A PROJECT REPORT ON “ASTUDY ONWORKING CAPITAL MANAGEMENT At Bharat Earth Movers Limited (BEML)” SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF THE DEGREE OF BACHELOR OF BUSINESS MANAGEMENT BANGALORE UNIVERSITY BY MS. K.THANUSHREE (Reg.no.13VFC24116) UNDER THE GUIDELINES OF Mrs. ASHIMA GUPTA B.B.M Faculty of Management NEW HORIZON COLLEGE MARATHALLI BANGALORE -560087 2015-2016

Transcript

A PROJECT REPORT

ON

“ASTUDY ONWORKING CAPITAL MANAGEMENT

At Bharat Earth Movers Limited (BEML)”

SUBMITTED IN PARTIAL FULFILLMENT OF THE

REQUIREMENTS FOR THE AWARD OF THE DEGREE OF

BACHELOR OF BUSINESS MANAGEMENT

BANGALORE UNIVERSITY

BY

MS. K.THANUSHREE

(Reg.no.13VFC24116)

UNDER THE GUIDELINES OF

Mrs. ASHIMA GUPTA B.B.M

Faculty of Management

NEW HORIZON COLLEGE

MARATHALLI BANGALORE -560087

2015-2016

DECLARATION

I, THANUSHREE.K a student of New Horizon college Bangalore university,

Bangalore here by affirm that the project work “ A STUDY ON WORKING

CAPITAL MANAGEMENT” is bonafide work carried out entirely by me at

BEML, Bangalore under the guidance of Mrs.AshimaGupta , for partial

fulfilment for the award of bachelor of business management to Bangalore

University, Bangalore.

I also declare that this project has not been submitted to any other university/

institution for the award of any degree.

Place: Bangalore Name: THANUSHREE. K

Date: Reg.no.13VFC24116

GUIDE CERTIFICATE

Certified that the project report entitled “A Study on working capital

management at BEML” submitted by Thanushree.K, for the award of “

Bachelor of Business Management” of Bangalore University, Bangalore is

a record of independent project work under taken by her, under my supervision

and guidance and the project has not be submitted either in part or whole for the

award of any other degree or diploma of any university.

Place : Bangalore MRS. ASHIMA GUPTA

Date: (Internal guide)

HOD CERTIFICATE

This is to certify that THANUSHREE. K(13VFC24116) is bonafide student of

bachelor of business management. The project work entitle “A study on

working capital management at BEML” is bonafide work carried out by

Thanushree. K (13VFC24116) on partial fulfilment of the requirement for the

award of degree in business management of Bangalore university during the

year 2015-2016. It is to certify that all corrections/suggestions have been

incorporated in the project report and a copy is deposited in the department

library. This project work as been approved as it satisfies the academic

requirement for the award of bachelors of business management degree.

Place: Bangalore PRASANNA PRAKASH

Date: (HOD)

PRINCIPAL CERTIFICATE

This is to certify that THANUSHREE.K(13VFC24116) bonafide student of

this college. The project work entitled “A study on working capital

management at BEML” is bonafidework carried out by THANUSHREE.K

(13VFC24116) in partial fulfilment of requirement for the award of degree in

business management of Bangalore University during the year 2015-2016.

Place: Bangalore Dr.BODHI SATHVAN

Date: (principal)

ACKNOWLEDGEMENT

I would like to thank all those persons who have contributed towards the

successful completion of the project work. I am glad to say that working on this

project was illuminating and enjoyable for me.

I take this opportunity to thank our respected chairman Sri.Mohan Manghnani,

and our beloved principal Dr. Bodhi Sathvan for their generosity and kindness

to embrace us in, New Horizon college, Bangalore university .I have deep sense

of gratitude to Mrs. PrasannaPrakash professor and head of the department.

And Mrs. Ashima Gupta my internal project guide for her encouragement,

guidance and valuable suggestions throughout the project.

I deem it a great pleasure in acknowledge my external guide Mrs.Vijaya

Lakshmi, for her kind heart in allowing me to do the project work in the

organization and for his able guidance, expert advice and encouragement.

I would like to thank all the faculty members of BBM and my friends who

directly and indirectly helped me to complete this project.

Words fail me in expressing my deep sense of gratitude and affection to my

parents, for their constant love and moral support without them I could not have

been what I am.

THANUSHREE.K

(13VFC24116)

CONTENTS

Sl. No

CONTENTS

PAGE.

NO

1 Introduction

1-15

2 Company profile

16-42

3 Research design

43-44

4 Analysis and interpretation

45-73

5 Findings, suggestions and

conclusion

74-76

Bibliography

77

Annexure

78-83

LIST OF TABLES

TABLE

NO

TITLE OF TABLES

PAGE NO

1.1 Table showing current ratio 48

1.2 Table showing absolute liquid ratio

50

1.3 Table showing inventory to working

capital

52

1.4 Table showing inventory turnover ratio 54

1.5 Table showing working capital turnover

ratio

56

1.6 Table showing current assets turnover

ratio

58

1.7 Table showing fixed assets turnover

ratio

60

1.8 Table showing total assets turnover ratio 62

1.9 Table showing net- profit ratio

64

1.10 Table showing proprietary ratio

66

1.11 Table showing fixed assets to net worth

ratio

68

1.12 Table showing current assets to net

worth ratio

70

1.13 Table showing current liabilities to net

worth ratio

72

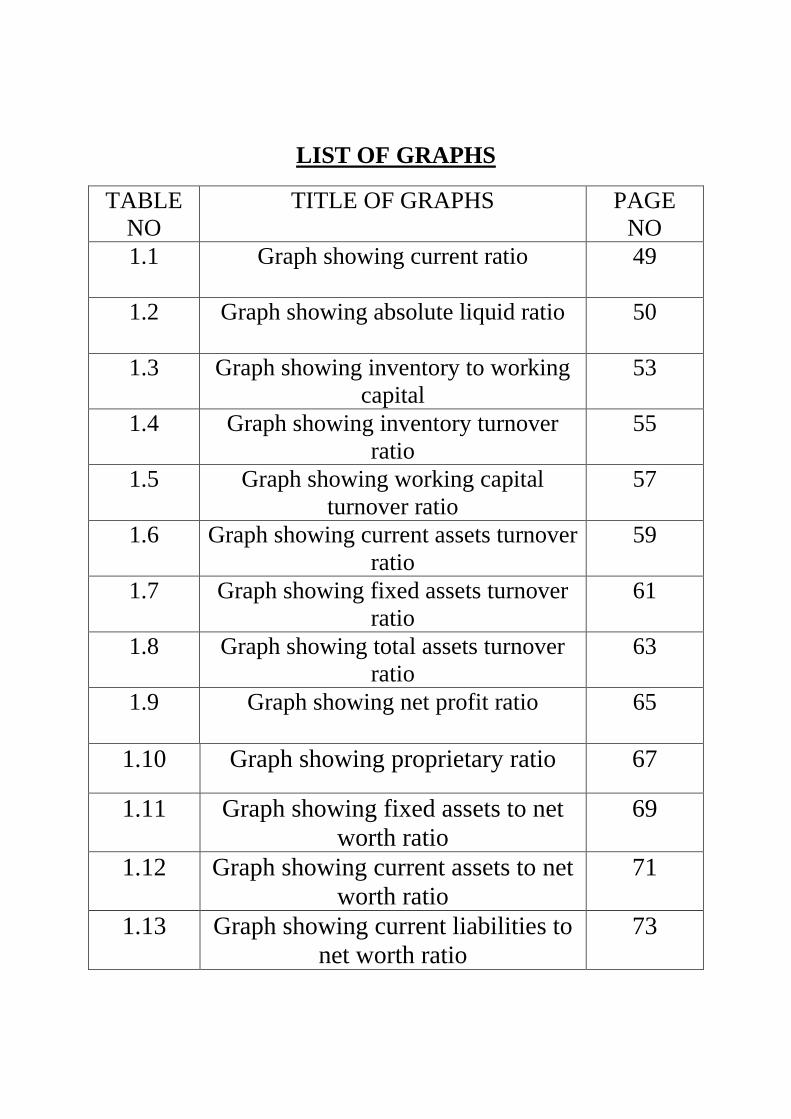

LIST OF GRAPHS

TABLE

NO

TITLE OF GRAPHS PAGE

NO

1.1 Graph showing current ratio

49

1.2 Graph showing absolute liquid ratio

50

1.3 Graph showing inventory to working

capital

53

1.4 Graph showing inventory turnover

ratio

55

1.5 Graph showing working capital

turnover ratio

57

1.6 Graph showing current assets turnover

ratio

59

1.7 Graph showing fixed assets turnover

ratio

61

1.8 Graph showing total assets turnover

ratio

63

1.9 Graph showing net profit ratio

65

1.10 Graph showing proprietary ratio 67

1.11 Graph showing fixed assets to net

worth ratio

69

1.12 Graph showing current assets to net

worth ratio

71

1.13 Graph showing current liabilities to

net worth ratio

73

EXECUTIVE SUMMARY

A Study on working capital management at “BEML”

Working capital management most significant part of assets of large majority of the

companies..

Suitable measures to overcome them and to find out the operating strength and weakness of

the firm.

The scope was to considering the availability of time, information and sources Of study is

confined to the performance of BEML. This study aims at analyzing the overall working

capital management of the company by using various tools and techniques.

The limitations was availability of information for the working capital management at

company was limited and restricted.

The findings are total working capital growth showing the progress trend. As the company

can use just in time technique, so that cost incurred on raw materials can be saved. The major

part of the inventory can be seen in raw materials and finished goods and remaining part in

work in progress.

The project work at working capital management has given me a clear idea of an

organization. The internship helped me a lot in theoretical concepts, which I learnt in my

regular course.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 1

CHAPTER-1

INTRODUCTION

FINANACE

Financial is the science of funds management. The general areas of finance are business finance,

personal finance, and public finance. Finance includes saving money and often includes lending money.

The field of finance deals with the concept of time, money risk how they are interrelated. It also deals

with how money is spent and budgeted, finance works most basically through individual and business

organisations depositing money in a bank. The bank then lends then money out to other individuals or

corporations for consumption or investment, and charges interest on the loans.

Loans have become increasingly packaged for resale, meaning that an investor buys the loan (debt) from

a bank or directly from a corporation. Bonds are debt sold directly to investor from corporation, while that

investor can hold the debt and collect the interest or sell the debt on a secondary market. Banks are the

main facilitator of funding through the provision of credit, although private equity, mutual funds, hedge

funds, and other organisation have become as important as they invest in various forms of debt. Financial

asset, know as investments, are financially managed with careful attention to financial risk management

to control financial risk. Financial instruments allow many forms of securitised asset to be traded on

securities exchanges such as stock exchanges, including debt such as bonds as well as equity in publicly-

traded corporation. Central banks , such as the federal reserve system banks in the united states and bank

of England in the united kingdom , are strong players in public finance , acting as lenders of last resort

as well as strong influence monitory and credit conditions in the economy.

Finance is also considered to be the life blood of business. Financial management is concerned with

procurement and utilization funds in a proper way. Therefore, financial management enjoys great

importance in an organization. Financial management is crucial for the success of a business.

IMPORTANCE OF FINANCE

Finance is associated with plans and results of every functional department because every proposal and

every decision entails financial problems and has an influence on financial results. Finance is an

important function of every organization and its importance is listed below:

To set up an enterprise is very necessary.

For achievement of organizational goals finance is necessary.

Knowledge of finance and its tools and techniques provide strong and sound basis for making decision

in all business matters.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 2

For the achievement of wealth maximization gaols, finance required.

Finance helps business entrepreneurs and management in getting over there business problems.

Finance is important for increasing the market value of the shares.

TRADITIONAL APPROACH TO FINANCE

Traditional financial theory or approach to finance was positive in its nature as it was rather collection or

review of “ rules “ used by investors and managers in decision making process than consistent and

complete explanation of reason lending to and consequence following the financial decisions. The aim of

the traditional approach to finance was discovered encompass financial decisions that proved worthy in

practise over longer period of time and afterwards established characteristics of chosen assets are

companies that made those very same decisions. At that time it seemed to be a way to construct some

kind of rules of decisions-making in finance.

Approach to decision- making when it came to investment as explained by Graham and Dodd (1951)

became very popular at that time. Their rule are rather suggestion on how to efficient chose among

financial assets was to by the asset that were under – priced and sell those that were over-period, which is

obviously a no – brainer sense of what to do once u know which asset are mispriced. The real question is

how to discover the mispriced assets. Graham Dodd for example identified characteristics of the

company‟s stock that may cause stock to be mispriced.

Traditional approach was primarily based on actual behaviour of investor and managers. It attempted to

define characteristics of financial assets and companies that affect the behaviour and decision – making

process as well as the way they affect them it did not assume some sort of universal rational behaviour of

the people (was not normative in its nature), but rather extracted “best practice “(was positive in its

nature) with respect of decision- making process by observing actual behaviour of people in given

environment and time.

MODERN FINANCIAL THEORY

The beginnings of the modern financial theory in finance are marked with contributions made by

Markowitz (1952) , Kendal (1953) , Modigliani and miller (1958) and Sharp (1964). Foundations, on

which the modern financial theory was put on, were drawn from the neoclassical economic theory, which

assumes rational behaviour of the individuals. The effectively meant that universal financial theory could

be derived under certain assumptions.

Individuals undertake financial decisions that maximize their welfare.

The welfare is at its maximum, when the utility of the consumption is at its maximum.

The utility of the consumption is at its maximum, when the consumption is at its maximum.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 3

The consumption is at its maximum, when value of investor‟s financial assets is at its maximum.

The value of financial assets is maximized when with respect to each other.

1. Expected returns are maximized.

2. Expected returns occur in the nearest possible future.

3. Probably that expected returns materialize is maximize.

Individuals can:

1. Accurately measure risk and.

2. Being risk averse.

3. Can translate measured risk into additional required return from an investment.

4. Can trade financial assets at prices that equal additional expected return with additional required

returns.

FINANCIAL MANAGEMENT

Management of funds is a critical aspect of financial management. Management of funds acts as

thereforemost concern whether it is a business undertaking or in an educational institution. Financial

management is simply meant dealing with management of money matters.

MEANING OF FINANCIAL MANAGEMENT

Financial management means efficient use of economic resource namely capital funds. Financial

management is concerned with the managerial decision that results in the acquisitions and financing of

short term and long term credits foot the firms. It deals with the situation that required selection of

specific assets, or a combination of affects on the selection of specific problem of size and growth of an

enterprise. Herein the analysis deals with the expected inflows and outflows of funds and their effect on

managerial objectives. In short, financial management deals with procurement of fund and their effective

utilization in the business.

The analysis simply states two main aspects of financial management;

1. Procurement of funds and

2. Effective use of funds to achieve business objectives.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 4

SCOPE OF FINANCIAL MANAGEMENT

Sound financial management is essential in all types of organizations whether it be profit or non

profit. Financial management essential in a planned economy as well as in a capitalist set-up as it involves

efficient use of the resources. Financial management optimizes the output from the given input of funds.

In a country India where resources are scarce and the demand for funds are many; the need for proper

financial management is required. In case of newly started companies with high growth rate it is more

important to have sound financial management since finance alone guarantees their survival. Financial

management is very important in case non profit organizations, which do not pay adequate attentions to

financial management. However a sound system of financial management has to be cultivated among

bureaucrat‟s administrators, engineers, educationalist and public at large.

FINANCIAL SYSTEM

The world “system “, in that term “financial system”, implies a set of complex and closely or

interlined institutions, agents,practices,markets, transactions, claims, and liabilities in the economy. The

financial system is concerned about money; credit and finance the three terms are intimately related yet

are somewhat different from cash. Other Indian financial system consists of financial market,

financialinstruments and financial intermediation.

PURPOSE OF FINANCIAL SYSTEM

Financial systems help to inform your organization‟s planning and action plans. Financial systems

also help you to track and manage the resource required to successfully complete your work. These tips

provide basic practices you will need to build financial sustainability in your organization. Demonstrating

good stewardship of resources assists CSOs in efforts to be accountable to stakeholders and funders, and

helps build confidence that your organization isa good place for funders to invest.Other reasons why

developing financial system is important include:

Financial system and capacity help the organization to make sound decision based on cash flow and

available resources.

Monitoring funds, or comparing actual income and expenses virus budgeted amounts, help managers

ensure that the necessary funds are in place to complete an activity.

Most government require that registered charitable organizations which create accounts that track

income and expenses.

Funders require reports that demonstrate the grants which were used for intended purpose.

Establishing financial controls and clear accounting procedures help to ensure that fund are used for

intended purposes.

Transparency, clear planning and realistic projections contribute to the creditability of the

organization.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 5

FINANCIAL STATEMENTS

Financial statements are formal records of the financial activities of a business, person, person or

other entity. In British English, including United Kingdom company law, financial statements are often

referred to as accounts, although the term financial statements are also used, particularly by

accountants.Financial statements provide an overview of a business or person‟s financial condition both

short and long term. All the relevant financial information of a business enterprises presented in a

structured manner and in a form easy to understand is called the financial statements.

There are four basic financial statements;

1. Balance sheet: It also referred to as statement of financial position or condition, reports on a

company‟s assets liabilities, and Ownership equity at a given point in time.

2. Income statements: It also referred to as profit and loss statement, reports on a company‟s income and

expenses profit over a period of time. Profit and loss accounts provide information on the operation

of the enterprise. These include sale and the various expenses incurred during the processing state.

3. Statement of retained earnings: It explains the changes in a company‟s retained earnings over the

reporting period.

4. Statement of cash flows: It reports on a company‟s cash flow activities, particularly its operating,

investing and financial activities.

PURPOSE OF FINANCIAL STATEMENT

“The objectives of financial statements is to provide information about the financial position

performance and changes in financial and changes in financial position of an enterprise that is useful to a

wide range of users in making economic decision”. Financial statements should be most understandable,

relevant and comparable. Reported assets, liabilities and equity are directly related to an organisation‟s

financialposition. Reported income and expenses are directly to an organization‟s financial position.

Financial statements are intended to be under stable by readers who have “a reasonable knowledge of

business and economic activities and accounting who are willing to study the information diligently”.

Financial statements may be used by users for different purposes.Owners and Managers require financial

statements to make important business decision that effect its continued operations. Financial analysis is

then performed on these statements to provide management with a more detailed understanding of the

figures.

These statements are also used as part of management‟s annual report to the stockholders.

Employees also need these reports in making collective bargaining agreements with the managements,

in the case of labour unions or for individuals in discussing their compensation, promotion and

rankings.

Prospective investors make use of financial statements to access the viability of investing in a business.

Financial analyses are often used by investors and are prepared by professionals, thus providing them

with the basis for making investment decisions.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 6

Financial institutions use them to decide whether to grant a company with fresh working capital or

extend debt securities to finance expansion and other significant expenditures.

Government entities (tax authorities) need financial statements to ascertain the propriety and accuracy

of taxes and other duties declared and paid by a company.

Vendors who extend credit a business require financial statements to access the credit worthiness of

the business.

Media and the general public are also interested in financial statements for a variety of reason.

WORKING CAPITAL MANAGMENT

INTRODUCTION

Working capital is the blood and nerve centre of a business. Just as circulation of blood is

essential in the human body for maintaining life,working capital is very essential to maintain the smooth

running of a business .No business can run successfully without an adequate amount of working capital.

Working capital refers to that part of firm‟s capital which is required for financing short term or current

assets such as cash, marketable securities, debtors and inventories. In other words working capital is the

amount of funds necessary to cover the cost of the operating enterprise.

MEANING:

Working capital means the funds (i.e. capital) available and used for the day to day operation (i.e.

working) of an enterprise.

It refers to funds which are used during an accounting period to generate a current income of a type

which is consistent with major purpose of a firm existence.

DEFINITION:

According to Weston& Brigham-

”Working capital refers to a firm‟s investment in short term assets such as cash accounts receivables,

inventories etc”.

According to J.S.Mill-

“The sum of the current assets is the working capital of the business”.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 7

CONCEPT OF WORKING CAPITAL

1) Gross working capital

It refers to the firm‟s investment invarious components like currentassets namelycash, marketable

securities, raw materials, work in progress, receivables etc.current assets are the assets which can be

converted into cash with in an accounting year.

The gross working capital concept focuses attention on two aspects of current asset management:

Optimum investment in current assets

Financing of current assets.

2) Net working capital

It considers both current assets and current liability .It refers to the difference between current

assets and current liabilities .current liabilities are those claims of outsiders which are expected to mature

for payment within an accounting year like sundry creditors ,outstanding expenses , short term loans ,

bank over draft, dividends and payable etc.

Net working capital =Current Assets – Current Liabilities

Net working capital is a qualitative concept and it indicates the:

Liquidity position of the firm.

Suggests the extent to which working capital needs may be financed by permanent sources of funds.

OBJECTIVES OF WORKING CAPITAL

Every business needs some amount of working capital. It is need for following purposes:-

For the purchase of raw materials, components and spares.

To pay wages and salaries.

To incur day to day expenses and over head cost such as fuel, power, and office expenses etc.

To provide credit facilities to customers etc.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 8

FACTORS THAT DETERMINE WORKING CAPITAL

The following factors determine the amount of working capital;

Size of business:

A business size may be measured in terms of a scale of operations. A firm with larger scale of

operation will need more working capital than small firm.

Manufacturing cycle:

Longer the manufacturing process, the higher will be requirements of working capital and vice versa.

Production policy:

The production schedule has a great influence on the level of inventories. In case of labour intensive

industry, working capital requirement will be more. While in case of highly automated plant

requirement of long –term fund is more.

Terms of purchase and sales:

A firm, which allows liberal credits to its customers may enjoy higher sales but will need more

working capital as compared to a firm enforcing strict credit terms.

Business cycle:

Business expands during the period of prosperity and declines during the period of depression.

Consequently, more working capital is required during the period of prosperity and less during the

period of depression.

Growth and Expansion:

If business firm has ambitious plan for expansion, it requires more working capital to fulfil

requirements.

Fluctuations in the supply of raw materials:

Certain companies have to obtain and maintain large reserves of raw materials due to their irregular

sales and intermittent supply. Thus working capital requirements of such industries are lard.

Price level changes:

Generally, rising price levels will require a firm to maintain higher amount of working capital. The

same level of current assets will need increased investment when prices are increasing.

Profit margin:

A net profit margin contributes towards the working capital poor. In fact net profit is a source

working capital to the extent it has been earned in cash.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 9

Length of operating cycle:

Operating cycle of the firm also influence the working capital. Longer the Orating Cycle, the higher

will be the working capital requirement of the organization.

SOURCES OF WORKING CAPITAL The working capital requirements should be the met both from short-term as well as long-termsource of

funds.

Financing of working capital through short term source of funds has the benefitsof lower cost and

establishing close relations with banks.

Financing of working capital through long term source provides the benefits of reduce risk and

increase liquidity.

NEED FOR WORKING CAPITAL

The need for working capital gross or current assets cannot be over emphasized.

As already observed, the objective of financial decision making is to maximize the shareholders

wealth.

To achieve this, it is necessary to generate sufficient profits can be earned will naturally depend upon

the magnitude of the sales among other things but sales cannot convert into cash.

There is a need for working capital in the form of current assets to deal with the problem arising out

of lack of immediate realization of cash against goods sold.

Therefore sufficient working capital is necessary to sustain sales activity.

Technically this is refers to operating or cash cycle.

If the company has certain amount of cash, it will be required for purchasing the raw materials may

be available on credits basis.

Then the company has to spend some amount for labour and factory overhead to convert the raw

material in work progress, and ultimately finished goods.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 10

The amount required to be invested in this current assets is always higher than the funds available

from current liabilities.

This is the precise reason why the needs for working capital arise.

TYPES OF WORKING CAPITAL

Working capital can be divided into two categories:

a) Permanent working capital :

It refers to that minimum amount of investment in all current assets which is required at all times to

carryout minimum level of business activities

b) Temporary working capital:

The amount of such working capital keeps on fluctuating from time to time on the basis of business

activities.

Operating cycle

Operating cycle is the durations required to convert sales into cash after the conversion of resources into

inventories. So Operating cycle can be known as following:

Raw materials.

Work in progress.

Cash from Debtors collections.

Sales

Finished goods, credit sales & cash sales.

Operating cycle may be of two types:

a) Gross Operating Cycle

Gross operating Cycle is the total time period from the conversion of raw material into finished goods

and finished goods into sales and then sales into cash.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 11

b) Net Operating cycle

As we provide period to debtors for the payments, our creditors also provide period to us for payment

to them. So this reduces our requirements of working capital. This also affects the operating cycle.

Operating cycle length reduces with so many days as provided by the creditors to us. The difference

between gross operating cycle and period allowed by the creditors for payment is known as net

operating cycle.

ADVANTAGES OF WORKING CAPITAL

1) It helps the business concern in maintaining the goodwill.

2) It can arrange loans from banks and others on easy and favourable terms.

3) It enables a concern to face business crisis in emergencies such as depression.

4) It creates an environment of security,confidence, and the overall efficiency in a business.

5) It helps maintaining solvency of the business.

DISADVANTAGES OF WORKING CAPITAL

1) Rate of return on investment also fall with the shortage of working capital.

2) Excess working capital may result into overall inefficiency in organization.

3) Excess working capital means idle funds which earn no profits.

4) Inadequate working capital cannot pay its short term liabilities on time.

COMPONENTS OF WORKING CAPITAL

1) Current Assets:

Inventories:

Inventories represent raw materials and components, work-in-progress and finished goods.

Trade Debtors:

Trade Debtors comprise credit sales to customers.

Prepaid Expenses:

These are those expenses, which have been paid for goods and service whose

Benefits have yet to be received.

Loan and Advances:

They represent loans and advances given by the firms for a short period of time.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 12

Investment:

These Assets comprise short-term surplus funds invested in government securities, shares and short-

terms bonds.

Cash and Bank Balance:

These assets represent cash in hand and at bank, which are used f meeting operations requirements.

One thing you can see here is that this current assets is purely liquid non- productive.

2) Current Liabilities:

Sundry creditors :

These liabilities stem out of purchase of raw materials on credit terms usually for a period of one to

two months.

Bank overdrafts:

These include withdrawals in excess of credit balance standing in the firm‟s current accounts with

banks.

Short-terms Loans:

Short-term borrowings by the firm from banks and others form part of current liabilities as short-term

loans.

Provision:

These include provision for taxations, proposed dividends and contingencies.

THREAT OF EXCESSIVE WORKING CAPITAL

Excessive WC means idle funds which earn no profit for the business and hence, business cannot

earn a proper rate of return on its investments.

When there is redundant WC, it may lead to unnecessary purchasing and accumulation of inventories

causing more chance of theft, waste and losses.

Excessive WC implies excessive debtors and defective credit policy which may cause higher

incidences of bad-debts.

It may result in overall inefficiency in org.

When there is excessive WC, relationships with banks and other financial institutions may not be

maintained due to low rate of returns on investments, the value of shares may also fall.

Availability of excess working capital may lead to carelessness about cost, and therefore, to

inefficiency of operations.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 13

IMPORTANCE OF ADEQUATE WORKING CAPITAL

The main advantage of maintain adequate amount of working capital is as follows:

Solvency of business :

Adequate working capital helps in maintaining solvency of the business by providing uninterrupted

flow of production.

Goodwill :

Sufficient working unable a business concern to make prompt payments and hence helps in creating

and maintaining goodwill.

Easy loans:

A concern having adequate working capital, high solvency and good credit standing can arrange loans

from banks and other on easy and favourable terms.

Cash discount :

Adequate working capital also unable a concern to avail cash discounts on the purchase and hence it

reduces cost.

Regular supply of raw materials:

Sufficient working capital ensures regular supply of raw materials and continuous production.

Regular payment of salaries, wages and other day commitment:

A company which has ample working capital can make regular capital salaries, wages and other day

to day commitments which raise the morale of its employees, increase their efficiency, reduces

wastage and cost and enhances production and profile.

Exploitation of favourablemarket condition :

Only concerns with adequate working capital can exploit favourable market conditions such as

purchasing its requirement in bulk when the prices are lower and by holding its inventories for higher

prices.

Ability of face crisis :

Adequate working capital enables a concern to face business crisis in emergencies such as depression

because during such periods, generally, there is must presence on working capital.

Quick and regular return on investment:

Every investor wants a quick and regular return on his investments. Sufficient of working capital

enables a concern to pay quick dividends to its investors as there may not be much pressure to plough

back profit. This gains the confidence of its investors and creates favourable markets to raise additional

funds in future.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 14

High morale :

Adequacy of working capital creates an environment of securities, confidence, and high morale and

creates overall efficiency in a business.

APPROACHES TO WORKING CAPITAL

There are 3 approaches

Matching or hedging approach.

Conservative approach.

Aggressive approach

Matching or hedging approach

The firm can adopt a financial plan which matches the expected life of assets with the expected life of

the source of funds raised to finance assets. When the firms follow the matching approach (known as

hedging approach), long-term financing will be used to finance the fixed assets and permanent current

assets and short-term financing to finance temporary or variable current assets.

When the firm uses long term sources to finance fixed assets and permanent current assets, short term

financing to finance temporary assets

.

Conservative approach:

Under this approach a firm finances its permanent assets and also a part of temporary current assets

with long term financing. It relies heavily on long term financing and is less risky so far as solvency is

concerned, however, the funds may be invested in such instruments which fetch small returns to build

up liquidity. This adversely affects profitability.

The financing policy of the firm is said to be conservative when it depends more on long term funds

for financing needs. Under conservative plan, the firm finances its permanent assets and also a part of

temporary current assets with long term financing.

Aggressive approach

A firm may be aggressive in financing its assets. An aggressive policy is said to be followed by the

firm when its users more short term financing than warranted by the matching plan. Under an

aggressive policy, the firm finances a part of its permanent current assets with short term financing.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 15

The firm uses more short term financing than what is justified, in this approach. The firm finance a

part of its permanent current assets with short term financing. This is more risky but may have to the

return on assets.

SOURCES OF WORKING CAPITAL

Sources of working capital can be broadly divided into 2 types

1. Internal sources

2. External sources

Internal sources

1. Provisions.

2. Retained earnings.

3. Depression fund.

External sources

1. Bank credit.

2. Customer advances.

3. Short term public deposits.

4. Instalment credit.

5. Factoring.

6. Commercial papers.

7. Indigenous banker.

8. Trade credit.

9. Outstanding expense,

10. Depression.

11. Share capital.

WORKING CAPITAL MANAGEMENT

NEW HORIZON COLLEGE Page 16

CHAPTER-2

INDUSTRY AND COMPANY PROFILE

BEML Limited (formerly Bharat Earth Movers Limited) was established in May 1964 as a public

sector undertaking for manufacture of Rail coaches & spare parts and Mining Equipment at its Bangalore

complex. The company has partially disinvested and presently Government of India owns 54 percent of

total equity and rest 46 percent is held by public, financial Institutions, Foreign Institutional Investors,

Banks and Employees.

BEML Limited , a „Miniratna-Category-1‟, plays a pivotal role and serves India‟s core sectors like

defence , Rail, power , Mining and Infrastructure. The company started with a modest turnover of 5Cr

during 1965 and today, thanks to the diverse business portfolio, the company has been able to a turnover

of more than 3,500 Cr. Its three major business verticals viz., Mining &construction, Defence Rail and

Metro are serviced by its nine manufacturing units located in Bangalore, kola gold Fields (KGF), Mysore,

peaked and subsidiary-Vigny an Industries Ltd, in chikmangalur District. BEML‟s are sold and serviced

through its large Marketing Network spread all over the country. BEML‟s products are exported to more

than 56 countries. AS part of company„s globalization strategy, the company has expanded its global

reach by opening local company at Indonesia and Brazil recently in addition to Malaysia and china

offices.

The company operates under these major Business vertical-viz. Mining and construction, Defence and

Rail and Metro. Each of the above business is headed by a Director who acts as CEO of the business and

reports to the chairman & Managing Director of the company.

In addition to the above, Technology Division of the company provides end-to-end technology solutions

in Auto,Aero,Defence,Rail, and Metro areas. Trading division deals in non-company products. BEML

manufactures and supplies Defence Ground Support Equipment such as Tetra based high Mobility Trucks

, Recovery Vehicles, Bridge system , Vehicle for missile projects, Tank Transportation Trailers ,

![INDEX [shodh.inflibnet.ac.in:8080]](https://static.documents.pub/doc/80x56/617729fad5903d63bd1810b7/index-shodh-.jpg)