11

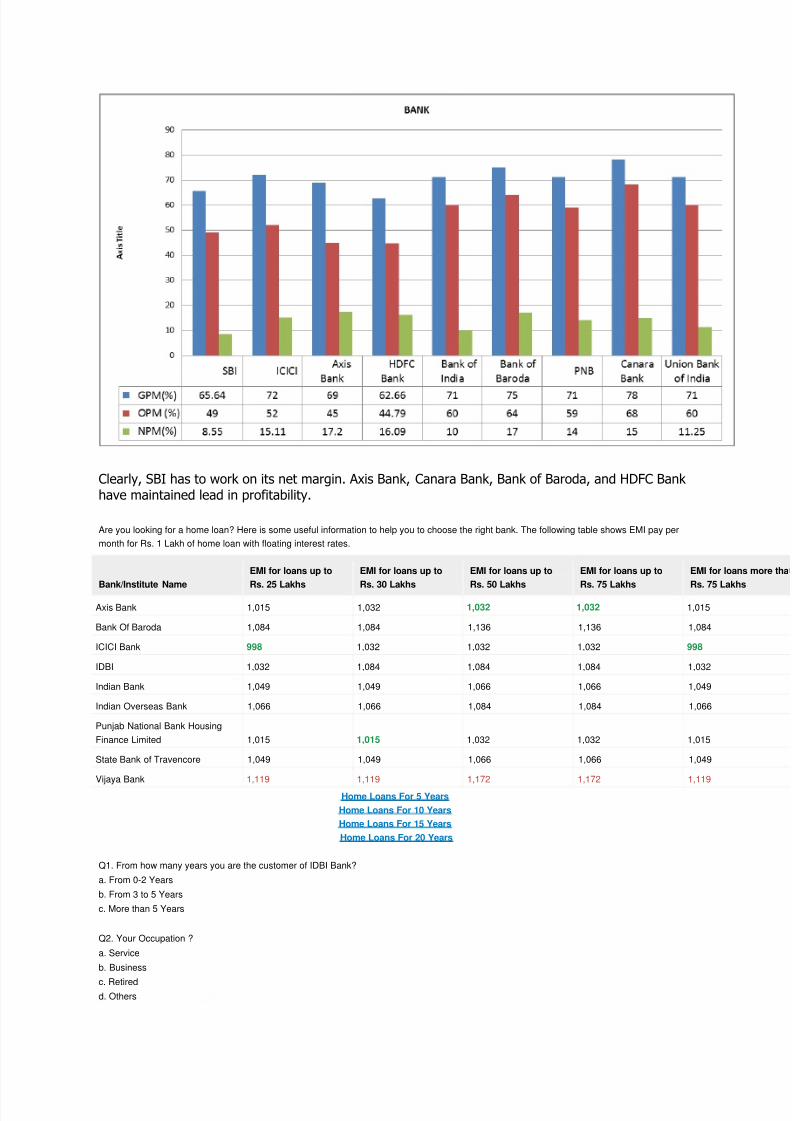

A comparative analysis of banks Written by Vertical Grass Friday, 24 February 2012 00:00 Banking sector is going to be the most watched sector in the coming quarters. There are reasons for this. RBI has hinted that it will reduce th e CRR rate and repo rates. Kingfisher air line has impacted few banks and it will play its own part. NPAs of banks have gone up recently. The debt/GDP ratio of the Government is scary at 80% essentially meaning that the Government cannot borrow much without jeopardizing stability of banking sector. In this backdrop, we studies 10 banks on various parameters which are important for banks to track. These parameters impact the outlook of banks. RESULT FOR Q3 FY 2011 - 12 Parameters SBI ICICI Axis HDFC BoI BoB PNB Can Bank UBI IDBI CAR (%) 11.6 18.88 11.78 16.3 11.18 13.45 11.48 13.22 11.72 13.53 NIM(%) 4.05 2.7 3.75 4.1 2.55 3.44 3.85 2.52 3.31 1.89 GROSS NPA(%) 4.61 - 1.1 1.1 2.74 1.48 2.42 1.81 3.33 2.94 NET NPA(%) 2.22 0.7 0.39 0.2 1.78 0.51 1.11 1.49 1.88 1.96 CASA (%) 48.95 43.6 42.2 47.7 32.41 35 36.2 25 32.54 19.67 Capital adequacy ratio (CAR) is fine with all the banks. All of them are adequately secured on this front. SBI is the one of PSU bank with high CASA ratio giving it the advantage to collect low cost deposit from people. This essentially reduces the cost of money for SBI which it can lend at higher rate to borrowers thus pocketing the difference as their profit. HDFC is equally strong when it comes to CASA ratio. This is surprising though. ICICI and Axis banks have done very well on this front too. IDBI has shown good improvement in last few quarters. The management of IDBI started focusing on retail investors recently and it will take some time before they catch up with big banks. NIM (net interest margin) the most important number for banks is best for SBI. This conforms t o the observation that SBI has highest CASA ratio. A high CASA ratio gives SBI enormous flexibility. This, in turn, results into higher NIM. HDFC is once again is equally good on NIM. IDBI, Bank of India, Canara Bank, and ICICI bank need to work on this front. IDBI’s aggressive foray into retail banking is costing it in terms of NIM. Gross NPA, even though net NPA is not scary, should be a cause of concern for SBI, IDBI, and BoI. Banks typically turn very liberal when it comes to calculati ng net NPA. Hence people should look at gross NPA first and then the net NPA. If there is huge difference (such as net NPA is 50% of gross NPA), it is time to see how the banks have defined NPA. Net NPA, ratio which scares banks, is highest for SBI. This could be the result of teaser loans offered by it and also economic slowdown which has hit the indu stry hard. Since SBI has significant exposure to companies, its net NPA is showing high number. Let’s take a look at profit margin.