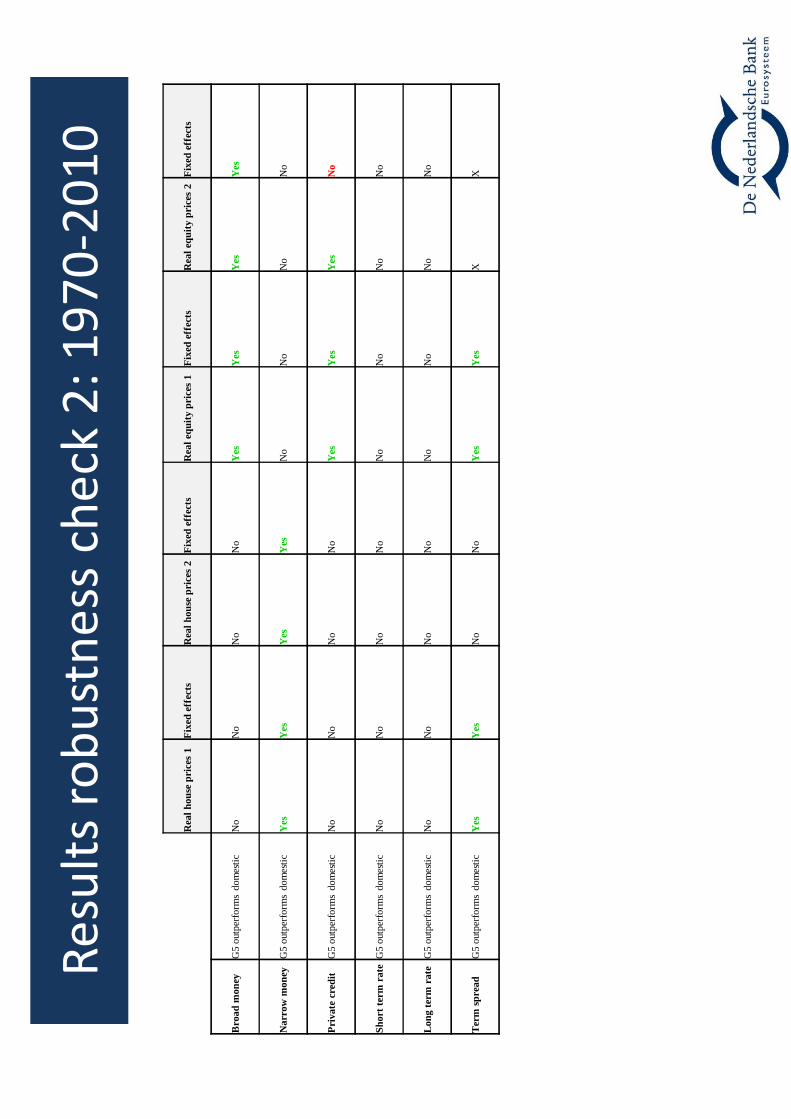

30

Global liquidity as EWI for asset price booms: G5 versus broader measures Dr Beata K. Bierut (DNB) Seminarium Narodowy Bank Polski 13 November 2012 The views expressed here are solely the responsibility of the author and should not be interpreted as reflecting the views of De Nederlandsche Bank.

![Michael Bierut - Carnegie Mellon School of Design · Michael Bierut’s strong focus on ideas and concepts in his work.[13] Following his studies in Ohio, Bierut moved to New York](https://static.documents.pub/doc/80x56/5f2ab8f7fd404435f31b41f5/michael-bierut-carnegie-mellon-school-of-design-michael-bierutas-strong-focus.jpg)