24

Asian Petrochemicals Markets Conference 2017 Insights into GCC Petrochemical Industry April 19, 2017 Samir Al-Jishi General Manager, Strategy & Business Development Sipchem

| Date post: | 27-Mar-2018 |

| Category: |

Documents |

| Upload: | nguyenkhuong |

| View: | 218 times |

| Download: | 2 times |

Asian Petrochemicals Markets Conference 2017

Insights into GCC Petrochemical Industry

April 19, 2017

Samir Al-Jishi General Manager, Strategy & Business Development Sipchem

2

Contents

Introduction to Sipchem

Overview of Petrochemical Industry in GCC

Adopted strategies by GCC government and

Petrochemical companies

Where GCC companies are looking at

What is the relation with Asia

3

Contents

Introduction to Sipchem

Overview of Petrochemical Industry in GCC

Adopted strategies by GCC government and

Petrochemical companies

Where GCC companies are looking at

What is the relation with Asia

4

• Established in 1999, in Saudi Arabia. • Produces 2.7 million tons of basic,

intermediate and polymers. • Sells products globally through its

offices in Saudi Arabia, Switzerland and Singapore

• Strategic partnership with reputable international companies as equity partner, licensor or off-taker.

• State of art R&D facilities. • Employs 1000+ people from various

nationalities.

Saudi International Petrochemical Company

5

Wire & Cable, EVA/LDPE, EVA film, PBT, and TMF plant commenced operations.

2012

Established marketing unit in Singapore

Acquired Aectra, (Marketing in Europe)

Achieved Responsible Care Certification

1999 Incorporated as a

closed joint stock company

2005

Methanol plant commenced operations

2006 Went public

through a successful IPO

2007 Established

Sipchem Marketing Company

2010 CO, Acetic Acid,

and VAM plants commenced operations

2011 2013 EA / BA plants

commenced operations

Sipchem Overview Our Journey and growth

2014

BDO plant commenced operations

2004

2015 MANAR

inauguration

6

Sipchem Overview Locations in Saudi Arabia

Khobar

Jubail

Dhahran Jubail ● Dammam ●

Riyadh

Jeddah ● Mecca ●

Medina ● Yanbu ●

Doha ●

Dubai ●

Dhahran ● Khobar

Sipchem

Technology and

Innovation

Center

(MANAR)

Headquarter

World-scale

integrated

manufacturing

complex

Riyadh

Ha'il

Tools and

Manufacturing

Facilities

Ha'il EVA films

7

Contents

Introduction to Sipchem

Overview of Petrochemical Industry in GCC

Adopted strategies by GCC government and

Petrochemical companies

Where GCC companies are looking at

What is the relation with Asia

8

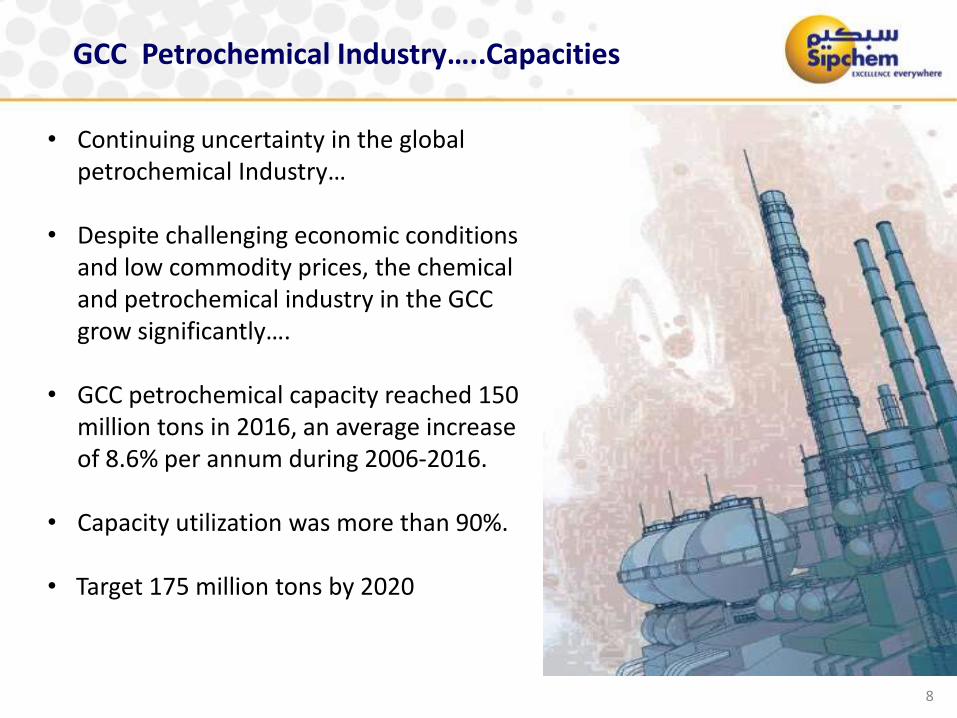

• Continuing uncertainty in the global petrochemical Industry…

• Despite challenging economic conditions

and low commodity prices, the chemical and petrochemical industry in the GCC grow significantly….

• GCC petrochemical capacity reached 150

million tons in 2016, an average increase of 8.6% per annum during 2006-2016.

• Capacity utilization was more than 90%.

• Target 175 million tons by 2020

GCC Petrochemical Industry…..Capacities

9

GCC Petrochemical Industry….. Saudi Arabia leads…

Source: GPCA Annual Report

10

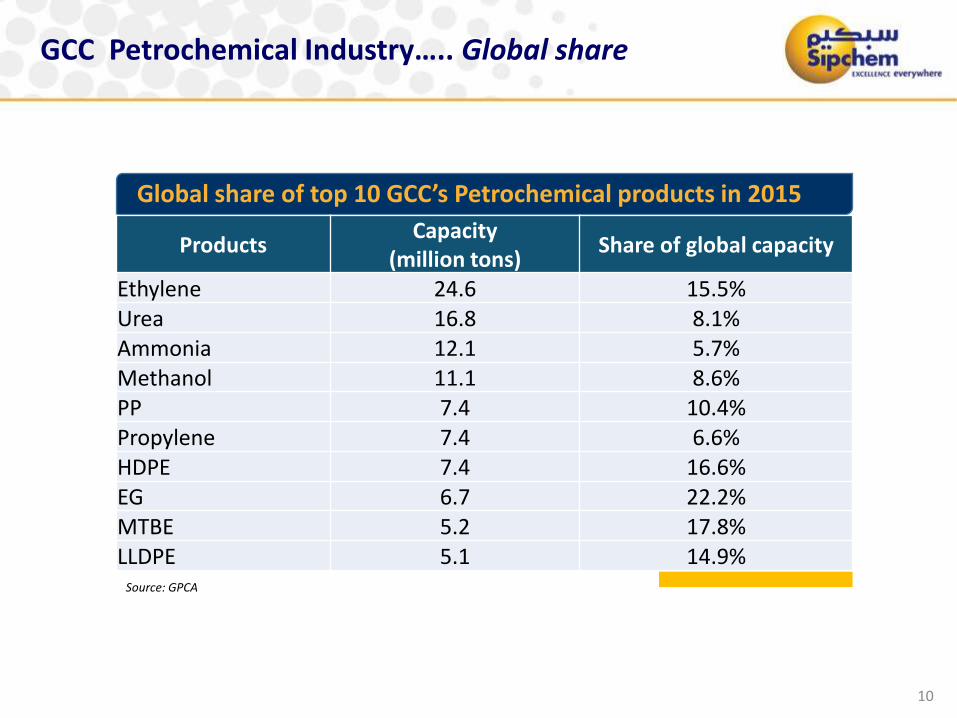

GCC Petrochemical Industry….. Global share

Source: GPCA

Global share of top 10 GCC’s Petrochemical products in 2015

Products Capacity

(million tons) Share of global capacity

Ethylene 24.6 15.5% Urea 16.8 8.1% Ammonia 12.1 5.7% Methanol 11.1 8.6% PP 7.4 10.4% Propylene 7.4 6.6% HDPE 7.4 16.6% EG 6.7 22.2% MTBE 5.2 17.8% LLDPE 5.1 14.9%

11

GCC Petrochemical Industry…..Investment

• More petrochemical complexes are being established • New Projects worth US$ 13 billion were announced in 2016 in the

region, coming online between 2020-2024. • Taking steps to diversify the product lines beyond basic gas-based

chemicals to overcome the diminishing feedstock advantage.

12

GCC Petrochemical Industry….. Key Assumptions for Future Investments…

• Global crude oil price scenarios.

• Global economic growth outlook.

• North American energy market.

• China structural changes.

• Iran sanctions.

• India’s economic growth.

• Non-conventional technology.

• Sustainability.

• Level of integration.

• Functional excellence.

• Geopolitical considerations.

13

GCC Petrochemical Industry…..Competitive advantages

• Feedstock drives the industry: o flexibility; mixed feedstock o Reliability of supply o Cost advantage

• Energy advantage; o one-third of the oil and one-fourth of the world’s natural gas reserves

are found in the region. o Low cost of energy….

• Ongoing expansion of value chain… • Business friendly tax regime… • Relaxed terms on Financing from government institutions

• Well developed infrastructure & ideally located close to the major markets.

14

Contents

Introduction to Sipchem

Overview of Petrochemical Industry in GCC

Total Production

Total Investment

Competitive Advantages

Adopted strategies by GCC government and Petrochemical companies

Where GCC companies are looking at

What is the relation with Asia

15

GCC Petrochemical Industry…..adopted strategies

• Consolidation and privatization to counter weak product prices, optimize cost and introduce new efficiencies o Creating synergies and optimizing current

assets

• Companies look for growth through acquisitions……………

• Encouraging more local production of consumer and business goods for both domestic and export markets……

16

GCC Petrochemical Industry…..adopted strategies

• Greater functional excellence; o Commercial; strengthen sales and marketing capabilities by reducing

reliance on off takers and traders/agents, avoid 3-5% of their product value to middlemen.

o Operational; improve plant reliability, drive down fixed and variable costs.

o Innovation excellence; going farther downstream and increasing specialization of products

17

New strategy to respond…..

A new strategy to respond to the

competitive threats

Explore new gas targets Expand into

performance and specialty value added

products

Invest in petrochemical

projects in driven by Shale Gas

A bio-based alternative to conventional polyethylene

Diversify business model

Merger & Acquisition of basic chemical

producers

Competitive feedstock

supply from upstream to downstream

Invest in the right

technology

R&D Center

18

Contents

Introduction to Sipchem

Overview of Petrochemical Industry in GCC

Total Production

Total Investment

Competitive Advantages

Adopted strategies by GCC government and Petrochemical companies

Where GCC companies are looking at What is the relation with Asia

19

Where GCC companies are looking at …..

• Expanding downstream sector (specialty chemicals): o better profit margin o develop domestic market

• GCC have been looking for new markets in Asia to substitute the decreasing export to other region, particularly in Europe (as Iran gears up to re-enter markets).

• New frontier markets including in Africa:

o Egypt and Nigeria are seen as the next frontier for future growth. o need to compete against relatively less disadvantaged competitors.

Develop domestic markets & maintain access to the international market is crucial…

20

Where GCC companies are looking at …..

• Chinese overseas investment is active; Saudi Arabia to link Chinese investments in Saudi Arabia to the facilitation of more Saudi downstream investments in China..

• Saudi Arabia’s move to invest USD 13 billion in new projects in Malaysia

and Indonesia will play an important part in the Kingdom’s plan:

o to diversity its economy and reduce its dependence on oil revenue,

o ensuring that it will maintain its market share in the region

21

Contents

Introduction to Sipchem

Overview of Petrochemical Industry in GCC

Total Production

Total Investment

Competitive Advantages

Adopted strategies by GCC government and Petrochemical companies

Where GCC companies are looking at

What is the relation with Asia

22

What is the relation with Asia ..

• China has a high cost of ethylene due to the long production chain: o Coal gasification o Methanol synthesis o MTO

• Increasing consumer spending will continue to drive consumption of basic chemicals and plastics. o > 75% of Chinese plastics demand is

in consumer non-durable.

• Asia has become the GCC’s most important trading partner, accounting for importing around 70% of its oil exports.

23

In Brief…..

• The chemical and petrochemical industry in the GCC grows significantly.

• Capacity utilization is very high.

• Feedstock drives the industry.

• Diversify the product lines beyond basic gas-based chemicals.

• Maximum utilization of energy advantage.

• Creating synergies and optimizing current assets.

• Develop domestic markets

• Turning to new frontier markets including in Africa.

GCC protects its leadership position in the global Petrochemicals & Chemicals industry

THANK YOU