BACKGROUND Incorporated in 1973, Alkem Labs is leading India based pharmaceutical company engaged in the development, manufacture and sale of pharmaceutical and neutraceutical products. Alkem Labs produces branded generics, generic drugs, active pharmaceutical ingredients and neutraceuticals, which they market in India and 55 countries internationally, primarily the United States. Company's pharmaceutical business is organized into domestic and international operations. Alkem Labs has a portfolio of over 736 brands in India. Company's most significant therapeutic areas in domestic market are anti-infectives, gastro-intestinal, pain and analgesics, and vitamins, minerals and nutrients. Alkem Labs have a total of 16 manufacturing facilities: 14 manufacturing facilities at five locations in India and two in the United States. Company has four research and development facilities, two in India and two in the United States. As of June 30, 2015, company employed 483 scientists in research and development functions. Highlights: Alkem Labs is 5th largest pharmaceutical company in India in terms of domestic sales. Alkem Labs products are also sold in 56 countries. In the United States, company has filed 66 abbreviated new drug applications. Company sells a range of high-quality, cost effective generic drugs to major drug chains, pharmaceutical retailers, wholesalers, food and grocery stores, distributors and managed care companies in the United States. Particulars For the year/period ended (in Rs. Millions) 31-Mar-12 31-Mar-13 31-Mar-14 31-Mar-15 Total Income 20,640.10 24,690.10 28,395.80 33,595.20 Profit After Tax (PAT) 4,318.10 4,667.80 4,402.00 4,370.90 RECOMMENDATION Considering company's position, popular brands in the pharma sector and the given track records with over 22% CAGR in revenue growth for last five fiscals and over 36% growth in first half of current fiscal, reasonable pricing, it's a worthy bet for short to long term. 12 th Dec 2015 Alkem Laboratories Rating : BUY ATS Wealth Managers Pvt. Ltd.

Transcript

BACKGROUND

Incorporated in 1973, Alkem Labs is leading India based pharmaceutical company engaged in the development, manufacture and sale of pharmaceutical and

neutraceutical products.

Alkem Labs produces branded generics, generic drugs, active pharmaceutical ingredients and neutraceuticals, which they market in India and 55 countries

internationally, primarily the United States. Company's pharmaceutical business is organized into domestic and international operations. Alkem Labs has a portfolio

of over 736 brands in India. Company's most significant therapeutic areas in domestic market are anti-infectives, gastro-intestinal, pain and analgesics, and

vitamins, minerals and nutrients.

Alkem Labs have a total of 16 manufacturing facilities: 14 manufacturing facilities at five locations in India and two in the United States. Company has four research

and development facilities, two in India and two in the United States. As of June 30, 2015, company employed 483 scientists in research and development

functions.

Highlights:

Alkem Labs is 5th largest pharmaceutical company in India in terms of domestic sales.

Alkem Labs products are also sold in 56 countries. In the United States, company has filed 66 abbreviated new drug applications.

Company sells a range of high-quality, cost effective generic drugs to major drug chains, pharmaceutical retailers, wholesalers, food and grocery stores,

distributors and managed care companies in the United States.

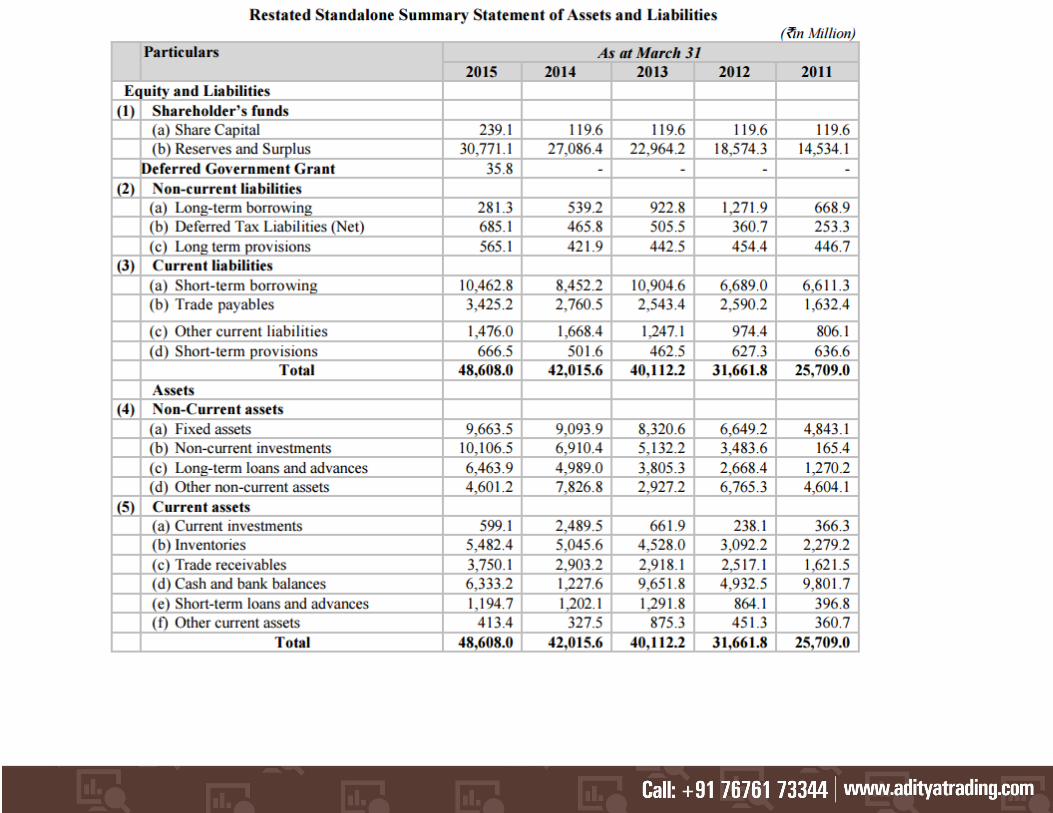

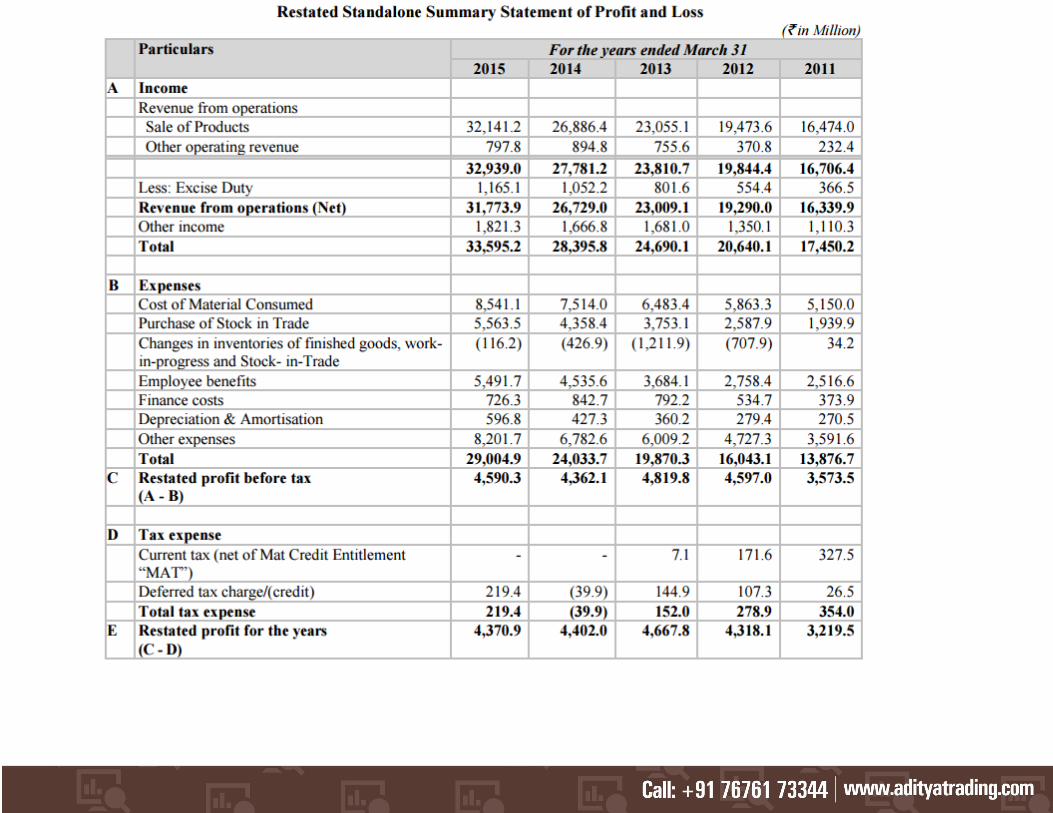

Particulars For the year/period ended (in Rs. Millions)

31-Mar-12 31-Mar-13 31-Mar-14 31-Mar-15

Total Income 20,640.10 24,690.10 28,395.80 33,595.20

Profit After Tax (PAT) 4,318.10 4,667.80 4,402.00 4,370.90

RECOMMENDATION

Considering company's position, popular brands in the pharma sector and the given track records with over 22% CAGR in revenue growth for last five fiscals and

over 36% growth in first half of current fiscal, reasonable pricing, it's a worthy bet for short to long term.

Alkem Labs has 23 Promoters who jointly hold 64,302,440 Equity Shares of the Company which, in aggregate, constitutes 53.8% of the issued and paid-up Equity

Share capital of our Company.

Issue Subscription Detail / Current Bidding Status

Day 1 - Dec 8, 2015 17:00 IST 0.41 0.09 0.44 0.14 0.35

BUSINESS PROFILE

Alkem Laboratories Ltd (ALL) is a leading Indian pharmaceutical company with global operations, engaged in the development, manufacture and sale of

pharmaceutical and neutraceutical products. For fiscal year 2015, ALL was the fifth largest pharmaceutical company in India in terms of domestic sales. Further, it

had the largest number of brands (five) in the top 50 brands of the Indian pharmaceutical industry for fiscal year 2015 in terms of domestic sales (along with another

leading pharmaceutical company) and the second largest number of brands (five) in the top 50 brands of the Indian pharmaceutical industry for the six months ended

September 30, 2015 in terms of domestic sales (along with another leading pharmaceutical company) (Source: IMS SSA MAT September 2015).

ALL produces branded generics, generic drugs, active pharmaceutical ingredients ("APIs") and Nutraceuticals, which are market in India and 55 countries

internationally, primarily the United States. For fiscal year 2015, ALL's domestic and international operations accounted for 74.7% and 25.3%, respectively, of its net

revenues from operations. For six months ended September 30, 2015, its domestic and international operations accounted for 74.9% and 25.1%, respectively, of its

net revenues from operations. Their consolidated net revenues from operations grew at a compounded annual growth rates ("CAGR") of 22.3% in the period from

fiscal year 2011 to fiscal year 2015.

To unlock the value for its stake holders, the company is coming out with a maiden IPO in the form of offer for sale. It is offering 12853442 equity share of Rs. 2 each

via book building route in a price band of Rs. 1020-1050. Minimum application is to be made for 14 shares and in multiples thereon, thereafter. Issue opens for

subscription on 08.12.15 and will close on 10.12.15. Anchor bids will open on 07.12.15. It has issued bonus shares in the ratio of 13 for 1 in March 1995, 1 for 1 in

October 2006 and 1 for 1 in March 2015. Being secondary offer, equity post issue will remain at the same level of Rs. 23.91 crore as no fresh funds coming to the

company. The company is offering a special discount of Rs. 100 per share to eligible employees for this IPO subscription. This offer constitutes around 10.6% equity

dilution of the post offer paid up equity. Average cost of acquisition by the promoters ranges between Rs. 0.03 to Rs. 3.15 per share except for around 1.51 lakh

shares of HUF holder at Rs. 30.10. Post allotment, shares will be listed on BSE/NSE. BRLMs to this offer are Nomura Financial Advisory and Securities India Pvt Ltd,

Axis Capital Ltd, J. P. Morgan India Pvt Ltd and Edelweiss Financial Services Ltd. Link Intime India Pvt Ltd is the registrar to the issue.

On performance front, it has posted an average EPS of Rs. 36.80 on a consolidated basis for last three fiscals. For the first half of the current fiscal it has posted net

profit of Rs. 438.55 crore on a turnover of Rs. 2659 crore against net profit of Rs. 462.56 crore on a turnover of Rs. 3969.74 crore for the entire previous fiscal. Thus it

has marked near 95% of the previous full year's net in first six months itself. As on 30.09.15 its Rs. 23.91 crore equity capital has a support of free reserves of Rs.

3375 crore plus. If we annualize the current working and attribute it on the equity, then asking price is at a P/E of 28% and at a P/BV of 4.3 based on its NAV of Rs.

241.80 (as on 30.09.15). It has filed 69 ANDs in US out of which 21 are already approved. Having cash surplus status, the company will continue its acquisition

programme at opportune time to keep expanding and growing on domestic as well as global front.

As per IMS, SSA and MAT, In terms of domestic sales figures last year, company has attained fifth position with a total domestic market share of 3.60%.

Company enjoys the largest number of brands in top fifty most popular and recognized brands of Indian Pharmaceutical Industry for the year ended 2015.

IMS awarded Company with the third-fastest growing company in terms of domestic sales for the past 12 years.

In a short span of just 5 years company has doubled net revenues from international market from 12.6% in 2011 to 25% in 2015.

Company has got 16 manufacturing facilities out of which 14 are located in India and 2 are in United States. Out of these 16 manufacturing units, 5 are

approved by USFDA, TGA and UK-MHRA.

Company’s top management personnel are highly experience and are associated with pharmaceutical sector for over 40 years

RATIONALE & FINANCIALS

Market leadership in various therapeutic areas and ability to build market leading brands in the domestic market

They are one of India’s leading pharmaceutical companies and were ranked fifth in the Indian pharmaceutical market in terms of domestic sales for fiscal year 2015.

For fiscal year 2015, they were the leader in the largest therapeutic area (anti-infective) with a 11.2% market share and were ranked third in terms of market share for

both the gastro-intestinal (with a market share of 5.6%) and pain/analgesics therapeutic areas (with a market share of 5.0%), in each case, in India. Revenues from

the anti-infectives, gastro-intestinal and pain/analgesics therapeutic areas in India grew at a CAGR of 10.1%, 17.5% and 12.0% in the period from fiscal year 2011 to

fiscal year 2015. In the same period, these therapeutic areas in India as a whole grew at a lower CAGR of 6.8%, 12.8% and 10.9%, respectively. They are also

among the top ten companies in the vitamins, minerals, nutrients and gynaecology therapeutic areas in terms of Indian market share for March 2015. According to

IMS Health, they were the third-fastest growing company in terms of sales in this period among the ten largest pharmaceutical companies in the Indian domestic

formulations market.

Extensive sales, marketing and distribution network in India

They have strong sales, marketing and distribution capabilities in India. Marketing and distribution network in India comprises a field force of 5,856 medical

representatives. As a result of strong sales, marketing and distribution capabilities, products were prescribed by an estimated 210,885 prescribers (constituting 70.7%

of total prescribers, as defined by IMS) across various specialties in fiscal year 2015. Their medical representatives cover all states in India, including rural areas. As

of June 30, 2015, domestic distribution network includes 39 sales depots, 55 clearing and forwarding (“C&F”) agents, 15 consignees and eight central warehouses

covering 6,576 stockists. They also market products to various hospitals, government institutions and medical institutions.

Strong research and development capabilities which enhance product portfolio

As of June 30, 2015, they employed 483 scientists working on various drug products and substances in India and the United States. Research and development

department carries out process development, formulation development and analytical research for domestic and international markets. In addition, they also have a

regulatory affairs team, which is responsible for various filings and approvals related to products in India and internationally. They also have a dedicated in-house

team of intellectual property experts, who work towards understanding and filing with respect to intellectual property rights of products and processes in various

geographical markets.

Consolidate and further grow domestic sales

They intend to continue to consolidate market leadership positions in therapeutic areas such as anti-infective, pain and gastroenterology and aim for growth in these

areas through the following initiatives:

Focus on brand building and driving the growth of focused set of brands with high growth potential;

identification of gaps in product portfolio for the introduction of new products;

growth in prescriptions and prescriber base in key specialty areas;

invest in the training and effectiveness of field force; and

Increasing market shares in those geographies where their market shares are lower than the national average.

Fast growing and established international operations

Having established in the Indian pharmaceuticals market, they have expanded internationally through both organic growth and certain strategic acquisitions. The

United States is the key focus market for their international operations. They market and sell products in the United States under the brand “Ascend” to major

pharmacy chains’ stores, wholesalers, managed care companies, distributors, food and grocery stores and pharmaceutical retailers. Ascend currently sells 17

products in the market, out of which 12 are Alkem’s products and five are in-licensed from third parties. For fiscal year 2015, ThePharmaNetwork LLC’s consolidated

net revenues (through Ascend) were `6,459.7 million. Further, they own two manufacturing and two R&D facilities in the United States is believed to provide

infrastructure required to support the growth in operations in the United States.

Use of strategic international and domestic acquisitions and partnership arrangements to enhance growth

In the past, they have used a combination of organic initiatives and acquisitions to drive growth, and intend to continue to use this strategy in the future. They have

undertaken acquisitions as part of entry strategy into new geographies or new market segments. For instance, in July 2010, they acquired The Pharmanetwork LLC in

the United States, the holding company of Ascend Laboratories LLC. ThePharmanetwork LLC provided with the commercial platform through which they were able to

market and sell Alkem’s portfolio of products in the United States.

They have also recently acquired a manufacturing facility with capabilities of manufacturing semi-solids, liquid and nasals in the United States. They intend to

continue to actively seek and evaluate potential acquisitions of brands, companies or assets that will enhance capabilities. As regards to their international business,

company plan to continue to acquire targets to enhance capabilities, enter new market segments and expand their presence in focused markets.

PHARMACEUTICALS INDUSTRY

The pharmaceuticals industry is one of the largest industries in the world and comprises companies that are involved in the development, production and marketing of

pharmaceutical products.

Its continued growth has been driven by factors such as an increase in elderly populations and a growing middle class in emerging economies that have boosted the

demand for pharmaceuticals. The increased focus by governments to improve healthcare infrastructure that provide people with greater access to treatment and

medication has also contributed to the growth in the global pharmaceuticals industry.

According to IMS Health, the size of the global pharmaceuticals market is expected to grow at a CAGR of approximately 4.1% between 2014 and 2019, to reach sales of

approximately US$1,294.6 billion by 2019, compared with US$1,057.1 billion in 2014. (Source: Market Prognosis Global 2015-2019 dated May 2015, published by IMS

Health)

The Indian Pharmaceuticals Industry

According to CRISIL Research, the Indian pharmaceuticals market is estimated to be worth US$36.8 billion in revenues for the fiscal year 2015. The Indian

pharmaceuticals market can be broadly classified into the domestic and export segments in terms of the target geographical sales markets.

RISKS RELATING TO BUSINESS

1. There are outstanding litigations involving Company, Promoters, Directors and Subsidiaries.

Company, Promoters, Directors and Subsidiaries are involved in certain legal proceedings which are pending at different levels of adjudication before various

courts, tribunals and appellate authorities. Decisions in such proceedings adverse to such person/ entity’s interests may have a significant adverse effect on

the business, results of operations, cash flows and financial condition.

A summary of the pending civil and criminal proceedings involving Company, Promoters, Directors and Subsidiaries is provided below:

2. Their top 20 brands account for a majority of domestic sales. Additionally, certain therapeutic areas and certain states generate a significant portion of total

domestic revenue. Their business, prospects, results of operations and financial condition may be adversely affected if any of the top 20 brands or other

products in key therapeutic or geographic areas do not perform as expected or if competing products become available and gain wider market acceptance.

3. Pharma sector is subject to extensive regulation and if company fails to company with any regulations prescribed by Government or regulatory body, than

there may be severe damage to company operations and goodwill.

4. Company’s 25% revenue comes from international market primarily primary United States and we know US is severely strict in quality control and has

banned various Indian Pharmaceutical Company from entering in US market (Ranbaxy now Sun Pharma). Thus dependency on one market may harm

company revenues and profits.

5. Results of operations are subject to risks arising from exchange rate fluctuations.

Although Company’s reporting currency is Indian Rupees, they transact a significant portion of business in several other currencies. Revenues attributable to

sales outside of India were `9,569.6 million and represented 25.3% of consolidated revenue from operations (net) for fiscal year 2015. Substantially all of non-

Indian revenue is denominated in foreign currencies, primarily United States Dollars. Additionally, they also procure a portion of raw material requirements

outside India and, as a result, incur such costs in currencies other than Indian Rupees.

6. Contingent liabilities and financial condition could be adversely affected if any of these contingent liabilities materializes.

As at March 31, 2015, the contingent liabilities disclosed in Restated Consolidated Financial Information represented an aggregate principal amount of

`2,630.6 million as further detailed below:

7. Some of Group Companies have incurred losses in the last three financial years, details of which are as follows:

RECOMMENDATION & INVESTMENT STRATEGY

As far as the ratios are concerned, P/E ratio for Alkem at a higher price band of Rs 1050 comes at around 28.5 based on the EPS of last year which was 36.5.

Compared it to other competitors like Torrent pharma and Stride Shasun, which trade at P/E of higher that 50, the issue seems to be priced aggressively. A run up

can be expected one the issue hits the market.

Considering company's position, popular brands in the pharma sector and the given track records with over 22% CAGR in revenue growth for last five fiscals and

over 36% growth in first half of current fiscal, reasonable pricing, it's a worthy bet for short to long term.

Research Analyst: Vinay Gowda Equity Research Analyst ATS Wealth Managers Pvt Ltd Email: [email protected] Phone: +91-9900778510

Disclaimer: This report is only for the information of our customers. Recommendations, opinions or suggestions are given with the understanding that readers acting on this

information assume all risks involved. The information provided herein is not to be constructed as an offer to buy or sell securities of any kind. ATS and/or its group companies

do not as assume any responsibility or liability resulting from the use of such information.