56

Microfinance Strategies David Piesse Head of Insurance Sun Microsystems, Inc. ASIAN Banker Summit March 25 th Jakarta Indonesia

Microfinance Strategies

David PiesseHead of Insurance

Sun Microsystems, Inc.

ASIAN Banker SummitMarch 25th Jakarta Indonesia

TRENDS

HISTORY

Geographical repartition of clients

13%

63%

2%

12%

10%

AfricaAsiaECA Latin AmericaMENA

Geographical repartition of active borrowers

Source : MicroBanking Bulletin in 2004

• With 63 % of clients in Asia, microfinance is a promising sector in this region

Micro Finance – the confluence of :-

Micro FinanceMitigation

Micro Credit and Savings

Micro Insurance

Micro Pensions

Steps involved in microfinance

a) Create micro finance division as alternate distribution channel

b) Downscale the division and products

c) Apply Specific Technical Assistance

d) Get Rating

e) Apply Downscaling diagnostic

f) Do Capacity building

Different types of Regulation :

1. Institution-Centric : Regulation encourages the creation of dedicated institutions to develop micro credit and micro insurance activities

2. Services-Centric : Regulation regulates the service line (micro credit and micro insurance) and allows any type of providers to offer those services.

3. Risk Based capital regimes and action against informal schemes

Trend 1 - Improvement of Regulatory Framework

+ 50% of developing / emerging countries are controlled by specific microfinance regulation covering in recent times insurance

Insurance Industry as a whole enters a period of reform and convergence

1. Decrease in new comers: Donors are not encouraging anymore the creation of new non profit MFIs, except in countries where microfinance is in its infancy

2. Transformation of most successful NGO type MFIs into profit Microfinance Institutions, either under specific country regulation as MicroBanks or in some cases with full bank licenses (KREP, etc.)

3. In a few countries, decrease of number of NGOs because of high competition

Trend 2 - Consolidation of non-profit MFIs

In the last 5 years, the Microfinance NGO have entered a stage of consolidation.

1. A bank supports microfinance through a donation

2. A bank allows microfinance institutions to use its infrastructure

3. A bank refinances Microfinance Institutions

4. A bank invests (equity) in the microfinance institution

5. A bank launches and manages mutual funds for microfinance

6. A bank downscales operations to microfinance/SME Banking/Insurance

7. Banc Assurance Models enter the microfinance world

8. Insurers devise own microfinance products and distribution

Trend 3 - New relationships emerge between microfinance

1. Cost per Transaction

2. Orphaned Policies

3. Mandatory versus Voluntary Insurance

4. Beneficiary issues – riders and gifts left to women

5. No screening and age restrictions

6. MFI changing insurance partners too often

7. Exclusion dropping

8. Efficient Claims processing – MFI education and fraud issues

9. Insurers understanding difference between insurance and micro insurance

ChallengesTrend 4 – Move to Partner : Agent Model – Micro Insurance

1. Staff and client education

2. Insurance as risk management

3. Training on health screening

4. Livestock/crop care education

5. Education scholarships for children

6. Claim settlement and dealing with people with no bank accounts

7. Rural ombudsman

Trend 5 – e-Learning and education in the field

SUSTAINABILITY

Permanent Access toFinancial Transactions

SUSTAINABILITY TRIANGLEOutreach

Clients Banks and Insurers

AffordabilityOperatingCosts

Sustainability Strategies - 1• Apply Credit Life on the Loan

• Benefit Capping

• Targeting Certain Benefits

• Focus On Big Issues

• Affinity Membership

• Low Cost Premium Payments

• Inexpensive Distribution

• Control Costs

Sustainability Strategies - 2• Buy Benefits in Bulk

• Cross Sell from Other Markets

• Subsidize from Endowment Fund

• Access to Government Subsidy

• Operational Risk Securitization

• Partnership with Technology

• Takaful Integration

• Regulation

PRODUCTS

Group Pension PlansAsset ManagementLoans

With RidersAccidental DeathLife Insurance

Healthcare Insurance

Credit InsuranceTerm AssuranceAgricultural

Simple Products

Personal AccidentBasket ProductsLoss of Wages

Very Simple Products

Bank Microfinance Cluster Financing

HospitalisationMedicationOutpatients

Approved Insurer

Healthcare, PA

Livestock/Farms

Motor, Property (hut)

Group/Term Life /Funeral

MICRO INSURANCE FUNDAMENTALS

Mission of Micro Pensions

• Micro entrepreneurs must invest for old age

• Under financed must invest to beat inflation

• Striking balance between risk and average return by diversifying

• Low transaction cost capital accumulation

• Low risk capital appreciation by pooling of resources

• To increase the formal sector by long term asset building

Challenges of Micro Pensions• Must cater to the outreach category

• Must have a good technical distribution strategy and record keeping

• Getting the correct perception by MFI’s on Micro Pensions

• Differing skills to Traditional Microfinance Product Selling

• Conveyance of Financial Planning Concepts to Micro Entrepreneurs

• Pension Fund Asset Management

• Build Hybrid Scheme

Typical Features of Micro Pension• 10 Year Minimum term with Roll Over Option

• Minimum Age 18 and Maturity at 60

• Regulators and State Banks Regulate Interest Rates

• Premature withdrawal of funds reduce interest rates up to 1%

• Pay in Options – scale of $1 to $10 equivalent

• Payout Options – lump sum at maturity

• Annuity Options – lifelong, 5, 10, 15 ,20 years

•Distribution – sales force, alternate channels, MFI’s and Banks

Micro Pension Product Dimensions

• Interest Rates – foundation product price

• Premium Size – value of minimum required premium payment.

• Degree of Flexibility – seasonal cash flows

• Product terms and Roll Overs

• Withdrawal options

• Terms of Pay Out

Micro Pension Product Add-Ons

• Life Insurance with defined contribution

• Doorstep Deposit Collection

• Access to Loans

• Lottery Options

• Pension Products as Collateral to Loans

Best of Breed Banks and

Insurers

Affinities / Retailers

Rural

Community

Loyalty

Cards

Post Offices

On Demand Micro Pensions

Semi Urban Community

“On Request Pensions”“Provision of annuities for old age”by small value defined contribution

DISTRIBUTION

Microfinance Profitable Delivery Strategy?

Diverse

financial services2

Innovative Technology 1

Improved

MIS/Data Warehousing3

Sound regulatory and

legal environment4

What is Required for Delivery ???

An “On Request” or “Pay as You Go”Global Financial Service

Rapidly Create, Launch and Manage Micro Finance Products

via any distribution channelany currency, any language, anywhere in the worldaccessible 24x7 via the web and any pervasive deviceend to end process control with real-time information

Schemes and Affinity Model– a well trodden path – win win

Best of Breed Banks and

Insurers

Affinities / Retailers

Urban

Community

Farmers

Post Offices

MFI’sDirect to End User

Connecting brands and their customers with insurance products and underwriting capacity.

Connecting insurers with niche distribution channels and brand loyal customer segments.

“On Request Distribution”

MFI’s/Insurers need support to :

Manage their internal distribution network

Respond to workflow requests

Manage the relevant information and reporting facilities in Real-Time

Enter loan/risk details, and produce respective loan and policy forms

Have access to both billing and claims information

Be able to aggregate exposures

RISK MANAGEMENT

Long Term Sustaining

Outreach of Customer

Pervasive technology

Cost per Unit of Money Lent

BPOOperationSelf Sufficient

Identity Manage

Total ExpensesActive

Depositors

Gender Active Savers

No. Active Loan Clients

Average Loan Bal. Per Client

Portfolio Outstanding

Low CostOf

Transaction Per

Person

Loan Portfolio Analysis

Technology Responses

Key Performance/Risk Indicators

Loss Ratio

IBNR AggregateExposure

Pricing

Things Happen ….. naturaldisasters and epidemics exclusion –no such thing as micro reinsurance

Government Relief and Capital

Reinsurers/Brokers

Catastrophe Pool

Insurers

Loaning Banks

Contingency DebtWeather Derivative

Cat BondsSecuritizationSUKUK Bonds

Create Risk Financing Team

Aspects of Microfinance Reinsurance

Catastrophe Risk Financing Strategy

Promote Risk

Management

Reduce Customer

Vulnerability

Limit Government

Fiscal Exposure

Passes Risk to Capital Markets

Create Policy Trigger for

Natural Calamity

Planet Finance

Institutional Investors

Re insurers

Donors

World Bank/ Asian Development Bank

Pandemic Preparedness

Risk Evaluation

Facultative Reinsurance

ALTERNATE RISKTRANSFER

CATASTROPHE Bonds

Parametric Triggers

Risk Assessment Underwriting

Treaty Reinsurance

Communities

NGO’s

MFI’s

Insurers/Banks

Pervasive Computing

Micro loan Agents

Loss of Breadwinner

Loss of shelter and Contents

Loss of Crops

Healthcare Indemnity

Motor / Tractor Vehicles

Personal Accident –Operating Times

Commercial Banks

Government

Islamic Finance

Reserving

Salvage

Communities

NGO’s

Insurers

MFI’s

Customer Portals

Funeral Costs

Self-Service

Post Disaster Morbidity

Enables………

Post Office

• Removes Reliance on Post Disaster Funding

• Lack of Liquidity After Disaster Inhibits Recovery

• Years of Unstable Fiscal Deficit Jeopardise Growth

• Poorest Segments are the Most Vulnerable

Benefits

ISLAMIC FINANCE and

TAKAFUL

Takaful Key Facts - 1Takaful Insurance or Sharia compliant insurance productswill aid institutions that are trying to reach the low incomemarket.

Local religious leaders are the key for Sharia microfinance ormicro takaful to be effective.

Takaful has a large impact on the potential for microinsurance asmost Sharia insurance has been focussed on upper middle and higher wealth sectors.

The low income market in Muslim communities most likely toresist non Sharia compliant products.

Takaful Key Facts - 2Intermediaries must charge fee and not commission.

Buyers must be made aware by education that an intermediary is a pass through only for efficiency of getting cover quickly.

All premiums held in the field by intermediaries need to be held in separate accounts from other intermediary monies.

Outreach of Takaful penetration limited by lack of trained personnel.

Islamic Law allows linkages between Takaful companies and cooperatives in general but restrictions on cooperatives andcommercial insurers.

MUDARABA – Trustee MUSHARAKA– equity shareMUSAQAT – orchard MUZAR’AH – harvest shareDirect Investment

Source: TowerGroup

Nexus of Islamic FinanceAnd Microfinance

QARD AL-HASANAH - loanBAI’MUA’JIAL – spot saleBAI’SALAM – ForwardsIJARA WA IQTINA – leasingMURABAHA – cost markupJO’ALAH – service charge

Banc TAKAFULIslamic Capital MarketsRE TAKAFULMUDARABAH – profit shareWAKALAH - Agency

.

For Institutions: Optional and Alternative Investments

Deployment as MICROFINANCE IN RED

Profit and Loss Sharing Non Profit and Loan Sharing TAKAFUL Insurance

Concessionary

Participating Mechanism

Trade Financing

Components of Islamic Finance

TECHNOLOGY and PAYMENTS

Key Technology Facts Reducing transaction costs is important for highly dispersed populations.

Mobile deposit collections reduce costs of policyholders not willing to pay the cost of travel and this can increase policy value.

Mobile banks and micro payment bundling reduce cost of transaction.

Electronic innovations drive down the cost providing high tech alternatives to manual processes.

The Secure Device War Chest

Digital TVSatellite Black Box

Transport

Digital Watches

Enterprise Secure Network Infrastructure

Biometric

USB Port

Kissan / Agriculture

Emergency Loans

Remittances

Claims and Emergency

Identity/MedicalLoyalty

MICRO FINANCE CARDS

Mobile Money

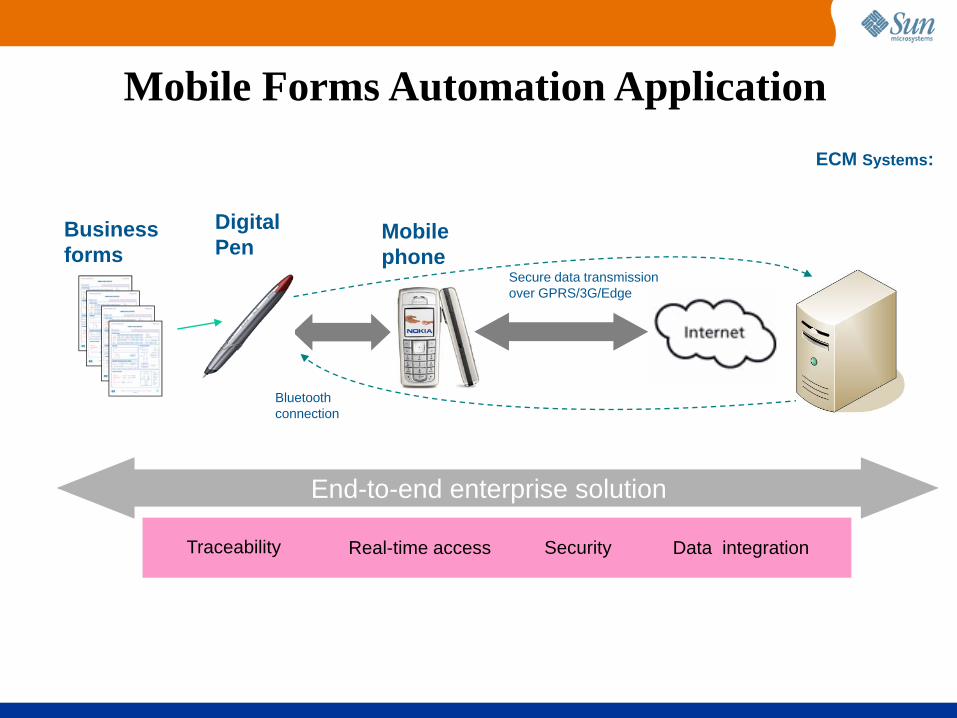

Mobile Forms Automation Application

Mobilephone

Bluetooth connection

ECM Systems:

Secure data transmission over GPRS/3G/Edge

End-to-end enterprise solution

Traceability Security Data integrationReal-time access

Businessforms

DigitalPen

Web Server

Directory ServerApp Server

Identity ManagementPortal ServerMessaging ServerClusteringDatabaseFile System

-Per CPU-Per CPU-Per Entry-Per Identity-Per CPU-Per Mailbox

-Per CPU Core-Per Terabyte

-Per Node

$/Client-Yr$/Loan

Making Penny transactions

Possible

Redefining TechnologyA Partnership of Insurance Industry / Telco and IT

Web Services

CASE STUDY

CONCLUSION

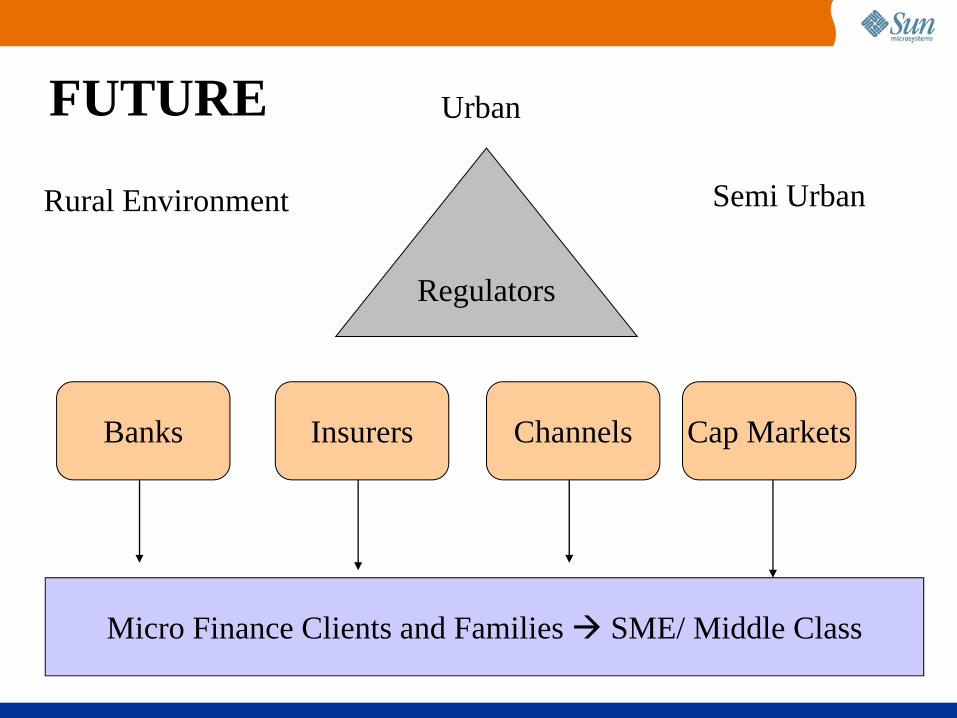

Regulators

Banks Insurers Channels Cap Markets

Micro Finance Clients and Families SME/ Middle Class

Rural Environment

Urban

Semi Urban

FUTURE