2011 Submitted By: Bashir Uj Jaman Markfield Institute of Higher Education (Mihe) University of Gloucestershire Benchmarking in Islamic Finance This paper is an initiative to analyze and justify benchmarking of interest rate (LIBOR) for Islamic Finance and Banking. To do so author has tried to find the answer of following questions: How interest based benchmarking affects Islamic finance as an industry? In what extant Islamic Sharia allows it to benchmark a rate based on interest (Riba)? What are the recent researches have been done to establish an alternative of Interest based benchmarking? Due to incorporation of interest benchmarking in the practice of Islamic banking and finance, this industry is not considered an interest free industry as it is claimed. Do you agree? Argue.

Transcript

2011

Submitted By:

Bashir Uj Jaman

Markfield Institute of Higher Education (Mihe)

University of Gloucestershire

Benchmarking in Islamic Finance

This paper is an initiative to analyze and

justify benchmarking of interest rate

(LIBOR) for Islamic Finance and Banking.

To do so author has tried to find the

answer of following questions: How

interest based benchmarking affects

Islamic finance as an industry? In what

extant Islamic Sharia allows it to

benchmark a rate based on interest

(Riba)? What are the recent researches

have been done to establish an alternative

of Interest based benchmarking?

Due to incorporation of interest benchmarking in the

practice of Islamic banking and finance, this industry is

not considered an interest free industry as it is claimed.

Do you agree? Argue.

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 2

Benchmarking interest rate in Islamic banking has become subject of debate and

controversy from the inception of Islamic finance. In order to find out answers to the

doubt and bring solution on the issue, one need to understand the term „‟ benchmarking‟‟

and „‟Islamic finance‟‟ clearly.

Benchmark:

Robert Demilio (1995) defines „‟benchmarking as an improvement process used to

discover and incorporate best practice into your operation. Benchmarking is the preferred

process used to identify and understand the elements (causes) of a superior or world class

performance in a particular work process‟‟.

Xerox corporation, which is the pioneer of the technique‟s application in management

practice, defines it as „‟ The search for industry best practices which lead to superior

performance (Codling,S.,1992)‟‟.

From above two definitions key points identified are best practice and superior

performance. For instance Allah says in the Quran, “Indeed in the Messenger of Allah

you have an excellent example (best practice) to follow for whoever hopes in Allah and

the Last Day and remembers Allah much (best performance).” (33:21).

So any muslim wants to worships Allah in the best possible manner should follow the

sunnah of the prophet (pbuh). For instance, if you want to be a best husband, you need to

look and follow the way prophet (pbuh) has behaved with his wife. So a muslim is

expected to benchmark the sunnah of prophet (pbuh) in each and every sphere of life to

get the best performance in both worlds, here and hereafter.

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 3

Islamic Finance:

Islamic finance has been established with an initial intention to save Muslims from

adverse effects of Riba. But it is now benchmarking riba. So, we need to justify how does

interest based benchmarking in Islamic banking is the best practice and how it is leading

to superior outcomes. Some of the authors has termed Islamic Finance as „‟Ethical

finance‟‟ which is free from injustice. Specifically, Islamic finance is a system which

prohibits riba, avoids any gharar (uncertainity), gambling (Mysir) and investment in

haram (prohibited) activities. Other authors have defined Islamic finance as asset backed

finance instead of debt based finance which shares both profit and risk.

Logic in favor of interest rate benchmarking:

Allah has forbidden riba and allowed trade (Quranic verse 2: 275). Trade is of mainly two

types; sale of any product or services, and investment. Sale can be on spot or on deferred

payment basis. Unlike Musawama sale there is no scope of bargaining in murabaha sale

or in ijara. So IFI needs to fix profit rate beforehand. On the other hand, in investment

based trade like mudaraba or musharaka though bank will know the profit rate later, still

it needs to declare expected rate of return beforehand to attract deposit on investment

account. To standardized this mark up or profit rate, bank benchmark interest rate like

LIBOR (London interbank offered rate). According to some prominent sharia scholar of

Islamic finance, benchmarking interest rate (riba) is not forbidden (haram) but it is not

desired. Islamic banks can use LIBOR as benchmark of profit rate until any alternative

Islamic benchmark has been established.

According to Justice Taqi Usmani, ‘’If all the pillars of sale is valid from sharia point

of view, just mere use of interest rate as a benchmark cannot invalidate whole sale’’

(ibid: 119). On the other hand, if conventional banks use any Islamic benchmark to fix

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 4

their interest rate, only use of Islamic benchmark cannot Islamized their haram

transaction.

At a discussion board at opalesque Islamic finance intelligence Sheikh. Yusuf DeLorenzo

(2009) states;

‘’A benchmark is no more than a number, and therefore non-objectionable from a sharia

perspective. If it is used to determine the rate of repayment on a loan, then it is the

interest bearing loan that will be haram. LIBOR as a mere benchmark, has nothing to do

with actual transaction or, more specifically with the creation of revenue or return’’.

Islamic bank is still a niche market and need to co-exist with the conventional banking.

So, comparison of the profit margin with the prevailing interest rate would be difficult to

avoid (Hamoud, 1994: 74-75). Therefore because of the competition with the

conventional banks to attract deposits from customers, Islamic banks are forced to

benchmark interest rate. This argument is supported by some surveys in Iran and

Malaysia. Seyed-Nezamaddin Makiyan (date unavailable) from Iran has found that

changes in the rate of return and the rate of inflation generate changes in the levels of the

supply of loans and of total deposits. Another study in Malaysia by Dr Sudin Haron &

Norafifah Ahmad (date unavailable) provides evidence regarding the relationship

between the amount of deposits placed in the Islamic banking system in Malaysia and

returns given to these deposits. The findings confirmed that customers who place their

deposits at saving and investment account facilities are guided by the profit motive. The

existence of the utility maximization theory among the Muslim customers is further

confirmed by the negative relationship between the interest rate of conventional banks

and the amount deposited in interest-free deposit facilities. Therefore, if profit rate of

Islamic banks is lower than conventional interest rate, then Islamic banks will lose

depositors. On the other hand, if profit rate is higher than interest rate, then Islamic banks

will lose clients/ entrepreneurs who will refuge to take investment from Islamic banks.

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 5

Logic against Interest rate Benchmarking:

Prophet (pbuh) has forbidden copying non Muslims. He suggests fasting for two days on

the day of Ashura while jews fast for only one day, only to differentiate practice of

muslims from non muslims. Narrated by al-Bukhaari (1865) from Ibn „Abbaas, who said:

„‟The Prophet (saws) came to Madinah and saw the Jews fasting on the day of

Ashoora. He said, “What is this?” They said, “This is a good day, this is the day when

Allah saved the Children of Israel from their enemy and Moosa fasted on this day.” He

(the Prophet Muhammad) said, “We are closer to Moosa than you.”

So he Prophet (pbuh) fasted on this day and told the people to fast. The prophet observed

the fast on Ashuraa (the 10th of Muharram), and ordered (Muslims) to fast on that day

(Bukhari & Muslim). This is the Sunnah that is proven from the Prophet (pbuh), as he

said, “If I am still alive next year, I will certainly fast the ninth” (Narrated by Muslim,

1134). So, while jews fast only on 10th

of Muharram, prophet (pbuh) recommended

musims to fast on both 9th

and 10th

of Muharram. Riba is a practice of non muslims. So it

should not be benchmarked. Every kinds of transaction in Islamic finance should be able

to differentiate from the practice of conventional finance.

Dr, Zakir Naik, the most famous Islamic scholar of time argued that „‟ Profit rate of

islamic banking products cannot be same for all the products‟‟. In a general day to day

sale transaction we can see that profit rate of sale of computer and vegetable is not same.

Therefore Islamic banks should have a price index or profit index for different types of

products.

In a recent study by post graduate students of International Islamic university Malaysia

shows that using rental rate is better than interest rate as because it is stable and linked

with real economy. They suggested that there should be different rental index for

different areas to fix rental rate to implement ijara contract for home financing based on

Musharakah Mutanaqisah Partnership (MMP).

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 6

Impact of interest rate benchmarking on Islamic banking:

Benchmarking interest rate though does not invalidate sharia rulings but it resembles like

a conventional banking product from the outfit. That is why some critics of Islamic

banking says „‟ Islamic banking allows riba from the back door‟‟. Benchmarking interest

rate cannot completely differentiate between a Islamic products and conventional

products, hence, stakeholders loses confidence on Islamic branding. Mohammad Amin

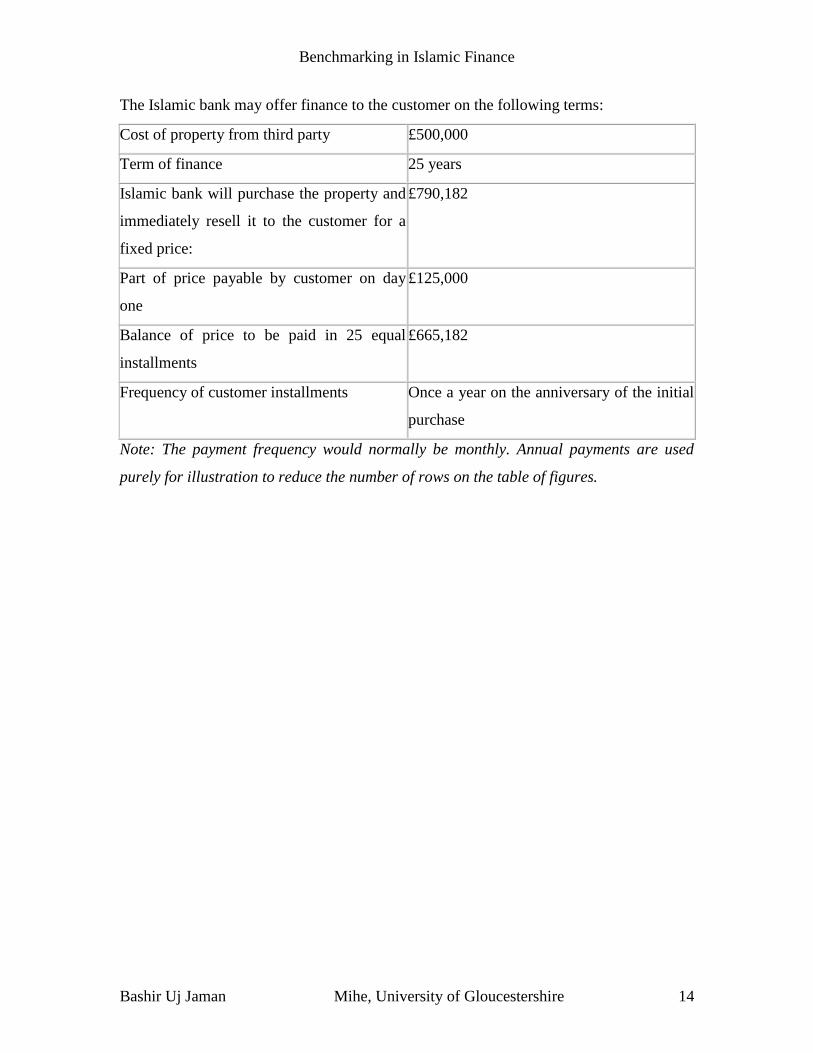

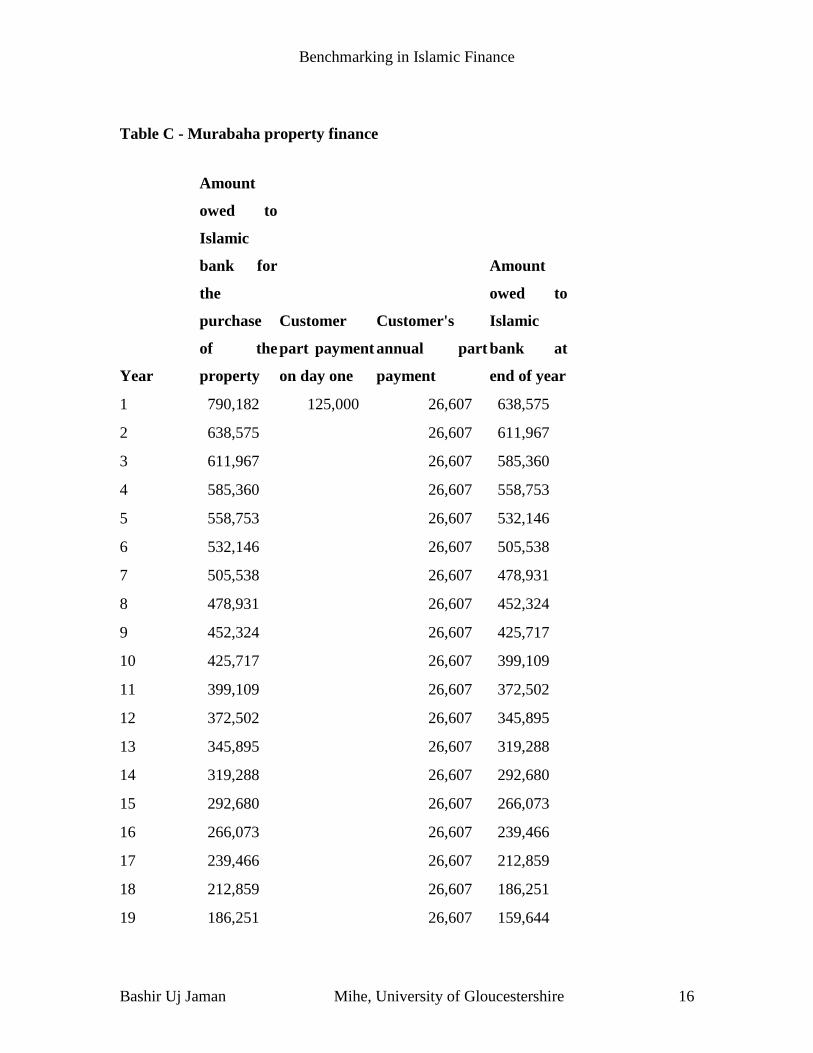

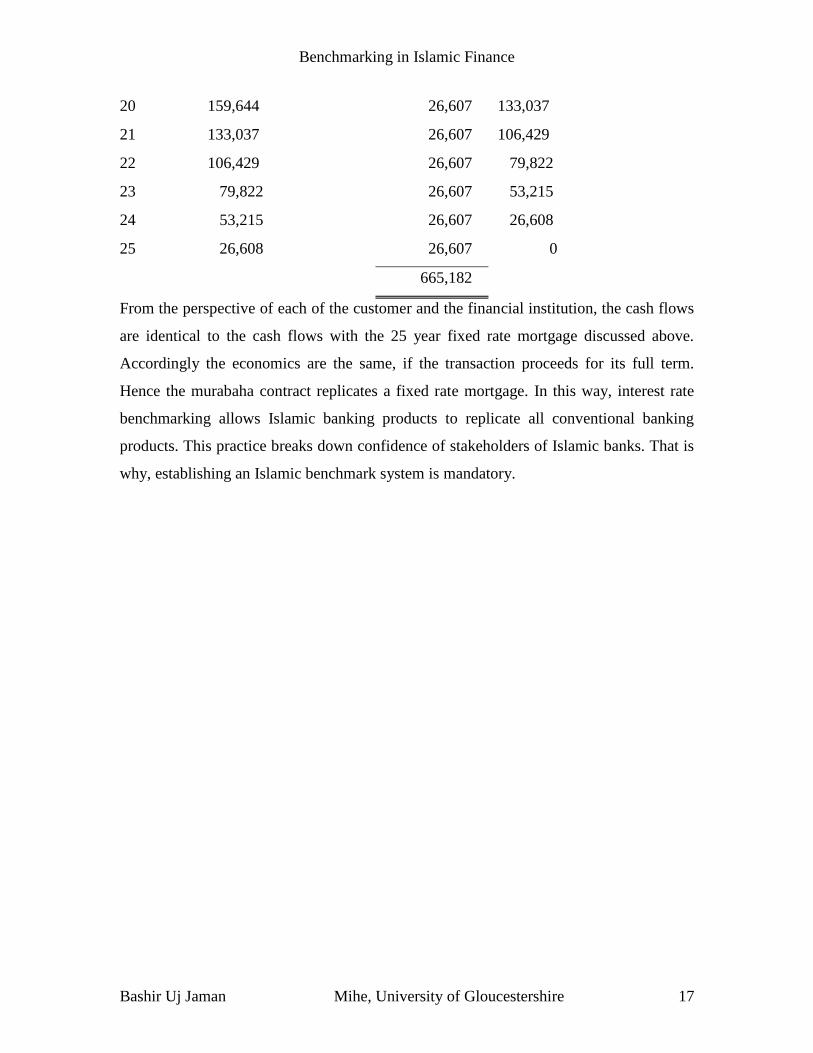

(2011) has shown how interest rate benchmarking brings same result in fixed rate

mortgage and property finance using Murabaha (Appendix A).

Criticism and obstacles of implementing Islamic benchmarking:

When Islamic benchmark is established, how can two benchmarks, interest based

conventional one and Islamic one can go parallel? Is it sustainable?

„‟A dual system which has both Islamic and conventional benchmark financing rates

could throw markets into disarray, a respected sharia scholar said, highlighting the

difficulty in creating a rate that would free Islamic banks from interest-based

markets‟‟. …Liau Y-Sing (Reuters)

Sing further added in his article that sharia adviser Aznan Hasan an advisor to Malaysia's

stock exchange Bursa Malaysia said in an interview, "If you were to have in one

country, two benchmarks -- Islamic and conventional -- together, it won't be easy for a

country to adopt the situation. People will arbitrage. Once they see conventional

financing is much better, they will go for conventional. Once they see Islamic is much

better, they will go for Islamic. In that situation, it will give a big turbulence to a

country."

In response to Abdulkader‟s (Abdulkader Thomas, president and CEO, Shape Financial

Corporation) question on the need to develop a unique Islamic benchmark, Rafe (Rafe

Haneef, head of Islamic banking, Citigroup Asia) said that as long as the Islamic product

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 7

fits within the mainstream product, there is no need to develop aunique Islamic

benchmark. “In my opinion, we could not create another benchmark for an Islamic

product that fits within the mainstream product (Sukuk is like a bond) because the

dominant benchmark will force the new benchmark to converge. This is the law of one

price in economics. However, if we change the way we structure our product (for

example, if the redemption price of Sukuk is based on market price), then the pricing

criteria would be different. We would have to look into the internal rate of return [IRR] in

that case. If we do not change the product, neither will the price,” he concluded.

...M.Faisal Panawala(date unknown)-A student of Hamdard University

Proposed alternative Islamic benchmarks:

However some efforts have been made to develop Islamic financial benchmark. The best

effort has been made by a group of the prominent academicians from Islamic university

Malaysia under supervision of ISRA (Islamic Sharia Research Academy for Islamic

Finance). In that research paper named „‟ Islamic Pricing Benchmarking’’, authors

have composed all the previous proposals on Islamic benchmark. They found mainly five

proposals:

1. Rate of Profit Mechanism Model proposed by Abd al Hamed al-Ghazalie (1414

AH): According to him, this can be achieved by analyzing the rate of profits in the money

market. He proposes that it is a more rational way that promotes justice for all and fits the

nature of economics.

2. Rate of Dividend of Islamic Bank Deposits and Investment Accounts

Model suggestion by Muhammad Abdul Halim Umar (2000): According to him, a

benchmark can be created from the dividends distributed by Islamic banks to their

depositors. It will remove uncertainty and doubt by replacing the interest rate with a rate

of profit. It will provide a mathematical index as compared to its conventional

counterpart.

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 8

3. The Creation of an Inter Islamic Banks Market Based on Islamic

Principles suggested by Shaykh Muhammad Taqi Usmani (2007). According to him, the

purpose can be achieved by creating a common pool which invests in asset-backed

instruments like musharakah, ijarah, etc. If the majority of the asset pool is in tangible

form, like leased property or equipment, shares in business concerns, etc., its units can be

sold and purchased on the basis of their net asset value determined on a periodic basis.

These units may be negotiable and may be used for overnight financing as well. Banks

having surplus liquidity can purchase these units, and when they need liquidity they can

sell them. This arrangement may create an inter-bank market, and the value of the units

may serve as an indicator for determining the profit in murabaha and leasing also.

4. Tobin’s Q Theory proposed by Abbas Mirakhor (1996). He proposes a method by

which, the cost of capital can be measured without resort to a fixed and predetermined

interest rate. The suggested procedure is simple. It is based on the well known Tobin‟s q,

and can be used in the private as well as the public sector to obtain a benchmark in

reference to which investment decisions can be made.

5. A Benchmark That Fits both Islamic and Conventional Banks by Aznan Hasan.

According to him, in Malaysia there are various ways to determine the interest rate based

on different sectors; for instance, KLIBOR, Interbank Money Market, BLR, BFR and

Overnight Policy Rate (OPR). It is possible to use the rate of OPR in line with Shariah

principles which suit both Islamic banks as well as conventional banks. It is usually

determined by BNM in order to strengthen the monetary policy as well as to control the

supply and demand and fair circulation of funds in the money market. Then, based on

that rate, the banks will determine their own respective interest rates that will be used to

price all loans and financing. Indeed, all the previously mentioned pricing rates are

affected directly by OPR, which is determined by BNM.

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 9

After analyzing all previously offered model for Islamic benchmark, ISRA research

team have tested two models based on CAPM (Capital Asset Pricing Model) and APT

(The Arbitrage Pricing Theory). After examining both models with different theory of

economics, they found some limitation of CAPM model. With the objective of linking

benchmark with real economic performances, they proposed APT model for Islamic

benchmark. Their study recognized four macroeconomic variables as having good return

predictability for all the sectors: industry production growth, to capture the overall

economic growth; the money supply changes (M2), to capture the monetary liquidity; the

ringgit exchange rate, to reflect the relative global competitiveness; and the Kuala

Lumpur Composite Index returns, to reflect the overall market condition. A weighted

average of the sector‟s returns determined through the APT is suggested here as a viable

Islamic pricing benchmark rate for the market as a whole.

From the above discussion, it is seen that criticizing Islamic finance for benchmarking

interest rate is easy but in practice, there are many limitations in findings an alternative of

it. Many researches have been done on this issue, but still Islamic finance is waiting for

viable solution. There is no do doubt that Islamic finance should get rid of this criticism

as early as possible. Hopefully, with the maturity of Islamic finance better suggestions

will come in future.

Benchmarking in Islamic Finance

Bashir Uj Jaman Mihe, University of Gloucestershire 10

References:

Ali, R. et al (date unavailable),‘’ Islamic Benchmarking- An alternative to interest rate’’

(Evidence from Home Financing in Malaysia), International Islamic university Malaysia.

Available at: http://www.cba.edu.kw/wtou/download/conf4/Ali.pdf. [Accessed on 5th

June, 2011].

Amin, M. (2011) „A simple introduction to Islamic mortgages’; Available at