32

Review of Automobile Sector In India

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | pradeepbandi |

| View: | 11 times |

| Download: | 0 times |

Review of Automobile Sector In India

Ofer Ashtamkar 03Kishor Choudhary 12Ajay Jaiswal 25Kunal Mane 31Santosh Saud 46Sagar Vijan 61

Presented by:

IntroductionThe automobile industry is one of India’s most vibrant and growing

industries. This industry accounts for 22 per cent of the country's manufacturing gross domestic product (GDP).

The auto sector is one of the biggest job creators, both directly and indirectly.

India's domestic market and its growth potential have been a big attraction for many global automakers. India is presently the world's third largest exporter of two-wheelers after China and Japan.

The next few years are projected to show solid but cautious growth due to improved affordability, rising incomes and untapped markets.

HistoryIndian market before independence - imported vehicles while assembling of cars manufactured by General Motors (GM) and other brands

Indian automobile industry mainly focused on servicing, dealership, financing and maintenance of vehicles. Later only after a decade from independence manufacturing started.

After independence - manufacturing capability was restricted by the rule of license and could not be increased.

In 1953 an import substitution program was launched, and the import of fully built-up cars began to be impeded.

The production was confined to three main manufacturers Hindustan Motors, Premier Automobiles and Standard Motors.

Hindustan motors was launched in 1942, long time competitor Premier in 1944. They built GM and Fiat products respectively.

Mahindra & Mahindra was established by two brothers in 1945, and began assembly of Jeep CJ-3A utility vehicles.

Tata entered the commercial vehicle sector in 1945 after forming a joint venture with Daimler-Benz of Germany.

To promote the auto industry the government started the Delhi Auto Expo which had its debut showcasing in 1986.

There was no expertise or research & development initiative.

Evolution of Automobile Industry

Initial Years Manufacturing was licensed•High Customs duty on import•Steep excise duties & •sales tax•2 Major players: Premier Automobiles Ltd & Hindustan Motors

1980s•Entry of MUL, better product, with government support

•Seller’s Market

•Long Waiting Periods

Early to mid 90s

•Seller’s market and long waiting periods

•De-licensing in 1993

•Removal of capacity restrictions

•Decrease in customs & excise

•Auto finance boom- more players (foreign banks & non banking companies, better schemes.

Mid 90s – Early 2000s

•Buyers market

•Increase in Indigenization

•Easy Auto finance

•Manufactures diversifying into related activities: finance lease, fleet management, insurance and used car market

After 2000 - Era of globalization and evolution of India as a global manufacturing hub

Top & Major Manufacturers in Automobile Industry

Maruti suzuki Ltd. General Motors India Ford India Ltd. Eicher Motors Bajaj Auto Hero Motors Hindustan Motors Hyundai Motor India Ltd. Royal Enfield Motors TVS Motors Swaraj Mazda Ltd Toyota Nissan Chevrolet Tata motors

India is….

Is one of the largest automotive markets in the world

Largest TRACTOR manufacturer

2nd Largest TWO WHEELER manufacturer

2nd Largest BUS manufacturer

5th Largest HEAVY TRUCK manufacturer

6th Largest CAR manufacturer

8th Largest COMMERCIAL VEHICLE manufacturer

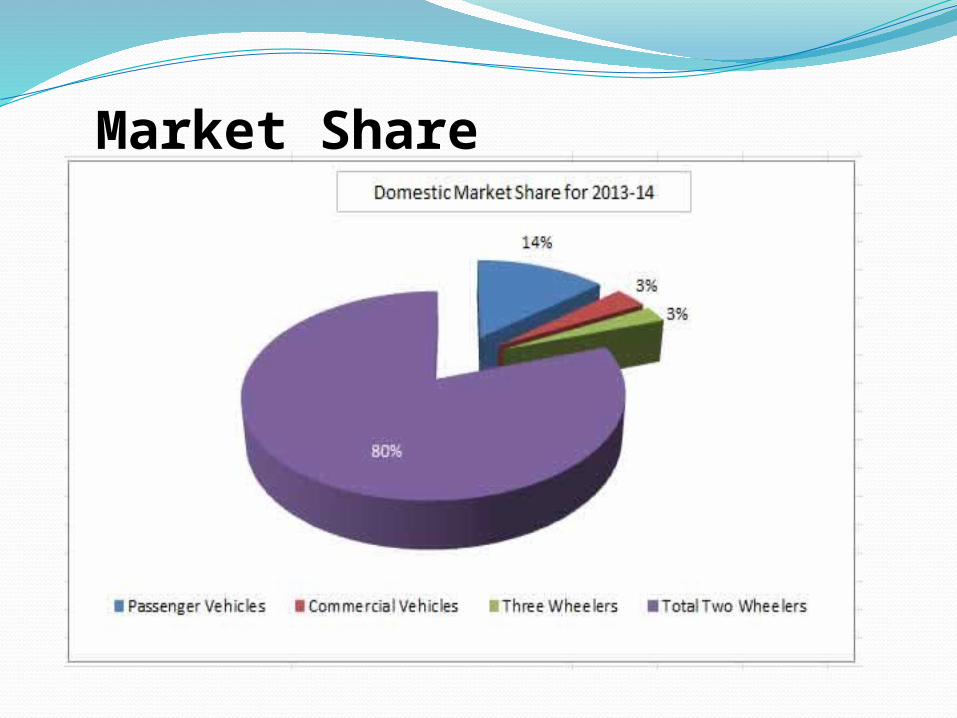

Market Share

(Number of

Vehicles)

Category2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Passenger Vehicles

15,52,703

19,51,333 25,01,542 26,29,839 26,65,015 25,03,685

Commercial Vehicles

3,84,194 5,32,721 6,84,905 8,09,499 7,93,211 6,32,738

Three Wheelers

3,49,727 4,40,392 5,26,024 5,13,281 5,38,290 4,79,634

Two Wheelers

74,37,619

93,70,951 1,17,68,910

1,34,09,150

1,37,97,185

1,48,05,481

Grand Total

97,24,243

1,22,95,397

1,54,81,381

1,73,61,769

1,77,93,701

1,84,21,538

Automobile Domestic Sales Trends

Automotive industry crisis

Global financial crisis in the auto industry that began during the latter half of 2008

Weakened by the substantially more expensive automobile fuels linked to the 2003-2008 oil crisis

The global financial crisis and the related credit crunch placed pressure on the prices of raw materials

In 2009, the vehicle companies of the world are being hit hard by the economic slowdown across national boundaries

Analysis of current scenario

• A total of 16.9 m two-wheelers were sold in FY14, a growth of a tepid 7% over the previous year.

•Passenger vehicles (PV) also did badly as volumes declined by 6%. Slowdown in the economy, firm interest rates and fuel prices had an adverse impact on demand.

•It was a second consecutive challenging year for the medium and heavy commercial vehicles (M/HCVs) segment as volumes plunged by 25%. LCVs were at the receiving end as well as volumes dropped by 17.6% YoY

Both Tata Motors and Ashok Leyland faced heavy challenges during the year given that both of them corner a significant chunk of the CV pie.

Analysis of current scenarioTractors did very well during the year as

monsoons in 2013 were quite healthy and M&M, which is a market leader in the tractors space, benefitted from this as its auto division faced rough weather.

As volumes took a beating, few of the companies did manage to report an improvement in operating margins largely on account of various cost rationalization measures undertaken.

Porter five forces analysisPorter five forces analysis is a framework to analyze

level of competition within an industry and business strategy development.

BCG MATRIX OF TATA MOTORS

Safari Dicor , Indica Vista , Star bus , Manza , Winger, Magic

???Nano, versa & other new inventions

Safari, Sumo, Indigo CS

Indigo Sedan, Sierra, Estate

HIGH

LOW

HIGH LOW

BUSINESS

GROWTH RATE

Marketing Strategies adopted by Automobile industry in India

Advertisements

Digital medium

Print medium

Celebrity endorsements and testimonial advertisements

Segmentation

1. Based on the price of the car:-Economy SegmentMid- Size SegmentLuxury car segmentSuper luxury car segment

2. Based on the length of the car:-A segment - Cars that are less than 3.5 meters long (800, Omni)B segment- Cars between 3.5 meters to 4 meters long (Zen and Santro)C Segment- Cars between 4 meters to 4.5 meters long (Honda city)D segment- Cars that are more than 4.5 meters long (Mercedes,

Sonata, Accord, Skoda)

3. Based on the user segmentIndividual BuyersTaxi operators Government /non-government institutions

PEST analysis

PoliticalThe Government of India allows 100 % FDI under the

automatic route.The government had lowered excise duty on small cars,

motorcycles, scooters & commercial vehicles to 8 % from 12 %, on sports utility vehicles to 24 % from 30 %, on mid-segment cars to 20 % from 24 % and on large-segment cars to 24 % from 27 %.

The Government of India-appointed Society of Indian Automobile Manufacturers (SIAM) and Automotive Components Manufacturers Association (ACMA) are responsible in working for the development of the Indian automobile industry

EconomicalThe level of inflation, Employment, level of per capita .Economic pressures on the industry are causing

automobile companies to reorganize the traditional sales process.

Weighted tax deduction of up to 150% for in-house research and R & D activities.Govt. has granted concessions, such as reduced interest rates for export

SocialGrowth in urbanization, 4th largest economy by PPP

index.Upward migration of household income levels.

85% of cars are financed in India.Car priced below 720000 accounts for nearly 80% of the market.

Vehicles priced between 420000-720000 form the largest segment in the passenger car market.Indian customers are highly discerning, educated and well informed

TechnologicalTechnological solutions helps in integrating the supply

chain, hence reduce losses and increase profitability.Customized solutions (designer cars, etc) can be provided

with the proliferation of technology Internet makes it easy to collect and analyse customer feedback

With the entry of global companies into the Indian market, advanced technologies, both in product and production process have developed.

With the development or evolution of alternate fuels, hybrid cars have made entry into the market.

Various ChallengesIn Indian Automotive Market, there are some challenges by virtue

of

which automobile industry faces lot of problems. These challenges

should be overcome and the challenges are listed below:

• Growth in input costs

• Fuel price volatility

• Slowdown in demand

• Production cuts

• Growing competition

• Changing consumer preferences

• Environmental issues

• Low R&D orientation

The Future of the Automotive IndustryDevelopment of the domestic electric and hybrid

vehicles in the country.Industry gearing up for GREEN VEHICLE

manufacturing.Development of smaller engines to be high on

agenda.Penetration of telematics: In-vehicle infotainment

and embedded software to riseCost optimization: The survival tool.Used cars market set for rapid expansion.

ConclusionIndia has the potential to develop into a significant market for

automobile manufacturers.

Indian automotive industry holds significant scope for expansion, both,

In the domestic market ,Where the vehicle penetration level is on the lower side as compared to world average, and in the international market, where India could position itself as a manufacturing hub.

References:Automotive Component Manufacturers Association of India

(ACMA)Society of Indian Automobile Manufacturers (SIAM)Union Budget 2014-15Department of Industrial Policy and Promotion (DIPP)Press ReleasesMedia Reports

Thank You !

Budget Proposals Directly Impacting the Indian Automotive Industry