Information Memorandum Shailen Jasani MA Vet MB MRCVS DACVECC Iqbal Dhanji MBA BSc FCA Co-Founders and Directors The Ralph Veterinary Referral Centre PLC An Enterprise Investment Scheme (“EIS”) Investment Opportunity JULY 2016 centre centre ® centre centre

Transcript

Information MemorandumShailen Jasani MA Vet MB MRCVS DACVECC

Iqbal Dhanji MBA BSc FCA

Co-Founders and Directors

The Ralph Veterinary Referral Centre PLC

An Enterprise Investment Scheme (“EIS”) Investment Opportunity

JULY 2016cent

rece

ntre

®

cent

rece

ntre

®

®

3

Information Memorandum

Sapphire Capital Partners LLP which is authorised and regulated by the Financial Conduct Authority (“FCA”), has approved the issue of this Document as a financial promotion in accordance with the provisions of section 21 of the Financial Services and Markets Act 2000. This document is not a prospectus and has not been filed with the FCA or made available to the public as such.

The purpose of this document is to provide information to persons who have expressed an interest in the possibility of investing in The Ralph Veterinary Referral Centre PLC (the “Company” or “The Ralph”). It does not constitute an offer to subscribe for shares in the Company which will be made by way of a separate Offer and Application Form.

To the best of the knowledge and belief of the Company and the Directors of the Company who have taken all reasonable care to ensure this is the case, the information contained in this document is in accordance with the facts and does not omit anything likely to affect the importance of such information. The Directors accept responsibility accordingly.

The Company has received advance assurance from HM Revenue & Customs that its activities qualify under the Enterprise Investment Scheme (“EIS”) (as set out in the Income Tax Act 2007). Following the issue of Ordinary Shares, the Company can apply to HM Revenue & Customs for authorisation to issue tax relief certificates (Form EIS 3) to Investors. Investors should note that there is no guarantee that tax relief under EIS will be available or that if it is initially available, it will not be subsequently withdrawn. Prospective Investors are advised to take their own taxation advice. The targeted financial returns highlighted in Section 3.3 are dependent upon EIS being available and in the event that such relief cannot be claimed, then actual returns will be considerably lower.

Your attention is drawn to Section 8 of this document, which set out certain risk factors relating to any investment in Shares. All statements regarding the Company’s business, financial position and prospects should be viewed in the light of the risk factors set out in Section 8 of this document.

All statements of opinion and/or belief in this document and all views expressed regarding the Company’s projections, forecasts and statements relating to expectations of future events are those of the Company. No representation or warranty is made, or assurance given that such statements, views, projections or forecasts are correct or that the Company’s objectives will be achieved.

The information in this document is provided on a confidential basis.

1. Summary2. The Company3. Financial Illustration4. Exit

SECTION 4: THE MARKET AND ILLUSTRATIVE FINANCIAL PROJECTIONS PAGE 15

1. The Market2. Illustrative Financial Projections

SECTION 5: KEY TEAM MEMBERS PAGE 201. Key Team Members

SECTION 6: INFORMATION ON THE COMPANY PAGE 241. Statutory Information2. Share Capital3. Articles of Association4. Directors interest and other matters5. Material Contracts 6. Working capital7. Litigation8. Other information9. Documents available for Inspection

SECTION 7: PROPOSED TERMS OF THE OFFER PAGE 321. The Offer2. Conditions to the Offer3. How to Apply4. Terms for Intermediaries

SECTION 8: RISK FACTORS PAGE 341. Investment Risks2. Risks Relating to the Company3. Taxation Risks4. Other Risks

SECTION 1: SUMMARYThe following is a summary of the key points pertaining to the opportunity to invest in The Ralph and should be read in conjunction with the full text of this Information Memorandum.

®

®

7

Information Memorandum

Key Highlights

The Ralph is a new unlisted public company set up to develop a state-of-the-art multidisciplinary small animal specialist referral hospital in the M4/M40 corridor. It also aims to offer the second largest Emergency and Critical Care (ECC) service in the United Kingdom at its launch.

Market Sector and Investment highlights:

• Growth in Business Sector: the companion animal veterinary sector is buoyant, in particular within the referral space. Purchases of top tier referral centres by venture capital firms and corporate service providers over the last two to three years demonstrates clear confidence in the veterinary referral sector. The two largest independently owned referral hospitals in the South East increased turnover by 11% (from £9.15m to £10.11m) and 43% (from £6.6m to £9.4m) between March 2014 and March 2015.

• Growth in Pet Insurance: “85% of referral practice business is now made up of complex/expensive insurance cases” (Onswitch, 2014). One report suggests that between 2014 and 2018 the pet insurance market will grow by 37.6% topping the £1 billion mark for the first time by 2017. Another report suggests that pet insurance in the UK is expected to reach £1.1 billion by 2018 at a compound annual growth rate (CAGR) of 6.9% during the forecast period of 2014-2018.

• Growth of Referral ECC Service: The largest referral ECC service in the United Kingdom has experienced consistent growth and service expansion. At launch The Ralph aims to offer the second largest referral ECC service in the UK alongside key clinical services such as Orthopaedics, Soft Tissue Surgery, Internal Medicine and Neurology & Neurosurgery amongst others.

• Experienced Management Team: the Management team have strong clinical, strategic, operational, financial and management experience to successfully launch The Ralph and have already identified some of the key specialists and senior management who have provided indicative intention of joining the hospital when it opens.

• Enterprise Investment Scheme: The Ralph has obtained Advance Assurance from HM Revenue & Customs on 22 January 2016 that its trade will qualify for Enterprise Investment Scheme relief.

• Secured Referral Stream: independent veterinary professionals in the hospital’s catchment area will be incentivised to refer their cases to The Ralph by being offered a direct investment opportunity and an additional share-based referral incentive scheme. Professional regulatory approval has been received.

• Premises: The Ralph will seek premises, located in the M4-M40 corridor. It is intended for the premises to also house a new affiliated charity, set up to provide low cost basic and specialist healthcare to stray, shelter and other eligible companion animals.

• Financial Returns: Projected after four years to deliver a targeted amount of 21.7 pence for every one share at a cost of 14 pence (or £1.54 per 70p of net EIS investment cost).

• Brand Recognition: The Ralph brand is already well-known by Vets with “The Ralph Site”, a non-profit online pet bereavement resource founded and funded by Shailen Jasani (the founder of The Ralph), being known for its compassionate values. This resource has allowed many veterinary colleagues to direct hundreds of grieving Pet carers to a caring and empathetic community of Pet lovers at their time of need.

Investment Offer

The Company will seek to raise up to £3,700,000 by issuing 26,428,572 Ordinary ‘A’ Shares at a price of £0.14 each to prospective investors in the Company to fund the lease and refurbishment of premises, fixtures, fittings & equipment and for working capital.

Led by the services of an experienced management team, the Company is targeting financial returns for qualifying EIS investors of £1.54 per £0.70 net invested cost (being £1 less 30% EIS income tax relief) after four years.

The Company has obtained advance assurance from HM Revenue & Customs on 22 January 2016 that its activities qualify under the Enterprise Investment Scheme (“EIS”) (as set out in the Income Tax Act 2007). Following the issue of Ordinary ‘A’ Shares and the commencement of trading, the Company can apply to HM Revenue & Customs for authorisation to issue tax relief certificates (Form SEIS 3 and Form EIS 3) to qualifying Investors.

The targeted financial returns highlighted above are dependent upon EIS Relief (defined below) being available and in the event that such relief cannot be claimed, then actual returns will be considerably lower. Prospective Investors are advised to take their own taxation advice.

Attractive tax incentives:

Investors who qualify for EIS can avail of:

• EIS – 30% upfront income tax relief on amount subscribed (up to a maximum investment of £1 million in the year of investment and/or carried back to the previous tax year);

• 100% inheritance tax relief after two years (provided the Ordinary ‘A’ Shares are held at the time of death);

• Capital Gains Tax deferral for the life of the investment on amount subscribed;

• Tax free growth (provided income tax relief has been given and not withdrawn and disposal takes place more than three years after the Company begins to trade);

• Loss relief (any shares disposed of at a loss can be set against an Investor’s income to reduce tax); and

• Business Investment Relief (for certain UK resident non-UK domiciled Investors).

Immediately following closing of the Offer and assuming the Maximum Subscription is reached:

Number Issue Price(£)

Nominal Value

(£)

% of Total Issued Share

Capital

Ordinary ‘A’ Shares held by Investors after the Offer

27,500,000 £0.14 £0.001 34.6%

Ordinary ‘B’ Shares held by Co-Founders

44,050,000 £0.001 £0.001 55.4%

Ordinary ‘B’ Shares for Referral Incentive Scheme

3,975,000 £0.001 £0.001 5.0%

Ordinary ‘B’ Shares held in a trust for a compasion Animal Charity

3,975,000 £0.001 £0.001 5.0%

TOTAL 79,500,000 100.0%

The raise of £3,850,000 for a 34.6% shareholding (being 27,500,000 shares) in the Company includes the shares to be issued under SEIS described below.

The share-based referral incentive scheme will be facilitated by allocating founders’ Ordinary ‘B’ shares.The Royal College of Veterinary Surgeons (professional regulatory body) was consulted prior to offering this scheme and has provided its approval, while emphasising the need for transparency and discloure by all parties involved.

On a return of capital, the Ordinary ‘A’ shares and ‘B’ shares shall receive the amounts paid up on such shares on a liquidation or sale of the Company. Thereafter all Ordinary ‘A’ Shares and ‘B’ Shares shall rank equally on returns of capital on the basis of nominal amounts paid up. It is noted that Ordinary ‘A’ Shares and Ordinary ‘B’ Shares shall both be voting shares.

Commitments have been received in respect of 1,071,428 shares at £0.14 p/share under the terms of SEIS which will be allotted prior to the remaining Ordinary ‘A’ shares under the Offer.

Risks

Investment in the Company involves a high degree of risk. The value of investments can go down as well as up and you could lose part of or all of your capital invested. You should consider your investment in the Company to be a medium to long term investment and that an investment into the Company is likely to be illiquid. Investors are strongly advised to seek independent legal, financial and tax advice before making a decision to invest. Full details of the risk factors can be found in Section 8.

How to Apply

After reading this Information Memorandum if you are interested in investing you should register your interest with the Company online by visiting www.theralph.vet. Potential Investors are welcome to contact the co-founders via email:

Directors Shailen Jasani MA VetMB MRCVS DipACVECC (age 41 years) – Chief Executive Officer and Clinical Director.

Iqbal Dhanji MBA BSc FCA (age 50 years) – Chief Operating Officer and Finance Director.

Two Non-Executive Directors will be sought to join the Board when the Company achieves its Minimum Subscription.

Company Secretary Iqbal Dhanji

Registered Office 30 High Street, Great Bookham, Surrey, KT23 4AG

EIS Adviser Sapphire Capital Partners LLP

34 South Molton Street Mayfair London W1K 5RG

Solicitors Edwin Coe LLP

Stone Buildings Lincoln’s Inn London WC2A 3TH

Bank Lloyds Bank

Banstead Branch P O Box 1000 BX1 1LT

Information Memorandum

SECTION 3: INVESTMENT OPPORTUNITY

®

®

13

Information Memorandum

1. Summary

BackgroundThe Ralph is a new unlisted public company set up to develop a state-of-the-art multidisciplinary small animal specialist referral hospital in the M4/M40 corridor that will be staffed by Board-certified Diplomates. At launch it aims to offer the second largest referral Emergency and Critical Care (ECC) service in the United Kingdom alongside key clinical services such as Orthopaedics, Soft Tissue Surgery, Internal Medicine and Neurology & Neurosurgery amongst others. The hospital will also offer a Primary Care Out-of-Hours service to surrounding primary care practices on an opt-in basis.

The Ralph aims to be a top tier tertiary referral centre on a par with, and indeed at times exceeding, both University-grade small animal hospitals and a very small number of other comparable private referral centres. On the basis of the Directors’ current targeted area for the hospital the nearest centre considered to be a significant competitor would be a 45-60 minute drive away and it is notable that only one of the significant competitors currently has a specialist ECC service embedded in a large multidisciplinary hospital.

In keeping with its ethical core values, The Ralph will work closely with a new affiliated charity, operating from within the premises and to which equity will be gifted, to provide low cost basic and specialist healthcare to stray, shelter and other eligible companion animals. The Ralph’s charity affiliation should substantially benefit the reputation of the for-profit business. Income will be additionally raised from providing services to charity cases, albeit for a reduced fee, and the charity affiliation will importantly also serve to enhance staff morale and retention in a vocational sector. The Ralph Site, a non-profit online pet loss support resource founded by Shailen Jasani in 2011, will also be run by the new charity.

Discussions are also on-going about a potential partnership with the Animal Management Department at the Berkshire College of Agriculture.

2. The Company

The Ralph aims to be the top of the pyramid of small animal veterinary services. This segment of the market has the following key characteristics:

• Growth of Business Sector: the referral segment of the companion animal veterinary sector is buoyant. Purchases of top tier referral centres by venture capital firms and corporate service providers over the last two to three years demonstrate clear confidence in the growth of the veterinary referral sector. The Pet Food Manufacturers’ Association 2015 annual report estimates that 12 million UK households have pets, with 8.5 million dogs and 7.4 million cats. Available data suggests that many of these are to be found in south-east England. The two largest independently owned referral hospitals in this region increased turnover by 11% (from £9.15m to £10.11m) and by 43% (from £6.6m to £9.4m) between March 2014 and March 2015. It is noteworthy that, in the Directors’ experience, pet carers often travel an hour or two to attend top tier specialist hospitals and indeed it is not unheard of for pet carers to travel much further to see specific specialists if required.

• Growth in Pet Insurance: “85% of referral practice business is now made up of complex/expensive insurance cases” (Onswitch, 2014). One report suggests that between 2014 and 2018 the pet insurance market will grow by 37.6% topping the £1 billion mark for the first time by 2017. Another report suggests that pet insurance in the UK is expected to reach £1.1 billion by 2018 at a compound annual growth rate (CAGR) of 6.9% during the forecast period of 2014-2018.

• Growth of referral ECC service: The largest referral ECC service in the United Kingdom has experienced consistent growth and service expansion. The Ralph aims to offer the second largest referral ECC service in the United Kingdom alongside key clinical services such as Orthopaedics, Soft Tissue Surgery, Internal Medicine and Neurology & Neurosurgery amongst others.

The Company has assembled an experienced management team with strong clinical, strategic, operational, financial and management experience to successfully launch The Ralph. They have also identified some of the key specialists who have provided indicative intention of joining The Ralph when it opens.

The Company has obtained Advance Assurance from HM Revenue & Customs on 22 January 2016 that its trade will qualify for Enterprise Investment Scheme relief.

The Ralph will seek its own premises, located in the M4-M40 corridor. It is intended for the premises to also house a new affiliated charity, set up to provide low cost basic and specialist healthcare to stray, shelter and other eligible companion animals. It is noted that at the time of preparing this Information Memorandum, the premises has yet to be secured. If a lease tenure cannot be secured, the business model may change substantially if a property has to be acquired or a new one built.

The Company is targeting financial returns for qualifying EIS investors of £1.54 per £0.70 net invested cost (being £1 less 30% EIS income tax relief) after four years.

3. Financial Illustration

The tables below illustrates the potential returns from an investment of £100,000 in the Company with EIS Relief at the rate of 30%, but excluding any potential benefits from IHT Relief or CGT Reliefs:

With EIS benefits

Assumed performance over three year period: 0% Target Return of £1.40

£ £Investment in the Company 100,000 100,000Less: EIS Income Tax Relief at 30% (30,000) (30,000)

Net cost investment 70,000 70,000

Exit proceeds (based on assumed performance) 100,000 154,000

Tax free gains 30,000 84,000

Net tax free return1 12.6% p.a. 21.8% p.a.Gross equivalent return2 (to a 40% taxpayer) 21.0% p.a. 36.3% p.a.Gross equivalent return (to a 45% taxpayer) 22.9% p.a. 39.6% p.a.

1 The net tax free return is the internal rate of return (IRR) based on the above cashflows, estimated dates and assumed rates of tax, ignoring personal allowances.

2 The gross equivalent return is calculated by dividing the net tax free return by 0.6 for a 40% taxpayer and 0.55 for a 45% taxpayer.

®

15

Information Memorandum

Each of the performance cases has been constructed using the industry experience and knowledge of the Directors. It is important to note, however, that objective data in relation to EIS qualifying shares is difficult to obtain.

The above returns are set out for illustrative purposes only and no forecast or projection is implied or should be inferred. The projections above may not be a reliable indicator of future performance. The value of investments in the Company may fall as well as rise. No warranty as to future outcome is implied or should be inferred. Investors’ attention is drawn to the information set out at the front of this Information Memorandum and the specific Risk Factors referred to in Section 8 of this Information Memorandum.

4. The Exit

The Directors will actively monitor opportunities for Investors to realise their investment at the end of the three year EIS Qualifying Period, with an expected exit to occur after four years.

Possible routes for a realisation include:

• re-financingbytheCompanyandutilisingsignificantbankdebtasameansofreturningfunds to Investors.

• asaleofsharestoathirdparty.

• amanagementbuyout.

At the present time, the Directors consider a management buyout or a Company buy-back through debt restructuring as the most likely exit routes. For either of these two exits, it is likely that the Shareholders will realise their investment for cash.

The Directors hold nearly all the Ordinary ‘B’ Shares in issue. These incentivise the Directors, as such shares will only receive a return on a liquidation or sale of the Company after all amounts subscribed by Ordinary ‘A’ Shareholders have been paid back. Thereafter the Ordinary ‘A’ Shares and Ordinary ‘B’ Shares rank pari passu for returns. On the basis of Maximum Subscription under the Offer such surplus returns after repayment of invested capital to Ordinary ‘A’ Shares will therefore be divided between as to approximately 34.6% to Ordinary ‘A’ Shareholders and 65.4% to Ordinary ‘B’ Shareholders.

In the event that the Company was valued at £10 million after 4 years, on the basis of a Maximum Subscription under the Offer investors would receive the amount subscribed (£3.85m/£0.14 per share) and a 34.6% share of the remaining £6.15m (i.e. £2.13m), equivalent to 7.7 pence for every 14 pence subscribed. The total projected return to investors is therefore 21.7 pence for every 14 pence subscribed (or £1.54 for every £1 total subscribed).

The Company has received Advance Assurance from HM Revenue & Customs to confirm that the Ordinary ‘A’ Shares will qualify for Enterprise Investment Scheme relief.

Please note that the Directors can make no guarantee about the timing of the realisation of an investment in the Company. Potential Investors should be aware that EIS investments may be considered risky and the Ordinary ‘A’ Shares must be considered a longer term investment.

SECTION 4: THE MARKET AND ILLUSTRATIVE FINANCIAL PROJECTIONS

®

17

Information Memorandum

1. The Market

Market Analysis:

Referrals are commonplace within the Vet sector with an Onswitch* focus group research finding that 94% of primary care practices had referred at least one case in the previous year. Important aspects in the choice of referral centre include geographical location, and the reputation of the clinicians and of the hospital in general. In this piece of research past experience of a referral centre was the highest ranked reason for an individual choosing to refer there again; maximising the experience of future referring practitioners is a key aim of The Ralph’s customer care strategy.

(* Onswitch is a leader in business, marketing and customer care in the veterinary sector.)

Onswitch data also suggests that “85% of referral practice business is now made up of complex/expensive insurance cases” and that an increasing proportion of referral cases are acute presentations versus more elective or chronic disorders (Onswitch, 2014).

One report suggests that between 2014 and 2018 the pet insurance market will grow by 37.6% topping the £1 billion mark for the first time by 2017. Another report suggests that pet insurance in the UK is expected to reach £1.1 billion by 2018 at a compound annual growth rate (CAGR) of 6.9% during the forecast period of 2014-2018. Data reported from the Association of Business Insurers in 2014 suggests that the UK pet insurance market was worth £0.4 billion in 2006 and £0.78 billion in 2014 with an expected increase to £1.1 billion by 2017.

The spate of purchases of top tier referral centres by venture capital firms and corporate service providers over the last two to three years demonstrates clear confidence in the on-going buoyancy and growth of both the veterinary referral sector and the pet insurance market.

With its proposed 24/7 referral ECC service supported by a multidisciplinary clinical team, The Ralph will be very well placed to service the growing demand for referral of acute cases, as witnessed by the consistent growth and service expansion seen at the only other sizeable referral ECC service in the United Kingdom which is located within the same region. A comprehensive online and offline brand development and marketing strategy is proposed to enable The Ralph to compete effectively for referral cases, gain early traction and experience growth consistent with the financial projections presented in this document.

“Vet services grew...from 2012–14, ahead of the general pet market growth...Vet service spend will be driven by increased availability of complex procedures, widening insurance coverage and a desire by owners to treat their pets’ health as they would their own”

(Pets At Home Group PLC, Annual Report and Accounts 2015).

Key Assumptions:

Key assumptions that have been made for the business plan to be achievable:

• Dogandcatownershipinthesouth-eastofEnglandwilleitherremainstableorincrease.Currently, nearly half of households in the UK share their home with a pet.

• Asaresultofcontinuedhumanisationofpets,petcarerswillcontinuetoseekthemostadvanced healthcare for their pets within their financial means.

• Thepetinsurancemarketandthepercentageofdogsandcatscoveredbypetinsurancewill remain stable or increase.

• EmergencyandCriticalCare(ECC)willcontinuetodevelopasaveterinaryspecialityintheUnited Kingdom and there will be increasing recognition of its value.

• Astrategybasedongreatcustomer(pet,petcarer,referringpractice)serviceandreasonable but not extravagant pricing is likely to offer the most successful and sustainable model.

• Astrategywhichincorporatessocialenterprise,education(bothveterinaryandpetcarers)and charity components offers benefits with respect to reputation and rewards for staff that will outweigh any financial costs that are incurred.

®

19

Information Memorandum

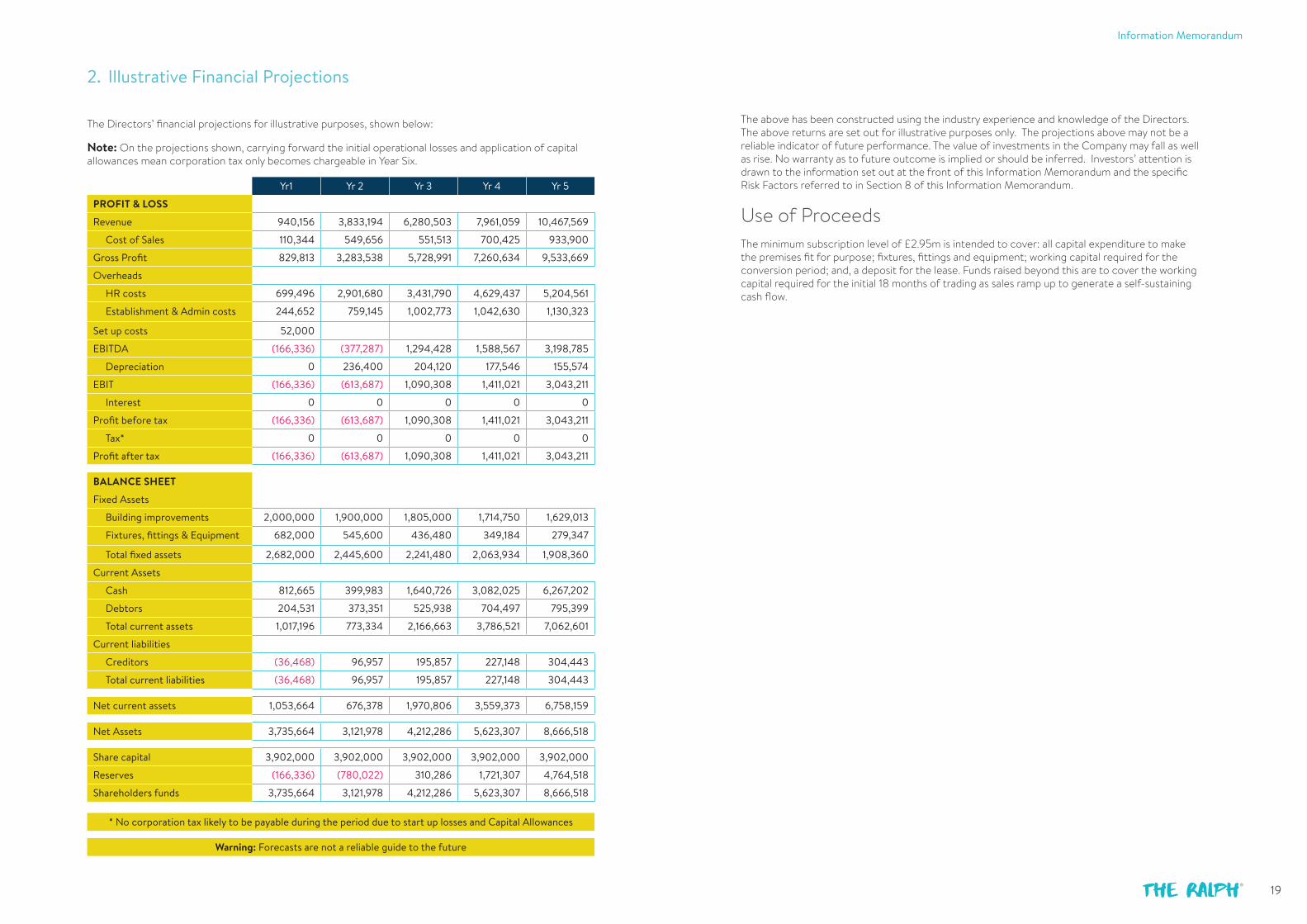

2. Illustrative Financial Projections

The Directors’ financial projections for illustrative purposes, shown below:

Note: On the projections shown, carrying forward the initial operational losses and application of capital allowances mean corporation tax only becomes chargeable in Year Six.

* No corporation tax likely to be payable during the period due to start up losses and Capital Allowances

Warning: Forecasts are not a reliable guide to the future

The above has been constructed using the industry experience and knowledge of the Directors. The above returns are set out for illustrative purposes only. The projections above may not be a reliable indicator of future performance. The value of investments in the Company may fall as well as rise. No warranty as to future outcome is implied or should be inferred. Investors’ attention is drawn to the information set out at the front of this Information Memorandum and the specific Risk Factors referred to in Section 8 of this Information Memorandum.

Use of ProceedsThe minimum subscription level of £2.95m is intended to cover: all capital expenditure to make the premises fit for purpose; fixtures, fittings and equipment; working capital required for the conversion period; and, a deposit for the lease. Funds raised beyond this are to cover the working capital required for the initial 18 months of trading as sales ramp up to generate a self-sustaining cash flow.

®

21

Information Memorandum

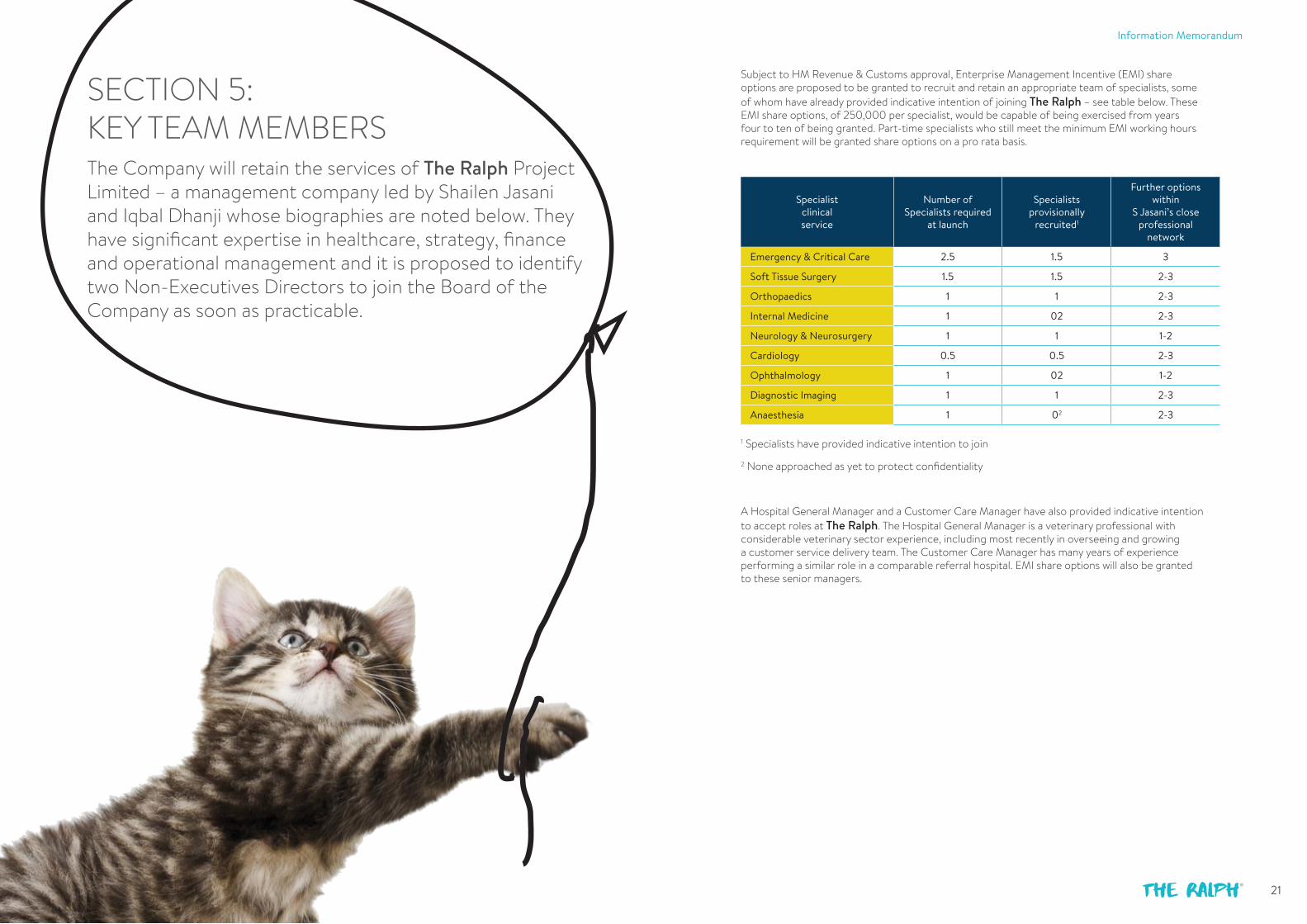

SECTION 5: KEY TEAM MEMBERSThe Company will retain the services of The Ralph Project Limited – a management company led by Shailen Jasani and Iqbal Dhanji whose biographies are noted below. They have significant expertise in healthcare, strategy, finance and operational management and it is proposed to identify two Non-Executives Directors to join the Board of the Company as soon as practicable.

Subject to HM Revenue & Customs approval, Enterprise Management Incentive (EMI) share options are proposed to be granted to recruit and retain an appropriate team of specialists, some of whom have already provided indicative intention of joining The Ralph – see table below. These EMI share options, of 250,000 per specialist, would be capable of being exercised from years four to ten of being granted. Part-time specialists who still meet the minimum EMI working hours requirement will be granted share options on a pro rata basis.

Specialist clinical service

Number of Specialists required

at launch

Specialists provisionally

recruited1

Further options within

S Jasani’s close professional

network

Emergency & Critical Care 2.5 1.5 3

Soft Tissue Surgery 1.5 1.5 2-3

Orthopaedics 1 1 2-3

Internal Medicine 1 02 2-3

Neurology & Neurosurgery 1 1 1-2

Cardiology 0.5 0.5 2-3

Ophthalmology 1 02 1-2

Diagnostic Imaging 1 1 2-3

Anaesthesia 1 02 2-3

1 Specialists have provided indicative intention to join

2 None approached as yet to protect confidentiality

A Hospital General Manager and a Customer Care Manager have also provided indicative intention to accept roles at The Ralph. The Hospital General Manager is a veterinary professional with considerable veterinary sector experience, including most recently in overseeing and growing a customer service delivery team. The Customer Care Manager has many years of experience performing a similar role in a comparable referral hospital. EMI share options will also be granted to these senior managers.

®

23

Information Memorandum

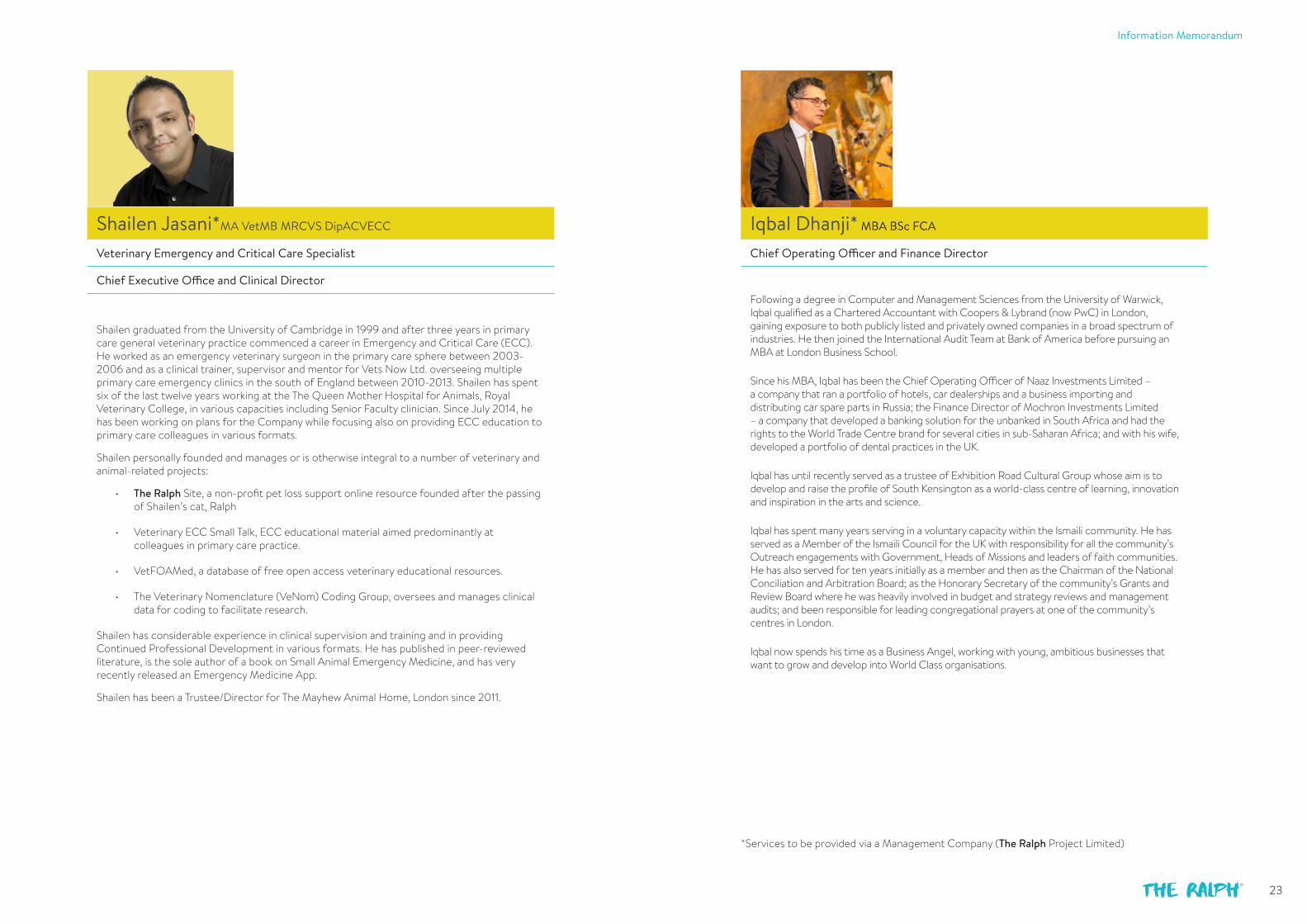

Iqbal Dhanji* MBA BSc FCA

Chief Operating Officer and Finance Director

Following a degree in Computer and Management Sciences from the University of Warwick, Iqbal qualified as a Chartered Accountant with Coopers & Lybrand (now PwC) in London, gaining exposure to both publicly listed and privately owned companies in a broad spectrum of industries. He then joined the International Audit Team at Bank of America before pursuing an MBA at London Business School.

Since his MBA, Iqbal has been the Chief Operating Officer of Naaz Investments Limited – a company that ran a portfolio of hotels, car dealerships and a business importing and distributing car spare parts in Russia; the Finance Director of Mochron Investments Limited – a company that developed a banking solution for the unbanked in South Africa and had the rights to the World Trade Centre brand for several cities in sub-Saharan Africa; and with his wife, developed a portfolio of dental practices in the UK.

Iqbal has until recently served as a trustee of Exhibition Road Cultural Group whose aim is to develop and raise the profile of South Kensington as a world-class centre of learning, innovation and inspiration in the arts and science.

Iqbal has spent many years serving in a voluntary capacity within the Ismaili community. He has served as a Member of the Ismaili Council for the UK with responsibility for all the community’s Outreach engagements with Government, Heads of Missions and leaders of faith communities. He has also served for ten years initially as a member and then as the Chairman of the National Conciliation and Arbitration Board; as the Honorary Secretary of the community’s Grants and Review Board where he was heavily involved in budget and strategy reviews and management audits; and been responsible for leading congregational prayers at one of the community’s centres in London.

Iqbal now spends his time as a Business Angel, working with young, ambitious businesses that want to grow and develop into World Class organisations.

*Services to be provided via a Management Company (The Ralph Project Limited)

Shailen Jasani*MA VetMB MRCVS DipACVECC

Veterinary Emergency and Critical Care Specialist

Chief Executive Office and Clinical Director

Shailen graduated from the University of Cambridge in 1999 and after three years in primary care general veterinary practice commenced a career in Emergency and Critical Care (ECC). He worked as an emergency veterinary surgeon in the primary care sphere between 2003-2006 and as a clinical trainer, supervisor and mentor for Vets Now Ltd. overseeing multiple primary care emergency clinics in the south of England between 2010-2013. Shailen has spent six of the last twelve years working at the The Queen Mother Hospital for Animals, Royal Veterinary College, in various capacities including Senior Faculty clinician. Since July 2014, he has been working on plans for the Company while focusing also on providing ECC education to primary care colleagues in various formats.

Shailen personally founded and manages or is otherwise integral to a number of veterinary and animal-related projects:

• The Ralph Site, a non-profit pet loss support online resource founded after the passing of Shailen’s cat, Ralph

• VeterinaryECCSmallTalk,ECCeducationalmaterialaimedpredominantlyatcolleagues in primary care practice.

• TheVeterinaryNomenclature(VeNom)CodingGroup,overseesandmanagesclinicaldata for coding to facilitate research.

Shailen has considerable experience in clinical supervision and training and in providing Continued Professional Development in various formats. He has published in peer-reviewed literature, is the sole author of a book on Small Animal Emergency Medicine, and has very recently released an Emergency Medicine App.

Shailen has been a Trustee/Director for The Mayhew Animal Home, London since 2011.

®

25

Information Memorandum

SECTION 6: INFORMATION ON THE COMPANY

1. Statutory InformationThe Company was incorporated as a public limited company on 7 December 2015 with the name The Ralph Project PLC and with registered number 09905661. A special resolution was passed on 12th February 2016 to change the name to The Ralph Veterinary Referral Centre PLC. The principal legislation under which the Company operates is the Companies Act 2006. The liability of members of the Company is limited.

The Company obtained its certificate to do business on 16 December 2015.

2. Share CapitalOn incorporation of the Company the issued share capital was 6,500,000 ordinary shares of £0.001 each paid up at par.

On 14 December 2015 the Company issued 45,500,000 ordinary shares of £0.001 each paid up at par.

Prior to the issue of shares under the Offer the Company will pass resolutions to:

(i) convert the 52,000,000 ordinary shares of £0.001 each into 52,000,000 Ordinary ‘B’ Shares of £0.001 each;

(ii) authorise the Directors pursuant to section 551 of the Act to exercise any power of the Company to allot and grant rights to subscribe for or to convert securities into shares of the Company up to a maximum nominal amount £160,000 provided that the authority thereby given would expire 5 years after the passing of the resolution (unless previously renewed or varied) save that the Directors may, notwithstanding such expiry, allot any shares or grant any such rights under the authority in pursuance of an offer or agreement so to do made by the Company before the expiry of the authority;

(iii) empower the Directors to allot equity securities (as defined in section 560 of the Act) for cash pursuant to the authority conferred by the resolution above as if section 561(1) of the Act did not apply to any such allotment, provided that such power would be limited to the allotment of equity securities up to an aggregate nominal amount of £160,000 and such power would expire (unless previously revoked, varied or extended by the Company as a general meeting) five years after the passing of the resolution save that the Company may before such expiry make an offer or agreement which would or might require such equity securities to be granted in pursuance of such offer or agreement or agreement as if the power conferred hereby had not expired;

(iv) adopt the Articles inter alia providing for the rights of the Ordinary ‘A’ Shares and Ordinary ‘B’ Shares.

Applications have been received in respect of 1,071,428 shares at £0.14 p/share under the terms of SEIS which will be allotted immediately prior to the remaining Ordinary ‘A’ shares under the Offer.

Save as disclosed above, there has been no issue of share capital of the Company since its incorporation and no share or loan capital of the Company is under option or agreed conditionally or unconditionally to be issued.

The issued share capital of the Company at the date of this document and following the Offer, assuming full subscription to the Offer is and would be £3,902,000

®

27

Information Memorandum

3. Articles of AssociationThe Articles contain, amongst others, the following provisions:

Shailen Jasani and Iqbal Dhanji, as Founders, are entitled at any time, by notice in writing to the Company, to appoint one Director each and to remove such person and appoint another person in his place. The so appointed Directors may be the Founders and shall not be required to retire by rotation.

Rights of Ordinary ‘A’ Shares Ordinary ‘B’ SharesOn a return in a liquidation or sale of the Company, the holders of Ordinary ‘A’ Shares and ‘B’ Shares shall be first entitled to a return of amounts subscribed. Thereafter the holders of Ordinary ‘A’ Shares and Ordinary ‘B’ Shares shall rank pari passu for returns pro rata to the number of shares held.

Save as specified the Ordinary ‘A’ Shares the Ordinary ‘B’ Shares shall rank pari passu in all respects.

Votes of membersSubject to any rights or restrictions attached to any shares and to any other provisions of the Articles:

(i) on a show of hands every member who is present in person shall have one vote;

(ii) on a poll every member who is present in person or by duly appointed proxy shall have one vote for every share of which he is the holder or for every share for which he has been appointed proxy or corporate representative.

Transfer of shares(i) The Ordinary ‘A’ Shares and the Ordinary ‘B’ Shares of the Company are transferable.

Dividends(i) Company may declare dividends

Subject to any statutes affecting the Company, the Company may by ordinary resolution declare dividends in accordance with the respective rights of the members, but no dividend shall exceed the amount recommended by the Board.

(ii) Board may pay interim dividends and fixed dividends Subject to the Act, the Board may declare and pay such interim dividends (including any dividend at a fixed rate) as appears to the Board to be justified by the profits of the Company available for distribution.

Share capital(i) Variation of rights

Subject to any statutes affecting the Company, all or any of the rights attached to any class may (unless otherwise provided by the terms of issue of the shares of that class) be varied with the written consent of the holders of three-fourths in nominal value of the issued shares of that class, or with the sanction of an extraordinary resolution passed at a separate meeting of the holders of the shares of that class. The provisions of the statutes affecting the Company and of the Articles relating to general meetings shall mutatis mutandis apply to any such separate meeting, except that the necessary quorum shall be not less than two

persons holding or representing by proxy not less than one-third in nominal amount of the issued shares of that class or, at any adjourned meeting of holders of shares of that class at which such a quorum is not present, shall be any such holder who is present in person or by proxy whatever the number of shares held by him.

Directors(i) Number of Directors

Unless otherwise determined by ordinary resolution of the Company, the number of Directors (disregarding alternate directors) shall not be less than two but shall not be subject to any maximum number.

(ii) Directors’ fees Each of the Directors shall be paid a fee for his services at such rate as may from time to time be determined by the Board provided that the aggregate of such fees (excluding any amounts payable under any other provision of these Articles) shall not exceed £250,000 per annum or such higher amount as the Company by ordinary resolution may determine from time to time. Such fee shall be deemed to accrue from day to day.

(iii) Remuneration of executive directors The salary or remuneration of any Director appointed to hold any employment or executive office in accordance with these Articles may be either a fixed sum of money, or may altogether or in part be governed by business done or profits made or otherwise determined by the Board, and may be in addition to or instead of any fee payable to him for his services as Director under these Articles.

Appointment of Directors(i) Power of the Company to appoint directors

The Company may by ordinary resolution appoint any person who is willing to act to be a Director, either to fill a vacancy on or as an addition to the existing Board.

(ii) Power of the Board to appoint Directors Subject to these Articles, the Board shall have power at any time to appoint any person who is willing to act as a Director, either to fill a vacancy or as an addition to the existing Board but the total number of Directors shall not exceed any maximum number fixed in accordance with these Articles.

(iii) Retirement of Directors At each annual general meeting of the Company, any Director in office who has been appointed by the Board since the previous annual general meeting, or for whom it is the third annual general meeting following the annual general meeting at which he was elected or last re-elected, shall retire from office but shall be eligible for re-appointment. An executive director shall not be subject to retirement by rotation.

Shareholder meetings(i) Subject to the requirements of the statutes affecting the Company, annual general

meetings shall be held at such time and place as the Board may determine.

(ii) The Board may convene an extraordinary general meeting whenever it thinks fit and shall do so if the statutes affecting the Company so require.

(iii) A general meeting shall be called by at least such minimum notice as is required or permitted by the Act. The period of notice shall in either case be exclusive of the day on which it is served or deemed to be served and of the day on which the meeting is to be

®

29

Information Memorandum

held and shall be given to all members other than those who are not entitled to receive such notices from the Company. The Company may give such notice by any means or combination of means permitted by the Act.

(iv) No business shall be transacted at any general meeting unless a quorum is present. If a quorum is not present a chairman of the meeting can still be chosen and this will not be treated as part of the business of the meeting. Two members present in person or by proxy and entitled to attend and to vote on the business to be transacted shall be a quorum.

4. Directors interests and other mattersAt the date of this document, the Directors are interested directly or indirectly in the issued share capital of the Company and their percentage holdings following the Offer, assuming it is fully subscribed:

Ordinary ‘A’ Shares Percantage Ordinary Capital

Percentage on full subscription

Shailen Jasani 26,000,000 50% 32.7%

Iqbal Dhanji 26,000,000 50% 32.7%

*Of the shares held by Messers Jasani and Dhanji, each will hold 1,987,500 shares in trust for the charity company to be set up and a further similar amount will be available for the referral scheme.

There are no loans or guarantees provided by the Company for the benefit of the Directors.

Shailen Jasani and Iqbal Dhanji each own 50% of the share capital of The Ralph Project Limited which company will enter into the management agreement with the Company as described in Material Contracts below.

There are no service contracts proposed to be entered into between the Directors and the Company. Shailen Jasani may provide his services as a clinical specialist in respect of which he will receive fees at the appropriate rate.

In addition to their directorships of the Company, the Directors are or have been members of the administrative, management or supervisory bodies or partners of the following companies or partnerships (which unless otherwise stated are incorporated in the UK) within the five years prior to the publication of this document:

Current Past

Shailen Jasani Khushi Ltd

The Mayhew Animal Home (a charity)

Iqbal Dhanji Azamour Investments Limited

EHDP Limited

Celebrations Global Limited

CFR (UK) (a charity)

Exhibition Road Cultural Group (a charity)

Mochron investments Limited (a South African company now in liquidation)

Except as disclosed above, within the past five years, no Director has:

(i) any convictions in relation to fraudulent offences or unspent convictions in relation to indictable offences;

(ii) had a bankruptcy order made against him or entered into an individual voluntary arrangement;

(iii) been a director of any company or been a member of the administrative, management or supervisory body of a company or a senior manager of a company which has been placed in receivership, compulsory liquidation, creditors’ voluntary liquidation, administration, company voluntary arrangement or which entered into any composition or arrangement with its creditors generally or any class of its creditors whilst he was acting in that capacity for that company or within the 12 months after he ceased to be so acting;

(iv) been a partner in any partnership placed into compulsory liquidation, administration or partnership voluntary arrangement where such director was a partner at the time of or within the 12 months preceding such event;

(v) been subject to the receivership of any asset of such director or of a partnership of which the director was a partner at the time of or within 12 months preceding such event; or

(vi) been subject to any official public incrimination and/or sanctions by any statutory or regulatory authority (including designated professional bodies) nor has he been disqualified by a court from acting as a director of a company or from acting as a member of the administrative, management or supervisory bodies of an issuer or from acting in the management or conduct of the affairs of any issuer.

Other than as set out in this document, no Director has been interested in any transaction with the Company, which was unusual in its nature or conditions or significant to the business of the Company during the current financial year, which remains outstanding or unperformed.

®

31

Information Memorandum

5. Material ContractsThe following material contracts (not being contracts entered into in the ordinary course of business) have been entered into by the Company within two years preceding the date of this document:

By agreement made on 9th December 2015 the Company appointed Sapphire Capital Partners LLP (“Sapphire”) to assist in the Offer on the following terms:

• thesumof£2,000plusVATforobtainingAdvancedAssurancefromHMRevenue&Customs that the Company’s trade will be eligible for EIS relief;

• anarrangementfeeof2%oftheamountofsharecapitalsubscribedbyinvestorsintroduced by Sapphire and an arrangement fee of 1% of the amount of share capital subscribed by investors not introduced by Sapphire.

In addition it is proposed for the Company to enter into a management services agreement with The Ralph Project Limited (“Service Company”), a company in which the Directors are interested on the following terms:

• theServiceCompanywillprovidemanagementservicestotheCompanyforaminimumfee of £50,000 per annum. This will be reviewed regularly and adjusted in the light of the performance of the business. VAT will additionally be payable if applicable.

• theServiceCompanywilllicencetheuseofthename“The Ralph” in the Company’s business the rights to which name shall belong to the Service Company.

6. Working capitalTaking into account the minimum net proceeds of the Offer, assuming the Offer raises the minimum amount the Directors are of the opinion that the Company has sufficient working capital for its present requirements, that is for at least 12 months from the date of this document.

7. LitigationThe Company is not engaged in legal or arbitration proceedings, active (or so far as the Company is aware pending or threatened) against, or being brought by, the Company which are having or may have a significant effect on the Company’s financial position.

8. Other informationThe Company’s accounts will be prepared under the historical cost convention and in accordance with applicable accounting standards in the United Kingdom. The accounts will be drawn up on a going concern basis

The accounting reference date of the Company is 31 December each year. Financial statements have not been prepared or filed with the Registrar of Companies since incorporation

9. Documents available for InspectionCopies of the following documents may be inspected at the registered offices of the Company during usual business hours on any week day (weekends and public holidays excepted), or can be emailed on request:

(i) The Articles.

(ii) HM Revenue & Customs EIS advance assurance letter.

(iii) The contracts referred to in the section headed Material Contracts.

®

33

Information Memorandum

SECTION 7: PROPOSED TERMS OF THE OFFER

1. The OfferThe Company is seeking to raise a minimum amount of £2,950,000 under the Offer, with a Maximum Subscription of £3,700,000.

The Offer will be made for up to 26,428,572 Ordinary ‘A’ Shares at the Offer Price of £0.14 per Ordinary ‘A’ Share. Applications by Investors must be for a minimum of 70,000 Ordinary ‘A’ Shares, which equates to £9,800.

The Company is therefore seeking to raise £3,700,000 through its offer to Investors for subscription in 26,428,572 Ordinary ‘A’ Shares at a price of £0.14 each.

2. Conditions to the Offer

The Offer will be subject to the following conditions being satisfied on or before the Closing Date:

• TheMinimumSubscriptionof£2,950,000beingreached.

The Directors will not proceed to allot and issue Ordinary ‘A’ Shares to Investors until the above conditions have been satisfied and if any of the conditions have not been satisfied on or before the Closing Date, Investors’ monies will be returned without interest. It is noted that no part of the Offer has been underwritten.

3. How to ApplyAfter reading this Information Memorandum if you are interested in investing you should register your interest with the Company online by visiting www.theralph.vet. Potential Investors are welcome to contact the co-founders via email:

4. Terms for IntermediariesThe Company is prepared to pay commissions for introductions by regulated intermediaries. For further details, please contact the Company.

®

35

Information Memorandum

SECTION 8: RISK FACTORS

The Directors believe that the principal risk factors relevant to investing in the Company are as set out below. The following risk factors should be considered, but it should be noted that these are not exhaustive and not in any particular order of priority.

Potential Investors should be aware that the various tax advantages currently available might change in future. This document is based on the understanding of the existing law and HMRC practice as at the date of this document. Future changes to the tax legislation may adversely affect the performance of the Company and the return to the Investor.

1. Investment Risks

• Subscribingforsharesinacompany,whichwillbeunquoted,involvesadegreeofrisk.Itmay be difficult to obtain information on the current value of the Shares and as there is no formal market for the Shares it may be difficult for Investors to realise their investment. Investors should note that the value of shares may go down as well as up and there is no certainty that Investors will get back the full amount that they invest and may consequently lose some or all of the monies invested. Past performance and the experience of the Directors is no guide to future performance and hopes, assumed performance, aims, targets, plans, financial illustrative returns or intentions contained in this document are no more than that and should not be construed as forecasts.

• ThereisnoguaranteethattheCompany’sstrategyortradingactivitieswillbesuccessful.The returns from the trading activities undertaken will inevitably vary from the target financial returns set out in this Information Memorandum.

• ItisnotintendedthatanyincomeorcapitalwillberealisedbyInvestorsforatleastfouryears. Even then it may be difficult to sell an investment in the Company. Although it is hoped that exit routes will be available, for example via a trade sale, there is no guarantee that there will be any exit route for Investors.

2. Risks Relating to the Company

• TheCompany’sbusinessstrategydependsontheabilityoftheDirectorsandmanagementto successfully execute the business plan to set up and run a multidisciplinary small animal specialist referral hospital as described. If there are any delays or other factors outside the control of the Directors and the management, this may have a materially adverse effect upon the trading performance and value of the Company and ultimately upon the value of its Shares.

• TheCompany’sfuturesuccessissubstantiallydependentontheperformanceoftheDirectors and management and their ability to recruit and retain the relevant Specialists and staff. The Directors cannot give assurances that the Specialists recruited will remain with the Company, although the Directors believes the Company’s remuneration packages will be attractive and the Specialists and staff will be committed to the long term success of the Company. The loss of service of any of the Specialists and other key employees could damage the business of the Company.

• Anydelaysinsecuringtheappropriatepremisesand/orintherefurbishmentofthepremises to make it ready for use may impact returns. The Company is reliant on its contractor to deliver the premises within an agreed time frame. It is also dependent on the strength of its contractor. As far as possible, risks will be passed on to its contractor and the Company will cover risks such as specification risks.

• TheillustrativefinancialprojectionsinthisdocumentarebasedonThe Ralph being referred a certain number of average cases per specialist per week and achieving a certain average income per case.

• Asignificantcompetitoropeninginthesamegeographicallocationcouldimpactonthenumber of referrals to The Ralph. Given the Board-certified specialist status of clinicians to be employed by The Ralph and the intention to position the hospital as reasonably priced for the services provided, it is anticipated that the hospital will receive referrals from a wide geographical catchment.

• Increasingsectorcorporatisation-overthelast10to15yearstherehasbeenagrowingtrend towards corporatisation of the primary care veterinary sector. A recent phenomenon among corporates is to acquire or establish referral centres to which to then feed primary care cases internally, i.e. creating an internal referral vertical. These trends may have an impact on the referral base for The Ralph and other independent referral centres.

• Potentialchangesinthepetinsurancemarket.Researchsuggeststhat85%ofpetstreatedby top tier referral centres are insured and clearly the referral sector, especially at the top end, is highly dependent on a stable and growing pet insurance market. Any changes to the pet insurance market could have an impact on The Ralph.

• RoyalSunAlliancehasrecentlypublishedalistofpreferredreferralcentres.Howeveratthe time of writing, the new RSA policy does not apply to the emergency/non-elective cases which are expected to be a significant percentage of the new hospital’s caseload. RSA continues to invite applications from referral centres to be included on their list which The Ralph will undertake once operational.

• AtthetimeofpreparingthisInformationMemorandum,thepremiseshasyettobesecured. If a lease tenure cannot be secured, the business model may change substantially if a property has to be acquired or a new one built.

3. Taxation Risks

• Itispossiblethatlegislationmaychangeinthefuture,ormaybeintroducedwithretrospective effect. This may affect the conditions under which tax reliefs were granted, the assumptions relating to the yields shown, or the qualifying status defined.

• IftheCompanyceasestocarryonthetradingactivitiesoutlinedinthisdocumentandisnot then carrying on other permitted business activities, or if it carries on an activity other than a permitted business activity, this could result in its failing to comply with the relevant regulations and loss of SEIS and / or EIS benefits for investors.

• AlthoughtheCompanyhasobtainedadvanceassurancefromHMRevenue&Customsthat the Company’s activities qualify under EIS, there is no guarantee that formal EIS claims will be agreed or that such agreement will not be subsequently withdrawn and in those circumstances subscription monies will not be returned to Investors. Returns to Investors would be lower in the event that the Company ultimately fails to obtain SEIS and / or EIS status or that it is subsequently withdrawn, in which case the SEIS Reliefs and the EIS Income Tax Relief and Capital Gains Tax Deferral Relief referred to in this document would not be granted.

• UnderSEISandEISrulestheCompanyisrequiredtohaveemployed100%ofitsnetfunds (after the deduction of issue costs) within 24 months of the later of the date of commencing its qualifying trade or the date of the issue of the Ordinary ‘A’ Shares. If the Company fails to employ this level of funds within the required deadline, the Company would have breached SEIS and EIS rules and tax relief would be withdrawn from Investors. Investors would then be liable to repay any income tax rebate previously received to HMRC.

• AnylossofstatusofaSEISand/orEISQualifyingCompany,whetherthroughactionstakenby the Company or otherwise, may lead to the loss of Tax Advantages for the Investor. No guarantee can be given that all investments will qualify, or continue to qualify, for the Tax Advantages.

• IndividualtaxcircumstancesmaydifferfromInvestortoInvestorandpersonswantingtoinvest are advised to seek specific tax advice based on their personal circumstances.

4. Other risks

• TheUKFinancialServicesCompensationSchemewillnotapplytoInvestorsintheCompany. In addition, Investors in the Company will not have access to the UK Financial Ombudsman Service.

• CertaininformationcontainedinthisInformationMemorandumconstitutes“forward-looking statements,” which can be identified by the use of forward-looking terminology such as “assumed” “example” “illustrative” “may,” “will,” “should,” “expect,” “intend,” “anticipate,” “project,” “estimate,” “plan,” “seek,” “continue,” “target,” or “believe,” or the negatives thereof or other variations thereof or comparable terminology, and include projected or targeted minimum returns to be made by the Company. Such forward looking statements are inherently subject to material economic, market and other risks and uncertainties, including the risk factors set out in the Summary and Risk Factors sections of this Information Memorandum and, accordingly, actual events or results or the actual performance of the Company may differ materially from those reflected or contemplated in such forward-looking statements.

• Investorsshouldnotplaceunduerelianceon“forward-lookingstatements”,whichspeakonly as of the date of this Information Memorandum.

• AninvestmentintheCompanyshouldbeviewedasalongerterminvestmentandmaynot be suitable for all recipients of this document. A prospective Investor should consider carefully whether an investment in the Company is suitable for them in the light of their personal circumstances and the financial resources available to them.

• TheCompanyshallnotbeliabletoanyInvestorintheeventofaninsolvencyofanybankwith which such funds held by the Company have been deposited nor in the event of any restriction on the ability of the Company to withdraw funds from such bank for reasons which are beyond the reasonable control of the Company.

®

39

Information Memorandum

SECTION 9: TAX BENEFITS

The summary below gives a brief outline of the Tax Advantages. It does not set out all of the rules that must be met and is intended only as a general guide of UK tax law. This summary should not be constructed as constituting tax advice which Investors should obtain from their own professional advisers before investing in the Company. The taxation levels, bases and reliefs described in the summary below are based on existing law and what is understood to be current HMRC practice, but this may be subject to change in the future.

As the majority of the investment will be eligible for EIS relief, this Information Memorandum deals only with the tax reliefs associated with EIS. Investors wishing to learn more about Seed EIS and associated tax reliefs should seek independent tax advice and/or contact HMRC.

Tax Advantages

The Tax advantages for Investors making investments in the Company include the following:

Income Tax Relief- EISIndividuals may subscribe for shares and obtain Income Tax Relief at up to 30% on amounts of up to £1,000,000 in any one income tax year. This provides a maximum income tax reduction of £300,000 in any one year. Income Tax Relief is given in the income tax year in which investment is made or can be carried back to the prior year.

Under current rules an individual may carry back unused Income Tax Relief arising at any time in one income tax year to the previous income tax year of any amount up to the full amount of the subscription. This is subject only to the overall cap of £1,000,000 per income tax year, and subject to the individual having sufficient income tax liability to utilise the Income Tax Relief.

The certificate stating and confirming the Income Tax Relief obtainable by an individual is on a Form EIS 3 issued by the Company. The latest date on which an Investor can claim Income Tax Relief is five years after 31 January following the tax year to which the claim relates.

EIS Income Tax Relief will be withdrawn in whole or in part if an individual’s shares are not held for three years from the beginning of the EIS Qualifying Period, or if the individual is or becomes “connected” with the EIS Qualifying Company in which an investment is made during the period beginning two years before and ending three years after the date of investment in the EIS Qualifying Company. There are other circumstances in which Income Tax Relief could be withdrawn which have not been detailed here.

Example £

Initial Investment 10,000

Less EIS Relief at 30% (3,000)

Net cost of Investment 7,000

Capital Gains DeferralIndividuals can defer CGT chargeable gains by subscribing for eligible shares in an SEIS or EIS Qualifying Company of an amount equivalent to the chargeable gain. The investment must be made in the period beginning twelve months before and ending three years after the date of the disposal giving rise to the capital gains to be deferred.

Deferral of a capital gain is only a deferral of the original liability to CGT. The capital gain is deferred until there is a chargeable event, such as a disposal of the shares in the EIS Qualifying Company. The value of deferral depends on the tax rate applying to the gains in question. It should be noted in particular that the rate of CGT prior to 23 June 2010 was 18%, but since that date the rate depends on other taxable income and could be 18% or 28%. Some gains may have benefitted from a lower rate than the above rates by reason of Entrepreneur’s Relief. Accordingly Investors should seek the advice of their tax advisers before evaluating the effect of deferral of CGT.

®

41

Information Memorandum

Inheritance Tax Relief (“IHT”)The shares held by Investors should in most cases qualify for 100% of IHT Business Property Relief in the event of the death of an Investor or any other chargeable transfer as long as the shares have been held for two years from the date they were issued to the Investor.

Exemption from Capital Gains Tax (“CGT”)No CGT is payable on capital gains realised on the disposal of shares in an EIS Qualifying Company provided that the shares are held for at least three years from the date of the Investment (or from the date of commencement of the EIS Qualifying Company’s trade, if later) and are investments in respect of which Income Tax Relief had been obtained and not withdrawn.

Example £

Realised value of Investment after 3 years 13,000

Less initial Investment (10,000)

Tax free gain 3,000

Loss ReliefAny capital losses realised in respect of a qualifying investment in an EIS Qualifying Company (net of Income Tax Relief attribute to the investment), qualify for loss relief so that the capital loss can be set off against capital gains of that tax year or a later tax year or against total income of that tax year or total income of the preceding tax year.

SECTION 10: QUESTIONS AND ANSWERS

If you have any questions regarding the Offer or the Company please email us in the first instance as follows:

1. How does it work?Investors will subscribe for new Ordinary ‘A’ Shares in The Ralph Veterinary Referral Centre PLC for investment purposes.

2. What is the advantage of investing in The Ralph Veterinary Referral Centre PLC?

The Company aims to provide a targeted return of 21.7 pence for every one share at 14 pence. (equivalent to £1.54 per total £1 invested) over a four-year period for EIS qualifying investors. The return is based on the period from the issue of the Shares to return of funds. If for example, the targeted return of 21.7 pence for every one share at 14 pence (or £1.54 for every £1 total invested) is achieved in a four-year period, the Internal Rate of Return (IRR) to EIS qualifying investors will be 21.8% per annum tax free, which is the equivalent to 27.2% to a basic rate taxpayer, 36.3% per annum gross to a higher rate taxpayer or 39.6% per annum gross to an additional/top rate taxpayer.

3. How will I realise my investment?The Company will actively monitor opportunities for Investors to realise their investment at the end of the three year EIS qualifying period, with an expected exit to occur after four years.

Possible routes for a realisation include:

• re-financingbytheCompanyandutilisingsignificantbankdebtasameansofreturningfunds to Investors

• asaleofsharestoathirdparty,

• amanagementbuyout.

At the present time, the Directors consider a management buyout or a Company buy-back through debt restructuring as the most likely exit routes. For either of these two exits, it is likely that the Shareholders will realise their investment for cash.

Please note that the Company can make no guarantee about the timing of the realisation of an investment in the Company. Potential Investors should be aware that EIS investments may be considered risky and the Ordinary ‘A’ Shares and must be considered a longer term investment.

4. What happens if I die during the term?In the event of the death of an Investor, the shareholdings may be transmitted to the executors or other personal representatives.

In the event of a liquidation of the investment the proceeds will go to the named shareholders. Investments held for a minimum of two years are, under current legislation, exempt from Inheritance Tax.

Income Tax Relief is not clawed back in the event of death.

If an Investor took advantage of Capital Gains Tax Re-Investment Relief and subsequently dies, the original gain does not come back into charge.

5. What is the minimum and maximum investment I can make?

The minimum investment is £9,800. There is no maximum investment, however for EIS qualifying investment, they cannot own more than 30% (together with persons connected with them) of the Ordinary Shares in order to qualify for Income Tax Relief.

6. Can I own my investment jointly with my spouse/ civil partner?

No, but spouses/civil partners can each make individual investments.

7. How do I check the progress and performance of the Company?

Investors will be provided with a copy of the financial statements annually.

8. What are the “qualifying conditions” of an EIS investment?

An EIS investment affords various tax benefits for an Investor (who meets the EIS qualifying conditions) and in turn it is important that the qualifying conditions for both an Investor and the Company are adhered to throughout the term of the investment. The qualifying conditions can be complex, but the main conditions for EIS investments are summarised below. The Directors do not intend to breach these conditions.

• Theremustbenopre-arrangedexit.Thereforenoguaranteecanbemadethatmoneywillbe returned to the Investor.

Investor

The Investor qualifying conditions are as follows:

• ForIncomeTaxReliefpurposes,theInvestorcannotbe‘connected’totheCompanyinthetime period beginning two years before the issue of the shares, and ending immediately before the termination date. Connection can occur in several ways:

1) the Investor is an employee, director or partner of the Company,

2) the Investor subscribes for shares under certain arrangements. Broadly an arrangement would be where an Investor subscribes for shares in the Company in return for investment in their own Company.

®

45

Information Memorandum

• TheInvestorscannothaveany‘linkedloans’.TheDirectorswillnotacceptloansfromInvestors and as such, an Investor should not fail this requirement.

• TheInvestorcannotinvestforthepurposeoftaxavoidance.Theshareswillbesubscribedfor genuine commercial reasons and not as part of a scheme or arrangement involving the avoidance of tax. The ‘avoidance of tax’ term in this respect is an odd one as many Investors will subscribe purely for the tax benefits, however, it is understood that the use of the term ‘tax avoidance’ in this respect refers to a broader scheme of avoidance to which Income Tax Relief is also party, and therefore investment in the Company for Income Tax Relief should not be a concern.

Articles The articles of association of the Company.Board or Directors or Director The Board of Directors of the Company or any one of them, whose

names are set out in Section 6.Business Property Relief Business property relief available for qualifying shares under IHTA

1984.Capital Gains Tax Deferral Relief The deferral of capital gains tax by investment in Ordinary Shares in

an EIS Qualifying Company.Company The Ralph Veterinary Referral Centre PLC, which company passed

a resolution to change its name from The Ralph Project Plc on 12 February 2016.

EIS The Enterprise Investment Scheme as set out in ITA 2007.EIS Qualifying Company A company meeting the qualifying conditions, as set out in ITA 2007.EIS Relief or Income Tax Relief Income Tax Relief available for qualifying Investors, as defined in ITA

2007.Financial Adviser A professional (such as an IFA) who renders financial planning

services to individuals and companies.FCA The United Kingdom Financial Conduct Authority.FSMA The United Kingdom Financial Services and Markets Act 2000.IFA An independent Financial Adviser regulated by the FCA, or a similarly

qualified and regulated Financial Adviser in other jurisdictions.IHTA The Inheritance Tax Act 1984, as amended.Information Memorandum This information memorandum as amended, substituted or

supplemented from time to time.Investor The persons who subscribe for the Ordinary ‘A’ Shares pursuant to

the Offer.ITA 2007 The Income Tax Act 2007, as amended.Minimum Investment The minimum investment by an applicant is £9,800.Minimum Subscription The aggregate minimum subscription of £2,950,000 by Investors

pursuant to the Offer.Offer The proposed offer of Ordinary ‘A’ Shares to be made by the

Company.Offer Price £0.14 per Ordinary ‘A’ Share.Ordinary ‘A’ Shares The ordinary shares in the capital of the Company having the rights

set out in the Articles.Qualifying Business Assets Assets which qualified for 100% Business Property Relief for

Inheritance Tax purposes.Qualifying Investors Investors who qualify for full Income Tax Relief on their investment in

Ordinary Shares.Shareholders The holders of Shares.Shares The entire issued share capital in the Company from time to time.Subscription The subscription for Ordinary ‘A’ Shares under the Offer.Tax Advantages The various tax advantages, including EIS Relief, arising from

subscriptions for shares in EIS Qualifying CompaniesUK or United Kingdom United Kingdom of Great Britain and Northern Ireland.

Capitalised terms used in this Information Memorandum and not otherwise defined in this Information Memorandum have the meanings ascribed to them in the Articles.References in this Information Memorandum to statutory or regulatory provisions shall be construed as references to those provisions as amended or re-enacted from time to time. References to the singular include the plural and vice versa and references to one gender include all genders. All references to time are references to UK time.

notes

theralph.vet

desig

n by

new

engl

ish.c

o.uk

Potential Investors are welcome to contact us for any clarification. For general enquiries email Shailen Jasani, [email protected] or for investment enquiries email Iqbal Dhanji, [email protected]

Why ‘The Ralph’ ?Ralph was an adorable rescue cat that Shailen helped to treat after he (Ralph) was hit by a car in 2008. They went on to spend two years sharing a home together before Ralph passed in 2010. It was in his memory that Shailen set up The Ralph Site (theralphsite.com), a non-profit online pet loss community that supports countless carers through the bereavement process. The site is complemented by a public Facebook page, which now has over 41,000 followers, and a thriving private Facebook group.