45

Introduc)on to Financial Economics 351473 Eugenia Andreasen

| Date post: | 07-Apr-2016 |

| Category: |

Documents |

| Upload: | fernando-villanueva |

| View: | 215 times |

| Download: | 0 times |

Introduc)on to Financial Economics 351473

Eugenia Andreasen

Contact informa)on

• Professor: Eugenia Andreasen

– Office: 13 – Phone: 2718-‐0752

– Email: [email protected]

– Office hours: Thursday from 1pm to 3pm • Teaching Assistant: Cris)an Lagos Reyes

Course material • Course’s web page (Intranet)

– Lecture slides – Exercises and Problem sets – Ar)cles – Addi)onal material

• Textbooks

– Brealy, Myers, and Allen, Principles of Corporate Finance (10th edi)on). – Hull, Op5ons, Futures, and Other Deriva5ves (7th edi)on). – Bodie, Kane, and Marcus, Investments (10th edi)on).

How to get the best from this course?

• AYend lectures and par)cipate

• Study the slides

• Read the textbooks and suggested ar)cles • Work on the exercises and problem sets

Grading • 4 Controls (5% each).

– Tenta)ve dates: 2/4, 23/4, 4/6 y 25/6 – Either on the second part of the class or on the next Friday

• Midterm (40%)

– Date: 7/5

• Final Exam (40%)

– Date: 9/7

IMPORTANT: The grading of the controls will only be considered if the average of the midterm and the final exam is above 3.6. Otherwise, the controls will not be considered and the student will disapprove the course.

This course • The main goal of this course is to provide a market-‐oriented framework

for analyzing the major types of financial decisions made by agents.

• Valua%on of financial assets: Here you will learn to value financial assets such as bonds, stocks, futures, and op)ons, and to evaluate investment projects using a rigorous framework.

• Diversifica%on and risk: These classes provide a comprehensive framework in the trade-‐off between risk and return given by modern porholio theory.

• Arbitrage and hedging: We will explore how to hedge stock and commodity market risk, interest rate risk, and foreign exchange risk using futures and op)ons.

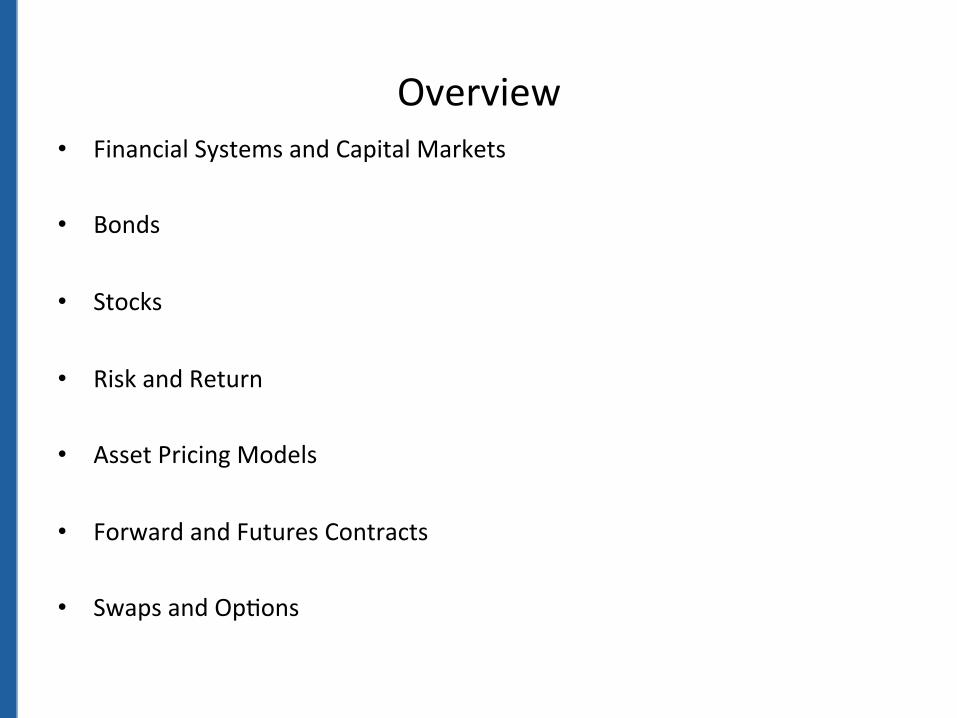

Overview • Financial Systems and Capital Markets

• Bonds

• Stocks

• Risk and Return

• Asset Pricing Models • Forward and Futures Contracts

• Swaps and Op)ons

Introduc)on

What is finance?

• Finance is the study of how people allocate their assets over )me under condi)ons of certainty and uncertainty.

• A key point in finance, which affects decisions, is the )me value of money, which states that a unit of currency today is worth more than the same unit of currency tomorrow.

• Finance aims to price assets based on their risk level, and expected rate of return.

• Finance can be broken into three different sub categories: – Public Finance – Corporate Finance – Personal (Household) Finance

Financial decisions • Corpora)ons face two principal financial decisions:

– Financing decisions – Investment decisions

• The stockholders who own the corpora)on want its managers to maximize its overall current value and the current price of its shares. – This can be achieved taking good financing and investment decisions.

• Investment decisions force a trade-‐off. The firm can either invest cash or return it to shareholders, for example, as an extra dividend.

• When the firm invest cash rather than paying it out, shareholders forgo the opportunity to invest it for themselves in financial markets.

• The return that they are giving up is called the opportunity cost of capital.

Capital markets

Market Capitaliza)on

Source: Securi)es and Insurance Supervisor

Present Value

Learning Objec)ves

Review of Concepts • Compounding/discoun)ng • PV/FV • Real vs. nominal rate • Annui)es and perpetui)es Examples • CD • Auto loan • Scholarship fund • Project planning

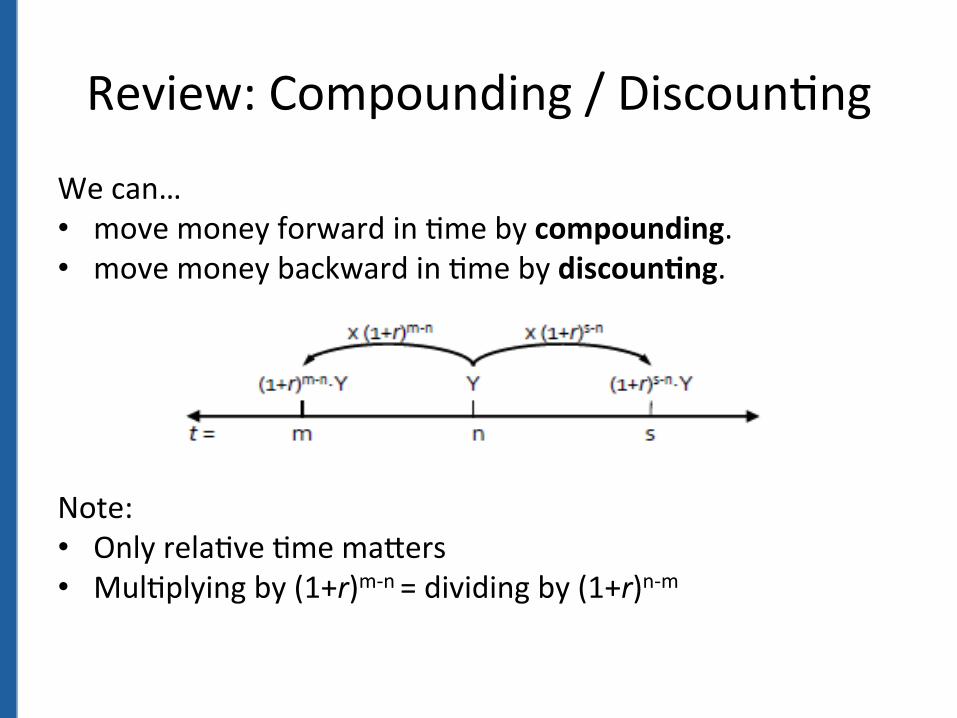

Review: Compounding / Discoun)ng

We can… • move money forward in )me by compounding. • move money backward in )me by discoun%ng. Note: • Only rela)ve )me maYers • Mul)plying by (1+r)m-‐n = dividing by (1+r)n-‐m

Review: Compounding / Discoun)ng

• If we invest money for more than one period at the interest rate r, – the investment grows at a compound rate; and – the interest rate you earn is called compound interest

Review: APR vs. EAR Annual percentage rate (APR) vs. equivalent annual return (EAR):

• Note: – always use the EAR when compounding and discoun)ng

– Due to interest compounding, the EAR is higher than the APR whenever the compounding frequency is higher than once a year.

Con)nuous Compounding

• Given a fixed APR, higher compounding frequency leads to higher EAR.

• Suppose we take compounding frequency to infinity, then

• The con)nuously compounded EAR is the highest possible EAR for a given APR.

Review: PV / FV

• Cash flow:

• Present value (PV): • Future value (FV) :

Which discount factor should we use?

• To discount flows we need to consider the opportunity cost – Which is the return that is foregone by inves)ng in the project rather than inves)ng in the financial market

• So far we are assuming risk free flows, then we should use the risk free rate of the market – Typically, the rate of return of some government bond

• If we consider risky investments we need to use as discount factor the return offered by a risk-‐equivalent investment in financial markets.

Net Present Value

• Net Present Value Criterion: Undertake investment if NPV is posi)ve: – Where C0 is usually nega)ve

• Alterna)vely, invest if return is higher than the opportunity cost of capital:

Review: Nominal vs. Real Interest Rate

• Nominal-‐real interest rate conversion:

• Nominal-‐real cash flow conversion:

• When you discount or compound, – Either use the nominal cash flow and the nominal interest rate

– Or use the real cash flow and the real interest rate – Do not mix and match

Evalua)ng mul)ple cash flows • If you wish to value a stream of cash flows over a number of years it is necessary to use the discounted cash flow formula

• To find the NPV we add the usually nega)ve ini)al value

Review: Annuity/Perpetuity

• Annuity:

• Perpetuity:

• Note that both flows begin in period 1

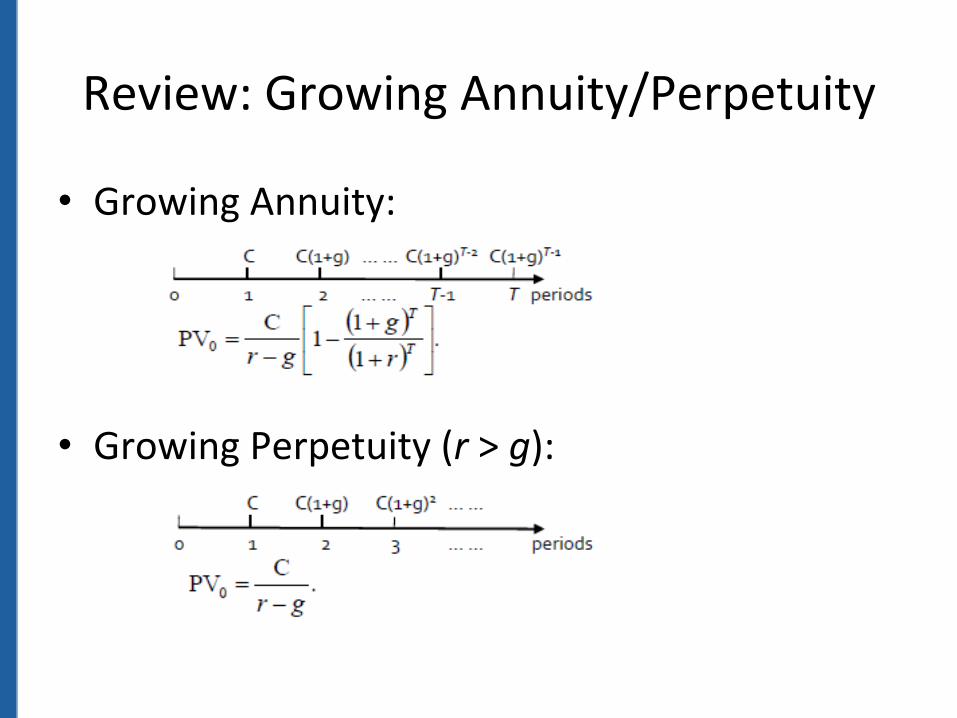

Review: Growing Annuity/Perpetuity

• Growing Annuity:

• Growing Perpetuity (r > g):

Shortcut formulas for calcula)ng Present Values

Ar)cle

• ¨The discount rate illusion¨, The Economist, May 23rd, 2013

• hYp://www.economist.com/blogs/buYonwood/2013/05/inves)ng

Example 1: CD

• You can invest $10,000 in a CD offered by your bank.

• The CD matures in 5 years and the bank quotes you a rate of 4.5%.

• How much will you have in 5 years, if the 4.5% is: – a) EAR – b) Quarterly APR – c) Monthly APR

Example 1: CD

Answer

Example 2: Auto Loan

• You would like to buy a new car for $22,000. • The dealer requires: – a down payment of $10,000 – and offers you 6% APR financing (compounded monthly) for 5 years for the remaining balance.

What is your monthly payment?

Example 2: Auto Loan

Answer • Let C be the monthly payment, then:

Example 3: Scholarship Fund

• You would like to establish a scholarship fund that will help outstanding students with financial difficul)es pay their college tui)on.

– Star)ng today, you hope to give 50 students $20,000 each in today’s money (i.e., adjusted for infla)on) every year.

– The effec)ve nominal interest rate is 5%/yr. – Infla)on is 2%/yr.

• How much money do you need now if you want the fund to last forever?

Example 4: Project Planning

• GeneriCorp is considering whether or not to expand into a new market.

• The company faces the following cash flow (in $million) if it decides to expand:

• A commiYee appointed by the CEO determined that the appropriate discount rate is 9%

• Should the company take on the expansion project?