56

Citibank European Credit Conference Citibank- European Credit Conference London November 30, 2011

Citibank European Credit ConferenceCitibank- European Credit Conference LondonNovember 30, 2011

Disclaimer

This presentation does not constitute or form part of, and should not be construed as, any offer or invitation to subscribe for, underwrite or otherwise acquire, any securities of the Company or any member of its group nor should it or any part of it form the basis of, or beCompany or any member of its group nor should it or any part of it form the basis of, or be relied on in connection with, any contract to purchase any securities of the Company or any member of its group or any commitment whatsoever.

THIS DOCUMENT MAY NOT BE DISTRIBUTED AND MAY NOT BE REPRODUCED IN ANYTHIS DOCUMENT MAY NOT BE DISTRIBUTED AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER. ANY DISTRIBUTION OR REPRODUCTION OF THE ATTACHED DOCUMENT IN WHOLE OR IN PART IS UNAUTHORIZED.

This presentation comprises publicly available information and the Company undertakes noThis presentation comprises publicly available information and the Company undertakes no obligation to update this information after the date hereof. The information contained in this presentation is for background purposes only and is subject to amendment, revision and updating. No representation or warranty, express or implied, is made as to the fairness, accuracy or completeness of the information contained herein and no reliance should be

l d it N f th C th i d i th t li bilitplaced on it. None of the Company, their advisers or any other person accepts any liability for any loss howsoever arising, directly or indirectly, from the issue of this document or its contents.

Thi t ti i l d t i f d l ki t t t A t l lt ld diffThis presentation includes certain forward-looking statements. Actual results could differ materially from those included in the forward-looking statements due to various risks and uncertainties, including but not limited to changes in business, economic and competitive conditions, regulatory reforms, foreign exchange rate fluctuations, uncertainties in litigation or investigative proceedings and availability of financing.or investigative proceedings and availability of financing.

2

Agenda

● Executive Summary

St t d b i d l● Strategy and business model

● Financial overview and capitalization

● Growth and business plan

● Supplementary materials

3

Executive summary

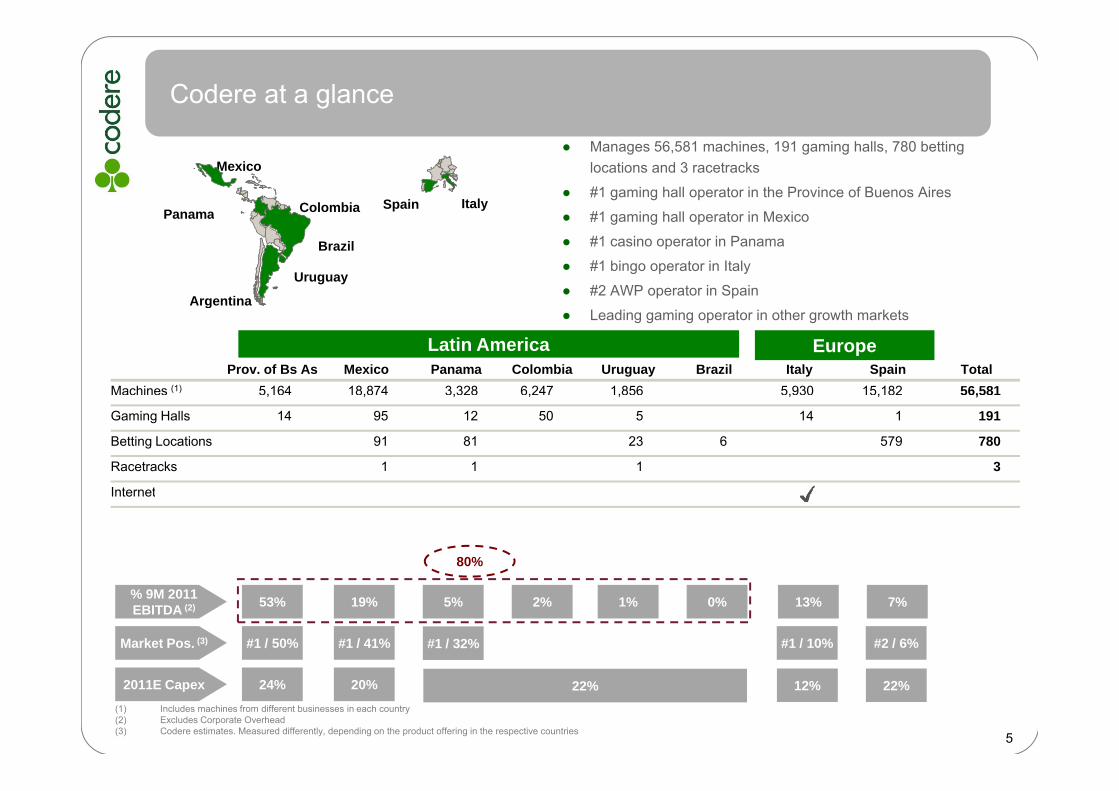

Codere at a glance

● Manages 56,581 machines, 191 gaming halls, 780 betting locations and 3 racetracks

● #1 gaming hall operator in the Province of Buenos Aires

● #1 gaming hall operator in MexicoColombiaPanama

Mexico

ItalySpain● #1 gaming hall operator in Mexico

● #1 casino operator in Panama

● #1 bingo operator in Italy

● #2 AWP operator in SpainUruguay

Brazil

Panama

Argentina● Leading gaming operator in other growth markets

Latin AmericaProv. of Bs As Mexico Panama Colombia Uruguay Brazil Italy Spain Total

Machines (1) 5,164 18,874 3,328 6,247 1,856 5,930 15,182 56,581

g

Europe

, , , , , , , ,

Gaming Halls 14 95 12 50 5 14 1 191

Betting Locations 91 81 23 6 579 780

Racetracks 1 1 1 3

Internet

80%

Market Pos. (3) #1 / 50% #1 / 41% #1 / 10% #2 / 6%

% 9M 2011 EBITDA (2) 53% 19% 5% 2% 1% 0% 13% 7%

#1 / 32%

(1) Includes machines from different businesses in each country(2) Excludes Corporate Overhead(3) Codere estimates. Measured differently, depending on the product offering in the respective countries

2011E Capex 24% 20% 12% 22%

5

22%

Key investment highlights

Compelling growth story in Latin America

• Strong track record of organic and non organic growth• Low gaming penetration in a context of high GDP growth rates in Latin America• Well positioned for legalization of gaming halls in Brazil and launch of on-line

• #1 gaming operator in the Province of Buenos Aires, in Mexico and casino operator in Panama

yand Italy activities in Latin America

• Competitive advantage in nascent VLT market in Italy

in Panama• Leading market position in Italy (#1 in bingo) and Spain (#2 in AWP machines)• Market share of c. 50% in Argentina and in c. 41% Mexico, the two largest markets• Entrenched operator with key local relationships and licenses in a highly regulated

market

Leading position in all markets

market• First mover advantage in most markets

Strong management• Experienced management team and Board with unique knowledge of the business• Proven track record navigating market cyclesStrong management

team and operations g g y

• Unrivaled local market expertise• Six years reporting as a public company

• Limited near-term maturitiesStrong balance sheet and cash flow profile

ed ea e a u es• Cash generative business• Low maintenance capex• Flexible investment program

Unique international gaming footprint with exceptional growth potential6

Strategy and business model

Growth drivers are not directly linked to economic cycles

Increasing gaming as % of GDP● Regulatory dialogue

○ Tax authorities outsourcing, large employer,

Increase market share● Strategic alliances

○ Attracting best partners successful partnershipg, g p y ,responsible gaming

● Technological & game innovation○ Video, server-based gaming, TITO, jackpots,

multigame● Market knowledge

○ Attracting best partners, successful partnership dialogue

● Driving consolidation○ Leadership in core markets, successful integration of

acquisitions, cross-fertilization of best practices● Market knowledge

○ Customer preferences, distribution footprint

GGY as % of GDP (1) Population per machine (2)

300,000

400,000

ines

It.60Mn

Sp 47Mn

2.71

1.37 1 11 0 99

0

100,000

200,000

Mac

hi

Prov. of Bs. As. 14 Mn

Sp.47Mn

Pan. 4Mn

Mex. 111Mn

Uru. 3Mn

1.11 0.99 0.93 0.71 0.67 0.670.25 0.17

00 500 1,000 1,500 2,000

Mac

hine

in

trod

uctio

n

1979 199619401936 na 200420041968

1- Gross Gaming Yield 2010 GBGC Report (data 2007)

na

Population/Machine2- Codere estimates

1979

8

Integrate market knowledge, regulatory expertise and technology, to develop successful, legal, gaming experiences

Codere’s business model

180

Characteristics Codere vs. Las Vegas revenues

100

120

140

160● Regional model of gaming

● Growth focused on profitability rather than scale

● Horizontal versus vertical integration

40

60

80

Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

g

● Institutionalisation / professionalization

07 07 07 07 08 08 08 08 09 09 09 09 10 10 10 10 11 11 11

Las Vegas revenues Codere revenues

Regulation

Regional model Destination model

High Low

vs.

Target market

Stakes / prizes

Regulation

Local clientele

Low

High

Tourist

High

Low

Capital intensity

Marketing

Taxes

Low

High

High

Low

Restricted Permitted

9

Number of players / licensees Low High

Successful implementation of business model has resulted in a solid track record

3001.200

Revenues EBITDA(€ in millions) (€ in millions)

233 231 241 250

1.050

968

1.127

1.000

184 200

200

732

880

800

101

150

455

600

60 71 76

70 73

101

100

272

428

354 352 318 400

0

50

0

200

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '100

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

Notes: Discontinued operations are excluded between 2004 and 2008Gains or losses on asset disposals are excluded from EBITDA since 2008Figures for 2000-2004 are in Spanish GAAP, thereafter in IFRS 10

Argentina – Province of Buenos Aires53% ebitda

1.8006.000

Market Net win vs. machinesKey value drivers

53% ebitda

C G %

1.000

1.200

1.400

1.600

5.000

● Leadership position (c. 50% market share with 14 out of 46 halls) in fast growing market.

● Significant unmet demand resulting from limitation on number of licenses (regional monopolies)

achi

nes

CAGR 05-10 21.9%

Net w

inA

R

400

600

800

3.000

4.000

2005 2006 2007 2008 2009 2010 Q3 2011

Outlook

● Optimization of hall locations and capacity increase (7%-10% growth expected FY2011)

● Continued optimization of park via installation of coinless systems (i e TITO)

# of

m

R$/day

2011

# of machines net win in AR$

Evolution of machines per hall Net win CDR vs. competitors

systems (i.e. TITO)

● Economic growth (7% 2011E) and inflation (24% 2011E)

800

1.000

1.200

1.400

1.600Hall 2005 Q3 2011 Var.%SAN MARTIN 485 642 32%LOMAS DEL MIRADOR 115 656 470%LA PLATA 366 558 52%LANUS 388 512 32%SAN JUSTO 351 410 17%

348 471 35%111%

R$/

day

0

200

400

600

800MORON 348 471 35%SAN MIGUEL 312 388 24%LOMAS DE ZAMORA 256 323 26%MAR 224 204 (9%)SOL 179 310 73%TEMPERLEY 115 129 12%RAMOS MEJIA 186 322 73%

56%

79%H1N1 Flu

AR

Jan‐03 Jan‐04 Jan‐05 Jan‐06 Jan‐07 Jan‐08 Jan‐09 Jan‐10

Codere Rest of the market

11

PEATONAL 121 121 0%CENTRO 99 118 19%

TOTAL 3.545 5.164 46%

(1) Codere estimates

(1)

Mexico19% ebitda

24.000 1.200

Net win vs. machines Market

Key value drivers

L di i i ( 41%) i l l d i k

Anti-smoking law

19% ebitda

(1)

16.000

20.000

24.000

800

1.000

1.200

ac

hin

es

Ne

t win

(MX

● Leading position (c.41%) in recently regulated, growing market

● Growth through machine deployment

● Net win impacted by regulation and technological changes

Outlook

4.000

8.000

12.000

400

600# o

f M

X$

/da

y)

● Improve net wins via improved competitive position of Joint Opcos including hall refurbishments to adapt to anti-smoking regulation

● Continued machine deployment (5%-7% growth expected FY2011)

# of machines Net win Mx$

Gaming hall permitsMachine and hall evolution (2)

FY2011)

● Improvement of regulatory framework

(1)

90

100

110

16,000

19,000

22,000

es

In operation Total232 513

41%

9%

33% 26%

10%

39%

50

60

70

80

7,000

10,000

13,000# of halls

# of

mac

hin

8%9%12%13%

12

404,0002005 2006 2007 2008 2009 2010 Q3

2011# of halls # of machines

(2) Codere estimates

Codere Caliente Cirsa Televisa Others

(1) Data shown for the Caliente part of our Mexican operations beginning 2009 corresponds only to the halls included in the agreements signed in July 2010.

Italy13% ebitda

3005.600

Net win vs. machinesMarketKey value drivers

● Relevant presence in fast growing market via 3 businesses:

13% ebitda

140

180

220

260

2.100

2.800

3.500

4.200

4.900p g g

o 14 gaming halls with AWPs and VLTs and bingo (10% market share)

o 1 of 10 network concessionaires with 1,359 VLT rights and 9,000 interconnected AWPs

M hi ti ith 5 168 AWP

Net w

in€/dayof

mac

hine

s

60

100

140

0

700

1.400

Jan-10

Mar-10

May-10

Jul-10

Sept-10

Nov-10

Jan-11

Mar-11

May-11

Jul-11

Sept-11

o Machine operation with 5,168 AWPs

● Growth driven by machine deployment

Outlook

● Continued deployment of VLTs

● Selected acquisitions (AWP machine operators, halls and/or VLT

#

# of AWP machines # of VLT machines

AWP Net Win €/Day VLT Net Win €/Day

Machine ComparisonItalian gaming market

Selected acquisitions (AWP machine operators, halls and/or VLT rights)

(in € billions) CAGRVLT AWP

Minimum payout 85% 75%

Max. prize €5,000 - €500K €100

Taxes (amount 2.8%/18.6% 13.4%/53.6%

(in € billions) CAGR

10%

7%35

28

42

51%

4854

3%

61

51%50%

45%

3%51%wagered/net win)

Location Bingo hallsLBOs

Gaming halls

Bars, cafesBingo halls

89%

25

15

45%

4%52%

18%40% 44%

46% 47%

8%6%

5%5%

3%3%

90%

76%54%

51%

45%

52%4%

13

Net win Q3 2011 €243.4 €70.4

Source: AAMS

18%8%

2003 2004 2005 2006 2007 2008 2009 2010

BingoAWP

Spain7% ebitda

MarketKey value drivers

● Leading position in three businesses:

Net win (seasonally adjusted) vs. regulatory changes

7% ebitda

Castilla la Mancha

5355575961

Leading position in three businesses:

o 2nd largest operator of AWPs with 15,182 machines (6% market share)

o Canoe gaming hall (largest bingo in Spain)

o Sports betting (579 sports betting locations in Madrid, the Basque Region, Navarra and Aragon)

Cataluña (19%)

Valencia

(14%)

Castilla la Mancha (8%)

win

€/da

y

414345474951Outlook

● Decrease in AWP net win in 2011 (est. -12.2%) resulting from national anti-tobacco ban (since Jan. 2, 2011) and macroeconomic situation.

● Decrease in machine portfolio following rationalization

● Synergies from combination of businesses (AWP Sports Betting and Bingo)

Andalucia(12%)

(14%)

Madrid (22%)

Net

Smoking ban(national)

Q1 05 Q4 05 Q3 06 Q2 07 Q1 08 Q4 08 Q3 09 Q2 10 Q1 11● Synergies from combination of businesses (AWP, Sports Betting and Bingo)

● Growth of sports betting locations and increase in the types of machines allowed in gaming halls

Codere net win vs rest of market

(1)

Note: Figures in parenthesis represent percentage of Codere’sportfolio in that region when regulation was introduced.

# Sports betting locationsCodere net win vs. rest of market(in €/day)

# Sports betting locations

461

580 611 579

34 39 3649 50 49

59 56 49 49 44,5 41,6 40,2175 210 205

287

Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 112007 2008 2009 2010 Q1 11 Q2 11 Q3 11

Market Cirsa Codere

14Source: Spanish National Gaming Commission and Cirsa annual Report

Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11

Financial overview and capitalization

Codere’s strong performance has been achieved through geographic and product diversification…

Revenue EBITDA(US$ in millions) (US$ in millions)

208182

18

19

CAGR CAGR

14% 30%

1,544

1,350

1,492343

322316

346

283

263148

182

98

90

5859

7

2119

0%

14%

(5%)

902

1,207

226

275

261

311107

226

287264 278

74

12%

902

530

747

988883

1.046 174

226

(15)

19%12%

2006 2007 2008 2009 2010

(15)(28)(34) (53)

(21) (40)

2006 2007 2008 2009 20102006 2007 2008 2009 2010

16

Latin America Spain Italy Headquarters

…driven by Argentina and Mexico…

Revenue in constant currency

CAGR

EBITDA in constant currency

CAGR(US$ in millions)(US$ in millions )

1 268

12

134 6%

CAGR CAGR

(4%)

9951,047

1,268

311

357

10523

25

331

347119

119

29% 18%

746

995

227

290

80

101

100

15

12

201

348

331

107

132

531172

135

166186

24054

414

529596

788125

107

28%

23%

103

135

2006 2007 2008 2009 2010

295

414

2006 2007 2008 2009 2010

Other Latin AmericaMexicoArgentina

17Excludes gains or losses on the foreign currency contracts

… reflecting sustantial investment in the business…

(4)Spain 87.3 67.3 50.4 21.2 24.2

2009 2010 (€ in million) 2006 2007 2008

19.0

9M 2011

(4)(5)

(6) (11)

(13)

Maintenance 45.5 45.9 38.5 19.0 19.5Growth 41.8 21.4 11.9 2.2 4.7

Argentina 57.1 21.3 51.7 25.1 29.4Maintenance 7.8 9.2 17.5 21.3 16.0

16.92.1

17.19.7

(1)

(6)

(7)(10)

(11)Growth 49.3 12.1 34.2 3.8 13.4

Mexico 60.5 203.1 12.6 12.3 13.8Maintenance 0.5 0.5 7.1 13.4 0.1Growth 60.0 202.6 5.5 (1.1) 13.7

7.4

15.19.45.7

(2)

( )

(8) (12) (14)

( )

Italy 22.5 26.6 5.2 19.0 29.8Maintenance 1.7 3.5 7.2 6.2 3.5Growth 20.8 23.1 (3.3) 12.8 26.3

9.54.25.3

(14)

(3)

(9)(15)

Other 53.0 27.4 22.7 8.5 44.1Maintenance 8.1 14.9 9.8 3.5 7.4Growth 44.9 12.5 12.9 5.3 36.7

Total 280.4 345.7 141.3 86.4 141.3

15.07.27.8

75.7

(8) Bingo Palace (€12m)(9) Codere Network (€6m)(10) Includes acquisition of 49% stake in ICELA and 10% of minorities

(1) Net of repayments from Caliente(2) Numbers for 2007 and 2008 exclude discontinued operations(3) Includes holding company, Panama, Brazil, Colombia and

Total 280.4 345.7 141.3 86.4 141.3Maintenance 63.6 23% 74.0 21% 80.1 57% 63.4 73% 46.5 33%Growth 216.8 77% 271.7 79% 61.2 43% 23.0 27% 94.8 67%

75.747.4 63%28.3 37%

18

( ) q(11) Includes €25.1 million related to the minority purchase(12) Includes €2.8 million in proceeds for the sale in WHCI(13) Includes €11.2 million related to licenses renewals(14) Includes €10 million related to the purchase of the VLT rights(15) Includes €30 million related to the purchase of 6 casinos in Panama

(3) Includes holding company, Panama, Brazil, Colombia and Uruguay.

(4) One-off RF portfolio purchase (5) Includes mainly MAE acquisition(6) Includes 6 license renewals (€30m)(7) Related to the opening of 42 bingo halls

… and driving robust growth in cash generation…

(€ in millions) 2006 2007 2008 2009 2010 CAGR06-10

EBITDA 176 200 233 231 241 8.2%

( ) N t i t t 55 56 66 69 69 5 8%(-) Net interest 55 56 66 69 69 5.8%

(-) Taxes 41 41 47 37 45 2.4%

Operating cash flow 80 104 120 126 126 12.0%

(-) Maintenance capex 64 74 80 63 46 (7.9%)

Discretionary cash flow 16 30 40 63 80 49.5%

( ) Growth capex 217 272 61 23 95 (18 7%)(-) Growth capex 217 272 61 23 95 (18.7%)

Free cash flow (201) (242) (22) 40 (15) n.a.

19

…maintaining prudent leverage ratios and long-dated debt.

€142 million

Prudent leverage Cash as of September 30, 2011

3.9x

3.1x 3.2x2.9x 2.9x

3.1x2.7x

3.2x3.7x 3.5x 3.4x 3.5x 3.6x Europe

41%

(1) (1)

1.0x

2005 2006 2007 2008 2009 2010 Q3 2011

Net debt /LTM EBITDA LTM EBITDA / LTM Net interest

(1) (1)

Others20%

Argentina 24%

Mexico15%

Maturity profile

17% of Argentinein € or US$(1) 2005-2006 EBITDA not adjusted for gains or losses on asset disposals

(€ in millions)

RCF781.2

20.3

2011 2012 2013 2014 2015+

37.7

20

18.311.4 10.0

Operating data (I)

# of machine seats and gaming halls

As of September 30, As of September 30,

2010 2011 % change 2010 2011 % change

Gaming machine seats Gaming halls

Argentina 5,042 5,164 2.4% 14 14 0.0%

Mexico 18,953 18,874 (0.4%) 94 95 0.0%

2 3 930 12 1 16 %(2)

(1)

Italy 2,355 5,930 n.a. 12 14 16.7%

Spain 15,340 15,182 (1.0%) 1 1 0.0%

Panama 3,389 3,382 (1.8%) 12 12 0.0%

C l bi 6 377 6 247 (2 0%) 49 50 2 0%

(2)

(3)

Colombia 6,377 6,247 (2.0%) 49 50 2.0%

Uruguay 1,604 1,856 15.7% 4 5 25.0%

Total 53,060 56,581 6.6% 187 191 2.1%

1- As a result of the Caliente transaction signed on July 16, 2010 data shown for the Caliente part of our Mexican operations corresponds only to the halls included in these new agreements. Data for 2010 has also been adjusted to reflect this change

21

2010 has also been adjusted to reflect this change. 2.- 2011 data includes 762 VLTs

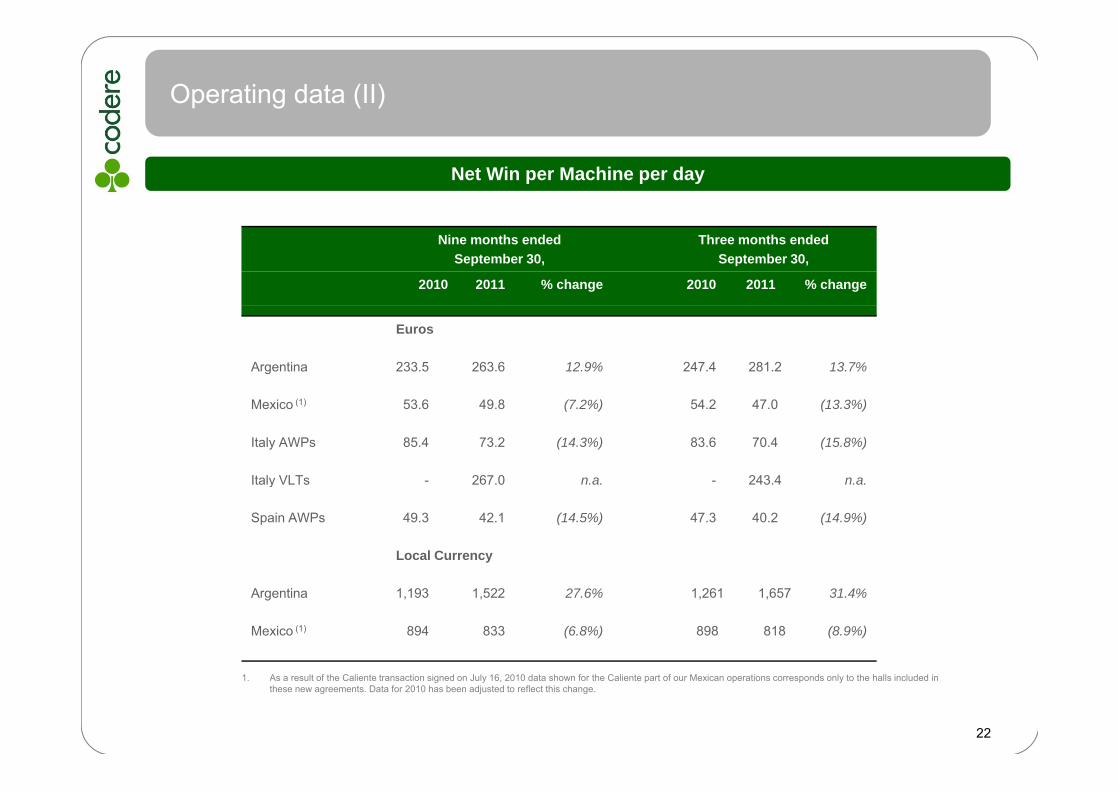

Operating data (II)

Net Win per Machine per day

Nine months endedSeptember 30,

Three months endedSeptember 30,

2010 2011 % change 2010 2011 % change

Euros

Argentina 233.5 263.6 12.9% 247.4 281.2 13.7%

Mexico (1) 53.6 49.8 (7.2%) 54.2 47.0 (13.3%)

Italy AWPs 85.4 73.2 (14.3%) 83.6 70.4 (15.8%)

Italy VLTs - 267.0 n.a. - 243.4 n.a.y

Spain AWPs 49.3 42.1 (14.5%) 47.3 40.2 (14.9%)

Local Currency

Argentina 1,193 1,522 27.6% 1,261 1,657 31.4%

Mexico (1) 894 833 (6.8%) 898 818 (8.9%)

22

1. As a result of the Caliente transaction signed on July 16, 2010 data shown for the Caliente part of our Mexican operations corresponds only to the halls included in these new agreements. Data for 2010 has been adjusted to reflect this change.

Growth and business plan

Business plan is a continuation of succesful growth strategy in ourprincipal markets

• Continue implementation of TITO and other coinless systems• Optimization of hall location and capacity increases

Argentina

Mexico

• Consolidate halls purchased pursuant to Caliente transaction• Improve competitive position of Joint Opcos halls • Continue build-out of permits and installation of machinesp• Continue adaptation of halls to anti-tobacco regulation

Other Latin American O ti

• Uruguay- Continue build-out of Carrasco• Panama- Consolidate synergies following casinos acquisition

Italy• Continue deployment of VLTs in Codere-managed and third party locations• Analyze growth opportunities

Operationsy g g q

• Analyze opportunities in existing or adjacent markets and products

Spain

• Manage effect of anti-tobacco regulation• Achieve synergies from combination of business (AWP, Sports Betting and Bingo)• Consolidate sports betting operations in existing regions and monitor regulatory p g p g g g y

developments in other regions.

Corporate• Continue optimization of intercompany charges• Maintain the effective tax rate• Analyze alternatives to match currency of debt to cash flowsAnalyze alternatives to match currency of debt to cash flows• Explore opportunities to crystallize the value of the business

24

2011 projected KPI growth is in line with track record…

Evolution in the machine portfolio Net wins

2009 2010 2011E2009 2010 2011E

(1) (1)

2009 2010 2011EArgentina

Euros 189.8 236.2% change 24.4%

local currency 989 1,223% h 23 7%

+

2009 2010 2011EArgentina 4,679 5,043 5,396 - 5,547

Absolute change 364 353 - 504% change 7.8% 7% -10%

M i 17 421 19 299 20 264 20 650 % change 23.7%

MexicoEuros 47.0 52.9

% change 12.6% -

Mexico 17,421 19,299 20,264 – 20,650Absolute change 1,878 965 – 1,350

% change 10.8% 5% - 7%

Italylocal currency 883 881

% change (0.2%)

ItalyAWPs

-AWPs 2,181 2,178 +Absolute change (3)

% change (0.1%)

VLTs NA 402 804 1 005Euros NA (1) 86 -

VLTsEuros NA 176.2 +

Spain AWPs 15 587 15 347 -

(1)

VLTs NA 402 804-1,005Absolute change 402 402-603

% change n.a. 100%-150%

Spain AWPs 15,587 15,347Absolute change (240)

% change (1.5%) Spain AWPsEuros 49.2 49.2

% change 0.0%43.2(12.2%)

25

(1) In 2009 the net win for machines placed in bingos was €123.5 and €75 in non-specialized locations

… and expected to generate strong EBITDA growth supported by investments in our key markets

EBITDA

28418%

Total Capex(€ in million) (€ in million)

241

284

28117%

141 141 140

2010 2011E

61

95

65

86(1)

( ) f

Capex

2010 2011E

23

(1) At November 2011 foreign exchange rates

Arg

Others31%

Spain17% Spain 20%

Others21%

Mex

80

63

46

75

Arg. 21%

Mex. 10% Italy

21%

Arg. 30%Italy

18%

Mex11%

6

2008 2009 2010 2011E

26

Maintenance Growth

Outlook 2011: Underlying assumptions and expectations

● Assumptions○ Foreign exchange rates based on forward rates on November 4, 2011

Avg. Averages based on FX forwards as of August 17, 2011 % change 10 vs. 11FY 10 1Q 11A 2Q 11A 3Q 11A 4Q 11F Avg. FY 11

€/AR$ 5.19 5.51 5.87 5.89 5.98 5.81 11.9%

€/MXP 16 74 16 59 16 91 17 41 18 50 17 35 3 6%

● Expectations○ Reported EBITDA expected in range of €281-€284 million

€/MXP 16.74 16.59 16.91 17.41 18.50 17.35 3.6%

€/US$ 1.32 1.37 1.44 1.41 1.39 1.40 6.1%

○ EBITDA projected to improve throughout the year as positive factors progressively outweigh negative factors impacting 2011.• Positive factors:

– Consolidation of Panama casinos– Increases in machine park in Argentina and Mexico– Increases in net win in Argentina– Gradual deployment of VLTs in Italy– Consolidation of Italian acquisitions

• Negative factors:– Implementation of anti-tobacco legislation at national level in Spain on January 2 2011Implementation of anti tobacco legislation at national level in Spain on January 2, 2011– Weak performance of Joint Opcos– Costs associated with new ventures (Carrasco in Uruguay, Internet, Sports Betting in new regions)

• Fourth quarter reported EBITDA expected in range of €72-75 million, compared to €68.9 million in Q4 2010 and €74 2 million in Q2 20112010 and €74.2 million in Q2 2011

27

Icela Option Agreement

Rationale● Achieves strategic objective of becoming majority

Agreement● Signed August 15 2011 ● Achieves strategic objective of becoming majority

owner of all licenses which the Company operates in Mexico

● Consolidates market leadership position in Mexico

● Signed August 15, 2011

● Non-binding option to purchase additional 36% stake in ICELA from CIE

● Gives Codere full control of the day-to-day operations of the business

● ICELA operates 53 halls, next largest players manage c 26 halls

● Purchase price MX$ 2,657 million (c. €144MM) 1

● Subject to certain conditions to closing manage c. 26 halls

● Increases weight of Mexican operations, with potential efficiencies for Codere, including possibility to transfer debt to subsidiaries

● Subject to certain conditions to closing

● COFECO approval October 31, 2011

● Expect to fund with debt financing

(€ in millions) Transaction Proforma

R t d Adj t t PFReported Adjustment PF Transaction

LTM EBITDA September 2011

278 40 318

28(1) At November 14, 2011 €/MX$ of 18.40 (2) Adjustment is equity value for 35.8% (€144MM) +51% of net debt assumed (€32MM)

Net Debt 2 737 176 1 913

EBITDA/Net Debt 2.7x 4.3x 2.9x

The Brazilian market presents a significant opportunity…

• Private gaming is illegal excluding betting on horse races

Private gaming in Brazil

• An estimated 1,100 bingo halls with machines operated as a “gray market” throughout the country prior to a government crack down in 2004

• Codere present in Brazil since 2004 is uniquely positioned for the

Brazil

• Codere, present in Brazil since 2004 is uniquely positioned for the regulation of the activity

•Codere has 10-year exclusivity agreements with major jockey clubs to offer betting services, including on international simulcast racing

Alternatives for Codere

BA

Operator of machines in the racetracks operated by the jockey clubs with

which Codere has

Operation of bingo halls with machines

throughout the country

Pote

ntia

l A

ctiv

ity

agreementsP Asa

ry

tion

29

Decree by Ministry of Agriculture

National law

Nec

ess

regu

lat

… and the company is developing know-how in on-line gaming in anticipation of regulation of the Latin American and Spanish marketsp g p

● Began on-line activities November 2010

○ Launched www.codere.it, an interconnected web of online bingo in Italy, with SISAL, among the leading gaming operators in that country

○ Announced agreement with Playtech to source software applications and technology○ Announced agreement with Playtech to source software, applications and technology

● Italy launch marks first of what are expected to be a number of online initiatives which we expect to develop in Latin America and Spain, upon regulation of the activity

● Currently, Italy is the only jurisdiction in which Codere operates which has regulated on-line gaming

30

● Expect on-line activities to reinforce our leadership position in the off-line market

Key investment highlights

Compelling growth story in Latin America

• Strong track record of organic and non organic growth• Low gaming penetration in a context of high GDP growth rates in Latin America• Well positioned for legalization of gaming halls in Brazil and launch of on-line

• #1 gaming operator in the Province of Buenos Aires, in Mexico and casino operator in Panama

yand Italy activities in Latin America

• Competitive advantage in nascent VLT market in Italy

in Panama• Leading market position in Italy (#1 in bingo) and Spain (#2 in AWP machines)• Market share of c. 50% in Argentina and in c. 41% Mexico, the two largest markets• Entrenched operator with key local relationships and licenses in a highly regulated

market

Leading position in all markets

market• First mover advantage in most markets

Strong management• Experienced management team and Board with unique knowledge of the business• Proven track record navigating market cyclesStrong management

team and operations g g y

• Unrivaled local market expertise• Six years reporting as a public company

• Limited near-term maturitiesStrong balance sheet and cash flow profile

ed ea e a u es• Cash generative business• Low maintenance capex• Flexible investment program

Unique international gaming footprint with exceptional growth potential31

Supplementary materials- FY 2010 and Q2 2011 results and updated guidance

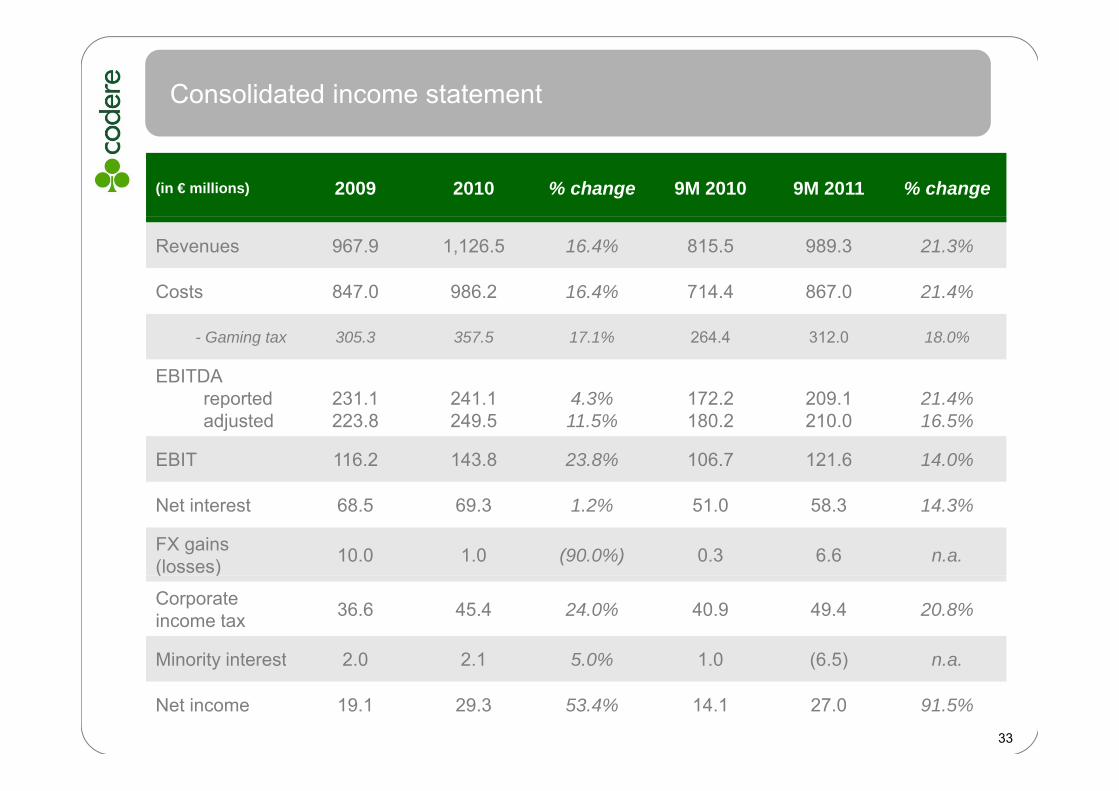

Consolidated income statement

(in € millions) 2009 2010 % change 9M 2010 9M 2011 % change

Revenues 967.9 1,126.5 16.4% 815.5 989.3 21.3%

Costs 847.0 986.2 16.4% 714.4 867.0 21.4%

- Gaming tax 305.3 357.5 17.1% 264.4 312.0 18.0%

EBITDA reported 231 1 241 1 4 3% 172 2 209 1 21 4%reportedadjusted

231.1223.8

241.1249.5

4.3%11.5%

172.2180.2

209.1210.0

21.4%16.5%

EBIT 116.2 143.8 23.8% 106.7 121.6 14.0%

Net interest 68.5 69.3 1.2% 51.0 58.3 14.3%

FX gains (losses) 10.0 1.0 (90.0%) 0.3 6.6 n.a.( )

Corporateincome tax 36.6 45.4 24.0% 40.9 49.4 20.8%

Minority interest 2.0 2.1 5.0% 1.0 (6.5) n.a.Minority interest 2.0 2.1 5.0% 1.0 (6.5) n.a.

Net income 19.1 29.3 53.4% 14.1 27.0 91.5%

33

Focus on cash flow generation

2009 Q3 20102010 Q3 2011

EBITDA

Net interest

231

68 69

241 62

18

74

19Net interest

Income tax

Operating CF

37

126 126

45

30

14

38

17

M capex

Discretionary CF

63

63 80

46

12

18

22

16

G capex

Free CF 39

23 95

(15)

42

(30)

11

12

Strong cash flow growth driven by tight discipline on capital expenditure

34

Strong cash flow growth driven by tight discipline on capital expenditure

Debt breakdown

Effective interest rate Final Maturity € million Currency

As of September 30, 2011

(1)HQ (Bond) 8,25% 2015 765,2 EURHQ (RCF) Euribor + 4,50% 2013 20,3 EURSpain 3,96% 2012 - 2025 2,3 EURMexico TIIE + 3,50% 2014 17,2 MXNMexico- Icela TIIE + 2,27% 2015 26,9 MXNMexico Icela TIIE + 5 00% 2011 5 4 MXN

(1)

Mexico- Icela TIIE + 5,00% 2011 5,4 MXNItaly 4,10% 2012 - 2014 15,5 EUR

PanamaLíbor 3M + 3,50%

(Floor 6,75%) 2016 15,9 USD

Sub - Total 868,6Sub Total 868,6

Uruguay (HRU) 4,79% 2011 10,3 UYU / UI

Total 878,9

Distribution of debt by currency3% Othercurrencies6% Mx$

(1) Includes €18.3 MM of interest

91% euros

currencies

Euros Mx$ Other currencies 35

9 % eu os

Debt structure and headroom

11.713.2 88.833.532.323.0

(141.3)

(€ in millions, at September 30, 2011)

878.9Senior Debt

(141.3)

737.3790.1765.2

Bonds (1) Pari Passu @ subs.

Unrestricted RCF (2) ICELA (49%)

Senior @ subs.

GrossDebt

Cash & equivalents

Net Debt( ) Debt

Headroom under senior● Maximum Senior under HY:€200MM● (-) Senior balance:

Debt TermsBank financing:● New Senior Facility Agreements renewed June 15, 2010

Key bond covenants● 3.0x FCCR incurrence test

○ RCF (2) (€23 MM)○ ICELA (100%) (€66MM)○ Senior @ subs (€33MM)○ Other debt (3) (€19 MM)

(€141MM)

○ €120MM multicurrency revolving credit facility • €60MM cash and LC at Euribor (or Libor) + 4.5%• €40MM LC at 4.5%• €40MM Surety bonds between 1.3% - 4%

○ Key covenants:

● €200m senior debt limit

Between both, not more than €60 millions

36

(€141MM)● Senior Headroom: €59MM(1) Includes €18.3MM of interest(2) Gross amount excludes €2.7 MM in expenses(3) Includes non-financial debt

y• Net financial debt / EBITDA <4.25x• Net senior debt / EBITDA <1.5x• EBITDA / Net interest >2.5x

○ Arranged by CS, Barclays, BBVA and HCC

Revenues and EBITDA evolution

(US$ in millions) 2006 2007 2008 2009 2010 2006 2007 2008 2009 2010Argentina 298 410 518 491 610 106 135 162 154 180

EBITDARevenues

Mexico 125 199 341 269 290 54 79 101 84 84Panama 43 60 67 67 82 9 16 14 14 5Colombia 39 47 39 32 36 7 (0) 9 7 7Uruguay 25 29 19 21 22 3 4 5 5 4Brazil 0 2 3 3 4 (5) (8) (3) (0) (3)( ) ( ) ( ) ( ) ( )HQ & Other 4 ‐ ‐ ‐ ‐ (20) (25) (38) (16) (26)Latam operating revenues 534 747 988 883 1,046 154 201 249 248 252Spain 261 311 346 283 263 74 98 90 58 59Italy 107 148 208 182 182 7 (15) 18 21 19HQ adjusted 1 1 3 2 0 (8) (9) (14) (5) (14)

(1)

(2)(1)

(€ in millions) 2006 2007 2008 2009 2010 2006 2007 2008 2009 2010Argentina 242 299 352 352 461 86 98 110 110 136

HQ adjusted 1 1 3 2 0 (8) (9) (14) (5) (14)Total Codere 902 1,207 1,544 1,350 1,492 226 275 343 322 316

Avg FX Rates 1.23 1.37 1.47 1.39 1.32 1.23 1.37 1.47 1.39 1.32

Argentina 242 299 352 352 461 86 98 110 110 136Mexico 101 145 232 193 219 43 58 69 60 64Panama 35 44 45 48 62 8 12 10 10 4Colombia 31 34 27 23 27 6 (0) 6 5 5Uruguay 20 21 13 15 17 3 3 3 4 3Brazil 0 2 2 2 3 (4) (6) (2) (0) (2)HQ & Other 3 ‐ ‐ ‐ ‐ (16) (18) (26) (12) (20)Latam operating revenues 433 545 672 633 790 125 146 169 178 190Spain 211 226 235 203 199 60 71 61 42 44Italy 87 108 141 131 137 5 (11) 12 15 14

(1)

y ( )HQ adjusted 1 1 2 1 0 (7) (7) (10) (3) (8)Total Codere 732 880 1,050 968 1,127 184 200 233 231 241

37(1) Split according to regional contrbution(2) Includes the internet business for 2009 and 2010

(2)(1)

Supplementary materialsSupplementary materials- Other

Shareholder structure

Masampe PIK loan

At September 30, 2011

OTHER BOARD Term Description

Issue amount €340.0 million

Issue date June 2007

Use of proceeds Purchase shares of Codere S.A.BOARD

OTHER BOARD MEMBERS 0.6% JAMS

12.4%

JMS 2 5%

17.1%

p

Amount held by MS 10% of the nominal (not cancelled)

Bloomberg code XS0305817842 Corp

Maturity 15 December 2015 (6 month outside existing HY)

FREE FLOAT30.2%

BOARD MEMBERS

17.8%

2.5%

EMS2.2%

EMS 2.2%

Maturity 15 December 2015 (6 month outside existing HY)

Interest 3 months EURIBOR + 750 bps.

Par call window From June 2008 to December 2009

Covenant Net debt to EBITDA < 6.5xMASAMPE HOLDING* MS FAMILY

MS FAMILY68 5% Mandatory

PrepaymentIf Masampe fails to own at least 50.1% of the issued and outstanding shares of Codere S.A.

Principal amount outstanding as

of September 30, €519.6 million

HOLDING*51.3%

MANAGEMENT

MS FAMILY68.5%

68.5%

20110.7%MANAGEMENT 0.7%

* Masampe Holding Partners: JAMS, LJMS y EMS

Total Shares Outstanding: 55,036,470

39

Argentine licenses

(1) (2)(2)(3)

(2) (2)(1)

% consol. Sales 10 % Argentine sales 10 % consol. EBITDA 10 % Argentine EBITDA 10Ar$ EURO AR$ EURO 1.136,9 467,4 251,5 142,1

1 Mar Sep-06 Mar-07 Jun-21 14,3 2,5 33,4 5,9 0,9% 2,3% 0,9% 1,6%2 Lomas de Zamora Jul-06 Jun-07 Jun-21 16,6 2,9 38,6 6,8 2,6% 6,3% 3,6% 6,3%3 Sol Jun-06 Mar-07 Jun-21 15,6 2,8 36,9 6,5 1,9% 4,7% 2,6% 4,7%

Original expiration

Renovation date

Renewal through

Hall Up-front fee (MM) Canon tax surcharge (MM)(1) (1) (2) (2) (2) (2)

3 Sol Jun 06 Mar 07 Jun 21 15,6 2,8 36,9 6,5 1,9% 4,7% 2,6% 4,7%4 Peatonal Jun-06 May-07 Jun-21 5,7 1,0 13,4 2,4 0,5% 1,3% 0,8% 1,4%5 Lanus Apr-07 Apr-07 Jun-21 38,2 6,8 89 15,7 4,9% 12,0% 7,3% 12,9%6 Platense Jun-07 Oct-09 Jun-21 28,4 5,0 137,7 24,3 4,9% 11,9% 6,8% 12,0%7 San Martín Oct-09 jun-10 jun-21 55,5 9,8 72,3 12,8 5,6% 13,7% 10,1% 17,9%8 Puerto Jan-09 jul-10 jun-21 5,5 1,0 7,2 1,3 0,4% 1,0% 0,8% 1,4%9 M ó J 13 4 2% 10 3% 7 7% 13 6%9 Morón Jun-13 4,2% 10,3% 7,7% 13,6%

10 Ramos Mejía Apr-14 2,1% 5,0% 3,2% 5,6%11 San Miguel May-14 3,5% 8,4% 6,2% 11,0%12 Lomas del Mirador Sep-14 5,1% 12,4% 9,9% 17,6%13 San Justo Oct-14 4,0% 9,7% 7,4% 13,2%14 Temperley Aug-16 0,4% 1,0% 0,6% 1,0%

Central -11,3% -20,1%

TOTAL 41,1% 100,0% 56,5% 100,0%

Renewal fee Canon Surcharge (3) EBITDA 10Ar$ Renewal fee Canon surcharge Total Surcharge canon % EBITDA 10Ar$

Total Charges / EBITDA Yearly

(1) Based on the Eur/Ar$ exchange at September 30 2011

Platense 28,4 137,7 166,1 87,9 0,3x 1,6x 1,9x 27,54 31,3%Puerto 5,5 7,2 12,7 10,0 0,6x 0,7x 1,3x 1,44 14,4%

San Martin 55,5 72,3 127,8 131,5 0,4x 0,5x 1,0x 14,46 11,0%

(2) Exclude the gains or losses on the foreign exchange contracts.

(1) Based on the Eur/Ar$ exchange at September 30, 2011

(3) Payable monthly over 5 years

40

Smoking bans overview

ScopeEffective

DateRegulation for gaming venues

General regulation

Italy National Jan 2005 50%* of total surface Total ban No clear effectsItaly National Jan. 2005 50% of total surface Total ban

Spain National Jan. 2011 Total ban (3) Same as gaming

No clear effects identified

Daily win reductionUruguay National March 2006 Total ban Same as gaming

MexicoD.F. April 3, 2008 Total ban

Same as gamingMaximum of 33%* of total

Daily win reduction of up to 15%.

Recovery in 9 to 12 months

Daily win reduction of up to 20% Recovery

National July 1, 2009 (1) Maximum of 33% of total surface (TBD by state)

Panama National April 25, 2008 Total ban Same as gaming

Distrito Mar Total ban (3)

Daily win reduction of up to 15%. Recovery

in 6 months

up to 20%. Recovery in 12 months

Argentina (Prov Bs.As.)

Distrito Mar del Plata April 25, 2011

Total ban (3)Same as gaming

National June 1, 2011 Pending regulation on Prov. Bs As (2) Total ban

Colombia National Dec. 4, 2008 Total ban Same as gaming

There is a world trend to regulate smoking in public places. Codere’s experience suggests a

Daily win reduction around 10%.

Recovery in 9 months

41

There is a world trend to regulate smoking in public places. Codere s experience suggests a moderate negative impact in revenues but with a recovery in the medium term

* Percentage of space allowed for smokers(1) Effective date of the Federal regulation that develops the Federal Act (2) Since April 2009 there is a total ban in the Prov. Bs As with exception of gaming halls(3) In 2006 and 2007 in Spain and Mar del Plata, respectively there was a partial ban implemented

Comparative gaming taxes

Machine Gaming Taxes(As percentage of Net Win)

Comments

24% 48%Spain

(As percentage of Net Win)●Fixed gaming tax per machine, “tasa”, that differs by

Comunidad Autónoma. In 2010, the average annual tax per machine was circa €3,600. The stated percentage was determined considering Codere’s actual average net win levels M f 12 6% + 0 8% (i l di PREU + C )

Over Codere’sshare of Net Box

54%

36%

Italy

Argentina

●Max. of 12.6% + 0.8% (including PREU + Canon) over amounts wagered (“coin-in”). The stated percentage was determined based on the current pay out ratio (75%)

● Includes payments to Non Profit Organizations (2% of net win, on average, in 2010). Canon tax surcharge of renewed halls %

30%

g

Mexico

g , ) gsuppose, on average, an extra 7% to 12% of total net win for these halls

●Federal tax of 30% over net win from January 2010. Reimbursement of SEGOB and state taxes at 100%.

12.5%Panama●Fixed percentage over slot machines net win. Increased

January 2010. Slots in racetrack remain 10% of net win.

●Depending on the installed portfolio. After the tax reform (Feb. 2010) gaming taxes are calculated as a % of the net win.

17%

60%

Colombia

Uruguay

2010) gaming taxes are calculated as a % of the net win.

●Percentage of net win that the “Dirección General de Casinos” (DGC) withholds to Codere for the operation of the halls. No further gaming taxes exist

42

g y

Simpleaverage 33%

Management of foreign exchange exposure

Risk SourceForeign Exchange Risk Coverage

Practice

● Foreign exchange risk is principally related to the potential negative impact in the consolidated financial statements (denominated in euros) of non euro currencies devaluations against the euro

● Contract foreign exchange forwards on a rolling forward four-quarter basis for approximately 50% of projected Argentina and Mexico EBITDA

● The Argentine Peso (Ar$) and the Mexican Peso (Mx$) are the most relevant sources of foreign exchange risk as operations in those countries generated the 53% and 19% of the EBITDA(1) for 9M

● Make financial projections based on forwards rates available on the market

Forwards contracted as of November 15, 20112011, respectively

Risk Mitigation By Natural Coverage

● In addition to forward contracts, natural coverage l l t l i f i h i k

(in millions)

€/Mx$ US$/Mx$ €/US$

- - 21.2

Quarter €/Ar$ US$/Ar$

4Q11 - 28.0

1Q12 28 0plays a relevant role in foreign exchange risk mitigation as most significant operating cost (typically gaming taxes and personnel expenses) are denominated in local currency

21.2--

---

- - -

- - -

116.0-Total

30.0-2Q12

3Q12 - 30.0

1Q12 - 28.0

43(1) EBITDA pre Headquarters' costs

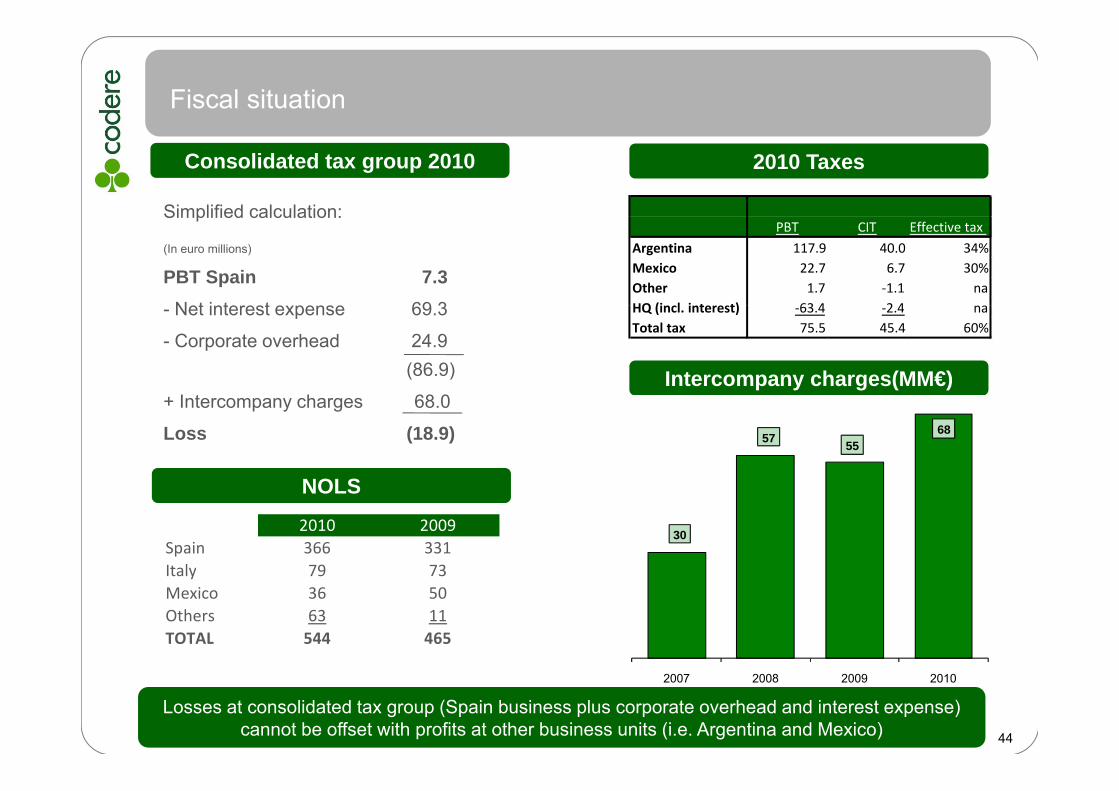

Fiscal situation

2010 TaxesConsolidated tax group 2010

Simplified calculation:PBT CIT Effective tax

Argentina 117.9 40.0 34%Mexico 22.7 6.7 30%Other 1.7 ‐1.1 naHQ (incl interest) 63 4 2 4 na

Simplified calculation:

(In euro millions)

PBT Spain 7.3Net interest expense 69 3

Intercompany charges(MM€)

HQ (incl. interest) ‐63.4 ‐2.4 naTotal tax 75.5 45.4 60%

- Net interest expense 69.3

- Corporate overhead 24.9(86.9)

I t h 68 0+ Intercompany charges 68.0

Loss (18.9)

NOLS

57 5568

NOLS

302010 2009

Spain 366 331Italy 79 73Italy 79 73Mexico 36 50Others 63 11TOTAL 544 465

44

Losses at consolidated tax group (Spain business plus corporate overhead and interest expense) cannot be offset with profits at other business units (i.e. Argentina and Mexico)

2007 2008 2009 2010

Strategic initiatives

#1 Match currency of debt to cash flows

- Refinance portion of euro bond with us dollar bond (portable to Latam)Refinance portion of euro bond with us dollar bond (portable to Latam)

- Finance acquisition of ICELA stake in US dollars or Mexican pesos

#2 Explore opportunities to crystallize value of the businessp pp y- IPO of minority stake in Latam business (listing in US markets)

• Position company relative to US gaming companies and Latin American comps trading at higher multiples than European gaming comps

• Use proceeds to repay remaining eurobond at HQ = reduction in effective tax rate

45

Selected economic indicators

Real GDP% CPI

2010 2011E 2012E 2010 2011E 2012E

Argentina 9.2 7.1 3.1 21.5 23.5 26.1

Mexico 5.4 3.7 3.2 4.4 3.3 3.6

Italy 1.2 0.6 (1.0) 1.5 2.8 2.1

Spain (0.1) 0.7 (1.0) 1.8 3.3 1.5

Latam 6.3 4.4 3.5 6.8 6.6 6.2

Source: Morgan Stanley, except Argentine CPI (Barclays)

Average exchange ratesAverage exchange rates

2007 2008 2009 2010 07/08 08/09 09/10

EUR/Ar$ 4.28 4.63 5.22 5.19 8.2% 12.8% (0.6%)

EUR/Mx$ 14.99 16.32 18.83 16.74 8.9% 15.3% (11.1%)

EUR/US$ 1 37 1 47 1 39 1 32 7 3% (5 2%) (5 0%)

46

EUR/US$ 1.37 1.47 1.39 1.32 7.3% (5.2%) (5.0%)

Source: Central Banks

Long term contracts

9

3

Italy VLTs & network

Italy AWP machines

12

10

10

Italy bingos

Spain AWP machines

Spain Sports betting

25

20

15

Mexican halls and racetrack

Panamá casinos & racetrack

Argentine halls

30

25

0 5 10 15 20 25 30 35

Uruguay racetrack and casino

Mexican halls and racetrack

Years (1)

1- Indicates number of years at inception and the maximum term of the contracts where they vary

Di ifi d tf li f l t t t

47

Diversified portfolio of long term contracts

Caliente Agreement

Rationale● Achieves strategic objective of owning all licenses

AgreementAcquisition by Codere of majority stake in three ● Achieves strategic objective of owning all licenses

which the Company operates in Mexico

● Consolidates market leadership position in Mexico

Acquisition by Codere of majority stake in three

Caliente licensees which hold an aggregate of 46

permits (32 halls in operation at July 2010) throughout

Mexico (‘Joint OpCos’)

● Gives Codere full control of the day-to-day operations of the business

( p )

Phase 1 –Effective July 2010

● Mgmt Services Agreement between Codere and

● Simplifies and streamlines relationship with Caliente

Joint OpCos: $36m annually through 2014, plus $1m monthly from July 1, 2010 through December 31st 2010 or Cofeco approval

● Management Services Agreement between

● Significantly reduces obligations from Caliente

● Increases weight of Mexican operations, with

g gCodere and Promojuegos and Mio: $8m annually through 2014

● Codere loan to Joint OpCos (“Caliente RCF”)

Ph 2 Eff i C f l potential efficiencies for Codere, including possibility to transfer debt to subsidiaries

● Adds €19 7m to pro forma 2009 EBITDA

Phase 2- Effective upon Cofeco approval

(approved in May 2011)

● Codere acquires 67.3% of Joint OpCos (Caliente will hold remaining 32.7%)

48

● Adds €19.7m to pro forma 2009 EBITDAwill hold remaining 32.7%)

● Caliente acquires 32.7% share in Promojuegosand Mio for $5.1m ( 32.7% of $15.5m)

Supplementary materialsSupplementary materials- Resistance of business

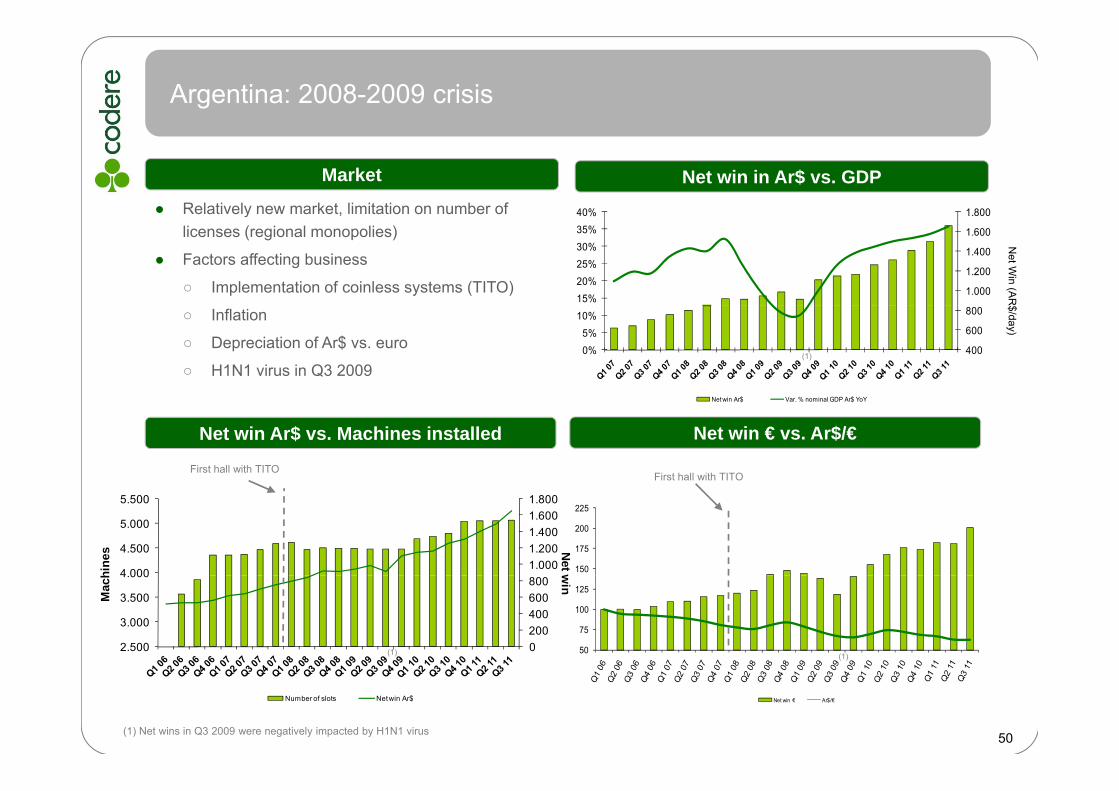

Argentina: 2008-2009 crisis

40% 1.800

Market

● Relatively new market, limitation on number of

Net win in Ar$ vs. GDP

15%20%25%30%35%

%

1.000

1.200

1.400

1.600

y ,licenses (regional monopolies)

● Factors affecting business

○ Implementation of coinless systems (TITO)

Net W

in(A

R

0%5%

10%

400

600

800○ Inflation

○ Depreciation of Ar$ vs. euro

○ H1N1 virus in Q3 2009(1)

$/day)

Net win Ar$ Var. % nominal GDP Ar$ YoY

Net win Ar$ vs. Machines installed Net win € vs. Ar$/€

First hall with TITOFirst hall with TITO

4 000

4.500

5.000

5.500

1.0001.2001.4001.6001.800

hine

s Net w 150

175

200

225

2.500

3.000

3.500

4.000

0200400600800

Mac

h win

50

75

100

125

(1) (1)

Number of slots Net win Ar$ Net win € Ar$/€

50(1) Net wins in Q3 2009 were negatively impacted by H1N1 virus

Argentina 2001-2002 Devaluation and “Corralito”

● December 31, 2001 Argentine government eliminated Peso peg to US$

Net Win per Day in US$

● Peso devalued 67% versus US$ in 2001-2002

● By August 2003 net win per machine was back to July 2001 levels in real terms

● 2002 EBITDA decreased 25% in euro terms following4 0

6 0

8 0

10 0

12 0

14 0

AR$

/ US$

de

valu

atio

n

2002 EBITDA decreased 25% in euro terms following the devaluation of the Peso

● Strong profitability maintained throughout economic crisis

0

2 0

4 0

Dec-

01

Jan-

02

Feb-

02

Mar

-02

Apr-

02

May

-02

Jun-

02

Jul-

02

Aug-

02

Sep-

02

Oct-

02

Nov-

02

Dec-

02

Jan-

03

Feb-

03

Mar

-03

Apr-

03

May

-03

Jun-

03

Jul-

03

Aug-

03

Net Win per Day (constant July 2001 pesos) EBITDA

220

6 6 222

228 54.0

(Ar$m / US$m / EURm)Devaluation

$2

$167

$150 $1

58

$161

$144

$178

$175

$200

$172

$172

$175 $181

$185

$154 $1

75

$180

$178 $1

97

$189 $2

06

$192 $2

06

$202 $2 $

32.032.0

18.115 7

Jul-0

1

ug-0

1

ep-0

1

Oct

-01

ov-0

1

ec-0

1

an-0

2

eb-0

2

Mar

-02

Apr-

02

ay-0

2

un-0

2

Jul-0

2

ug-0

2

ep-0

2

Oct

-02

ov-0

2

ec-0

2

an-0

3

eb-0

3

Mar

-03

Apr-

03

ay-0

3

un-0

3

Jul-0

3

ug-0

3

14.010.810.2

14.0 14.8

9.611.8

15.7

2001 2002 2003 2004

51

J A S O No

D J F M A M J J A S O No

D J F M A M J J A

-4.5% -10.9% +8.7%

GD

P

+9.0%

Net wins in US$ in Argentina have not been correlated withdevaluation of AR$

Codere net wins (US$) vs. AR$/US$ devaluation since 2006

200

250Var. % 06-11

+135.8%

100

150

50

100Var. % 06-11

(26.3%)

STRICTLY CONFIDENTIAL

0

Q1 06

Q2 06

Q3 06

Q4 06

Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Net win in Usd UsdArs FxNet win in Usd UsdArs Fx

Mexico: 2008-2009 crisis

16% 1.100

Market

● Newly regulated market (machines allowed 2005)

Net win in Mx$ vs. GDP

4%

8%

12%

800

900

1.000

y g ( )

● Factors affecting business

○ Aggressive machine deployment

○ Competition from illegal players

Net W

in(M

X

-8%

-4%

0%

500

600

700○ Smoking bans (D.F. 2008 and national 2009)

○ Depreciation of Mx$ vs. euro

○ H1N1 virus Q2 2009 (1)(2)

X$/day)

Net win MxP Var. % nominal GDP MxN YoY

Net win Mx$ vs. machines installed Net win € vs. Mx$/€Smoking bansSmoking bans

75

100

125

16.000

20.000

24.000

800

1.000

1.200

hine

s

Net w

in (

Smoking bansS o g ba s

0

25

50

4.000

8.000

12.000

400

600

800

# of

Mac

(MX

$/day)

(1)(1)

(2)(2)

53

Net win in € Mx$/€

# of machines Net win Mx$

(1) Net wins in Q2 2009 were negatively impacted by H1N1 virus

(2) As a result of the Caliente transaction signed on July 16, 2010 data shown for the Caliente part of our Mexican operations corresponds only to the halls included in these new agreements .

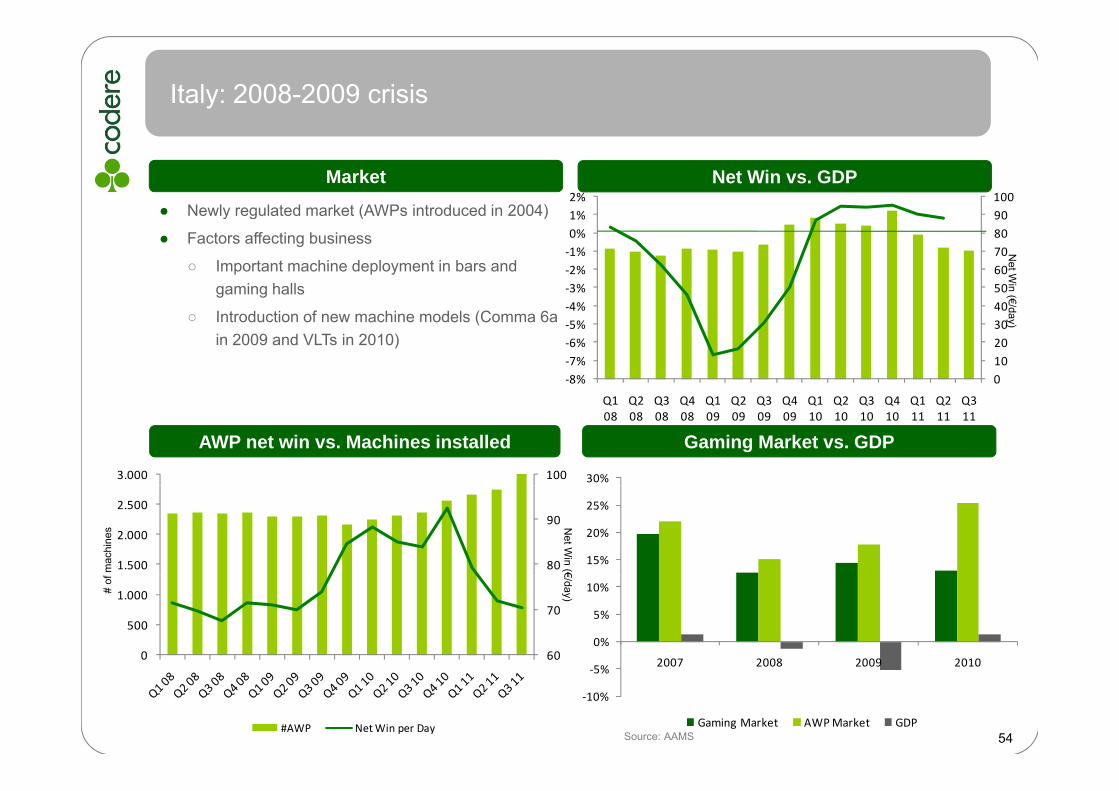

Italy: 2008-2009 crisis

1%2%

90100

Net Win vs. GDPMarket

● Newly regulated market (AWPs introduced in 2004)

4%‐3%‐2%‐1%0%1%

405060708090y g ( )

● Factors affecting business

○ Important machine deployment in bars and gaming halls

Net W

in(€/

‐8%‐7%‐6%‐5%‐4%

010203040

○ Introduction of new machine models (Comma 6a in 2009 and VLTs in 2010)

/day)

1003.000

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Net Win Italy AWPs Var. % nominal GDP YoY

30%

AWP net win vs. Machines installed Gaming Market vs. GDP

80

90

1.500

2.000

2.500

15%

20%

25%

Net W

in(€m

achi

nes

60

70

0

500

1.000

0%

5%

10%

2007 2008 2009 2010

€/day)# of

#AWP Net Win per Day

‐10%

‐5% 2007 2008 2009 2010

Gaming Market AWP Market GDP54Source: AAMS

Spain: 2008-2011 crisis

6210%

Net win vs. GDPMarket

● Mature, highly fragmented AWP market Smoking ban

38

42

46

50

54

58

(4%)(2%)

-2%4%6%8%

(€/ day)

, g y g

● Factors affecting business

○ Significant macroeconomic downturn

○ Absence of regulatory changes

34

38

(6%)(4%)

Net win Spain AWP Var. % nominal GDP YoY

○ Lack of technological innovation

○ Smoking ban January 2, 2011

100130

Spain AWP vs Spanish Small - Mid Caps Spain AWP net win vs. Spanish indicators

Revenues in Spain

60

80

100

20

40

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 40

70

55

07 07 07 08 08 08 08 09 09 09 09 10 10 10 10 11 11 11Q1 07

Q2 07

Q3 07

Q4 07

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

CDR Spain AWP Media group Hotel sector

Beauty / Healthcare sector Media group

Spain AWP CDR Car registrations

Consumer confidence indexMortages Cement consumption

For further information, please contact:

Investor Relations Department

Tel. +34 91354 [email protected]