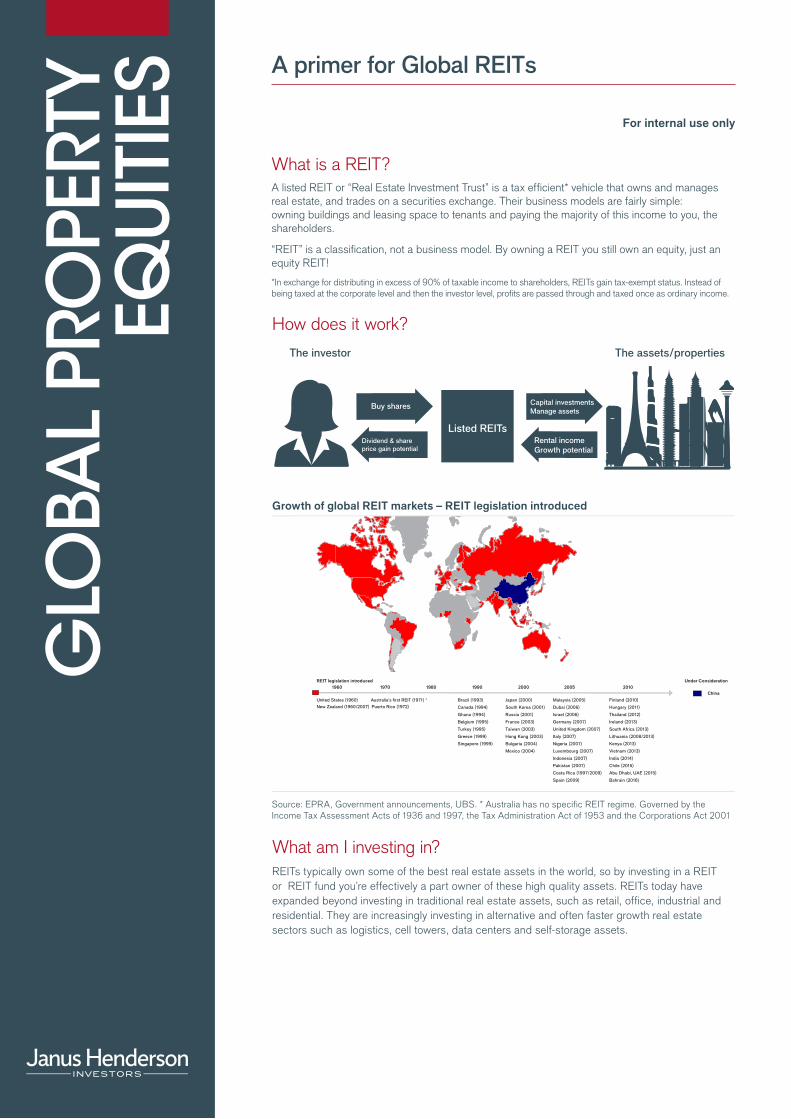

GLOBAL PROPERTY EQUITIES How does it work? Growth of global REIT markets – REIT legislation introduced What am I investing in? REITs typically own some of the best real estate assets in the world, so by investing in a REIT or REIT fund you’re effectively a part owner of these high quality assets. REITs today have expanded beyond investing in traditional real estate assets, such as retail, office, industrial and residential. They are increasingly investing in alternative and often faster growth real estate sectors such as logistics, cell towers, data centers and self-storage assets. A primer for Global REITs For internal use only What is a REIT? A listed REIT or “Real Estate Investment Trust” is a tax efficient* vehicle that owns and manages real estate, and trades on a securities exchange. Their business models are fairly simple: owning buildings and leasing space to tenants and paying the majority of this income to you, the shareholders. “REIT” is a classification, not a business model. By owning a REIT you still own an equity, just an equity REIT! *In exchange for distributing in excess of 90% of taxable income to shareholders, REITs gain tax-exempt status. Instead of being taxed at the corporate level and then the investor level, profits are passed through and taxed once as ordinary income. REIT legislation introduced Under Consideration 1960 1970 1980 1990 2000 2005 2010 China United States (1960) Australia's first REIT (1971) * Brazil (1993) Canada (1994) Ghana (1994) Belgium (1995) Turkey (1995) Greece (1999) Singapore (1999) Japan (2000) South Korea (2001) Russia (2001) France (2003) Taiwan (2003) Hong Kong (2003) Bulgaria (2004) Mexico (2004) Malaysia (2005) Dubai (2006) Israel (2006) Germany (2007) United Kingdom (2007) Italy (2007) Nigeria (2007) Luxembourg (2007) Indonesia (2007) Pakistan (2007) Costa Rica (1997/2009) Spain (2009) Finland (2010) Hungary (2011) Thailand (2012) Ireland (2013) South Africa (2013) Lithuania (2008/2013) Kenya (2013) Vietnam (2013) India (2014) Chile (2015) Abu Dhabi, UAE (2015) Bahrain (2016) New Zealand (1960/2007) Puerto Rico (1972) Source: EPRA, Government announcements, UBS. * Australia has no specific REIT regime. Governed by the Income Tax Assessment Acts of 1936 and 1997, the Tax Administration Act of 1953 and the Corporations Act 2001 The investor The assets/properties Dividend & share price gain potential Rental income Growth potential Capital investments Manage assets Buy shares Listed REITs

Transcript

GLO

BAL

PRO

PERT

Y E

QU

ITIE

S

How does it work?

Growth of global REIT markets – REIT legislation introduced

What am I investing in?REITs typically own some of the best real estate assets in the world, so by investing in a REIT or REIT fund you’re effectively a part owner of these high quality assets. REITs today have expanded beyond investing in traditional real estate assets, such as retail, office, industrial and residential. They are increasingly investing in alternative and often faster growth real estate sectors such as logistics, cell towers, data centers and self-storage assets.

A primer for Global REITs

For internal use only

What is a REIT? A listed REIT or “Real Estate Investment Trust” is a tax efficient* vehicle that owns and manages real estate, and trades on a securities exchange. Their business models are fairly simple: owning buildings and leasing space to tenants and paying the majority of this income to you, the shareholders.

“REIT” is a classification, not a business model. By owning a REIT you still own an equity, just an equity REIT!

*In exchange for distributing in excess of 90% of taxable income to shareholders, REITs gain tax-exempt status. Instead of being taxed at the corporate level and then the investor level, profits are passed through and taxed once as ordinary income.

United States (1960) Australia's rst REIT (1971) * Brazil (1993)

Canada (1994)

Ghana (1994)

Belgium (1995)

Turkey (1995)

Greece (1999)

Singapore (1999)

Japan (2000)

South Korea (2001)

Russia (2001)

France (2003)

Taiwan (2003)

Hong Kong (2003)

Bulgaria (2004)

Mexico (2004)

Malaysia (2005)

Dubai (2006)

Israel (2006)

Germany (2007)

United Kingdom (2007)

Italy (2007)

Nigeria (2007)

Luxembourg (2007)

Indonesia (2007)

Pakistan (2007)

Costa Rica (1997/2009)

Spain (2009)

Finland (2010)

Hungary (2011)

Thailand (2012)

Ireland (2013)

South Africa (2013)

Lithuania (2008/2013)

Kenya (2013)

Vietnam (2013)

India (2014)

Chile (2015)

Abu Dhabi, UAE (2015)

Bahrain (2016)

New Zealand (1960/2007) Puerto Rico (1972)

guy.barnard@ janushenderson.com

Source: EPRA, Government announcements, UBS. * Australia has no specific REIT regime. Governed by the Income Tax Assessment Acts of 1936 and 1997, the Tax Administration Act of 1953 and the Corporations Act 2001

From 1998 to 2016 lisedREITs delivered a 9.4% annualised return versus7.1% for unlisted real estate*

The investor The assets/properties

Dividend & share price gain potential

Rental incomeGrowth potential

Capital investments Manage assets

Buy shares

Listed REITs

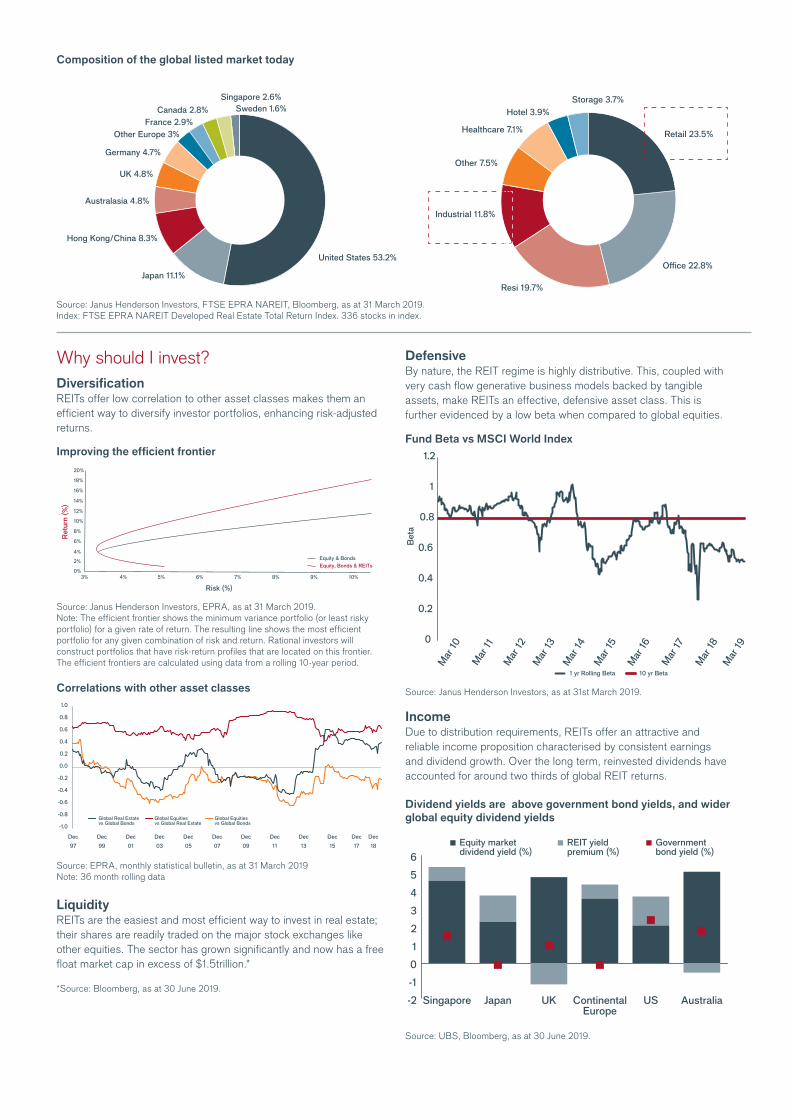

Composition of the global listed market today

Why should I invest?Diversification REITs offer low correlation to other asset classes makes them an efficient way to diversify investor portfolios, enhancing risk-adjusted returns.

Improving the efficient frontier

Source: Janus Henderson Investors, EPRA, as at 31 March 2019. Note: The efficient frontier shows the minimum variance portfolio (or least risky portfolio) for a given rate of return. The resulting line shows the most efficient portfolio for any given combination of risk and return. Rational investors will construct portfolios that have risk-return profiles that are located on this frontier. The efficient frontiers are calculated using data from a rolling 10-year period.

Correlations with other asset classes

Source: EPRA, monthly statistical bulletin, as at 31 March 2019 Note: 36 month rolling data

LiquidityREITs are the easiest and most efficient way to invest in real estate; their shares are readily traded on the major stock exchanges like other equities. The sector has grown significantly and now has a free float market cap in excess of $1.5trillion.*

*Source: Bloomberg, as at 30 June 2019.

DefensiveBy nature, the REIT regime is highly distributive. This, coupled with very cash flow generative business models backed by tangible assets, make REITs an effective, defensive asset class. This is further evidenced by a low beta when compared to global equities.

Fund Beta vs MSCI World Index

Source: Janus Henderson Investors, as at 31st March 2019.

IncomeDue to distribution requirements, REITs offer an attractive and reliable income proposition characterised by consistent earnings and dividend growth. Over the long term, reinvested dividends have accounted for around two thirds of global REIT returns.

Dividend yields are above government bond yields, and wider global equity dividend yields

Source: UBS, Bloomberg, as at 30 June 2019.

Australasia 4.8%

UK 4.8%

Germany 4.7%

Other Europe 3%France 2.9%

Hong Kong/China 8.3%

Japan 11.1%

Sweden 1.6%

United States 53.2%

Singapore 2.6%

Canada 2.8%

Retail 23.5%

O�ce 22.8%

Resi 19.7%

Industrial 11.8%

Other 7.5%

Storage 3.7%Hotel 3.9%

Healthcare 7.1%

Source: Janus Henderson Investors, FTSE EPRA NAREIT, Bloomberg, as at 31 March 2019. Index: FTSE EPRA NAREIT Developed Real Estate Total Return Index. 336 stocks in index.

Ret

urn

(%)

Risk (%)

Equity & BondsEquity, Bonds & REITs

3% 4%0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

5% 6% 7% 8% 9% 10%

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Dec

18

Dec

17

Dec

15

Dec

13

Dec

11

Dec

09

Dec

07

Dec

05

Dec

03

Dec

01

Dec

99

Dec

97

Global Real Estate vs Global Bonds

Global Equities vs Global Real Estate

Global Equities vs Global Bonds

-50%

-40%

-30%

-20%

-10%0%

10%20%30%

Mar19

Mar17

Mar15

Mar13

Mar11

Mar09

Mar07

Mar05

Mar03

Global property premium/discount to NAV

0

0.2

0.4

0.6

0.8

1

1.2

Bet

a

1 yr Rolling Beta 10 yr Beta

Mar

10

Mar

11

Mar

12

Mar

13

Mar

14

Mar

15

Mar

16

Mar

17

Mar

18M

ar 19

-2

-1

0

1

2

3

4

5

6

AustraliaUSContinentalEurope

UKJapanSingapore

Equity market dividend yield (%)

REIT yield premium (%)

Government bond yield (%)

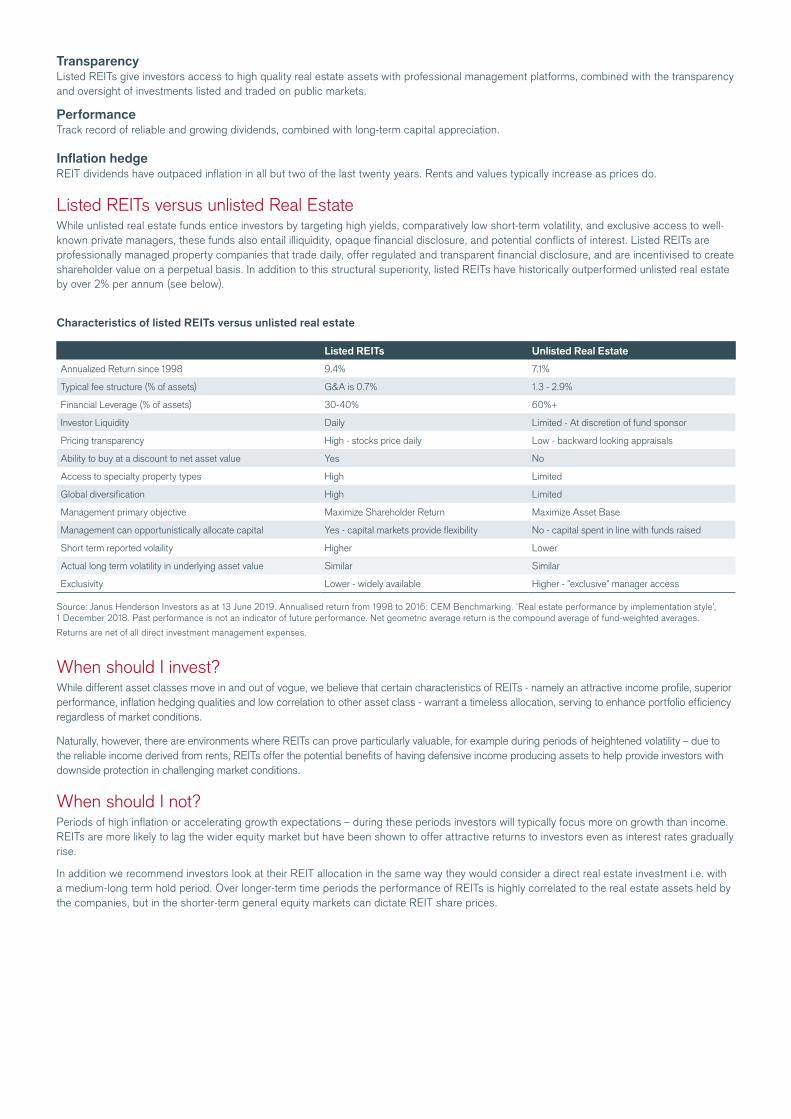

TransparencyListed REITs give investors access to high quality real estate assets with professional management platforms, combined with the transparency and oversight of investments listed and traded on public markets.

PerformanceTrack record of reliable and growing dividends, combined with long-term capital appreciation.

Inflation hedgeREIT dividends have outpaced inflation in all but two of the last twenty years. Rents and values typically increase as prices do.

Listed REITs versus unlisted Real EstateWhile unlisted real estate funds entice investors by targeting high yields, comparatively low short-term volatility, and exclusive access to well-known private managers, these funds also entail illiquidity, opaque financial disclosure, and potential conflicts of interest. Listed REITs are professionally managed property companies that trade daily, offer regulated and transparent financial disclosure, and are incentivised to create shareholder value on a perpetual basis. In addition to this structural superiority, listed REITs have historically outperformed unlisted real estate by over 2% per annum (see below).

Characteristics of listed REITs versus unlisted real estate

Listed REITs Unlisted Real Estate

Annualized Return since 1998 9.4% 7.1%

Typical fee structure (% of assets) G&A is 0.7% 1.3 - 2.9%

Financial Leverage (% of assets) 30-40% 60%+

Investor Liquidity Daily Limited - At discretion of fund sponsor

Ability to buy at a discount to net asset value Yes No

Access to specialty property types High Limited

Global diversification High Limited

Management primary objective Maximize Shareholder Return Maximize Asset Base

Management can opportunistically allocate capital Yes - capital markets provide flexibility No - capital spent in line with funds raised

Short term reported volaility Higher Lower

Actual long term volatility in underlying asset value Similar Similar

Exclusivity Lower - widely available Higher - "exclusive" manager access

Source: Janus Henderson Investors as at 13 June 2019. Annualised return from 1998 to 2016: CEM Benchmarking. ‘Real estate performance by implementation style’, 1 December 2018. Past performance is not an indicator of future performance. Net geometric average return is the compound average of fund-weighted averages.

Returns are net of all direct investment management expenses.

When should I invest?While different asset classes move in and out of vogue, we believe that certain characteristics of REITs - namely an attractive income profile, superior performance, inflation hedging qualities and low correlation to other asset class - warrant a timeless allocation, serving to enhance portfolio efficiency regardless of market conditions.

Naturally, however, there are environments where REITs can prove particularly valuable, for example during periods of heightened volatility – due to the reliable income derived from rents, REITs offer the potential benefits of having defensive income producing assets to help provide investors with downside protection in challenging market conditions.

When should I not?Periods of high inflation or accelerating growth expectations – during these periods investors will typically focus more on growth than income. REITs are more likely to lag the wider equity market but have been shown to offer attractive returns to investors even as interest rates gradually rise.

In addition we recommend investors look at their REIT allocation in the same way they would consider a direct real estate investment i.e. with a medium-long term hold period. Over longer-term time periods the performance of REITs is highly correlated to the real estate assets held by the companies, but in the shorter-term general equity markets can dictate REIT share prices.

Important InformationThis document is intended solely for the use of professionals and is not for general public distribution. Any investment application will be made solely on the basis of the information contained in the Fund’s prospectus (including all relevant covering documents), which will contain investment restrictions. This document is intended as a summary only and potential investors must read the Fund’s prospectus and key investor information document before investing. A copy of the Fund’s prospectus and key investor information document can be obtained from Henderson Global Investors Limited in its capacity as Investment Manager and Distributor. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes. Past performance is not a guide to future performance. The performance data does not take into account the commissions and costs incurred on the issue and redemption of units. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Tax assumptions and reliefs depend upon an investor’s particular circumstances and may change if those circumstances or the law change. If you invest through a third party provider you are advised to consult them directly as charges, performance and terms and conditions may differ materially. The securities included in this document are not registered in the Foreign Securities Registry of the Superintendencia de Valores y Seguros for public offering and, therefore, the use of this document is only for general information purposes. Nothing in this document is intended to or should be construed as advice. This document is not a recommendation to sell or purchase any investment. It does not form part of any contract for the sale or purchase of any investment. The Fund is a recognised collective investment scheme for the purpose of promotion into the United Kingdom. Potential investors in the United Kingdom are advised that all, or most, of the protections afforded by the United Kingdom regulatory system will not apply to an investment in the Fund and that compensation will not be available under the United Kingdom Financial Services Compensation Scheme.

The Janus Henderson Horizon Fund (the “Fund”) is a Luxembourg SICAV incorporated on 30 May 1985, managed by Henderson Management S.A. Issued by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Capital International Limited (reg no. 3594615), Henderson Global Investors Limited (reg. no. 906355), Henderson Investment Funds Limited (reg. no. 2678531), AlphaGen Capital Limited (reg. no. 962757), Henderson Equity Partners Limited (reg. no. 2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Henderson Management S.A. (reg. no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier).

A copy of the Fund’s prospectus, key investor information document, articles of incorporation, annual and semi-annual reports can be obtained free of cost from the local offices of Janus Henderson Investors: 201 Bishopsgate, London, EC2M 3AE for UK, Swedish and Scandinavian investors; Via Dante 14, 20121 Milan, Italy, for Italian investors and Roemer Visscherstraat 43-45, 1054 EW Amsterdam, the Netherlands. for Dutch investors; and the Fund’s: Austrian Paying Agent Raiffeisen Bank International AG, Am Stadtpark 9, A-1030 Vienna; French Paying Agent BNP Paribas Securities Services, 3, rue d’Antin, F-75002 Paris; German Information Agent Marcard, Stein & Co, Ballindamm 36, 20095 Hamburg; Belgian Financial Service Provider CACEIS Belgium S.A., Avenue du Port 86 C b320, B-1000 Brussels; Spanish Representative Allfunds Bank S.A. Estafeta, 6 Complejo Plaza de la Fuente, La Moraleja, Alcobendas 28109 Madrid; Singapore: Singapore Representative Janus Henderson Investors (Singapore) Limited,138 Market Street, #34-03/04 CapitaGreen, Singapore 048946; or Swiss Representative BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich who are also the Swiss Paying Agent. RBC Investor Services Trust Hong Kong Limited, a subsidiary of the joint venture UK holding company RBC Investor Services Limited, 51/F Central Plaza, 18 Harbour Road, Wanchai, Hong Kong, Tel: +852 2978 5656 is the Fund’s Representative in Hong Kong.

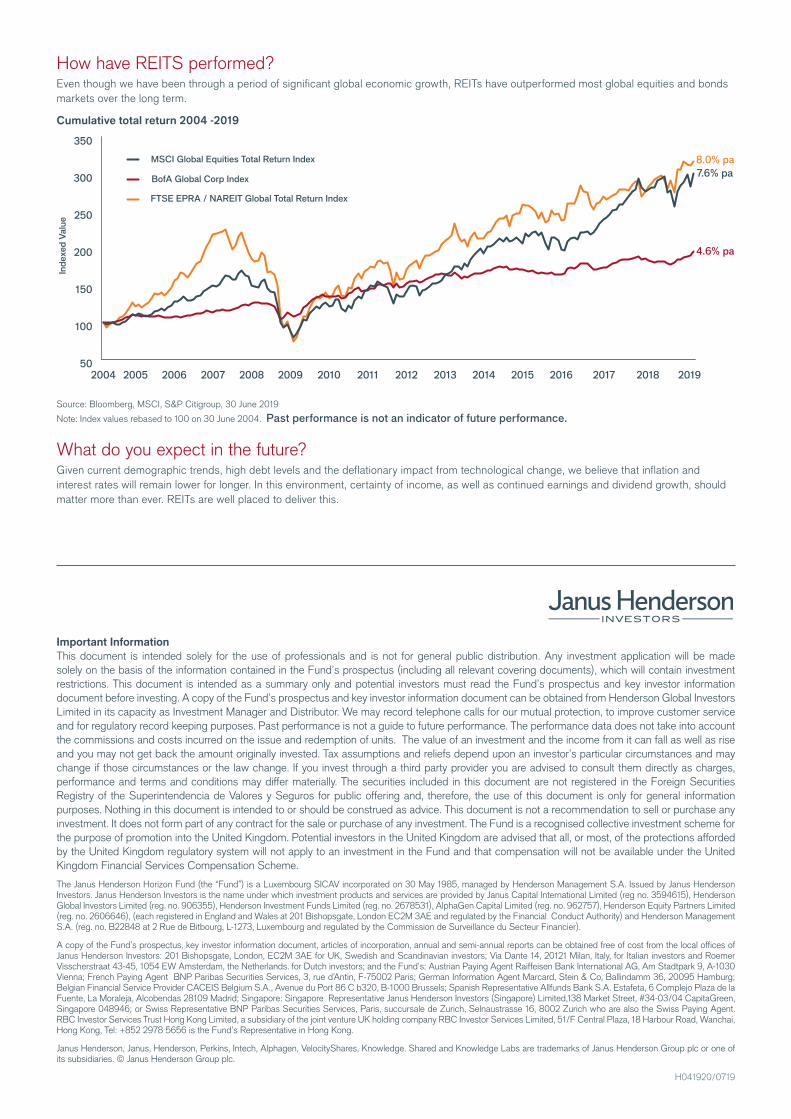

How have REITS performed?Even though we have been through a period of significant global economic growth, REITs have outperformed most global equities and bonds markets over the long term.

Cumulative total return 2004 -2019

Source: Bloomberg, MSCI, S&P Citigroup, 30 June 2019

Note: Index values rebased to 100 on 30 June 2004. Past performance is not an indicator of future performance.

What do you expect in the future?Given current demographic trends, high debt levels and the deflationary impact from technological change, we believe that inflation and interest rates will remain lower for longer. In this environment, certainty of income, as well as continued earnings and dividend growth, should matter more than ever. REITs are well placed to deliver this.