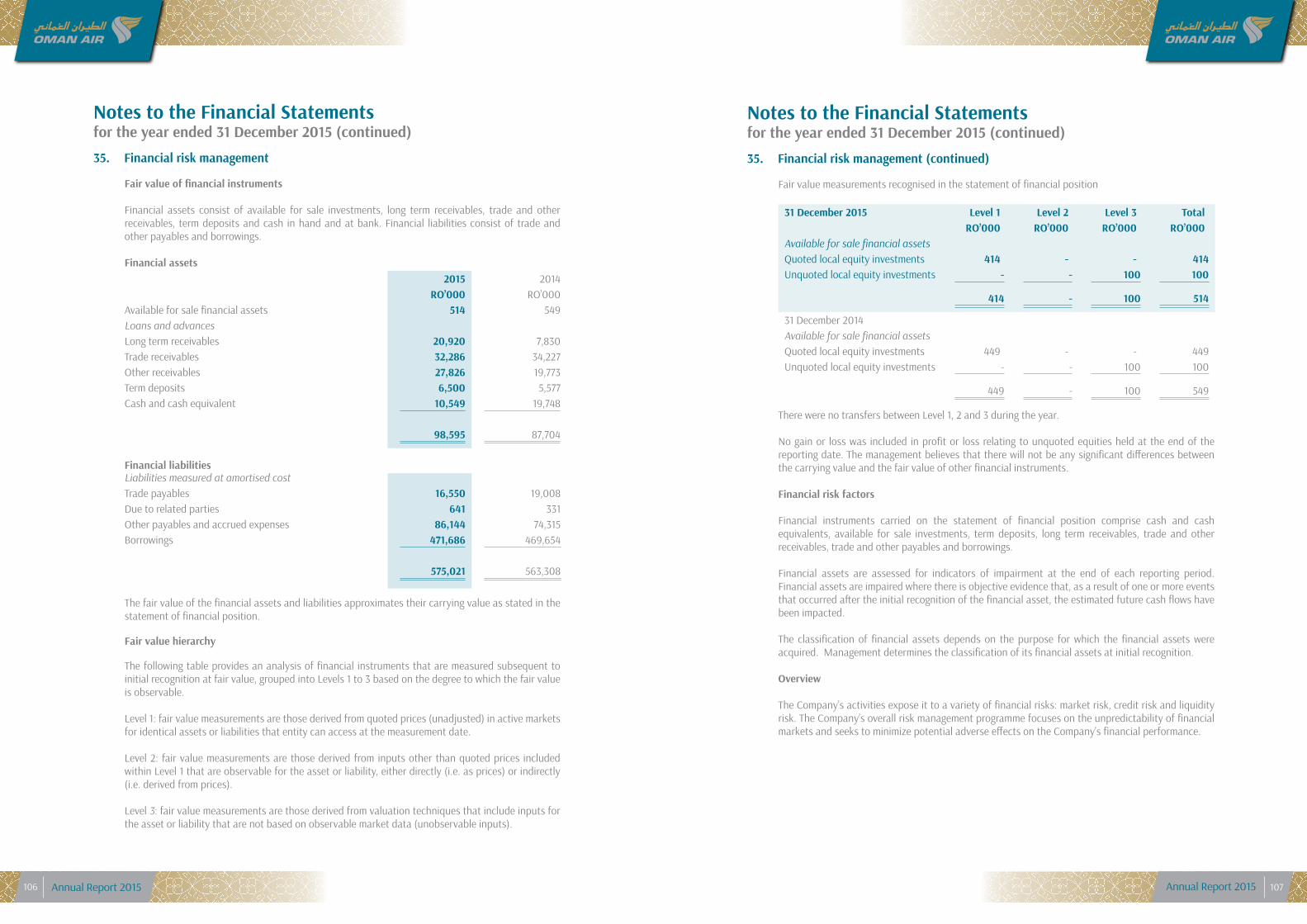

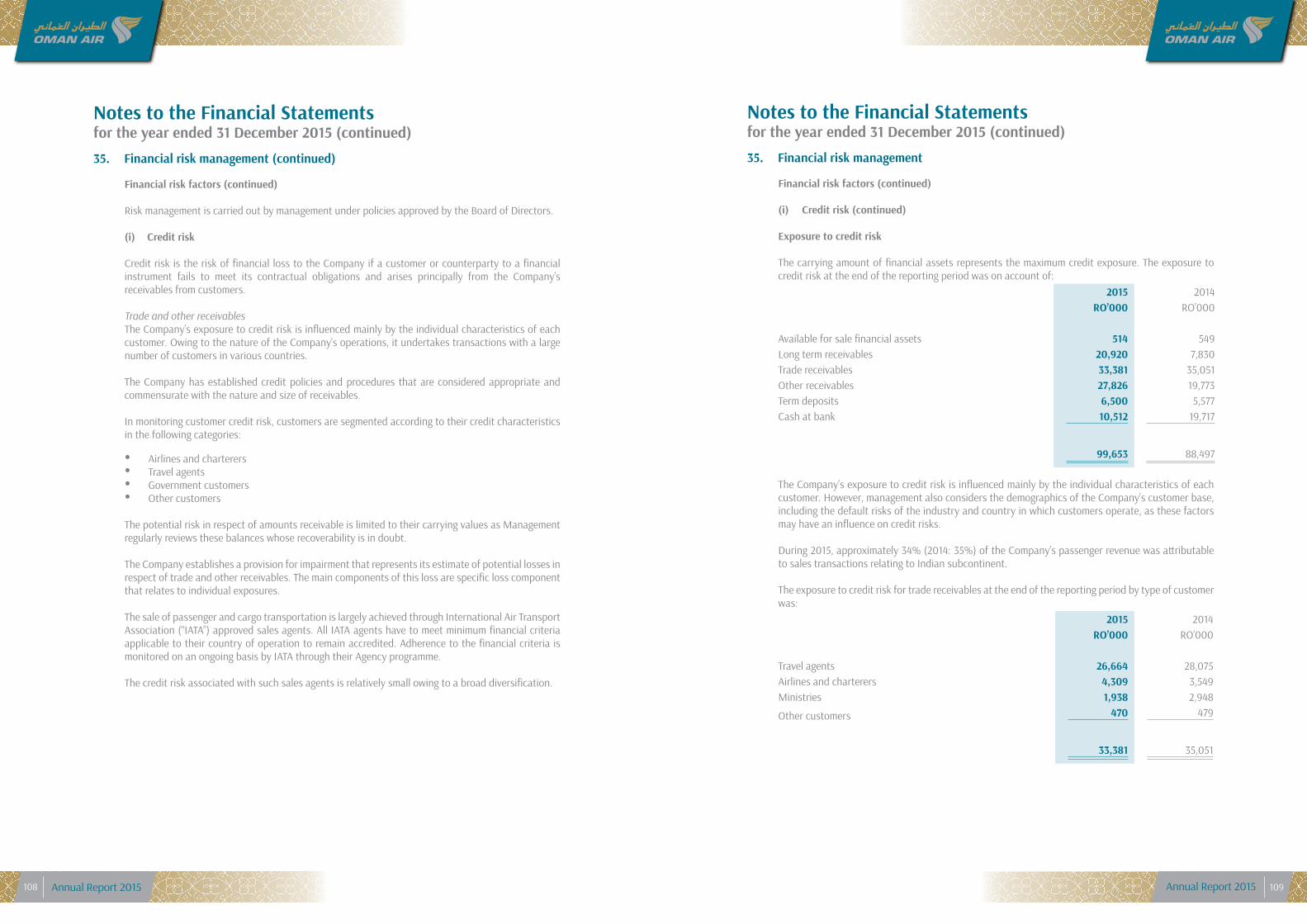

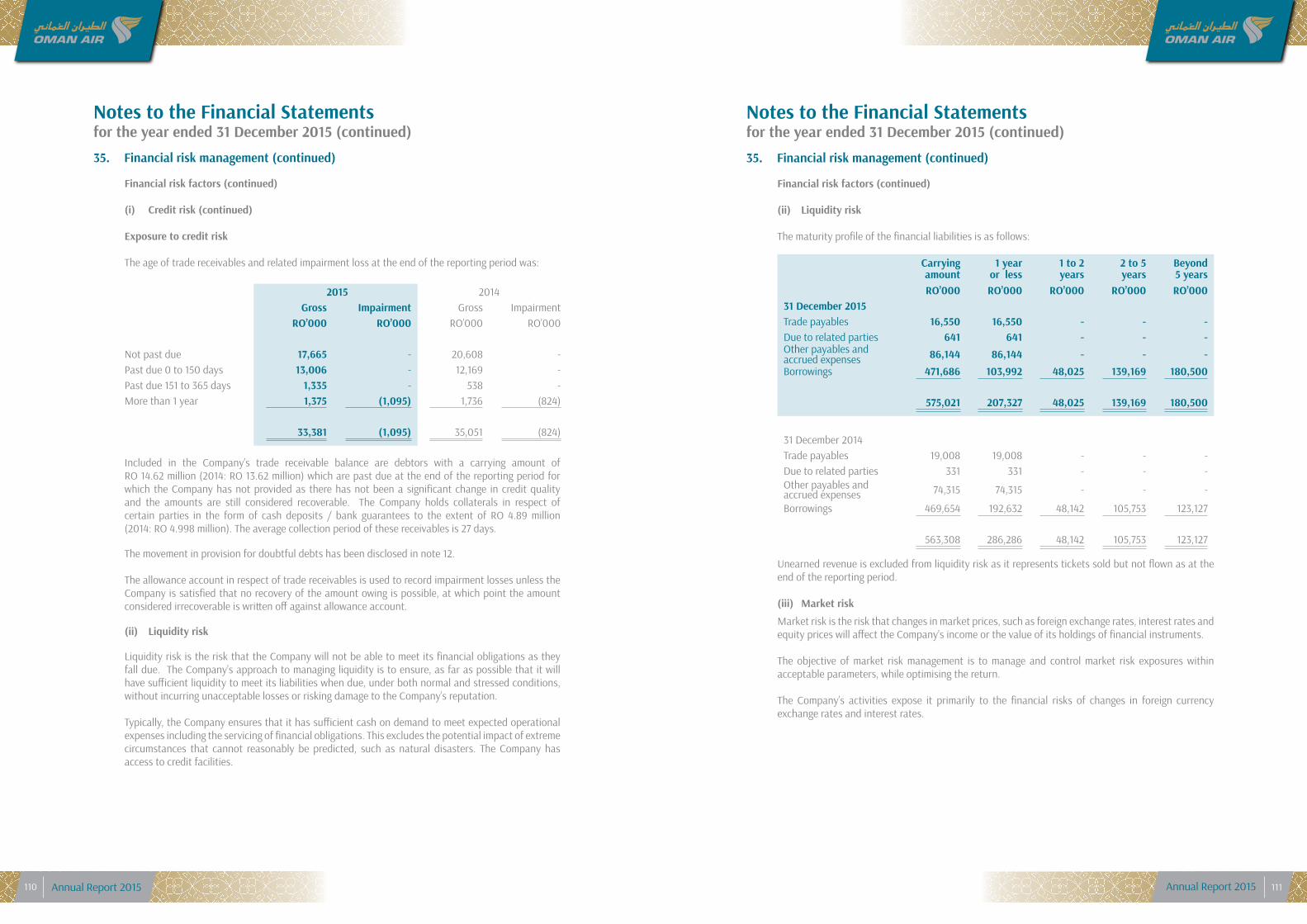

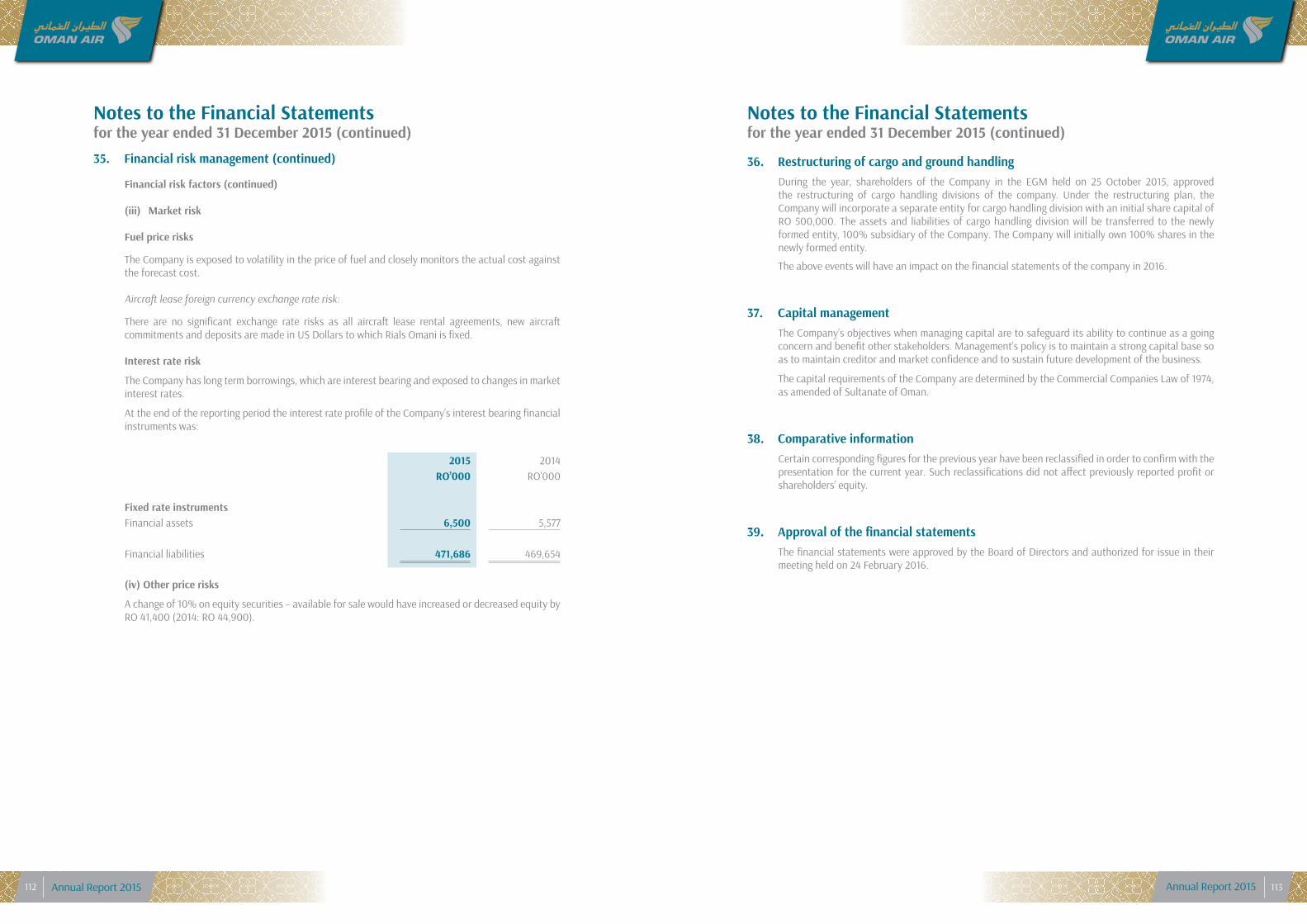

58

His Majesty Sultan Qaboos bin Said

As the Sultanate of Oman makes rapid strides forward in all spheres such as tourism, Oman Air has taken off on an ambitious growth strategy in our endeavour ‘To Become The Best’. It will see us expand our existing international network even further, increase the strength of our fleet, fly even more passengers to more destinations than ever before.

As a result, thousands of guests will have the opportunity to experienceOman Air’s award-winning services and the welcoming Omani hospitality.

As the national carrier, we will continue to strive harder to be the first choice airline and keep the Sultanate’s flag flying higher, as we continue our journey of excellence.

To Become The Best

Annual Report 2015 Annual Report 20154 5

ContentsOur Board of Directors …………………………………………………………. 08

Chairman’s Statement …………………………………………………………… 10

Chief Executive Officer’s Statement ………………………………………….... 14

Our Core Team…………………..……………………........................................ 18

Management Discussion and Analysis…………………..…………............… 40

Auditor’s Report on Corporate Governance…………………..……..............… 46

Corporate Governance Report…………………..…………………………........ 47

Auditor’s Report on Financial Statements…………………..……….............…. 52

Statement of Financial Position…………………..………………………........... 54

Statement of Comprehensive Income…………………..……………............… 55

Statement of Changes in Equity……….…………………..………….........…… 56

Statement of Cash Flows………………….…………………..……………….... 57

Notes to the Financial Statements………………….………………............…… 58

Annual Report 2015 Annual Report 20156 7

Our Board of Directors(Sitting from left to right)

H.E. Maitha bint Saif bin Majid Al MahruqiDeputy Chairman - Undersecretary of the Ministry of Tourism

H.E. Darwish bin Ismail bin Ali Al BulushiChairman of the Board - Minister Responsible for Financial Affairs

Major General Sulaiman bin Mohamed Al HarthyDirector - Assistant Inspector General of Police and Customsfor Administrative and Financial Affairs

H.E. Mohsin bin Khamis bin Ghulam Al BalushiDirector - Advisor of the Ministry of Commerce & Industry

(Standing from left to right)

Sheikh/Nasser bin Sulaiman bin Hamed Al HarthyDirector General of Investments, Ministry of Finance

Dr. Mohamed bin Ali bin Mohamed Al BarwaniDirector - Chairman, MB Holding

Eng. Ahmed bin Said bin Salim Al RawahiAdvisor to H.E. The Minister of Transport & Communicationsfor Civil Aviation Affairs

Mr. Vasudevan ThulasidasDirector - Aviation Expert (Advisor to the Board)

Annual Report 2015 Annual Report 20158 9

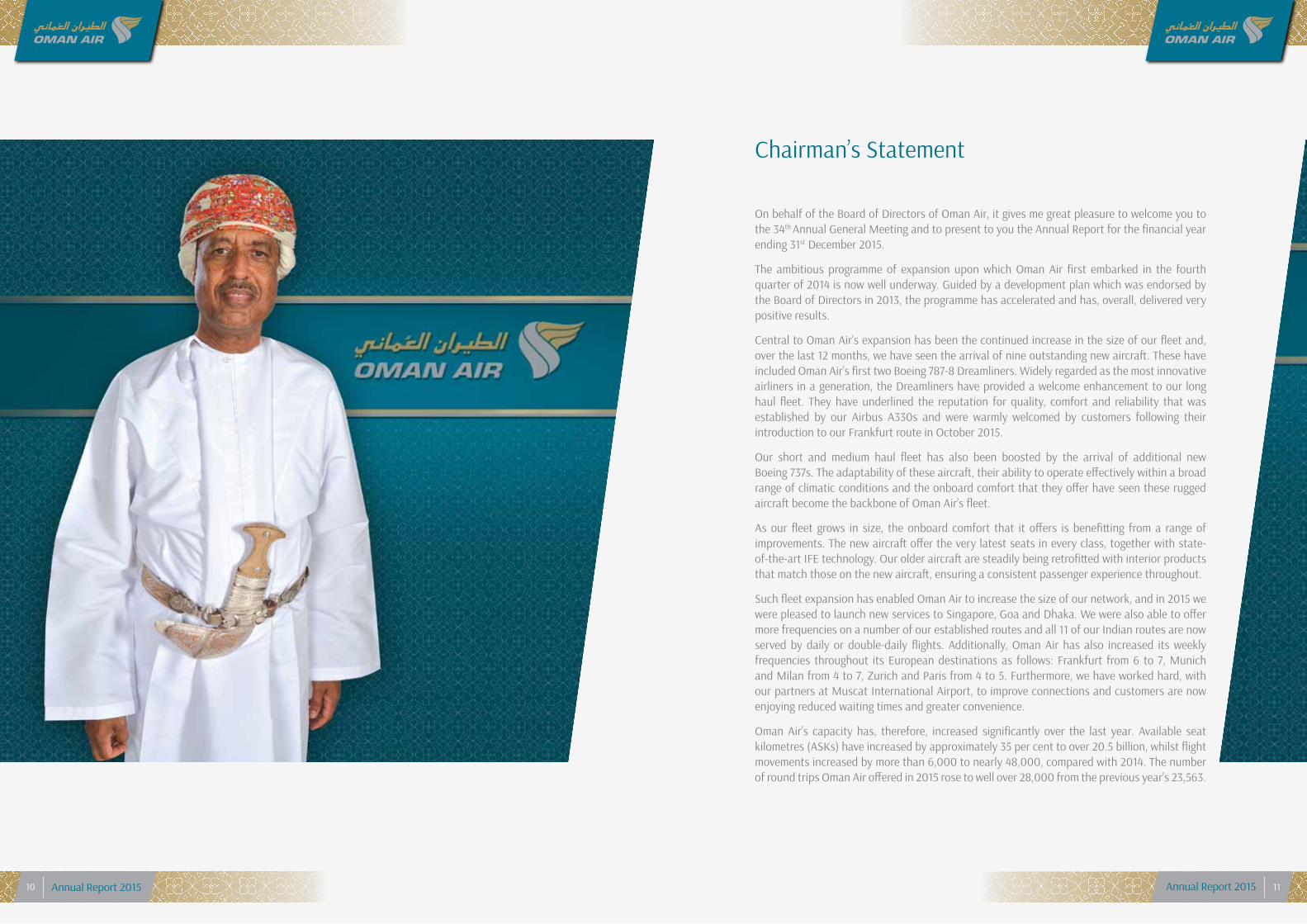

On behalf of the Board of Directors of Oman Air, it gives me great pleasure to welcome you to the 34th Annual General Meeting and to present to you the Annual Report for the financial year ending 31st December 2015.

The ambitious programme of expansion upon which Oman Air first embarked in the fourth quarter of 2014 is now well underway. Guided by a development plan which was endorsed by the Board of Directors in 2013, the programme has accelerated and has, overall, delivered very positive results.

Central to Oman Air’s expansion has been the continued increase in the size of our fleet and, over the last 12 months, we have seen the arrival of nine outstanding new aircraft. These have included Oman Air’s first two Boeing 787-8 Dreamliners. Widely regarded as the most innovative airliners in a generation, the Dreamliners have provided a welcome enhancement to our long haul fleet. They have underlined the reputation for quality, comfort and reliability that was established by our Airbus A330s and were warmly welcomed by customers following their introduction to our Frankfurt route in October 2015.

Our short and medium haul fleet has also been boosted by the arrival of additional new Boeing 737s. The adaptability of these aircraft, their ability to operate effectively within a broad range of climatic conditions and the onboard comfort that they offer have seen these rugged aircraft become the backbone of Oman Air’s fleet.

As our fleet grows in size, the onboard comfort that it offers is benefitting from a range of improvements. The new aircraft offer the very latest seats in every class, together with state-of-the-art IFE technology. Our older aircraft are steadily being retrofitted with interior products that match those on the new aircraft, ensuring a consistent passenger experience throughout.

Such fleet expansion has enabled Oman Air to increase the size of our network, and in 2015 we were pleased to launch new services to Singapore, Goa and Dhaka. We were also able to offer more frequencies on a number of our established routes and all 11 of our Indian routes are now served by daily or double-daily flights. Additionally, Oman Air has also increased its weekly frequencies throughout its European destinations as follows: Frankfurt from 6 to 7, Munich and Milan from 4 to 7, Zurich and Paris from 4 to 5. Furthermore, we have worked hard, with our partners at Muscat International Airport, to improve connections and customers are now enjoying reduced waiting times and greater convenience.

Oman Air’s capacity has, therefore, increased significantly over the last year. Available seat kilometres (ASKs) have increased by approximately 35 per cent to over 20.5 billion, whilst flight movements increased by more than 6,000 to nearly 48,000, compared with 2014. The number of round trips Oman Air offered in 2015 rose to well over 28,000 from the previous year’s 23,563.

Chairman’s Statement

Annual Report 2015 Annual Report 201510 11

I am pleased to inform you that, as a result of this enhanced capacity, Oman Air has experienced a major increase in the number of passengers we carried in 2015. More than 6.3 million customers flew with Oman Air in 2015, compared with just over 5.1 million in 2014. This growth is a major achievement which illustrates that our strategic planning is broadly producing the desired results.

I am also pleased to report that positive progress is being elsewhere within our company. The amount of cargo that Oman Air handled in 2015 increased from less than 125,000 tonnes to approaching 140,000 tonnes and our catering operation prepared nearly 900,000 more meals in 2015 than in 2014. Furthermore, extensive work continues to improve the efficiency and effectiveness of every area of our business.

Challenges remain, however. For example, net yield with respect to revenue per kilometre (RPK) fell by a little over 14 per cent across our network. Whilst this reflects the need for highly competitive price setting within the airline sector, together with our rapid growth in capacity, the situation is already stabilising. With continued work in this area, yields will in time exceed their previous level.

Oman Air does not, of course, operate in isolation and global economic changes can have a significant impact on our work. Significant among the changes witnessed in 2015 was the major drop in oil prices. This has affected Oman Air in two very different ways.

The fall in oil prices has been mirrored by a fall in aviation fuel prices. Accordingly, Oman Air has paid lower prices for our fuel, enabling us to reduce the company’s losses. This, together with the major increase in the number of passengers carried, the amount of cargo handled and the continued development of ancillary revenues, has put Oman Air on a positive financial footing in 2015. It gives me great satisfaction to announce that Oman Air’s revenues for the last financial year increased to OMR 465.971 million – a 14.1 per cent increase on 2014’s figures and a higher level than at any previous time in our history. In parallel, we have been able to reduce our losses for the second year in a row and by the end of 2015 they stood at OMR 86.333 million. This is a 21.2 per cent reduction compared with 2014.

There is, however, a darker side to the fall in oil prices, namely the impact on the economy of the Sultanate of Oman. Oman’s oil resources provide a vital income stream for the country and the fall in prices continues to have a significant effect on our exchequer. As the proud national airline of our country, we are determined to make the greatest possible contribution to Oman’s prosperity. I am therefore pleased to say that the level of support provided to Oman Air by the Government was reduced in 2015 to OMR 54 million. Furthermore, our increased revenues, continued expansion and lower financial loss have meant that we are able to request a further reduction in the level of financial support for the coming year. Oman Air remains on track to achieve its stated aim of reaching an operational break-even point by the end of 2017.

I am also pleased to say that Oman Air’s contribution to the Sultanate of Oman extends beyond the purely financial. We are committed to reflecting the rich culture and time-honoured heritage of Oman both at home and overseas and we play an instrumental role in promoting the Sultanate as a warmly hospitable destination for both business and leisure travellers. Furthermore, as one of the country’s largest employers, we continue to make an important investment in enhancing the skills, experience and capacity of Oman’s workforce. In 2015, we expanded our programme of recruiting Omani pilots, participated in a range of educational initiatives which aim to develop the Omani business leaders of the future and supported the growth of the Sultanate’s SME (small and medium sized enterprise) sector. Furthermore, in accordance with the decree issued by His Majesty Sultan Qaboos bin Said, we have reaffirmed Oman Air’s commitment to Omanisation. While we value our diverse and international workforce, we are also proud that by the end of 2015, 62.67 per cent of our employees are Omani citizens. As Oman Air continues to expand, we will do all in our power to increase this figure over the coming years.

The year 2015 was the first full year in which Oman Air’s Chief Executive Officer, Paul Gregorowitsch, has helmed the company. Having made an impressive start in the second half of 2014, Paul has continued to lead Oman Air with vigour, vision and clarity. His experience, expertise and organisational ability are transforming Oman Air, in terms of both its operational activity and its business culture. As a result, we are becoming a leaner, fitter and more effective company well-prepared for sustainable success. On behalf of the Board of Directors of Oman Air, I would like to thank him for his invaluable contribution.

I would also like to take this opportunity to thank my esteemed colleagues on the Board of Directors, the Executive Committee and the Audit Committee. They have provided essential support and advice to the management of Oman Air, helping to continue and expand Oman Air’s year-on-year success.

Finally, I would like to thank His Majesty Sultan Qaboos bin Said and his Government for their invaluable advice, timely encouragement and wise guidance. My colleagues on the Board and within Oman Air’s management join me in expressing our gratitude to His Majesty for his vision, his kind benevolence and his support.

Darwish bin Ismail bin Ali Al Bulushi Chairman, Oman Air

Annual Report 2015 Annual Report 201512 13

2015 was my first full year as the Chief Executive of Oman Air and it has been one of intensive activity on all fronts.

The year has been both challenging and rewarding. However, due to the hard work and commitment of each of the company’s 6,733 members of staff, Oman Air has been able to make significant progress on its journey ‘To Become the Best’. My gratitude goes to all for their invaluable contributions.

Guided by the vision of His Majesty Sultan Qaboos bin Said, the trust and confidence of our respected Board, and the leadership of our Chairman, Oman Air is spreading its wings further than ever before.

The highest quality of air travel has been provided for 6,365,780 guests during 2015 – an increase of more than 1.3 million guests compared with the previous year. The number of available seat kilometres increased in 2015 to 20,597 billion and the number of flight movements operated grew to nearly 48,000.

Such increases in Oman Air’s passenger services have only been possible as a result of the airline’s continued, ambitious fleet and network expansion programme. This was first launched in the fourth quarter of 2013, at which point the fleet strength stood at 30 aircraft. In 2015 alone, Oman Air has taken receipt of nine new aircraft and the airline remains on course to operate 70 aircraft by 2020.

Of the aircraft delivered in 2015, one was an Airbus 330-300, two were Boeing 737-800s, four were Boeing 737-900ERs and two were Boeing 787-8 Dreamliners. Each is a superb aircraft in its own right, but Oman Air’s first two Dreamliners are worthy of special note. They offer extraordinary levels of style and comfort for long haul passengers. Furthermore, their unique technology and innovative engineering have ensured that the aircraft has fast become an icon of 21st Century air travel. It was a proud moment for all at Oman Air when we saw our first Dreamliner take off for Salalah, before entering scheduled services to Frankfurt in October.

Chief Executive Officer’s Statement

Annual Report 2015 Annual Report 201514 15

The growing fleet has enabled the launch of some important new routes in 2015. On 29th March a new service was unveiled to the world-renowned leisure destination of Goa – the company’s 11th destination in India. Three days later Oman Air’s first flight to Singapore took off, signifying the start of a much-anticipated daily service. And on 26th October, a new service – Oman Air’s second to Bangladesh - was opened to Dhaka.

Frequencies on a number of established routes have also been increased. All Oman Air’s Indian destinations are now served by daily or double-daily services, following a very positive response from the Indian Government to the company’s proposals. A fifth weekly service to Paris has also been launched and work to introduce a second daily service to Heathrow will come to fruition in 2016.

Significant growth has also been reported in other areas of the business. Notable amongst these was the increase in cargo tonnage handled by Oman Air. The cargo operation has also benefitted from a Joint Venture that Oman Air agreed in April 2015 with Luxembourg-based full freighter specialist Cargolux.

Such expansion, together with the effects of the company’s intensive ‘Shape and Size’ efficiency programme, have had a healthy impact on Oman Air’s financial performance in 2015. Over the last year, the business has increased its total revenues by 14.1 per cent to OMR 465.971 million. The losses that have been made in 2015, largely the legacy of major investment in new aircraft, have been reduced by 21.2 per cent to OMR 86.333 million. As a result, the company has been able to request a significantly lower level of financial support from the Government of Oman for the forthcoming year.

Oman Air therefore remains on course to achieve an operational break-even point by the year end 2017, in line with the company’s agreed plan. At that time, the airline will be in a strong position to make an even greater contribution to the economic and social growth of our nation.

However, the rewards of expansion have not only been financial. Building on Oman Air’s record for winning international awards for the quality of our products and services, the company has been pleased to accept a number of prestigious accolades in 2015. These include ‘Best Airline Staff Service in the Middle East’ at the World Airline Awards, and ‘World’s Leading Airline Economy Class 2015’ and ‘World’s Leading Airport Lounge – Business Class 2015’ at the World Travel Awards. In addition, Oman Air won ‘Best Business Class Airline – Middle East’ at

the Business Destinations Travel Awards, four categories at the Oman Airports Management Company Second Annual Awards, and Corporate Social Responsibility Initiative of the Year at the Aviation Business Awards.

Finally, please allow me to express my highest appreciation and gratitude to all our valued customers for the confidence they have placed in Oman Air, and for their loyalty to the airline. By continuing to choose Oman Air, they will ensure that our company achieves its key aspirations: ‘To Become the Best’ and remain the ‘Airline of First Choice’.

Paul Gregorowitsch Chief Executive Officer

Annual Report 2015 Annual Report 201516 17

Our Core Team(Sitting from left to right) Japeen Shah – Chief Financial Officer

Abdulrahman Al Busaidy – Chief Operating Officer

Paul Gregorowitsch – Chief Executive Officer

Salim bin Mohammed Al Kindy – Chief Technical Officer

Captain Ali bin Hassan Sulaiman – Chief Officer Flight Operations

(Standing from left to right)

Eng. Abdulaziz bin Saud Al Raisi – Chief Officer Management Affairs

Sheikh Ahmed bin Himyar Al Nabhani – Chief Officer Support Services

Andrew Walsh – Chief Officer Service Delivery

Dr. Rashid bin Mohammed Al Ghailani – Chief Officer Human Resources

Mohammed bin Mubarak Al Shikely – General Marketing Manager

Annual Report 2015 Annual Report 201518 19

Oman Air’s contribution to the GDP of Oman

by

Well supported by Oman Air’s well-connected network, tourists visit the Sultanate of Oman to explore what our beautiful nation has to offer. From discovering the rich arts and crafts in the souqs of Oman to experiencing the cultural heritage and partaking in outdoor adventures like scuba diving, snorkelling and rock climbing, Oman delights the heart and senses.

By 2022, Oman Air’s overall contribution to the nation’s GDP is forecast to rise to OMR 1.1 billion. Meanwhile, the overall contribution of the travel and tourism sector to the GDP in Oman is expected to grow to OMR 1,762.2 million (5.8% of the GDP) in 2015 fromOMR 1,697.5 million (5.7% of the GDP) in 2014.

Tourism grows leaps and bounds

Om

ani R

ials

(In

Mill

ions

)

1100

1000

900

800

700

600

500

400

300

200

02011Year 2014 2022

420

1100

333

Annual Report 2015 Annual Report 201520 21

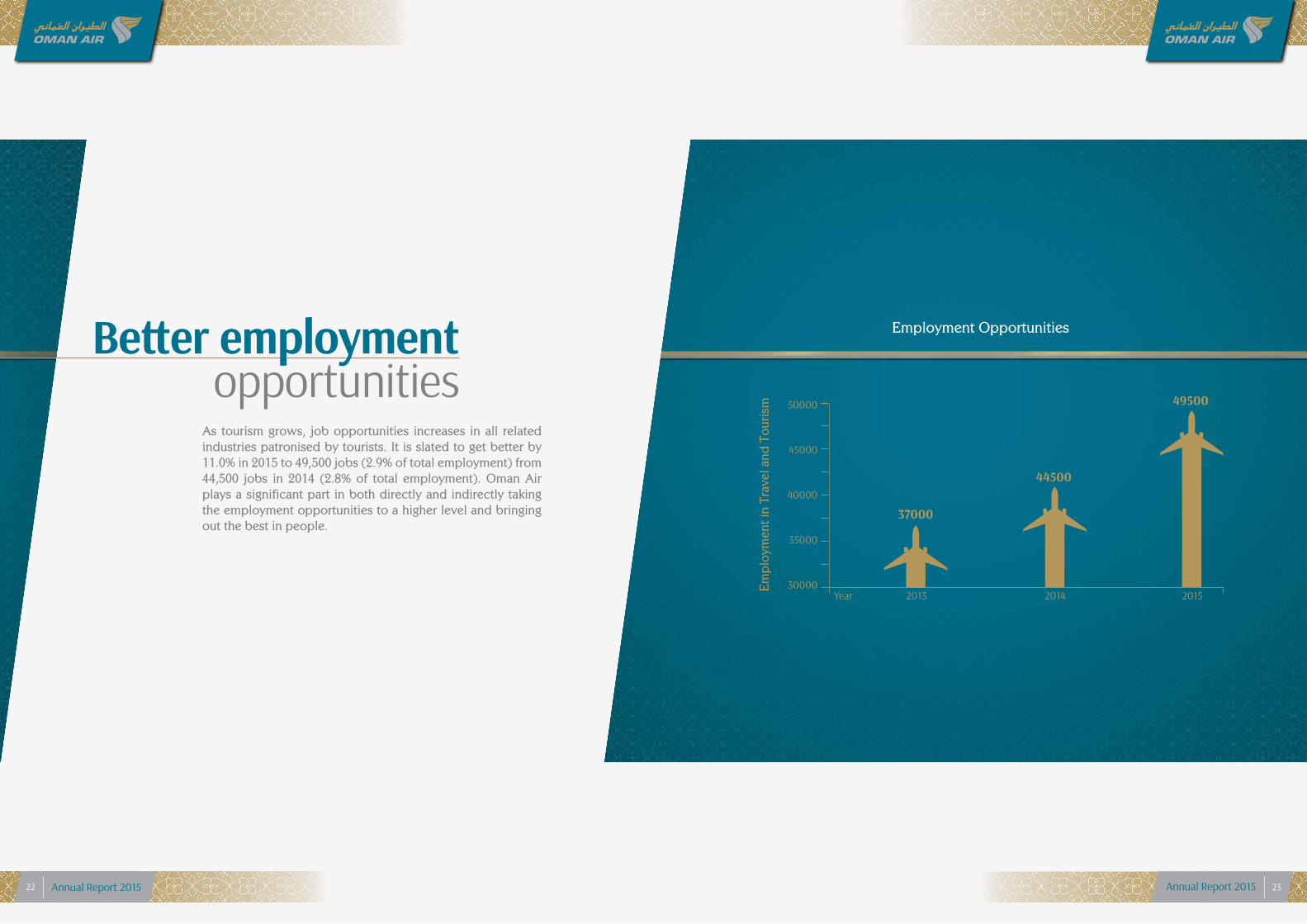

As tourism grows, job opportunities increases in all related industries patronised by tourists. It is slated to get better by 11.0% in 2015 to 49,500 jobs (2.9% of total employment) from 44,500 jobs in 2014 (2.8% of total employment). Oman Air plays a significant part in both directly and indirectly taking the employment opportunities to a higher level and bringing out the best in people.

opportunitiesBetter employment Employment Opportunities

Em

plo

ymen

t in

Trav

el a

nd T

ouri

sm

37000

44500

4950050000

45000

40000

35000

300002013Year 2014 2015

Annual Report 2015 Annual Report 201522 23

Investment in Travel and Tourism

As seen in many countries and cities, developing the infrastructure is extremely important for developing tourism and brings in long-term rewards.

In Oman, the investments were slated to rise by 10.3% toOMR 294.5 million in 2015 from OMR 267.0 million in 2014. New infrastructure investments increase, particularly around the expansion of the Muscat International Airport designed to handle 12 million passengers. Several mega tourism projects such as the Duqm frontier town and Ras Al Hadd development are taking shape.

This would change the course of tourism for the betterin the country.

the best rewardsInvestments bring out

Om

ani R

ials

(In

Mill

ions

) 267

294.5300

200

1002014Year 2015

Annual Report 2015 Annual Report 201524 25

According to the United Nations World Tourism Organisation (UNWTO) Travel Barometer, Oman is ranked among the top 17 of the world’s fastest growing tourism destinations, being the only GCC and Arab country to be listed. The number of tourist arrivals more than doubled in 2015 to around2.6 million from 891,000 tourist arrivals in 2005.

The increasing visitor spends on hotel stay, travelling, shopping and dining, benefits the national economy. Tourist spends were slated to grow by 6.0% in 2015 from OMR 743.8 million in 2014.

Oman Air is constantly expanding its network from over 45 international destinations, to bring in more people to experience all that Oman has to offer.

get even betterVisitor exports Visitor Exports

710.05

743.8

788.4800

780

760

740

720

700

680

660

640Year 2013

Om

ani R

ials

(In

Mill

ions

)

2014 2015

Annual Report 2015 Annual Report 201526 27

With the growth in tourism, passenger arrivals at Muscat International Airport stood at 5,212,769 while it was 498,810 at Salalah International Airport in 2015.

To cope with the rising demand, Oman has been witnessing rapid expansion works at the Muscat International Airport which is slated to be completed by the end of 2016.The opening of the Salalah International Airport in June brought special joy as an Oman Air flight touched down, followed by the Boeing 787-8 Dreamliner in October.

Striving harder to become the best, our Cargo Division launched their freighter services in association with Cargolux, one of the largest all-cargo airlines in Europe with a global network, registering a growth of 35% in tonnage.

passenger and cargo handling

Excelling in

Annual Report 2015 Annual Report 201528 29

We pay meticulous attention to every detail, right from on-time performance, spaciousness of our wide-bodied aircraft, comfortable business class seats to excellent cuisine and unmatched customer services - your satisfaction is our best reward. Indeed, our achievements drive us to work even harder to become the best.

global recognitionWinning

• ‘World’s Leading Airline Economy Class 2015’ and Oman Air’s lounge at the Muscat International Airport was also named ‘World’s Leading Airport Lounge – Business Class 2015’ at the World Travel Awards 2015

• ‘Middle East’s Leading Airline - Business Class’ and ‘Middle East’s Leading Airline – Economy Class’ at the World Travel Awards 2015

• ‘Best Airline Staff Service Middle East’ at the World Airline Awards

• Corporate Social Responsibility Initiative of the Year at the 9th Aviation Business Awards 2015

• Best Business Class Airline 2015 – Middle East at the Business Destinations Travel Awards

• Oman Air’s Business Class Seats awarded Chicago Athenaeum Museum’s ‘Good Design Award’

• Best Airline Operating to and from Chittagong by Bangladesh’s Bureau of Manpower, Employment and Training Centre

• Best International Airline 2015 at the North India Travel Awards

• Oman Air’s Inflight Magazine ‘Wings of Oman’ received ‘Best In-flight Magazine’ award at the World Marketing Congress, Mumbai, India 2015

• Oman Air’s Website omanair.com acclaimed as one of ‘The Best Airline Website Designs’, by leading international design magazine Onextrapixel

• 2nd place for being the ‘Best Arabian Airline’ at the ITB 2015 Go Asia Award

• One of the top five airlines by number of passengers carried at Muscat International Airport and one of the top three airlines at Salalah International Airport - Oman Airports Management Company Second Annual Awards 2015

Annual Report 2015 Annual Report 201530 31

Oman is gradually ascending several notches higher as a must visit place on the tourists list. Tourists from all over the world would like to experience first-hand the potpourri of delights that Oman has to offer from pristine beaches, majestic forts, natural springs, unending sand dunes and so much more.

Our footprints now span over 45 international destinations, connecting people, business and opportunities all over the world. We added new destinations of Singapore, Goa and Dhaka, offering our customers even more choice within our continually expanding network. On the domestic front, Oman Air continues its daily return flights from Muscat to Salalah, Khasab and Sohar.

even furtherSpreading our wings

Annual Report 2015 Annual Report 201532 33

AIRBUS A330-300 BOEING 737-900AIRBUS A330-200 BOEING 737-800 BOEING 737-700 EMBRAER 175

BOEING 787-8 DREAMLINER

The addition of two Boeing 787-8 Dreamliners is a dream come true for our passengers. It features Oman Air’s newly designed, spacious and comfortable Business Class and Economy Class cabins, which ensure a relaxing and enjoyable flight. In addition, it offers the latest inflight entertainment technology, inflight connectivity with WiFi and Mobile Phone services, delicious inflight dining and, of course, our world-renowned Omani hospitality. Our fleet strength now rises to 40 aircraft in 2015. We are all set to reach even greater heights of around 57 aircraft by the year 2018 and 70 by 2020.

in the skiesComfort

Annual Report 2015 Annual Report 201534 35

In keeping with the vision of His Majesty Sultan Qaboos bin Said, we continuously invest in local talent. Our drive to recruit Omani pilots is bearing fruit. 21 Omanis joined the Cadet Training Programme to be part of our journey to become the best. Following successful completion of their training, each new pilot will become an invaluable asset of the airline. They therefore represent an investment not just for Oman Air but for the future of Oman. Meanwhile, we have achieved 62.67% Omanisation during 2015.

in local talentBringing out the best

Annual Report 2015 Annual Report 201536 37

We strive to make a difference to society by supporting people with special needs, as well as encouraging small and medium-sized enterprises (SMEs). Our environment-friendly initiatives go down to our Boeing B787-8 Dreamliners that reduce fuel and noise levels on long haul flights. Moreover, we promote sporting activities from football and sailing to rally driving and golf and aim to keep the Sultanate’s flag flying high.

*Details provided are from published sources.

to the societyCommitment

Annual Report 2015 Annual Report 201538 39

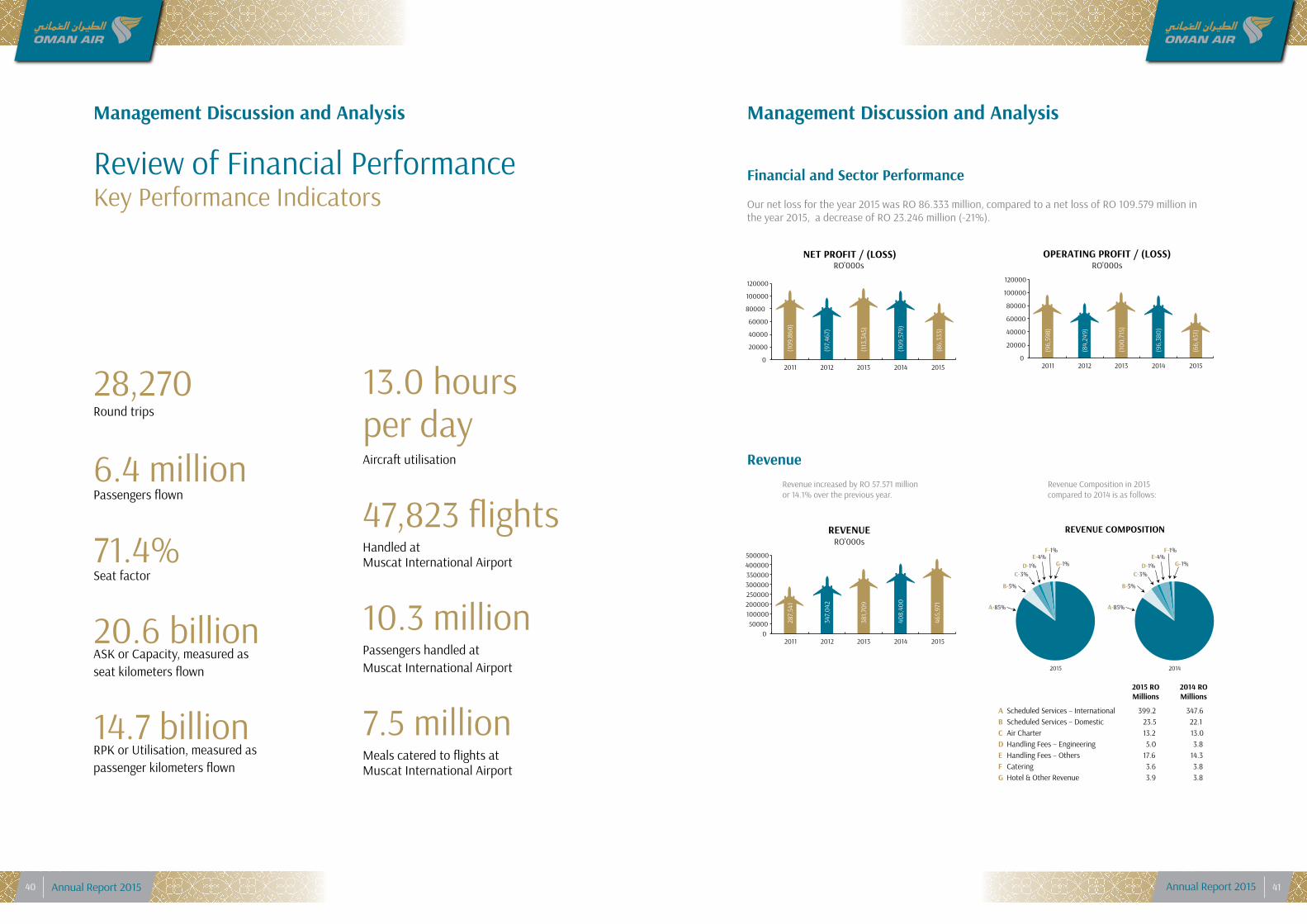

Review of Financial Performance Key Performance Indicators

28,270Round trips

6.4 millionPassengers flown

71.4%Seat factor

20.6 billionASK or Capacity, measured asseat kilometers flown

14.7 billionRPK or Utilisation, measured aspassenger kilometers flown

13.0 hours per dayAircraft utilisation

47,823 flights Handled at Muscat International Airport

10.3 millionPassengers handled at Muscat International Airport

7.5 millionMeals catered to flights at Muscat International Airport

Management Discussion and Analysis

Financial and Sector Performance

Our net loss for the year 2015 was RO 86.333 million, compared to a net loss of RO 109.579 million in the year 2015, a decrease of RO 23.246 million (-21%).

RevenueRevenue increased by RO 57.571 million or 14.1% over the previous year.

Revenue Composition in 2015 compared to 2014 is as follows:

Management Discussion and Analysis

287,

541

347,

042

381,7

09

408,

400

(66,

451)

(96,

598)

(84,

249)

(100

,715

)

(96,

380)

(86,

333)

NET PROFIT / (LOSS)RO'000s

RO'000sOPERATING PROFIT / (LOSS)

REVENUERO'000s

(109

,860

)

(97,

467)

(113

,345

)

(109

,579

)

0

20000

40000

60000

80000

100000

120000

20152011 2012 2013 2014

0

20000

40000

60000

80000

100000

120000

2015 2011 2012 2013 2014

465,

971

0 50000

100000 200000 250000 300000 350000 400000 500000

2015 2011 2012 2013 2014

287,

541

347,

042

381,7

09

408,

400

(66,

451)

(96,

598)

(84,

249)

(100

,715

)

(96,

380)

(86,

333)

NET PROFIT / (LOSS)RO'000s

RO'000sOPERATING PROFIT / (LOSS)

REVENUERO'000s

(109

,860

)

(97,

467)

(113

,345

)

(109

,579

)

0

20000

40000

60000

80000

100000

120000

20152011 2012 2013 2014

0

20000

40000

60000

80000

100000

120000

2015 2011 2012 2013 2014

465,

971

0 50000

100000 200000 250000 300000 350000 400000 500000

2015 2011 2012 2013 2014

287,

541

347,

042

381,7

09

408,

400

(66,

451)

(96,

598)

(84,

249)

(100

,715

)

(96,

380)

(86,

333)

NET PROFIT / (LOSS)RO'000s

RO'000sOPERATING PROFIT / (LOSS)

REVENUERO'000s

(109

,860

)

(97,

467)

(113

,345

)

(109

,579

)

0

20000

40000

60000

80000

100000

120000

20152011 2012 2013 2014

0

20000

40000

60000

80000

100000

120000

2015 2011 2012 2013 2014

465,

971

0 50000

100000 200000 250000 300000 350000 400000 500000

2015 2011 2012 2013 2014

REVENUE COMPOSITION

A Scheduled Services – International 399.2 347.6B Scheduled Services – Domestic 23.5 22.1C Air Charter 13.2 13.0D Handling Fees – Engineering 5.0 3.8E Handling Fees – Others 17.6 14.3F Catering 3.6 3.8G Hotel & Other Revenue 3.9 3.8

2015 ROMillions

2014 ROMillions

F-1%

A-85%

B-5%

C-3%D-1%

E-4%G-1%

2015

F-1%

A-85%

B-5%

C-3%D-1%

E-4%G-1%

2014

Annual Report 2015 Annual Report 201540 41

Scheduled ServicesScheduled services revenue rose from RO 369.7 million in 2014 to RO 422.7 million in 2015,up RO 53.0 million or 14.3%. During the year, Oman Air commenced operations to Goa, Singapore and Dhaka. Available Seat Capacity (ASK) increased by 35.2%. Utilization (RPK) increased by 29.7%, lower than increase in capacity resulting decline in average Seat Factor from 74.4% in 2014 to 71.4% in 2015. Average passenger yield decreased by 14.6%. Despite increasing competition from the major players, Oman Air has successfully established its presence on most of its routes. This has been achieved with continued focus on product, high frequencies, on-time performance, quick turnarounds, convenient flight timings, good connectivity and high standards of customer service both on the ground and in the air.

Air Charter ServicesAir charter services comprising of jet aircraft operations dedicated to Petroleum Development of Oman and Embraer aircraft operations dedicated to Occidental, Duqm and Sohar recorded revenue of RO 13.215 million in 2015.

Handling FeesHandling revenue from airlines other than Oman Air for the year was RO 17.610 million compared toRO 14.346 million in last year, an increase of RO 3.264 million or (+23%). This was mainly due to:

ss Airlines, other than Oman Air, increased their operations from 18,078 to 19,830 flights, (+10%)ss Wide body flight movement, other than Oman Air, increased from 3,134 to 3,754 flights, (+20%)

and narrow body flight movement increased from 14,944 to 16,076 flights, (+8%)

Management Discussion and Analysis Management Discussion and Analysis

15,2

33

47,8

23

138,

972

10,3

19

34,5

55

97,7

06

37,18

8

111,6

92

40,8

41

119,

785

41,4

50

124,

010

6,48

0

7,54

7

8,31

1

8,72

0

2015 2011 2012 2013 2014

PASSENGERSNo. of Passengers '000s

Flights Handled at Muscat International Airport

Passengers Handled at Muscat International Airport '000s

Cargo Tonnage Handled - Tonnes

2015 2011 2012 2013 2014

6,36

6

3,79

6

4,43

0

4,99

5

5,05

2

OPERATING METRICS

20,5

97

14,7

08

0

3000

8000

11000

17000

21000

20152011 2012 2013 2014

ASK (Millions) RPK (Millions) Seat Factor (%)

0%

25%

50%

75%

100% 71.4%

11,6

35

13,3

51

14,9

60

8,45

7

10,2

86

11,3

30

11,3

36

72.7% 77.0% 75.7% 74.4%

15,2

33

47,8

23

138,

972

10,3

19

34,5

55

97,7

06

37,18

8

111,6

92

40,8

41

119,

785

41,4

50

124,

010

6,48

0

7,54

7

8,31

1

8,72

0

2015 2011 2012 2013 2014

PASSENGERSNo. of Passengers '000s

Flights Handled at Muscat International Airport

Passengers Handled at Muscat International Airport '000s

Cargo Tonnage Handled - Tonnes

2015 2011 2012 2013 2014

6,36

6

3,79

6

4,43

0

4,99

5

5,05

2

OPERATING METRICS

20,5

97

14,7

08

0

3000

8000

11000

17000

21000

20152011 2012 2013 2014

ASK (Millions) RPK (Millions) Seat Factor (%)

0%

25%

50%

75%

100% 71.4%

11,6

35

13,3

51

14,9

60

8,45

7

10,2

86

11,3

30

11,3

36

72.7% 77.0% 75.7% 74.4%

Catering

Catering revenue from airlines other than Oman Air for the year was RO 3.615 million, decrease of RO 192,000 or (-5%) over the previous year’s revenue of RO 3.807 million.

Rooms, Food and Beverage Revenue

Revenue for the year was RO 3.268 million, an increase of RO 0.271 million or 9% over the previous year’s revenue of RO 2.997 million, owing to higher internal occupancy by Oman Air.

7,54

3

2015

5,07

7

6,03

8

6,45

6

6,65

0

2011 2012 2013 2014

Meals upli�ed at Muscat International AirportNo. of Meals '000s

Note: Above includes, meal upli�ed for Oman Air

64,6

05

43,0

28

64,7

82

43,7

39

64,6

05

54,10

7

64,6

05

53,16

3

64,6

05

47,3

87

66.6% 67.5% 83.8% 82.3% 73.3%

0

10000

20000

30000

40000

50000

60000

70000

2011 2012 2013 2014 2015

Total Available Rooms

Total Occupied Rooms Occupancy Ratio (%)

0%

25%

50%

75%

100%

7,54

3

2015

5,07

7

6,03

8

6,45

6

6,65

0

2011 2012 2013 2014

Meals upli�ed at Muscat International AirportNo. of Meals '000s

Note: Above includes, meal upli�ed for Oman Air

64,6

05

43,0

28

64,7

82

43,7

39

64,6

05

54,10

7

64,6

05

53,16

3

64,6

05

47,3

87

66.6% 67.5% 83.8% 82.3% 73.3%

0

10000

20000

30000

40000

50000

60000

70000

2011 2012 2013 2014 2015

Total Available Rooms

Total Occupied Rooms Occupancy Ratio (%)

0%

25%

50%

75%

100%

Annual Report 2015 Annual Report 201542 43

Expenditure

Net Expenditure increased by 5% from RO 504.780 million to RO 532.422 million.

Our Fuel cost decreased by RO 38.8 million or 24% mainly due to decrease in Fuel Price. The average network fuel price was 1.74 USD/USG compared to 2.90 USD/USG in the previous year, down (-40%).

Maintenance costs and other aircraft operating expenses comprising of handling, landing, navigation, crew layover and simulator cost increased due to the increase in operations in comparison with the previous year.

Passenger related cost increased by RO 6.0 million or 15% compared to 26% increase in passenger traffic in 2015, due to increase in passenger meal cost, reservation cost and passenger service cost.

Our employee cost increased by RO 16.3 million or 14% compared to last year mainly due to increase in staff strength. The Company’s manpower increased from 6,322 in 2014 to 6,778 in 2015, up 7%. During the year, the increase in manpower was restricted to critical operational requirements to support the increase in operations and to positions that would add value in terms of enhanced customer service, productivity and profitability.

Depreciation increased by RO 8.8 million or 30% compared to last year, due to increase in fleet strength.

Impairment cost comprising of impairment of goodwill paid for acquisition of Hotel Golden Tulip, Seeb.

Concession Fee

The Company pays a concession fee to Oman Airport Management Company, the airport operator at Muscat and Salalah airports. The Company pays concession fee on its ground handling, cargo handling and catering revenue. The impact of the concession fee in 2015 was RO 1.733 million as against RO 1.290 million in 2014.

384,

139

431,2

91

482,

424

504,

780

2011 2012 2013 2014

EXPENDITURERO '000s

532,

422

2015

A-7%

B-23%

2015 2014

C-12%

D-9%E-9%

F-7%

G-1%

H-25%

I-7%

COMPOSITION OF EXPENDITURE

Expenditure composition in 2015 compared to 2014 is as follows:

A Operating lease rentals on aircra� 36.0 29.1B Fuel cost 122.8 161.6C Other aircra� operating expenses 64.2 52.6D Maintenance cost 45.7 38.0E Passenger related cost 46.8 40.8

2015 ROMillion

2014 ROMillion

F Depreciation 38.5 29.7G Catering materials consumed 5.8 6.1H Employee cost 131.2 114.9I Others (Including insurance and impairment of goodwill) 41.4 32.0

2015 ROMillion

2014 ROMillion

A-6%

B-32%

C-10%D-8%

E-8%

F-6%

G-1%

H-23%

I-6%

Management Discussion and Analysis Management Discussion and Analysis

Financial Position

Non-current assets decreased from RO 650.263 million in December 2014 to RO 633.292 millionin December 2015 mainly on account of sale and lease back of five B737, during the year. Apart from this,the increase is on account of security deposit paid in respect of aircraft taken on operating lease.

During the year, the Government of Oman contributed RO 54 million, reaffirming their support.

Non-current liabilities increased by RO 104.955 million as at 31 December 2015, compared to 2014 mainly on account of long term loans availed for purchase of two B787 aircraft in Q4 2015. Current liabilities decreased by RO 85.764 million as at 31 December 2015, primarily attributable to reclassification of pre-delivery payments of aircraft payable within one year.

Current assets increased by RO 3.794 million as at 31 December 2015, as it includes two ATR aircraft classified as held for sale based on Board resolution.

Internal ControlsThe Company has an adequate internal control system commensurate with its size and the nature of its business. The Internal Audit department continues to maintain its focus on internal controls in all critical activities. Further, Statutory audit, State audit and the Audit Committee augment review of internal controls within the Company. During 2015, no material lapse or weakness in controls has been identified.

The People of Oman AirWith its development as an airline of stature internationally, Oman Air has also become an employer of choice, offering premium employment and career development opportunities to a wide cross section of people.

In keeping with the national initiative that seeks to enhance job opportunities for Omani nationals, the airline prioritizes job offers to Omani nationals possessing the requisite skills.

The Company staff strength at 31 December 2015 was 6,778 employees. Oman Air achieved an Omanisation ratio of 62.67%, without compromise on the quality of service provided to customers. This is a significant achievement considering the fact that the airline requires staff with multi-linguistic skills to serve a wide spectrum of customers across the network.

Career Development Path programmes have been successfully implemented across key functions and responsibilities in all departments, and staffs are undergoing external and internal programmes to improve their skill sets.

5,37

5

5,56

2

5,83

1

6,32

2

2011 2012 2013 2014

65% 66% 64% 59%

6,77

8

0

1000

2000

3000

4000

5000

6000

7000

2015

MANPOWER STRENGTH AND OMANISATION RATIO

* As per Ministry of Manpower

0%

20%

40%

60%

80% 62.67%*

Annual Report 2015 Annual Report 201544 45

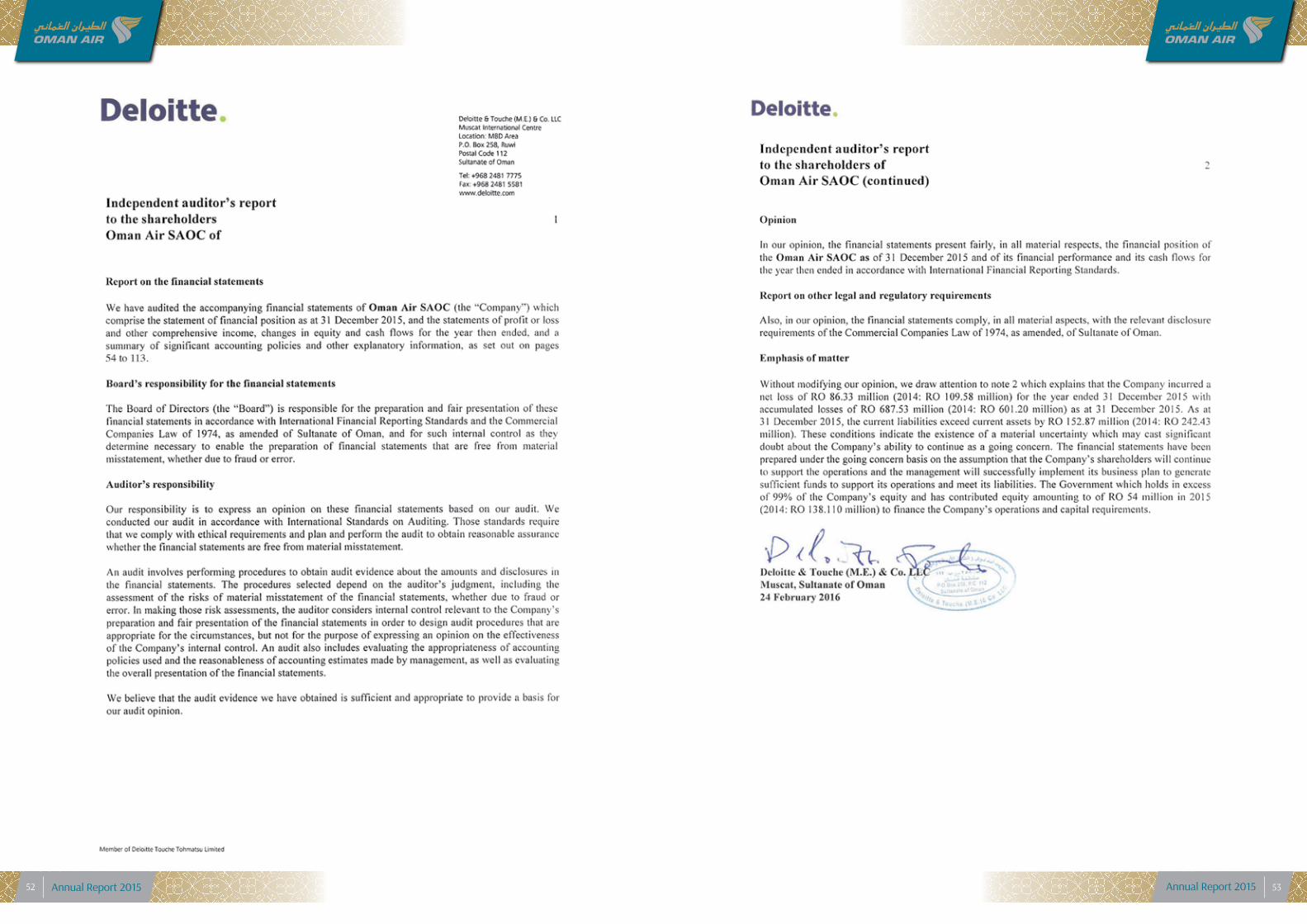

In accordance with the Capital Market Authority (“CMA”) circular # 11/2002 dated 3 June 2002, we are pleased to present the fourteenth Corporate Governance Report of Oman Air (SAOC) (“the Company”) for the year ended 31 December 2015.

Corporate Governance is mandatory for all the public companies listed in Muscat Securities Market (MSM). The Company is a closed Omani joint stock company (SAOC) and therefore is not required to comply with CMA circular stated above. However, the Board is adopting this circular as a best corporate governance practice to ensure high levels of transparency and accountability in its conduct of business.

The Auditors have performed the procedures prescribed in the Capital Market Authority Circular No. 16/2003 dated 29 December 2003 with respect to the Corporate Governance Report of the Company and its application of the Corporate Governance practices in accordance with the CMA Code of Corporate Governance issued under Circular No. 11/2002 dated 3 June 2002, and its amendments.

Company’s Philosophy

The Company has and will continue to uphold the highest standards of corporate governance. The Company’s focus has been on best business practices that are ethical and fair while achieving ultimate objective of enhancing long term shareholder value. Appropriate systems and procedures are continuously developed to evaluate and monitor the Company’s processes and performance to ensure they meet high standards of corporate governance.

Board of Directors

The Company’s Board comprises of eight Non-Executive and Non-Independent Directors. Seven Directors are appointed by the cabinet of ministers; six of them, including the Chairman represent the Government’s shareholding and one businessman to represent the private sector. The Government Nominees are Ministers, Undersecretaries and Directors in the Government undertakings. The eighth member has been appointed by the Board as a member and advisor to the Board with relevant airline industry background.

Functions of the Board

The Board appoints all members of the Executive Management (Chief Executive Officer and his direct reports) and decides their remuneration. The Board approves business plans and financial policies of the Company. The Board reviews policies and regulations governing company activities and specifies authorities and responsibilities of key management members. The Board reviews the Company’s long term and yearly financial plans and key objectives. The Company’s performance is reported to the Board on monthly basis and the same is reviewed and discussed in the Board meetings.

The Board appoints sub-committees including audit committee and evaluates their functions and performance. The Disclosure policy of the Company, which is in line with the Code of Corporate Governance, has been approved by the Board and implemented. The Board reviews the risk management strategy implemented by the Management to ensure that the major risks faced by the Company are adequately mitigated and the processes are in place to maintain Integrity of the financial statements, compliance with law and internal control systems. The Board approves the quarterly, half yearly and annual financial statements. The Board reports to the shareholders, through the annual report, about the going concern status of the Company, with supporting assumptions.

Corporate Governance Report

Annual Report 2015 Annual Report 201546 47

Remuneration - Top Fourteen Executives

Total(RO Per Annum)

Salary 1,447,739.828

Allowances 358,124.90

PASI/ESB 71,176.34

Total 1,877,041.068

Note: Top fourteen executives include CEO and Chief Officers.

Executive Committee

At present the Executive Committee carries out specific functions delegated by the Board of Directors. These functions include, review of budget proposals, review of management proposals concerning new routes, fleet rationalization and new ventures.

Objective of the Executive Committee is to conduct an in-depth review of specific issues before the same are approved by the Board.

During 2015 the Executive Committee members consisted of four Non-Executive and Non-Independent Directors and one member is appointed by the Board of Directors as a member and advisor with relevant airline industry background. Six meetings were held during 2015.

Audit Committee

During 2015 the Audit Committee members consisted of three Non-Executive and Non-Independent Directors. Four meetings were held during 2015 to discuss issues concerning Internal Control, Internal Audit plans and Internal / External Audit reports, quarterly financial statements and other related issues.

Audit and Internal Control

The Audit Committee has reviewed, on behalf of the Board, the effectiveness of the internal controls by meeting the internal auditor, reviewing the internal audit reports and recommendations, meeting the external auditor, reviewing the audit findings and the external audit management letter. The Audit Committee and the Board are pleased to inform the shareholders that reasonable internal control / systems are in place and that there are no significant concerns.

Means of Communication with the Shareholders and Investors

The complete quarterly results are also mailed to any shareholder upon written request, and are also available for inspection at the Company’s registered office. The Company produces comprehensive annual report for its shareholders. Audited annual financial statements with the Chairman’s report are sent by mail to each shareholder.

At the same time the Company gives press releases from time to time for all strategic issues, such as opening of new routes, change in fleet, financing agreements, etc. The Company also has its own website where airline related information is available.

Corporate Governance Report

Process of Nomination of the Directors

Seven members including Chairman of the Board are appointed by the Government and one member is appointed by the Board of Directors as a member and advisor with relevant airline industry background.

Entity Represented by Non-Independent Directors

There are six Non-Executive and Non-Independent Directors representing the Government of Sultanate of Oman’s Shareholding in the Company and one director representing the private sector.

Board Meeting Number and Dates

Board Meeting No. Board Meeting Date1 18/01/2015

2 08/02/2015

3 08/03/2015

4 29/04/2015

5 21/06/2015

6 09/09/2015

7 29/09/2015

8 11/11/2015

9 20/12/2015

There have been no material related party transactions between the Company and its directors. Specific related party transactions are disclosed to the shareholders at the ordinary general meeting.

Remuneration Matters

All directors including Chairman are Non-Executive and do not draw any fixed salary from the Company except one director who has been appointed as a member and advisor to the Board with relevant industry background, who is paid retainer fees as per terms of contract.

The total remuneration paid to the Board of Directors as sitting fees for financial year 2015 was RO 29,500 for Board meetings, RO 6,000 for Executive Committee meetings and RO 3,500 for Audit Committee meetings.

Each employee of the Company draws salary based on ‘job group’ assigned to his job. Job groups are assigned to different jobs based on the duties, responsibilities, skills and experience relevant to such jobs.

Corporate Governance Report

Annual Report 2015 Annual Report 201548 49

Acknowledgement by the Board of Directors

The Board of Directors acknowledges:

• Thatthefinancialstatementspreparedbythemanagementareinaccordancewiththeapplicablestandardsand rules applicable in the Sultanate of Oman.

• ThereviewoftheefficiencyandadequacyofinternalcontrolsystemoftheCompanyandcompliancewithinternal rules and regulations.

• ThattherearenomaterialthingsthataffectthecontinuationoftheCompanyanditsabilitytocontinueits operations during the next financial year.

Darwish bin Ismail bin Ali Al BulushiChairman, Oman Air

Corporate Governance Report

Market Price Data

Due to change in the status of the Company from General Omani Joint Stock Company (SAOG) to Closed Omani Joint Stock Company (SAOC), Oman Air shares are traded in the parallel third market ofMuscat Securities Market effective May 2007. Hence, market price data is not available.

Distribution of Shareholding

The major shareholders of the Company are as follows, with the Government of Sultanate of Oman being the major shareholder.

Major Shareholders

Name of the shareholder No. of Shares held Shareholding %

The Government of Sultanate of Oman 683,663,285 99.92773

Specific Areas of Non-compliance with the Provisions of Corporate Governance

There are no specific areas of non-compliance, except individual cases which are currently handled by the competent authorities.

Professional Profile of the Statutory Auditor

About Deloitte:Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 220,000 professionals are committed to making an impact that matters.

About Deloitte & Touche (M.E.)Deloitte & Touche (M.E.) is a member firm of Deloitte Touche Tohmatsu Limited (DTTL) and is a leading professional services firm established in the Middle East region with uninterrupted presence since 1926.

Deloitte provides audit, tax, consulting, and financial advisory services through 26 offices in 15 countries with more than 3,300 partners, directors and staff. It is a Tier 1 Tax advisor in the GCC region since 2010 (according to the International Tax Review World Tax Rankings). It has also received numerous awards in the last few years which include best employer in the Middle East, best consulting firm, the Middle East Training & Development Excellence Award by the Institute of Chartered Accountants in England and Wales (ICAEW), as well as the best CSR integrated organization.

The audit fee for the year 2015 is RO 23,500 plus out of pocket expenses.

Corporate Governance Report

Annual Report 2015 Annual Report 201550 51

Annual Report 2015 Annual Report 201552 53

Statement of Financial Position

at 31 December 2015Notes 31 December

201531 December

20141 January

2014ASSETS RO’000 RO’000 RO’000Non-current assets (Restated) (Restated)

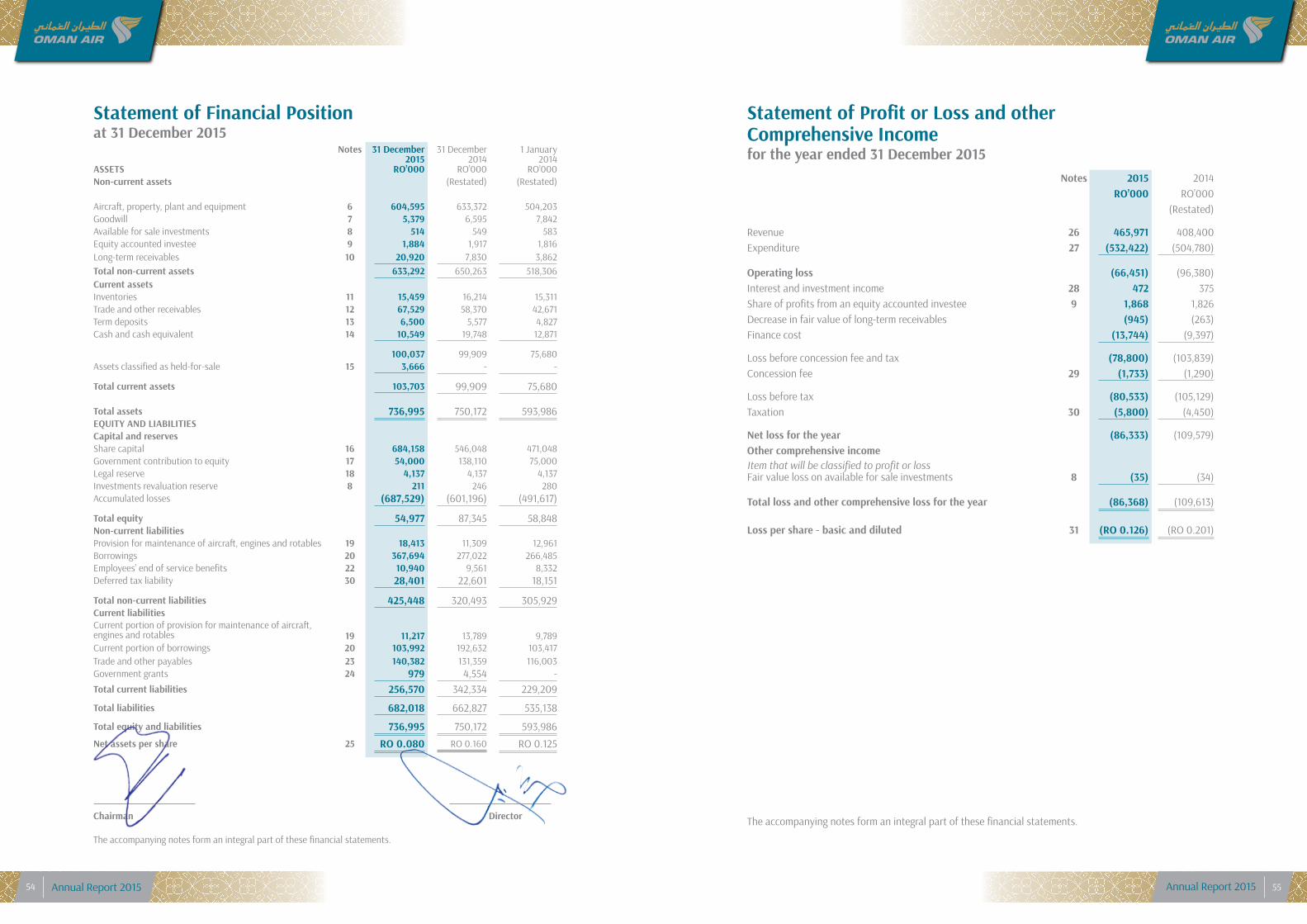

Aircraft, property, plant and equipment 6 604,595 633,372 504,203 Goodwill 7 5,379 6,595 7,842Available for sale investments 8 514 549 583Equity accounted investee 9 1,884 1,917 1,816Long-term receivables 10 20,920 7,830 3,862Total non-current assets 633,292 650,263 518,306Current assetsInventories 11 15,459 16,214 15,311Trade and other receivables 12 67,529 58,370 42,671Term deposits 13 6,500 5,577 4,827Cash and cash equivalent 14 10,549 19,748 12,871

100,037 99,909 75,680Assets classified as held-for-sale 15 3,666 - -

Total current assets 103,703 99,909 75,680

Total assets 736,995 750,172 593,986 EQUITY AND LIABILITIESCapital and reservesShare capital 16 684,158 546,048 471,048Government contribution to equity 17 54,000 138,110 75,000Legal reserve 18 4,137 4,137 4,137Investments revaluation reserve 8 211 246 280Accumulated losses (687,529) (601,196) (491,617)

Total equity 54,977 87,345 58,848Non-current liabilitiesProvision for maintenance of aircraft, engines and rotables 19 18,413 11,309 12,961Borrowings 20 367,694 277,022 266,485Employees’ end of service benefits 22 10,940 9,561 8,332Deferred tax liability 30 28,401 22,601 18,151

Total non-current liabilities 425,448 320,493 305,929Current liabilities Current portion of provision for maintenance of aircraft,

engines and rotables 19 11,217 13,789 9,789Current portion of borrowings 20 103,992 192,632 103,417Trade and other payables 23 140,382 131,359 116,003Government grants 24 979 4,554 -Total current liabilities 256,570 342,334 229,209

Total liabilities 682,018 662,827 535,138

Total equity and liabilities 736,995 750,172 593,986 Net assets per share 25 RO 0.080 RO 0.160 RO 0.125

Chairman Director

The accompanying notes form an integral part of these financial statements.

Statement of Profit or Loss and otherComprehensive Incomefor the year ended 31 December 2015

Notes 2015 2014RO’000 RO’000

(Restated)

Revenue 26 465,971 408,400Expenditure 27 (532,422) (504,780)

Operating loss (66,451) (96,380)Interest and investment income 28 472 375Share of profits from an equity accounted investee 9 1,868 1,826Decrease in fair value of long-term receivables (945) (263)Finance cost (13,744) (9,397)

Loss before concession fee and tax (78,800) (103,839)Concession fee 29 (1,733) (1,290)

Loss before tax (80,533) (105,129)Taxation 30 (5,800) (4,450)

Net loss for the year (86,333) (109,579)Other comprehensive incomeItem that will be classified to profit or lossFair value loss on available for sale investments 8 (35) (34)

Total loss and other comprehensive loss for the year (86,368) (109,613)

Loss per share - basic and diluted 31 (RO 0.126) (RO 0.201)

The accompanying notes form an integral part of these financial statements.

Annual Report 2015 Annual Report 201554 55

Stat

emen

t of C

hang

es in

Equ

ityfo

r the

yea

r end

ed 3

1 D

ecem

ber 2

015

Shar

e ca

pita

l

Gove

rnm

ent

cont

ribut

ion

to

equi

ty

Lega

l re

serv

e

Inve

stm

ents

re

valu

atio

n re

serv

e

Accu

mul

ated

lo

sses

Tota

l

RO’0

00RO

’000

RO’0

00RO

’000

RO’0

00RO

’000

1 Jan

uary

201

4 (a

s pr

evio

usly

repo

rted

)47

1,048

75,0

004,

137

280

(500

,673

)49

,792

Impa

ct o

f cha

nge

in a

ccou

ntin

g po

licy

(not

e 4)

--

--

9,05

69,

056

1 Jan

uary

201

4 (r

esta

ted)

471,0

4875

,000

4,13

728

0(4

91,6

17)

58,8

48N

et lo

ss fo

r the

yea

r-

--

-(1

09,5

79)

(109

,579

)O

ther

com

preh

ensi

ve lo

ss fo

r the

yea

r-

--

(34)

-(3

4)

Tota

l com

preh

ensi

ve lo

ss fo

r the

yea

r-

--

(34)

(109

,579

)(1

09,6

13)

Tran

sact

ions

with

ow

ners

,re

cogn

ised

dire

ctly

in e

quity

:

Gov

ernm

ent c

ontr

ibut

ion

tran

sfer

red

to s

hare

cap

ital

75,0

00(7

5,00

0)-

--

-G

over

nmen

t con

trib

utio

n re

ceiv

ed-

138,

110

--

-13

8,11

0

1 Jan

uary

201

5 (r

esta

ted)

546,

048

138,

110

4,13

724

6(6

01,1

96)

87,3

45

Tota

l com

preh

ensi

ve lo

ss fo

r the

yea

r:N

et lo

ss fo

r the

yea

r-

--

-(8

6,33

3)(8

6,33

3)O

ther

com

preh

ensi

ve lo

ss fo

r the

yea

r-

--

(35)

-(3

5)

Tota

l com

preh

ensi

ve lo

ss fo

r the

yea

r-

--

(35)

(86,

333)

(86,

368)

Tran

sact

ions

with

ow

ners

,re

cogn

ised

dire

ctly

in e

quity

:G

over

nmen

t con

trib

utio

n tr

ansf

erre

d to

sha

re c

apita

l13

8,11

0(1

38,1

10)

--

--

Gov

ernm

ent c

ontr

ibut

ion

rece

ived

-54

,000

--

-54

,000

31 D

ecem

ber 2

015

684,

158

54,0

004,

137

211

(687

,529

)54

,977

The

acco

mpa

nyin

g no

tes

form

an

inte

gral

par

t of t

hese

fina

ncia

l sta

tem

ents

.

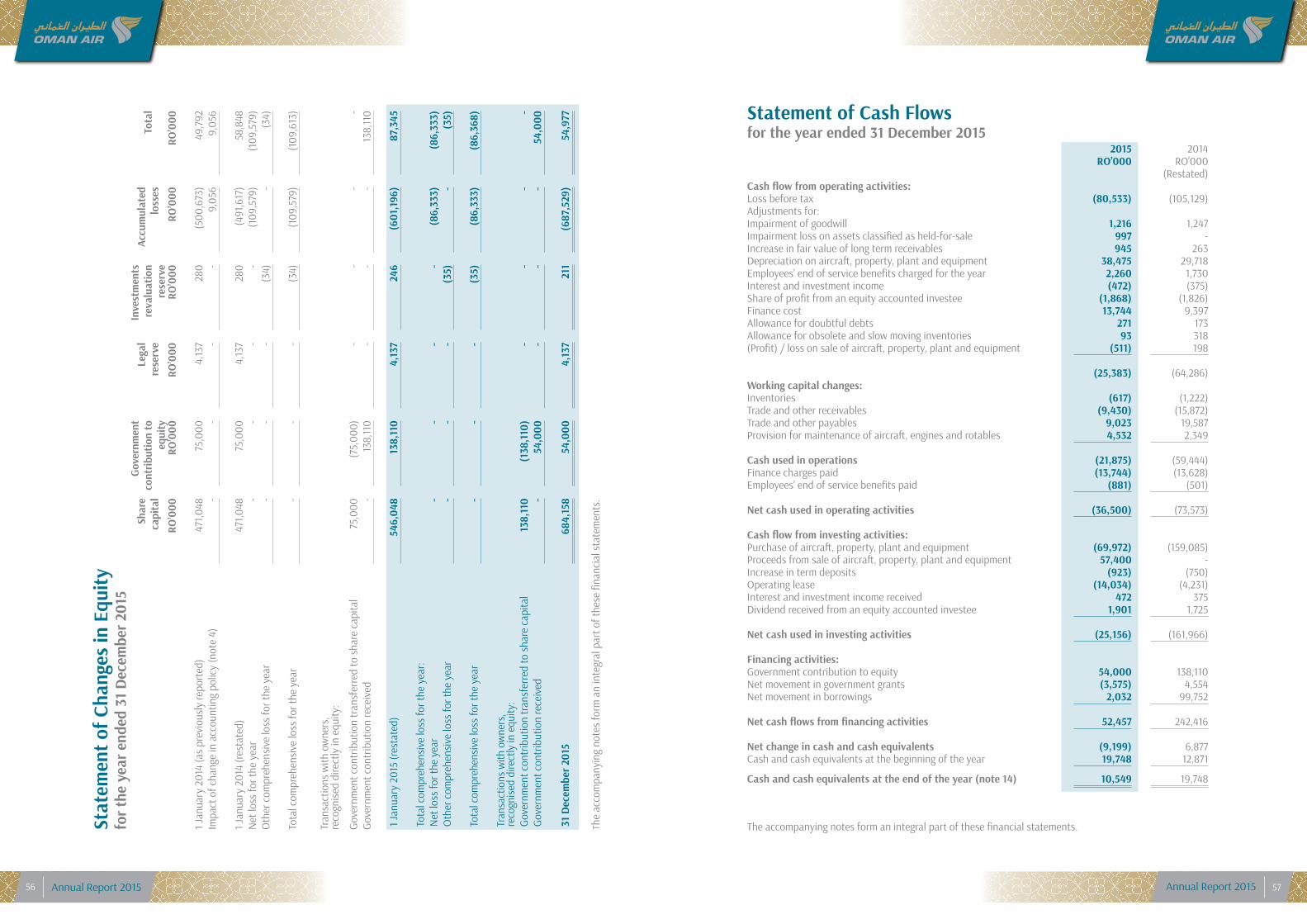

Statement of Cash Flows for the year ended 31 December 2015

2015 2014RO’000 RO’000

(Restated)Cash flow from operating activities:Loss before tax (80,533) (105,129)Adjustments for:Impairment of goodwill 1,216 1,247Impairment loss on assets classified as held-for-sale 997 -Increase in fair value of long term receivables 945 263Depreciation on aircraft, property, plant and equipment 38,475 29,718Employees’ end of service benefits charged for the year 2,260 1,730Interest and investment income (472) (375)Share of profit from an equity accounted investee (1,868) (1,826)Finance cost 13,744 9,397Allowance for doubtful debts 271 173Allowance for obsolete and slow moving inventories 93 318(Profit) / loss on sale of aircraft, property, plant and equipment (511) 198

(25,383) (64,286)Working capital changes:

Inventories (617) (1,222) Trade and other receivables (9,430) (15,872) Trade and other payables 9,023 19,587 Provision for maintenance of aircraft, engines and rotables 4,532 2,349

Cash used in operations (21,875) (59,444)Finance charges paid (13,744) (13,628)Employees’ end of service benefits paid (881) (501)

Net cash used in operating activities (36,500) (73,573)

Cash flow from investing activities:Purchase of aircraft, property, plant and equipment (69,972) (159,085)Proceeds from sale of aircraft, property, plant and equipment 57,400 -Increase in term deposits (923) (750)Operating lease (14,034) (4,231)Interest and investment income received 472 375Dividend received from an equity accounted investee 1,901 1,725

Net cash used in investing activities (25,156) (161,966)

Financing activities:Government contribution to equity 54,000 138,110

Net movement in government grants (3,575) 4,554 Net movement in borrowings 2,032 99,752

Net cash flows from financing activities 52,457 242,416

Net change in cash and cash equivalents (9,199) 6,877Cash and cash equivalents at the beginning of the year 19,748 12,871

Cash and cash equivalents at the end of the year (note 14) 10,549 19,748

The accompanying notes form an integral part of these financial statements.

Annual Report 2015 Annual Report 201556 57

Notes to the Financial Statementsfor the year ended 31 December 2015

1. General

Oman Air SAOC (“the Company”) is a closed Omani joint stock company registered under the Commercial Companies Law of 1974, as amended.

The Company was formed under Royal Decree 52/81 dated 24 May 1981 and commenced its operations on 1 October 1981. The initial duration of the Company was for a period of 20 years from the date of commercial registration to 31 January 2002. Prior to expiry, the Company’s shareholders passed a resolution in an extraordinary general meeting on 27 January 2002 extending the Company’s duration for an indefinite period.

The principal activities of the Company are to transport passengers and freight on a scheduled and chartered basis and to provide ground handling, catering and other airline related services.

In an extraordinary general meeting held on 12 April 2009, the shareholders approved an amendment to the articles of association of the Company. The amended articles of association allow the Company to establish and manage restaurants, coffee shops, hotels, apartments, tourist utilities, both inside and outside the airports, within the Sultanate of Oman or abroad.

Acquisition of business

Effective 1 January 2009 the Company acquired Golden Tulip Seeb (“the Hotel”). The Hotel is a division of the Company and is not a separately registered entity. The Hotel was acquired by the Company as a going concern from the Ministry of Tourism, Government of the Sultanate of Oman.

As on 1 January 2009, the assets and liabilities of the Hotel were transferred to the Company except the land on which the Hotel is located. The Company has been given a right by the Government to use the said land on a rental basis initially for a period of 50 years, subsequently renewable with the mutual consent of both the parties.

Goodwill arising on acquisition: RO’000

Consideration transferred 16,000Add: additional consideration paid in 2010 738Less: fair value of identifiable net assets acquired (1,601)

Goodwill 15,137

Notes to the Financial Statementsfor the year ended 31 December 2015

2. Going concern

The Company incurred a net loss of RO 86.33 million (2014: RO 109.58 million) during the year ended 31 December 2015, with accumulated losses of RO 687.53 million (2014: RO 601.2 million) as at 31 December 2015. As at 31 December 2015, the current liabilities of the Company exceed current assets by RO 152.87 million (2014: RO 242.43 million). These conditions indicate the existence of a material uncertainty which may cast significant doubt about the Company’s ability to continue as a going concern. The financial statements have been prepared under the going concern basis on the assumption that the Company’s shareholders will continue to support the operations and the management will successfully implement its business plan to generate sufficient funds to support its operations and meet its liabilities. The Government holds in excess of 99% of the Company’s equity and has contributed capital of RO 54 million in 2015 (2014: RO 138.11 million) to finance the Company’s operations and capital requirements.

3. Adoption of new and revised International Financial Reporting Standards (IFRS)

3.1 New and revised IFRSs applied with no material effect on the combined financial statements

The following new and revised IFRSs, which became effective for annual periods beginning on or after 1 January 2015, have been adopted in these financial statements. The application of these revised IFRSs has not had any material impact on the amounts reported for the current and prior years but may affect the accounting for future transactions or arrangements.

• Annual Improvements to IFRSs 2010 - 2012 Cycle that includes amendments to IFRS 2, IFRS 3, IFRS 8, IFRS 13, IAS 16, IAS 24 and IAS 38.

• Annual Improvements to IFRSs 2011 - 2013 Cycle that includes amendments to IFRS 1, IFRS 3, IFRS 13 and IAS 40.

• Amendments to IAS 19 Employee Benefits to clarify the requirements that relate to how contributions from employees or third parties that are linked to service should be attributed to periods of service.

Annual Report 2015 Annual Report 201558 59

Notes to the Financial Statementsfor the year ended 31 December 2015

3. Adoption of new and revised International Financial Reporting Standards (IFRS) (continued)

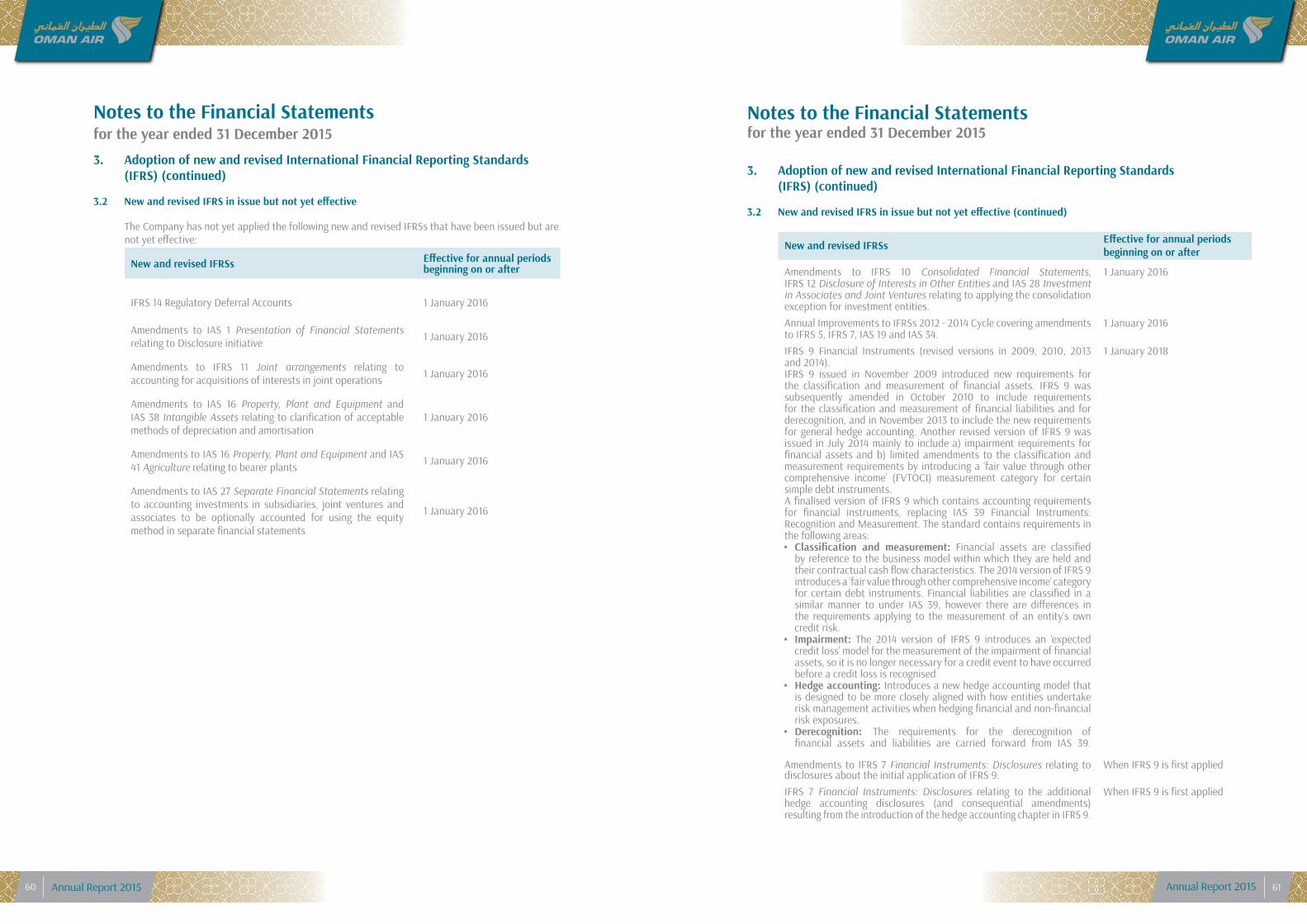

3.2 New and revised IFRS in issue but not yet effective

The Company has not yet applied the following new and revised IFRSs that have been issued but are not yet effective:

New and revised IFRSs Effective for annual periods beginning on or after

IFRS 14 Regulatory Deferral Accounts 1 January 2016

Amendments to IAS 1 Presentation of Financial Statementsrelating to Disclosure initiative 1 January 2016

Amendments to IFRS 11 Joint arrangements relating toaccounting for acquisitions of interests in joint operations 1 January 2016

Amendments to IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assets relating to clarification of acceptablemethods of depreciation and amortisation

1 January 2016

Amendments to IAS 16 Property, Plant and Equipment and IAS41 Agriculture relating to bearer plants 1 January 2016

Amendments to IAS 27 Separate Financial Statements relating to accounting investments in subsidiaries, joint ventures and associates to be optionally accounted for using the equitymethod in separate financial statements

1 January 2016

Notes to the Financial Statementsfor the year ended 31 December 2015

3. Adoption of new and revised International Financial Reporting Standards (IFRS) (continued)

3.2 New and revised IFRS in issue but not yet effective (continued)

New and revised IFRSs Effective for annual periods beginning on or after

Amendments to IFRS 10 Consolidated Financial Statements,IFRS 12 Disclosure of Interests in Other Entities and IAS 28 Investment in Associates and Joint Ventures relating to applying the consolidation exception for investment entities.

1 January 2016

Annual Improvements to IFRSs 2012 - 2014 Cycle covering amendments to IFRS 5, IFRS 7, IAS 19 and IAS 34.

1 January 2016

IFRS 9 Financial Instruments (revised versions in 2009, 2010, 2013 and 2014).IFRS 9 issued in November 2009 introduced new requirements for the classification and measurement of financial assets. IFRS 9 was subsequently amended in October 2010 to include requirements for the classification and measurement of financial liabilities and for derecognition, and in November 2013 to include the new requirements for general hedge accounting. Another revised version of IFRS 9 was issued in July 2014 mainly to include a) impairment requirements for financial assets and b) limited amendments to the classification and measurement requirements by introducing a ‘fair value through other comprehensive income’ (FVTOCI) measurement category for certain simple debt instruments.A finalised version of IFRS 9 which contains accounting requirements for financial instruments, replacing IAS 39 Financial Instruments: Recognition and Measurement. The standard contains requirements in the following areas:• Classification and measurement: Financial assets are classified

by reference to the business model within which they are held and their contractual cash flow characteristics. The 2014 version of IFRS 9 introduces a ‘fair value through other comprehensive income’ category for certain debt instruments. Financial liabilities are classified in a similar manner to under IAS 39, however there are differences in the requirements applying to the measurement of an entity’s own credit risk.

• Impairment: The 2014 version of IFRS 9 introduces an ‘expected credit loss’ model for the measurement of the impairment of financial assets, so it is no longer necessary for a credit event to have occurred before a credit loss is recognised

• Hedgeaccounting:Introduces a new hedge accounting model that is designed to be more closely aligned with how entities undertake risk management activities when hedging financial and non-financial risk exposures.

• Derecognition: The requirements for the derecognition of financial assets and liabilities are carried forward from IAS 39.

1 January 2018

Amendments to IFRS 7 Financial Instruments: Disclosures relating to disclosures about the initial application of IFRS 9.

When IFRS 9 is first applied

IFRS 7 Financial Instruments: Disclosures relating to the additional hedge accounting disclosures (and consequential amendments) resulting from the introduction of the hedge accounting chapter in IFRS 9.

When IFRS 9 is first applied

Annual Report 2015 Annual Report 201560 61

Notes to the Financial Statementsfor the year ended 31 December 2015

3. Adoption of new and revised International Financial Reporting Standards (IFRS) (continued)

3.2 New and revised IFRS in issue but not yet effective (continued)

New and revised IFRSs Effective for annual periods beginning on or after

IFRS 15 Revenue from Contracts with Customers

In May 2014, IFRS 15 was issued which established a single comprehensive model for entities to use in accounting for revenue arising from contracts with customers. IFRS 15 will supersede the current revenue recognition guidance including IAS 18 Revenue, IAS 11 Construction Contracts and the related interpretations when it becomes effective.

The core principle of IFRS 15 is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. Specifically, the standard introduces a 5-step approach to revenue recognition:

• Step 1: Identify the contract(s) with a customer.• Step 2: Identify the performance obligations in the contract.• Step 3: Determine the transaction price.• Step 4: Allocate the transaction price to the performance

obligations in the contract.• Step 5: Recognise revenue when (or as) the entity satisfies

a performance obligation.

Under IFRS 15, an entity recognises when (or as) a performance obligation is satisfied, i.e. when ‘control’ of the goods or services underlying the particular performance obligation is transferred to the customer. Far more prescriptive guidance has been added in IFRS 15 to deal with specific scenarios. Furthermore, extensive disclosures are required by IFRS 15.

1 January 2018

IFRS 16 Leases

IFRS 16 specifies how an IFRS reporter will recognise, measure, present and disclose leases. The standard provides a single lessee accounting model, requiring lessees to recognise assets and liabilities for all leases unless the lease term is 12 months or less or the underlying asset has a low value. Lessors continue to classify leases as operating or finance, with IFRS 16’s approach to lessor accounting substantially unchanged from its predecessor, IAS 17.

1 January 2019

Amendments to IFRS 10 Consolidated Financial Statements and IAS 28 Investments in Associates and Joint Ventures (2011) relating to the treatment of the sale or contribution of assets from and investor to its associate or joint venture

Effective date deferred indefinitely

Notes to the Financial Statementsfor the year ended 31 December 2015

3. Adoption of new and revised International Financial Reporting Standards (IFRS) (continued)

The Board of Directors anticipates that these new and revised standards, interpretations and amendments will be adopted in the Company’s financial statements for the year beginning 1 January 2016 or as and when they are applicable and adoption of these new standards, interpretations and amendments, except for IFRS 9, IFRS 15 and IFRS 16 may have no material impact on the financial statements of the Company in the period of initial application.

Management anticipates that IFRS 15 and IFRS 9 will be adopted in the Company’s financial statements for the annual year beginning 1 January 2018 and IFRS 16 in the annual year beginning 1 January 2019. The application of IFRS 9, IFRS 15 and IFRS 16 may have significant impact on amounts reported and disclosures made in the Company’s financial statements in respect of revenue from its customers, the Company’s financial assets and financial liabilities, lease liabilities and right to use assets. However, it is not practicable to provide a reasonable estimate of effects of the application of these standards until the Company performs a detailed review.

4. Basis of preparation and summary of significant accounting policies

Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards, (IFRS) and the requirements of the Commercial Companies Law of 1974, as amended.

A summary of significant accounting policies, which have been consistently applied by the Company and are consistent with those used in the previous year, is set out below:

Functional and presentation currency

These financial statements are presented in Rial Omani (“RO”), which is the Company’s functional currency. All financial information presented in RO has been rounded to the nearest thousands, except when otherwise indicated.

Basis of measurement

These financial statements are prepared on the historical cost basis except for available for sale financial assets which are measured at fair value. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date, regardless of whether that price is directly observable or estimated using another valuation technique. In estimating the fair value of an asset or a liability, the Company takes into account the characteristics of the asset or liability if market participants would take those characteristics into account when pricing the asset or liability at the measurement date. Fair value for measurement and/or disclosure purposes in these financial statements is determined on such a basis.

.

Annual Report 2015 Annual Report 201562 63

Notes to the Financial Statementsfor the year ended 31 December 2015

4. Basis of preparation and summary of significant accounting policies (continued)

Change in accounting policy during the year

During the current year, the Company changed its accounting policy of creating a maintenance provision for major maintenance costs for its owned aircraft, to capitalising the major maintenance costs and depreciating over the appropriate period until the next major maintenance event, in line with IAS 16 Property, plant and equipment.

The change in policy has been made to provide a more accurate disclosure of the benefit of the maintenance cost over the expected life of that component.

The impact of change in accounting policy on maintenance provision and aircraft, property, plant and equipment, accumulated losses and loss for the year are as follows:

31 December 2014 1 January 2014RO’000 RO’000

(Restated) (Restated)

Aircraft, property, plant and equipment (previously reported) 643,918 512,593Impact of change in accounting policy (10,546) (8,390)

Aircraft, property, plant and equipment (restated) 633,372 504,203

Provision for maintenance of aircraft, engines and rotables(previously reported) (44,186) (40,196)Impact of change in accounting policy 19,088 17,446

(25,098) (22,750)

Accumulated losses (previously reported) (609,738) (500,673)Impact of change in accounting policy 8,542 9,056

Accumulated losses (restated) (601,196) (491,617)

Impact on total loss for the year (514) 1,157

Notes to the Financial Statementsfor the year ended 31 December 2015

4. Basis of preparation and summary of significant accounting policies (continued)

Aircraft, property, plant and equipment

Aircraft, property, plant and equipment are stated at cost less accumulated depreciation and any identified impairment loss. Borrowing costs, net of interest income, which are directly attributable to acquisition of qualifying items of aircraft, property, plant and equipment, are capitalized as part of the cost of aircraft, property, plant and equipment.

An element of the cost of an aircraft is attributed on acquisition to prepaid maintenance and is depreciated over a period until the next maintenance event occurs based on the number of hours flown or cycles completed.

Subsequent expenditureSubsequent costs incurred which lend enhancement to future periods, such as long-term scheduled maintenance and major overhaul of aircraft and engines, are capitalised and depreciated over the length of period benefiting from these enhancements. All other maintenance costs are charged to the income statement as incurred. Other subsequent expenditure is capitalized only when it increases the future economic benefits embodied in the item of aircraft, property, plant and equipment.

Cost of expenses incurred for regular inspections of airframe and engines are capitalized and depreciated over the period between consecutive inspections which is generally 8 and 3 years, respectively.