25

1

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | september-middleton |

| View: | 20 times |

| Download: | 1 times |

1

1. Understanding the basics of diasporas and development;

2. Looking at the Latin America and Caribbean experience;

3. Options and possibilities4. Caveats and precautions

2

1. Diasporas are a peculiar group with distinct economic activities;

2. They are not necessarily short of ‘migrants’ and the word should not be used as a euphemistic expression;

3. Their activities intersect in different contexts with development, investment being one area;

4. The modalities of investment are also varied: individual [self-interested]; familiar [self-int/altruistic]; community based [altruism].

5. Learning to distinguish between preferences and willingness is an essential ingredient of success

3

Immigrant economic practices (annual expenses)

ConsumptionDonationsFamily remittancesCapital investment

Household economy (US$3600)

Community(US$10,000 year)

Trade and services retail(US$3,000) Property

and other I(US$5,000)

4

5

CountryCountry COLCOL CUBCUB ECUECU ELSELS GUAGUA GUYGUY HONHON MEXMEX NICNIC DRDR BOLBOL JAMJAM LACLAC

Calls once a Calls once a weekweek 8080 4848 9898 4141 5656 4242 5757 6666 7070 7777 3333 7575 6161

Sends over $300Sends over $300 2727 1515 5353 3232 4343 3333 88 4646 1313 1717 2121 4242 3131

Buys HCGBuys HCG 8888 2929 9595 6666 5050 8484 7474 8686 8383 6565 7070 6464 7373

Has a saving Has a saving account.account. 3939 22 5555 1616 1919 4848 1616 2121 55 2929 1010 5858 2727

Travels once a Travels once a yearyear 3434 1313 5151 2424 99 4545 1212 2323 1919 6969 1313 6969 3232

(& Spends over (& Spends over US$1,000)US$1,000) (61(61 5050 9090 6161 4848 5454 4343 7070 2626 6464 9191 5858 60)60)

Has a mortgage. Has a mortgage. LoanLoan 1212 22 1414 1313 44 1818 1212 33 66 66 3636 1515 1010

Owns a small Owns a small bus.bus. 55 22 11 33 22 88 44 22 33 33 44 22 33

Helps. Family w/ Helps. Family w/ mort.mort. 2121 11 2424 1313 11 2121 88 55 77 1313 3131 1616 1212

Belongs to HTABelongs to HTA 66 1010 22 33 2929 77 22 44 33 11 1616 66

To have a practical understanding of impacts, consider the volume of transactions performed by an immigrant. Salvadorans, for example, make 750,000 remittance transfers a month on an average of $330 totaling $3 billion/yr. Similarly, those visiting once a year spent on aggregate $168,750,000/yr.

0

10

20

30

40

50

60

Germany USA UK Nigerians in U.S.A.

Three or more times a year

Twice a year

Once a year

Once every two years

Once every three years

I travel very rarely

$0.00

$20,000,000.00

$40,000,000.00

$60,000,000.00

$80,000,000.00

$100,000,000.00

$120,000,000.00

$140,000,000.00

$160,000,000.00

ONE THOUSAND DOLLARS OR LESS BETWEEN ONE AND THREE THOUSAND DOLLARS MORE THAN THREE THOUSAND DOLLARS

THREE OR MORE TIMES A YEAR

TWICE A YEAR

ONCE A YEAR

ONCE EVERY TWO YEARS

ONCE EVERY THREE YEARS

I TRAVEL VERY RARELY

$339,972,715

$211,002,729$95,402,456

$0.00

$50,000,000.00

$100,000,000.00

$150,000,000.00

$200,000,000.00

$250,000,000.00

$300,000,000.00

$350,000,000.00

$400,000,000.00

ONE THOUSAND DOLLARS OR LESS BETWEEN ONE AND THREE THOUSAND DOLLARS MORE THAN THREE THOUSAND DOLLARS

In 2004 total tourist revenue was at U$480,000,000).

0

10

20

30

40

50

60

70

80

90

Germany UK USA

Peas

Peppers

Fresh fruits and vegetables

Noodles

Salted fish

Fresh fish and shrimp

Spices

80 % of remittance senders buy home country goods

DevelopmentActivities

In the diaspora Through the diaspora

By the diaspora

Family remittances

Banking the unbanked

Financial intermediation;MFI

MTO

Consumption of goods and services

Access to a demand of products

Supply of home country commodities

Small business development

Investment of capital

Diaspora related businesses;

Technical training in remittance receiving areas; bonds

Manufactured goods; nostalgic trade; tourism; other SMEs

Cash and in kind donations or investments

Capacity building

Project identification; networking

Social philanthropy

9

10

11

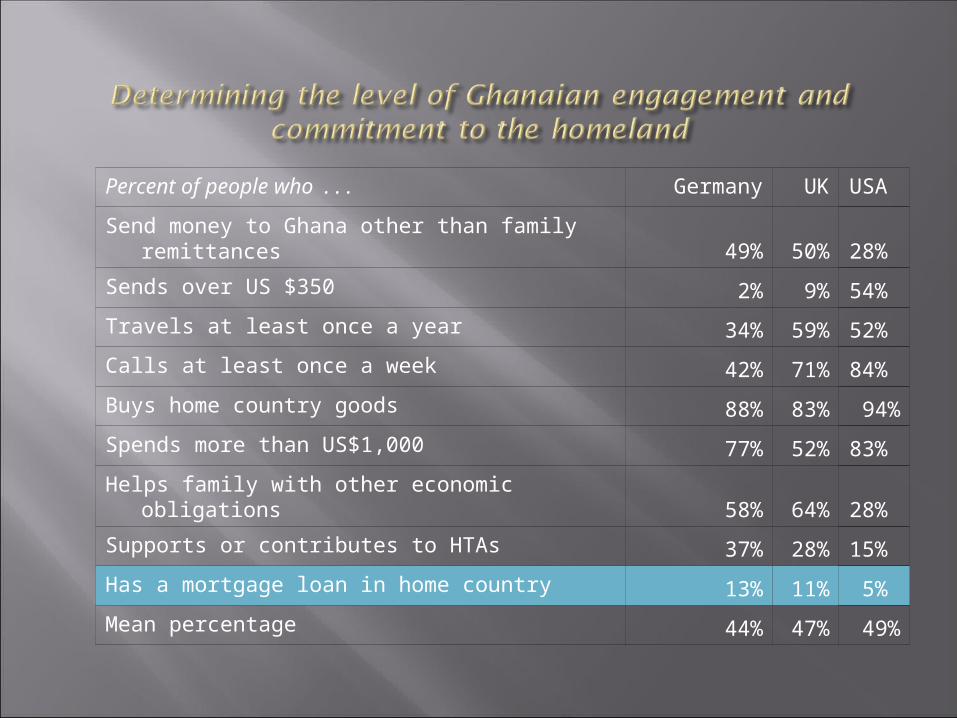

Percent of people who . . . Germany UK USA

Send money to Ghana other than family remittances 49% 50% 28%

Sends over US $350 2% 9% 54%

Travels at least once a year 34% 59% 52%

Calls at least once a week 42% 71% 84%

Buys home country goods 88% 83% 94%

Spends more than US$1,000 77% 52% 83%

Helps family with other economic obligations 58% 64% 28%

Supports or contributes to HTAs 37% 28% 15%

Has a mortgage loan in home country 13% 11% 5%

Mean percentage 44% 47% 49%

13

14

0

5

10

15

20

25

30

35

Mutual funds

Unit trust

Real estate trust

Stock market

2 year bonds

3 year bonds

5 year bonds

Every year less than 5% of migrants or families do invest in some economic activity.

That can be between 10,000 to 50,000 people investing on average of US$7,000

However the large majority of investments are informal and outside the financial and business systems: use local contractors, local informal lenders, cash payments, etc.

Thus, first step of enabling investment environment for diasporas is to formalize the economy by improving financial access

15

DevelopmentActivities

In the diaspora Through the diaspora

By the diaspora

Family remittances G-Xchange (Philippines); Wells Fargo (US); Directo a México (US/MX)

Atikha Foundation; (Phi); BANSEFI (MEX); Salcajá (GUA); Financiera El Comercio (PAR); AMUCCS (MEX);ADOPEM (DR); Banco Solidario (EC); Banco Salvadoreno (SAL); Fedecaces (SAL)

MFIC (LAC); JNBS (JAM)

Consumption of goods and services

Thamel (US-NEP)

Investment of capital IntEnt; Construmex ; ERCOF

Por Mi Jalisco; Fuproca

Cash and in kind donations or investments

IME; SEDESOL Oxfam Novib: DIR Foundation; HIRDA; Sankofa;

South African Reconstruction & Development Bond; New Horizon Investment Club

Considerations: 1) policy driven or spontaneous; 2) how they measured success, 3) what factors triggered success, 4) what challenges they encountered, and 5) what solutions did they found to mitigate the challenges.

16

a) Financial Intermediationi) Financial literacy: public-private partnershipii) Banks and SCA investment intermediation

b) Migrant Outreachi) Confidence buildingii) Contact and identificationiii) Outreach Program

c) Regulatory issuesi) Standards in financial accessii) Easing of rules for migrants to access the financial

systemd) Economic and Social issues

i) Investment: business investment plans and partnerships

ii) Construction

17

i) Financial Literacy: public-private partnership

a) set up 20 educators at 10 bank branches who will explain basic and practical concepts and skills on financial management, indicate relevant financial products, refer her/him to a bank liaison, and invite her/him to form a financial relationship.

ii) Banks and SCA intermediation

a) set up a grant facility or financial development program that announces competitive bids on TA grants for financial institution development in remittance transfer and financial intermediation (savings and investments).

18

i) Develop confidence building

a) establish department of outreach and communication within Ministry of Foreign Affairs;

b) develop in tandem with the office of the president confidence building incentives.

ii) Establish contact and identification

a) formalize a partnership with MTOs in the country to identify migrant communities;

b) jointly establish communication with the community leaders and prepare a minimum database of its diasporas.

iii) Outreach Program:

a) learning about the logistical implementation of IME and 3x1 program type of schemes in cooperation with Mexican government;

b) inviting private sector participation (MTOs, banks, donors and other entities);

c) establish a minimum partnership fund on social development projects.

19

i) Standards in financial access

a) establish annual targets on bankarizing migrants as clients, banking women recipients, loan provision and collateralization from remittances;

b) identify immigrants’ financial and economic preferences

ii) Ease rules on financial access

a) Allow migrants to open bank accounts without severe restrictions in identification;

b) Introduce investment loan opportunities to migrants

20

i) Investment: business investment plans and partnerships

a) identification of 20 competitive investment opportunities;

b) obtaining cooperation from the international community in technical assistance with Business Plan preparation and marketing schemes design;

c) taking on the lessons of IntEnt in the Netherlands

iii) Investment promotion in housing

a) exploration of financing facility followed by a housing investment fund.

21

Four premises to keep in mind1. Impact of remittances is significant2. The impact however is not a solution to the challenges of development: Structural

problems of poverty and inequality are beyond migration and remittances; and the broader effect depends on the productive base of local economy to absorb foreign savings;

3. Policies can be implemented that can leverage the economic relationships migrants have with home country;

4. Any development approach demands a transnational outlook and a gender

perspective; Investment climate is the proxy to attract

diaspora investments (political and economic stability);

Realism of the possible is essential Communication is also important

22

Country of origin

Remitters who belong

to an HTA (percent)

Median Income

Philippines 35.0 35,000

Guyana 26.3 24303

Nigeria 16.0 43,000

Jamaica 15.5 34,437

Ghana 15.0 46,000

Ecuador 10.0 16,067

Haiti 9.5 23,000

Honduras 6.7 21,828

Colombia 5.6 21,995

Mean 5.5

Nicaragua 4.0 22,814

Dominican Republic

3.3 24,194

Guatemala 2.8 12,975

Mexico 2.1 18,376

El Salvador 1.5 19,789

Bolivia 1.4 25,551

An economic profile of four An economic profile of four Latin American citiesLatin American cities

Jerez, ZacatecasMexico

Salcaja, Quetzaltenango,

Guatemala

Suchitoto,El Salvador

Catamayo,Loja,

Ecuador

Basic profile

Population 37,558 14,829 17,869 27,000

Labor force (%) 41% 37% 34% 31%

Population ages 5-19 34.7% (ages 0-14) 36.81% (5,459)

34% (7 to 18) 30%

Main economic activities (%)--Commerce and Services--Agriculture--Manufacturing--Construction

35%; 19%;13%; 11%;

42%;4% (excl.

subs.);6%;

15.5%;52.2%; 7.6%;

39%; 20%; est.8%

Proximity to major urban center

45kms to Zacatecas

9 kms to Quetzaltenango

45 kms to San Salvador

45 kms to Loja

Cost of living . . .

Food 219 228 209 201

Services (utilities) 60 44 40 43

Education 13 32 29 56

Health 40 41 34 68

Entertainment 27 3 40 35

Income . . .

Wages 323 303 125 162

Total earnings, remittances included

930 501 622 353

Monthly remittances amount received

637 331 515 181

0.00 0.20 0.40 0.60 0.80

Trade dependence on major partner=exppartner/totexp

0.20

0.40

0.60

0.80

FL

D (

maj

or

mig

rati

on

co

un

try

# m

igr)

/ (to

tal #

mig

r)

0 50 100 150 200

Durability of democracy

0.000

0.200

0.400

0.600

0.800

% m

igra

nts

% migrants = 0.09 + -0.00 * durableR-Square = 0.02

0.00 25.00 50.00 75.00

% rural population

0.00

0.25

0.50

0.75

1.00

Rat

io o

f p

c re

mit

tan

ces

to p

c G

DP

20.00 40.00 60.00

POVERTY

0.00

0.25

0.50

0.75

1.00

Rat

io o

f p

c re

mit

tan

ces

to p

c G

DP

Ratio of pc remittances to pc GDP = 0.08 + 0.00 * povertyR-Square = 0.04

Investment climate is essential