48

Annual Report 2015 Presentation 11 Feb 2016 1 Annual Report 2015 Copenhagen, 11 February 2016

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Annual Report 2015 Presentation

11 Feb 2016 1 Annual Report 2015

Copenhagen, 11 February 2016

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

FLSmidth – One source of productivity

One source of productivity

11 Feb 2016 Annual Report 2015 2

Market leading key products

Boosting productivity and maximising return on assets

Minimising impact on society and environment

Providing uptime and performance guarantees

Reducing total cost of ownership

Customised equipment, complete plants and full Operation & Maintenance

Parts, services and maintenance

Working closely with

customers to understand performance

data

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Key highlights - Annual Report 2015

11 Feb 2016 Annual Report 2015 3

2015

• Order intake up 7% despite challenging market conditions

• Revenue and EBITA-margin in line with guidance

• Products and services provide a stable and profitable business

• Positive free cash flow reduced net debt by DKK 0.9bn

2016

• EBITA-margin guidance of 7-9% reflects low visibility and investments in people

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Safety ambition: No injuries

2015 LTIFR target achieved: < 2.6

New 2016 LTIFR target: < 1.6

Strong safety performance in 2015 Lost Time Injury Frequency Rate (LTIFR) 1.8

4

Safety

11 Feb 2016 Annual Report 2015

LTIFR (annually) Number of lost time injuries per million working hours

4.2 4.7

3.9

2.7

1.8

0.0

1.0

2.0

3.0

4.0

5.0

2011 2012 2013 2014 2015

33% improvement vs. 2014

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer Large maintenance contract for copper plant in Chile

New service agreement concept to support Heidelberg cement plant in Norway

Supply of key process technology for two gold mines in West Africa and Canada

Ongoing business right-sizing and efficiency improvement activities in Minerals

Continued investments in leadership and technical competencies

523 managers on Leadership Transition Training in 2015

190 senior managers/specialists completed ‘Flying the Flag’ programme at Henley Business School in 2015

R&D partnership with BASF on arsenic-challenged copper deposits

Operational highlights in Q4 2015

Operation highlights

11 Feb 2016 Annual Report 2015 5

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Sustainable technology highlights in Q4 2015

Technology highlights

11 Feb 2016 Annual Report 2015 6

TRIBOMAX™ wear solution: Unique resistance against tramp metal and oversize feed – as well as heat and corrosion

First order booked January 8, 2016 for Lehigh Hanson Materials Limited

Advantages:

Increases strength of steel construction surfaces ~15 times

~5 times stronger than traditional welded coatings

Built-in surface roughness due to the welding technology (Plasma Transfer ARC) developed by leading engineers from FLSmidth R&D together with Aalborg University

Can be applied on all types of steel and aluminum – with low maintenance requirements

~10% reduction in capital investment

Strategic rationale:

Improving productivity for our customers and strengthening our position in wear parts

Supercoating of metallic surfaces multiplies resistance

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Revenue from total service activities +7% in 2015

Total service activities

11 Feb 2016 Annual Report 2015 7

Customer Services

Minerals Cement

Cement Product

Companies

Projects / Customised equipment Products

Products aftermarket

Cement Operation & Maintenance

Customised equipment aftermarket

Total service activities 55% of revenue 52% of order intake

Revenue growth +7% vs. 2014 Order intake growth unchanged vs. 2014

2015

Product Companies

Total capital business 45% of revenue 48% of order intake

Revenue growth -15% vs. 2014 Order intake growth +15% vs. 2014

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

High market volatility and low visibility

Minerals Division High exposure to copper and gold => more favourable long term outlook Flattish order intake until end 2017

Cement Division Slower recovery based on shift in demand from oil-exporting to oil-importing countries Increasing utilisation rates to underpin growth over time Customer focus on both new capacity and productivity

Product Companies and Customer Services Overall stable and profitable business Mainly OPEX-related business

Customers focus on productivity and environment

Market developments for FLSmidth

Market update

11 Feb 2016 Annual Report 2015 8

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

26%

21%

19%

18%

10% 6%

Revenue and order intake in 2015

Annual Report 2015

11 Feb 2016 Annual Report 2015 9

Revenue - by geography

North America

Africa

Europe

Australia

South America

Asia

32%

17% 7%

8%

5% 2%

29%

Order intake - by commodity

Cement

Coal

Iron ore

Adjacent

Copper Gold

Fertilizers

Order intake - by division

Product Companies

Minerals Cement

2015 2014 2015 2014 2015 2014 2015 2014

Customer Services

6,847

5,192

3,142

2,943

6,710

5,742

4,112

2,803

DKKm

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Financial performance in Q4 2015

Annual Report 2015

11 Feb 2016 10 Annual Report 2015

Reported numbers reflect challenging business environment and risk provisions

Organic growth in revenue -11%

One-off costs DKK 89m

Business right-sizing/efficiency (incl. discontinuation of product line)

Costs related to O&M contract in oil-exporting country

Order backlog declined DKK 1.8bn in Q4, reflecting the difference between order intake and revenue in the quarter.

Discontinuation, scope changes and run-off of O&M contracts reduced the backlog by DKK 2.5bn in 2015

Continuing activities (DKKm)

Q4 2015

Q4 2014

Change

Order intake 3,691 3,734 -1%

Revenue 5,297 5,627 -6%

Gross margin % 23.7% 22.5%

EBITA 384 419 -8%

EBITA % 7.2% 7.4%

EBITA % adjusted 8.9% 10.1%

Order backlog 14,858 17,726 -16%

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Announced orders Unannounced orders

Stable level of unannounced orders No large orders in Q4’15

Annual Report 2015

11 Feb 2016 Annual Report 2015 11

Order intake (quarterly)

Order intake decreased 1% in Q4 2015

Unannounced orders increased in Q4’15 vs. Q4’14

DKKm

42%

32%

16%

10%

Order intake Q4 2015

– classified by segment

Customer Services

Product Companies

Cement

Minerals

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Annual Report 2015

11 Feb 2016 Annual Report 2015 12

1,938

1,451

1,407

1,098

1,920

1,473

1,126 985

Stable revenue in Customer Services and Product Companies

Revenue (quarterly)

DKKm

Revenue Q4 2015 vs. Q4 2014 - by division

Product Companies

Minerals Cement

Q4’15 Q4’14 Q4’15 Q4’14 Q4’15 Q4’14 Q4’15 Q4’14

Customer Services

Revenue declined 4% as a result of lower order intake the last two years

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

DKKm

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

22.5%

26.1%

16.2%

20.1%

29.5% 27.6%

15.9%

12.6%

Gross margin improvement in services and products more than offset decline in project divisions

Annual Report 2015

11 Feb 2016 Annual Report 2015 13

Gross margin

22.5% 23.7%

0%

10%

20%

30%

40%

0

200

400

600

800

1,000

1,200

1,400

1,600

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Gross profit (quarterly)

DKKm

Gross margin Q4 2015 vs. Q4 2014 - by division

Customer Services

Product Companies

Minerals Cement

Q4’15 Q4’14 Q4’15 Q4’14 Q4’15 Q4’14 Q4’15 Q4’14

Gross margin negatively impacted by DKK -64m one-off costs in Q4’15 (Q4’14: DKK -121m) (related to efficiency programme/business right-sizing and O&M contracts in oil-exporting countries)

Adjusted gross margin 24.9% in Q4 2015 (Q4 2014: 24.6%)

DKKm

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

SG&A impacted by currency developments

Annual Report 2015

11 Feb 2016 Annual Report 2015 14

SG&A ratio*

14.3% 13.7% 15.0%

0%

3%

6%

9%

12%

15%

18%

0

200

400

600

800

1,000

1,200

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

SG&A costs (quarterly)

DKKm

*) SG&A ratio: SG&A costs (Sales, General and Administration) as percentage of revenue

In local currencies, SG&A costs decreased 3% in Q4

Initiatives taken to further reduce costs, optimise global footprint, and to consolidate sites.

One-off costs DKK 25m in Q4 (Q4’14: DKK 26m)

Front-end loaded costs related to proposals and order intake

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

0%

2%

4%

6%

8%

10%

12%

0

100

200

300

400

500

600

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Adjusted 10.1%

Adjusted EBITA margin Q4’15 8.9% (reported 7.2% incl. one-off costs DKK -89m)

Adjusted EBITA margin Q4’14 10.1% (reported 7.4% incl. one-off costs DKK -147m)

419 384

58 14 26

81

0

100

200

300

400

500

600

EBITA Q4'14 Change inone-off costs

Increase ingross margin

Increase inSG&A

Impact ofdecrease in

revenue

EBITA Q4'15

EBITA impacted by lower revenue in the quarter

Annual Report 2015

11 Feb 2016 Annual Report 2015 15

EBITA margin

EBITA (quarterly)

-8% vs. Q4 2014 DKKm DKKm

EBITA bridge Q4’15 vs. Q4’14

Adjusted 8.9%

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Financial performance in 2015

Annual Report 2015

11 Feb 2016 Annual Report 2015 16

Continuing activities (DKKm) 2015 2014 Change

Order intake 18,490 17,267 +7%

Revenue 19,682 20,499 -4%

Gross margin 25.1% 25.0%

EBITA 1,582 1,823 -13%

EBITA margin 8.0% 8.9%

EBITA margin adjusted 9.7% 9.7%

Financial costs net (256) (137)

Tax (282) (398)

Profit, discontinued activities (178) (68)

Profit for the year, Group 425 813 -48%

ROCE 10% 12%

Employees 12,969 14,765 -12%

Revenue -12% in local currencies due to low order intake in past couple of years

Adjusted EBITA margin 9.7% (2014: 9.7%) excl. one-off costs of DKK -321m

Tax rate 32% (2014: 31%)

Headcount impacted by sale of Cembrit (1,042 employees) and business right-sizing

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

EBITA declined from 2014 to 2015 due to higher one-off costs and lower revenue, partly offset by an improvement in the underlying gross margin

Adjusted EBITA margin 2015: 9.7% (reported 8.0% incl. non-recurring costs DKK -321m)

Adjusted EBITA margin 2014: 9.7% (reported 8.9% incl. non-recurring costs DKK -175m)

EBITA margin 8.0% in 2015

Annual Report 2015

11 Feb 2016 Annual Report 2015 17

DKKm

EBITA bridge 2015 vs. 2014

1,823

1,582

172 146

60

207

1,400

1,500

1,600

1,700

1,800

1,900

EBITA 2014 Change inone-off costs

Increase ingross margin

Increase inSG&A

Impact ofdecrease in

revenue

EBITA 2015

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Annual Report 2015

11 Feb 2016 Annual Report 2015 18

NWC impacted by reduction in prepayments

NWC increased by DKK 0.3bn to DKK 2,583m in 2015

A combined reduction in inventories and trade receivables from 2014 to 2015 of DKK 0.3bn was more than offset by a reduction in net prepayments of DKK 0.6bn

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15

Trade Payables

0

500

1,000

1,500

2,000

2,500

3,000

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15

Net prepayments

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15

Inventories

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15

Net work-in-progress

0

1,000

2,000

3,000

4,000

5,000

6,000

Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15

Trade Receivables

All charts include Cembrit before Q4’14 and bulk material handling before Q3’15

Not overdue Overdue

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Annual Report 2015

11 Feb 2016 Annual Report 2015 19

Cash flow statement in 2015

Group (DKKm) 2015 2014

EBITDA continuing adjusted 1,878 2,118

EBITDA discontinued (289) (60)

Change in provisions 68 (431)

Change in NWC*) (733) 168

Financial payments (50) (86)

Taxes paid (338) (411)

CFFO (Group) 538 1,298

CFFO (continuing activities) 991 1,178

CFFI excl. acquisitions & disposals (123) (414)

Acquisitions & disposals 873 (184)

CFFI 750 (598)

Free cash flow 1,288 700

CFFO declined in 2015 mainly due to lower adjusted EBITDA and negative impact from NWC

EBITDA from discontinued activities impacted cash flow by DKK -289m in 2015 (2014: DKK -60m)

Positive free cash flow attributable to divestment of Cembrit and a modest level of ‘ordinary’ investments

*) Cash flow effect from NWC includes discontinued activities and is

adjusted for currency effects

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Annual Report 2015

11 Feb 2016 Annual Report 2015 20

1148

1720

-157

1298

538

-500

0

500

1000

1500

2000

2011 2012 2013 2014 2015

Free cash flow highest in last five years - Supported by divestment of Cembrit

CFFO (annual)

DKKm

Free cash flow (annual) DKKm

-3000

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

2011 2012 2013 2014 2015

Acquisitions & disposals

FCF excl. acquisitions and disposals

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

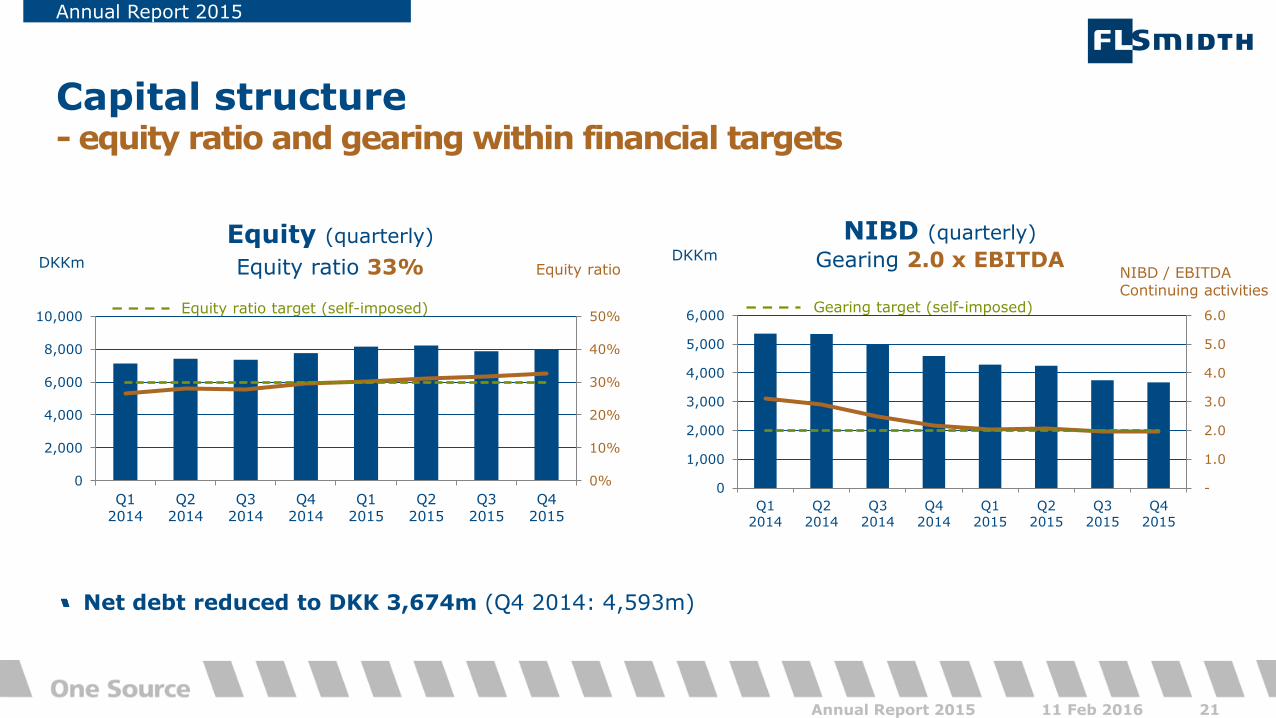

Capital structure - equity ratio and gearing within financial targets

Annual Report 2015

11 Feb 2016 Annual Report 2015 21

NIBD (quarterly) DKKm Gearing 2.0 x EBITDA

Gearing target (self-imposed)

0%

10%

20%

30%

40%

50%

0

2,000

4,000

6,000

8,000

10,000

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Equity (quarterly)

DKKm Equity ratio Equity ratio 33%

Equity ratio target (self-imposed)

NIBD / EBITDA Continuing activities

*) Last 12 months EBITDA

Net debt reduced to DKK 3,674m (Q4 2014: 4,593m)

-

1.0

2.0

3.0

4.0

5.0

6.0

0

1,000

2,000

3,000

4,000

5,000

6,000

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

ROCE 10% in 2015 (2014: 12%)

Reaching the 20% ROCE target requires an increase in EBITA to around DKK 3bn through a combination of top-line growth and margin expansion

Return on capital employed

Annual Report 2015

11 Feb 2016 Annual Report 2015 22

ROCE* Average capital employed

DKKm

0%

5%

10%

15%

20%

25%

30%

0

3,000

6,000

9,000

12,000

15,000

18,000

2011 2012 2013 2014 2015

ROCE

10% in 2015

*) ROCE: Return on capital employed calculated on a before tax basis, including goodwill and based on last 12 months’ EBITA and average capital employed

ROCE target

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

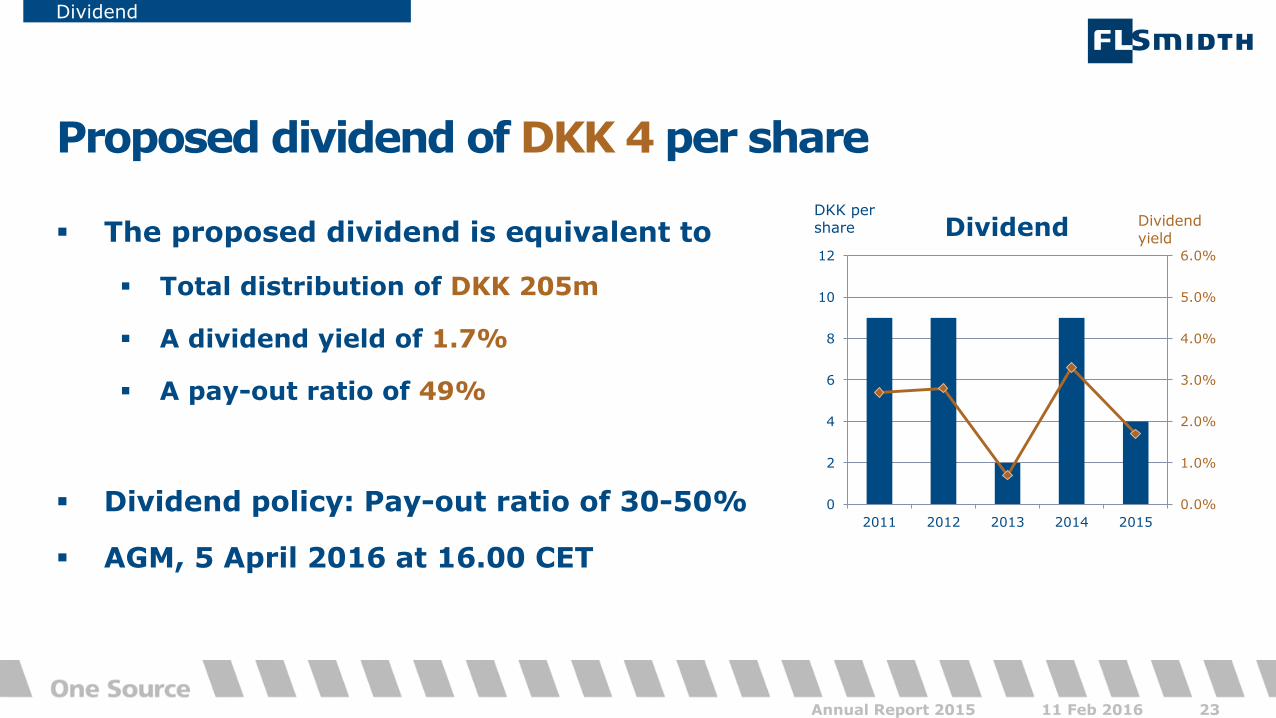

Dividend

11 Feb 2016 Annual Report 2015 23

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0

2

4

6

8

10

12

2011 2012 2013 2014 2015

Proposed dividend of DKK 4 per share

The proposed dividend is equivalent to

Total distribution of DKK 205m

A dividend yield of 1.7%

A pay-out ratio of 49%

Dividend policy: Pay-out ratio of 30-50%

AGM, 5 April 2016 at 16.00 CET

Dividend DKK per share Dividend

yield

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

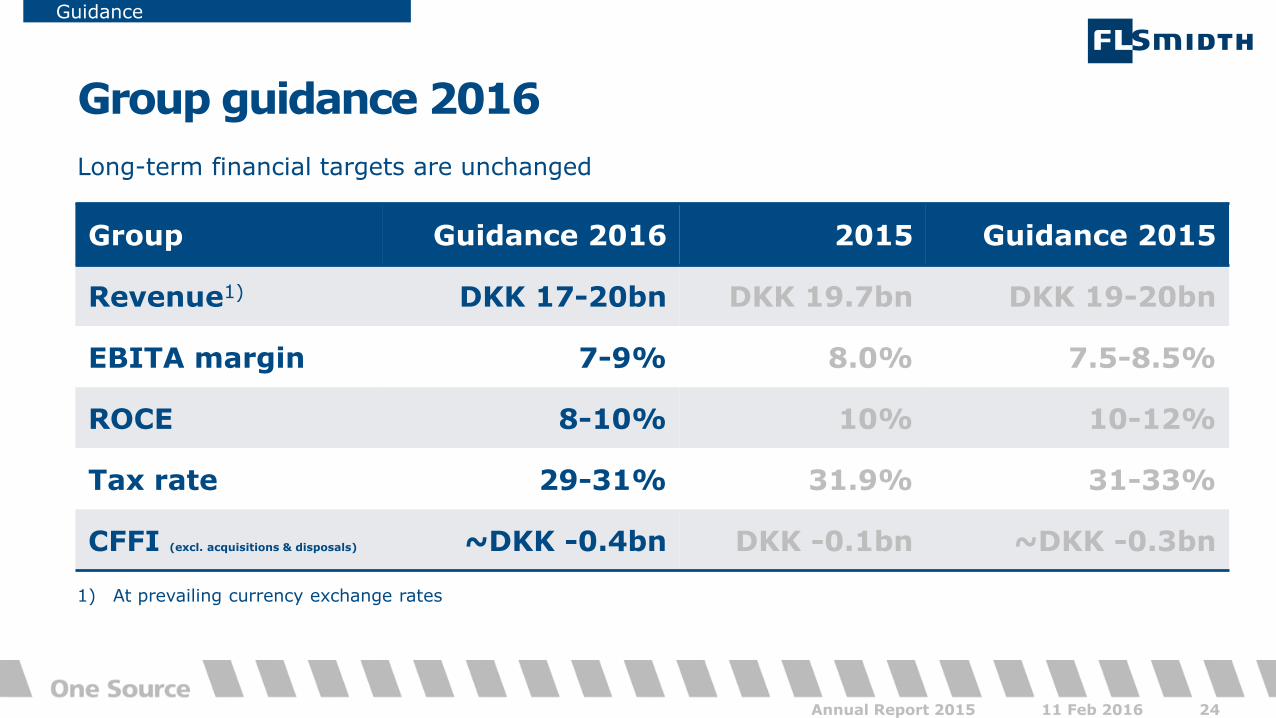

Guidance

11 Feb 2016 Annual Report 2015 24

Group Guidance 2016 2015 Guidance 2015

Revenue1) DKK 17-20bn DKK 19.7bn DKK 19-20bn

EBITA margin 7-9% 8.0% 7.5-8.5%

ROCE 8-10% 10% 10-12%

Tax rate 29-31% 31.9% 31-33%

CFFI (excl. acquisitions & disposals) ~DKK -0.4bn DKK -0.1bn ~DKK -0.3bn

Group guidance 2016 Long-term financial targets are unchanged

1) At prevailing currency exchange rates

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Key highlights – Annual Report 2015

11 Feb 2016 Annual Report 2015 25

2015

• Order intake up 7% despite challenging market conditions

• Revenue and EBITA-margin in line with guidance

• Products and services provide a stable and profitable business

• Positive free cash flow reduced net debt by DKK 0.9bn

2016

• EBITA-margin guidance of 7-9% reflects low visibility and investments in people

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Questions & Answers

11 Feb 2016 26 Annual Report 2015

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Forward-looking statements

Interim Report Q3 2015

11 Feb 2016 Annual Report 2015 27

FLSmidth & Co. A/S’ financial reports, whether in the form of annual reports or interim reports, filed with the Danish Business Authority and/or announced via the company’s website and/or NASDAQ OMX Copenhagen, as well as any presentations based on such financial reports, and any other written information released, or oral statements made, to the public based on this interim report or in the future on behalf of FLSmidth & Co. A/S, may contain forward-looking statements. Words such as ‘believe’, ‘expect’, ‘may’, ‘will’, ‘plan’, ‘strategy’, ‘prospect’, ‘foresee’, ‘estimate’, ‘project’, ‘anticipate’, ‘can’, ‘intend’, ‘target’ and other words and terms of similar meaning in connection with any discussion of future operating or financial performance identify forward-looking statements. Examples of such forward-looking statements include, but are not limited to: • statements of plans, objectives or goals for future operations, including those related to FLSmidth & Co. A/S markets, products, product research and product

development • statements containing projections of or targets for revenues, profit (or loss), capital expenditures, dividends, capital structure or other net financial items • statements regarding future economic performance, future actions and outcome of contingencies such as legal proceedings and statements regarding the underlying

assumptions or relating to such statements • statements regarding potential merger & acquisition activities. These forward-looking statements are based on current plans, estimates and projections. By their very

nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, which may be outside FLSmidth & Co. A/S’s influence, and which could materially affect such forward-looking statements.

FLSmidth & Co. A/S cautions that a number of important factors, including those described in this presentation, could cause actual results to differ materially from those contemplated in any forward-looking statements. Factors that may affect future results include, but are not limited to, global as well as local political and economic conditions, including interest rate and exchange rate fluctuations, delays or faults in project execution, fluctuations in raw material prices, delays in research and/or development of new products or service concepts, interruptions of supplies and production, unexpected breach or termination of contracts, market-driven price reductions for FLSmidth & Co. A/S’ products and/or services, introduction of competing products, reliance on information technology, FLSmidth & Co. A/S’ ability to successfully market current and new products, exposure to product liability and legal proceedings and investigations, changes in legislation or regulation and interpretation thereof, intellectual property protection, perceived or actual failure to adhere to ethical marketing practices, investments in and divestitures of domestic and foreign enterprises, unexpected growth in costs and expenses, failure to recruit and retain the right employees and failure to maintain a culture of compliance. Unless required by law FLSmidth & Co. A/S is under no duty and undertakes no obligation to update or revise any forward-looking statement after the distribution of this presentation.

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 28

Backup slides Next update: Annual General Meeting: 5 April 2016 1st Quarter interim report: 18 May 2016 Follow us on Twitter and LinkedIn

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

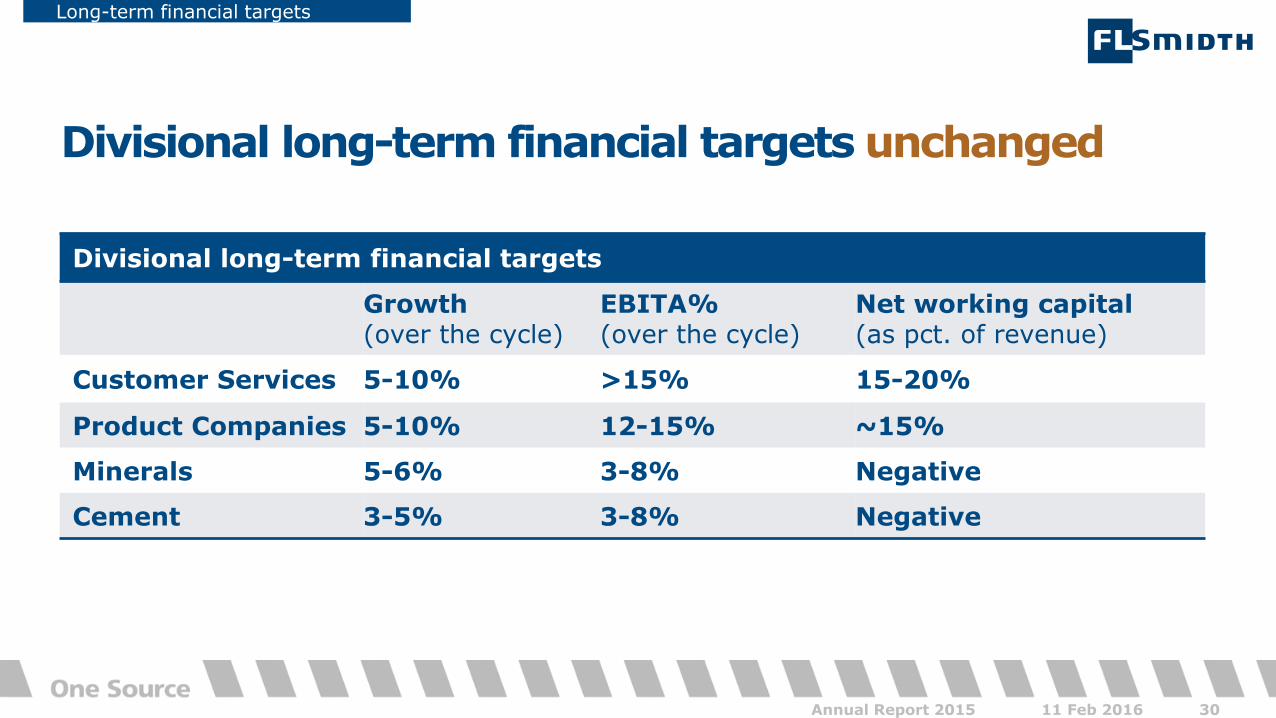

Long-term financial targets

11 Feb 2016 Annual Report 2015 29

Long-term financial targets unchanged

Group long-term financial targets

Annual revenue growth Above market average

EBITA margin 10-13%

ROCE* >20%

Tax rate 32-34%

Equity ratio >30%

Financial gearing (NIBD/EBITDA) <2

Pay-out ratio 30-50% *) ROCE: Return on capital employed calculated on a before tax basis as EBITA divided by average Capital Employed including goodwill

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Long-term financial targets

11 Feb 2016 Annual Report 2015 30

Divisional long-term financial targets unchanged

Divisional long-term financial targets

Growth (over the cycle)

EBITA% (over the cycle)

Net working capital (as pct. of revenue)

Customer Services 5-10% >15% 15-20%

Product Companies 5-10% 12-15% ~15%

Minerals 5-6% 3-8% Negative

Cement 3-5% 3-8% Negative

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 31

Customer Services

Customer Services

(DKKm) Q4

2015 Q4

2014 Change 2015 2014 Change

Order intake 1,655 1,580 5% 6,710 6,847 -2%

Order backlog 2,469 3,575 -31% 2,469 3,575 -31%

Revenue 1,920 1,938 -1% 7,294 7,061 3%

Gross profit margin 29.6% 22.5% 28.9% 28.1%

EBITDA 305 222 37% 1,056 1,060 0%

EBITA 279 197 42% 951 968 -2%

EBITA margin 14.5% 10.2% 13.0% 13.7%

EBIT 240 150 60% 790 827 -4%

EBIT margin 12.5% 7.7% 11.7%

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 32

Organic order intake growth of -1%

EBITA margin in Q4’14 impacted by DKK -90m related to delay of the now terminated O&M contract

Customer Services

Customer Services

0

500

1,000

1,500

2,000

2,500

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Order intake (quarterly)

5% vs. Q4 2014 DKKm

Revenue (quarterly)

DKKm EBITA margin -1% vs. Q4 2014

0%

4%

8%

12%

16%

20%

0

500

1,000

1,500

2,000

2,500

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 33

Product Companies

Product Companies

(DKKm) Q4

2015 Q4

2014 Change 2015 2014 Change

Order intake 1,252 1,194 5% 5,742 5,192 11%

Order backlog 2,536 2,667 -5% 2,536 2,667 -5%

Revenue 1,473 1,451 2% 5,711 5,523 3%

Gross profit margin 27.5% 26.1% 28.9% 28.3%

EBITDA 205 160 28% 849 774 10%

EBITA 184 138 33% 756 672 13%

EBITA margin 12.5% 9.5% 13.2% 12.2%

EBIT 166 119 39% 689 596

EBIT margin 11.3% 8.2% 12.1% 10.8%

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 34

Organic order intake growth of 3%

Product Companies

Product Companies

Revenue (quarterly)

DKKm EBITA margin

2% vs. Q4 2014

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Order intake (quarterly)

+5% vs. Q4 2014 DKKm

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 35

Minerals

Minerals

(DKKm) Q4

2015 Q4

2014 Change 2015 2014 Change

Order intake 630 604 4% 4,112 3,142 31%

Order backlog 4,614 4,298 7% 4,614 4,298 7%

Revenue 1,126 1,407 -20% 3,576 4,933 -28%

Gross profit margin 15.9% 16.2% 16.3% 18.6%

EBITDA (10) 35 (193) 72

EBITA (32) 17 (258) 11

EBITA margin -2.8% 1.2% -7.2 0.2%

EBIT (70) (50) (424) (153)

EBIT margin -6.2% -3.6% -3.1%

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 36

0

500

1,000

1,500

2,000

2,500

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Organic order intake growth of 3%

EBITA result negatively impacted by one-off costs related to efficiency and right-sizing activities

Material Handling legacy projects amounted to 7 (Q3’15: 8) with a total order backlog of DKK 147m (Q3’15: DKK 138m)

Minerals

Minerals

Revenue (quarterly)

DKKm EBITA margin -20% vs. Q4 2014

Order intake (quarterly)

4% vs. Q4 2014 DKKm

Announced orders Unannounced orders

-20%

-10%

0%

10%

20%

30%

-2,000

-1,000

0

1,000

2,000

3,000

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 37

Cement

Cement

(DKKm) Q4

2015 Q4

2014 Change 2015 2014 Change

Order intake 396 547 -28% 2,803 2,943 -5%

Order backlog 5,852 7,768 -25% 5,852 7,768 -25%

Revenue 985 1,098 -10% 3,911 3,951 -1%

Gross profit margin 12.5% 20.1% 15.4% 16.7%

EBITDA (15) 71 132 203 -35%

EBITA (29) 64 99 181 -45%

EBITA margin -3.0% 5.8% 2.5% 4.6%

EBIT (39) 52 52 155 -66%

EBIT margin -3.9% 4.7% 1.3% 3.9%

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

11 Feb 2016 Annual Report 2015 38

0

500

1,000

1,500

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Order intake decreased due to lack of large orders

Revenue declined as result of lower order intake last two years

EBITA impacted by one-off costs of DKK -48m in Q4’15 related to O&M contracts in oil-exporting countries as well as execution of low margin orders – adjusted EBITA margin in Q4: +1.9%

Cement

Cement

Revenue (quarterly)

DKKm EBITA margin -10% vs. Q4 2014

Order intake (quarterly)

-28% vs. Q4 2014 DKKm

Announced orders Unannounced orders

-10%

-5%

0%

5%

10%

15%

-1,000

-500

0

500

1,000

1,500

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Cash flow statement in Q4 2015

Annual Report 2015

11 Feb 2016 39 Annual Report 2015

Group (DKKm) Q4 2015 Q4 2014

EBITDA adjusted 295 483

Change in provisions (62) (91)

Change in NWC (74) 475

Financial payments 24 (68)

Taxes paid (35) (60)

CFFO (Group) 148 739

CFFI excl. acquisitions & disposals (32) (221)

Acquisitions & disposals 52 4

CFFI 20 (217)

Free cash flow (FCF) 168 522

CFFO down from Q4’14 due to lower EBITDA and no positive contribution from change in NWC

Despite modest CFFO in Q4’15, a positive free cash flow was achieved through a prudent investment level and DKK 52m contribution from disposals

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Working capital improved slightly in Q4

Annual Report 2015

11 Feb 2016 Annual Report 2015 40

Net working capital continuing activities DKKm

Net working capital developments in Q4´15

DKKm continuing activities

End Q4 2015 End Q3 2015

Change Change - currency adjusted

Inventories 2,445 2,517 -72 -120

Trade Receivables

4,884 4,476 +408 +368

Trade Payables

-2,546 -2,296 -250 -233

WIP Assets net 73 176 -103 -111

Prepayments net -920 -1,333 +413 +422

Other -1,353 -914 -439 -439

NWC total 2,583 2,626 -43 -113

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Current level is related to market situation in minerals and O&M contracts in oil-exporting countries

NWC 12.3% of revenue on average in 2015 (target over the cycle: <10%)

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Annual Report 2015

11 Feb 2016 Annual Report 2015 41

Growth Customer Services

Product Companies

Minerals Cement Group

Growth (currency adj.)

-1% +3% +3% -31% -5%

Currency effect

+6% +2% +1% +3% 4%

Total +5% +5% +4% -28% -1%

Order intake growth Q4 2015 vs. Q4 2014

Order intake by segment

42%

32%

16%

10%

Order intake Q4 2015

– classified by segment

Customer Services

Product Companies

Cement

Minerals

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Annual Report 2015

11 Feb 2016 Annual Report 2015 42

35%

27%

20%

18%

Product Companies

Minerals

Growth Customer Services

Product Companies

Minerals Cement Group

Growth (currency adj.)

-7% -2% -25% -15% -11%

Currency effect

6% 4% 5% 5% 5%

Total -1% 2% -20% -10% -6%

Revenue growth Q4’15 vs. Q4’14

Revenue by segment

Revenue Q4 2015

– classified by segment

Customer Services Cement

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Minerals EBITA improvement

11 Feb 2016 Annual Report 2015 43

Order backlog and conversion to revenue

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0

5,000

10,000

15,000

20,000

25,000

Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

Order backlog (quarterly)

-16% vs. Q4 2014 DKKm

Order backlog/Revenue

*Order backlog divided by last 12 months revenue

Expected backlog conversion to revenue:

69% in 2016

17% in 2017

14% in 2018 and beyond

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Revenue and order intake

Annual Report 2015

11 Feb 2016 Annual Report 2015 44

0

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

27,000

30,000

2011 2012 2013 2014 2015

Revenue Order intake

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

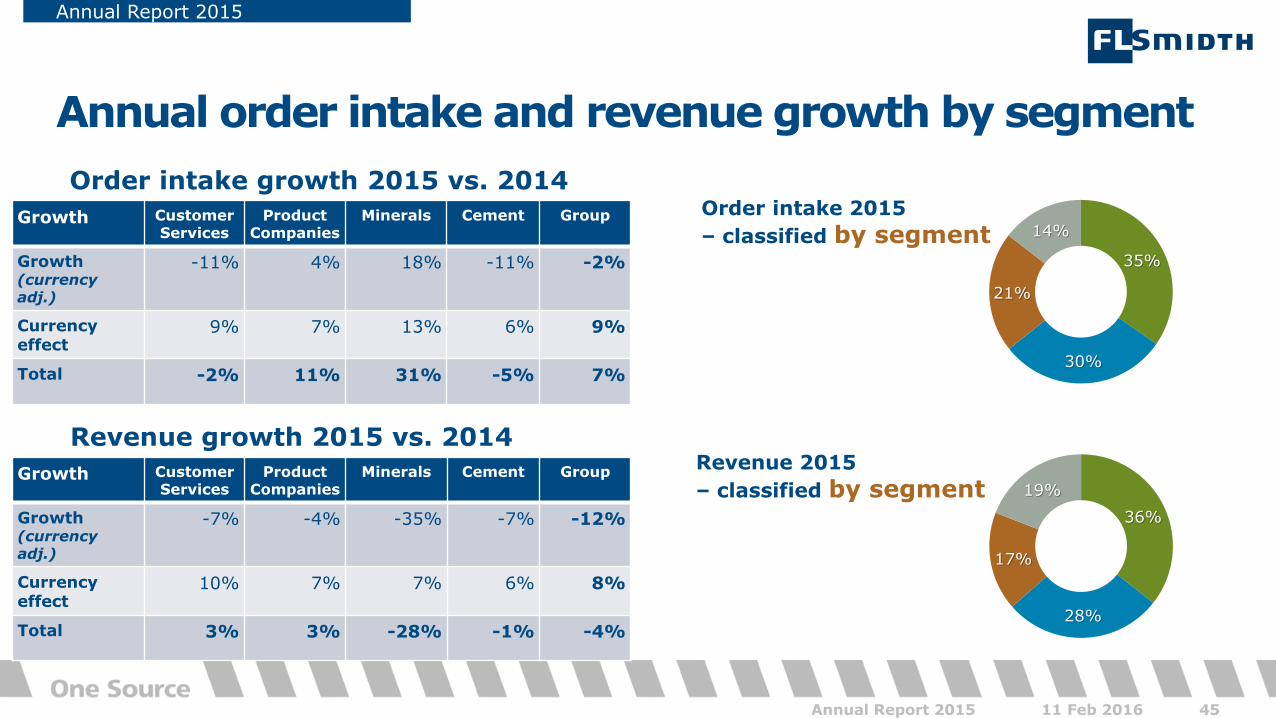

Annual Report 2015

11 Feb 2016 Annual Report 2015 45

Annual order intake and revenue growth by segment Order intake growth 2015 vs. 2014

Growth Customer Services

Product Companies

Minerals Cement Group

Growth (currency adj.)

-11% 4% 18% -11% -2%

Currency effect

9% 7% 13% 6% 9%

Total -2% 11% 31% -5% 7%

Revenue growth 2015 vs. 2014

Growth Customer Services

Product Companies

Minerals Cement Group

Growth (currency adj.)

-7% -4% -35% -7% -12%

Currency effect

10% 7% 7% 6% 8%

Total 3% 3% -28% -1% -4%

35%

30%

21%

14%

Order intake 2015

– classified by segment

36%

28%

17%

19%

Revenue 2015

– classified by segment

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

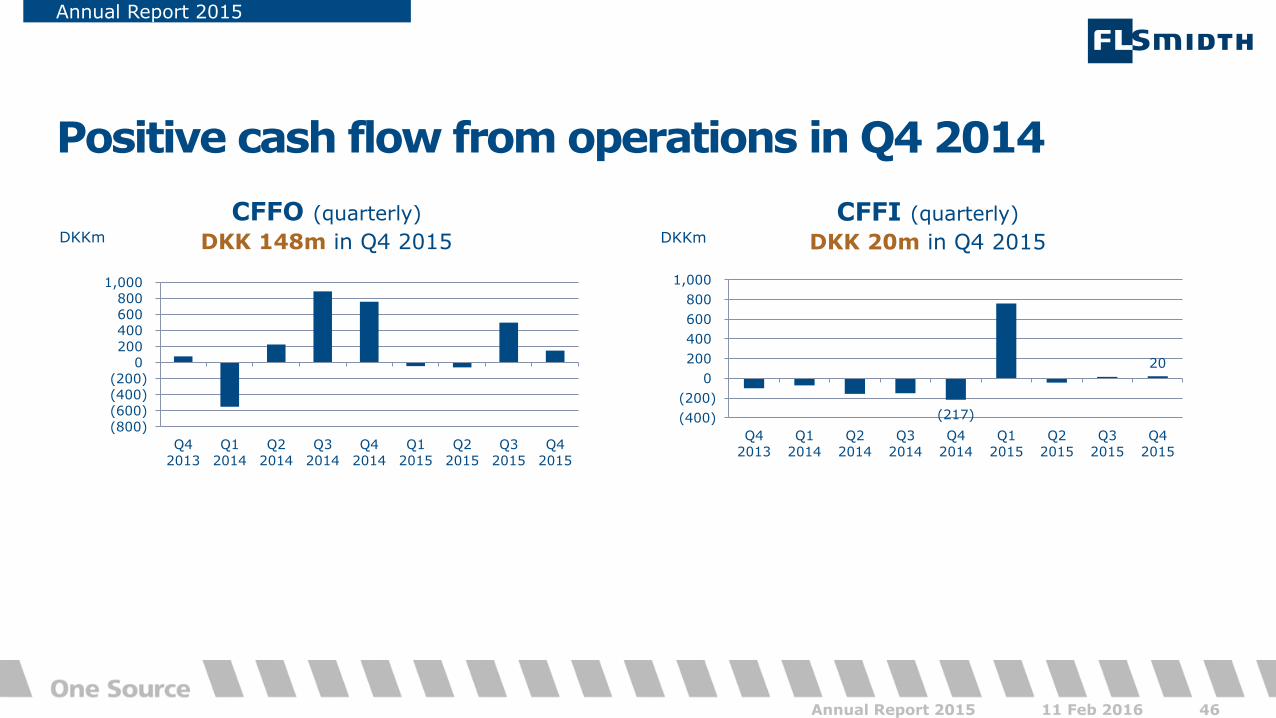

Annual Report 2015

11 Feb 2016 Annual Report 2015 46

Positive cash flow from operations in Q4 2014

CFFO (quarterly) DKKm

CFFI (quarterly)

DKK 20m in Q4 2015 DKKm DKK 148m in Q4 2015

(217)

20

(400)

(200)

0

200

400

600

800

1,000

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

(800)(600)(400)(200)

0200400600800

1,000

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

Annual Report 2015

11 Feb 2016 Annual Report 2015 47

Number of employees decreasing

Number of employees Q4’15 vs. Q4’14 - by segment

4,473

3,376

2,386

3,227

4,731

3,325

1,881

2,793

Customer Services

Product Companies

Mineral Processing

Cement

Q4’15 Q4’14

Total number of employees Q4’15: 12,969

Number of employees decreased by 1,796 vs. Q4’14

Decline explained by divestment of Cembrit and efficiency programme and business right-sizing

Q4’15 Q4’14 Q4’15 Q4’14 Q4’15 Q4’14

Disclaimer included in Footer: The information contained or referenced in this presentation is confidential and proprietary to FLSmidth and is protected by copyright or trade secret laws. DO NOT CHANGE FOOTER! AND KEEP DISCLAIMER ON ALL SLIDES IN THE PRESENTATION. If by chance the footer is changed. Provide the upper text in the footer. Click Insert in the top menu - Click Header & Footer and change the settings under Footer

One-off costs (DKKm) Q4'15 Q4'14 2015 2014

Efficiency programme/Business right-sizing -70 -28 -151 -88

Gain on assets sold 29 0 34 0

Costs & provisions related to O&M contracts -48 -90 -121 0

Bad debt provisions Q2'15 (Chapter 11 filings) 0 0 -83 0

Other 0 -29 0 -87

Total one-off costs -89 -147 -321 -175

Impact on Gross profit -64 -121 -201 -57

Impact on SG&A costs -25 -26 -120 -118

Gross margin reported 23.7% 22.5% 25.1% 25.0%

Gross margin adjusted for one-off costs 24.9% 24.6% 26.2% 25.3%

SG&A ratio 15.0% 13.7% 15.6% 14.7%

SG&A ratio adjusted for one-off costs 14.5% 13.3% 15.0% 14.2%

EBITA margin reported 7.2% 7.4% 8.0% 8.9%

EBITA margin adjusted for one-off costs 8.9% 10.1% 9.7% 9.7%

Impact of one-off costs in Q4’15 and 2015

One-off costs

11 Feb 2016 Annual Report 2015 48