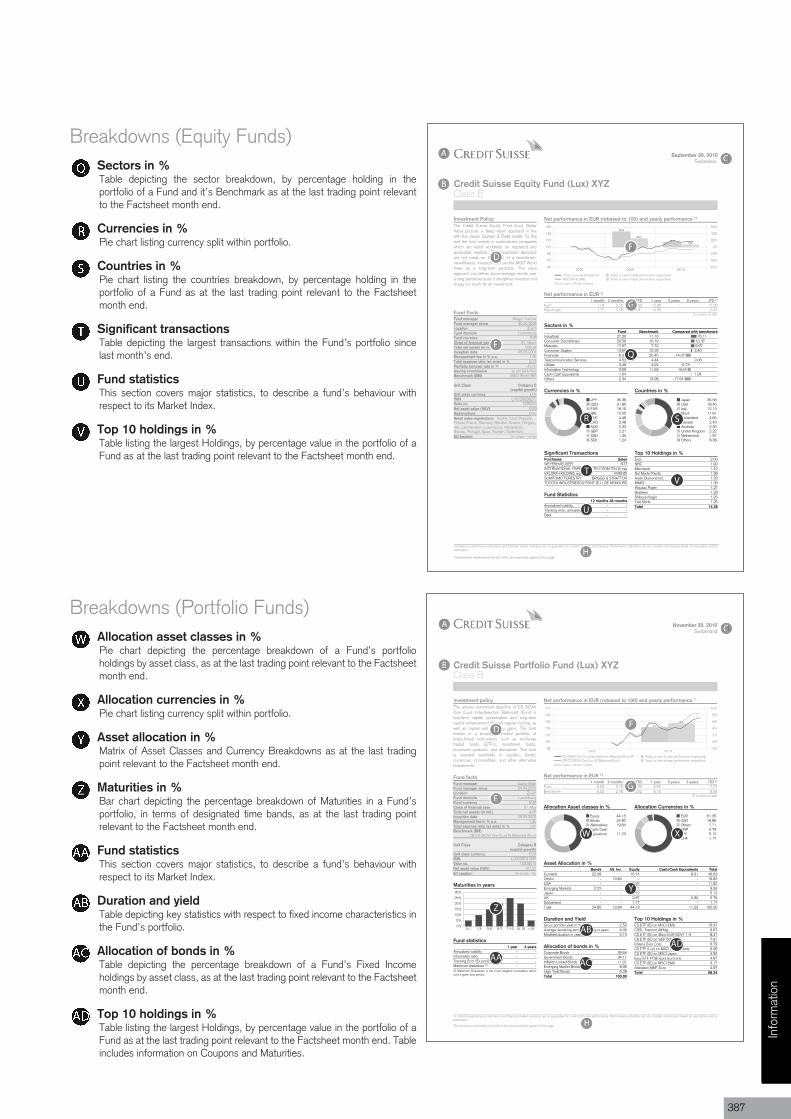

394

Fund Factbook Swiss Market Data as at March 2012

| Date post: | 27-Mar-2018 |

| Category: |

Documents |

| Upload: | phungtuong |

| View: | 221 times |

| Download: | 4 times |

booklet issuerId channelId languageId perDateFund Factbook9926 9913 18 20120330

Fund FactbookSwiss MarketData as at March 2012

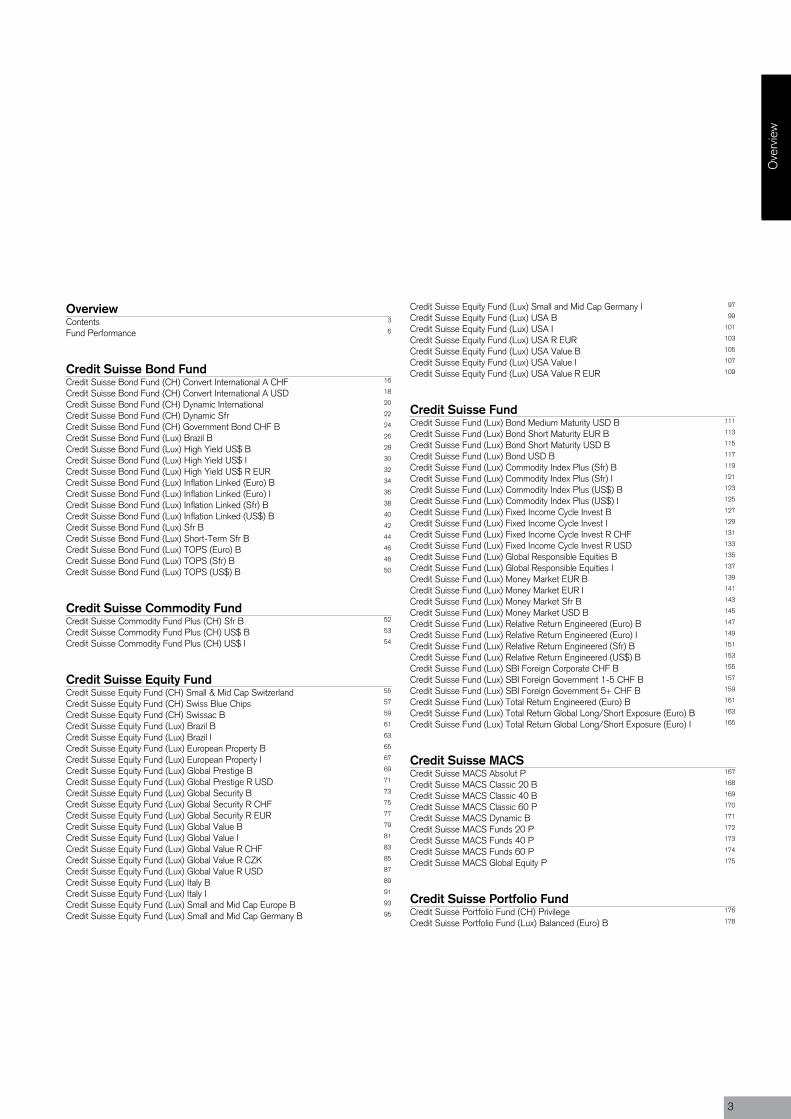

OverviewContents 3

Fund Performance 6

Credit Suisse Bond FundCredit Suisse Bond Fund (CH) Convert International A CHF 16

Credit Suisse Bond Fund (CH) Convert International A USD 18

Credit Suisse Bond Fund (CH) Dynamic International 20

Credit Suisse Bond Fund (CH) Dynamic Sfr 22

Credit Suisse Bond Fund (CH) Government Bond CHF B 24

Credit Suisse Bond Fund (Lux) Brazil B 26

Credit Suisse Bond Fund (Lux) High Yield US$ B 28

Credit Suisse Bond Fund (Lux) High Yield US$ I 30

Credit Suisse Bond Fund (Lux) High Yield US$ R EUR 32

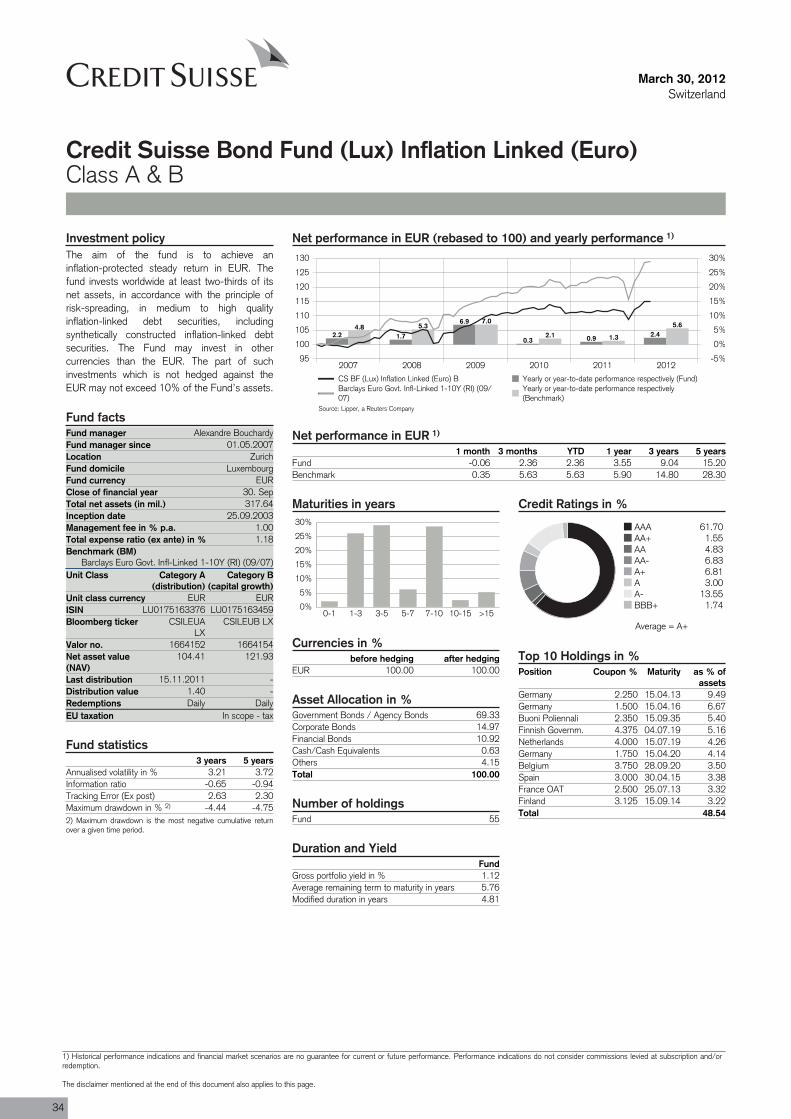

Credit Suisse Bond Fund (Lux) Inflation Linked (Euro) B 34

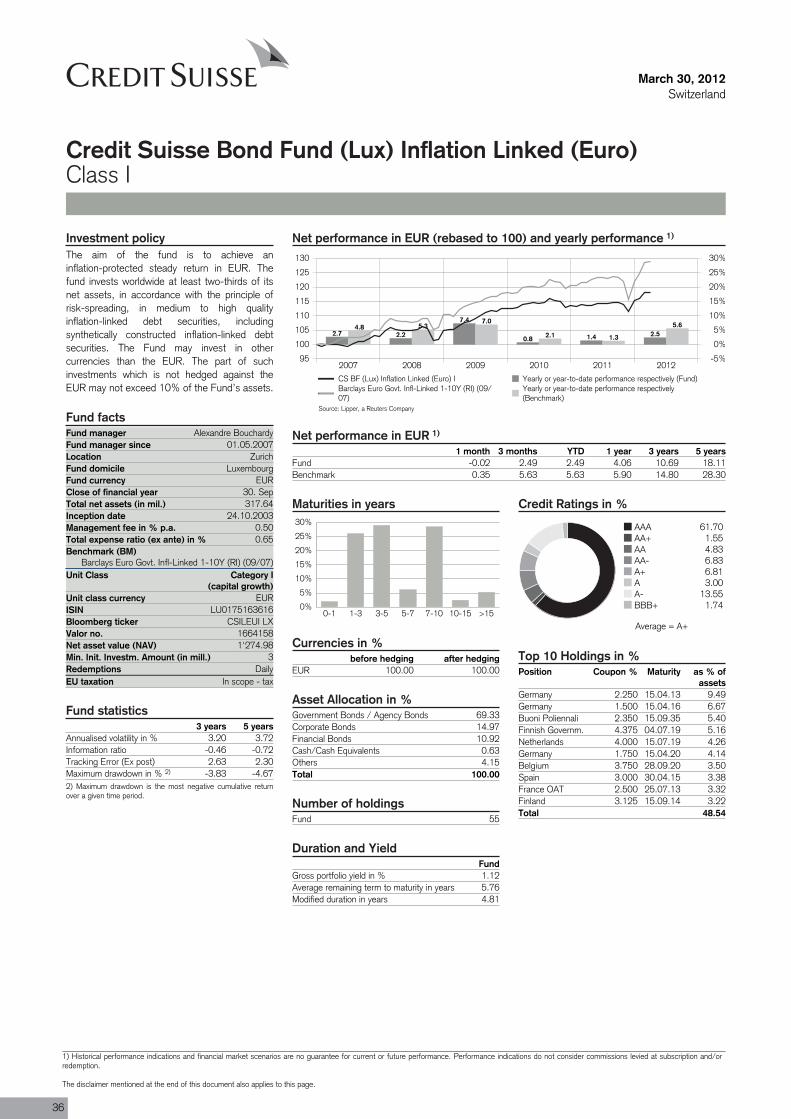

Credit Suisse Bond Fund (Lux) Inflation Linked (Euro) I 36

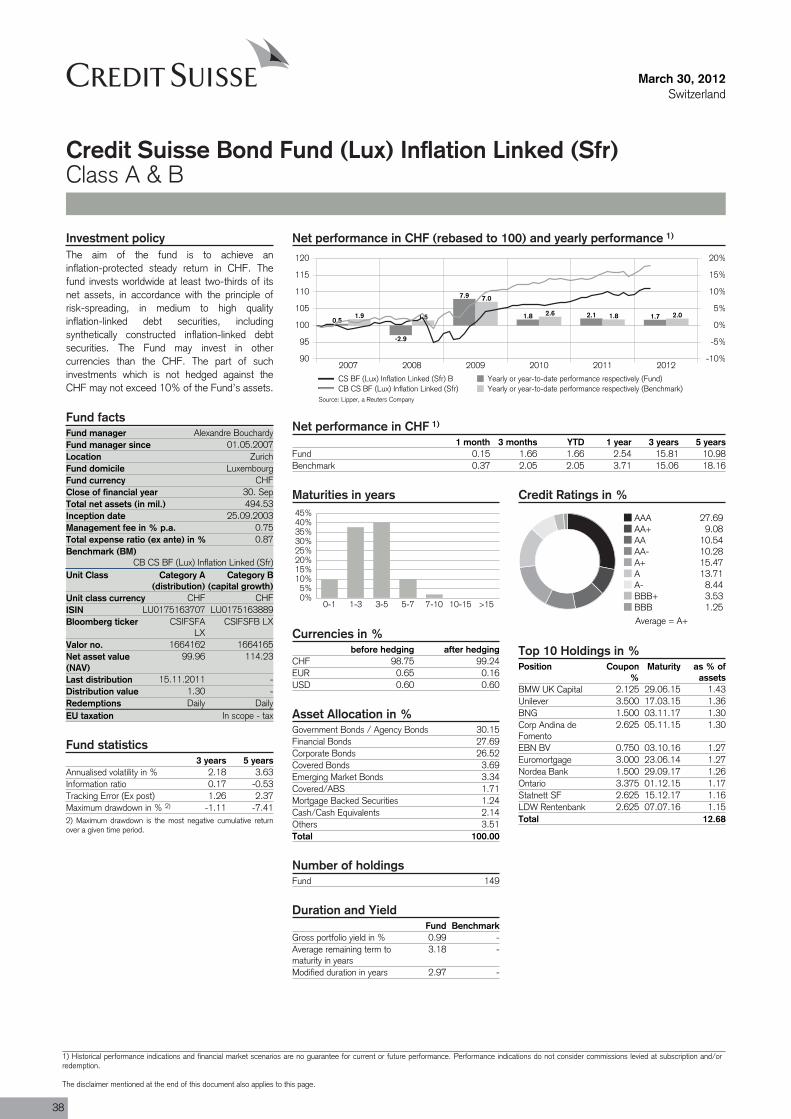

Credit Suisse Bond Fund (Lux) Inflation Linked (Sfr) B 38

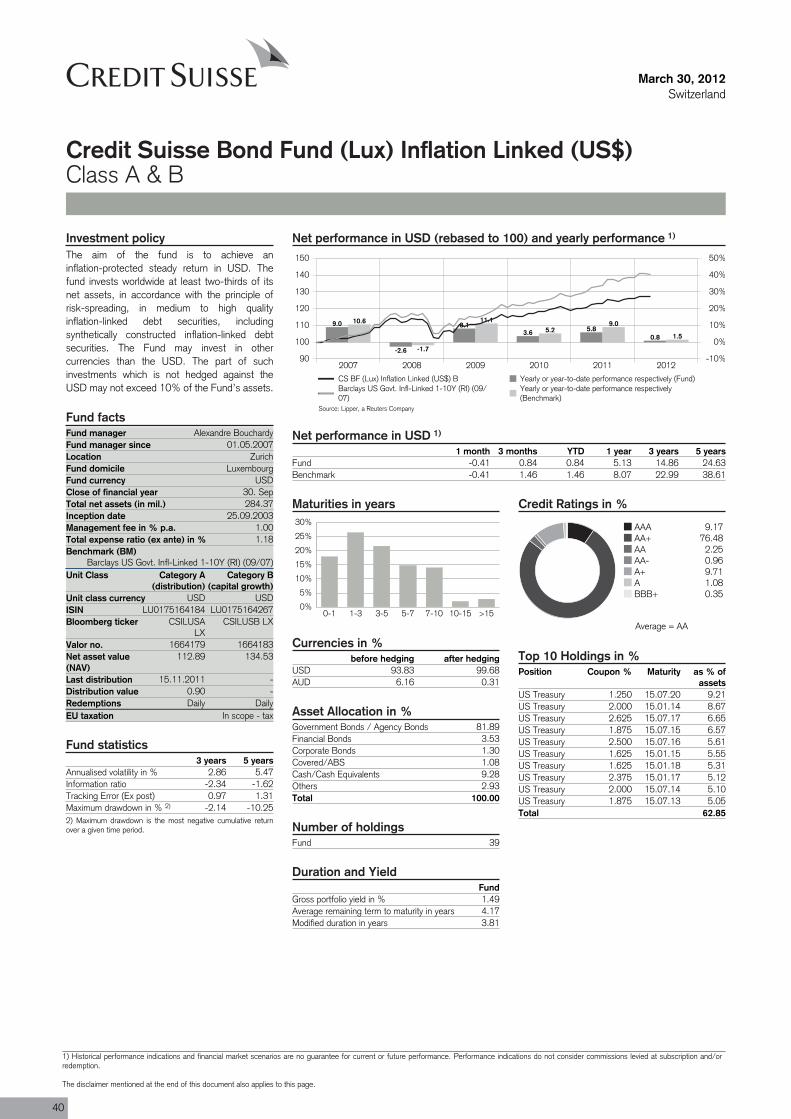

Credit Suisse Bond Fund (Lux) Inflation Linked (US$) B 40

Credit Suisse Bond Fund (Lux) Sfr B 42

Credit Suisse Bond Fund (Lux) Short-Term Sfr B 44

Credit Suisse Bond Fund (Lux) TOPS (Euro) B 46

Credit Suisse Bond Fund (Lux) TOPS (Sfr) B 48

Credit Suisse Bond Fund (Lux) TOPS (US$) B 50

Credit Suisse Commodity FundCredit Suisse Commodity Fund Plus (CH) Sfr B 52

Credit Suisse Commodity Fund Plus (CH) US$ B 53

Credit Suisse Commodity Fund Plus (CH) US$ I 54

Credit Suisse Equity FundCredit Suisse Equity Fund (CH) Small & Mid Cap Switzerland 55

Credit Suisse Equity Fund (CH) Swiss Blue Chips 57

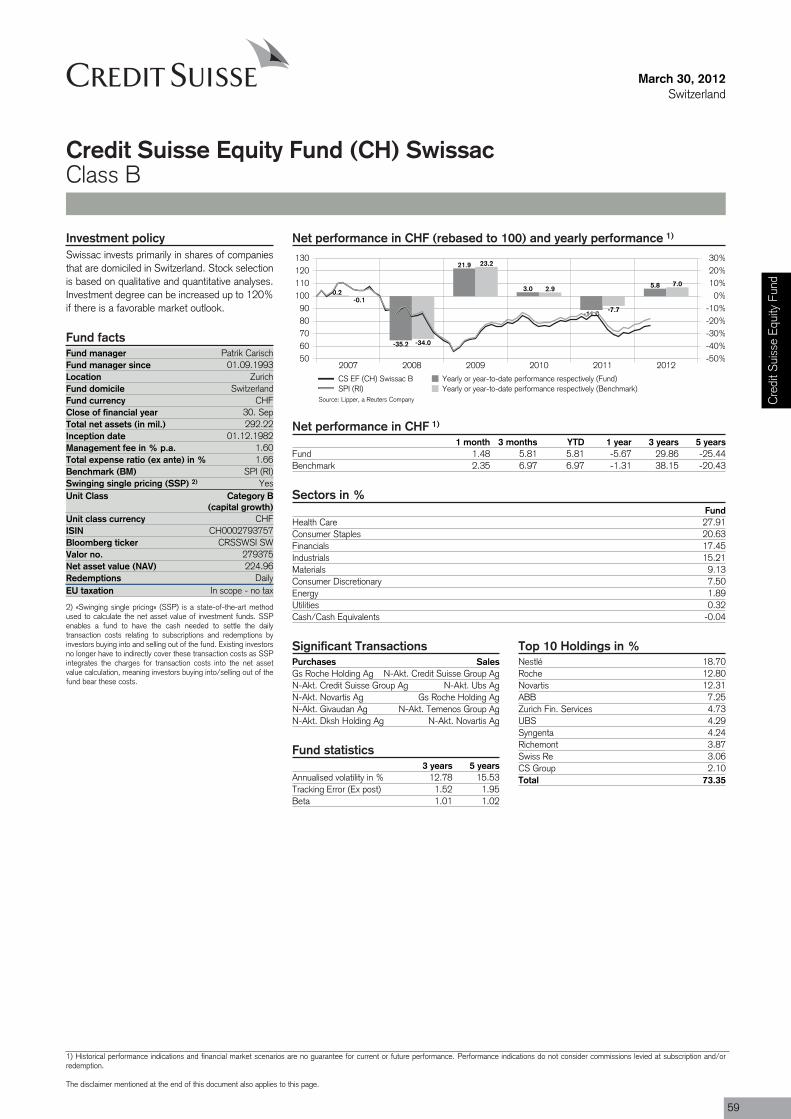

Credit Suisse Equity Fund (CH) Swissac B 59

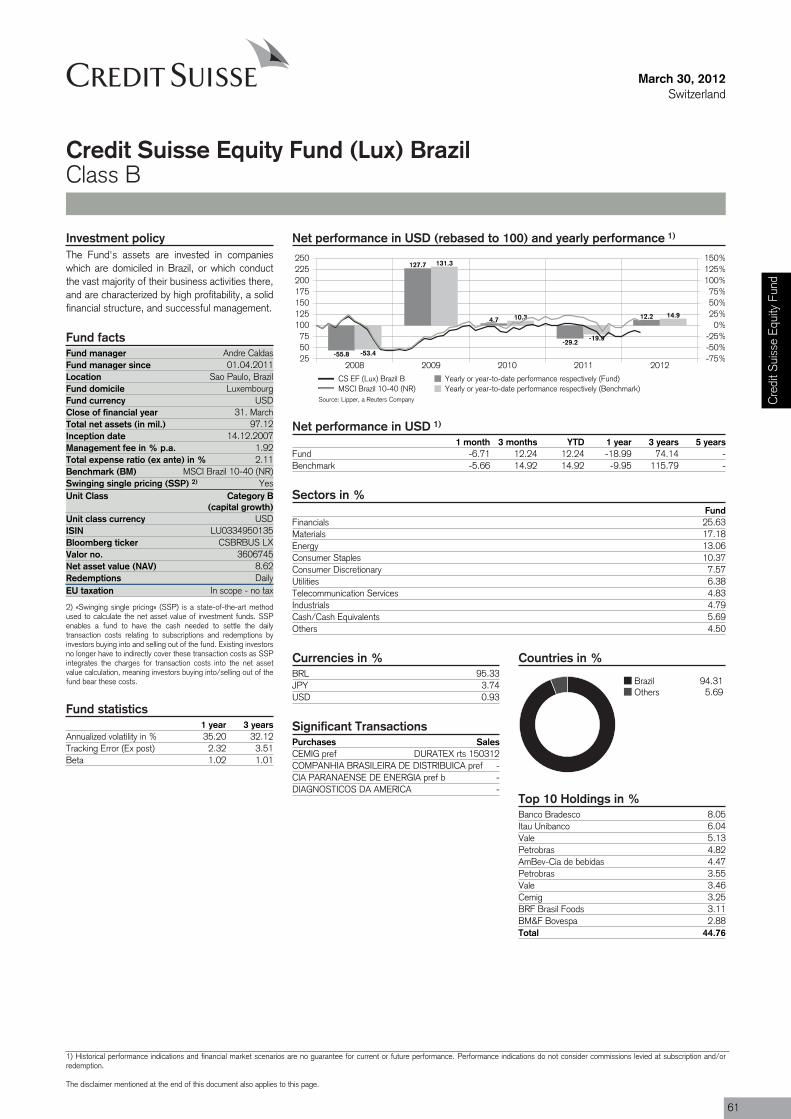

Credit Suisse Equity Fund (Lux) Brazil B 61

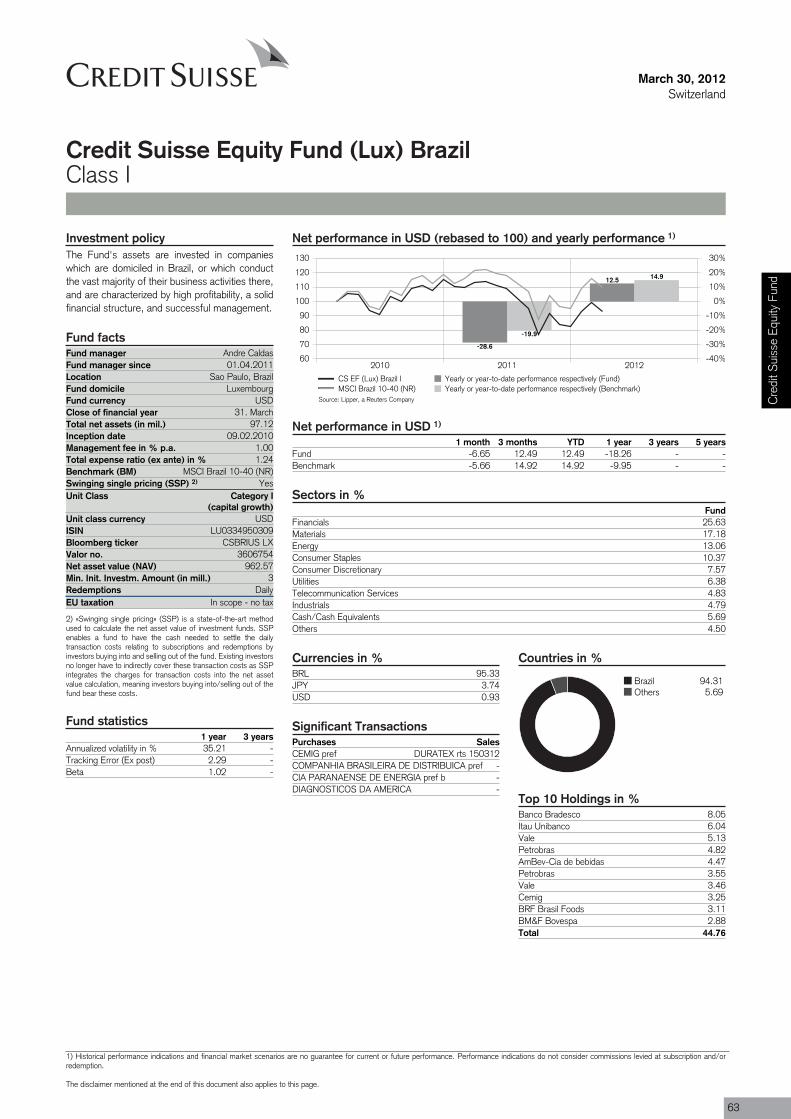

Credit Suisse Equity Fund (Lux) Brazil I 63

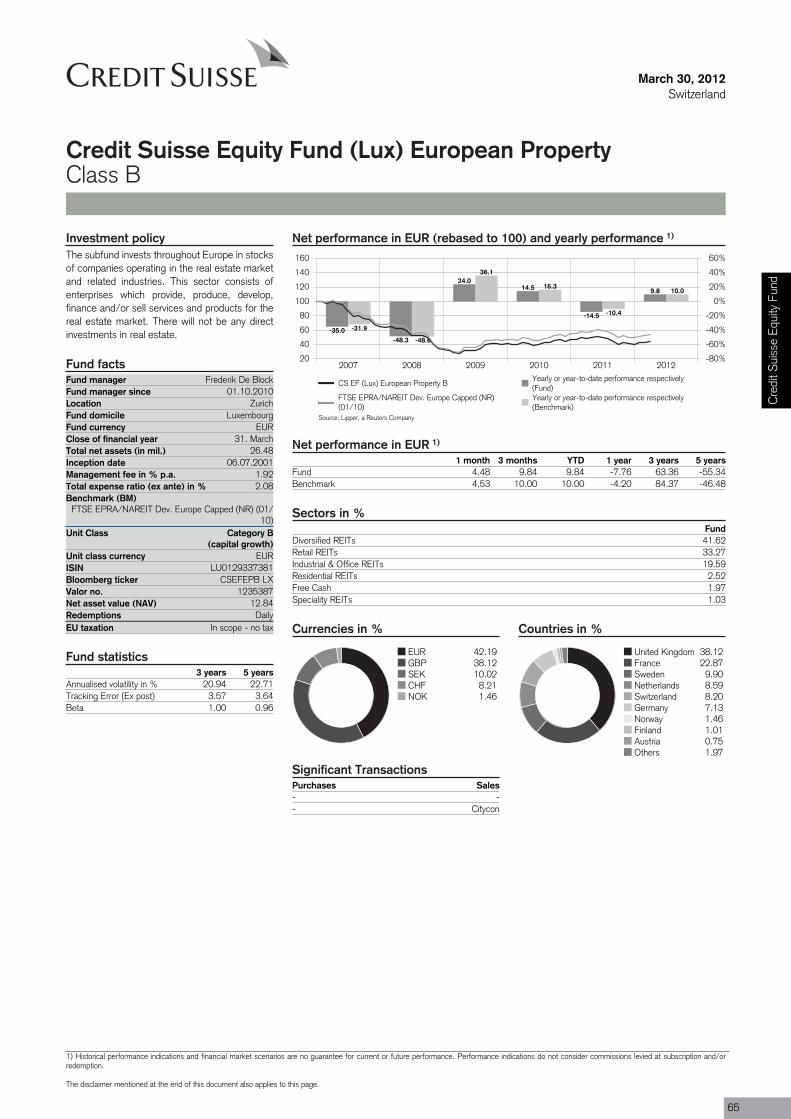

Credit Suisse Equity Fund (Lux) European Property B 65

Credit Suisse Equity Fund (Lux) European Property I 67

Credit Suisse Equity Fund (Lux) Global Prestige B 69

Credit Suisse Equity Fund (Lux) Global Prestige R USD 71

Credit Suisse Equity Fund (Lux) Global Security B 73

Credit Suisse Equity Fund (Lux) Global Security R CHF 75

Credit Suisse Equity Fund (Lux) Global Security R EUR 77

Credit Suisse Equity Fund (Lux) Global Value B 79

Credit Suisse Equity Fund (Lux) Global Value I 81

Credit Suisse Equity Fund (Lux) Global Value R CHF 83

Credit Suisse Equity Fund (Lux) Global Value R CZK 85

Credit Suisse Equity Fund (Lux) Global Value R USD 87

Credit Suisse Equity Fund (Lux) Italy B 89

Credit Suisse Equity Fund (Lux) Italy I 91

Credit Suisse Equity Fund (Lux) Small and Mid Cap Europe B 93

Credit Suisse Equity Fund (Lux) Small and Mid Cap Germany B 95

Credit Suisse Equity Fund (Lux) Small and Mid Cap Germany I 97

Credit Suisse Equity Fund (Lux) USA B 99

Credit Suisse Equity Fund (Lux) USA I 101

Credit Suisse Equity Fund (Lux) USA R EUR 103

Credit Suisse Equity Fund (Lux) USA Value B 105

Credit Suisse Equity Fund (Lux) USA Value I 107

Credit Suisse Equity Fund (Lux) USA Value R EUR 109

Credit Suisse FundCredit Suisse Fund (Lux) Bond Medium Maturity USD B 111

Credit Suisse Fund (Lux) Bond Short Maturity EUR B 113

Credit Suisse Fund (Lux) Bond Short Maturity USD B 115

Credit Suisse Fund (Lux) Bond USD B 117

Credit Suisse Fund (Lux) Commodity Index Plus (Sfr) B 119

Credit Suisse Fund (Lux) Commodity Index Plus (Sfr) I 121

Credit Suisse Fund (Lux) Commodity Index Plus (US$) B 123

Credit Suisse Fund (Lux) Commodity Index Plus (US$) I 125

Credit Suisse Fund (Lux) Fixed Income Cycle Invest B 127

Credit Suisse Fund (Lux) Fixed Income Cycle Invest I 129

Credit Suisse Fund (Lux) Fixed Income Cycle Invest R CHF 131

Credit Suisse Fund (Lux) Fixed Income Cycle Invest R USD 133

Credit Suisse Fund (Lux) Global Responsible Equities B 135

Credit Suisse Fund (Lux) Global Responsible Equities I 137

Credit Suisse Fund (Lux) Money Market EUR B 139

Credit Suisse Fund (Lux) Money Market EUR I 141

Credit Suisse Fund (Lux) Money Market Sfr B 143

Credit Suisse Fund (Lux) Money Market USD B 145

Credit Suisse Fund (Lux) Relative Return Engineered (Euro) B 147

Credit Suisse Fund (Lux) Relative Return Engineered (Euro) I 149

Credit Suisse Fund (Lux) Relative Return Engineered (Sfr) B 151

Credit Suisse Fund (Lux) Relative Return Engineered (US$) B 153

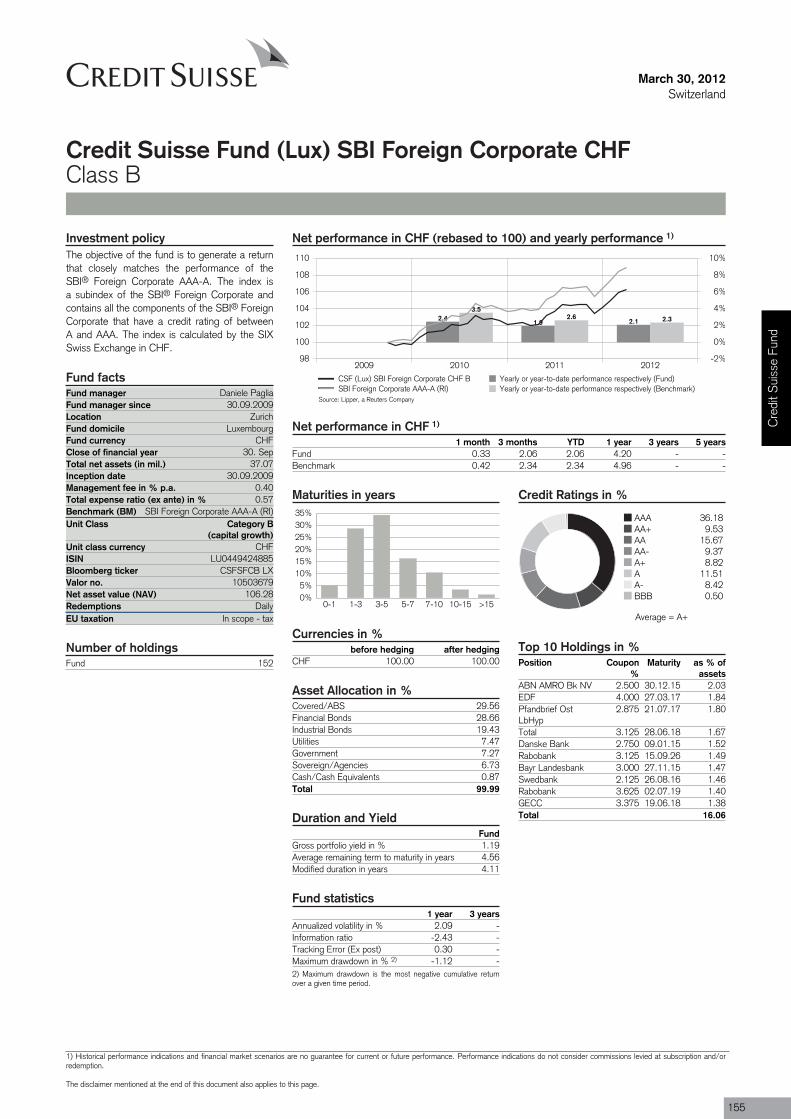

Credit Suisse Fund (Lux) SBI Foreign Corporate CHF B 155

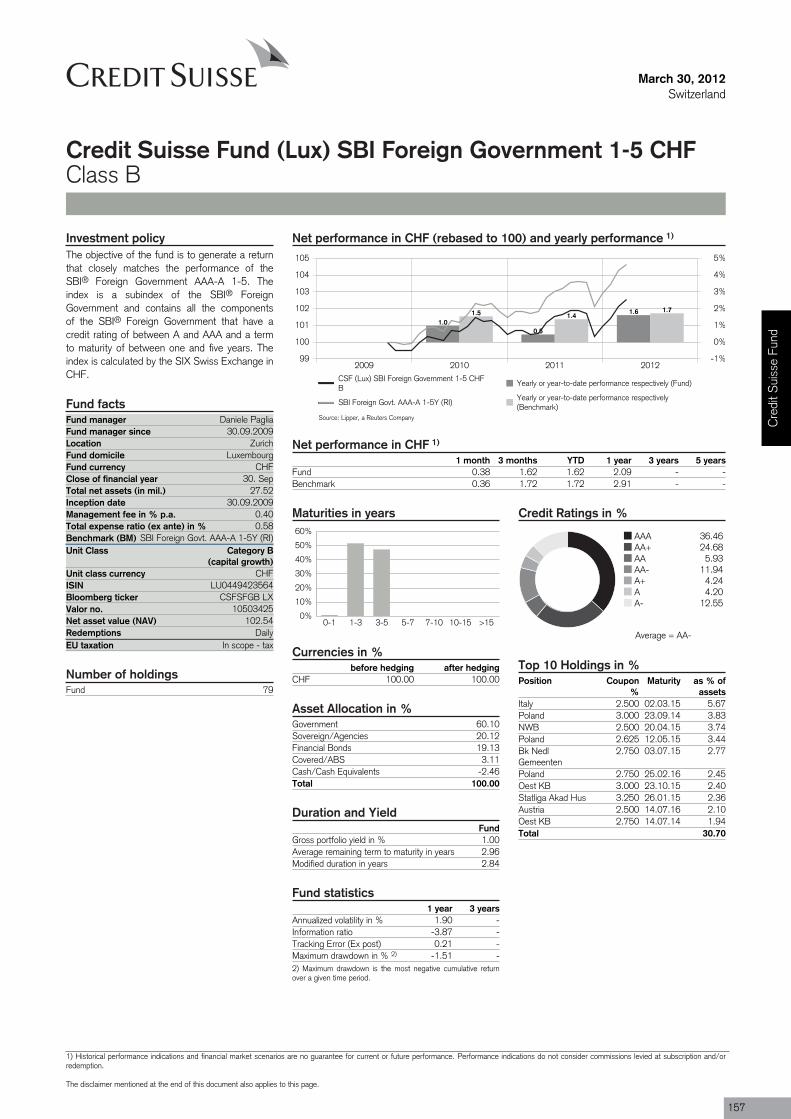

Credit Suisse Fund (Lux) SBI Foreign Government 1-5 CHF B 157

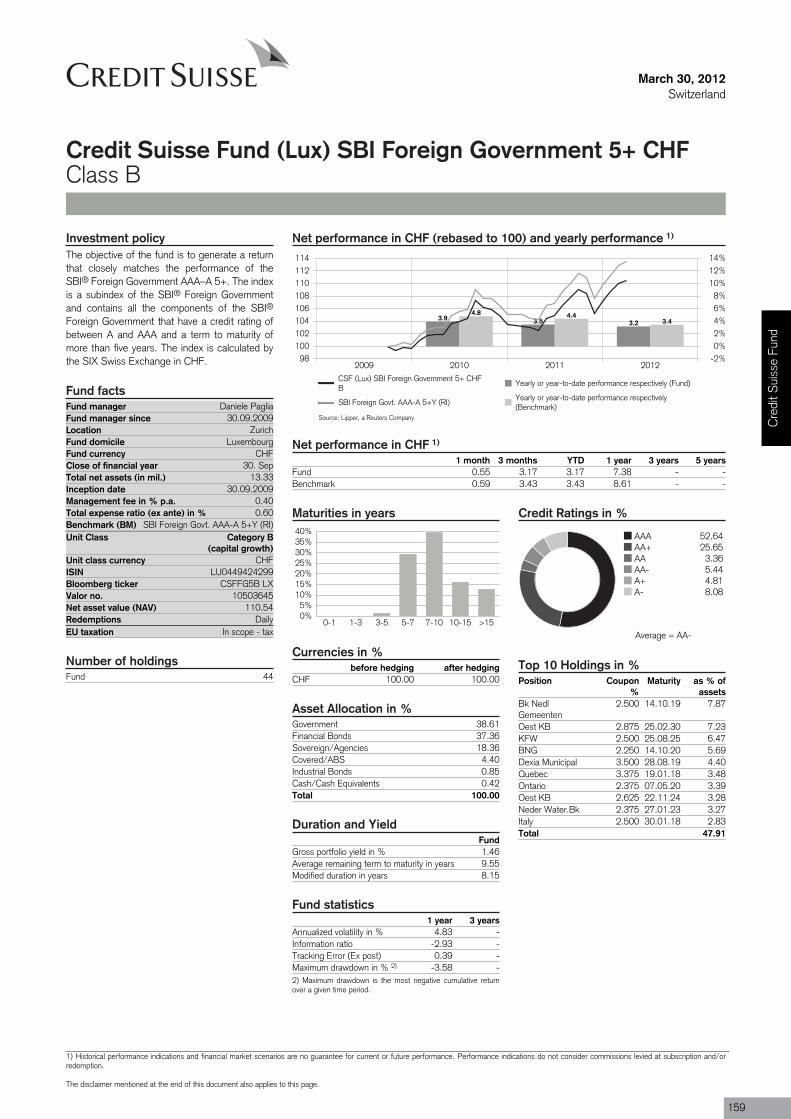

Credit Suisse Fund (Lux) SBI Foreign Government 5+ CHF B 159

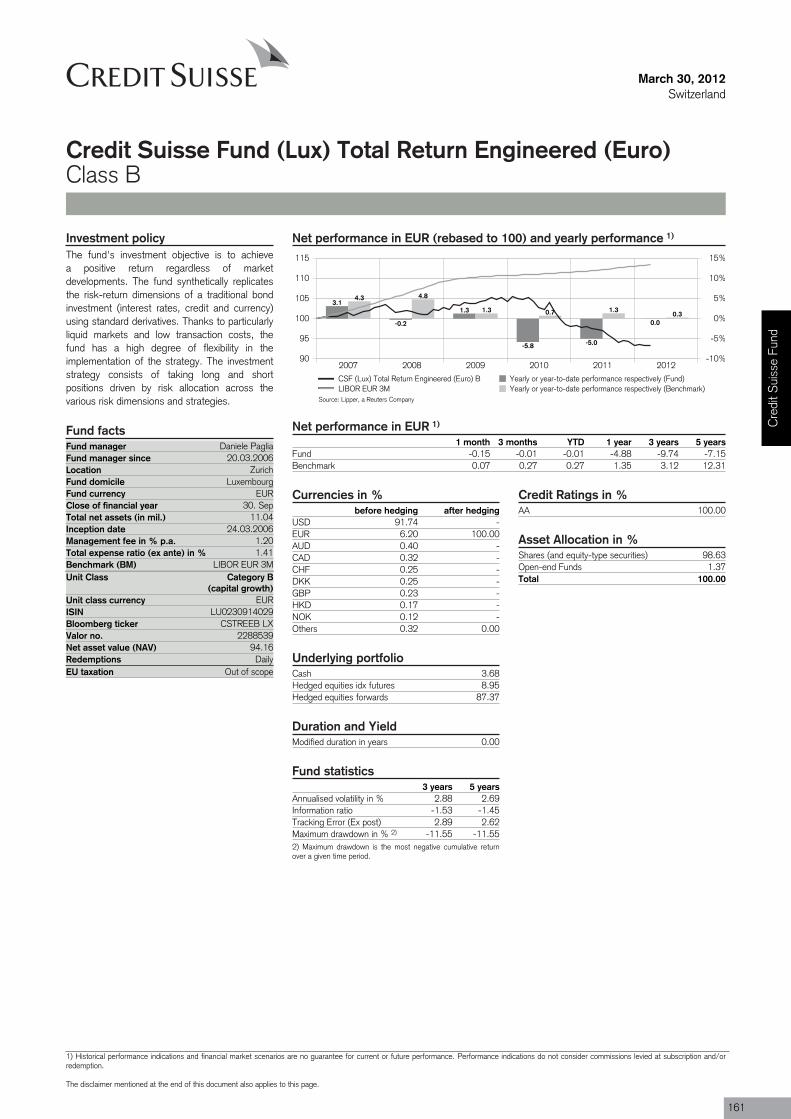

Credit Suisse Fund (Lux) Total Return Engineered (Euro) B 161

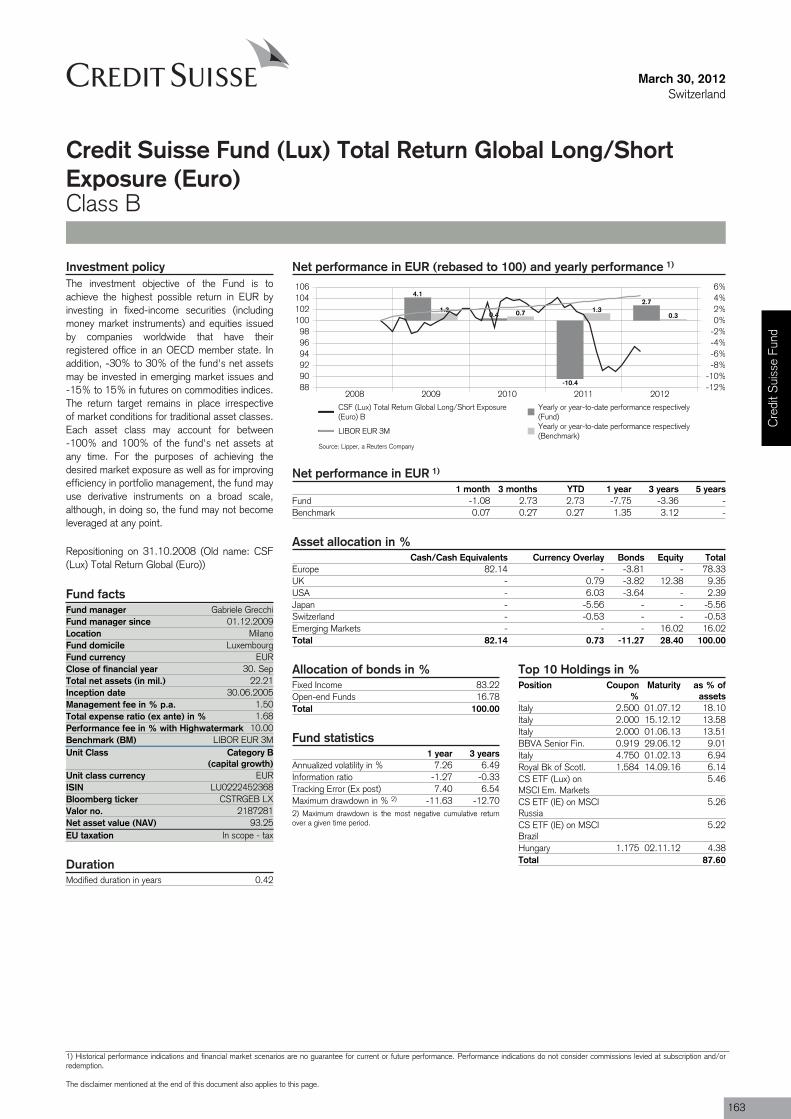

Credit Suisse Fund (Lux) Total Return Global Long/Short Exposure (Euro) B 163

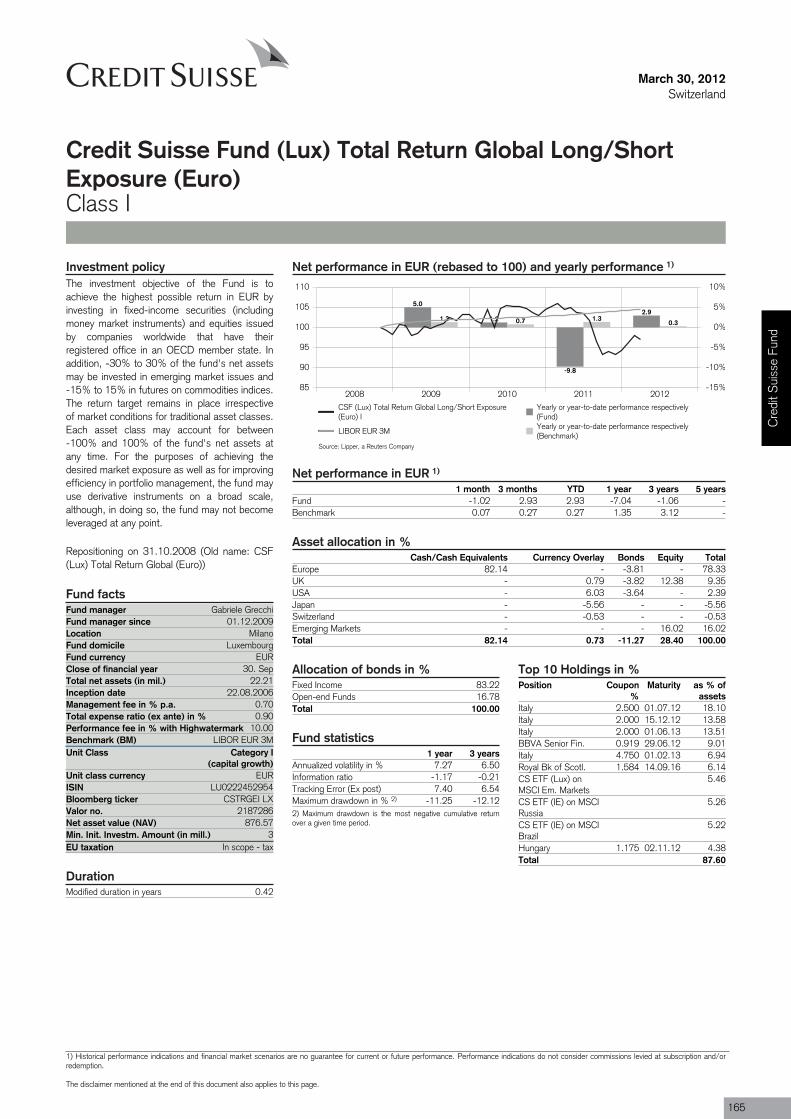

Credit Suisse Fund (Lux) Total Return Global Long/Short Exposure (Euro) I 165

Credit Suisse MACSCredit Suisse MACS Absolut P 167

Credit Suisse MACS Classic 20 B 168

Credit Suisse MACS Classic 40 B 169

Credit Suisse MACS Classic 60 P 170

Credit Suisse MACS Dynamic B 171

Credit Suisse MACS Funds 20 P 172

Credit Suisse MACS Funds 40 P 173

Credit Suisse MACS Funds 60 P 174

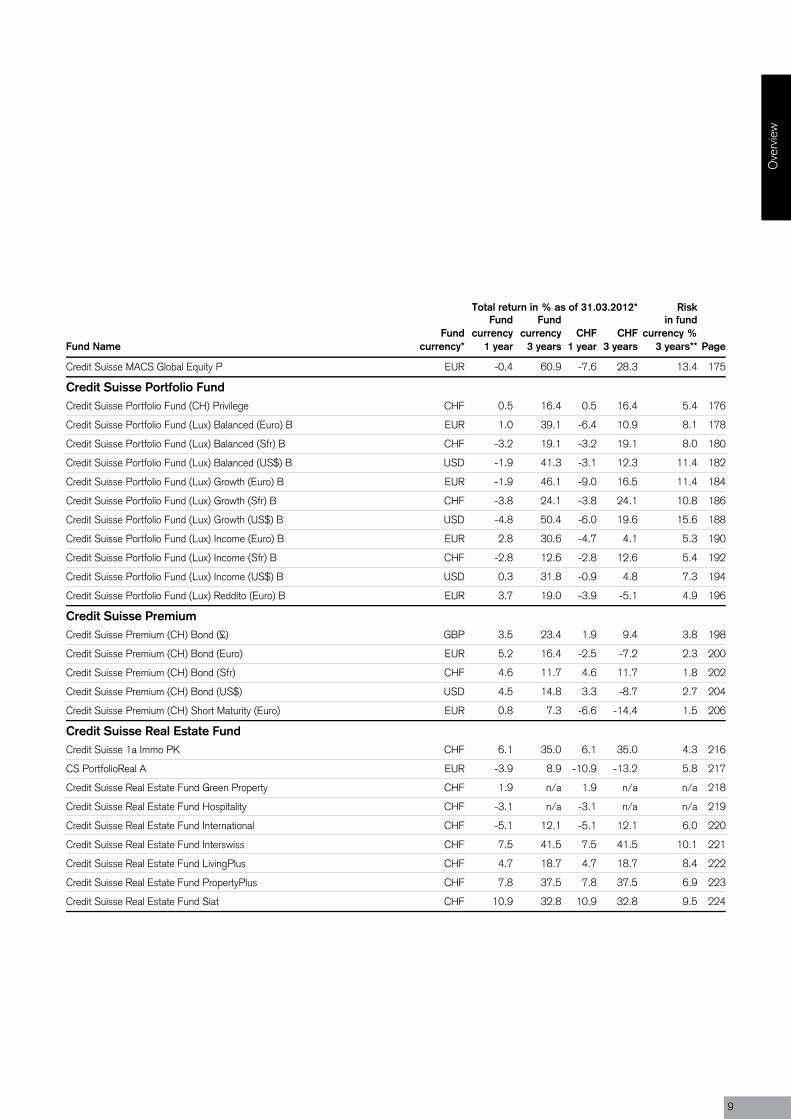

Credit Suisse MACS Global Equity P 175

Credit Suisse Portfolio FundCredit Suisse Portfolio Fund (CH) Privilege 176

Credit Suisse Portfolio Fund (Lux) Balanced (Euro) B 178

Ove

rvie

w

3

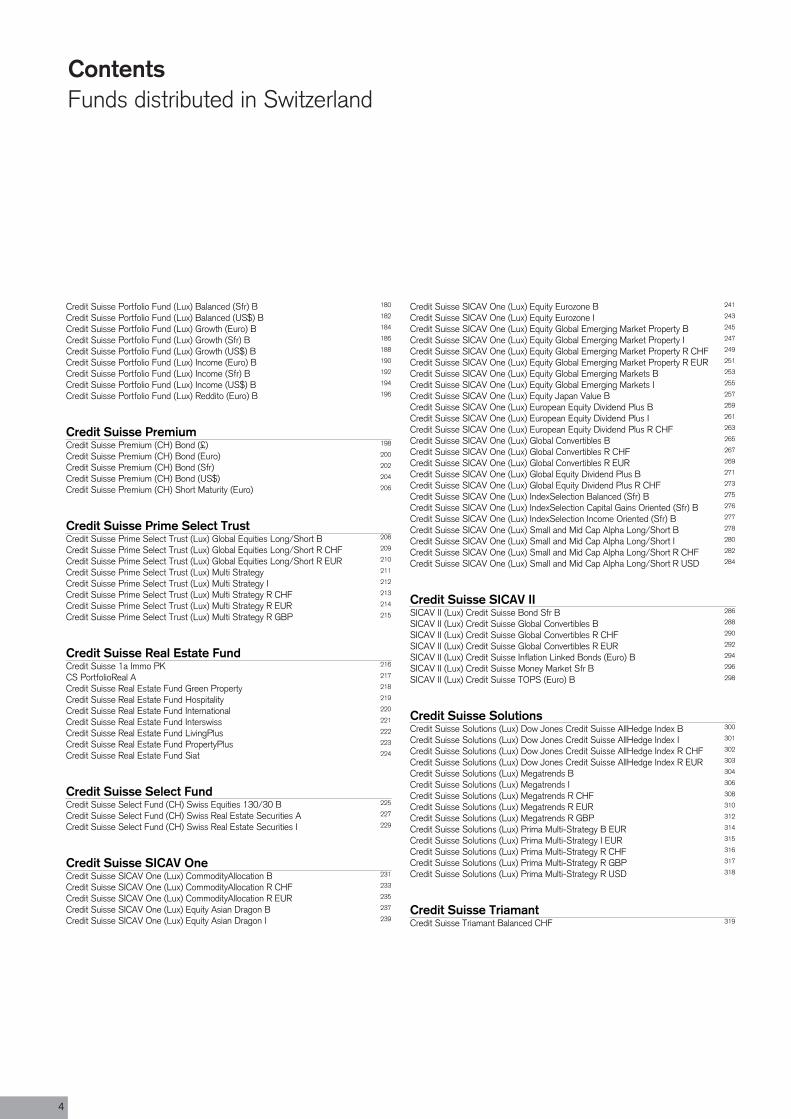

Credit Suisse Portfolio Fund (Lux) Balanced (Sfr) B 180

Credit Suisse Portfolio Fund (Lux) Balanced (US$) B 182

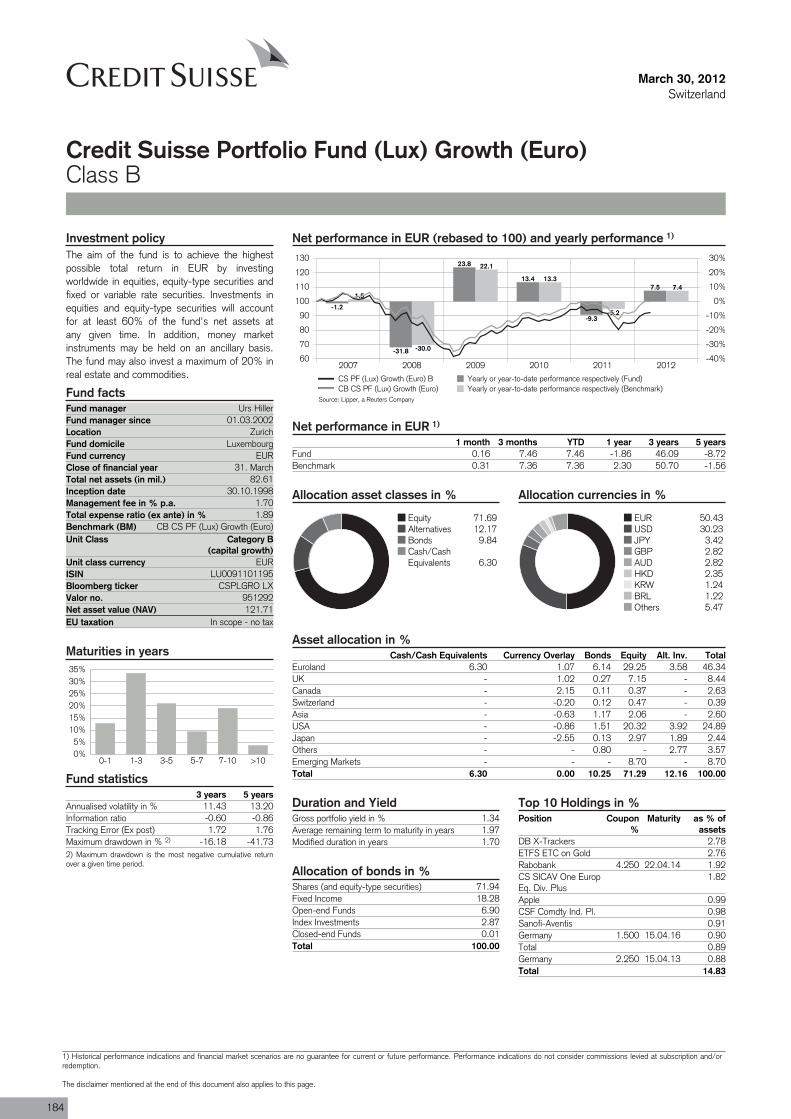

Credit Suisse Portfolio Fund (Lux) Growth (Euro) B 184

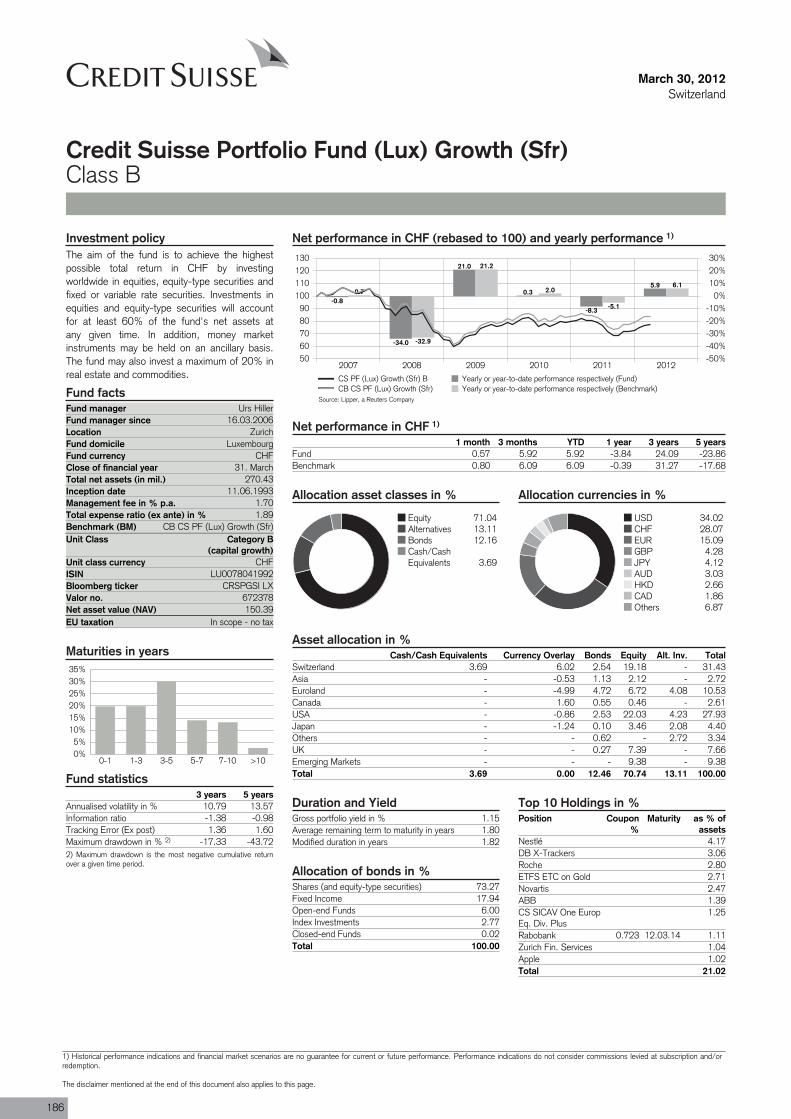

Credit Suisse Portfolio Fund (Lux) Growth (Sfr) B 186

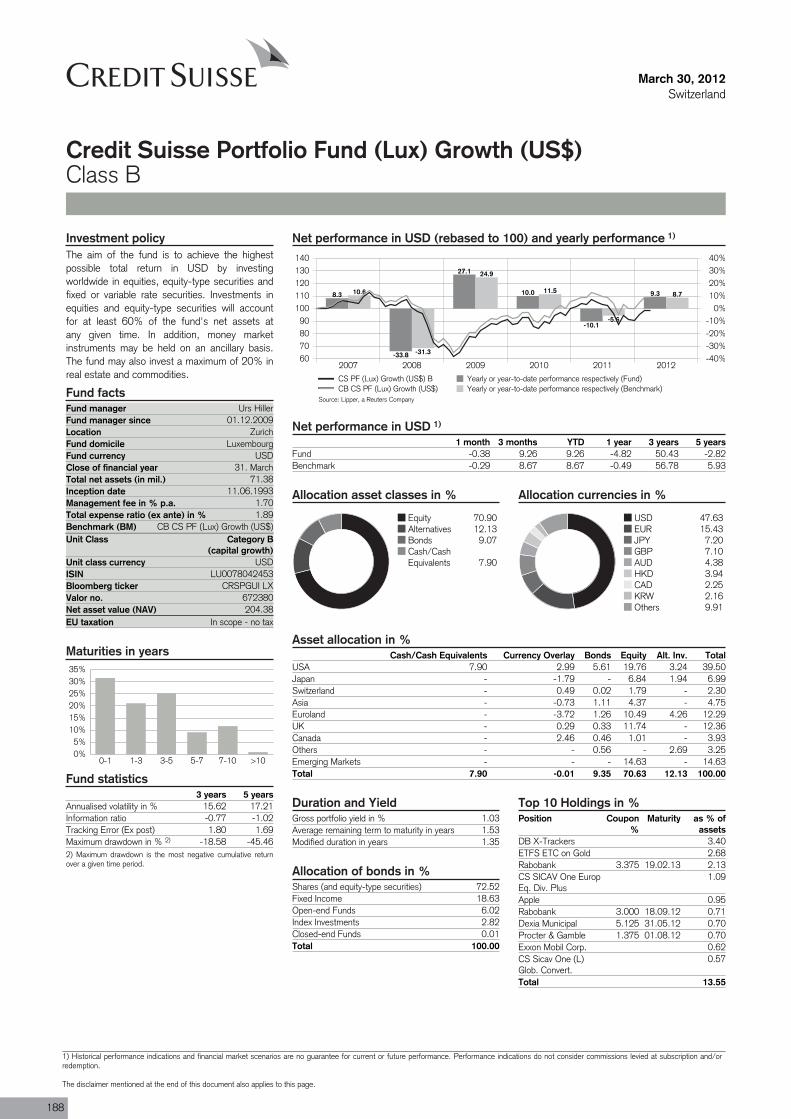

Credit Suisse Portfolio Fund (Lux) Growth (US$) B 188

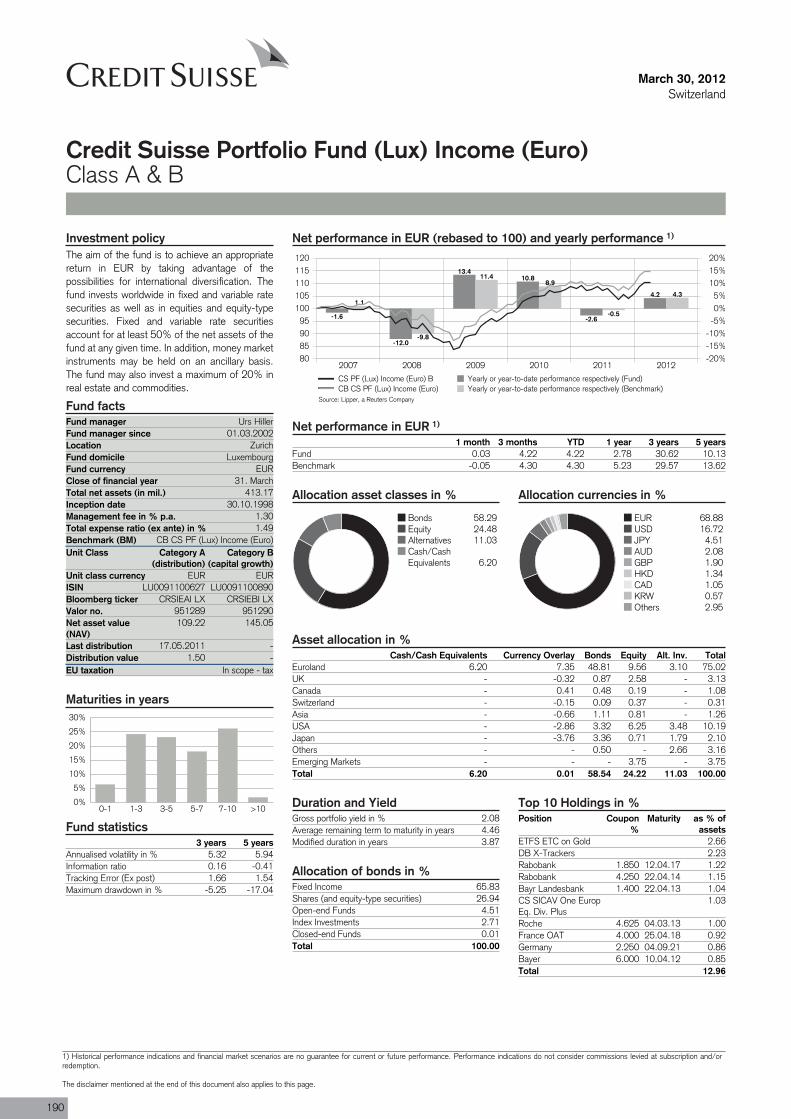

Credit Suisse Portfolio Fund (Lux) Income (Euro) B 190

Credit Suisse Portfolio Fund (Lux) Income (Sfr) B 192

Credit Suisse Portfolio Fund (Lux) Income (US$) B 194

Credit Suisse Portfolio Fund (Lux) Reddito (Euro) B 196

Credit Suisse PremiumCredit Suisse Premium (CH) Bond (£) 198

Credit Suisse Premium (CH) Bond (Euro) 200

Credit Suisse Premium (CH) Bond (Sfr) 202

Credit Suisse Premium (CH) Bond (US$) 204

Credit Suisse Premium (CH) Short Maturity (Euro) 206

Credit Suisse Prime Select TrustCredit Suisse Prime Select Trust (Lux) Global Equities Long/Short B 208

Credit Suisse Prime Select Trust (Lux) Global Equities Long/Short R CHF 209

Credit Suisse Prime Select Trust (Lux) Global Equities Long/Short R EUR 210

Credit Suisse Prime Select Trust (Lux) Multi Strategy 211

Credit Suisse Prime Select Trust (Lux) Multi Strategy I 212

Credit Suisse Prime Select Trust (Lux) Multi Strategy R CHF 213

Credit Suisse Prime Select Trust (Lux) Multi Strategy R EUR 214

Credit Suisse Prime Select Trust (Lux) Multi Strategy R GBP 215

Credit Suisse Real Estate FundCredit Suisse 1a Immo PK 216

CS PortfolioReal A 217

Credit Suisse Real Estate Fund Green Property 218

Credit Suisse Real Estate Fund Hospitality 219

Credit Suisse Real Estate Fund International 220

Credit Suisse Real Estate Fund Interswiss 221

Credit Suisse Real Estate Fund LivingPlus 222

Credit Suisse Real Estate Fund PropertyPlus 223

Credit Suisse Real Estate Fund Siat 224

Credit Suisse Select FundCredit Suisse Select Fund (CH) Swiss Equities 130/30 B 225

Credit Suisse Select Fund (CH) Swiss Real Estate Securities A 227

Credit Suisse Select Fund (CH) Swiss Real Estate Securities I 229

Credit Suisse SICAV OneCredit Suisse SICAV One (Lux) CommodityAllocation B 231

Credit Suisse SICAV One (Lux) CommodityAllocation R CHF 233

Credit Suisse SICAV One (Lux) CommodityAllocation R EUR 235

Credit Suisse SICAV One (Lux) Equity Asian Dragon B 237

Credit Suisse SICAV One (Lux) Equity Asian Dragon I 239

Credit Suisse SICAV One (Lux) Equity Eurozone B 241

Credit Suisse SICAV One (Lux) Equity Eurozone I 243

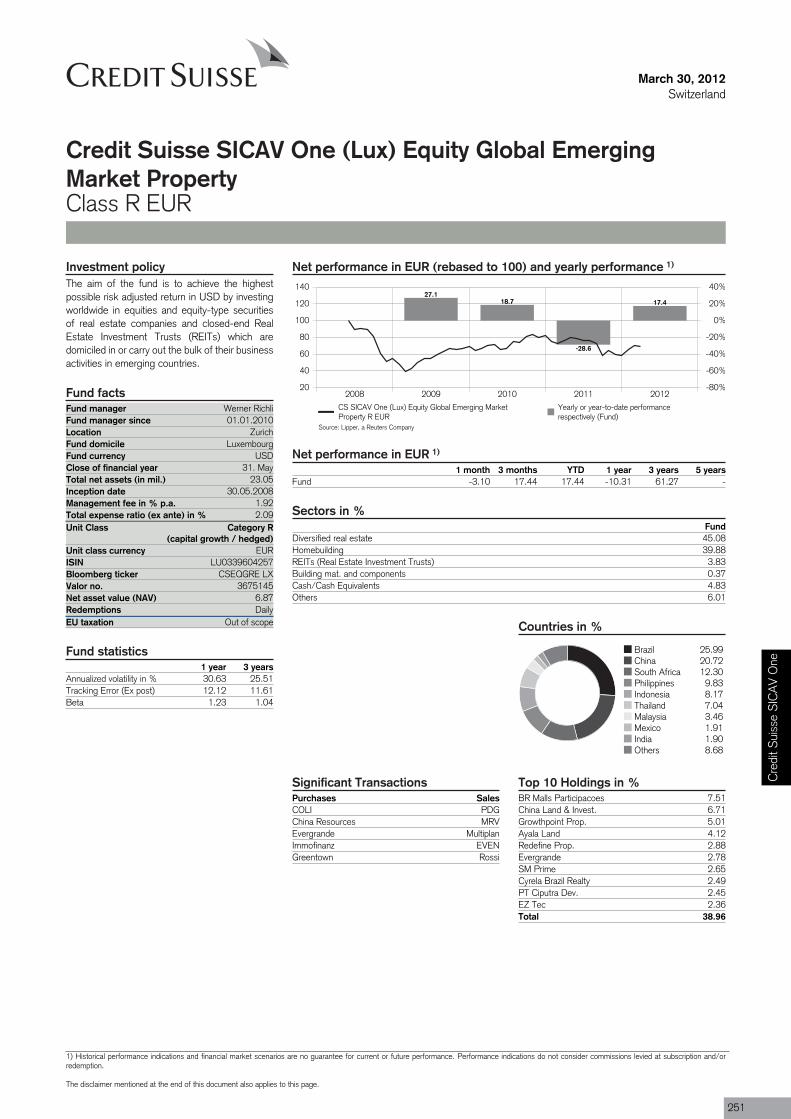

Credit Suisse SICAV One (Lux) Equity Global Emerging Market Property B 245

Credit Suisse SICAV One (Lux) Equity Global Emerging Market Property I 247

Credit Suisse SICAV One (Lux) Equity Global Emerging Market Property R CHF 249

Credit Suisse SICAV One (Lux) Equity Global Emerging Market Property R EUR 251

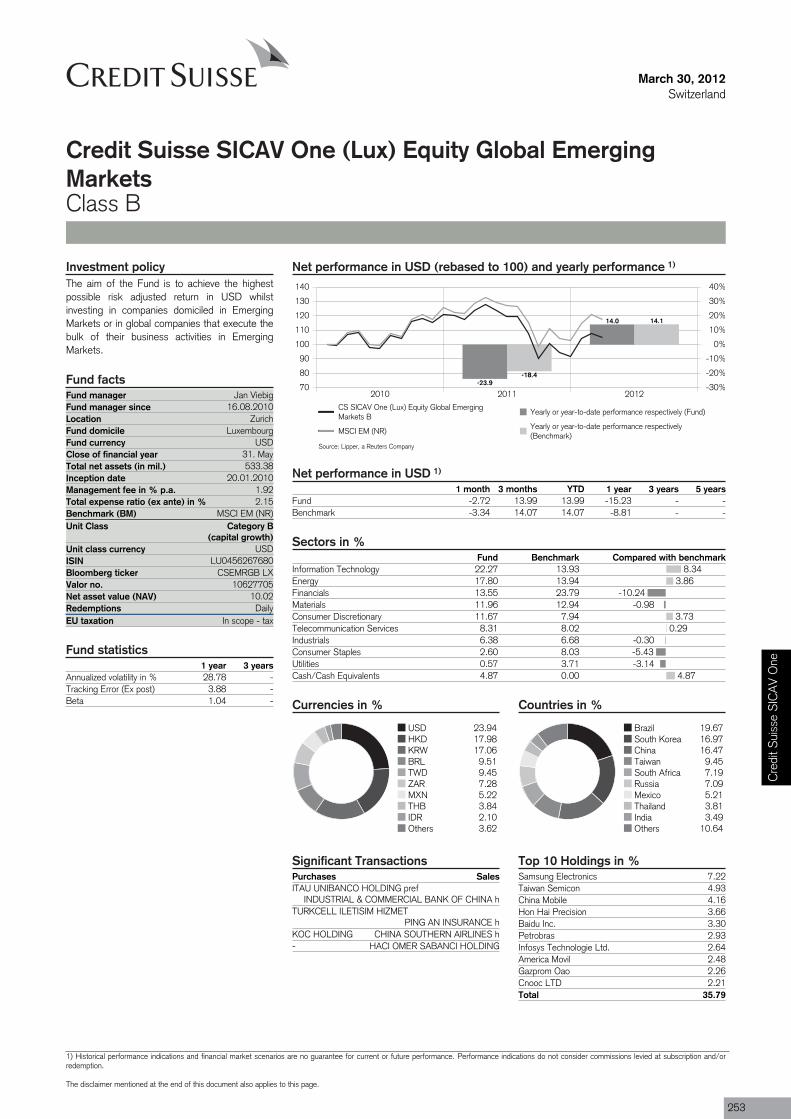

Credit Suisse SICAV One (Lux) Equity Global Emerging Markets B 253

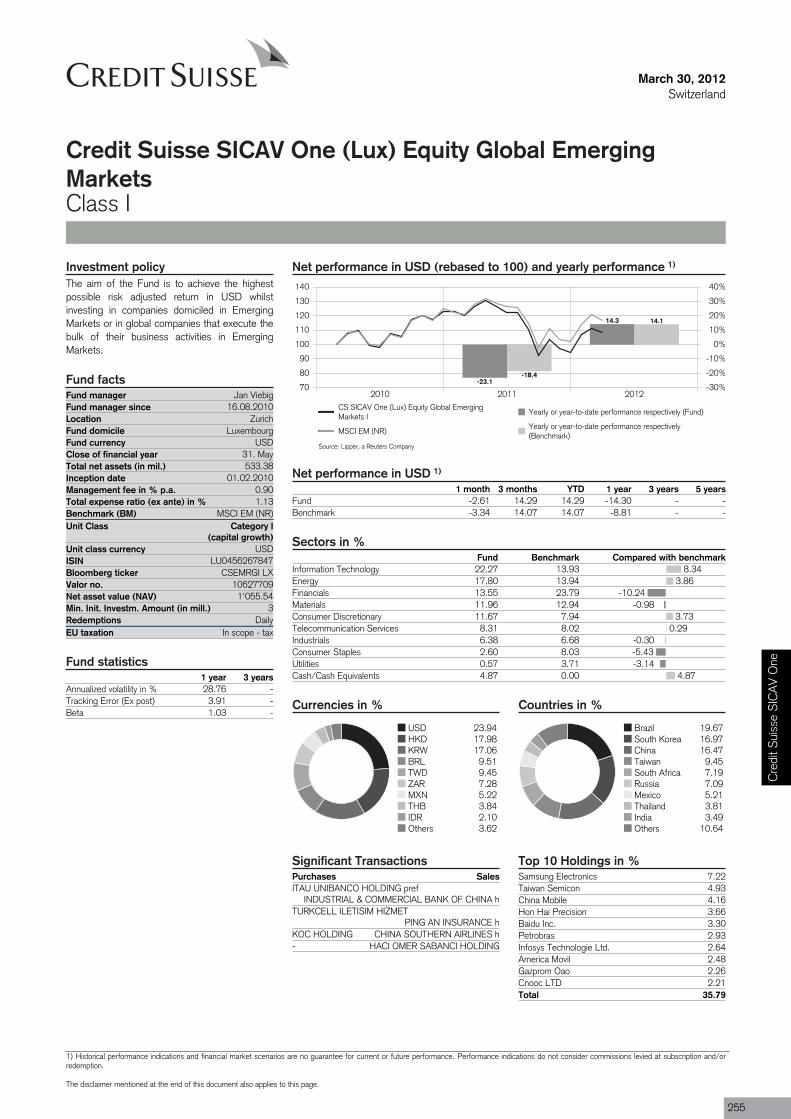

Credit Suisse SICAV One (Lux) Equity Global Emerging Markets I 255

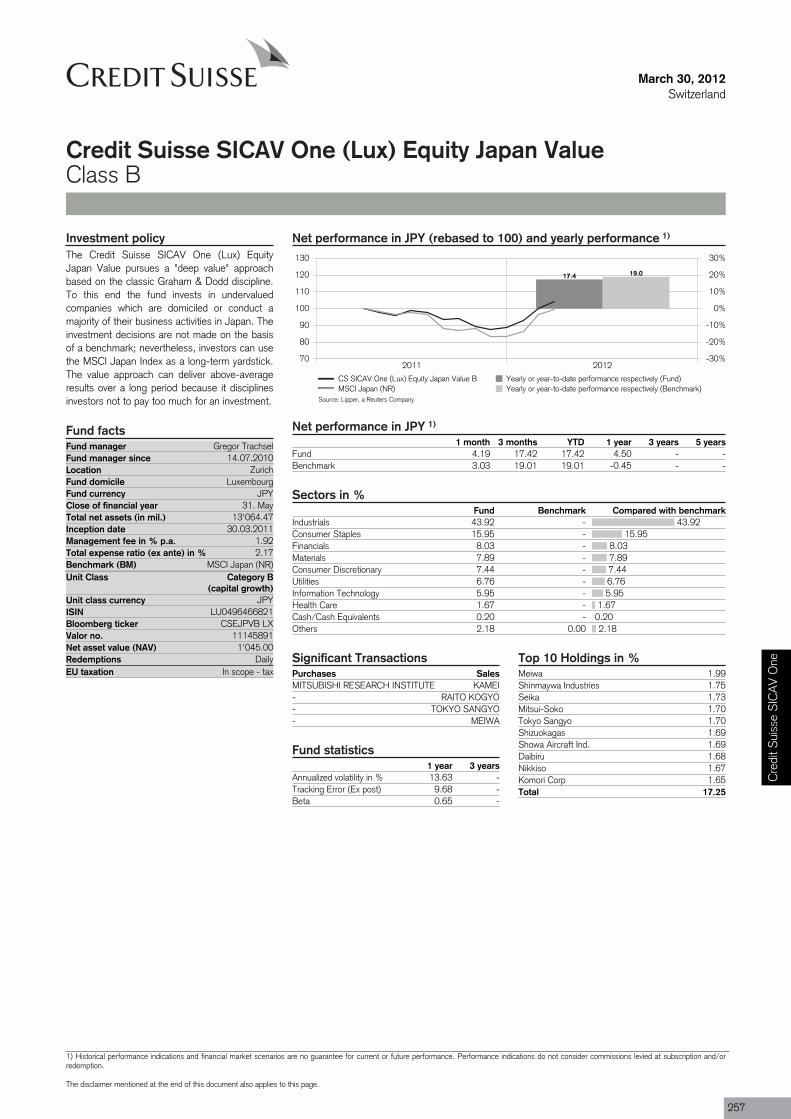

Credit Suisse SICAV One (Lux) Equity Japan Value B 257

Credit Suisse SICAV One (Lux) European Equity Dividend Plus B 259

Credit Suisse SICAV One (Lux) European Equity Dividend Plus I 261

Credit Suisse SICAV One (Lux) European Equity Dividend Plus R CHF 263

Credit Suisse SICAV One (Lux) Global Convertibles B 265

Credit Suisse SICAV One (Lux) Global Convertibles R CHF 267

Credit Suisse SICAV One (Lux) Global Convertibles R EUR 269

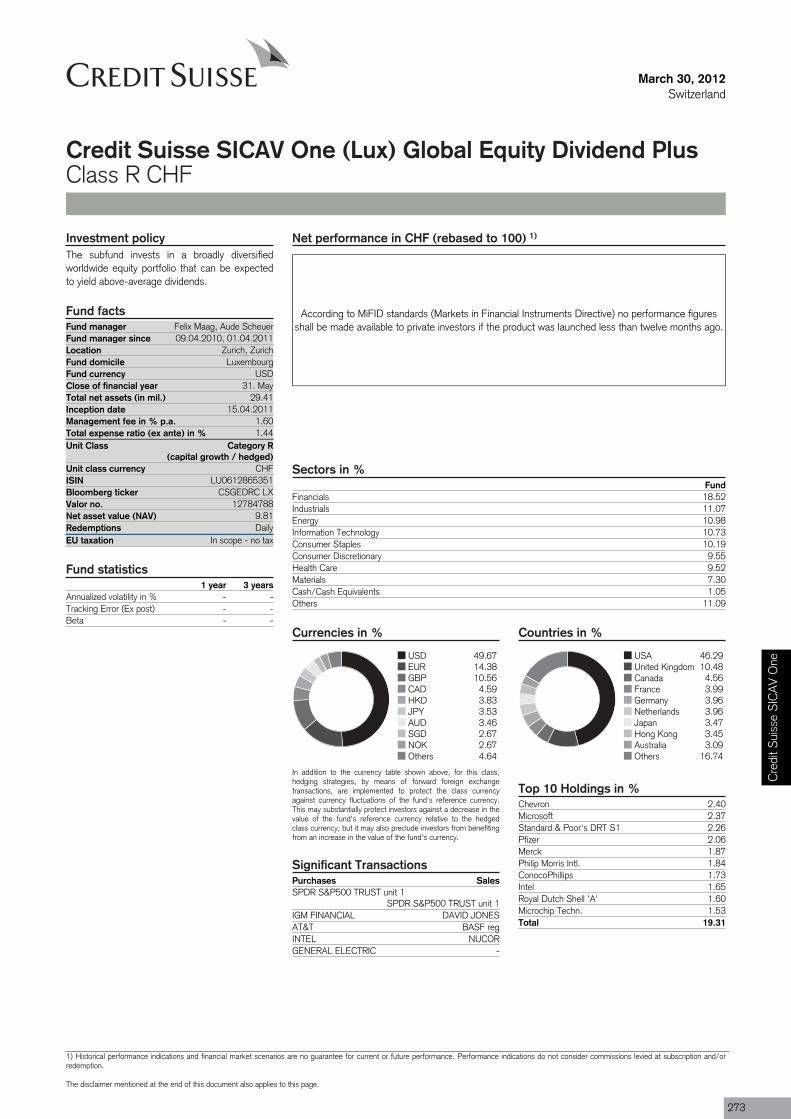

Credit Suisse SICAV One (Lux) Global Equity Dividend Plus B 271

Credit Suisse SICAV One (Lux) Global Equity Dividend Plus R CHF 273

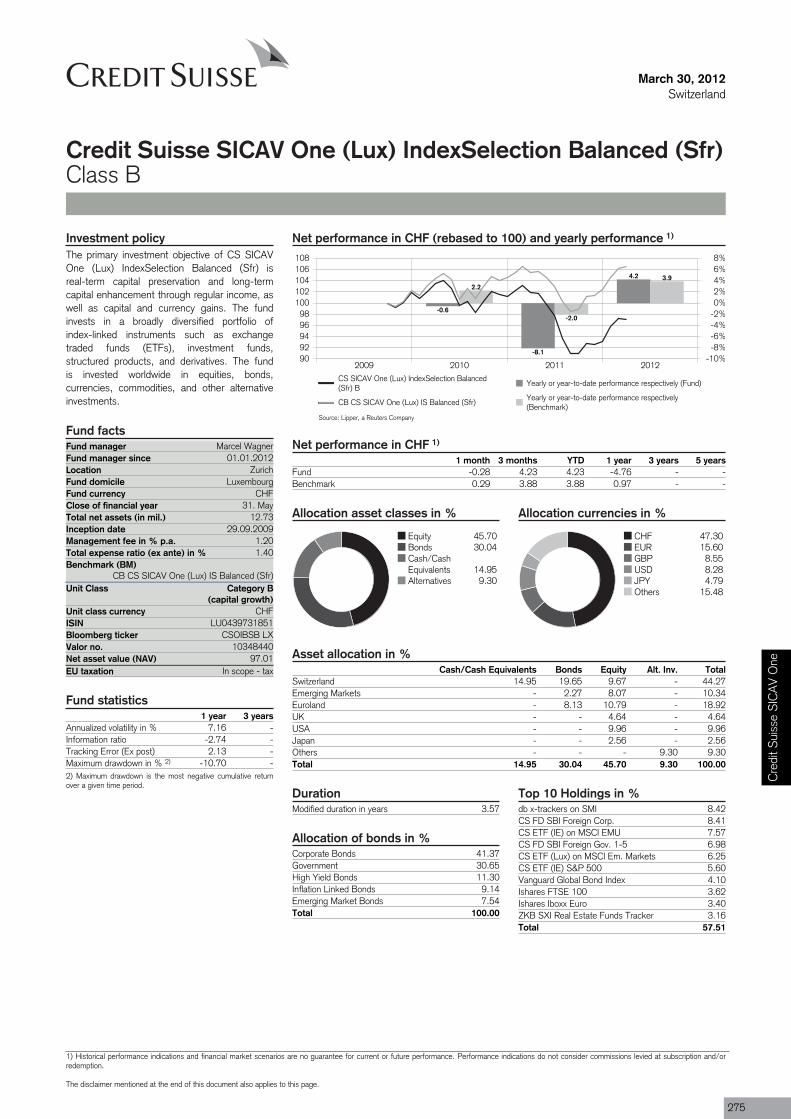

Credit Suisse SICAV One (Lux) IndexSelection Balanced (Sfr) B 275

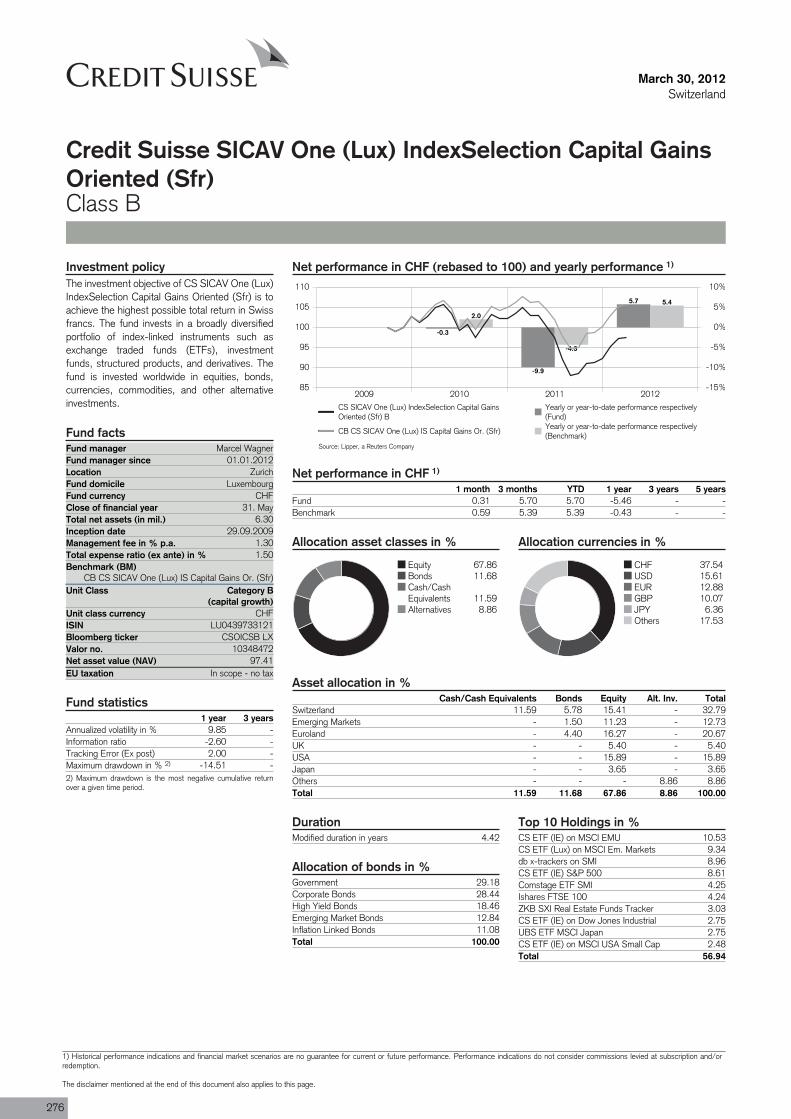

Credit Suisse SICAV One (Lux) IndexSelection Capital Gains Oriented (Sfr) B 276

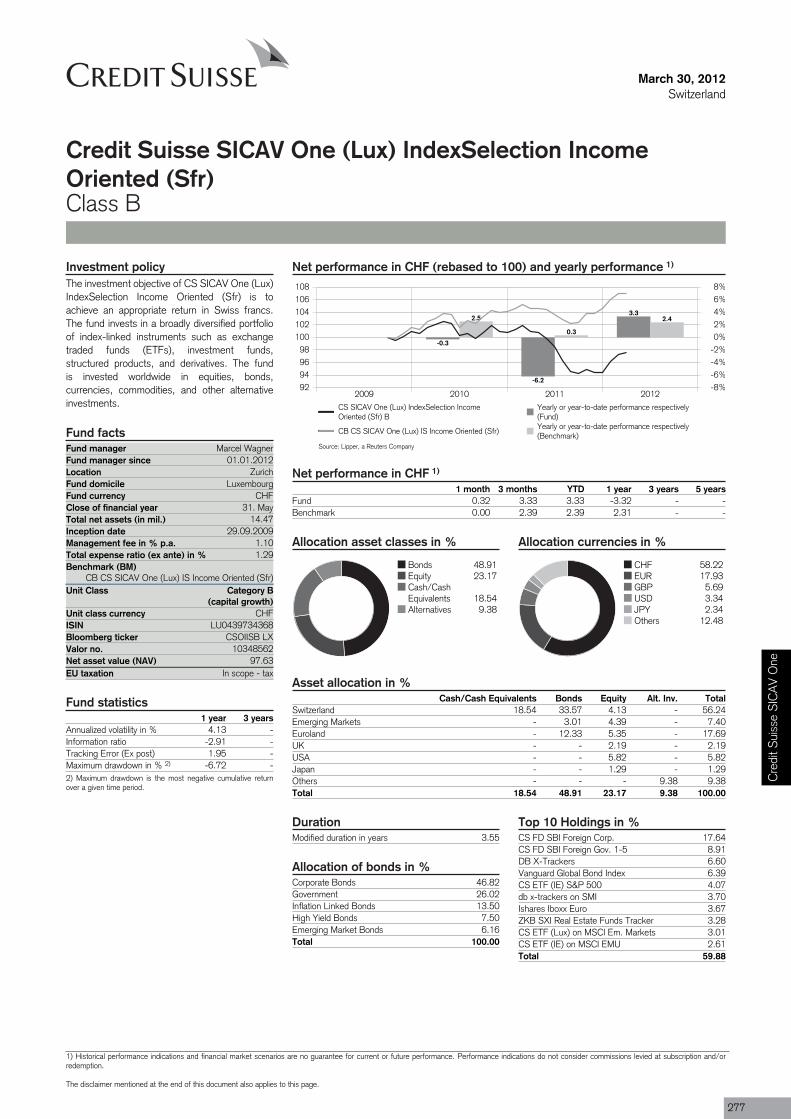

Credit Suisse SICAV One (Lux) IndexSelection Income Oriented (Sfr) B 277

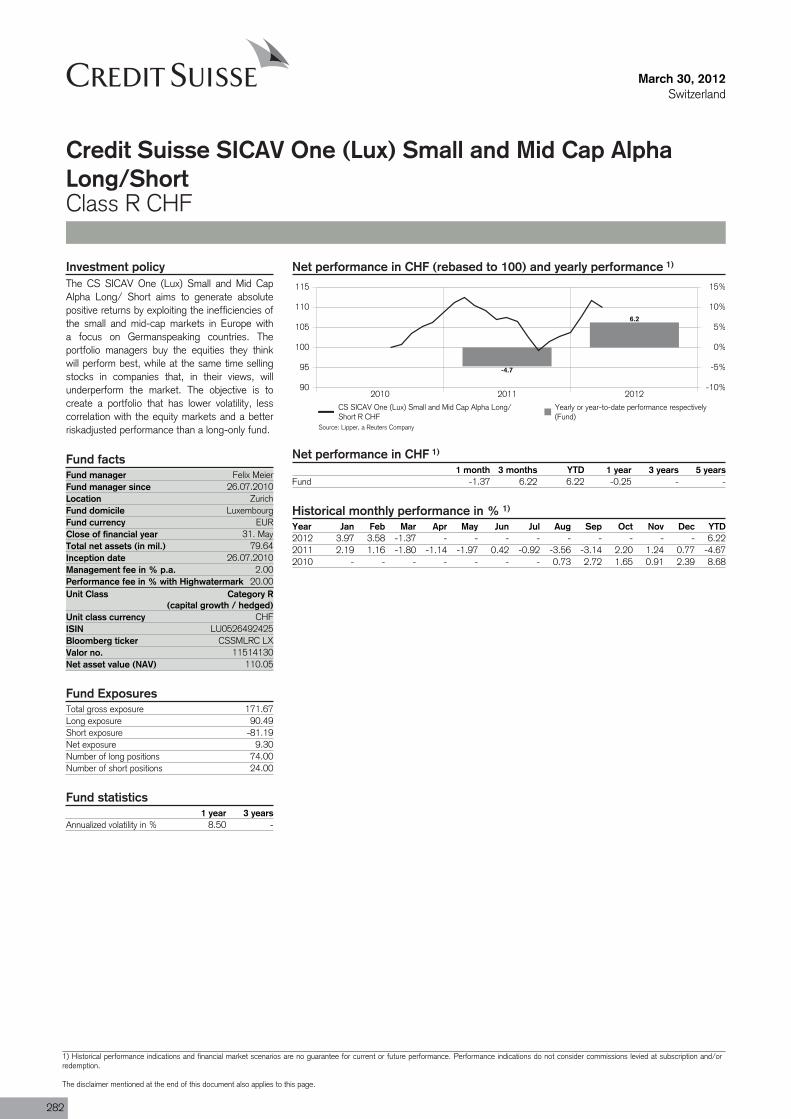

Credit Suisse SICAV One (Lux) Small and Mid Cap Alpha Long/Short B 278

Credit Suisse SICAV One (Lux) Small and Mid Cap Alpha Long/Short I 280

Credit Suisse SICAV One (Lux) Small and Mid Cap Alpha Long/Short R CHF 282

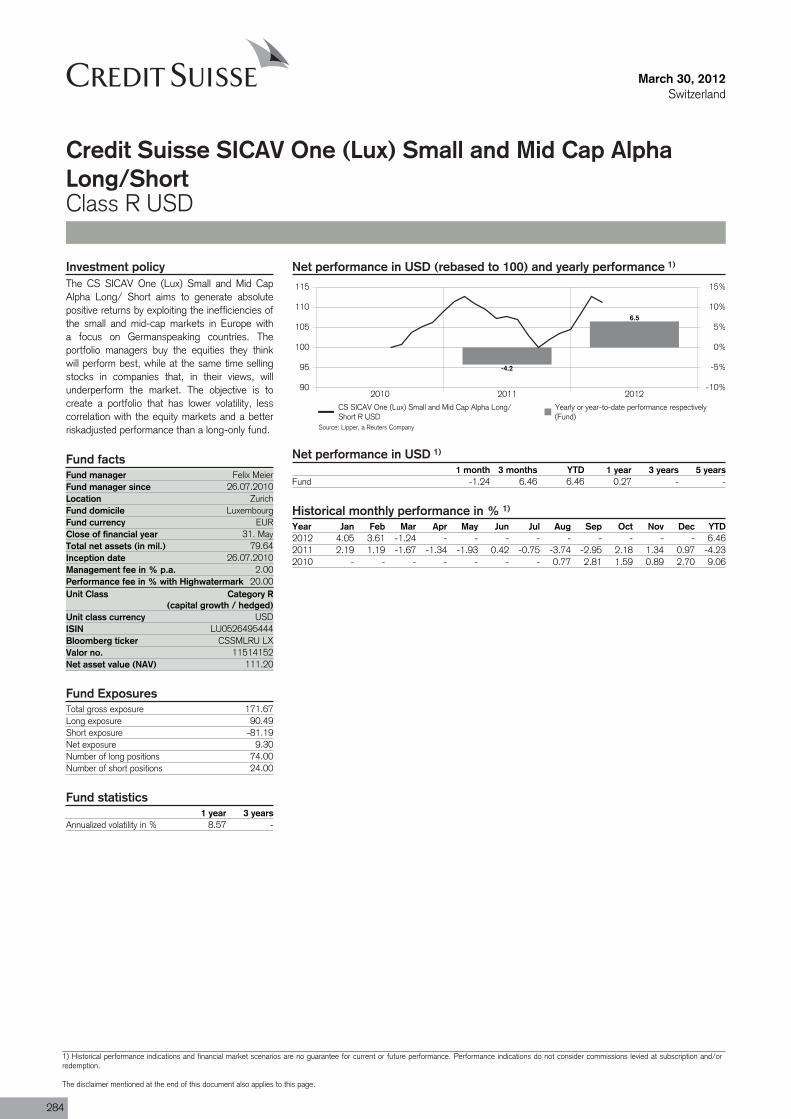

Credit Suisse SICAV One (Lux) Small and Mid Cap Alpha Long/Short R USD 284

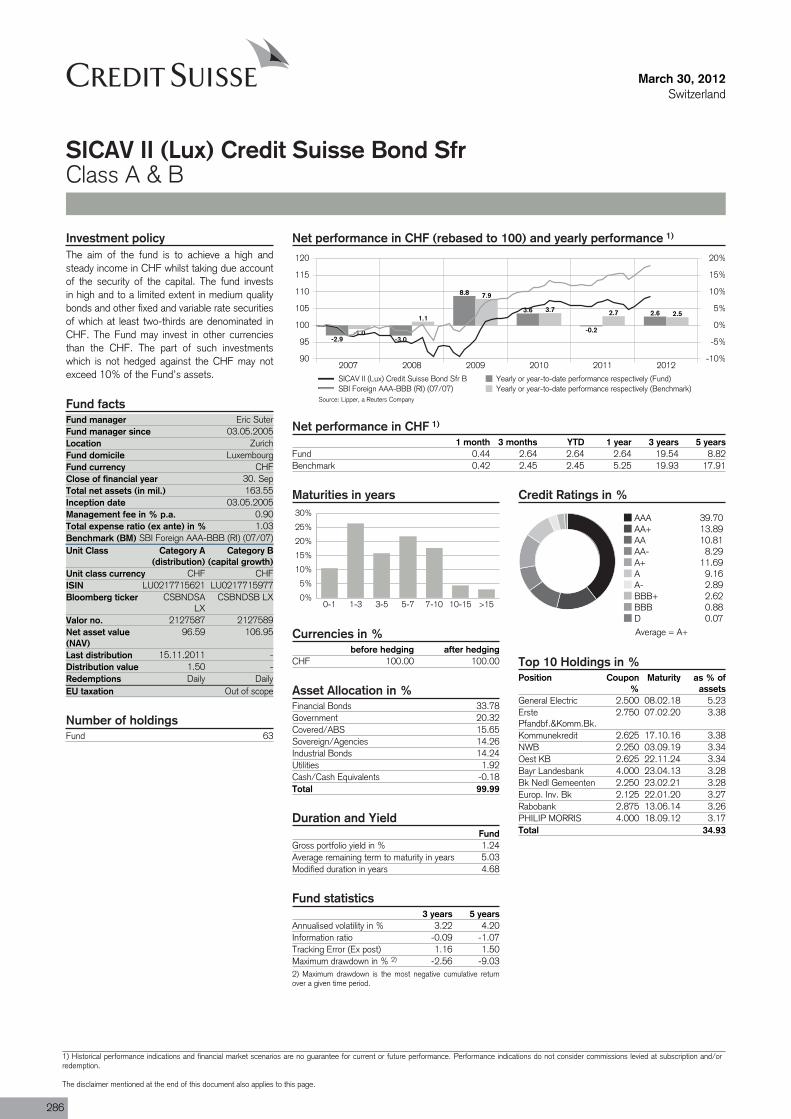

Credit Suisse SICAV IISICAV II (Lux) Credit Suisse Bond Sfr B 286

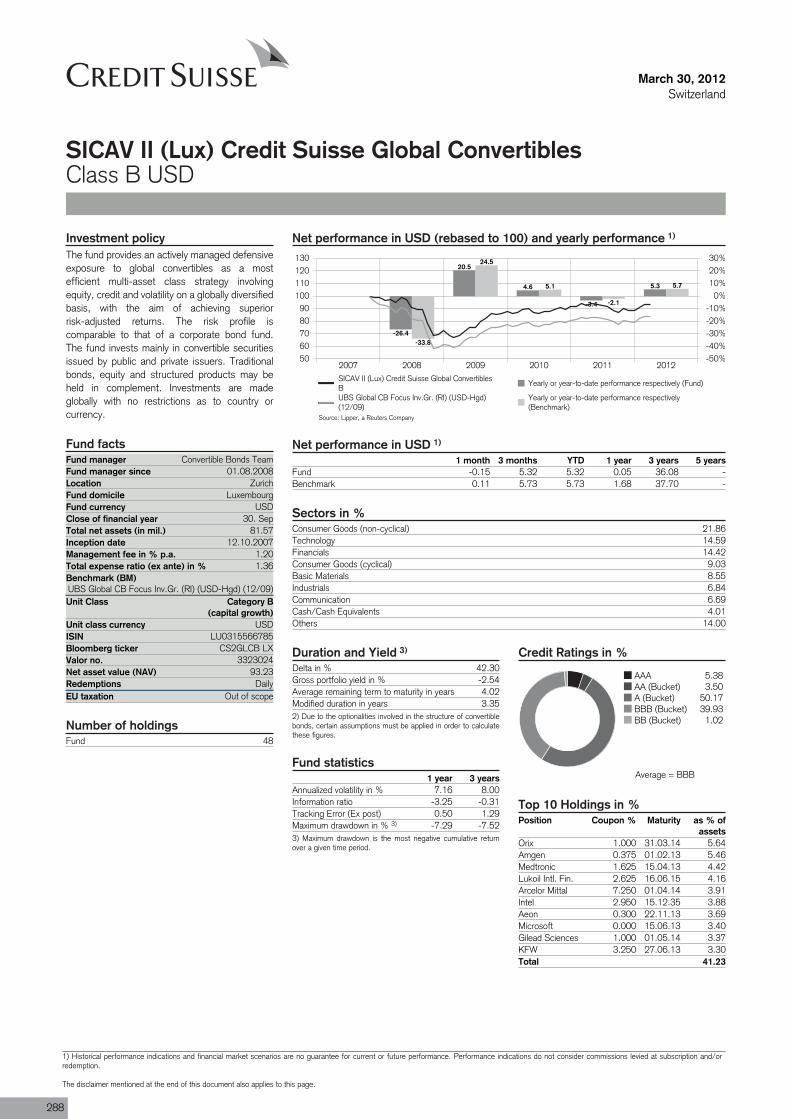

SICAV II (Lux) Credit Suisse Global Convertibles B 288

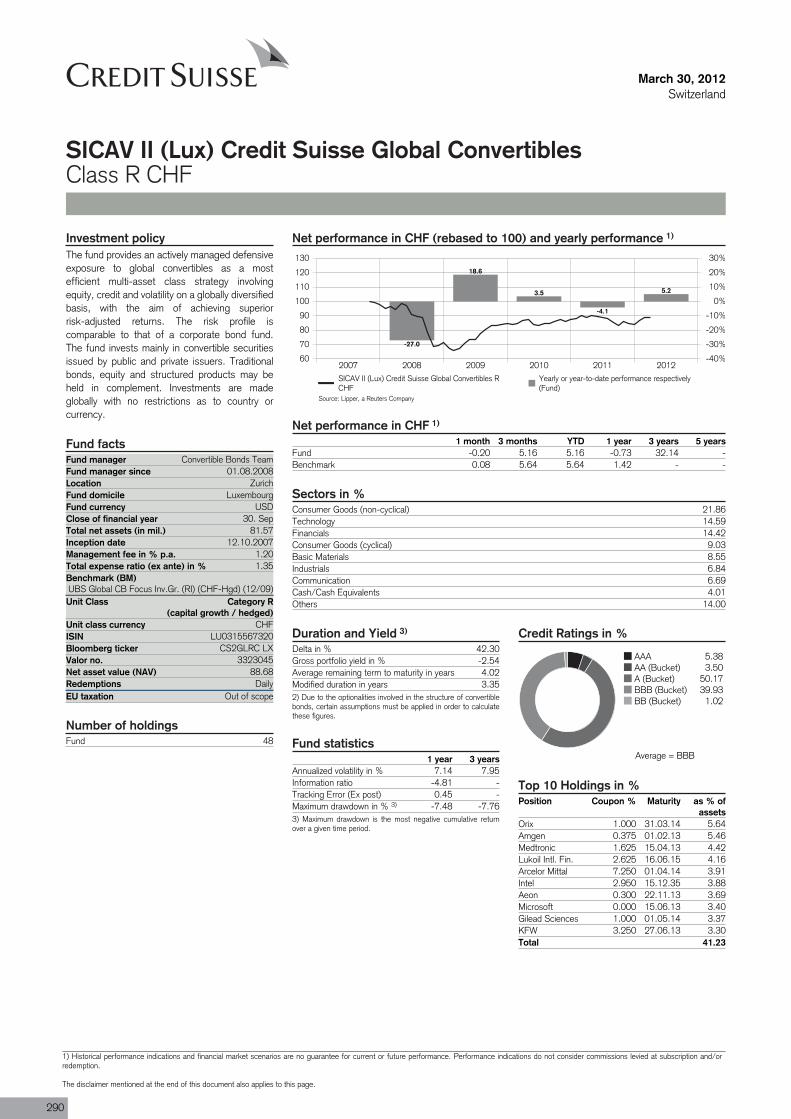

SICAV II (Lux) Credit Suisse Global Convertibles R CHF 290

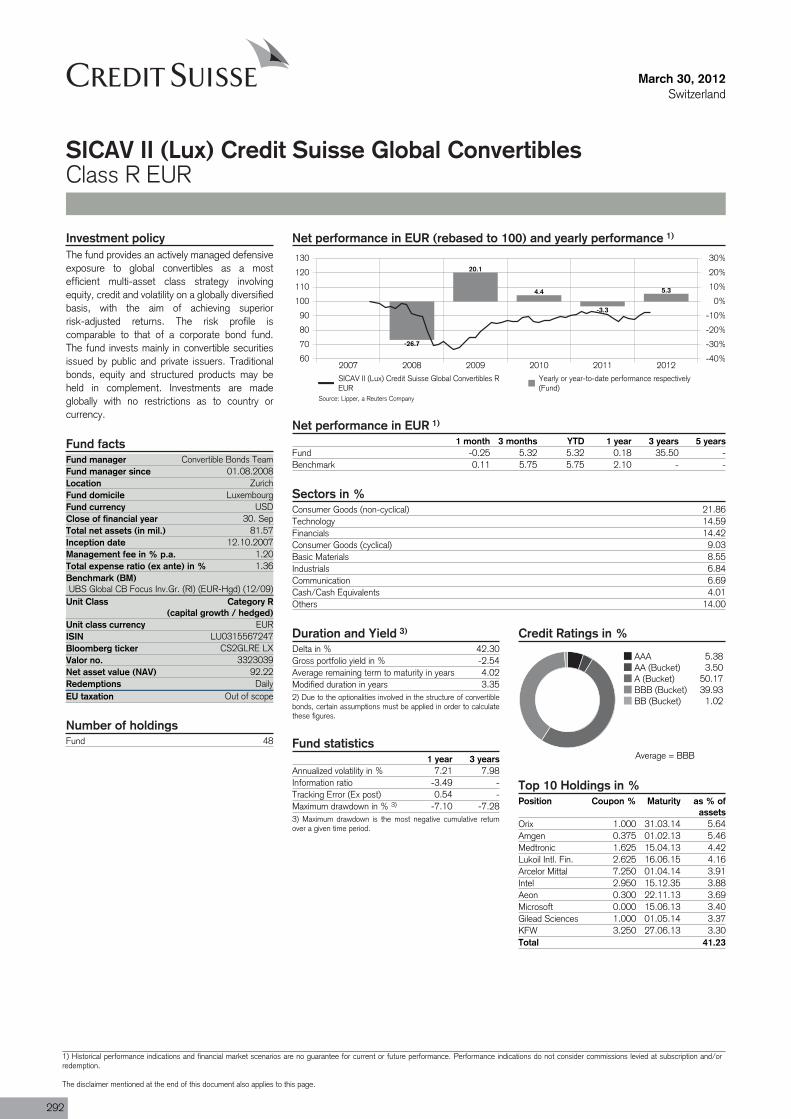

SICAV II (Lux) Credit Suisse Global Convertibles R EUR 292

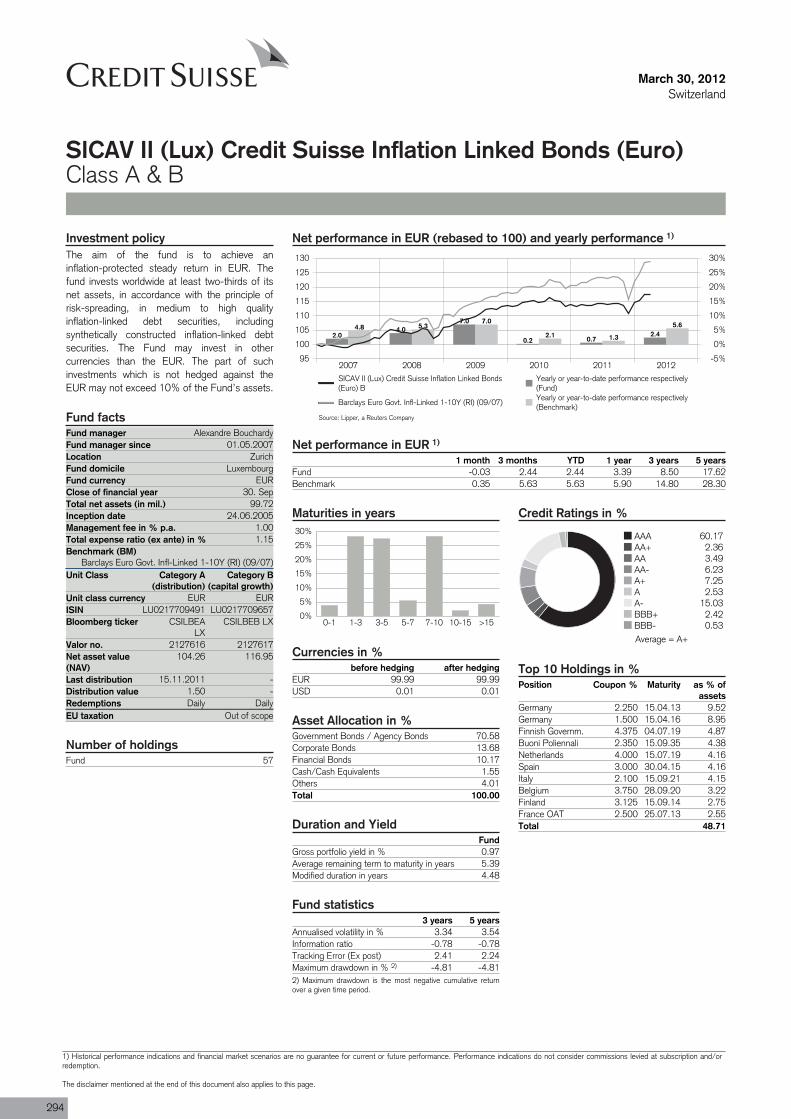

SICAV II (Lux) Credit Suisse Inflation Linked Bonds (Euro) B 294

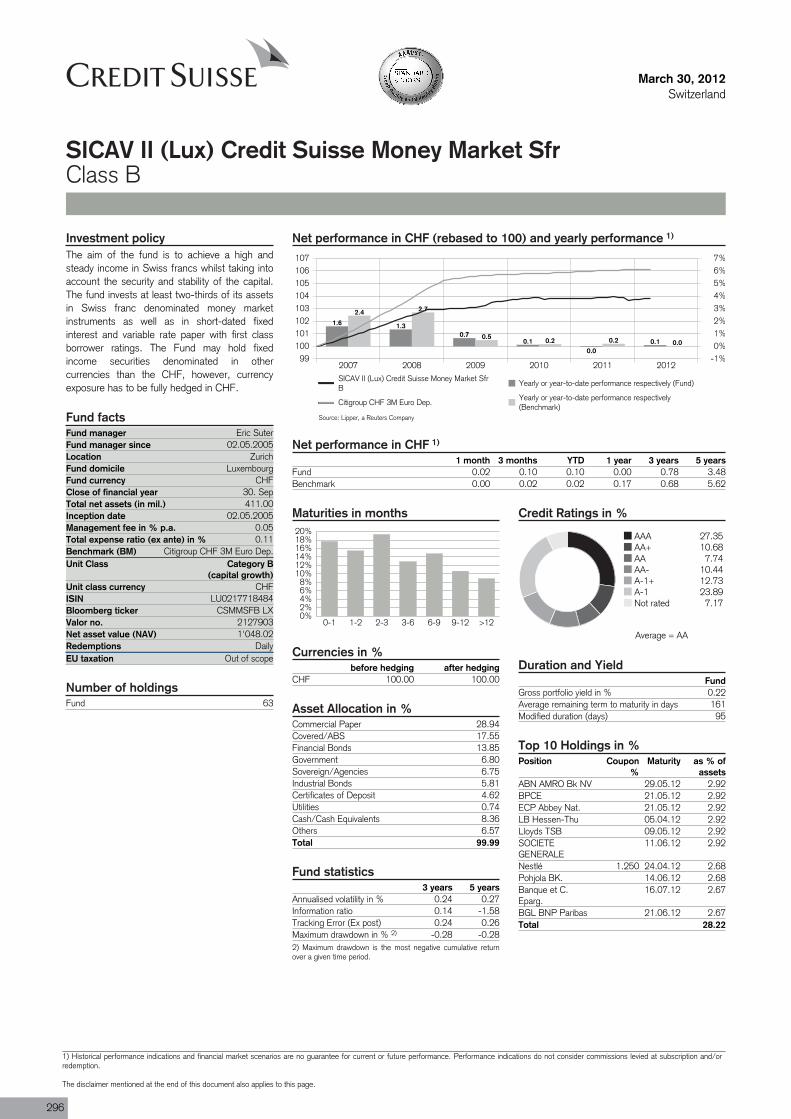

SICAV II (Lux) Credit Suisse Money Market Sfr B 296

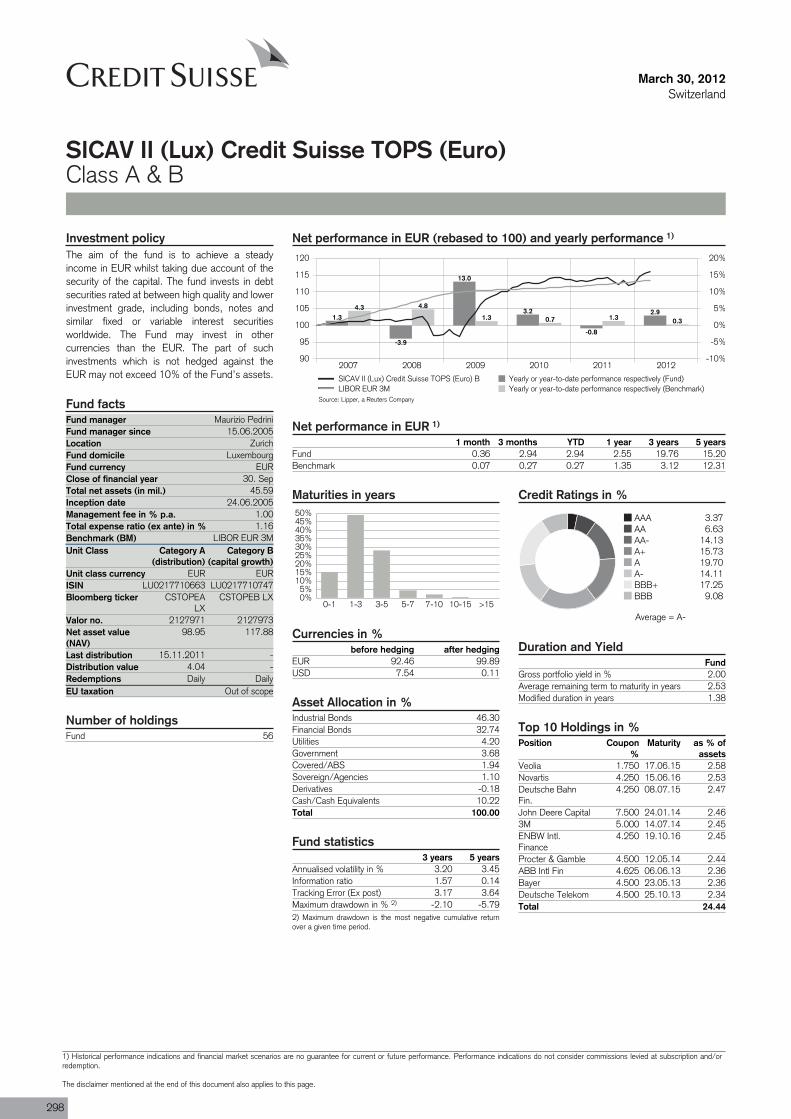

SICAV II (Lux) Credit Suisse TOPS (Euro) B 298

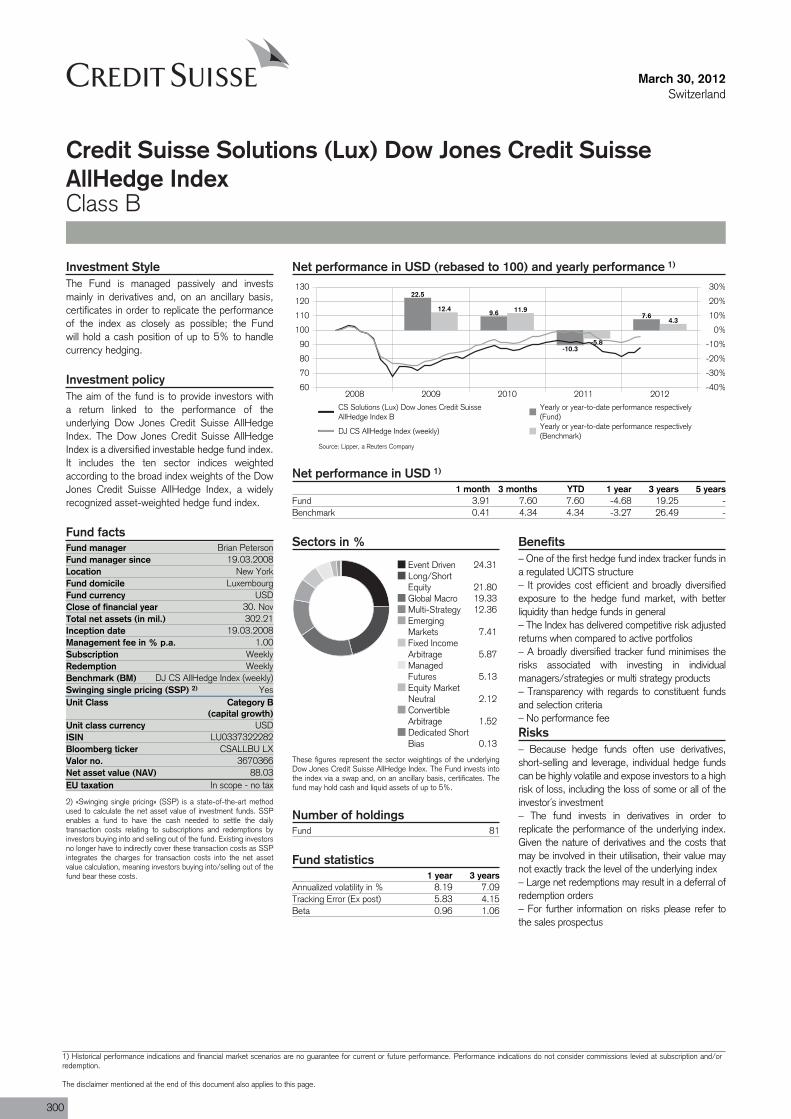

Credit Suisse SolutionsCredit Suisse Solutions (Lux) Dow Jones Credit Suisse AllHedge Index B 300

Credit Suisse Solutions (Lux) Dow Jones Credit Suisse AllHedge Index I 301

Credit Suisse Solutions (Lux) Dow Jones Credit Suisse AllHedge Index R CHF 302

Credit Suisse Solutions (Lux) Dow Jones Credit Suisse AllHedge Index R EUR 303

Credit Suisse Solutions (Lux) Megatrends B 304

Credit Suisse Solutions (Lux) Megatrends I 306

Credit Suisse Solutions (Lux) Megatrends R CHF 308

Credit Suisse Solutions (Lux) Megatrends R EUR 310

Credit Suisse Solutions (Lux) Megatrends R GBP 312

Credit Suisse Solutions (Lux) Prima Multi-Strategy B EUR 314

Credit Suisse Solutions (Lux) Prima Multi-Strategy I EUR 315

Credit Suisse Solutions (Lux) Prima Multi-Strategy R CHF 316

Credit Suisse Solutions (Lux) Prima Multi-Strategy R GBP 317

Credit Suisse Solutions (Lux) Prima Multi-Strategy R USD 318

Credit Suisse TriamantCredit Suisse Triamant Balanced CHF 319

ContentsFunds distributed in Switzerland

4

Credit Suisse Triamant Balanced EUR 320

Credit Suisse Triamant Capital Gains Oriented CHF 321

Credit Suisse Triamant Capital Gains Oriented EUR 322

Credit Suisse Triamant Income Oriented CHF 323

Credit Suisse Triamant Income Oriented EUR 324

CS ETFCS ETF (CH) on Swiss Bond Index Domestic Government 1-3 325

CS ETF (CH) on Swiss Bond Index Domestic Government 3-7 326

CS ETF (CH) on Swiss Bond Index Domestic Government 7-15 327

CS ETF (CH) on SLI® 328

CS ETF (CH) on SMI® 329

CS ETF (CH) on SMIM® 330

CS ETF (IE) on Credit Suisse Global Alternative Energy 331

CS ETF (IE) on CSI 300 332

CS ETF (IE) on Dow Jones Industrial Average 333

CS ETF (IE) on EONIA 334

CS ETF (IE) on EURO STOXX 50® 335

CS ETF (IE) on Fed Funds Effective Rate 336

CS ETF (IE) on FTSE 100 337

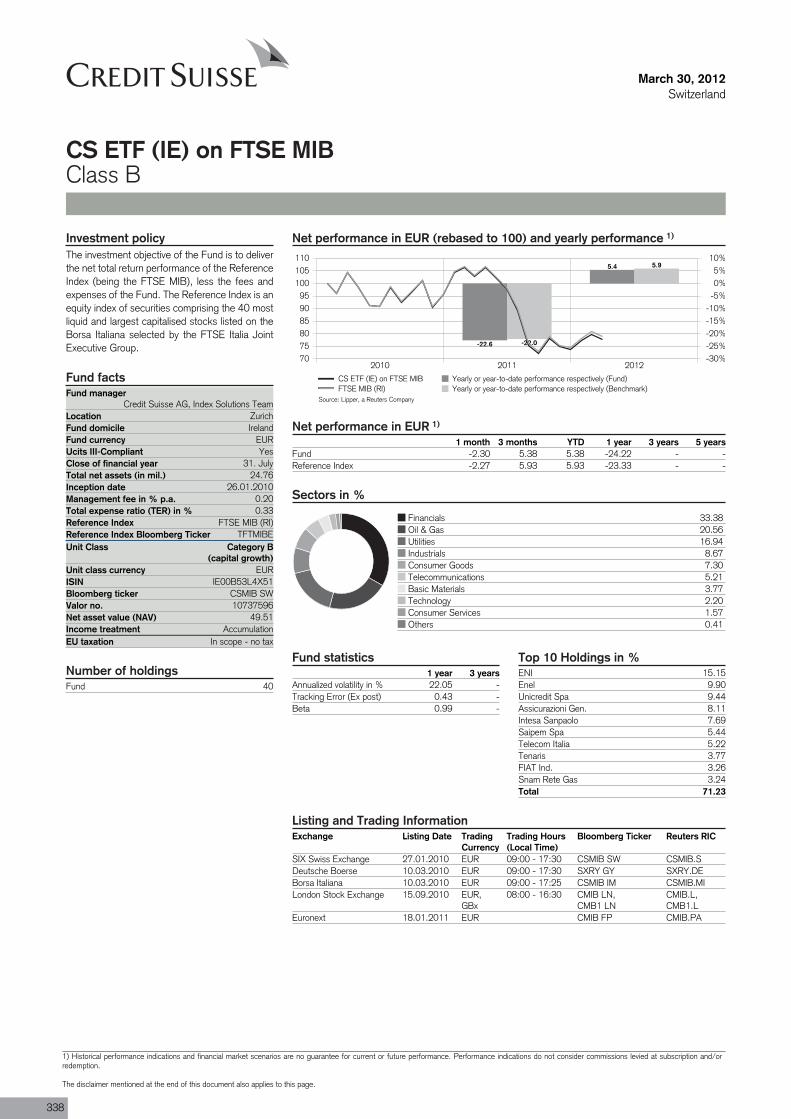

CS ETF (IE) on FTSE MIB 338

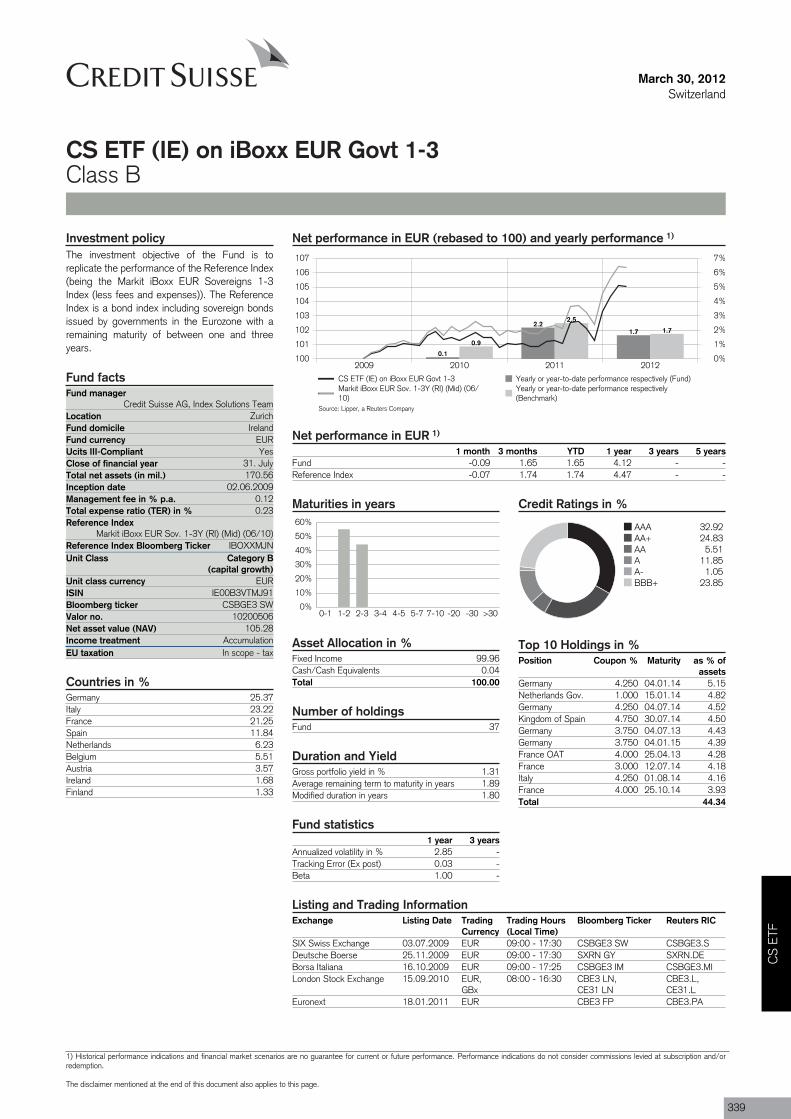

CS ETF (IE) on iBoxx EUR Govt 1-3 339

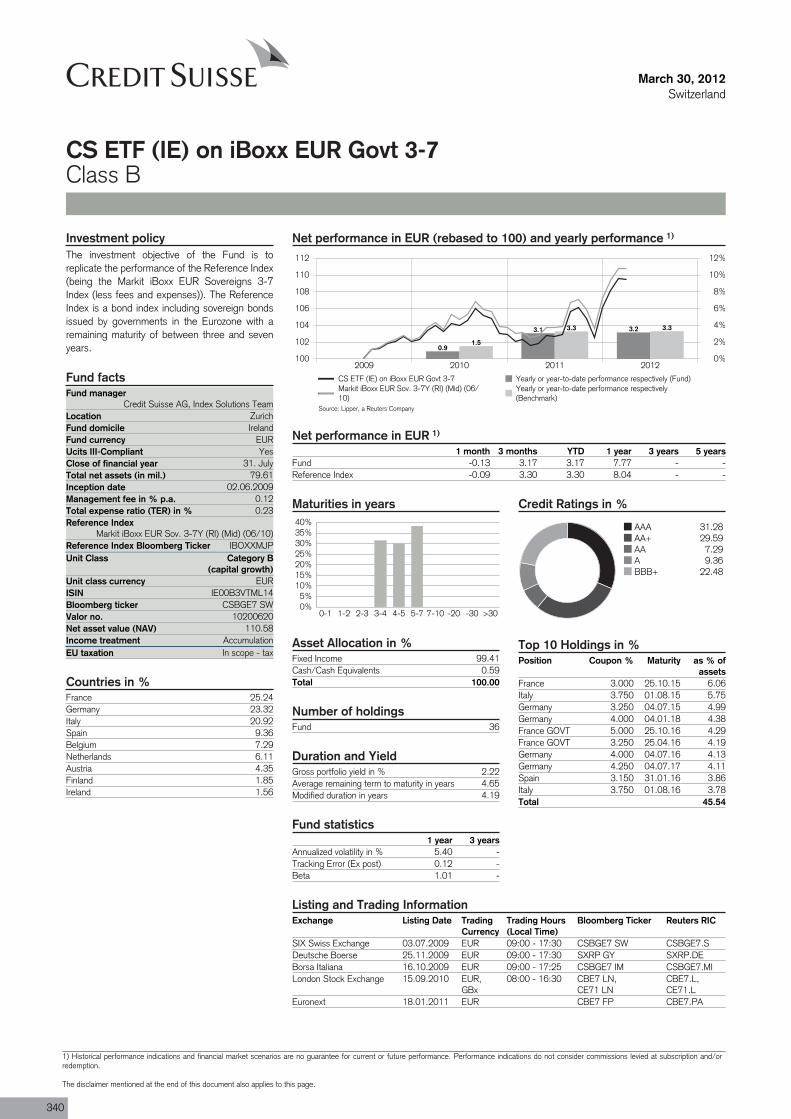

CS ETF (IE) on iBoxx EUR Govt 3-7 340

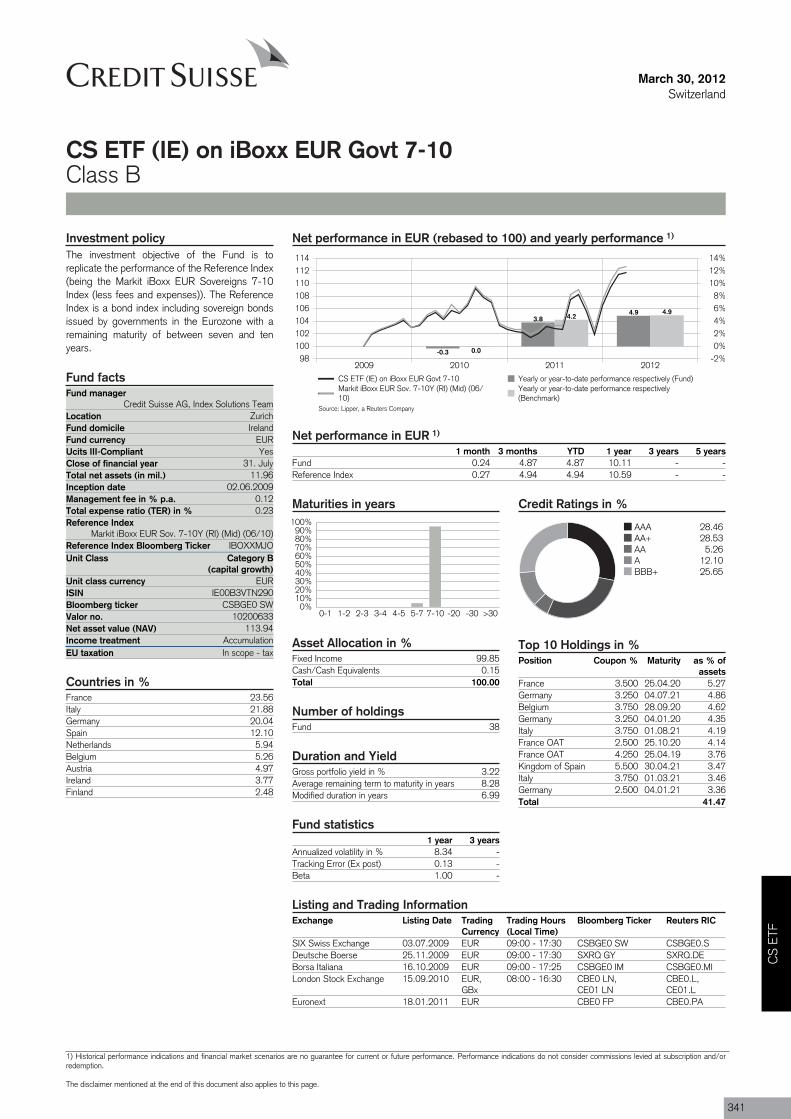

CS ETF (IE) on iBoxx EUR Govt 7-10 341

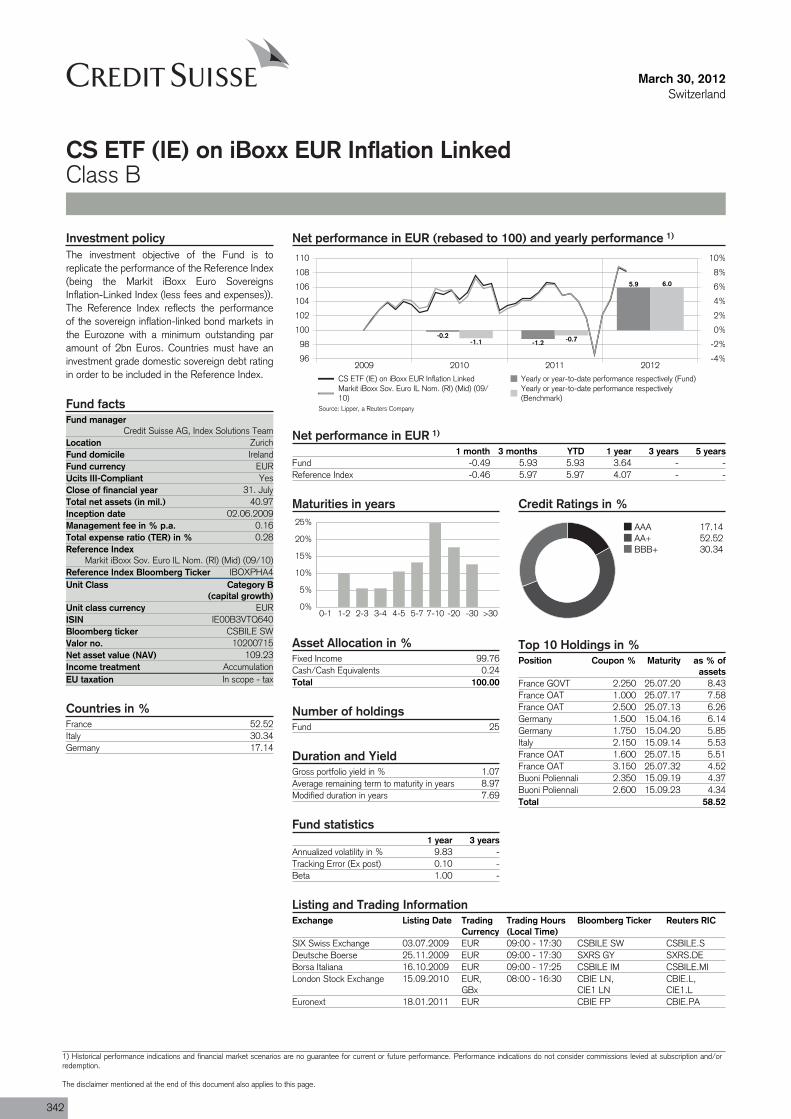

CS ETF (IE) on iBoxx EUR Inflation Linked 342

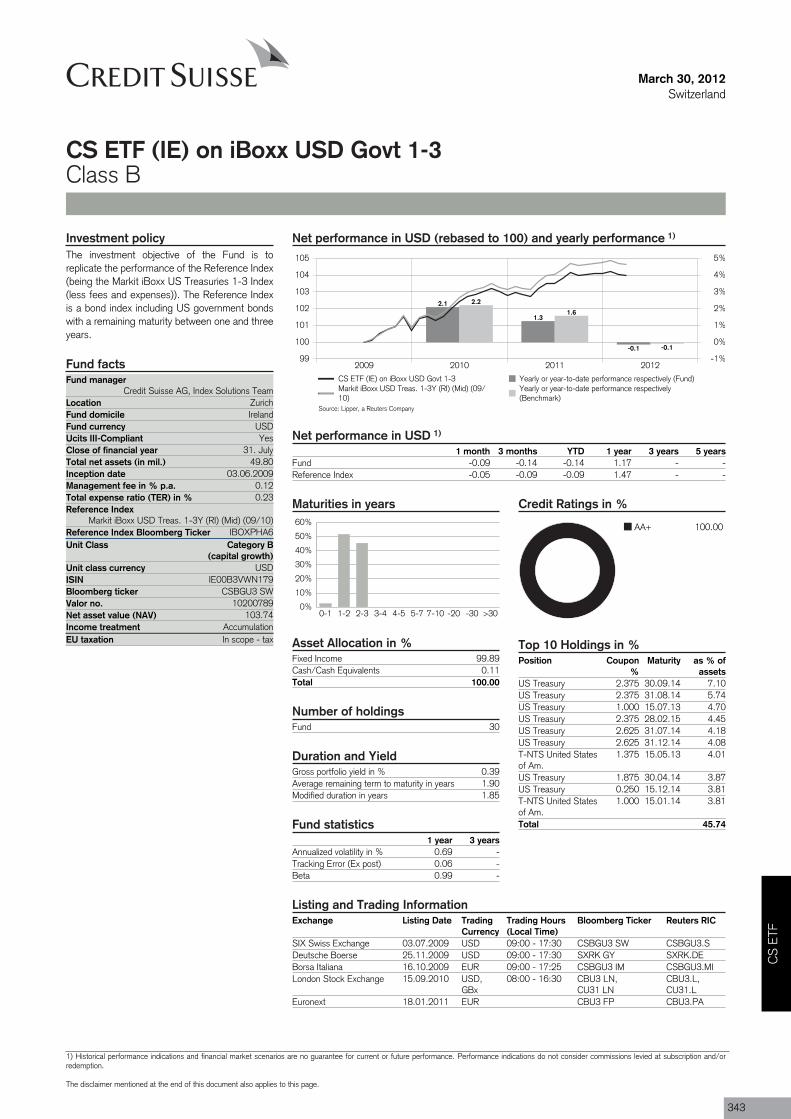

CS ETF (IE) on iBoxx USD Govt 1-3 343

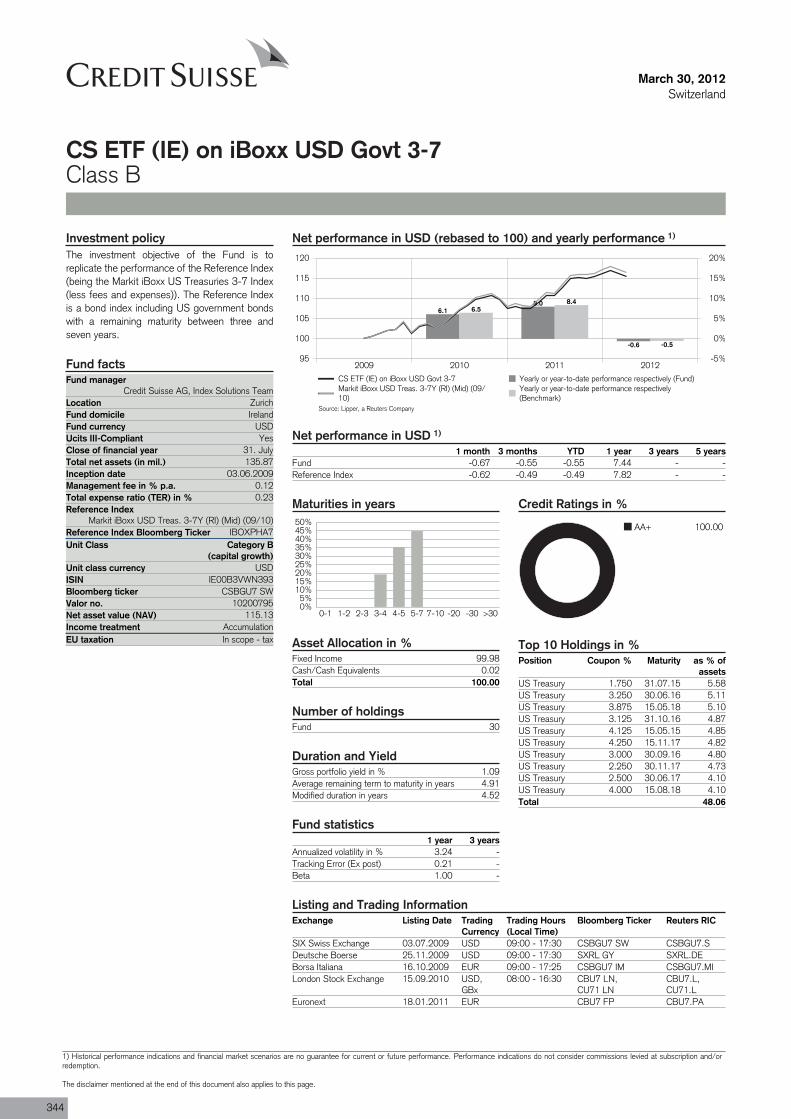

CS ETF (IE) on iBoxx USD Govt 3-7 344

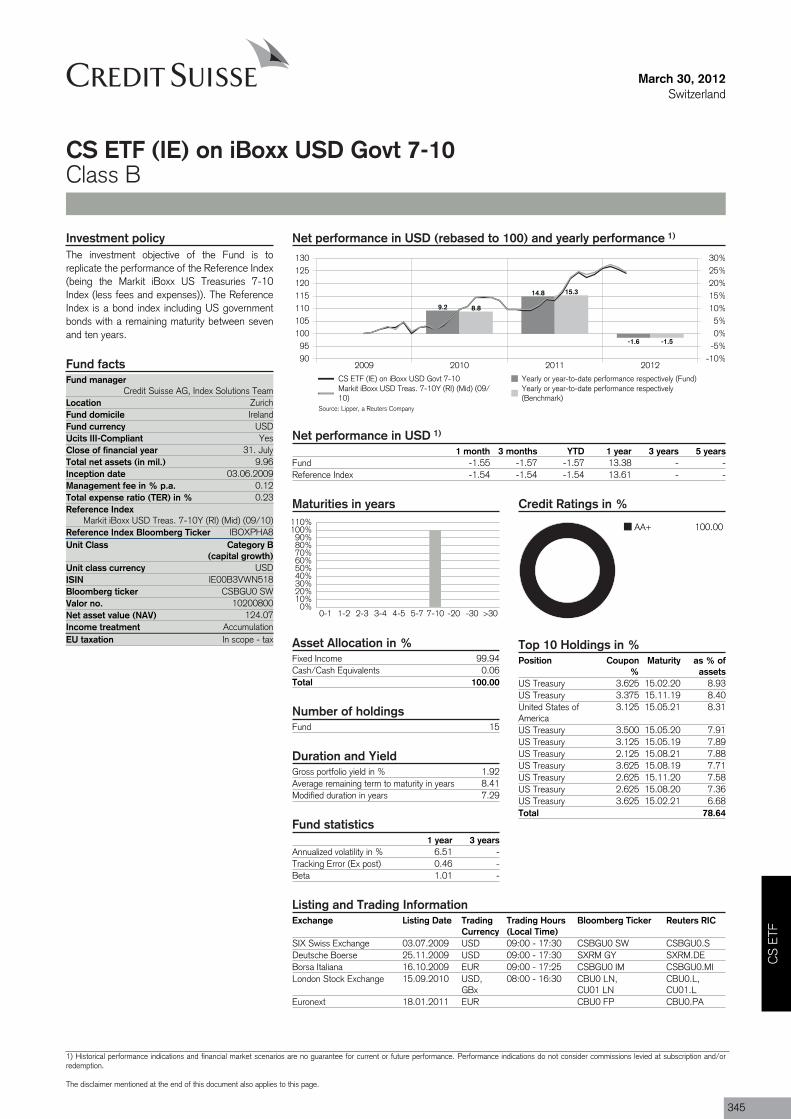

CS ETF (IE) on iBoxx USD Govt 7-10 345

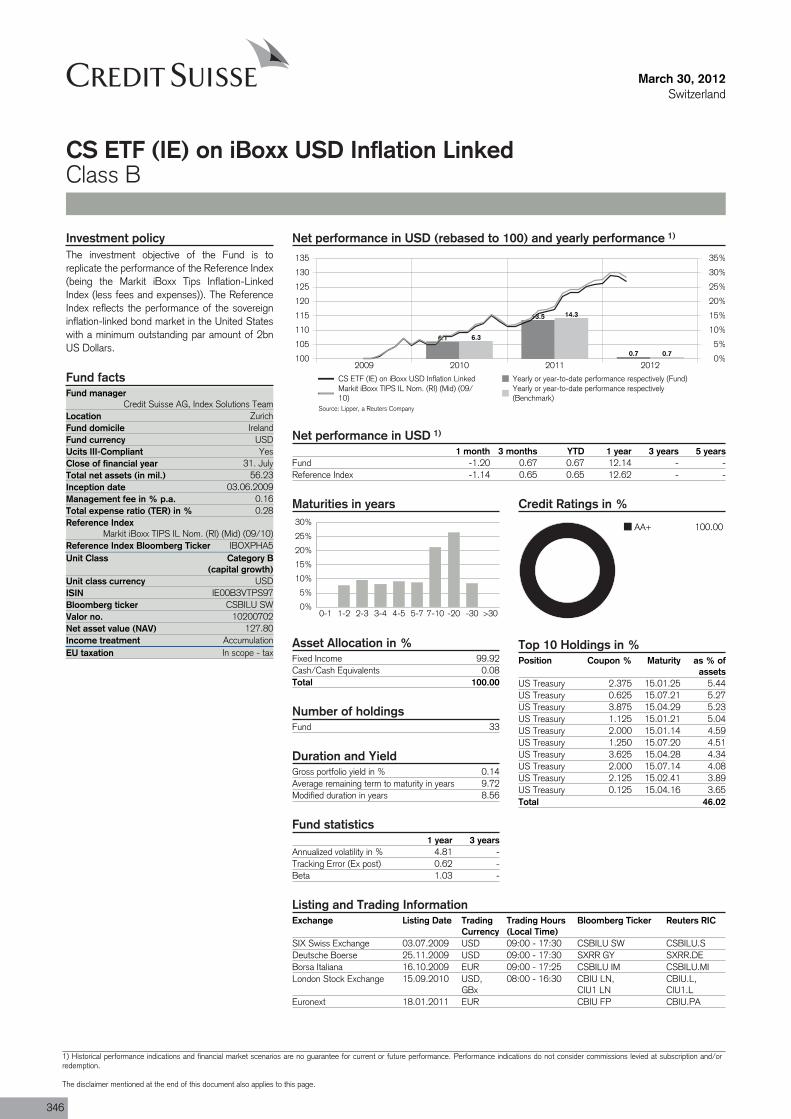

CS ETF (IE) on iBoxx USD Inflation Linked 346

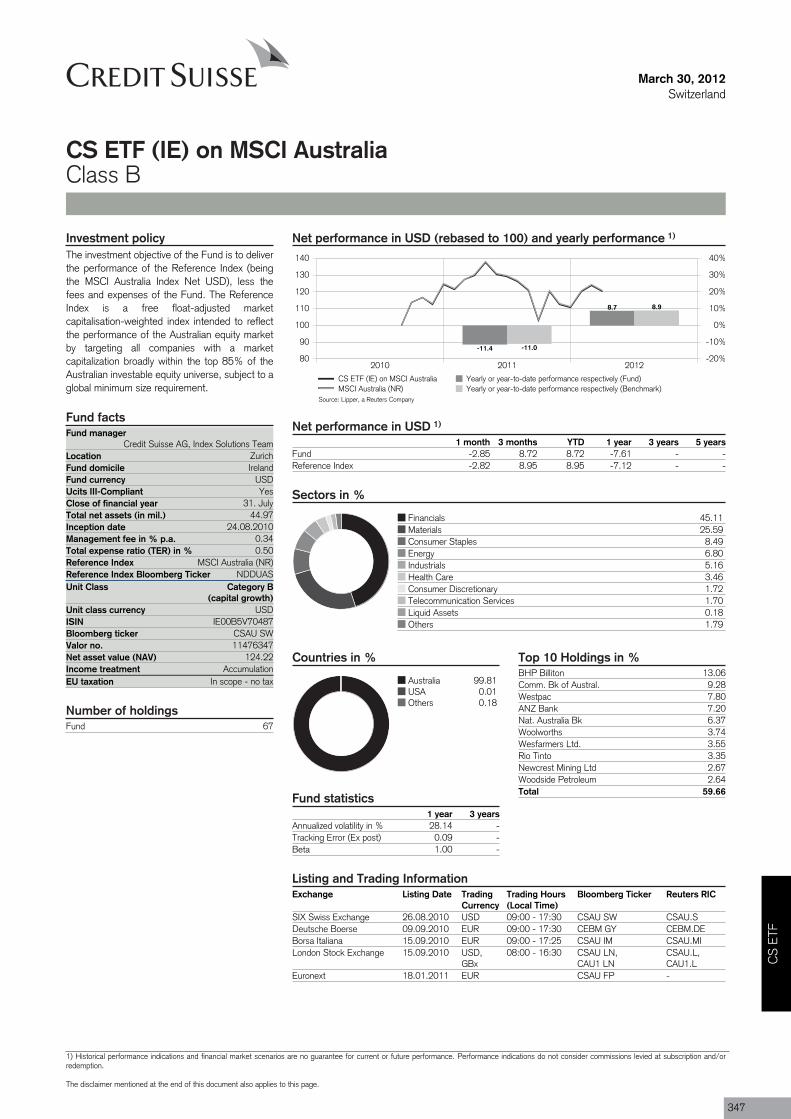

CS ETF (IE) on MSCI Australia 347

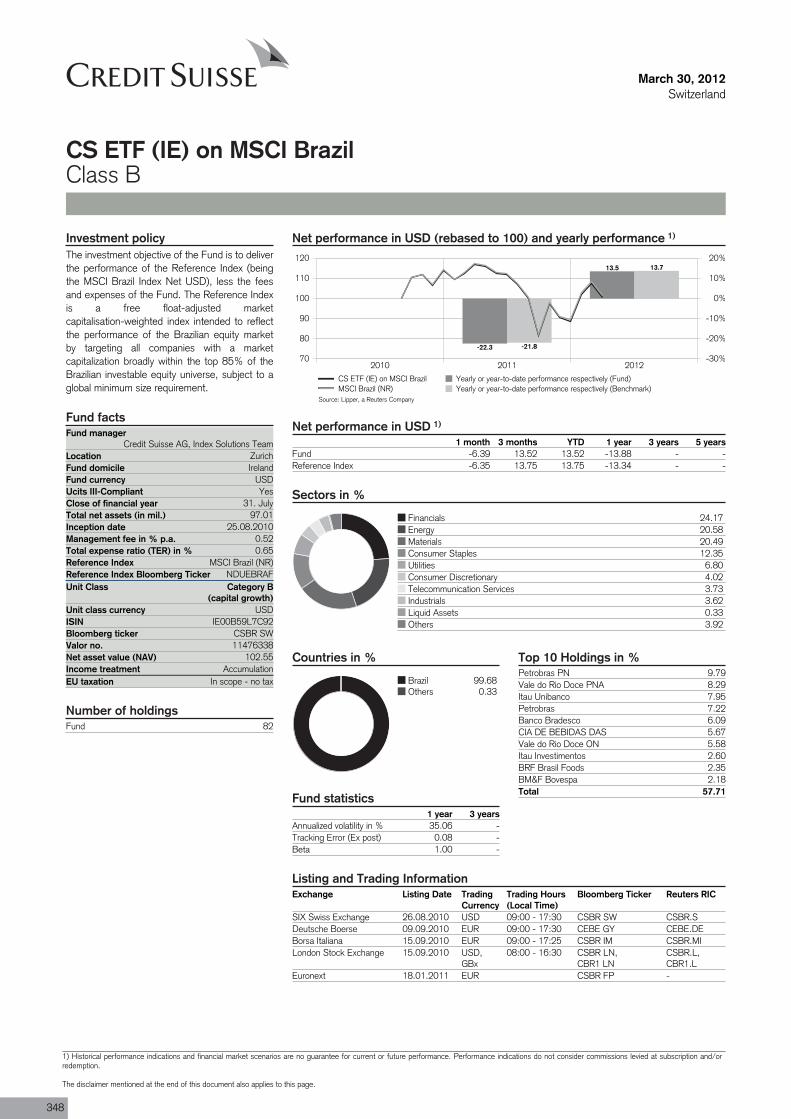

CS ETF (IE) on MSCI Brazil 348

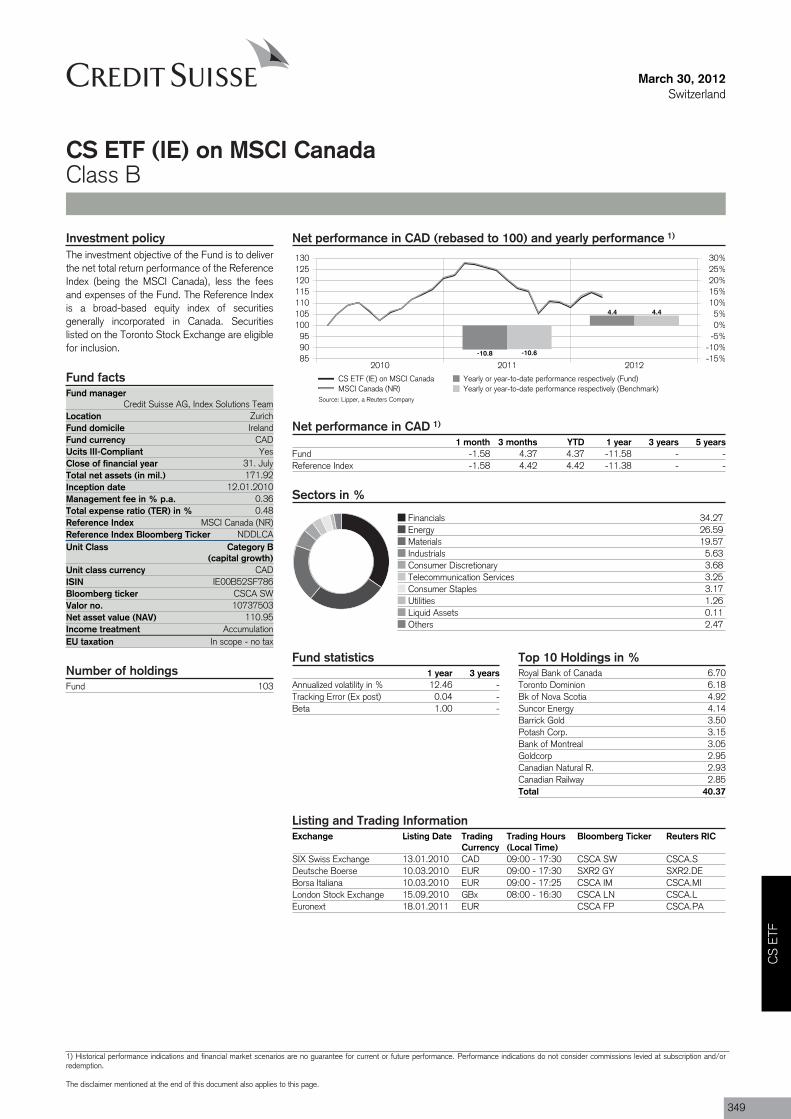

CS ETF (IE) on MSCI Canada 349

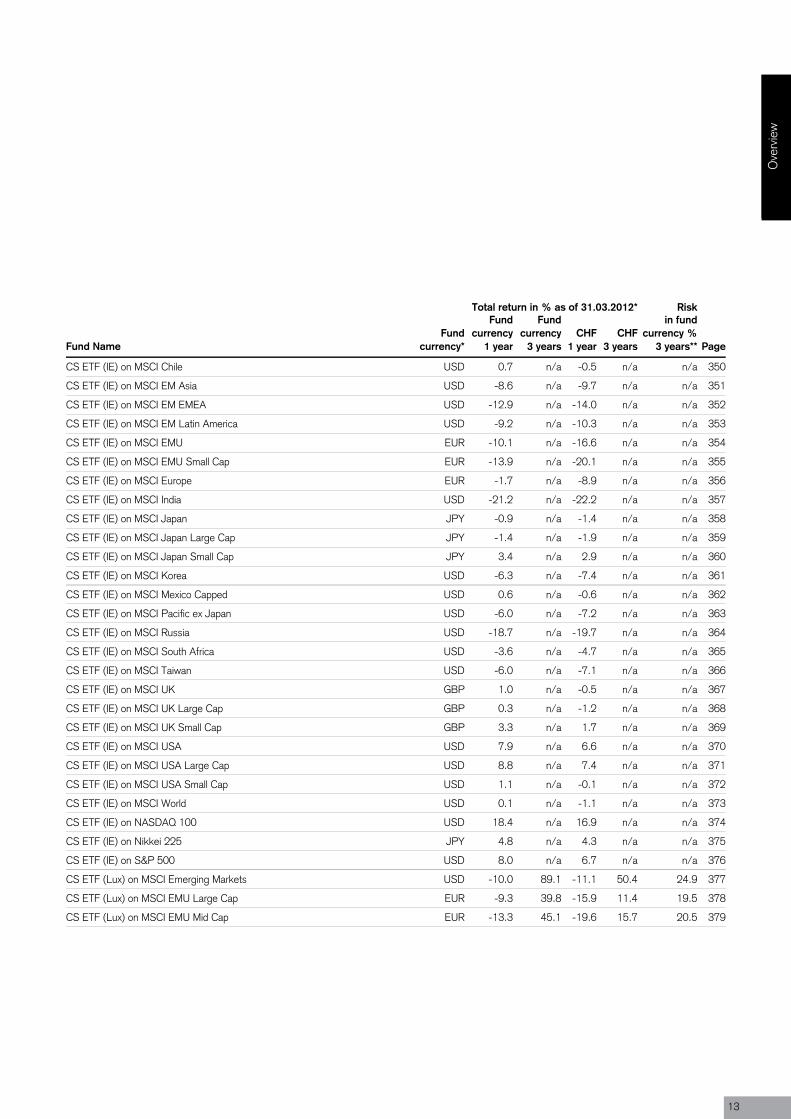

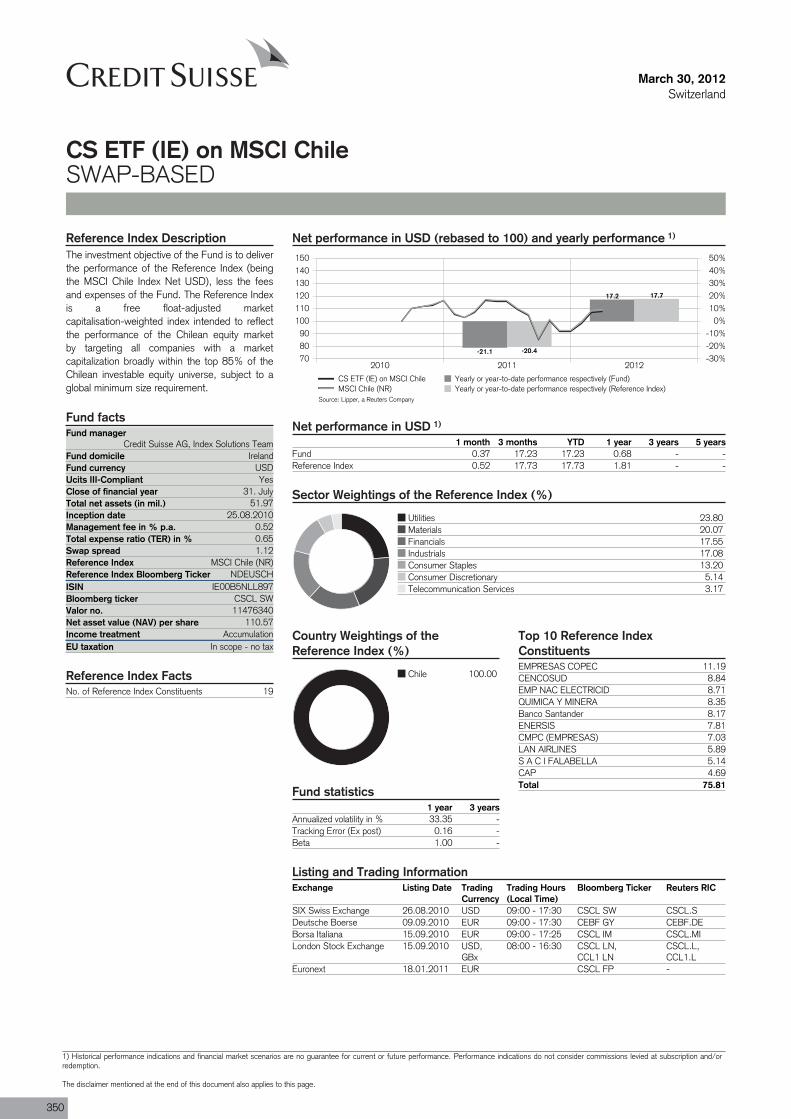

CS ETF (IE) on MSCI Chile 350

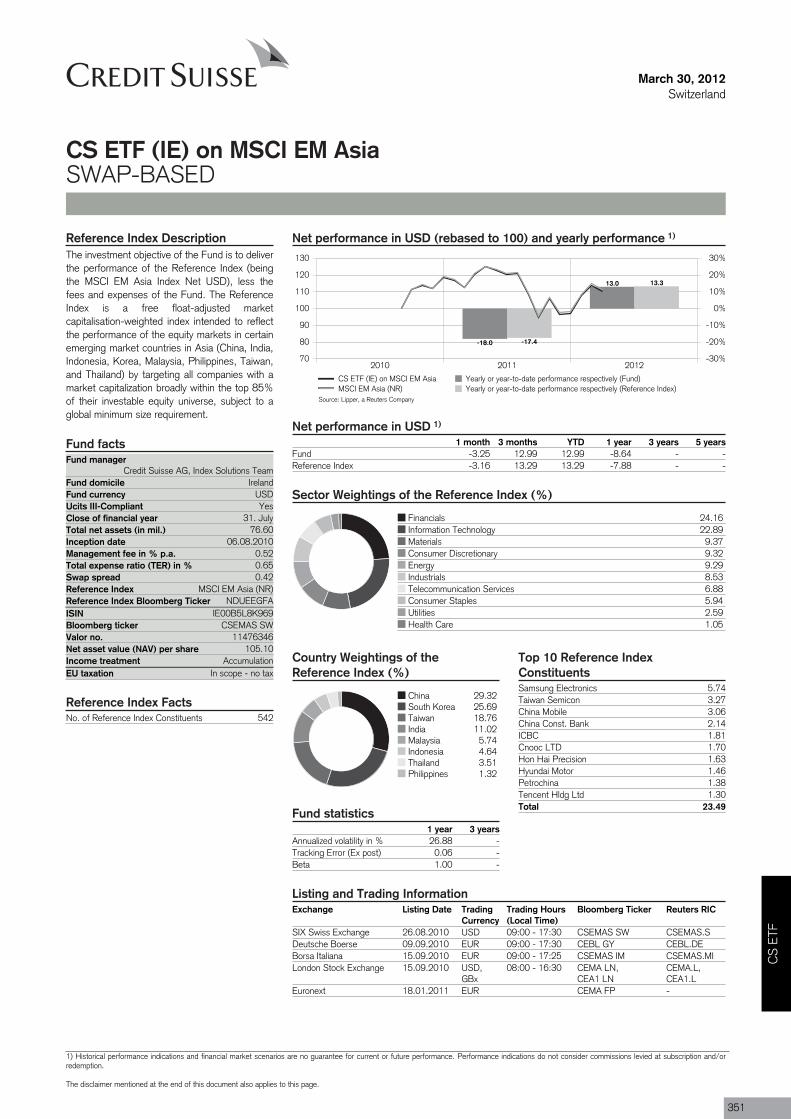

CS ETF (IE) on MSCI EM Asia 351

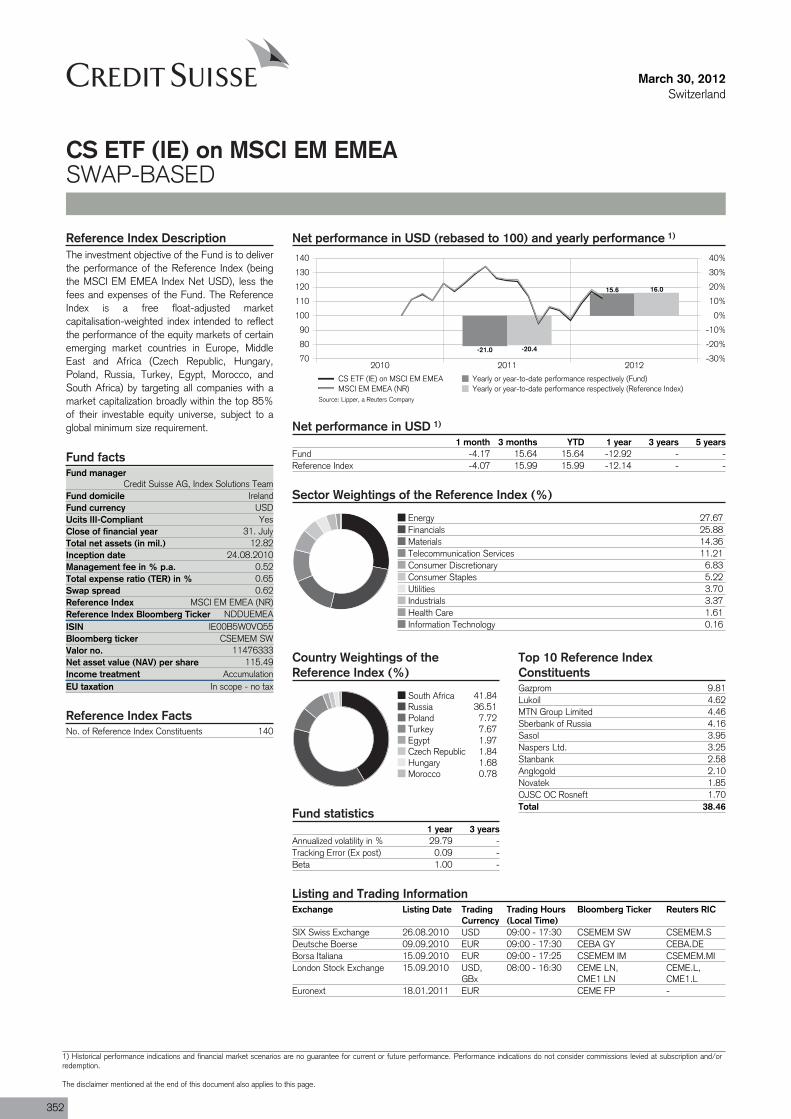

CS ETF (IE) on MSCI EM EMEA 352

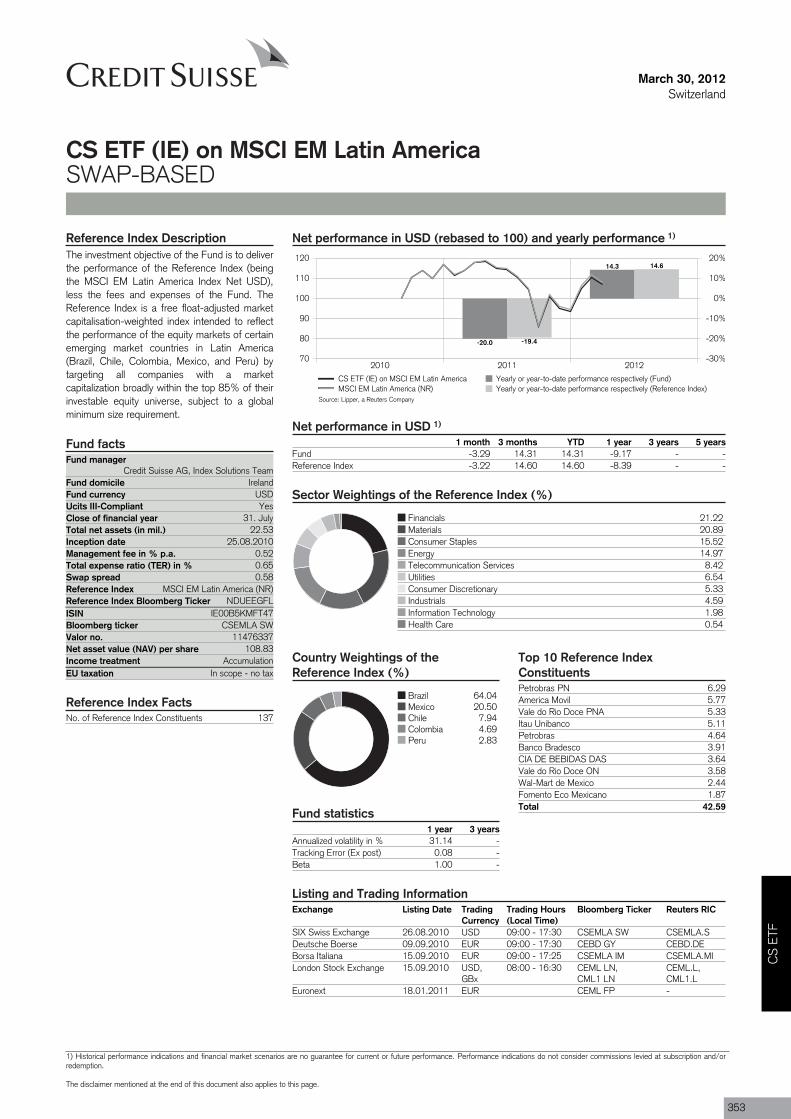

CS ETF (IE) on MSCI EM Latin America 353

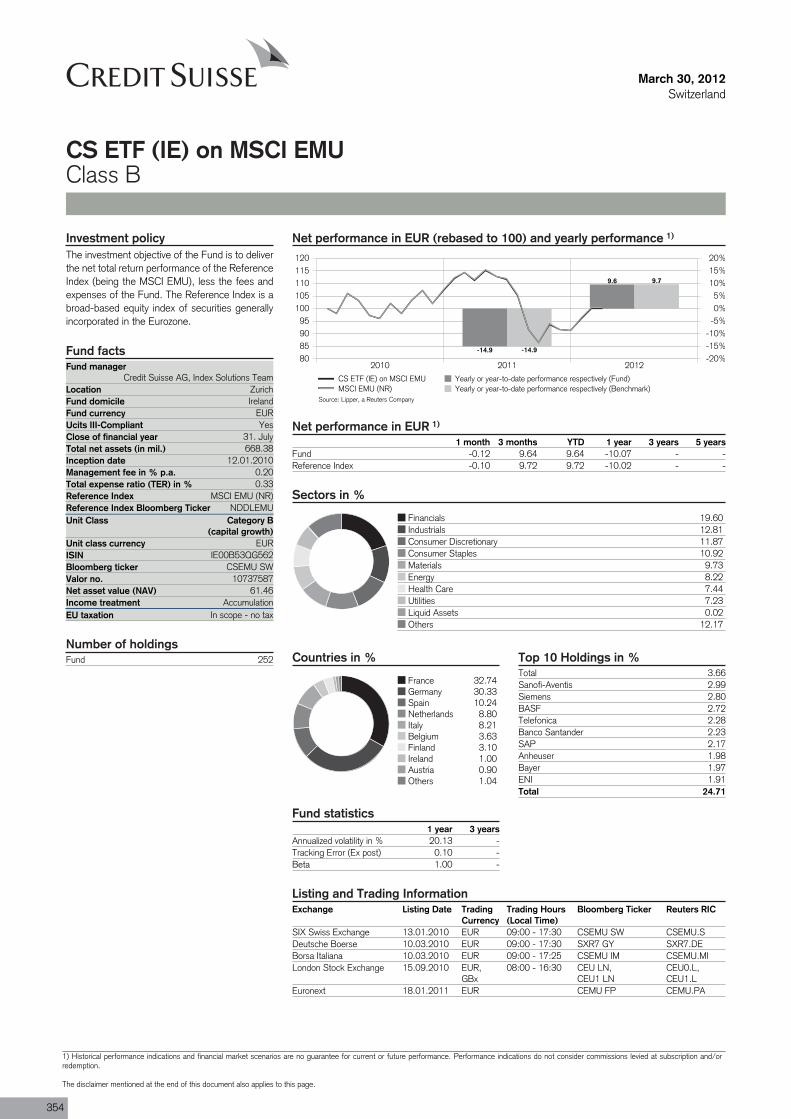

CS ETF (IE) on MSCI EMU 354

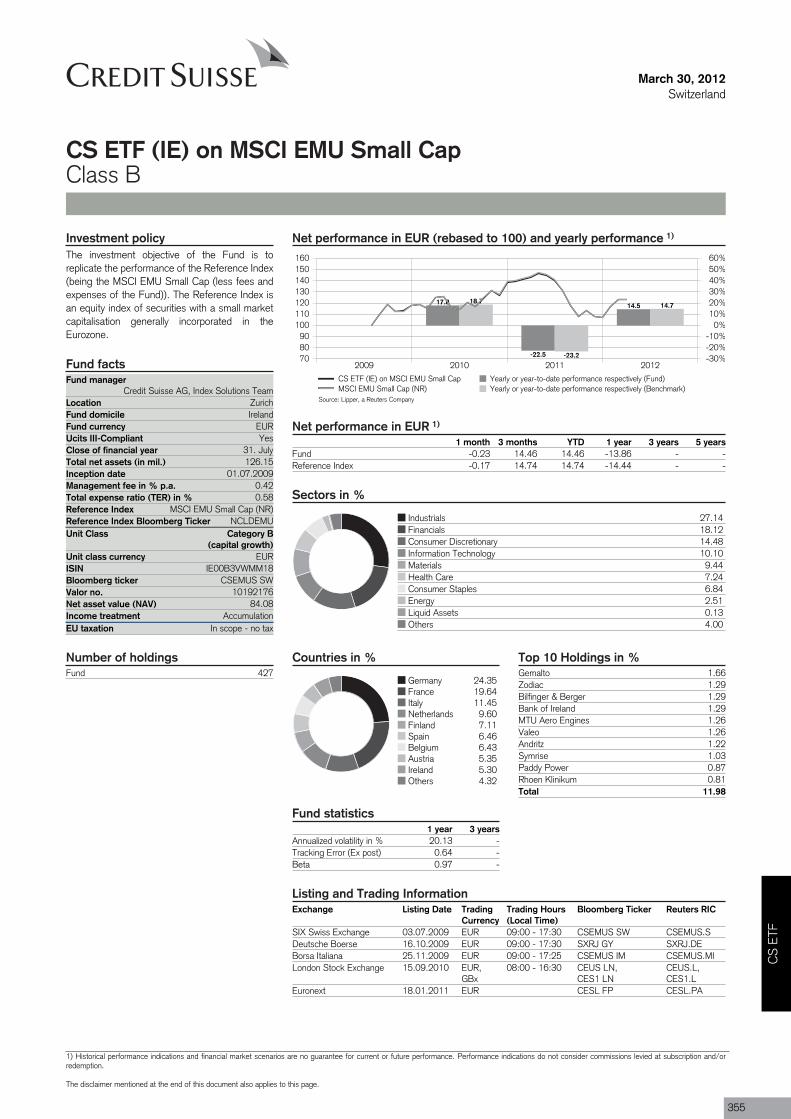

CS ETF (IE) on MSCI EMU Small Cap 355

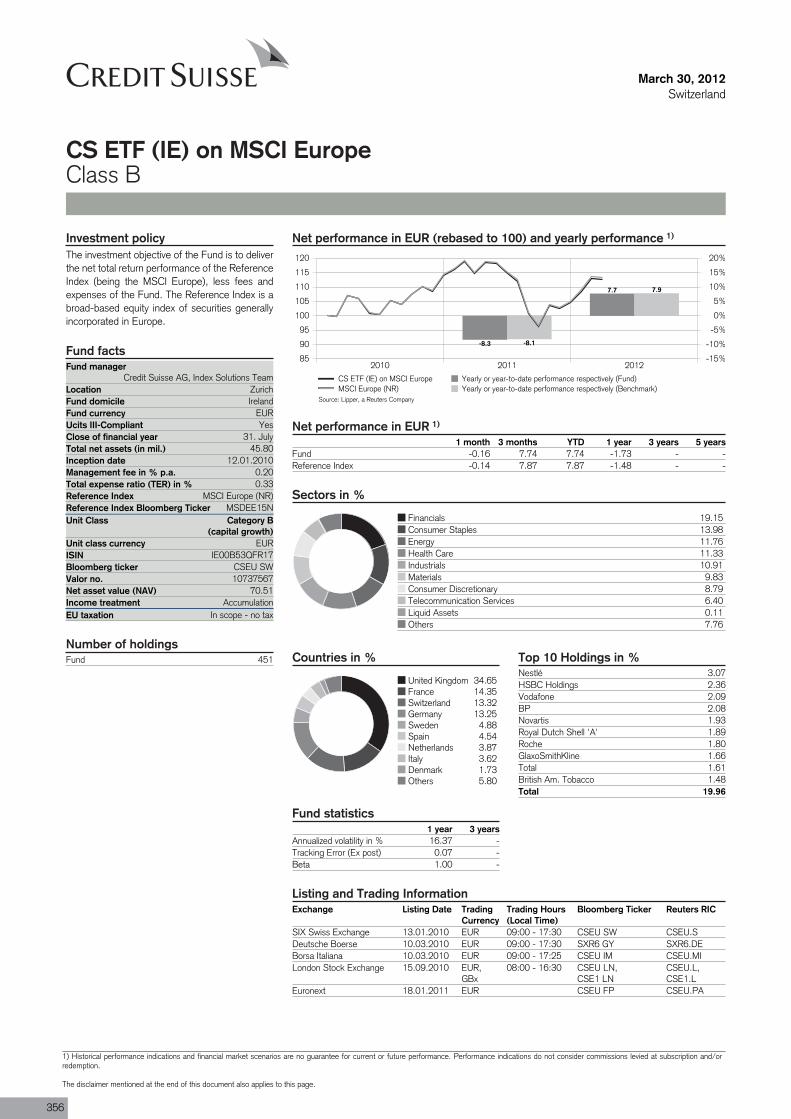

CS ETF (IE) on MSCI Europe 356

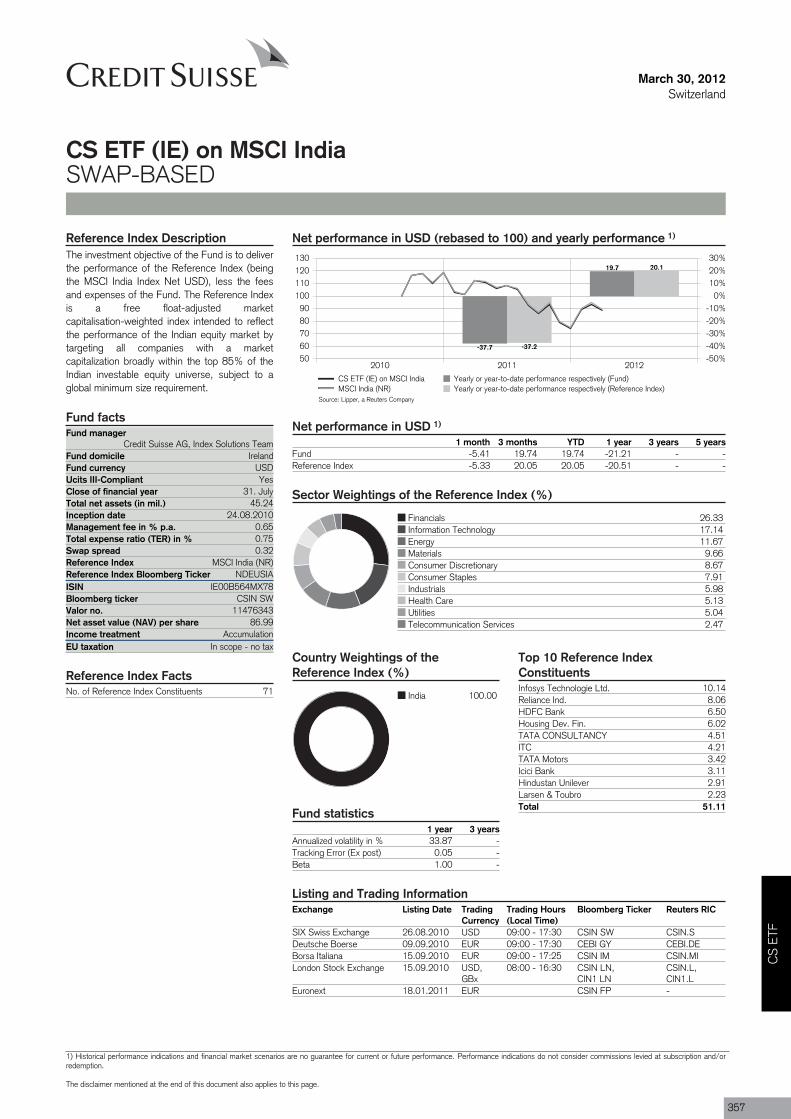

CS ETF (IE) on MSCI India 357

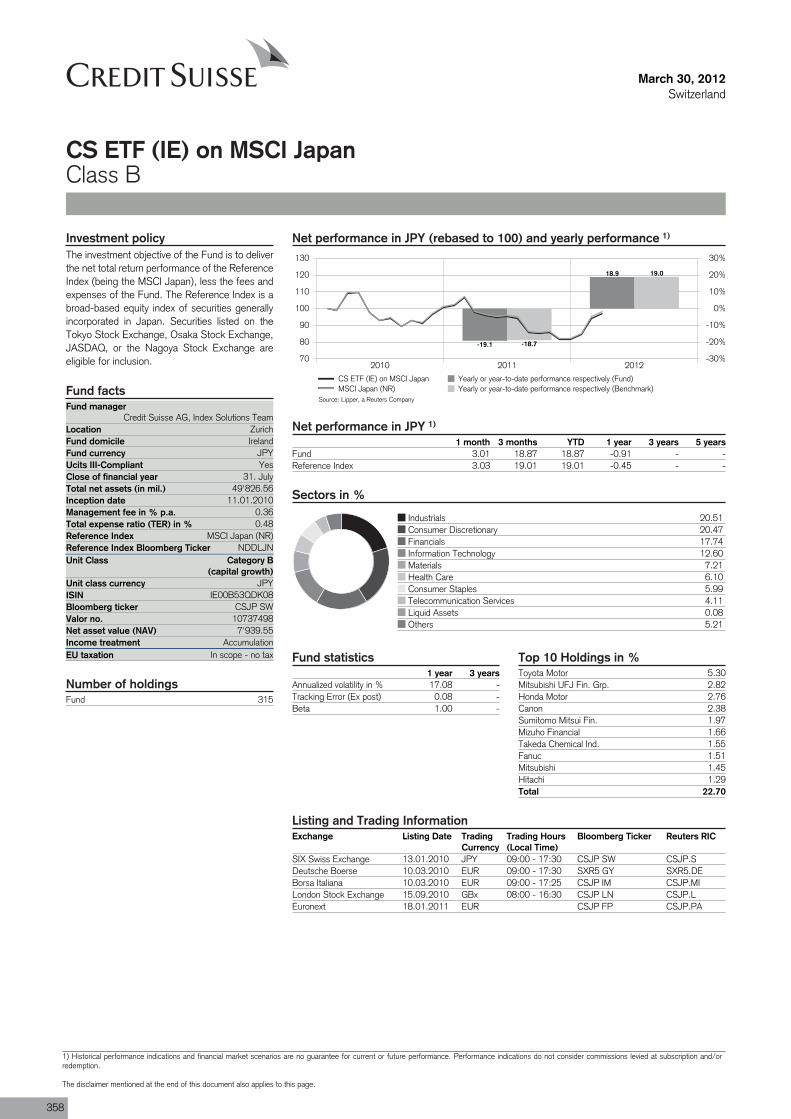

CS ETF (IE) on MSCI Japan 358

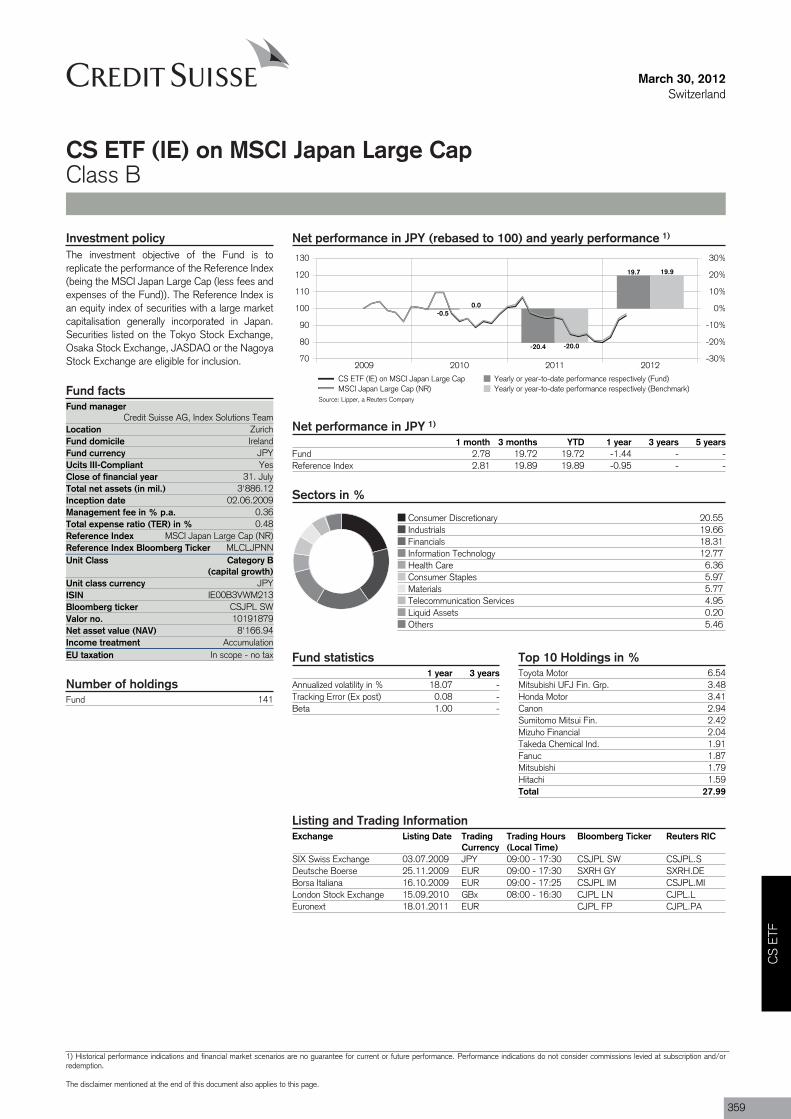

CS ETF (IE) on MSCI Japan Large Cap 359

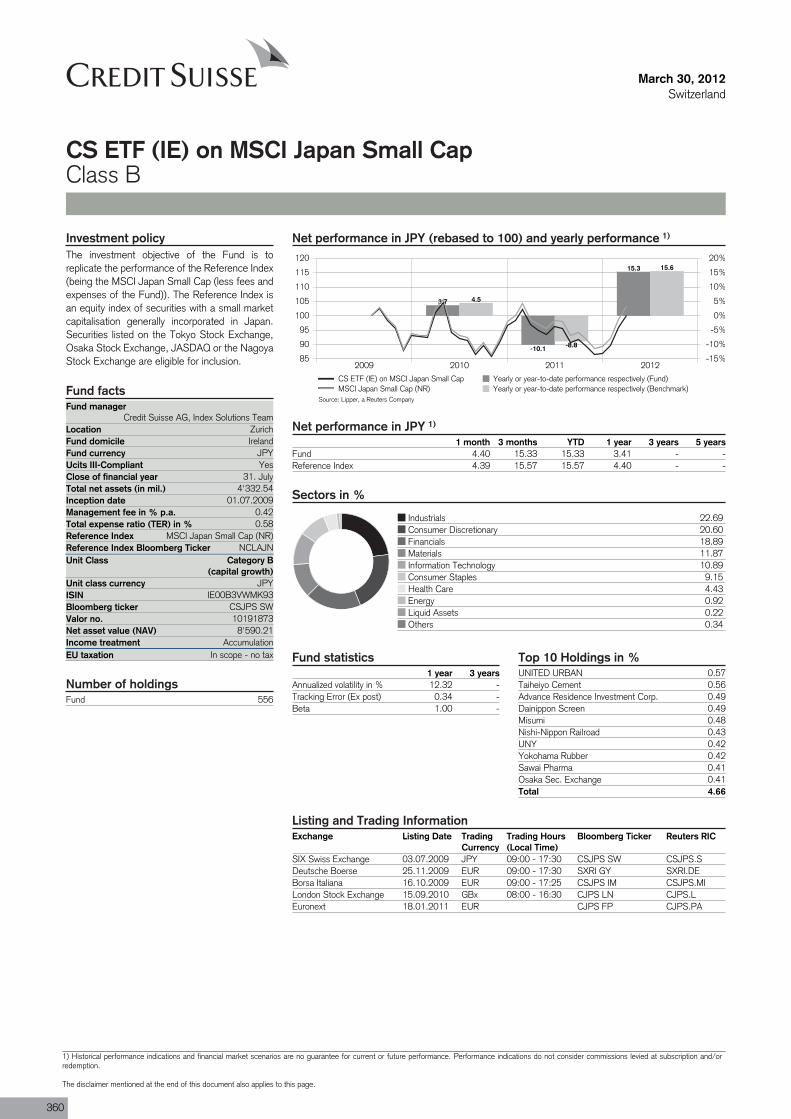

CS ETF (IE) on MSCI Japan Small Cap 360

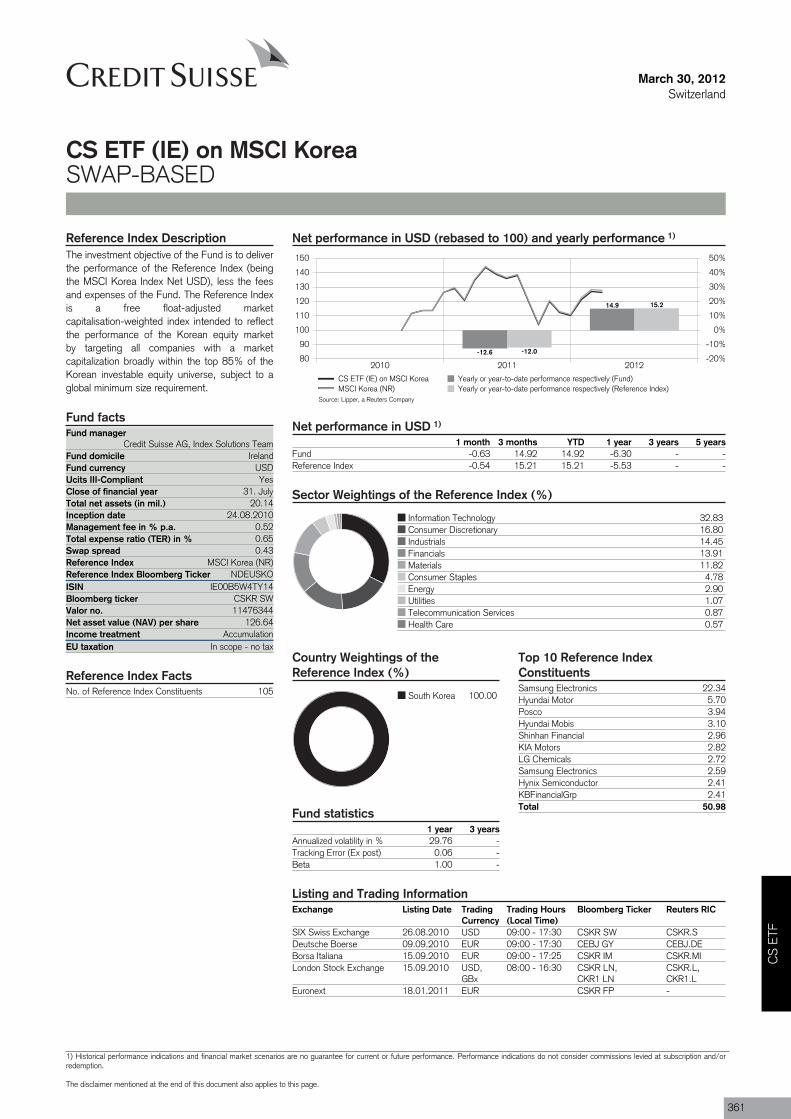

CS ETF (IE) on MSCI Korea 361

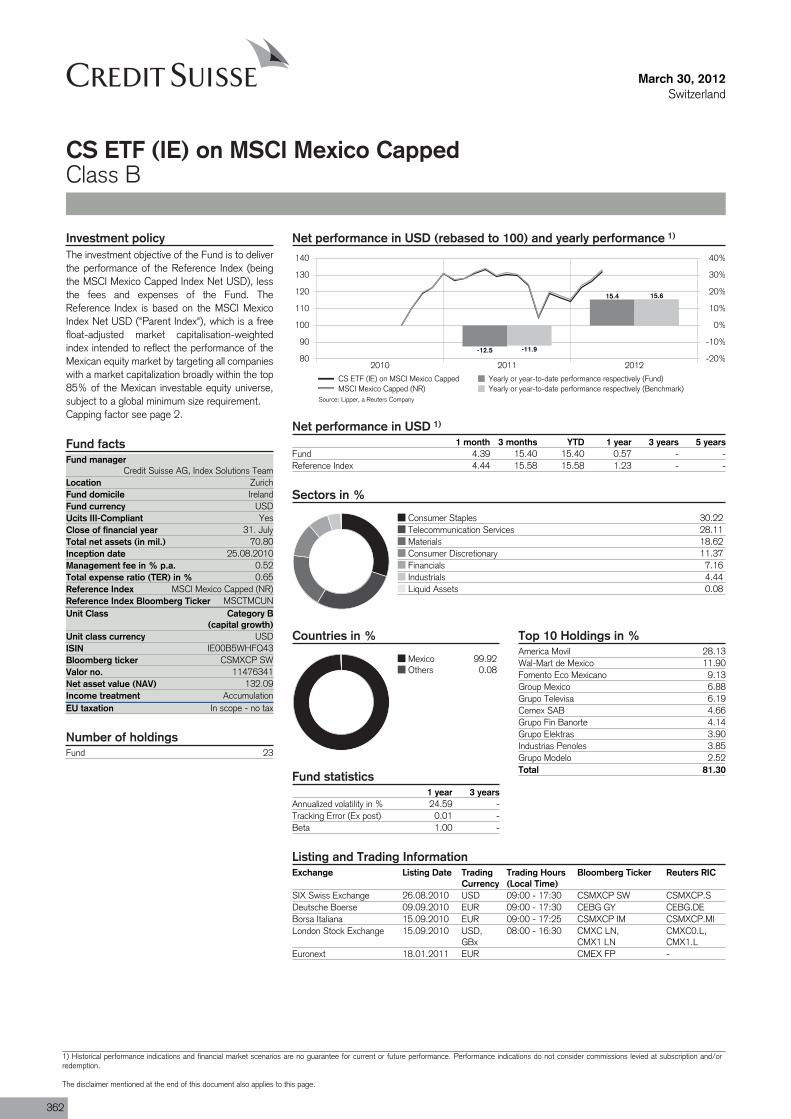

CS ETF (IE) on MSCI Mexico Capped 362

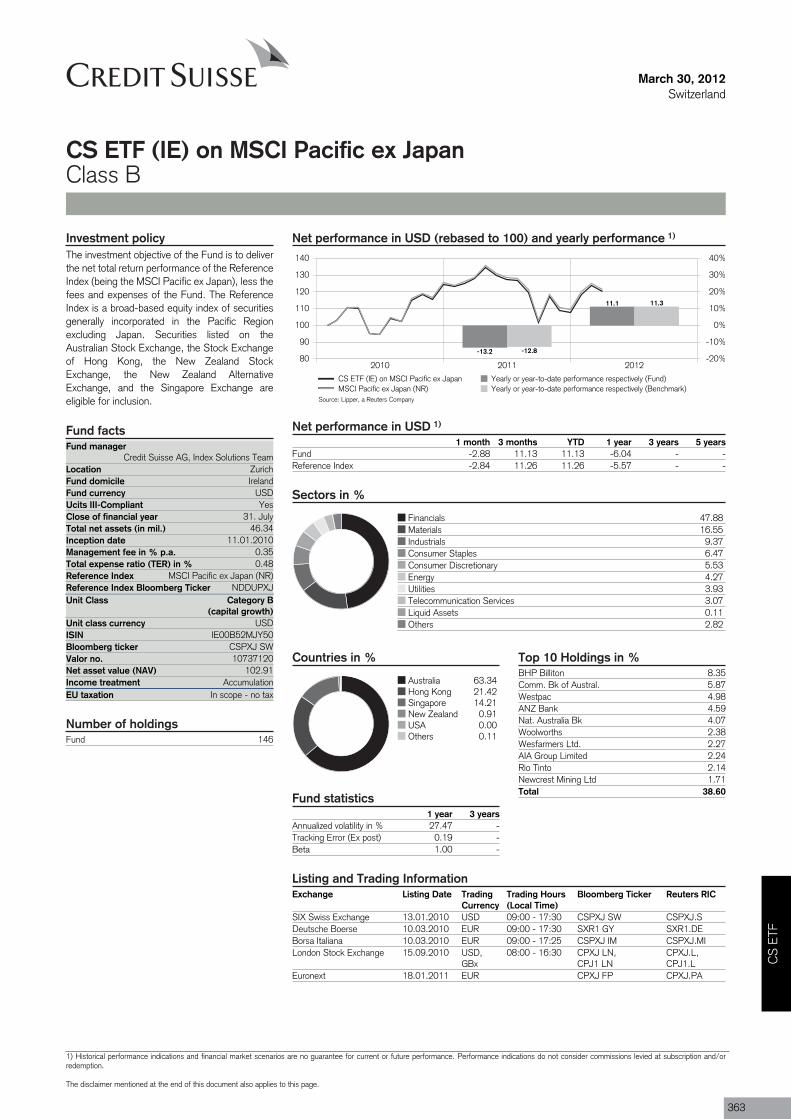

CS ETF (IE) on MSCI Pacific ex Japan 363

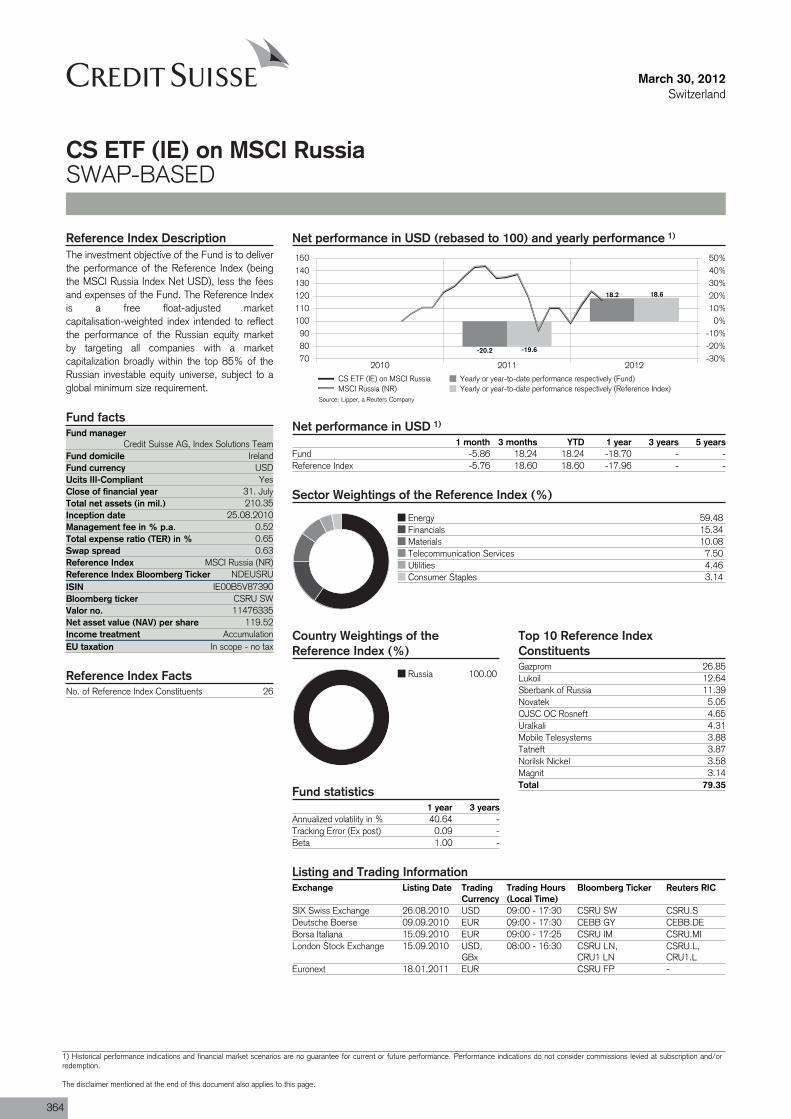

CS ETF (IE) on MSCI Russia 364

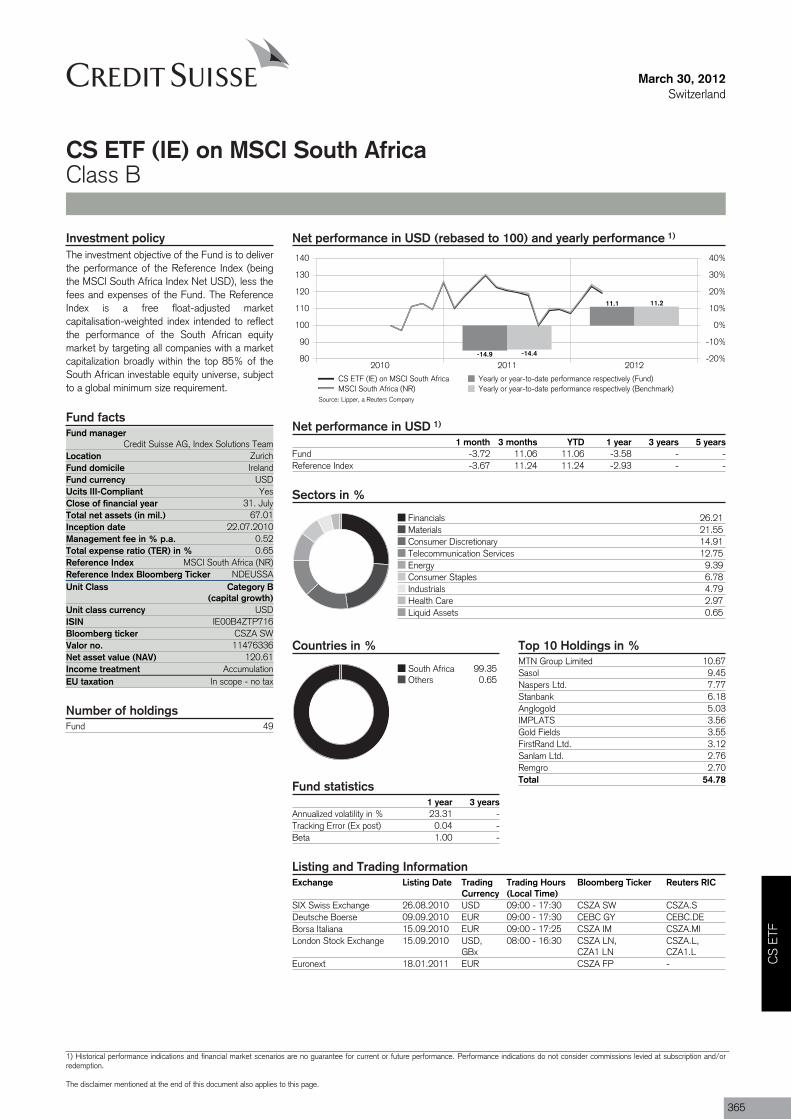

CS ETF (IE) on MSCI South Africa 365

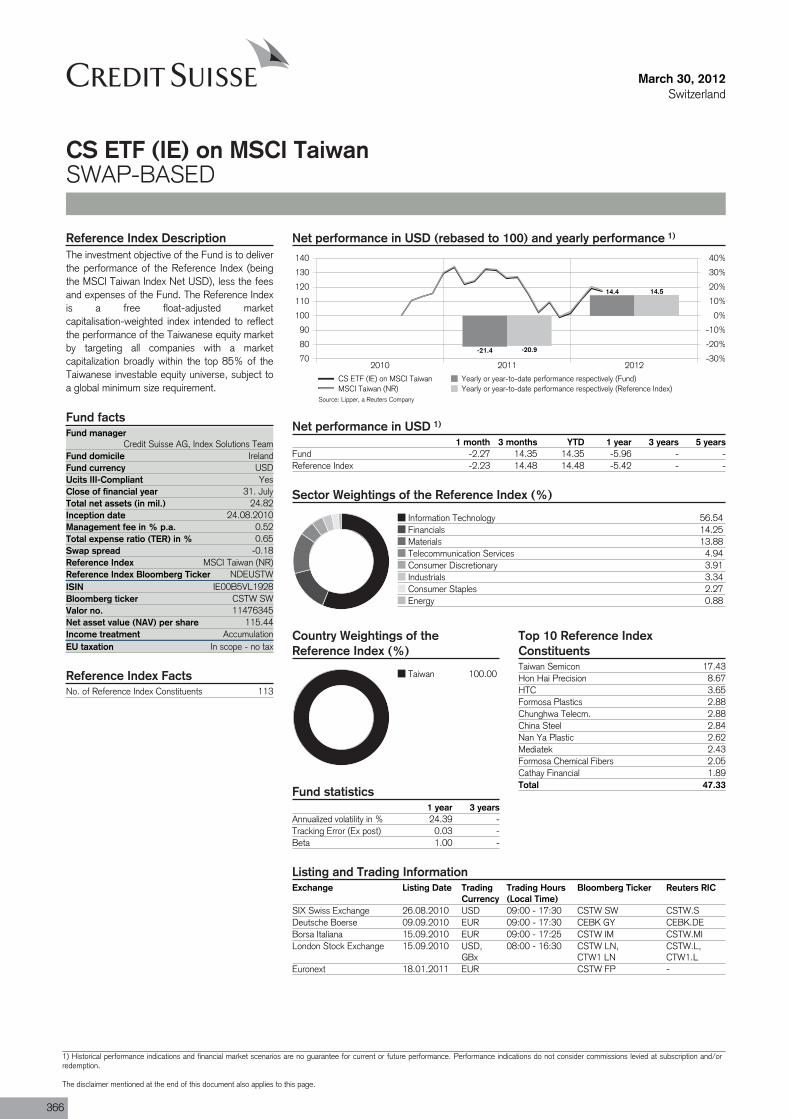

CS ETF (IE) on MSCI Taiwan 366

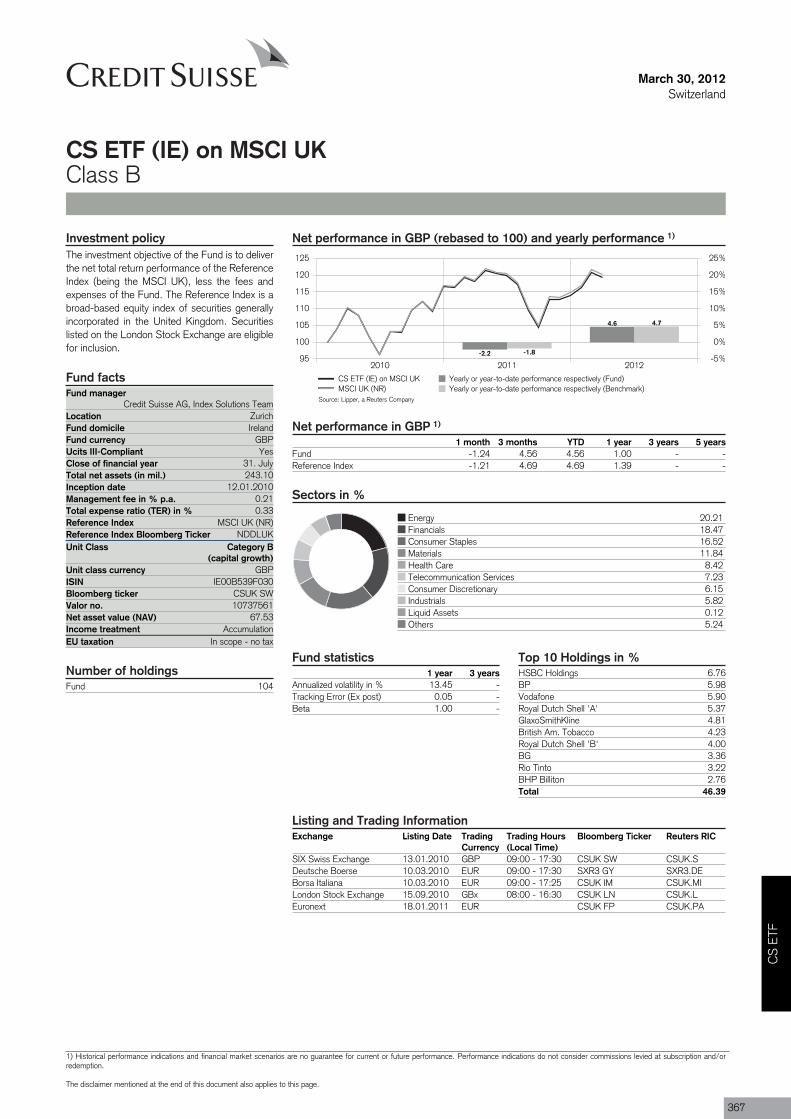

CS ETF (IE) on MSCI UK 367

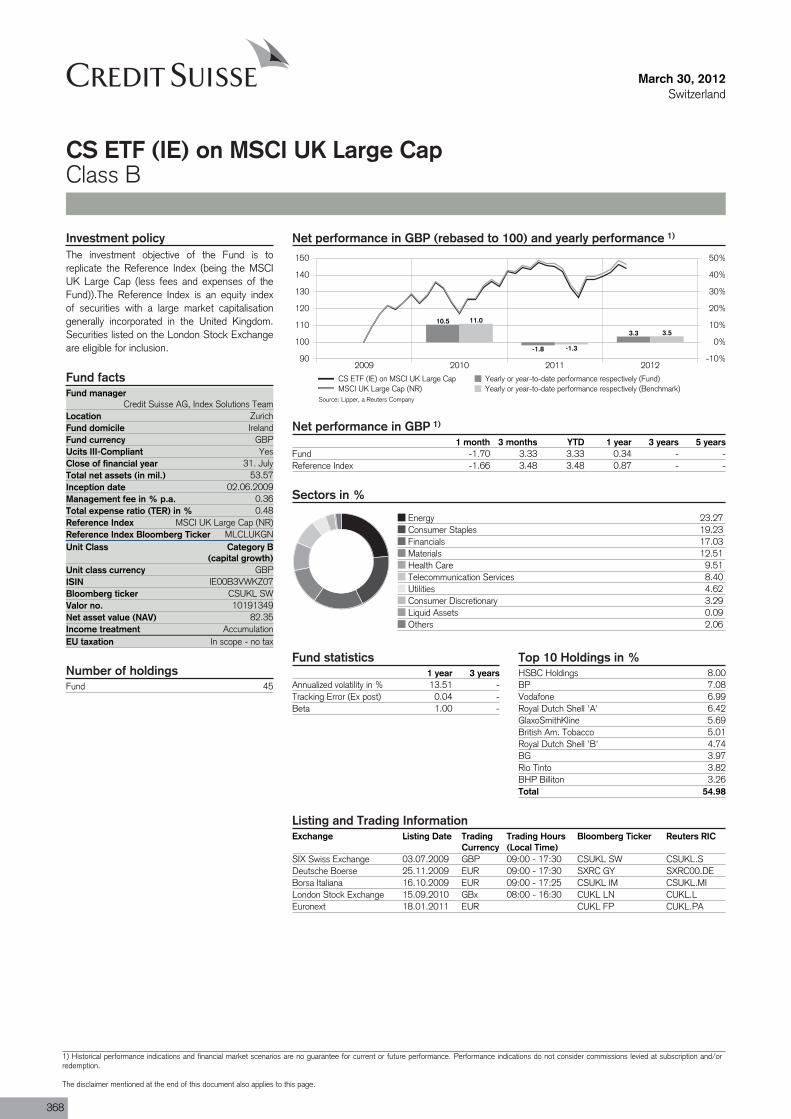

CS ETF (IE) on MSCI UK Large Cap 368

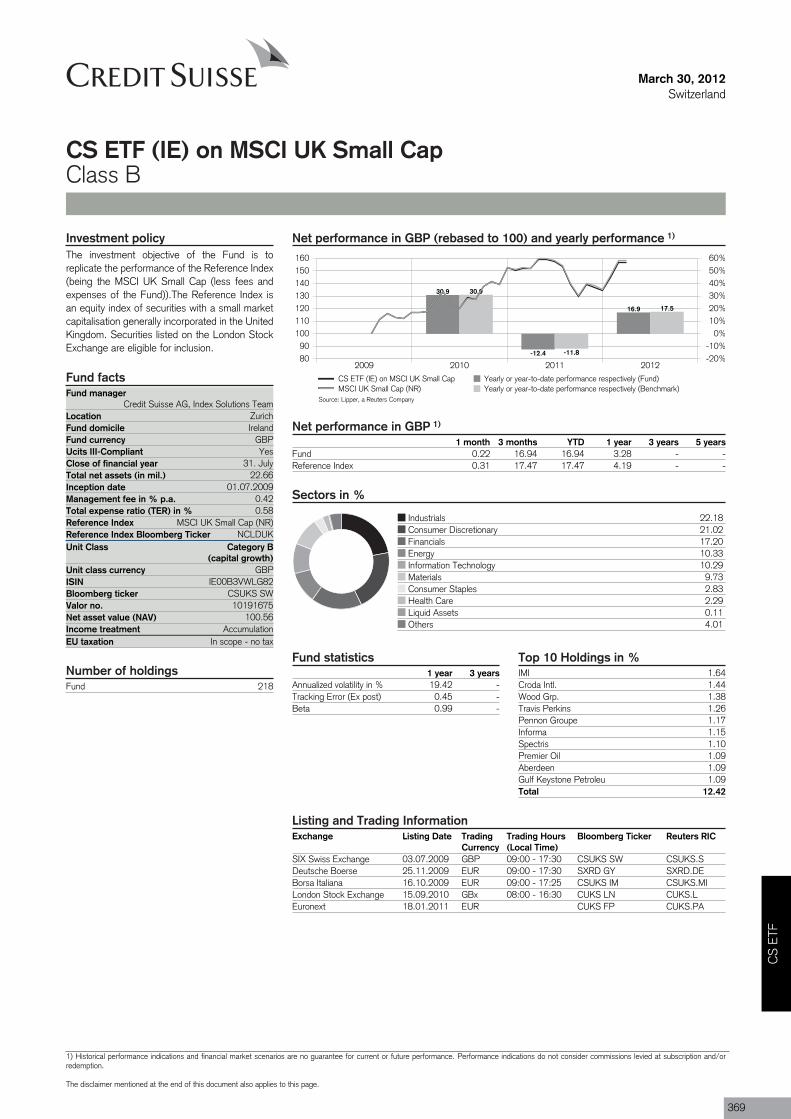

CS ETF (IE) on MSCI UK Small Cap 369

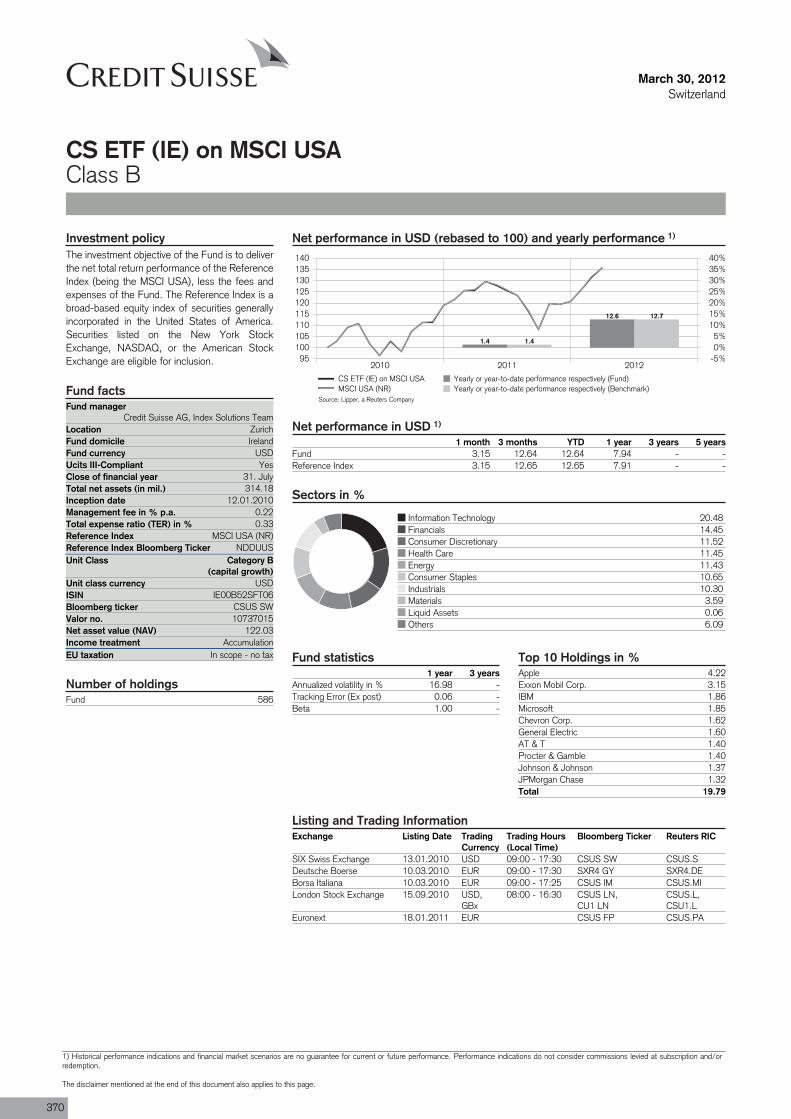

CS ETF (IE) on MSCI USA 370

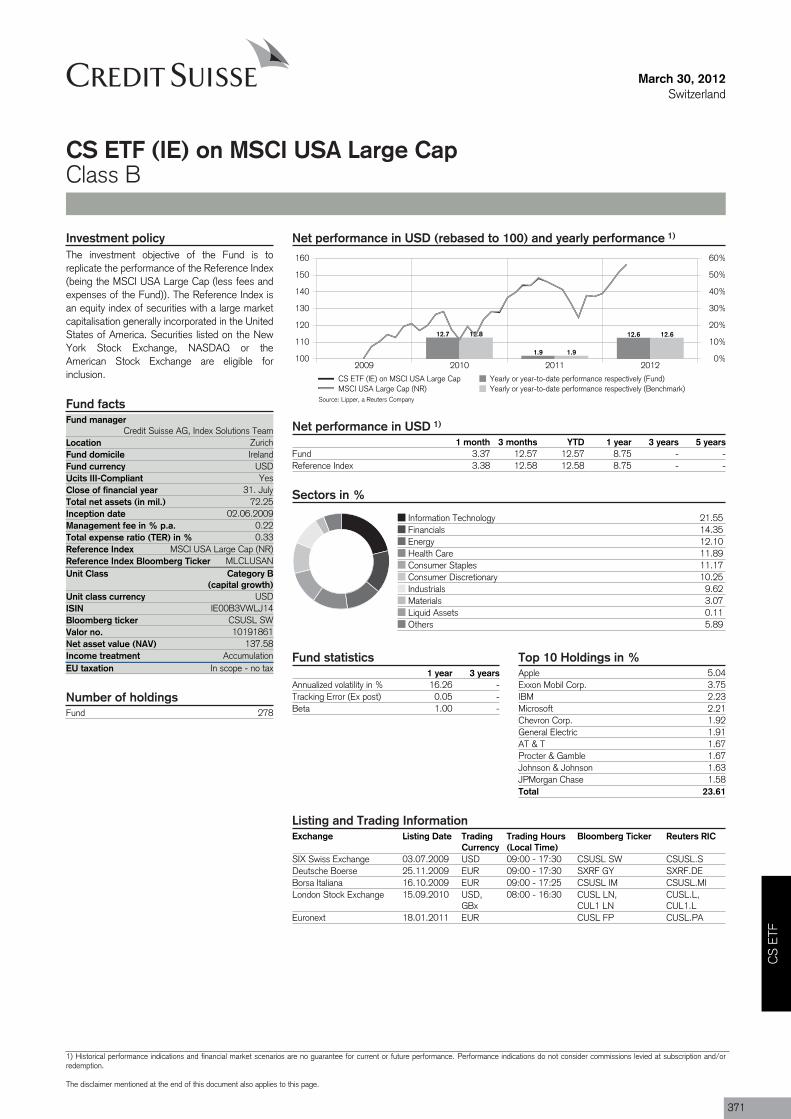

CS ETF (IE) on MSCI USA Large Cap 371

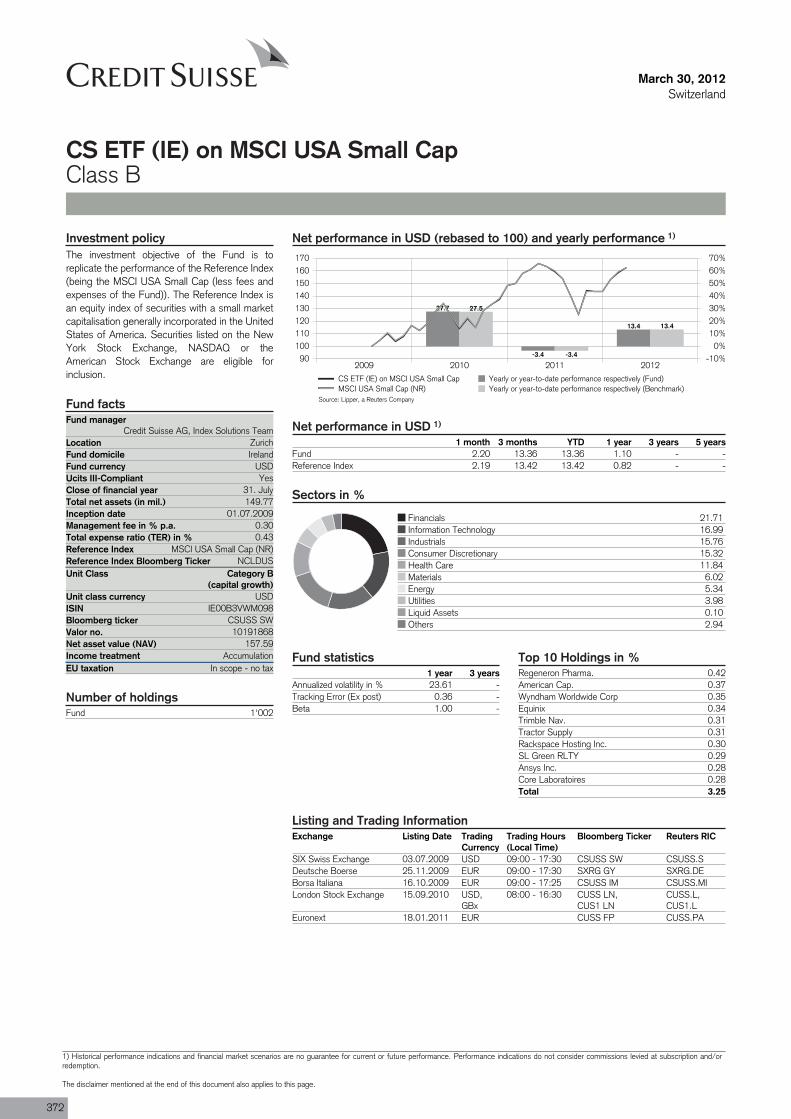

CS ETF (IE) on MSCI USA Small Cap 372

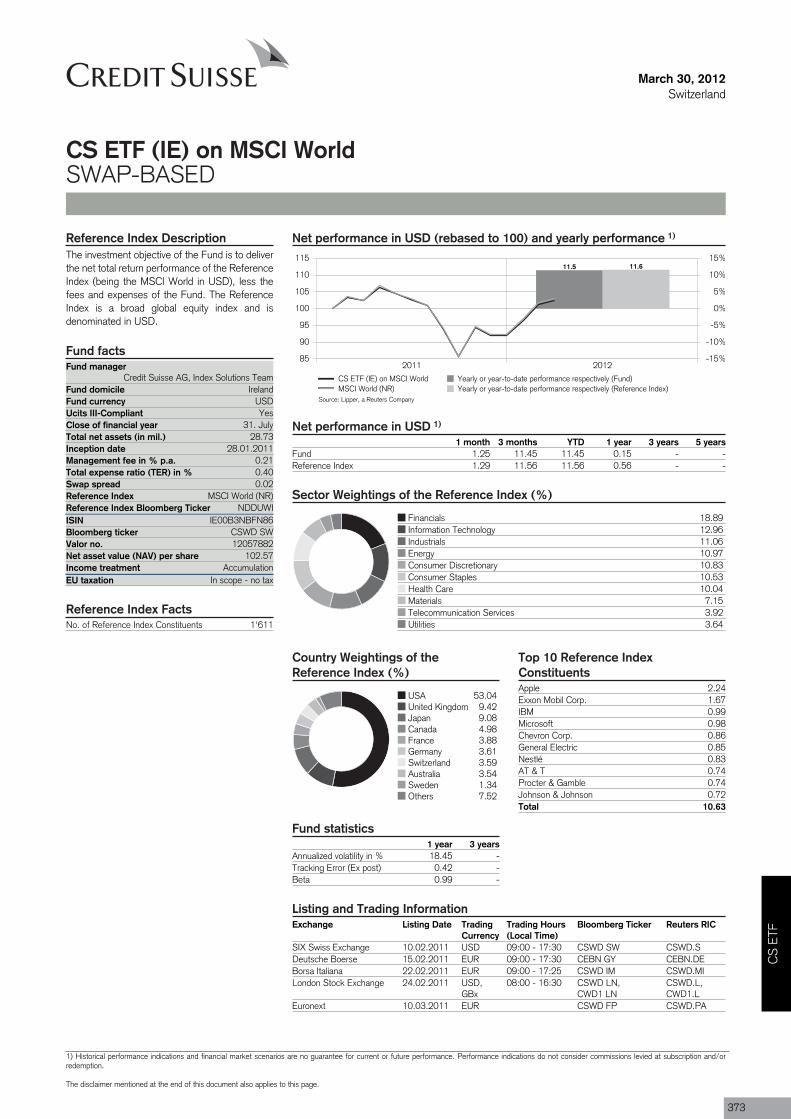

CS ETF (IE) on MSCI World 373

CS ETF (IE) on NASDAQ 100 374

CS ETF (IE) on Nikkei 225 375

CS ETF (IE) on S&P 500 376

CS ETF (Lux) on MSCI Emerging Markets 377

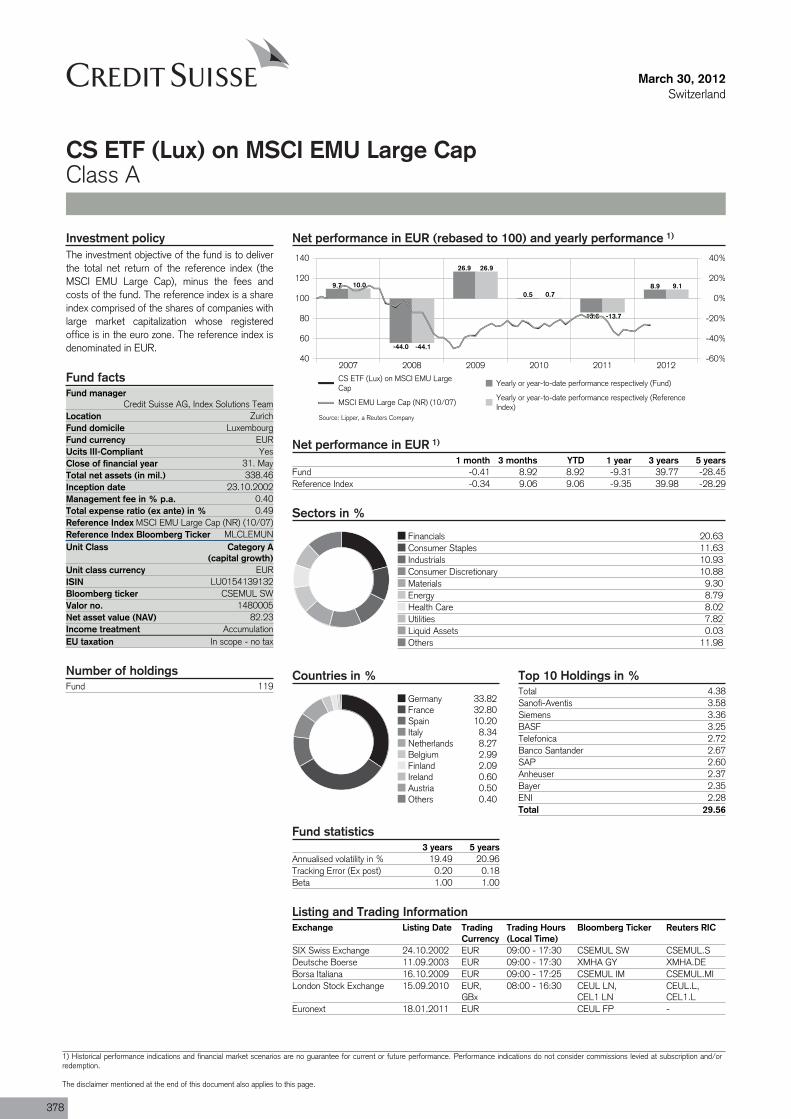

CS ETF (Lux) on MSCI EMU Large Cap 378

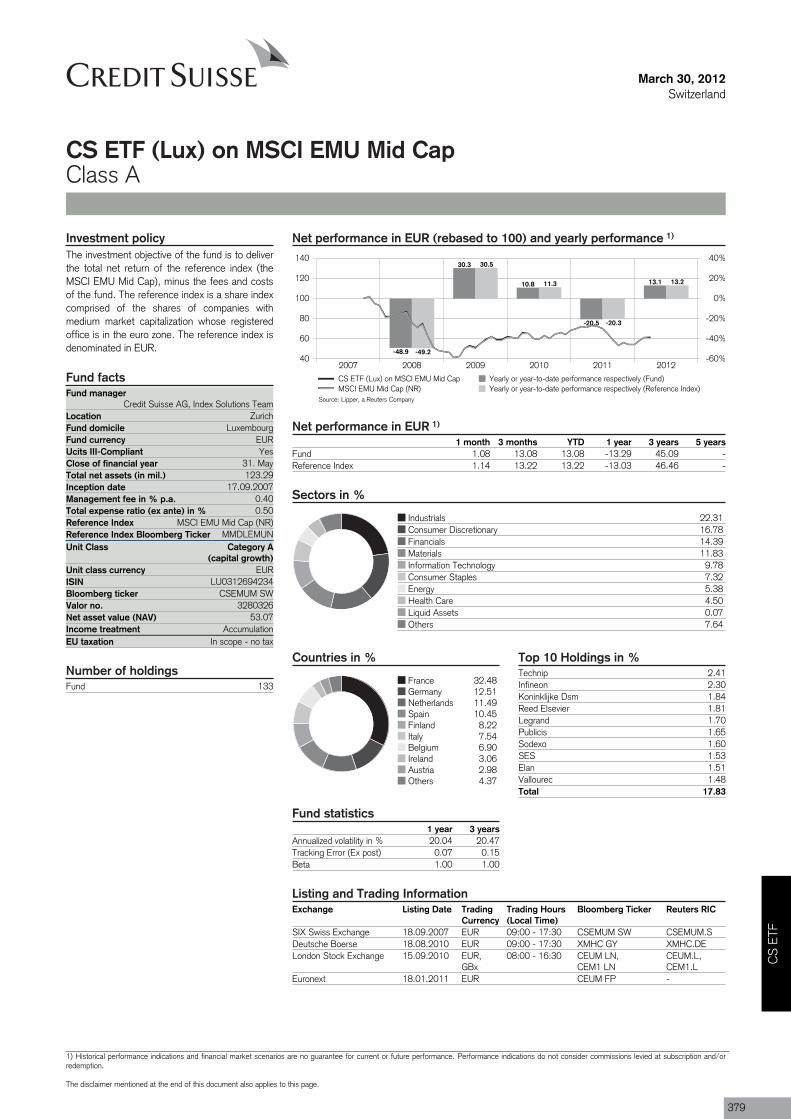

CS ETF (Lux) on MSCI EMU Mid Cap 379

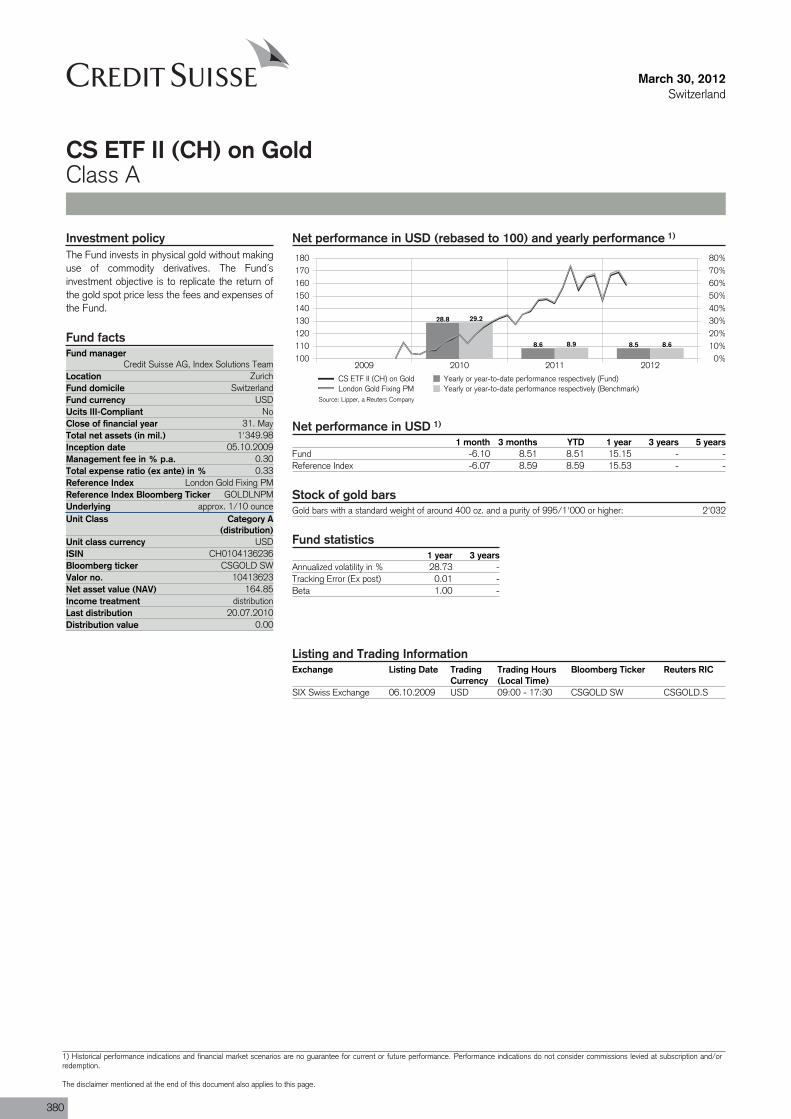

CS ETF II (CH) on Gold 380

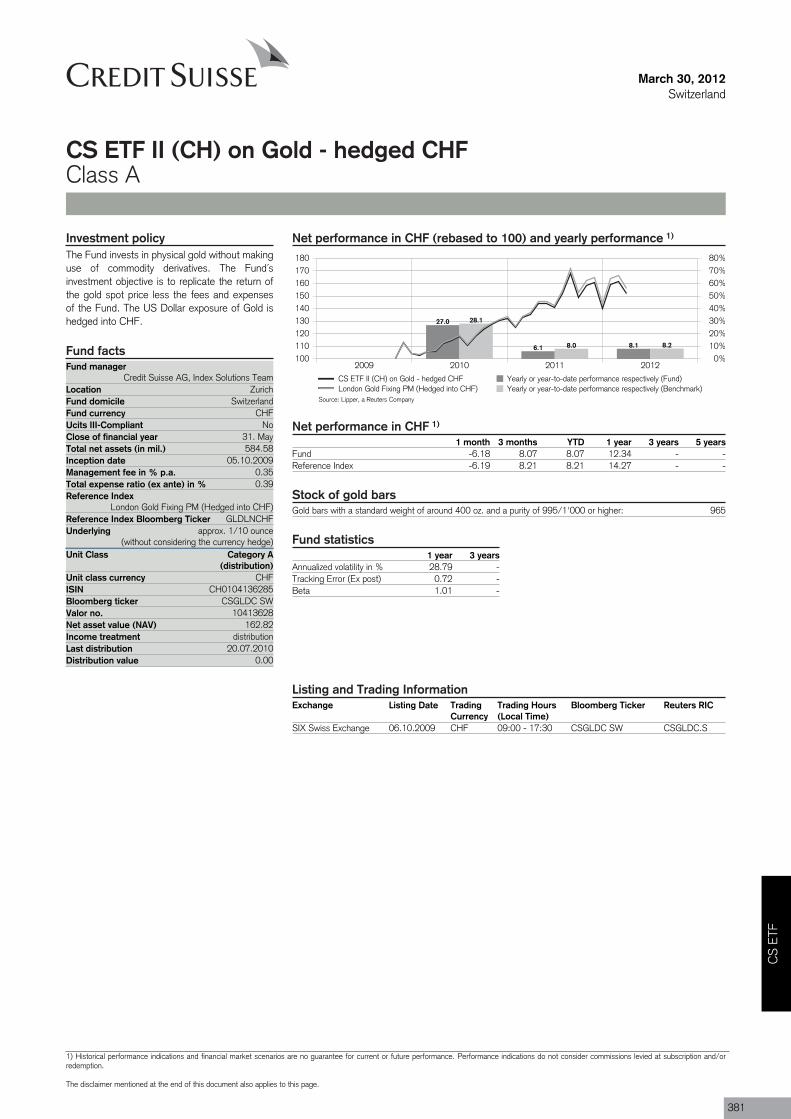

CS ETF II (CH) on Gold - hedged CHF 381

CS ETF II (CH) on Gold - hedged EUR 382

InformationGlossary 384

Factsheet Explained 386

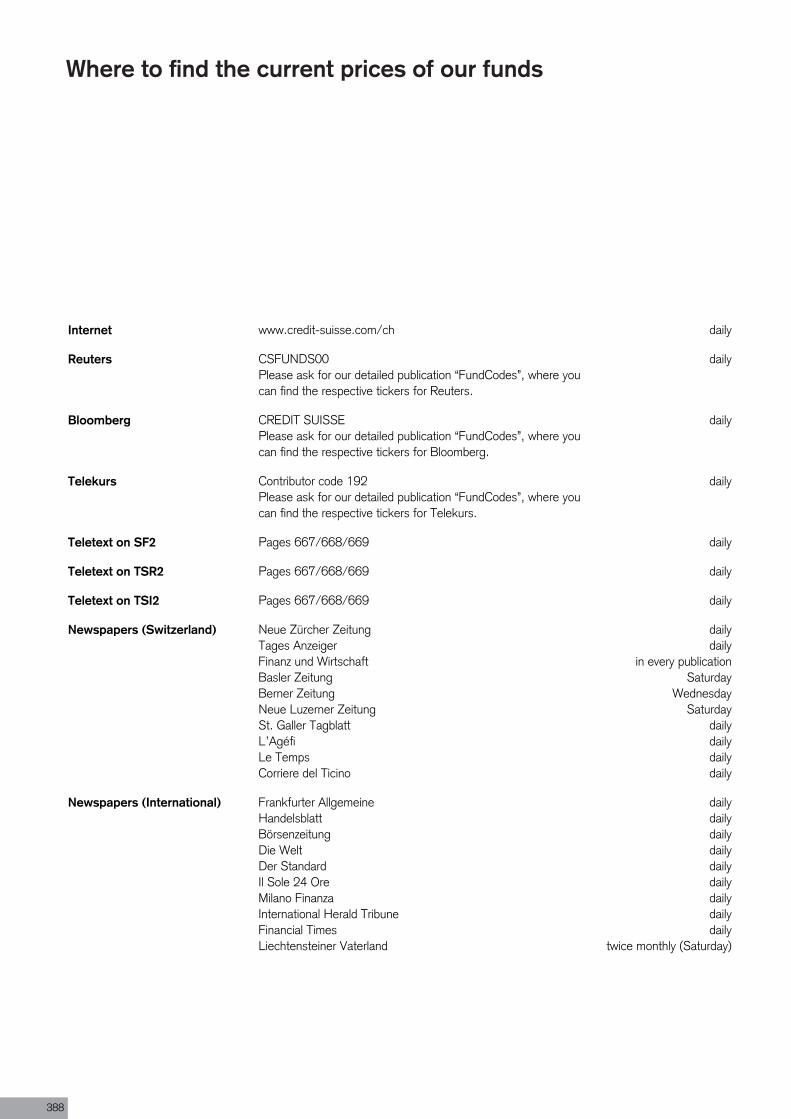

Where to find the current prices of our funds 388

Important Information 389

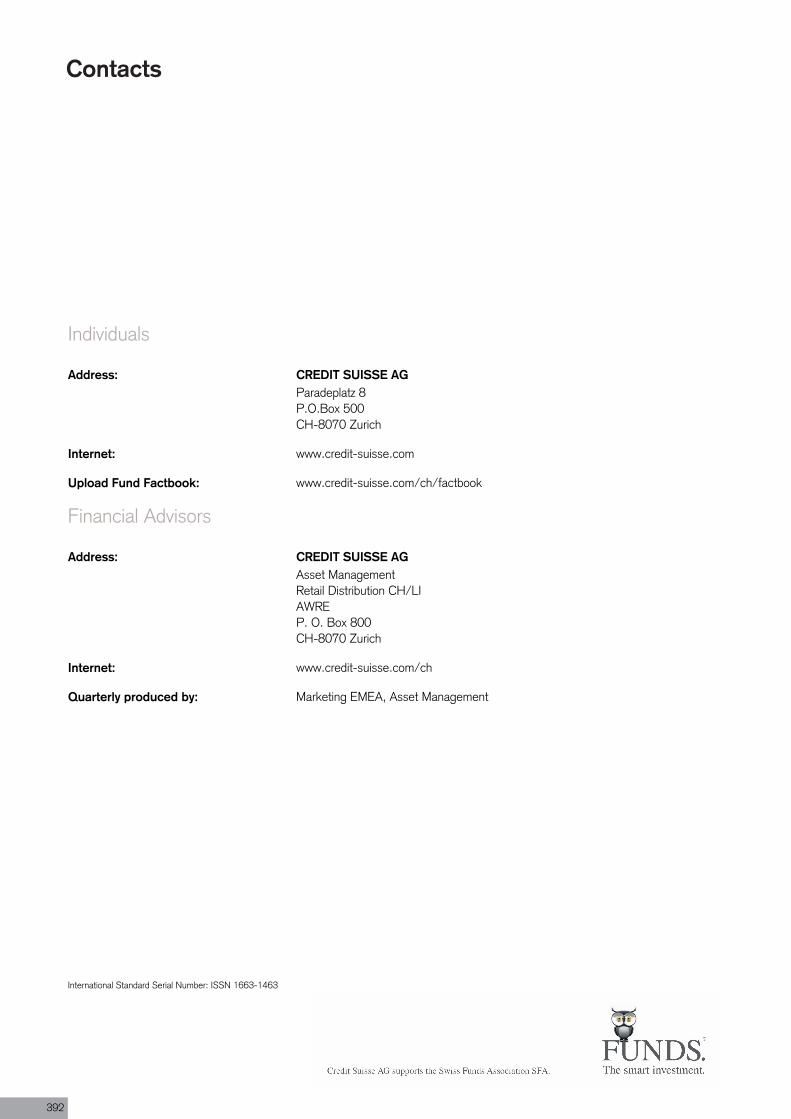

Contacts 392

Ove

rvie

w

5

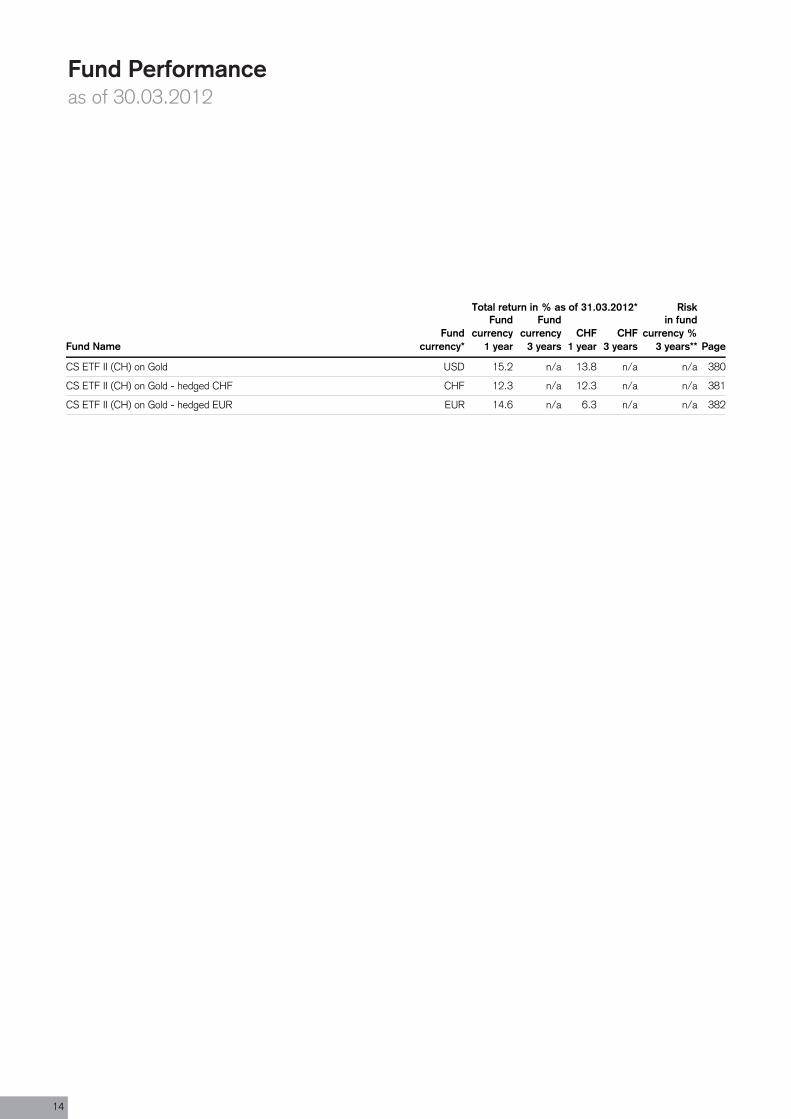

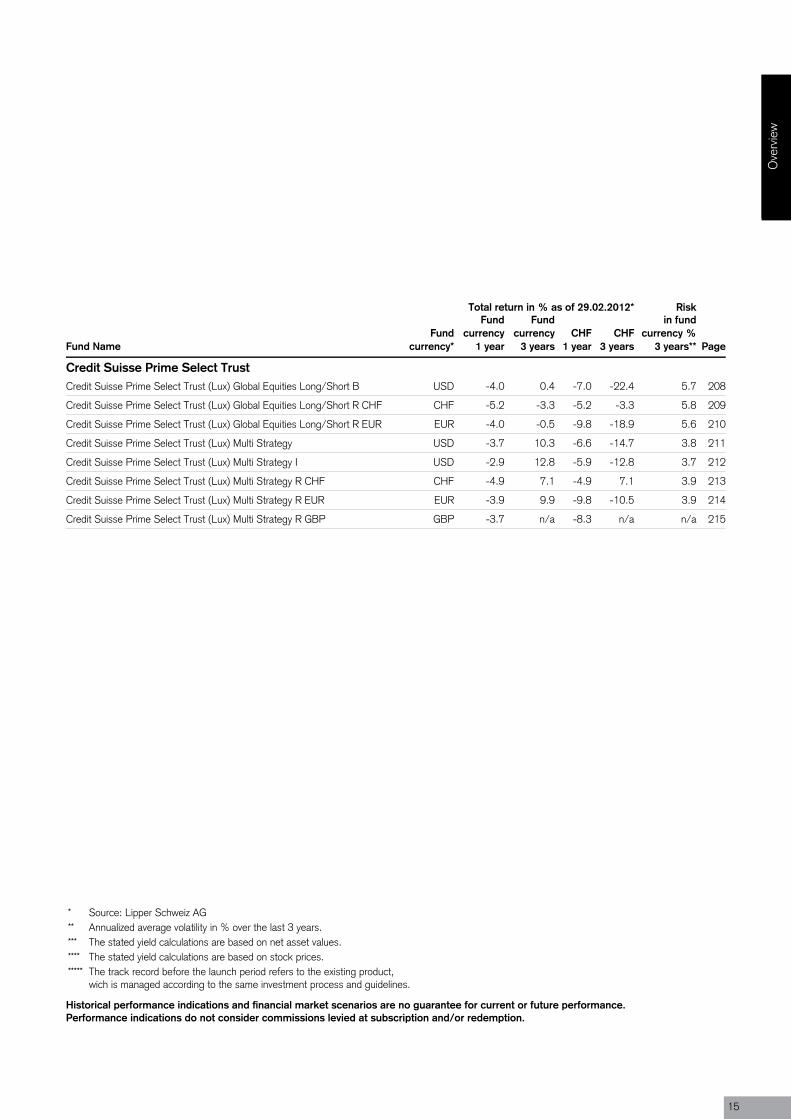

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

Credit Suisse Bond FundCredit Suisse Bond Fund (CH) Convert International A CHF CHF -5.6 25.2 -5.6 25.2 11.7 16

Credit Suisse Bond Fund (CH) Convert International A USD USD -4.7 57.1 -5.8 24.9 13.4 18

Credit Suisse Bond Fund (CH) Dynamic International USD 3.9 31.4 2.7 4.5 8.0 20

Credit Suisse Bond Fund (CH) Dynamic Sfr CHF 3.8 30.2 3.8 30.2 4.5 22

Credit Suisse Bond Fund (CH) Government Bond CHF B CHF 8.3 n/a 8.3 n/a n/a 24

Credit Suisse Bond Fund (Lux) Brazil B USD -0.8 64.9 -2.0 31.1 18.1 26

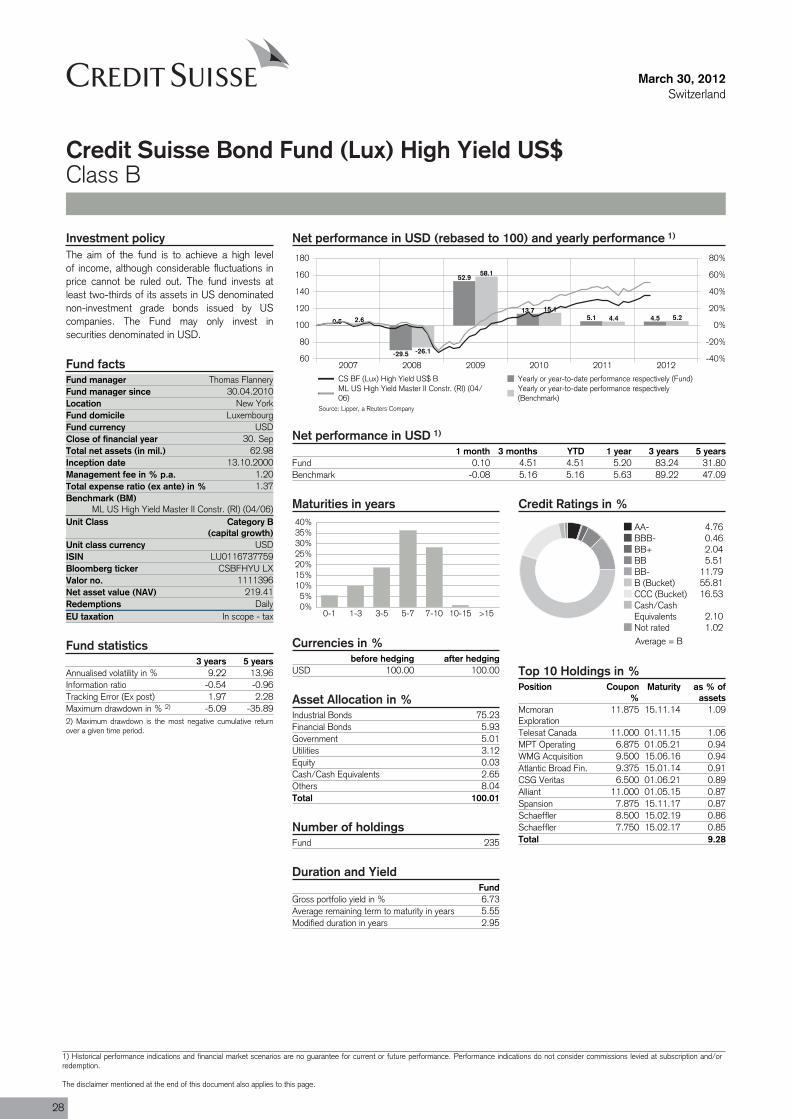

Credit Suisse Bond Fund (Lux) High Yield US$ B USD 5.2 83.2 3.9 45.7 9.2 28

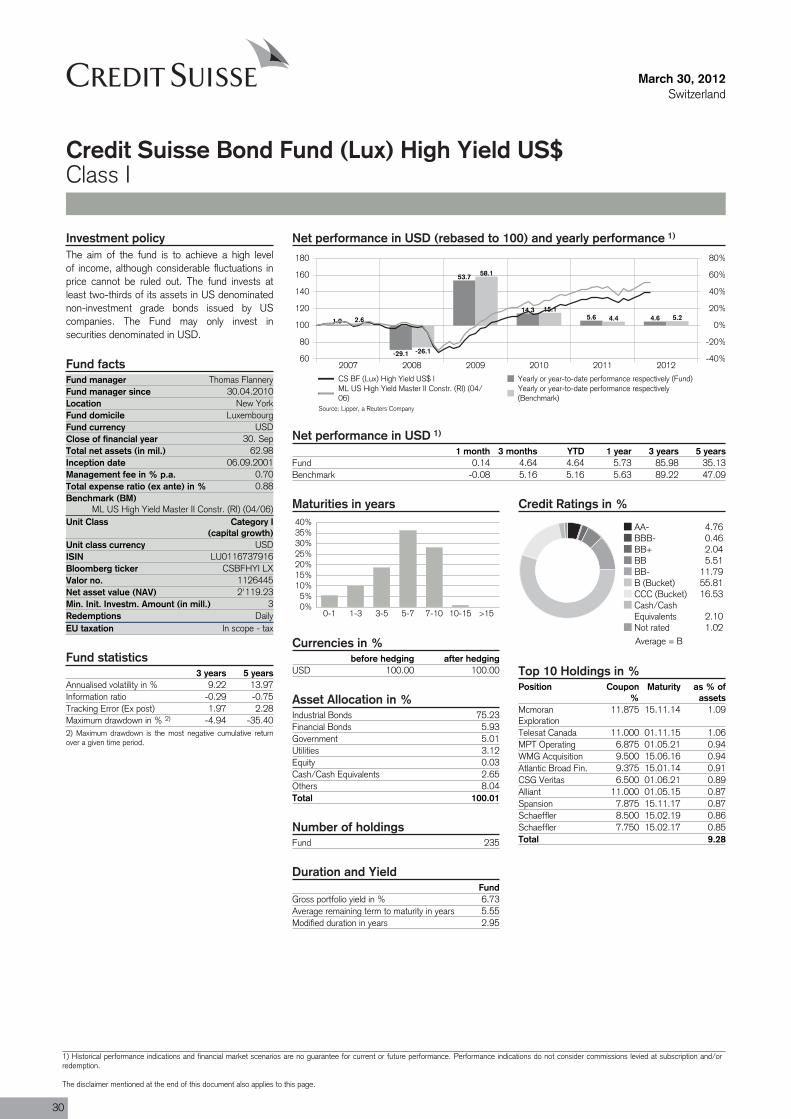

Credit Suisse Bond Fund (Lux) High Yield US$ I USD 5.7 86.0 4.5 47.8 9.2 30

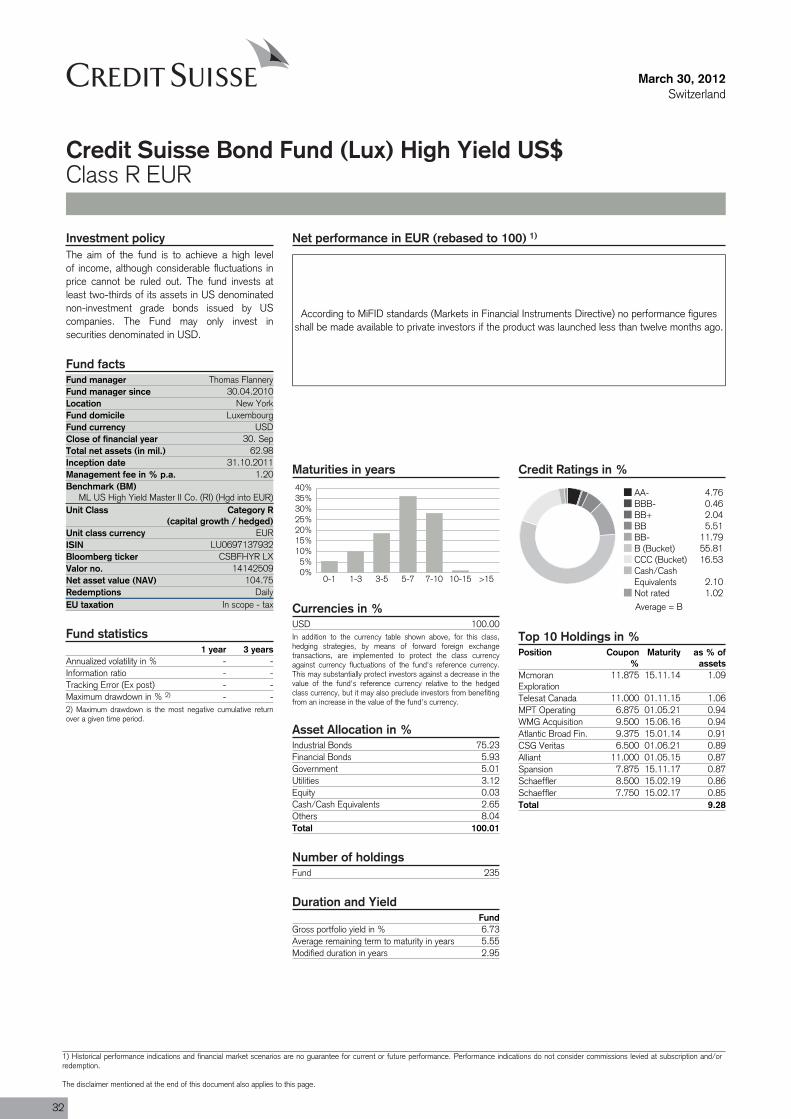

Credit Suisse Bond Fund (Lux) High Yield US$ R EUR EUR n/a n/a n/a n/a n/a 32

Credit Suisse Bond Fund (Lux) Inflation Linked (Euro) B EUR 3.5 9.0 -4.0 -13.1 3.2 34

Credit Suisse Bond Fund (Lux) Inflation Linked (Euro) I EUR 4.1 10.7 -3.5 -11.8 3.2 36

Credit Suisse Bond Fund (Lux) Inflation Linked (Sfr) B CHF 2.5 15.8 2.5 15.8 2.2 38

Credit Suisse Bond Fund (Lux) Inflation Linked (US$) B USD 5.1 14.9 3.9 -8.7 2.9 40

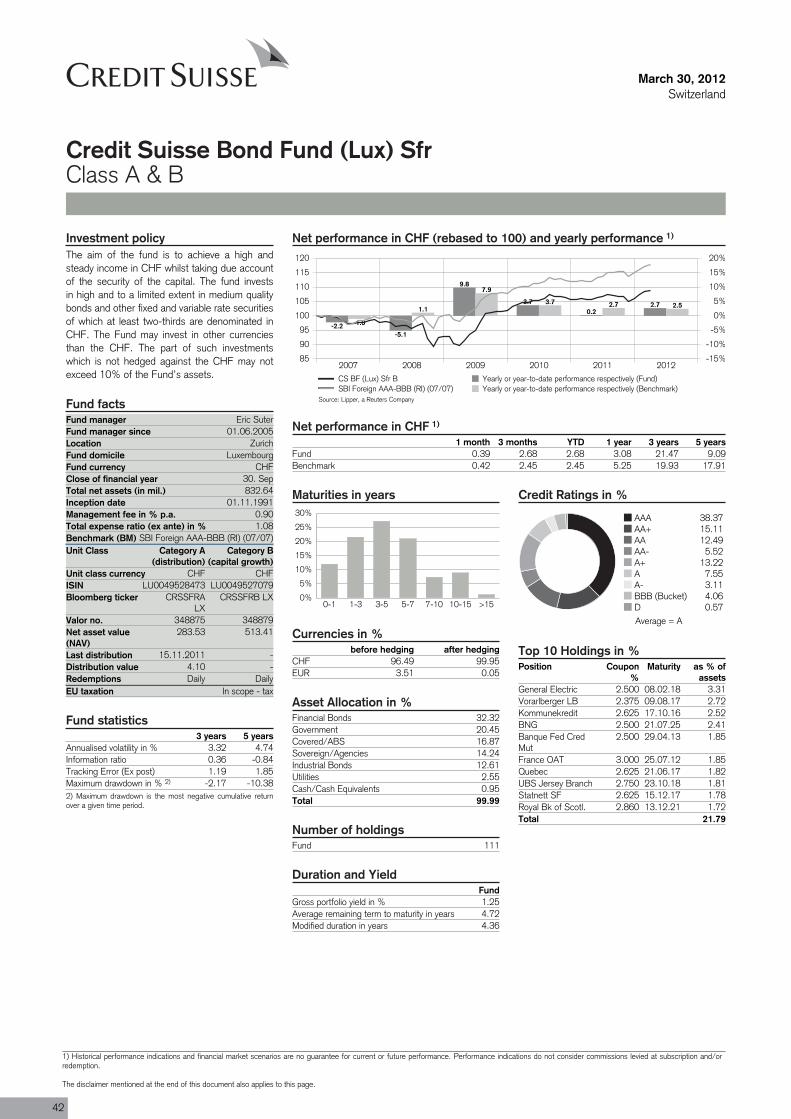

Credit Suisse Bond Fund (Lux) Sfr B CHF 3.1 21.5 3.1 21.5 3.3 42

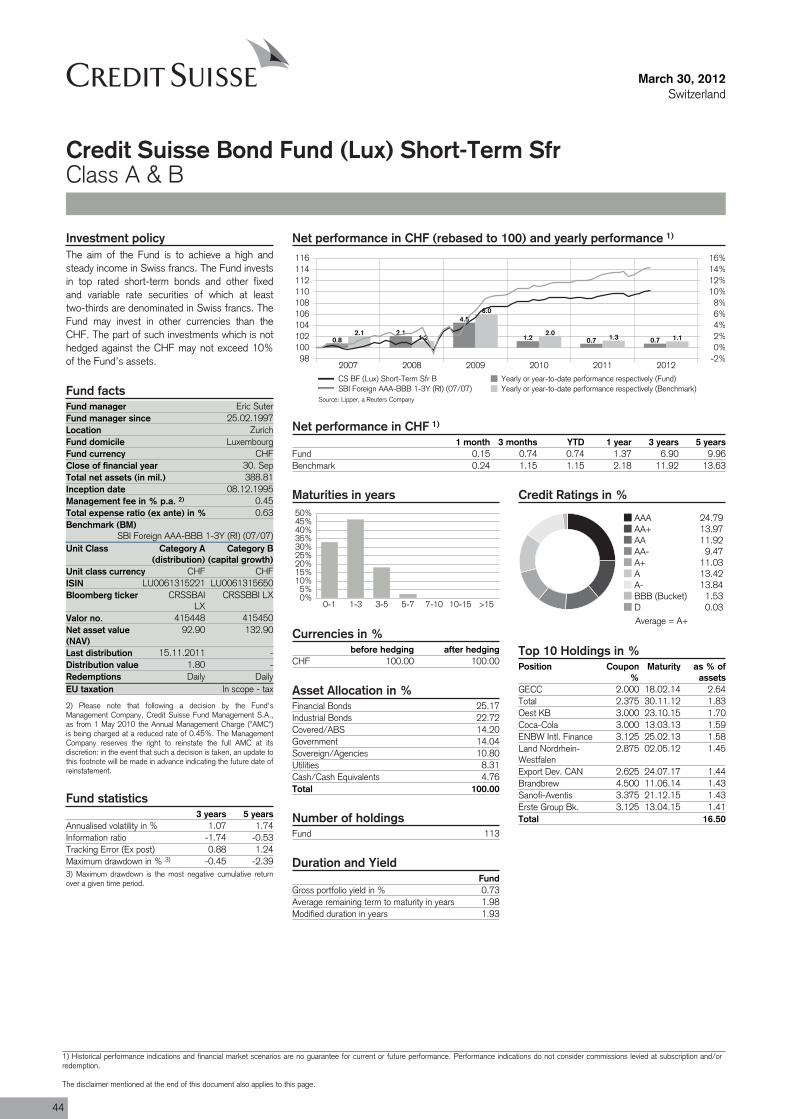

Credit Suisse Bond Fund (Lux) Short-Term Sfr B CHF 1.4 6.9 1.4 6.9 1.1 44

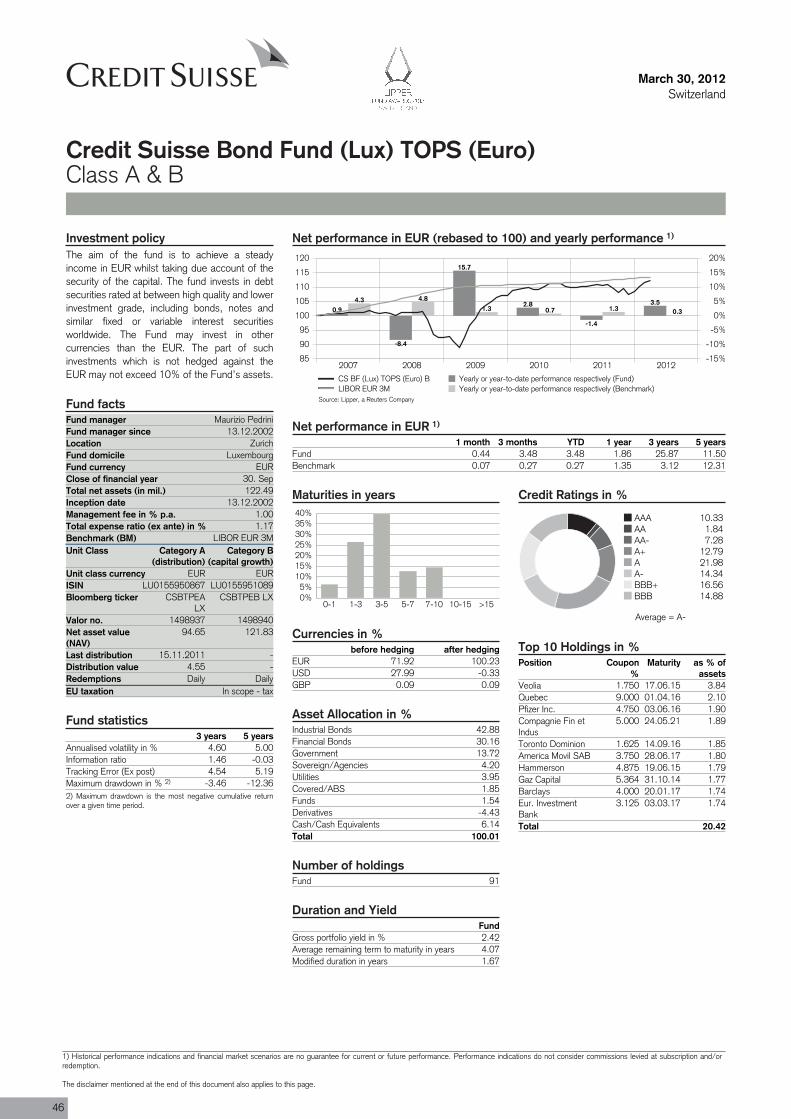

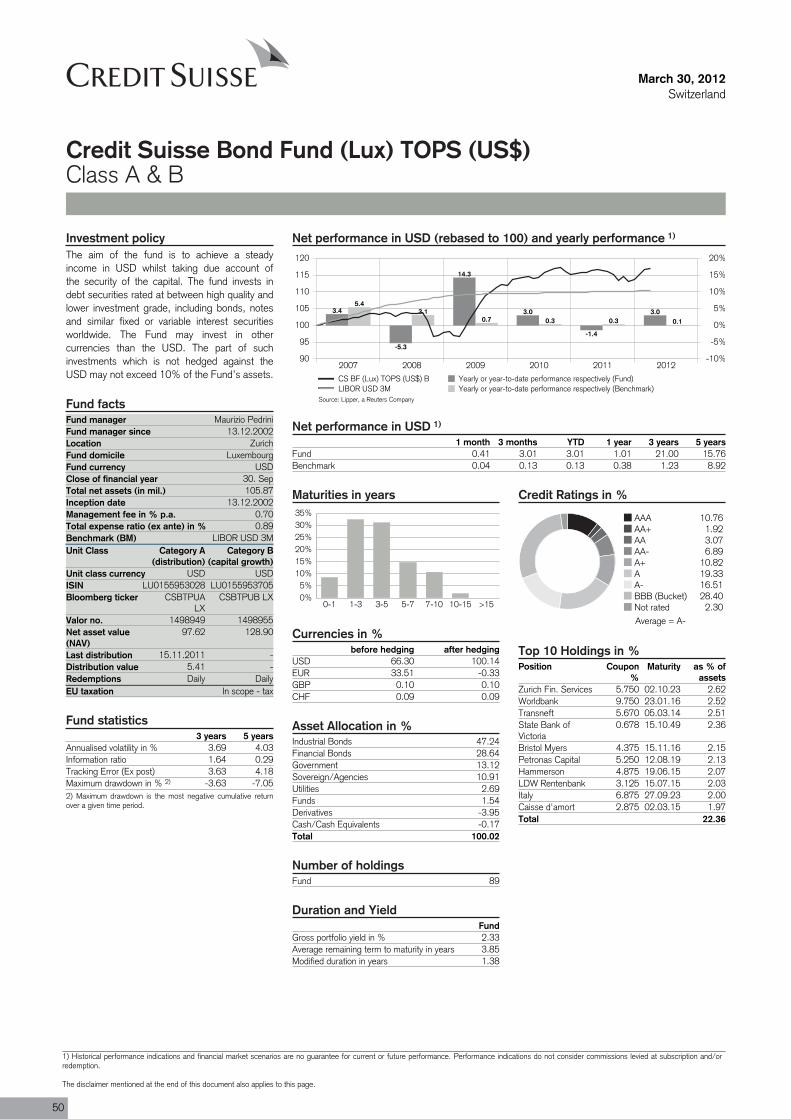

Credit Suisse Bond Fund (Lux) TOPS (Euro) B EUR 1.9 25.9 -5.6 0.4 4.6 46

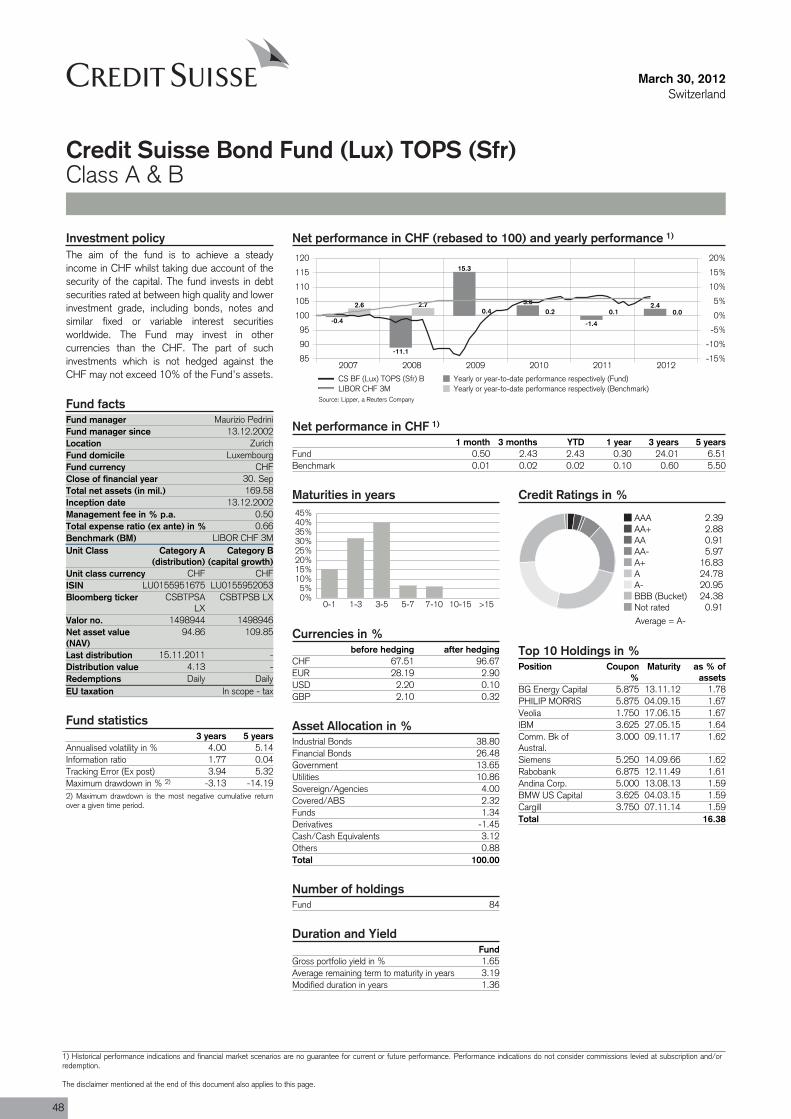

Credit Suisse Bond Fund (Lux) TOPS (Sfr) B CHF 0.3 24.0 0.3 24.0 4.0 48

Credit Suisse Bond Fund (Lux) TOPS (US$) B USD 1.0 21.0 -0.2 -3.8 3.7 50

Credit Suisse Commodity FundCredit Suisse Commodity Fund Plus (CH) Sfr B CHF -8.0 36.5 -8.0 36.5 20.8 52

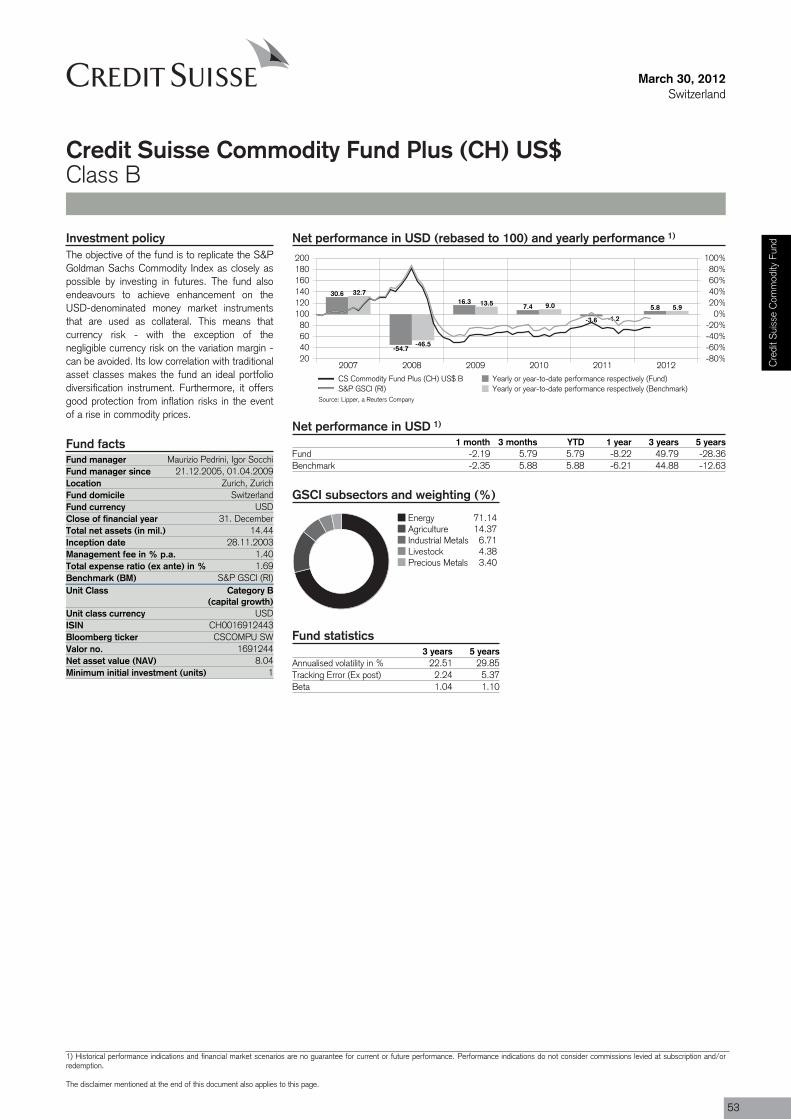

Credit Suisse Commodity Fund Plus (CH) US$ B USD -8.2 49.8 -9.3 19.1 22.5 53

Credit Suisse Commodity Fund Plus (CH) US$ I USD -7.2 54.8 -8.3 23.0 22.5 54

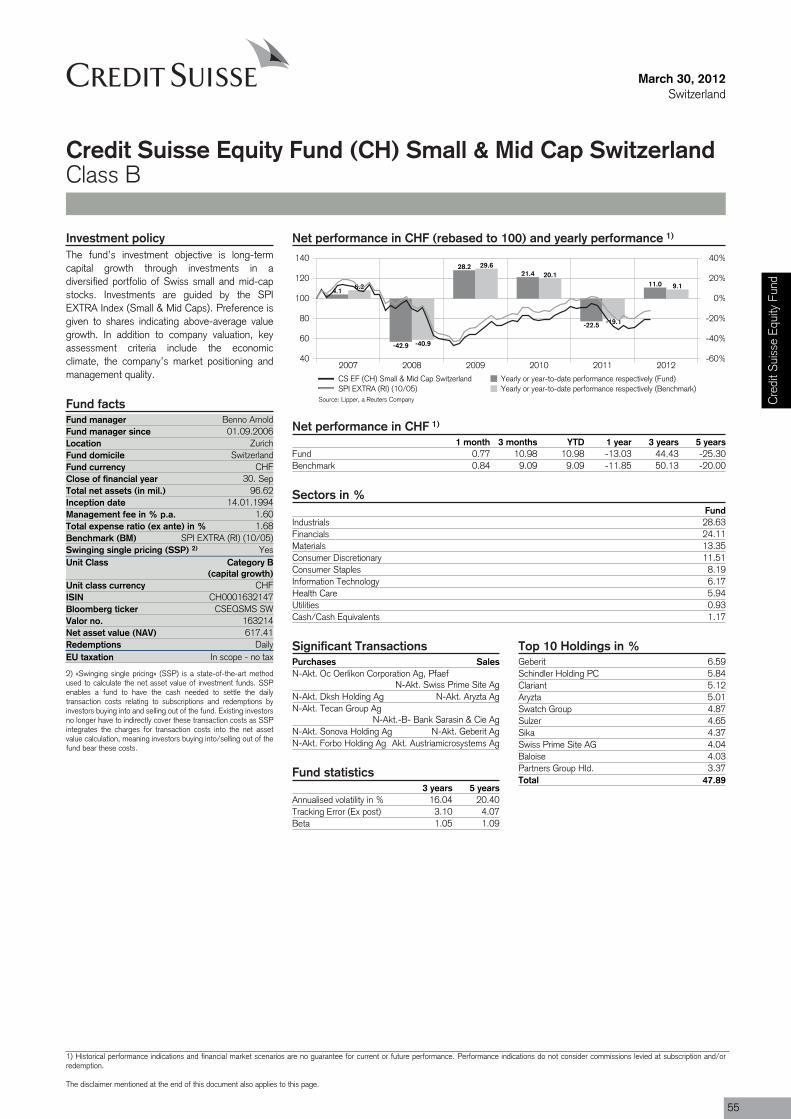

Credit Suisse Equity FundCredit Suisse Equity Fund (CH) Small & Mid Cap Switzerland CHF -13.0 44.4 -13.0 44.4 16.0 55

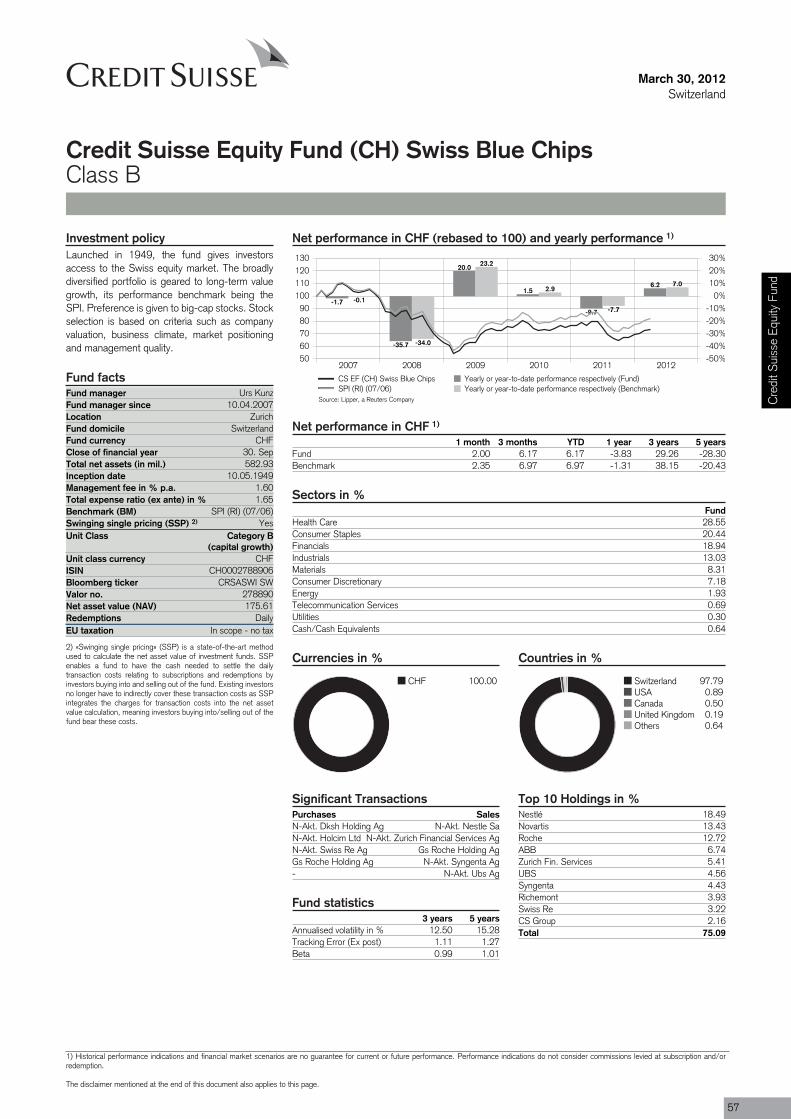

Credit Suisse Equity Fund (CH) Swiss Blue Chips CHF -3.8 29.3 -3.8 29.3 12.5 57

Credit Suisse Equity Fund (CH) Swissac B CHF -5.7 29.9 -5.7 29.9 12.8 59

Credit Suisse Equity Fund (Lux) Brazil B USD -19.0 74.1 -20.0 38.4 32.1 61

Credit Suisse Equity Fund (Lux) Brazil I USD -18.3 n/a -19.2 n/a n/a 63

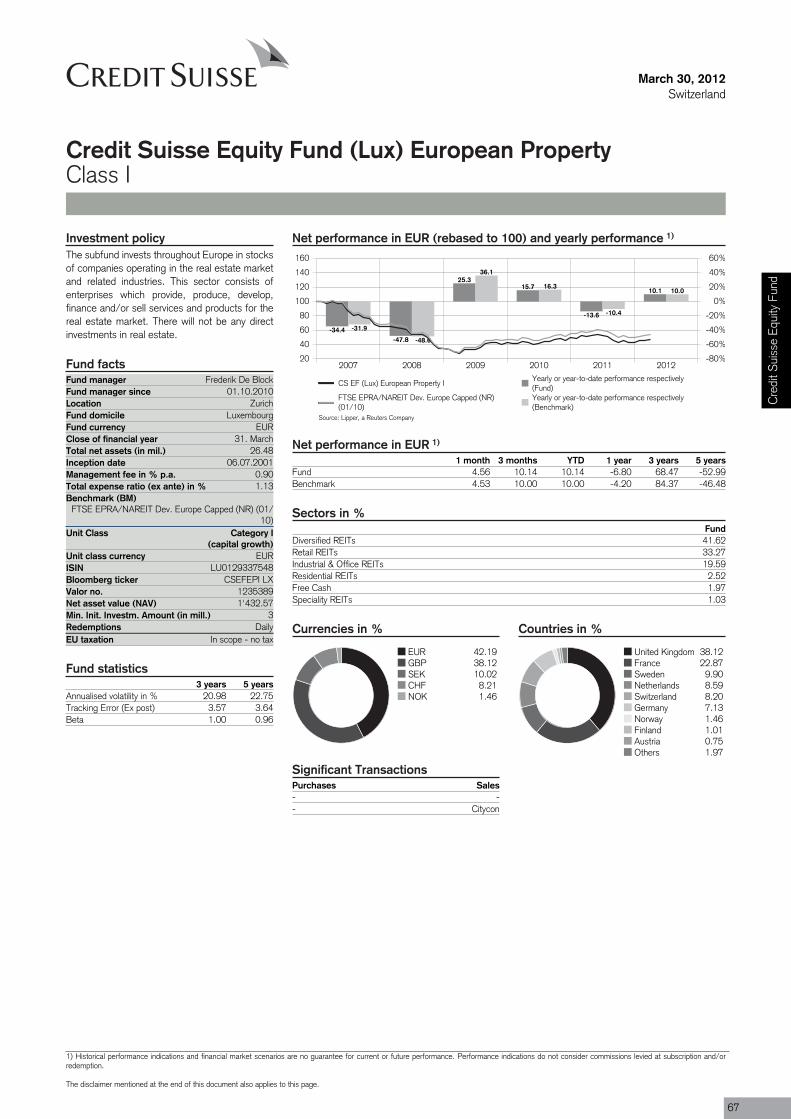

Credit Suisse Equity Fund (Lux) European Property B EUR -7.8 63.4 -14.5 30.2 20.9 65

Fund Performanceas of 30.03.2012

6

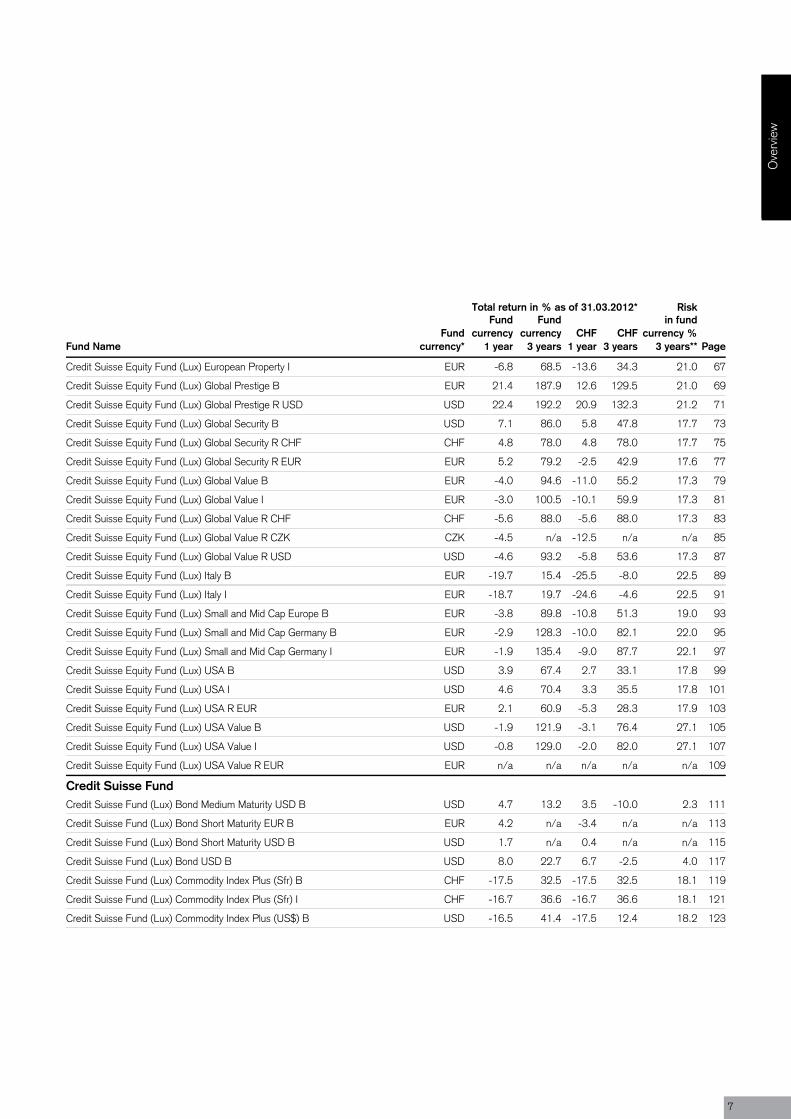

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

Credit Suisse Equity Fund (Lux) European Property I EUR -6.8 68.5 -13.6 34.3 21.0 67

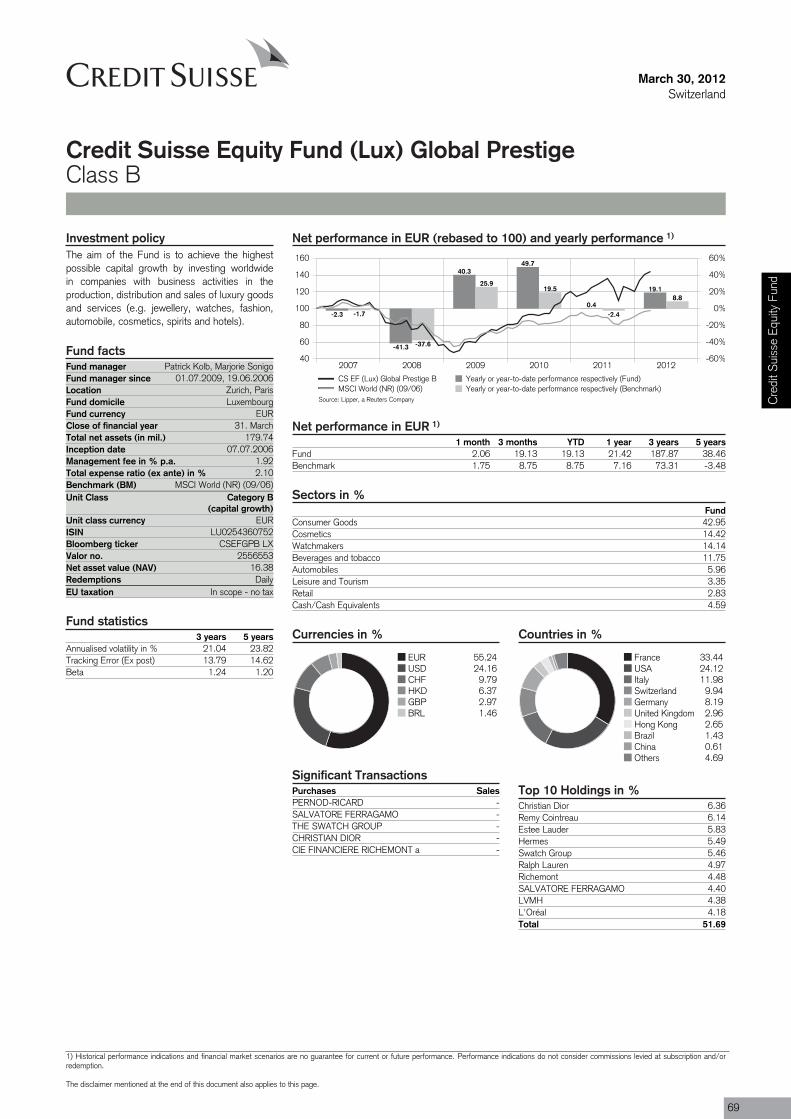

Credit Suisse Equity Fund (Lux) Global Prestige B EUR 21.4 187.9 12.6 129.5 21.0 69

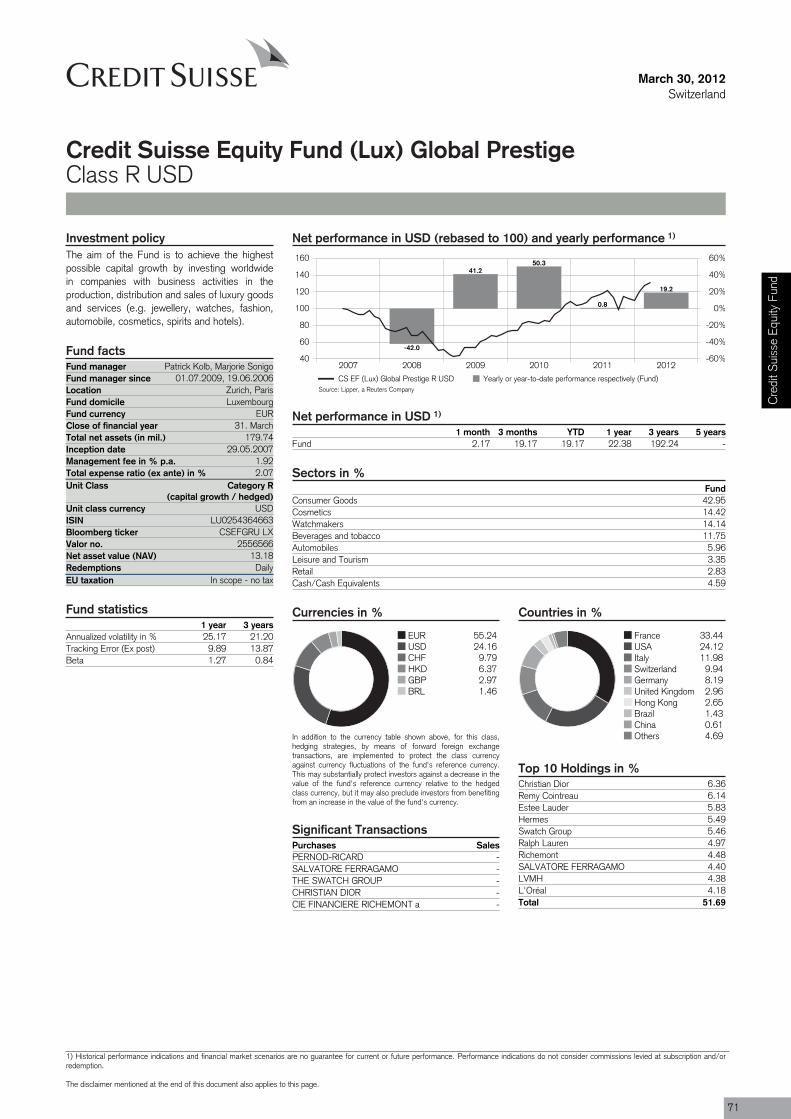

Credit Suisse Equity Fund (Lux) Global Prestige R USD USD 22.4 192.2 20.9 132.3 21.2 71

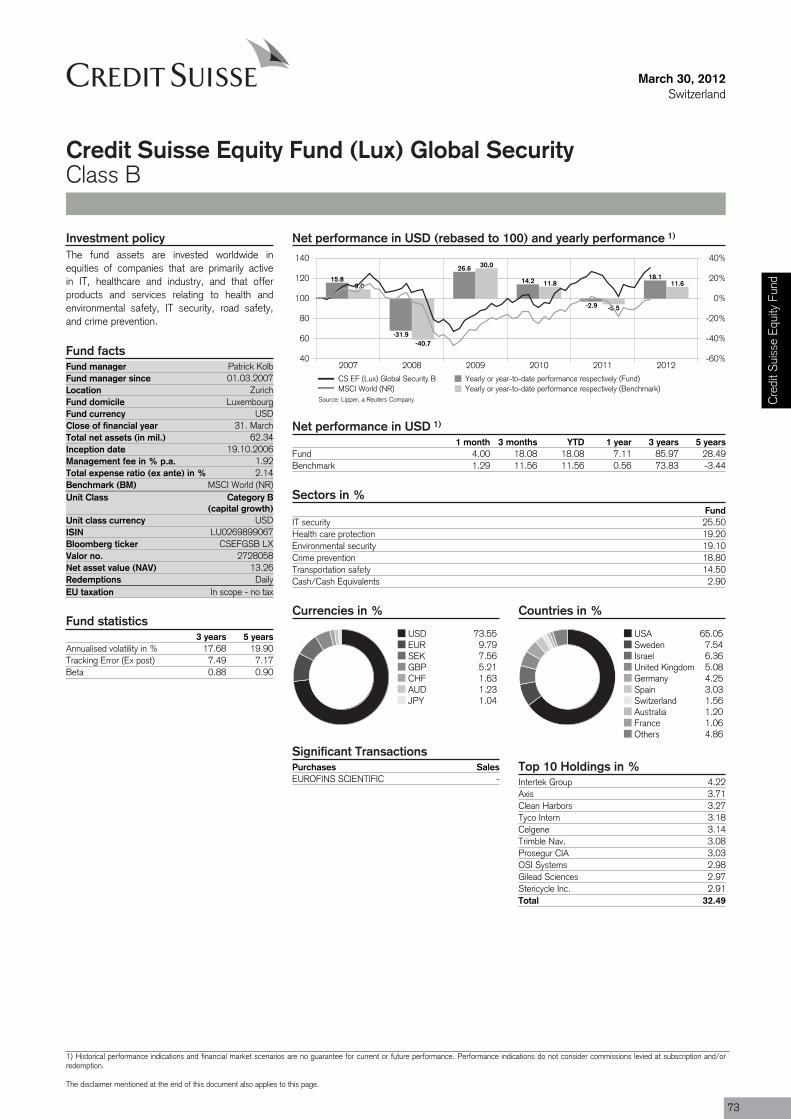

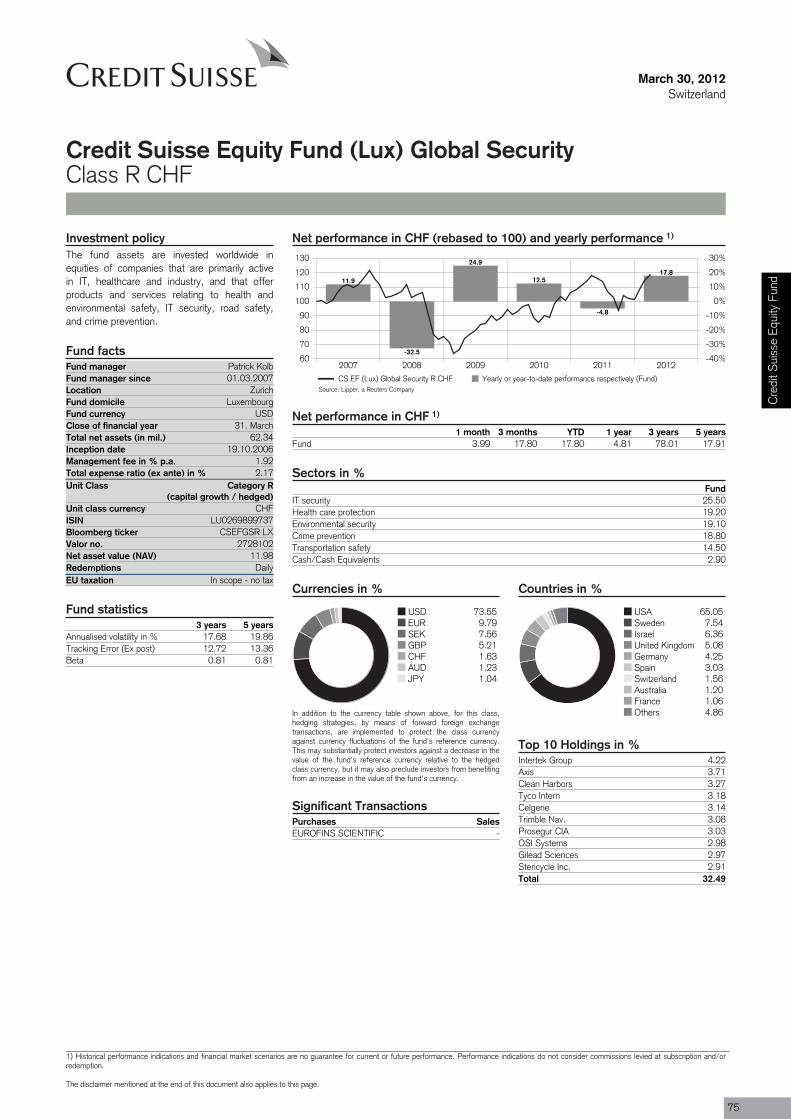

Credit Suisse Equity Fund (Lux) Global Security B USD 7.1 86.0 5.8 47.8 17.7 73

Credit Suisse Equity Fund (Lux) Global Security R CHF CHF 4.8 78.0 4.8 78.0 17.7 75

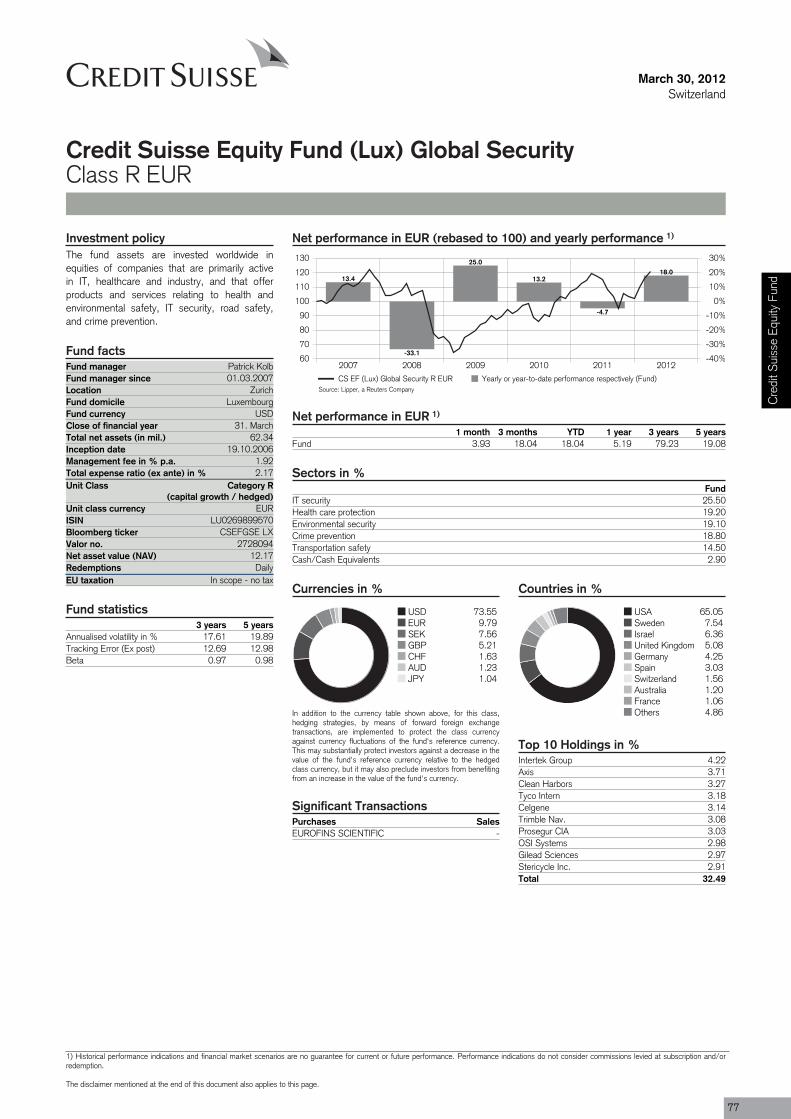

Credit Suisse Equity Fund (Lux) Global Security R EUR EUR 5.2 79.2 -2.5 42.9 17.6 77

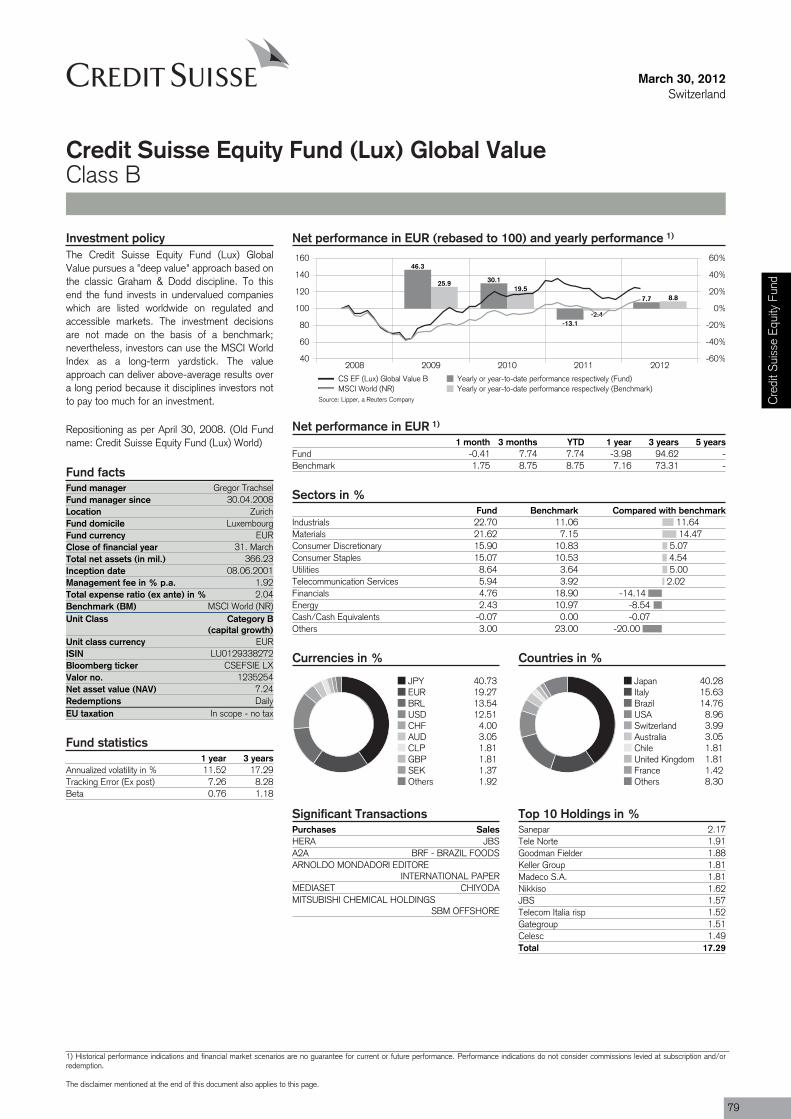

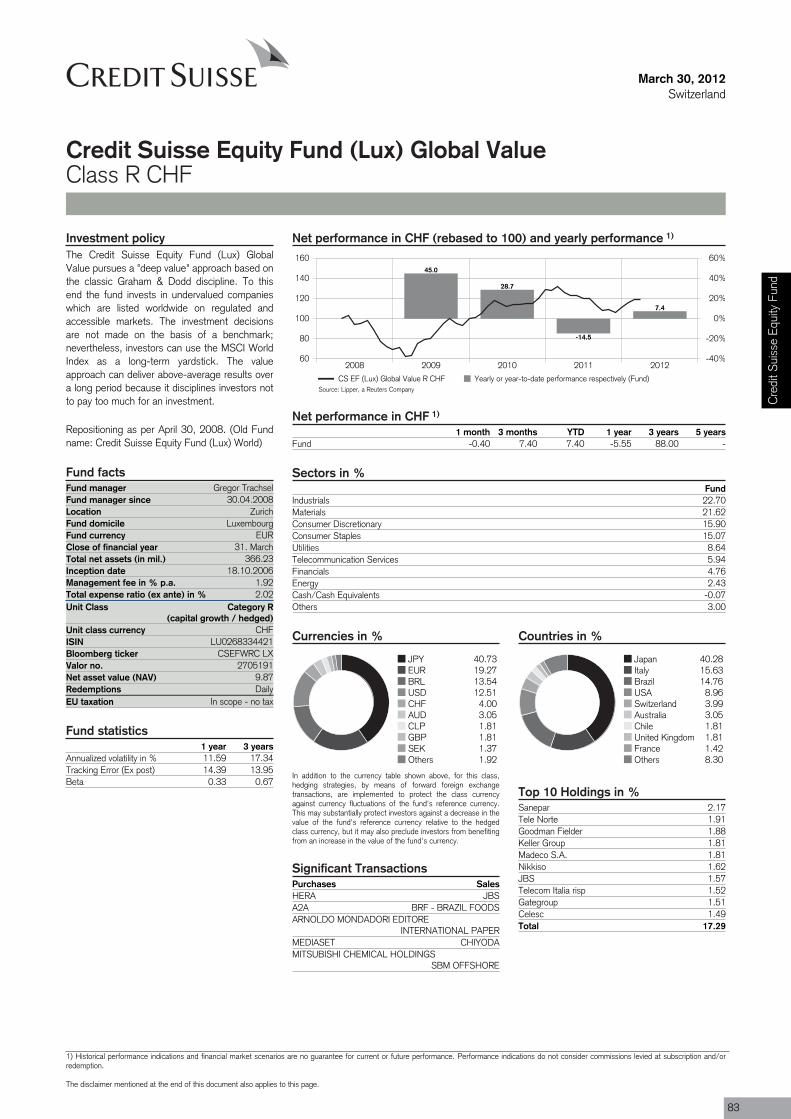

Credit Suisse Equity Fund (Lux) Global Value B EUR -4.0 94.6 -11.0 55.2 17.3 79

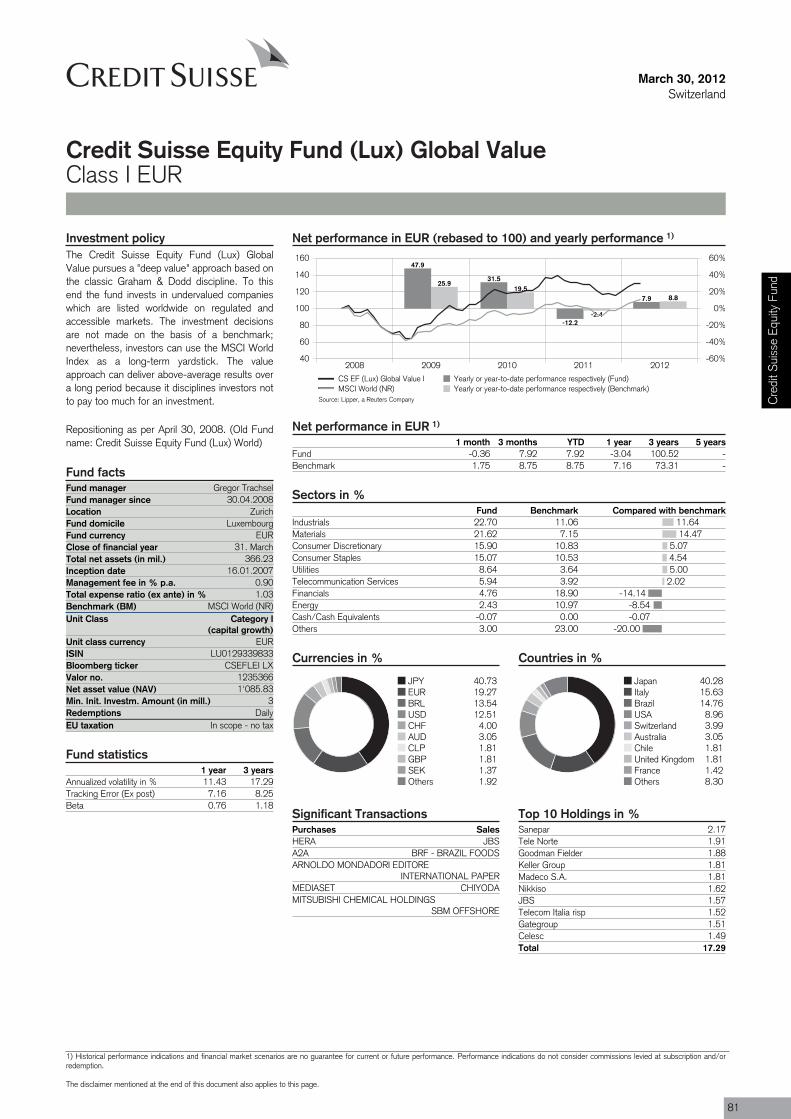

Credit Suisse Equity Fund (Lux) Global Value I EUR -3.0 100.5 -10.1 59.9 17.3 81

Credit Suisse Equity Fund (Lux) Global Value R CHF CHF -5.6 88.0 -5.6 88.0 17.3 83

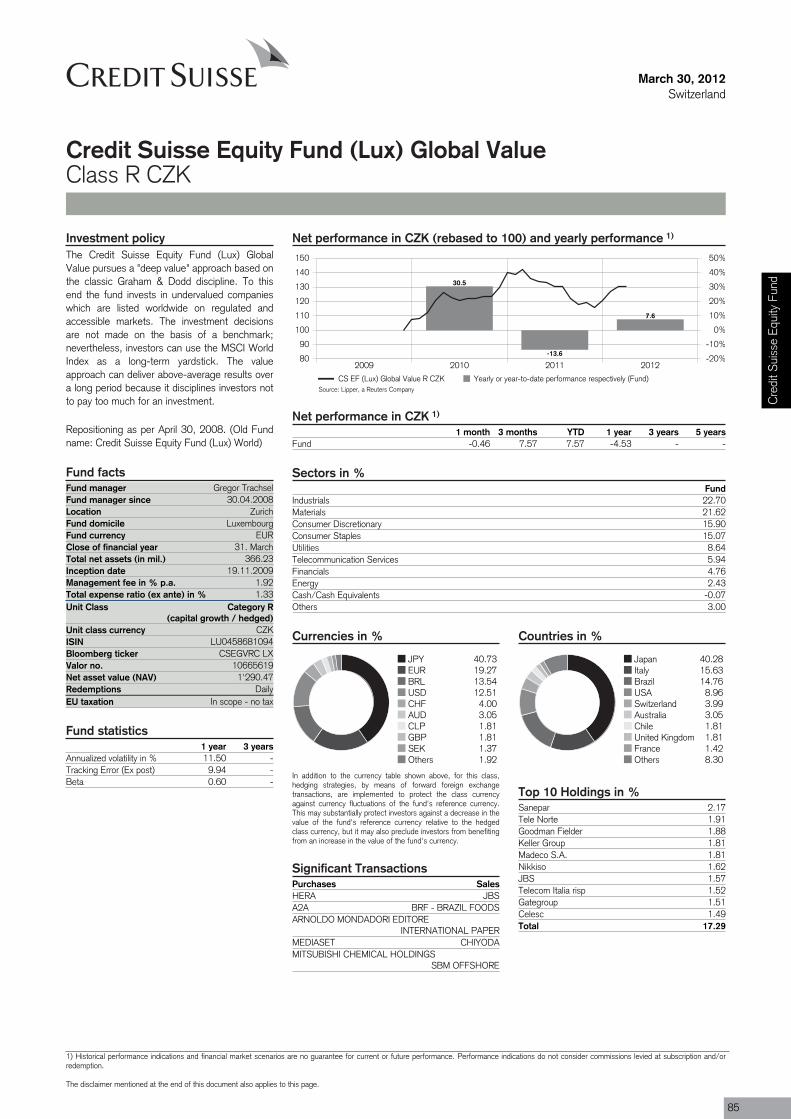

Credit Suisse Equity Fund (Lux) Global Value R CZK CZK -4.5 n/a -12.5 n/a n/a 85

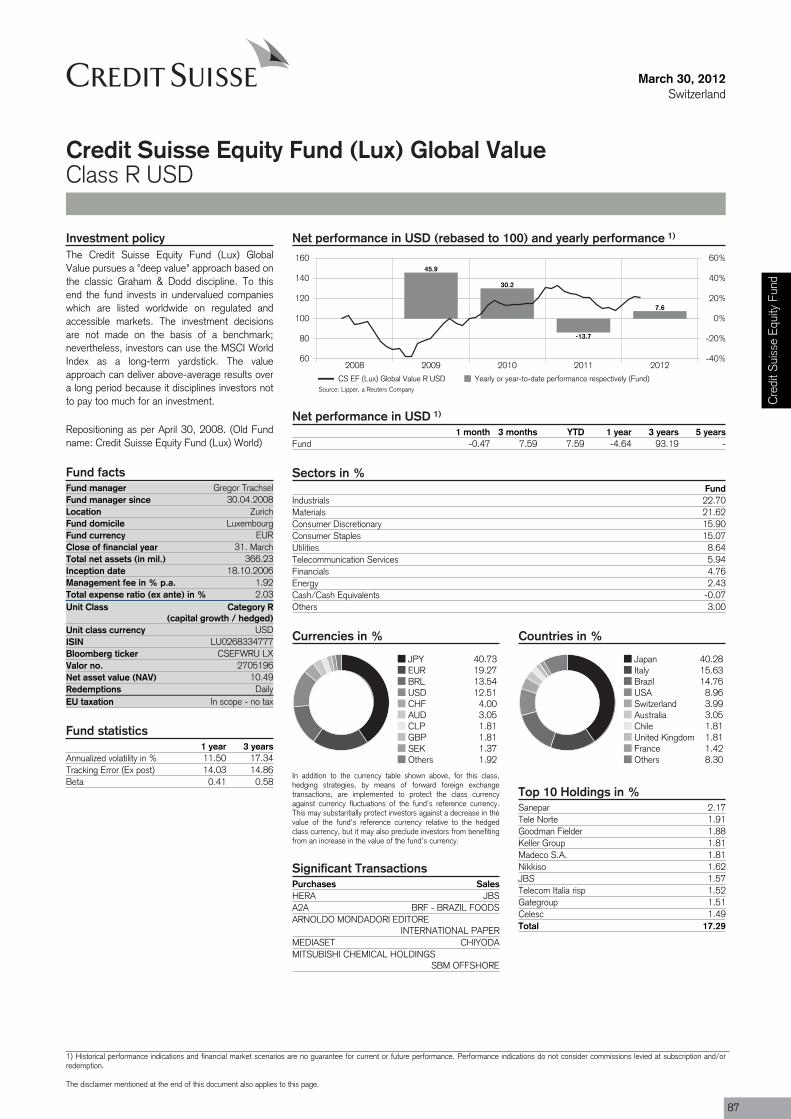

Credit Suisse Equity Fund (Lux) Global Value R USD USD -4.6 93.2 -5.8 53.6 17.3 87

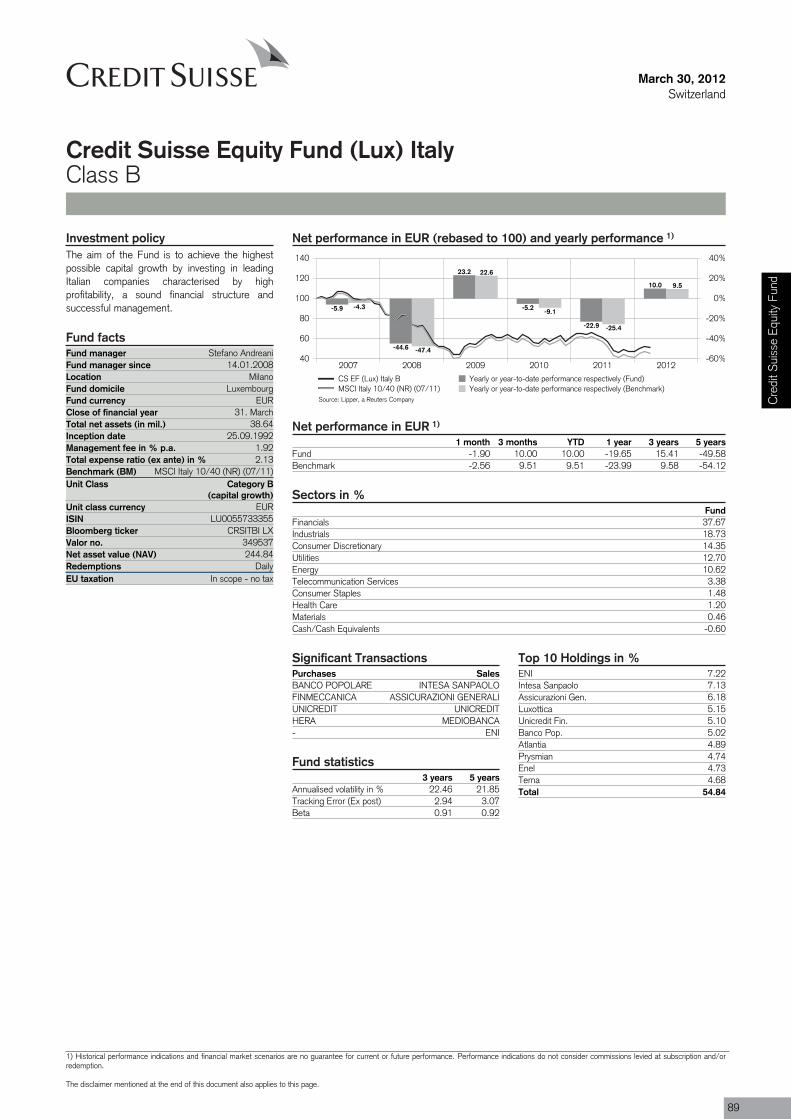

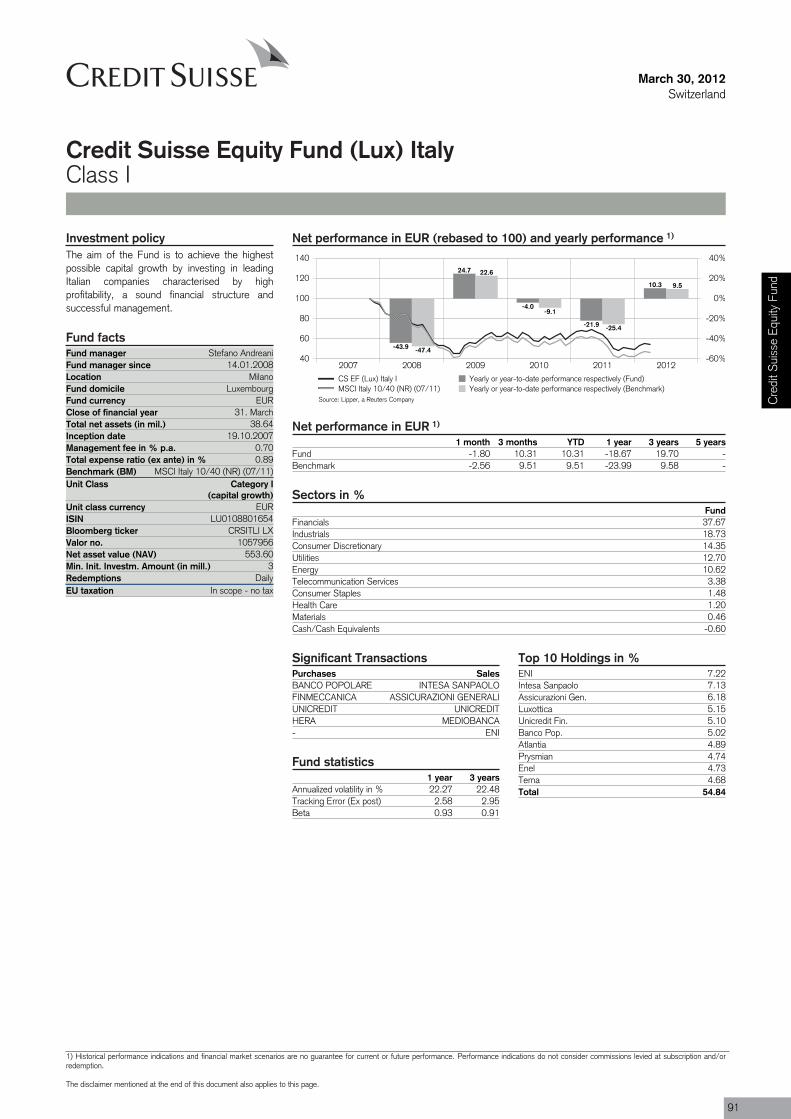

Credit Suisse Equity Fund (Lux) Italy B EUR -19.7 15.4 -25.5 -8.0 22.5 89

Credit Suisse Equity Fund (Lux) Italy I EUR -18.7 19.7 -24.6 -4.6 22.5 91

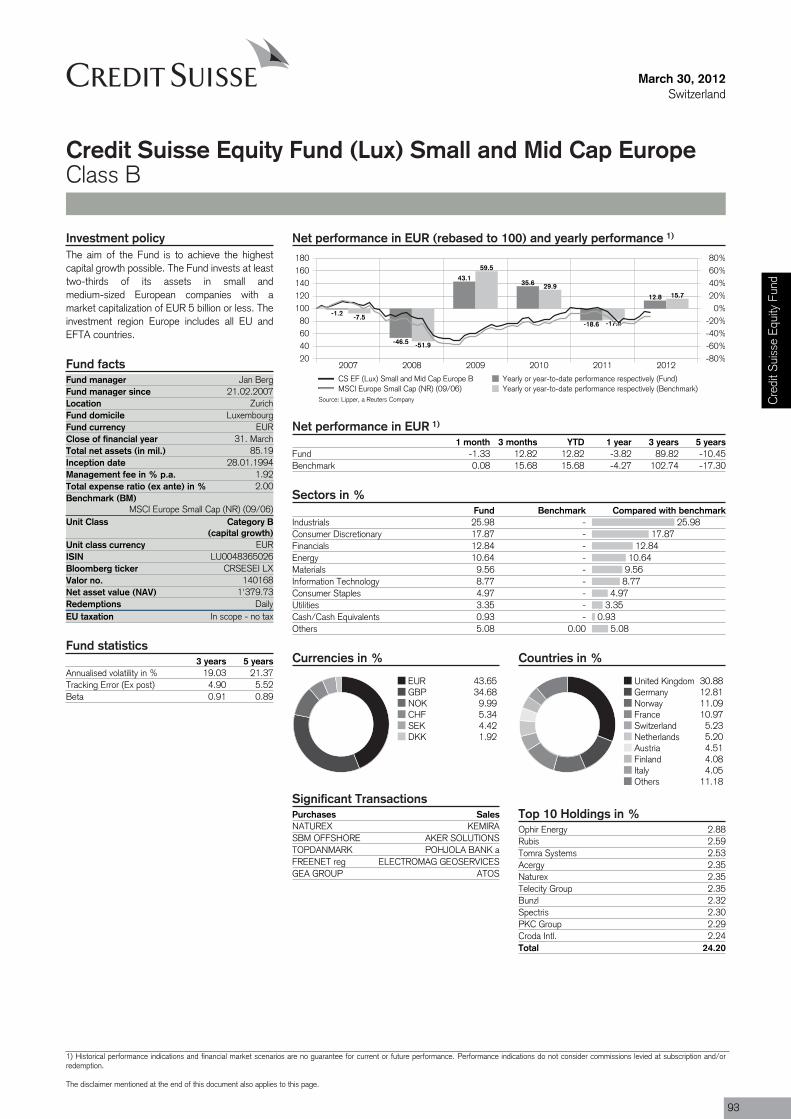

Credit Suisse Equity Fund (Lux) Small and Mid Cap Europe B EUR -3.8 89.8 -10.8 51.3 19.0 93

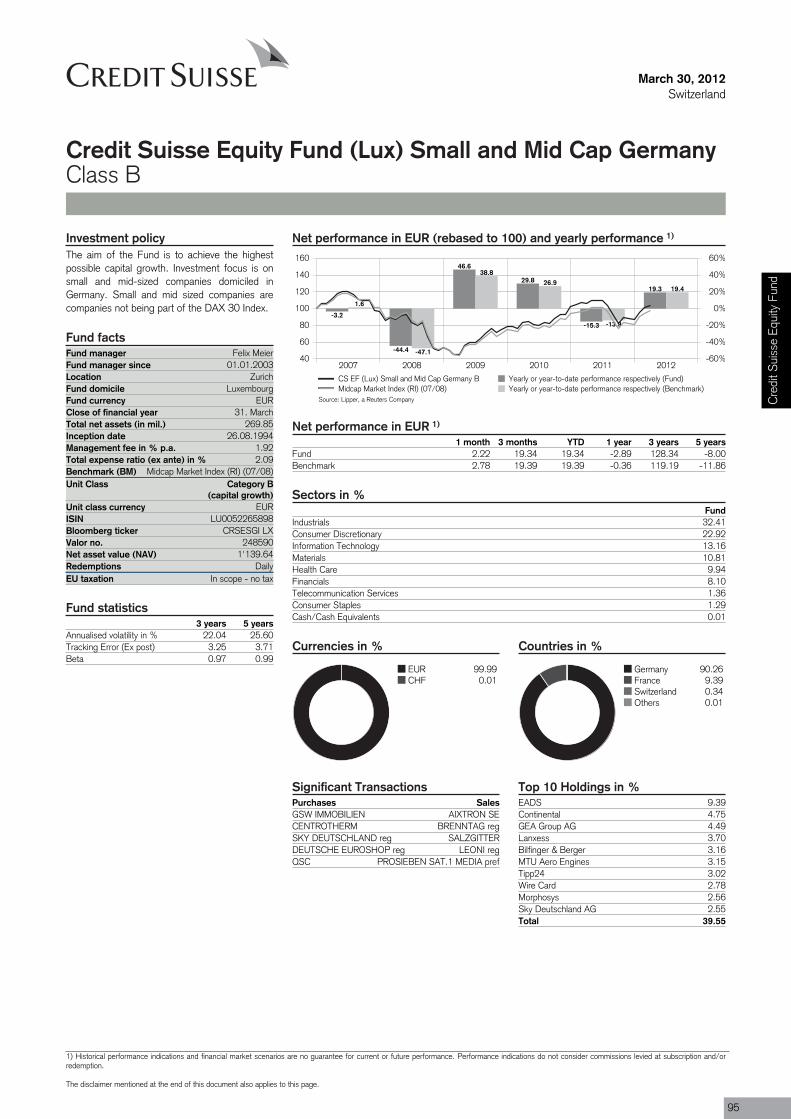

Credit Suisse Equity Fund (Lux) Small and Mid Cap Germany B EUR -2.9 128.3 -10.0 82.1 22.0 95

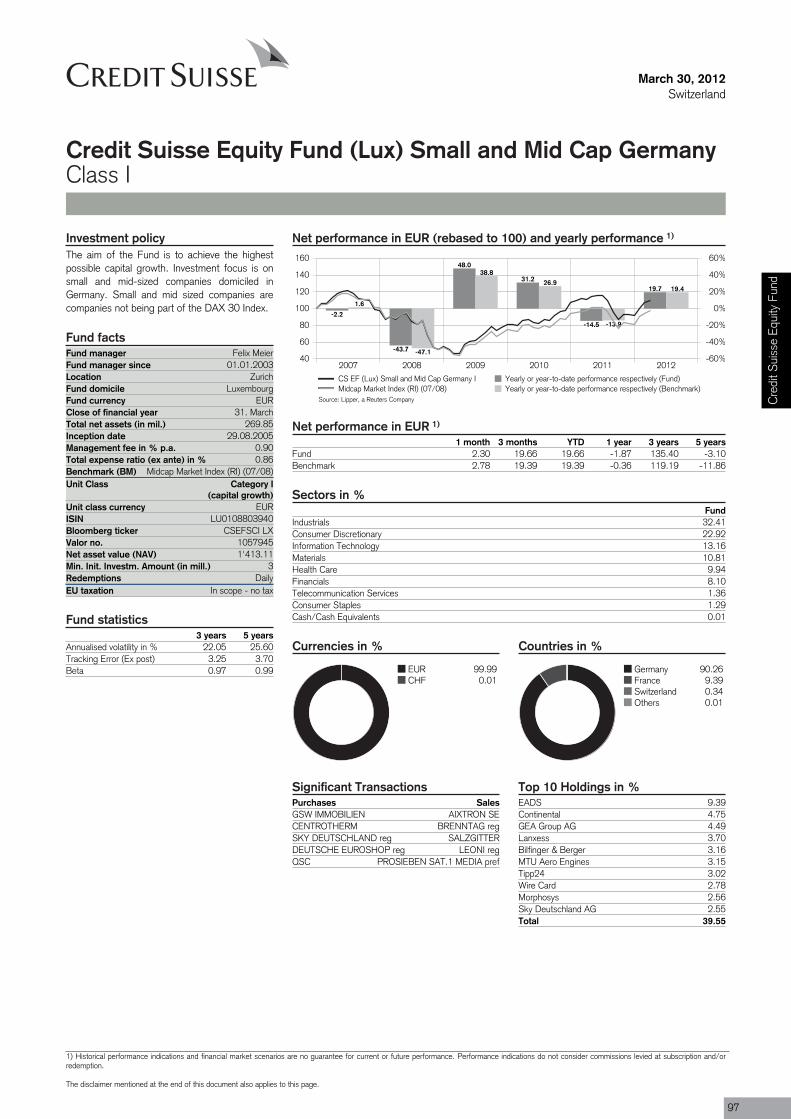

Credit Suisse Equity Fund (Lux) Small and Mid Cap Germany I EUR -1.9 135.4 -9.0 87.7 22.1 97

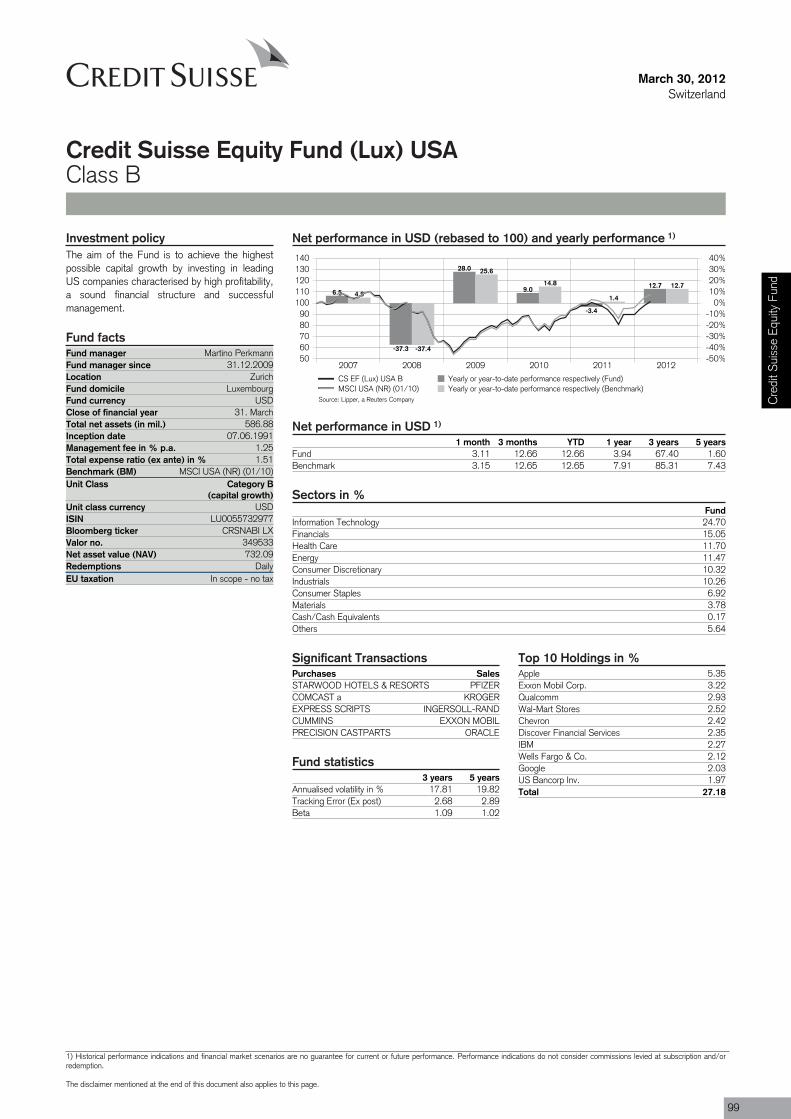

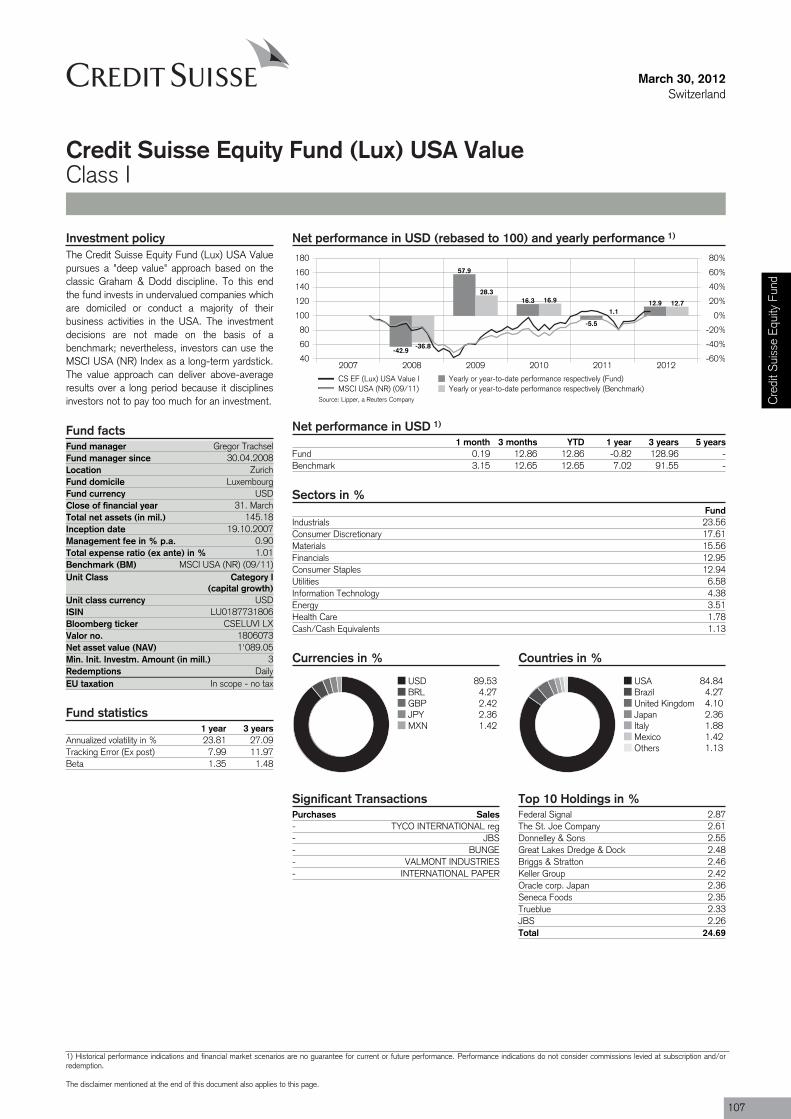

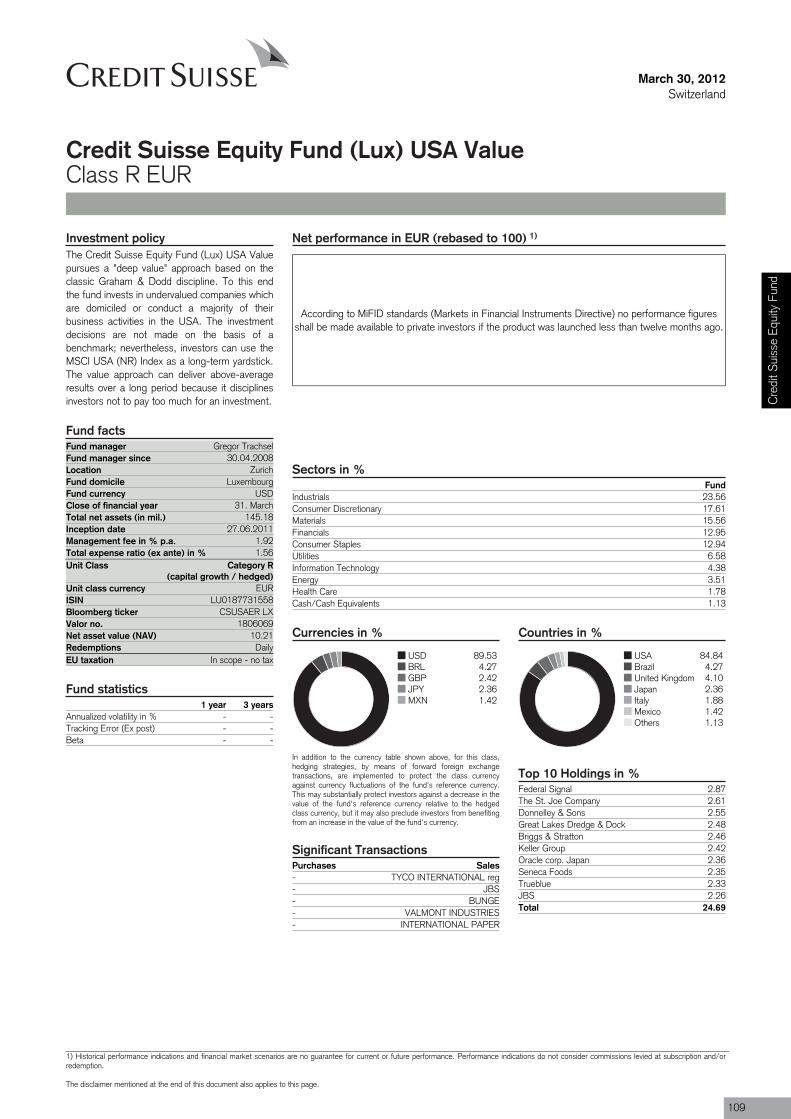

Credit Suisse Equity Fund (Lux) USA B USD 3.9 67.4 2.7 33.1 17.8 99

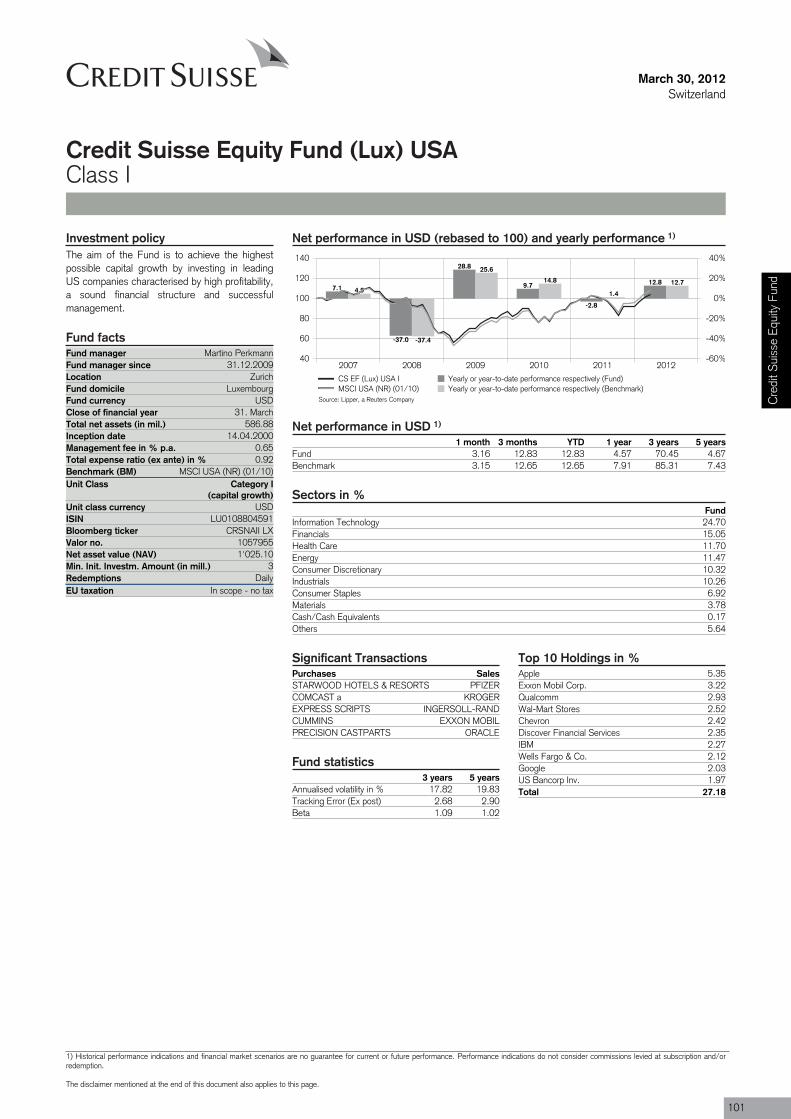

Credit Suisse Equity Fund (Lux) USA I USD 4.6 70.4 3.3 35.5 17.8 101

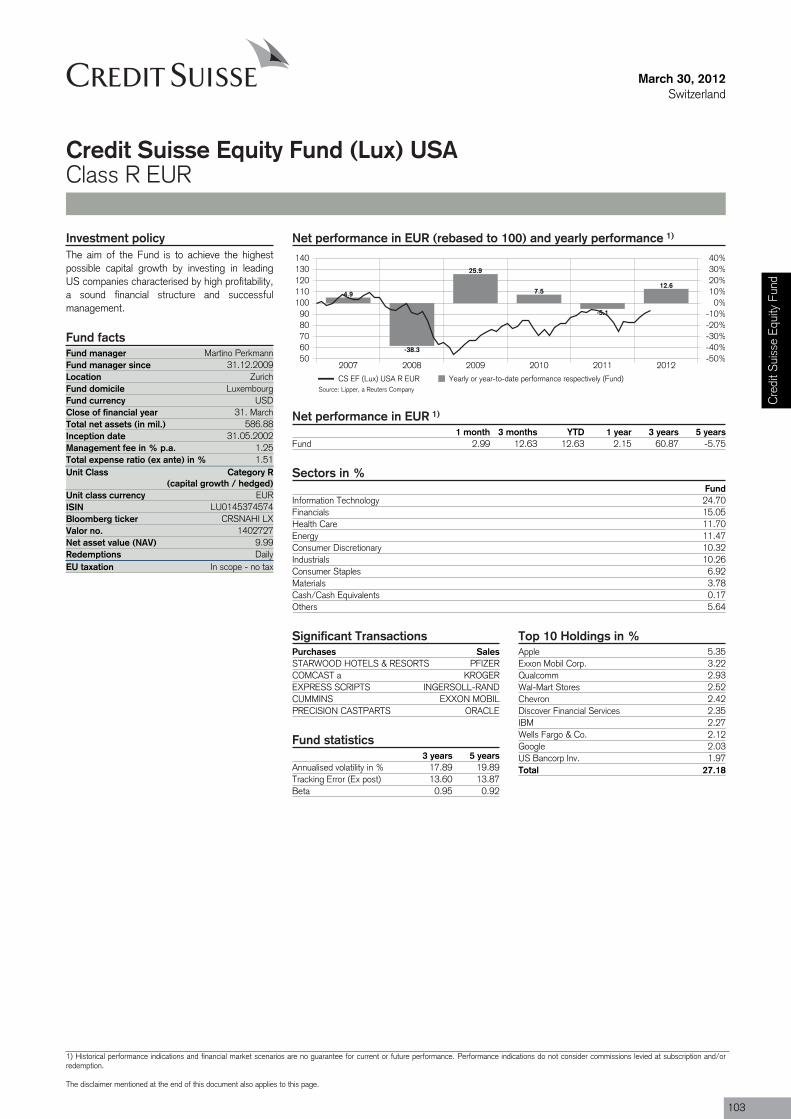

Credit Suisse Equity Fund (Lux) USA R EUR EUR 2.1 60.9 -5.3 28.3 17.9 103

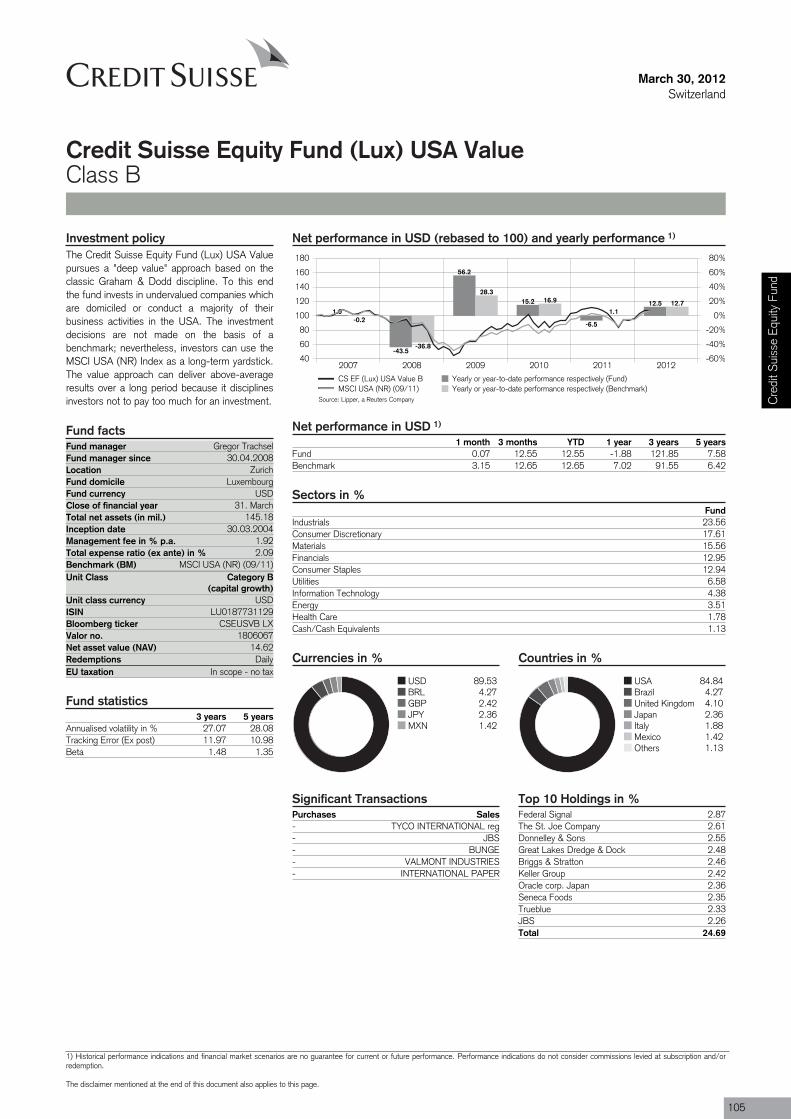

Credit Suisse Equity Fund (Lux) USA Value B USD -1.9 121.9 -3.1 76.4 27.1 105

Credit Suisse Equity Fund (Lux) USA Value I USD -0.8 129.0 -2.0 82.0 27.1 107

Credit Suisse Equity Fund (Lux) USA Value R EUR EUR n/a n/a n/a n/a n/a 109

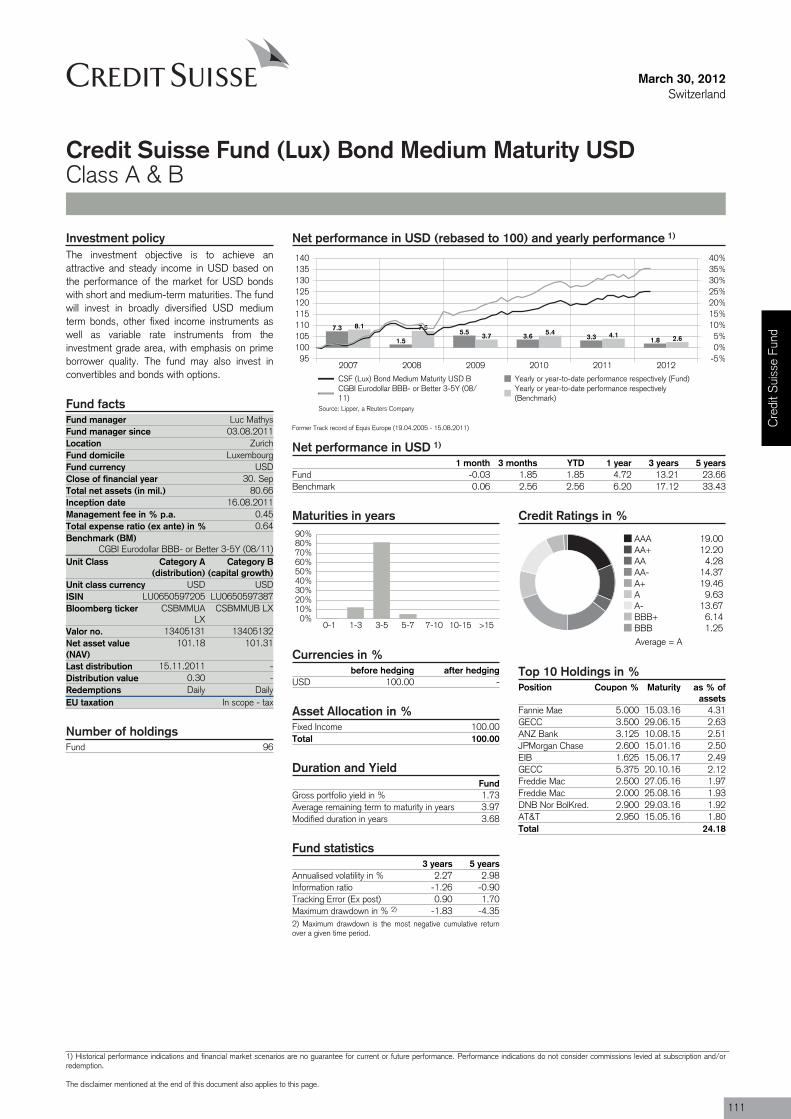

Credit Suisse FundCredit Suisse Fund (Lux) Bond Medium Maturity USD B USD 4.7 13.2 3.5 -10.0 2.3 111

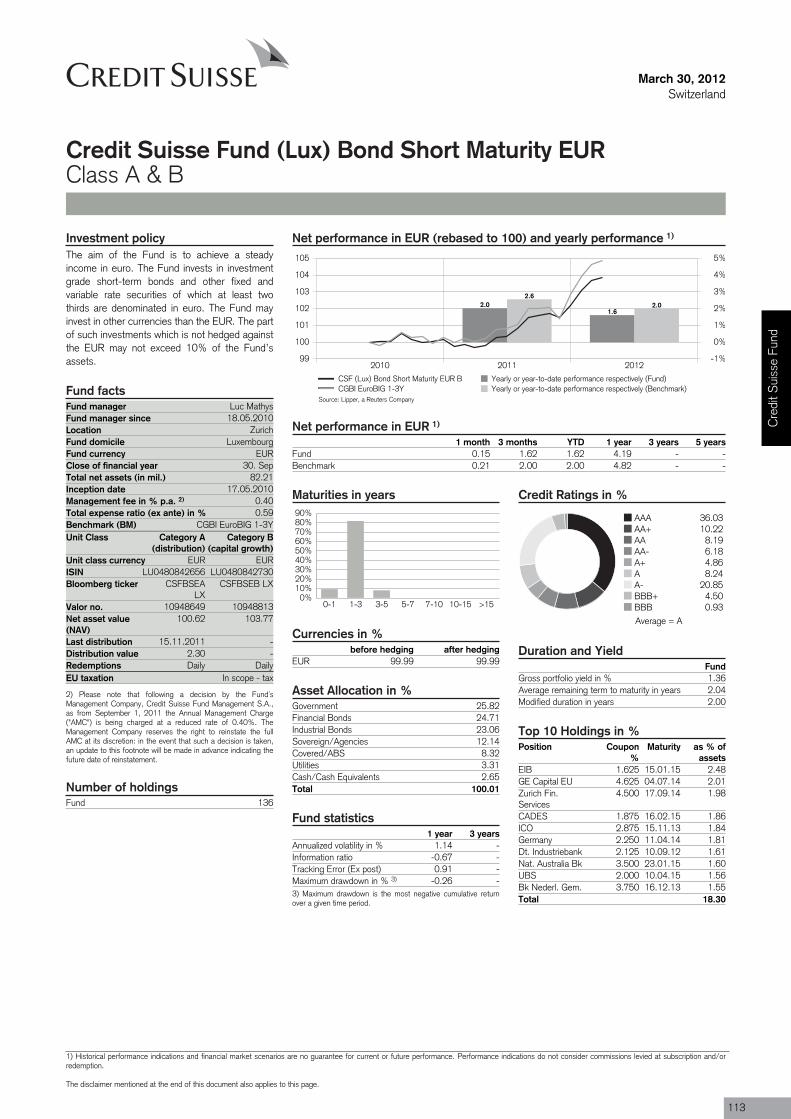

Credit Suisse Fund (Lux) Bond Short Maturity EUR B EUR 4.2 n/a -3.4 n/a n/a 113

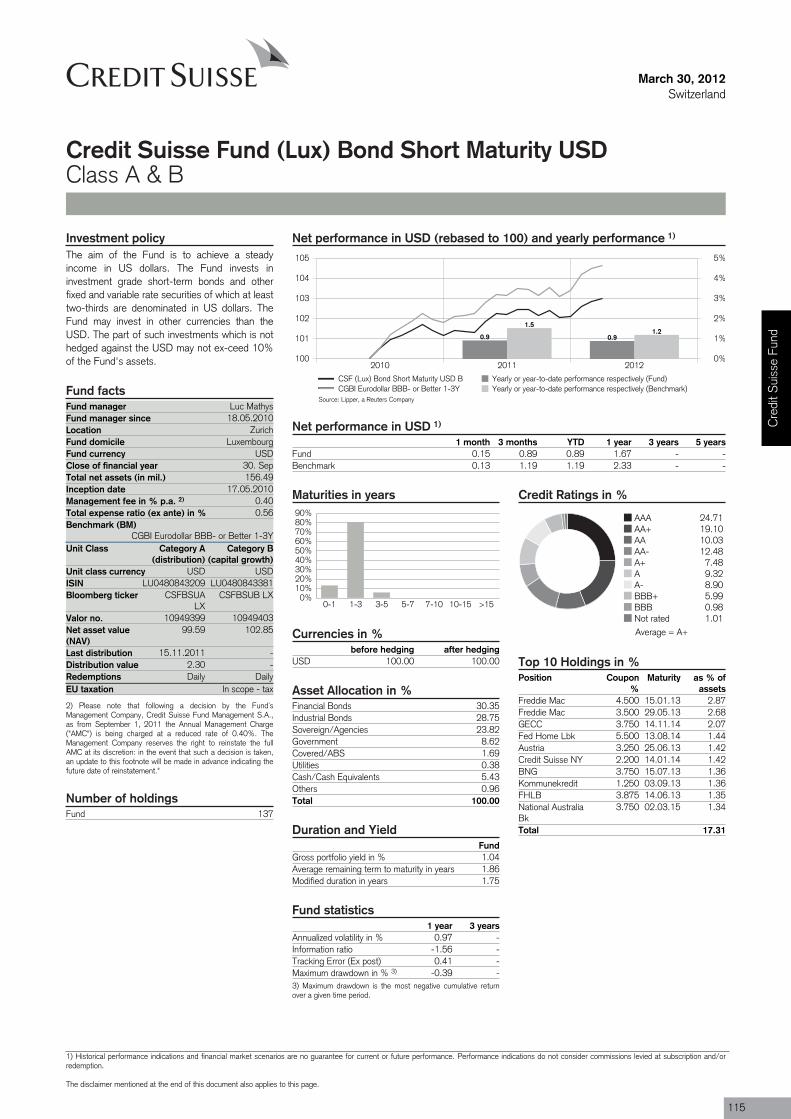

Credit Suisse Fund (Lux) Bond Short Maturity USD B USD 1.7 n/a 0.4 n/a n/a 115

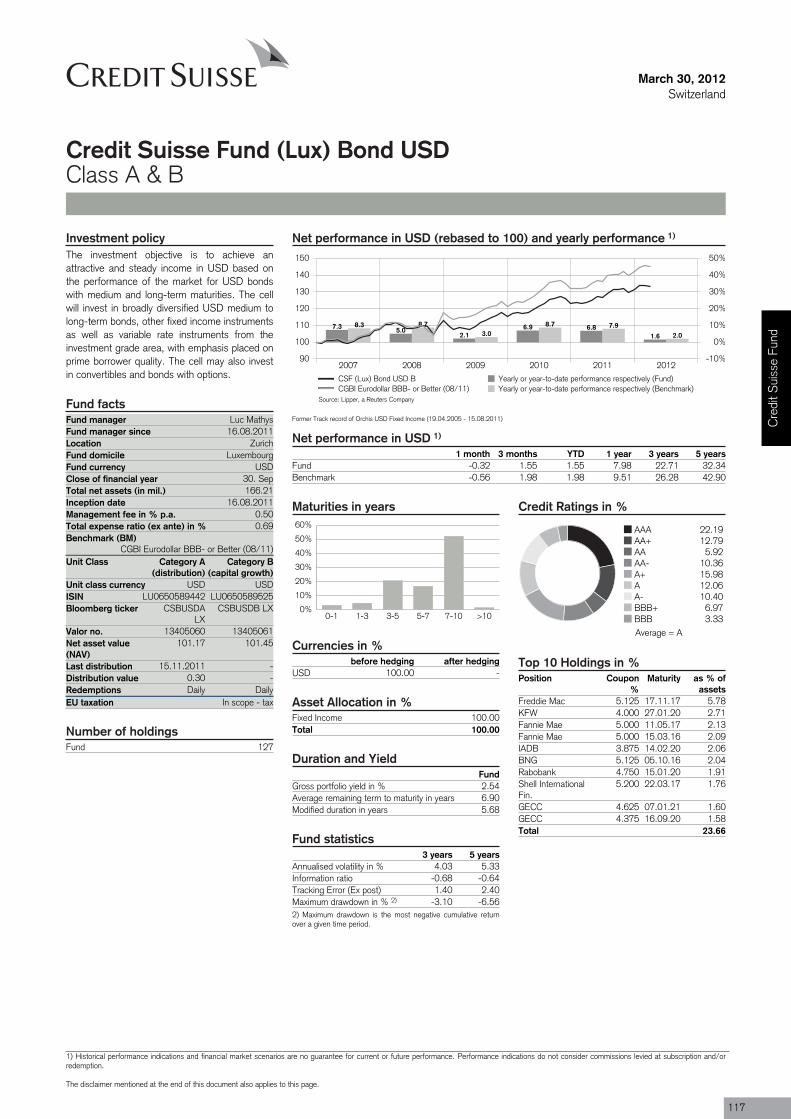

Credit Suisse Fund (Lux) Bond USD B USD 8.0 22.7 6.7 -2.5 4.0 117

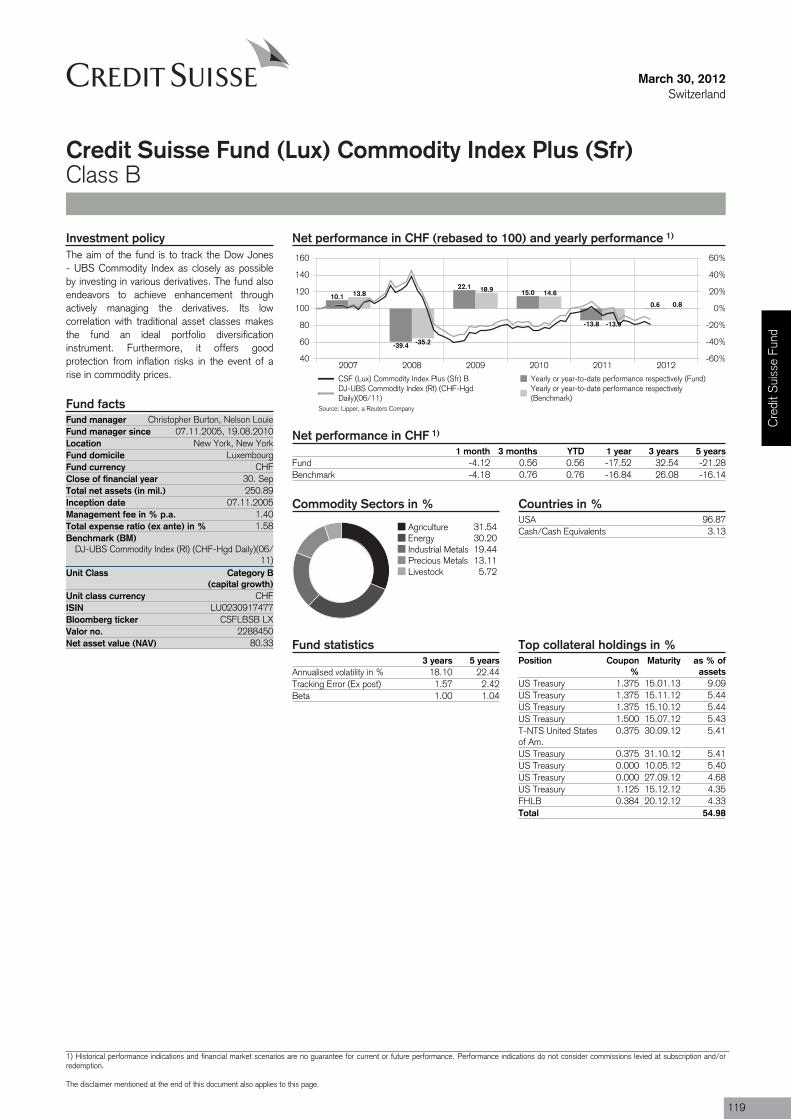

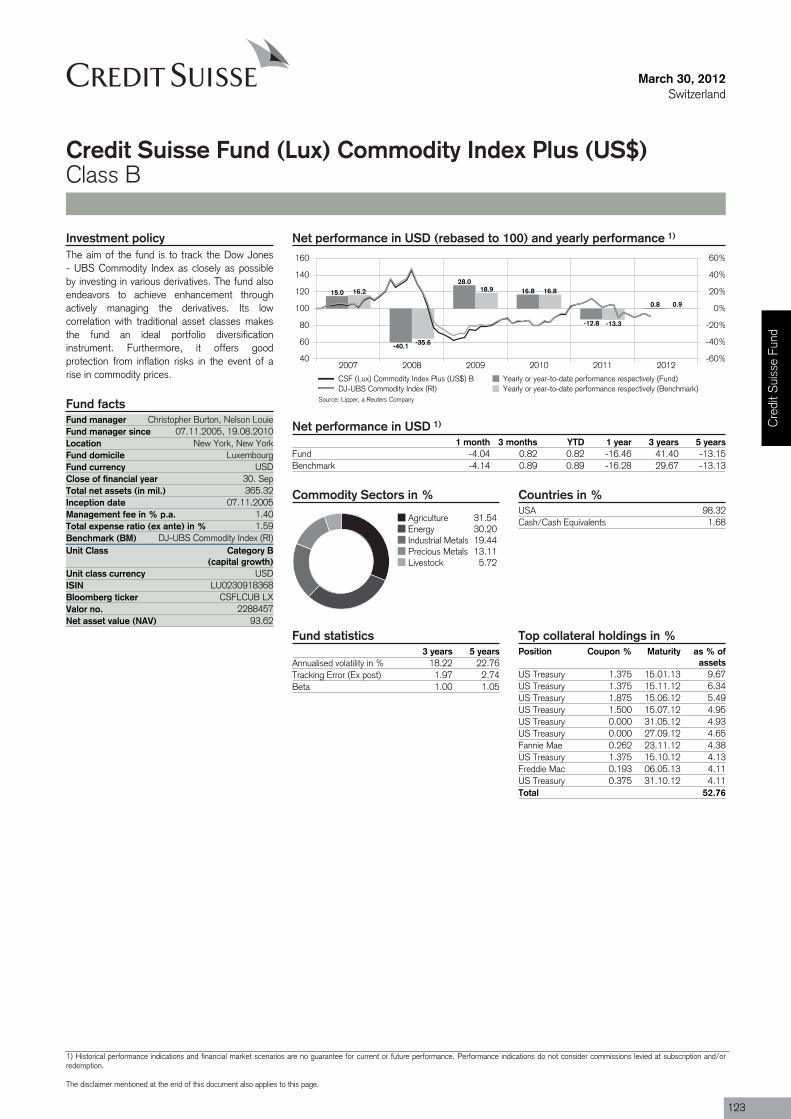

Credit Suisse Fund (Lux) Commodity Index Plus (Sfr) B CHF -17.5 32.5 -17.5 32.5 18.1 119

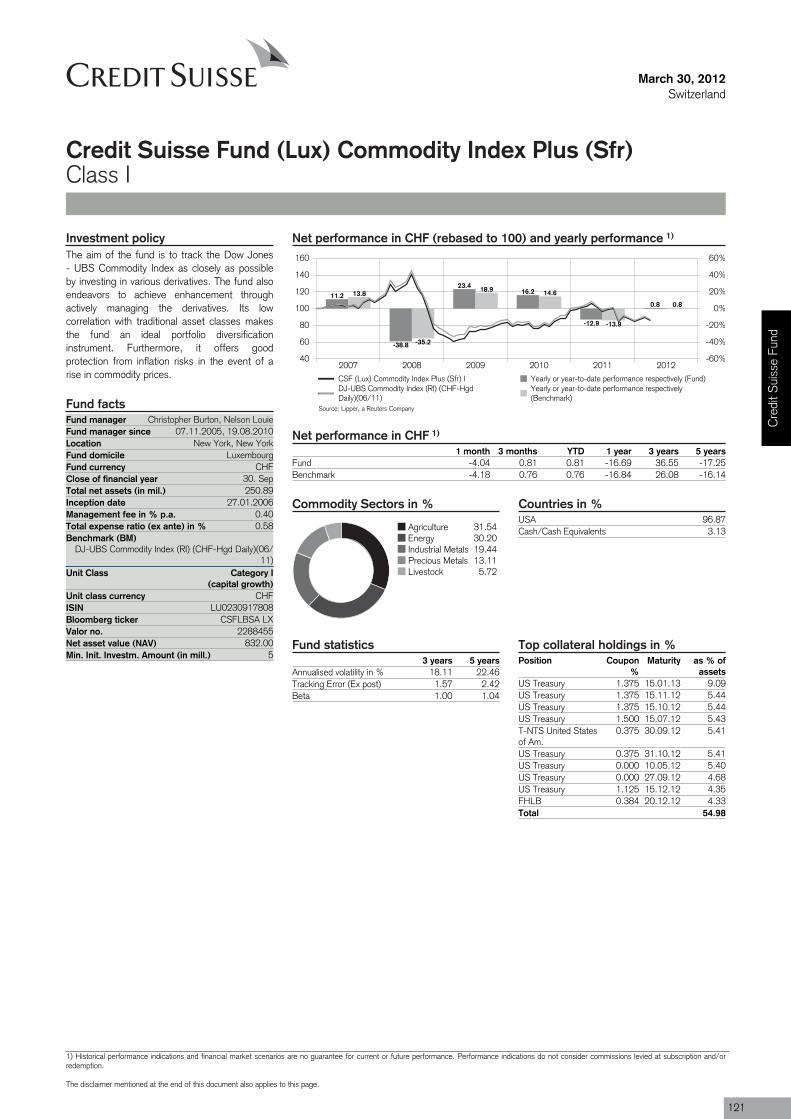

Credit Suisse Fund (Lux) Commodity Index Plus (Sfr) I CHF -16.7 36.6 -16.7 36.6 18.1 121

Credit Suisse Fund (Lux) Commodity Index Plus (US$) B USD -16.5 41.4 -17.5 12.4 18.2 123

Ove

rvie

w

7

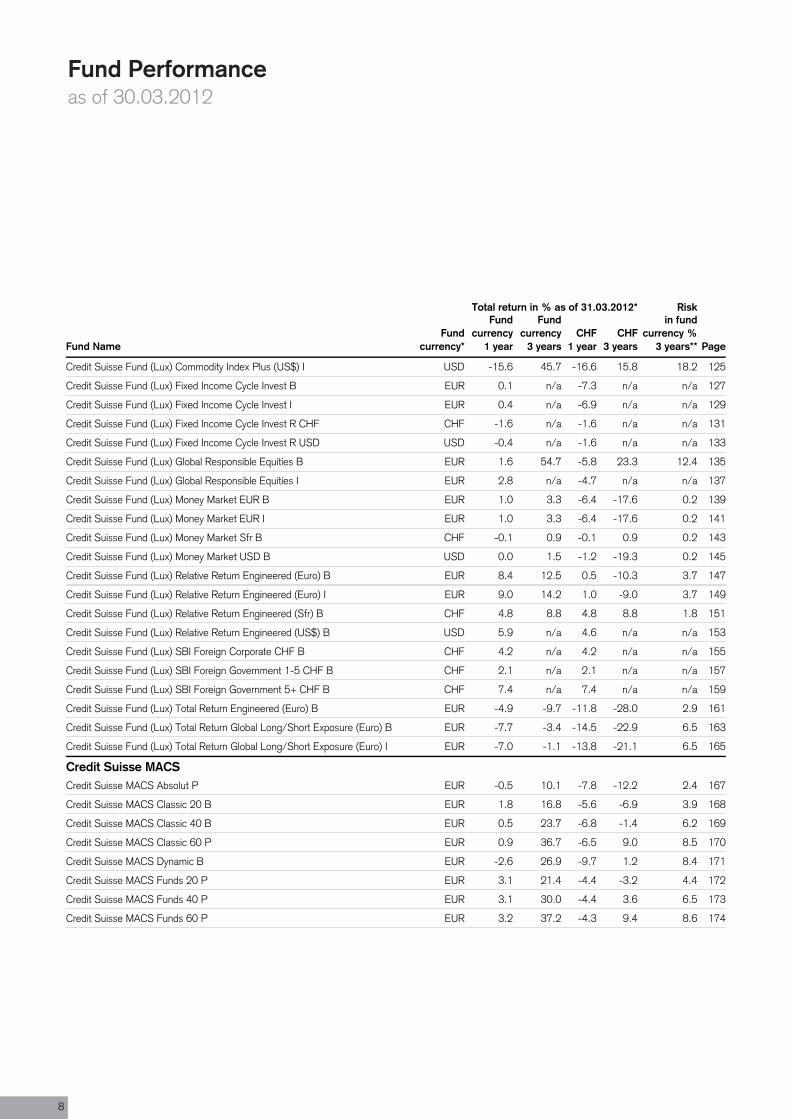

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

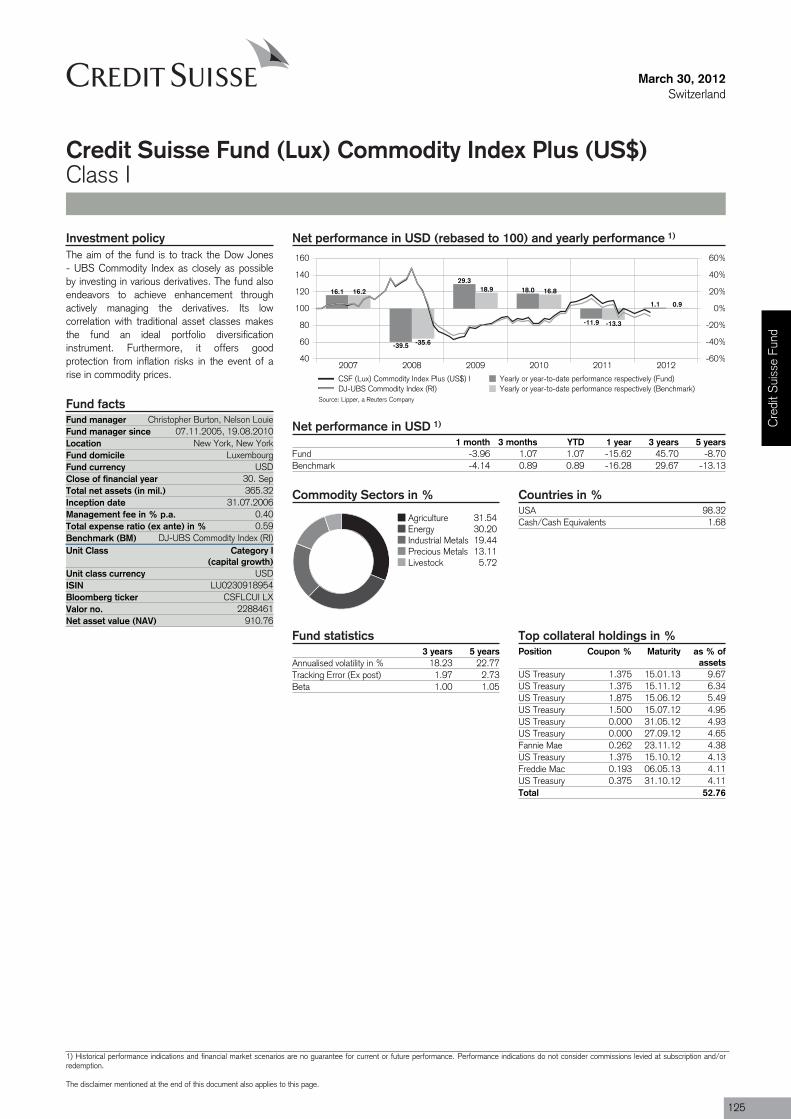

Credit Suisse Fund (Lux) Commodity Index Plus (US$) I USD -15.6 45.7 -16.6 15.8 18.2 125

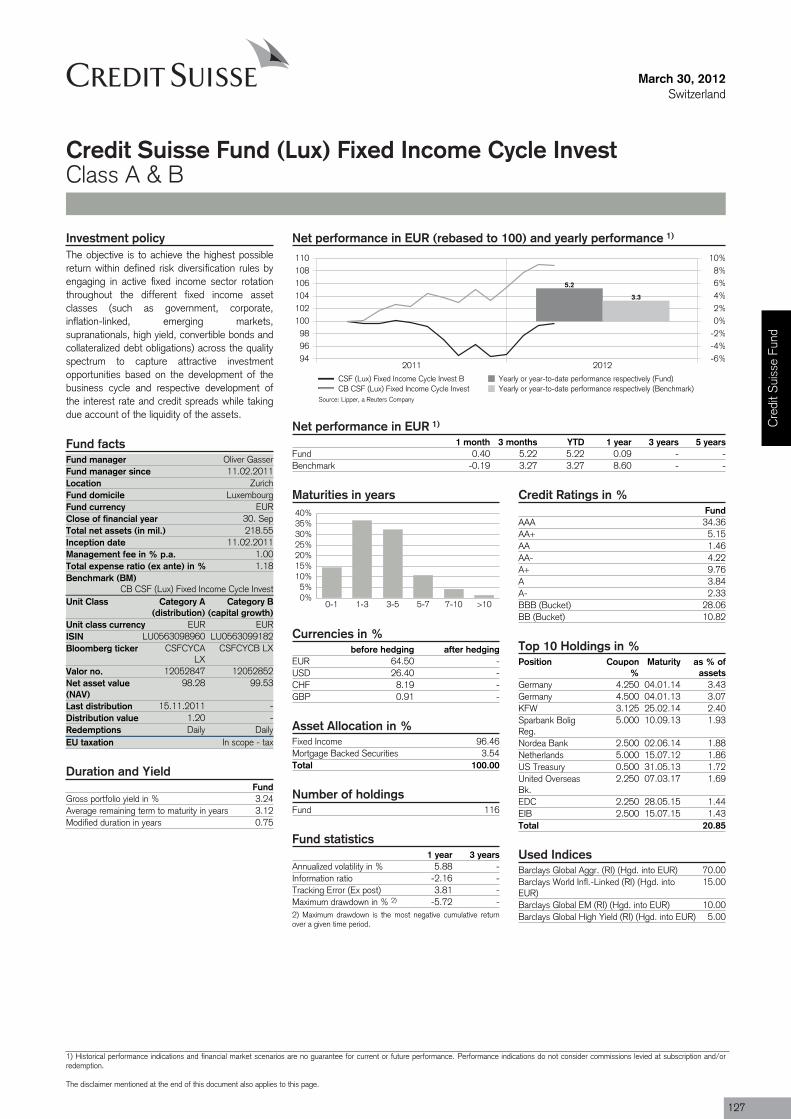

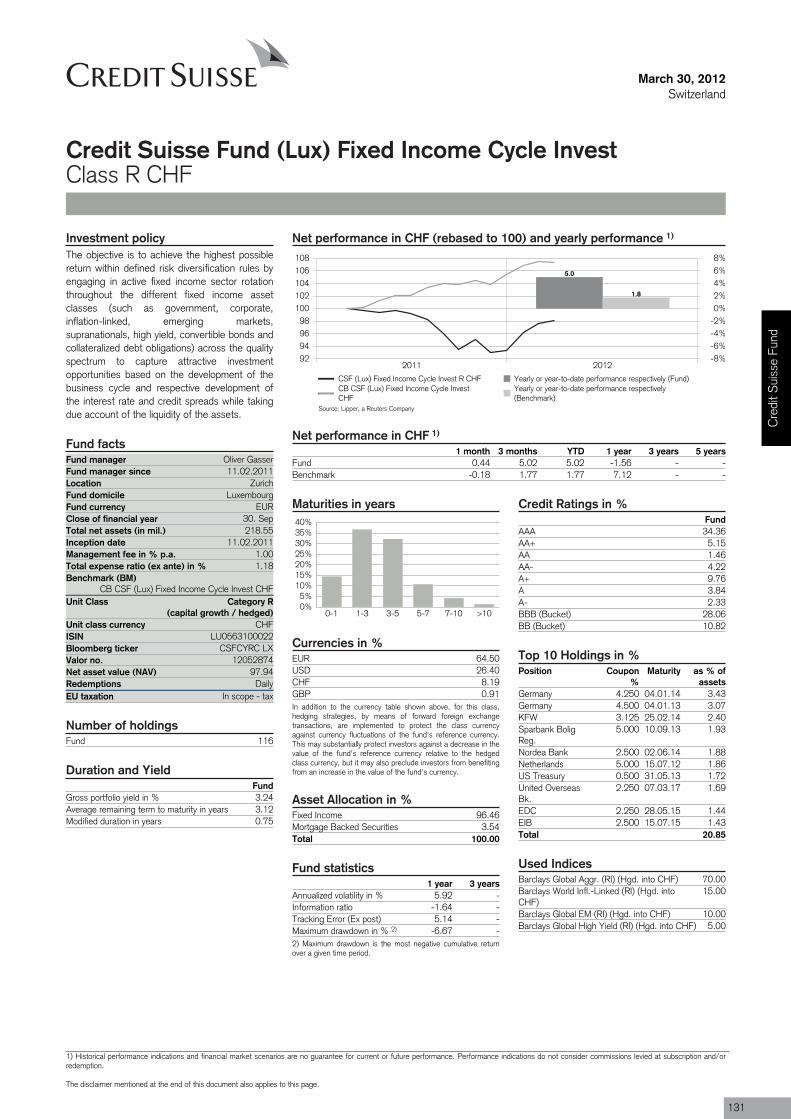

Credit Suisse Fund (Lux) Fixed Income Cycle Invest B EUR 0.1 n/a -7.3 n/a n/a 127

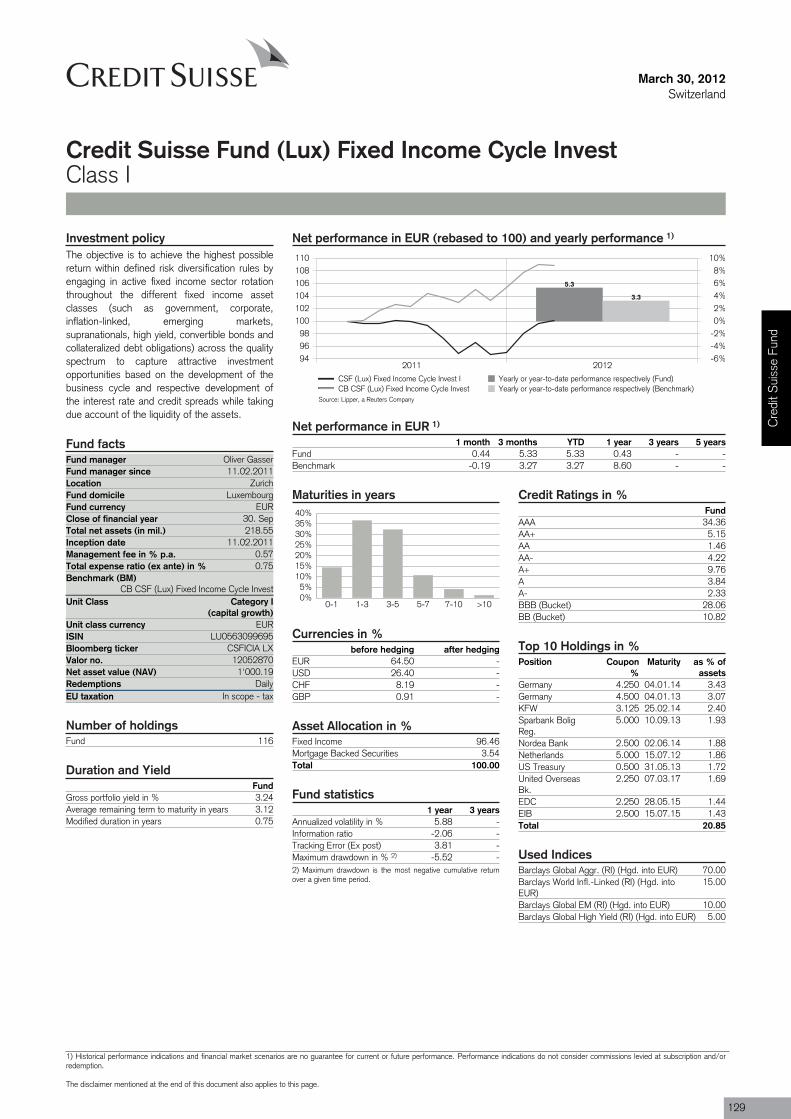

Credit Suisse Fund (Lux) Fixed Income Cycle Invest I EUR 0.4 n/a -6.9 n/a n/a 129

Credit Suisse Fund (Lux) Fixed Income Cycle Invest R CHF CHF -1.6 n/a -1.6 n/a n/a 131

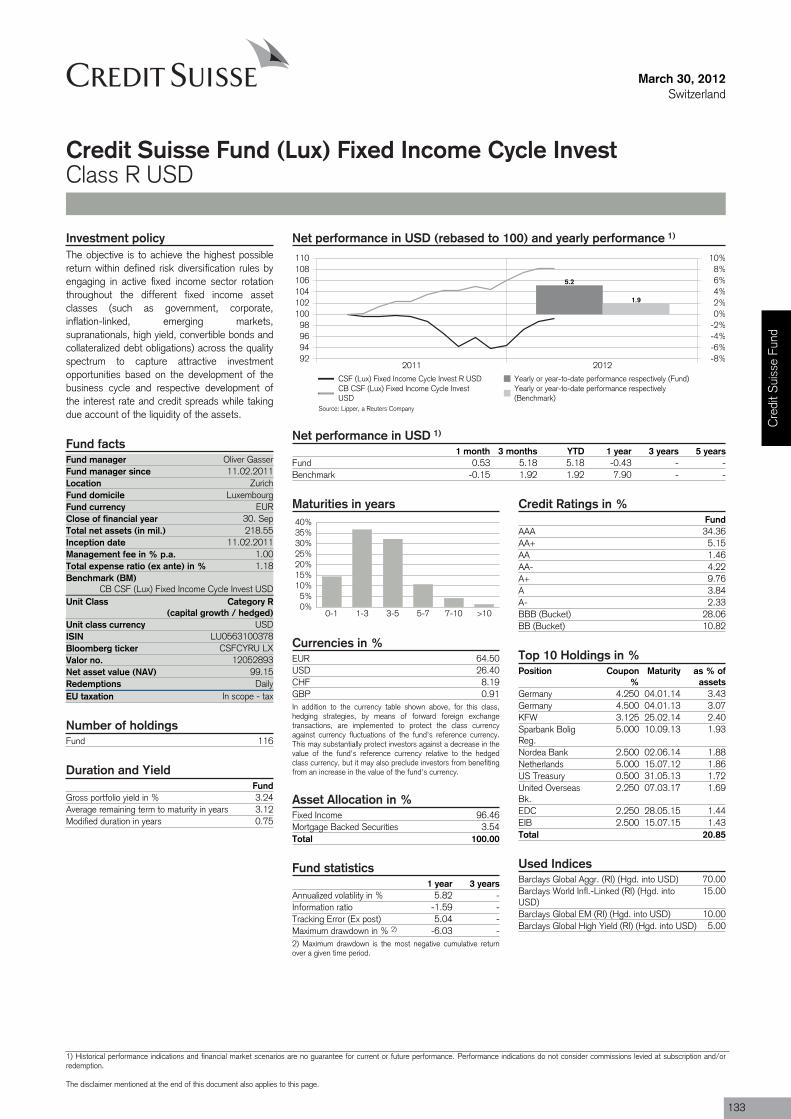

Credit Suisse Fund (Lux) Fixed Income Cycle Invest R USD USD -0.4 n/a -1.6 n/a n/a 133

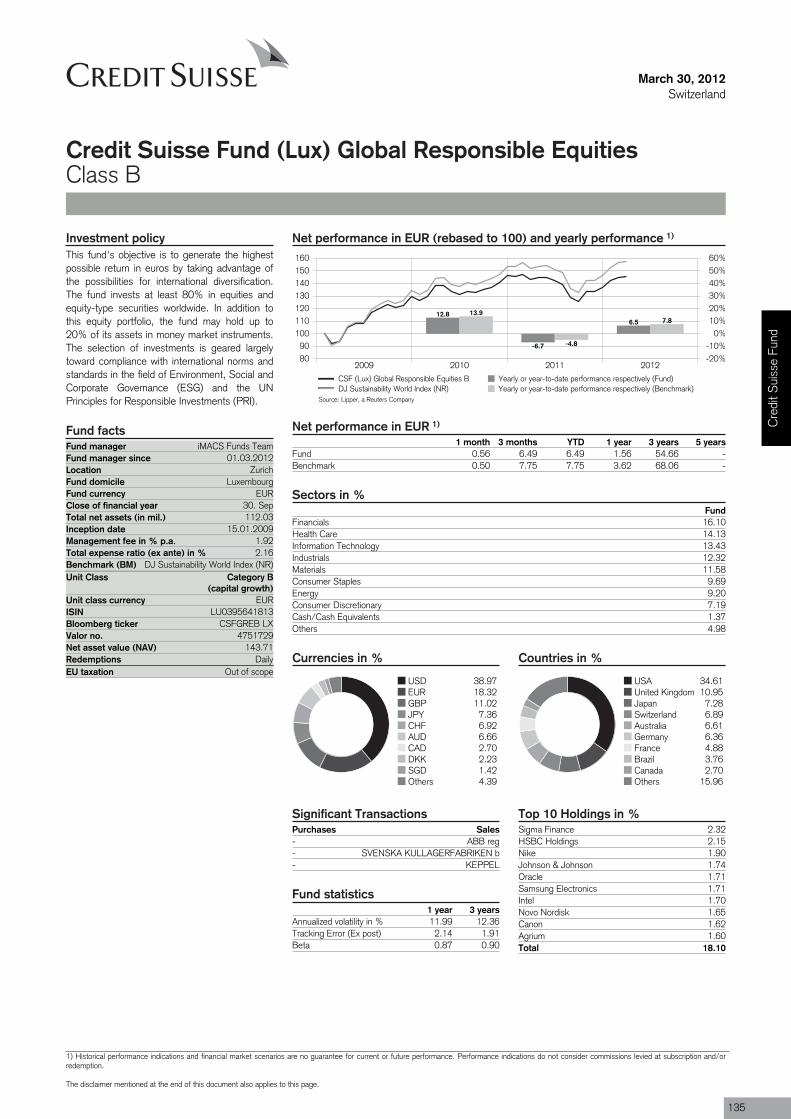

Credit Suisse Fund (Lux) Global Responsible Equities B EUR 1.6 54.7 -5.8 23.3 12.4 135

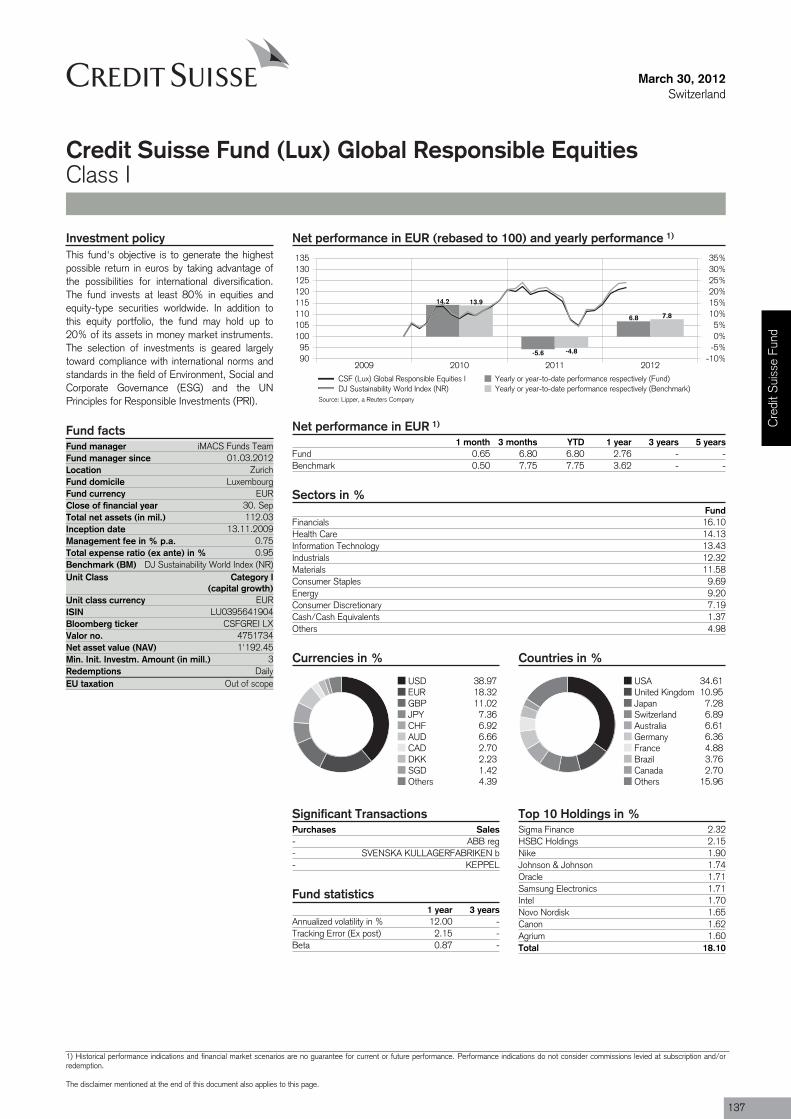

Credit Suisse Fund (Lux) Global Responsible Equities I EUR 2.8 n/a -4.7 n/a n/a 137

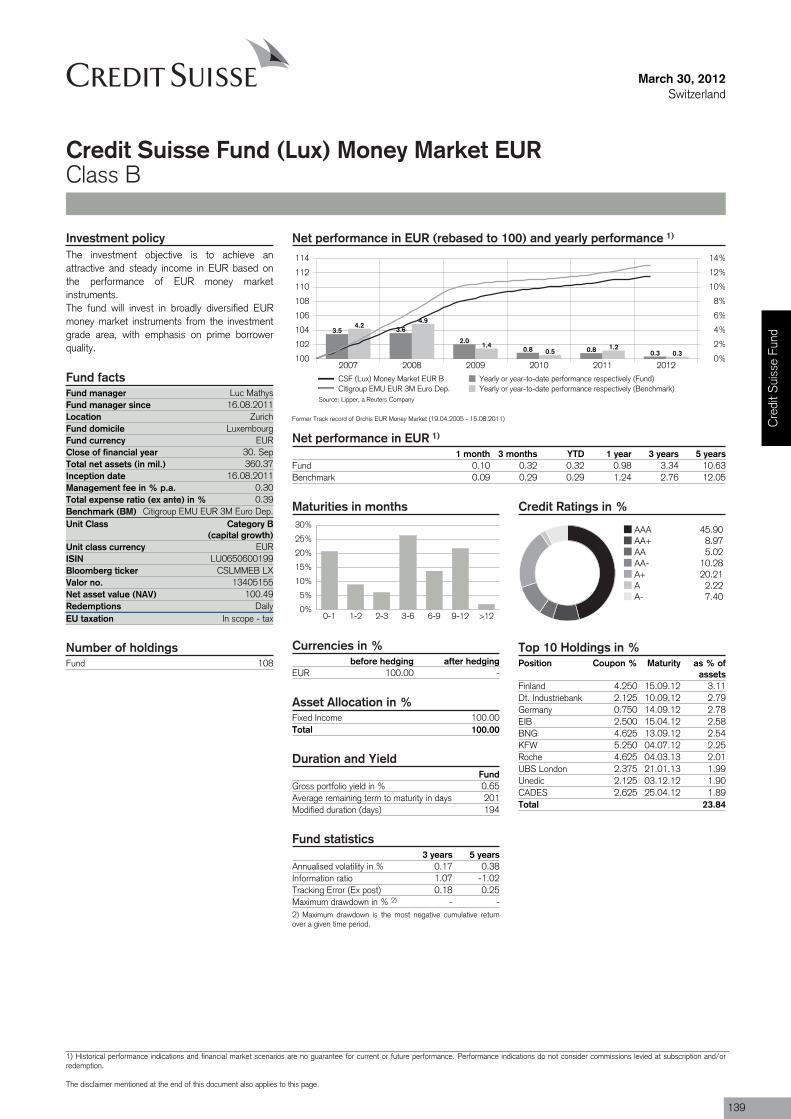

Credit Suisse Fund (Lux) Money Market EUR B EUR 1.0 3.3 -6.4 -17.6 0.2 139

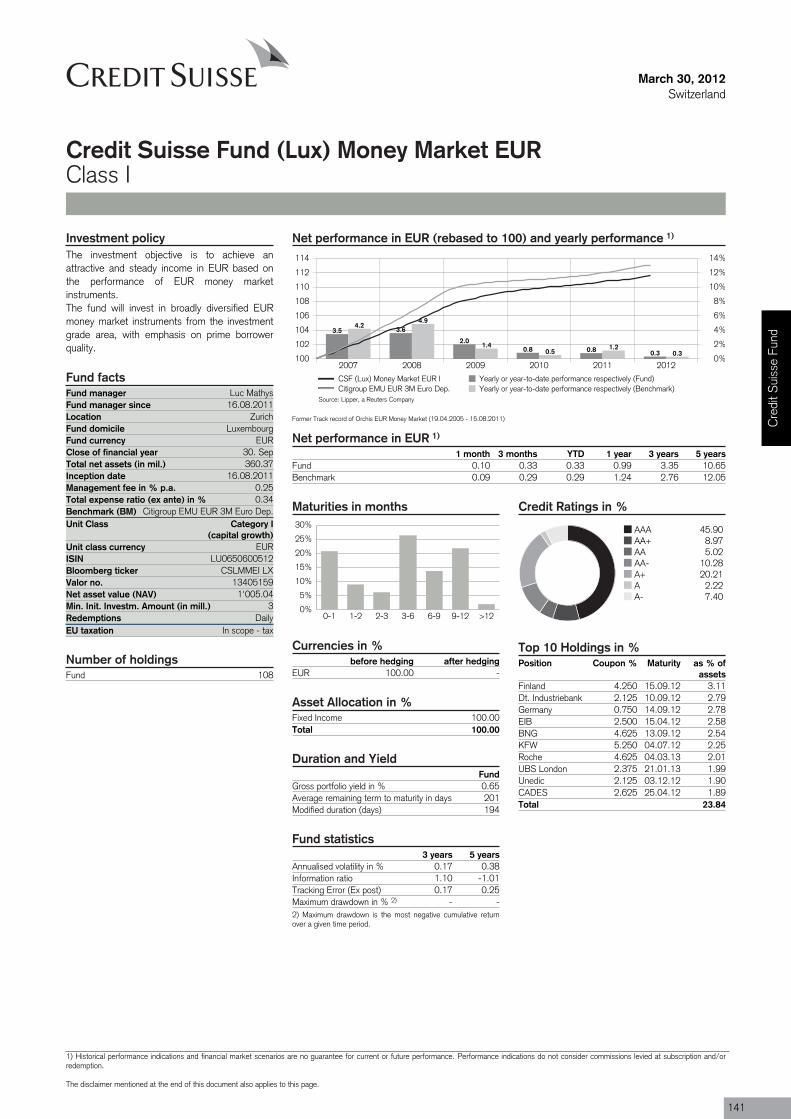

Credit Suisse Fund (Lux) Money Market EUR I EUR 1.0 3.3 -6.4 -17.6 0.2 141

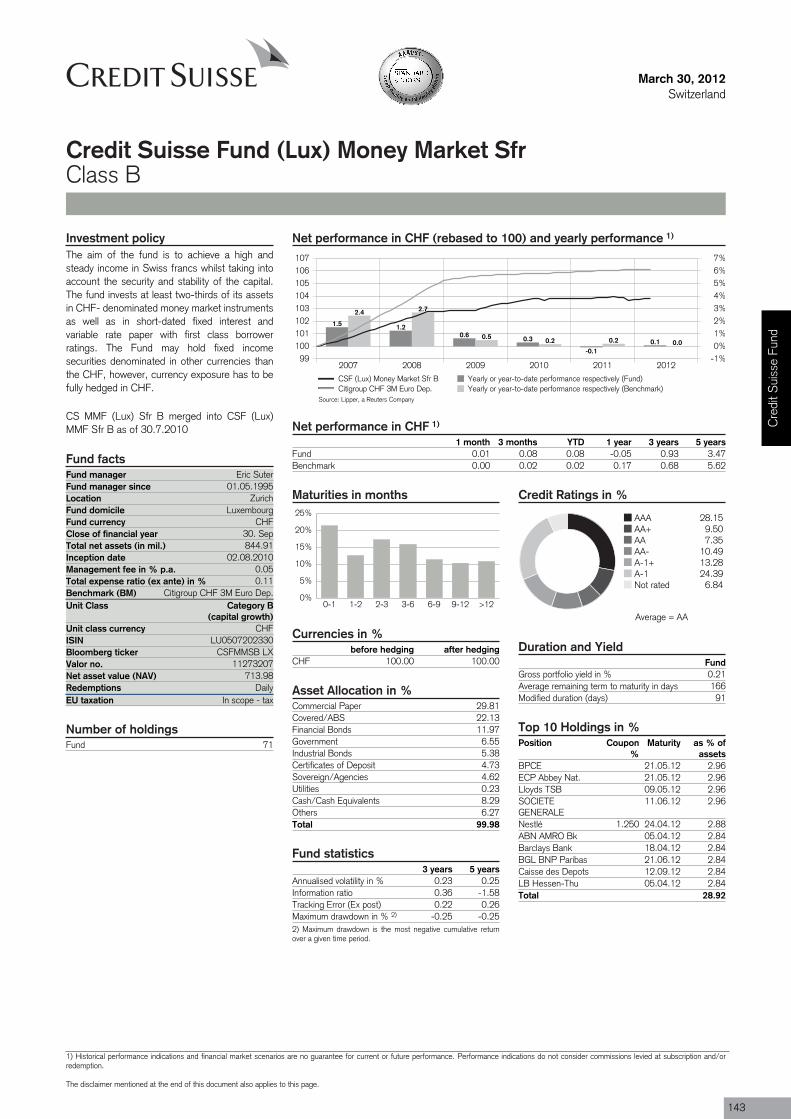

Credit Suisse Fund (Lux) Money Market Sfr B CHF -0.1 0.9 -0.1 0.9 0.2 143

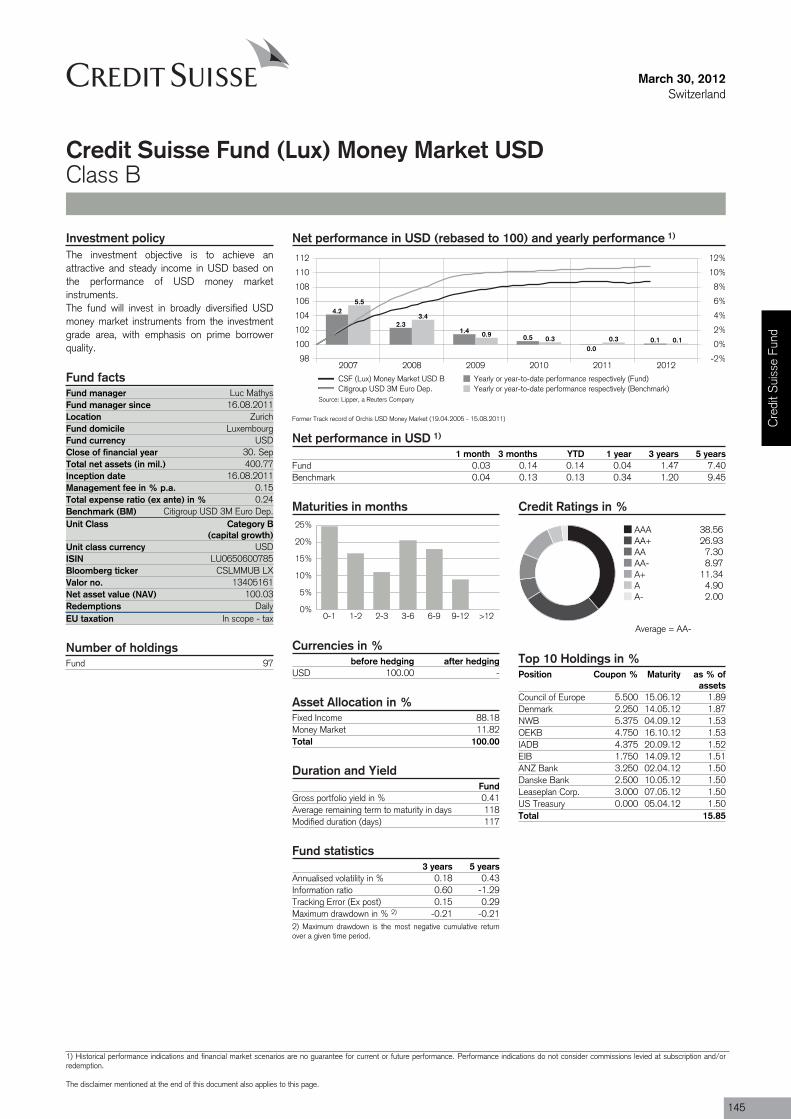

Credit Suisse Fund (Lux) Money Market USD B USD 0.0 1.5 -1.2 -19.3 0.2 145

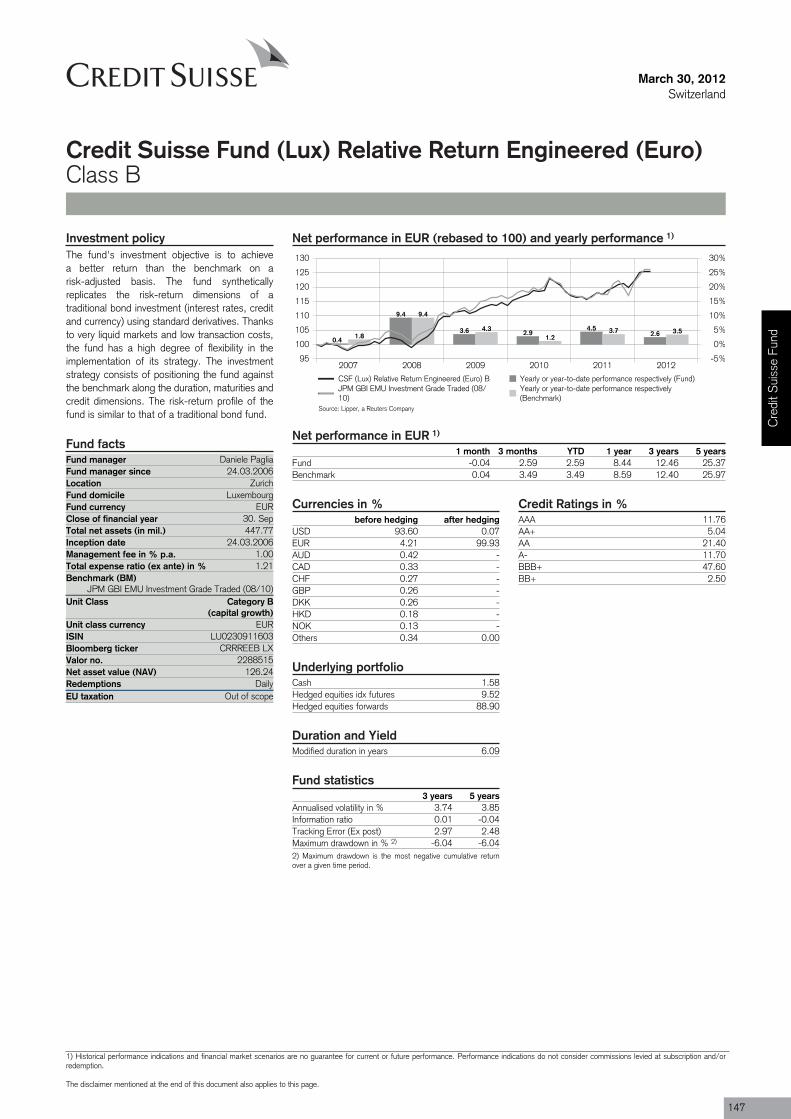

Credit Suisse Fund (Lux) Relative Return Engineered (Euro) B EUR 8.4 12.5 0.5 -10.3 3.7 147

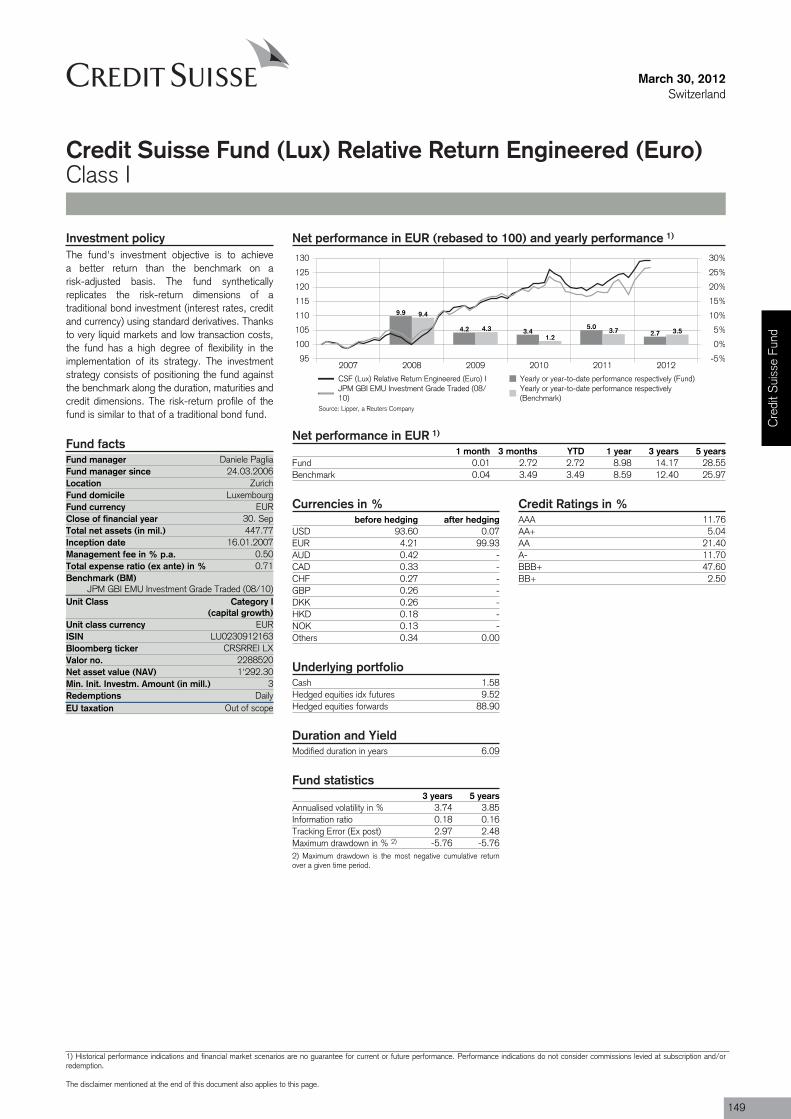

Credit Suisse Fund (Lux) Relative Return Engineered (Euro) I EUR 9.0 14.2 1.0 -9.0 3.7 149

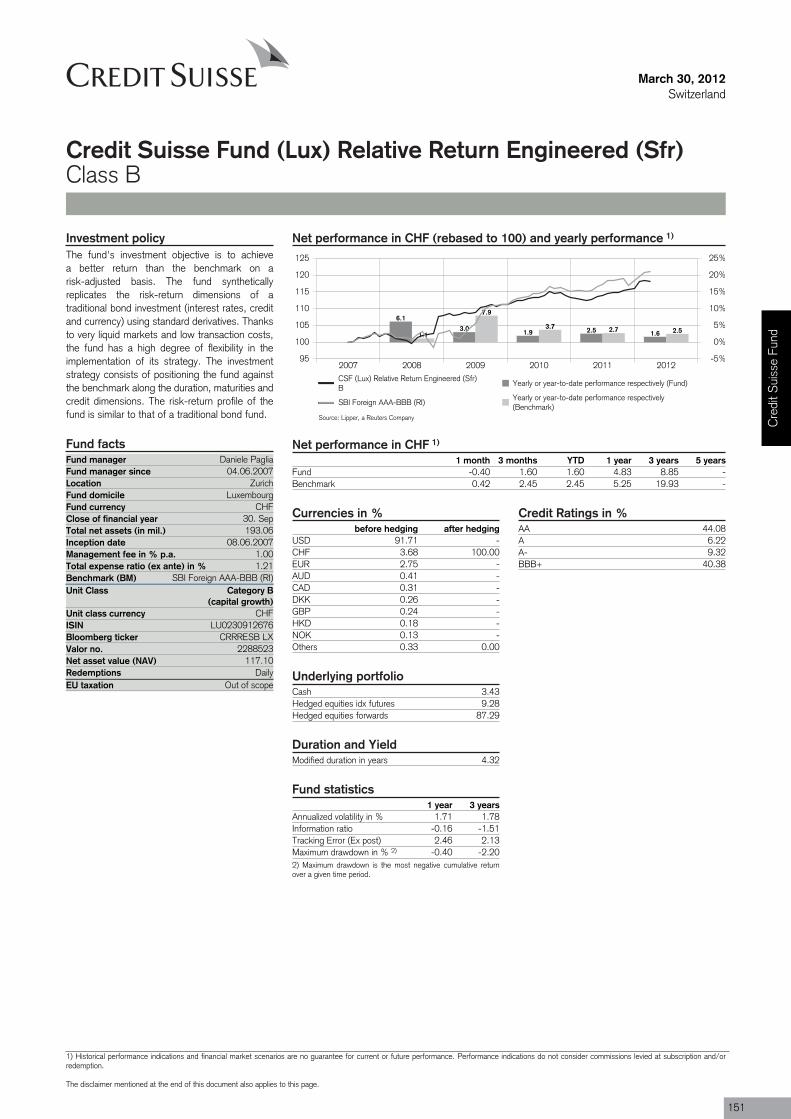

Credit Suisse Fund (Lux) Relative Return Engineered (Sfr) B CHF 4.8 8.8 4.8 8.8 1.8 151

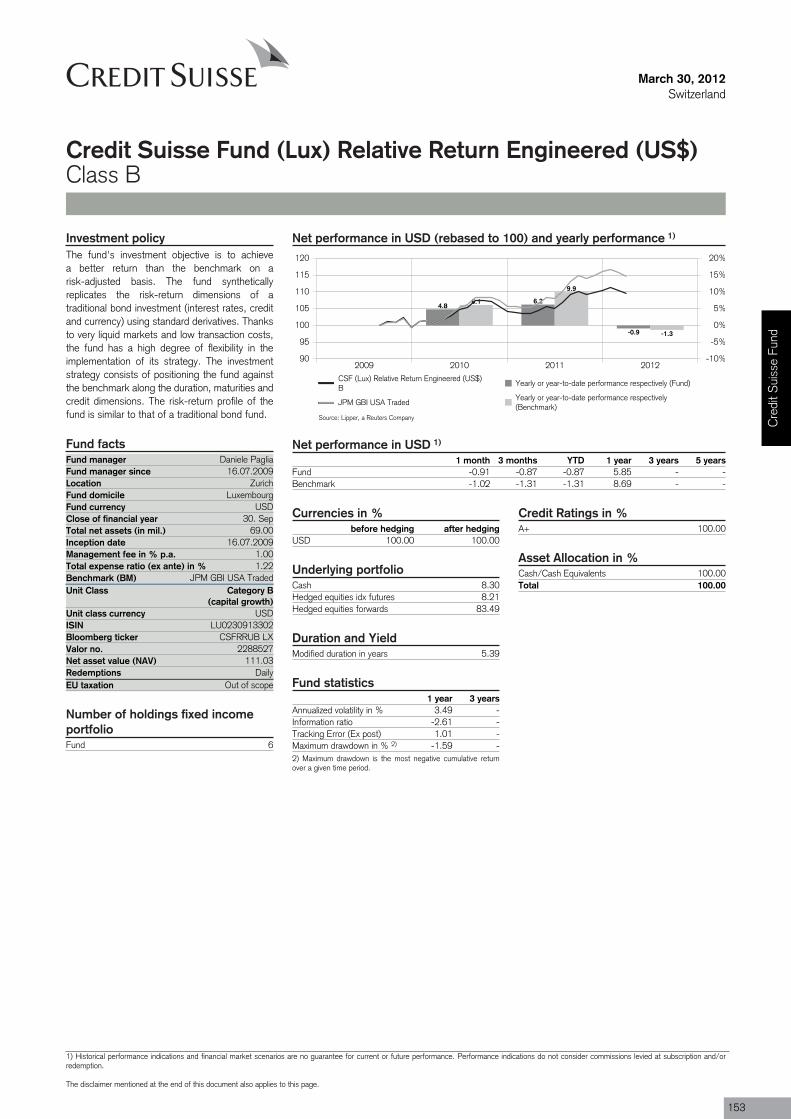

Credit Suisse Fund (Lux) Relative Return Engineered (US$) B USD 5.9 n/a 4.6 n/a n/a 153

Credit Suisse Fund (Lux) SBI Foreign Corporate CHF B CHF 4.2 n/a 4.2 n/a n/a 155

Credit Suisse Fund (Lux) SBI Foreign Government 1-5 CHF B CHF 2.1 n/a 2.1 n/a n/a 157

Credit Suisse Fund (Lux) SBI Foreign Government 5+ CHF B CHF 7.4 n/a 7.4 n/a n/a 159

Credit Suisse Fund (Lux) Total Return Engineered (Euro) B EUR -4.9 -9.7 -11.8 -28.0 2.9 161

Credit Suisse Fund (Lux) Total Return Global Long/Short Exposure (Euro) B EUR -7.7 -3.4 -14.5 -22.9 6.5 163

Credit Suisse Fund (Lux) Total Return Global Long/Short Exposure (Euro) I EUR -7.0 -1.1 -13.8 -21.1 6.5 165

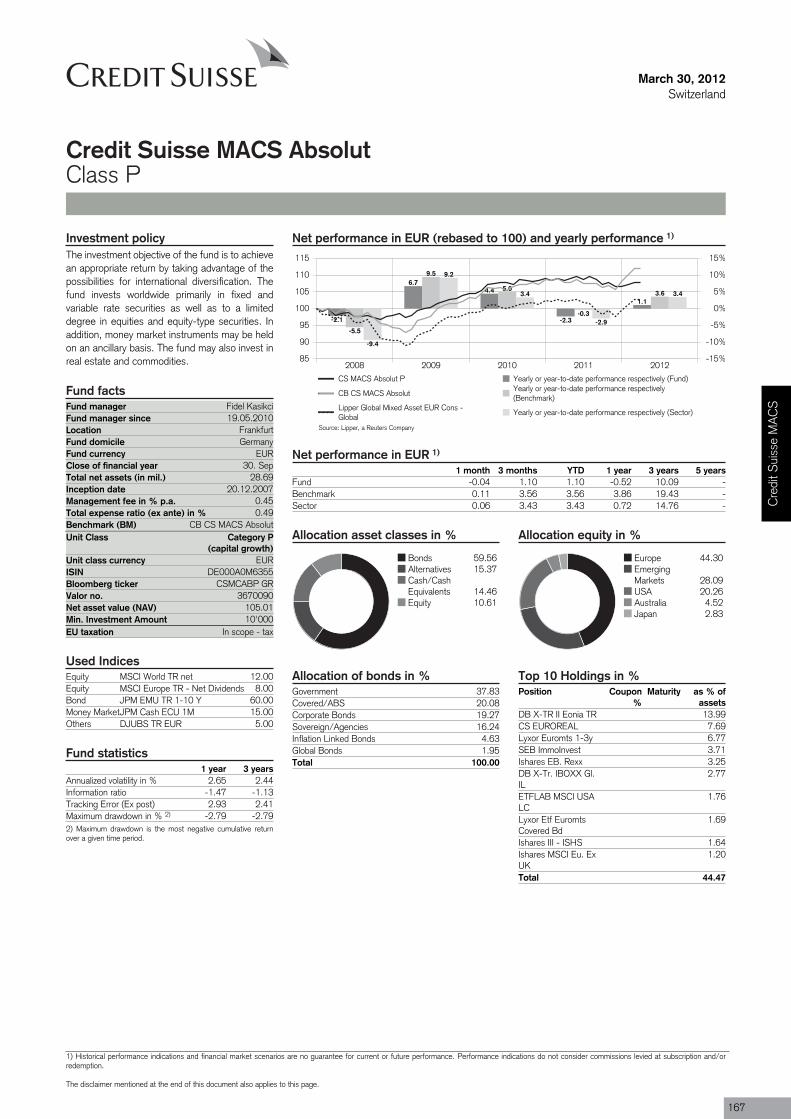

Credit Suisse MACSCredit Suisse MACS Absolut P EUR -0.5 10.1 -7.8 -12.2 2.4 167

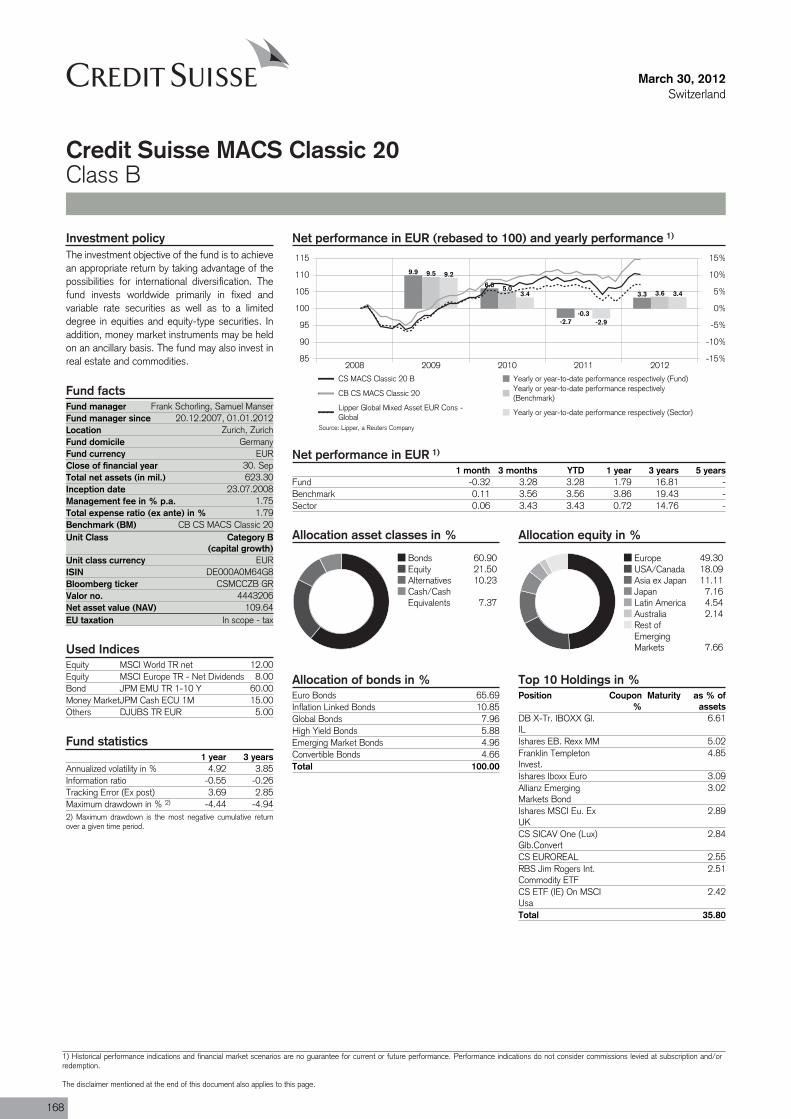

Credit Suisse MACS Classic 20 B EUR 1.8 16.8 -5.6 -6.9 3.9 168

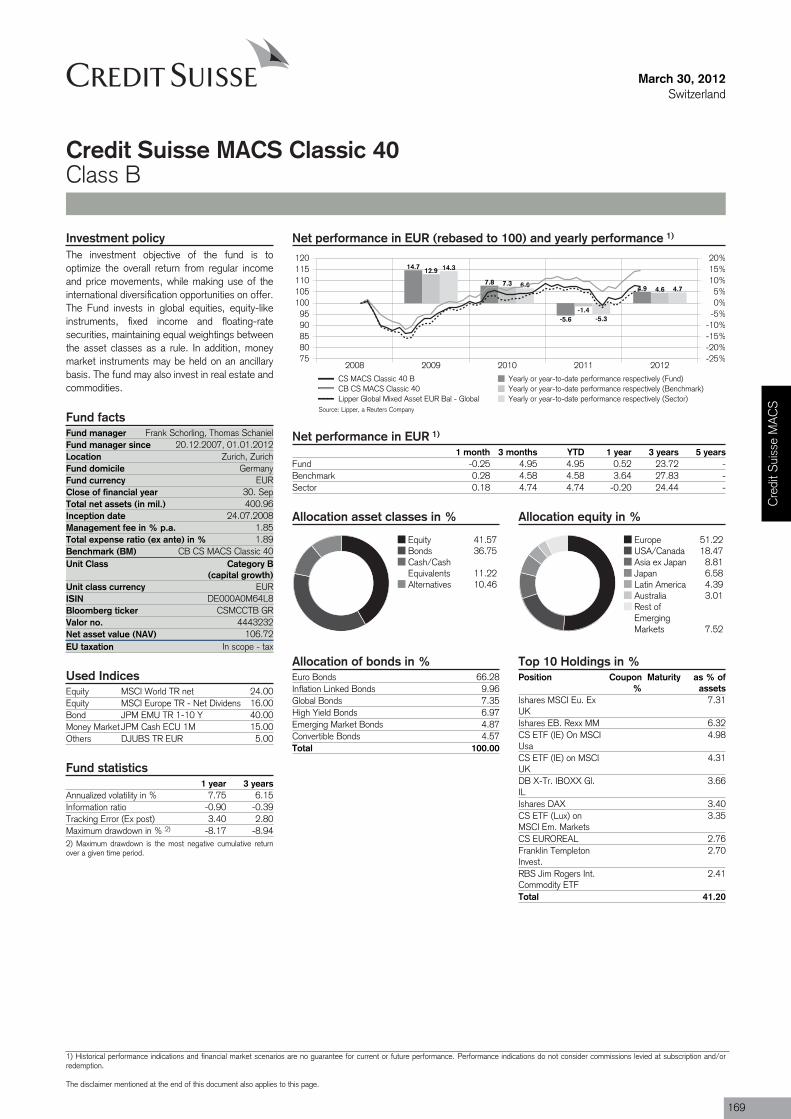

Credit Suisse MACS Classic 40 B EUR 0.5 23.7 -6.8 -1.4 6.2 169

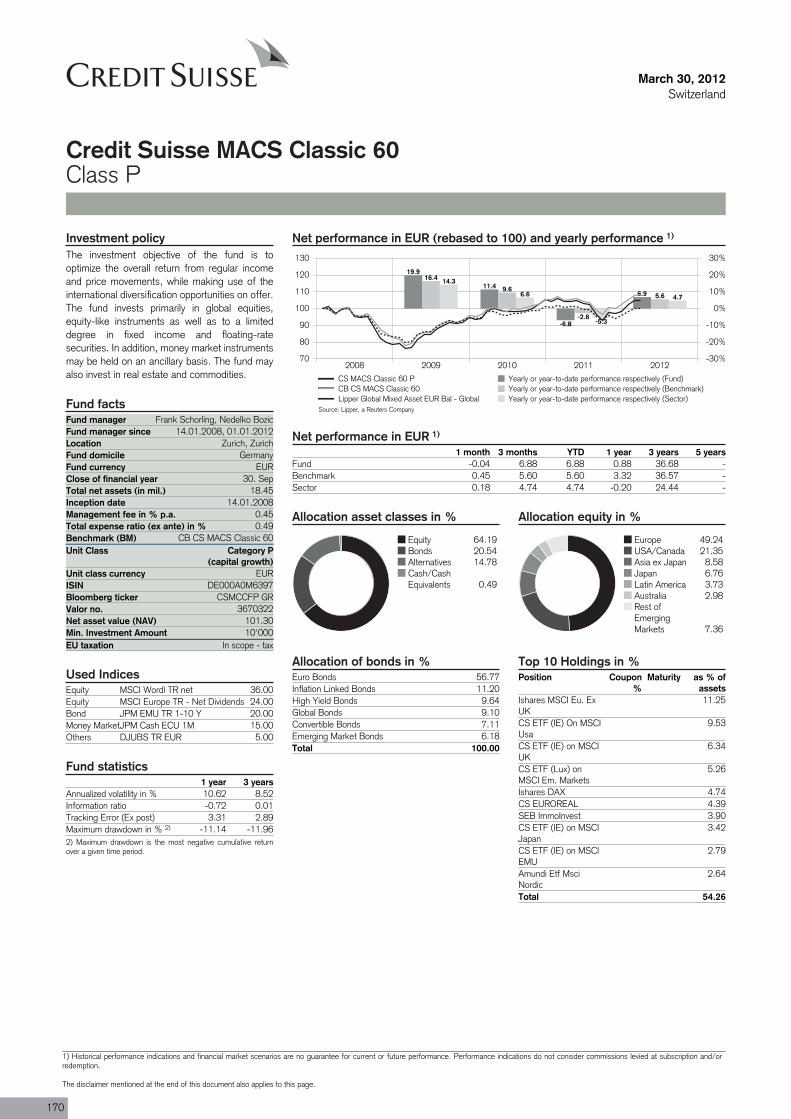

Credit Suisse MACS Classic 60 P EUR 0.9 36.7 -6.5 9.0 8.5 170

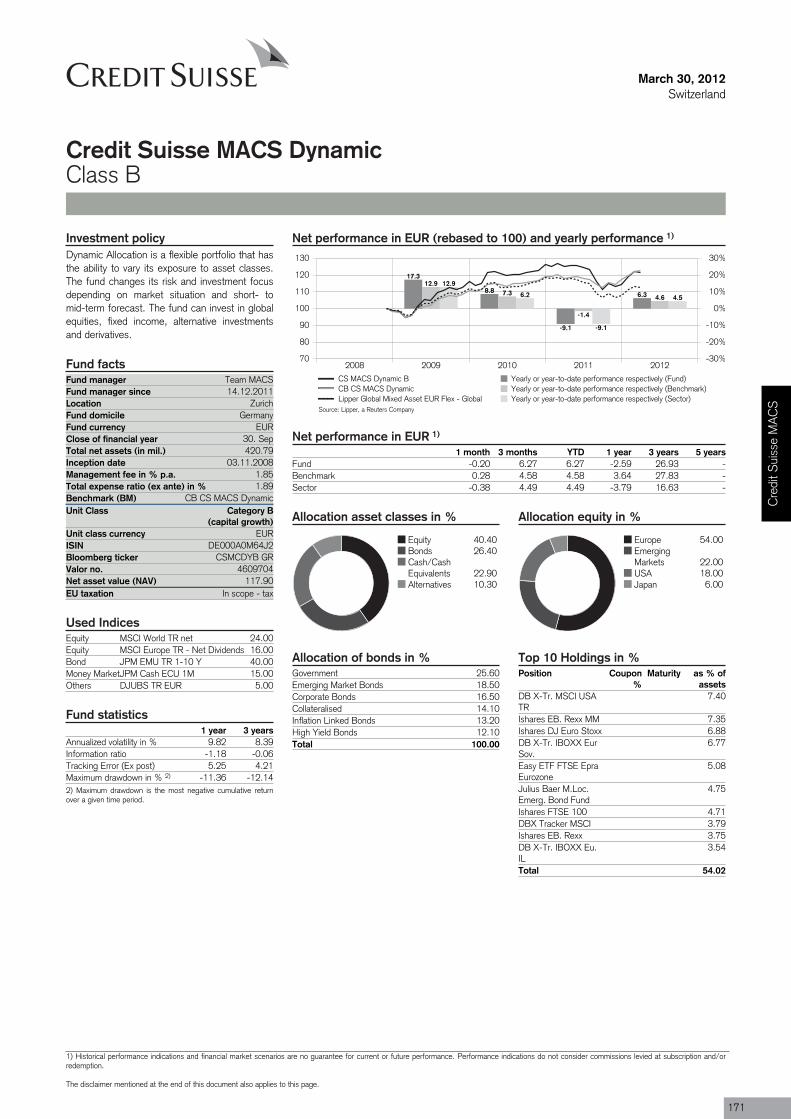

Credit Suisse MACS Dynamic B EUR -2.6 26.9 -9.7 1.2 8.4 171

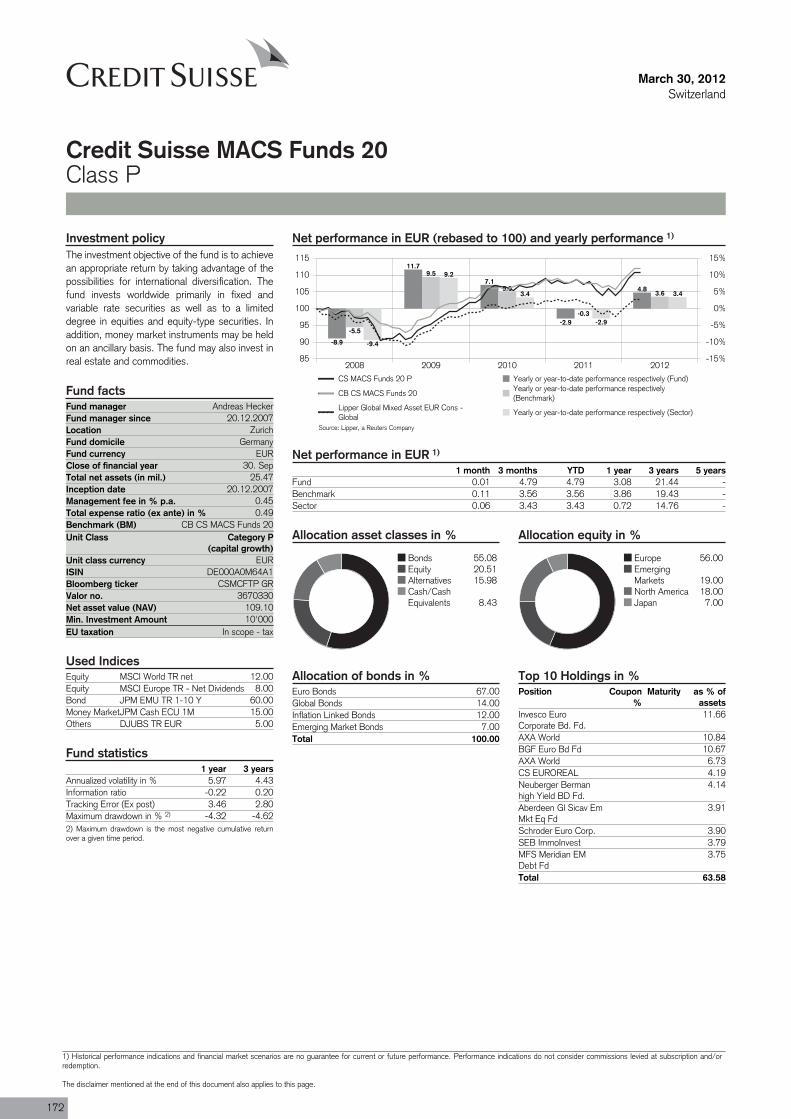

Credit Suisse MACS Funds 20 P EUR 3.1 21.4 -4.4 -3.2 4.4 172

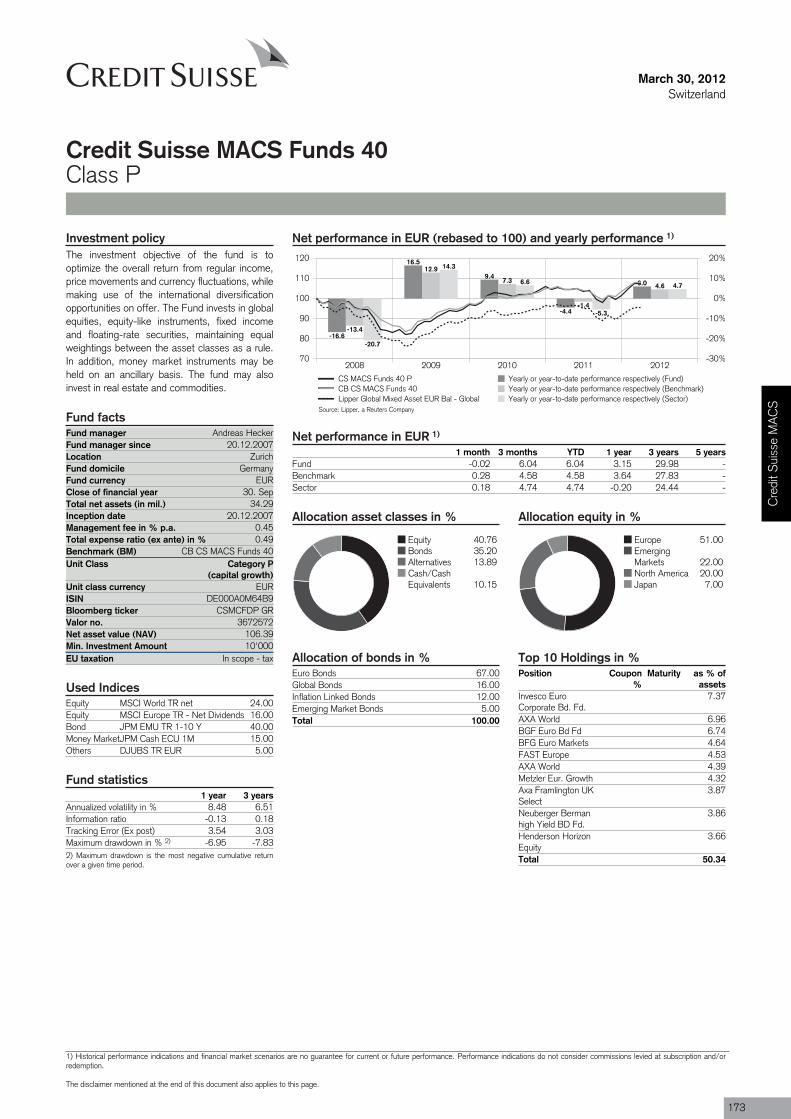

Credit Suisse MACS Funds 40 P EUR 3.1 30.0 -4.4 3.6 6.5 173

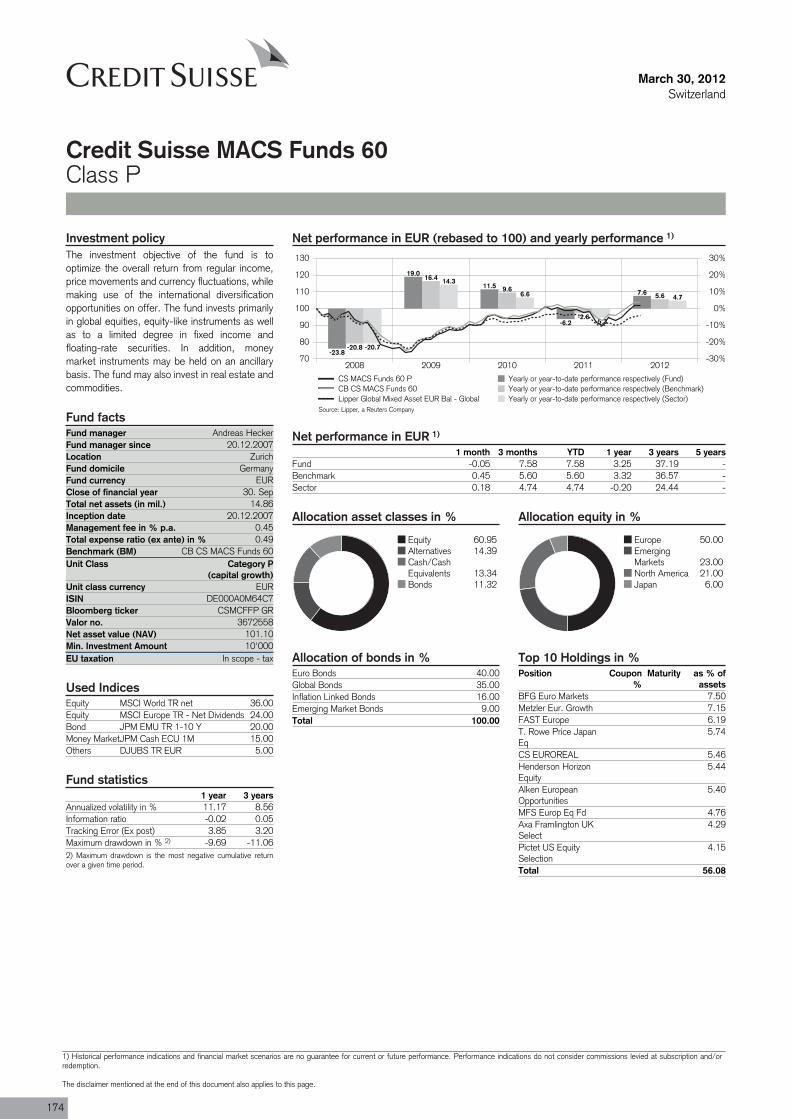

Credit Suisse MACS Funds 60 P EUR 3.2 37.2 -4.3 9.4 8.6 174

Fund Performanceas of 30.03.2012

8

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

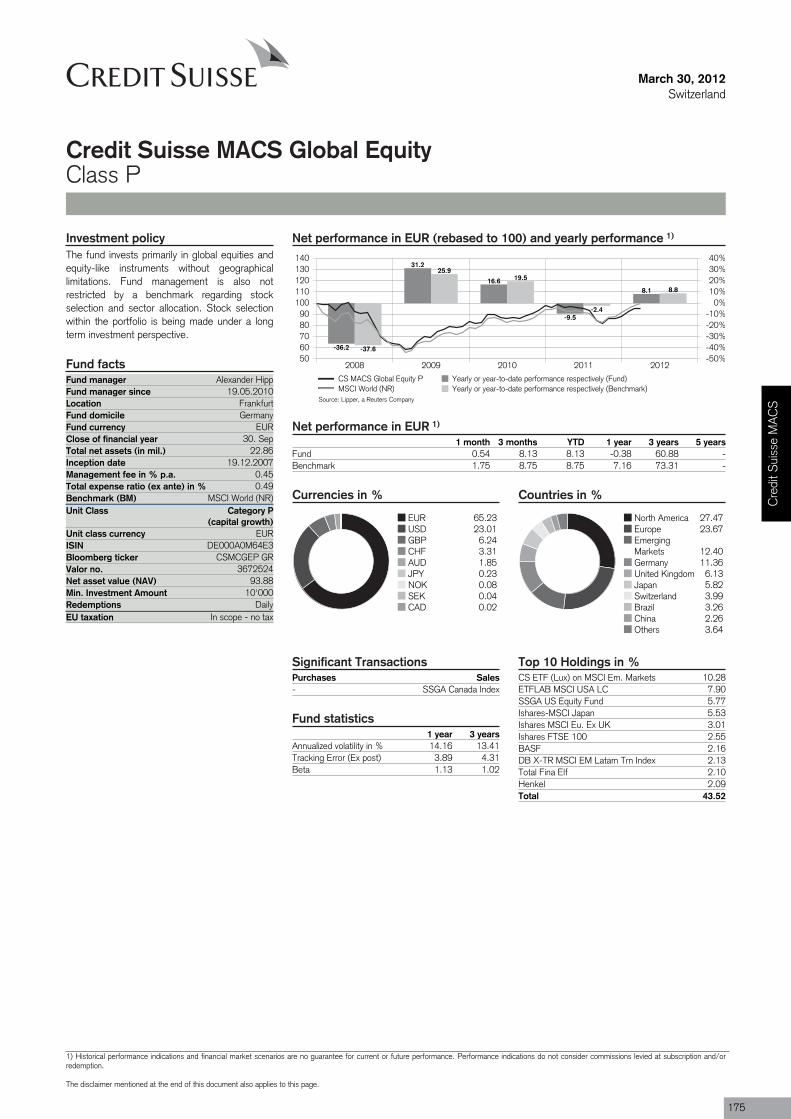

Credit Suisse MACS Global Equity P EUR -0.4 60.9 -7.6 28.3 13.4 175

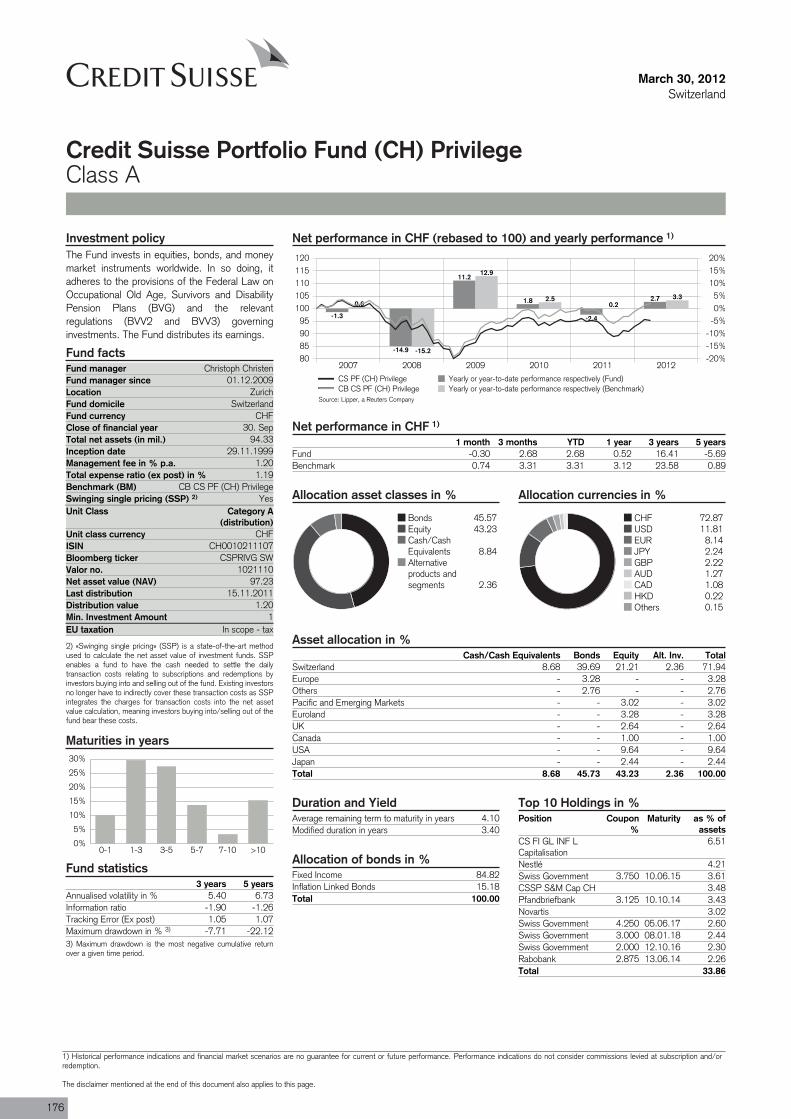

Credit Suisse Portfolio FundCredit Suisse Portfolio Fund (CH) Privilege CHF 0.5 16.4 0.5 16.4 5.4 176

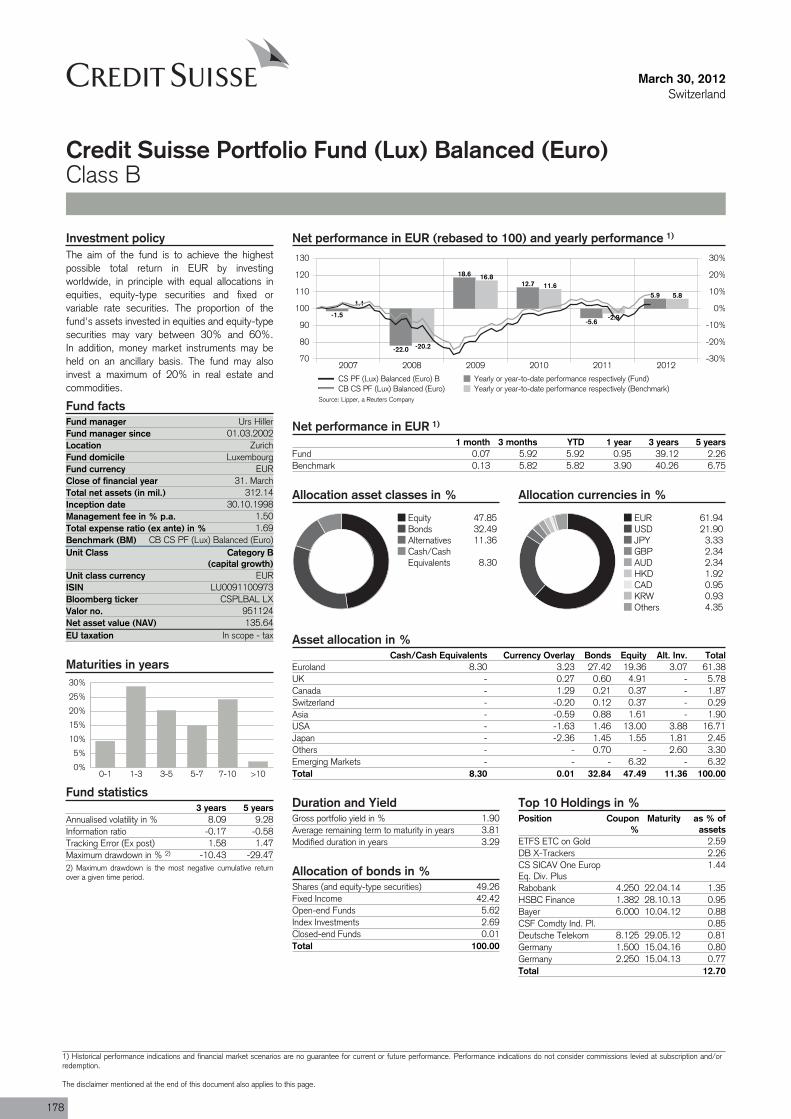

Credit Suisse Portfolio Fund (Lux) Balanced (Euro) B EUR 1.0 39.1 -6.4 10.9 8.1 178

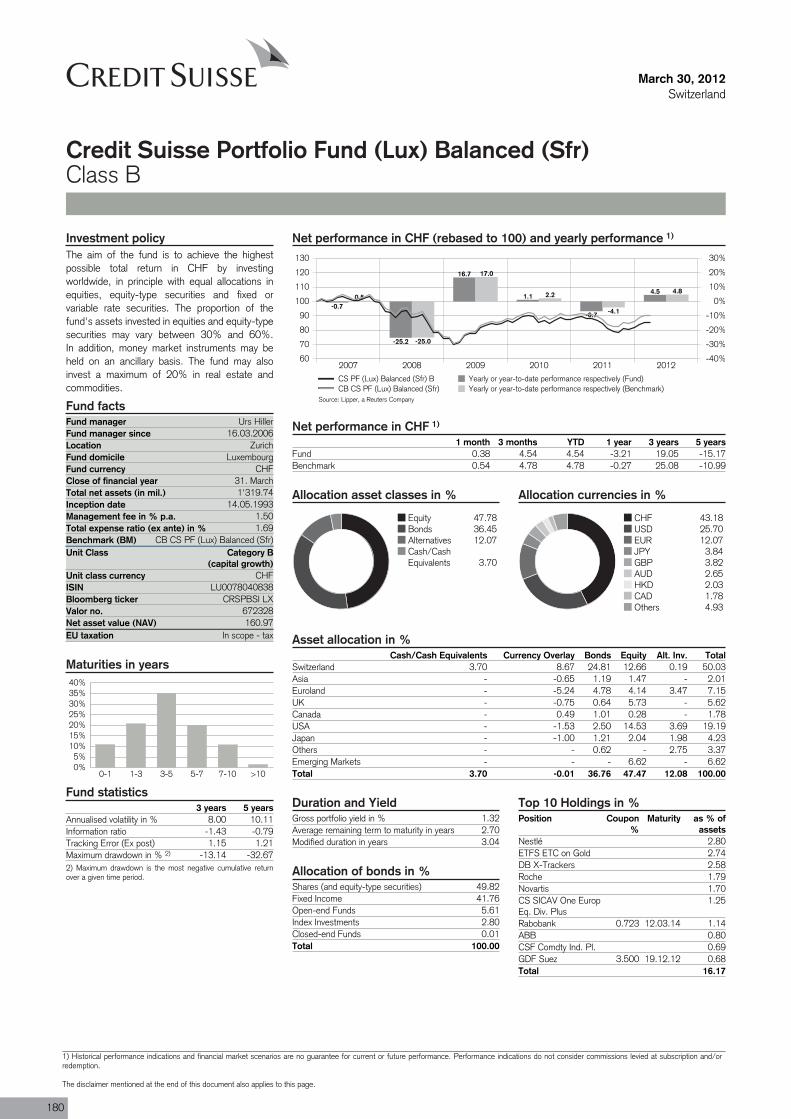

Credit Suisse Portfolio Fund (Lux) Balanced (Sfr) B CHF -3.2 19.1 -3.2 19.1 8.0 180

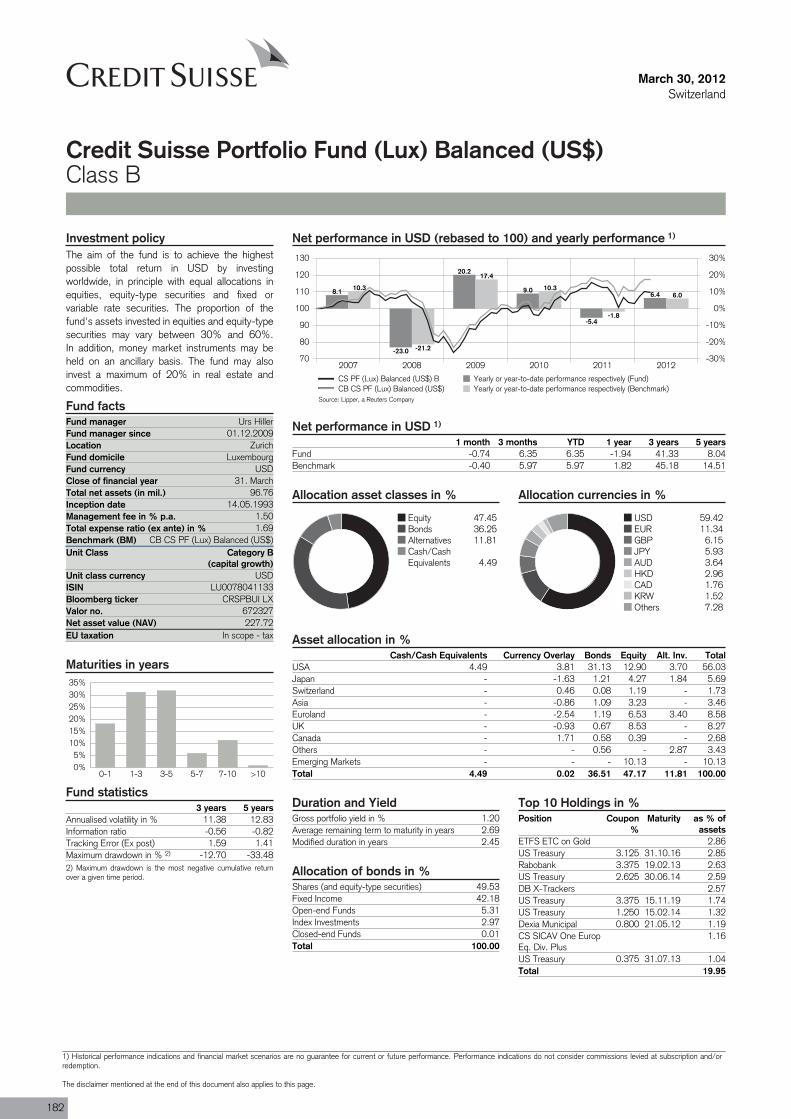

Credit Suisse Portfolio Fund (Lux) Balanced (US$) B USD -1.9 41.3 -3.1 12.3 11.4 182

Credit Suisse Portfolio Fund (Lux) Growth (Euro) B EUR -1.9 46.1 -9.0 16.5 11.4 184

Credit Suisse Portfolio Fund (Lux) Growth (Sfr) B CHF -3.8 24.1 -3.8 24.1 10.8 186

Credit Suisse Portfolio Fund (Lux) Growth (US$) B USD -4.8 50.4 -6.0 19.6 15.6 188

Credit Suisse Portfolio Fund (Lux) Income (Euro) B EUR 2.8 30.6 -4.7 4.1 5.3 190

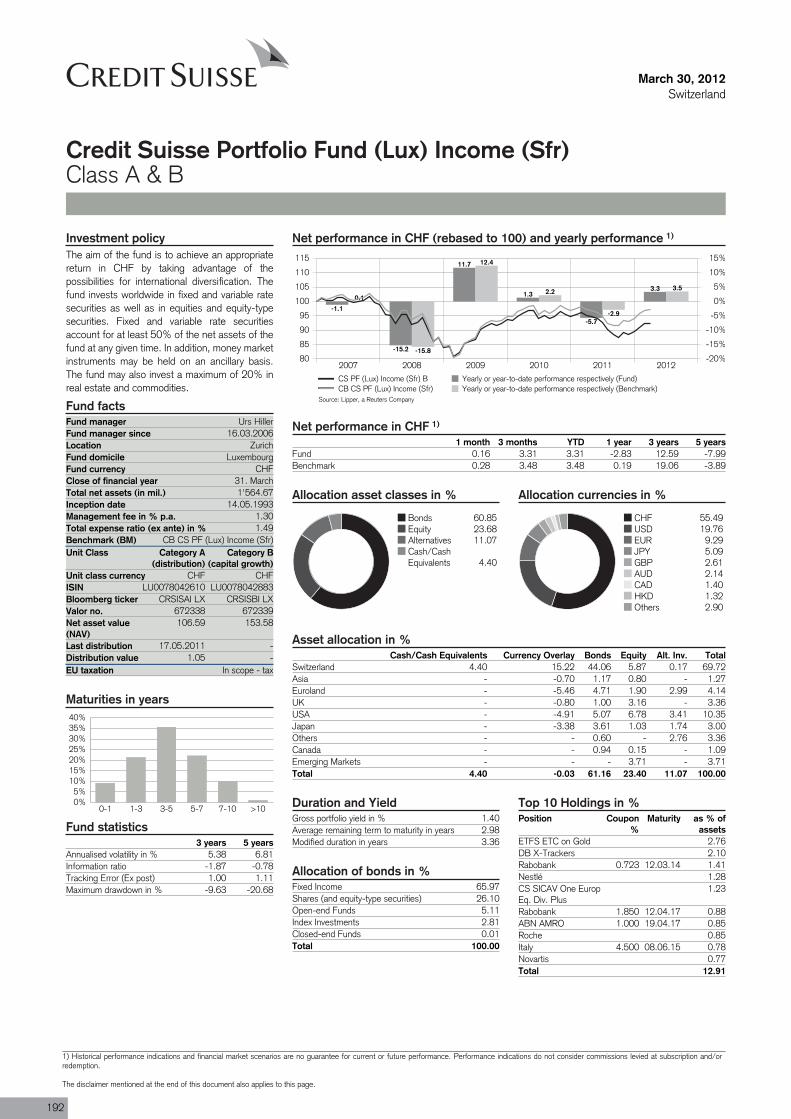

Credit Suisse Portfolio Fund (Lux) Income (Sfr) B CHF -2.8 12.6 -2.8 12.6 5.4 192

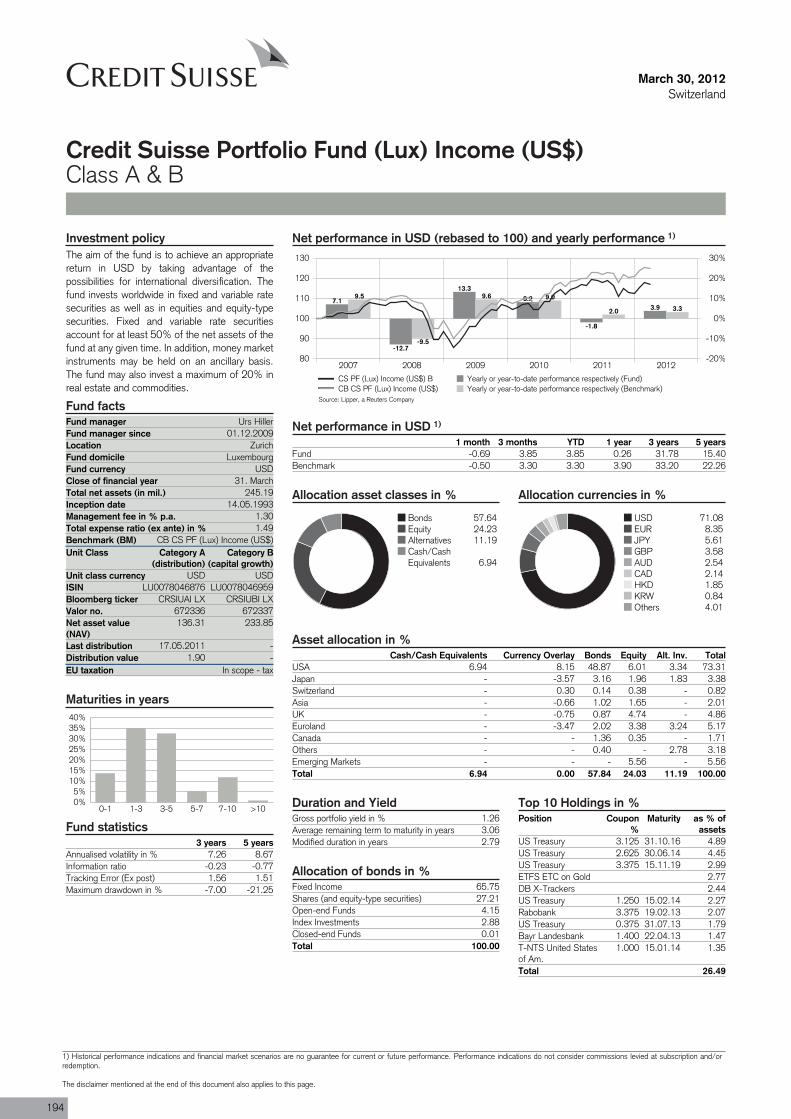

Credit Suisse Portfolio Fund (Lux) Income (US$) B USD 0.3 31.8 -0.9 4.8 7.3 194

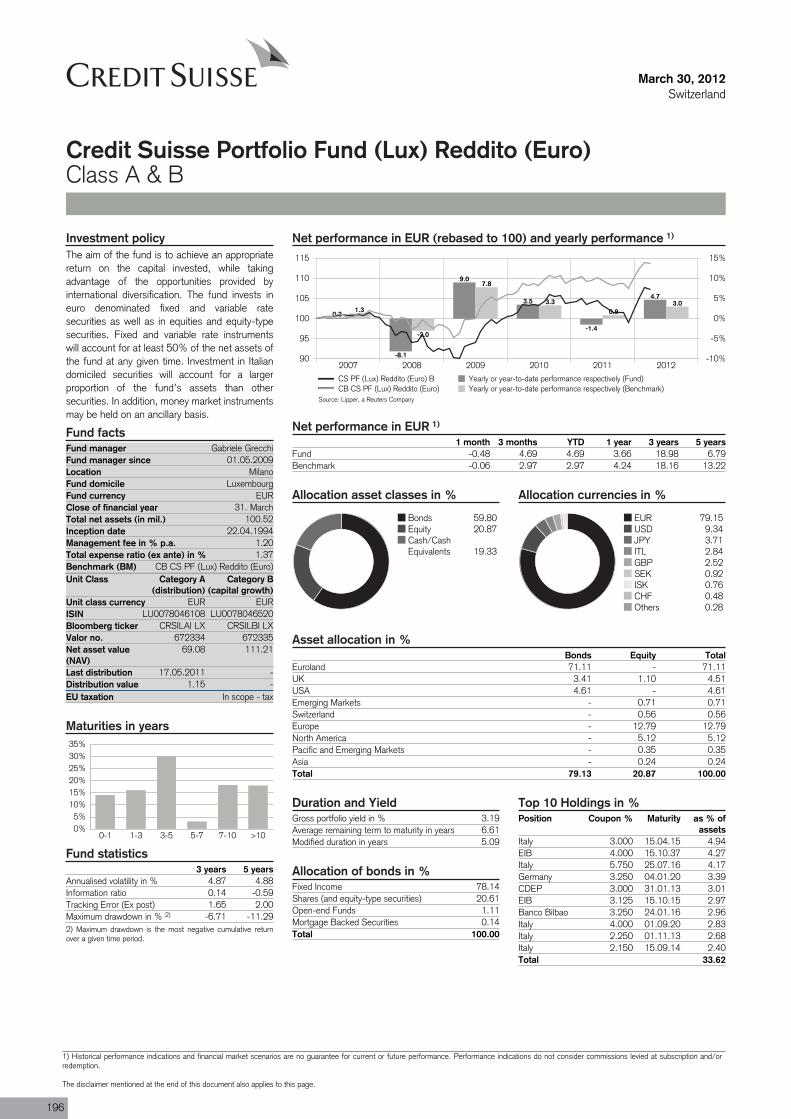

Credit Suisse Portfolio Fund (Lux) Reddito (Euro) B EUR 3.7 19.0 -3.9 -5.1 4.9 196

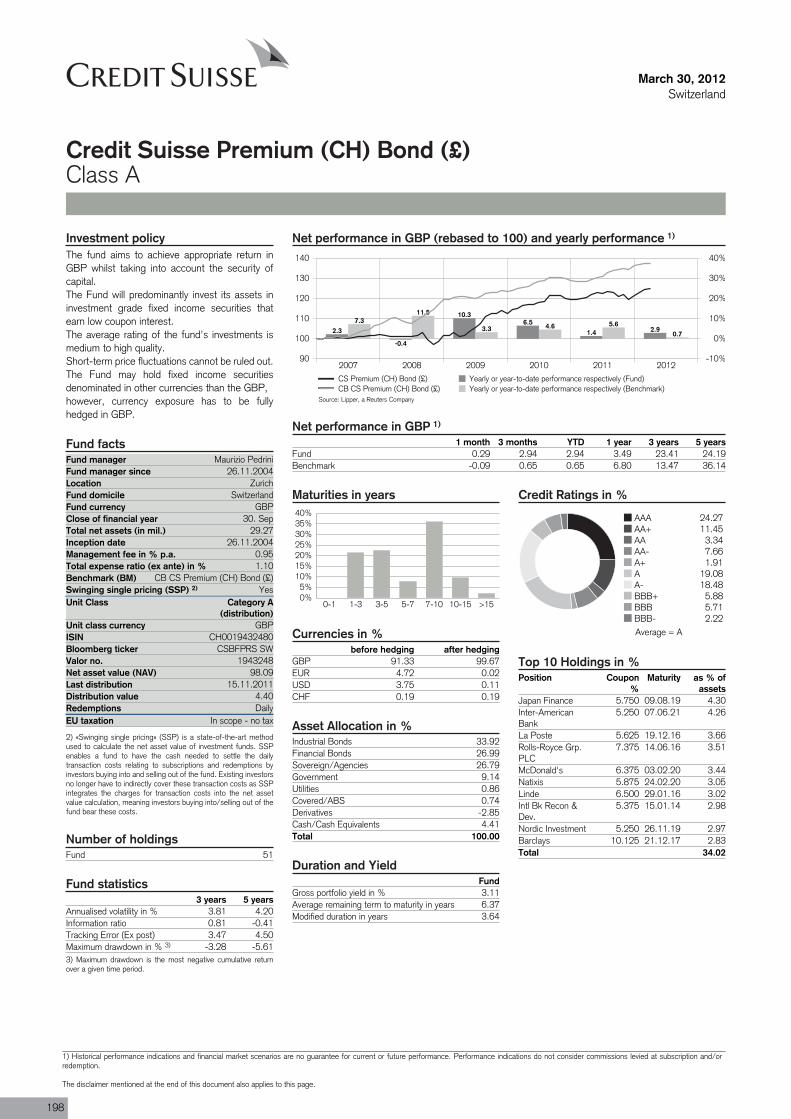

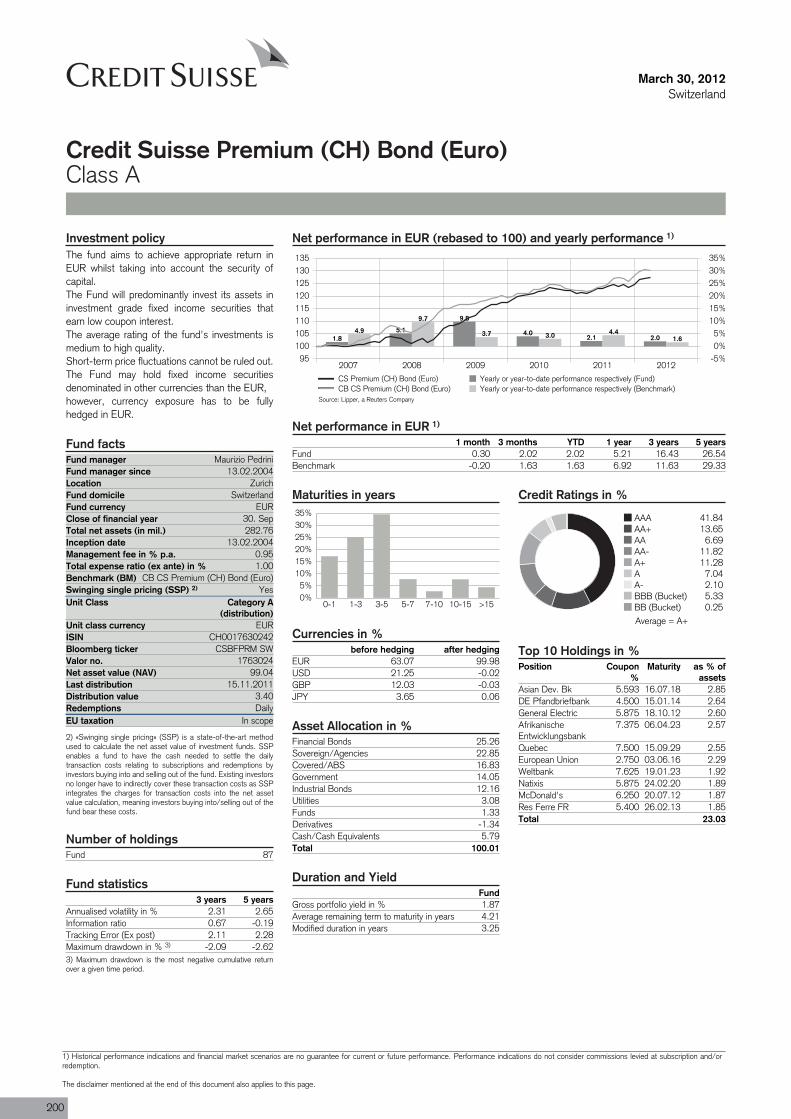

Credit Suisse PremiumCredit Suisse Premium (CH) Bond (£) GBP 3.5 23.4 1.9 9.4 3.8 198

Credit Suisse Premium (CH) Bond (Euro) EUR 5.2 16.4 -2.5 -7.2 2.3 200

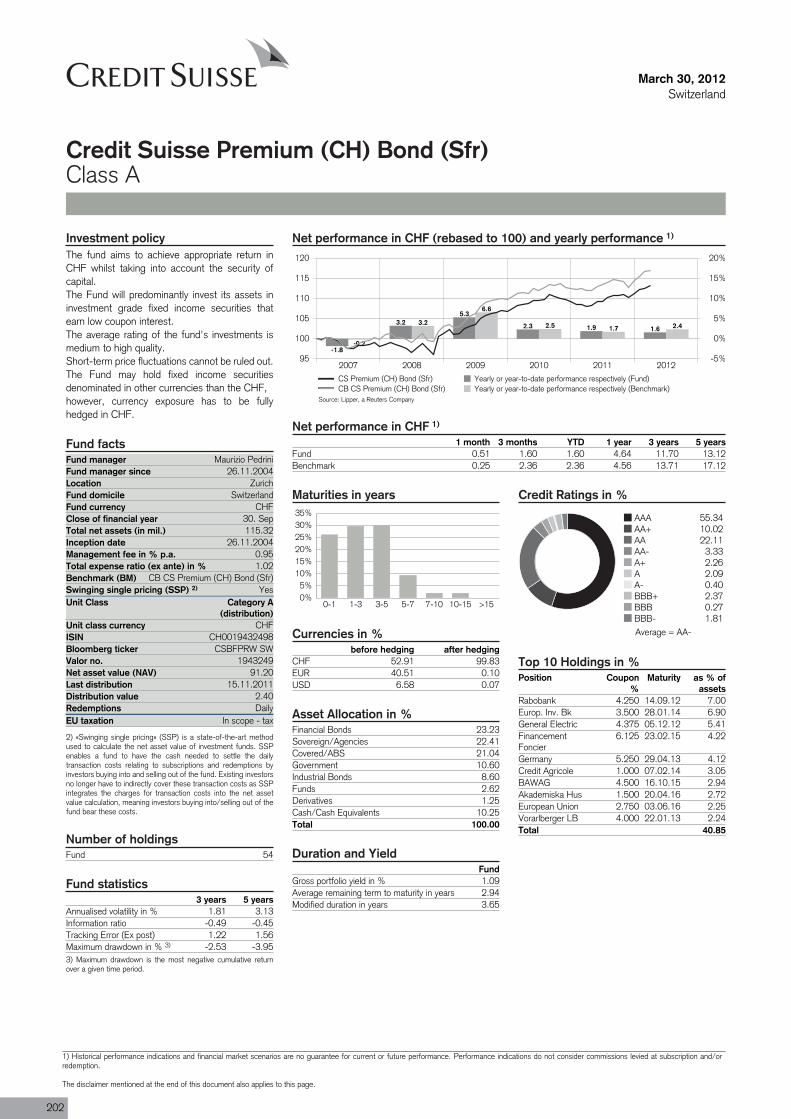

Credit Suisse Premium (CH) Bond (Sfr) CHF 4.6 11.7 4.6 11.7 1.8 202

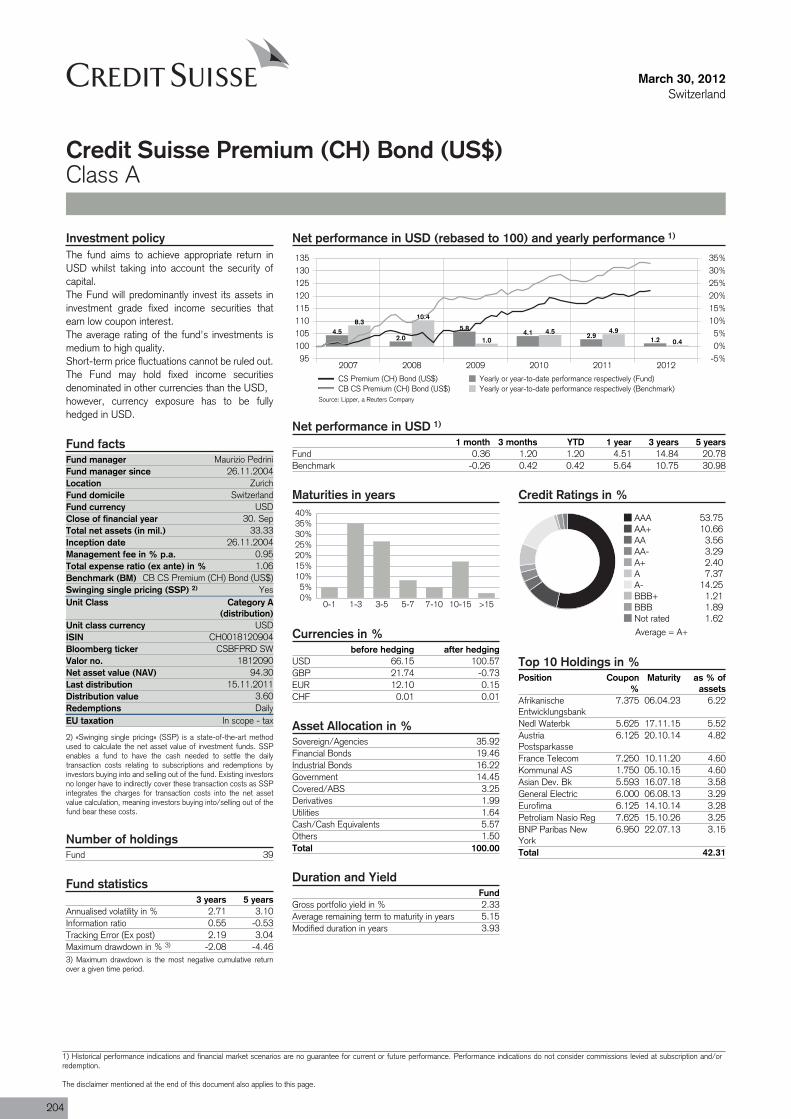

Credit Suisse Premium (CH) Bond (US$) USD 4.5 14.8 3.3 -8.7 2.7 204

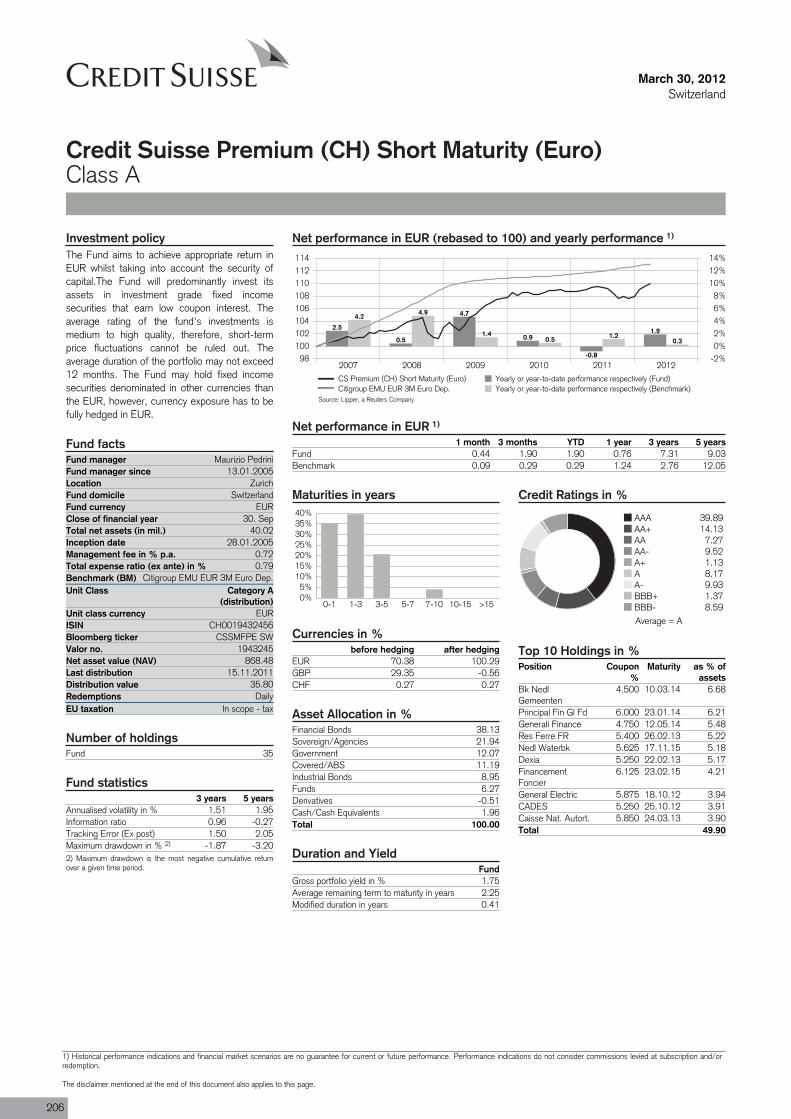

Credit Suisse Premium (CH) Short Maturity (Euro) EUR 0.8 7.3 -6.6 -14.4 1.5 206

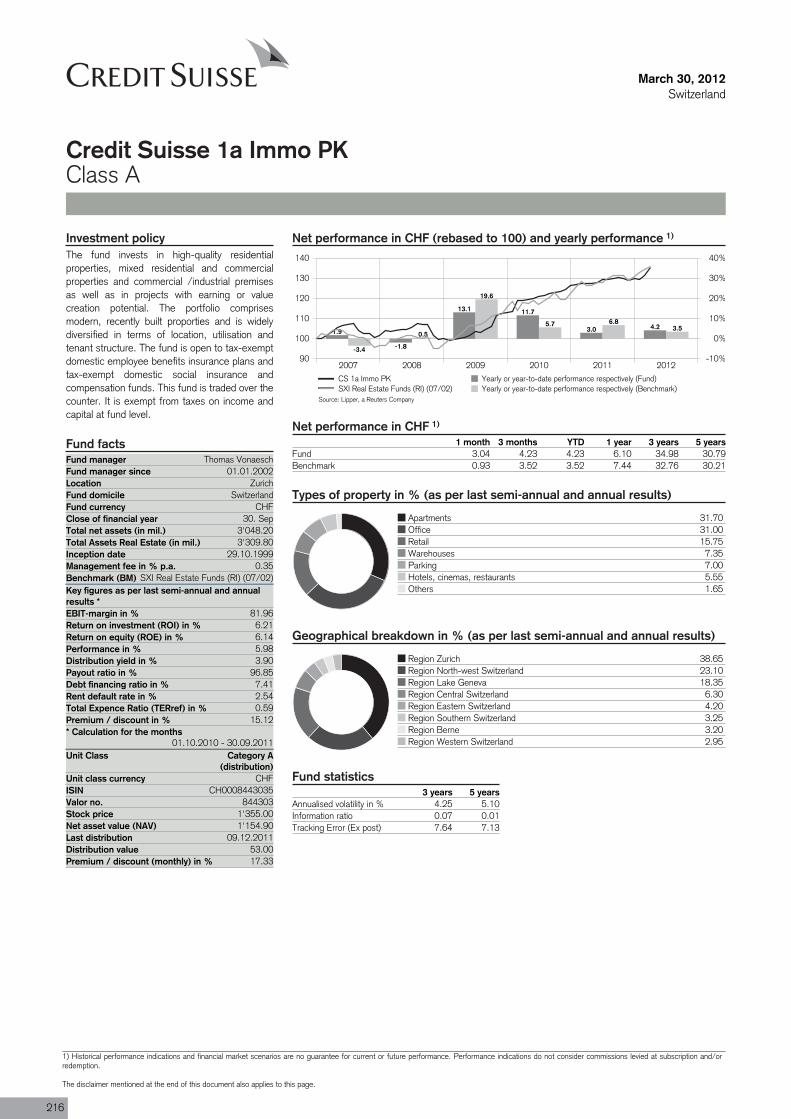

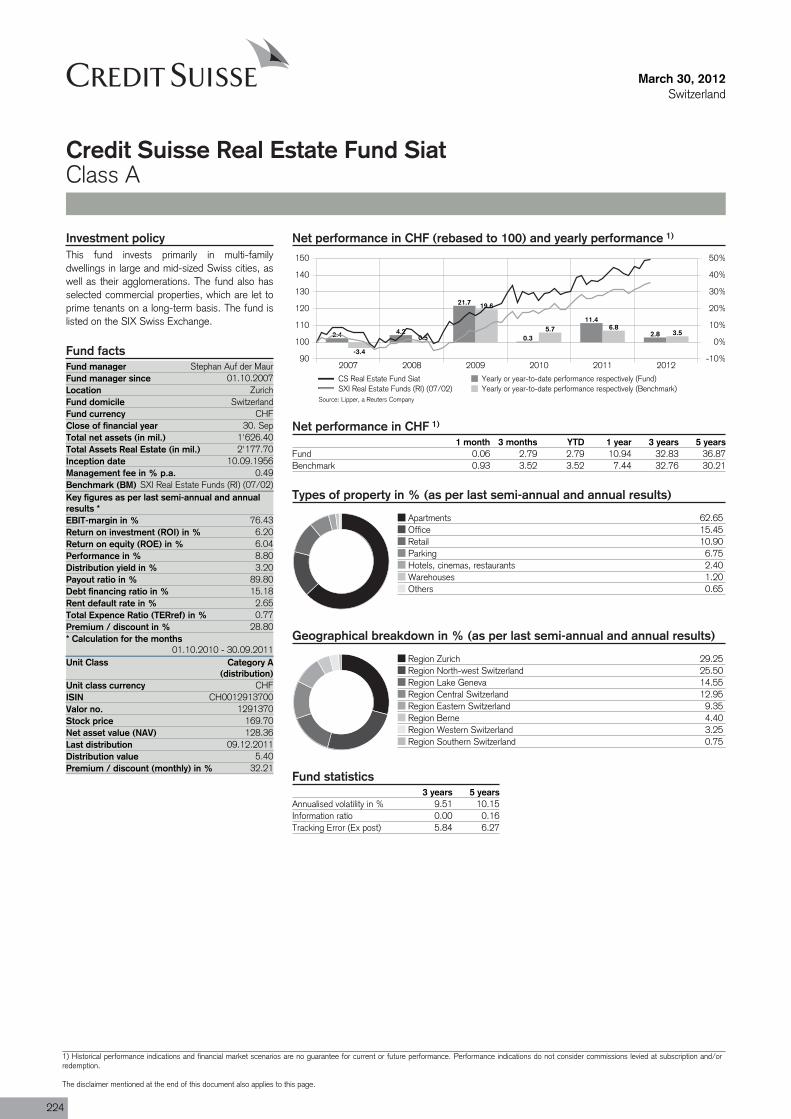

Credit Suisse Real Estate FundCredit Suisse 1a Immo PK CHF 6.1 35.0 6.1 35.0 4.3 216

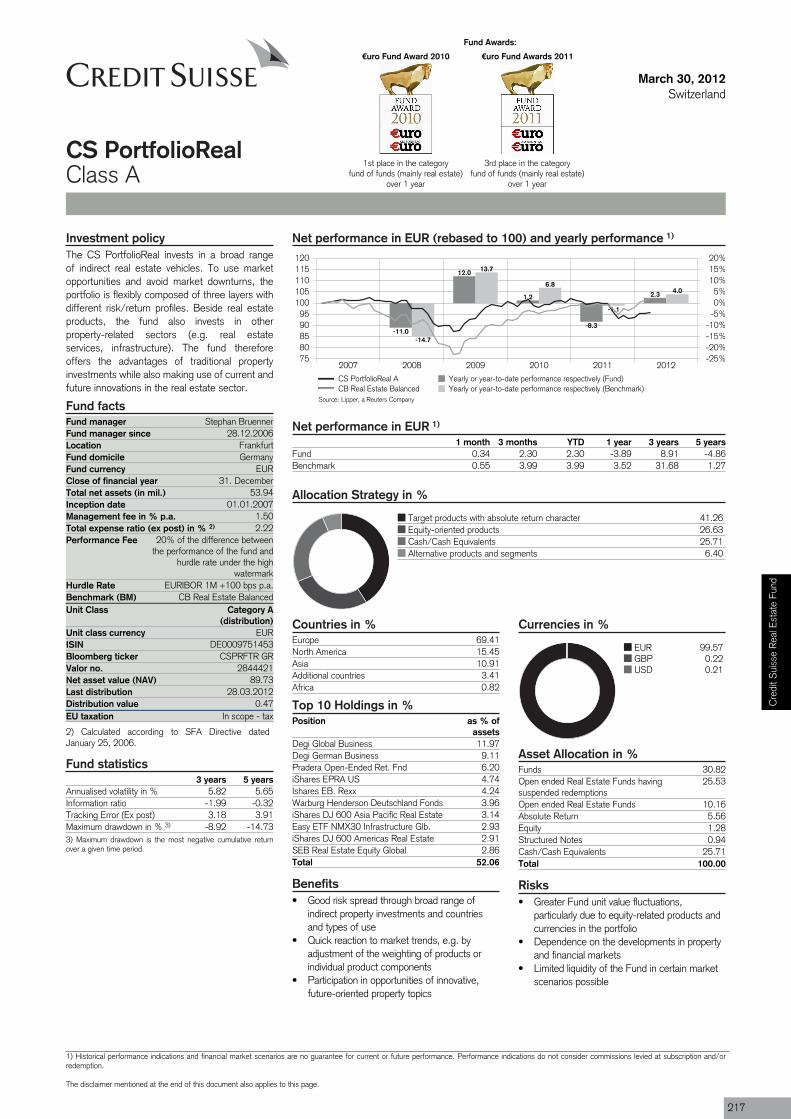

CS PortfolioReal A EUR -3.9 8.9 -10.9 -13.2 5.8 217

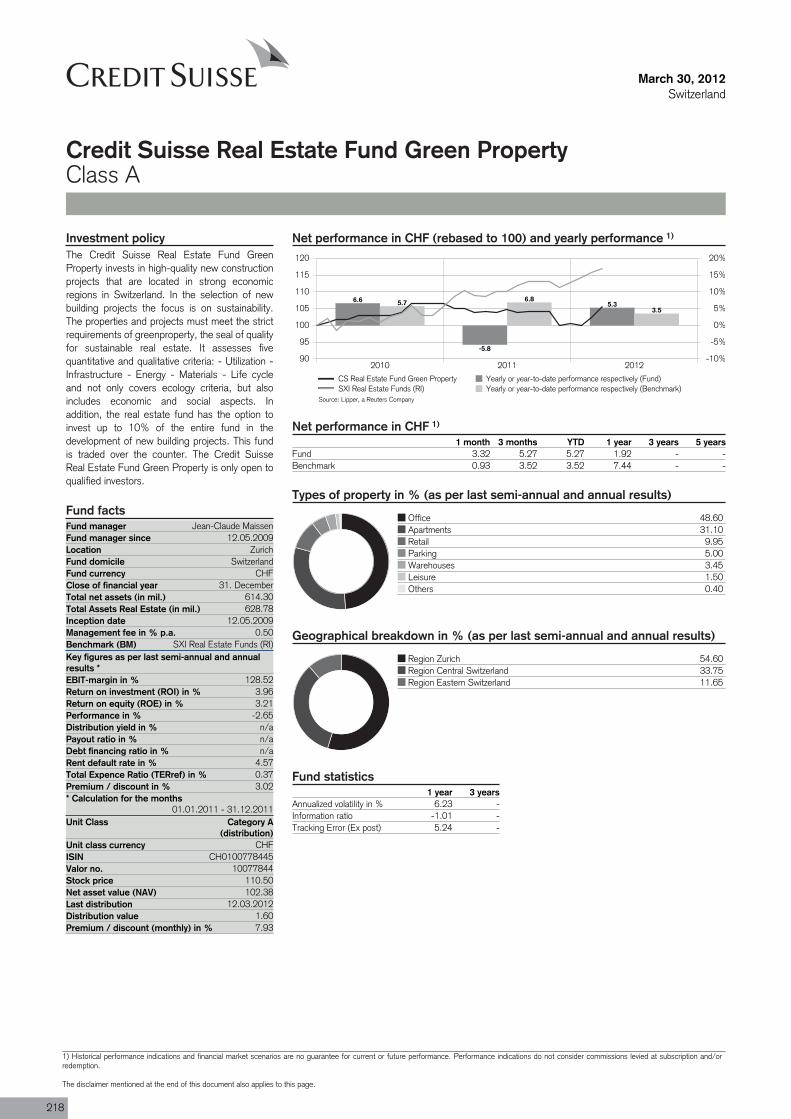

Credit Suisse Real Estate Fund Green Property CHF 1.9 n/a 1.9 n/a n/a 218

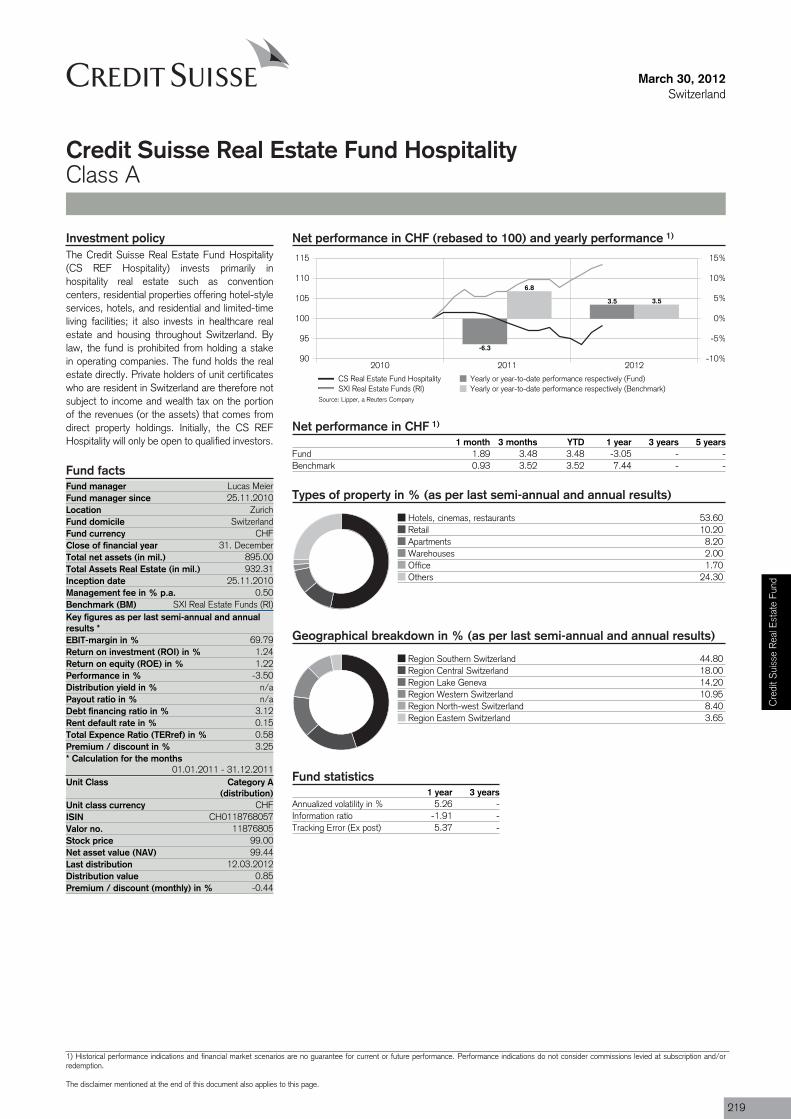

Credit Suisse Real Estate Fund Hospitality CHF -3.1 n/a -3.1 n/a n/a 219

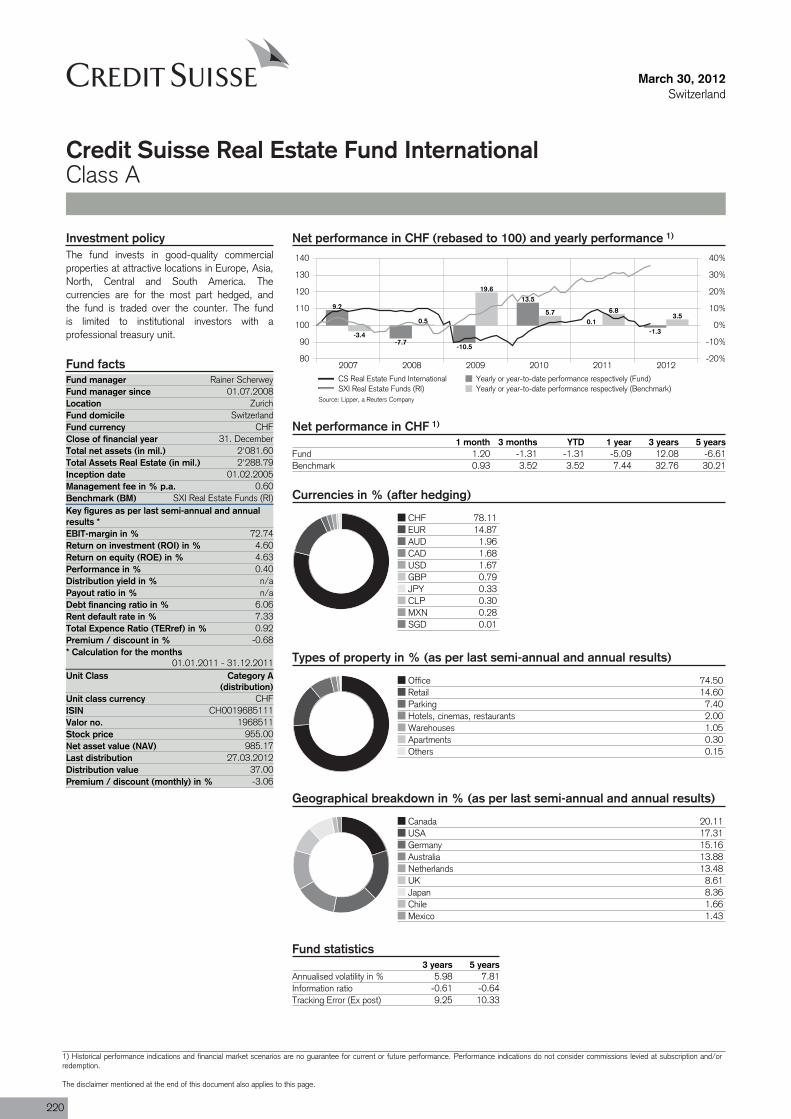

Credit Suisse Real Estate Fund International CHF -5.1 12.1 -5.1 12.1 6.0 220

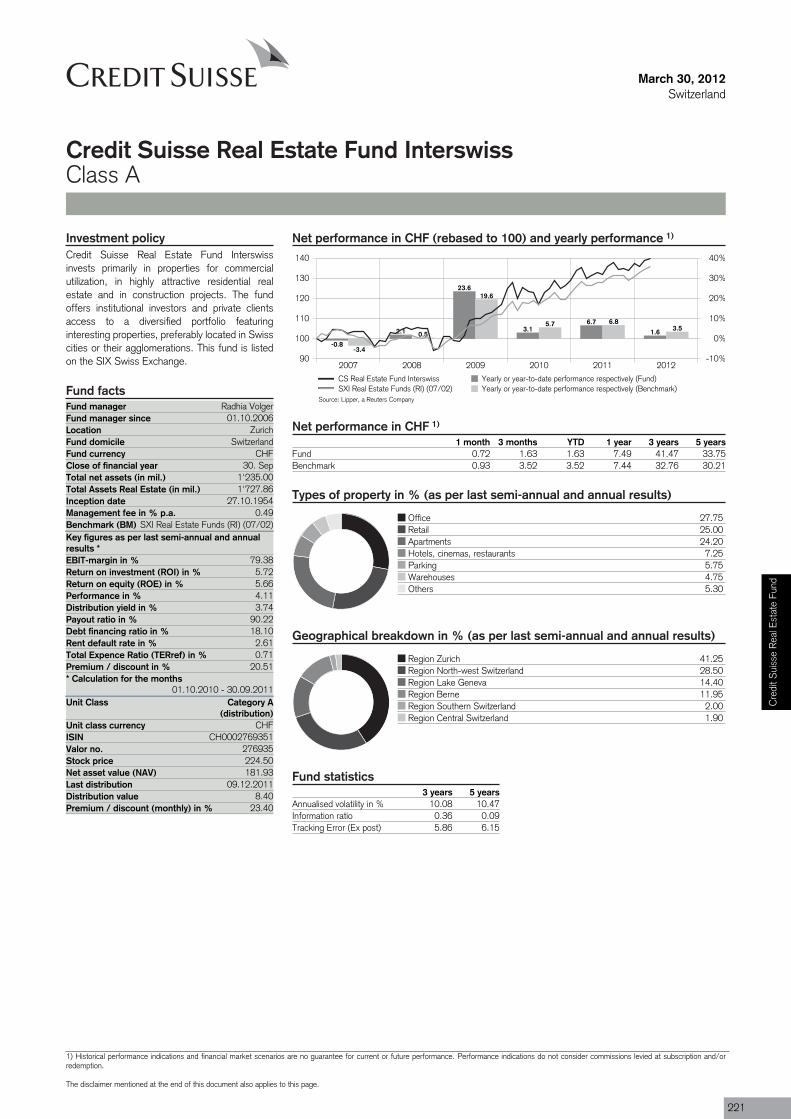

Credit Suisse Real Estate Fund Interswiss CHF 7.5 41.5 7.5 41.5 10.1 221

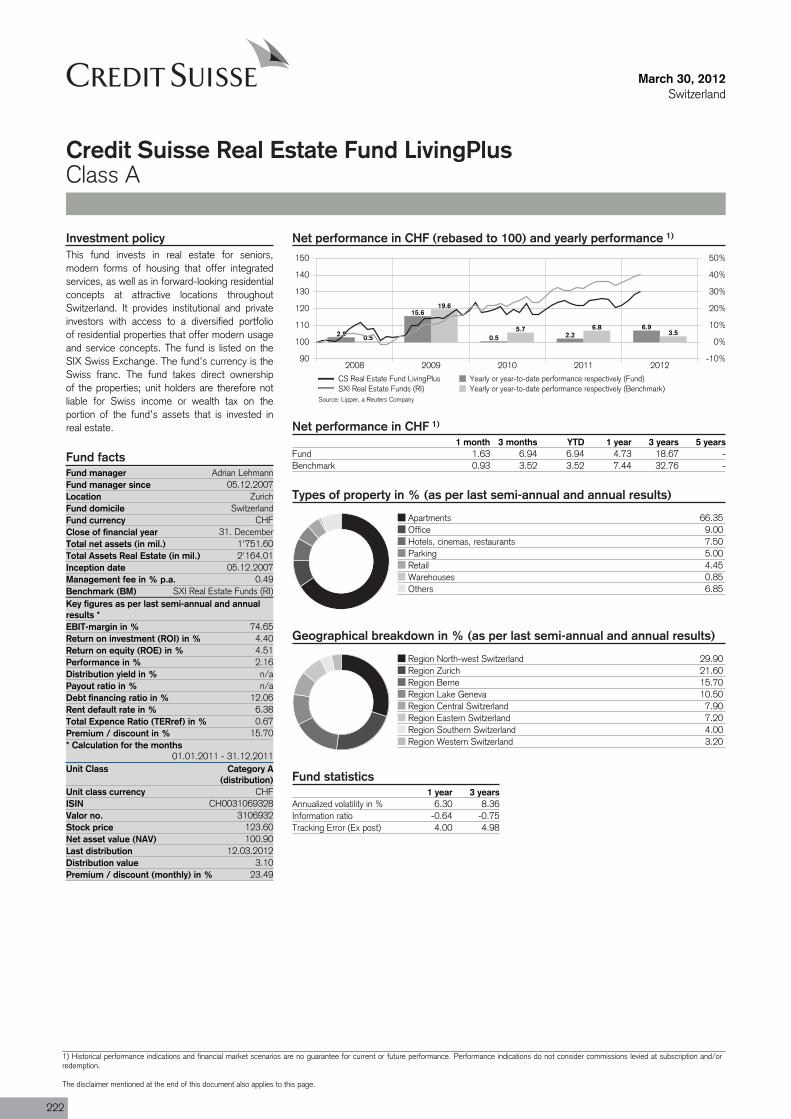

Credit Suisse Real Estate Fund LivingPlus CHF 4.7 18.7 4.7 18.7 8.4 222

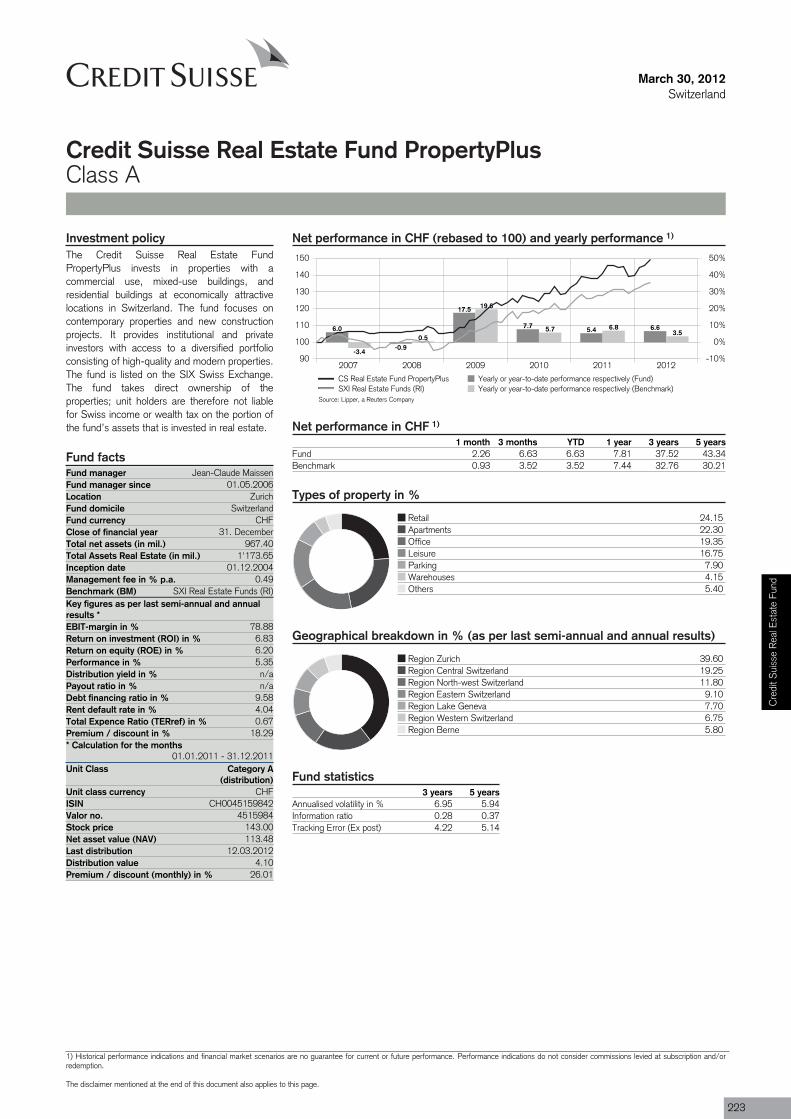

Credit Suisse Real Estate Fund PropertyPlus CHF 7.8 37.5 7.8 37.5 6.9 223

Credit Suisse Real Estate Fund Siat CHF 10.9 32.8 10.9 32.8 9.5 224

Ove

rvie

w

9

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

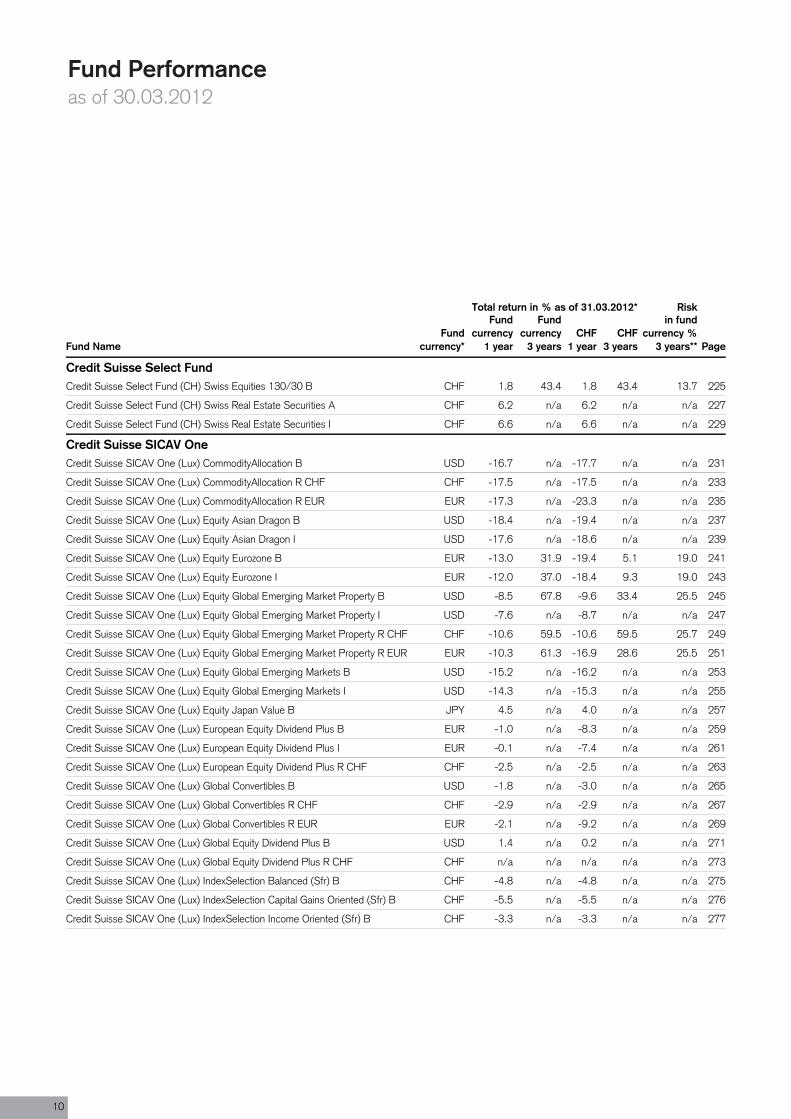

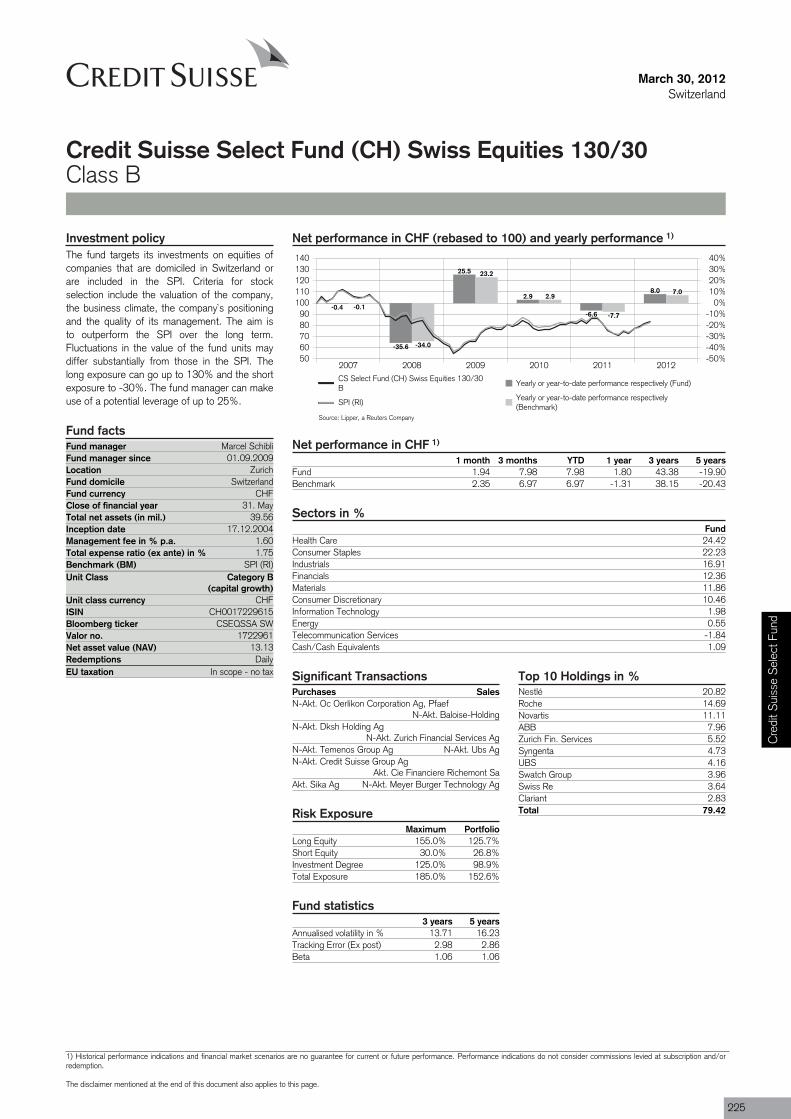

Credit Suisse Select FundCredit Suisse Select Fund (CH) Swiss Equities 130/30 B CHF 1.8 43.4 1.8 43.4 13.7 225

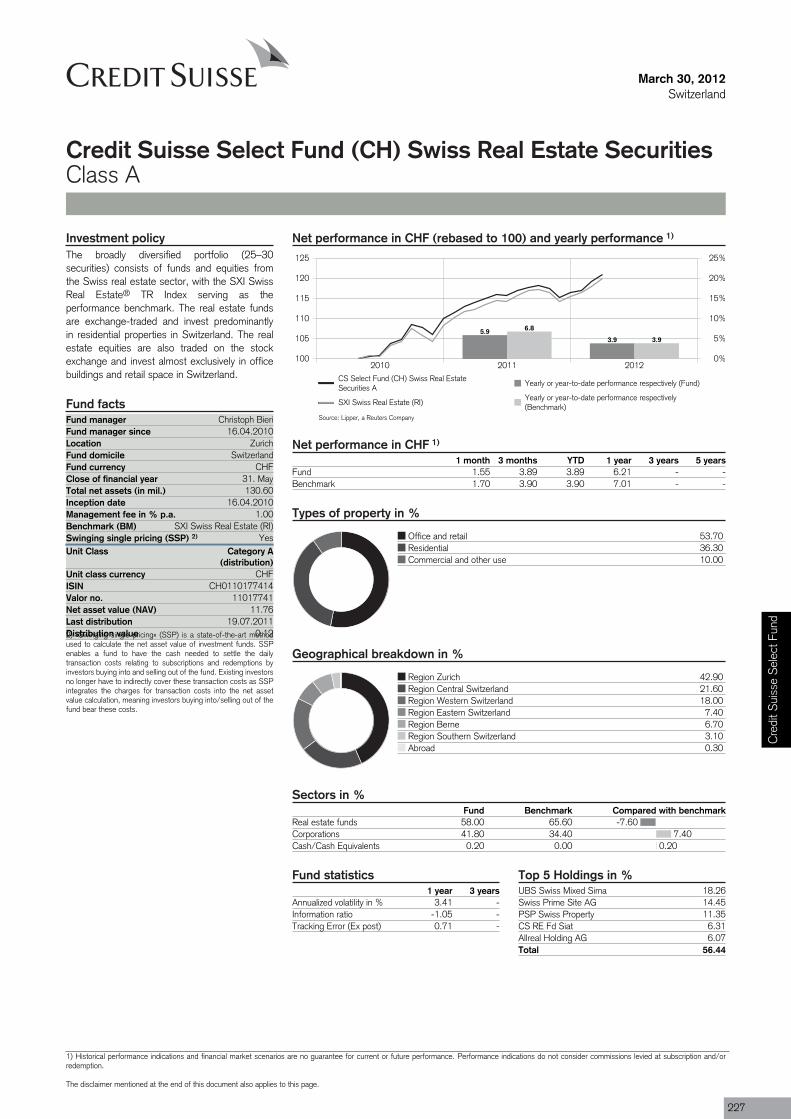

Credit Suisse Select Fund (CH) Swiss Real Estate Securities A CHF 6.2 n/a 6.2 n/a n/a 227

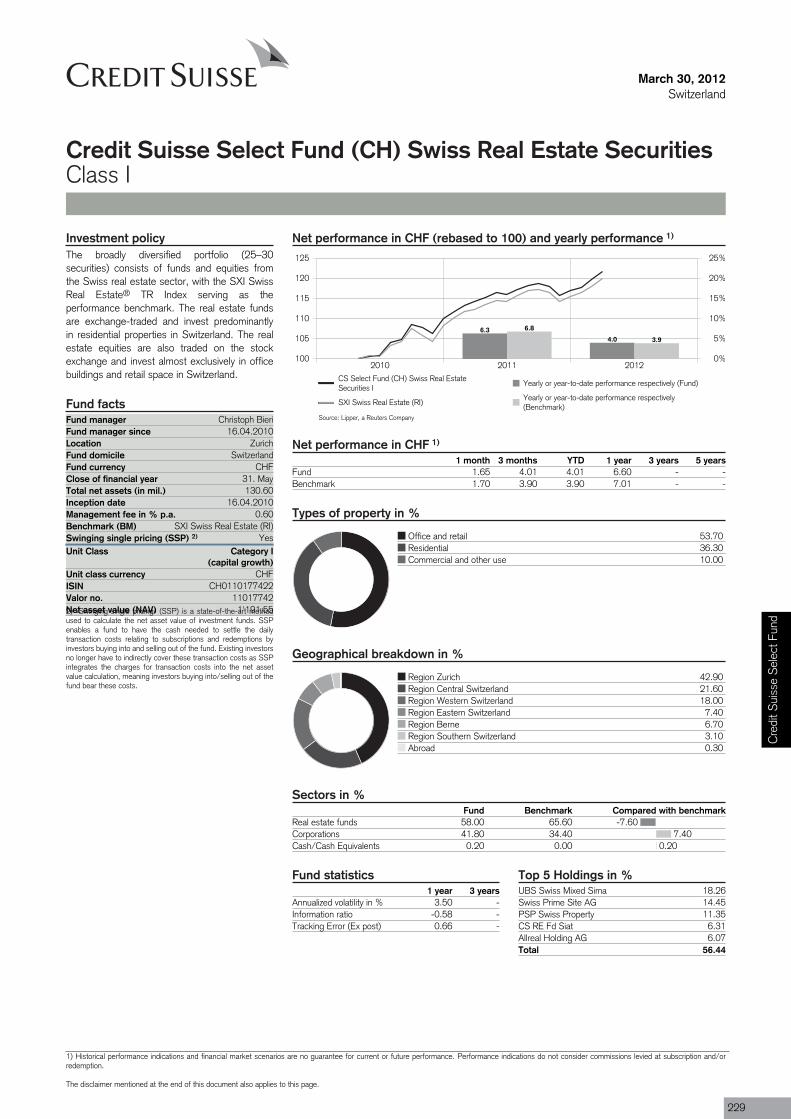

Credit Suisse Select Fund (CH) Swiss Real Estate Securities I CHF 6.6 n/a 6.6 n/a n/a 229

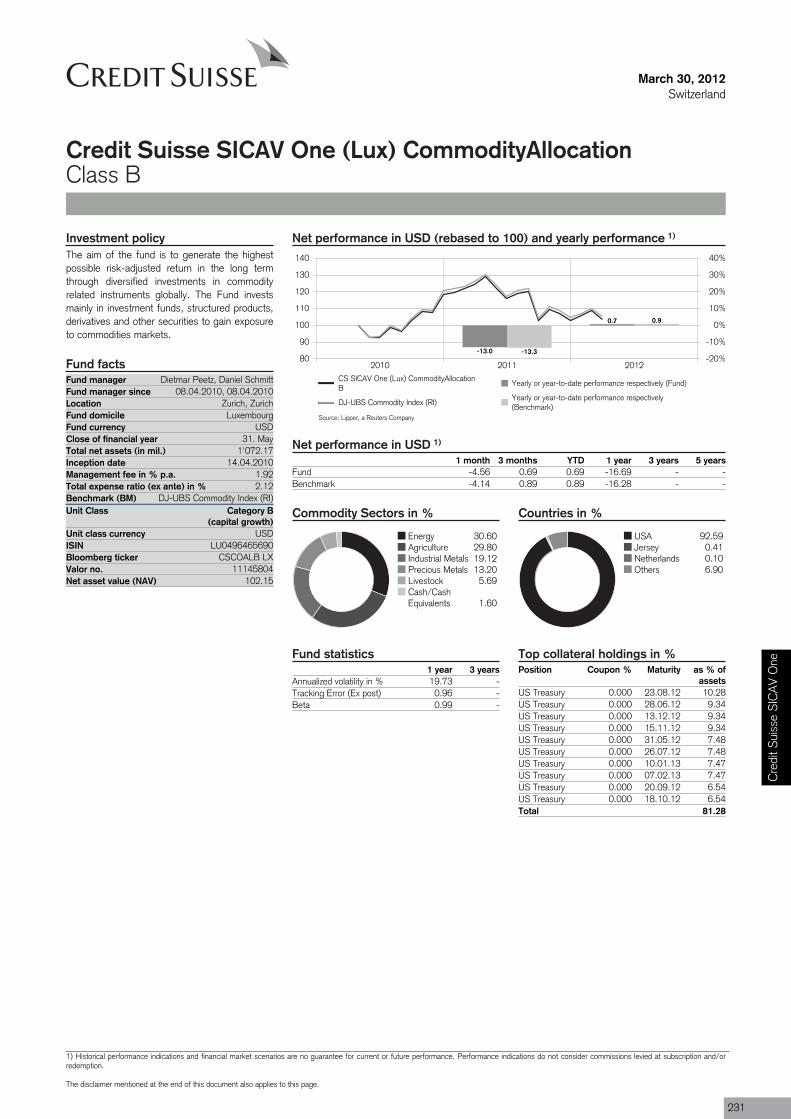

Credit Suisse SICAV OneCredit Suisse SICAV One (Lux) CommodityAllocation B USD -16.7 n/a -17.7 n/a n/a 231

Credit Suisse SICAV One (Lux) CommodityAllocation R CHF CHF -17.5 n/a -17.5 n/a n/a 233

Credit Suisse SICAV One (Lux) CommodityAllocation R EUR EUR -17.3 n/a -23.3 n/a n/a 235

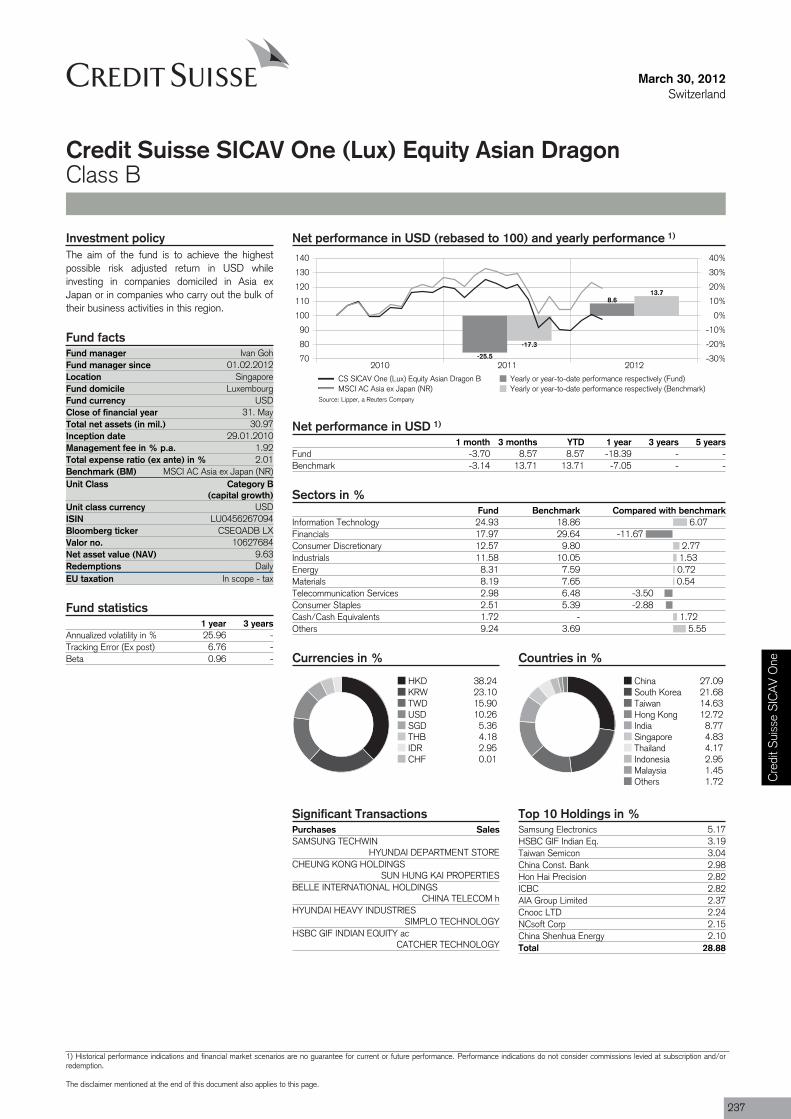

Credit Suisse SICAV One (Lux) Equity Asian Dragon B USD -18.4 n/a -19.4 n/a n/a 237

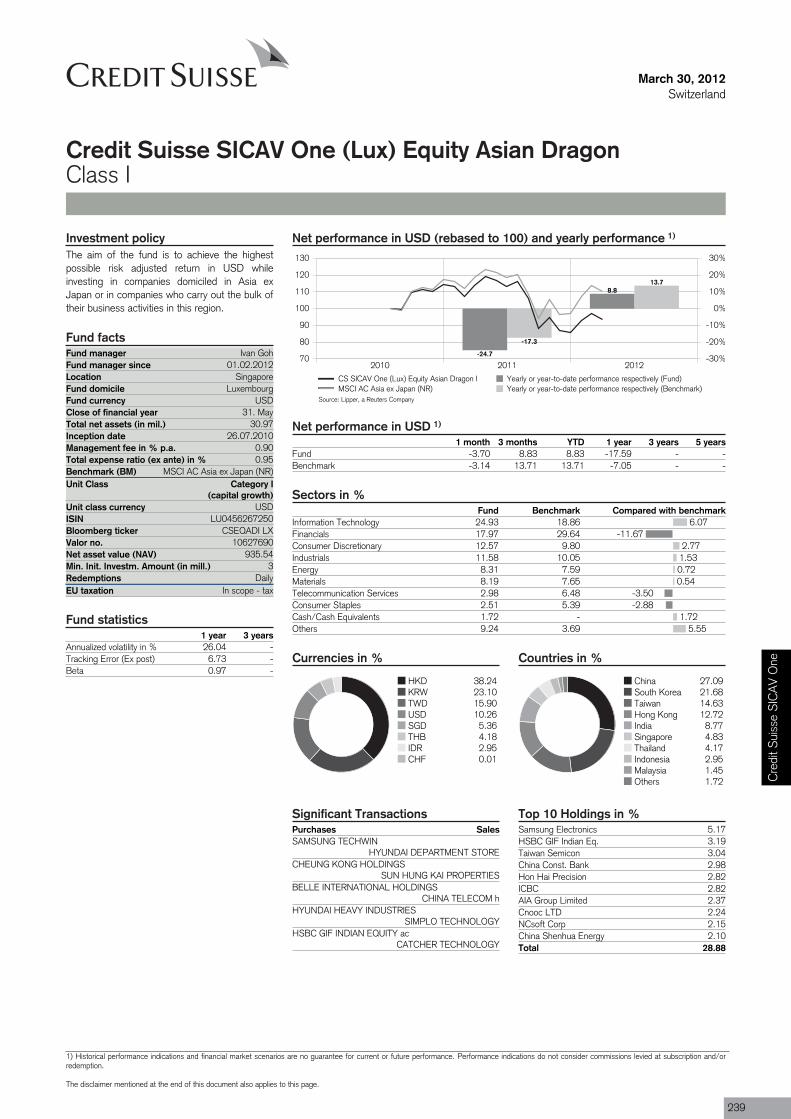

Credit Suisse SICAV One (Lux) Equity Asian Dragon I USD -17.6 n/a -18.6 n/a n/a 239

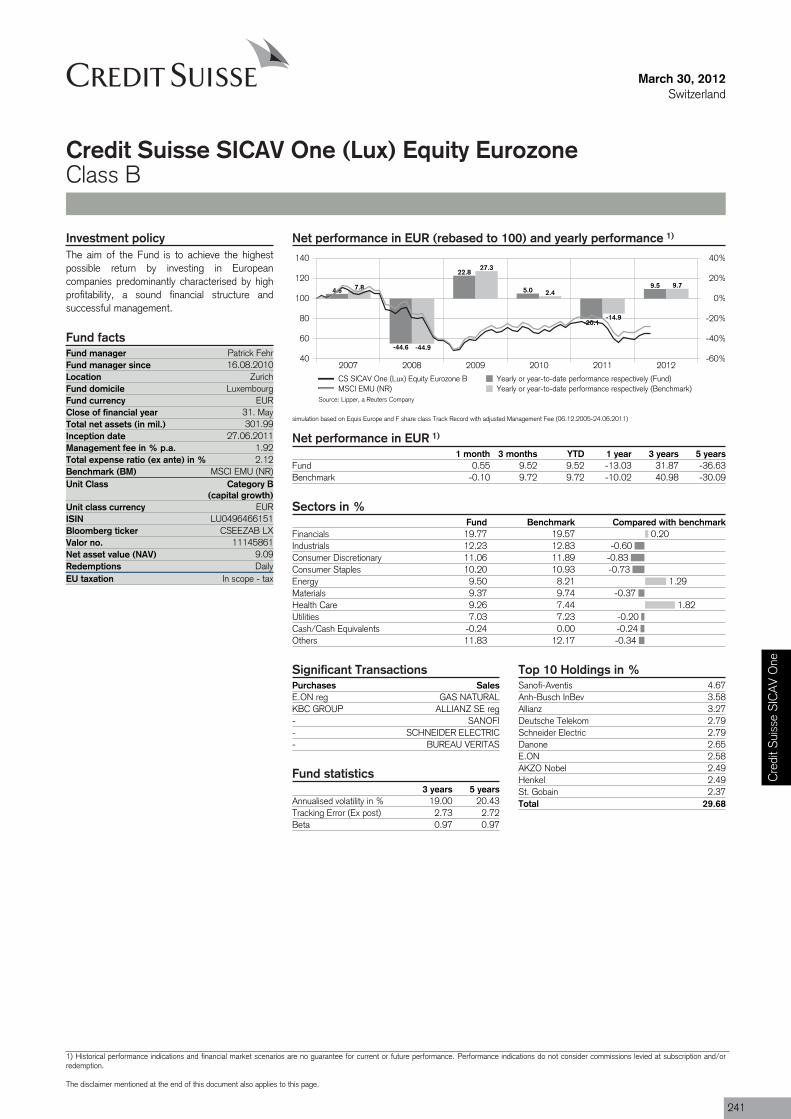

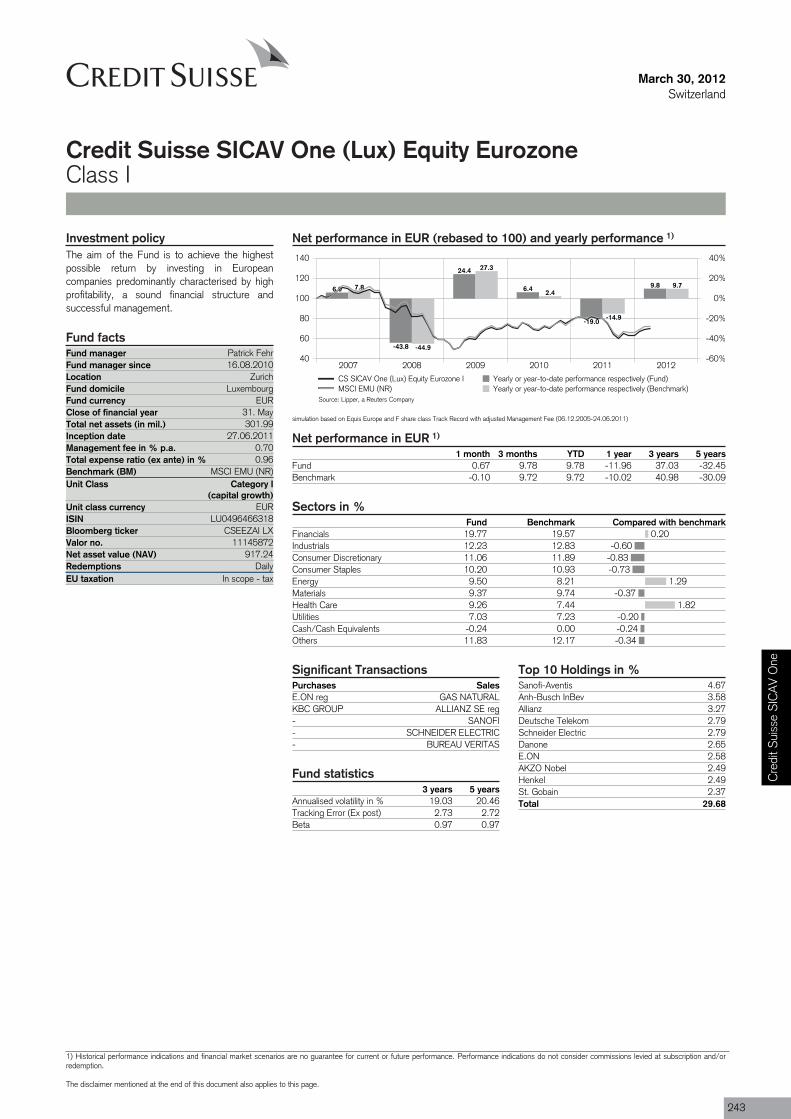

Credit Suisse SICAV One (Lux) Equity Eurozone B EUR -13.0 31.9 -19.4 5.1 19.0 241

Credit Suisse SICAV One (Lux) Equity Eurozone I EUR -12.0 37.0 -18.4 9.3 19.0 243

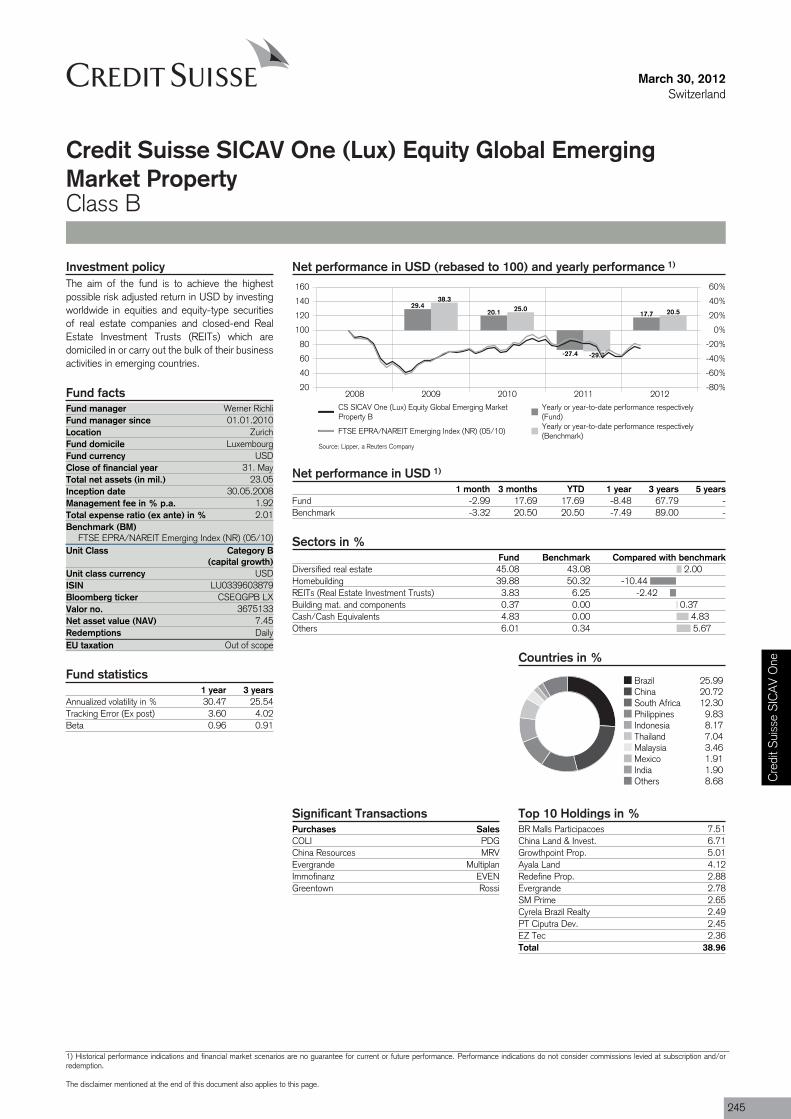

Credit Suisse SICAV One (Lux) Equity Global Emerging Market Property B USD -8.5 67.8 -9.6 33.4 25.5 245

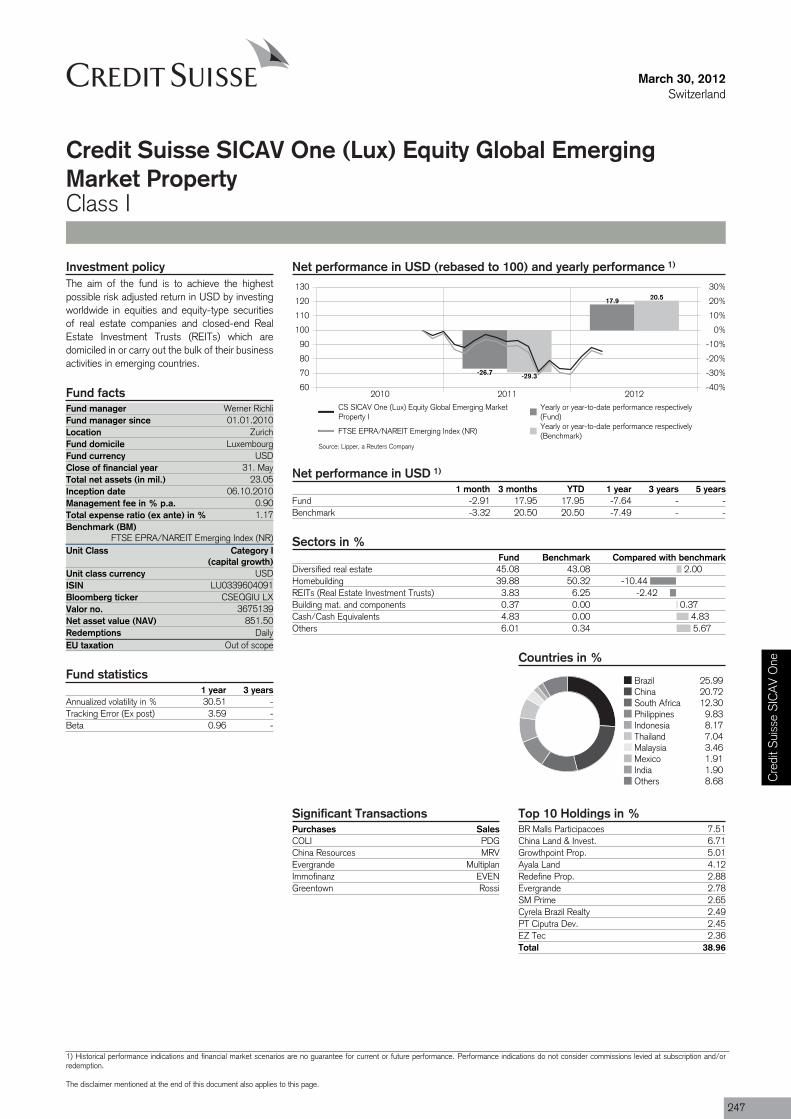

Credit Suisse SICAV One (Lux) Equity Global Emerging Market Property I USD -7.6 n/a -8.7 n/a n/a 247

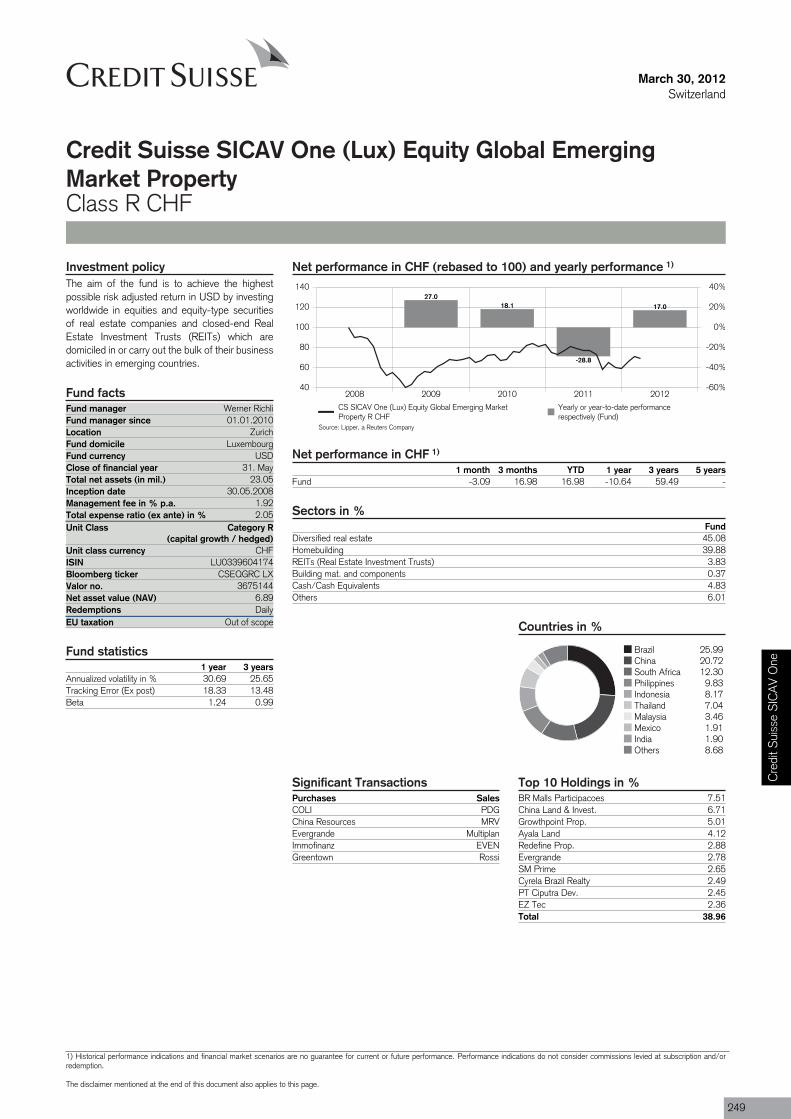

Credit Suisse SICAV One (Lux) Equity Global Emerging Market Property R CHF CHF -10.6 59.5 -10.6 59.5 25.7 249

Credit Suisse SICAV One (Lux) Equity Global Emerging Market Property R EUR EUR -10.3 61.3 -16.9 28.6 25.5 251

Credit Suisse SICAV One (Lux) Equity Global Emerging Markets B USD -15.2 n/a -16.2 n/a n/a 253

Credit Suisse SICAV One (Lux) Equity Global Emerging Markets I USD -14.3 n/a -15.3 n/a n/a 255

Credit Suisse SICAV One (Lux) Equity Japan Value B JPY 4.5 n/a 4.0 n/a n/a 257

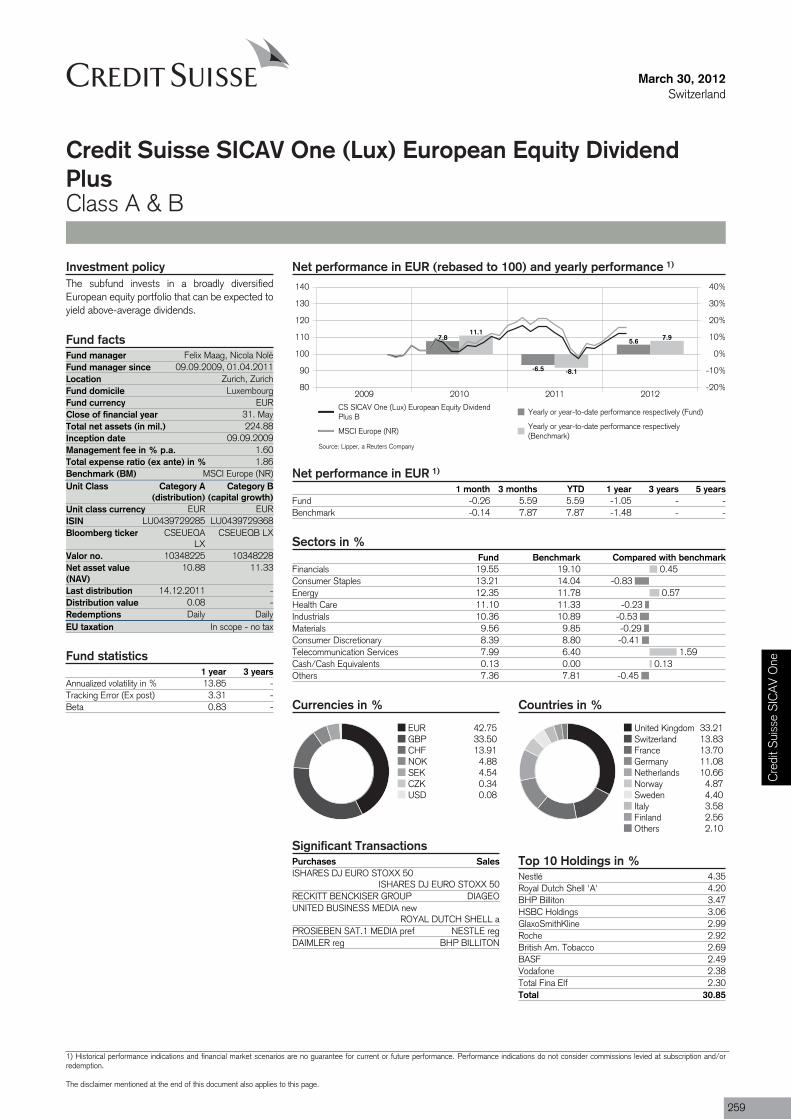

Credit Suisse SICAV One (Lux) European Equity Dividend Plus B EUR -1.0 n/a -8.3 n/a n/a 259

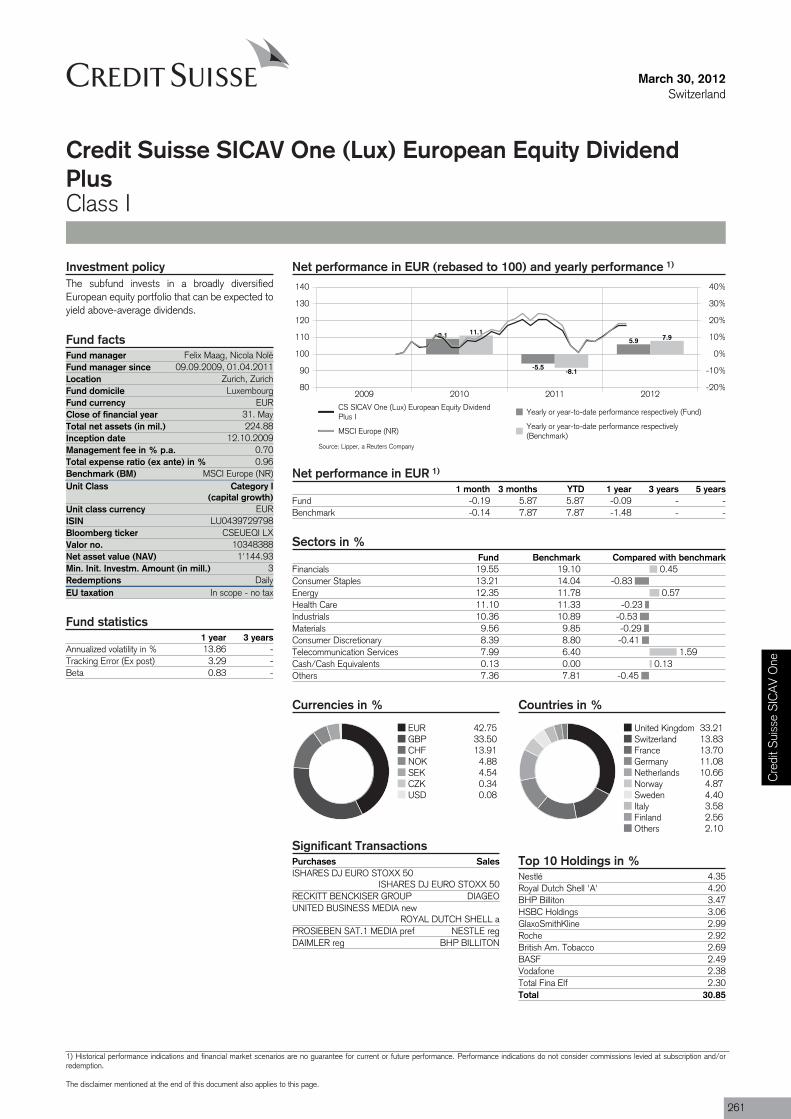

Credit Suisse SICAV One (Lux) European Equity Dividend Plus I EUR -0.1 n/a -7.4 n/a n/a 261

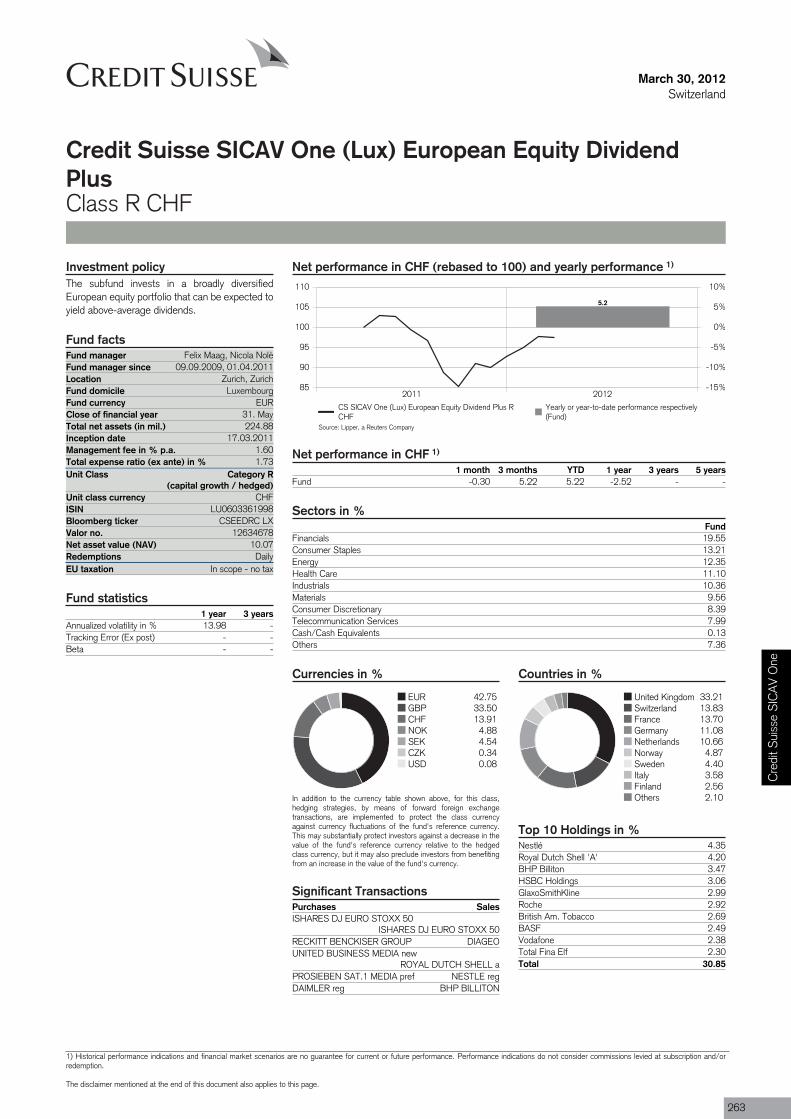

Credit Suisse SICAV One (Lux) European Equity Dividend Plus R CHF CHF -2.5 n/a -2.5 n/a n/a 263

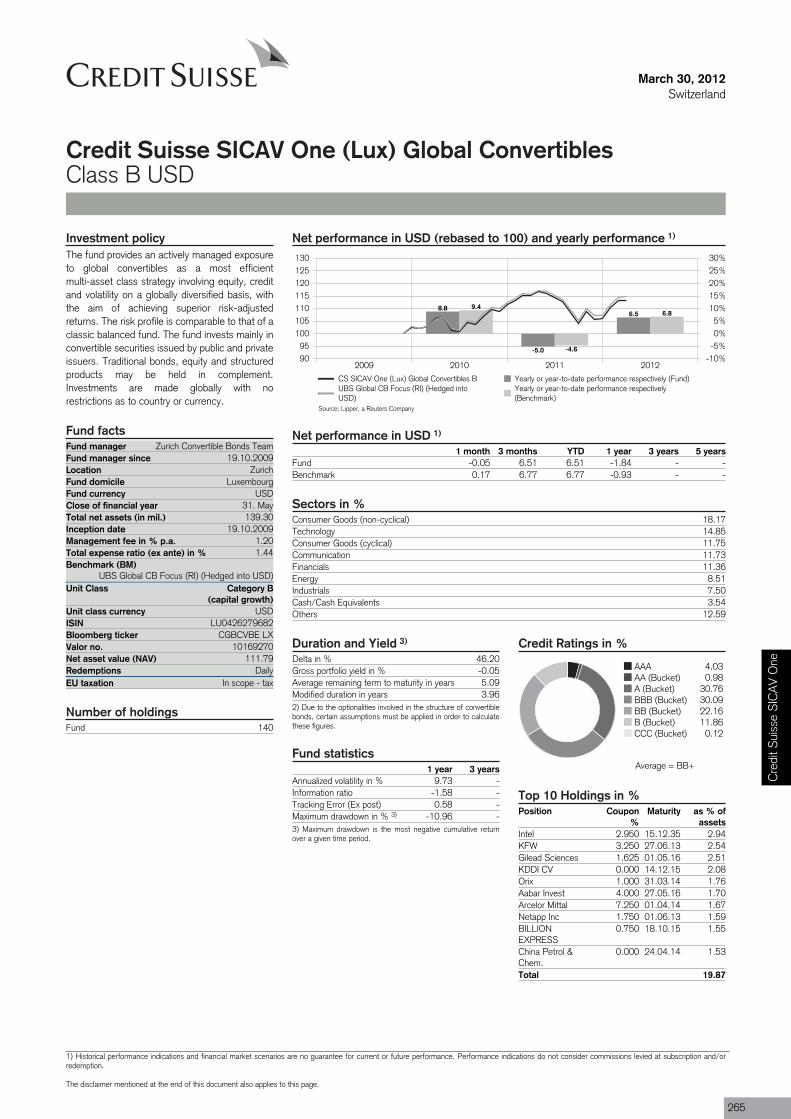

Credit Suisse SICAV One (Lux) Global Convertibles B USD -1.8 n/a -3.0 n/a n/a 265

Credit Suisse SICAV One (Lux) Global Convertibles R CHF CHF -2.9 n/a -2.9 n/a n/a 267

Credit Suisse SICAV One (Lux) Global Convertibles R EUR EUR -2.1 n/a -9.2 n/a n/a 269

Credit Suisse SICAV One (Lux) Global Equity Dividend Plus B USD 1.4 n/a 0.2 n/a n/a 271

Credit Suisse SICAV One (Lux) Global Equity Dividend Plus R CHF CHF n/a n/a n/a n/a n/a 273

Credit Suisse SICAV One (Lux) IndexSelection Balanced (Sfr) B CHF -4.8 n/a -4.8 n/a n/a 275

Credit Suisse SICAV One (Lux) IndexSelection Capital Gains Oriented (Sfr) B CHF -5.5 n/a -5.5 n/a n/a 276

Credit Suisse SICAV One (Lux) IndexSelection Income Oriented (Sfr) B CHF -3.3 n/a -3.3 n/a n/a 277

Fund Performanceas of 30.03.2012

10

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

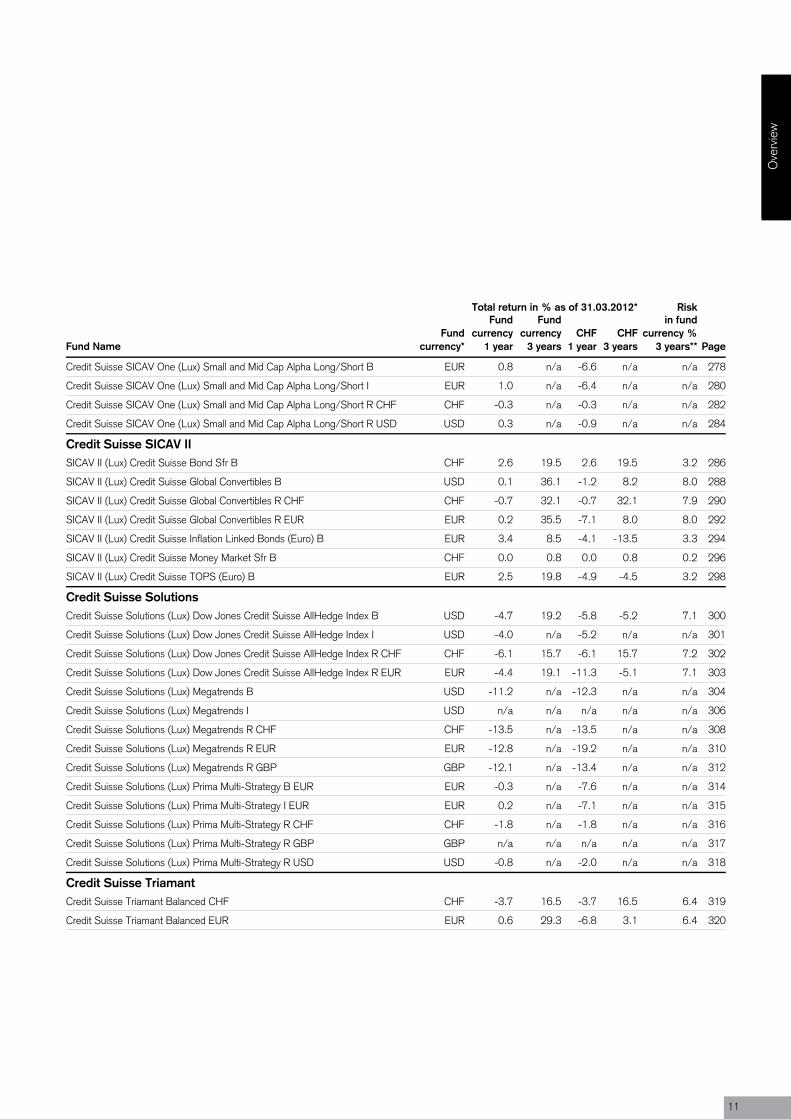

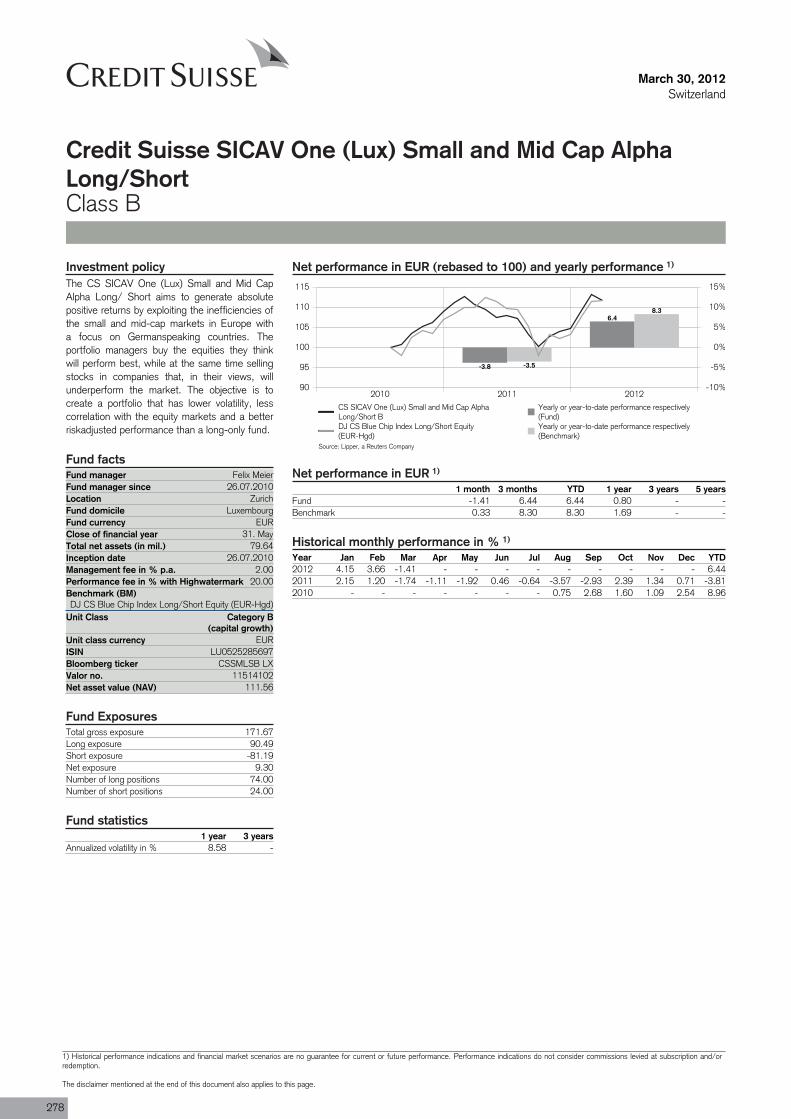

Credit Suisse SICAV One (Lux) Small and Mid Cap Alpha Long/Short B EUR 0.8 n/a -6.6 n/a n/a 278

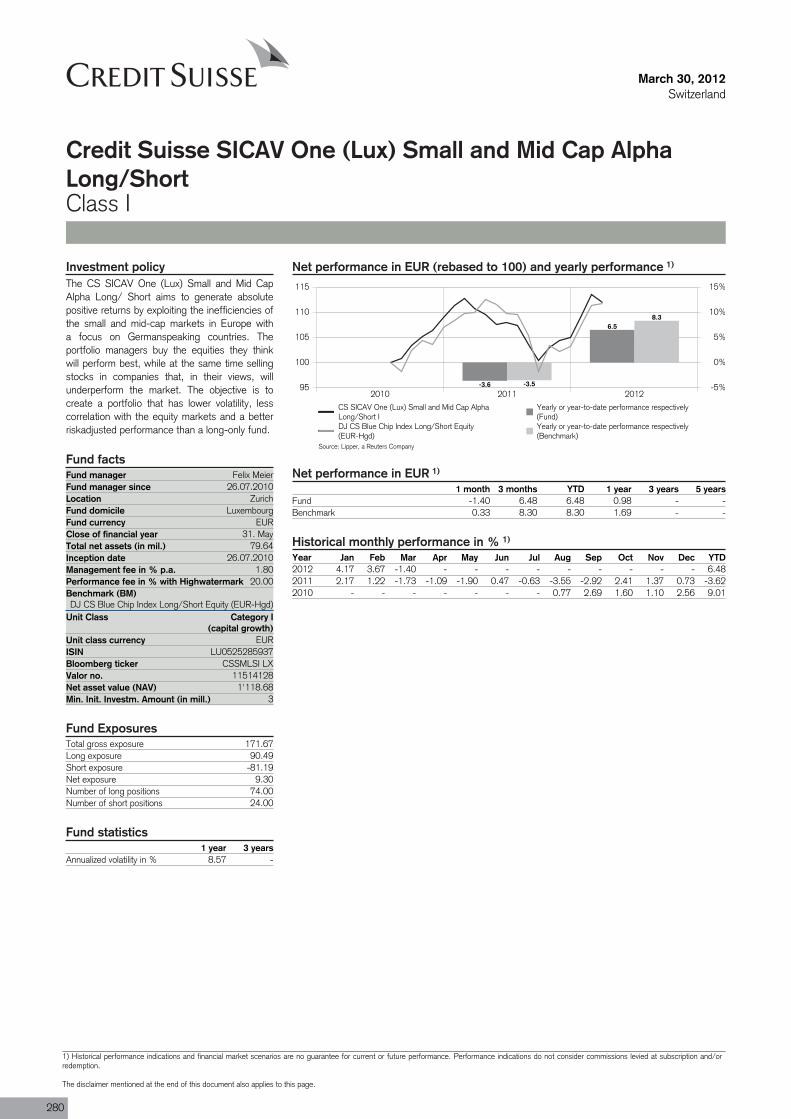

Credit Suisse SICAV One (Lux) Small and Mid Cap Alpha Long/Short I EUR 1.0 n/a -6.4 n/a n/a 280

Credit Suisse SICAV One (Lux) Small and Mid Cap Alpha Long/Short R CHF CHF -0.3 n/a -0.3 n/a n/a 282

Credit Suisse SICAV One (Lux) Small and Mid Cap Alpha Long/Short R USD USD 0.3 n/a -0.9 n/a n/a 284

Credit Suisse SICAV IISICAV II (Lux) Credit Suisse Bond Sfr B CHF 2.6 19.5 2.6 19.5 3.2 286

SICAV II (Lux) Credit Suisse Global Convertibles B USD 0.1 36.1 -1.2 8.2 8.0 288

SICAV II (Lux) Credit Suisse Global Convertibles R CHF CHF -0.7 32.1 -0.7 32.1 7.9 290

SICAV II (Lux) Credit Suisse Global Convertibles R EUR EUR 0.2 35.5 -7.1 8.0 8.0 292

SICAV II (Lux) Credit Suisse Inflation Linked Bonds (Euro) B EUR 3.4 8.5 -4.1 -13.5 3.3 294

SICAV II (Lux) Credit Suisse Money Market Sfr B CHF 0.0 0.8 0.0 0.8 0.2 296

SICAV II (Lux) Credit Suisse TOPS (Euro) B EUR 2.5 19.8 -4.9 -4.5 3.2 298

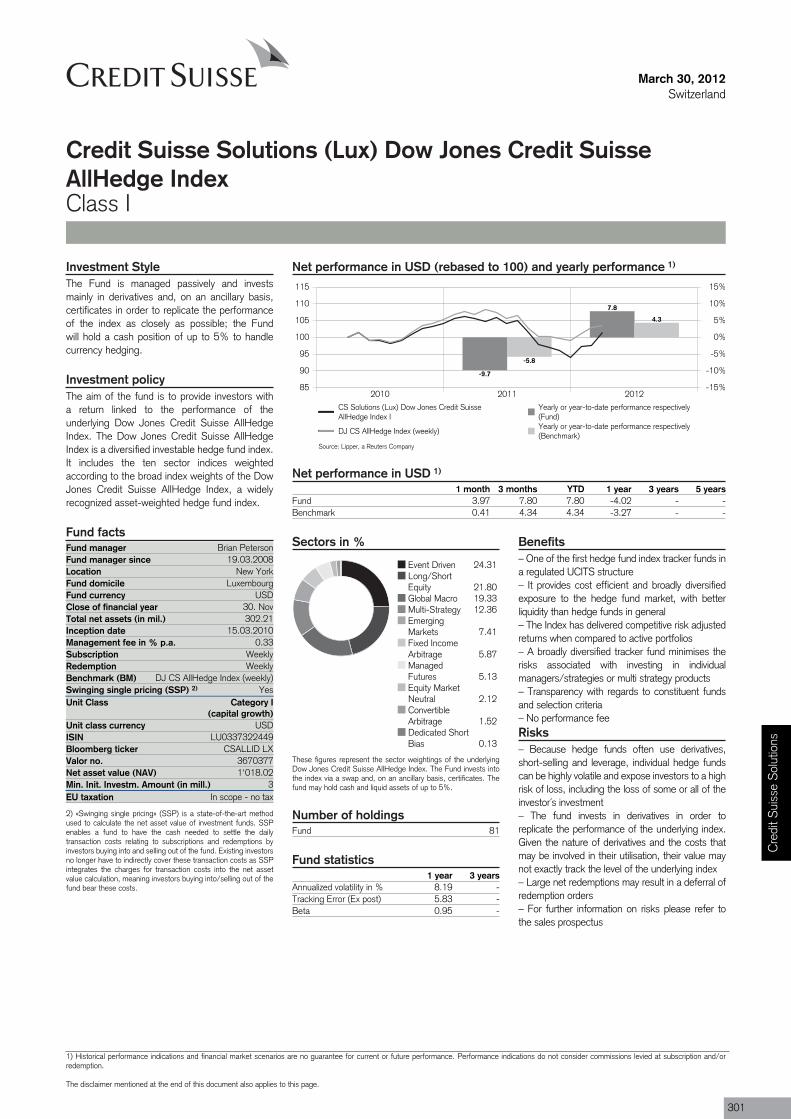

Credit Suisse SolutionsCredit Suisse Solutions (Lux) Dow Jones Credit Suisse AllHedge Index B USD -4.7 19.2 -5.8 -5.2 7.1 300

Credit Suisse Solutions (Lux) Dow Jones Credit Suisse AllHedge Index I USD -4.0 n/a -5.2 n/a n/a 301

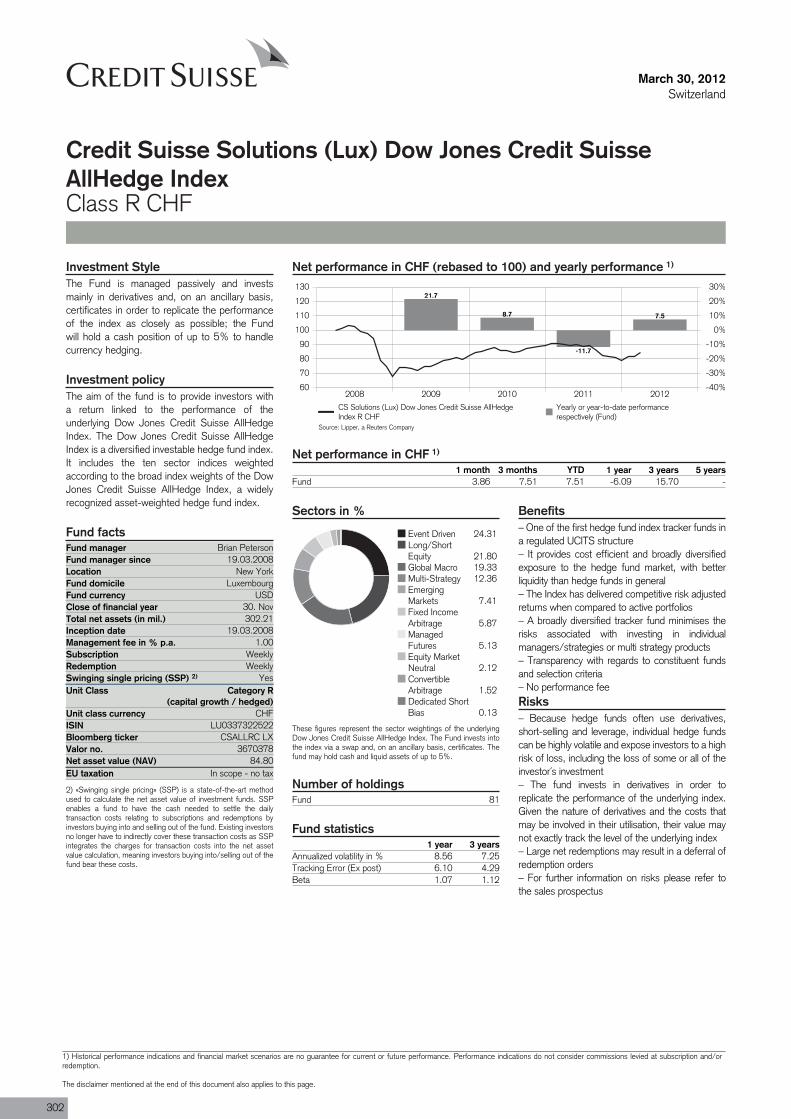

Credit Suisse Solutions (Lux) Dow Jones Credit Suisse AllHedge Index R CHF CHF -6.1 15.7 -6.1 15.7 7.2 302

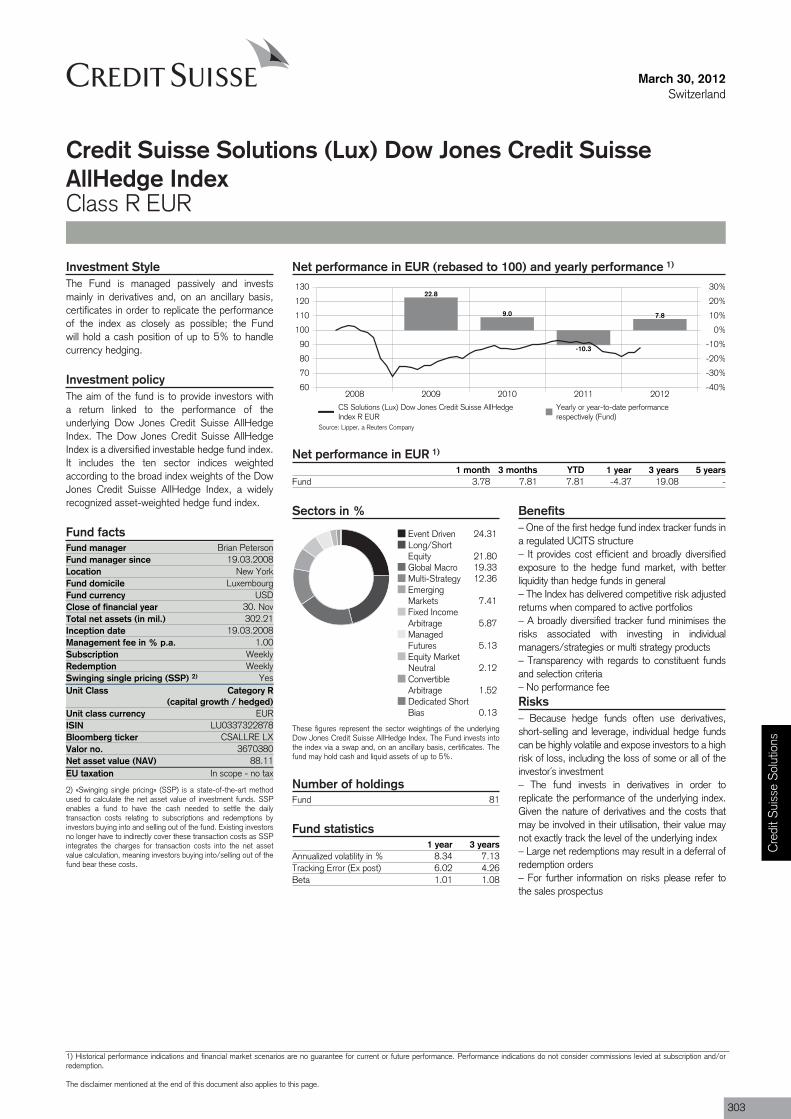

Credit Suisse Solutions (Lux) Dow Jones Credit Suisse AllHedge Index R EUR EUR -4.4 19.1 -11.3 -5.1 7.1 303

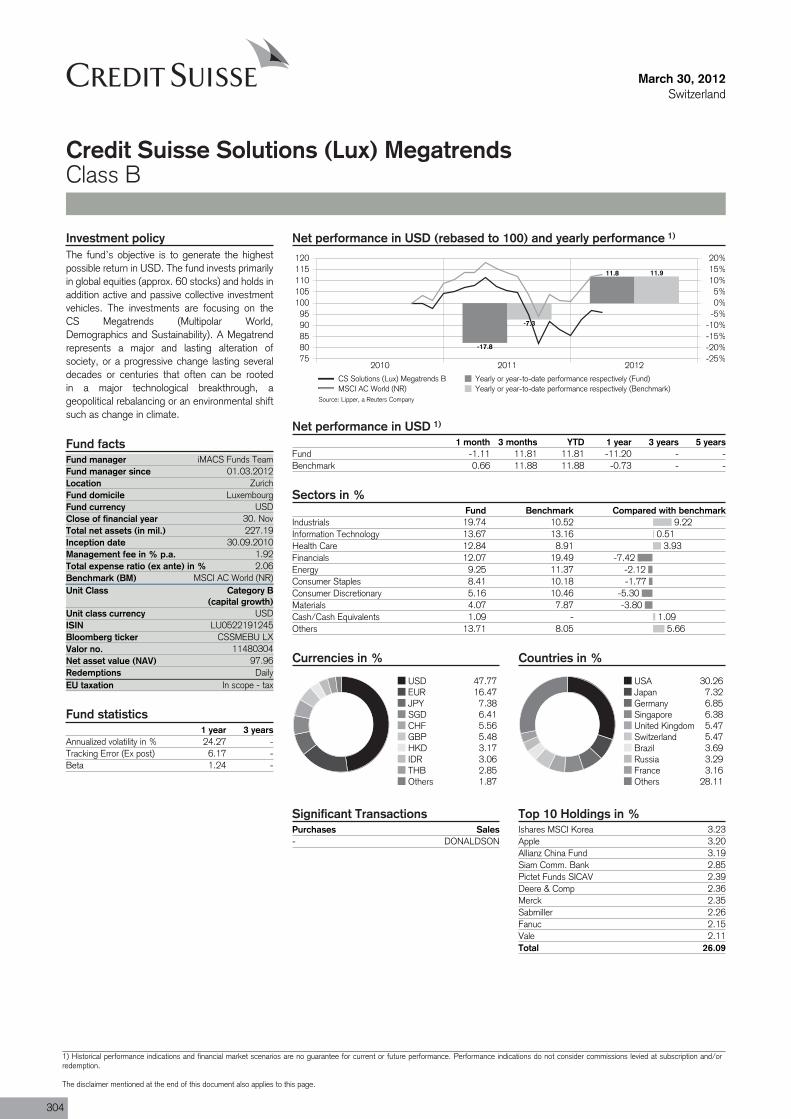

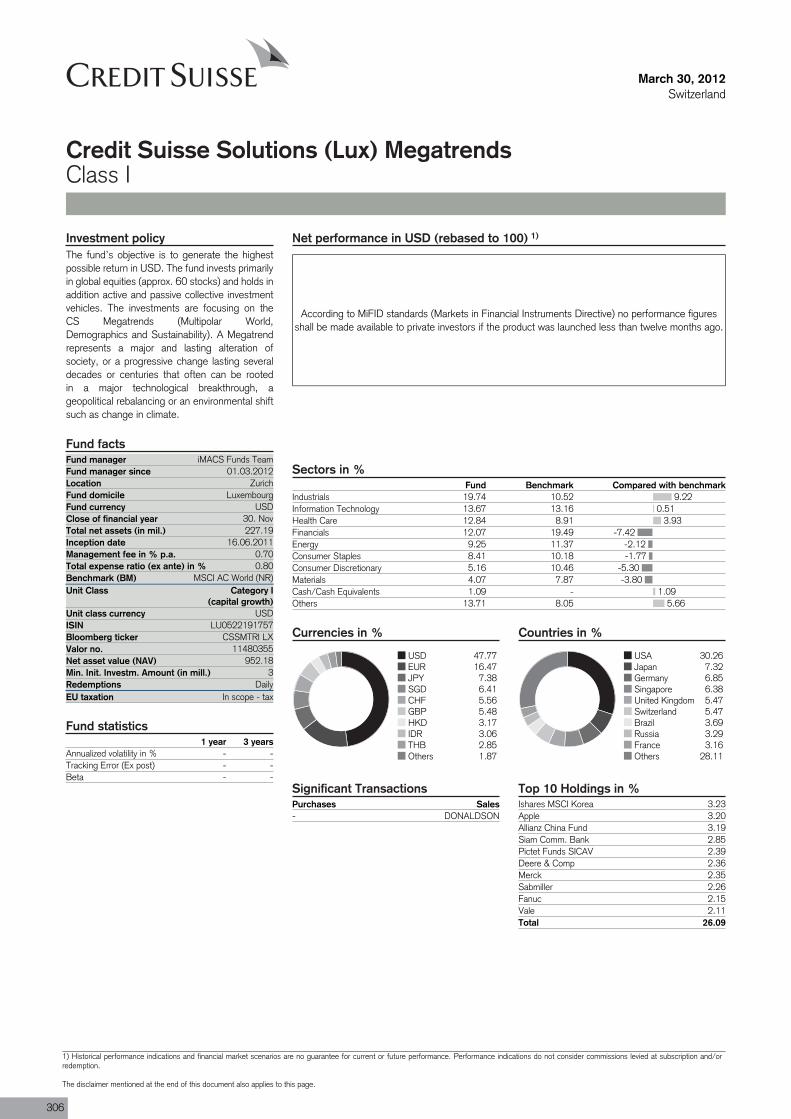

Credit Suisse Solutions (Lux) Megatrends B USD -11.2 n/a -12.3 n/a n/a 304

Credit Suisse Solutions (Lux) Megatrends I USD n/a n/a n/a n/a n/a 306

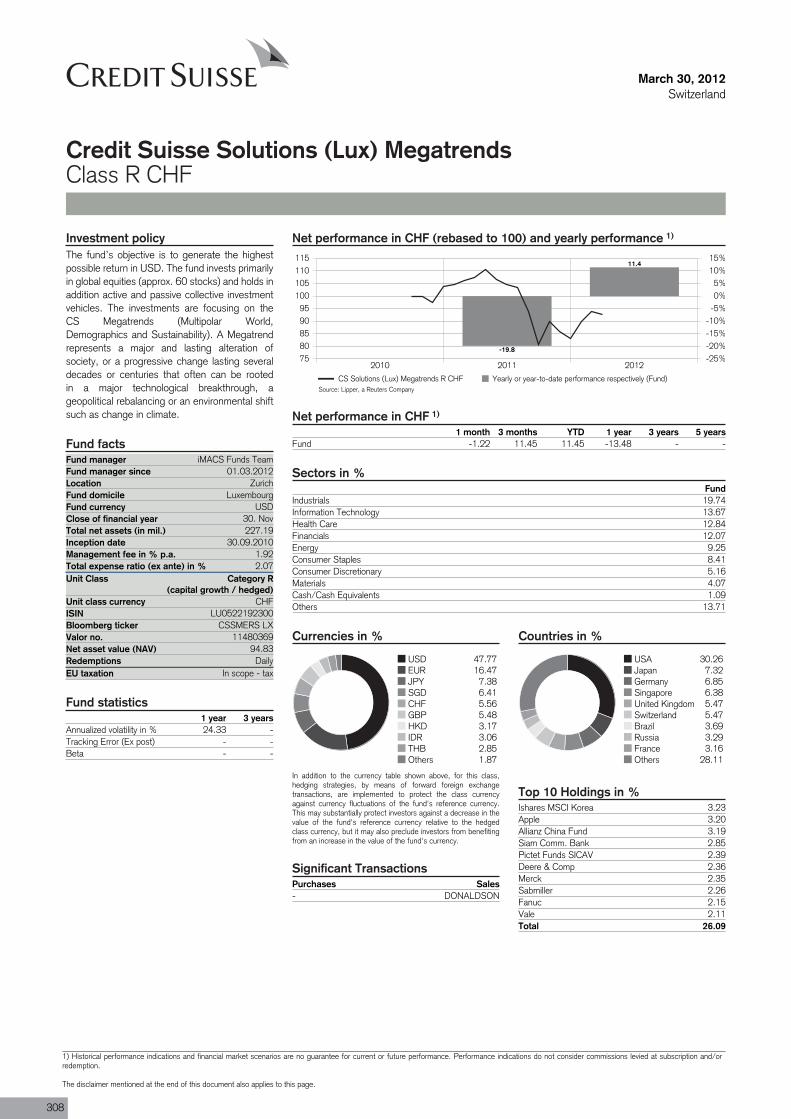

Credit Suisse Solutions (Lux) Megatrends R CHF CHF -13.5 n/a -13.5 n/a n/a 308

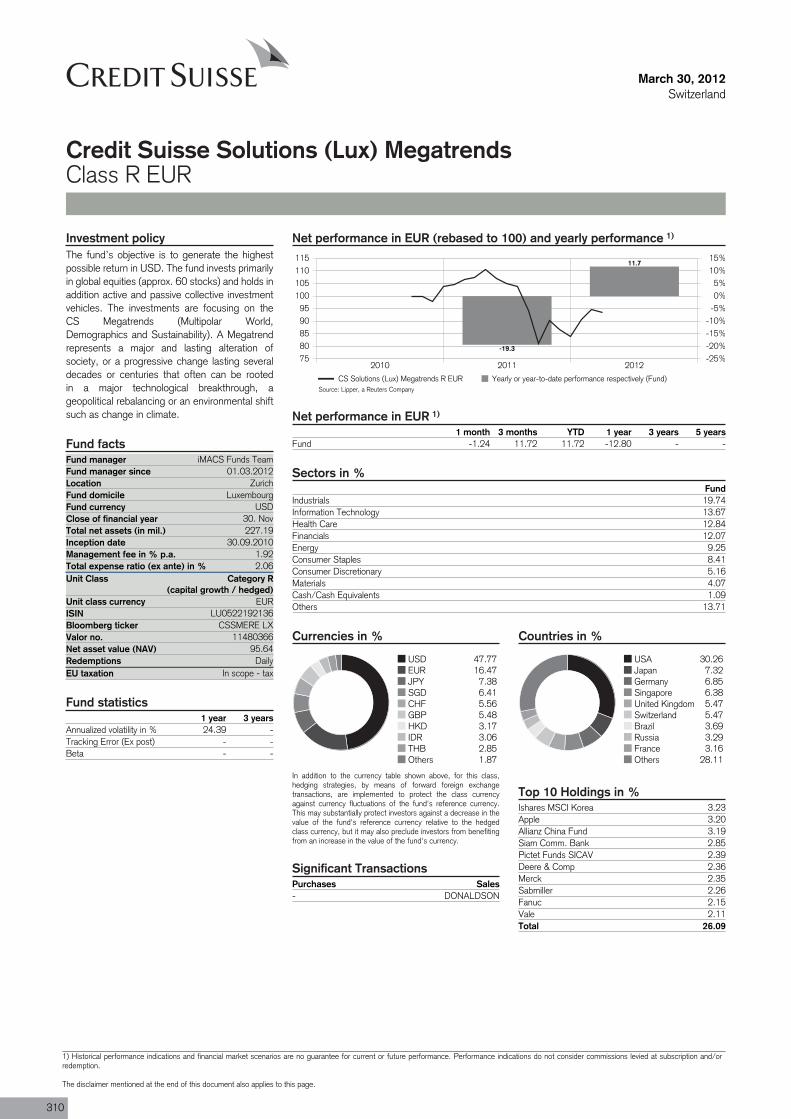

Credit Suisse Solutions (Lux) Megatrends R EUR EUR -12.8 n/a -19.2 n/a n/a 310

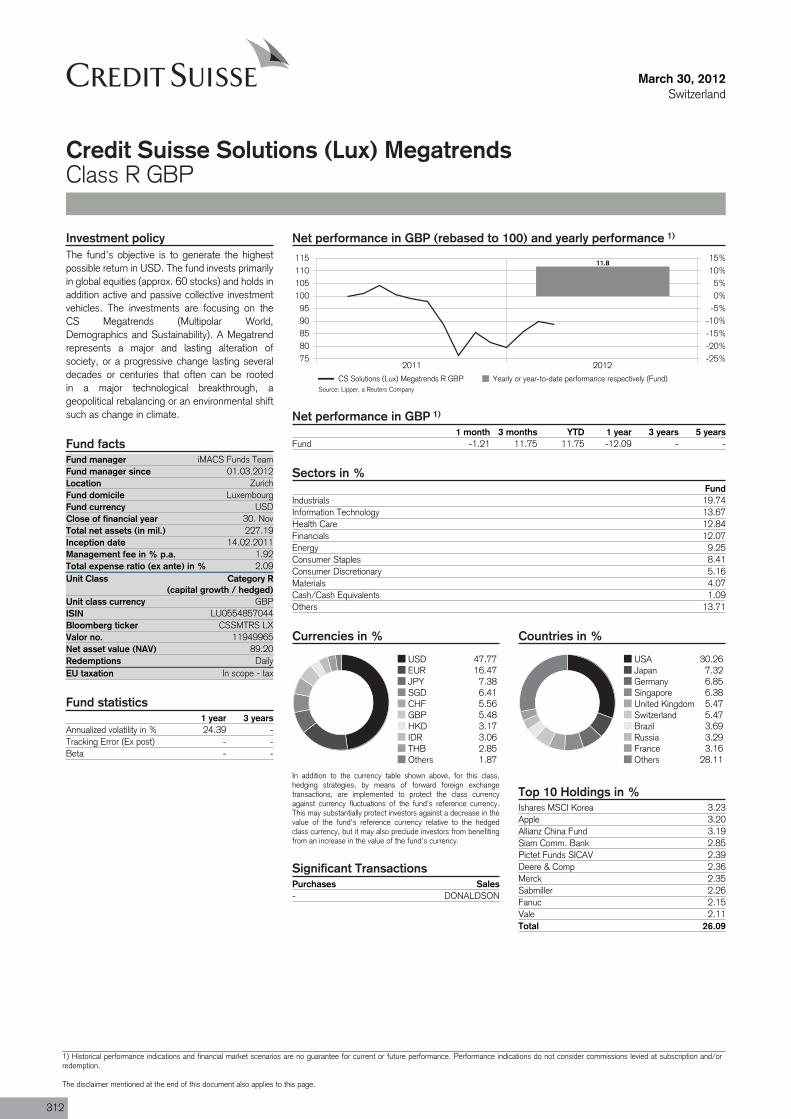

Credit Suisse Solutions (Lux) Megatrends R GBP GBP -12.1 n/a -13.4 n/a n/a 312

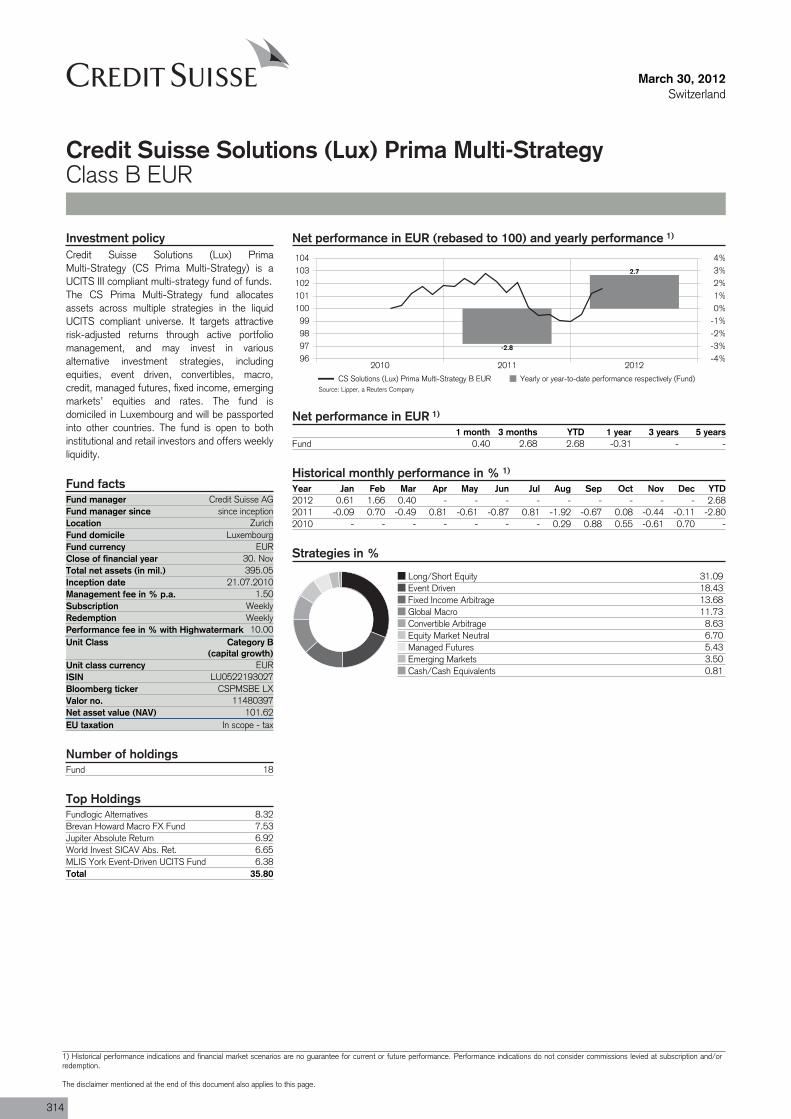

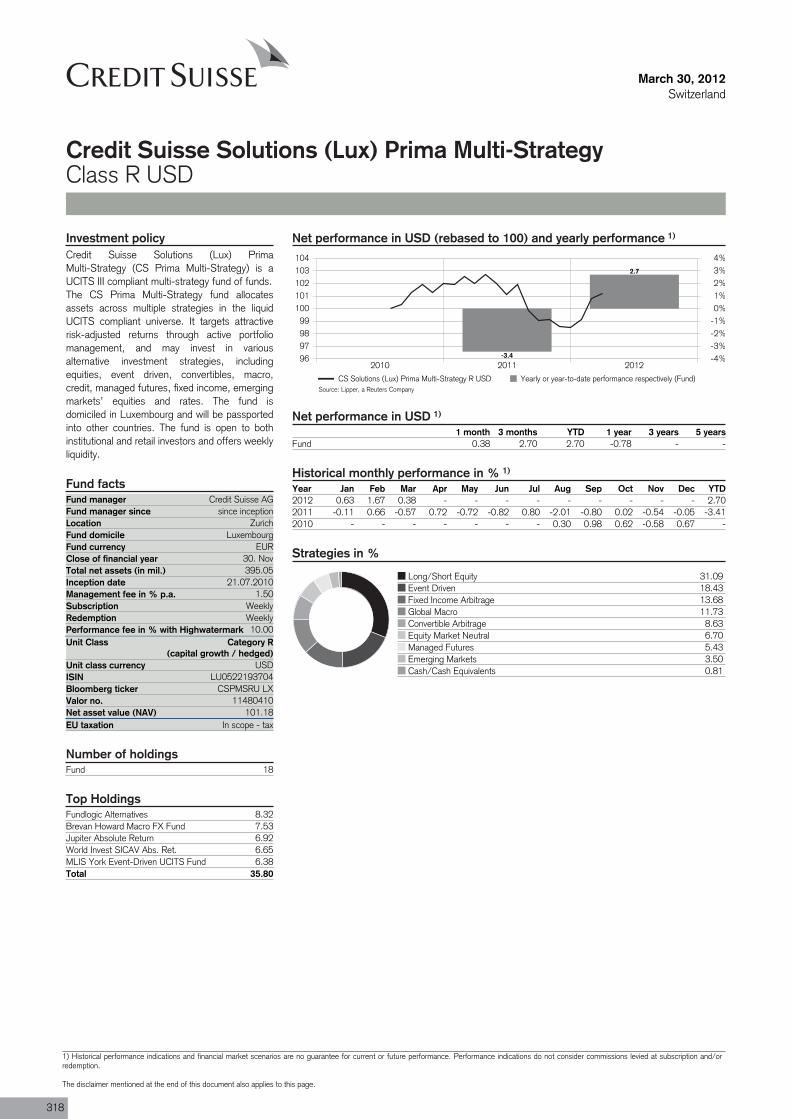

Credit Suisse Solutions (Lux) Prima Multi-Strategy B EUR EUR -0.3 n/a -7.6 n/a n/a 314

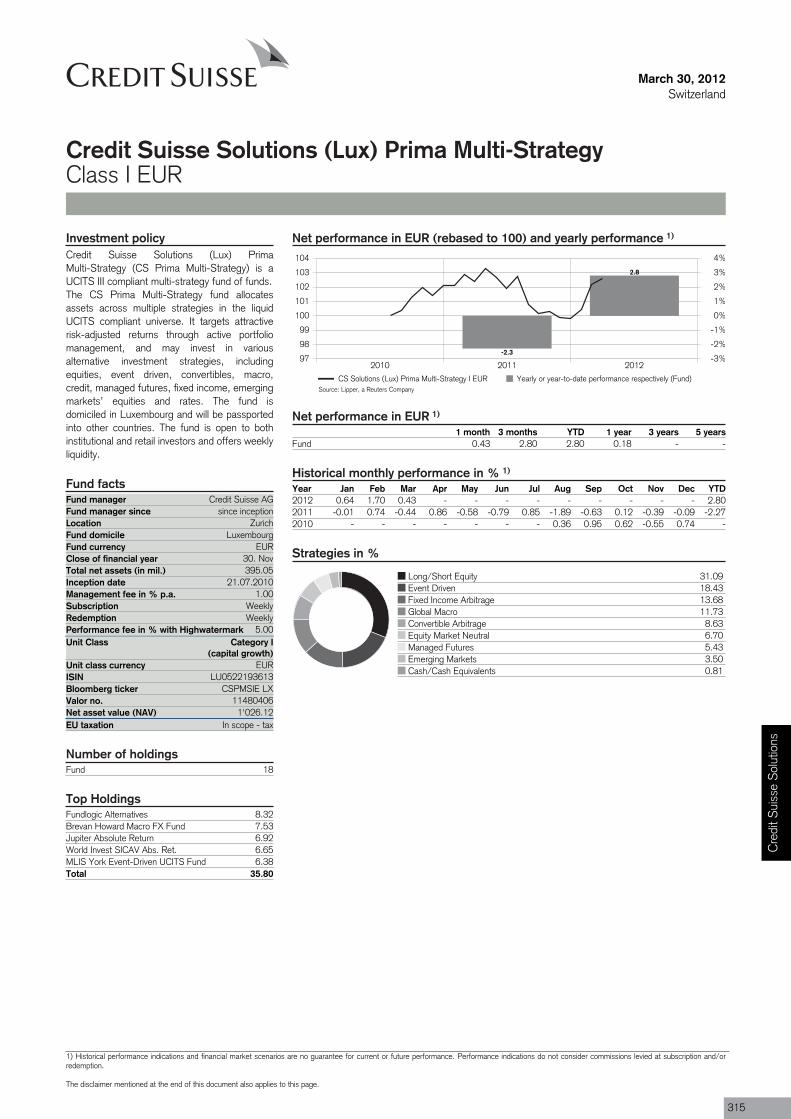

Credit Suisse Solutions (Lux) Prima Multi-Strategy I EUR EUR 0.2 n/a -7.1 n/a n/a 315

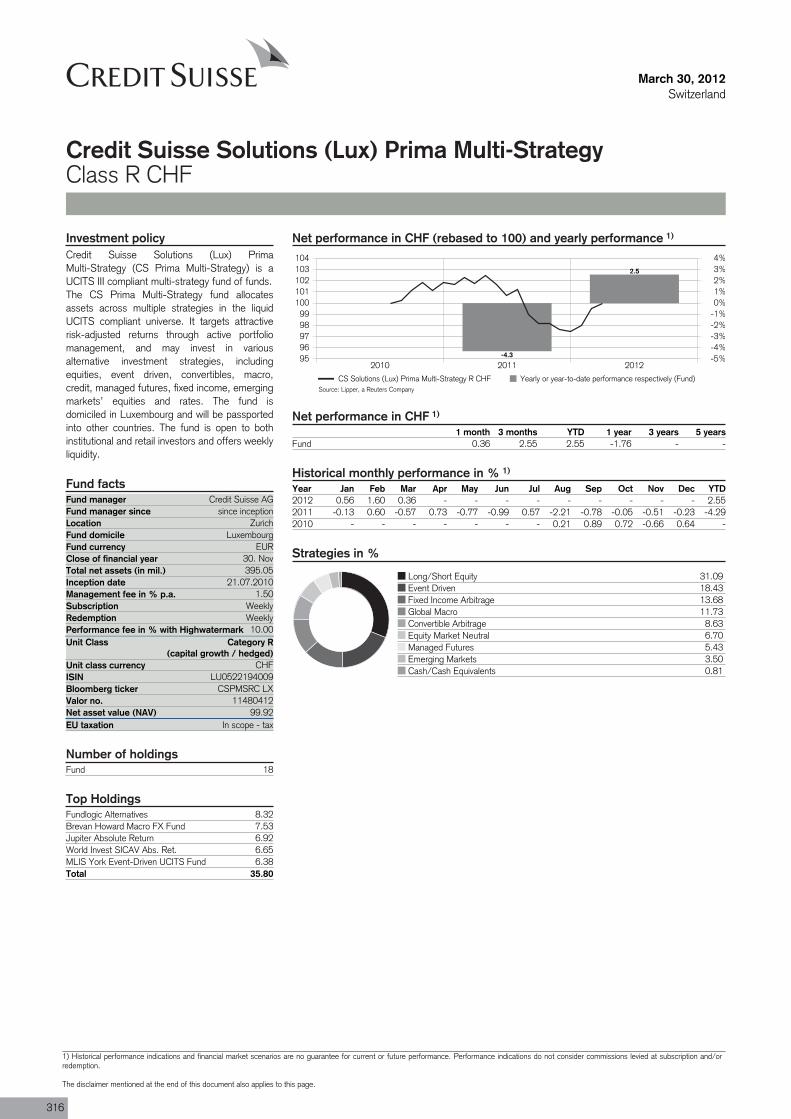

Credit Suisse Solutions (Lux) Prima Multi-Strategy R CHF CHF -1.8 n/a -1.8 n/a n/a 316

Credit Suisse Solutions (Lux) Prima Multi-Strategy R GBP GBP n/a n/a n/a n/a n/a 317

Credit Suisse Solutions (Lux) Prima Multi-Strategy R USD USD -0.8 n/a -2.0 n/a n/a 318

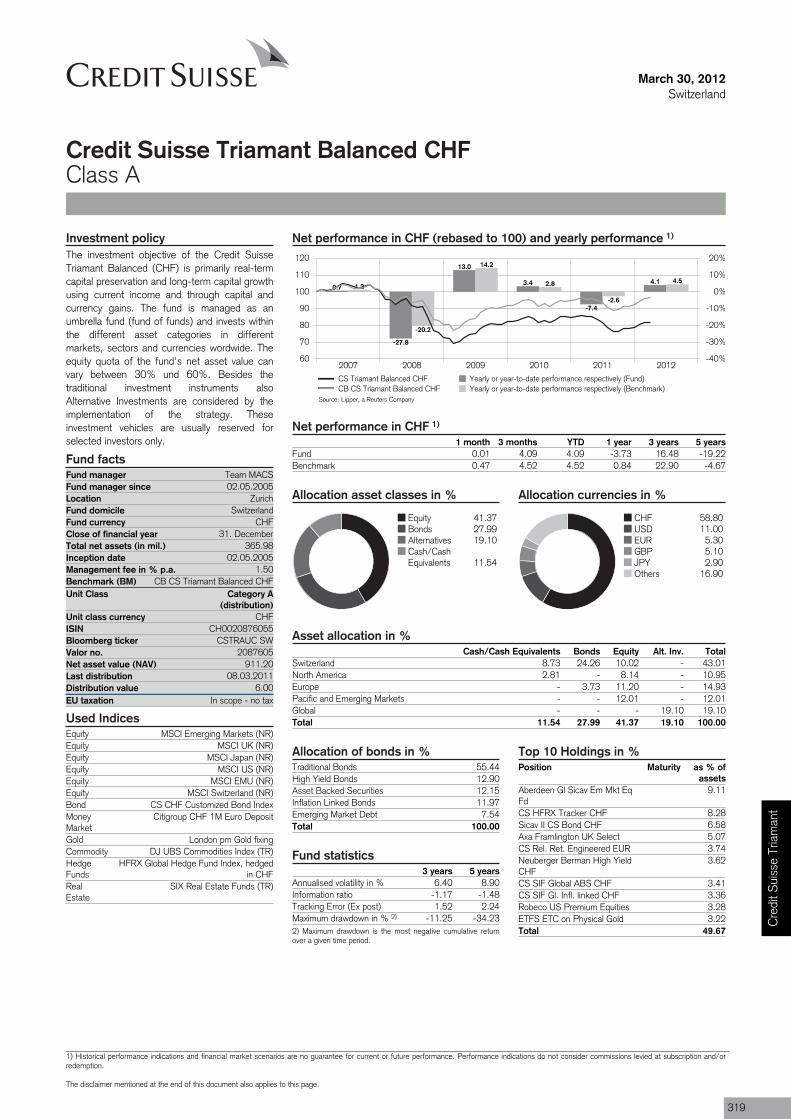

Credit Suisse TriamantCredit Suisse Triamant Balanced CHF CHF -3.7 16.5 -3.7 16.5 6.4 319

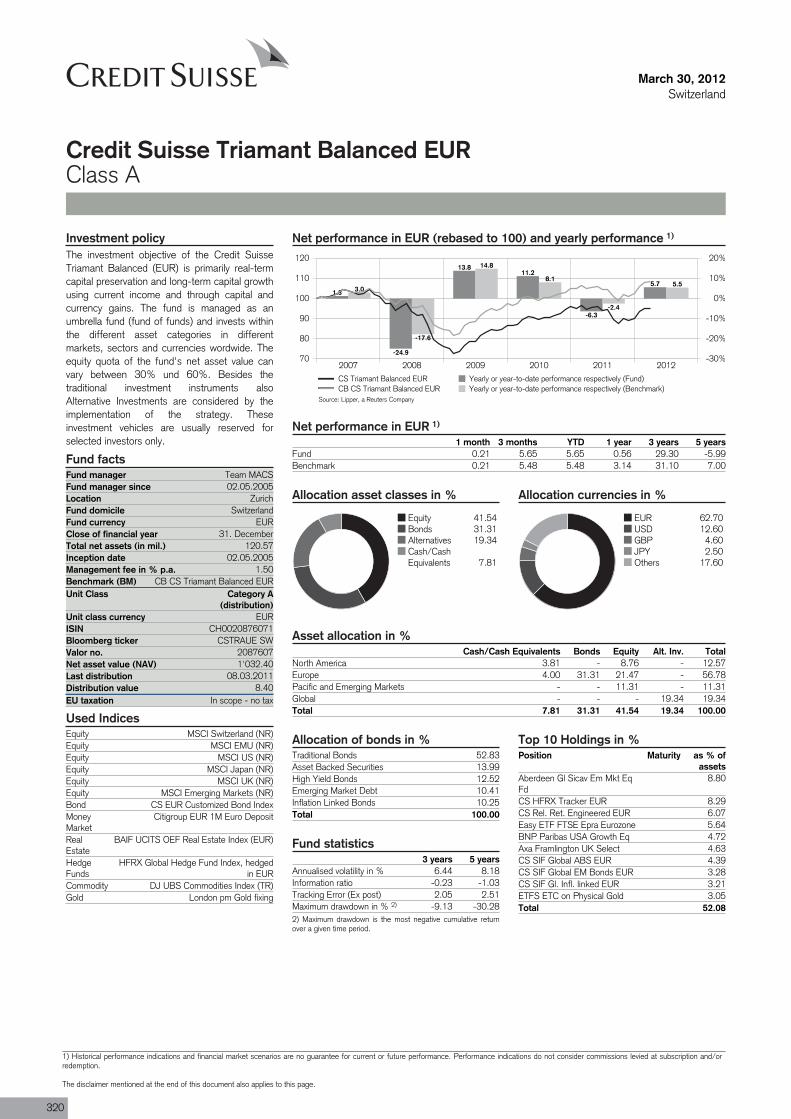

Credit Suisse Triamant Balanced EUR EUR 0.6 29.3 -6.8 3.1 6.4 320

Ove

rvie

w

11

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

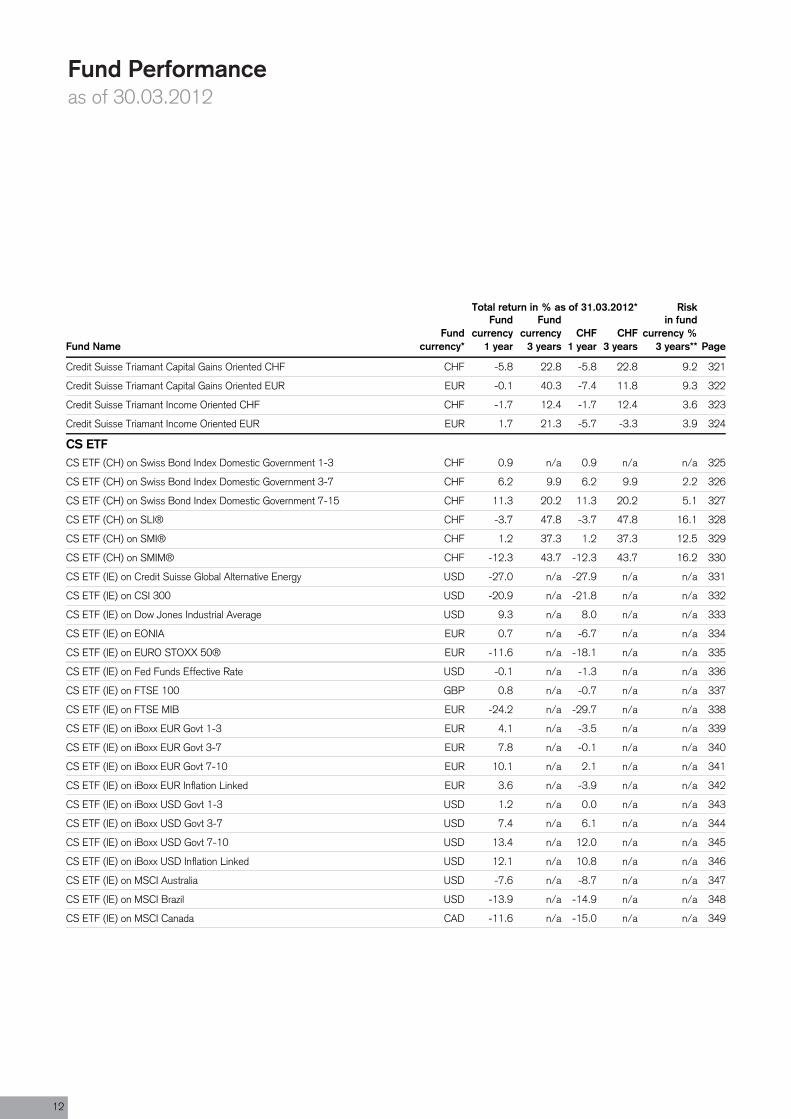

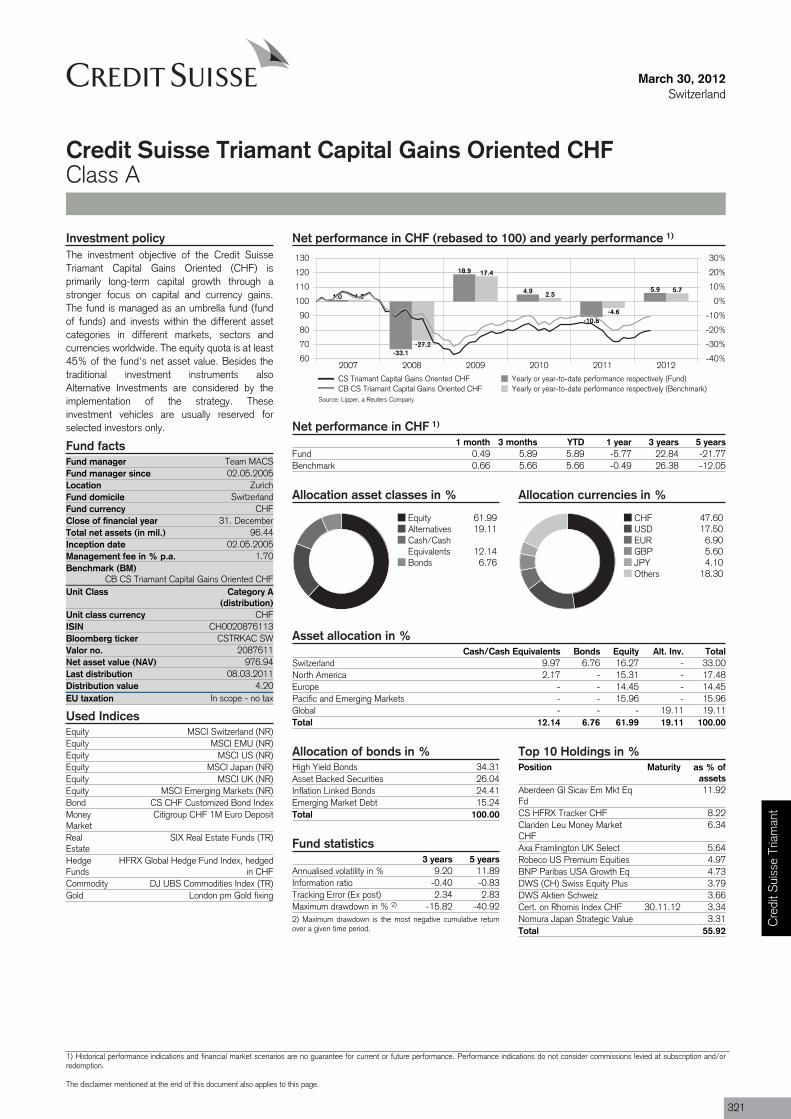

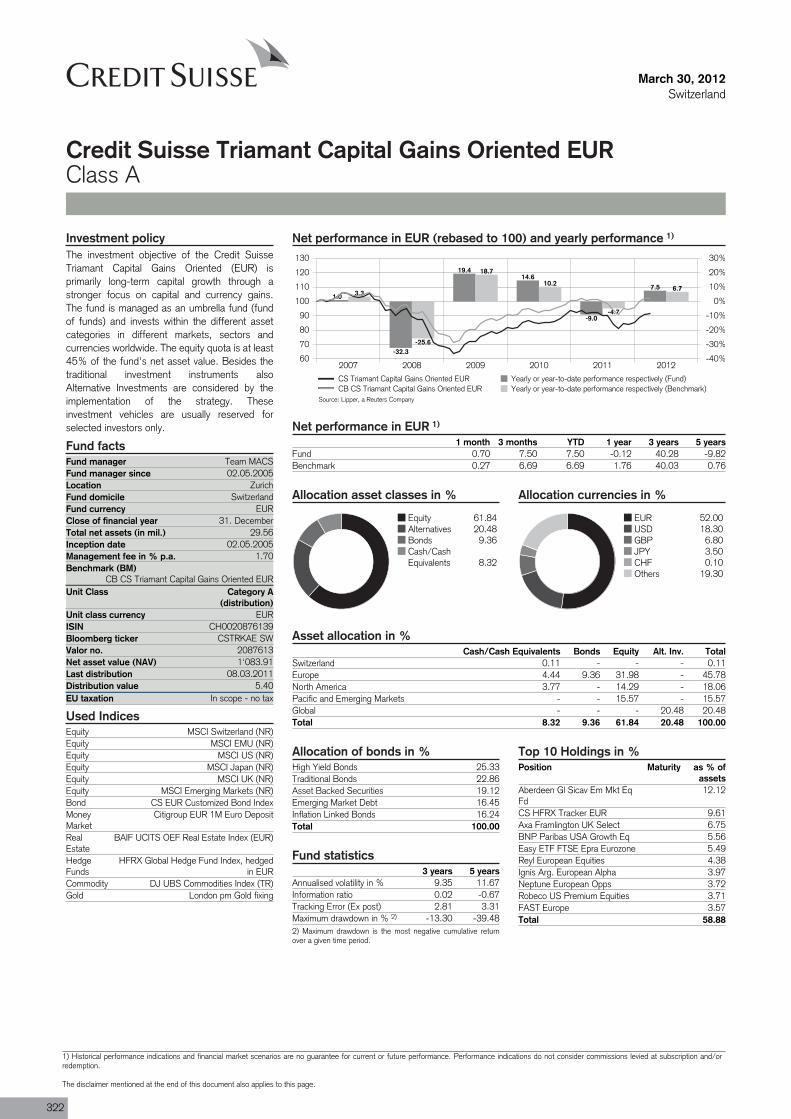

Credit Suisse Triamant Capital Gains Oriented CHF CHF -5.8 22.8 -5.8 22.8 9.2 321

Credit Suisse Triamant Capital Gains Oriented EUR EUR -0.1 40.3 -7.4 11.8 9.3 322

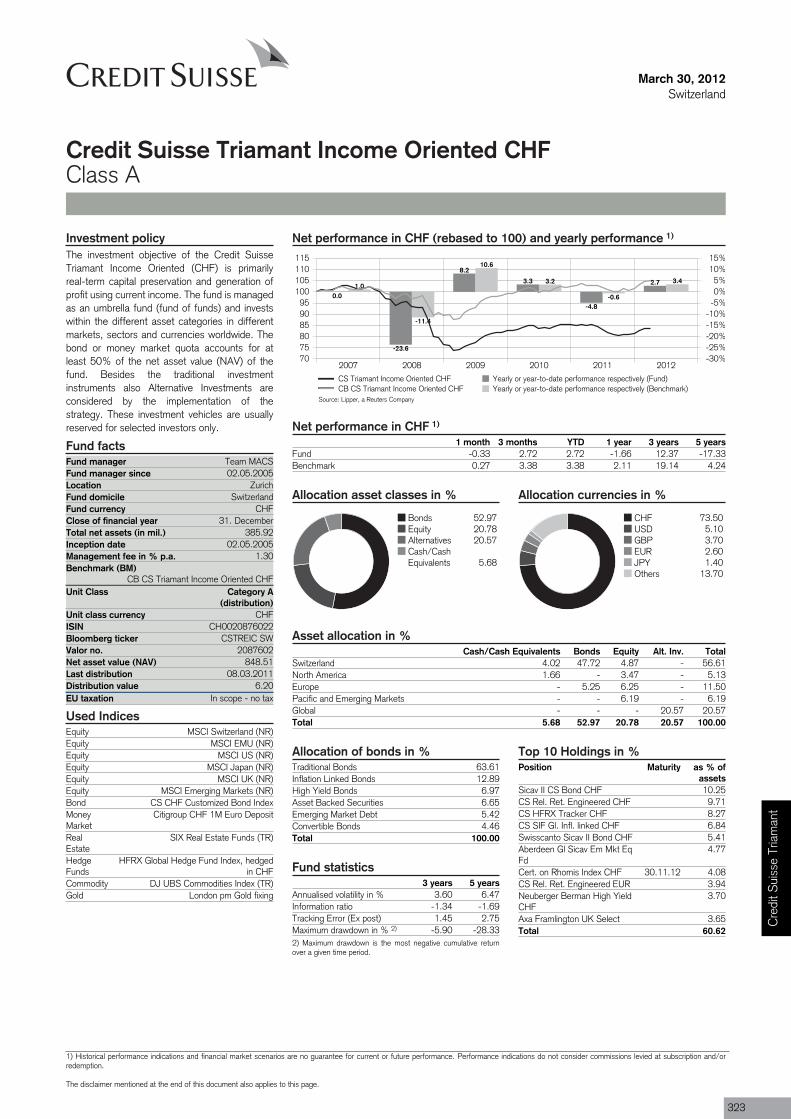

Credit Suisse Triamant Income Oriented CHF CHF -1.7 12.4 -1.7 12.4 3.6 323

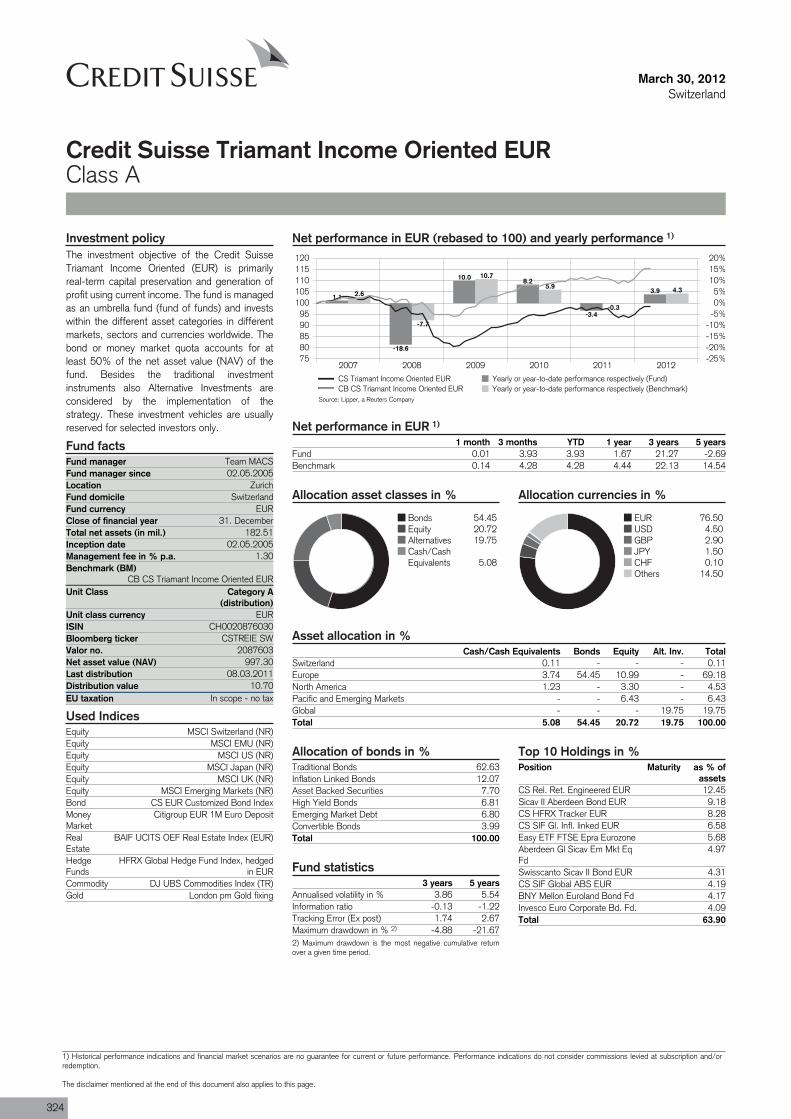

Credit Suisse Triamant Income Oriented EUR EUR 1.7 21.3 -5.7 -3.3 3.9 324

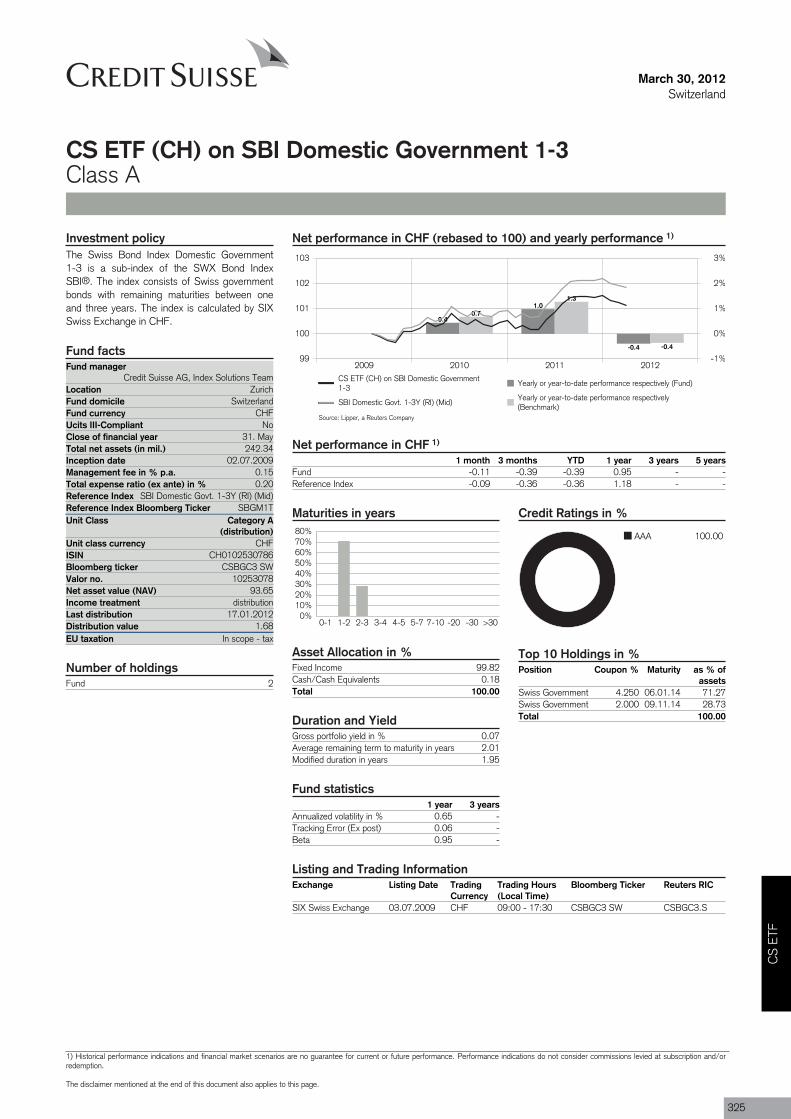

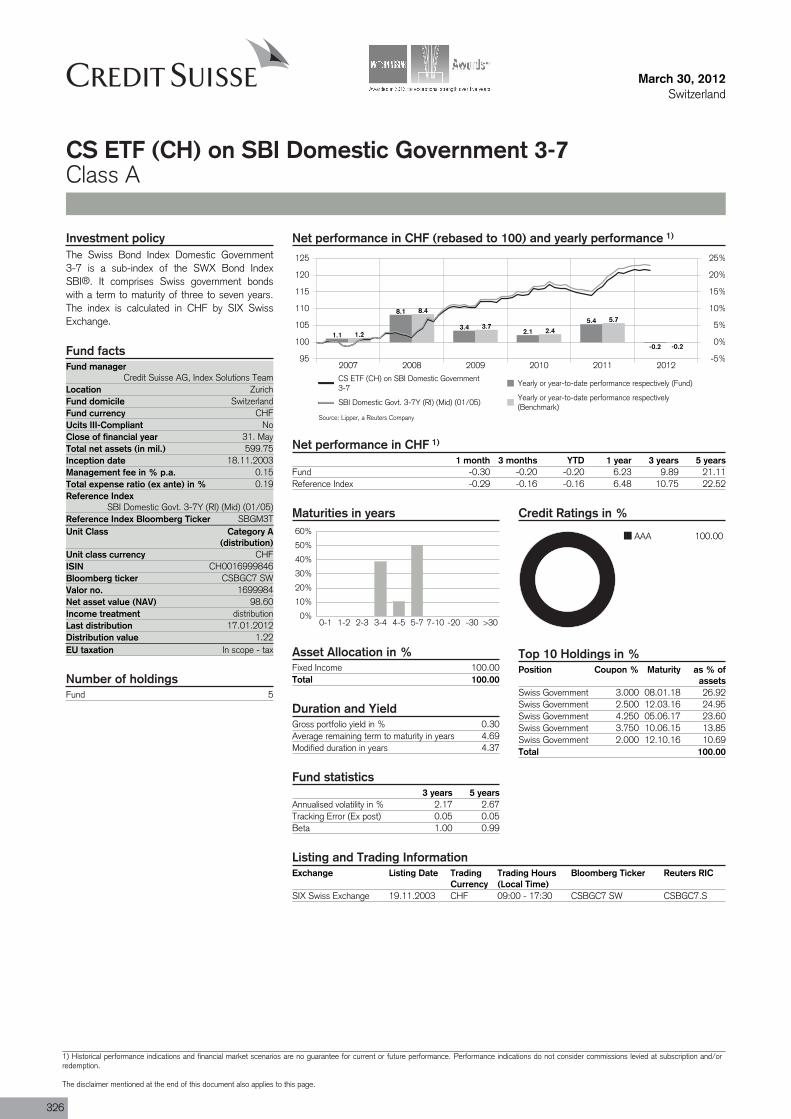

CS ETFCS ETF (CH) on Swiss Bond Index Domestic Government 1-3 CHF 0.9 n/a 0.9 n/a n/a 325

CS ETF (CH) on Swiss Bond Index Domestic Government 3-7 CHF 6.2 9.9 6.2 9.9 2.2 326

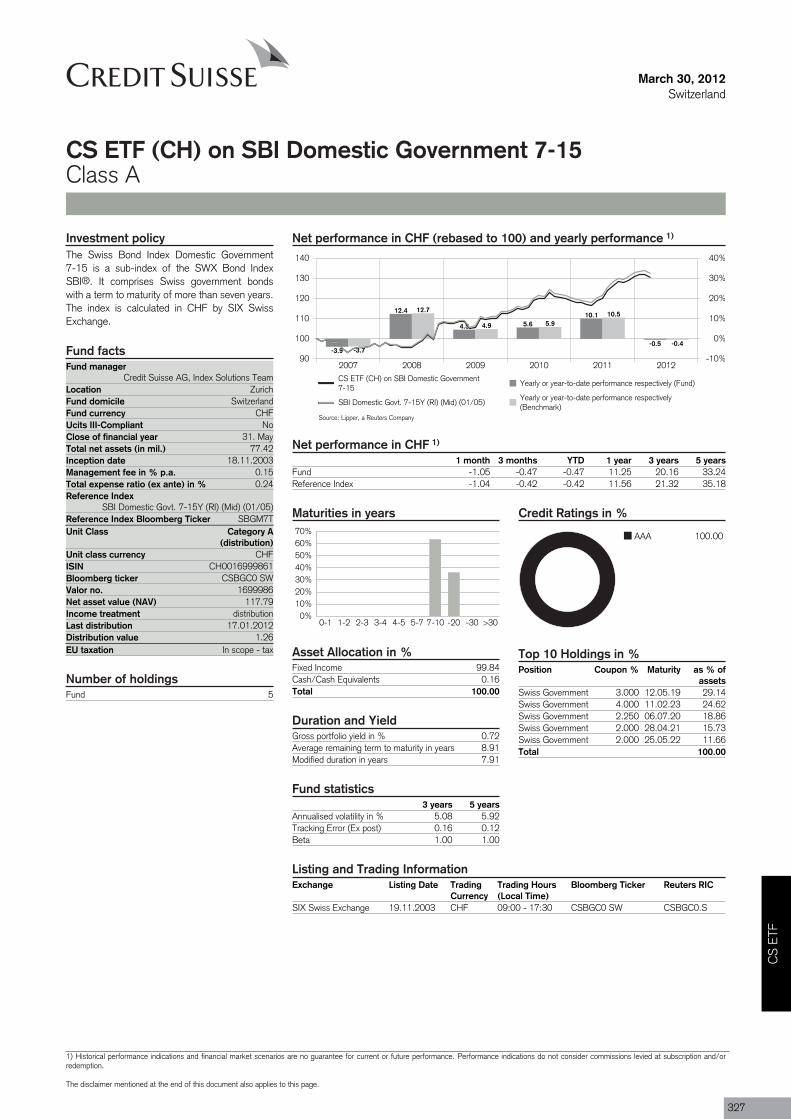

CS ETF (CH) on Swiss Bond Index Domestic Government 7-15 CHF 11.3 20.2 11.3 20.2 5.1 327

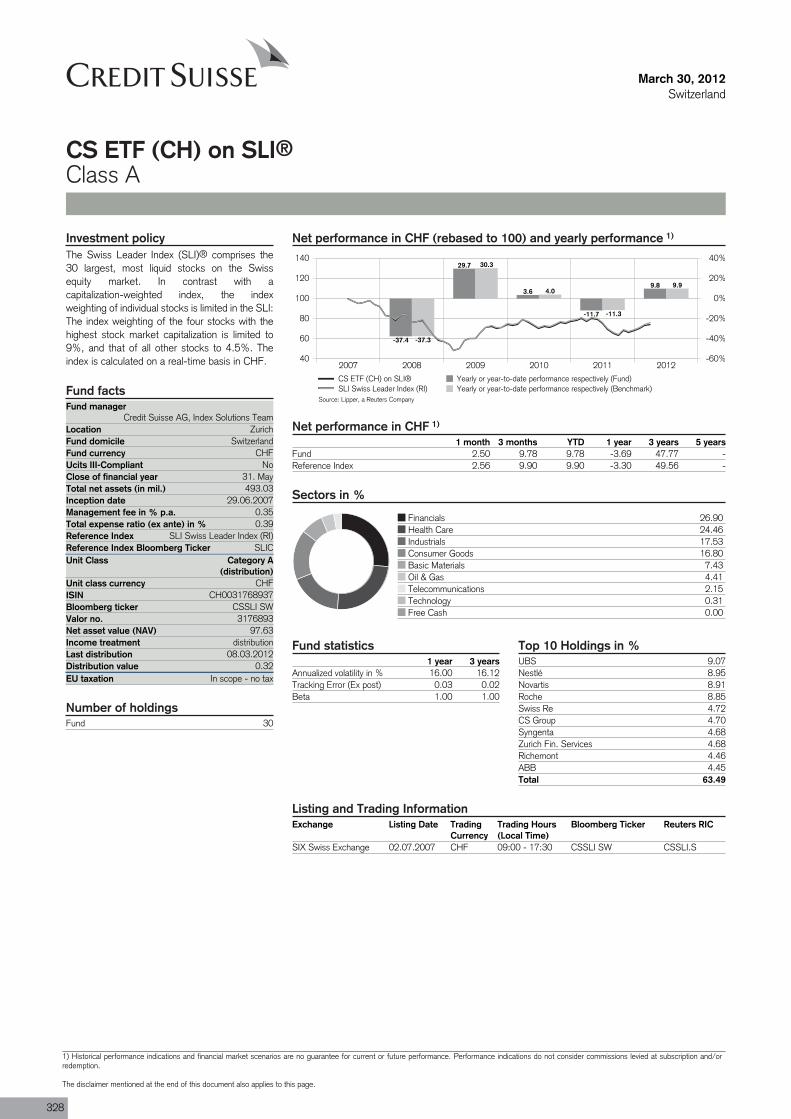

CS ETF (CH) on SLI® CHF -3.7 47.8 -3.7 47.8 16.1 328

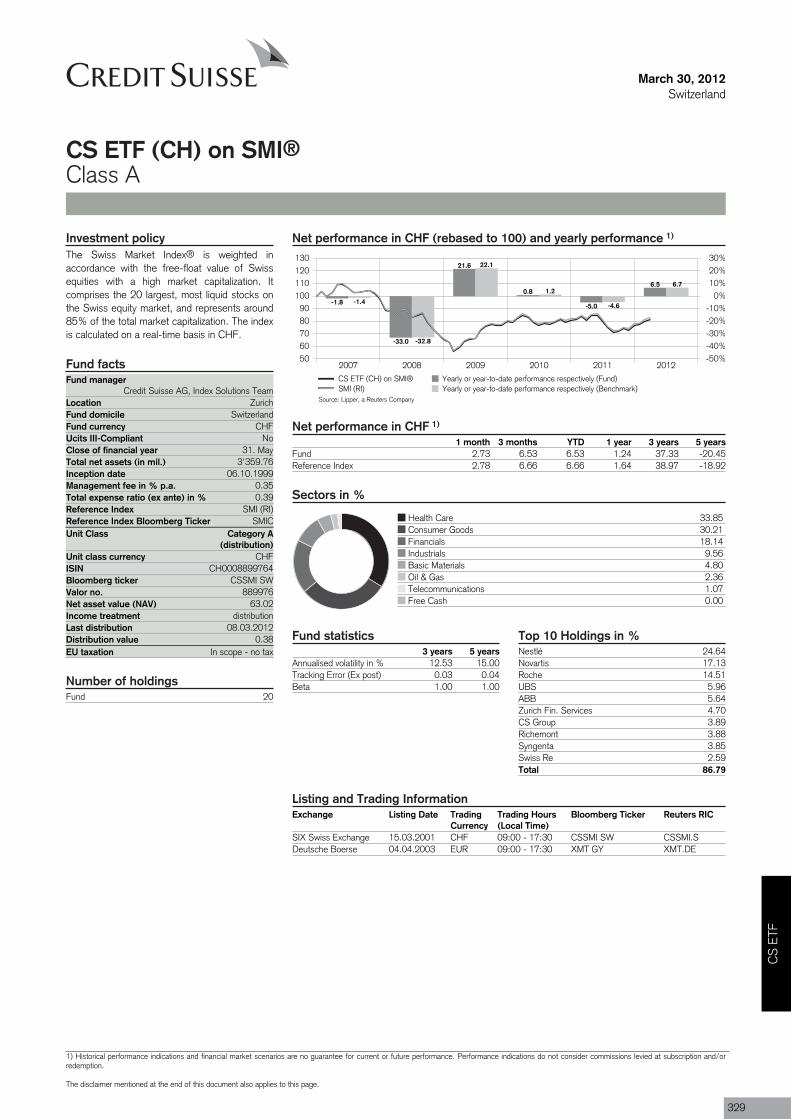

CS ETF (CH) on SMI® CHF 1.2 37.3 1.2 37.3 12.5 329

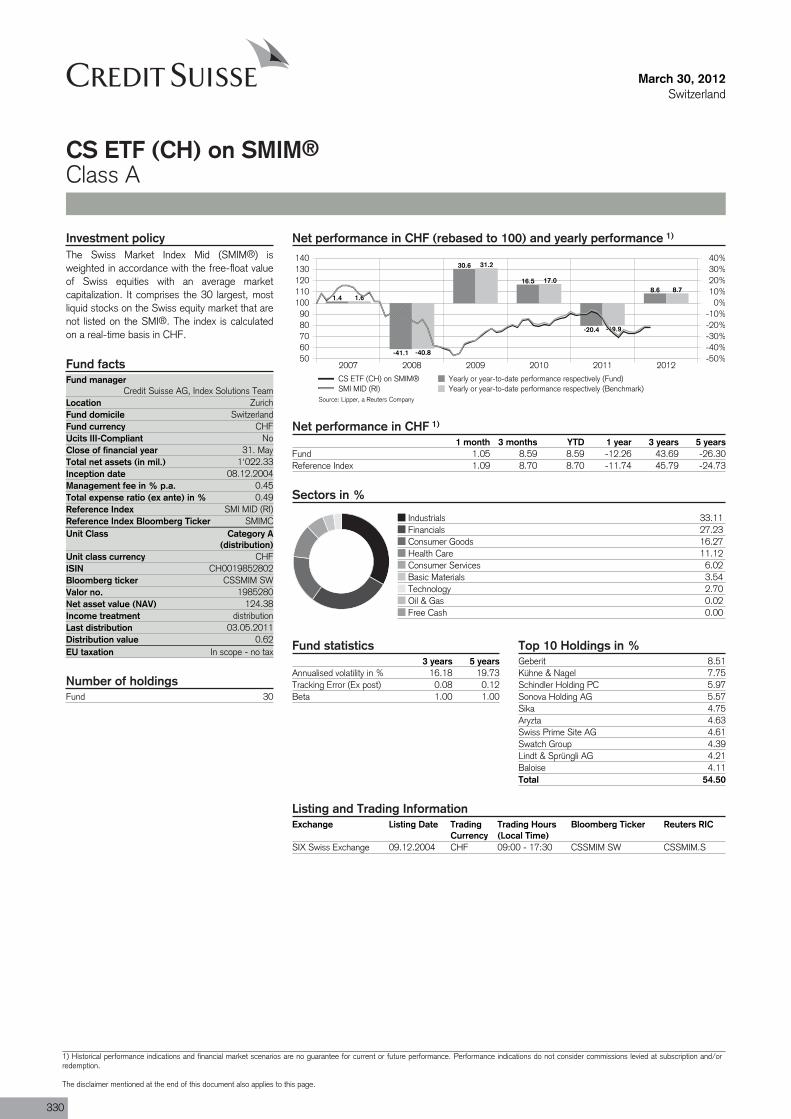

CS ETF (CH) on SMIM® CHF -12.3 43.7 -12.3 43.7 16.2 330

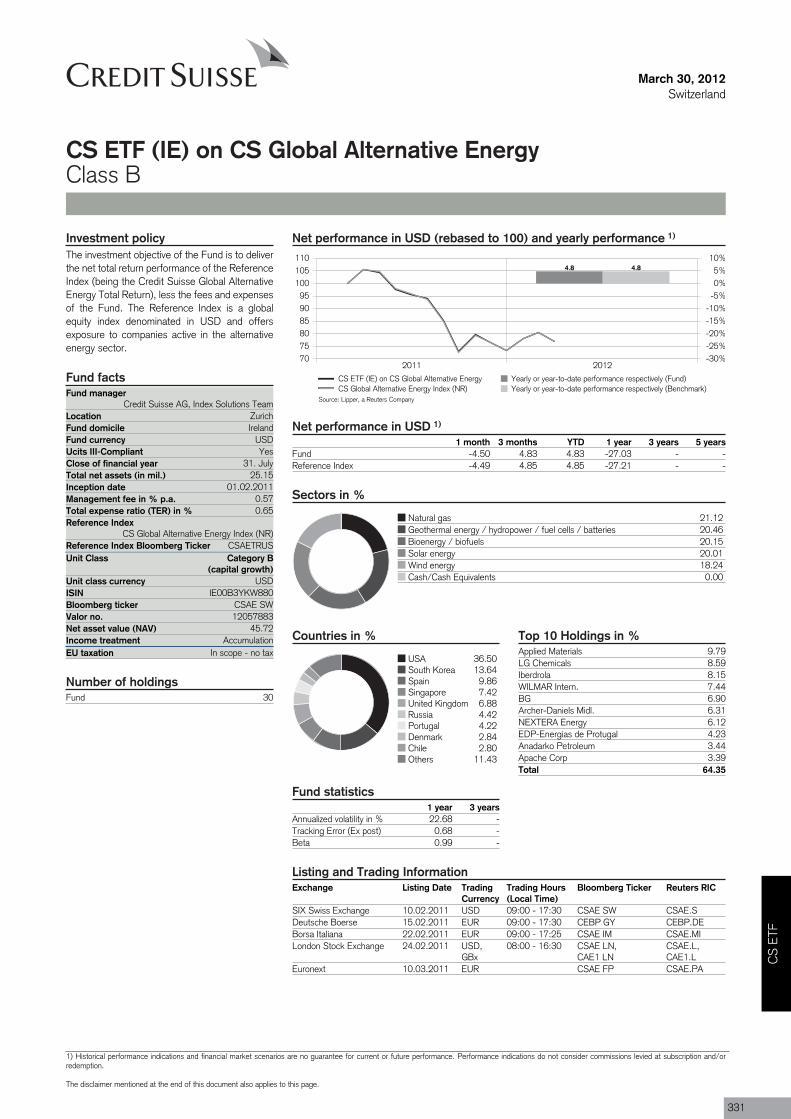

CS ETF (IE) on Credit Suisse Global Alternative Energy USD -27.0 n/a -27.9 n/a n/a 331

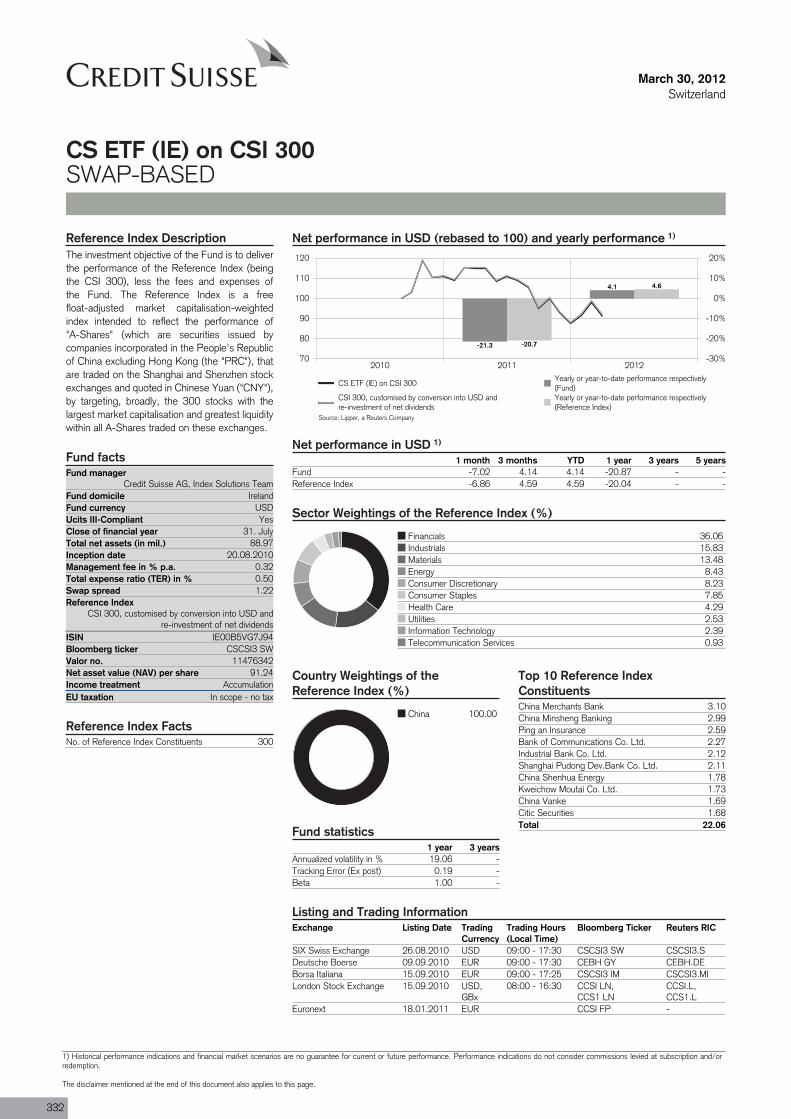

CS ETF (IE) on CSI 300 USD -20.9 n/a -21.8 n/a n/a 332

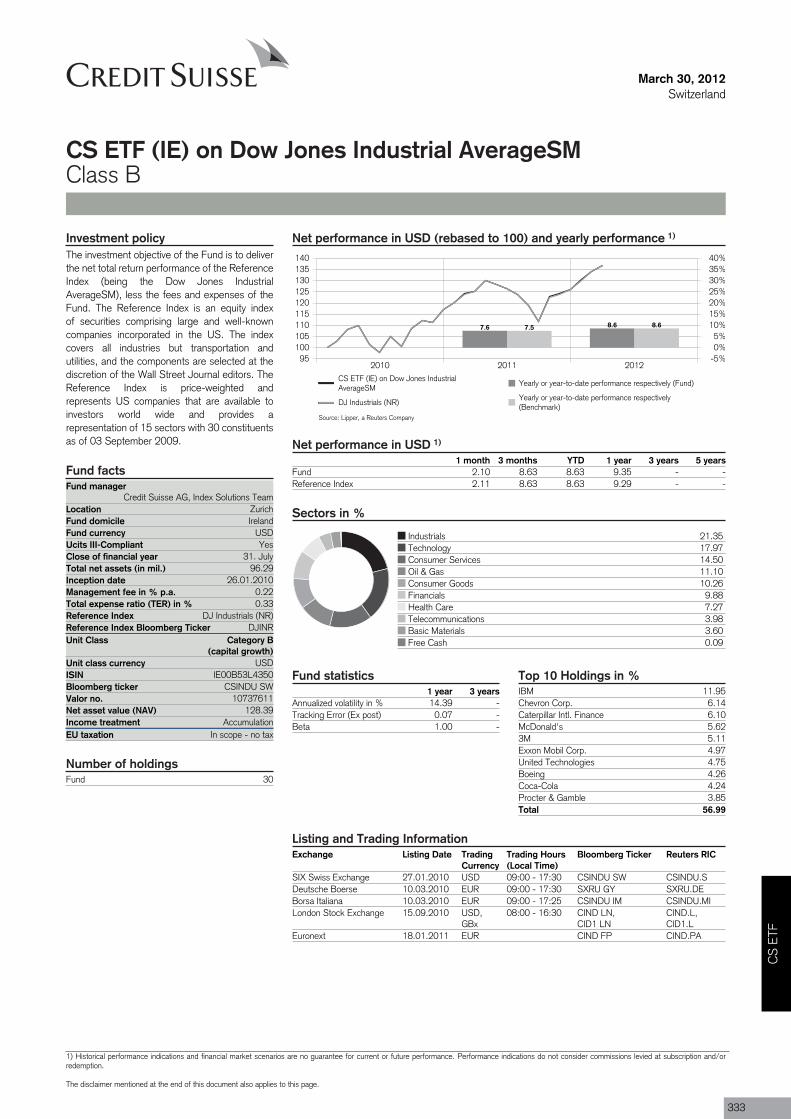

CS ETF (IE) on Dow Jones Industrial Average USD 9.3 n/a 8.0 n/a n/a 333

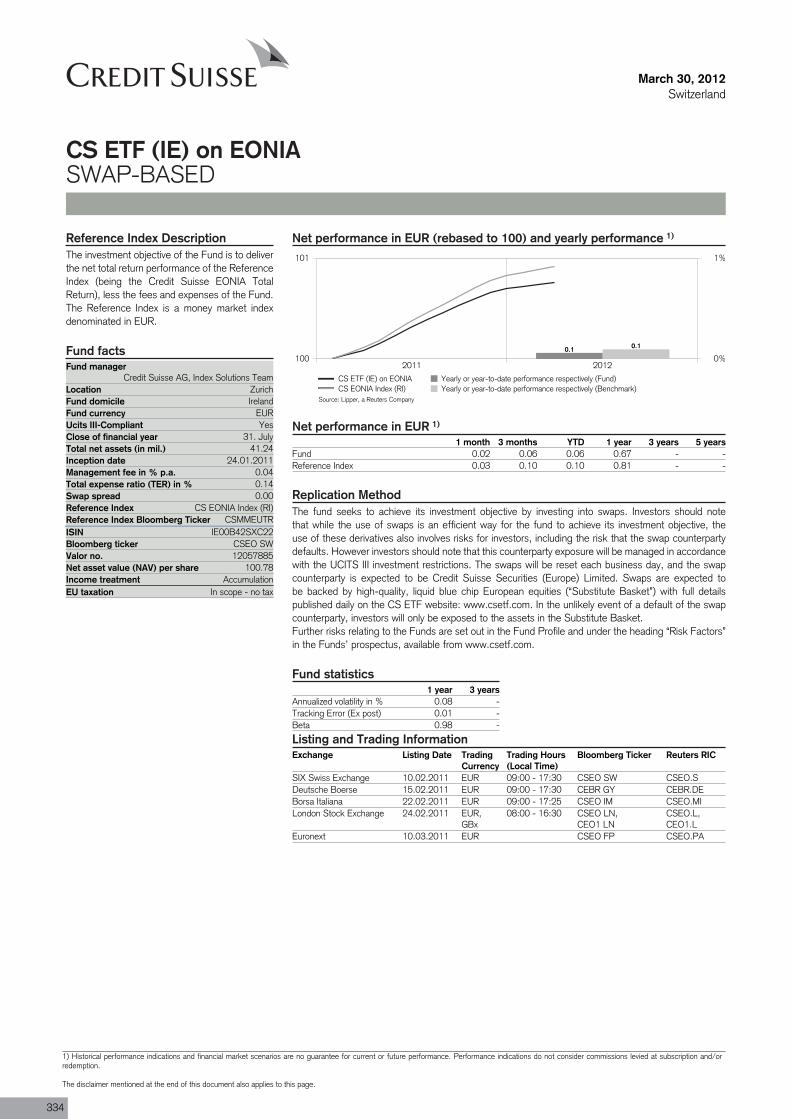

CS ETF (IE) on EONIA EUR 0.7 n/a -6.7 n/a n/a 334

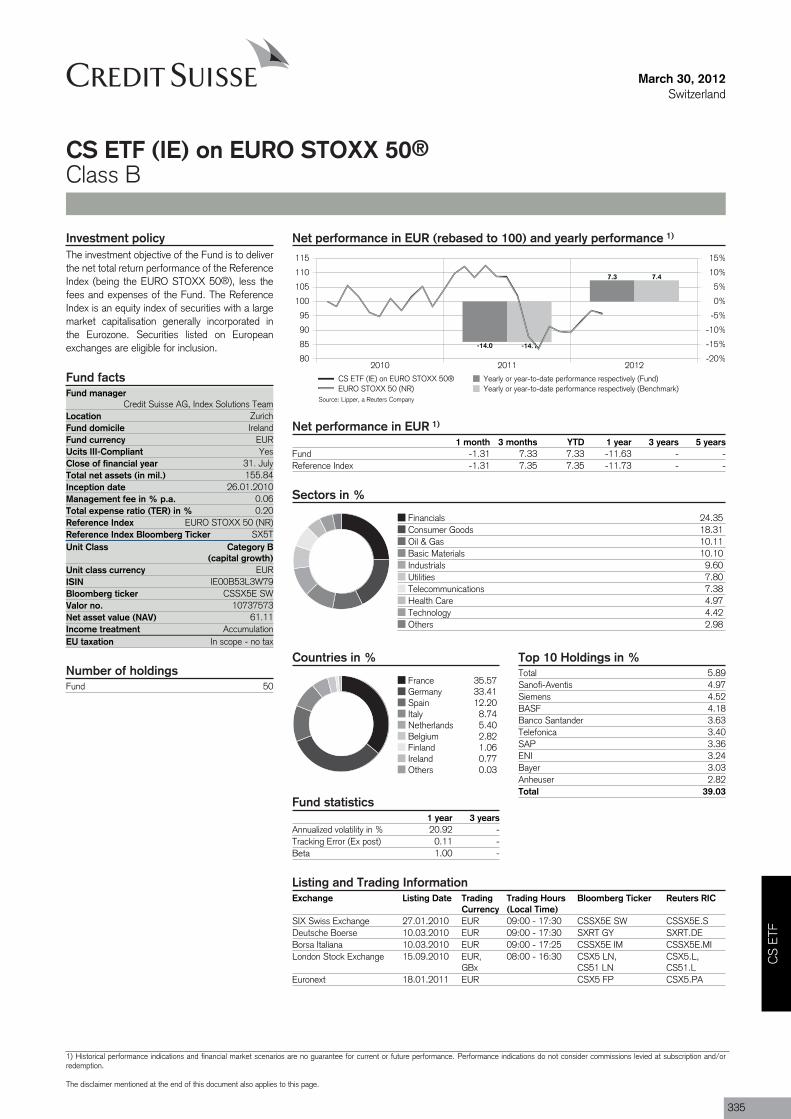

CS ETF (IE) on EURO STOXX 50® EUR -11.6 n/a -18.1 n/a n/a 335

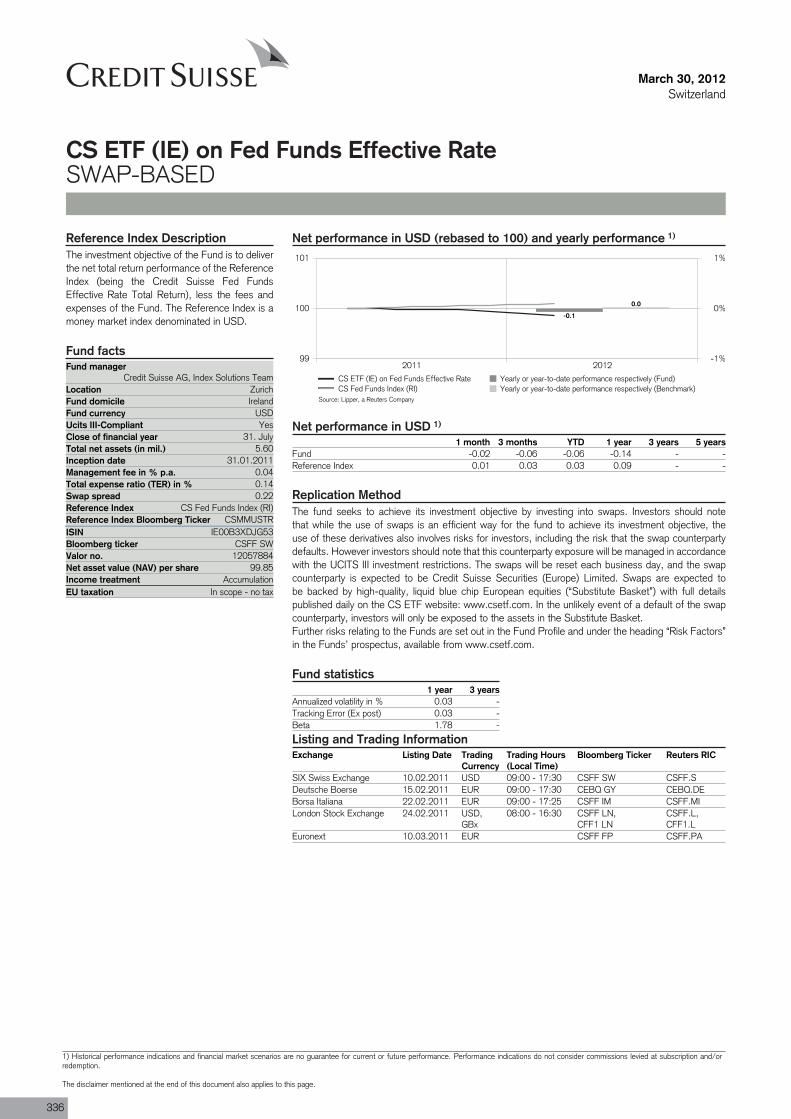

CS ETF (IE) on Fed Funds Effective Rate USD -0.1 n/a -1.3 n/a n/a 336

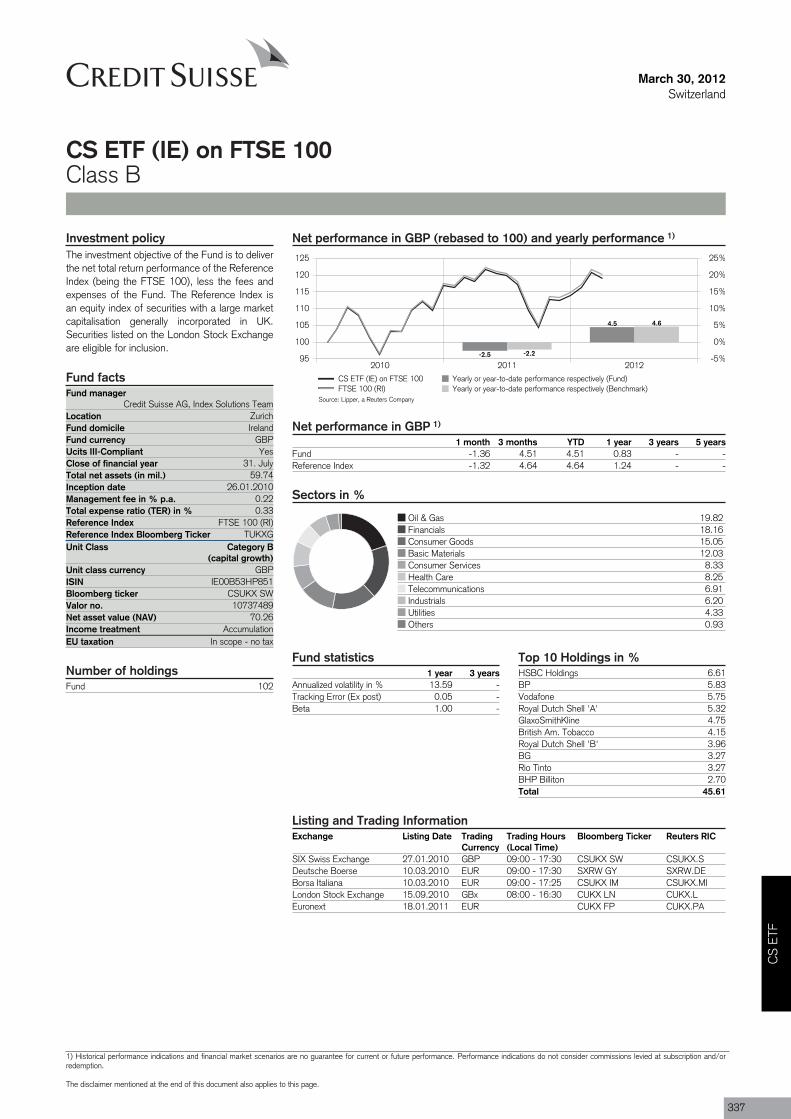

CS ETF (IE) on FTSE 100 GBP 0.8 n/a -0.7 n/a n/a 337

CS ETF (IE) on FTSE MIB EUR -24.2 n/a -29.7 n/a n/a 338

CS ETF (IE) on iBoxx EUR Govt 1-3 EUR 4.1 n/a -3.5 n/a n/a 339

CS ETF (IE) on iBoxx EUR Govt 3-7 EUR 7.8 n/a -0.1 n/a n/a 340

CS ETF (IE) on iBoxx EUR Govt 7-10 EUR 10.1 n/a 2.1 n/a n/a 341

CS ETF (IE) on iBoxx EUR Inflation Linked EUR 3.6 n/a -3.9 n/a n/a 342

CS ETF (IE) on iBoxx USD Govt 1-3 USD 1.2 n/a 0.0 n/a n/a 343

CS ETF (IE) on iBoxx USD Govt 3-7 USD 7.4 n/a 6.1 n/a n/a 344

CS ETF (IE) on iBoxx USD Govt 7-10 USD 13.4 n/a 12.0 n/a n/a 345

CS ETF (IE) on iBoxx USD Inflation Linked USD 12.1 n/a 10.8 n/a n/a 346

CS ETF (IE) on MSCI Australia USD -7.6 n/a -8.7 n/a n/a 347

CS ETF (IE) on MSCI Brazil USD -13.9 n/a -14.9 n/a n/a 348

CS ETF (IE) on MSCI Canada CAD -11.6 n/a -15.0 n/a n/a 349

Fund Performanceas of 30.03.2012

12

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

CS ETF (IE) on MSCI Chile USD 0.7 n/a -0.5 n/a n/a 350

CS ETF (IE) on MSCI EM Asia USD -8.6 n/a -9.7 n/a n/a 351

CS ETF (IE) on MSCI EM EMEA USD -12.9 n/a -14.0 n/a n/a 352

CS ETF (IE) on MSCI EM Latin America USD -9.2 n/a -10.3 n/a n/a 353

CS ETF (IE) on MSCI EMU EUR -10.1 n/a -16.6 n/a n/a 354

CS ETF (IE) on MSCI EMU Small Cap EUR -13.9 n/a -20.1 n/a n/a 355

CS ETF (IE) on MSCI Europe EUR -1.7 n/a -8.9 n/a n/a 356

CS ETF (IE) on MSCI India USD -21.2 n/a -22.2 n/a n/a 357

CS ETF (IE) on MSCI Japan JPY -0.9 n/a -1.4 n/a n/a 358

CS ETF (IE) on MSCI Japan Large Cap JPY -1.4 n/a -1.9 n/a n/a 359

CS ETF (IE) on MSCI Japan Small Cap JPY 3.4 n/a 2.9 n/a n/a 360

CS ETF (IE) on MSCI Korea USD -6.3 n/a -7.4 n/a n/a 361

CS ETF (IE) on MSCI Mexico Capped USD 0.6 n/a -0.6 n/a n/a 362

CS ETF (IE) on MSCI Pacific ex Japan USD -6.0 n/a -7.2 n/a n/a 363

CS ETF (IE) on MSCI Russia USD -18.7 n/a -19.7 n/a n/a 364

CS ETF (IE) on MSCI South Africa USD -3.6 n/a -4.7 n/a n/a 365

CS ETF (IE) on MSCI Taiwan USD -6.0 n/a -7.1 n/a n/a 366

CS ETF (IE) on MSCI UK GBP 1.0 n/a -0.5 n/a n/a 367

CS ETF (IE) on MSCI UK Large Cap GBP 0.3 n/a -1.2 n/a n/a 368

CS ETF (IE) on MSCI UK Small Cap GBP 3.3 n/a 1.7 n/a n/a 369

CS ETF (IE) on MSCI USA USD 7.9 n/a 6.6 n/a n/a 370

CS ETF (IE) on MSCI USA Large Cap USD 8.8 n/a 7.4 n/a n/a 371

CS ETF (IE) on MSCI USA Small Cap USD 1.1 n/a -0.1 n/a n/a 372

CS ETF (IE) on MSCI World USD 0.1 n/a -1.1 n/a n/a 373

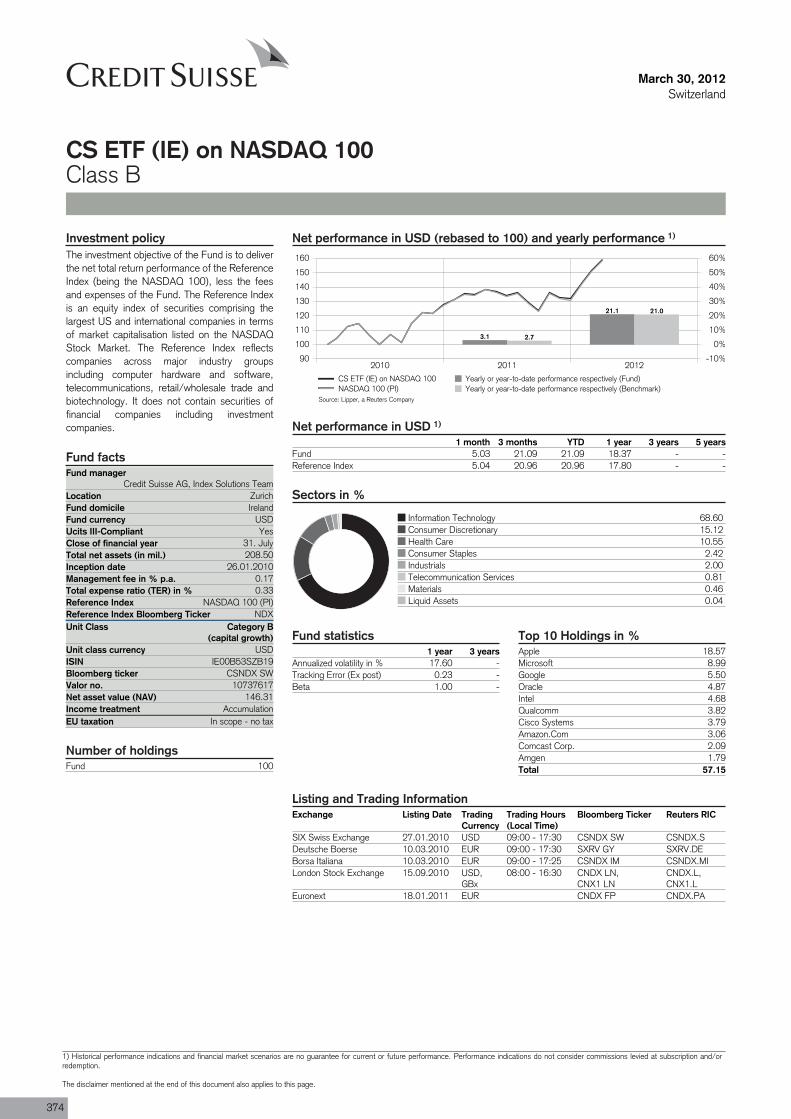

CS ETF (IE) on NASDAQ 100 USD 18.4 n/a 16.9 n/a n/a 374

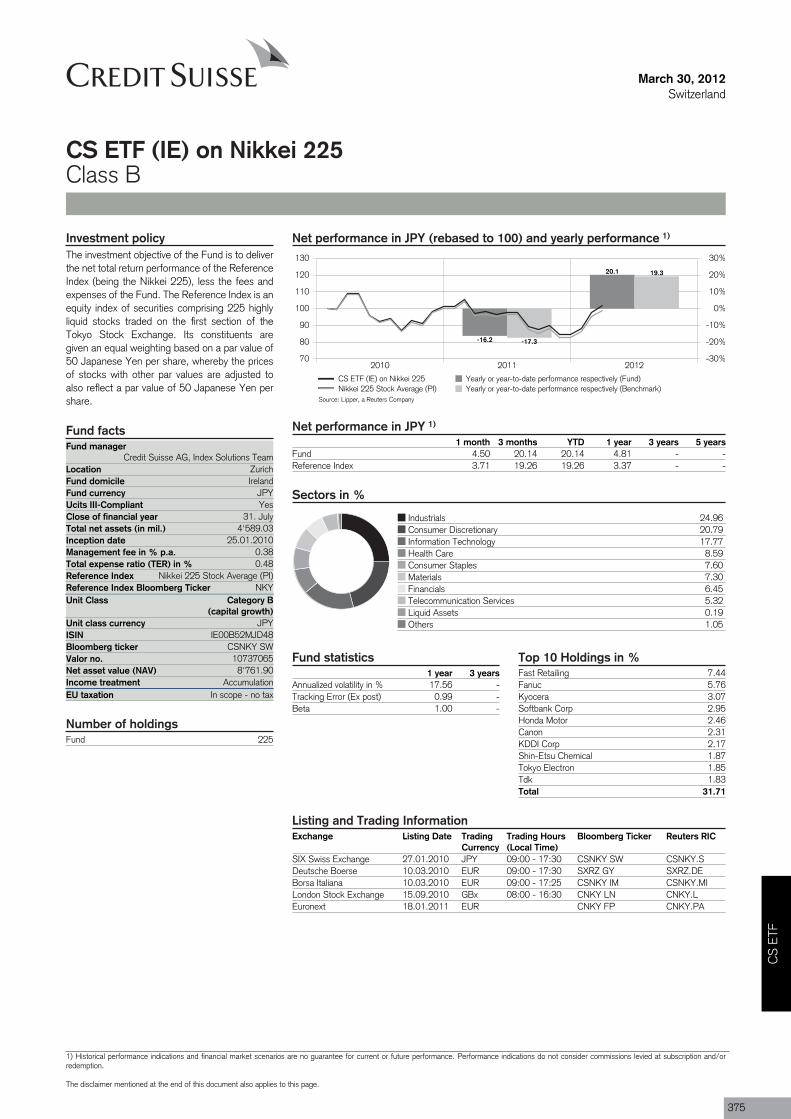

CS ETF (IE) on Nikkei 225 JPY 4.8 n/a 4.3 n/a n/a 375

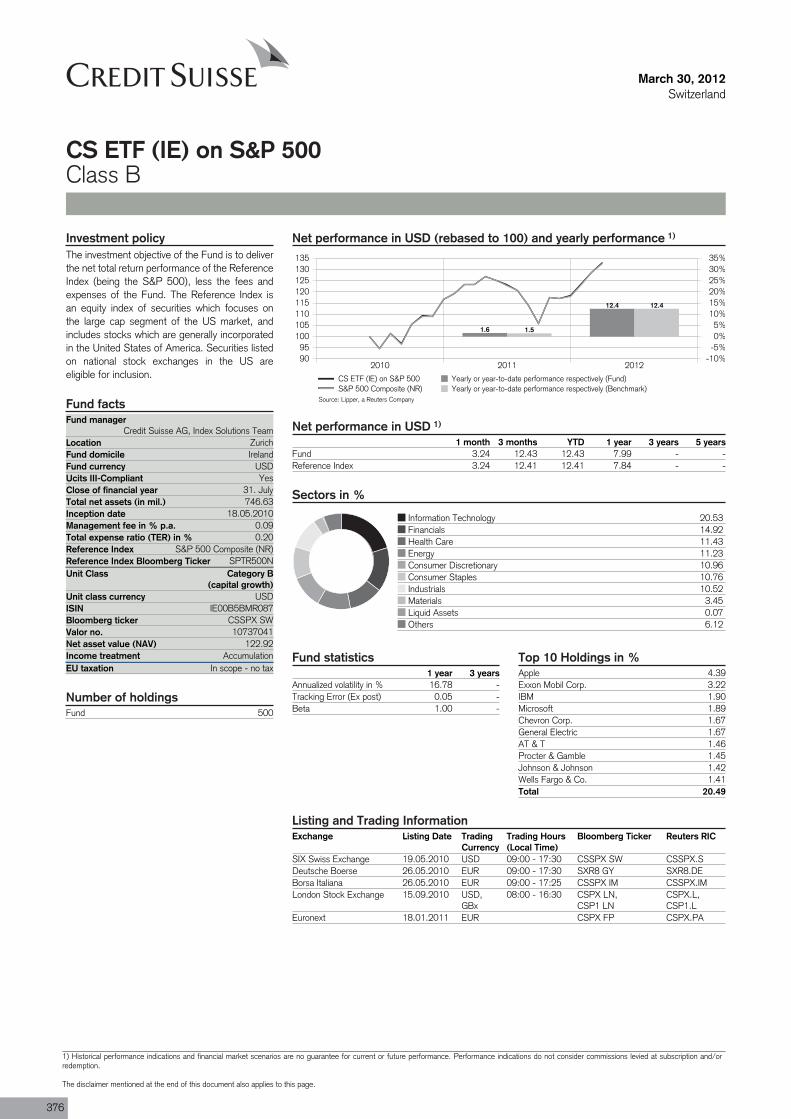

CS ETF (IE) on S&P 500 USD 8.0 n/a 6.7 n/a n/a 376

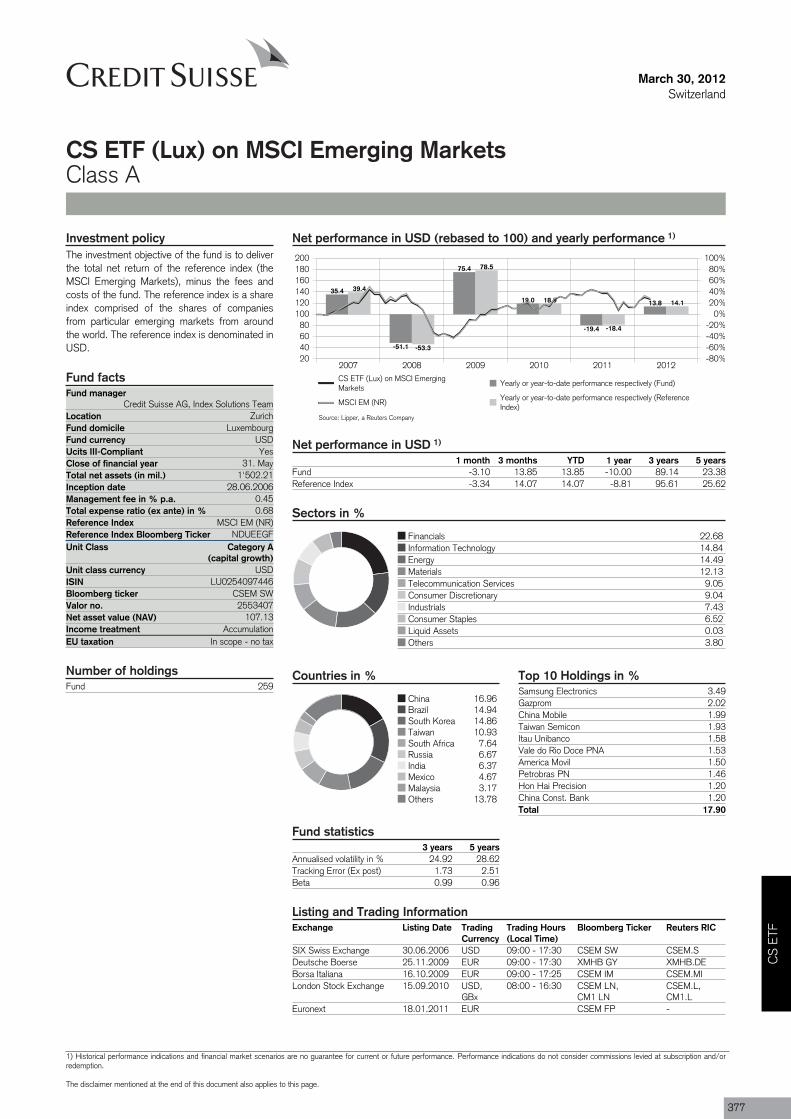

CS ETF (Lux) on MSCI Emerging Markets USD -10.0 89.1 -11.1 50.4 24.9 377

CS ETF (Lux) on MSCI EMU Large Cap EUR -9.3 39.8 -15.9 11.4 19.5 378

CS ETF (Lux) on MSCI EMU Mid Cap EUR -13.3 45.1 -19.6 15.7 20.5 379

Ove

rvie

w

13

Total return in % as of 31.03.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

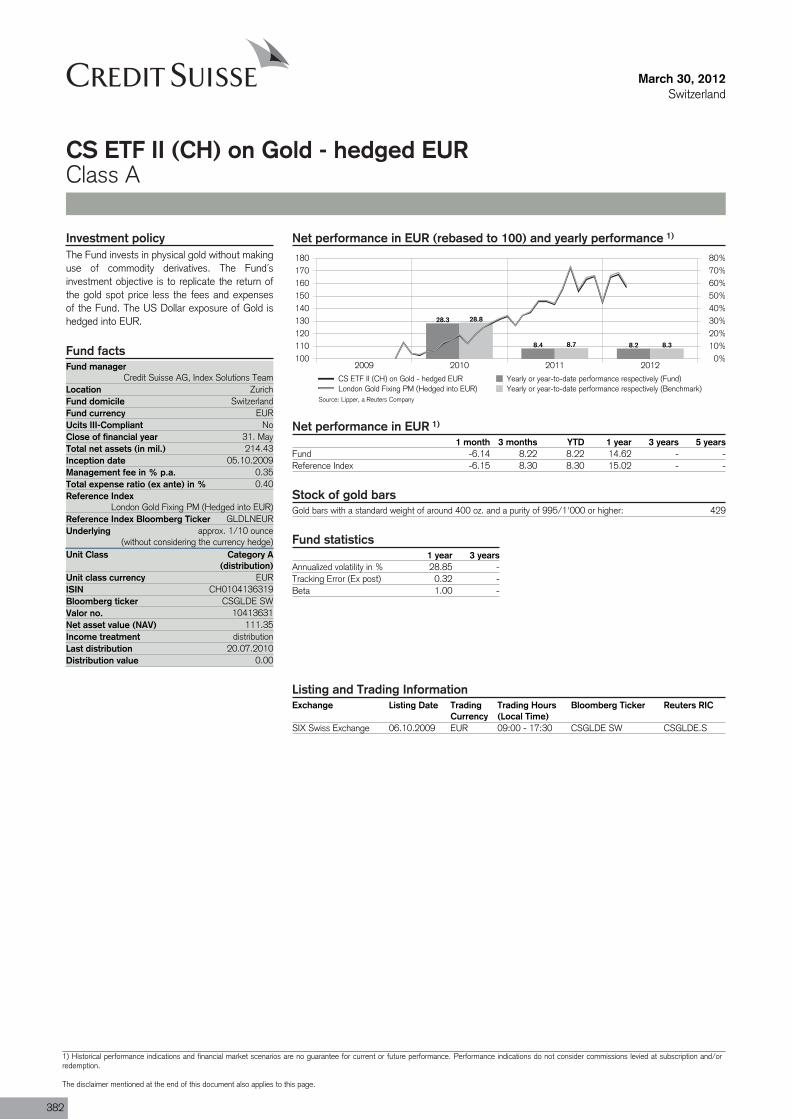

CS ETF II (CH) on Gold USD 15.2 n/a 13.8 n/a n/a 380

CS ETF II (CH) on Gold - hedged CHF CHF 12.3 n/a 12.3 n/a n/a 381

CS ETF II (CH) on Gold - hedged EUR EUR 14.6 n/a 6.3 n/a n/a 382

Fund Performanceas of 30.03.2012

14

Total return in % as of 29.02.2012* Risk

Fund NameFund

currency*

Fundcurrency

1 year

Fundcurrency

3 yearsCHF

1 yearCHF

3 years

in fundcurrency %

3 years** Page

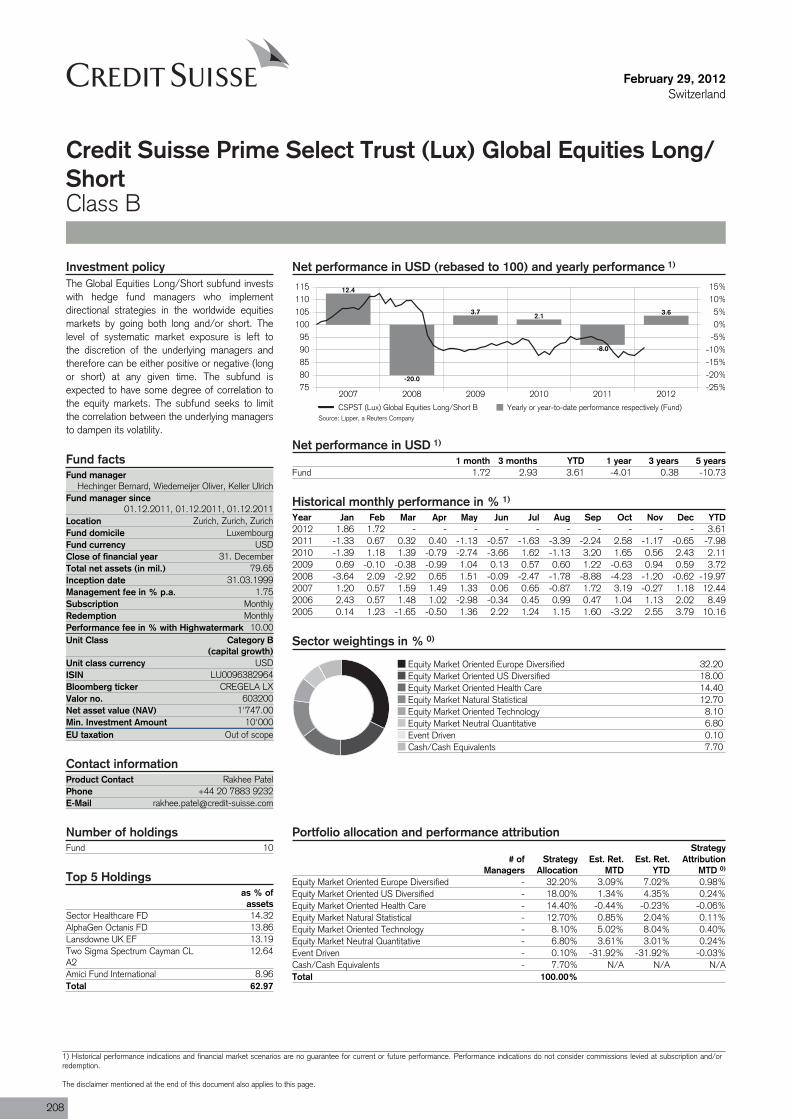

Credit Suisse Prime Select TrustCredit Suisse Prime Select Trust (Lux) Global Equities Long/Short B USD -4.0 0.4 -7.0 -22.4 5.7 208

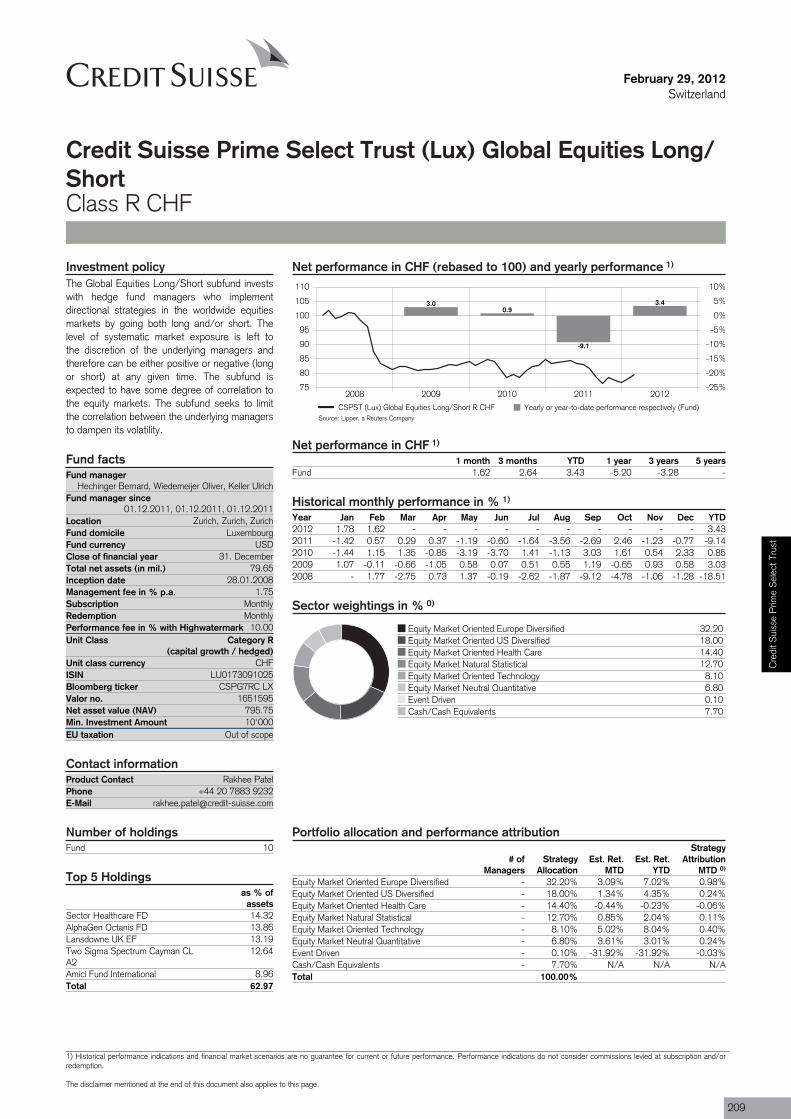

Credit Suisse Prime Select Trust (Lux) Global Equities Long/Short R CHF CHF -5.2 -3.3 -5.2 -3.3 5.8 209

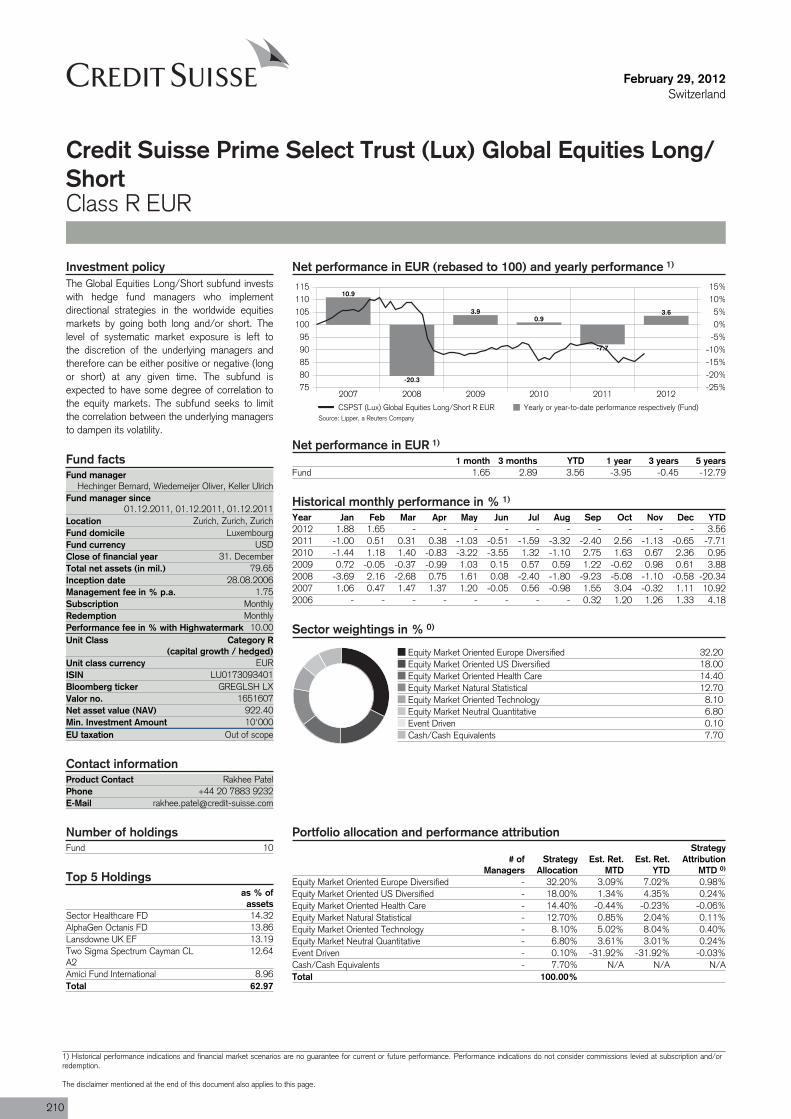

Credit Suisse Prime Select Trust (Lux) Global Equities Long/Short R EUR EUR -4.0 -0.5 -9.8 -18.9 5.6 210

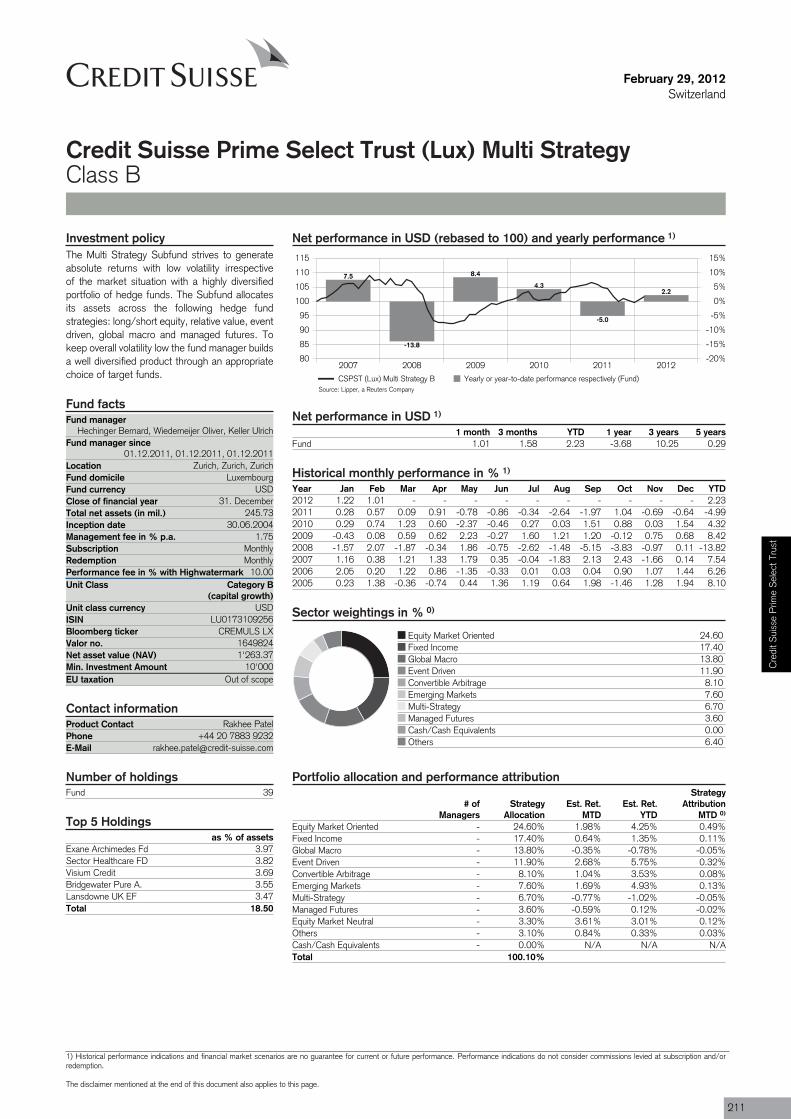

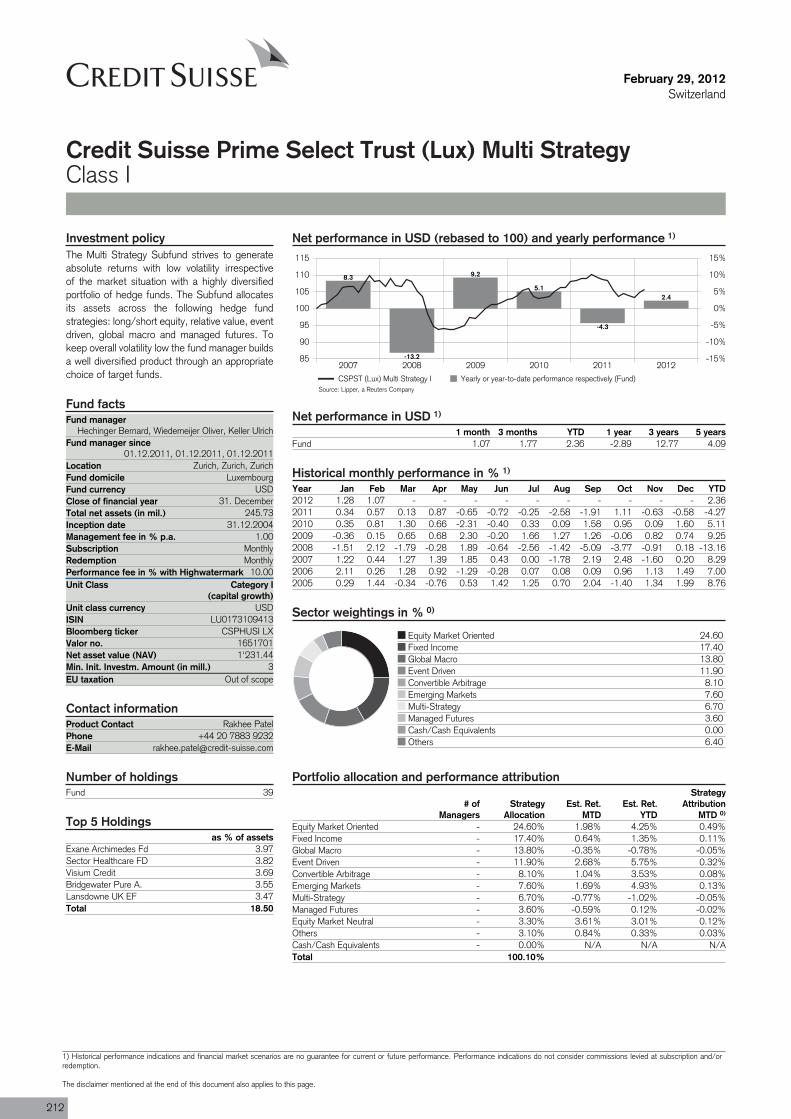

Credit Suisse Prime Select Trust (Lux) Multi Strategy USD -3.7 10.3 -6.6 -14.7 3.8 211

Credit Suisse Prime Select Trust (Lux) Multi Strategy I USD -2.9 12.8 -5.9 -12.8 3.7 212

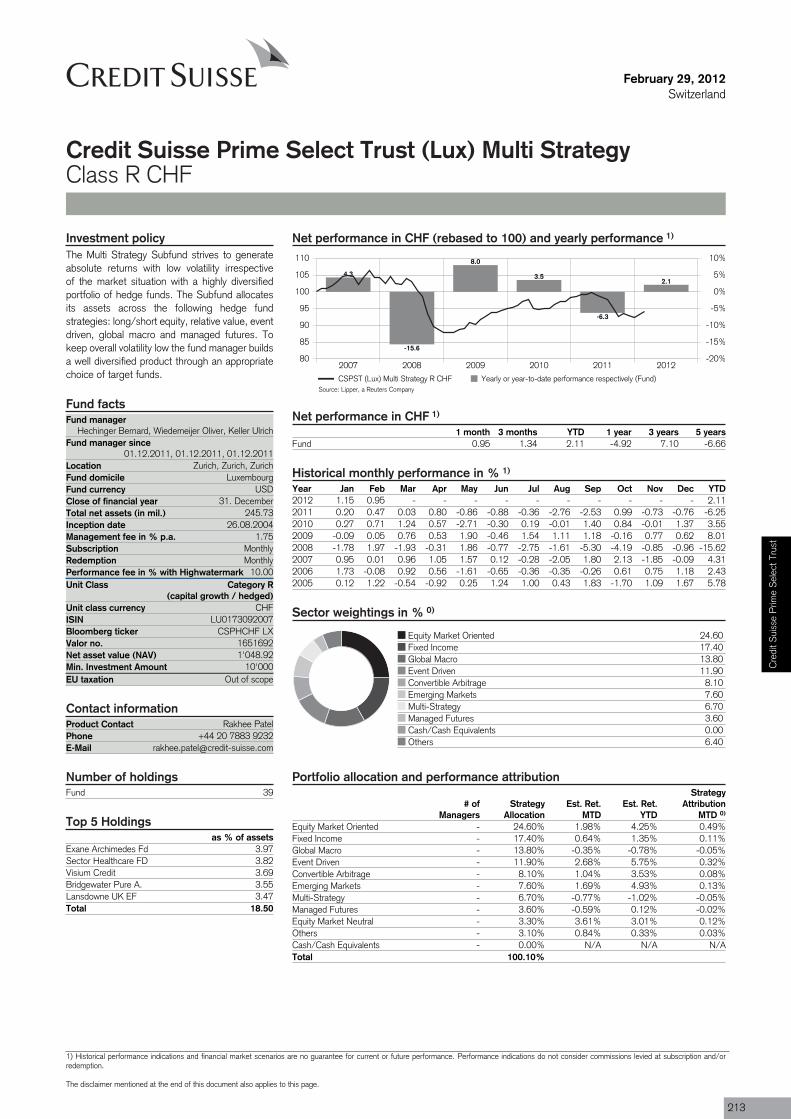

Credit Suisse Prime Select Trust (Lux) Multi Strategy R CHF CHF -4.9 7.1 -4.9 7.1 3.9 213

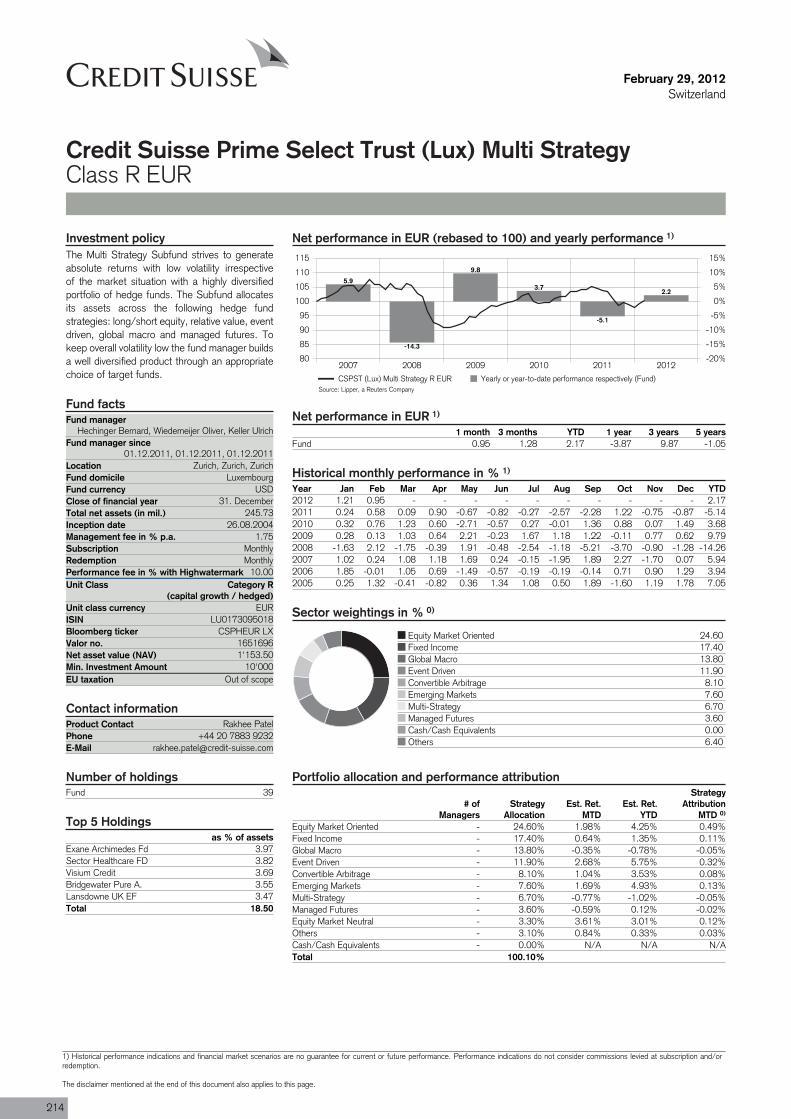

Credit Suisse Prime Select Trust (Lux) Multi Strategy R EUR EUR -3.9 9.9 -9.8 -10.5 3.9 214

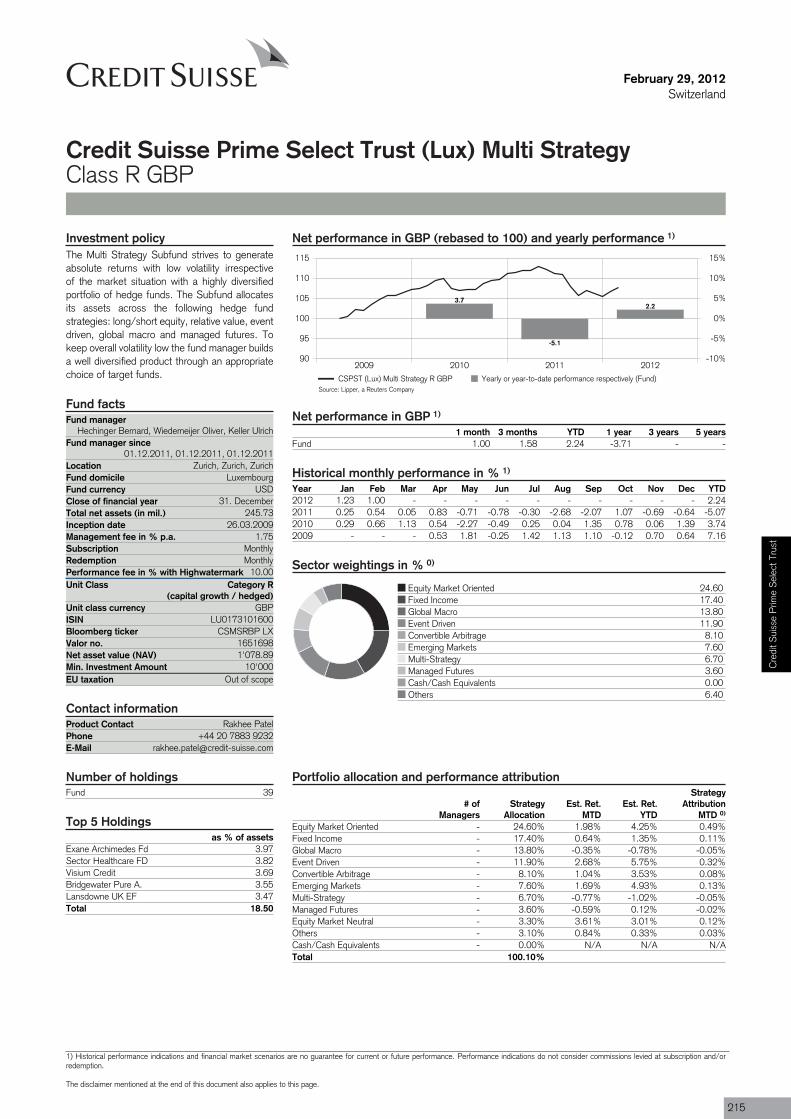

Credit Suisse Prime Select Trust (Lux) Multi Strategy R GBP GBP -3.7 n/a -8.3 n/a n/a 215

* Source: Lipper Schweiz AG** Annualized average volatility in % over the last 3 years.*** The stated yield calculations are based on net asset values.**** The stated yield calculations are based on stock prices.***** The track record before the launch period refers to the existing product,

wich is managed according to the same investment process and guidelines.

Historical performance indications and financial market scenarios are no guarantee for current or future performance.Performance indications do not consider commissions levied at subscription and/or redemption.

Ove

rvie

w

15

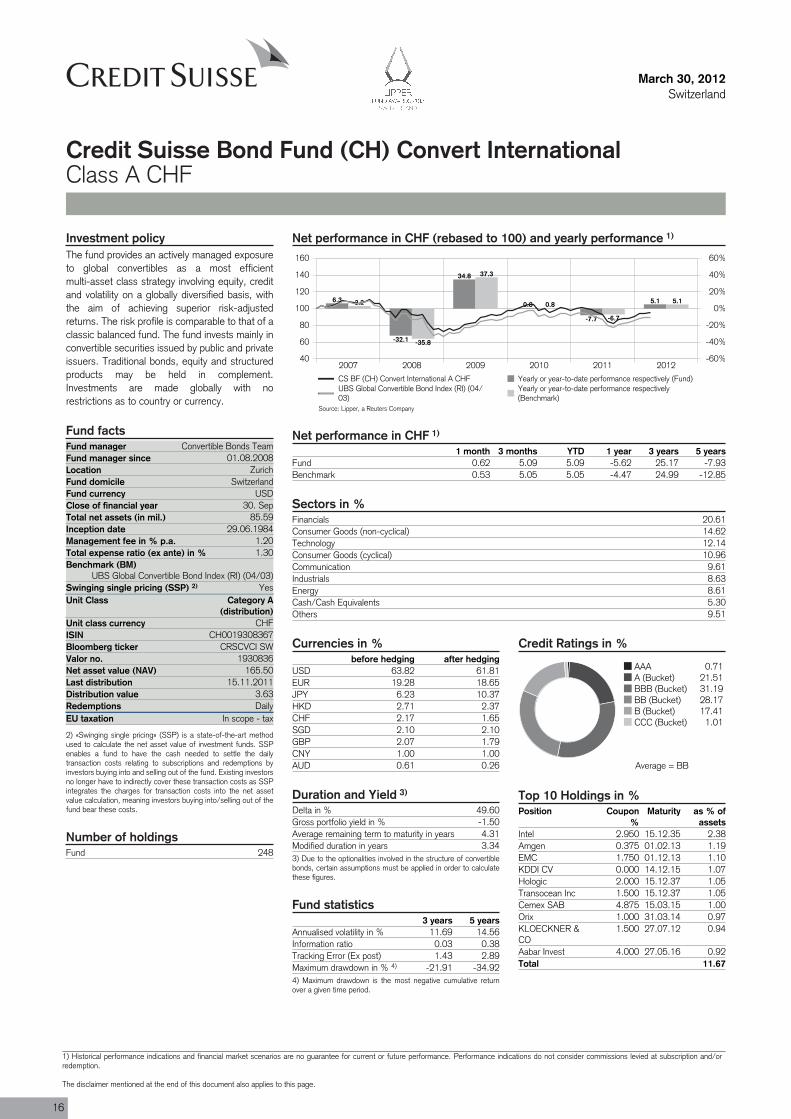

Fund manager Convertible Bonds TeamFund manager since 01.08.2008Location ZurichFund domicile SwitzerlandFund currency USDClose of financial year 30. SepTotal net assets (in mil.) 85.59Inception date 29.06.1984Management fee in % p.a. 1.20Total expense ratio (ex ante) in % 1.30Benchmark (BM)

UBS Global Convertible Bond Index (RI) (04/03)Swinging single pricing (SSP) 2) YesUnit Class Category A

(distribution)

ISIN CH0019308367

Valor no. 1930836

Last distribution 15.11.2011Distribution value 3.63Redemptions DailyEU taxation In scope - tax

Fund 248

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Convert InternationalClass A CHF

Net performance in CHF (rebased to 100) and yearly performance 1)

2007 2008 2009 2010 2011 201240

60

80

100

120

140

160

-60%

-40%

-20%

0%

20%

40%

60%

6.3

-32.1

34.8

0.8

-7.7

5.13.2

-35.8

37.3

0.8

-6.7

5.1

CS BF (CH) Convert International A CHF Yearly or year-to-date performance respectively (Fund)UBS Global Convertible Bond Index (RI) (04/03)

Yearly or year-to-date performance respectively(Benchmark)

Net performance in CHF 1)

1 month 3 months YTD 1 year 3 years 5 yearsFund 0.62 5.09 5.09 -5.62 25.17 -7.93Benchmark 0.53 5.05 5.05 -4.47 24.99 -12.85

Sectors in %Financials 20.61Consumer Goods (non-cyclical) 14.62Technology 12.14Consumer Goods (cyclical) 10.96Communication 9.61Industrials 8.63Energy 8.61Cash/Cash Equivalents 5.30Others 9.51

Currencies in %before hedging after hedging

USD 63.82 61.81EUR 19.28 18.65JPY 6.23 10.37HKD 2.71 2.37CHF 2.17 1.65SGD 2.10 2.10GBP 2.07 1.79CNY 1.00 1.00AUD 0.61 0.26

Credit Ratings in %

AAA 0.71A (Bucket) 21.51BBB (Bucket) 31.19BB (Bucket) 28.17B (Bucket) 17.41CCC (Bucket) 1.01

Top 10 Holdings in %Position Coupon

%Maturity as % of

assetsIntel 2.950 15.12.35 2.38Amgen 0.375 01.02.13 1.19EMC 1.750 01.12.13 1.10KDDI CV 0.000 14.12.15 1.07Hologic 2.000 15.12.37 1.05Transocean Inc 1.500 15.12.37 1.05Cemex SAB 4.875 15.03.15 1.00Orix 1.000 31.03.14 0.97KLOECKNER &CO

1.500 27.07.12 0.94

Aabar Invest 4.000 27.05.16 0.92Total 11.67

Duration and Yield 3)

Delta in % 49.60Gross portfolio yield in % -1.50Average remaining term to maturity in years 4.31Modified duration in years 3.343) Due to the optionalities involved in the structure of convertiblebonds, certain assumptions must be applied in order to calculatethese figures.

Fund statistics3 years 5 years

Annualised volatility in % 11.69 14.56Information ratio 0.03 0.38Tracking Error (Ex post) 1.43 2.89Maximum drawdown in % 4) -21.91 -34.924) Maximum drawdown is the most negative cumulative returnover a given time period.

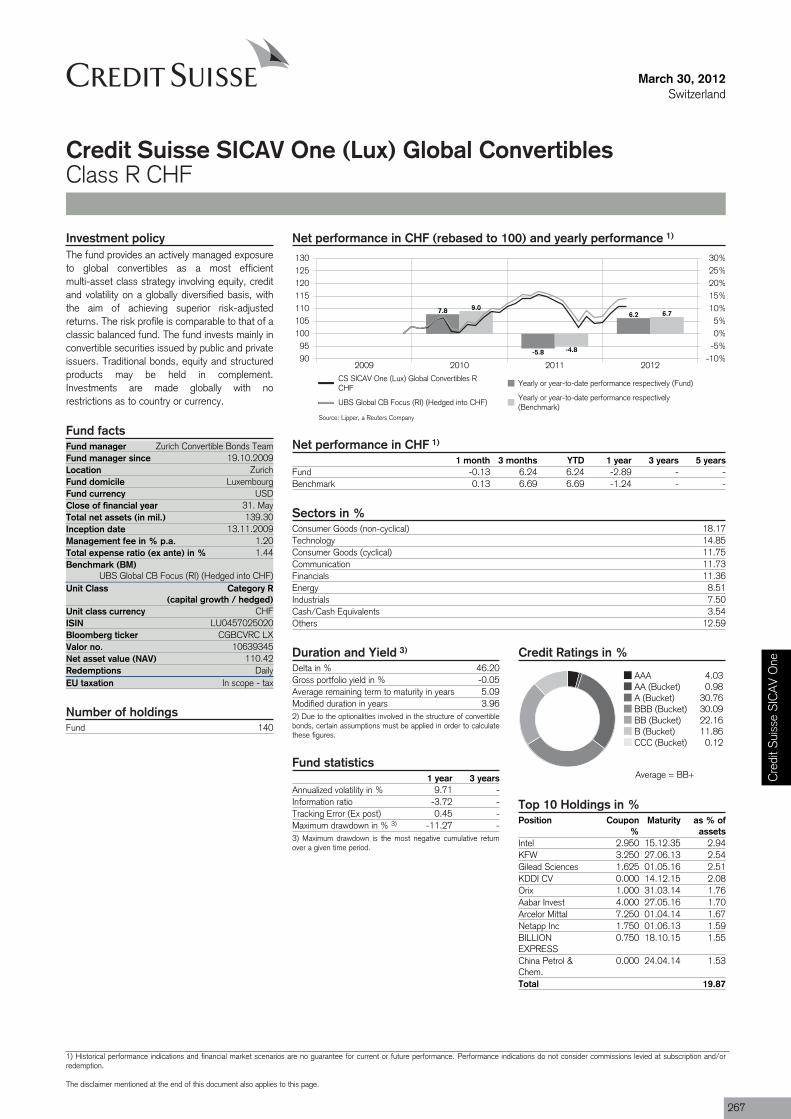

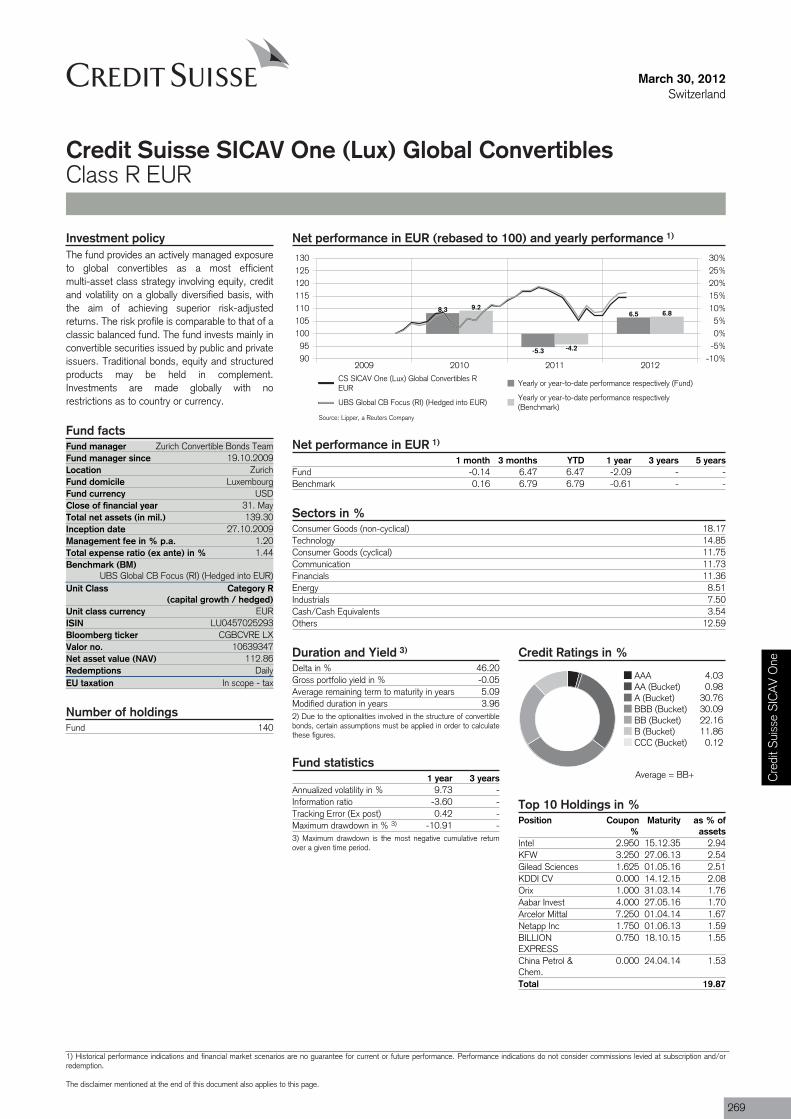

Investment policyThe fund provides an actively managed exposureto global convertibles as a most efficientmulti-asset class strategy involving equity, creditand volatility on a globally diversified basis, withthe aim of achieving superior risk-adjustedreturns. The risk profile is comparable to that of aclassic balanced fund. The fund invests mainly inconvertible securities issued by public and privateissuers. Traditional bonds, equity and structuredproducts may be held in complement.Investments are made globally with norestrictions as to country or currency.

Fund facts

Unit class currency CHF

Bloomberg ticker CRSCVCI SW

Net asset value (NAV) 165.50

2) «Swinging single pricing» (SSP) is a state-of-the-art methodused to calculate the net asset value of investment funds. SSPenables a fund to have the cash needed to settle the dailytransaction costs relating to subscriptions and redemptions byinvestors buying into and selling out of the fund. Existing investorsno longer have to indirectly cover these transaction costs as SSPintegrates the charges for transaction costs into the net assetvalue calculation, meaning investors buying into/selling out of thefund bear these costs.

Number of holdings

Source: Lipper, a Reuters Company

Average = BB

16

1) Historical performance indications and financial market scenarios are no guarantee for current or future performance. Performance indications do not consider commissions levied at subscription and/orredemption.

The disclaimer mentioned at the end of this document also applies to this page.

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Convert InternationalClass A CHF

Review previous quarter 5)

Global convertibles had a great start to the yearand returned 8.8% in Q1 2012 (currencyhedged), whereas the investment grade part ofthe universe showed a return of 5.7%. Thispositive performance was mainly attributed tostrong global equity markets and further spreadtightening.

In general, the investment environment improvedand rising investor sentiment gave equity marketsthe needed support for growth. Since themassive interventions by the ECB, financial

system stability has improved and the downsiderisk to the global economy has been reduced. Inthe US, with the unemployment rate remainingstable at 8.3% and unemployment benefit claimsfalling to the lowest level since April 2008,consumer confidence reached thesecond-highest level in four years and retail salesclimbed by most in five months. On the otherhand, inflation rose in February the most in 10months, mainly driven by gasoline prices.

In the BRIC countries (especially China and

India), stimulating monetary policy improved theoutlook for risky assets and equity marketscontinued to rise in light of the momentum builtup in December. With regards to convertiblessector performances, all were in positive territory.The highest contributions came fromTechnology, Industrial Goods and Healthcare,whereas Food & Beverage, Chemicals and Retailwere more or less flat. Convertibles primarymarket activity of USD 8.8bn in March, thehighest since June 2011, brought the totalissuance in the first quarter to USD 15.1bn.

Outlook for the market 5)

The economic climate remains supportive, butoverbought market conditions are impairing thenear-term technical picture. We are proceedingon the assumption that the headwinds(technicals, euro area crisis and geopoliticalrisks) will have only very short-livedconsequences for the markets.

We have a positive medium-term stance on

stocks and would therefore take advantage ofshare price setbacks to increase the exposure insome convertibles. On the regional side, we stillfavor the US due to its defensive characteristicsand its further improving fundamentals, whereasour view on Japan is neutral. We still likeemerging markets in the long-term due to theirpositive fundamentals and growth prospects, butare cautious in the short-term.

In general, global valuations and sentiment haveimproved and we expect a robust earningsseason ahead. We remain neutrally positioned interms of equity sensitivity across all convertibleproducts, looking for alpha generation oncompany selection level.

Portfolio ManagementThe portfolio is managed by a team of experienced investment professionals who are based in Zurich. The fund is managed according to the team's view onsecurity selection, equity sectors, equity sensitivity, credit, and duration. The team includes several portfolio managers who contribute to the co-managementof the fund according to their area of expertise.

Cre

dit S

uiss

e B

ond

Fund

5) If not expressly indicated otherwise, all quantitative data contained in this comment is based on Lipper, Bloomberg or Datastream.

17

Fund manager Convertible Bonds TeamFund manager since 01.08.2008Location ZurichFund domicile SwitzerlandFund currency USDClose of financial year 30. SepTotal net assets (in mil.) 85.59Inception date 29.06.1984Management fee in % p.a. 1.20Total expense ratio (ex ante) in % 1.30Benchmark (BM)

UBS Global Convertible Bond Index (RI) (01/02)Swinging single pricing (SSP) 2) YesUnit Class Category A

(distribution)

ISIN CH0002771514

Valor no. 277151

Last distribution 15.11.2011Distribution value 6.00Redemptions DailyEU taxation In scope - tax

Fund 248

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Convert InternationalClass A USD

Net performance in USD (rebased to 100) and yearly performance 1)

2007 2008 2009 2010 2011 201260708090

100110120130140150

-40%-30%-20%-10%

0%10%20%30%40%50%

14.6

-27.8

38.8

11.7

-8.2

8.711.3

-31.7

41.4

11.8

-7.0

8.7

CS BF (CH) Convert International A USD Yearly or year-to-date performance respectively (Fund)UBS Global Convertible Bond Index (RI) (01/02)

Yearly or year-to-date performance respectively(Benchmark)

Net performance in USD 1)

1 month 3 months YTD 1 year 3 years 5 yearsFund 0.29 8.73 8.73 -4.66 57.13 23.95Benchmark 0.20 8.68 8.68 -3.31 57.24 17.71

Sectors in %Financials 20.61Consumer Goods (non-cyclical) 14.62Technology 12.14Consumer Goods (cyclical) 10.96Communication 9.61Industrials 8.63Energy 8.61Cash/Cash Equivalents 5.30Others 9.51

Currencies in %before hedging after hedging

USD 63.82 61.81EUR 19.28 18.65JPY 6.23 10.37HKD 2.71 2.37CHF 2.17 1.65SGD 2.10 2.10GBP 2.07 1.79CNY 1.00 1.00AUD 0.61 0.26

Credit Ratings in %

AAA 0.71A (Bucket) 21.51BBB (Bucket) 31.19BB (Bucket) 28.17B (Bucket) 17.41CCC (Bucket) 1.01

Top 10 Holdings in %Position Coupon

%Maturity as % of

assetsIntel 2.950 15.12.35 2.38Amgen 0.375 01.02.13 1.19EMC 1.750 01.12.13 1.10KDDI CV 0.000 14.12.15 1.07Hologic 2.000 15.12.37 1.05Transocean Inc 1.500 15.12.37 1.05Cemex SAB 4.875 15.03.15 1.00Orix 1.000 31.03.14 0.97KLOECKNER &CO

1.500 27.07.12 0.94

Aabar Invest 4.000 27.05.16 0.92Total 11.67

Duration and Yield 3)

Delta in % 49.60Gross portfolio yield in % -1.50Average remaining term to maturity in years 4.31Modified duration in years 3.343) Due to the optionalities involved in the structure of convertiblebonds, certain assumptions must be applied in order to calculatethese figures.

Fund statistics3 years 5 years

Annualised volatility in % 13.37 15.67Information ratio -0.02 0.36Tracking Error (Ex post) 1.46 2.91Maximum drawdown in % 4) -15.94 -34.864) Maximum drawdown is the most negative cumulative returnover a given time period.

Investment policyThe fund provides an actively managed exposureto global convertibles as a most efficientmulti-asset class strategy involving equity, creditand volatility on a globally diversified basis, withthe aim of achieving superior risk-adjustedreturns. The risk profile is comparable to that of aclassic balanced fund. The fund invests mainly inconvertible securities issued by public and privateissuers. Traditional bonds, equity and structuredproducts may be held in complement.Investments are made globally with norestrictions as to country or currency.

Fund facts

Unit class currency USD

Bloomberg ticker CRSCVUI SW

Net asset value (NAV) 279.63

2) «Swinging single pricing» (SSP) is a state-of-the-art methodused to calculate the net asset value of investment funds. SSPenables a fund to have the cash needed to settle the dailytransaction costs relating to subscriptions and redemptions byinvestors buying into and selling out of the fund. Existing investorsno longer have to indirectly cover these transaction costs as SSPintegrates the charges for transaction costs into the net assetvalue calculation, meaning investors buying into/selling out of thefund bear these costs.

Number of holdings

Source: Lipper, a Reuters Company

Average = BB

18

1) Historical performance indications and financial market scenarios are no guarantee for current or future performance. Performance indications do not consider commissions levied at subscription and/orredemption.

The disclaimer mentioned at the end of this document also applies to this page.

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Convert InternationalClass A USD

Review previous quarter 5)

Global convertibles had a great start to the yearand returned 8.8% in Q1 2012 (currencyhedged), whereas the investment grade part ofthe universe showed a return of 5.7%. Thispositive performance was mainly attributed tostrong global equity markets and further spreadtightening.

In general, the investment environment improvedand rising investor sentiment gave equity marketsthe needed support for growth. Since themassive interventions by the ECB, financial

system stability has improved and the downsiderisk to the global economy has been reduced. Inthe US, with the unemployment rate remainingstable at 8.3% and unemployment benefit claimsfalling to the lowest level since April 2008,consumer confidence reached thesecond-highest level in four years and retail salesclimbed by most in five months. On the otherhand, inflation rose in February the most in 10months, mainly driven by gasoline prices.

In the BRIC countries (especially China and

India), stimulating monetary policy improved theoutlook for risky assets and equity marketscontinued to rise in light of the momentum builtup in December. With regards to convertiblessector performances, all were in positive territory.The highest contributions came fromTechnology, Industrial Goods and Healthcare,whereas Food & Beverage, Chemicals and Retailwere more or less flat. Convertibles primarymarket activity of USD 8.8bn in March, thehighest since June 2011, brought the totalissuance in the first quarter to USD 15.1bn.

Outlook for the market 5)

The economic climate remains supportive, butoverbought market conditions are impairing thenear-term technical picture. We are proceedingon the assumption that the headwinds(technicals, euro area crisis and geopoliticalrisks) will have only very short-livedconsequences for the markets.

We have a positive medium-term stance on

stocks and would therefore take advantage ofshare price setbacks to increase the exposure insome convertibles. On the regional side, we stillfavor the US due to its defensive characteristicsand its further improving fundamentals, whereasour view on Japan is neutral. We still likeemerging markets in the long-term due to theirpositive fundamentals and growth prospects, butare cautious in the short-term.

In general, global valuations and sentiment haveimproved and we expect a robust earningsseason ahead. We remain neutrally positioned interms of equity sensitivity across all convertibleproducts, looking for alpha generation oncompany selection level.

Portfolio ManagementThe portfolio is managed by a team of experienced investment professionals who are based in Zurich. The fund is managed according to the team's view onsecurity selection, equity sectors, equity sensitivity, credit, and duration. The team includes several portfolio managers who contribute to the co-managementof the fund according to their area of expertise.

Cre

dit S

uiss

e B

ond

Fund

5) If not expressly indicated otherwise, all quantitative data contained in this comment is based on Lipper, Bloomberg or Datastream.

19

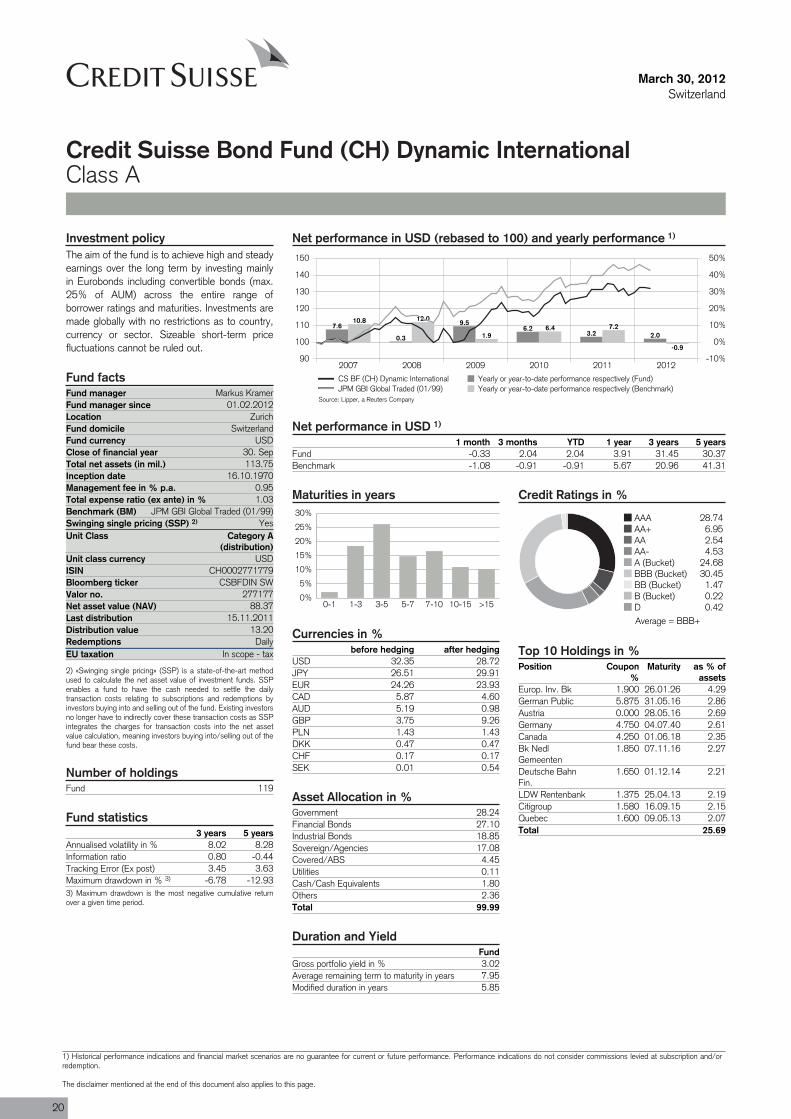

Fund manager Markus KramerFund manager since 01.02.2012Location ZurichFund domicile SwitzerlandFund currency USDClose of financial year 30. SepTotal net assets (in mil.) 113.75Inception date 16.10.1970Management fee in % p.a. 0.95Total expense ratio (ex ante) in % 1.03Benchmark (BM) JPM GBI Global Traded (01/99)Swinging single pricing (SSP) 2) YesUnit Class Category A

(distribution)

ISIN CH0002771779

Valor no. 277177

Last distribution 15.11.2011Distribution value 13.20Redemptions DailyEU taxation In scope - tax

Fund 119

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Dynamic InternationalClass A

Net performance in USD (rebased to 100) and yearly performance 1)

2007 2008 2009 2010 2011 201290

100

110

120

130

140

150

-10%

0%

10%

20%

30%

40%

50%

7.6

0.3

9.56.2

3.2 2.0

10.8 12.0

1.96.4 7.2

-0.9

CS BF (CH) Dynamic International Yearly or year-to-date performance respectively (Fund)JPM GBI Global Traded (01/99) Yearly or year-to-date performance respectively (Benchmark)

Net performance in USD 1)

1 month 3 months YTD 1 year 3 years 5 yearsFund -0.33 2.04 2.04 3.91 31.45 30.37Benchmark -1.08 -0.91 -0.91 5.67 20.96 41.31

Maturities in years

0%

5%

10%

15%

20%

25%

30%

0-1 1-3 3-5 5-7 7-10 10-15 >15

Currencies in %before hedging after hedging

USD 32.35 28.72JPY 26.51 29.91EUR 24.26 23.93CAD 5.87 4.60AUD 5.19 0.98GBP 3.75 9.26PLN 1.43 1.43DKK 0.47 0.47CHF 0.17 0.17SEK 0.01 0.54

Asset Allocation in %Government 28.24Financial Bonds 27.10Industrial Bonds 18.85Sovereign/Agencies 17.08Covered/ABS 4.45Utilities 0.11Cash/Cash Equivalents 1.80Others 2.36Total 99.99

Duration and YieldFund

Gross portfolio yield in % 3.02Average remaining term to maturity in years 7.95Modified duration in years 5.85

Credit Ratings in %

AAA 28.74AA+ 6.95AA 2.54AA- 4.53A (Bucket) 24.68BBB (Bucket) 30.45BB (Bucket) 1.47B (Bucket) 0.22D 0.42

Top 10 Holdings in %Position Coupon

%Maturity as % of

assetsEurop. Inv. Bk 1.900 26.01.26 4.29German Public 5.875 31.05.16 2.86Austria 0.000 28.05.16 2.69Germany 4.750 04.07.40 2.61Canada 4.250 01.06.18 2.35Bk NedlGemeenten

1.850 07.11.16 2.27

Deutsche BahnFin.

1.650 01.12.14 2.21

LDW Rentenbank 1.375 25.04.13 2.19Citigroup 1.580 16.09.15 2.15Quebec 1.600 09.05.13 2.07Total 25.69

Investment policyThe aim of the fund is to achieve high and steadyearnings over the long term by investing mainlyin Eurobonds including convertible bonds (max.25% of AUM) across the entire range ofborrower ratings and maturities. Investments aremade globally with no restrictions as to country,currency or sector. Sizeable short-term pricefluctuations cannot be ruled out.

Fund facts

Unit class currency USD

Bloomberg ticker CSBFDIN SW

Net asset value (NAV) 88.37

2) «Swinging single pricing» (SSP) is a state-of-the-art methodused to calculate the net asset value of investment funds. SSPenables a fund to have the cash needed to settle the dailytransaction costs relating to subscriptions and redemptions byinvestors buying into and selling out of the fund. Existing investorsno longer have to indirectly cover these transaction costs as SSPintegrates the charges for transaction costs into the net assetvalue calculation, meaning investors buying into/selling out of thefund bear these costs.

Number of holdings

Fund statistics3 years 5 years

Annualised volatility in % 8.02 8.28Information ratio 0.80 -0.44Tracking Error (Ex post) 3.45 3.63Maximum drawdown in % 3) -6.78 -12.933) Maximum drawdown is the most negative cumulative returnover a given time period.

Source: Lipper, a Reuters Company

Average = BBB+

20

1) Historical performance indications and financial market scenarios are no guarantee for current or future performance. Performance indications do not consider commissions levied at subscription and/orredemption.

The disclaimer mentioned at the end of this document also applies to this page.

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Dynamic InternationalClass A

Review previous quarter 4)

Despite the return of risk appetite, sovereignbond yields remained surprisingly low in the firstquarter. While US Treasury yields rose by asmuch as 40bps at the long end of the curve,the German Bund curve remained roughlyunchanged over the quarter. Within Europe, Italy,Portugal and Ireland had double digit returnswhile core EU markets ended the quarter inslightly positive territory.

Government bonds returned 0.3% in Q1 in localcurrencies as measured by the JPM GBI GlobalIndex. Best performers were EMU governmentbonds, which returned an overall 3.6%, driven byItaly (+11.4%), Ireland (+10.4%) and Portugal(+10.0%). UK Gilts, on the other hand,performed worst and lost 2.0%, while USTreasuries returned -1.3%.

The increasing risk appetite in Q1 resulted ina negative performance of the USD against allmajor currencies except for the JPY. Among thebest performers were the commodity currencies,with the NZD and the NOK appreciating by6.1% and 5.6% respectively. The EUR gained3.2%, while the JPY lost a hefty 7.2%..

Outlook for the market 4)

The US economy gathered considerablemomentum in the second half of 2011 asconsumer spending rebounded. The pace islikely to slow somewhat in the short run, butcontinued gains in employment suggest thatgrowth may surprise on the upside in 2012.However, oil prices being back close to their2011 peaks keep us from turning overlyoptimistic as they begin to hurt still very subduedconsumers, while wage gains remain fairlyanemic. Also, corporate investment looks robust,but is unlikely to accelerate. The massive liquidityinjections by the ECB and the Greek debt

restructuring have succeeded in stabilizing banksand government debt.

However, the outlook for consumers andbusinesses remains subdued. Fiscal tighteningis already “biting” in many countries and, afterthe elections, the French government will likelyfollow. After the increase in major benchmarkyields (except German Bunds), we do not expectsignificant interest rate increases in the comingmonths, with current levels broadly in line withactual economic fundamentals and the continuedaccommodation from major central banks likely

to cap large moves. After the sharp tighteningof the past few months, credit spreads in manymarket segments are now close to their historicalaverages. While the ample liquidity provided bycentral banks is likely to remain supportive,potential for strong credit returns has abated, inour view. Additionally, political headlines in theeurozone could continue to drive short-termvolatility, with the market likely to focus ondevelopments in Spain and the Frenchpresidential election, while Greece should movemore to the background.

Portfolio ManagementMarkus Kramer, Vice President, is a senior portfolio manager for Global Fixed Income portfolios. Prior to joining Credit Suisse in

September 2011, he worked at Zurich Cantonal Bank Asset Management for six years. Mr. Kramer holds a Masters Degree from the University of Zurich(specializing in banking and finance) and is a CFA charterholder and a Certified FRM holder. He is a board member of the Swiss Bond Commission.

Cre

dit S

uiss

e B

ond

Fund

4) If not expressly indicated otherwise, all quantitative data contained in this comment is based on Lipper, Bloomberg or Datastream.

21

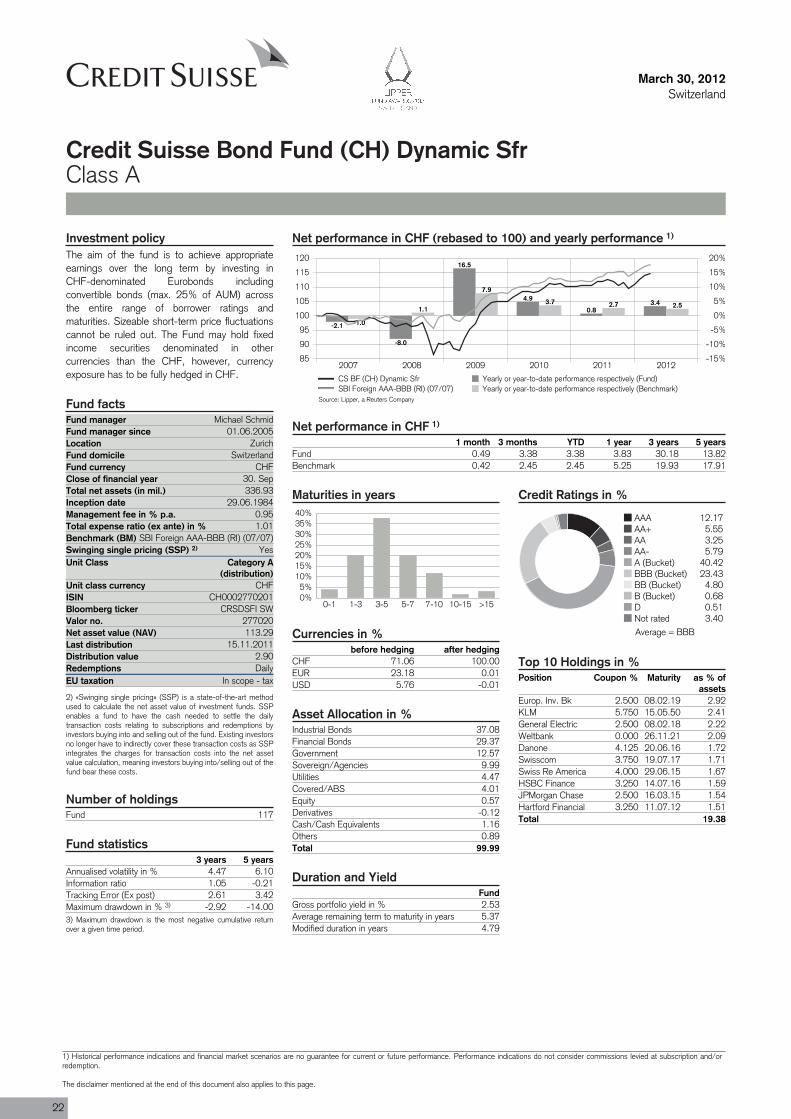

Fund manager Michael SchmidFund manager since 01.06.2005Location ZurichFund domicile SwitzerlandFund currency CHFClose of financial year 30. SepTotal net assets (in mil.) 336.93Inception date 29.06.1984Management fee in % p.a. 0.95Total expense ratio (ex ante) in % 1.01Benchmark (BM) SBI Foreign AAA-BBB (RI) (07/07)Swinging single pricing (SSP) 2) YesUnit Class Category A

(distribution)

ISIN CH0002770201

Valor no. 277020

Last distribution 15.11.2011Distribution value 2.90Redemptions DailyEU taxation In scope - tax

Fund 117

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Dynamic SfrClass A

Net performance in CHF (rebased to 100) and yearly performance 1)

2007 2008 2009 2010 2011 201285

90

95

100

105

110

115

120

-15%

-10%

-5%

0%

5%

10%

15%

20%

-2.1

-8.0

16.5

4.9

0.83.4

-1.0

1.1

7.9

3.7 2.7 2.5

CS BF (CH) Dynamic Sfr Yearly or year-to-date performance respectively (Fund)SBI Foreign AAA-BBB (RI) (07/07) Yearly or year-to-date performance respectively (Benchmark)

Net performance in CHF 1)

1 month 3 months YTD 1 year 3 years 5 yearsFund 0.49 3.38 3.38 3.83 30.18 13.82Benchmark 0.42 2.45 2.45 5.25 19.93 17.91

Maturities in years

0%5%

10%15%20%25%30%35%40%

0-1 1-3 3-5 5-7 7-10 10-15 >15

Currencies in %before hedging after hedging

CHF 71.06 100.00EUR 23.18 0.01USD 5.76 -0.01

Asset Allocation in %Industrial Bonds 37.08Financial Bonds 29.37Government 12.57Sovereign/Agencies 9.99Utilities 4.47Covered/ABS 4.01Equity 0.57Derivatives -0.12Cash/Cash Equivalents 1.16Others 0.89Total 99.99

Duration and YieldFund

Gross portfolio yield in % 2.53Average remaining term to maturity in years 5.37Modified duration in years 4.79

Credit Ratings in %

AAA 12.17AA+ 5.55AA 3.25AA- 5.79A (Bucket) 40.42BBB (Bucket) 23.43BB (Bucket) 4.80B (Bucket) 0.68D 0.51Not rated 3.40

Top 10 Holdings in %Position Coupon % Maturity as % of

assetsEurop. Inv. Bk 2.500 08.02.19 2.92KLM 5.750 15.05.50 2.41General Electric 2.500 08.02.18 2.22Weltbank 0.000 26.11.21 2.09Danone 4.125 20.06.16 1.72Swisscom 3.750 19.07.17 1.71Swiss Re America 4.000 29.06.15 1.67HSBC Finance 3.250 14.07.16 1.59JPMorgan Chase 2.500 16.03.15 1.54Hartford Financial 3.250 11.07.12 1.51Total 19.38

Investment policyThe aim of the fund is to achieve appropriateearnings over the long term by investing inCHF-denominated Eurobonds includingconvertible bonds (max. 25% of AUM) acrossthe entire range of borrower ratings andmaturities. Sizeable short-term price fluctuationscannot be ruled out. The Fund may hold fixedincome securities denominated in othercurrencies than the CHF, however, currencyexposure has to be fully hedged in CHF.

Fund facts

Unit class currency CHF

Bloomberg ticker CRSDSFI SW

Net asset value (NAV) 113.29

2) «Swinging single pricing» (SSP) is a state-of-the-art methodused to calculate the net asset value of investment funds. SSPenables a fund to have the cash needed to settle the dailytransaction costs relating to subscriptions and redemptions byinvestors buying into and selling out of the fund. Existing investorsno longer have to indirectly cover these transaction costs as SSPintegrates the charges for transaction costs into the net assetvalue calculation, meaning investors buying into/selling out of thefund bear these costs.

Number of holdings

Fund statistics3 years 5 years

Annualised volatility in % 4.47 6.10Information ratio 1.05 -0.21Tracking Error (Ex post) 2.61 3.42Maximum drawdown in % 3) -2.92 -14.003) Maximum drawdown is the most negative cumulative returnover a given time period.

Source: Lipper, a Reuters Company

Average = BBB

22

1) Historical performance indications and financial market scenarios are no guarantee for current or future performance. Performance indications do not consider commissions levied at subscription and/orredemption.

The disclaimer mentioned at the end of this document also applies to this page.

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Dynamic SfrClass A

Review previous quarter 4)

Substantial liquidity injections by the ECB (LTROI and LTRO II) and the restructuring of the Greekgovernment debt helped to stabilize markets inQ1 2012. There are still structural problemsrelated to European borrowers andheterogeneous global growth patterns.Nevertheless, the Swiss economy narrowlyavoided recession thanks to domesticconsumption and high demand for Swisswatches and pharmaceutical products in other

countries. The SNB stuck to its guns andmaintained its expansive monetary policy, onceagain confirming a minimum exchange rate of1.20 francs to the euro.

Interest rates remained very low for all termsin the quarter under review. The 10-year swaprate even dipped below the 1% mark in earlyMarch to 0.99%, setting a new record low. Whileshort-term Confederation bonds of up to three

years still exhibited negative yields at the start ofthe reporting period, the curve has since returnedto normal. At the end of the quarter, the 3-monthCHF LIBOR was 6bps higher at 0.11%, whilethe yield on 2-year Confederation bonds rose to0.02% (+6bps) and 10-year bonds came in at0.85% (+21bps). The performance of the firstquarter was mostly positive thanks to investordemand for high yielding bonds which resulted ina reduction of credit spreads.

Outlook for the market 4)

While the US economy performed surprisinglywell, production in Japan and Europe stagnated.Switzerland's GDP managed to grow at a rateof 0.1% in Q4 2011 despite the continuousstrength of the Swiss franc. A number of leadingindicators are showing early signs of stabilization,which could suggest that the economy hasbottomed out. The Swiss economy is dependenton global economic trends, and it remains to beseen whether the progress made with regard toovercoming the European sovereign debt crisiswill bring a lasting improvement to the situation.That said, a resurgence of the debt crisis cannot

be ruled out. Other geopolitical tensions couldlead to increased volatility in commodity prices. Inits first assessment of monetary policy in March2012 the SNB maintained its expansive courseand confirmed the minimum exchange rate of1.20 francs to the euro. The target range forthe CHF 3-month LIBOR is still 0-0.25%, andliquidity is still being kept high. On the otherhand, inflation is expected to rise modestly(2013: 0.3% and 2014: 0.6%). Also, theforecast for economic growth has been revisedupwards to 1% for 2012.

For the first time since last year the score ofour interest rate factor model turned negative asthe more friendly fundamental picture suggestshigher yields going forward. The technical inputalso changed to negative due to an overboughtsituation in the short term. The behavioral inputalso neutralized because of the recent strongflattening of the yield curve. We will reduce ourduration in the portfolios towards a shorterposition than the benchmark. We recommendtop quality issues and would increase thediversification in the portfolio as even somefrequent issuers have become expensive.

Portfolio ManagementMichael Schmid, Director, is a senior portfolio manager in the fixed-income Total Return Strategy team. He is a member of CSAM's GlobalCredit Committee. Before he joined the Total Return Strategy team he was head of the Credit Portfolios team and portfolio manager forvarious European high-yield mandates. Prior to joining CSAM in 1998, he worked for three years at Revisuisse PricewaterhouseCoopersas a bank auditor. Michael Schmid graduated from the University of Zurich (specialising in banking and finance) and is a Certified EFFASFinancial Analyst.

Cre

dit S

uiss

e B

ond

Fund

4) If not expressly indicated otherwise, all quantitative data contained in this comment is based on Lipper, Bloomberg or Datastream.

23

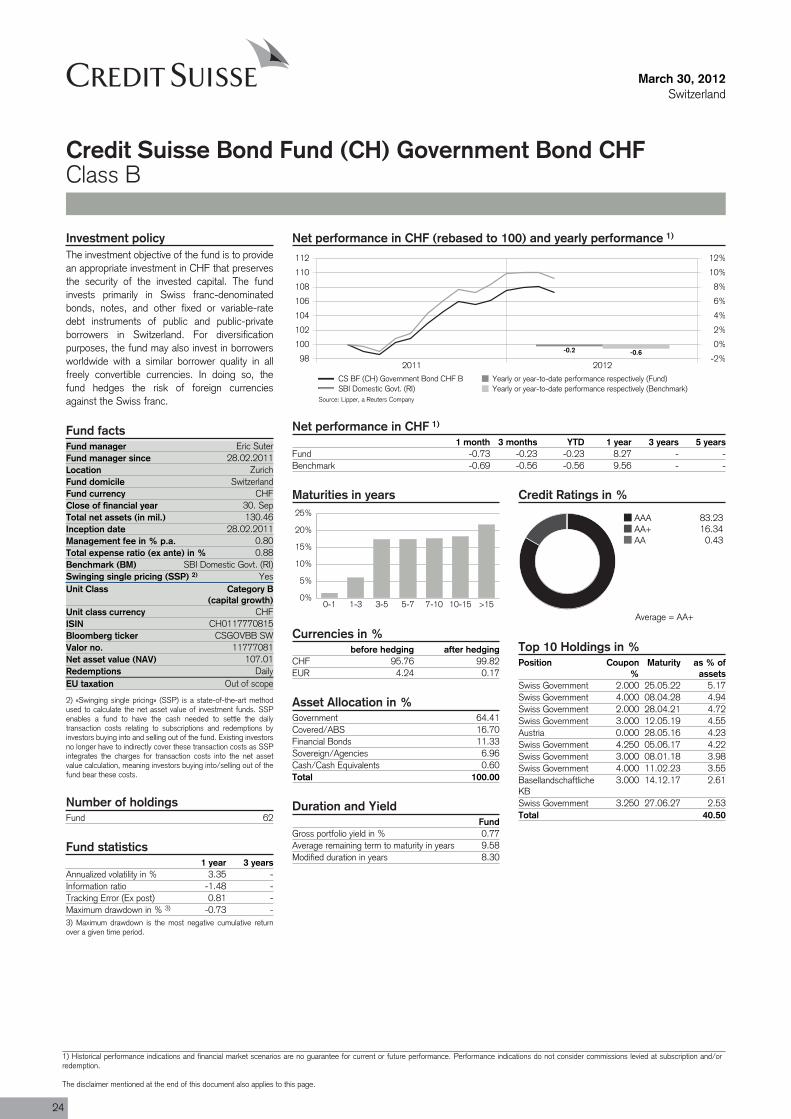

Fund manager Eric SuterFund manager since 28.02.2011Location ZurichFund domicile SwitzerlandFund currency CHFClose of financial year 30. SepTotal net assets (in mil.) 130.46Inception date 28.02.2011Management fee in % p.a. 0.80Total expense ratio (ex ante) in % 0.88Benchmark (BM) SBI Domestic Govt. (RI)Swinging single pricing (SSP) 2) YesUnit Class Category B

(capital growth)

ISIN CH0117770815

Valor no. 11777081

Redemptions DailyEU taxation Out of scope

Fund 62

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Government Bond CHFClass B

Net performance in CHF (rebased to 100) and yearly performance 1)

2011 201298

100

102

104

106

108

110

112

-2%

0%

2%

4%

6%

8%

10%

12%

-0.2 -0.6

CS BF (CH) Government Bond CHF B Yearly or year-to-date performance respectively (Fund)SBI Domestic Govt. (RI) Yearly or year-to-date performance respectively (Benchmark)

Net performance in CHF 1)

1 month 3 months YTD 1 year 3 years 5 yearsFund -0.73 -0.23 -0.23 8.27 - -Benchmark -0.69 -0.56 -0.56 9.56 - -

Maturities in years

0%

5%

10%

15%

20%

25%

0-1 1-3 3-5 5-7 7-10 10-15 >15

Currencies in %before hedging after hedging

CHF 95.76 99.82EUR 4.24 0.17

Asset Allocation in %Government 64.41Covered/ABS 16.70Financial Bonds 11.33Sovereign/Agencies 6.96Cash/Cash Equivalents 0.60Total 100.00

Duration and YieldFund

Gross portfolio yield in % 0.77Average remaining term to maturity in years 9.58Modified duration in years 8.30

Credit Ratings in %

AAA 83.23AA+ 16.34AA 0.43

Top 10 Holdings in %Position Coupon

%Maturity as % of

assetsSwiss Government 2.000 25.05.22 5.17Swiss Government 4.000 08.04.28 4.94Swiss Government 2.000 28.04.21 4.72Swiss Government 3.000 12.05.19 4.55Austria 0.000 28.05.16 4.23Swiss Government 4.250 05.06.17 4.22Swiss Government 3.000 08.01.18 3.98Swiss Government 4.000 11.02.23 3.55BasellandschaftlicheKB

3.000 14.12.17 2.61

Swiss Government 3.250 27.06.27 2.53Total 40.50

Investment policyThe investment objective of the fund is to providean appropriate investment in CHF that preservesthe security of the invested capital. The fundinvests primarily in Swiss franc-denominatedbonds, notes, and other fixed or variable-ratedebt instruments of public and public-privateborrowers in Switzerland. For diversificationpurposes, the fund may also invest in borrowersworldwide with a similar borrower quality in allfreely convertible currencies. In doing so, thefund hedges the risk of foreign currenciesagainst the Swiss franc.

Fund facts

Unit class currency CHF

Bloomberg ticker CSGOVBB SW

Net asset value (NAV) 107.01

2) «Swinging single pricing» (SSP) is a state-of-the-art methodused to calculate the net asset value of investment funds. SSPenables a fund to have the cash needed to settle the dailytransaction costs relating to subscriptions and redemptions byinvestors buying into and selling out of the fund. Existing investorsno longer have to indirectly cover these transaction costs as SSPintegrates the charges for transaction costs into the net assetvalue calculation, meaning investors buying into/selling out of thefund bear these costs.

Number of holdings

Fund statistics1 year 3 years

Annualized volatility in % 3.35 -Information ratio -1.48 -Tracking Error (Ex post) 0.81 -Maximum drawdown in % 3) -0.73 -3) Maximum drawdown is the most negative cumulative returnover a given time period.

Source: Lipper, a Reuters Company

Average = AA+

24

1) Historical performance indications and financial market scenarios are no guarantee for current or future performance. Performance indications do not consider commissions levied at subscription and/orredemption.

The disclaimer mentioned at the end of this document also applies to this page.

March 30, 2012Switzerland

Credit Suisse Bond Fund (CH) Government Bond CHFClass B

Review previous quarter 4)

Substantial liquidity injections by the ECB (LTROI and LTRO II) and the restructuring of the Greekgovernment debt helped to stabilize markets inQ1 2012. There are still structural problemsrelated to European borrowers andheterogeneous global growth patterns.Nevertheless, the Swiss economy narrowlyavoided recession thanks to domesticconsumption and high demand for Swisswatches and pharmaceutical products in other

countries. The SNB stuck to its guns andmaintained its expansive monetary policy, onceagain confirming a minimum exchange rate of1.20 francs to the euro.

Interest rates remained very low for all termsin the quarter under review. The 10-year swaprate even dipped below the 1% mark in earlyMarch to 0.99%, setting a new record low. Whileshort-term Confederation bonds of up to three

years still exhibited negative yields at the start ofthe reporting period, the curve has since returnedto normal. At the end of the quarter, the 3-monthCHF LIBOR was 6bps higher at 0.11%, whilethe yield on 2-year Confederation bonds rose to0.02% (+6bps) and 10-year bonds came in at0.85% (+21bps). The performance of the firstquarter was mostly positive thanks to investordemand for high yielding bonds which resulted ina reduction of credit spreads.

Outlook for the market 4)

While the US economy performed surprisinglywell, production in Japan and Europe stagnated.Switzerland's GDP managed to grow at a rateof 0.1% in Q4 2011 despite the continuousstrength of the Swiss franc. A number of leadingindicators are showing early signs of stabilization,which could suggest that the economy hasbottomed out. The Swiss economy is dependenton global economic trends, and it remains to beseen whether the progress made with regard toovercoming the European sovereign debt crisiswill bring a lasting improvement to the situation.That said, a resurgence of the debt crisis cannot

be ruled out. Other geopolitical tensions couldlead to increased volatility in commodity prices. Inits first assessment of monetary policy in March2012 the SNB maintained its expansive courseand confirmed the minimum exchange rate of1.20 francs to the euro. The target range forthe CHF 3-month LIBOR is still 0-0.25%, andliquidity is still being kept high. On the otherhand, inflation is expected to rise modestly(2013: 0.3% and 2014: 0.6%). Also, theforecast for economic growth has been revisedupwards to 1% for 2012.

For the first time since last year the score ofour interest rate factor model turned negative asthe more friendly fundamental picture suggestshigher yields going forward. The technical inputalso changed to negative due to an overboughtsituation in the short term. The behavioral inputalso neutralized because of the recent strongflattening of the yield curve. We will reduce ourduration in the portfolios towards a shorterposition than the benchmark. We recommendtop quality issues and would increase thediversification in the portfolio as even some wellregarded names have gotten into trouble.

Portfolio ManagementEric Suter, Director, is a senior portfolio manager. He heads the Swiss Fixed Income Team and is responsible for the Swiss Fixed Incomeinvestment decision process. Eric joined CS Group in 1983 and worked in trading, product development and structuring of fixed incomeproducts. In 1995 he moved to fixed income asset management. He received a Bachelor in Business Administration from the KaderschuleZurich (KSZ), is a Certified International Investment Analyst (CIIA) and a member of the Swiss Bond Commission. Eric Suter, Director,leitet das Schweizer Franken Obligationen Team und ist verantwortlich für den Schweizer Franken Anlageprozess. Er stiess 1983 zur CSGroup und arbeitete im Handel, der Produkteentwicklung sowie in der Strukturierung von Zinsprodukten. 1995 wechselte er insObligationen Portfolio Management. Hr. Suter hat einen Abschluss in Betriebsökonomie der Kaderschule Zürich (KSZ), ist dipl.Finanzanalytiker und Vermögensverwalter (AZEK) sowie Mitglied der Schweizer Obligationenkommission (OKS).

Eric Suter, Director, dirige l'équipe Obligations CHF. Il a rejoint le CS Group en 1983 et a travaillé dans la vente, le développement produits ainsi que lastructuration de produits obligataires. En 1995, il est passé dans le domaine Portfolio Management Obligations. E. Suter dispose de diplômes en économied'entreprise de l'Ecole de cadres de Zurich (KSZ), d'analyste financier et gestionnaire de fortune (CFPI) et est membre de la Commission Suisse desObligations (OKS).

Cre

dit S

uiss

e B

ond

Fund

4) If not expressly indicated otherwise, all quantitative data contained in this comment is based on Lipper, Bloomberg or Datastream.

25

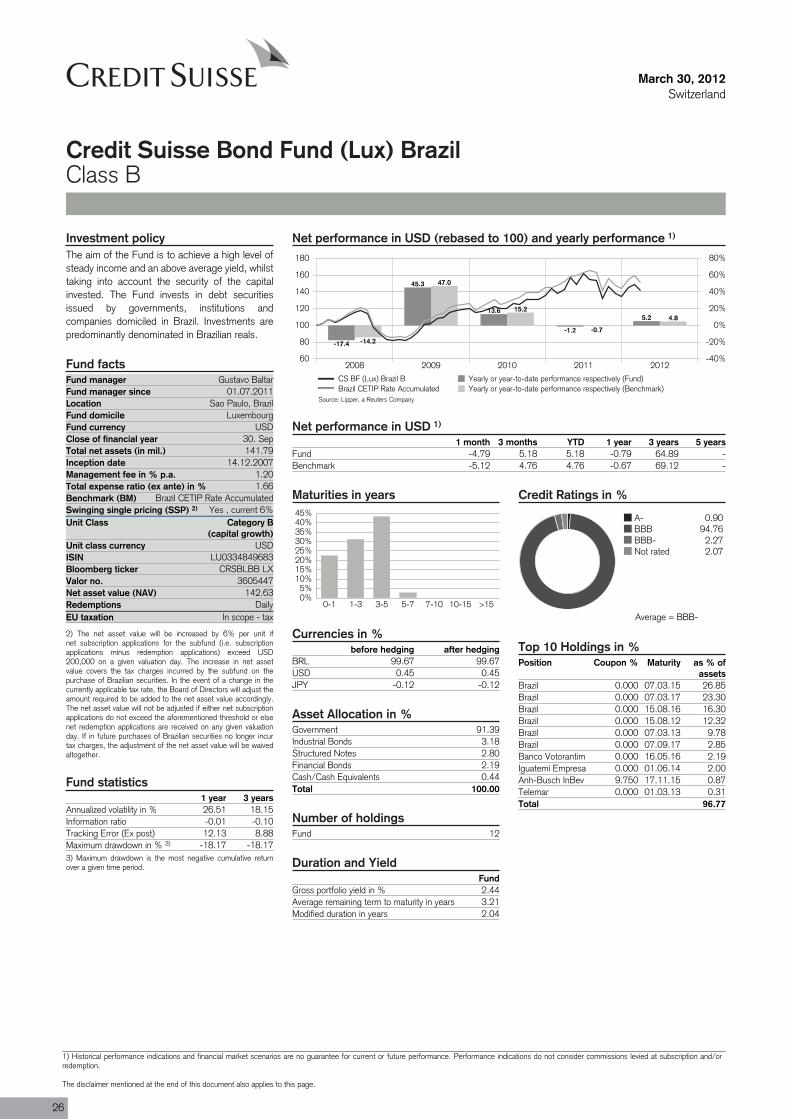

Fund 12

Fund manager Gustavo BaltarFund manager since 01.07.2011Location Sao Paulo, BrazilFund domicile LuxembourgFund currency USDClose of financial year 30. SepTotal net assets (in mil.) 141.79Inception date 14.12.2007Management fee in % p.a. 1.20Total expense ratio (ex ante) in % 1.66Benchmark (BM) Brazil CETIP Rate AccumulatedSwinging single pricing (SSP) 2) Yes , current 6%Unit Class Category B

(capital growth)

ISIN LU0334849683

Valor no. 3605447

Redemptions DailyEU taxation In scope - tax

March 30, 2012Switzerland

Credit Suisse Bond Fund (Lux) BrazilClass B

Net performance in USD (rebased to 100) and yearly performance 1)

2008 2009 2010 2011 201260

80

100

120

140

160

180

-40%

-20%

0%

20%

40%

60%

80%

-17.4

45.3

13.6

-1.2

5.2

-14.2

47.0

15.2

-0.7

4.8

CS BF (Lux) Brazil B Yearly or year-to-date performance respectively (Fund)Brazil CETIP Rate Accumulated Yearly or year-to-date performance respectively (Benchmark)

Net performance in USD 1)

1 month 3 months YTD 1 year 3 years 5 yearsFund -4.79 5.18 5.18 -0.79 64.89 -Benchmark -5.12 4.76 4.76 -0.67 69.12 -

Maturities in years

0%5%

10%15%20%25%30%35%40%45%

0-1 1-3 3-5 5-7 7-10 10-15 >15

Currencies in %before hedging after hedging

BRL 99.67 99.67USD 0.45 0.45JPY -0.12 -0.12

Asset Allocation in %Government 91.39Industrial Bonds 3.18Structured Notes 2.80Financial Bonds 2.19Cash/Cash Equivalents 0.44Total 100.00

Number of holdings

Duration and YieldFund

Gross portfolio yield in % 2.44Average remaining term to maturity in years 3.21Modified duration in years 2.04

Credit Ratings in %

A- 0.90BBB 94.76BBB- 2.27Not rated 2.07