39

COVID-19 SMALL AND MEDIUM ENTERPRISE SENTIMENT TRACKER – WAVE 17 – 24 th September 2020

COVID -19 SMALL AND MEDIUM ENTERPRISE

SENTIMENT TRACK ER

– W A V E 1 7 –

2 4 t h S e p t e m b e r 2 0 2 0

ABOUT US

ACA Research & Fifth Quadrant have worked closely with TEG Insights on

business and consumer research projects for over a decade. Our strong partnership allowed us to collaborate

on this new tracker aiming at understanding the impact of COVID-19 on SMEs during these unprecedented

times.

Please do not hesitate to contact us should you have any questions!

T W O B R A N D S O P E R A T I N G U N D E R A S I N G L E M A N A G E M E N T

ACA Research is a full-service market research consultancy, with a strong focus

on B2B projects.

Our consultants provide strategic qualitative and quantitative research

solutions to support business decision making.

Fifth Quadrant is our specialist customer experience brand providing industry analysis, benchmarking, research and

consulting services.

Our consultants work on strategic and operational projects to help clients

optimise CX delivery and reduce cost to serve.

TEG Insights is committed to delivering quality data, analytics and online

research services with access to one of Australia’s largest and most responsive online research panels. Our wide reach

includes professionals, from small business owners to executives, across a

variety of industries.

Our continued success is based on integrity and passion to ensure the best

outcomes for both our Clients and Members alike.

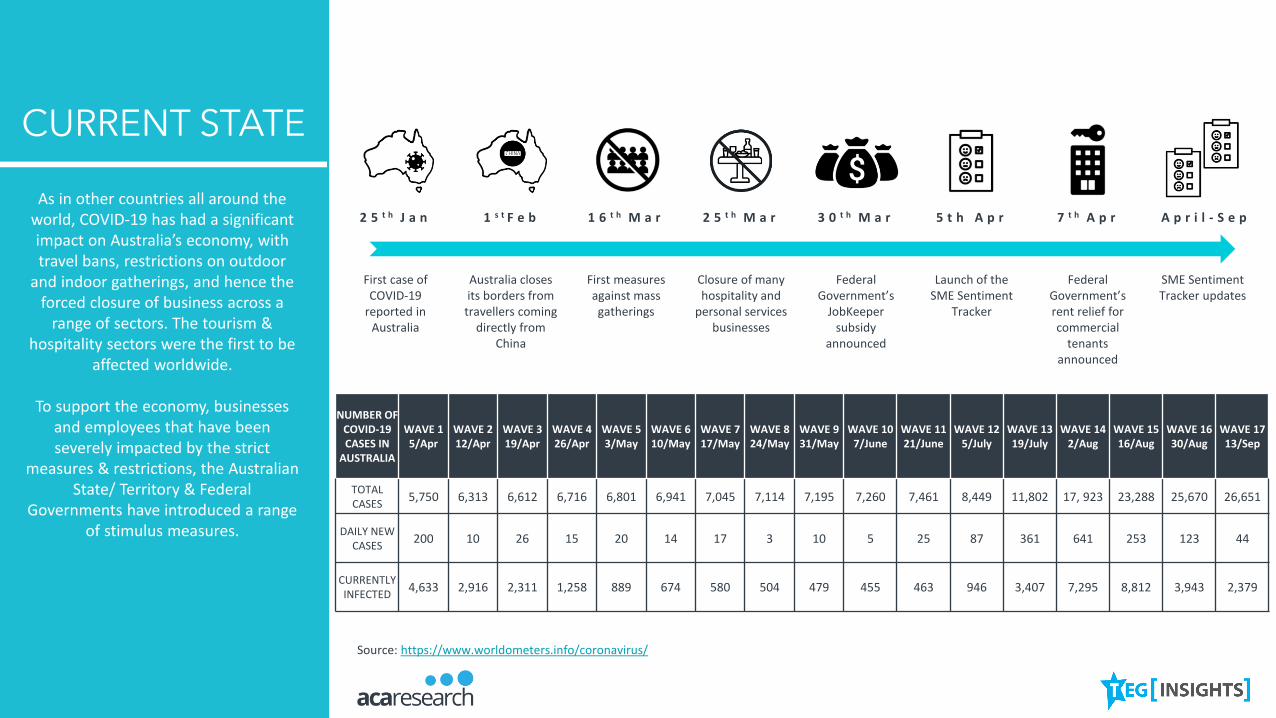

CURRENT STATE

As in other countries all around the world, COVID-19 has had a significant impact on Australia’s economy, with travel bans, restrictions on outdoor

and indoor gatherings, and hence the forced closure of business across a

range of sectors. The tourism & hospitality sectors were the first to be

affected worldwide.

To support the economy, businesses and employees that have been severely impacted by the strict

measures & restrictions, the Australian State/ Territory & Federal

Governments have introduced a range of stimulus measures.

First case of COVID-19

reported in Australia

2 5 t h J a n

Australia closes its borders from

travellers coming directly from

China

1 s t F e b

First measures against mass gatherings

1 6 t h M a r

Closure of many hospitality and

personal services businesses

2 5 t h M a r

Federal Government’s

JobKeeper subsidy

announced

3 0 t h M a r

Launch of the SME Sentiment

Tracker

5 t h A p r

Federal Government’s rent relief for commercial

tenants announced

7 t h A p r

SME Sentiment Tracker updates

A p r i l - S e p

Source: https://www.worldometers.info/coronavirus/

NUMBER OF COVID-19 CASES IN

AUSTRALIA

WAVE 1 5/Apr

WAVE 2 12/Apr

WAVE 3 19/Apr

WAVE 4 26/Apr

WAVE 5 3/May

WAVE 610/May

WAVE 717/May

WAVE 8 24/May

WAVE 9 31/May

WAVE 10 7/June

WAVE 11 21/June

WAVE 12 5/July

WAVE 13 19/July

WAVE 14 2/Aug

WAVE 15 16/Aug

WAVE 16 30/Aug

WAVE 17 13/Sep

TOTAL CASES

5,750 6,313 6,612 6,716 6,801 6,941 7,045 7,114 7,195 7,260 7,461 8,449 11,802 17, 923 23,288 25,670 26,651

DAILY NEW CASES

200 10 26 15 20 14 17 3 10 5 25 87 361 641 253 123 44

CURRENTLY INFECTED

4,633 2,916 2,311 1,258 889 674 580 504 479 455 463 946 3,407 7,295 8,812 3,943 2,379

METHODOLOGY

The COVID-19 Tracker was first launched w/e 5th April 2020.

In each wave we get minimum n=300 completed surveys.

TEG Insights ensures a consistent sample of financial decision makers and

influencers at Small and Medium Size Businesses each wave.

5-minute questionnaire All surveys completed online(TEG Insights Business Panel)

All respondents are financial decision makers/influencers in Small and Medium Businesses

with up to 500 employees

Respondents are from across Australia, including metro and

regional areas

A wide selection of industry sectors are represented, allowing

for deep dive analysis on a regular basis

Data is weighted by state and number of employees to reflect

the national distribution of businesses across the country

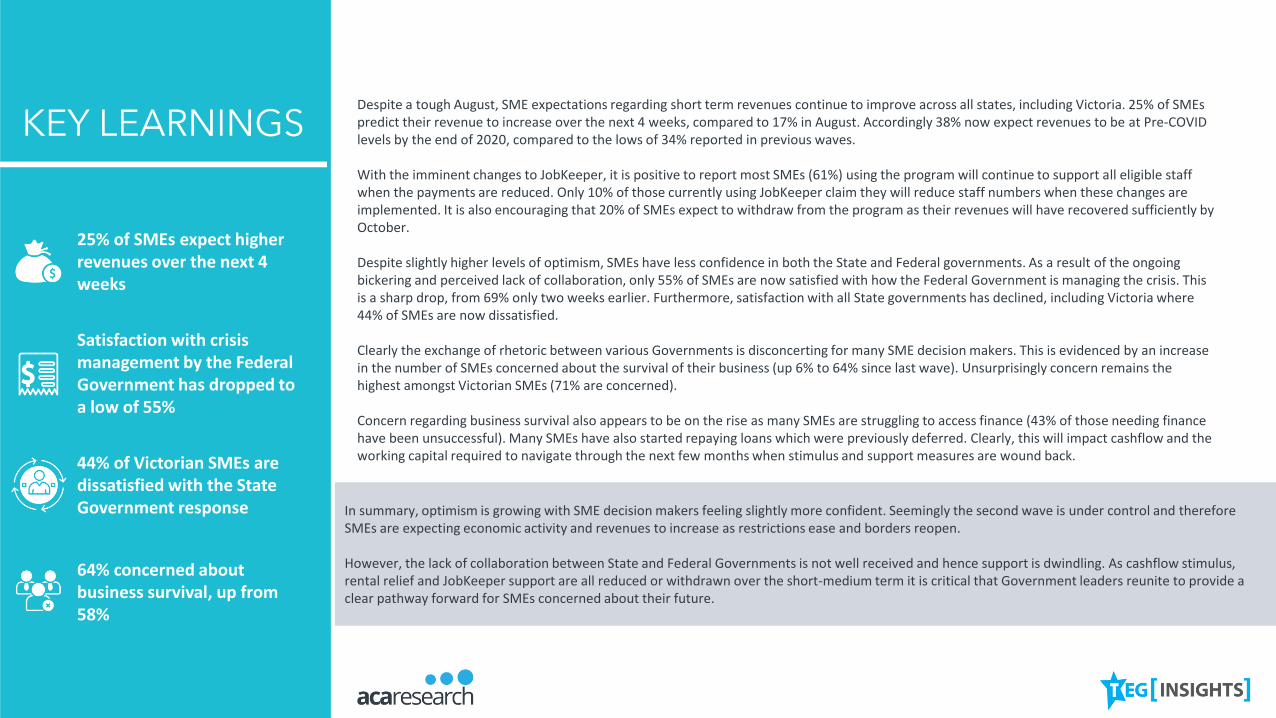

In summary, optimism is growing with SME decision makers feeling slightly more confident. Seemingly the second wave is under control and therefore SMEs are expecting economic activity and revenues to increase as restrictions ease and borders reopen.

However, the lack of collaboration between State and Federal Governments is not well received and hence support is dwindling. As cashflow stimulus, rental relief and JobKeeper support are all reduced or withdrawn over the short-medium term it is critical that Government leaders reunite to provide a clear pathway forward for SMEs concerned about their future.

KEY LEARNINGSDespite a tough August, SME expectations regarding short term revenues continue to improve across all states, including Victoria. 25% of SMEs predict their revenue to increase over the next 4 weeks, compared to 17% in August. Accordingly 38% now expect revenues to be at Pre-COVID levels by the end of 2020, compared to the lows of 34% reported in previous waves.

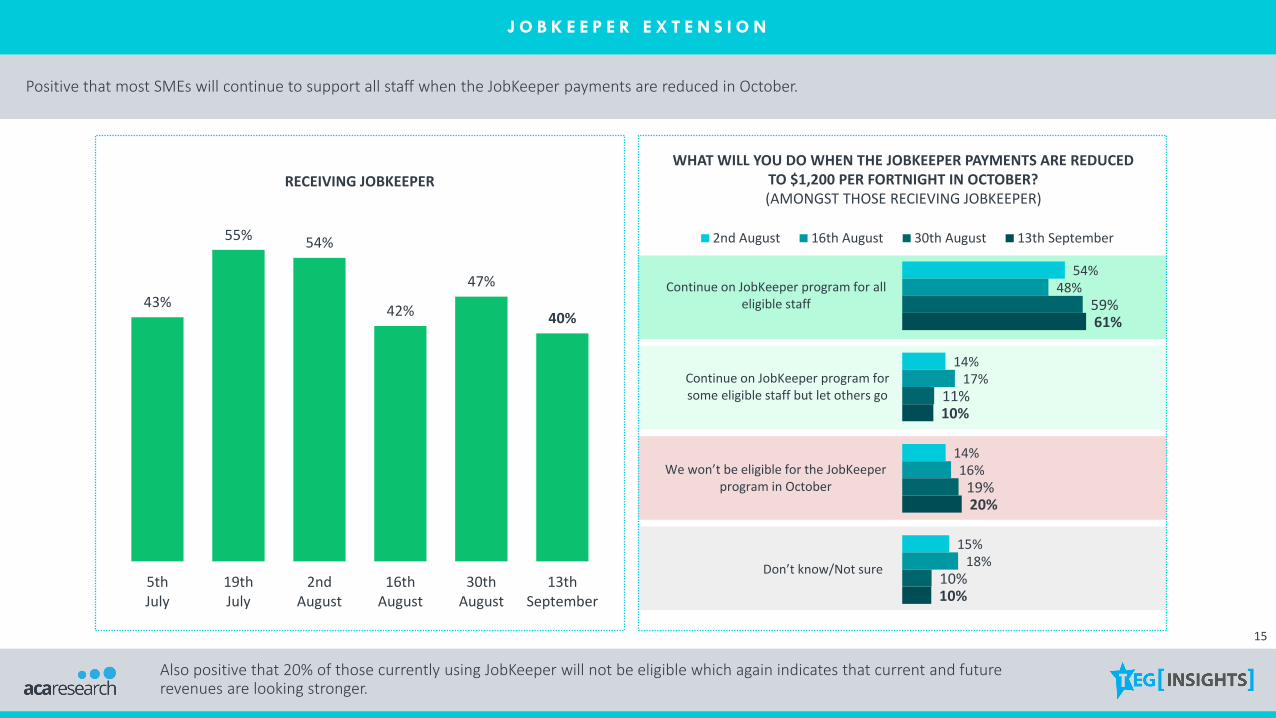

With the imminent changes to JobKeeper, it is positive to report most SMEs (61%) using the program will continue to support all eligible staff when the payments are reduced. Only 10% of those currently using JobKeeper claim they will reduce staff numbers when these changes are implemented. It is also encouraging that 20% of SMEs expect to withdraw from the program as their revenues will have recovered sufficiently by October.

Despite slightly higher levels of optimism, SMEs have less confidence in both the State and Federal governments. As a result of the ongoing bickering and perceived lack of collaboration, only 55% of SMEs are now satisfied with how the Federal Government is managing the crisis. This is a sharp drop, from 69% only two weeks earlier. Furthermore, satisfaction with all State governments has declined, including Victoria where 44% of SMEs are now dissatisfied.

Clearly the exchange of rhetoric between various Governments is disconcerting for many SME decision makers. This is evidenced by an increase in the number of SMEs concerned about the survival of their business (up 6% to 64% since last wave). Unsurprisingly concern remains the highest amongst Victorian SMEs (71% are concerned).

Concern regarding business survival also appears to be on the rise as many SMEs are struggling to access finance (43% of those needing finance have been unsuccessful). Many SMEs have also started repaying loans which were previously deferred. Clearly, this will impact cashflow and the working capital required to navigate through the next few months when stimulus and support measures are wound back.

25% of SMEs expect higher revenues over the next 4 weeks

Satisfaction with crisis management by the Federal Government has dropped to a low of 55%

44% of Victorian SMEs are dissatisfied with the State Government response

64% concerned about business survival, up from 58%

C O N T E N T

H O W I S T H E C O V I D - 1 9 PA N D E M I C

I M PA C T I N G S M E s A C R O S S T H E

F O L L O W I N G A R E A S :

I M PA C T O F C O V I D - 1 9 O N R E V E N U E S1

S AT I S FA C T I O N W I T H S T I M U L U S & S U P P O R T M E A S U R E S2

T H E R E C O V E R Y3

7

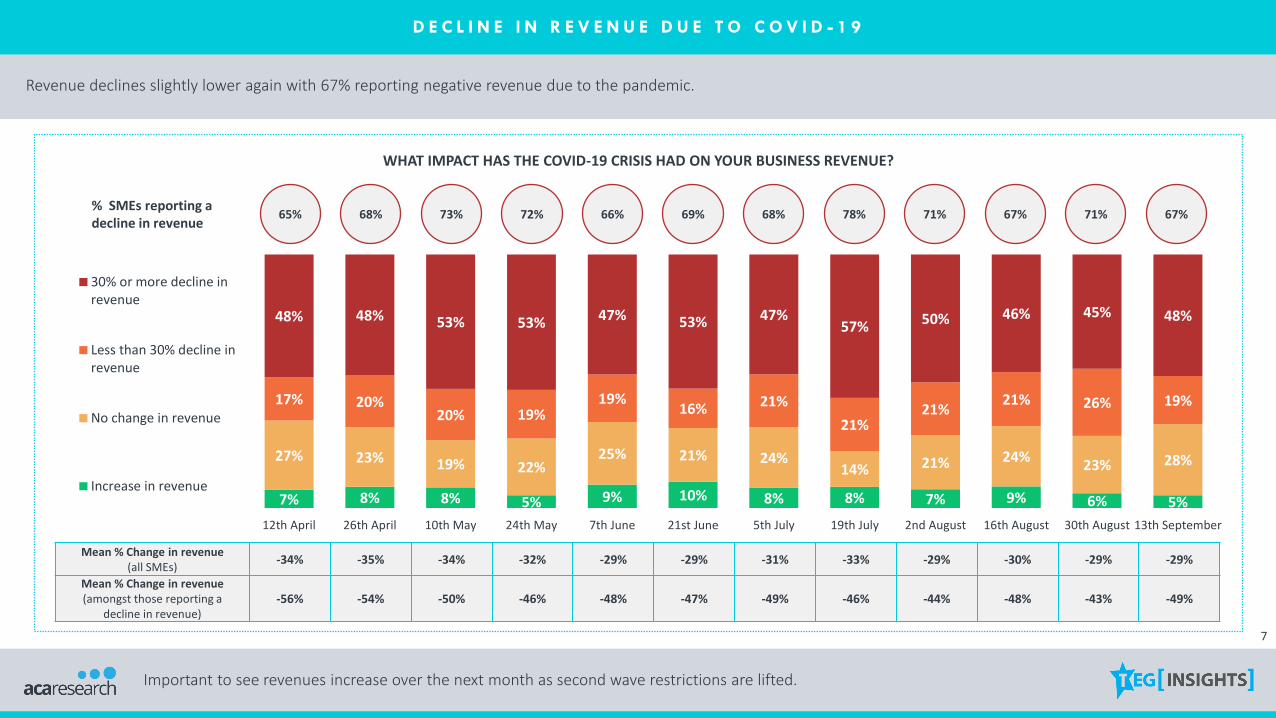

D E C L I N E I N R E V E N U E D U E T O C O V I D - 1 9

Revenue declines slightly lower again with 67% reporting negative revenue due to the pandemic.

WHAT IMPACT HAS THE COVID-19 CRISIS HAD ON YOUR BUSINESS REVENUE?

7% 8% 8% 5% 9% 10% 8% 8% 7% 9% 6% 5%

27% 23% 19% 22%25% 21% 24%

14% 21% 24%23% 28%

17% 20%20% 19%

19%16% 21%

21%21%

21% 26% 19%

48% 48% 53% 53% 47% 53% 47%57% 50% 46% 45% 48%

12th April 26th April 10th May 24th May 7th June 21st June 5th July 19th July 2nd August 16th August 30th August 13th September

30% or more decline inrevenue

Less than 30% decline inrevenue

No change in revenue

Increase in revenue

% SMEs reporting a decline in revenue

65% 68% 73% 72% 66% 69% 68% 78%

Mean % Change in revenue (all SMEs)

-34% -35% -34% -32% -29% -29% -31% -33% -29% -30% -29% -29%

Mean % Change in revenue (amongst those reporting a

decline in revenue)-56% -54% -50% -46% -48% -47% -49% -46% -44% -48% -43% -49%

71% 67% 71% 67%

Important to see revenues increase over the next month as second wave restrictions are lifted.

8

D E C L I N E I N R E V E N U E D U E T O C O V I D - 1 9 B Y S T A T E

Downward trend in VIC continues, but stronger data for WA with those reporting higher revenues continuing to climb.

WHAT IMPACT HAS THE COVID-19 CRISIS HAD ON YOUR BUSINESS REVENUE?

NSW VIC

QLD WA SA

5% 5% 5% 5% 2%15% 17% 25% 22% 25%

21% 16%18% 28% 26%

59% 62% 52% 45% 48%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

12% 9% 10% 6% 5%

22% 17% 18% 20% 18%

23% 28% 24% 23% 25%

43% 45% 47% 50% 52%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

9% 13% 12% 11% 7%

20% 18% 20% 16% 31%10% 11%

22% 22%17%

61% 58%47% 50% 45%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

7% 4% 9% 11% 14%20% 17%

20% 22% 22%

41%42% 24% 17% 20%

32% 38% 48% 50% 43%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

7% 7% 4% 5% 7%

30% 32% 30%40% 34%

16% 19% 23%27% 28%

47% 42% 43%28% 31%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

Stronger data for WA with those reporting higher revenues climbing to 14%.

9

32%42% 45%

35%22%

35%

31%47%

27%

35% 36%

13%33%

19%

43%

27%

34%19%

31%

35%45%

35%

34%

24%

34% 27% 33%

17%31%

18%

38%

19%

22% 15% 15% 8%

12%12% 18% 30%

49%42%

50% 43%

11%23%

13% 15%6% 8% 5% 4%

Maycompared to April

Junecompared

to May

Julycompared

to June

Augustcompared

to July

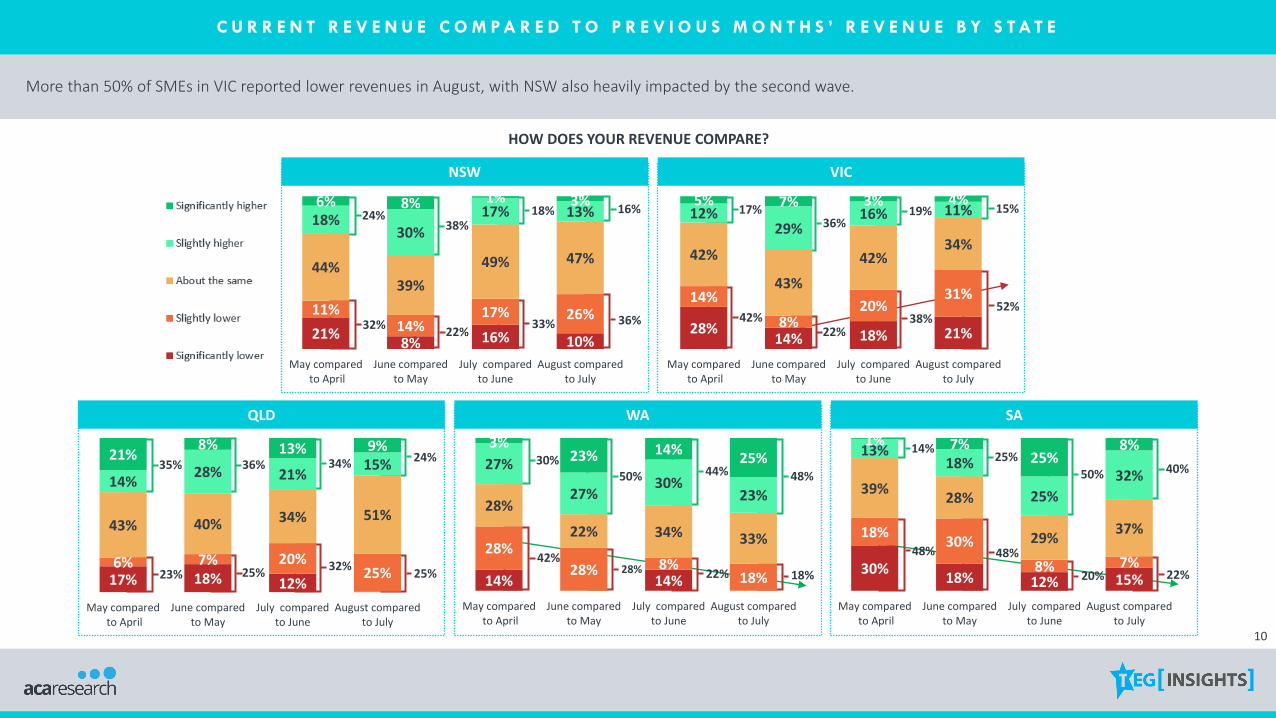

C U R R E N T R E V E N U E C O M P A R E D T O P R E V I O U S M O N T H S ’ R E V E N U E

Not surprisingly, month on month revenues declined again in August as the lockdown measures took their toll. Hopefully, this is the peak of the trend and we start to see a turnaround as restrictions are eased.

HOW DOES YOUR REVENUE COMPARE?

Businesses with 20-99 employees have been hit hard with 1 in 5 reporting significantly lower revenue in August compared to July.

< 5 EMPLOYEES

20 TO 99 EMPLOYEES

5 TO 19 EMPLOYEES

100 TO 500 EMPLOYEES

18% 14% 7% 2%

17% 22%

6% 25%

33% 22%

41%30%

25%26% 28%

37%

7% 16% 17%6%

Maycompared to April

Junecompared

to May

Julycompared

to June

Augustcompared

to July

22%6% 15% 12%

12%

13%16% 22%

31%36%

35%42%

25% 36%26% 13%

10% 9% 9% 11%

Maycompared to April

Junecompared

to May

Julycompared

to June

Augustcompared

to July

12% 5%18% 20%

23%17%

17% 13%

33%

31%

39% 47%

20%37%

23% 17%11% 10% 4% 2%

Maycompared to April

Junecompared

to May

Julycompared

to June

Augustcompared

to July

34%25%

32%

25%

37%

25%

36%

22%

21%12% 15%

10%

13%

13%17% 26%

41%

39%

43%42%

17%

28%

19% 15%

8% 9% 6% 7%

May compared to April

June comparedto May

July comparedto June

August compared to July

Significantlyhigher

Slightly higher

About the same

Slightly lower

Significantlylower

10

42%22%

38%

17%36%

19%

52%

15%24%

38%18%

32%22%

33%

16%

36%21%

8% 16% 10%

11%14%

17% 26%

44%39%

49% 47%

18%30%

17% 13%6% 8% 1% 3%

May compared to April

June comparedto May

July comparedto June

August comparedto July

C U R R E N T R E V E N U E C O M P A R E D T O P R E V I O U S M O N T H S ’ R E V E N U E B Y S T A T E

More than 50% of SMEs in VIC reported lower revenues in August, with NSW also heavily impacted by the second wave.

HOW DOES YOUR REVENUE COMPARE?

28%14% 18% 21%

14%

8%20%

31%

42%

43%

42%34%

12%29%

16% 11%5% 7% 3% 4%

May compared to April

June comparedto May

July comparedto June

August comparedto July

NSW VIC

QLD WA SA

48% 48%

20%

14%25%

50%

42%22%

30%50% 44%

28%23% 25%32%

35% 36% 34%

22%

40%

18%

48%

25%

24%

17% 18% 12%

6% 7% 20%25%

43% 40% 34% 51%

14%28% 21%

15%21%

8% 13% 9%

May compared to April

June comparedto May

July comparedto June

August comparedto July

14% 14%

28%

28% 8%18%

28%

22% 34% 33%

27%

27%30%

23%

3%23% 14%

25%

May compared to April

June comparedto May

July comparedto June

August comparedto July

30%18% 12% 15%

18%30%

8% 7%

39%28%

29%37%

13%18%

25%

32%

1% 7%25%

8%

May compared to April

June comparedto May

July comparedto June

August comparedto July

11

F U T U R E R E V E N U E E X P E C T A T I O N S

Despite a tough August, expectations regarding short term revenues continue to improve as lockdown and border restrictions are lifting.

WHERE DO YOU EXPECT YOUR REVENUE TO BE IN 4 WEEKS’ TIME, COMPARED TO TODAY?

8% 7% 5% 9% 4% 10% 9% 14% 8% 7%

21%

8% 11%9%

9%

19% 15%14%

13% 12%

48%

56%45% 46% 56%

51% 59% 55%56% 55%

20%23%

35% 33% 26%18%

16% 14% 22% 24%

3% 5% 4% 4% 5% 3% 1% 3% 1% 1%

10th May 24th May 7th June 21st June 5th July 19th July 2nd August 16th August 30th August 13th September

Significantly better

Slightly better

About the same

Slightly worse

Significantly worse

% Better 28%23% 39% 37% 31% 21% 17%

% Net score(Better - Worse)

-6% 13% 23% 19% 18% -8% -7% -11% 2% 6%

17% 23% 25%

12

25% 8% 2% 9% 22%11% 21% 28% 27% 35%11% 18% 7% 1% 1%

F U T U R E R E V E N U E E X P E C T A T I O N S B Y S T A T E

There are positive signs of stronger revenues across most states, including a significant jump in VIC.

WHERE DO YOU EXPECT YOUR REVENUE TO BE IN 4 WEEKS’ TIME, COMPARED TO TODAY?

9% -12% -11% 2% 4%% Net score -13% -35% -33% -35% -15%

3% 3% 1% 4%4% 12% 16% 15% 7%

61%62% 64% 61%

56%

28% 15% 12% 20% 33%4% 8% 7% 4%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

3% 4% 9% 8% 4%9% 10% 12% 10% 15%

65% 53% 52% 63% 62%

21% 30% 26% 17% 20%2% 2% 2% 2%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

4% 5% 6% 5% 5%14% 8% 4% 8% 4%

53% 54% 53% 46% 46%

27% 34% 38% 40% 44%

2%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

10% 16% 22% 24% 15%22%

26% 19% 20%17%

50%50% 50% 47%

52%

16%7% 5% 6% 15%

3% 3% 3% 2%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

9% 11% 9% 7% 8%13% 17% 15% 14% 13%

48%56% 64%

56% 55%

25%14% 12% 21% 24%

6% 2% 1% 2% 1%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

NSW VIC

QLD WA SA

13

P E R C E N T A G E C H A N G E I N T H E N U M B E R O F S T A F F B E F O R E T H E C R I S I S V S N O W

Employee data has remained steady with one third of SMEs reporting overall declines in their staff numbers due to the pandemic.

CHANGE IN NUMBER OF EMPLOYEES SINCE THE PANDEMIC

% of SMEs reporting a decrease in the number of staff

35% 40% 33% 33% 32% 39% 34% 41%

Mean % Change in staff (all SMEs)

-18% -21% -17% -17% -14% -14% -12% -18% -13% -14% -14% -14%

Mean % Change in staff (amongst those reporting a decline

in staff)-51% -54% -54% -53% -48% -43% -40% -46% -39% -46% -46% -46%

40% 31% 34%

1% 1% 2% 2% 2% 4% 2% 2% 4% 4% 3% 2%

64% 60%65% 65% 66% 58% 64%

57% 56%65% 62% 66%

14%15%

14% 11%16%

20%20%

20% 24%18% 19% 15%

21% 25% 19% 22% 16% 19% 14%21% 16% 13% 15% 17%

12th April 26th April 10th May 24th May 7th June 21st June 5th July 19th July 2nd August 16th August 30th August 13th September

50% or more decrease inthe number of staff

Less than 50% decrease inthe number of staff

No change in the numberof staff

Increase in the number ofstaff

32%

14

P E R C E N T A G E C H A N G E I N T H E N U M B E R O F S T A F F B E F O R E T H E C R I S I S V S N O W

Despite a slight decline in employment numbers in VIC, the majority of SMEs across all states continue to keep their teams in place.

CHANGE IN NUMBER OF EMPLOYEES SINCE THE PANDEMIC

2% 2% 3% 3%

56% 49% 55% 60% 62%

24% 28%25% 22% 18%

18% 21% 16% 15% 19%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

3% 4% 5% 4% 5%

61% 54% 57% 61% 57%

21% 23% 21% 15% 18%

16% 19% 18% 20% 21%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

4% 4% 2% 2%

64% 65% 70% 67% 71%

15% 14% 14% 19%23%21% 17% 12% 12% 4%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

5% 4% 6% 12% 8%

63% 67% 59% 48% 63%

21% 19% 28%29% 12%

10% 9% 6% 12% 17%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

1% 5% 4% 1%

74% 66% 74%92% 83%

14% 15%13%

5%7%

11% 14% 8% 2% 9%

19thJuly

2ndAugust

16th August

30thAugust

13thSeptember

NSW VIC

QLD WA SA

15

J O B K E E P E R E X T E N S I O N

Positive that most SMEs will continue to support all staff when the JobKeeper payments are reduced in October.

RECEIVING JOBKEEPER

43%

55% 54%

42%

47%

40%

5thJuly

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

WHAT WILL YOU DO WHEN THE JOBKEEPER PAYMENTS ARE REDUCED TO $1,200 PER FORTNIGHT IN OCTOBER? (AMONGST THOSE RECIEVING JOBKEEPER)

54%

14%

14%

15%

48%

17%

16%

18%

59%

11%

19%

10%

61%

10%

20%

10%

Continue on JobKeeper program for alleligible staff

Continue on JobKeeper program forsome eligible staff but let others go

We won’t be eligible for the JobKeeper program in October

Don’t know/Not sure

2nd August 16th August 30th August 13th September

Also positive that 20% of those currently using JobKeeper will not be eligible which again indicates that current and future revenues are looking stronger.

16

N E G A T I V E I M P A C T O F C O V I D - 1 9

In line with short term revenue expectations, we can also report more optimism regarding the longer term impact on the Australian economy and the number of staff employed by SMEs.

WHAT NEGATIVE IMPACT DO YOU THINK THE COVID-19 SITUATION WILL HAVE ON THE FOLLOWING?(W/E 13th SEPTEMBER)

3%

3%

13%

14%

30%

4%

6%

10%

16%

20%

13%

17%

19%

27%

26%

80%

74%

58%

42%

24%

Global economy

Australian economy

Salary increases

Your business spending/capitalinvestment

The number of staff you employ

No negative impact Short term impact (up to 6 months) Medium term impact (6-12 months) Long term impact (more than 12 months)

% Long term impact % Change

from last wave

W/E 21st

JuneW/E 5th

JulyW/E 19th

JulyW/E 2nd

AugustW/E 16th

AugustW/E 30th

August

77% 76% 77% 88% 73% 80% 0%

66% 69% 73% 82% 77% 82% -8%

- - - - 47% 54% +4%

29% 32% 33% 37% 43% 39% +3%

18% 16% 25% 32% 29% 27% -3%

However, the long term negative impact (more than 12 months) on wage growth continues to trend upwards.

17

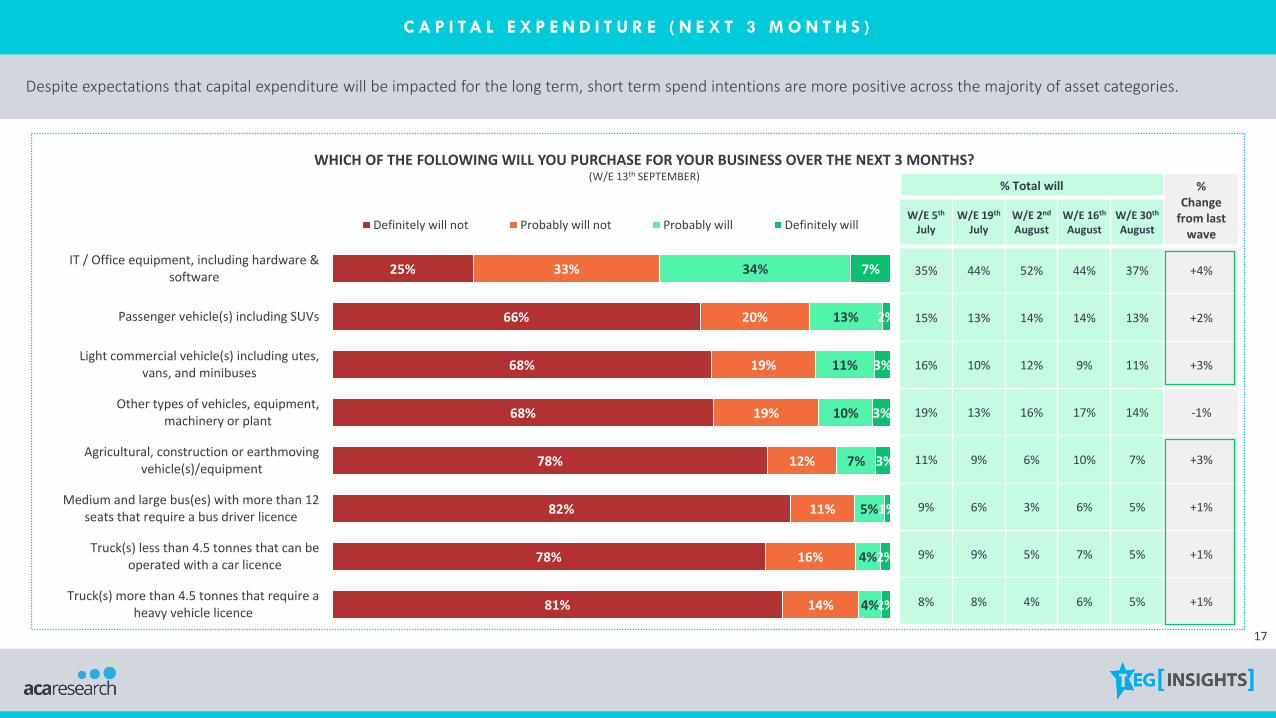

C A P I T A L E X P E N D I T U R E ( N E X T 3 M O N T H S )

Despite expectations that capital expenditure will be impacted for the long term, short term spend intentions are more positive across the majority of asset categories.

WHICH OF THE FOLLOWING WILL YOU PURCHASE FOR YOUR BUSINESS OVER THE NEXT 3 MONTHS? (W/E 13th SEPTEMBER)

25%

66%

68%

68%

78%

82%

78%

81%

33%

20%

19%

19%

12%

11%

16%

14%

34%

13%

11%

10%

7%

5%

4%

4%

7%

2%

3%

3%

3%

1%

2%

2%

IT / Office equipment, including hardware &software

Passenger vehicle(s) including SUVs

Light commercial vehicle(s) including utes,vans, and minibuses

Other types of vehicles, equipment,machinery or plant

Agricultural, construction or earthmovingvehicle(s)/equipment

Medium and large bus(es) with more than 12seats that require a bus driver licence

Truck(s) less than 4.5 tonnes that can beoperated with a car licence

Truck(s) more than 4.5 tonnes that require aheavy vehicle licence

Definitely will not Probably will not Probably will Definitely will

% Total will % Change

from last wave

W/E 5th

JulyW/E 19th

JulyW/E 2nd

AugustW/E 16th

AugustW/E 30th

August

35% 44% 52% 44% 37% +4%

15% 13% 14% 14% 13% +2%

16% 10% 12% 9% 11% +3%

19% 13% 16% 17% 14% -1%

11% 9% 6% 10% 7% +3%

9% 6% 3% 6% 5% +1%

9% 9% 5% 7% 5% +1%

8% 8% 4% 6% 5% +1%

C O N T E N T

H O W I S T H E C O V I D - 1 9 PA N D E M I C

I M PA C T I N G S M E s A C R O S S T H E

F O L L O W I N G A R E A S :

I M PA C T O F C O V I D - 1 9 O N R E V E N U E S1

S AT I S FA C T I O N W I T H S T I M U L U S & S U P P O R T M E A S U R E S2

T H E R E C O V E R Y3

19

S A T I S F A C T I O N W I T H T H E F E D E R A L G O V E R N M E N T ’ S R E S P O N S E

Support for the Federal Government has been negatively impacted by the ongoing bickering with various State Governments. Satisfaction with the overall management of the crisis has dropped to a low of 55%.

HOW SATISFIED ARE YOU WITH THE WAY THE AUSTRALIAN FEDERAL GOVERNMENT HAS MANAGED THE COVID-19 CRISIS OVERALL SO FAR?

8% 4% 5% 5% 5% 4% 4% 4% 2%8% 4%

10%

13%11% 8% 9% 9% 13%

6%11% 13%

9%6%

9%

16%

15%14%

22% 17%18%

23%22% 24% 19%

21%

26%

42% 53%

43%

41%40%

39% 46%47% 39%

39% 45%

38%

21% 17%

31%24%

29% 25% 22%16%

22% 26% 24%17%

12thApril

26thApril

10thMay

24thMay

7thJune

21stJune

5thJuly

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

Extremely satisfied

Somewhat satisfied

Neutral

Somewhat dissatisfied

Extremely dissatisfied

% Total satisfied 63% 70% 74% 65% 69% 64% 68% 63% 61% 65% 69% 55%

20

S A T I S F A C T I O N W I T H T H E S T A T E G O V E R N M E N T ’ S R E S P O N S E

Satisfaction with most State Governments is declining, with pressure on the VIC Government continuing to mount, with 44% of SMEs now dissatisfied.

HOW SATISFIED ARE YOU WITH THE WAY YOUR STATE GOVERNMENT HAS MANAGED THE COVID-19 CRISIS SO FAR?

3% 3% 5%3% 2%5% 9% 7%10% 5%

10%18% 18%

27% 30%36%

43%29%

56% 61%46%

28%41%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

8% 4% 4% 5% 5%10% 13% 12% 7% 13%

21% 24% 25% 27%30%

46% 40% 35% 38%36%

16% 19% 24% 23% 17%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

Extremely satisfied

Somewhat satisfied

Neutral

Somewhat dissatisfied

Extremely dissatisfied

3% 3% 2% 2%4% 2% 5% 8%17% 14% 16% 17% 20%23% 24% 35%

43% 38%

56% 58% 46%33% 32%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

3% 9% 11%2% 8% 7% 7% 13%16% 14% 10%

15%19%

58% 54% 52%45%

39%

24% 24% 28% 24% 18%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

13% 19% 23% 25% 27%13%

19% 20% 16% 17%21%19% 16% 17% 20%

33%30% 31% 31% 27%

20% 14% 10% 11% 9%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

77% 87% 74% 59% 58%80% 70% 70% 53% 33%

44% 42% 43% 49% 35%% Net score 27% 6% -2% 1% -8%

75% 77% 78% 69% 60%

NSW VIC

QLD WA SA

% Net score

The ongoing negative trend in QLD will be concerning for the State Government as the election draws closer.

21

S A T I S F A C T I O N W I T H T H E C O L L A B O R A T I O N O F G O V E R N M E N T S

The lack of collaboration between State & Federal Governments is undermining the goodwill developed with SMEs throughout the pandemic. Only 36% of SMEs are now satisfied with the ongoing collaboration.

HOW SATISFIED ARE YOU WITH THE COLLABORATION BETWEEN THE AUSTRALIAN FEDERAL GOVERNMENT AND YOUR STATE GOVERNMENT WHEN IT COMES TO MANAGING THE COVID-19 CRISIS?

6% 5% 4% 7% 8% 6% 4% 5% 7% 6% 9% 11%10% 11% 14% 12% 13% 14% 13% 17% 15% 12%

20%23%

18% 19% 17%26% 21% 28%

28% 23% 25%25%

25%

31%

44% 44% 44%

39% 40% 35% 39% 40% 34% 41%

35%

29%

22% 21% 21%16% 17% 17% 16% 16% 20% 15% 11% 7%

12thApril

26thApril

10thMay

24thMay

7thJune

21stJune

5thJuly

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

Extremely satisfied

Somewhat satisfied

Neutral

Somewhat dissatisfied

Extremely dissatisfied

% Total satisfied 66% 65% 65% 55% 57% 52% 55% 56% 54% 56% 46% 36%

22

S U P P O R T F R O M T H E B A N K S

The level of positive sentiment towards the Banks has also continued the downward trend, with 17% now negative about the support banks are providing.

65%69%

65%62%

66%62%

68% 67% 66% 65%

10thMay

24thMay

7thJune

21stJune

5thJuly

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

% AWARE OF THE SUPPORT THAT BANKS ARE PROVIDING BUSINESS CUSTOMERS AFFECTED BY THE COVID-19 CRISIS

PERCEPTIONS OF SUPPORT PROVIDED BY THE BANKS TO BUSINESS CUSTOMERS (AMONGST THOSE AWARE OF BANK SUPPORT)

3% 2% 5% 2% 5% 4% 5% 3% 1% 4%10% 7%

11% 14% 6% 9% 4% 9%7%

13%

41% 41% 32% 29% 33% 36%28%

31% 34%

33%

42% 43% 45%45% 49% 44%

46%46% 50%

44%

6% 6% 7% 10% 6% 8%17%

11% 8% 6%

10thMay

24thMay

7thJune

21stJune

5thJuly

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

Very positive

Somewhatpositive

Neutral

Somewhatnegative

Very negative

48% 49%% Positive 52% 55% 55% 52% 63% 57% 58% 50%

23

Decreasing positive sentiment towards the Banks is probably linked to the increasing number of SMEs unable to access finance.

HAVE YOU REQUIRED ANY ADDITIONAL FINANCE SINCE THE ONSET OF THE COVID-19 CRISIS? AND WHAT IS THE PURPOSE OF THIS FINANCE?

72%

26%

13%

16%

5%

6%

74%

12%

5%

13%

10%

4%

67%

11%

13%

16%

5%

9%

62%

19%

11%

9%

6%

4%

Cashflow/ working capital

Purchase plant, machinery orequipment

Fund growth into new markets

Fund growth in Australia

Fund export growth

Fund merger/ acquisition

2nd August 16th August 30th August 13th September

23%

23%

55%

19%

23%

58%

18%

20%

62%

18%

24%

58%

Yes

No, but we mayneed in the next

6 months

No

2nd August 16th August 30th August 13th September

A D D I T I O N A L F I N A N C E

15%

17%

29%

39%

29%

26%

22%

24%

11%

21%

40%

28%

7%

5%

45%

43%

We obtained sufficientfinance

We obtained sufficientfinance for now, but will

probably need more

We obtained finance, butgot less than requested

We sought finance, butwere unsuccessful

24

L O A N D E F E R R A L

Likely that positivity towards the Banks is also impacted by SMEs having to restart payments on deferred loans.

GOVERNMENT STIMULUS AND SUPPORT MEASURES CURRENTLY USED BY THE BUSINESS:

LOAN DEFERRAL

WHAT WILL YOU DO AT THE END OF YOUR LOAN DEFERRAL PERIOD? (AMONGST THOSE UTILISING LOAN DEFERRAL)

25%

36%

23%

16%

43%

19%

12%

27%

Restart repayments in full

Ask for an extension (up to 4 months foreligible customers)

Restructure loans to reduce repayments

Don’t know/ Not sure

August September

22%

16%

August September

C O N T E N T

H O W I S T H E C O V I D - 1 9 PA N D E M I C

I M PA C T I N G S M E s A C R O S S T H E

F O L L O W I N G A R E A S :

I M PA C T O F C O V I D - 1 9 O N R E V E N U E S1

S AT I S FA C T I O N W I T H S T I M U L U S & S U P P O R T M E A S U R E S2

T H E R E C O V E R Y3

26

62%

54%

46%

37%34%

39%

34%

38%

7th June 21st June 5th July 19th July 2nd August 16th August 30th August 13th September

R E V E N U E R E T U R N I N G T O P R E - C O V I D L E V E L S B E F O R E E N D O F 2 0 2 0

Although expectations of returning to Pre-COVID revenues remain low compared to June, we would expect an upward trend moving forward if cases continue to drop and restrictions are lifted.

BUSINESS REVENUE EXPECTED TO RETURN TO PRE-COVID-19 LEVELS BY END OF 2020

27

L E V E L O F C O N C E R N A B O U T B U S I N E S S S U R V I VA L

Despite signs of positivity in this wave, 2/3s of SME decision makers remain concerned about the survival of their business.

7% 9% 10% 8% 11% 9% 14%7% 5% 7% 12% 10%

23% 22%28%

22%

32%

22%24%

20% 22%28%

30%27%

29%38%

36%42%

30%

39% 27%36% 38%

36%32%

32%

41%32%

26% 28% 27% 30% 35% 36% 35%28% 26%

32%

12thApril

26thApril

10thMay

24thMay

7thJune

21stJune

5thJuly

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

Very concerned

Quite concerned

Not that concerned

Not at all concerned

% Total concerned 70% 70% 62% 70% 57% 69% 62% 72% 73% 64% 58% 64%

HOW CONCERNED ARE YOU ABOUT THE SURVIVAL OF YOUR BUSINESS DUE TO THE COVID-19 CRISIS?

28

L E V E L O F C O N C E R N A B O U T B U S I N E S S S U R V I VA L

Unsurprisingly concern remains the highest for Victorian SMEs.

HOW CONCERNED ARE YOU ABOUT THE SURVIVAL OF YOUR BUSINESS DUE TO THE COVID-19 CRISIS?

8% 8% 11% 10%22% 22% 17% 19%

33% 32% 33% 31%

38% 38% 39% 40%

2nd August 16th August 30th August 13th September

6% 2% 8% 10%

26% 36%43% 42%

35%34%

32% 32%

33% 27% 17% 16%

2nd August 16th August 30th August 13th September

9% 3% 11% 14%

39%35%

34% 24%

29%36%

35%35%

23% 26% 20% 27%

2nd August 16th August 30th August 13th September

7% 8% 8% 11%15% 23% 31% 28%34%

32%32% 29%

45% 38% 29% 32%

2nd August 16th August 30th August 13th September

NSW VIC

QLD WA SA

5% 5%26% 21%

27% 31%

54% 62% 48% 41%

20% 17% 20% 23%

2nd August 16th August 30th August 13th September

% Total concerned 79% 70% 61% 61% 71% 70% 72% 71%

68% 61% 49% 48% 74% 79% 68% 64% 52% 62% 55% 62%% Total concerned

Despite ongoing contradictory commentary it is interesting to note that QLD SMEs again report the lowest levels of concern.

29

L E V E L O F C O N C E R N A B O U T P E R S O N A L W E L L B E I N G

Positive to see the ongoing downward trend in concern for personal health and wellbeing.

64% 65% 45%

HOW CONCERNED ARE YOU FOR YOUR OWN HEALTH & WELLBEING DURING THIS CRISIS?

56% 60% 56% 50% 69% 67% 69% 58%

3% 7%15% 11% 7% 7% 10%

4% 5% 9% 8% 9%

32% 27%

40%

33%34% 36%

40%

26% 28% 22%34% 36%

38%47%

35%

38% 44% 41%36%

49% 46% 48%

42% 39%

26%18%

10%18% 16% 15% 14%

20% 21% 21% 16% 15%

12thApril

26thApril

10thMay

24thMay

7thJune

21stJune

5thJuly

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

Very concerned

Quite concerned

Not that concerned

Not at all concerned

% Total concerned 54%

30

21%

25%

52%

57%

76%

78%

79%

75%

48%

43%

24%

22%

Join a meeting with your colleagues inperson

Join a meeting with your clients and/ orsuppliers in person

Allow your employees to travel interstatefor business if there were no travel

restrictions

Fly interstate for business if there were notravel restrictions

Allow your employees to travel overseasfor business if there were no travel

restrictions

Fly overseas for business if there were notravel restrictions

No Yes

M E E T I N G S A N D M O B I L I T Y

With the number of COVID cases dropping it is not surprising that the willingness to meet in person and travel interstate is again increasing.

WOULD YOU BE COMFORTABLE DOING THE FOLLOWING ACTIVITIES IN THE CURRENT ENVIRONMENT?(W/E 13th SEPTEMBER)

% Yes % Change

from last wave

W/E 7TH

JuneW/E 21st

JuneW/E 5th

JulyW/E 19th

JulyW/E 2nd

AugustW/E 16th

AugustW/E 30TH

August

74% 80% 80% 75% 64% 67% 75% +4%

72% 78% 73% 72% 55% 68% 67% +8%

54% 54% 54% 40% 27% 31% 34% +14%

53% 59% 57% 38% 26% 38% 35% +8%

18% 23% 34% 21% 16% 25% 21% +3%

22% 25% 33% 21% 16% 25% 21% +1%

31

P R O D U C T I V I T Y O F T E A M M E M B E R S W O R K I N G F R O M H O M E

Overall less negativity regarding WFH productivity, but smaller businesses (5-19 employees) are struggling with 44% reporting productivity is down.

HOW WOULD YOU RATE THE PRODUCTIVITY OF YOUR TEAM MEMBERS WHEN WORKING FROM HOME COMPARED TO AT THE

OFFICE/WORKPLACE?(AMONGST THOSE WHO EMPLOY STAFF)

< 5 EMPLOYEES 5 TO 19 EMPLOYEES

20 TO 99 EMPLOYEES 100 TO 500 EMPLOYEES

6% 6% 5%11%

5%

23% 24% 21%

24%

20%

46% 48%50%

49%

55%

13% 11% 14%7% 14%

12% 11% 10% 10% 7%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

Much better

Slightly better

About the same

Slightly worse

Much worse

4% 5% 5% 6% 4%14% 15% 18% 19% 15%

53% 56% 54% 53% 64%

8% 10% 12% 8% 6%20% 14% 11% 13% 11%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

7% 7% 5% 13% 15%

29% 31% 26%27% 29%

44% 41% 44%45% 40%

14% 12% 11%10% 13%

6% 10% 9% 5% 3%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

5% 6% 11% 10% 4%

31% 30% 25% 25% 27%

32% 33% 34% 33% 41%

21% 20% 19% 19% 16%

11% 11% 11% 12% 10%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

4% 4% 2%

31% 27%18% 20% 26%

26% 34%43% 42%

43%

27% 19% 16% 20%21%

11% 16% 19% 17% 10%

19thJuly

2ndAugust

16thAugust

30thAugust

13thSeptember

C O N T E N T

A P P E N D I X :

M E T H O D O L O G Y & S A M P L E

A B O U T A C A R E S E A R C H & F I F T H Q U A D R A N T

1

2

METHODOLOGY

The COVID-19 Tracker was first launched w/e 5th April 2020.

In each wave we get minimum n=300 completed surveys.

TEG Insights ensures a consistent sample of financial decision makers and

influencers at Small and Medium Size Businesses each wave.

5-minute questionnaire All surveys completed online(TEG Insights Business Panel)

All respondents are financial decision makers/influencers in Small and Medium Businesses

with up to 500 employees

Respondents are from across Australia, including metro and

regional areas

A wide selection of industry sectors are represented, allowing

for deep dive analysis on a regular basis

Data is weighted by state and number of employees to reflect

the national distribution of businesses across the country

34

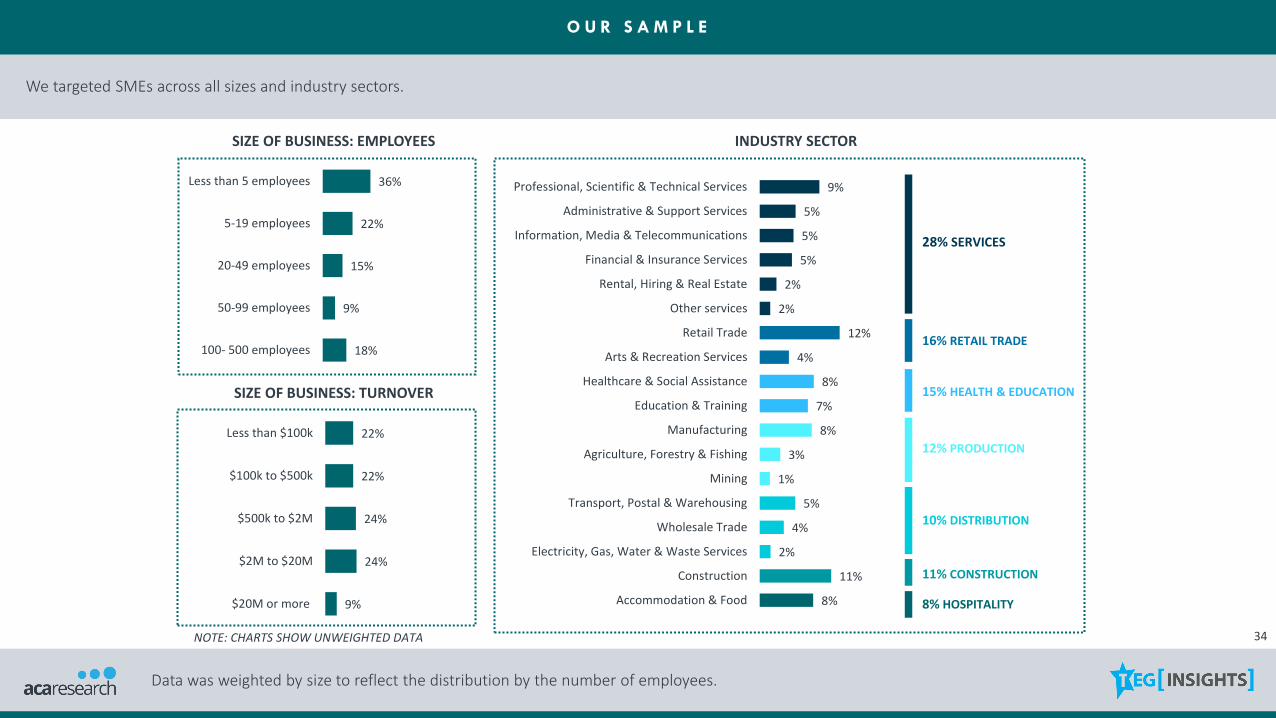

9%

5%

5%

5%

2%

2%

12%

4%

8%

7%

8%

3%

1%

5%

4%

2%

11%

8%

Professional, Scientific & Technical Services

Administrative & Support Services

Information, Media & Telecommunications

Financial & Insurance Services

Rental, Hiring & Real Estate

Other services

Retail Trade

Arts & Recreation Services

Healthcare & Social Assistance

Education & Training

Manufacturing

Agriculture, Forestry & Fishing

Mining

Transport, Postal & Warehousing

Wholesale Trade

Electricity, Gas, Water & Waste Services

Construction

Accommodation & Food

O U R S A M P L E

We targeted SMEs across all sizes and industry sectors.

Data was weighted by size to reflect the distribution by the number of employees.

SIZE OF BUSINESS: EMPLOYEES INDUSTRY SECTOR

36%

22%

15%

9%

18%

Less than 5 employees

5-19 employees

20-49 employees

50-99 employees

100- 500 employees

22%

22%

24%

24%

9%

Less than $100k

$100k to $500k

$500k to $2M

$2M to $20M

$20M or more

SIZE OF BUSINESS: TURNOVER

16% RETAIL TRADE

28% SERVICES

8% HOSPITALITY

15% HEALTH & EDUCATION

12% PRODUCTION

10% DISTRIBUTION

NOTE: CHARTS SHOW UNWEIGHTED DATA

11% CONSTRUCTION

35

O U R S A M P L E

Key decision makers and influencers at SMEs across all states and territories responded to the survey, including metro and regional areas.

Data was also weighted by state to reflect the distribution of SMEs across the country.

HEAD OFFICE LOCATION POSITION IN BUSINESS

50%

17%

16%

12%

6%

Business Owner/ Partner

CFO/ Financial Controller

CEO/ Managing Director

Other Manager/ Executive

Other (e.g. admin)

QLD15%

WA10%

SA/NT9%

NSW/ACT36%

VIC/TAS31%

19%

81%

METRO

REGIONAL

NOTE: CHARTS SHOW UNWEIGHTED DATA

C O N T E N T

A P P E N D I X :

M E T H O D O L O G Y & S A M P L E

A B O U T A C A R E S E A R C H & F I F T H Q U A D R A N T

1

2

O U R P R O M I S E T O C L I E N T S

Providing meaningful insight to allow you to make informed business decisions that drive

growth, competitive advantage and productivity

W E H E L P O U R C L I E N T S M A K E I N F O R M E D

B U S I N E S S D E C I S I O N S

T O E X E C U T E C U S T O M I S E D R E S E A R C H

A N D C O N S U L T I N G P R O G R A M S

B Y L E V E R A G I N G O U R S P E C I A L I S T

C A P A B I L I T I E S

T O D E L I V E R A C T I O N A B L E

R E C O M M E N D A T I O N S A N D A D V I C E

Leveraging our deep industry expertise and customer

experience specialisation to drive better outcomes for your business,

customers, employees, business partners, shareholders and the

community

Working in partnership with you to design and deliver research & consulting programs aligned to

your individual needs

Helping you achieve your goals by delivering pragmatic, actionable recommendations and strategic

advice

O U R R E S E A R C H F R A M E W O R K

W e d e l i v e r i n s i g h t s t h r o u g h o u t t h e c u s t o m e r j o u r n e y e n a b l i n g y o u t o …

T H A N K Y O U !

F O R F U R T H E R I N F O R M A T I O N , P L E A S E C O N T A C T :

J A M E S O R G A N , M A N A G I N G D I R E C T O RA C A R E S E A R C H & F I F T H Q U A D R A N T

E : j o r g a n @ a c a r e s e a r c h . c o m . a u

L I S A S A L A S , H E A D O F C O M M E R C I A LT E G I N S I G H T S

E : l i s a . s a l a s @ t e g i n s i g h t s . c o m