EXECUTIVE MANAGEMENT COMMITTEE RECOMMENDATION The Committee concurred with the staff recommendation to close out the performance audit contract with Booz-Allen Hamilton upon completion of Phase I work products, and reallocate the remaining $49,200 budgeted for Phase II. Executive Management Committee, September i, 1993

Transcript

EXECUTIVE MANAGEMENT

COMMITTEE RECOMMENDATION

The Committee concurred with the staff recommendation to close out

the performance audit contract with Booz-Allen Hamilton upon

completion of Phase I work products, and reallocate the remaining

$49,200 budgeted for Phase II.

Executive Management Committee, September i, 1993

July 26, 1993

MEMO TO:

Los Angeles County THROUGH :Metropolitan

Transportation FROM :

AuthoritySUBJECT :

8~8 West Seventh StreetSuite 300 - "

Los Angeles. CA 9oo~7

213.623.u94

EXECUTIVE MANAGEMENT COMMITTEE -8/11/93 MEETING

RECOMMENDATIONS

Consider consultant presentation of Los Angeles CountyTransit Operator Phase I Triennial Performance Auditresults; and

direct the CEO to close-out the performance auditcontract with Booz-Allen & Hamilton upon completion ofPhase I work products, and reallocate the remaining$49,200 budgeted for Phase II.

ALTERNATIVES CONSIDERED

Based on the results of Phase I of the transit operators’FY 89 - FY 91 Triennial Performance Audits, the consultantpresented staff with four options for Phase II analysis, asdiscussed below. These options were discussed by the BusOperations Subcommittee and by MTA executive management,and their input has been incorporated into the staffrecommendation above.

IMPACT ON BUDGET AND OBJECTIVES

In approving the original contract, the LACTC approved$49,200 for Phase II of the operator triennial performanceaudits, with the understanding that the scope of work forPhase II would .be determined based on Phase I auditresults.

BACKGROUND

Phase I of the State-required triennial performance auditsof transit operators (PUC Section 99246) has beencompleted. The consultant, Booz-Allen & Hamilton, Inc.,presented the summary results of the performance audits,and options for Phase II analysis, to the Bus OperationsSubcommittee on June 29, 1993.

EXECUTIVE MANAGEMENT cOMMITTEE - 8/11/93 MEETINGFY 89 - FY 91 TRIENNIAL~PERFORMANcE -AU DIT S

OF LOS ANGELES COUNTY TRANSIT OPERATORSPage 2.

Section 99246 of the Public Utilities Code requires certificationthat performance audits under MTA’s jurisdiction are ~completedevery three years. The performance audits evaluate the efficiency,effectiveness, and economy of the operation and should include, at

a minimum, verification of the operators’:

-OE~erating Cost per Passenger-Operating Cost per vehicle Service Hour-Passengers per Vehicle Service Hour-Passengers per Vehicle Service Mile-Vehicle Service Hours per Employee

These performance indicators were evaluated by the consultant,Booz-Allen & Hamilton, Inc., using Transit Performance Measurement(TPM) data provided by audited Section 15 reports. Phase I focused

on the analysis of the TPM performance indicators, TPM datacollection and reporting, and other specific areas of analysis.The consultant has prepared an Executive Summary of the FY 89-FY 91Transit Operator Triennial Performance Audits (Attachment A). Theoperator performance audit results will be presented by Booz-Allen& Hamilton to the Executive Management Committee on August ii,1993.

Phase II may include analysis of specific functional areas, asrecommended in Phase I. Functional areas include operations,maintenance, service planning, management reporting, etc. Thecontract awarded to Booz-Allen & Hamilton to conduct these auditsincluded $49,200 to conduct Phase II, contingent upon approval of

the Phase II focus.

The consultant has prepared an outline of potential areas ofanalysis for Phase II (see Attachment B). Briefly, the consultanthas summarized four areas which may benefit from Phase II analysis,

These areas, and their estimated costs, are:

2.

3.

4.

Analysis of SCRTD administrative cost growth ($49,200).Analysis of Montebello’s risk management cost growth($20,000).Development of a strategic planning process for the MTAOperating Division ($i00,000).Streamlining transit operator reporting requirements($49,200).

The Phase II options were discussed with the Bus OperationsSubcommittee (BOS) on June 29 and July 27, 1993. The BOSdiscussion focused on Option #4 - Streamlining transit operatorreporting requirements. Staff believes that a concerted effort to

EXECUTIVE MANAGEMENT coMMITTEE - 8/11/93 MEETINGFY 89 - FY 91 TRIENNIAL PERFORMANCE AUDITSOF LOS ANGELES COUNTY TRANSIT OPERATORSPage 3.

streamline reporting requirements and review funding guidelines forconsistency is very important, and also timely, given the status ofthe merqer between LACTC and SCRTD. The Southeast Area Team isproposing funds in the FY 94 budget for a similar project. The BOSand MTA staff concur tha~ to proceed with Phase II, Option #4 wouldduplicate the Southeasn Area Team’s effort. Therefore, staff isrecommending that the Area Teams develop a scope of work forstreamlining and consistency efforts, with input from municipaloperators and MTA operations, and that the CEO close-out theperformance audit contract with Booz-Allen & Hamilton.

The other three options were discarded as either no longerapplicable (SCRTD cost growth), too expensive (strategic planningprocess for MTA operating), or as something that could be addressedoutside of this audit (Montebello’s risk management cost andstreamlining transit operator reporting requirements).

PREPARED BY:

JULIE AUSTINPOLICY PROJECT MANAGER

Attachments

opaud.rpt

presentation to the

LOS ANGELES COUNTY METROPOLITAN TRANSPORTATION AUTHORITY

FY89-FY91PERFORMANCE AUDITS

EXECUTIVE SUMMARYTRANSIT OPERATOR TRIENNIAL

prepared by

BOOZoALLEN & HAMILTON INC.

in association with

Mundle & Associates, Inc.

MacDorman & ASsociates

June 9,1993

TABLE OF CONTENTS

¯ Audit Requirements ..............

¯ Data Reporting Compliance .............

¯ Proposition A Discretionary Guidelines Compliance.

¯ Progress To Implem,ent Prior Audit Recommendations.

¯ Performance Trends ...........

¯ Recommendations ......

¯ Potential Phase II Analyses .......... .

Page

.5

.6

........... 10

......... 13

, , , ................ BOOZ o ALLEN & HAMILTON

,quart F, equtrernents.,.

PERFORMANCE AUDITS ARE A TRIENNIAL REQUIREMENT

The California Public Utilities Code Section 99246 requires audits for continued receipt of StateTransit Assistance (STA) and Transportation Development Act (TDA) Article 4 transit funds.Operators audited to meet this requirement include:

During this cycle, the LACMTA required triennial performance audits, for the first time, oftransportation zones and other transit operators who are "eligible" to receive formula equivalentfunding. These operators include:

- Foothill Transit (Transportation Zone)

City of Los Angeles Central City DASH and Bus Se,rvice Continuation Program (BSCP) services

County of Los Angeles North County Public TranspOrtation System (i.e., Antelope and SantflClarita Valleys):

BOOZ.ALLEN & HAMILTON ,,

Audit Requirements...

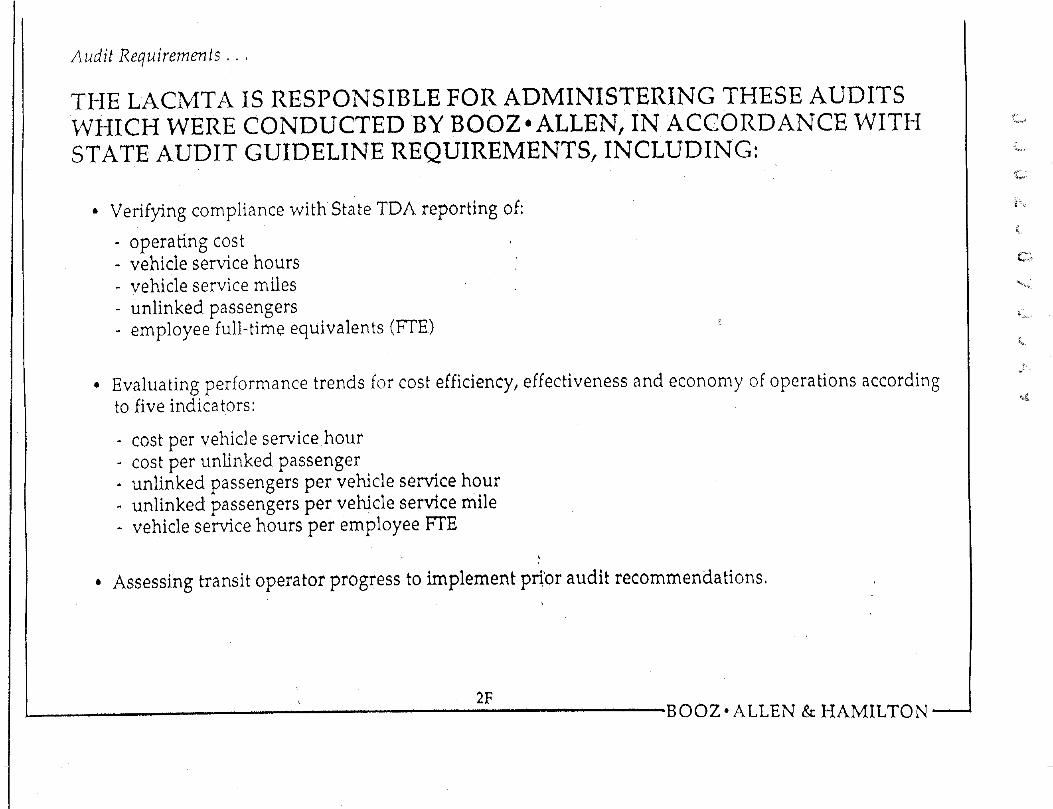

THE LACMTA IS RESPONSIBLE FOR ADMINISTERING THESE AUDITSWHICH WERE CONDUCTED BY BOOZ ° ALLEN, IN ACCORDANCE WITHSTATE AUDIT GUIDELINE REQUIREMENTS, INCLUDING:

Verifying compliance with State TDA reporting of:

- operating cost- vehicle service hours

vehicle service milesunlinked passengers

- employee full-time equivalents (FTE)

Evaluating performance trends for cost efficiency, effectiveness and economy of operations accordingto five indicators:

cost per vehicle service hourcost per unlinked passengerunlinked passengers per vehicle service hourunlinked passengers per vehicle service milevehicle service hours per employee FTE

Assessing transit operator progress to implement pri’or audit recommendations,

,. 2F.............................. BOOZoALLEN & HAMILTON ....

Audit Approach,.,

THE LACMTA USES A TWO-PHASED APPROACH TO PERFORMANCEAUDITING. THIS EXECUTIVE SUMMARY ADDRESSES, PHASE I ANDIDENTIFIES POTENTIAL AREAS FOR PHASE II REVIEW,

Phase I is a high-level compliance and performance review designed to meet:

- minimum state requirements- other LACMTA compliance review requirements

Phase II provides:

- more detailed review of the causes of issues identified in Phase I- the resources to develop specific improvement plans

¯ LACMTA approval is required prior to Phase II analysis; potential Phase II analyses arediscussed herein, ",

~ O O O O O O O O O¯ o, o o o o o o o o¯ o o o o o 0 o o o® O 0 O O O O ~ ~ ~,~ 0 0 0 0 0 0 0 0 00 0 0 0 0 0 0 ~ 0 ~,~ ~ ,~ 0 0 ~ 0 0 0 0¯ 0 0 0 O 0 0 0 0 O,~ 0 ~ 0 0 0 0 0 0 ,~0 0 0 0 0 0 0 0 0 0o o o o o o o o o o

--~ 0 0 ~ 0 0 ~ 0 0 0,~ 0 0 @ O 0 0 O O O0 0 ’~ ,~ 0 0 0 0 O 00 0 0 O 0 0 O" 0 0 0

.49

Pt~ase I Data F, eportmg c.ompllance , , ,

THE MAJORITY OF OPERATORS ARE IN FULL COMPLIANCE WITHSTATE TDA AND LACMTA TPM REPORTING REQUIREMENTS,SEVERAL REPORTING REQUIREMENTS, HOWEVER, ARE NOTCLEARLY UNDERSTOOD,

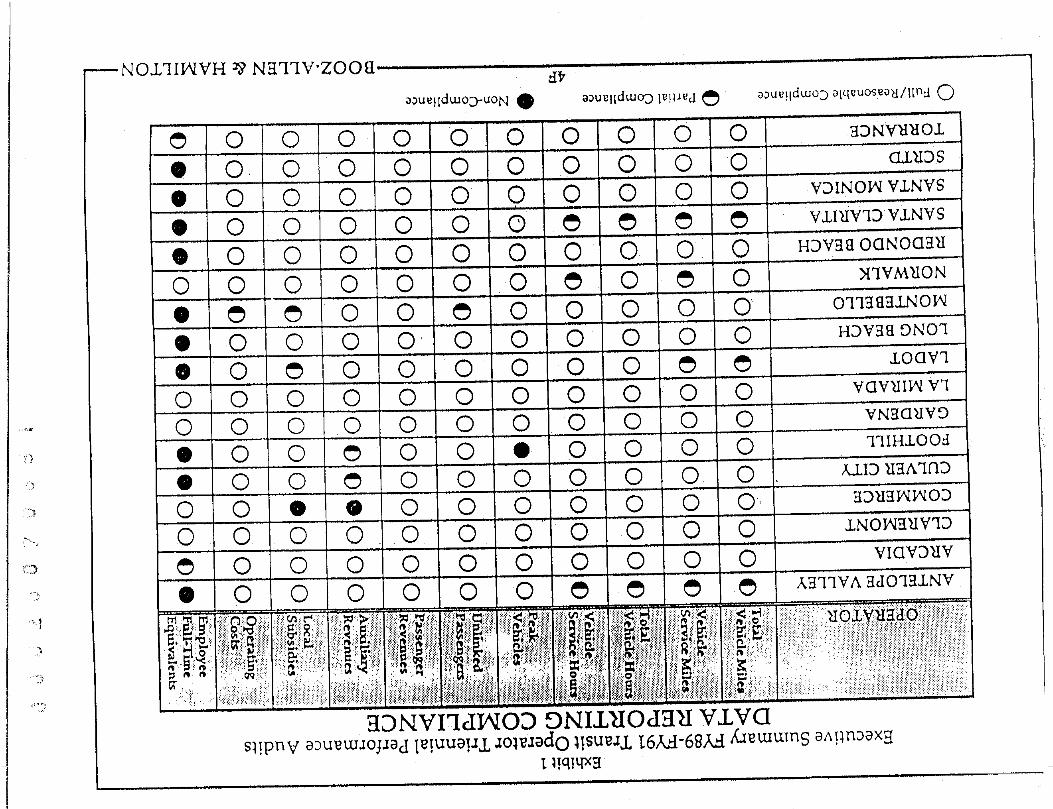

¯ Exhibit I shows compliance by operator

Employee Full-Time Equivalents is the data item most frequently misreported:

- State and LACMTA definition based on 2,000 hours for both public employees and employeesproviding purchased trans’portation services

the Federal Section 15 definition is 2,080 hours for public employees only

the State has recently clarified this definition

Auxiliary revenues are used in determining the minimum farebox recovery ratios of 38%specified in Prop A Discretionary Guidelines

The LACMTA definition of "auxiliary revenues" shguld be clarified; some operators includeinterest earnings in this category while others do not,

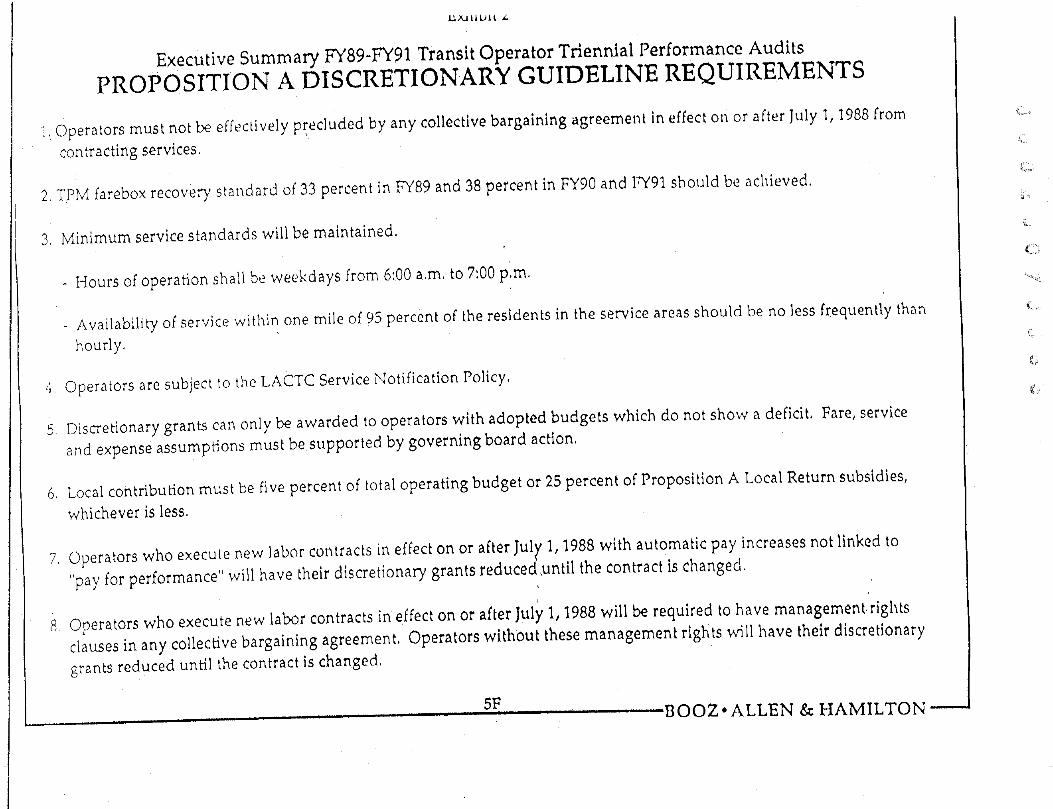

PROPOSITION A DISCRETIONARY GUIDELINE REQUIREMENTS

Operators must not be effectively pr, ecluded by any collective bargaining agreement in effect on or after July 1, 1988 fromcontracting services.

2. TPM farebox recovery standard of 33 percent in FY89 and 38 percent in FY90 and I,’Y91 should be achieved.

3. Minimum service standards will be maintained.

Hours of operation shall be weekdays from 6:00 a.m, to 7:00 p.m.

Availability of service within, one mile of 95 percent of the residents in the service areas should be no less frequently thanhourly.

4. Operators are subject to the LACTC Service Notification Policy.

5. Discretionary grants can only be awarded to operators with adopted budgets which do not show a deficit, Fare, serviceand expense assumptions must be supported by governing board action,

6. Local contribution must be five percent of total operating budget or 25 percent of Proposition A Local Return subsidies,

whichever is less.

7. Operators who execute new labor contracts in effect on or after Jul}, 1, 1988 with automatic pay increases not linked to"pay for performance" will have their &scret~on ry grants reduced,until the contract is changed,

8 Operators who execute new labor contracts in effect on or after July 1, 1988 will be required to have management.rightsclauses in any collective bargaining agreement. Operators without these management rigti!s will have their discretionarygrants reduced until the contract is changed.

5F ............ BOOZ. ALLEN & HAMILTON ¯

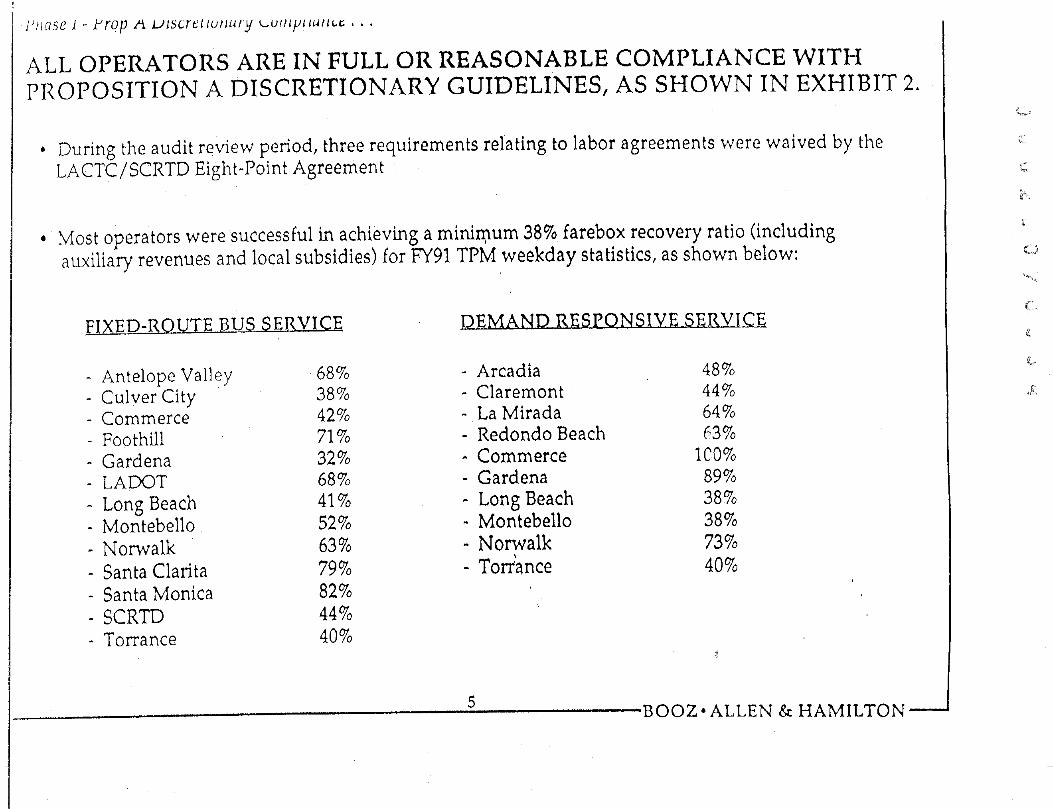

ALL OPERATORS ARE IN FULL OR REASONABLE COMPLIANCE WITHPROPOSITION A DISCRETIONARY GUIDELINES, AS SHOWN IN EXHIBIT 2.

¯ During the audit review period, three requirements relating to labor agreements were waived by theLACTC/SCRTD Eight-Point Agreement

. Most operators were successful in achieving a minim, um 38% farebox recovery ratio (including"aauxfl~ ry revenues and local subsidies) for FY91 TPM weekday statistics, as shown below:

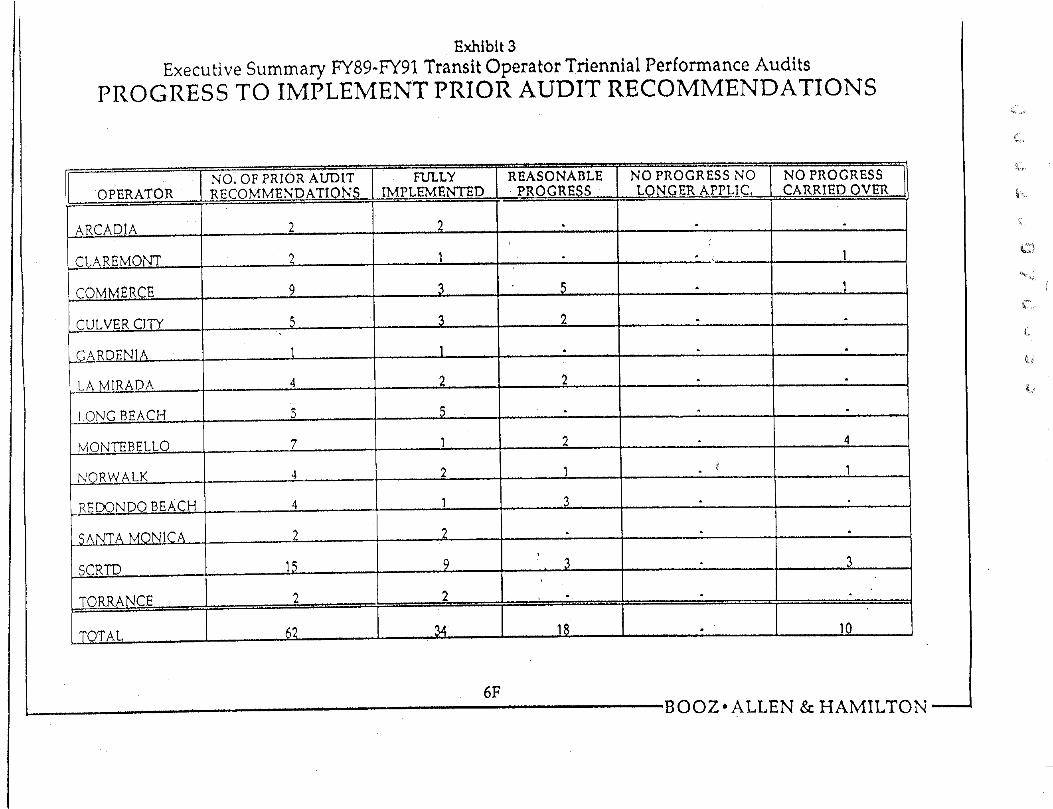

TRANSIT OPERATORS HAVE IMPLEMENTED THE MAJORITY OF PRIORAUDIT RECOMMENDATIONS

¯ Exhibit 3 shows that 34 out of 62 recommendations were fully implemented; reasonable progresswas made on another 18

Ten recommendations were not implemented and i~re still valid today -, these have been carriedover

T1ne SCRTD achieved significant cost savings through implementation of recommendationsrelating to:

absence reduction: $50 million between FY88 and FY91

risk management: $24 million over two years.

6............... BOOZ.ALLEN & HAMILTON ¯

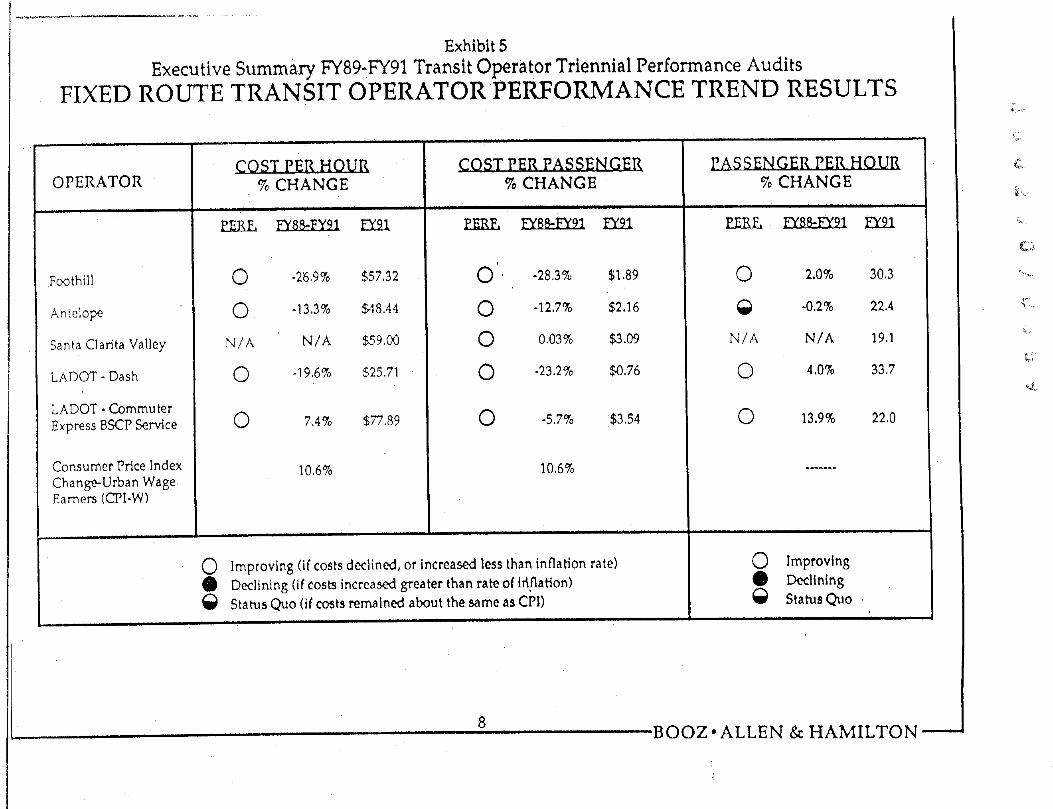

Phase I- Performance Trends ,,,

FIXED ROUTE SERVICES IMPROVED FOR MANY OPERATORS WHILEDEMAND RESPONSE SERVICES DECLINED.

_Fixe.d Route

Commerce, Long Beach, Santa Monica and Torrance experienced positive cost efficiency, costeffectiveness and productivity improvements betw.een FY88 and FY91, as shown in Exhibit 4

. Montebello showed declines in all three categories (i.e., cost efficiency, cost effectiveness andproductivity) between FY88 and FY91 while the SCRTD remained about status quo

¯ Performance results for other fixed-route bus operators were mixed

First time auditees - -Foothiil, Antelope Valley, Santa Clarita Valley and LADOT - - all experiencedpositive performance trends between FY89 and FY91, as shown in Exhibit 5

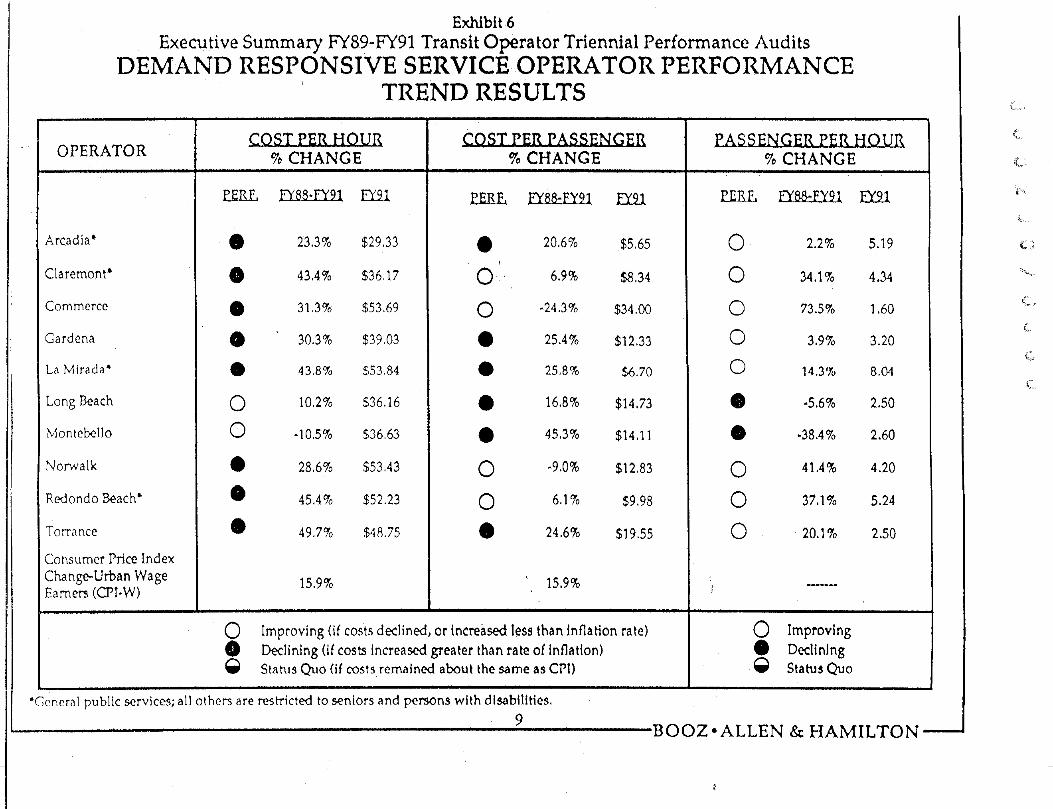

pemand Response

. Performance trends for demand responsive services as: a group were mostly declining in terms of costefficiency and effectiveness with some improvements ih, service productivity, as shown in Exhibit 6.

Improving (if costs declined, or increased less than inflation rate)Declining (if cost~ increased greater than rate of inflation)Status Quo (if costs rematned about the same as CPI)

*General public services; all others are res~cted to seniors and persons with disabilities.9

PASSENGER PER HOUR% CHANGE

PX~G FY88-FY91 FY91

2.2% 5.19

34,1% 4.34

73.5% 1.60

3.9% 3.20

14.3% 8.04

.5,6~o2.so-38.4% 2.60

41,4% 4.20

37,1% 5.24

20.1% 2.50

ImprovingDecliningStatus Quo

BOOZoALLEN & HAMILTON’ ¯

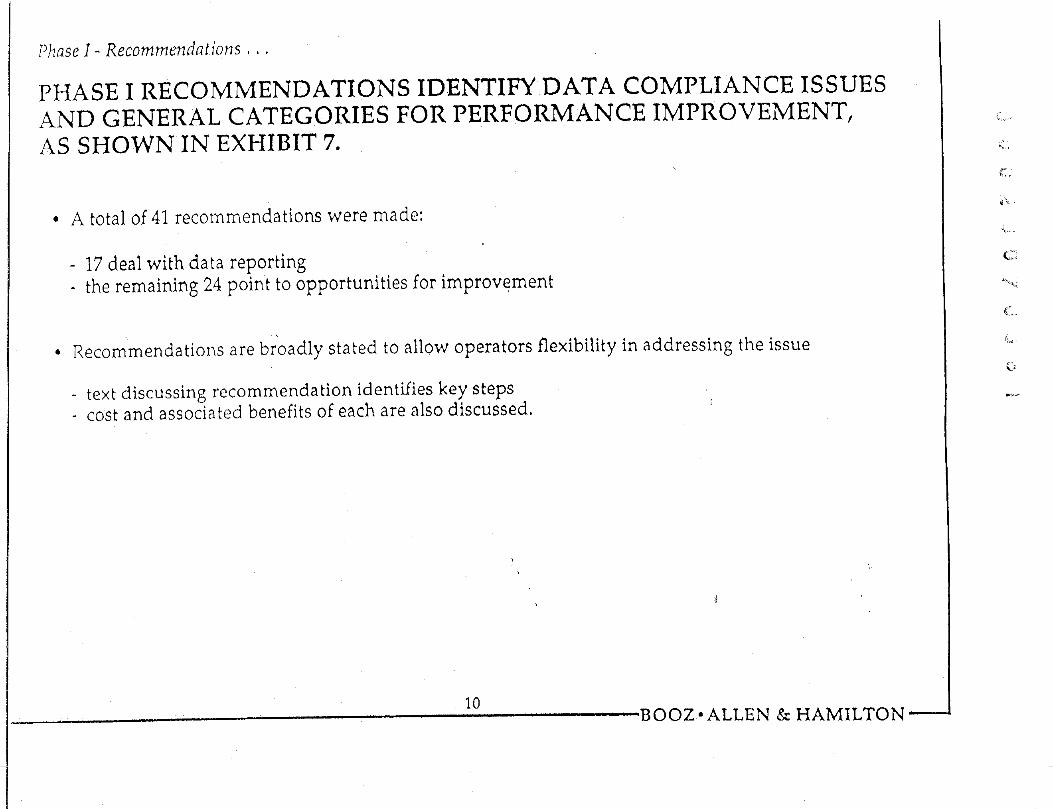

I~hase I - Recommendations,,,

PHASE I RECOMMENDATIONS IDENTIFY DATA COMPLIANCE ISSUESAND GENERAL CATEGORIES FOR PERFORMANCE IMPROVEMENT,AS SHOWN IN EXHIBIT 7.

A total of 41 recommendations were made:

- 17 deal with data reportingthe remaining 24 point to opportunities for improvement

Recommendations are broadly stated to allow operators flexibility in addressing the issue

text discussing recommendation identifies key stepscost and associated benefits of each are also discussed.

10.......... BOOZ.ALLEN & HAMILTON’

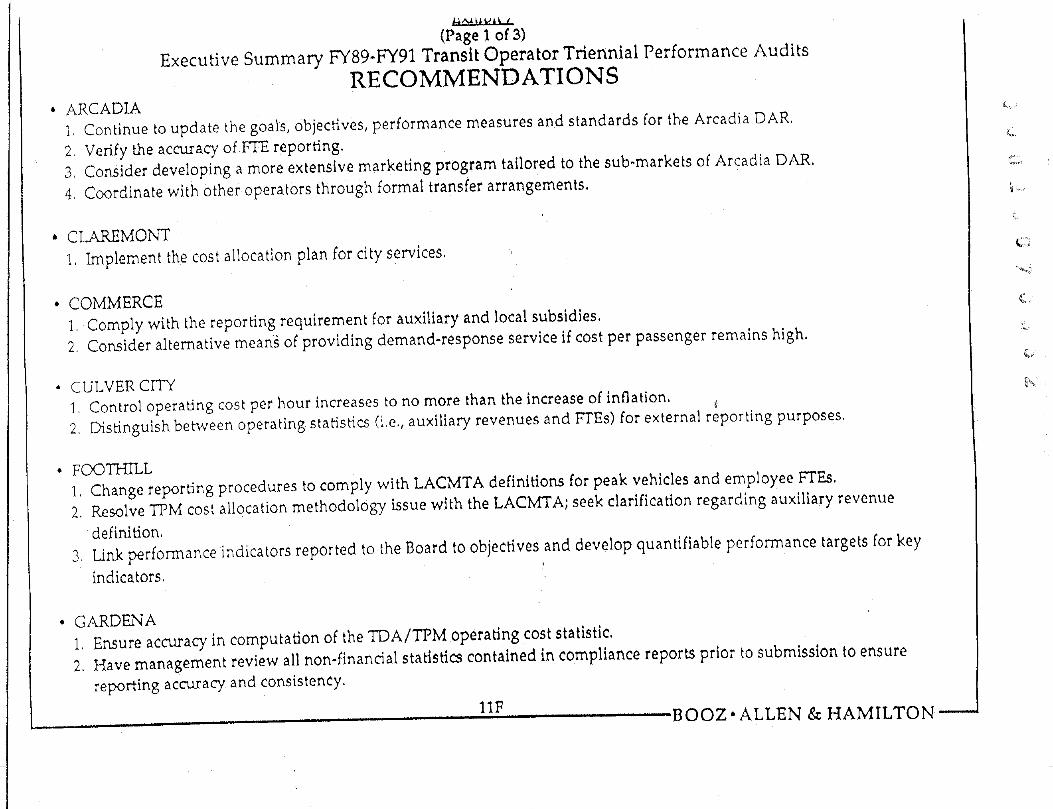

(Page I of 3)E×ecutive Summary F3(89-FY91 Transit Operator Triennial Performance Audits

RECOMMENDATIONSARCADIA1, Continue to update the goals, objectives, performance measures and standards for the Arcadia DAR.2, Verify the accuracy of FTE reporting.3, Consider developing a more extensive marketing program tailored to the sub-markets of Arcadia DAR.4, Coordinate with other operators through formal transfer arrangements.

CLAREMONTImplement the cost allocation plan for city services,

COMMERCE1, Comply with the reporting requirement for auxiliary and local subsidies,2, Consider alternative mean~ of providing demand-response service if cost per passenger remains high,

CULVER CITYControl operating cost per hour increases to no more than the increase of inflation. ,~Distinguish between operating statistics (i,e,, auxiliary revenues and FTEs) for external reporting purposes.

FOOTHILL1. Change reporting procedures to comply with LACMTA definitions for peak vehicles and employee FTEs,2. Resolve TPM cost allocation methodology Lssue with the LACMTA; seek clarification regarding auxiliary revenue

definition,3, Link performance indicators reported to the Board to objectives and develop quantifiable performance targets for key

indicators,

. GARDENA1. Ensure accuracy in computation of the TDA/TPM operating cost statistic.

2, Have management review all non-financial stat’isties contained in compliance reports prior to submission to ensurereporting accuracy and consistency.

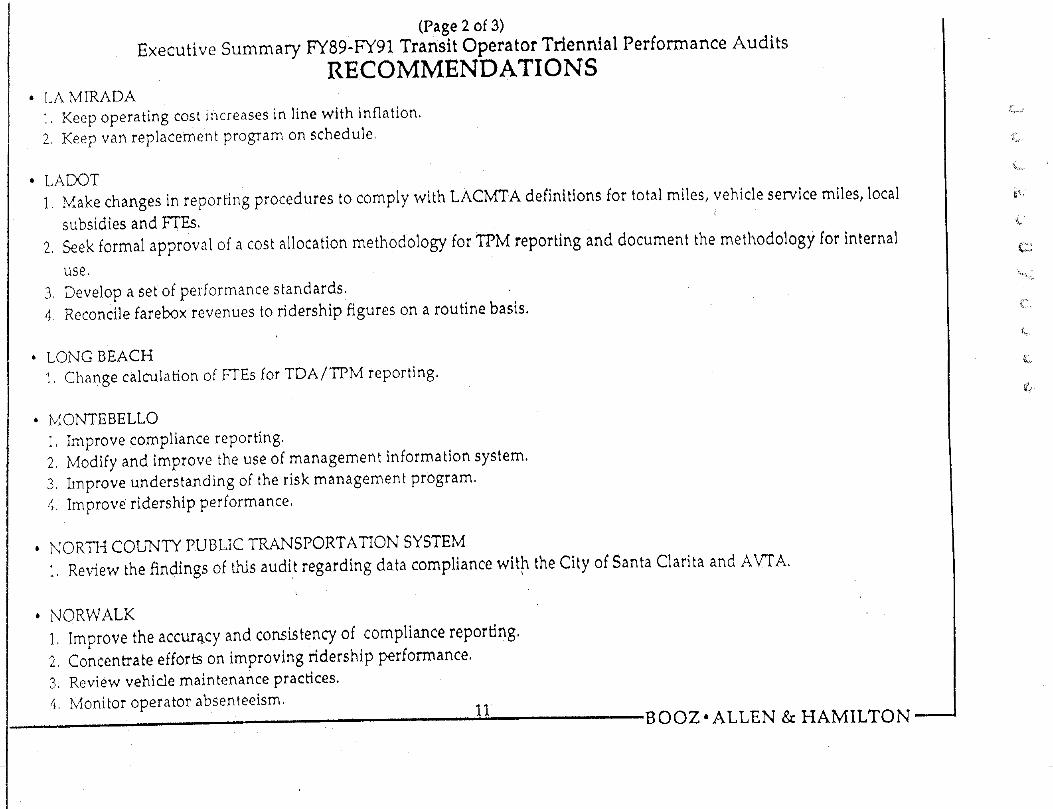

Keep operating cost ~ncreases m line with inflation.Keep van replacement program on schedule,

¯ LADOT1 Make changes in reporting proceaures to comply with LACM’TA definitions for total miles, vehicle service miles, local

subsidies and FTEs,2 S~ek formal approval of a cost allocation methodology for TPM reporting and document the methodology for internal

use.3 Develop a set of performance standards,4 Reconcile farebox revenues to ridership figures on a routine basis,

LONG BEACH1 Change calculation of FTEs for TDA/TPM reporting.

MONTEBELLO1, Improve compliance reporting,2, Modify and improve the use of management information system.3. Improve understanding of the risk management program.4~ Improve ridership performance,

NORTH COUNTY PUBLIC TRANSPORTATION SYSTEM1, Review We findings of this audit regarding data compliance wit,h the City of Santa Clarita and AV’TA,

NORWALK1, Improve the accuracy and consistency of compliance reporting,2, Concent:rate efforts on improving ridership performance.3, Review vehicle maintenance practices.4, Monitor operator absenteeism, ,11

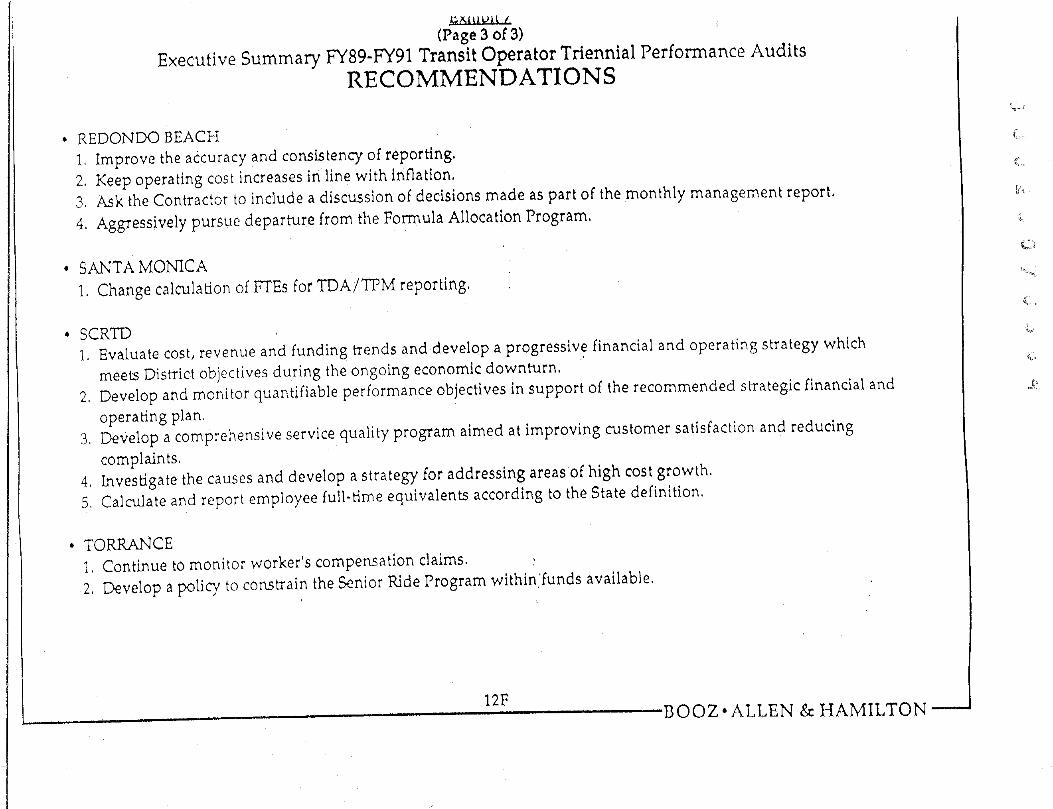

REDONDO BEACH1, Improve the accuracy and consistency of reporting.2, Keep operating cost increases in line with inflation.3. Ask the Contractor to include a discussion of decisions made as part of the monthly management report,

4, Aggressively pursue departure from the Formula Allocation Program,

1. Change calculation of FTEs for TDA/TPM reporting,

SCRTD1. Evaluate cost, revenue and funding t’rends and develop a progressiv.e financial and operating strategy which

meets District objectives during the ongoing economic downturn,2. Develop and monitor quaniifiable performance objectives in support of the recommended strategic financial and

operating plan.3. Develop a comprehensive service quality program aimed at improving customer satisfaction and reducing

complaints,4, Investigate the causes and develop a strategy for addressing areas of high cost growth,

5. Calculate and report employee full-time equivalents according to the State definition,

¯ TORRANCE1, Continue to monitor worker’s compensation claims, ~2, Develop a policy to constrain the Senior Ride Program within,’funds available.

,,, 12F ....BOOZ. ALLEN & HAMILTON

Phase I - Recommendations..,

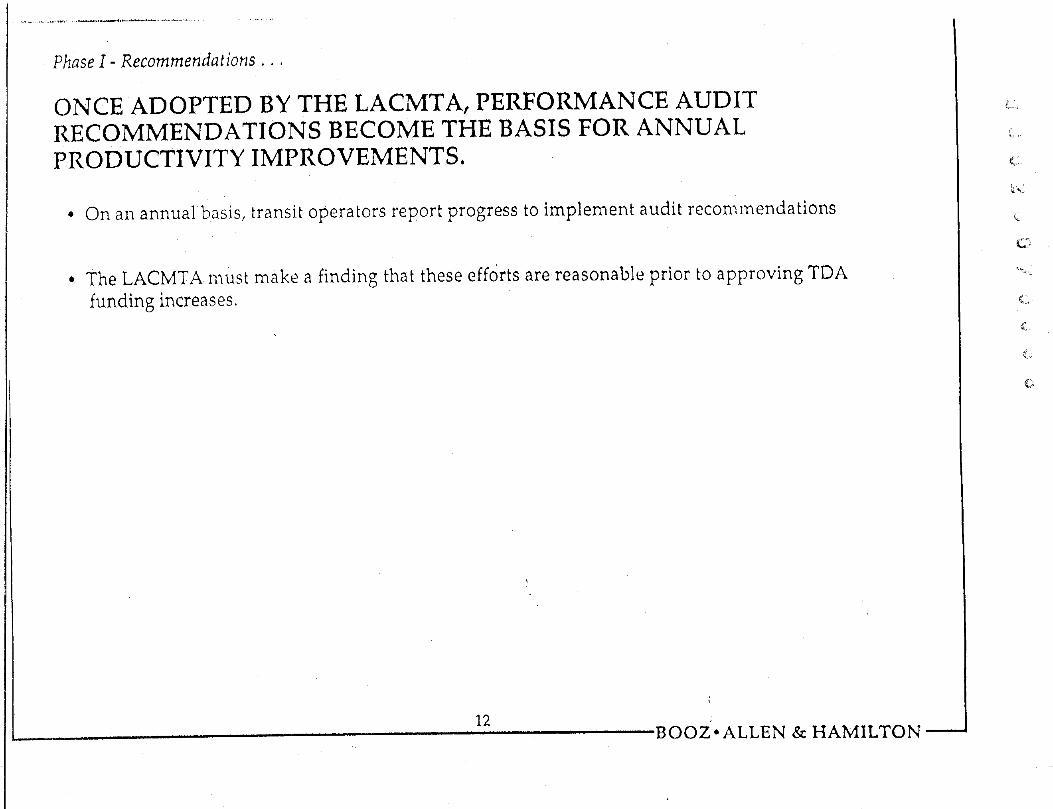

ONCE ADOPTED BY THE LACMTA, PERFORMANCE AUDITRECOMMENDATIONS BECOME THE BASIS FOR ANNUALPRODUCTIVITY IMPROVEMENTS.

¯ On an annual basis, transit operators report progress to implement audit recommendations

¯ The LACMTA must make a finding that these eff6rts are reasonable prior to approving TDAfunding increases,

12’BOOZoALLEN & HAMILTON’

Potential Phase II Analyses..,

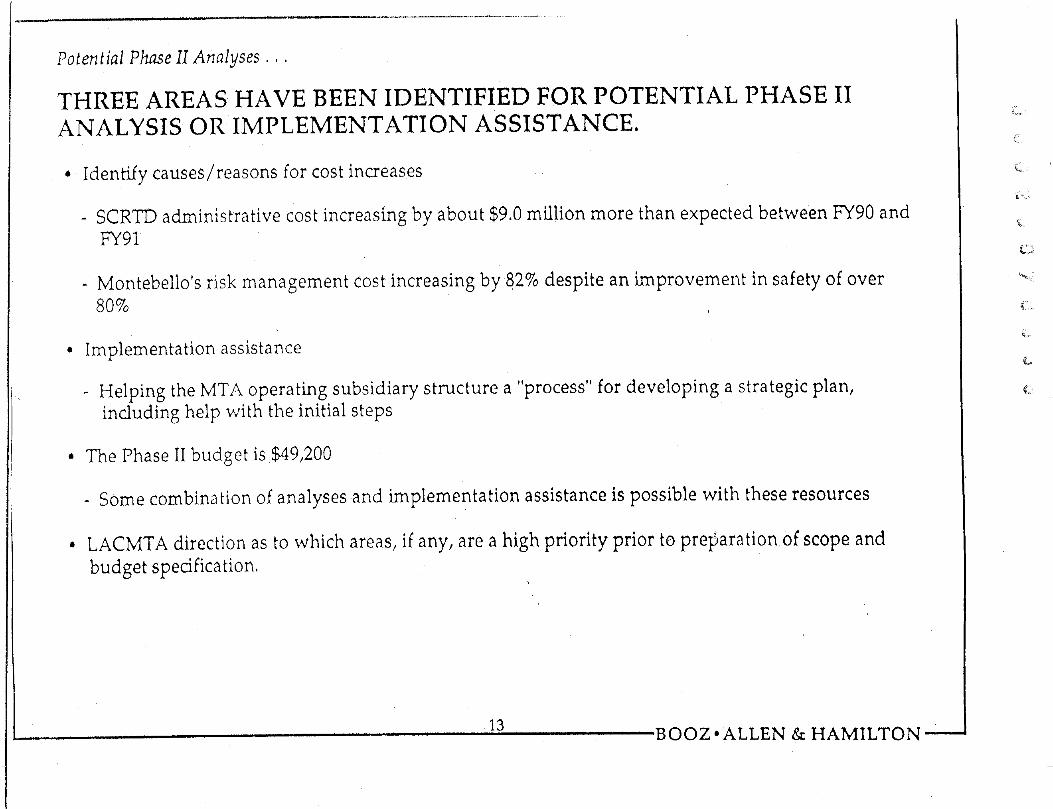

THREE AREAS HAVE BEEN IDENTIFIED FOR POTENTIAL PHASE IIANALYSIS OR IMPLEMENTATION ASSISTANCE.

¯ Identify causes/reasons for cost increases

SCRTD administrative cost increasing by about $9.0 million more than expected between FY90 andFY91

- Montebello’s risk management cost increasing by 82% despite an improvement in safety of over8O%

¯ Implementation assistance

Helping the MTA operating subsidiary structure a "process" for developing a strategic plan,including help with the initial steps

¯ The Phase II budget is $49,200

Some combination of analyses and implementation assistance is possible with these resources

¯ LACMTA direction as to which areas, if any, are a high priority prior to preparation of scope andbudget specification.

, , 13BOOZoALLEN & HAMILTON

ATTACHMENT "B"

BOOZ-AI I .EN & HAMILTON INC.SUITE 616 - 523 WEST SIXTH STREET - LOS ANGELES, CALIPORNIA 90014 ¯ TELEPHONE: 6213) 62~1900

June 17, 1993

Ms. Julie AustinLos Angeles County Metropolitan

Transportation Authority818 West Seventh Street, Suite 1100Los Angeles, CA 90017-4606

Los Angeles has typically had a two-phased performance audit process with PhaseI focusing on compliance issues and a high level review of system-wide performance trendsof all transit operators. Phase II typically involved a more detailed review of selectedoperators and issues identified in Phase I. In the FY86, Phase II resources were devotedto SCRTD absenteeism issues. In FY89, Phase II resources were used to conduct a peerreview of absentee rotes and opportunities to reduce SCRTD risk management costs.

During the Phase I FY91 triennial performance audits, four areas have beenidentified for potential Phase II assistance, including:

Analysis of SCRTD administrative cost growthAnalysis of Montebello’s risk management cost growthDevelopment of a strategic planning process for the MTA/SCRTDStreamlining transit operator reporting requirements.

The attached outlines findings leading to the identification of these four areas,potential benefits of Phase II assistance, and the scope of work and cost for Phase IIassistance. The total budget for Phase II is $49,200.

Very truly your_s,

BOOZoALLEN & HAMILTON INC.

Doug CarterPrincipal

Attachment

ANALYSIS OF $CRTD ADMINISTRATIVE COST GROWTH

Phase I Audit F’mdlngs: Betweea FY90 and FY91, SCRTD administrative costs(excluding PL/PD and Blue Line operating expenses) increased by 21 percent (i.e.,$19.3million) compared to an inflationary increase of 5.2 percent. Approximately $5.4 millionof this growth is attributable to policy directed growth for transit police and customerrelations. Another $4.1million is attributable to inflationary increases. The remaining $9.8million in cost growth is unexplained. In FY91, $9.8 million equated to approximately120,000 vehicle service hours.

Between FY90 and FY91, the SCRTD was successful in reducing PL/PD costs by$21.2 million (i.e.,64 percent). This positive performance in the area. of risk managementmasked cost increases in other administrative areas.

Phase I Recommendation: Investigate the causes and develop a strategy foraddressing areas of high cost growth (Recommendation #4 of the SCRTD Phase I TriennialPerformance Audit).

Potential Phase 1/ Assistance: Analytical tasks to be performed are aimed atidentifying the specific areas of administrative cost growth and the long and short term needfor this growth. Tasks include:

profiling FY90 and FY91 administrative costs by department and account

profiling FY90 and FY91 authorized and filled positions by department andrifle

interviewing departmental managers regarding programs and policies leadingto areas identified as having cost increases and/or staffing increases

identifying merger activities likely to impact areas of high cost growth in thefuture

summarizing findings in a technical memorandum for presentation to MTAmanagement and Board.-

Phase 1I Budget: $49,200

Potential Benefits: A better understanding of the causes of administrative costincreases would allow for cost reduction strategies to be developed if the SCRTD continuedto operate as a separate entity. A better understanding of contributing factors could alsoresult in the conclusion that said increases were necessary and/or unavoidable. Informationprovided by this analysis, however, would most likely be of limited value given the significantorganizational changes that have occurred in SCRTD administrative functions as a resultof the recent merger with the LACTC.

Monitoring the cost efficiency of administrative functions is important and achallenge that the new LACMTA must address as cost experience is gained for reorganizedfunctions. LACMTA administrative functions are still being consolidated and reorganizedwith less than six months of actual cost data available. Looking at historical SCRTDadministrative costs will provide limited benefit at this time.

~ANALYSIS OF MONTEBELLO’$ RISK MANAGEMENT COST GROWTH

Phase I Audit Findings: Montebello Bus Lines’ casualty and liability costs per mileand per passenger increased by about 60 percent between FY88 and FY91. This experiencedoes not correlate with the downward cost trends of the insurance industry or with thesignificant improvement in MBL’s safety record during the performan_ce audit period (i.e.,miles between accidents improved by over 80 percen0. Each year during the period FY88through FY91, the audited MBL financial statements exhibited more "insurance" expensethan the total indemnity and medical benefit payments by the City of Montebello.

In FY91, MBL’s casualty and liability expense was over $1.0 million and accounted

for 13 percent of MBL’s total operating budget.

Phase I Recommendation: MBL needs to improve its understanding of the riskmanagement program (Recommendation #3 from the MBL Phase I Triennial PerformanceAudit).

Potential Phase II Assistance: In this task, BoozoAllen would provide technicalassistance to the MBL Director of Transportation and City Risk Manager to identifypotential causes of escalating castmlty and liability costs, as well as strategies and programsto reduce costs.

Phase H Budget: $20,000

Potential Benefits: The cost of this effort is about two percent of MBL’s FY91casuzlty and liability costs. Potential cost savings resulting from Phase II analyses are likelyto off-set the cost of this task given previous experience with similar studies. For example,in the FY89 Phase II analysis of SCRTD’s risk management costs, more than $20 millionwas saved as a result of implementing Phase II recommendations.

DEVELOPMENT OF A STRATEGIC PLANNING PROCESS FOR THE MTA/SCRTD

Phase I Audit Findings: Over the audit period, SCRTD has experienced the initialeffects of a sluggish and worsening economy. Several statistics describe trends to whichSCRTD will be required to respond in FY92, FY93 and FY94:

SCRTD has reduced total vehicle service hours by about three percent andmiles by more than five percent. Additional service reductions may warrantreview, depending on the financial results of the system in future years.

Total operating costs have increased at the rate of inflation (i.e., 15.9percentCPI-W) and hence, cost per hour and mile have increased at a rote greaterthan inflation. Given poor economic projections for employment andgovernment funding in the region, cost growth requires greater control at theSCRTD in the future.

Unlinked passengers have declined by two percent over the audit period, withmuch of this decline attributable to service reductions and regional- economicconditions. Given the negative economic outlook for Southern California andthe increasing jobless rate, SCRTD needs to develop a strategy which countersa potential decline to its market and hence, to fare revenue.

While government subsidies to SCRTD have ":ncreased over the current aa-ditperiod, Statewide collection of TDA revenues and regional collections of salestaxes are expected to decline in available economic forecasts. SCRTD’sfinancial and operating strategy should also address the risk of decliningsubsidies during the economic crises.

Significant future financial shortfalls will occur in FY92, FY93 and FY94 if currenttrends continue unabated.

Phase I Recommendation: Evaluate cost, revenue and funding trends and developa progressive financial and operating strategy which meets District objectives during the on-going economic downturn (Recommendation #1 from the SCRTD Phase I TriennialPerfo~n-~ance Audit).

Potential Phase II AssLstance: In this potential Phase II task, Booz.Allen wouldassist a team of MTA]SCRTD management and staff to pursue and develop a strategywhich offers alternative approaches and solutions to upcoming financial and operating issues.Because Phase II resources are limited, Boaz.Allen proposes to assist management todevelop a process, work plan and schedule for developing strategic future scenarios. Booz-.Allen would provide the technical tools, approach and training so that MTA/SCRTD staffcould develop and update strategic plans in a timely manner.

Specifically, BoozoAllen would be responsible for:

¯ Conducting up to three workshops with management, staff and Boardmembers to understand the strategic planning process and benefits from saidefforts

Work with management to develop a work plan and schedule for developinga strategic plan and alternative scenarios, including definition of sub-activitiesand where these activities may best be performed within the merged MTAorganization

Participate in monthly management meetings to review plan developmentprogress and trouble-shoot issues

¯ Independently critiquestrategic plan results.

Even with this joint effort, the cost of this Phase II task would exceed the currentPhase II budget of $49,200, as shown below.

Phase H Budget: $100,000

Potential Benefits: The recent reorganization of the SCRTD and the LACTCpresents a significant opportunity to develop a comprehensive strategic.plan that bridges thegap between the SCRTD yhort-range transit plan and the LACTC long-range 30-Year Plan.A strategic plan would provide for alternative future scenarios give a variety of economic,funding, technology and air quality assumptions. Given a wide range of future scenarios,separate strategies are developed to achieve transportation objectives. Projects andprograms to implement the potential strategy are evaluated relative to strategic objectives --what are the short- and long-term impacts of service, project and program decisionsrelative to objectives such as economic stimulus, air quality and congestion.

A strategic plan for the MTAJSCRTD would provide a financial and operatingstrategy which is flexible and which considers the risks and opportunities related to thecurrent and future negative economic impacts expected in the region. De~,elopment of astrategy will provide the LACMTA with viable alternatives to address future risk and allowtimely and prudent action to avoid a financial crisis. Performance measurement of service,project and program implementation relative to strategic, objectives is an iterative processthat can be applied to both annual budget and longer-term funding decisions. A soundprogram will be flexible and provide the greatest benefit given real and dire financialconstraints.

Phase I Audit F’mdings: Phase I included a review of operator compliance with datareporting requirements, as well as a review of goals, objective and management reportingsystems. General findings that cover the majority of transit operators include:

Transit operators hav~ developed a variety of data bases and spreadsheetapplications to assist with LACMTA reporting requirements

LACMTA staff have responsibility for checking and recalculatingoperator reported statistics

transit

Existing TPM guidelines contain ambiguities and LACMTA and transitoperator practices vary with regard to cost allocation and the definition ofauxiliary revenues

TPM reported costs for weekday services tend to understate the cost ofservice by the amount of deadhead mileage and hours

While LACMTA funding programs and guidelines have changed (e.g., PropA Discretionary, TPM) revisions in reporting requirements have not yet beenmade

Despite fairly status quo reporting requirements, some transit operators werefound to be in non-compliance

There is a group of core performance indicators that a majority of transitoperators monitor on a routine (e.g., monthly and/or quarterly) basis.

Existing reporting requirements are quite complex, contain some overlap (e.g.,sameitem reported multiple times to various external agencies), and require administrative stafftime of both transit operating agencies and the LACMTA to prepare and review. Therelationship between reporting requirements and the actual use of the information generatedare not always clear.

Phase I Recommendation: 17 of 41 transit operator performance auditrecommendations deal with data reporting and compliance.

Potential Phase II Assistance: Efforts to streamline reporting requfi-ements wouldfocus on five programs:

Proposition A Discretionary Grant Applications and Quarterly ReportsProposition C Transit Expansion Funding Applications and ReportingTPM and Annual Transit Productivity Program ReportingSTA Annual Efficiency FindingInformation used in the annual Formula Allocation Process.

In developing a streamlined and comprehensive reporting program the following stepswould be performed by BoozoAllen:

Interviews with transit operators and LACMTA staff regarding the use ofinformation routinely reported and monitored

Prepare legislative and compliance matrix noting which items are mandatedand/or required to assess compliance with funding guidelines and objectives

Prepare flow-chart of data sources, external reports, and use in meetingprogram and legislative requirements

Identify information which is collected but not used, as well as anyinformation that is needed but not collected

Work with the LACMTA staff and BOS to develop revised reportingrequirements

Prepare documentation of revised reporting requirements

Conduct of up to three training workshops regarding streamlined reportingrequirements.

Phase II Budget: $49,200

Potential Benefits: The benefits of taking action now as opposed to a later daterelate to the costs and level of effort on the part of transit ope~tors to comply withrepc-rting requirements, as well as the costs and level of effort on the part of MTA staff toaddress ambiguities noted in Phase I with the TPM program and perfolmance monitoringrequirements for Prop C Transit Service Expansion funds.

Phase I recommended that transit operators comply with LACMTA reportingrequirements. Implementation of recommendations is mandatory under State TDAregulations. The time to change and streamline reporting requirements is before transitoperators invest the time and money to comply with current audit recommendations.Mzking sure that reporting requirements are as economical and meaningful as possible islikely to motive transit operators to improve and comply.

During Phase I, weaknesses were observed in current reporting requirements andpractice. We believe that it is possible to streamline and reduce reporting requirements, aswell as provide more meaning and value from the information reported.