Repsol Economic Research Department. Antonio Merino Chief Economist “Crude Oil Outlook” Seventh IEA_IEF_OPEC Symposium on Energy Outlooks IEF Headquarters Riyadh, Saudi Arabia, February 2017

Transcript

Repsol Economic Research Department. Antonio Merino Chief Economist

“Crude Oil Outlook”

Seventh IEA_IEF_OPEC Symposium on Energy OutlooksIEF Headquarters

Riyadh, Saudi Arabia, February 2017

2

Discussion Points

Price Forecast

Demand Dynamics: Long term forecast and facts

Supply Dynamics: Integrated, Unconventional and OPEC

3

Discussion Points

Price Forecast

Demand Dynamics: Long term forecast and facts

Supply Dynamics: Integrated, Unconventional and OPEC

4

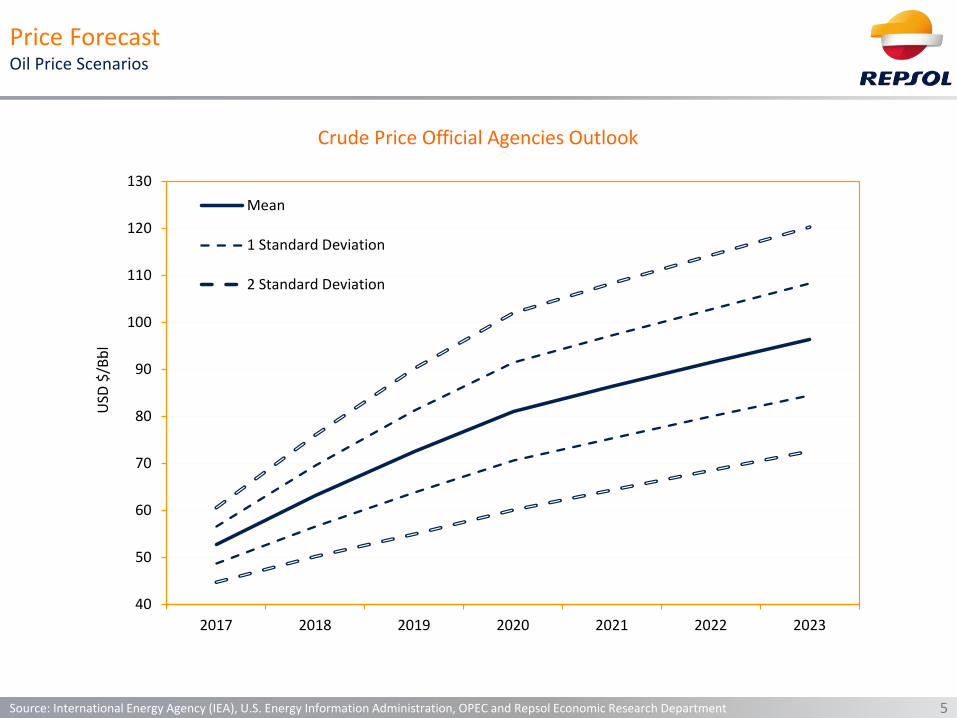

Crude Price Official Agencies Outlook

Price ForecastOil Price Scenarios

Source: International Energy Agency (IEA), U.S. Energy Information Administration, OPEC and Repsol Economic Research Department

40

50

60

70

80

90

100

110

120

130

2017 2018 2019 2020 2021 2022 2023

USD

$/B

bl

EIA Ref. (AEO 2017)*

EIA High R&T (AEO 2017)

EIA Low R&T (AEO 2017)

IEA (WEO 2016, NP Sc.)**

IEA (WEO 2016, CP Sc.)**

IEA (WEO 2016, 450 Sc.)**

OPEC (WOO 2016, RC)***

*** OPEC Reference Basket price

** Prices are calculated through lineal interpolation from IEA perspectives in the WEO2016. Nominal prices assume inflation of 2% per year from 2015. IEA forecasts OECD Crude oil import costs, which was 2.1 US$/Bbl below Brent in average in the 2006-2015 period. In this regard, 2.1 US$/Bbl is added to IEA estimation in nominal terms to obtain Brent perspectives.

* Short term prices from the EIA's Short Term Energy Outlook

5

Crude Price Official Agencies Outlook

Source: International Energy Agency (IEA), U.S. Energy Information Administration, OPEC and Repsol Economic Research Department

40

50

60

70

80

90

100

110

120

130

2017 2018 2019 2020 2021 2022 2023

USD

$/B

bl

Mean

1 Standard Deviation

2 Standard Deviation

Price ForecastOil Price Scenarios

6

Crude Price Official Agencies Outlook

Source: International Energy Agency (IEA), U.S. Energy Information Administration, OPEC and Repsol Economic Research Department

0

50

100

150

200

250

30020

17

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

USD

$/B

bl

Mean

1 Standard Deviation

2 Standard Deviation

Price ForecastOil Price Scenarios

7

Discussion Points

Price Forecast

Demand Dynamics: Long term forecast and facts

Supply Dynamics: Integrated, Unconventional and OPEC

8Source: UN and Repsol Research Department

Annual Growth of Working Age Population (%)

-1

0

1

2

3

World Africa Mid. East India Em.Asia*

Latin Am. China Em.Europe

DM

2000-15 2015-30

Demand Dynamics long-term population growth projection:

9

Oil Demand Growth forecast in the long term

Demand Dynamics In the long term, oil demand growth forecasts hoover around 0,7% -1%

Source: Different sources and Repsol Economic Research Department

-0,8%

-0,6%

-0,4%

-0,2%

0,0%

0,2%

0,4%

0,6%

0,8%

1,0%

1,2%

1,4%

Ener

data

(201

6)

Woo

dMac

kenz

ie (2

016)

OPE

P (W

orld

Oil

Out

look

201

6)

STAT

OIL

(201

6)

EXXO

N (2

016)

BP (2

016)

EIA

(Int

erna

tiona

l Ene

rgy

Out

look

201

6)

PIRA

(201

6)

IEA

(Wor

ld E

nerg

yO

utlo

ok 2

016)

- BU

IEA

(Wor

ld E

nerg

yO

utlo

ok 2

016)

- N

PS

IEA

(Wor

ld E

nerg

yO

utlo

ok 2

016)

- 45

0 Sc

en

2015

-203

0 CA

GR

Crude demand growth (2015-2030 CAGR)

10Source: International Energy Agency (IEA), IMF and Repsol Economic Research Department

Global Demand and Economic Growth → Recent Development & Perspectives

2.2%

1.7%

1.5%

1.9%

1%

5,4%

4,2%

3,5%

3,3%

3,4%3,2%

3,1%

3,4%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Demand Growth

Avg. growth 1986-2004

Avg. growth 2005-2014

Economic Growth

Demand Dynamics Demand growth is outstripping last years behavior at rates comparable to the 1986-2004 avg. growth. Lower prices → higher demand, moreover part of the increase in disposable income was used to reduce debt

11

Global Demand Growth → Recent Development & Perspectives

Source: International Energy Agency (IEA) and Repsol Economic Research Department

Semielasticity World Demand

∆ Oil prices

∆ GDP

OEF/Repsol -0,17 0,44

2.2%

1.7%

1.5%

1.9%

1%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Demand Growth

Avg. growth 1986-2004

Avg. growth 2005-2014

Demand Dynamics Demand growth is outstripping last years behavior at rates comparable to the 1986-2004 avg. growth. Lower prices → higher demand, moreover part of the increase in disposable income was used to reduce debt

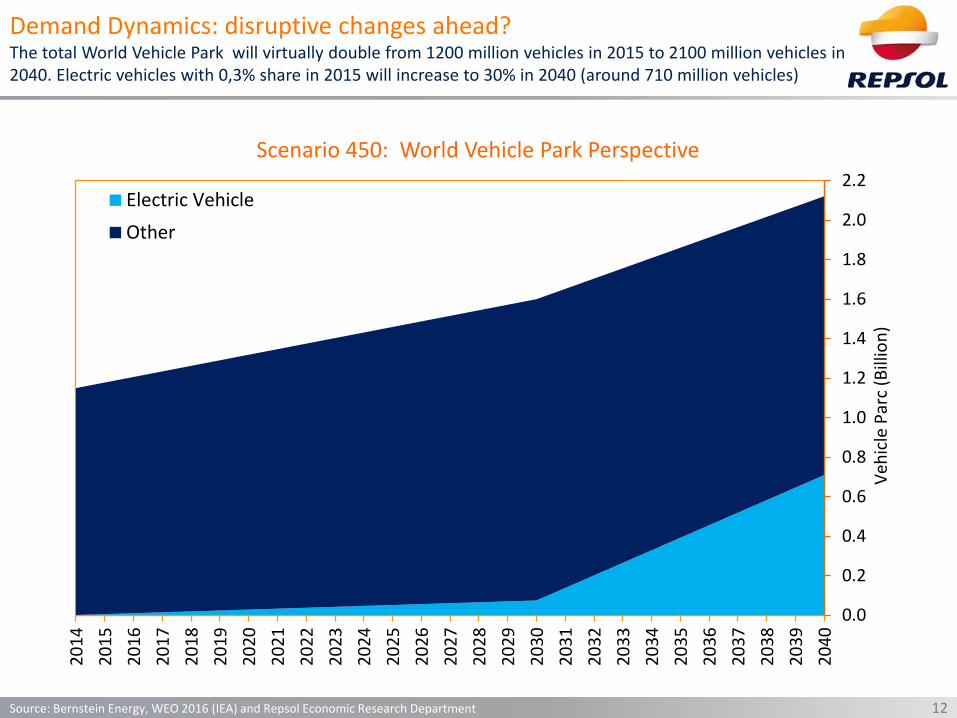

12

Scenario 450: World Vehicle Park Perspective

Demand Dynamics: disruptive changes ahead? The total World Vehicle Park will virtually double from 1200 million vehicles in 2015 to 2100 million vehicles in 2040. Electric vehicles with 0,3% share in 2015 will increase to 30% in 2040 (around 710 million vehicles)

Source: Bernstein Energy, WEO 2016 (IEA) and Repsol Economic Research Department

24Source: Bloomberg and Repsol Economic Research Department

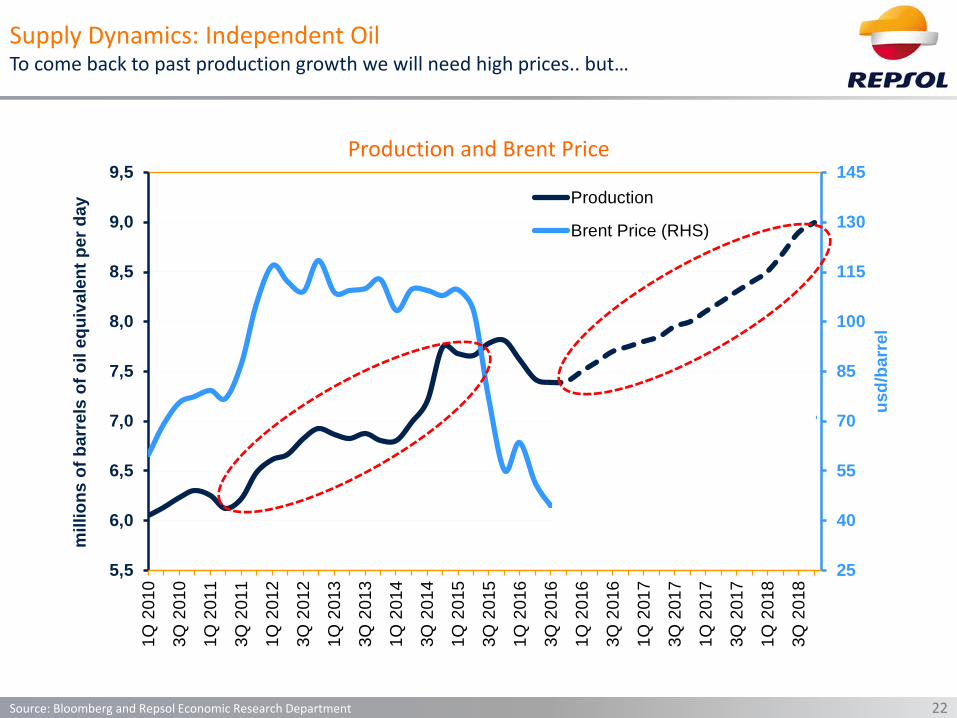

Production and Brent Price

25

40

55

70

85

100

115

130

145

5,5

6,0

6,5

7,0

7,5

8,0

8,5

9,0

9,51Q

201

0

3Q 2

010

1Q 2

011

3Q 2

011

1Q 2

012

3Q 2

012

1Q 2

013

3Q 2

013

1Q 2

014

3Q 2

014

1Q 2

015

3Q 2

015

1Q 2

016

3Q 2

016

1Q 2

016

3Q 2

016

1Q 2

017

3Q 2

017

1Q 2

017

3Q 2

017

1Q 2

018

3Q 2

018

usd/

barr

el

mill

ions

of b

arre

ls o

f oil

equi

vale

nt p

er d

ay

Production

Brent Price (RHS)

Supply Dynamics: Independent OilTo come back to past production growth, due to cost reduction we will need other prices. The rate of growth in productivity per well remains stable….

Monthly Crude Oil Price and PPI Drilling Oil and Gas Wells

Supply Dynamics: Independent OilHowever, E&P costs and oil prices co-move. And some of the reduction in costs should be considered cyclical no STRUCTURAL

25Source: Thomson Reuters and Repsol Economic Research Department

Price Cost96 → 98 -56% -19%00 → 01 -47% -17%06 → 07 -22% -14%08 → 09 -70% -20%14 → 16 -70% -34%* From máx 2014 to min 2016

26Source: Bloomberg and Repsol Economic Research Department

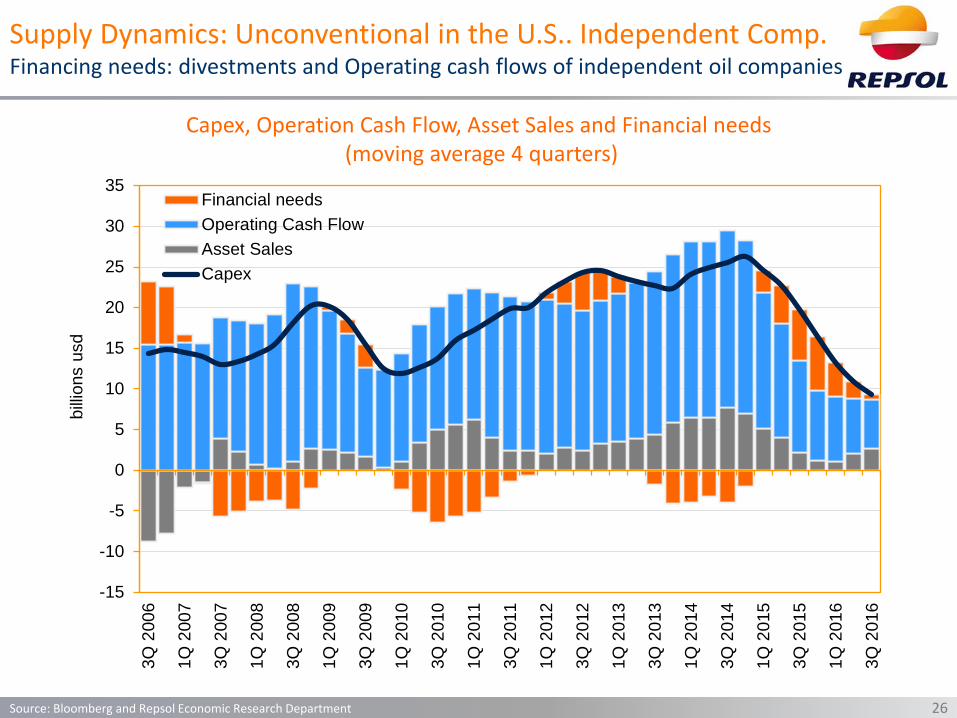

Capex, Operation Cash Flow, Asset Sales and Financial needs(moving average 4 quarters)

Supply Dynamics: Unconventional in the U.S.. Independent Comp.Financing needs: divestments and Operating cash flows of independent oil companies