Housing Finance in Emerging Markets: Functions, Instruments and Risks Conference: Housing Finance in Emerging Markets: Policy and Regulatory Challenges The World Bank, Washington D.C. 10 March, 2003 Presented by: Dr. Michael Lea President of Countrywide International Consulting Services

Transcript

Housing Finance in Emerging Markets: Functions, Instruments and Risks

Conference:

Housing Finance in Emerging Markets: Policy and Regulatory Challenges

The World Bank, Washington D.C.

10 March, 2003

Presented by:

Dr. Michael Lea

President of Countrywide International Consulting Services

2

Outline of Presentation

Discussion of the Organization and Economics of the Housing Finance Business

Overview of the Key Functions of Housing Finance

Brief Review of Mortgage Instruments and Mechanisms for Funding

Identification of Basic Risks, How They Can Be Managed, and How Policies Can Reduce Risk for Housing Finance Providers

Economics of Economics of Mortgage LendingMortgage Lending

4

Goals of the Mortgage Lending Business

Maximize Value of Franchise (ROE)

All Other Goals Contribute to the First

Customer satisfaction

Employee motivation

Investor confidence

Regulator and policy maker confidence

Constraints

Market (competitive product, input markets)

Risk (tolerance for variation in ROE)

In particular, the ability to manage interest rate risk

5

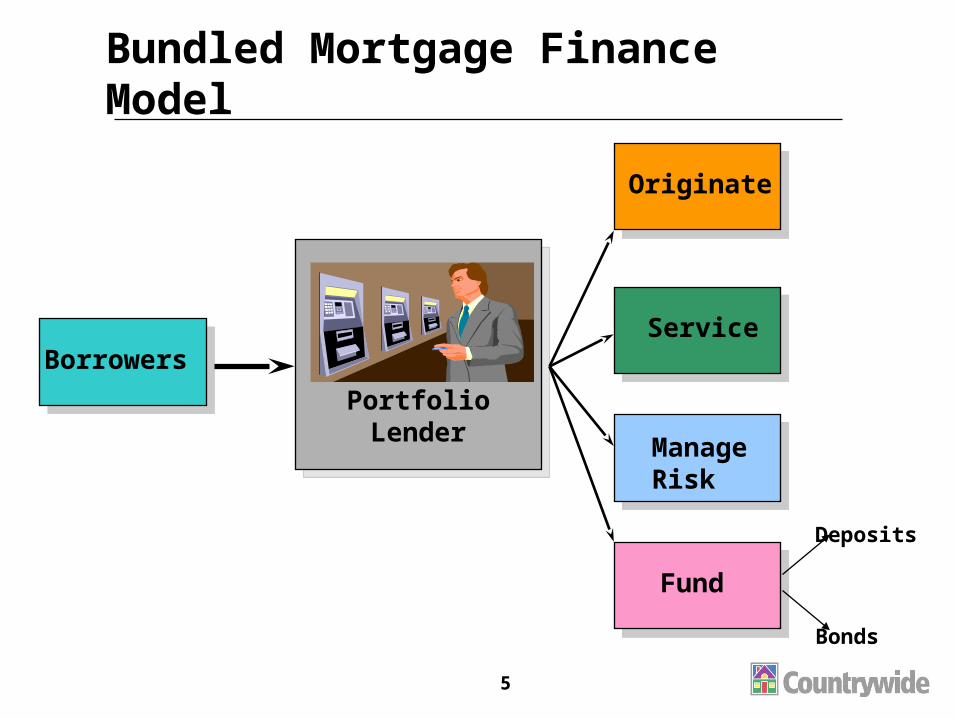

Bundled Mortgage Finance Model

PortfolioLender

PortfolioLender

Borrowers

Originate

Service

ManageRisk

Fund

Deposits

Bonds

6

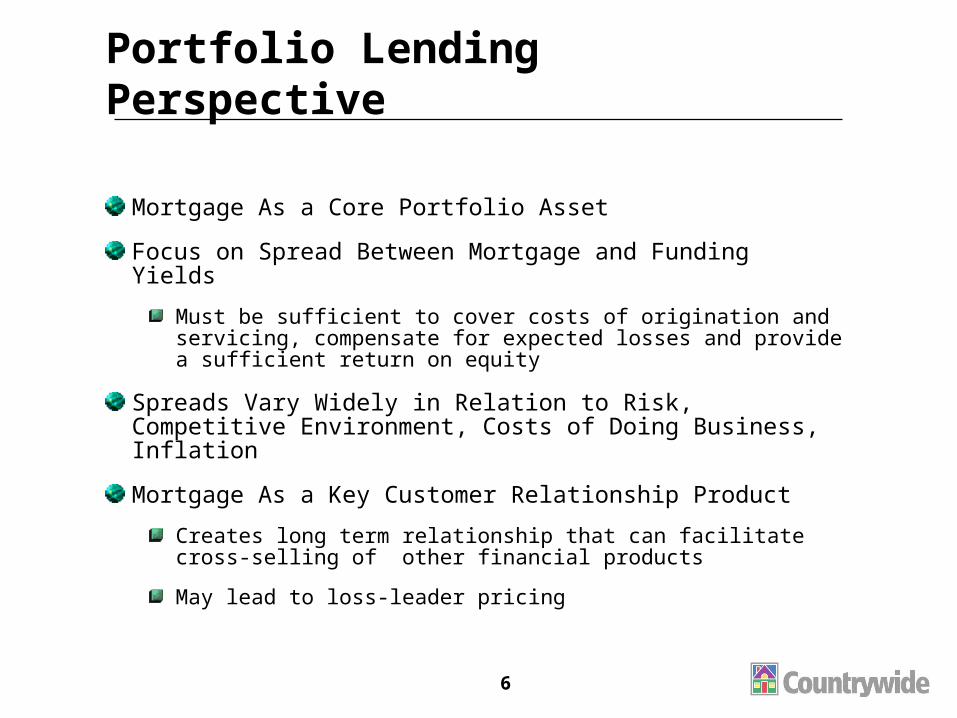

Portfolio Lending Perspective

Mortgage As a Core Portfolio Asset

Focus on Spread Between Mortgage and Funding Yields

Must be sufficient to cover costs of origination and servicing, compensate for expected losses and provide a sufficient return on equity

Spreads Vary Widely in Relation to Risk, Competitive Environment, Costs of Doing Business, Inflation

Mortgage As a Key Customer Relationship Product

Creates long term relationship that can facilitate cross-selling of other financial products

May lead to loss-leader pricing

7

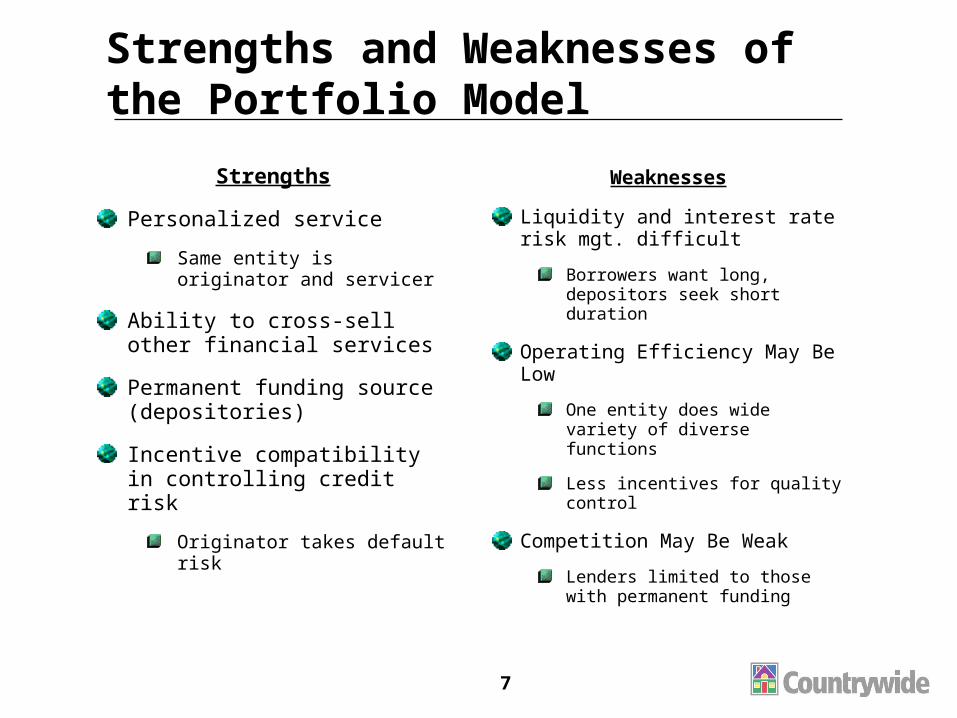

Strengths and Weaknesses of the Portfolio Model

Strengths

Personalized service

Same entity is originator and servicer

Ability to cross-sell other financial services

Permanent funding source (depositories)

Incentive compatibility in controlling credit risk

Originator takes default risk

Weaknesses

Liquidity and interest rate risk mgt. difficult

Borrowers want long, depositors seek short duration

Operating Efficiency May Be Low

One entity does wide variety of diverse functions

Less incentives for quality control

Competition May Be Weak

Lenders limited to those with permanent funding

8

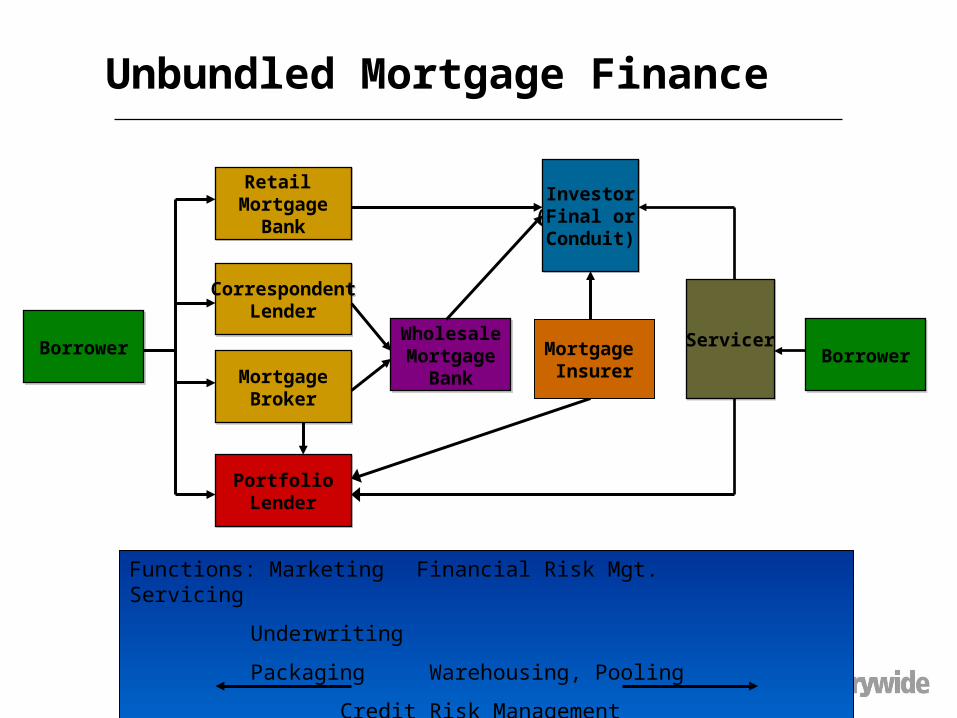

Functional Perspective

Mortgage Lending Functions Viewed As Separate Businesses

Goal Within Each Business Is Maximization of Shareholder Wealth

Integrated Lenders Can Treat Each Function As a Stand Alone Business

Allocate risk capital to each business line and require separate reporting of results

Provide proper disclosures (cost and terms of credit, conditions for providing loan etc.)

Consumer regulation a major issue in developed markets

16

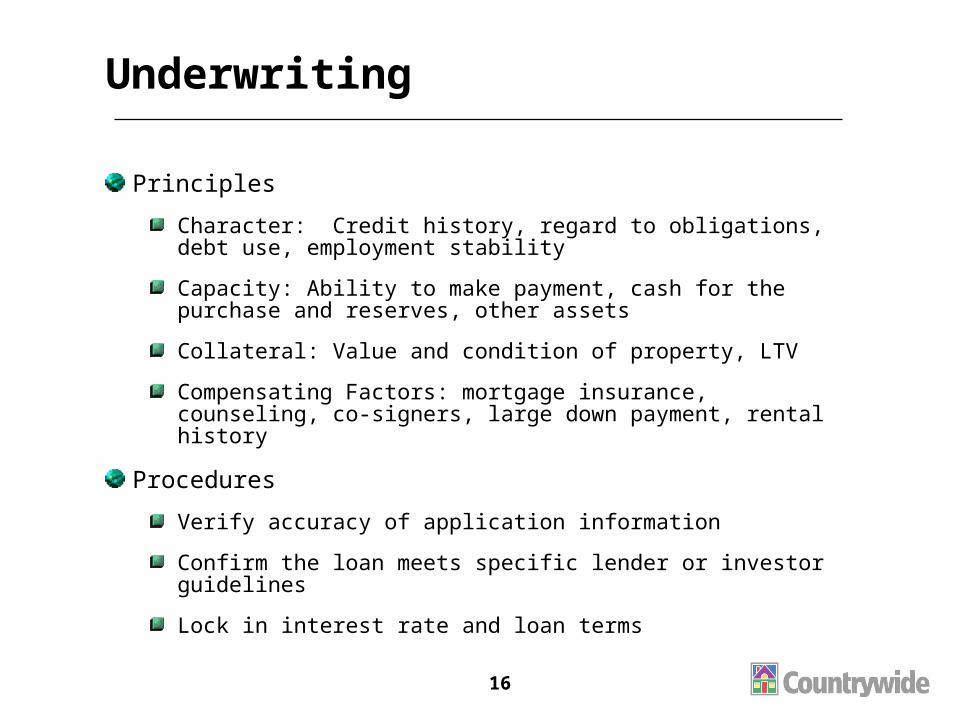

Underwriting

Principles

Character: Credit history, regard to obligations, debt use, employment stability

Capacity: Ability to make payment, cash for the purchase and reserves, other assets

Collateral: Value and condition of property, LTV

Compensating Factors: mortgage insurance, counseling, co-signers, large down payment, rental history

Procedures

Verify accuracy of application information

Confirm the loan meets specific lender or investor guidelines

Lock in interest rate and loan terms

17

Automated Underwriting and Credit Scoring

Credit Reports and Credit Scoring are used to determine credit stability and allow instant feedback on credit quality

Credit scoring is a statistical modeling technique that evaluates the degree of risk posed by a prospective borrower or existing customer

Automated Underwriting combines credit reports and scoring, loan program and pricing information to approve loan at point of sale or refer to underwriter

Assumes past performance of like borrowers profile can predict future performance

18

Closing

Major Contributor to Time and Risk in Origination

Functions

Verify clear title, occupancy permits, etc.

Confirm final terms of the loan and remaining conditions; List all fees and cash required for final payment

Verify insurance policies are active

Prepare all necessary legal documents and obtain signatures (notary)

Transfer cash to appropriate parties

Ensure that property transfer and liens are properly recorded

Delivery of documents and file to servicer

19

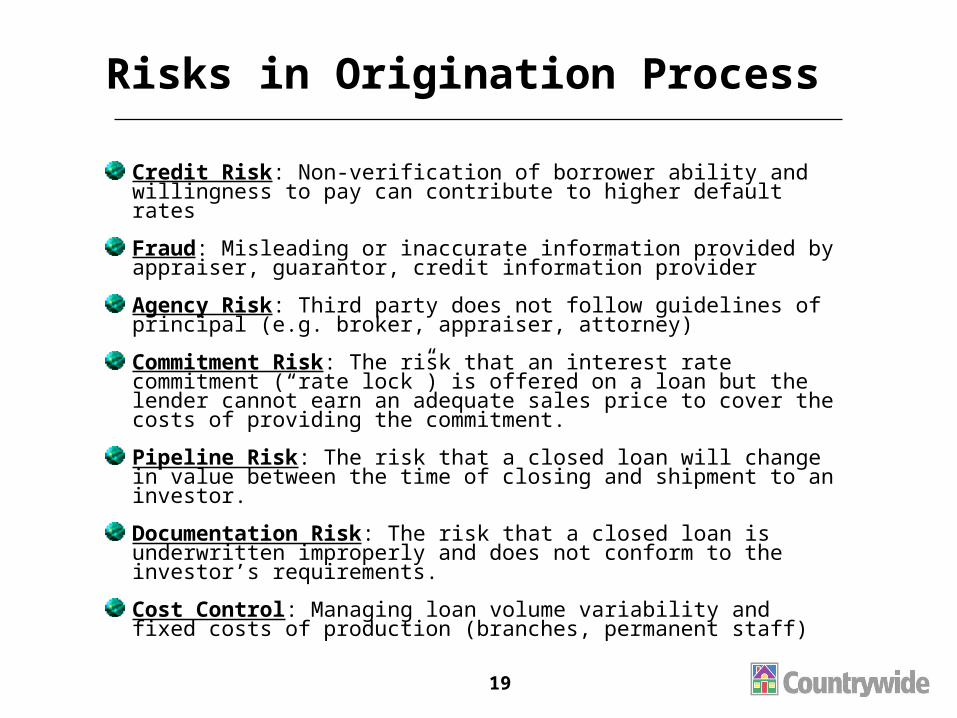

Risks in Origination Process

Credit Risk: Non-verification of borrower ability and willingness to pay can contribute to higher default rates

Fraud: Misleading or inaccurate information provided by appraiser, guarantor, credit information provider

Agency Risk: Third party does not follow guidelines of principal (e.g. broker, appraiser, attorney)

Commitment Risk: The risk that an interest rate commitment (“rate lock”) is offered on a loan but the lender cannot earn an adequate sales price to cover the costs of providing the commitment.

Pipeline Risk: The risk that a closed loan will change in value between the time of closing and shipment to an investor.

Documentation Risk: The risk that a closed loan is underwritten improperly and does not conform to the investor’s requirements.

Cost Control: Managing loan volume variability and fixed costs of production (branches, permanent staff)

20

Managing Risk in Origination

Automating the Process

Electronic Applications

Reduces processing time/one time entry

Improves accuracy

Creates data base for later use

Facilitates flow of information through the various processing steps

Electronic Credit reports and Automated Underwriting

Increase accuracy

More objective underwriting

Improve the Flow of Information to Decision Makers

Activity-based reporting and costs

Quality control policies and procedures

Real time information on pipeline for funding, hedging

Convert Fixed Cost to Variable Cost

In US wholesale channel and commissioned loan officers are variable costs

Funding Through the Secondary Markets

Creates discipline for underwriting, documentation, quality control

Rating agency and investor review can lead to quality improvement

ServicingServicing

22

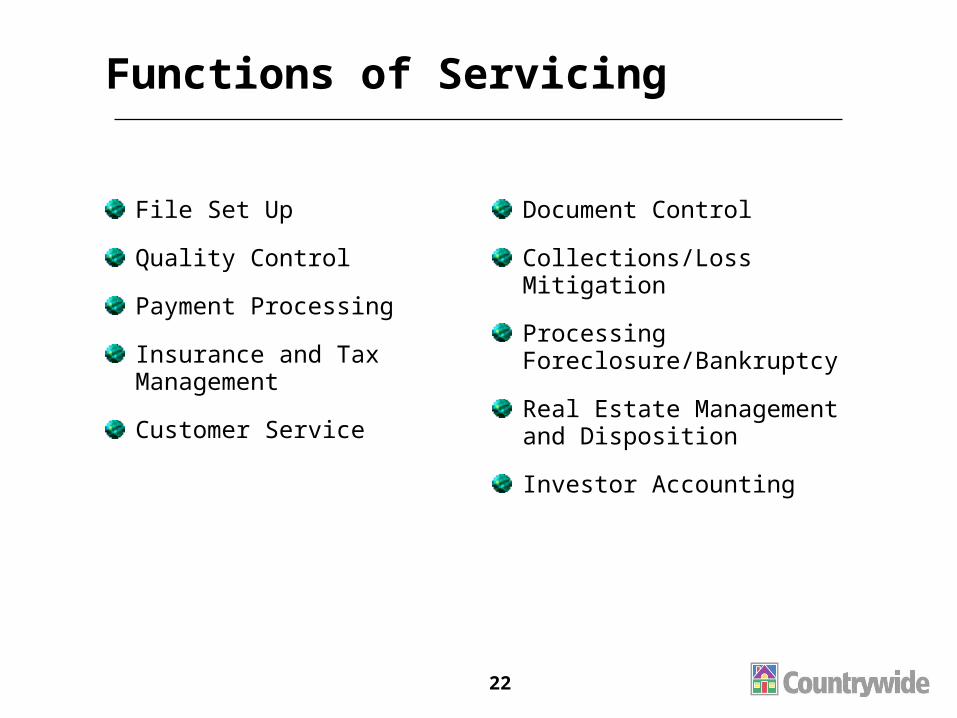

Functions of Servicing

File Set Up

Quality Control

Payment Processing

Insurance and Tax Management

Customer Service

Document Control

Collections/Loss Mitigation

Processing Foreclosure/Bankruptcy

Real Estate Management and Disposition

Investor Accounting

23

Servicing Objectives

File Set Up: Fast, error free entry of new loan data/documents into the servicing system

Quality Control: Avoid losses by catching errors and fraud early; ensure proper documentation and adherence to investor guidelines (reduce probability of repurchase

Payment Processing: Focus on efficiency, avoid loss through error

Customer Service: Handle requests and maintain customer satisfaction and retention

Document Control: Protect lender’s security, efficient handling of documents

Collections: Avoid foreclosure and improve cure rate on delinquent loans

Foreclosure and Repossession: Minimize loss severity, liquidate property to recover as much value as possible

Taking the property is a last resort for lenders but the possibility has strong deterrent value

Investor Accounting: Ensure Accurate And Timely Disbursement Of Funds To Investor

24

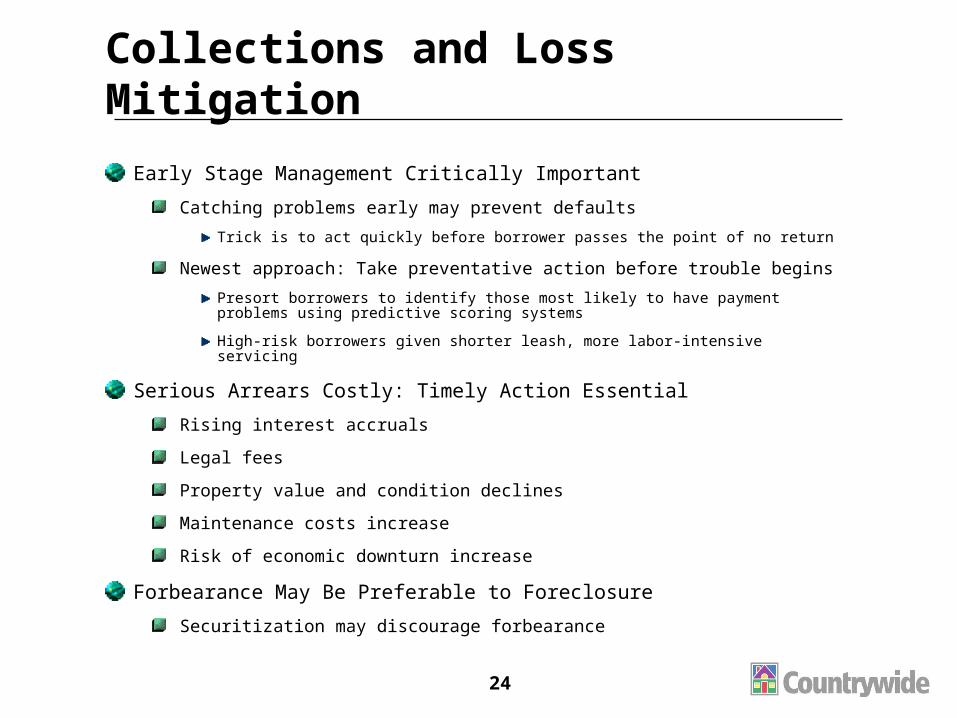

Collections and Loss Mitigation

Early Stage Management Critically Important

Catching problems early may prevent defaults

Trick is to act quickly before borrower passes the point of no return

Newest approach: Take preventative action before trouble begins

Presort borrowers to identify those most likely to have payment problems using predictive scoring systems

High-risk borrowers given shorter leash, more labor-intensive servicing

Serious Arrears Costly: Timely Action Essential

Rising interest accruals

Legal fees

Property value and condition declines

Maintenance costs increase

Risk of economic downturn increase

Forbearance May Be Preferable to Foreclosure

Securitization may discourage forbearance

25

Default Management Process

BorrowerDefaults

EvaluateOptions

Obtain Title

MarketProperty

ContinueNegotiationsWork out plan (forbearance)

Bring account current (waive late fees)Recast rate or termForgive or capitalize interest in arrearsRefinance

Deed in lieu of foreclosureShort saleForeclosure

BeginForeclosure

26

Risks in Servicing

High Level Of Defaults/Delinquencies

May reflect poor underwriting, volatile economy, ineffective collection policies

Errors Made In Other Departments That “Come To Roost” In Servicing

Securitization focuses attention on servicing functions of reporting, documentation, performance

Fluctuations in Value of Servicing Asset

In secondary market system, servicing rights may be capitalized and held on the balance sheet. Value of servicing asset will vary with changes in interest rates, prepayment

27

Managing Risks in Servicing

Automation

Facilitates cost control, information flow for managers, investors; reduces incidence of errors

Data Collection and Analysis

Understanding default and prepayment based on analysis of portfolio

Pro-active collections can reduce default loss

Quality control procedures can reduce errors and improve efficiency

Cost Control

The “Loan Factory” – loan processing is a commodity business

Outsourcing

28

Loan Servicing Economics

In Secondary Market System a Profitable Business

Servicer receives fee (bp/month on outstanding balance)

Other sources of income: float, late fees, investment of escrow balances

Strong incentive to minimize costs (processing, arrears)

Portfolio lenders can turn servicing into a profit center as well

Transfer pricing and cost accounting

Mortgage InstrumentsMortgage Instruments

30

Mortgage Instruments

Two Instruments

Mortgage is pledge of property as security for an obligation

Promissory Note defines debt and makes borrower liable for obligation

Recording (Registration) of Mortgage

Not essential to validity of obligation

Protects mortgagee from subsequent acts of mortgagor

31

Mortgage Design

Design Objectives

Borrower affordability

Borrowers have diverse needs

Lender profitability

Instruments have different risk-return profiles

General Rule About Mortgage Design

Changing design to solve one problem always creates a new problem

Anticipated inflation leads to affordability problems (“tilt problem”)

Protects borrowers against interest rate risk

Graduated Payment Mortgages

Payments start low and rise over time

Improves affordability and partially offsets tilt

But lengthens duration and creates negative amortization

Reduces interest rate risk protection

33

Adjustable Rate Mortgages

Allows Lenders to Manage Moderate Inflation

Three Major Types

Discretionary: Determined by lender

Rollover: Short term, fixed rate periods during long term amortization

Indexed: Rate change tied to external rate

Transfers Interest Rate Risk to Borrowers

Better match for depository portfolio lenders

Higher credit risk due to potential payment shock

34

Indexed Mortgages

Conventional Mortgages Do Not Perform Well With High and Volatile Inflation

Mortgage Designs Must Balance Affordability and Profitability

Two Major Designs

PLAM (Price Level Adjusted Mortgage)

DIM (Dual Indexed Mortgage)

35

Indexed Mortgages (cont’d)

PLAM

Interest rate fixed at “real” rate

Payment and balance adjusted by price index

Works well if incomes and property values rise with inflation

Can lead to payment shock or negative equity if income or property values do not rise with inflation

DIM

Separates payment and accrual rates

Solves problem that incomes may not rise with inflation

Payment rates typically indexed to wages

Dangers of minimum wage indexing

But creates new problem

DIM may not amortize

36

New Mortgage Designs

Equity Release Mortgages

Allows elderly home owners to consume some or all of their equity

Borrowers receive payments in exchange for portion of equity or capital gains

Flexible Mortgages

Allow uneven repayment patterns

Integrated Mortgages

Link mortgage with checking account, savings accounts, insurance policies etc.

Funding and Risk Funding and Risk ManagementManagement

38

Funding Options

Deposits

Other Corporate Liabilities

Whole Loan Sales

Mortgage Bond Sales

Mortgage Security Sales

Liquidity Facilities

39

Funding Mortgage Assets

Maximize the Value of the Earning Asset Through Selection of the Lowest Cost Funding on a Risk Adjusted Basis

Portfolio Lenders: Maximize spread through mix of retail and wholesale funding of various terms and equity in accordance with risk management guidelines

Secondary Market Lenders: Best execution on sale of mortgage (maximum price upon sale)

Pricing incorporates target profit margin

Temporary lenders need warehouse funding

40

Financial Institution Risks

Credit Risk: Loss Due to Default on Loan Obligation

Liquidity Risk: Risk That the Money Will Be Needed Before It Is Due

Interest Rate Risk: Risk That Interest Rate Changes Will Affect the Value of Assets and Liabilities

Basis Risk: Risk that margins on assets and liabilities will vary over time

41

Financial Institution Risks: II

Prepayment Risk: Risk That Mortgage Will Be Repaid Earlier Than Scheduled

Inflation Risk: Risk That Unexpected Inflation Will Affect the Value of Assets and Liabilities

Foreign Exchange Risk: Risk That Movements in Exchange Rates Will Affect the Value of Assets And/or Liabilities

42

Financial Institution Risks: III

Operations Risk: Risk That the Organization, Controls, Information Systems and Technologies Are Inadequate to Safeguard the Institution

Agency Risk: Risk That an Agent or Intermediary Will Misuse the Funds

Political Risk: the Risk That the Legal and Political Framework Within Which the Lending Takes Place Will Change

43

Cushions to Absorb Risk

Equity Capital

Basel II will more explicitly link equity requirements and risk broadly defined

Managerial Controls and Policies

Must have an understanding of how interest rates impact balance sheet and income statement

Importance of data, measures

Must have policies regarding tolerance for and management of various risks

Portfolio Structure

Inflows and outflows of funds

Maturities and interest re-setting periods of assets and liabilities

Management Judgment

44

How Policy Makers Can Reduce Risk in Housing Finance

Origination

Centralized credit bureau

Centralized house price database

Accurate, efficient and low cost title and lien registration

Encourage competition

Stable economy

Servicing

Stable economy

Effective foreclosure regime

Funding

Stable economy

Strong and flexible regulatory system for institutions, instruments

Develop capital markets and sources of long term funding