Page 1

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

99 | P a g e

Chapter 4 Data Analysis and Interpretation

4.1 Introduction

This chapter is dedicated to present the data analysis and interpretation for FIIs

investments and Indian stock index. Researcher has used secondary data for this present

study. There are two variables employed for data which are FIIs investments activities

consists with FIIs purchase, FIIs sales and FIIs net investments, Indian stock indexes

define BSE SENSEX and NIFTY50.

There are different kind of statistical tools used for analysis the data and interpret the

results. Here researcher has used descriptive statistical tools; mean, median, standard

deviation, standard error, coefficient variances, range, skewness and kurtosis for the

proper analysis study objectives.

Besides, Coefficient correlation (r), coefficient determination R2, and adjusted R2

employed for quantify the effects and association between Indian stock indexes and FIIs

investments. These tools used for find propositional effects and degree of correlation

between BSE SENSEX, NIFTY and FIIs investments activities; purchase, sales, net for

the 10 years.

Moreover, researcher has used regression residual analysis model for wrap the objective

that to come across effect of FIIs investments on the Indian stock market. The regression

analysis predicts the performance of Indian stock index SENSEX and nifty due to FIIs

purchase trend for the year 2003 to year 2012. The regression equation of the regression

model is presented cause and effect relationship between Indian stock indexes and FIIs

investments. There is hypothesis developed and tested in order to achieve objectives

toward role of FIIs on Indian stock market. Researcher has applied t-test for significant

predictive variables FIIs activities on Indian stock index and F-test to determine the

overall significance of the regression model. Subsequent, there are different section

employed for proper analysis and interpret results which are as follow:

Page 2

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

100 | P a g e

4.2 Trend analysis of BSE SENSEX & NIFTY with respect to descriptive statisticaltools

Researcher conducted trend analysis for BSE SENSEX & NIFTY. Researcher has

calculated daily average value of BSE SENSEX and NIFTY50 for the year 2003 to 2012.

Descriptive statistical analysis is conducted to define the effect of changing values on

measures of central tendency, variation and shape. The descriptive statistical tools

calculated for measurement of BSE SENSEX and NIFTY 50. This assists to define some

initiative for BSE SENSEX and NIFTY 50.

Table 4.1 Trend of average BSE SENSEX & NIFTY50

YearAverage of

BSE SENSEX INDEXAverage of

NIFTY50 INDEX

2003 3872.97 1233.71

2004 5563.09 1755.87

2005 7392.89 2268.91

2006 11440.04 3357.09

2007 15563.60 4571.29

2008 14492.68 4339.11

2009 13700.82 4113.96

2010 18206.91 5461.12

2011 17777.77 5335.91

2012 17617.04 5343.77

The above table shows daily average value of BSE SENSEX index and NIFTY50 index

for the year 2003 to 2012, the value of table present the chart for average value on

different plot which are exhibited in following chart 4.1:

Page 3

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

101 | P a g e

The above chart 4.1 and tables 4.1 show the average value of BSE SENSEX and

NIFTY50, the data represent for the 10 years start from 2003 to year 2012.

The average value of BSE SEBSEX shows that there was continuously positive trend for

the year 2003 to year 2007, Thus, Average of BSE SENSEX increased from 3872.97 to

4571.29 points which show the bull trends during this tenure. After that there was

declined trend for the year 2008 and 2009 due to global crisis. Market reached average

BSE SENSEX point 14492.68 and 13700.82 for the year 2008 and 2009 respectively. At

last, there was best performance of BSE SENSEX during the year 2010. In the contrary,

BSE SENSEX little bit declined and touched average point 17777.77 and 17617.04 for

the year 2011 to 2012. Thus, It terminated that performance of BSE SENSEX was good

and positive trend during the 2003 to year 2012.

Page 4

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

102 | P a g e

The average value of NIFTY50 presented that there was continuously positive trend for

the year 2003 to 2007, thus, Average of NIFTY50 increased from 1233.71 to 15563.60

points which proved the bull trends during these years. Subsequently there was declined

trend for the year 2008 and 2009 due to global crisis. Market contacted average NIFTY50

points 4339.11 and 4113.96 for the year 2008 and 2009 respectively. At last, there was

best performance of NIFTY50 during the year 2010 which shows that NIFTY50 slightly

declined and faced average point 5335.91 and 5343.77 for the year 2011 to 2012.

Consequently, It fulfilled that performance of NIFTY50 was excellent and encouraging

trend during the 2003 to year 2012.

Researcher has used descriptive statistical tools; mean, median, standard deviation,

standard error, coefficient variances, range, skewness and kurtosis for execute the

objectives of research study. Following calculation made by the researcher:

Page 5

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

103 | P a g e

Table 4.2 Analysis of descriptive statistical Average BSE SENSEX and NIFTY 50

Descriptive statistical tools BSE SENSEX NIFTY 50

Mean 12562.78 3778.08

Standard Error 1670.39 492.00

Median 14096.75 4226.54

Coefficient of variance% 41.18 41.18

Standard Deviation 5282.25 1555.84

Kurtosis -1.17 -1.20

Skewness -0.61 -0.56

Range 14333.94 4227.42

Minimum 3872.97 1233.71

Maximum 18206.91 5461.12

Year 2003 to 2012 10 10

The above descriptive statistical tools deliberated for average BSE SENSEX and

NIFTY50, for the year 2003 to year 2012.

BSE SENSEX has an average valued by 12562.78. It is deviated from mean value by

5282.25 in both surfaces. Standard error of BSE SENSEX is 1670.39. The average value

of NIFTY 50 is 3778.08 and standard deviation is 1555.84which indicates that mean

move away from mean value by 1555.84.The coefficient of variation measures the

variation that is expressed as percentage. The coefficient of variation of average BSE

SENSEX and NIFTY50 has equal value 41.18%.

Page 6

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

104 | P a g e

Median 14096.75 shows middle value in BSE SENSEX index that has been ordered from

lowest to highest value for the year 2003 to 2010. NIFTY 50 has 4226.54 middle values

that have been ordered from lowest to highest value for the year 2003 to 2012. BSE

SENSEX has wider range 14333.94 which defines from the average minimum index year

2003 and maximum index year 2010 is 3872.97 and 18206.91 respectively. The wider

range 14333.94 shows extremely volatility in the BSE SENSEX index during the year

2003 to year 2012.

Skewness and kurtosis use for the measure the normality of the data. BSE SENSEX and

NIFTY 50 have value by -0.61 and -0.56 correspondingly which shows that the

distribution is negative skewed. The average BSE SENSEX 12562.78 and 3778.08 is

lower than middle value of BSE SENSEX 14096.75 and NIFTY 50 4226.54. Kurtosis of

BSE SENSEX and NIFTY 50 has value by -1.17 and -1.20 correspondingly which is less

than 3. It means the distribution is platykurtic, so in this distribution quartile range is

preferred rather than mean

4.3 Trend analysis of FIIs activities; FIIs purchases, FIIs sales, FIIs net investmentswith respect to descriptive statistical tools

Researcher carried out trend analysis for FIIs activities; FIIs purchases, FIIs sales.

Researcher has calculated daily average investment of FIIs activities; FIIs purchases, FIIs

sales, FIIs net investments for the year 2003 to 2012. Descriptive statistical analysis is

employed to define the effect of varying values on measures of central tendency, disparity

and shape. The descriptive statistical tools calculated for measurement of FIIs activities;

FIIs purchases, FIIs sales.

Page 7

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

105 | P a g e

Table 4.3

Trend analysis of FIIs activities; FIIs purchases, FIIs sales, FIIs net investments

Amount in cr.

Year Average GrossPurchase

Average GrossSales

Average NetInvestments

2003 377.75 255.08 122.68

2004 735.53 580.74 154.79

2005 1135.45 948.48 186.97

2006 1854.49 1721.38 133.11

2007 3327.14 3034.00 293.14

2008 2953.93 3171.35 -217.43

2009 2597.53 2243.31 354.22

2010 3123.59 2577.69 571.13

2011 2554.98 2570.29 -15.30

2012 2777.61 2262.60 515.01

Page 8

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

106 | P a g e

The above chart 4.3 and tables 4.3 state the average FIIs purchases for the 10 years start

from year 2003 to 2012. There was large amount of FIIs sales 3171.35cr in the year 2008.

Same as in the year 2007, FIIs have sold 3034cr. securities in Indian stock market.

Remain all years FIIs sales continuously increase trend shows FIIs take off huge amount

capital from the Indian stock market last five years. Moreover, FIIs purchase also

increased with FIIs sales consequently, FIIs capital flow positive trend except year 2008

and year 2011 respectively.

The above chart 4.4 and table 4.3 disclosed the average FIIs sales for the 10 years start

from year 2003 to 2012.

The table value demonstrates that there was continuously optimistic trend for the year

2003 to 2007, thus, FIIs has purchased stock rs. 377.75 cr in the year 2003 than after

enhanced to 3327.14 cr. in the year 2007. The value shows that interest of FIIs optimistic

during these years. There was declined trend for the year 2008 and 2009 due to global

crisis. FIIs purchase was decreased to 2953.93 cr and 2597.53 cr. for the year 2008 and

2009 respectively.

Page 9

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

107 | P a g e

Besides, FIIs investment was increased to 3123.59 cr amount for the year 2010. In the

contrary, BSE SENSEX little bit declined and touched average point 2554.98 cr and

2777.61 cr for the year 2011 to 2012. Thus, last five years data indicates that interest of

foreign institutional investors superior toward Indian stock market.

The above chart 4.5 and table 4.3 show the average FIIs net investments consists with

FIIs purchases and FIIs sales for year 2003 to 2012.

FIIs net investments having upward trend for the year 2003 to year 2007. There was

negative FIIs net investments -217 cr. it presents huge sales of FIIs over FIIs purchases.

This data shows that huge sales trend of FIIs investments in Indian stock markets.

Moreover, there was negative net investments average -15.30 cr. FIIs net investments

was uppermost 571.13 cr in the year 2010 which shows FIIs purchase was excess over

FIIs sales. Same way, in the year 2012, FIIs have optimum net investments 515.01cr.

Page 10

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

108 | P a g e

Table 4.4 Analysis of descriptive statistical for average FIIs Investments activities

Descriptive statistical toolsFIIs Investments (cr.)

Purchases Sales Net

Mean 2143.80 1936.49 209.83

Standard Error 333.26 323.70 74.66

Median 2576.26 2252.96 170.88

Coefficient of variance% 49.16 52.86 112.52

Standard Deviation 1053.87 1023.63 236.11

Kurtosis -1.11 -1.07 0.03

Skewness -0.69 -0.57 -0.12

Range 2949.38 2916.27 788.55

Minimum 377.75 255.08 -217.43

Maximum 3327.14 3171.35 571.13

Year 2003 to 2012 10 10 10

The above descriptive statistical tools calculated for average FIIs purchase, sales and net

investments for the year 2003 to 2012.

The average value of FIIs investments activities purchase, sales and net is 2143.80 cr.

1936.49 cr. 209.83 cr. respectively. Its deviation defines through the standard deviation.

Standard deviation of average value of FIIs investments activities purchase, sales and net

is 1053.87 cr., 1023.63cr. 236.11cr. which diverged from the average from mean value in

both side. FIIs investments activities purchase, sales and net has standard error value of

333.26, 323.70 and74.66 respectively.

Page 11

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

109 | P a g e

FIIs purchase and FIIs sales are 49.16% and 52.86% which reveals that there is no huge

variation in FIIs purchase and FIIs sales during the year 2003 to year 2012, in the

contrary FIIs net having 112.52% coefficient of variation shows variation among the FIIs

purchase and FIIs sales during the year 2003 to year 2012.

FIIs purchase, FIIs sales and FIIs net investments have Median 2576.26cr, 2252.96cr,

170.88cr respectively which shows middle value in FIIs investments that has been

ordered from lowest to highest value for the year 2003 to year 2012.

FIIs purchase has 2948.38 wider ranges which define from the average minimum index

year 2003 and maximum index year 2010 is 377.75 and 3327.14 respectively. FIIs sales

has 2916.17 broad range which measures from the average minimum index year 2003 and

maximum index year 2010 is 255.08 and 3171.35 respectively. The ample range indicates

tremendously vary FIIs investment during the year 2003 to 2012.

Skewness and kurtosis use for the measure the normality of the data. For the year 2003 to

year 2012 FIIs purchase, sales and net investments have value -0.69, -0.57, -0.12

respectively which evidence that the distribution is negative skewed. The mean of FIIs

investments are lower than middle value. Kurtosis of FIIs purchase, sales and net

investments have -1.11, -1.07 and 0.03 respectively which is less than 3. It means the

distribution is platy-kurtic, so in this distribution quartile range is preferred rather than

mean

4.4 Analysis of regression residual model for FIIs investments activities and BSESENSEX

Regression model employed for measure the significance effect of independent variable

FIIs Investments activities on dependent variables Indian stock index; BSE SENSEX and

NIFTY50. Following different section shows the analysis of regression residual analysis

for FIIs investments activities and Indian stock indexes.

4.4.1 Regression model residual analysis for BSE SENSEX and FIIs purchase

The regression analysis predicts the SENSEX index due to FIIs purchase trend. The

regression equation of the regression model is presented in relationship between SENSEX

indexes due to FIIs purchases.

Page 12

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

110 | P a g e

Table 4.5

Coefficient of correlation and determination for BSE SENSEX and FIIs purchases

Coefficient correlation r 0.94

R Square 0.89

Adjusted R Square 0.88

Standard Error 1862.96

Observations 10

The correlation between BSE SENSEX index and FIIs purchase is r = 0.94 which shows

positive high degree of correlation between BSE SENSEX index and FIIs purchase. The

coefficient of determination is 0.88 in other word 88% of the volatility in the BSE

SENSEX index due to the variation in the FIIs purchase. This result shows that 0.12 or

12% of the changes due to the other factors other than FIIs purchase. A comparison of R2

0.88 with the adjusted R2 0.86 shows that the adjusted R2 reduced the overall proportion

of variation of the dependent variable accounted for by the independent variables by a

factor of 0.02 by 2%.

It concluded that FIIs purchase highly influenced on volatility of BSE SENSEX. The gap

between R2 and the adjusted R2 tends to increase as non significant independent variables

are added to the regression model. Standard error measures not only the size of chance

error that has been made but also the amount by which the regressed values away from

the actual values. Here larger standard error 1862.96 indicates a huge quantity of

variation or scatter around the regression line which constructed in chart 4.6.

Distributions of sample mean that wide spread is a better estimator of the population

mean than a distribution of sample mean.

Regression model line

Ŷ = α + βx

Ŷ = 2428.99 + 4.73 X

Page 13

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

111 | P a g e

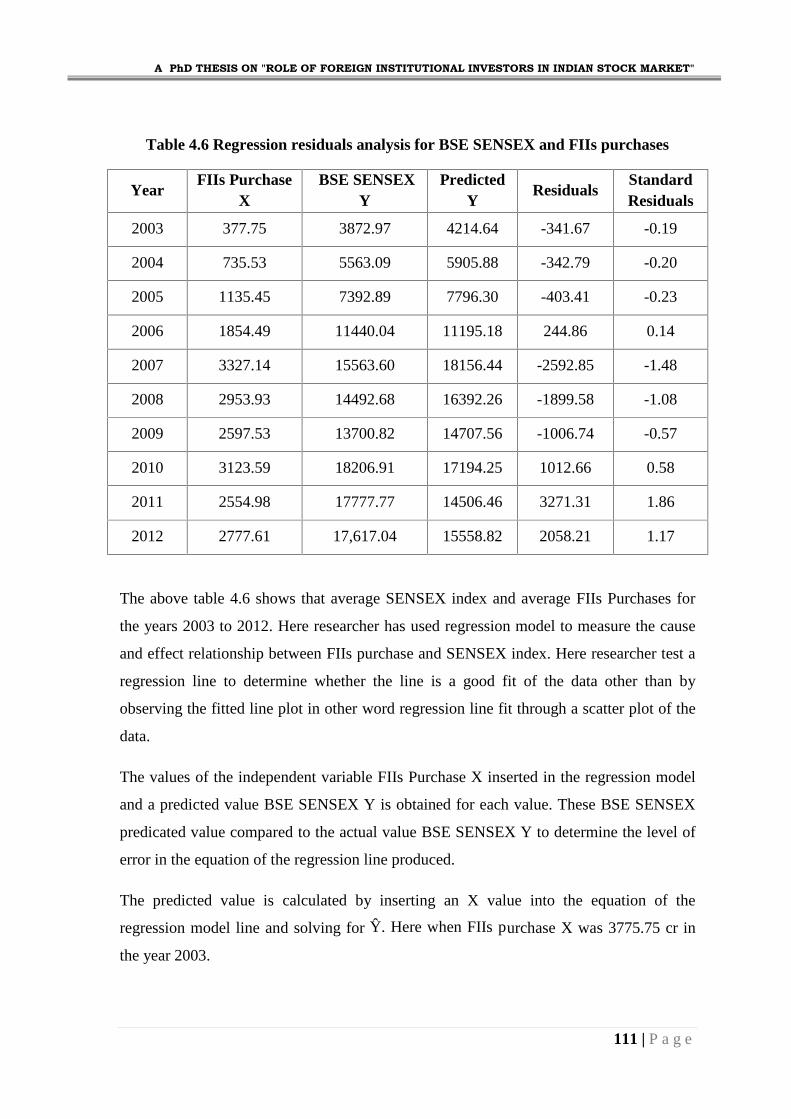

Table 4.6 Regression residuals analysis for BSE SENSEX and FIIs purchases

YearFIIs Purchase

XBSE SENSEX

YPredicted

YResiduals

StandardResiduals

2003 377.75 3872.97 4214.64 -341.67 -0.19

2004 735.53 5563.09 5905.88 -342.79 -0.20

2005 1135.45 7392.89 7796.30 -403.41 -0.23

2006 1854.49 11440.04 11195.18 244.86 0.14

2007 3327.14 15563.60 18156.44 -2592.85 -1.48

2008 2953.93 14492.68 16392.26 -1899.58 -1.08

2009 2597.53 13700.82 14707.56 -1006.74 -0.57

2010 3123.59 18206.91 17194.25 1012.66 0.58

2011 2554.98 17777.77 14506.46 3271.31 1.86

2012 2777.61 17,617.04 15558.82 2058.21 1.17

The above table 4.6 shows that average SENSEX index and average FIIs Purchases for

the years 2003 to 2012. Here researcher has used regression model to measure the cause

and effect relationship between FIIs purchase and SENSEX index. Here researcher test a

regression line to determine whether the line is a good fit of the data other than by

observing the fitted line plot in other word regression line fit through a scatter plot of the

data.

The values of the independent variable FIIs Purchase X inserted in the regression model

and a predicted value BSE SENSEX Y is obtained for each value. These BSE SENSEX

predicated value compared to the actual value BSE SENSEX Y to determine the level of

error in the equation of the regression line produced.

The predicted value is calculated by inserting an X value into the equation of the

regression model line and solving for Ŷ. Here when FIIs purchase X was 3775.75 cr in

the year 2003.

Page 14

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

112 | P a g e

The values of X fill in the regression model line

Ŷ = 2428.99 + 4.73 X,

Ŷ = 2428.99 + 4.73 (3775.75)

Ŷ = 4214.64 for the year 2003

As exhibit in 4th column of the above table 4.6, remain all year predicted value calculated

as per above calculation. The predicted values are calculated by inserting an X values in

to equation. Each predicted value BSE SENSEX Y value is subtracted from the actual Y

to determine the error, for the year 2003 residual value was 3872.97 - 42147.64 = -

341.67. Each different between the actual values and the predicated Y values is the error

of the regression line at a given point is referred to as residual value which given in the 5th

column. Residual gives the idea of how well the regression line fits the historical data

points.

The largest residual for the BSE SENSEX was 3271.31 in the year 2011 and smallest

residual was -341.67 in the year 2003. The regression line produces an error of 3271.31

point BSE SENSEX when there are 2554.98 cr FIIs purchase in the year 2011. There was

smallest error -341.67 when FIIs purchase 377.75 cr. in the year 2003. This result

presents the best and worst, bull or bear market performance. Other residuals determine

different BSE SENSEX market trend due to change in FIIs purchase for remaining time

period.

The residuals versus the fitted values graph indicate that the residuals seem to increase as

X increases, indicating a potential problem with different factors.

Page 15

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

113 | P a g e

Chart 4.6 Scatter Plots Of FIIs Purchases And BSE SENSEX

F-test : Test to determine the overall significance of the regression model

This F-test determines weather regression coefficients are different from zero. Regression

provides only one predictor and only one regression coefficient test. The regression

coefficient is the slop of the regression line, the F-test for overall significance is testing

the same thing as the t-test in regression. The hypotheses being tested in simple

regression by the F-test for overall significance are as follow:

Null H0 : β = 0

Alt H1 : β ≠ 0

OR

Null H0 : there is at least one of the regression coefficients is zero

Alt H1 : there is at least one of the regression coefficients is different from zero

Page 16

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

114 | P a g e

Table 4.7 F-test for regression coefficients of FIIs Purchase and BSE SENSEX

DF SS MS F Significance F

Regression 1 223354193.40 223354193.40 64.36 0.00001

Residual 8 27764925.20 3470615.65

The above table 4.7 shows the F-test for testing that value of coefficients for the FIIs

Purchase and BSE SENSEX. The values of sum of squares (SS), degree of freedom (df),

and mean squares (MS) are obtained from the analysis of variance table, which is

produced with other regression statistics as standard output from statistical calculation,

above shown table is F test value for the BSE SENSEX index. F-test table, the degree of

freedom is equal to 1. Here regression models have only one independent variable FIIs

purchase for BSE SENSEX, therefore the degree of freedom error in regression analysis

is n – 1 – 1 = n – 2.

The difference between F value = 64.36 and the value obtained by squaring the t-value

(8.02)2 = 64.32 is (0.04) incurred due to error. The probability of obtaining an F value this

large by chance if there is no regression prediction in the regression model is 0.00001

according to F test. The value of F for this is 64.36 with a p-value 0.00001 which is not

significant at 5% level (0.00001< 0.05). This output value means it is highly unlikely that

the population slope is zero and there is no prediction due to regression from this model

given the sample statics obtained. Hence, it is highly likely that this regression molded

adds significant predictability of the dependent variable BSE SENSEX.

On the base of this result, the null hypothesis would not be rejected for the overall test of

significance. None of the regression coefficients are significantly different from zero, and

no significant predictability of the volatility of SENSEX Index by the FIIs Purchases

given from this regression model.

Regression model line : Ŷ = 2428.99 + 4.73 X

Page 17

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

115 | P a g e

A slope of 4.73 indicates that there is a positive upward trend of BSE SENSEX and FIIs

Purchases over this period year 2003 to 2012 at a 4.73cr. The Y intercept of 2428.99

represents what the regression model trend line would estimate the BSE SENSEX to have

been in 10 years.

t-test for significant predictive variables FIIs investments on BSE SENSEX

This test is determined how well a regression model fits the data. Here researcher decides

that it is not worth the effort to develop a linear regression model to predict BSE

SENSEX (Y) from FIIs investments. An alternative approach might be to average the

INDEX (Y) values and use Ŷ as the predictor of y for all values of FIIs X values.

Null H0 : β = 0

Alt H1 : β > 0

OR

Null H0 : There is no relationship between FIIs Purchase and BSE SENSEX

Alt H1 : There is positive relationship between FIIs Purchase and BSE SENSEX

Table 4.8 t-test for relationship between FIIs Purchase and BSE SENSEX

CoefficientsStandard

Errort Stat P-value

Lower95%

Upper95%

Intercept (Y) 2428.99 1393.84 1.74 0.12 -785.21 5643.18

FIIs Purchase (X) 4.73 0.59 8.02 0.00 3.37 6.09

An examination of the t test supports this result using at 5% significant level. The t value

calculated from the sample slop fall in the rejection region and the p–value is 0.0001 for

FIIs purchase. Where, p-value is less than significant level 0.05 (0.0001 < 0.05). So, the

null hypothesis that populations slope is zero rejected. That the t statistic value for testing

to determine if the slope is significantly different from zero is 8.02 with a p-value of

0.0001. This linear regression model is adding significantly more predictive variable to

the BSE SEBSEX variable Y. It shows that SENSEX index significantly more analytical

variable by FIIs purchase. It is desirable to reject the null hypothesis in testing the slope

of the regression model. In rejecting the null hypothesis of a zero population slope, so the

regression model is adding something to the explanation of the variation of the dependent

Page 18

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

116 | P a g e

variable BSE SENSEX that the average value of Y model does not failure to reject the

null hypothesis in this test causes the researcher to conclude that the regression model has

no predictability of the dependent variable BSE SENSEX, and the model, therefore, has

little use. The standard error of the model Se = 1862.96 indicate that if the error terms are

approximately normally distributed, about 89% of the predicted BSE SENSEX index fall

with +1862.96 to -1862.96.

4.4.2 Regression model residual analysis for BSE SENSEX and FIIs sales

The regression analysis predicts the SENSEX index due to FIIs sales trend. The

regression equation of the regression model is presented in relationship between SENSEX

index and FIIs sales.

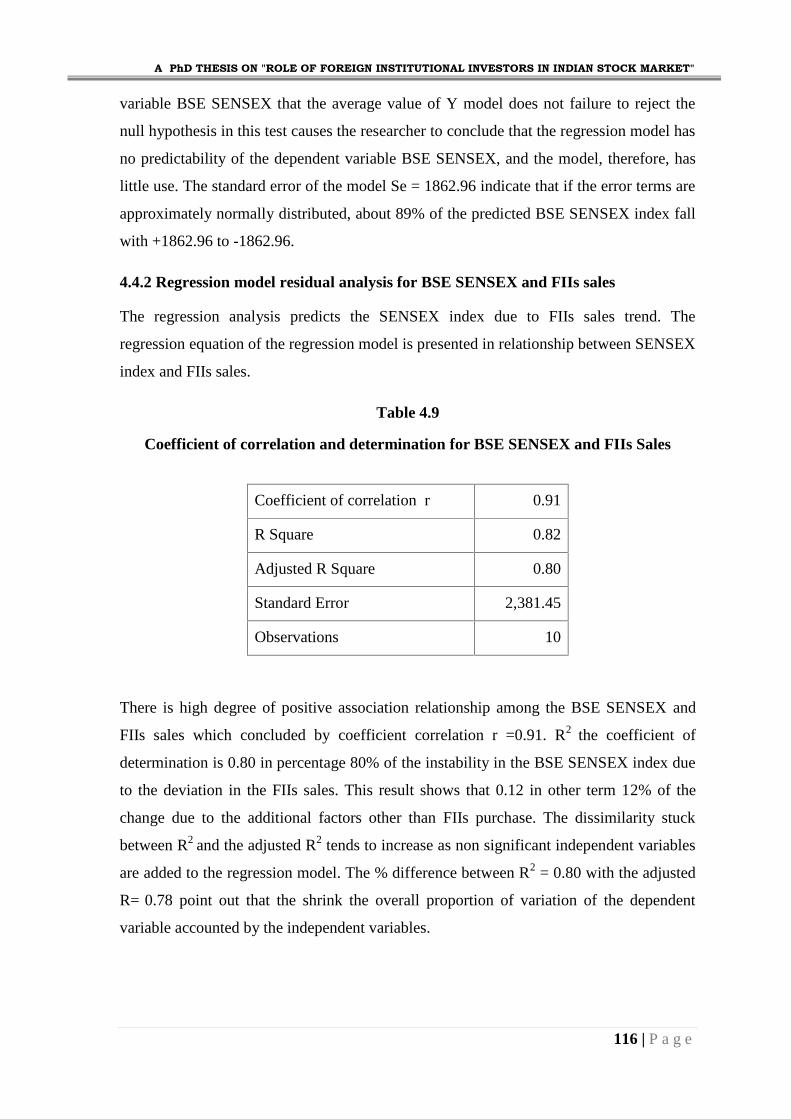

Table 4.9

Coefficient of correlation and determination for BSE SENSEX and FIIs Sales

Coefficient of correlation r 0.91

R Square 0.82

Adjusted R Square 0.80

Standard Error 2,381.45

Observations 10

There is high degree of positive association relationship among the BSE SENSEX and

FIIs sales which concluded by coefficient correlation r =0.91. R2 the coefficient of

determination is 0.80 in percentage 80% of the instability in the BSE SENSEX index due

to the deviation in the FIIs sales. This result shows that 0.12 in other term 12% of the

change due to the additional factors other than FIIs purchase. The dissimilarity stuck

between R2 and the adjusted R2 tends to increase as non significant independent variables

are added to the regression model. The % difference between R2 = 0.80 with the adjusted

R= 0.78 point out that the shrink the overall proportion of variation of the dependent

variable accounted by the independent variables.

Page 19

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

117 | P a g e

In short, It can be summarised that increase in change of FIIs sales trend which increase

the BSE SENSEX. Here larger standard error 2381.45 point toward a bulky amount of

variation or scatter around the regression line. Distributions of sample mean that wide

stretch is a enhanced estimator of the population mean than a distribution of sample mean

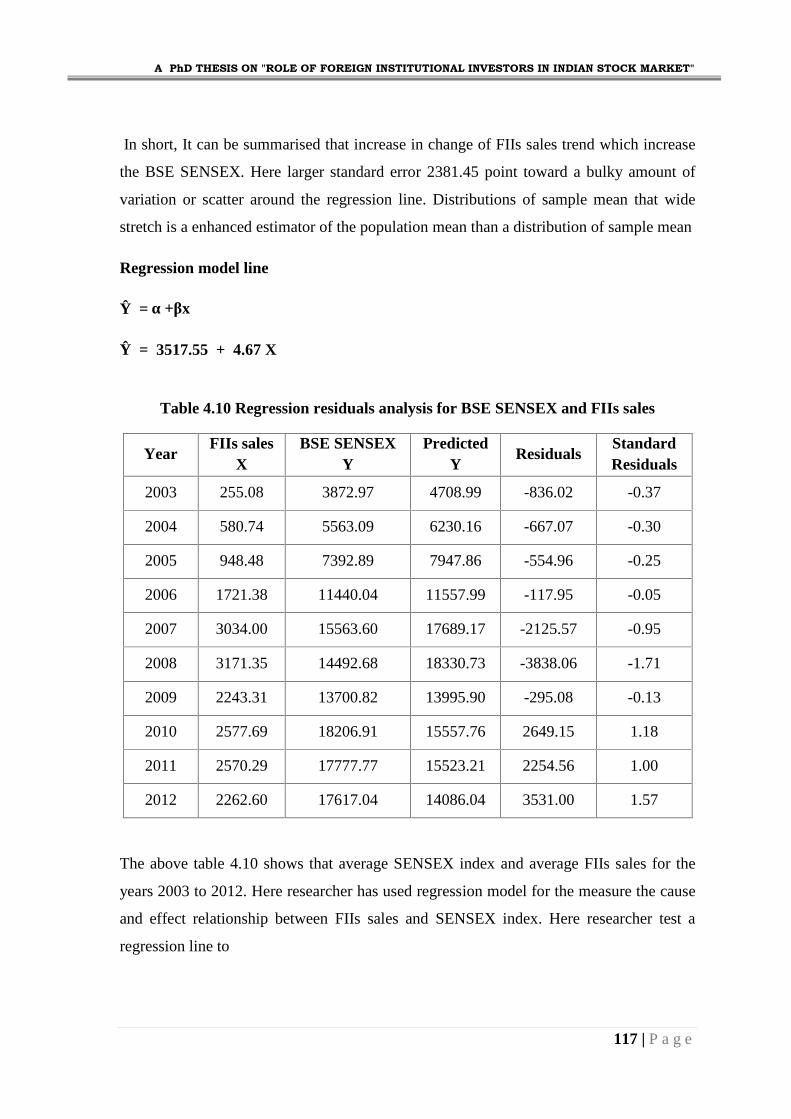

Regression model line

Ŷ = α +βx

Ŷ = 3517.55 + 4.67 X

Table 4.10 Regression residuals analysis for BSE SENSEX and FIIs sales

YearFIIs sales

XBSE SENSEX

YPredicted

YResiduals

StandardResiduals

2003 255.08 3872.97 4708.99 -836.02 -0.37

2004 580.74 5563.09 6230.16 -667.07 -0.30

2005 948.48 7392.89 7947.86 -554.96 -0.25

2006 1721.38 11440.04 11557.99 -117.95 -0.05

2007 3034.00 15563.60 17689.17 -2125.57 -0.95

2008 3171.35 14492.68 18330.73 -3838.06 -1.71

2009 2243.31 13700.82 13995.90 -295.08 -0.13

2010 2577.69 18206.91 15557.76 2649.15 1.18

2011 2570.29 17777.77 15523.21 2254.56 1.00

2012 2262.60 17617.04 14086.04 3531.00 1.57

The above table 4.10 shows that average SENSEX index and average FIIs sales for the

years 2003 to 2012. Here researcher has used regression model for the measure the cause

and effect relationship between FIIs sales and SENSEX index. Here researcher test a

regression line to

Page 20

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

118 | P a g e

determine whether the line is a good fit of the data other than by observing the fitted line

plot in other word regression line fit through a scatter plot of the data.

The value of the independent variable FIIs sales X inserted in the regression model and a

predicted value BSE SENSEX (Y) are obtained for each value. These BSE SENSEX

predicated value compared to the actual value BSE SENSEX (Y) to determine how much

error the equation of the regression line produced. Each different between the actual

values and the predicated Y values is the error of the regression line at a given point is

referred to as residual value which given in the 5th column. Residual gives the idea of how

well the regression line fits the historical data points.

The regression model fits these particular data SENSEX index and FIIs sales well for the

year 2006 and 2009, as indicated by residuals of -117.95 and -295.08 at standard residual

-0.05 and -0.13 BSE SENSEX, correspondingly, for remaining years the residuals are

relatively large, indicating that the regression model does not fit the data for these years.

The residuals versus the fitted values graph indicate that the residuals seem to increase as

FIIs sales X increases, indicating a potential problem with vary.

Page 21

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

119 | P a g e

Chart 4.7 Scatter Plots Of FIIs Sales And BSE SENSEX

F-test : Test to determine the overall significance of the regression model

This F-test establishes weather regression coefficients are different from zero. Regression

provides only one predictor and only one regression coefficient test. The regression

coefficient is the slop of the regression line, the F-test for overall significance is testing

the same thing as the t-test in regression. The hypotheses being tested in simple

regression by the F-test for overall significance are as follow:

Null H0 : β = 0

Alt H1 : β ≠ 0

OR

Null H0 : there is at least one of the regression coefficients is zero

Alt H1 : there is at least one of the regression coefficients is different from zero

Page 22

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

120 | P a g e

Table 4.11 F-test for regression coefficients of FIIs sales and BSE SENSEX

df SS MS F Significance F

Regression 1 205748504.39 205748504.39 36.28 0.00001

Residual 8 45370614.21 5671326.78

The above F-test table 4.11 shows the F-test for regression coefficients of FIIs Purchase

and BSE SENSEX. The values of sum of squares (SS), degree of freedom (df), and mean

squares (MS) are obtained from the analysis of variance table, which is produced with

other egression statistics as standard output from statistical calculation, above shown table

is F test value for the BSE SENSEX index. F-test table, the degree of freedom is equal to

1. Here regression models have only one independent variable FIIs purchase for BSE

SENSEX, therefore the degree of freedom error in regression analysis is n – 1 – 1 = n –

2.

The difference between F value = 36.28 and the value obtained by squaring the t-value

(6.02)2 = 36.24 is (0.04) incurred due to error. The probability of obtaining an F value this

large by chance if there is no regression prediction in the regression model is 0.0001

according to F test. The value of F for this is 56.56 with a p-value 0.0001 which is not

significant at 5% level (0.00001< 0.05). This output value means it is highly unlikely that

the population slope is zero and there is no prediction due to regression from this model

given the sample statics obtained. Hence, it is highly likely that this regression molded

adds significant predictability of the dependent variable.

Consequently, the null hypothesis would not be rejected for the overall test of

significance. None of the regression coefficients are significantly different from zero, and

no significant predictability of the volatility of BSE SENSEX by the FIIs Purchases given

from this regression model.

Regression model line: Ŷ = 3517.55+ 4.67X

Page 23

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

121 | P a g e

This regression line shows that a slope of 4.67 indicates that there is a encouraging

upward trend of BSE SENSEX and FIIs Purchases over this period year 2003 to 2012 at a

4.67cr. The BSE SENSEX Y intercept of 3517.55 represents what the regression model

trend line would estimate the BSE SENSEX to have been in 10 years.

t-test for significant predictive variables FIIs investments on BSE SENSEX

This t-test is determined how well a regression model fits the data. Here researcher

makes a decision that it is not worth the effort to develop a linear regression model to

forecast BSE SENSEX (Y) from FIIs investments. An alternative approach might be to

average the BSE SENSEX (Y) values and use Ŷ as the predictor of y for all values of FIIs

X values.

Null H0 : β = 0

Alt H1 : β > 0

OR

Null H0 : There is no relationship between FIIs sales and BSE SENSEX

Alt H1 : There is positive relationship between FIIs sales and BSE SENSEX

Table 4.12 t-test for relationship between FIIs Sales and BSE SENSEX

CoefficientsStandard

Errort Stat P-value

Lower95%

Upper95%

Intercept (Y) 3517.55 1679.98 2.09 0.07 -356.50 7391.60

FIIs sales (X) 4.67 0.78 6.02 0.00 2.88 6.46

An examination of the t test supports this result using at 5% significant level. The t value

calculated from the sample slop fall in the rejection region and the p – value is 0.00001

for FIIs sales respectively where p-value is less than significant level 0.05 (0.00001 <

0.05). So, the null hypothesis that populations slope is zero rejected. This linear

regression model is adding significantly more predictive variable to the BSE SEBSEX

variable Y. It shows that SENSEX index significantly more analytical variable by FIIs

sales. It is desirable to reject the null hypothesis in testing the slope of the regression

model. In rejecting the null hypothesis of a zero population slope, so the regression model

Page 24

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

122 | P a g e

is adding something to the explanation of the variation of the dependent variable BSE

SENSEX that the average value of Y model does not failure to reject the null hypothesis

in this test causes the researcher to conclude that the regression model has no

predictability of the dependent variable BSE SENSEX, and the model, therefore, has little

use.

In rejecting the null hypothesis of a zero population slope, so the regression model is

adding something to the explanation of the variation of the dependent variable BSE

SENSEX that the average value of Y model does not failure to reject the null hypothesis

in this test causes the researcher to conclude that the regression model has no

predictability of the dependent variable BSE SENSEX, and the model, therefore, has little

use. The standard error of the model Se = 2381.45 designate that if the error terms are

approximately normally distributed, about 88% of the predicted BSE SENSEX index fall

with +2381.45 points to -2381.45 points.

4.4.3 Regression model residual analysis for BSE SENSEX and FIIs Net investments

The regression analysis predicts the SENSEX index due to FIIs net investments. The

regression equation of the regression model is presented in relationship between SENSEX

index due to FIIs net investment.

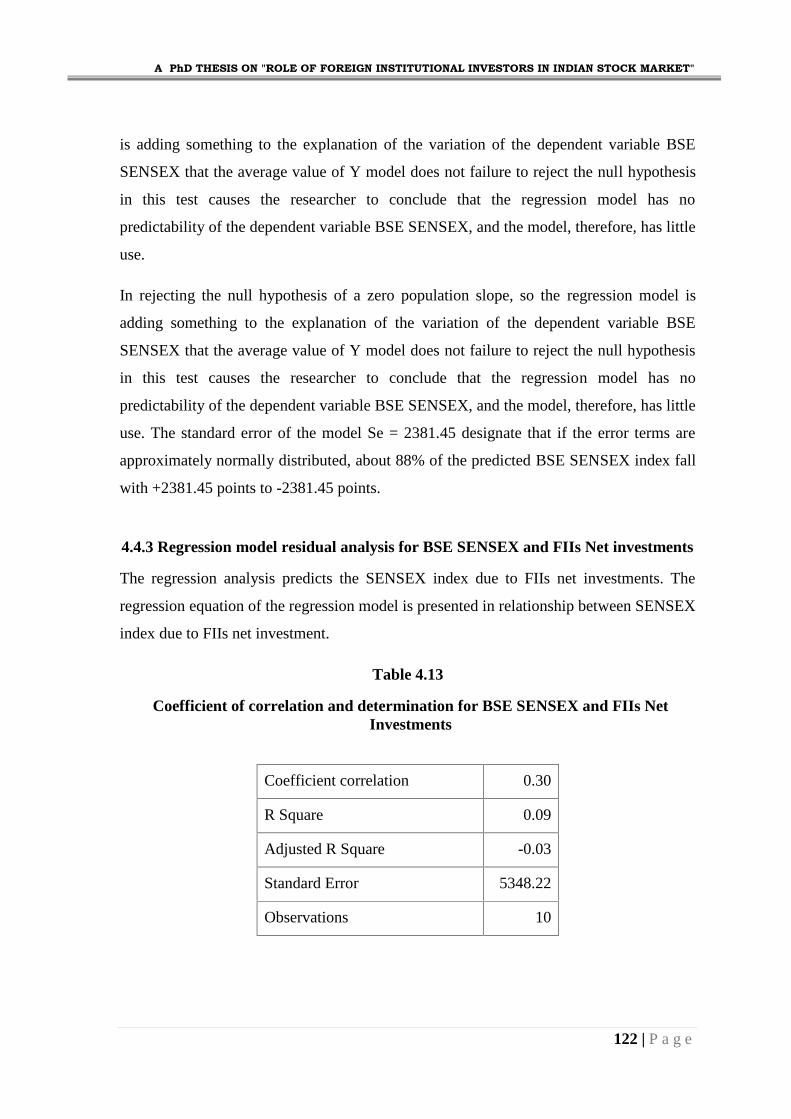

Table 4.13

Coefficient of correlation and determination for BSE SENSEX and FIIs NetInvestments

Coefficient correlation 0.30

R Square 0.09

Adjusted R Square -0.03

Standard Error 5348.22

Observations 10

Page 25

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

123 | P a g e

FIIs net investments stumpy influence on BSE SENSEX. It can be defines on the base of

r and R2. R2 the coefficient of determination is 0.09 in percentage 9% of the minute

wavering in the BSE SENSEX index due to the variation in the FIIs sales. This result

shows that 0.91 or 91% senses move FIIs specific activities and external factors.

However, the coefficient of correlation, r = 0.30 shows positive correlation between BSE

SENSEX and FIIs net investment. But there is not superior association among them. An

evaluation of R2 = 0.09 with the adjusted R = -0.03 shows that the adjusted R2 reduced the

overall proportion of variation of the dependent variable accounted for by the independent

variables by a factor of 0.12 by 12%. The loop between R2 and the adjusted R2 tend to

raise as non significant independent variables are supplementary to the regression model.

. Here larger standard error 5348.22 states a large amount of disparity or scatter around

the regression line which exhibit in chart 4.8.

Table 4.14 Regression residuals analysis for BSE SENSEX and FIIs Net Investments

Year FIIs Net X BSE SENSEX Y Predicted Y ResidualsStandardResiduals

2003 122.68 3872.97 11981.86 -8108.89 -1.61

2004 154.79 5563.09 12195.92 -6632.83 -1.32

2005 186.97 7392.89 12410.39 -5017.50 -1.00

2006 133.11 11440.04 12051.40 -611.35 -0.12

2007 293.14 15563.60 13118.07 2445.52 0.48

2008 -217.43 14492.68 9714.90 4777.78 0.95

2009 354.22 13700.82 13525.21 175.61 0.03

2010 571.13 18206.91 14970.99 3235.92 0.64

2011 -15.30 17777.77 11062.13 6715.63 1.33

2012 515.01 17,617.04 14596.93 3020.10 0.60

Page 26

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

124 | P a g e

The above residual analysis table 4.14 shows that average SENSEX index and average

FIIs Net investment for the years 2003 to 2012. Here researcher has used regression

model for the measure the cause and effect relationship between FIIs Net investments and

BSE SENSEX index. at this stage researcher examination a regression line to find out

whether the line is a good fit of the data excluding by observing the fitted line plot in

additional remark, regression line fit through a scatter plot of the data.

The value of the independent variable FIIs net investment X inserted in the regression

model and a predicted value BSE SENSEX Y is obtained for each value. This BSE

SENSEX predicated value compared to the actual value BSE SENSEX Y to determine

how much error the equation of the regression line produced. All dissimilar between the

genuine values and the predicated Y values is the error of the regression line at a given

point is referred to as residual value which given in the table 4.14 and 5th column.

Residual gives the design of how well the regression line fits the historical data points.

The regression model fits these particular data SENSEX index and FIIs Net investments

well for the year 2006 and 2009, as indicated by residuals of -611.35 and 175.61 BSE

SENSEX, correspondingly, for remaining years the residuals are comparatively huge,

indicating that the regression model does not fit the data for these years. The residuals

versus the fitted values graph indicate that the residuals appear to increase as FIIs net

investment X increases, indicating a possible problem with heteroscedasticity.

Page 27

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

125 | P a g e

Chart 4.8 Scatter Plots Of FIIs Net Investments And BSE SENSEX

Null H0 : β = 0

Alt H1 : β ≠ 0

OR

Null H0 : there is at least one of the regression coefficients is zero

Alt H1 : there is at least one of the regression coefficients is different from zero

Table 4.15 F-test for regression coefficients of FIIs net and BSE SENSEX

df SS MS F Significance F

Regression 1.00 22291057.28 22291057.28 0.78 0.40

Residual 8.00 228828061.32 28603507.66

Page 28

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

126 | P a g e

The above table 4.15 exhibits results of F-test regarding test of regression coefficient.

Here, the values of sum of squares (SS), degree of freedom (df), and mean squares (MS)

are obtained from the analysis of variance table, which is produced with other egression

statistics as standard output from statistical calculation, above shown table is F test value

for the BSE SENSEX index. F-test table, the degree of freedom is equal to 1. Here

regression models have only one independent variable FIIs net investments for BSE

SENSEX, therefore the degree of freedom error in regression analysis is n – 1 – 1 = n –

2.

The difference between F value = 0.78and the value obtained by squaring the t-value

(0.88)2 = 0.77 is (0.01) incurred due to error. The value of F for this is 0.78 with a p-value

0.00 which is significant at 5% level (0.40 > 0.05). This output value means that the

population slope is zero and there is prediction due to regression from this model given

the sample statics obtained.

On the base of this result, the null hypothesis would be accepted for the overall test of

significance. The regression coefficients are significantly similar to zero, and there is

significant predictability of the volatility of SENSEX Index by the FIIs net investments

given from this regression model.

Regression model line : Ŷ = 11164.14 + 6.67 X

A slope of 6.67 indicates that there is a positive upward trend of BSE SENSEX and FIIs

net over this period year 2003 to 2012 at a 6.67cr. The Y intercept of 11164.14 represents

what the regression model trend line would estimate the BSE SENSEX to have been in 10

years.

t-test for significant predictive variables FIIs net investments on BSE SENSEX

This test is determined how well a regression model fits the data. Here researcher decides

that it is not worth the effort to develop a linear regression model to predict BSE

SENSEX (Y) from FIIs investments. An alternative approach might be to average the

INDEX (Y) values and use Ŷ as the predictor of y for all values of FIIs X values.

Page 29

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

127 | P a g e

Null H0 : β = 0

Alt H1 : β > 0

OR

Null H0 : There is no relationship between FIIs net and BSE SENSEX

Alt H1 : There is positive relationship between FIIs net and BSE SENSEX

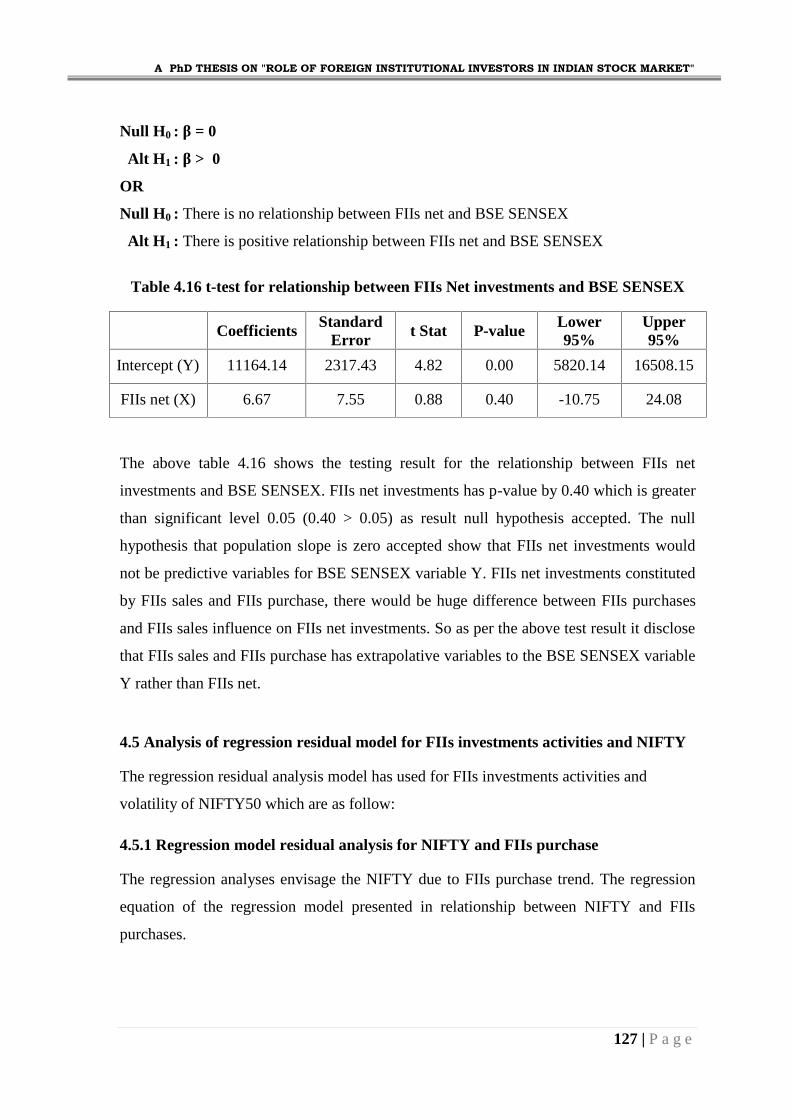

Table 4.16 t-test for relationship between FIIs Net investments and BSE SENSEX

Coefficients StandardError

t Stat P-value Lower95%

Upper95%

Intercept (Y) 11164.14 2317.43 4.82 0.00 5820.14 16508.15

FIIs net (X) 6.67 7.55 0.88 0.40 -10.75 24.08

The above table 4.16 shows the testing result for the relationship between FIIs net

investments and BSE SENSEX. FIIs net investments has p-value by 0.40 which is greater

than significant level 0.05 (0.40 > 0.05) as result null hypothesis accepted. The null

hypothesis that population slope is zero accepted show that FIIs net investments would

not be predictive variables for BSE SENSEX variable Y. FIIs net investments constituted

by FIIs sales and FIIs purchase, there would be huge difference between FIIs purchases

and FIIs sales influence on FIIs net investments. So as per the above test result it disclose

that FIIs sales and FIIs purchase has extrapolative variables to the BSE SENSEX variable

Y rather than FIIs net.

4.5 Analysis of regression residual model for FIIs investments activities and NIFTY

The regression residual analysis model has used for FIIs investments activities and

volatility of NIFTY50 which are as follow:

4.5.1 Regression model residual analysis for NIFTY and FIIs purchase

The regression analyses envisage the NIFTY due to FIIs purchase trend. The regression

equation of the regression model presented in relationship between NIFTY and FIIs

purchases.

Page 30

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

128 | P a g e

Table 4.17Coefficient of correlation and determination for NIFTY and FIIs purchases

Coefficient correlation 0.94

R Square 0.88

Adjusted R Square 0.86

Standard Error 580.91

Observations 10.00

The above table 4.17 formulates to measure the relation between NIFTY and FIIs

purchases. There is high degree of co relation between NIFTY and FIIs purchases which

can be states on the base of r = 0.94. The coefficient of determination is 0.88 in

additional 88% of the instability in the NIFTY index due to the deviation in the FIIs

purchase. This result shows that 0.12 in percentage 12% of the changes due to the other

factors other than FIIs purchase. A comparison of R2 = 0.88 with the adjusted R2 = 0.86

shows that the adjusted R2 reduced the overall proportion of variation of the dependent

variable accounted for by the independent variables by a factor of 0.02 by 2%.

It reveals that FIIs purchase highly influenced on volatility of NIFTY. The gap between

R2 and the adjusted R2 tends to increase as non significant independent variables are

added to the regression model. Standard error measures amount by which the regressed

values away from the actual values. Here larger standard error 580.91 indicates a huge

quantity of variation or scatter around the regression line (see chart 4.9). Distributions of

sample mean that wide spread is a better estimator of the population mean than a

distribution of sample mean.

Regression model line

Ŷ = α + βx

Ŷ = 815.75 + 1.38 X

Page 31

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

129 | P a g e

Table 4.18 Regression residuals analysis for NIFTY and FIIs purchase

YearFIIs Purchase

XNIFTY

YPredicted

Y ResidualsStandardResiduals

2003 377.75 1233.71 1337.74 -104.03 -0.19

2004 735.53 1755.87 1832.12 -76.25 -0.14

2005 1135.45 2268.91 2384.73 -115.82 -0.21

2006 1854.49 3357.09 3378.30 -21.20 -0.04

2007 3327.14 4571.29 5413.22 -841.93 -1.54

2008 2953.93 4339.11 4897.51 -558.40 -1.02

2009 2597.53 4113.96 4405.04 -291.08 -0.53

2010 3123.59 5461.12 5131.95 329.17 0.60

2011 2554.98 5335.91 4346.25 989.66 1.81

2012 2777.61 5343.77 4653.88 689.89 1.26

The above table 4.18 shows that average NIFTY and average FIIs Purchases for the years

2003 to year 2012. Here researcher has used regression model for the measure the cause

and effect relationship between FIIs purchase and NIFTY. Here researcher test a

regression line to determine whether the line is a good fit of the data other than by

observing the fitted line plot in other word regression line fit through a scatter plot of the

data.

For designed regression model line Ŷ = a + βX , The value of the independent variable

FIIs Purchase X inserted in the regression model and a predicted value NIFTY (Y) is

obtained for each value. This NIFT (Y) predicated value compared to the actual value

NIFTY (Y) to determine how much error the equation of the regression line produced.

The predicted values are calculated by inserting an X value into the equation of the

regression model line and solving for Ŷ. Here when FIIs purchase X was 377.75 cr in the

year 2003,

Page 32

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

130 | P a g e

The value of X inserted in the regression model line

Ŷ = 815.75 + 1.38 X

Ŷ = 815.75 + 1.38 (377.75)

Ŷ = 1337.74 for the year 2003

As exhibit in 4th column of the above table 4.18, remain all year predicted value

calculated as per above steps. The predicted values are calculated by inserting an X

values in to equation. Each predicted value NIFTY Y value is subtracted from the actual

Y to determine the error, for the year 2003 residual value was -104.03 (1337.74 –

1233.71). Each different between the actual values and the predicated Y values is the

error of the regression line at a given point is referred to as residual value which given in

the 5th column. Residual gives the design of how well the regression line fits the historical

data points.

The largest positive residual for the NIFTY was 998.66 in the year 2011 and smallest

negative residual was -21.20 in the year 2006. The regression line produces an error of

998.66 point NIFTY when there are 2554.98 cr. FIIs purchase in the year 2011. There

was smallest error-21.20 when FIIs purchase 1857.79 cr. in the year 2006. This result

presents the best and worst, bull or bear market performance for the residuals. Other

residuals determine different NIFTY market trend due to change in FIIs purchase for

remaining time period.

The residual versus the fitted values diagram indicates that the residuals appear to

increase as FIIs purchase X increases, indicating a potential problem with vary.

Page 33

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

131 | P a g e

Chart 4.9 Scatter Plots Of FIIs Purchases And NIFTY50

F-test: Test to determine the overall significance of the regression model

This F-test establishes weather regression coefficients are different from zero. Regression

provides only one predictor and only one regression coefficient test. The regression

coefficient is the slop of the regression line, the F-test for overall significance is testing

the same thing as the t-test in regression. The hypotheses being tested in simple

regression by the F-test for overall significance are as follow:

Null H0 : β = 0

Alt H1 : β ≠ 0

OR

Null H0 : there is at least one of the regression coefficients is zero

Alt H1 : there is at least one of the regression coefficients is different from zero

Page 34

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

132 | P a g e

Table 4.19 F-test for regression coefficients of FIIs Purchase and NIFTY

df SS MS F Significance F

Regression 1 19086021.97 19086021.97 56.56 0.00001

Residual 8 2699610.72 337451.34

The above F-test table 4.19 shows the F-test for regression coefficients of FIIs Purchase

and NIFTY. The values of sum of squares (SS), degree of freedom (df), and mean squares

(MS) are obtained from the analysis of variance table, which is produced with other

regression statistics as standard output from statistical calculation, above shown table is F

test value for the NIFTY index. F-test table, the degree of freedom is equal to 1. Here

regression models have only one independent variable FIIs purchase for NIFTY, therefore

the degree of freedom error in regression analysis is n – 1 – 1 = n – 2.

The difference between F value = 56.56 and the value obtained by squaring the t-value

(7.51)2 = 56.53 is (0.03) incurred due to error. The probability of obtaining an F value this

large by chance if there is no regression prediction in the regression model is 0.00001

according to F test. The value of F for this is 56.56 with a p-value 0.00001 which is not

significant at 5% level (0.00001< 0.05). This output value means it is highly unlikely that

the population slope is zero and there is no prediction due to regression from this model

given the sample statics obtained. Hence, it is highly likely that this regression molded

adds significant predictability of the dependent variable.

Therefore, the null hypothesis would not be rejected for the overall test of significance.

None of the regression coefficients are significantly different from zero, and no

significant predictability of the volatility of NIFTY by the FIIs Purchases given from this

regression model.

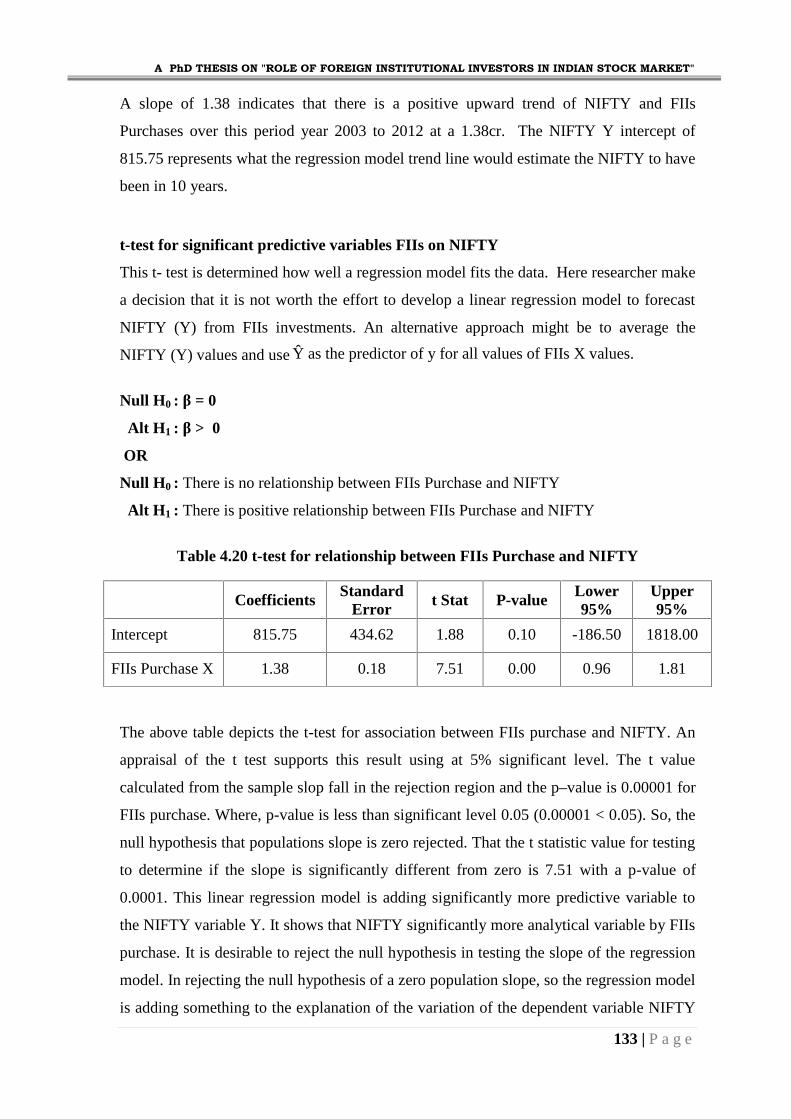

Regression model line: Ŷ = 815.75 + 1.38 X

Page 35

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

133 | P a g e

A slope of 1.38 indicates that there is a positive upward trend of NIFTY and FIIs

Purchases over this period year 2003 to 2012 at a 1.38cr. The NIFTY Y intercept of

815.75 represents what the regression model trend line would estimate the NIFTY to have

been in 10 years.

t-test for significant predictive variables FIIs on NIFTY

This t- test is determined how well a regression model fits the data. Here researcher make

a decision that it is not worth the effort to develop a linear regression model to forecast

NIFTY (Y) from FIIs investments. An alternative approach might be to average the

NIFTY (Y) values and use Ŷ as the predictor of y for all values of FIIs X values.

Null H0 : β = 0

Alt H1 : β > 0

OR

Null H0 : There is no relationship between FIIs Purchase and NIFTY

Alt H1 : There is positive relationship between FIIs Purchase and NIFTY

Table 4.20 t-test for relationship between FIIs Purchase and NIFTY

Coefficients StandardError

t Stat P-value Lower95%

Upper95%

Intercept 815.75 434.62 1.88 0.10 -186.50 1818.00

FIIs Purchase X 1.38 0.18 7.51 0.00 0.96 1.81

The above table depicts the t-test for association between FIIs purchase and NIFTY. An

appraisal of the t test supports this result using at 5% significant level. The t value

calculated from the sample slop fall in the rejection region and the p–value is 0.00001 for

FIIs purchase. Where, p-value is less than significant level 0.05 (0.00001 < 0.05). So, the

null hypothesis that populations slope is zero rejected. That the t statistic value for testing

to determine if the slope is significantly different from zero is 7.51 with a p-value of

0.0001. This linear regression model is adding significantly more predictive variable to

the NIFTY variable Y. It shows that NIFTY significantly more analytical variable by FIIs

purchase. It is desirable to reject the null hypothesis in testing the slope of the regression

model. In rejecting the null hypothesis of a zero population slope, so the regression model

is adding something to the explanation of the variation of the dependent variable NIFTY

Page 36

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

134 | P a g e

that the average value of Y model does not failure to reject the null hypothesis in this test

causes the researcher to conclude that the regression model has no predictability of the

dependent variable NIFTY, and the model, therefore, has little use. The standard error of

the model Se = 580.91 designate that if the error terms are approximately normally

distributed, about 88% of the predicted NIFTY index fall with +580.91 points to -580.91

points.

4.5.2 Regression model residual analysis for NIFTY and FIIs sales

The regression analysis predicts the NIFTY index owing to FIIs sales trend. The

regression equation of the regression model is presented in relationship between NIFTY

and FIIs sales

Table 4.21 Coefficient of correlation and determination for NIFTY and FIIs Sales

Coefficient correlation 0.90

R Square 0.80

Adjusted R Square 0.78

Standard Error 732.28

Observations 10

The above regression models determinant use for the measures the effect of FIIs sales on

NIFTY. There is high degree of optimistic contribution among the NIFTY and FIIs sales

which expressive by coefficient correlation r = 0.90. R2 the coefficient of determination is

0.80 in percentage 80% of the instability in the NIFTY index due to the deviation in the

FIIs sales. This result shows that 0.20 in other term 20% of the change due to the

additional factors other than FIIs purchase. The difference between R2 and the adjusted R2

tends to increase as non significant independent variables are added to the regression

model. The % difference between R2 = 0.80 with the adjusted R= 0.78 point out that the

shrink the overall proportion of variation of the dependent variable accounted by the

independent variables.

Page 37

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

135 | P a g e

In short, It can be summarised that increase in change of FIIs sales trend which increase

the NIFTY. Here, standard error 732.28 point toward a massive amount of variation or

scatter around the regression line (see figure). NIFTY index variability is fall with

+732.28 to -732.28 points. Distributions of sample mean that wide variation is a superior

estimator of the population mean than a distribution of sample mean.

Regression model line

Ŷ = α +βx

Ŷ = 1140.42 + 1.36 X

Table 4.22 Regression residuals analysis for NIFTY and FIIs sales

Year FIIs Sales X NIFTY Y Predicted Y ResidualsStandardResiduals

2003 255.08 1233.71 1487.85 -254.15 -0.37

2004 580.74 1755.87 1931.44 -175.57 -0.25

2005 948.48 2268.91 2432.33 -163.42 -0.24

2006 1721.38 3357.09 3485.07 -127.98 -0.19

2007 3034.00 4571.29 5272.97 -701.67 -1.02

2008 3171.35 4339.11 5460.05 -1120.94 -1.62

2009 2243.31 4113.96 4195.98 -82.02 -0.12

2010 2577.69 5461.12 4651.43 809.69 1.17

2011 2570.29 5335.91 4641.36 694.55 1.01

2012 2262.60 5343.77 4222.27 1121.50 1.62

Page 38

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

136 | P a g e

The above table 4.22 regression residual analysis for evaluates variability of NIFTY

index owning to FIIs sale. The above table shows the trend of FIIs sales and NIFTY index

for the year 2003 to 2012. Here, researcher compared the trend of FIIs sales and NIFTY

index for the measure the cause and effect relationship between FIIs sales and NIFTY

index. Here researcher test a regression line to determine whether the line is a good fit of

the data other than by observing the fitted line plot in other word regression line fit

through a scatter plot of the data.

The appreciated of the independent variable FIIs sales X inserted in the regression model

Ŷ = 1140.42 + 1.36 X

As per above regression line, predicted value NIFTY Y is obtained for each value for year

2003 to year 2012. This NIFTY predicated value compared to the actual value NIFTY Y

to determine how much error the equation of the regression line produced. Each different

between the actual values and the predicated Y values is the error of the regression line at

a given point is referred to as residual value which given in the 5th column. Residual gives

the idea of how well the regression line fits the historical data points.

The regression model fits these particular data NIFTY index and FIIs sales well for the

year 2006 and 2009, as indicated by residuals of -127.98 and -82.02 at standard residual -

0.05 and -0.13 NIFTY, there were extensive residual values 1121.50 in the year 2012

which shows enormous difference between actual value and predicated value, for

remaining years the residuals are relatively large, indicating that the regression model

does not fit the data for these years. The residuals versus the fitted values graph indicate

that the residuals seem to increase as FIIs sales X increases, indicating a potential

problem with different variables.

Page 39

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

137 | P a g e

Chart 4.10 Scatter Plots Of FIIs Sales And NIFTY50

F-test : Test to determine the overall significance of the regression model

This F-test determines weather regression coefficients are different from zero. Regression

provides only one predictor and only one regression coefficient test. The regression

coefficient is the slop of the regression line, the F-test for overall significance is testing

the same thing as the t-test in regression. The hypotheses being tested in simple

regression by the F-test for overall significance are as follow:

Null H0 : β = 0

Alt H1 : β ≠ 0

OR

Null H0 : there is at least one of the regression coefficients is zero

Alt H1 : there is at least one of the regression coefficients is different from zero

Page 40

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

138 | P a g e

Table 4.23 F-test for regression coefficients of FIIs sales and NIFTY

df SS MS F Significance F

Regression 1 17495778.40 17495778.40 32.63 0.00001

Residual 8 4289854.28 536231.79

The above table shows the F-test for regression coefficients of FIIs Sales and NIFTY. The

values of sum of squares (SS), degree of freedom (df), and mean squares (MS) are

obtained from the analysis of variance table, which is produced with other egression

statistics as standard output from statistical calculation, above shown table is F test value

for the NIFTY index. F-test table, the degree of freedom is equal to 1. Here regression

models have only one independent variable FIIs purchase for NIFTY, therefore the

degree of freedom error in regression analysis is n – 1 – 1 = n – 2.

Here, t-test value and F-test value compared for the result. The small gap between F value

= 32.63 and the value obtained by squaring the t-value (5.71)2 = 32.60 is (0.03) incurred

due to error. The probability of obtaining an F value this large by chance if there is no

regression prediction in the regression model is 0.00001 according to F test. The value of

F for this is 32.63 with a p-value 0.00001 which is not significant at 5% level (0.00001<

0.05). This output value means it is highly unlikely that the population slope is zero and

there is no prediction due to regression from this model given the sample statics obtained.

Hence, it is highly likely that this regression molded adds significant predictability of the

dependent variable.

Accordingly, the null hypothesis would not be rejected for the overall test of significance.

None of the regression coefficients are significantly different from zero, and no

significant predictability of the volatility of NIFTY by the FIIs sales given from this

regression model.

Regression model line: Ŷ = 1140.42 + 1.36 X

Page 41

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

139 | P a g e

As above regression model line, A slope of coefficient 1.36 indicates that there is a

positive rising tendency of NIFTY and FIIs sales over this period year 2003 to 2012 at a

1.36cr. The NIFTY Y cut off of 1140.42 represents what the regression model tendency

line would estimate the NIFTY to have been in 10 years.

t-test for significant predictive variables FIIs investments activities on NIFTY

This test is determined how well a regression model fits the data. Here researcher make a

decision that it is not worth the effort to develop a linear regression model to forecast

NIFTY (Y) from FIIs investments. An alternative approach might be to average the

NIFTY (Y) values and use Ŷ as the predictor of y for all values of FIIs X values.

Null H0 : β = 0

Alt H1 : β > 0

OR

Null H0 : There is no relationship between FIIs sales and NIFTY

Alt H1 : There is positive relationship between FIIs sales and NIFTY

Table 4.24 t-test for relationship between FIIs Sales and NIFTY

CoefficientsStandard

Error t Stat P-valueLower95%

Upper95%

Intercept 1140.42 516.58 2.21 0.06 -50.82 2331.66

FIIs sales X 1.36 0.24 5.71 0.00 0.81 1.91

An examination of the t test supports this result using at 5% significant level. The t value

calculated from the sample slop fall in the rejection region and the p –value is 0.0001 for

FIIs purchase. Where, p-value is less than significant level 0.05 (0.00001 < 0.05). So, the

null hypothesis that populations slope is zero rejected. That the t statistic value for testing

to determine if the slope is significantly different from zero is 8.02 with a p-value of

0.00001. This linear regression model is adding significantly more predictive variable to

the NIFTY variable Y. It shows that NIFTY index significantly more analytical variable

by FIIs sales. It is desirable to reject the null hypothesis in testing the slope of the

regression model. In rejecting the null hypothesis of a zero population slope, so the

Page 42

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

140 | P a g e

regression model is adding something to the explanation of the variation of the dependent

variable NIFTY that the average value of Y model does not failure to reject the null

hypothesis in this test causes the researcher to conclude that the regression model has no

predictability of the dependent variable NIFTY, and the model, therefore, has little use.

The standard error of the model Se = 732.28 indicate that if the error terms are

approximately normally distributed, about 89% of the predicted NIFTY index fall with

+732.28 to -732.28.

4.5.3 Regression model residual analysis for NIFTY and FIIs Net investments

The regression analysis predicts the NIFTY due to FIIs net investments. The regression

equation of the regression model is presented in relationship between NIFTY and FIIs net

investment.

Table 4.25

Coefficient of correlation and determination for NIFTY and FIIs Net Investments

Co efficient correlation 0.31

R Square 0.09

Adjusted R Square -0.02

Standard Error 1571.34

Observations 10

FIIs net investments stumpy influence on NIFTY 50. It can be defines on the base of r

and R2. R2 the coefficient of determination is 0.09 in percentage 9% of the small wavering

in the NIFTY 50 index due to the variation in the FIIs sales. This result shows that 0.91 or

91% senses move FIIs specific activities and external factors. However, the coefficient of

correlation, r = 0.31 shows positive correlation between NIFTY 50 and FIIs net

investment. But there is not superior association among them. A evaluation of R2 = 0.09

with the adjusted R = -0.03 shows that the adjusted R2 reduced the overall proportion of

variation of the dependent variable accounted for by the independent variables by a factor

of 0.12 by 12%. The loop between R2 and the adjusted R2 tend to rise as non significant

independent variables are supplementary to the regression model. Standard error 1531.34

Page 43

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

141 | P a g e

states a large amount of disparity or scatter around the regression line as displayed in

chart 4.11.

Table 4.26 Regression residuals analysis for NIFTY and FIIs Net Investments

Year FIIs Net X NIFTY Y Predicted Y ResidualsStandardResiduals

2003 122.68 1233.71 3602.65 -2368.94 -1.60

2004 154.79 1755.87 3667.29 -1911.42 -1.29

2005 186.97 2268.91 3732.06 -1463.15 -0.99

2006 133.11 3357.09 3623.65 -266.55 -0.18

2007 293.14 4571.29 3945.76 625.53 0.42

2008 -217.43 4339.11 2918.08 1421.04 0.96

2009 354.22 4113.96 4068.71 45.25 0.03

2010 571.13 5461.12 4505.30 955.82 0.65

2011 -15.30 5335.91 3324.91 2011.00 1.36

2012 515.01 5343.77 4392.35 951.43 0.64

The above constructed residual analysis table 4.26 shows that average NIFTY index and

average FIIs Net investment trend for the years 2003 to 2012. Here researcher has used

regression model for the measure the cause and effect relationship between FIIs Net

investments and NIFTY index. At this occasion researcher investigate a regression line to

find out whether the line is a good fit of the data excluding by observing the fitted line

plot in additional remark, regression line fit through a scatter plot of the data.

The value of the independent variable FIIs net investment X inserted in the regression

model and a predicted value NIFTY Y is obtained for each value. This NIFTY predicated

value compared to the actual value NIFTY Y to determine how much error the equation

of the regression line produced. All dissimilar between the genuine values and the

predicated Y values is the error of the regression line at a given point is referred to as

residual value which

Page 44

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

142 | P a g e

given in the 5th column. Residual gives the design of how well the regression line fits the

historical data points.

The regression model fits these particular data NIFTY index and FIIs Net investments

well for the year 2006 and 2009, as indicated by residuals of -266.55 and 45.25 NIFTY,

evenly, for remaining years the residuals are comparatively huge, indicating that the

regression model does not fit the data for these years. The residuals versus the fitted

values graph indicate that the residuals appear to increase as FIIs net investment X

increases, indicating a possible problem with vary variables.

Chart 4.11 Scatter Plots Of FIIs Net Investments And NIFTY50

F-test: Test to determine the overall significance of the regression model

This F-test determines a weather regression coefficient is different from zero. Regression

provides only one predictor and only one regression coefficient test. The regression

coefficient is the slop of the regression line, the F-test for overall significance is testing

the same thing as the t-test in regression. The hypotheses being tested in simple

regression by the F-test for overall significance are as follow:

Page 45

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

143 | P a g e

Null H0 : β = 0

Alt H1 : β ≠ 0

OR

Null H0 : there is at least one of the regression coefficients is zero

Alt H1 : there is at least one of the regression coefficients is different from zero

Table 4.27 F-test for regression coefficients of FIIs net and NIFTY

df SS MS F Significance F

Regression 1 2032744.09 2032744.09 0.81 0.39

Residual 8 19752888.59 2469111.07

The above F-test table 4.27 shows the F-test for regression coefficients of FIIs net

investments and NIFTY. The values of sum of squares (SS), degree of freedom (df), and

mean squares (MS) are obtained from the analysis of variance table, which is produced

with other egression statistics as standard output from statistical calculation, above shown

table is F test value for the NIFTY index. F-test table, the degree of freedom is equal to

1. Here regression models have only one independent variable FIIs net investments for

NIFTY, therefore the degree of freedom error in regression analysis is n – 1 – 1 = n – 2.

The difference between F value = 0.81 and the value obtained by squaring the t-value

(0.91)2 = 0.83 is (0.02) incurred due to error. The value of F for this is 0.81with a p-value

0.00 which is significant at 5% level (0.40 > 0.05). This output value means that the

population slope is zero and there is prediction due to regression from this model given

the sample statics obtained.

Thus, the null hypothesis would be accepted for the overall test of significance. The

regression coefficients are significantly similar to zero, and there is significant

predictability of the volatility of NIFTY Index by the FIIs net investments given from this

regression model.

Regression model line : Ŷ = 3355.72 + 2.01X

Page 46

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

144 | P a g e

A slope of 2.01 indicates that there is a positive upward trend of NIFTY and FIIs net over

this period year 2003 to 2012 at a 2.01cr. The Y intercept of 3355.72 represents what the

regression model trend line would estimate the NIFTY to have been in 10 years.

t-test for significant predictive variables FIIs net investments on NIFTY

This t- test is determined how well a regression model fits the data. Here researcher

decides that it is not worth the effort to develop a linear regression model to predict

NIFTY (Y) from FIIs investments. An alternative approach might be to average the

NIFTY (Y) values and use Ŷ as the predictor of y for all values of FIIs X values.

Null H0 : β = 0

Alt H1 : β > 0

OR

Null H0 : There is no relationship between FIIs net and NIFTY

Alt H1 : There is positive relationship between FIIs net and NIFTY

Table 4.28 t-test for relationship between FIIs Net investments and NIFTY

CoefficientsStandard

Errort Stat P-value

Lower95%

Upper95%

Intercept 3355.72 680.88 4.93 0.00 1785.62 4925.82

FIIs net 2.01 2.22 0.91 0.39 -3.10 7.13

The above table depicts the t-test for association between FIIs net investments and

NIFTY. An evaluation of the t test supports this result using at 5% significant level.

Result tested on the base of comparison with P-value and 5% significant level.

Consequently, FIIs net investments has p-value by 0.39 which is greater than significant

level 0.05 (0.40 > 0.05) as result null hypothesis accepted. The null hypothesis that

population slope is zero accepted show s that FIIs net investments would not be predictive

variables for NIFTY variable Y. FIIs net investments constituted by FIIs sales and FIIs

purchase, so as per the above test result it disclose that FIIs sales and FIIs purchase has

extrapolative variable to the NIFTY variable Y rather than FIIs net. The standard error of

the model Se = 1571.34 indicate that if the error terms are approximately normally

distributed, about 89% of the predicted NIFTY index fall with +1571.34 to -1571.34.

Page 47

A PhD THESIS ON "ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN INDIAN STOCK MARKET"

145 | P a g e

4.6 Correlation Co-efficient Matrix between FIIs investments activities: FIIspurchases FIIs sales, FIIs net investments and BSE SENSEX, NIFTY50

Correlation co-efficient computed to understand the relationship between FII activities;

FIIs purchases, FIIs sales, FIIs net investments and performance of Indian stock market

NIFTY & NIFTY50. The correlation matrix is presented in following Table:

Table 4.29

Correlation Co-efficient Matrix between FIIs investments, BSE SENSEX, NIFTY50

As per the above table correlation co-efficient matrix, shows that FII inflows and the BSE

SENSEX states a significant positive correlation. It was further observed that there is

good co-movement between FII inflows and volatility of stock market BSE SENSEX &

NIFTY50. Huge inflows from FIIs make the surplus in the Indian stock market.

Furthermore, there was good co-movement between the BSE SENSEX and FIIs sales &

FIIs purchases. In the contrary, BSE SENSEX and FIIs net investments have moderate

correlation with each other. Moreover, there was high degree of correlation among the

FIIs sales and FIIs purchases. FIIs net investments have sensible correlation with

performance of NIFTY50. So analysis of correlation of coefficient matrix demonstrates

performance of Indian stock market extremely associated with the FIIs investments

activities.

Consequently, this analysis shows that dependent variables Indian stock indexes BSE

SENSEX and NIFTY50 and in independent variables FIIs investments employed in this

model correlation of coefficient matrix can provide unbiased correlation and correct

measure on dependent variables.

Variables BSESENSEX