2010 2020 2030 2040 2050

00 4 5 3 24

240 00 4 53 4 52

2. China’s energy transition will move faster than the world, and energy efficiency will be greatly improved

20

GDP growth rate

Energy consumption growth rate

Total World China Europe US

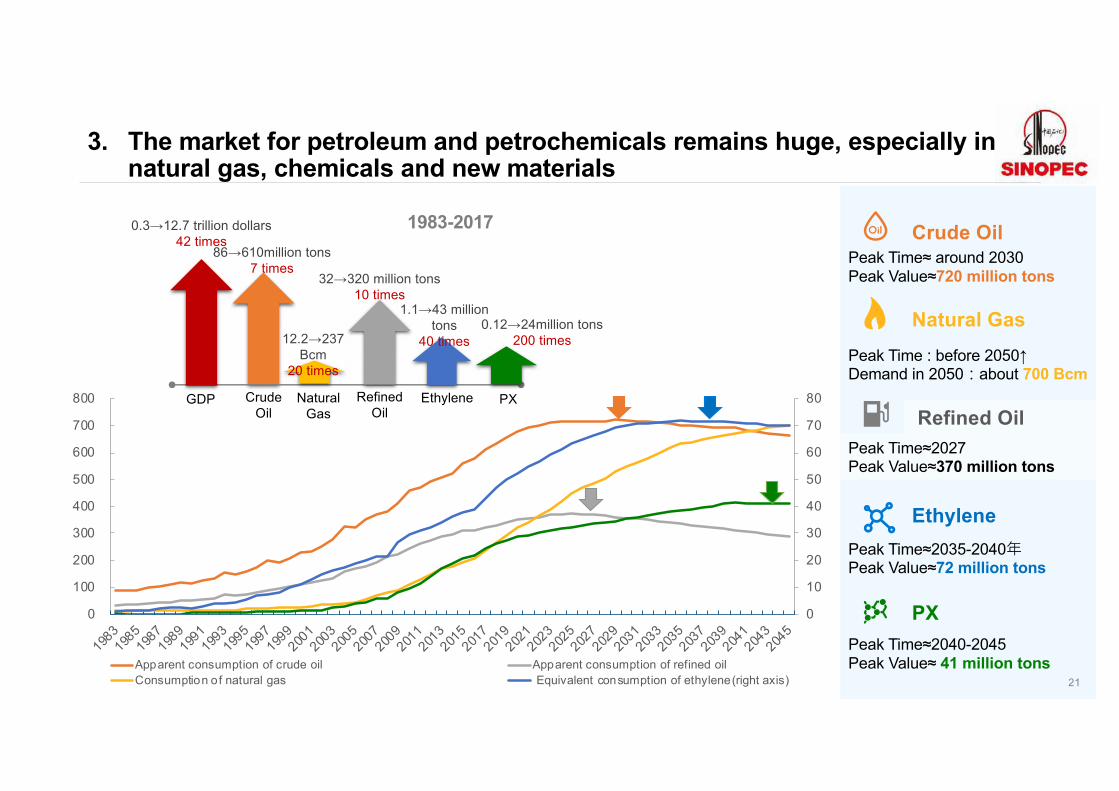

3. The market for petroleum and petrochemicals remains huge, especially in natural gas, chemicals and new materials

Peak Time : before 2050↑Demand in 2050�about 700 Bcm

0

10

20

30

40

50

60

70

80

0

100

200

300

400

500

600

700

800

1983198

5198

7198

9199

1199

3199

5199

7199

9200

1200

3200

5200

7200

9201

1201

3201

5201

7201

9202

1202

3202

5202

7202

9203

1203

3203

5203

7203

9204

1204

3204

5

Apparent consumption of crude oil Apparent consumption of refined oil

Consumption of natural gas Equivalent consumption of ethylene(right axis)

Peak Time≈ around 2030Peak Value≈720 million tons

Crude Oil

Peak Time≈2035-2040�Peak Value≈72 million tons

Ethylene

Peak Time≈2027Peak Value≈370 million tons

Refined Oil

Peak Time≈2040-2045Peak Value≈ 41 million tons

Natural Gas

PX

1983-2017

Crude Oil

Natural Gas

Refined Oil

Ethylene PX

86→610million tons7 times

12.2→237 Bcm

20 times

32→320 million tons10 times

1.1→43 million tons

40 times0.12→24million tons

200 times

GDP

0.3→12.7 trillion dollars42 times

21

4. China's market will be more competitive, with the gradual formation of a pluralistic supply system

22

Supply of Oil and Gas

Foreign and private-owned refining

projects perform actively

Refining and Petrochemical

Private LNG terminals operating International chemical giants

have entered ChinaFine Chemicals

Foreign and private-owned companies

have invested in gas station

Sale Terminals

Market Prediction for 2019

24

2019 Annual Report of China Energy and Petrochemical Industry Focuses on 6 Questions

What Are the Roads Ahead for World and China Economy�

How Do We Evaluate Forces that Influence the Sustainable Development of Energy?

How Will the New Expansion of Refinery and Petrochemical Capacity Influence the Market�

Will Gas Supply be very tight in 2019?

Will Business Cycle of Refining and Petrochemical Industry Continue in 2019?

How Will the Market Demand Be in 2019 �

1

2

3

4

5

6

1. What Are the Roads Ahead of World and China’s Economy�

25

Higher Risks

Stability First

2018�3.2%2019�3.1%

2018�6.6%2019�6.0-6.5%

Trade frictionUnilateral sanctions

I. Shrinking Trade

The manufacturing PMI has decreased by 3.8% since the beginning of 2018

II. Contracting Real

Economy

Employment Finance Foreign Trade

Foreign Investment Investment Expectation

StableStable Stable

Stable Stable Stable

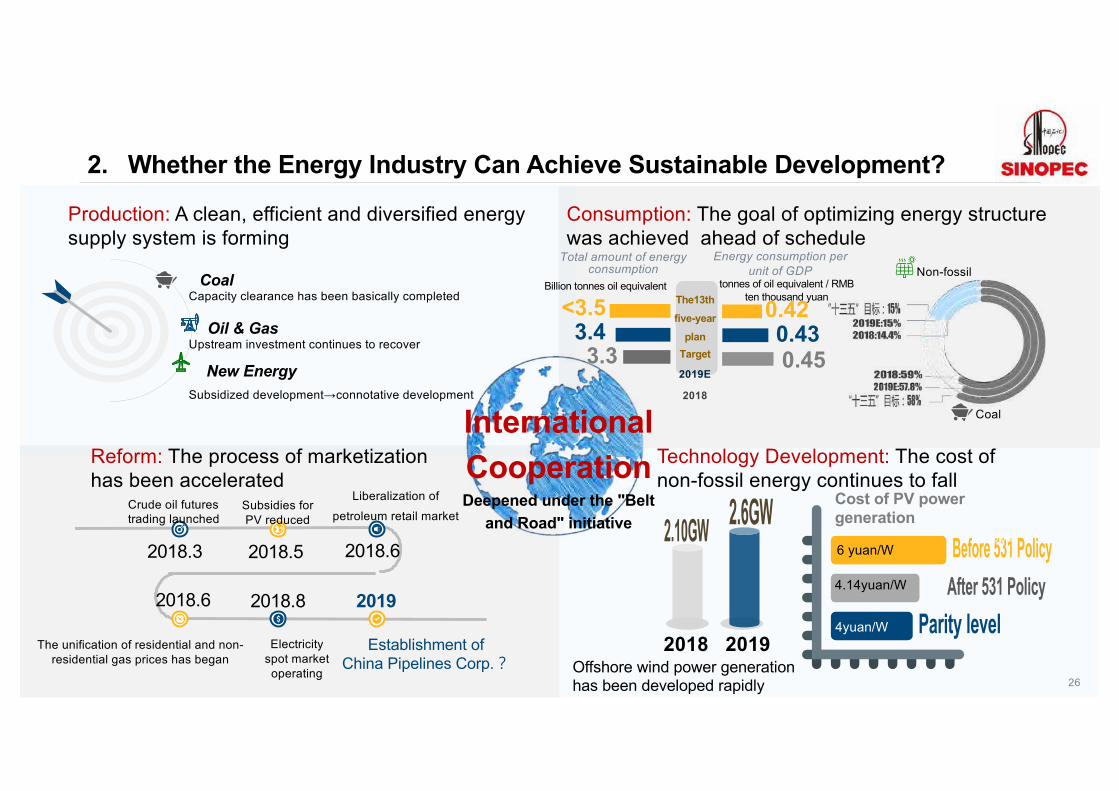

2. Whether the Energy Industry Can Achieve Sustainable Development?

26

Reform: The process of marketizationhas been accelerated

Technology Development: The cost of non-fossil energy continues to fall

Non-fossil

Coal

2018 2019Offshore wind power generation has been developed rapidly

Cost of PV power generation

6 yuan/W

4.14yuan/W

4�/�

4yuan/W

Production: A clean, efficient and diversified energy supply system is forming

Consumption: The goal of optimizing energy structure was achieved ahead of schedule

The unification of residential and non-residential gas prices has began

2018.6

Crude oil futures trading launched

2018.3

Subsidies for PV reduced

2018.5

Liberalization of petroleum retail market

2018.6

Electricity spot market operating

2018.8

Establishment of China Pipelines Corp.�

2019

Capacity clearance has been basically completedCoal

Upstream investment continues to recoverOil & Gas

Subsidized development→connotative development

New Energy

International

CooperationDeepened under the "Belt

and Road" initiative

0.42

0.45

Total amount of energy consumption

Billion tonnes oil equivalent

Energy consumption per unit of GDP

tonnes of oil equivalent / RMB ten thousand yuanThe13th

five-year

plan

Target

2019E

2018

0.43<3.5

3.43.3

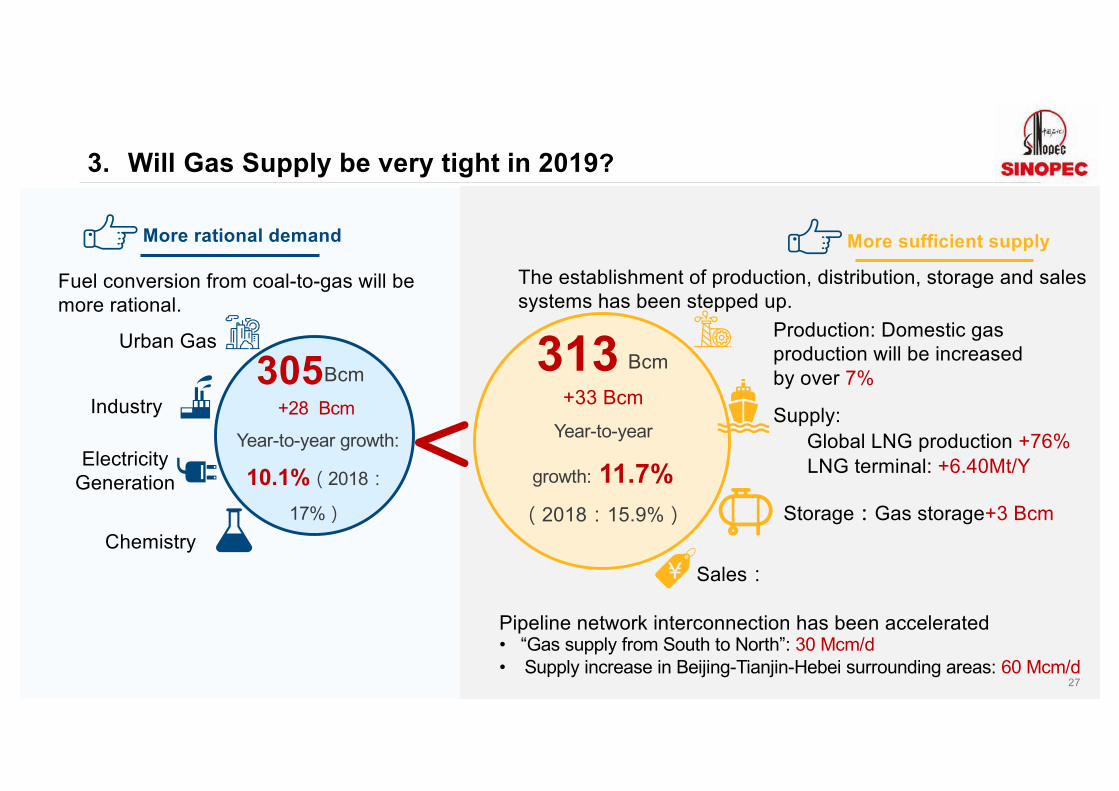

3. Will Gas Supply be very tight in 2019?

27

Bcm

+28 Bcm

Year-to-year growth:

10.1%�2018�

17%�

Fuel conversion from coal-to-gas will be

more rational.

More rational demand

Bcm

+33 Bcm

Year-to-year

growth: 11.7%�2018�15.9%�

Production: Domestic gas

production will be increased

by over 7%

Global LNG production +76%

Sales�

Storage�Gas storage+3 Bcm

Supply:

The establishment of production, distribution, storage and sales

systems has been stepped up.

More sufficient supply

Pipeline network interconnection has been accelerated

• “Gas supply from South to North”: 30 Mcm/d

• Supply increase in Beijing-Tianjin-Hebei surrounding areas: 60 Mcm/d

LNG terminal: +6.40Mt/Y

Urban Gas

Industry

Electricity

Generation

Chemistry

313305

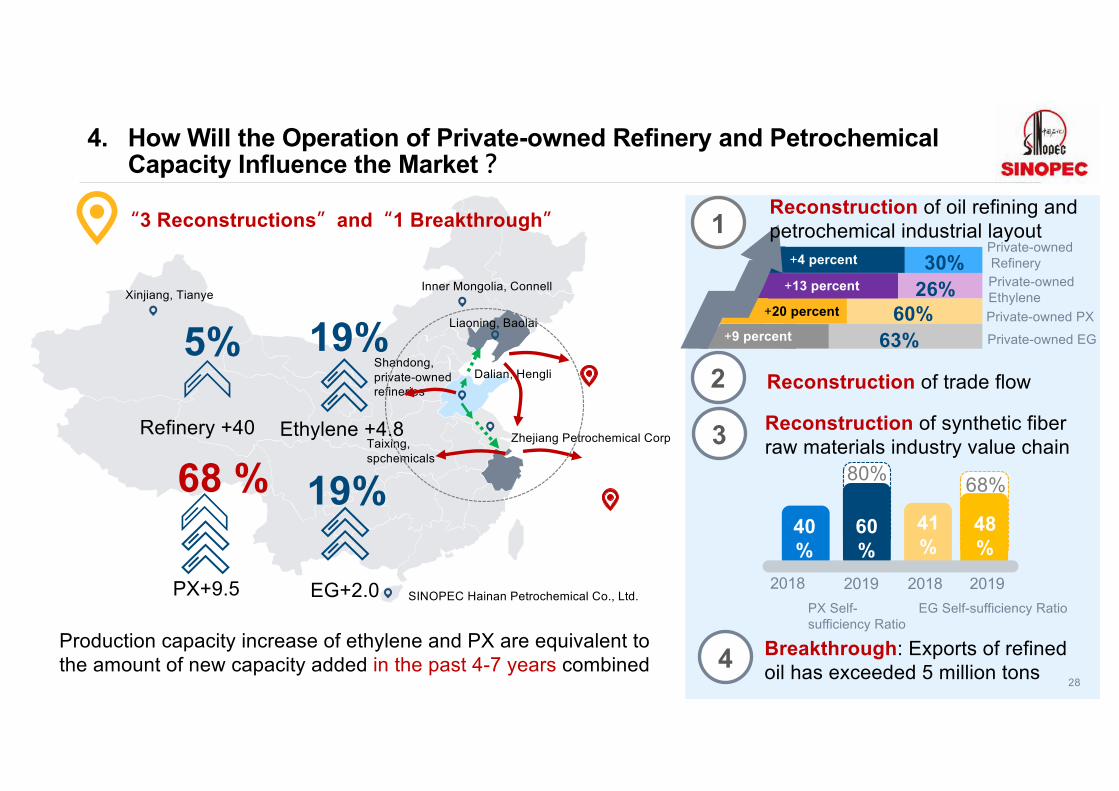

4. How Will the Operation of Private-owned Refinery and Petrochemical Capacity Influence the Market�

Dalian, Hengli

Zhejiang Petrochemical Corp

Shandong, private-owned refineries

Liaoning, Baolai

SINOPEC Hainan Petrochemical Co., Ltd.

Taixing, spchemicals

Inner Mongolia, ConnellXinjiang, Tianye

�3 Reconstructions�and�1 Breakthrough�

30%

60%63%

Private-ownedRefinery

Private-owned PX

Private-owned EG

1

2

Reconstruction of oil refining and petrochemical industrial layout

Reconstruction of trade flow

4 Breakthrough: Exports of refined oil has exceeded 5 million tons

+4 percent

+20 percent

+9 percent

Refinery +40

19%68 %

19%

Ethylene +4.8

PX+9.5 EG+2.0

Production capacity increase of ethylene and PX are equivalent to the amount of new capacity added in the past 4-7 years combined

26% Private-owned Ethylene

+13 percent

3 Reconstruction of synthetic fiber raw materials industry value chain

40%

2018 20192019 2018

60%

41%

48%

80% 68%

PX Self-sufficiency Ratio

EG Self-sufficiency Ratio

28

5%

5. How Will the Market Demand Be in 2019 �

29

2017 2018 2019E

5% 2%3%

366379 386

Total volume will increase

Growth rate will decrease

49.85.5%

4.3%

0.1 %

0%

0.1 %

0.6 %

2.1 %

1.5 %

4.9%

47.29.2%

The supporting factors of last year disappeared.

Unit: million tonsUnit: Million tons

1 %

Infrastructure constructionwill stand out

Downturn of Auto

-5%Growth rate of auto

consumption

-3%

Transportation from Highway to Railway

Alternative Fuel for Replacement

92%Ratio of refined oil

consumption

93%

Economic Slowdown

6-6.5%Growth of GDP

6.6%

Demand of refined oil will weaken Demand of petrochemicals will slow down

* end-use consumption

Focus on export→

Environmental protection /overhaul

Ban of plasticsimport

Basic growth→

→

→

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

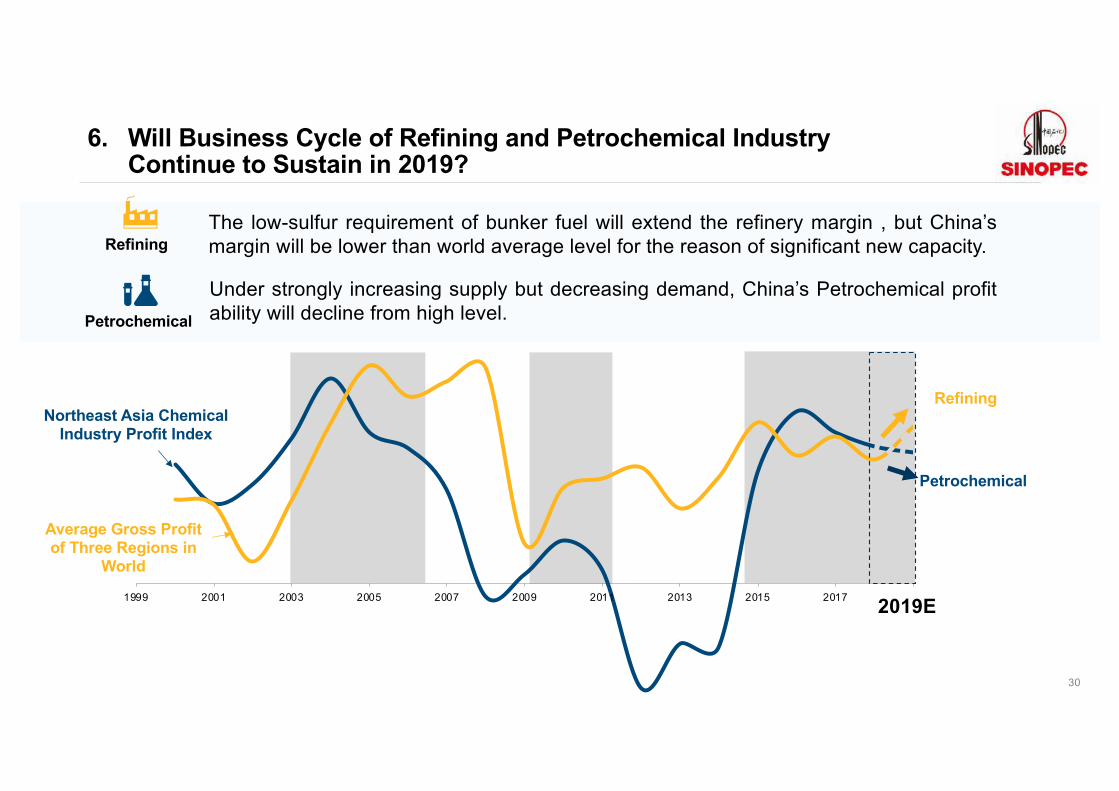

6. Will Business Cycle of Refining and Petrochemical Industry Continue to Sustain in 2019?

Petrochemical

Refining

2019E

The low-sulfur requirement of bunker fuel will extend the refinery margin , but China’smargin will be lower than world average level for the reason of significant new capacity.

Northeast Asia Chemical Industry Profit Index

Average Gross Profit of Three Regions in

World

Refining

Under strongly increasing supply but decreasing demand, China’s Petrochemical profitability will decline from high level.Petrochemical

30

Thank you

![Eliminierung von Aceton und Bildung von protoniertem Aceton …zfn.mpdl.mpg.de/data/Reihe_B/37/ZNB-1982-37b-1169.pdf · 2018-02-09 · [2.2.6.6]-Tetra[D3] ... pentanon die oben erwähnten](https://static.documents.pub/doc/80x56/5cc9404388c9936a208c3755/eliminierung-von-aceton-und-bildung-von-protoniertem-aceton-zfnmpdlmpgdedatareiheb37znb-1982-37b-1169pdf.jpg)