23

Rick Blasgen, President & CEO Council of Supply Chain Management Professionals (CSCMP)

Sean Monahan, PartnerA.T. Kearney

May 1, 2017

Navigating the Road Ahead: insights from CSCMP’s State of Logistics Report

A.T. Kearney CSCMP 3

A Professional Association: Evolution and Relevancy

1963

1985

2004

National Council of

Physical Distribution

Management

Council of

Logistics

Management

Council of Supply Chain

Management Professionals

A.T. Kearney CSCMP 4

EDUCATION

RESEARCH

CONNECTIONS

NETWORKING

CAREER RESOURCES

CSCMP – What You can Experience!

A.T. Kearney CSCMP 5

Join us in Atlanta, Georgia for CSCMP’s 2017

Annual Conference, September 24-27

Register today!cscmpconference.org

SCM professionals

under one roof

3000+

hours educational

content

120+

hours dedicated

networking

25+

A.T. Kearney CSCMP 6

Supply Chain Concierge Service

Join the Community – visit CSCMP.org!

CSCMP’s Evolving Role

• Goal

Connect, Educate and Develop the

world’s Supply Chain Professionals!

A.T. Kearney CSCMP 7

Meet A.T. Kearney• 90 year history

• Diverse global management consulting firm

• Known for Operations expertise, but full service – Digital

Transformation; Strategy; Leadership, Change & Organization

Industry

Expertise

Aerospace & Defense

Automotive Chemicals Comms, Media, &Technology

ConsumerProducts& Retail

FinancialInstitutions

Metals &Mining

Oil &Gas

PrivateEquity

PublicSector

Transportation,Travel, & Infrastructure

UtilitiesHealth

A.T. Kearney CSCMP 8

Our objectives today…

■ Share key insights from last year’s report and preview of perspectives from the 2017 report

■ Challenges on the road ahead

•Infrastructure

•Ecommerce

•Digital disruption

Stay tuned for June release!

A.T. Kearney CSCMP 9

State of Logistics Report is a

collaborative effort …

I Focused economic analysis

II Interviews with logistics industry leaders

III Logistics industry context and point of view

I

V

Trends and deep dives:global trends, sector trends, regulation, technology

State of Logistics

A.T. Kearney CSCMP 10

US business logistics costs

US Business Logistics Costs totaled

$1.4 Trillion in 2015

$ billion

1,169

1,243 1,245

1,063

1,127

1,223 1,273

1,321

1,373

1,408

1,000

1,100

1,200

1,300

1,400

1,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

5.1% CAGR2.6%

Source: CSCMP’s 27th Annual State of Logistics Report, A.T. Kearney

State of Logistics

A.T. Kearney CSCMP 11

As a percentage of GDP, USBLC declined

6 basis points to 7.85%

8.44%

8.59%

8.46%

7.37%

7.53%

7.88%

7.88%

7.93% 7.91%

7.85%

7.0

7.5

8.0

8.5

9.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US business logistics costs as a share of nominal GDP (%)

Note: bp is basis points.

-6 bp

Source: CSCMP’s 27th Annual State of Logistics Report, A.T. Kearney

State of Logistics

A.T. Kearney CSCMP 12

1,408

$0

$250

$500

$750

$1,000

$1,250

$1,500

Motor Carrier Parcel Rail Other Modes InventoryCarrying

Support/Admin Total

U.S. Business Logistics Costs – 2015$ billion

Source: CSCMP’s 27th Annual State of Logistics Report, A.T. Kearney

Truckload

LTL

Dedicated / Private

Intermodal

Carload

Storage

Other

Financing

Air

Pipeline

Water & Ports

Motor Carrier and Inventory are the major

drivers of U.S. Logistics Costs

State of Logistics

A.T. Kearney CSCMP 13

Asia 17% GDP

China 18% GDP

Europe 13% GDP

India 13% GDP

Japan 11% GDP

Mexico 14% GDP

Economy• Higher Output – GDP

• Better use of resources

• Multi-use Infrastructure

Businesses• Market Access

• Market Integration

• Cost Efficiency

Consumers• More Goods and Services

• Wider Availability

• Lower Prices/Income

U.S.

7.9% GDP

U.S. benefits from a highly efficient logistics system

State of Logistics

A.T. Kearney CSCMP 14

U.S. supply chain leverages an infrastructure of tremendous proportion

8.4 million lane miles

46,6320 Interstate highway miles

599,766 road bridges

360 commercial sea and river ports

9,627 miles of inland waterways

140,000 miles of rail

Source: U.S. Department of Commerce

Infrastructure

A.T. Kearney CSCMP 15

However, despite importance to U.S. Economy, that infrastructure is at risk

Surface

Transportation Rail

Waterways

& Ports

Roads Bridges Waterways Ports

Grade D C+ B D C+

Needs

( 2025)$2,042 $1,541 $37

Funding $941 $124 $22

Gap $1,101 $29 $15

Total $1,145 Funding GapSource: American Society of Civil Engineers 2017 Infrastructure Report Card, A.T. Kearney

2017 Infrastructure Report Card – Key Logistics Categories ($ billions)

Infrastructure

A.T. Kearney CSCMP 16

Growing Rapidly Impacting Major Categories

Online Penetration, % of Total Category (US 2016)

No Signs of Slowing Down

• Online growing 3X faster than traditional B&M channel

• From 2012 to 2016, ecommerce grew from 5.4% to 8.1% of retail sales

Widespread Adoption

• All cohorts buying online (boomers, millennial) and penetration is growing for all categories

• Current penetration is low for Food & Bev, however is forecasted to have a sales growth rate of 16% CAGR

Online is growing rapidly at 15% CAGR and the Food & Bev category is underpenetrated

Books, MediaApparel and Accessories

58%

19%

7%

16%

2- 3%

Food and Beverage

Consumer Electronics

Health & Personal

Care

Source: Statista., Euromonitor 2017, United States Census Bureau, A.T. Kearney analysis

$696

$610$532

$462$395

$343

2017F

+15%

2019F20162015 2018F 2020F

Online Sales (US $B)E-Commerce

Under-penetrated

Ecommerce

A.T. Kearney CSCMP 17

Accelerated growth in Food & Bev as consumers focus on convenience and price

US Online Channel Forecast

Year over year online channel usage

Convenience

Key Drivers

• Merging channels – shop anytime, anywhere

• Hassle-free – no commuting,

crowds, auto-replenishment

• Click-and-collect service becomes

commonly offered

Assortment

• Provides an opportunity to expand product offering e.g., “endless-aisle”

• Promotional and specialty item access

Price

• Instant comparison of price and promotion across retailers

• Free shipping as a source of attraction

Source: AlphaWise, Morgan Stanley Research

22%Home furnishings

18%

23%

Sporting goods 15%

15%Home improvement items

Auto parts

Baby food & products 13%

16%

Pet food & supplies25%

18%

6%

Food & Bev (packaged) 28%14%

Grocery (fresh)

22%

19%

8%26%

Next 12 months

Last 12 months

Ecommerce

A.T. Kearney CSCMP 18

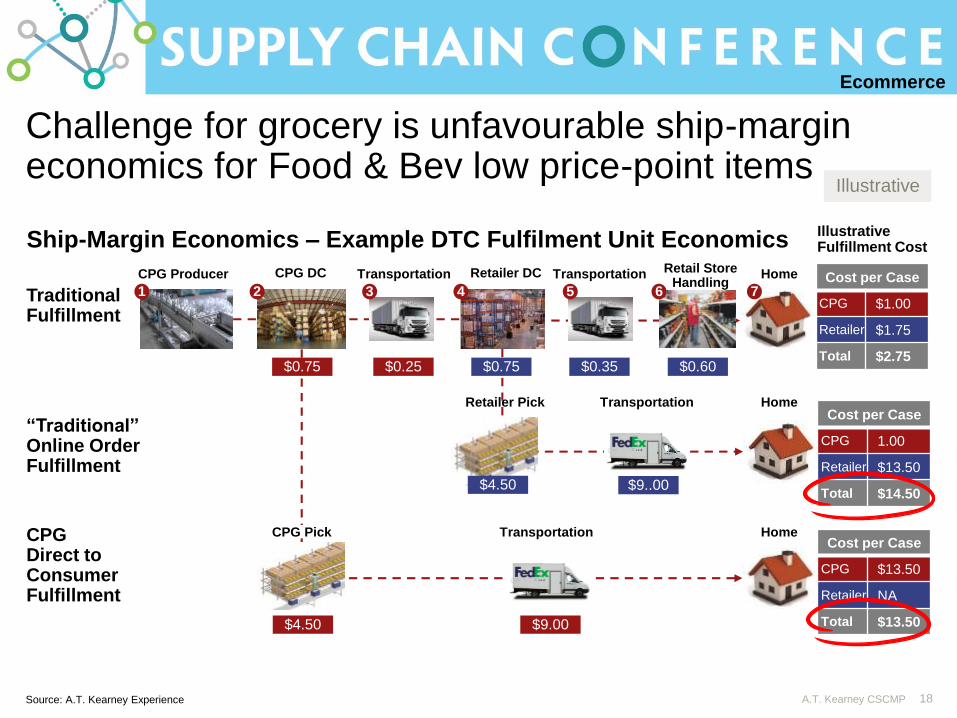

Challenge for grocery is unfavourable ship-margin economics for Food & Bev low price-point items

Illustrative

Retailers

Retailer DC Retail Store Handling

CPG Producer HomeTransportationCPG DC

Home

Transportation

CPG Pick

Retailer Pick Transportation

HomeTransportation

1 2 3 4 5 6 7Traditional Fulfillment

“Traditional” Online Order Fulfillment

CPG Direct to Consumer Fulfillment

Illustrative Fulfillment Cost

$0.75

$4.50 $9.00

$9..00$4.50

$0.25 $0.75 $0.35

Cost per Case

CPG $1.00

Retailer $1.75

Total $2.75$0.60

Cost per Case

CPG 1.00

Retailer $13.50

Total $14.50

Cost per Case

CPG $13.50

Retailer NA

Total $13.50

Source: A.T. Kearney Experience

Ship-Margin Economics – Example DTC Fulfilment Unit Economics

Ecommerce

A.T. Kearney CSCMP 19

Logistics industry disruptors

Logistics

industry

Technology adoption

• Autonomous vehicles, IoT• Artificial intelligence• “Uberization”• 3D printing• Big data• Alternative fuels

Macroeconomic trends

• Globalization• Volatile commodity prices• Climate disruption• Urbanization

Consumer requirements

• “Want it now”• Personalization• Millennial preferences• Omnichannel shopping• Aging consumer needs

Operational constraints

• Free trade agreements• Environmental legislation• Safety requirements• Resource availability

On the cusp of a new era: Industry disruptors

Key Disruptors

• Technology adoption: pace and breakthrough nature of technological innovation

• Operational constraints:regulations and resource scarcity will influence the ability to perform transportation and logistics activities

Note: IoT is the Internet of Things.

Sources: CSCMP; A.T. Kearney

Digital Disruption

A.T. Kearney CSCMP 20Source: CSCMP, A.T. Kearney

Long-term View – Four Possible Scenarios

Stop Signs & Red Lights

Fierce operational constraints in a regulated, low-growth environment. Due

to regulations, only the strongest and most easily adoptable technologies

flourish

Middle of the Road

Technology capabilities improve incrementally. Customers have a few more

choices, but no distinctive competitor emerges. Regulators are business-friendly

and rational

Unconstrained Operations

Crusin’ Down the Highway

Widespread and far-reaching tech adoption leads to a new paradigm: capital and technological expertise reframe the

industry

Technology Breakthrough

Dead End Street

Regulators are inflexible and hinder the entrepreneurial spirit and technological

advancement. Cost of regulatory compliance shakes out supply markets.

Great expectations remain unmet.

Incremental Technology Adoption

Constrained Operations

Digital Disruption

A.T. Kearney CSCMP 21

HMI, control units,E/E architecture

Sensors Actuators

Connectivity, context, maps

Source: A.T. Kearney

Autonomous driving will be the next breakthrough in trucking efficiencyDisruptive force: Autonomous driving

Warning only

Partial assist

Connected assist

Highway pilot

AutonomousDelivery Hwy.

No automation but warning functions (e.g. collision warning)

Automation of single functions(e.g. emergency braking)

Automation of connected functions (e.g. lane change assist)

Partial self-driving on highways(no permanent driver supervision required)

Self-driving on highways(autonomous hub-to-hub incl. platooning)

AutonomousDelivery Urban

Self-driving on highways and urban (autonomous hub-to-hub and last mile)

tod

ay

20

20

20

25

>2

03

0

Lidar

Radar

Wheel speed

Stereo camera

Steering angle Throttle Transmission

BrakeSteering

Digital Disruption

A.T. Kearney CSCMP 22

OEMs increasingly see trucks as mobile, connected data centers

Source: Daimler Trucks

Digital Disruption

A.T. Kearney CSCMP 23

Sean Monahan, A.T. KearneyCell: +1 212.365.4941

Email: [email protected]

Twitter: @SeanTMonahan

Rick Blasgen, CSCMPPhone: +1 630.645.3458

Email: [email protected]

Twitter: @RBlasgen