19

Economic Forecast

OUTPUT AND EMPLOYMENT WHAT THE TABLE SHOWS:

Washington’s GDP forecast is derived from

the national forecast by allocating output to

each of the 50 states based on employment

shares. So, forecast misses reflect surprises

in the aggregate forecast as well as

deviations in the state’s GDP share from the

employment share.

Washington’s economy matched the pace of

the national recovery in 2013.

KEY MESSAGES:

Washington’s economy is forecast to pick up

speed over the balance of 2014 and 2015, in

line with the rebound in the national

economy.

Note: GDP figures are based on quarterly values that are

interpolated from annual GDP estimates using quarterly

employment changes. Unbolded figures are reported actual

values and bold figures represent forecasts.

Sources: US Department of Commerce;

US Department of Labor.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 2

2007 2008 2009 2010 2011 2012 2013 2014 2015

United States

Real GDP

$ billions (fourth quarter) $14,996 $14,575 $14,540 $14,942 $15,242 $15,540 $15,942 $16,501 $17,120

% change over the four quarters 1.9% -2.8% -0.2% 2.8% 2.0% 2.0% 2.6% 3.5% 3.8%

Nonfarm employment

Job count (fourth quarter) 138,246,000 135,493,667 129,877,667 130,652,000 132,642,667 134,853,667 137,247,667 139,694,848 141,679,460

% change over the four quarters 0.9% -2.0% -4.1% 0.6% 1.5% 1.7% 1.8% 1.8% 1.4%

Average monthly change 101,667 -229,361 -468,000 64,528 165,889 184,250 199,500 203,932 203,932

Washington

Real GDP

$ billions (fourth quarter) $307 $305 $303 $310 $318 $328 $337 $350 $364

% change over the four quarters 3.5% -0.4% -0.7% 2.2% 2.6% 3.2% 2.8% 3.6% 4.1%

Nonfarm employment

Job count (fourth quarter) 2,991,100 2,960,467 2,827,967 2,848,033 2,884,300 2,947,133 3,005,900 3,071,764 3,120,792

% change over the four quarters 2.6% -1.0% -4.5% 0.7% 1.3% 2.2% 2.0% 2.2% 1.6%

Average monthly change 6,256 -2,553 -11,042 1,672 3,022 5,236 4,897 5,489 4,086

The Economy’s Structure

PERCENT OF TOTAL GDP DERIVED FROM SELECTED INDUSTRIES WHAT THE CHART SHOWS:

The figure compares the relative importance

of selected industries to the state’s economy

with the national footprint of each industry

(state and national figures reflect the value

added of each industry as a percent of

aggregate state or US nominal GDP,

respectively).

Information technology (representing

Microsoft’s influence) contributes more to

the state’s economy than it does for the

national economy.

KEY MESSAGES:

Information technology will be an important

driver for the state, once drags related to the

housing bust pass.

Source: US Department of Commerce. Updated through

2011.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 3

0

2

4

6

8

10

12

14

16

Agr

icul

ture

Min

ing

Util

ities

Con

stru

ctio

n

Dur

able

man

ufac

turin

g

Non

dudr

able

man

ufac

turin

g

Who

lesa

le tr

ade

Ret

ail t

rade

Tra

nspo

rtat

ion

Info

rmat

ion

Fin

ance

and

insu

ranc

e

Rea

l est

ate

Pro

fess

iona

l and

tech

nica

l ser

vice

s

Man

agem

ent o

f com

pani

es

Adm

inis

trat

ive

and

was

te m

anag

emen

t ser

vice

s

Edu

catio

nal s

ervi

ces

Hea

lth c

are

and

soci

al a

ssis

tanc

e

Art

s, e

nter

tain

men

t, an

d re

crea

tion

Hot

el a

nd fo

od s

ervi

ce

Oth

er s

ervi

ces

Gov

ernm

ent

US industry mix Washington industry mix

Bankruptcies

RATIO OF BANKRUPTCY FILINGS TO THE 2007 Q4 NUMBER WHAT THE CHART SHOWS:

The figure illustrates trends in bankruptcy

filings by businesses and persons relative to

the number of filings in 2007 Q4, prior to the

recession.

Bankruptcy filings are slowly falling back, as

commercial real estate conditions improve.

KEY MESSAGES:

Indicators of financial stress are a useful

coincident indication of economic distress.

Bankruptcy filings have climbed to an above-

normal pace, but are below levels reached in

the 1990s.

Source: Administrative Office of the U.S. Courts; Updated

through March 2014.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 4

0

1

2

3

4

5

0

1

2

3

4

5

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Business bankruptcy filingsNonbusiness bankruptcy filings

All US bankruptcy filings (shaded area)

FRB SF Business Survey

REAL GDP (% CHANGE 12 MONTHS EARLIER) DIFFUSION INDEXES (0 = NO CHANGE) WHAT THE CHART SHOWS:

The San Francisco Federal Reserve Bank

survey of local businesses has recovered

from last summer’s lull, and that is a positive

omen for the economy’s future.

The index readings represent the net

difference in the percent expecting

improving conditions and those expecting

worsening conditions.

The survey points to moderate growth in the

quarters ahead.

KEY MESSAGES:

The business outlook remains positive in

Washington.

Sources: Federal Reserve Bank of San Francisco; US

Department of Commerce. Updated through April 2014

(surveys) and 2014 Q1 (GDP).

Note: diffusion indexes represent the percentage of respondents seeing an increase in activity plus one half of the percentage

reporting no change in activity.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 5

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

-4

-2

0

2

4

6

8

10

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Washington real GDP (left scale)FRB-San Francisco tech impulse index (right scale)

Forecast

Private Business Surveys

REAL GDP (% CHANGE 12 MONTHS EARLIER) DIFFUSION INDEXES (50 = NO CHANGE) WHAT THE CHART SHOWS:

GDP growth in Washington state and the

Western Washington survey of purchasing

managers.

The survey of purchasing managers in the

western regions remains solid.

KEY MESSAGES:

The leading indicators are in positive

territory.

Sources: Institute of Supply Management; US Department

of Commerce. Updated through April 2014 (survey) and

2014 Q1 (GDP).

Note: diffusion indexes represent the percentage of respondents seeing an increase in activity plus one half of the percentage

reporting no change in activity.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 6

25

30

35

40

45

50

55

60

65

70

75

-2

0

2

4

6

8

10

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Washington real GDP (left scale)

Western Washington NAPM index (right scale)

Forecast

Initial Jobless Claims

RATIO OF INITIAL CLAIMS FOR UNEMPLOYMENT INSURANCE TO THE 2007 Q4 LEVEL WHAT THE CHART SHOWS:

The figure tracks layoffs in Washington and

the national level of claims.

Weekly layoffs, both the state and national

tallies, are illustrated in the figure as a ratio

to the level of layoffs in the fourth quarter of

2007, prior to the recession.

Layoffs are back to pre-recession levels.

KEY MESSAGES:

Layoffs, because they are reported so

promptly, are a useful indicator of changing

economic trends.

Underlying layoff trends point to a gradual

improvement in Washington.

Source: US Department of Labor. Updated through May 17,

2014 (state) and May 24, 2014 (US).

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 7

0.75

1.00

1.25

1.50

1.75

2.00

2.25

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2007 2008 2009 2010 2011 2012 2013 2014

Washington

US (solid area)

Economic Growth

REAL GDP GROWTH (PERCENT CHANGE FROM FOUR QUARTERS EARLIER) WHAT THE CHART SHOWS:

Real GDP growth in Washington (the line in

the figure) is superimposed on top of US

real GDP growth (bars in the figure).

Washington’s economy did not contract as

sharply as the national economy in the

recession, but again is expanding in line with

national output growth.

KEY MESSAGES:

Growth in Washington is forecast to pick up

speed in 2014 and 2015.

Source: US Department of Commerce. Updated through

2012 (state) and 2014 Q1 (US). Quarterly estimates for

states after 2012 are interpolated from employment figures

(through April 2014), based on the historical correlation of

state and national employment changes.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 8

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

WashingtonUS

Forecast

Economic Output

REAL GDP LEVEL (RATIO TO 2000 Q4) WHAT THE CHART SHOWS:

The figure illustrates the evolution of real

GDP of the state and the overall US

economy since the fourth quarter of 2000,

the peak of the previous business cycle—

that is, at any point in time the lines trace the

ratio of real GDP to its level in 2000 Q4.

Washington didn’t stumble as badly as the

national economy during the recession and

so is recovering from a higher elevation than

the national economy.

KEY MESSAGES:

Washington’s economy appears to be on the

mend.

Source: US Department of Commerce. Updated through

2012 (state) and 2014 Q1 (US). Quarterly estimates for

states after 2012 are interpolated from employment figures

(through April 2014), based on the historical correlation of

state and national employment changes.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 9

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Washington

US

Forecast

Employment Growth

NONFARM PAYROLL EMPLOYMENT (PERCENT CHANGE FROM 12 MONTHS EARLIER) WHAT THE CHART SHOWS:

The illustration above compares

Washington’s employment trend with the

nation’s.

Employment is expanding at a robust pace.

KEY MESSAGES:

The state’s job market is expected to

continue to expand at a respectable pace.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 10

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

WashingtonUS (shaded)

Forecast

Employment in Relative Terms

NONFARM PAYROLL EMPLOYMENT (RATIO TO THE 2000 Q4 LEVEL) WHAT THE CHART SHOWS:

The figure illustrates the evolution of

employment in the state compared with the

nation since 2000 Q4, the peak of the

previous business cycle. The lines trace out

the ratio of employment at the time to

employment in 2000 Q4.

Washington’s job market is performing well,

and the state’s employment base now is well

above the peak of the previous business

cycle.

KEY MESSAGES:

The employment picture is fairly positive.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 11

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

1.08

1.09

1.10

1.11

1.12

0.96

0.97

0.98

0.99

1.00

1.01

1.02

1.03

1.04

1.05

1.06

1.07

1.08

1.09

1.10

1.11

1.12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Washington

US

Forecast

Employment in Absolute Terms

NONFARM PAYROLL EMPLOYMENT (THOUSANDS) WHAT THE CHART SHOWS:

Trends in the actual employment count in

the state (left scale) and the level of

employment in the overall economy (right

scale).

In proportionate terms, the recession in

Washington was similar to the national

downturn and the recovery is tracking

similarly too.

Washington’s employment count is on the

rise.

KEY MESSAGES:

The job market recovery is forecast to

continue to track the national trend in 2014

and 2015.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 12

127,500

130,000

132,500

135,000

137,500

140,000

142,500

145,000

2,700

2,750

2,800

2,850

2,900

2,950

3,000

3,050

3,100

3,150

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Washington (left scale)

US (right scale)

Forecast

Intrastate Employment

NONFARM PAYROLL EMPLOYMENT IN SELECTED COMMUNITIES (RATIO TO 2000 Q4 LEVEL) WHAT THE CHART SHOWS:

Employment trends in local communities

across the state.

Lines are the cumulative percent change in

employment since 2000 Q4, the peak of the

previous business expansion.

KEY MESSAGES:

Employment trends in most communities are

beginning to stabilize.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 13

0.92

0.96

1.00

1.04

1.08

1.12

1.16

1.20

1.24

1.28

1.32

1.36

0.92

0.96

1.00

1.04

1.08

1.12

1.16

1.20

1.24

1.28

1.32

1.36

2001 2003 2005 2007 2009 2011 2013 2015

US forecast

US

Kennewick

Bellingham

Olympia

Tacoma

Wenatchee

Bremerton

Mt. Vernon

Spokane

Seattle-Bellevue

Seattle-Tacoma

Yakima

Longview

Washington forecast

Washington

Unemployment

UNEMPLOYMENT (PERCENT OF THE LABOR FORCE) WHAT THE CHART SHOWS:

Washington’s unemployment rate, compared

with the national average.

The state’s unemployment is receding in line

with the nation’s and is down to almost 6

percent.

KEY MESSAGES:

The unemployment rate is the single best

indicator of the relative economic

performance of a region.

The steep descent in the unemployment rate

implies that the economy is beginning to turn

up.

Source: US Department of Labor. Updated through April

2014 (state) and April 2014 (US).

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 14

0

2

4

6

8

10

12

0

2

4

6

8

10

12

1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

Washington

US (shaded)

Forecast

Relative House Prices

RATIO OF THE STATE’S HOUSE PRICES TO THE NATIONAL AVERAGE (1995 Q2 = 1.0) WHAT THE CHART SHOWS:

The figure tracks the relative price of houses

in the state and its neighbor versus the

nation—that is, it reflects the ratio of the

state price index to the national house price

index, with that ratio set to unity in the

summer of 1995. A drop in the line means

that house prices in the state lag the

national trend. States that did not suffer from

speculative conditions saw a decline in the

relative price of houses in this last decade.

House prices in Washington mirrored many

of the national trends but corrections

elsewhere and in local markets have

returned house prices back to normal

historical alignment.

KEY MESSAGES:

Real estate prices are stabilizing.

Source: FHFA. Updated through 2013 Q4.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 15

0.8

0.9

1.0

1.1

1.2

1.3

0.8

0.9

1.0

1.1

1.2

1.3

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Washington

Oregon

Real Estate Markets

HOUSE PRICES IN SELECTED COMMUNITIES (RATIO TO THE 1995 Q2 LEVEL) WHAT THE CHART SHOWS:

The figure tracks the cumulative percentage

deviation in house prices since 1995 in

selected local markets and compares those

with the national average.

House prices are rising in key markets.

KEY MESSAGE:

House prices should begin to firm, in lagged

response to the recovering economy.

Sources: FHFA; Standard & Poor’s. Updated through

2013 Q4.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 16

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

US

Yakima

Spokane

Olympia

Kennewick-Richland-Pasco

Seattle

Bremerton

Bellingham

Seattle (Case-Shiller)

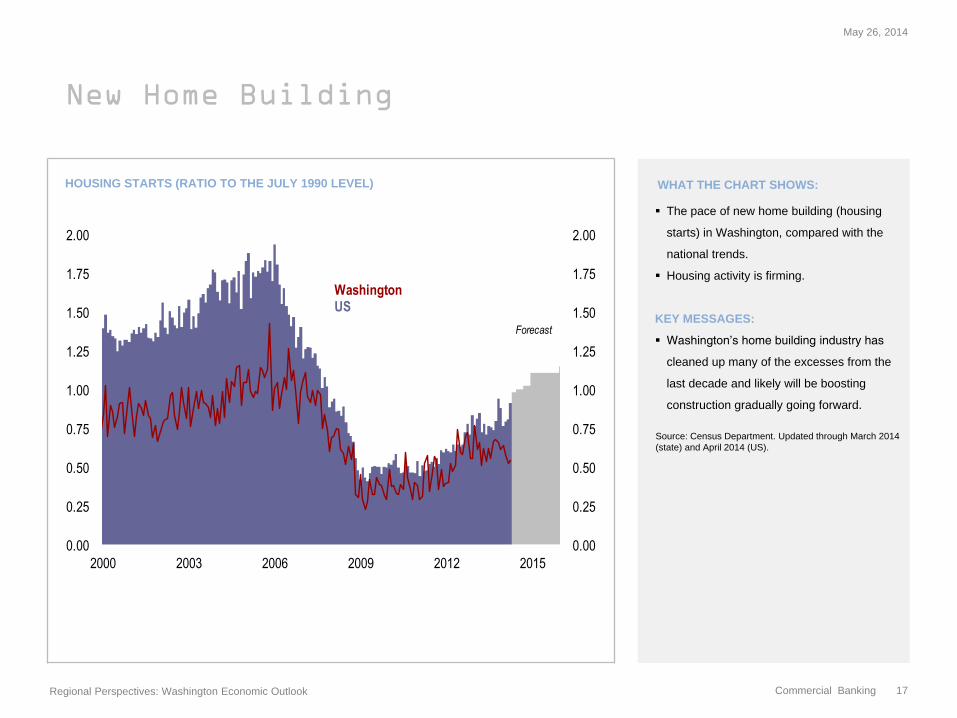

New Home Building

HOUSING STARTS (RATIO TO THE JULY 1990 LEVEL) WHAT THE CHART SHOWS:

The pace of new home building (housing

starts) in Washington, compared with the

national trends.

Housing activity is firming.

KEY MESSAGES:

Washington’s home building industry has

cleaned up many of the excesses from the

last decade and likely will be boosting

construction gradually going forward.

Source: Census Department. Updated through March 2014

(state) and April 2014 (US).

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 17

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2000 2003 2006 2009 2012 2015

WashingtonUS

Forecast

Office Markets

PERCENT OF OFFICE SPACE THAT IS VACANT WHAT THE CHART SHOWS:

Office market conditions in selected

markets.

Vacancy rates in Seattle are beginning to fall

back, confirming the revival of the region’s

economy.

KEY MESSAGES:

Washington’s office markets tend to parallel

the trends in the national market, but

conditions in commercial real estate markets

are improving more rapidly in Seattle than in

the office market nationally.

Source: CB Richard Ellis (formerly CB Commercial Property

Information Systems), Office Vacancy Index of the United

States. Updated through 2014 Q1.

May 26, 2014

Regional Perspectives: Washington Economic Outlook

Commercial Banking 18

0

5

10

15

20

25

0

5

10

15

20

25

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Seattle

All metropolitan areas (shaded area)

0

5

10

15

20

25

0

5

10

15

20

25

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Seattle

All metropolitan areas (shaded area)

CONTACT:

James E. Glassman

Telephone: (212) 270-0778

© 2014 JPMorgan Chase & Co. All rights reserved. Chase, JPMorgan and JPMorgan Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide

(collectively, “JPMC”). The material contained herein is intended as a general market commentary. To the extent indices have been used in this commentary, please note that it is not possible to

invest directly in an index. Opinions expressed herein are those of James Glassman and may differ from those of other J.P. Morgan employees and affiliates. This information in no way constitutes

J.P. Morgan research and should not be treated as such. Further, the views expressed herein may differ from that contained in J.P. Morgan research reports. The above

summary/prices/quotes/statistics have been obtained from sources deemed to be reliable, but we do not guarantee their accuracy or completeness.