16

Health & Beauty Sector Report

| Date post: | 10-Apr-2018 |

| Category: |

Documents |

| Upload: | nguyendien |

| View: | 216 times |

| Download: | 2 times |

Health & BeautySector Report

Introduction

As you would expect, Health & Beauty is a sector where appearances matter.

Many brands in this sector have traditionally taken a ‘catwalk glamour’ approach to in-store display, resulting in typically high unit costs.

Now, marketers are looking at ways to reduce costs, without compromising on quality. It’s a move that has seen many swap to alternative materials normally associated with temporary displays to deliver innovative in-store campaigns with real presence.

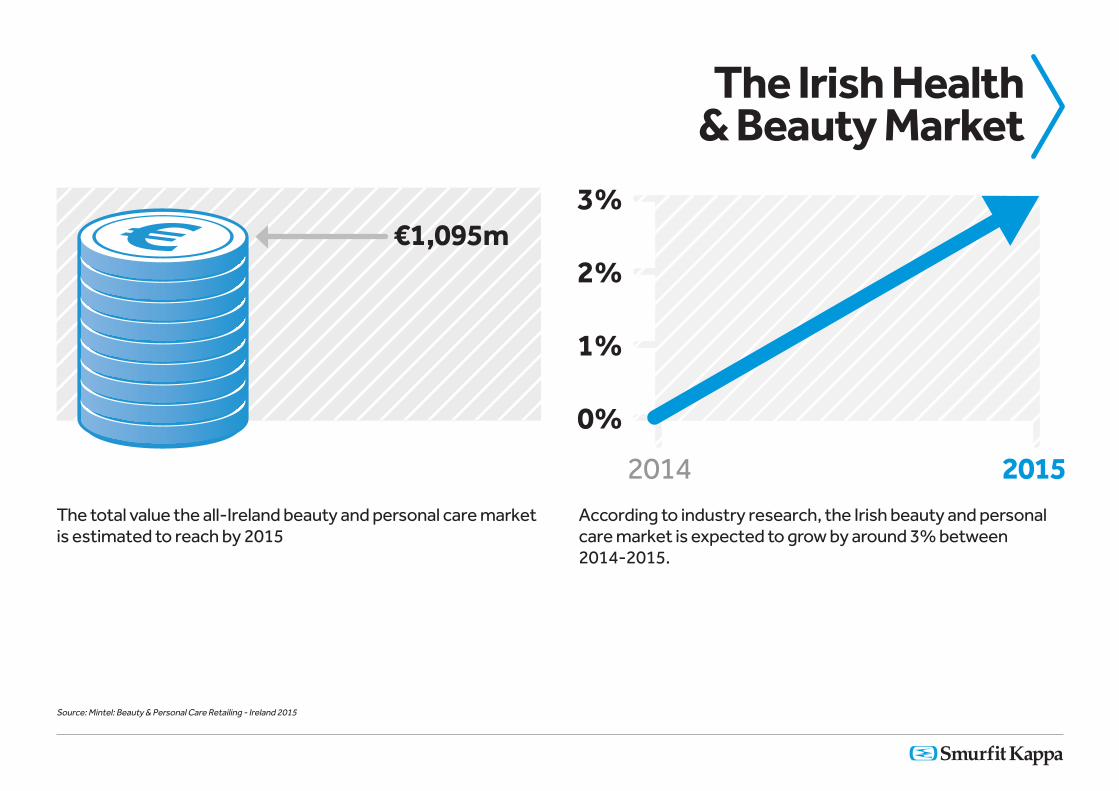

The Irish Health & Beauty Market

The total value the all-Ireland beauty and personal care market is estimated to reach by 2015

Source: Mintel: Beauty & Personal Care Retailing - Ireland 2015

According to industry research, the Irish beauty and personal care market is expected to grow by around 3% between 2014-2015.

€1,095m

0%

1%

2%

3%

2014 2015

The Irish Health & Beauty Market

Only a few small local players operating in the marketGlobal players continue to be the dominant force in the competitive environment, such as Procter & Gamble and L’Oréal.

Communicating value-for-money According to 2015 Euromonitor research, value remains important to Irish shoppers, but does not always mean the lowest price. Irish consumers want products which function properly and provide them with real value for money. Improvements in quality and packaging, for example within economy colour cosmetics, have led to a strong perception of these being as valuable as some of their mid-range counterparts.

Health & Beauty Shoppers

41% of global women agree they have different make up styles depending on whether it’s day or night

21% of shoppers claim to frequently experiment with new perfume/aftershaves.

67% of Irish shoppers use Boots to buy their beauty and personal care products

34% of Irish shoppers think premium own brand beauty product (e.g. Boots No.7) are better than value for money than premium/luxury brands

48% of Irish shoppers have bought beauty products from Tesco in the last 12 months

Source: Mintel: Men’s and Women’s Fragrance August 2014 Source: Mintel: Beauty & Personal Care Retailing - Ireland 2015

Health & Beauty Shoppers

Appealing to young, and oldIt’s not only the young who are concerned with looking and feeling good – 50+ shoppers are a key opportunity. However, understanding how younger audiences engage with digital in and out of the store, and how that impacts on the path to purchase is also key.

Male GroomingMale grooming has successfully moved into the mainstream. Taking pride in and taking greater confidence from maintaining a well groomed appearance is a message which is regularly used in the advertising of products targeting men. Rather than being a minority, men who buy grooming products to boost their self-esteem or feel more attractive are now in the majority

61% of Irish men have purchased beauty and personal care products from Boots in the last 12 months.

Source: Mintel: Beauty & Personal Care Retailing - Ireland 2015

Health & Beauty Shoppers

Innovation drives salesInnovation continues to be vital to the success of beauty and personal care. New product formulations are important to maintain consumer attention. There was a great deal of activity in hair care in 2014, with several brands launching their own dry shampoo ranges, e.g. Aussie, following on from the success of the Batiste brand. Other changes included the compressed range of male deodorants from Unilever, following the successful launch of their female counterparts.

Health & Beauty Shoppers

Natural preferenceAccording to research analysts at Mintel, Irish shoppers are keen to see more beauty ranges with natural ingredients. As a result, leading brands are looking to innovate across beauty and personal care sectors with a focus on botanical extracts as well as newer ingredients such as argan oil to appeal to skin-conscious shoppers.

“ You need shoppers to buy into brands and develop a connection with them on an emotional level. You need to sell a brand story to them and to demystify the product. With a combination of clear messaging, strong creative design and even choice of materials, P-O-P can prove key to achieving this, with or without the need for substantial above- the-line spend.”

Sustainability

The cosmetics sector is also renowned for its focus on ethical and sustainable practices, with many brands paying close attention to the materials and supply chain of custody that are involved within the production of P-O-P displays. As a result, leading brands are working with specialist producers, such as Smurfit Kappa Display to support their action in reducing the environmental impact through P-O-P and to advise on appropriate and sustainable designs.

“Givingapremiumfinishtotemporary P-O-P display means that it can sit comfortably within either its everyday category, or within the premium cosmetics and fragrances sector.”

Promotional Mechanics

FragranceDuring Mother’s Day 2015, retailers promoted heavily across product ranges deemed popular as gifts for women, such as fragrance.

In contrast, industry research shows a huge drop in the number of promotions in Fragrance between 2013 and 2014 over the Valentine’s Day promotional period. Between 31 January and 14 February 2013, Boots ran a total of 1867 fragrance promotions. In 2014, the retailer reduced its promotional activity by 73 per cent to only 498. 2014 saw Boots move away from Price Reduction promotions, but maintain its added value promotions, such as a free gift with purchase.

Some 42.6% of Boots promotions were Web only offers and the majority of these promotions offered a free gift when they purchased the product online. In addition to this 19.1% of Boots promotions were Purchase for a free product. The Perfume Shop was the only other retailer that used this strategy on Mother’s Day.

42.6%

73% Reduction

Promotion Activity

Web only offers

Promotional Mechanics

VitaminsThe most popular mechanics in the Health and Vitamins category over the last 2 years have been Multibuy promotions. However, research by BrandView shows that there has been a 40 per cent decrease in Multibuy offers used in the last twelve months, and a significant increase in Save Amount deals.

The key Multibuy mechanic used in the Health and Vitamins category is Buy 3 – Cheapest Free. Back in 2013, 3 for 2 accounted for 86 per cent of total promotions. Last year, this declined to 56 per cent.

As summer draws to a close, it seems an appropriate time to look at the Cold and Flu category, with promotions typically starting in September. Once again, 3 for 2 Mix and Match or Buy 3 – Cheapest Free promotions are commonplace.

86%56%

3 for 2 promotions

2013 2014

Key Trend

‘Me’-Tail:Beauty retail has seen a strong growth in personalised products recently, with shoppers drawn to the ‘just for me’ storylines and services.

Increasingly, a wider range of products across the Health & Beauty category are being created and positioned in a way to ‘personalise’ to each shoppers’ age, skin type, ethnicity, style.

As a result, in-store communication is beginning to focus less on the brand and more on the ‘value to me’, reflecting shoppers’ personality & lifestyle

The Me-Tail trend also translates to ‘Me Time’. Shoppers are purchasing products for different seasons, times of day and mood.

Success Tips

• Promote a seasonal approach to Health & Beauty to give shoppers a prompt to invest in a new summer/winter products and scents

• Create memorable experiences and ‘theatre’ for the shopper at fixture to promote a brand relationship rather than relying on discounts and price promotions

• Give shoppers the opportunity to trial cosmetics/host in-store workshops allowing them the chance to experience the products more fully

• Introduce the personal touch with services tailored to shoppers ‘likes’

• Assist the purchasing decision in-store and show shoppers how to ‘create the look’

• Ensure campaigns seamlessly integrate digital, above-the-line and in-store

• Shoppers attention is now much more distracted (e.g. focused on mobile devices) – P-O-P messages need to be quick and simple, relying more on visuals rather than text.

• Create the emotion and feeling of the brand through imaginative displays that deliver a sensory and inspiring retail experience

• Use high-end materials and finishes to clad onto more basic materials to reduce costs while still achieving a premium look and finish traditionally associated with Health & Beauty brands.

To f ind out more, get in touch with the Smurf it Kappa team on 014524333.

Smurfit Kappa DisplayUnit 17, Whitestown Industrial Estate, Tallaght, Dublin 24

www.smurfitkappadisplay.comwww.openthefuture.info