49

Annual Report 1996 Euratom Supply Agency EURATOM SUPPLY AGENCY ANNUAL REPORT 1996 DOCUMENT

Annual Report 1996

Euratom Supply Agency

EURATOM SUPPLY AGENCY

ANNUAL REPORT

1996

DOCUMENT

Annual Report 1996

Euratom Supply Agency

Annual Report 1996

Euratom Supply Agency

TABLE OF CONTENTS

PREFACE 1

INTRODUCTION, EINLEITUNG, INTRODUCTION 3-7

CHAPTER I 9

DEVELOPMENTS CONCERNING SUPPLY IN THE EUROPEAN UNION 9Security of Supply 9Supply of CIS origin materials 10Other Developments 11

CHAPTER II 15

SUPPLY OF NUCLEAR MATERIALS AND ENRICHMENT SERVICES IN THE EUROPEAN UNION 15Reactor Needs/Net Requirements 15Natural Uranium 15Special Fissile Materials 18

CHAPTER III 21

NUCLEAR ENERGY DEVELOPMENTS IN THE EUROPEAN UNION MEMBER STATES 21

CHAPTER IV 37

INTERNATIONAL RELATIONS 37International Agreements and Related Developments 37

CHAPTER V 41

ADMINISTRATIVE REPORT 41Personnel 41Finance 41Advisory Committee 41

Addresses 42

ORGANISATIONAL CHART 43

Annex 1 44Annex 2 45

Annual Report 1996

Euratom Supply Agency

Annual Report 1996Page 1

Euratom Supply Agency

PREFACE

With the approach of the fortieth anniversary of the signing of the EuratomTreaty in 1997, it is worth underlining the important recent developments atEuropean Union level in the field of energy policy which have placed thenuclear energy option firmly in the wider context of the Union’s energy needsand objectives for the 21st century. In 1996, the Commission published itsWhite Paper on energy policy and in September adopted a draft IndicativeNuclear Programme for the Community (PINC).

Alongside the key energy policy objectives of competitiveness andenvironmental protection identified in the White Paper, the objective ofsecurity of supply runs as a common thread through the development ofenergy policy in an EU which is the world’s biggest net importer of energy. Innatural uranium, for example, the EU was dependent for over 90% of itsneeds in 1996 on external supplies. In the nuclear sector, the prerogatives ofthe Euratom Supply Agency enable the Commission and the Supply Agencyto follow a policy of diversification of sources of supply and to pursue thefundamental objective of security of supply of nuclear fuels to Member Stateswhich choose to develop nuclear energy as part of their overall energy mix.

As Member of the Commission responsible for the Euratom Supply Agency, Iam pleased to present the 1996 Annual Report of the Agency, which aims toprovide for convenient reference an EU-wide overview of nuclear supply dataand issues for a readership in public organisations and industry in the nuclearsector and beyond, both within and outside the EU.

(signed)

Christos PAPOUTSISMember of the Commission

Annual Report 1996

Euratom Supply Agency

Annual Report 1996Page 3

Euratom Supply Agency

INTRODUCTION

As in previous years, the Agency satisfied itself, inthe context of exercising its exclusive right toconclude supply contracts, that users in theEuropean Union (EU) received a regular supply ofnuclear fuels.

1996 was characterised by an overall rise in naturaluranium prices, affecting both multiannual and spotcontracts, although by the end of the year spotprices had fallen from the high point they reached inthe middle of the year. Overall productionunderwent an increase, although while production inthe western world increased, it decreased in the restof the world. The prospect of a rise in pricescontributed to this increase, and to theannouncement that a number of new mines wouldbe opened or existing mines reopened, although thequestion remained open of whether in the longerterm the supply of natural uranium would besufficient to cover world requirements in theirentirety. In contrast, prices for enriched uranium andenrichment services remained stable. Given thesecircumstances, the Agency continued to encourageEU users to diversify their sources of supply and to

meet the majority of their needs through multiannualcontracts at prices which properly reflect productioncosts.

The Commonwealth of Independent States (CIS)was once more the biggest source of supply ofnatural uranium to the EU. The Russian Federationremained the EU’s single largest supplier country ofnatural uranium in 1996. In this context, the Agencypursued its policy of diversification of sources ofsupply and market-related prices in a flexible andpragmatic manner with regard to offers of materialarising from these countries’ fresh production orfrom military and other stockpiles.

The new Euratom/US agreement for cooperation,which replaces the old agreement of 1960 whichhad expired on 31 December 1995, entered intoforce on 12 April 1996. Routine contacts with manyof Euratom’s major nuclear trading partners alsotook place during the year. The Supply Agencycontinued to fulfil its well-established role in theCommission team which deals with internationalnuclear trade issues and negotiations in this field.

Annual Report 1996

Euratom Supply Agency

Annual Report 1996Page 5

Euratom Supply Agency

EINLEITUNG

Wie schon in den Vorjahren, hat sich dieVersorgungsagentur im Rahmen der Wahrnehmungihres ausschließlichen Rechts zum Abschluß vonVersorgungsverträgen davon überzeugen können,daß die Verbraucher in der Gemeinschaft eineregelmäßige Versorgung mit Kernbrennstoffenerhalten haben.

Das Jahr 1996 war durch einen umfassendenAnstieg der Preise für Natururan gekennzeichnet,der sowohl Mehrjahres- wie Spotverträge berührte,wenn auch zum Jahresende bei den Spot-Preisenim Vergleich zu den in der Jahresmitte erreichtenHöchstwerten eine Abschwächung zu verzeichnenwar. Insgesamt gab es eine Ausweitung derProduktion; während sie in der westlichen Weltstieg, ging die Produktion in der restlichen Weltzurück. Die Aussicht auf steigende Preise trug zudieser Ausweitung bei, und zu der Ankündigung,daß eine Reihe von neuen Minen eröffnet bzw. alteMinen wiedereröffnet werden würden. Die Frageaber blieb offen, ob langfristig die Versorgung mitNatururan ausreichen würde um den Weltbedarf zurGänze zu decken. Die Preise für angereichertesUran und Anreicherungs-dienstleistungen bliebenindessen stabil. Unter diesen Umständen hat dieVersorgungsagentur die Verbraucher der EUweiterhin darin bestärkt, ihre Versorgungsquellen zudiversifizieren und einen Großteil ihres Bedarfs

durch Mehrjahresverträge und zu Preisen zudecken, die die Produktionskosten inangemessener Weise widerspiegeln.

Die Gemeinschaft Unabhängiger Staaten (GUS)war einmal mehr die größte Versorgungsquelle fürNatururan der EU. Die Russische Föderation bliebfür die EU im Jahre 1996 bei Natururan daswichtigste Versorgungsland. Die Versorgungs-agentur hat in diesem Zusammenhang ihre Politikder Diversifizierung der Versorgungsquellen und derAnwendung von marktgerechten Preisen in flexiblerund pragmatischer Weise fortgesetzt, und zwar imHinblick auf Angebote sowohl aus der laufendenProduktion dieser Länder wie aus militärischen undsonstigen Beständen.

Das neue Kooperationsabkommen zwischenEuratom und den USA, das das alte, aus demJahre 1960 stammende und am 31. Dezember1995 ausgelaufene Abkommen ersetzt, ist am12. April 1996 in Kraft getreten. Auch mitzahlreichen anderen Handelspartnern von Euratomgab es im Laufe des Jahres routinemäßigeKontakte. Die Versorgungsagentur konnte ihreinzwischen wohletablierte Rolle imKommissionsteam, das mit Fragen desinternationalen Nuklearhandels und denentsprechenden Verhandlungen befaßt ist,weiterhin wahrnehmen.

Annual Report 1996

Euratom Supply Agency

Annual Report 1996Page 7

Euratom Supply Agency

INTRODUCTION

Comme pour les années précédentes, l’Agences’est assurée, dans le cadre de l’exercice de sondroit exclusif de conclure les contratsd’approvisionnement, que les utilisateurs de l’UnionEuropéenne bénéficiaient d’un approvisionnementrégulier en combustibles nucléaires.

L’année 1996 a été caractérisée par une remontéedes prix de l’uranium naturel, affectant les contratstant pluriannuels que ponctuels (spot), mais à la finde l’année les prix étaient retombés par rapport auxvaleurs qu’ils avaient atteintes au milieu de l’année.La production totale a progressé; cependant, alorsque la production du monde occidental augmentait,celle du reste du monde diminuait. La perspectived’une remontée des prix a contribué à cetteaugmentation, ainsi qu’à l’annonce de plusieursprojets d’ouverture ou de réouverture de minesd’uranium. Cependant la question est restée poséede savoir si à plus long terme l’approvisionnementen uranium naturel suffira pour couvrir la totalité desbesoins mondiaux. Les prix de l’uranium enrichi etdes services d’enrichissement sont en revancherestés stables. Dans ces conditions, l’Agence acontinué à encourager les utilisateurs de l’Union àdiversifier leurs sources d’approvisionnement et àcouvrir la plus grande partie de leurs besoins par

des contrats pluriannuels, à des prix couvrant lescoûts de production.

La Communauté des Etats Indépendants (CEI) a denouveau été la plus importante sourced’approvisionnement de l’Union européenne enuranium naturel. En 1996, la Fédération Russe estdemeurée le principal pays fournisseur d’uraniumnaturel de l’Union Européenne. Dans ce contexte,l’Agence a poursuivi de façon flexible etpragmatique sa politique de diversification de sessources d’approvisionnement et de prix liés aumarché à l’égard des offres provenant de nouvelleproduction, ou de stocks militaires et autres de cespays.

Le nouvel accord de coopération Euratom/Etats-Unis, qui remplace le précédent accord datant de1960 et venu à échéance le 31 décembre 1995, estentré en vigueur le 12 avril 1996. Des contacts deroutine avec plusieurs partenaires commerciauximportants d’Euratom ont également eu lieu dans lecourant de l’année. L’Agence d’Approvisionnementa continué à jouer un rôle bien établi au sein del’équipe de la Commission chargée des questionsdu commerce nucléaire international et desnégociations dans ce domaine.

Annual Report 1996

Euratom Supply Agency

Annual Report 1996Page 9

Euratom Supply Agency

CHAPTER I

DEVELOPMENTS CONCERNING SUPPLY IN THE EUROPEAN UNION

SECURITY OF SUPPLY

NATURAL URANIUM

In 1996 natural uranium deliveries continued to becovered mainly by long term contracts, whiledeliveries under spot contracts represented some4% of total deliveries under purchasing contracts.The countries of the CIS, and especially Russia,continued to be the largest source of supply.

Estimated annual total reactor requirements fornatural uranium will average 20,700 tonnes ofuranium (tU) over the next 10 years. Potentialdemand (uncovered requirements) will be verylimited in 1997, in the order of an estimated2,500 tU in 1998, and will increase graduallythereafter.

The Supply Agency’s average price for naturaluranium deliveries under long-term purchasingcontracts in 1996 continued to decrease, but thespot price increased. Several important new longterm contracts between EU users and primaryproducers were signed in 1996.

According to preliminary figures, Western Worldproduction in 1996 rose by some 12% toapproximately 28,500 tU, largely through better useof existing capacity (essentially in Australia andCanada), while production in the rest of the world(essentially the CIS, Eastern Europe and China)continued to decrease. Accordingly, total worldproduction rose only slightly to some 35,500 tU. Inthe EU production remained at a very low level, andit is anticipated that in France production mightcease towards the end of the century. However, EUcompanies are continuing their production effortsoutside the Community, mainly through theirsubsidiaries in Africa, Canada, the United Statesand Australia.

Notwithstanding the increase in production, currentworld consumption (estimated at some 64,000 tU in1996 and expected to rise to 70,000 tU by 2000) isnearby double current fresh production, and asubstantial proportion of this production comes frommines which are likely to be exhausted soon afterthe turn of the century. The natural uraniumsupplies derived from disarmament of Russianwarheads are expected to amount to some37,000 tU between 1997 and 2001, but even if theyreach the market on schedule, it cannot beexcluded that new production beyond that alreadyplanned will have to be brought on line in order tobridge the gap between production andconsumption.

The possible opening of new mines in Australia andCanada was announced for around the end of thecentury, but there are still uncertainties which mightdelay or even cause the cancellation of some ofthese projects. The Agency believes that asufficiently high price level will be necessary tomake projects worthwhile and ensure thatproduction is started on time at these miningprojects.

In the first half of the year, published spot priceindicators increased rapidly to some US $16 perpound U3O8, but in the second half prices remainedstable and after that decreased slowly to someUS $14. The spot market price for natural uraniumhence saw an increase to levels not seen since thelate 1980s, but towards the end of the year pricesstarted to fall again.

CONVERSION, ENRICHMENT, FABRICATION

The uranium conversion, enrichment and fabricationmarkets remained stable in 1996, and facilities inthe EU provided adequate cover for its needs.Worldwide capacity is more than sufficient

Annual Report 1996Page 10

Euratom Supply Agency

to meet future requirements. Almost all enrichmentsupply took place under multiannual contracts.Estimated total enrichment requirements over thenext 10 years will be on average 12,000 tonnes ofSeparative Work (tSW) per year.

SUPPLY OF CIS ORIGIN MATERIALS

CIS SUPPLY

The CIS remains the largest source of naturaluranium supply to the EU, and in 1996 the RussianFederation was once again the EU’s largest singlesupplier country. Although questions remain aboutthe size of the civil uranium stockpiles in Russia, itbecame clear during the course of the year that atleast in terms of new contracts, Russia was notcontracting for the large quantities at very low priceswhich were such a feature of the uranium market inthe early 1990s. However, deliveries under oldcontracts continued to take place at prices someway below the Supply Agency’s current averageprice. The main question now facing the market isby whom and on what timescale the large quantitiesof natural uranium arising from the US-RussiaHighly Enriched Uranium (HEU) deal, to whichRussia has title, will be marketed.

Euratom and the US continued to be Russia’s mainoverseas markets for natural uranium. Russia’scontinued access to the US market as a result ofthe “matched sales” programme under theamended Suspension Agreement between the USDepartment of Commerce (DOC) and Russia,deliveries of Low Enriched Uranium (LEU) to the USunder the US-Russia HEU deal, and the news latein the year that some Japanese utilities might nolonger be excluding Russian origin material in theircalls for tender, all contributed to less material beingmade available on the EU market.

The Supply Agency continued to monitor carefullycontracts for supplies from the CIS, and to report ondevelopments to its Advisory Committee. TheAgency maintained its flexible and pragmaticapproach to the application of the supply policy,which aims to ensure security of supply through

diversification of sources and the avoidance of over-dependence on any one source. The considerablemarket share of the CIS, and in particular Russia,demonstrates clearly that CIS supplies have fairaccess to the EU market.

Purchases of natural uranium equivalent of CISorigin by EU utilities were in the order of 5,900 tU in1996, and a further 900 tU were acquired as a resultof exchanges and return of loans. Total acquisitionsof natural uranium from the CIS were thereforesome 6,800 tU, representing about 43% of totaldeliveries to EU utilities under purchasing contractsin 1996 (33% in 1995).

Deliveries of enrichment of Russian origin to EUutilities in 1996 in the context of enrichmentcontracts or the Separative Work component ofEnriched Uranium Product (EUP) represented about18% of total deliveries under purchasing contracts(23% in 1995).

1996 saw the dialogue between the Commissionand the Russian authorities on nuclear tradematters continue. Exploratory talks took place on afuture specific bilateral nuclear tradearrangement/agreement. One of the issues onwhich the Commission would like to deepen thedialogue in this context is the question of Russia’scapacity to supply in terms of current levels ofproduction of natural uranium, of productioncapacities for natural uranium and enrichment, andof the level of stockpiles of both natural uraniumand EUP. More comprehensive knowledge on thesepoints should help both sides towards a betterunderstanding of each other’s interests.

PHYSICAL IMPORTS AND STOCKS OF CIS ORIGINMATERIAL

According to notifications from EU operators,physical imports from the CIS of natural uranium orfeed contained in EUP amounted to some 65,300 tof natural uranium equivalent in the period 1992-96,of which some 16,600 t was imported in

Annual Report 1996Page 11

Euratom Supply Agency

1996. These quantities exceed by far deliveries toEU users, but include material in storage not yetcontracted for delivery to EU customers, material intransit for final use outside the EU, and a smallamount of uranium feed of non-CIS origin returnedto the EU after enrichment in Russia.

US SUSPENSION AGREEMENTS

The Suspension Agreements between US DOC anda number of CIS countries, which limit their naturaluranium exports to the USA, were further amendedin 1996.

In October, the option was closed through whichRussian uranium could be imported into the USAoutside the relevant quotas (tied to US production) ifenriched in the EU (known as the “enrichmentbypass”). As a result of this amendment to DOC’sagreement with Russia, and similar amendmentsdating from 1995 to the agreements withKazakhstan and Uzbekistan, a certain amount ofuranium of these origins enriched in the EU onbehalf of US utilities became stuck in theenrichment bypass and could not be imported intothe US. Throughout the year, discussions werereported as continuing between DOC and USutilities on “grandfathering” these quantities. DOCagreed to grandfather certain of these contractssubject to an arrangement whereby 75% of thematerial could enter the US freely and the remaining25% could enter subject to the condition of makingmatched purchases of freshly-produced USuranium. Consequential amendments have beenmade to the Suspension Agreement with Russiaand are expected to be made to the Kazakh andUzbek Suspension Agreements.

LEU DERIVED FROM EX-MILITARY HEU

The implementation of the 1994 agreementbetween the US and Russia for the sale of 500 t ofHEU blended down to LEU over twenty yearsremained closely linked with the process ofprivatising the US Enrichment Corporation (USEC).As part of the Senate budget package, legislation topave the way for privatisation fell victim to the

political impasse over the budget until late April,when this impasse was finally unblocked. Thislegislation contains not only provisions for USEC’sprivatisation, but also sets the maximum level ofsales of uranium feed from the US-Russia deal inthe US market, and of UF6 and HEU to betransferred from the stockpiles of the USDepartment of Energy (DOE) to USEC.

The major development of 1996 in this area was arevision of the agreement whereby Russia willdeliver 24 t of blended-down HEU to the US in1998. This is considerably more than the 6 t and12 t delivered in 1995 and 1996 respectively, andmore than the 18 t due to be delivered in 1997. Thisacceleration of the delivery schedule under the HEUdeal raises a number of questions about how thismaterial will be marketed. There are importantlimiting factors on the disposition of the material onthe US market, because the USEC Privatisation Actitself restricts sales of Russian uranium in the US. Itseems very probable that much of this material willbe targeted for marketing in the EU. The SupplyAgency’s view is that supplies of Separative Workcontained in the blended-down HEU from Russia,arising out of the US/Russia HEU deal, should besubject to the same supply policy considerations asmaterial coming directly from the CIS. The samewould apply to the natural uranium feed equivalentreturned by USEC to the Russians for subsequentsale.

OTHER DEVELOPMENTS

ENU CASE

The oral arguments in the appeal of Portugueseproducer ENU in its case against the Commission,relating to Community preference for uraniumproduced within the Community, were heard on8 October 1996 by the Court of Justice. ENU’sappeal is against the judgement of the Court of FirstInstance of 15 September 1995, which decided infavour of the Commission both with regard to ENU’sannulment action against the

Annual Report 1996Page 12

Euratom Supply Agency

Commission’s decision of 19 July 1993, and withregard to ENU’s claim for compensation.

On 5 December 1996, the Advocate-Generalpresented his opinion. He recommended the Courtto decide in favour of the Commission by rejectingENU’s annulment action as inadmissible, and itscompensation action as unfounded.

At the year end no date had been set for the Court’sfinal judgement. Editor’s note: the judgement in theENU case was made on 11 March 1997.

KLE CASE

The oral arguments in the case of German utilityKLE against the Commission were heard on18 September 1996 by the Court of First Instance.This case concerned an annulment andcompensation action brought by KLE against theCommission’s decisions of 4 and 21 February 1994.These decisions had supported the Agency’sdecision to impose as a condition upon theconclusion of a given contract that the origin of thesupplies involved not be CIS.

The Court has declared that oral pleading is closed,but no date had been set at the year end for theCourt’s judgement. Editor’s note: the judgement inthe KLE case was made on 25 February 1997.

DRAFT ILLUSTRATIVE NUCLEAR PROGRAMMEOF THE COMMUNITY (PINC)

The draft Illustrative Nuclear Programme of theCommunity, known by its French acronym as the“PINC” (Programme Indicatif Nucléaire de laCommunauté), was approved by the Commissionon 25 September 1996. Established according toArticle 40 of the Euratom Treaty, the PINC takes theform of a Communication from the Commission onthe nuclear industries in the EU, and wastransmitted to the Economic and Social Committeefor consultation, and for information to the Counciland the Parliament. The Commission will be calledupon to adopt the PINC definitively once thisconsultation process has been completed.

The PINC sets the nuclear option clearly in thecontext of an energy policy for the EU and the WhitePaper “An Energy Policy for the European Union”1,which was adopted in 1995. Nuclear energy willhave to be judged according to the contribution itcan make to the fundamental energy policyobjectives of overall economic competitiveness,security of supply, and environmental protection.

On the subject of nuclear fuel supply conditions, thePINC confirms that “The Commission and theEuratom Supply Agency are applying a policy ofdiversification of sources of supply, implemented ina flexible way by the exercise of the Agency’s rightto conclude contracts and aiming at avoidingoverdependence on any single source of supply”.2

RESEARCH REACTOR FUEL CYCLE

The Supply Agency continued to provide its supportto research reactor operators and industry in thisfield, and followed closely the problems associatedwith the supply of HEU and the disposal andreprocessing of spent research reactor fuel.

The major development during the year was thepublication by US DOE in May of the Record ofDecision announcing the acceptance andmanagement of spent nuclear fuel from foreignresearch reactors containing uranium enriched inthe US. This decision paved the way for the returnof large quantities of US origin irradiated fuel storedat reactor sites, which was creating seriousdifficulties for the operators and raising questions, insome cases, about the continued operation of theirreactors.

However, the above policy concerns only theexisting inventory of spent fuel and the spent fuelproduced over the next 10 years (i.e. fuel irradiated

1 Commission document COM(95) 682/final of 13 December 1995.2 Commission document COM(96) 339/final of 25 September 1996

(page 19 of the English version).

Annual Report 1996Page 13

Euratom Supply Agency

until May 2006). It is unlikely that the policy will beextended, and there will therefore be a continuedneed within the Community for specialisedreprocessing capacity, and the development ofsolutions for the disposal of spent fuel and/or waste.The United Kingdom Atomic Energy Authoritycontinued to postpone its decision on closing downthe research reactor fuel reprocessing facility atDounreay, and Cogema announced that it wasprepared to offer reprocessing and wasteconditioning services for spent research reactor fuelat its plant at La Hague.

The long term security of supply of HEU for the fivereactors within Euratom requiring fresh supplies ofthis material gave cause for concern, but there werealso positive developments in this area. The use ofexisting inventories in the Community allowedcontinued operation of all those reactors which

require HEU in the near future, and a new source ofsupply was found for two of them. Furthermore, USDOE is now technically in a position to supplyfurther quantities of HEU to those reactors preparedto commit themselves to convert to LEU fuels, assoon as new high density fuels are made availableas a result of a development programme nowunderway in the US.

REPROCESSING, PLUTONIUM AND MOX

The use of MOX in the Community continued tobecome more widespread, and more productioncapacity is due to come on line in the next fewyears. The amount of natural uranium andSeparative Work saved by the use of MOX fuel inthe Community can be estimated at some 1,200 t ofnatural uranium and some 700 tSW annually.

Annual Report 1996Page 14

Euratom Supply Agency

Annual Report 1996Page 15

Euratom Supply Agency

CHAPTER II

SUPPLY OF NUCLEAR MATERIALS AND ENRICHMENT SERVICES IN THE EUROPEAN UNION

REACTOR NEEDS/NET REQUIREMENTS

During 1996, the fresh fuel loaded in EU reactorscontained the equivalent of 18,400 t of naturaluranium and 11,100 tSW - most tails assays were inthe order of 0.30%.

Future EU reactor needs and net requirements foruranium and Separative Work, based on datasupplied by EU utilities, rounded to the nearest100 tU and 100 tSW respectively, are estimated asshown in Table 1.

Table 1 - Reactor needs and net requirementsfor uranium and separative work

Year Natural Uranium(tU)

Separative Work(tSW)

Reactorneeds

Net require-ments

Reactorneeds

Net require-ments

1997 19,600 16,300 10,200 9,200

1998 20,300 17,200 11,800 10,500

1999 21,500 19,200 12,000 11,000

2000 20,900 18,900 11,800 10,800

2001 21,100 19,300 12,200 11,500

2002 21,400 19,400 12,600 11,600

2003 20,300 18,400 12,000 11,000

2004 20,800 18,900 12,500 11,500

2005 21,000 19,300 12,400 11,500

2006 19,800 18,100 12,100 11,200

TOTAL 206,700 185,000 119,600 109,800

Average 20,700 18,500 12,000 11,000

Net requirements are calculated on the basis ofreactor needs less the contributions from currentlyplanned uranium/plutonium recycling, and takingaccount of inventory management ascommunicated to the Agency by utilities.

Average reactor needs for natural uranium over thenext 10 years will be 20,700 tU/year, while averagenet requirements will be about 18,500 tU/year.Compared to last year's report, these figures showan increase in reactor needs of 200 tU/year and anincrease in net requirements of 400 tU/year.

Average reactor needs for enrichment over the next10 years will be 12,000 tSW, while average netrequirements will be in the order of11,000 tSW/year.

NATURAL URANIUM

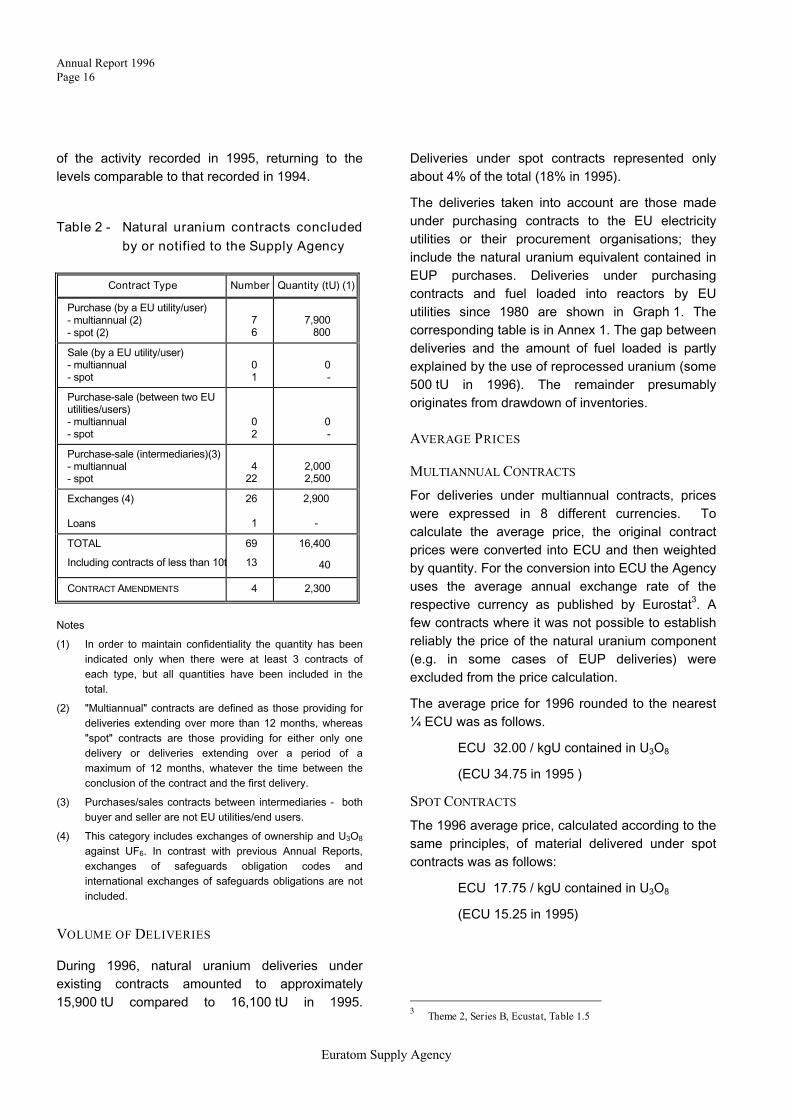

CONCLUSION OF CONTRACTS

The number of contracts and amendments relatingto ores and source materials (essentially naturaluranium) which were dealt with in accordance withthe Agency's procedures during 1996 is shown inTable 2.

Transactions involving natural uranium totalled16,400 tU, some 8,700 tU of which were the subjectof new purchase contracts by EU utilities. Some7,300 tU transacted related to purchases byproducers or intermediaries, as well as exchanges,loans, etc. This constitutes a drop to less than 50%

Annual Report 1996Page 16

Euratom Supply Agency

of the activity recorded in 1995, returning to thelevels comparable to that recorded in 1994.

Table 2 - Natural uranium contracts concludedby or notified to the Supply Agency

Contract Type Number Quantity (tU) (1)

Purchase (by a EU utility/user)- multiannual (2)- spot (2)

76

7,900800

Sale (by a EU utility/user)- multiannual- spot

01

0-

Purchase-sale (between two EUutilities/users)- multiannual- spot

02

0-

Purchase-sale (intermediaries)(3)- multiannual- spot

422

2,0002,500

Exchanges (4)

Loans

26

1

2,900

-

TOTAL

Including contracts of less than 10t

69

13

16,400

40

CONTRACT AMENDMENTS 4 2,300

Notes

(1) In order to maintain confidentiality the quantity has beenindicated only when there were at least 3 contracts ofeach type, but all quantities have been included in thetotal.

(2) "Multiannual" contracts are defined as those providing fordeliveries extending over more than 12 months, whereas"spot" contracts are those providing for either only onedelivery or deliveries extending over a period of amaximum of 12 months, whatever the time between theconclusion of the contract and the first delivery.

(3) Purchases/sales contracts between intermediaries - bothbuyer and seller are not EU utilities/end users.

(4) This category includes exchanges of ownership and U3O8

against UF6. In contrast with previous Annual Reports,exchanges of safeguards obligation codes andinternational exchanges of safeguards obligations are notincluded.

VOLUME OF DELIVERIES

During 1996, natural uranium deliveries underexisting contracts amounted to approximately15,900 tU compared to 16,100 tU in 1995.

Deliveries under spot contracts represented onlyabout 4% of the total (18% in 1995).

The deliveries taken into account are those madeunder purchasing contracts to the EU electricityutilities or their procurement organisations; theyinclude the natural uranium equivalent contained inEUP purchases. Deliveries under purchasingcontracts and fuel loaded into reactors by EUutilities since 1980 are shown in Graph 1. Thecorresponding table is in Annex 1. The gap betweendeliveries and the amount of fuel loaded is partlyexplained by the use of reprocessed uranium (some500 tU in 1996). The remainder presumablyoriginates from drawdown of inventories.

AVERAGE PRICES

MULTIANNUAL CONTRACTS

For deliveries under multiannual contracts, priceswere expressed in 8 different currencies. Tocalculate the average price, the original contractprices were converted into ECU and then weightedby quantity. For the conversion into ECU the Agencyuses the average annual exchange rate of therespective currency as published by Eurostat3. Afew contracts where it was not possible to establishreliably the price of the natural uranium component(e.g. in some cases of EUP deliveries) wereexcluded from the price calculation.

The average price for 1996 rounded to the nearest¼ ECU was as follows.

ECU 32.00 / kgU contained in U3O8

(ECU 34.75 in 1995 )

SPOT CONTRACTS

The 1996 average price, calculated according to thesame principles, of material delivered under spotcontracts was as follows:

ECU 17.75 / kgU contained in U3O8

(ECU 15.25 in 1995)

3 Theme 2, Series B, Ecustat, Table 1.5

Annual Report 1996Page 17

Euratom Supply Agency

Graph 1 Natural uranium feed contained in fuel loaded into EU reactors and natural uraniumdelivered to utilities under purchasing contracts (in tU)

0

5,000

10,000

15,000

20,000

1980 1985 1990 1995

tonn

es U

0

5,000

10,000

15,000

20,000

tonnes U

Fuel Loaded

Delivered

Graph 2 shows prices for deliveries undermultiannual as well as spot contracts since 1980,expressed in ECU. For ease of reference, historical

data on prices published in previous Annual Reportsand variations in exchange rates are presented inAnnex 2.

Graph 2 Average price for natural uranium delivered under spot and multiannual contracts(ECU/kgU)

0

25

50

75

100

125

1980 1985 1990 1995

EC

U/k

gU

0

25

50

75

100

125

EC

U/kgU

Multiannual

Spot

Annual Report 1996Page 18

Euratom Supply Agency

Graph 3 Acquisitions of CIS origin natural uranium by EU utilities (in tU)

0

2,000

4,000

6,000

8,000

1990 1991 1992 1993 1994 1995 1996

tonn

es U

0

2,000

4,000

6,000

8,000tonnes U

Exchanges / LoansPurchases / Sales

ORIGINS

EU utilities or their procurement organisationsobtained in 1996 approximately 90% of theirsupplies from 12 countries outside the EU. Thelargest single supplier was the Russian Federation,which represented 37% of total external supplyunder purchasing contracts and 33% of total supplyunder purchasing contracts.

Acquisitions of CIS origin natural uranium by EUutilities since 1990 are shown in Graph 3, which isprovided for reference purposes and brings togetherinformation already published in previous AnnualReports.

SPECIAL FISSILE MATERIALS

CONCLUSION OF CONTRACTS

The number of contracts and amendments relatingto special fissile materials (enrichment, enricheduranium and plutonium) which were dealt withduring 1996 in accordance with the Agency'sprocedures is shown in Table 3.

LOW ENRICHED URANIUM

In 1996, supply of enrichment services to EUutilities totalled approximately 11,700 tSW,delivered in 2,400 t of LEU which contained theequivalent of some 18,900 t of natural uraniumfeed. Some 75% of this Separative Work wasprovided by EU companies (Eurodif and Urenco).Some 4% of deliveries of Separative Work tookplace under spot contracts.

ENRICHED URANIUM FOR RESEARCH REACTORS

Enriched uranium for research reactors is normallysupplied in two enrichment assays: just under 20%(LEU) and about 90% (HEU).

Although the quantities involved represent a minoramount in terms of EU needs for enriched uranium,HEU supply is very important to the scientificcommunity and is of high political significance.

Supply of LEU to research reactors continuedunhindered. Reactor requirements for HEU weremet, but the source of future supplies continued tobe the object of considerable attention (see also

Annual Report 1996Page 19

Euratom Supply Agency

Chapter IV). The Supply Agency continued toprovide support to reactor operators in theprocurement of fuels.

PLUTONIUM

In 1996, transactions involving plutonium wereagain mainly related to its use for MOX fuelfabrication and the Agency concluded 17 suchcontracts.

Table 3 - Special fissile material contractsconcluded by or notified to theSupply Agency

Contract Type (1) Number

I. Special Fissile Materials

Purchase (by a EU utility/user)- multiannual- spot

312

Sale (by a EU utility/user)- multiannual- spot

816

Purchase-sale (between two EU utilities/users)- multiannual- spot

017

Purchase-sale (intermediaries)- multiannual- spot

424

Exchanges (swaps) 17

Loans 2

TOTAL, including (2)- Low enriched uranium- High enriched uranium- Plutonium

103602717

CONTRACT AMENDMENTS 2

II. Enrichment Contracts (3)

- multiannual- spot

61

CONTRACT AMENDMENTS 14

Notes

(1) See explanations under Table 2, as appropriate.

(2) Some contracts may involve both LEU and plutonium.

(3) Contracts with primary enrichers only.

Annual Report 1996Page 20

Euratom Supply Agency

Annual Report 1996Page 21

Euratom Supply Agency

CHAPTER III

NUCLEAR ENERGY DEVELOPMENTS IN THE EUROPEAN UNIONMEMBER STATES

BELGIQUE/BELGIË - BELGIUM

ENERGY POLICY CONSIDERATIONS

At the beginning of 1996 the Governmentauthorised new electricity production capacity equalto 1,885 MWe for the period 1996-2000, in order tocompensate for the shut-down of older installationsand to meet a rise in demand. This new capacityconsists of:

◊ 725 MWe nuclear power, which representsBelgium’s participation in the plants Chooz B1and B2;

◊ 1,160 MWe from gas-fired plants, equipped withgas-steam turbines.

The electricity sector has to introduce a newequipment plan for the period 1998-2008 at thebeginning of 1998.

The new law of 15 April 1994 concerning theprotection of the population and the environmentagainst the dangers of ionising radiation and thecreation of a Federal Agency for Nuclear Controlhas partly entered into force, and the GoverningBoard and the Government Commissioner of theAgency have been nominated. The Council of Statehas given its advice on the draft royal decreeconcerning the adaptation of the general regulationon ionising radiation. It is now adapted in order totake due account of the remarks of the Council ofState.

NUCLEAR ELECTRICITY GENERATION ANDCONSUMPTION

In 1996, Belgium’s nuclear power stations (includingthe French part of Tihange 1) generated

about 41.4 TWh. This is 5.7% more than in 1995. Itrepresents 57.3% of the country’s total electricityproduction in 1996, which is 2% more than in 1995.This positive development is due to the excellentload factor of the Belgian nuclear power plants andthe increase in production capacity of some plants.Above those already mentioned in the 1995 AnnualReport, the following increases were achieved in1996:

◊ Doel 3: an increase from 970 MWe to1,006 MWe

◊ Tihange 2: an increase from 930 MWe to955 MWe

This increase in production capacity was madepossible by the replacement of the turbine rotors.

FUEL CYCLE DEVELOPMENTS

Belgium produced 33 tonnes of natural uranium in1996, derived from imported phosphates.

The production of MOX fuel by Belgonucléaire in itsDessel plant amounted to 36 tonnes in 1996, to beused in Belgian and German nuclear power plants.

The recommendations of the resolution ofParliament adopted on 22 December 1993,concerning the use of MOX fuel in Belgium’snuclear power plants and the suitability ofreprocessing spent fuel, have continued to becarried out as in previous years. In this context thefollowing developments took place in 1996 :

◊ 20 MOX fuel elements were loaded in 1996 inunits Doel 3 (8 elements in March) andTihange 2 (12 elements in May), which bringsthe total to 36.

Annual Report 1996Page 22

Euratom Supply Agency

◊ In the framework of Synatom’s programme forthe encapsulation of spent fuel for directdisposal, some improvements have taken placein the conceptual design of the referencecontainer defined in 1995. The second phase ofthe programme was finalised. It consisted ofputting together the safety rules and definingthe basic hypotheses for the conceptual designof the spent fuel conditioning plant. The thirdphase, which is the conceptual design of theplant itself, has been started.

◊ In the framework of the R&D programme ongeological disposal of both high-level, medium-level and long-lived waste and of spent fuel,mainly carried out by the Nuclear ResearchCentre at Mol, but co-ordinated and managedby Niras/Ondraf, the following importantactivities took place:

• as part of the specific programme of theEuropean Commission on nuclear fissionsafety, the first performance assessment ofthe disposal of spent fuel in a clay layer hasbeen published. A more detailed safetyanalysis has been started;

• an experimental programme has beenlaunched into the interaction between theclay and the spent fuel elements;

• a study has been completed into thetransportation and handling of the spent fuelelements in the underground repository;

• for the PRACLAY programme, whichstudies the thermo-hydro-mechanic aspectsof the disposal of heat-producing waste,and which is also applicable to spent fuel, amodel representing a section of a disposalgallery has been prepared;

• an appropriate concept for the disposalgalleries for spent fuel elements was understudy.

◊ 56 spent fuel elements from Doel 3 have beenplaced in two dry storage containers in theinterim storage building constructed on the sitein 1995. At Tihange, the construction of a newwet storage building has continued.

A dummy test of all phases of the return to theBelgoprocess (daughter company of Niras/Ondraf)site of the High-Level Waste (HLW) glass canistersresulting from the reprocessing of Belgian spent fuelat La Hague has been successfully carried out. Onthe Belgoprocess site, the part of the building wherethe HLW glass canisters will be stored has beenoperational since mid-1994. The part which is toreceive the other types of reprocessing waste wasalmost completed in 1996.

RESEARCH REACTORS

The materials testing reactor BR2 of the NuclearResearch Centre CEN/SCK at Mol underwentrefurbishment throughout 1996. No particulartechnical problems have arisen during therefurbishment. It has been proposed to conclude acontract with Cogema for the reprocessing of all theexisting and future spent fuel elements from theBR2.

DANMARK - DENMARK

RADIOACTIVE WASTE

Denmark has no nuclear power plants and theamount of radioactive waste is therefore small. AtRisø National Laboratory there are two reactors inoperation: a research reactor and an educationalreactor. Spent fuel is sent by ship to the UnitedStates according to US policy for research reactorfuel of US origin. There are no plans for disposal ofHLW in Denmark.

Low-Level Waste (LLW) and Intermediate-LevelWaste (ILW) are collected, treated and stored intwo intermediate storage facilities on the site ofRisø. A storage facility for LLW receives about 100-120 200L-drums per year. Two-thirds of the amountis produced by Risø National Laboratory, the restcomes from hospitals, industry, laboratories andother users of radioactive isotopes in Denmark.

Annual Report 1996Page 23

Euratom Supply Agency

At the moment about 4,400 drums are stored in thisfacility, which has a total capacity of 5,000 drums. Astorage facility for ILW receives about 0-5 drumsper year. The amount is decreasing after the hot cellfacility was closed in 1994. At the moment about130 m3 of long-lived LLW is stored in this facility.

Solid LLW is compacted in drums and liquid LLW istreated in an evaporator and a bituminization plant.The waste embedded in bitumen is then stored indrums. The ILW is not treated but stored instainless steel containers or drums.

At the moment Denmark has no plans forconstruction of a repository for final disposal of LLWand ILW.

DEUTSCHLAND - GERMANY

GENERAL CONSIDERATIONS

The combined development of a EuropeanPressurised Water Reactor (EPR) by both Frenchand German utilities involved in nuclear powergeneration and the power plant constructors wentaccording to plan in 1996. An importantintermediate stage in the project will be reached inmid-1997 with the completion of a Basic DesignReport. Amongst other things, these studies shouldprovide an answer to the question of whether theEPR can be operated economically. The Germancompanies participating in the project announced inDecember 1996 that they would make availableabout DM 150 million for a further three-year studyphase, in which the emphasis would be on provingthe project’s ability in principle to obtain a licence,with the involvement of public authorities andtechnical standards bodies. This process shouldenable not only operators and constructors, but alsopublic authorities and technical standards bodies, tomaintain their capability to plan, licence andeventually carry out new projects involving nucleartechnology.

NUCLEAR ELECTRICITY GENERATION ANDCONSUMPTION

Germany’s nuclear power plants generated161.7 TWh of electricity in 1996, 4.9% more than inthe previous year. Nuclear power’s share inelectricity generation in Germany was again aboutone third.

The 1996 figure for nuclear electricity generation isthe highest since the advent of commercial nuclearpower in Germany. This is all the more remarkablebecause with the closure of the Würgassen powerplant in 1995 and the long outages at Biblis forpolitical reasons, there was nominally less availablecapacity. The decisive factors in this goodperformance were both the excellent level ofavailability of the power plants and the increasingachievement of efficiency improvements throughmodifications to the low-pressure turbines. Thisprogramme of improvements, put into action step-by-step since the early nineties, had resulted in acapacity increase of over 400 MWe by the end of1996.

Of Germany’s 20 commercial nuclear power plants,19 were connected to the grid for the majority of thetime at a high level of availability. The Mühlheim-Kärlich nuclear power plant is still out of operationbecause of the revocation by the Rheinland-PfalzAdministrative Court of the newly formulated permitfor partial construction. In the meantime, theFederal Administrative Court has accepted operatorRWE Energie AG’s application to appeal againstthis decision. Biblis A is now connected to the gridagain after a 13-month outage caused by a leak in avalve in one of the steam pipes.

FUEL CYCLE DEVELOPMENTS

Separation of uranium from the reclamation processat Wismut’s Königstein mine resulted in some 40 tUin concentrates. After 1996, Wismut will notcontinue to process uranium concentrates fromreclamation.

Annual Report 1996Page 24

Euratom Supply Agency

Urenco Deutschland GmbH’s uranium enrichmentfacility in Gronau ran uninterruptedly at nearly 100%capacity. Total production since entry into servicereached 5,000 tSW in September. The extension ofthe facility to its licensed capacity of 1,000 tSW/yearran to schedule and will be completed in one year’stime. At the end of 1996, capacity stood at800 tSW/year. The ongoing process of licensing afurther increase of the facility’s capacity to1,800 tSW/year has been slightly delayed. A licenceis expected to be granted in the course of 1997.

Siemens AG KWU covers its European marketshare in the fabrication of fuel elements through theANF fuel fabrication facility in Lingen. Since the lasthalf of 1996, ANF has had a second completeproduction line at its disposal. In October 1996, alicence application was made for an increase in thequantity of material being processed in thefabrication of fuel rods and the final assembly of fuelelements.

The Hanau facility, with its two sections devotedrespectively to uranium processing and MOXprocessing, is in the process of being shut down.More than 700 tU has been removed from theuranium processing section of the plant, and someparts of that section have already been downgradedto the level of controlled areas for radiationprotection purposes. The plan for the MOXprocessing section of the facility is that theremaining inventory of plutonium should beconverted into a form suitable for long term storage,and that the existing plant should be put back intooperation in the context of decommissioning thefacility.

Substantial changes have been made in the plansfor decommissioning the reprocessing facility inKarlsruhe. The intention is no longer to vitrify theliquid high level waste at the PAMELA facility at Molin Belgium, but instead to construct an on-sitevitrification plant at the Karlsruhe research centre.

No further spent fuel was placed in the interim storeat Ahaus in 1996. The process of obtaining alicence to extend the capacity of the store to 4,200 tHeavy Metal is ongoing, and a licence is expected

to be granted in 1997. The first transport andstorage container holding 28 vitrified waste blocksarising from reprocessing in France was placed inthe identically constructed interim store at Gorlebenin May 1996.

Storage of waste at the Morsleben final disposal sitewent smoothly in 1996. Between the resumption ofoperations on 13 January 1994 and the end of1996, some 10,600 m3 of low and intermediate levelwaste underwent final disposal. 1996 saw nonoticeable progress in the licensing procedure forthe planned Konrad final disposal site. Theexploratory work on the suitability of the saliferousrock at Gorleben as a final disposal site wentaccording to plan in 1996. The two shafts havebeen joined at a depth of 840m, and work hasbegun on the construction of spaces for equipmentand for storage.

ELLAS - GREECE

No new developments were reported.

ESPANA - SPAIN

NUCLEAR ELECTRICITY GENERATION ANDCONSUMPTION

Gross production of electrical energy of nuclearorigin in Spain during 1996 was 56,204 GWh, whichrepresents approximately 34% of total nationalproduction. As in recent years, the performance ofthe nuclear park has been highly satisfactory, asreflected in the average load factor of 86.1%.

The steam generators of unit 1 of the Almaraznuclear power plant and of Asco 2 have beenreplaced. In both cases, the units were stopped forabout two and a half months in accordance with theplanned programme. During these outagesmodifications were carried out to the turbines of

Annual Report 1996Page 25

Euratom Supply Agency

both units, increasing their electrical power by 52and 38 MWe respectively.

In March, the entry into service of a new coolingtower was authorised at the José Cabrera plant,allowing the plant to operate at full power whileminimising the thermal environmental impact on theriver water.

FUEL CYCLE DEVELOPMENTS

In July 1996, the Ministry of Industry and Energygranted the Empresa Nacional del Uranio, S.A.(ENUSA) an extension for a ten-year period of boththe Juzbado (Salamanca) fuel fabrication plant’sprovisional operating permit and its authorisation tofabricate fuel elements. This plant continues tomanufacture PWR and BWR fuel elements both forSpanish nuclear plants and for various Europeancountries. Its production in 1996 was 683 elements,containing 216 t of UO2.

In October, the Ministry of Industry and Energygranted the Empresa Nacional de ResiduosRadioactivos, S.A. (ENRESA) a five-year extensionto its provisional operating permit for theintermediate and low-level solid radioactive wastestorage facility at Sierra Albarrana (El Cabril). At theend of 1996, 4 of the existing 28 cells at the facilityhad been filled completely.

The Quercus uranium concentrates productionplant, which belongs to ENUSA, continued tooperate at below design capacity, producing about300 t of U3O8 in 1996.

The intermediate storage strategy for spent fuelcontinued to be developed, with increases in 1996in the capacity of the spent fuel pools at the Trillo,Vandellos 2, Santa Maria de Garona, Cofrentes andJosé Cabrera plants through the installation of racksof compact design. At Trillo, an additional buildingis planned for the storage of metal spent fuelcontainers, and will be used once the capacity of thespent fuel pool has been filled.

The preparatory work of processing low leveloperational radioactive waste continued prior to the

start of dismantling the definitively closed Vandellosnuclear power plant. When utility Hifrensa hascompleted these works, and once the NuclearSafety Council has given a favourable report andthe Ministry of the Environment has issued theEnvironmental Impact Report, the Ministry ofIndustry and Energy will be able to authorise theclosure and dismantling of the plant. The plan is toreach level 2 “restricted release of the site” in fouryears, and to complete dismantling up to level 3“unrestricted release of the site” after an estimatedwaiting period of 25 years.

By the end of 1996, the work on dismantling andclosure of ENUSA’s Lobo G uranium ore processingplant at La Haba (Badajoz), had reached anadvanced stage and should be completed in the firstquarter of 1997.

FRANCE

GENERAL CONSIDERATIONS

On 31 December 1996, French nuclear facilitiesnumbered 55 pressurised water reactors inoperation (thirty-four 900 MW PWR’s, twenty1,300 MW PWR’s and one 1,450 MW PWR) andtwo fast reactors (Phénix and Superphénix). 3reactors of 1,450 MW each are under constructionfor commissioning by 1998.

NUCLEAR ELECTRICITY GENERATION ANDCONSUMPTION

Gross national consumption of electricity rose to414 billion KWh, an increase of 4.2% comparedwith 1995.

Industrial consumption was up by 3.7% comparedto 1995. Tertiary industries and domesticconsumption increased by 4.7%. The exportbalance was relatively stable compared to 1995 andamounted to 69 TWh.

Annual Report 1996Page 26

Euratom Supply Agency

Total net production of electricity rose to 489 billionKWh, i.e. 3.7% more than 1995. 378.2 billion KWhwere produced by nuclear power stations,representing approximately 77% of nationalproduction. Thermal production from fossil fuelswas 41.8 TWh. Hydroelectric production decreasedby 9.1% compared with 1995 and amounted to68.9 TWh.

As regards nuclear operation, 1996 showed aprogression in availability levels, which increased to82.7% compared to 81% in 1995.

The daily peak of domestic consumption amountedto 69,000 MW, which is close to the record of70,000 MW reached on January 4, 1993.

The Creys-Malville fast breeder was operated to90% of its capacity on October 22, and thereforeproduced 1,060 MW.

The program of testing and removing vessel headshas been carried forward. Since 1994, 18 vesselheads out of the 54 in operation have beenreplaced. Also, 3 steam generator replacementshave been completed.

At the end of 1996, nine reactors were operatingwith MOX fuel.

FUEL CYCLE DEVELOPMENTS

URANIUM MINING

Uranium production in France amounted to 930 tUin concentrates in 1996, 5% down as compared to1995. The closure of the mining division of l’Héraulthas been announced by Cogema for mid-1997.

In Canada, the development of the McClean Lakeproject continued: mining of the JEB open pit hasbeen carried out and the ore reached the plant atthe end of the year. The construction of theprocessing plant has gone ahead with the objectiveof commissioning it in mid-1997.

URANIUM CONVERSION

In May 1996 Comurhex celebrated the delivery of its200,000th tonne of uranium as UF6, which wasdelivered to a Japanese utility.

URANIUM ENRICHMENT

The start-up authorisation for the TU5 installation atPierrelatte, at first expected in 1995, was receivedat the beginning of January 1996. The installation isdevoted to the conversion of reprocessed uraniuminto oxide.

REPROCESSING

The UP2 and UP3 plants operated satisfactorilyduring 1996. More than 321 spent fuel casks werereceived and unloaded for reprocessing. 820 t ofoxide fuel were reprocessed in 1996 in UP3(reaching the nominal capacity of the plant), andUP2 reprocessed 862 t of oxide fuel. A total of1,682 t of oxide fuel was reprocessed in 1996,bringing the cumulative quantity to 10,235 t since1976.

Regarding the reprocessing/recycle programme,commissioning of the MELOX plant continued.

RADIOACTIVE WASTE

Investigations with a view to setting up undergroundresearch laboratories continued at the start of 1996.Given the outcome of this work, the FrenchGovernment has authorised the NationalRadioactive Waste Management Agency (ANDRA)to file three documented applications forauthorisation to set up and operate undergroundlaboratories in the Gard and the Viennedepartments and in eastern France (on the borderbetween the Meuse and the Haute-Marnedepartments). Procedures are expected to last 18 to24 months.

IRELAND

Ireland does not have a nuclear power industry andthere are no plans for such. Ireland’s nuclear policyobjectives emphasise the need for the

Annual Report 1996Page 27

Euratom Supply Agency

enhancement of nuclear safety and radiationprotection world-wide. The Government is advisedon and assisted with the implementation of thispolicy by the Radiological Protection Institute ofIreland. Ireland remains opposed to the continuedoperation and expansion of the nuclear industry.

ITALIA - ITALY

A new impulse is being given by ENEL and ENEAon the one hand, and by ANPA on the other hand,to the implementation of the national policy onradioactive waste management.

ENEL is engaged in decommissioning its fourNuclear Power Plants (NPP’s) following a strategywhich is consistent with the one adopted by mostcountries. According to the programme, the firstNPP which will reach a safe state, in a year’s time,will be Garigliano power station, followed by Latinaand Trino power stations. In particular at Gariglianopower station, activities to put radioactive waste in asafe state by MOWA machine are under way andwill last 18 months. In the next few months Caorsopower station will start the preliminary licensingprocedure necessary to reach the safe stage.

ENEL is also engaged (together with Ansaldo andFIAT as the GENESI consortium) in a preliminarystudy into the construction of an interim dry store forirradiated fuel. Research activity on passively safereactors continued in 1996, both with Europeanpartners (utilities and constructors), and in theframework of an international agreement.

ENEA, in the context of a comprehensive actionprogramme on its nuclear waste, and following acall for tender launched at European level, hassigned a US $15 million contract with a consortiummade up by Techint, SGN, Ansaldo and Fiat(GENESI Consortium) and NUCLECO for theconstruction of a vitrification unit for the high andlow-level liquid wastes at Saluggia. The design,construction and testing of this facility is planned totake five years. ENEA has also set up a specificTask Force for implementing the actions related tothe selection and qualification of a site for a low-level waste repository. The same site is being

considered for the interim storage facility to beconstructed for spent fuel and vitrified high-levelwaste.

NEDERLAND - NETHERLANDS

ENERGY POLICY CONSIDERATIONS

As already pointed out in the 1995 Annual Report,at the end of 1995 the Netherlands Minister ofEconomic Affairs sent a White Paper to Parliamenton the energy policy for the Netherlands in the yearsto come. This White Paper outlines what stepsshould be taken towards a more sustainable energyeconomy, on the one hand in order to secure areliable long-term energy supply and on the otherhand in order to respond to the threatening climateproblem. The main objective of Dutch energy policyis to achieve an energy efficiency improvement ofone-third in the next 25 years and a 10% share forrenewables in total primary energy consumption bythe year 2020. This is in order to reach stabilisationof CO2 emissions, which at that time should notexceed the level of 1990. Furthermore, the marketsfor electricity and gas will be opened up while theresponsibilities of the government will be restricted.

In a liberalised international energy market, theDutch energy industry will be able to become moreinvolved in nuclear energy abroad, by means ofimports, financial participation in foreign electricitygenerators whose fuel mix includes nuclear, orsupplies by Dutch firms to the nuclear industry.

Like other energy sources, nuclear energy can beassessed on a number of criteria: relative costs,environmental impacts, safety, technologicaldevelopment and demand. In the Netherlands,nuclear energy currently has a number ofdrawbacks: limited public acceptance due to(perceived) risks, radioactive waste, the proliferationproblem and a moderate competitive position.However, it also has a number of specific

Annual Report 1996Page 28

Euratom Supply Agency

advantages: a relatively stable price, relatively largeuranium reserves and no CO2 emissions.

It is no simple matter to assess these dissimilaradvantages and disadvantages. But neither is itopportune to make such an assessment at present,when there is in the Netherlands a surplus ratherthan a shortage in capacity. However, that is not setin stone for eternity. Changing circumstances maylead to a change in the balance one way or theother. Against this background, the Dutch Cabinetdecided to pursue the following policy. First of all,activities in the past make it necessary to maintain acertain level of nuclear knowledge for supervision ofexisting plants and ultimate decommissioning ofplants, solving the problem of radioactive waste andsupporting non-proliferation policy. Knowledge isfurthermore needed to permit effective response topossible accidents with nuclear installations in othercountries. In addition, nuclear research and theknowledge generated keeps the possibility open forthe Netherlands to catch up in the next century ifdesirable. The Netherlands has no ambition in duecourse to be able to construct nuclear power plantsentirely by itself, but if such plants should be built inthe Netherlands in the future, it does want to be aknowledgeable partner.

NUCLEAR ELECTRICITY GENERATION ANDCONSUMPTION

At the moment there are two nuclear power plantsin the Netherlands :

◊ Dodewaard (1969) BWR 57 MWe net (will beshut down in the course of 1997, see below);

◊ Borssele (1973) PWR 459 MWe net (to beoperated until 2004).

Together, their percentage of centralised electricitygenerating capacity was 8%.

On 3 October 1996, the board of directors of theDutch utility SEP (N.V. Samenwerkendeelectriciteits-produktiebedrijven) decided to shut theDodewaard reactor permanently in the near future,with a tentative closure date of spring 1997. The

decision was taken by SEP because it could nolonger justify continued operation of the uneconomicplant in the light of impending European electricitymarket deregulation. Furthermore SEP concludedthat the perspective of a positive decision by theDutch government on nuclear energy in theNetherlands in the foreseeable future had ceased toexist.

Dodewaard, which began operation in 1969, wasbuilt by General Electric Co. as a unique design withnatural circulation and an isolation condenser,features that have led its promoters to bill it as theprototype of a future passively safe BWR. Originallyplanned to shut on 1 January 1995, its life wasextended once to 1 January 1997, and again lastyear to 2004.

N.V. GKN, the SEP daughter company thatoperates Dodewaard, initiated an upgrading projectin connection with that life extension, work on whichwas to have begun in 1997. SEP plans to finishinitial decommissioning activities by 2003 andmothball the plant for 40 years before completedismantling.

FUEL CYCLE DEVELOPMENTS

URANIUM ENRICHMENT

On 17 September 1996, Urenco Nederland B.V. gota licence on the basis of the Nuclear Energy Actwhich enables Urenco to replace some equipmentin order no longer to make use of gases thatdeplete the ozone layer. For the first time in manyyears no appeal against a nuclear energy licencehas been submitted.

ÖSTERREICH - AUSTRIA

ENERGY POLICY CONSIDERATIONS

Austria’s energy policy, based on the principles ofthe International Energy Agency of the OECD, islaid down in the 1996 Energy Report of the AustrianGovernment.

Annual Report 1996Page 29

Euratom Supply Agency

The implementation of this policy has been pursuedwith special attention to changing energy andenvironment policy requirements, both at nationaland international level, and with a view to meetingthe challenges posed by:

◊ the continued progression of Europeanintegration, which requires constructive co-operation as well as corresponding legaladaptations;

◊ the anticipated global climate change,necessitating CO2 emission reduction measureson a national basis;

◊ the far-reaching changes in the economies ofCentral and Eastern Europe, which are openingup new challenges and co-operationpossibilities.

Taking into account the above-mentionedchallenges, the most important objectives ofAustria’s long-term energy policy remainunchanged: satisfying energy requirements, securityof supplies, environmental compatibility andconservation of energy resources, socialacceptance, according the highest priority to energyefficiency and the reduction of oil consumption andoil import dependency as well as of energy importsin general, and the increased utilisation ofrenewable energy resources.

The following figures on the development of energyand oil consumption demonstrate that Austrianenergy policy has proved very successful:

◊ energy intensity (primary energy supply (PES)per unit of gross domestic product (GDP))decreased from 807 MJ/1000 ATS GDP in 1980to 658 MJ in 1994, i.e. by 18.5%;

◊ the share of oil in energy supply fell from 50% in1980 to 42% in 1994. The share of renewablesincreased from 22% in 1980 to 26% in 1994.Overall carbon dioxide emissions have beenstabilised at the level of the early seventies;

◊ specific energy demand in industry (industrialenergy input per unit of industrial net product)further decreased by one third between 1980and 1994.

Combined efforts by the Federal Government, theLänder (provinces) and of both the producer and theconsumer side and their representatives - the so-called social partners - will ensure that the commonenergy policy objectives will also be achieved in thefuture.

As regards the production of electricity, theutilisation of nuclear fission for the supply ofelectricity is prohibited in Austria by a federal law(Law Gazette N° 676/1978), as result of areferendum.

RADIOACTIVE WASTE

Having no nuclear power plants in operation, Austriadoes not produce high-level radioactive waste, andtherefore there are no plans to build intermediate orfinal storage facilities. The small quantities of high-level waste produced by research reactor fuel willbe shipped to the United States during the nextdecade according to the renewed US policy for fuelof US origin.

Low and medium-level waste from hospitals,industry and research laboratories (30-40 t/year) iscollected and treated by the Austrian ResearchCentre Seibersdorf. The research centre isequipped with suitable facilities to treat andcondition low and medium-level waste, e.g.,incinerator, supercompactor and waste waterevaporator. Cementing is predominantly used asthe conditioning process.

On the basis of a joint agreement between theRepublic of Austria, the community of Seibersdorfand the Austrian Research Centre Seibersdorf,intermediate storage is provided until 2012 on thesite of the research centre for a capacity of

Annual Report 1996Page 30

Euratom Supply Agency

15,000 drums of conditioned waste. After this date,the waste has to be transferred into a final plannedstorage facility which is supposed to be built on asite to be selected at the beginning of the nextdecade.

RESEARCH REACTORS

Austria has no nuclear power plants. However,three research reactors are in operation in Vienna,Seibersdorf and Graz.

The overall situation, as already reported in the1995 Annual Report, remains unchanged.

PORTUGAL

ENERGY POLICY CONSIDERATIONS

Portugal depends heavily on imported energy.Around 90% of the Total Primary Energy Supply(TPES), which in 1994 amounted to 18 Mtoe (Milliontonnes oil equivalent), is imported. Imported oil andcoal contribute 70% and 18% respectively to theTPES. Domestic sources are hydroelectricity andother renewables, mainly firewood, which in totalaccount for 12% of TPES.

In order to diversify energy supply and reduce CO2

emissions growth, a programme is underway for theintroduction of natural gas, imported from Algeriavia Morocco and Spain through the so calledEurope-Maghreb gas pipeline. The first deliveriesare expected to take place in early 1997.

A gas fired power plant (Tapada do Outeiro)consisting of three 330 MW units of the combined-cycle gas turbine type is under construction, and thefirst unit is scheduled to start operation in March1998, the second in November the same year, andthe third in March 1999. It is expected that around40% of the imported natural gas will be used inthose units.

NUCLEAR ELECTRICITY GENERATION ANDCONSUMPTION

Portugal has no nuclear power plants and atpresent there are no plans to use this source ofenergy.

FUEL CYCLE DEVELOPMENTS

Yellow cake production is currently being carried outat a reduced level that amounted to 17.3 t of U3O8 in1996.

There are plans to start exploitation of the Nisauranium ore deposit, located in the region of AltoAlentejo, if market conditions allow it. This wouldincrease annual production to 130 tU/year. The pre-feasibility study has already been concluded.

RESEARCH REACTORS

Until the end of the century no new fuel is expectedto be needed for the Portuguese Research Reactor(RPI), which is owned and operated by the InstitutoTechnológico e Nuclear (ITN) of the Ministry ofScience and Technology.

SUOMI/FINLAND - FINLAND

ENERGY POLICY CONSIDERATIONS

In 1996, energy taxes in the electricity sectorremained unchanged compared to 1995. From thebeginning of 1997, however, new energy taxlegislation will enter into force. A system where thefuels used for electricity production were subject totaxation will be replaced by a system where the endproduct, electricity, is taxed. The new systemweakens the competitiveness of nuclear powercompared with coal in electricity production, eventhough an extra tax to which nuclear electricity wassubject has now been abolished.

Annual Report 1996Page 31

Euratom Supply Agency

NUCLEAR ELECTRICITY GENERATION ANDCONSUMPTION

In 1996 the electricity produced by the two Finnishnuclear power plants, both comprising two units,totalled 18.7 TWh (net) and covered 27% ofelectricity consumption in Finland. The weightedaverage load factor for the four units was 91.4%.

Applications for permits to raise permanently thepower levels of all the existing nuclear power unitswere lodged with the Ministry of Trade and Industryat the end of 1996. The applicants aim at capacityadditions totalling 980 MWth. Environmental impactassessment procedures related to these additionshave been initiated for both sites.

FUEL CYCLE DEVELOPMENTS

RADIOACTIVE WASTE

The construction of a repository for low andmedium-level nuclear waste from the Loviisa powerplant has proceeded in accordance with thetimetable. The first stage will be completed in early1997.

Posiva Oy, a company owned jointly by the twoFinnish nuclear power operators and responsible forpreparations for the final disposal of all existing andfuture spent nuclear fuel in Finland, has completedinterim reporting on the studies for the future site ofa deep geological repository, and on safetyassessment of spent fuel disposal. Detailedgeological studies have been carried out at threelocalities in between 1993 and 1996. The studiessupport the earlier conclusion from preliminarystudies that all three locations are geologicallysuitable for a spent fuel repository. Based on recentpreliminary studies, the Loviisa NPP site has beenchosen as an additional location for detailedgeological studies due to its existing infrastructure.Posiva has also decided to start environmentalimpact assessments for all four localities.

RESEARCH REACTORS

Fir-1, the only research reactor in Finland, wasmodified to produce epithermal neutrons for BNCT(Boron Neutron Capture Therapy) use. This offersopportunities to continue its use for severaladditional years.

SVERIGE - SWEDEN

ENERGY POLICY CONSIDERATIONS

In July 1994, the Government appointed an EnergyCommission made up of members from the politicalparties in the Parliament. The Energy Commissionrecommended in February 1995 that deregulation ofthe electricity market should take place. Agovernment Bill was presented in May 1995. TheParliament approved the Bill in October 1995, andthe reform became effective on 1 January 1996.

The Energy Commission issued its main report on1 December 1995. The Commission considers thata number of conflicts of objectives remain to besolved. With regard to the Energy Commission’sforecasts and assessments, no exact time limit forthe year in which the last nuclear reactor is finallytaken out of operation is to be specified.

The Government invited all parties in the Parliamentto participate in discussions about future energypolicy in spring 1996. On 4 February 1997, an inter-party Agreement between the Social Democrats,the Centre Party and the Left Party was presented.The three political parties have agreed on a numberof measures to reduce electricity consumption anduse new methods of electricity production during thenext few years. A new, long-term transformationprogramme is being started to develop anecologically sustainable energy supply system.

Annual Report 1996Page 32

Euratom Supply Agency

A law on the decommissioning of nuclear powerplants will be passed. Negotiations will be startedwith the owner of the Barsebäck plant on closingone reactor before 1 July 1998, and a secondreactor before July 2001. According to the politicalparties, no fixed date should be set for closing downthe last reactor. Thereby, a sufficiently long period isgranted for the transformation of the energy system.

The energy policy programme will give rise to stateexpenditure of SEK 9 billion over a seven-yearperiod. The result of the energy policy programmeand the closure of the Barsebäck plant will form thebasis for future decisions on continuedtransformation. Decisions on the continueddecommissioning of nuclear reactors will be takenbefore the end of the next government term. AGovernment Bill is scheduled to be presented in theParliament in mid-March 1997. Editor’s note: this Billwas presented on 14 March 1997.

NUCLEAR ELECTRICITY GENERATION ANDCONSUMPTION

PRODUCTION AND CONSUMPTION

Electricity consumption in 1996 was 140.4 TWh,down about 0.6% from 1995. Electricity productionin 1995 and 1996 was :

1995 (TWh) 1996 (TWh)

Hydro-electric powerNuclear powerWind powerCombined heat/powerCondensing/gas turbine

Total production

Net export/importNet consumption

66.966.70.18.70.7

143.1

1.8141.3

51.770.90.19.13.4

135.3

-5.1140.4

Nuclear power represented about 52% and hydro-electric power only 38% of total production in 1996.The production of nuclear and hydro-electric powerdiffers a great deal between 1995 and 1996. 1996

was an extremely dry year. The flow to the hydro-electric power reservoirs was low which gave a lowproduction of hydro-electric power. It was howeveralso a dry year in Norway. This is also the reasonfor the relatively high production in the condensingpower stations and the net import of electricity.

Normally the production of nuclear power andhydro-electric power is roughly the same, each witha share of 45-50% of total production. During aclimatically statistically average year, hydro-electricpower production amounts to about 63.5 TWh.

NUCLEAR POWER

Reactors have been operating normally in 1996.Availability was on average 84.1%. The loweravailability of Oskarshamn 1 (BWR) lowered theaverage value. The availability of the PWR reactorswas on average about 90%.

After extensive repairs, the oldest Swedish reactor,Oskarshamn 1, was restarted and put back intocommercial operation in 1996. Extensive programsare planned for the modernisation of the oldestSwedish nuclear power plants. For example therewill be further modernisation of Oskarshamn 1,consisting of replacement of the core shroudincluding lid and core-spray system as well as thesteam separator. It is the first time work like this willbe performed and the order was placed with ABBAtom. The refuelling and maintenance outage atOskarshamn 1, which started in November 1996,has been extended due to tests and repairs.Surface cracks in the main circulation loop havebeen repaired. Testing and evaluating the results oftests on the moderator tank lid have been time-consuming. Power production is expected toresume in February 1997.

At Ringhals 1, an ABB-built BWR, a modernisationof the primary systems will be done, comprising acomplete overhaul including replacement of pipes,nozzles and components for the main circulationsystem and ancillary systems.

Annual Report 1996Page 33

Euratom Supply Agency

NUCLEAR FUEL CYCLE DEVELOPMENTS

ENVIRONMENTAL IMPACT OF NUCLEAR FUELSUPPLY

The Swedish utilities have established a jointventure called “Project Nuclear Fuel andEnvironment”. The main objective is to assess theenvironmental and occupational safety aspects,including radiation protection from production ofuranium, conversion, enrichment and fabrication byexisting and possible suppliers to the Swedishutilities.

FABRICATION

At the ABB Atom fuel fabrication plant, 400 tonnesof uranium dioxide powder were converted and280 tonnes of fresh fuel produced during 1996.About half of the production was for the exportmarket.

In November 1996, ABB Atom received a permit toincrease its production of converted uranium dioxidepowder from 400 tonnes to 600 tonnes per year. Atthe same time, the company will considerably lowermost of its emissions to the environment.

RADIOACTIVE WASTE

Four local municipalities, Malå in Northern Sweden,Nyköping, Östhammar and Oskarshamn inSouthern Sweden have agreed to carry outpreliminary studies for a final repository of spentnuclear fuel together with the Swedish Nuclear Fueland Waste Management Company, SKB.

These studies are focused on the social,environmental and economic consequences oflocating a final repository in their municipalities. SKBhas established local offices. After the study onMalå was published, the municipality started anindependent evaluation. The studies on Nyköpingand Östhammar have been ongoing in 1996, whilethe preliminary study on Oskarshamn was started atthe end of the year.

SKB has also recently decided to establish a pilotplant at Oskarshamn for testing the welding of thelid to copper cylinders, and the welds themselves.

UNITED KINGDOM

ENERGY POLICY CONSIDERATIONS