INTERNATIONAL CONVENTION AND EXHIBITION CENTRE FEASIBILITY STUDY Prepared for Auckland City Council July 2009 CONSULTANTS TO THE HOTEL, TOURISM & LEISURE INDUSTRIES A member of Horwath International prepared in conjunction with

Transcript

INTERNATIONAL CONVENTION AND EXHIBITION CENTRE

FEASIBILITY STUDY

Prepared for Auckland City Council

July 2009

CONSULTANTS TO THE HOTEL, TOURISM & LEISURE INDUSTRIES A member of Horwath International

prepared in conjunction with

International Convention and Exhibition Centre – Feasibility Study Page 2 Auckland City Council July 2009

CONTENTS

1. INTRODUCTION AND EXECUTIVE SUMMARY 3

2. HISTORICAL CONFERENCE ACTIVITY 18

3. CURRENT AND EXPECTED FUTURE MARKET TRENDS 40

4. NEW ZEALAND’S COMPETITIVE POSITION 50

5. SITE SELECTION CRITERIA AND LOCATION ANALYSIS 54

10. PUBLIC / PRIVATE OWNERSHIP, GOVERNANCE, OPERATIONS 91 APPENDICES

1A. BENEFIT-COST CALCULATIONS 96

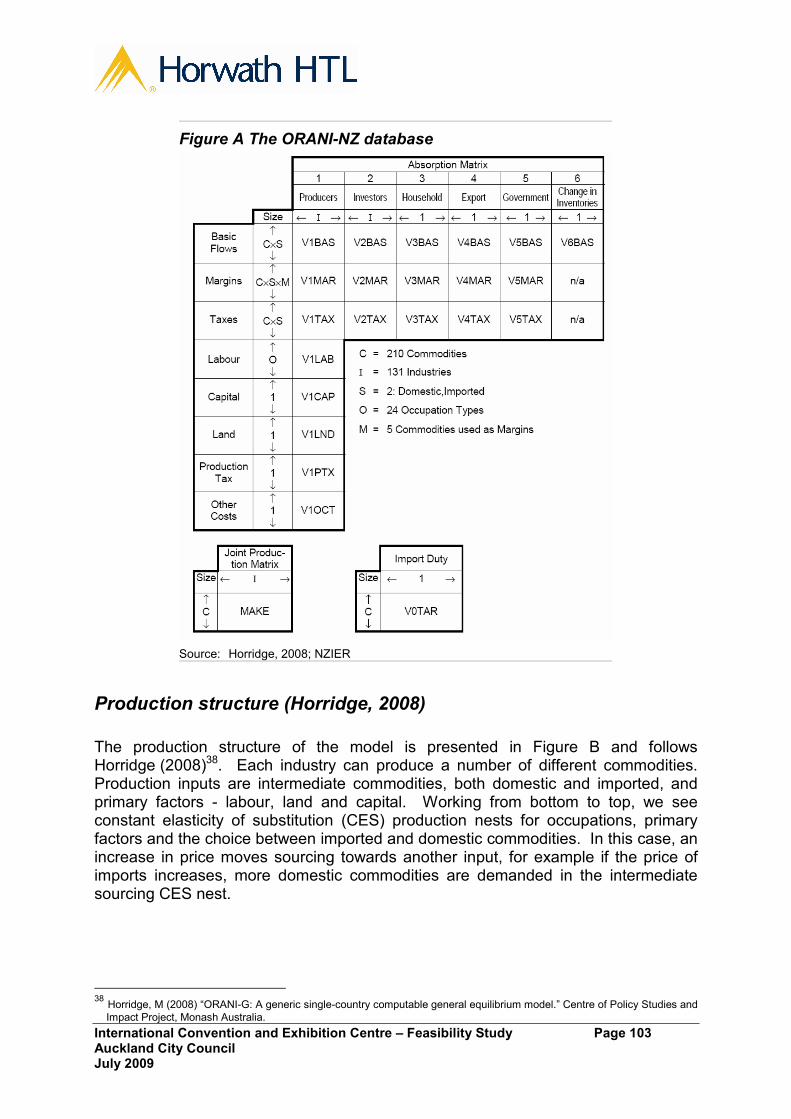

1B. TECHNICAL DETAIL OF THE NZIER MODEL 102

2. INTERNATIONAL PCO SURVEY 107

3. FEEDBACK FROM THE CONFERENCE COMPANY CLIENTS 125

4. INTERNATIONAL BAR ASSOCIATION CONVENTION NOTES 127

5. NEW ZEALAND VENUE COMPARISON 131

6. ASIA PACIFIC INTERNATIONAL CONVENTION AND EXHIBITION CENTRES 134

7. INTERNATIONAL ASSOCIATION CONFERENCES WITH NZ CONTACT 135

8. INTERVIEWEES / INFORMATION SOURCES 136

International Convention and Exhibition Centre – Feasibility Study Page 3 Auckland City Council July 2009

1. INTRODUCTION AND EXECUTIVE SUMMARY

1.1 BACKGROUND A Reference Group has been formed to oversee this feasibility study. The Reference Group comprises:

� Auckland City Council (John Duthie, General Manager, City Development)

� Ministry of Tourism (Ray Salter, General Manager)

� Ministry of Economic Development (Louise Marra, Director, Government Urban and Economic Development Office)

� Conventions and Incentives New Zealand (John Duncan, Chair).

The project has been managed on behalf of the Reference Group by:

� Auckland City Council (Gareth Stiven, Group Manager Economic Development)

� Ministry of Economic Development (Jami Williams, Chief Advisor, and Tariq Ashraf, Senior Policy Analyst, Government Urban and Economic Development Office).

1.2 SCOPE OF WORK AND APPROACH The agreed scope of work and approach is documented in the engagement letter from Auckland City, dated 30 April 2009, which is based on the Request for Quotations letter dated 14 April 2009, our letter dated 20 April 2009 and e-mail dated 22 April 2009. The scope of work and approach is as follows:

� conducting a robust assessment of the market for the proposed international convention and exhibition centre. This has involved:

o an assessment of economic climate and market. This has included conducting discussions with CINZ, leading convention centres and PCOs in New Zealand and Australia on current trends in conference activity with specific focus on the Asia / Pacific region; and undertaking a review of the ICCA database of the international convention centre activity concerning past “shocks” and the recovery

o an environmental considerations assessment concerning convention activity, convention centre design and market assessment. This has included conducting discussions and securing relevant sustainability information from MCI and global organisations such as Green Meetings Industry Council, Convention Industry Council based in the US, Green Globe Standards. From within New Zealand we have obtained

International Convention and Exhibition Centre – Feasibility Study Page 4 Auckland City Council July 2009

information from CINZ’s “Sustainability Action Group”. This has also addressed the impact of the pressure to reduce ‘carbon miles’ and any subsequent demand impacts

o an assessment of the impact on the market of changing technology. This has included conducting discussions with CINZ, leading convention centres and PCOs in New Zealand and Australia regarding current trends in:

� impact of communications and marketing (eg: social networks) on buyer behaviour and convention delegate attendance numbers

� impact of immersive telepresence on conference content and convention centre infrastructure / technology requirements

� impact of conference-related trade exhibitions on conference economics and convention centre design and functionality requirements

� impact of Awards programmes on delegate / accompanying person attendance and convention centre design and functionality requirements

� impact of ever-changing AV requirements (and supply-led development of technology capability) on convention centre design and functionality requirements

� trends in delegate / conference organiser adaptability to (or lack of) technology / gimmicks

� completing an economic impact assessment on the Auckland and New Zealand economies including sensitivity analysis. This work has involved:

o a review of existing data prepared from earlier studies of the convention centre options; amending the data in light of changes in projected visitor numbers or expenditure; modifications resulting from the peer review (undertaken by Covec); and conceptual differences required for use in the next stage

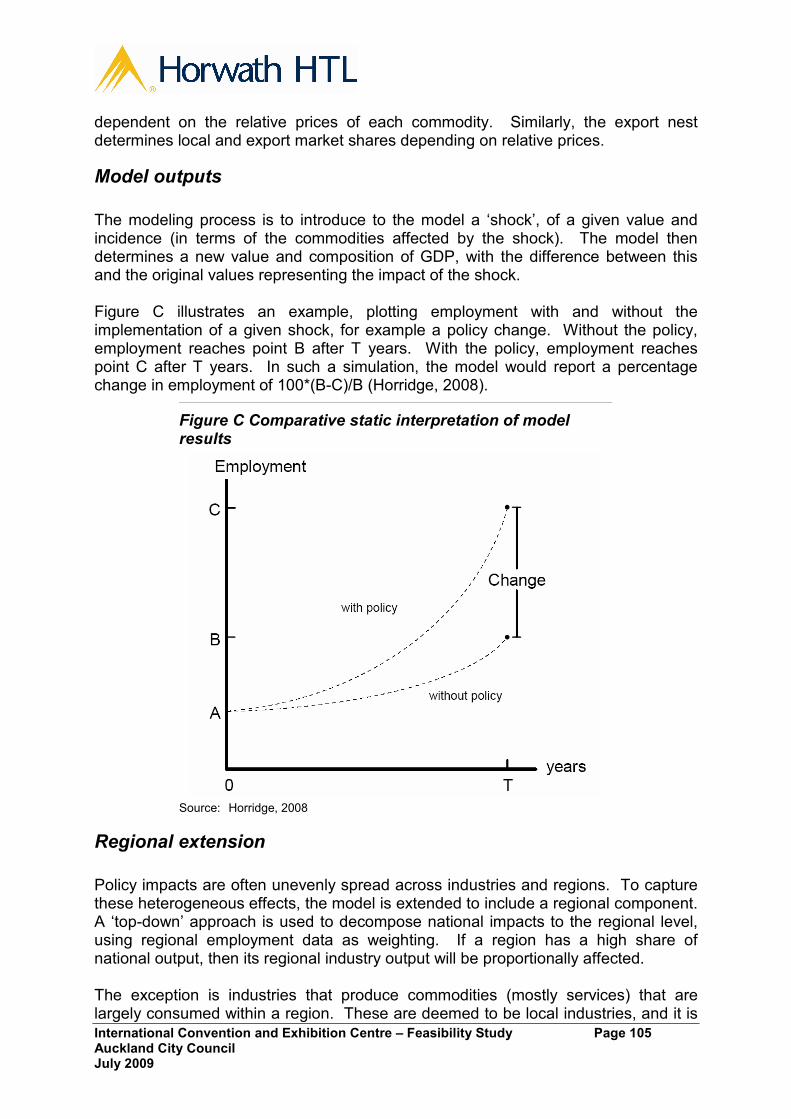

o putting the direct economic impacts into the NZIER CGE model as an external ‘shock’. The NZIER CGE model has a base run showing economic aggregates based on current economic forecasts. The resulting model outputs have been compared to the base run, with the differences representing the economy-wide impacts, in aggregate and by main component of economic activity

o modelling a number of scenarios based on medium, high and low visitation rates and up to three convention centre options. The estimates from the model are of the national impact and also estimate regional direct and indirect impacts within the outputs of the national model (ie: the distribution of impacts between Auckland and other regions, including direct impacts arising from pre- and post- conference touring and satellite conferences)

� completing a cost benefit analysis that addresses ‘non-economic’ factors:

International Convention and Exhibition Centre – Feasibility Study Page 5 Auckland City Council July 2009

o building on the economic impact analysis, applying a suitable discount rate to the time profile of costs of the convention centre (both investment and any other costs such as rates subsidies) and direct economic impacts (and total), to estimate the Net Present Value of a centre

o undertaking a review of the existing assessment of these, and any equivalent studies abroad, with a view to refining the assessment and if possible, forming a view as to the ‘order of magnitude’ importance of each of these

� identifying facility requirements and specifications including dimensions such as footprint and total gross floor area:

o undertaking a review of previous architectural work, IAPCO convention centre design / space criteria, updating criteria where required or justified and determining GFA requirements taking into account recent / emerging trends, New Zealand’s competitive position in the international market, critical success factors for competitive international convention centres, relationship with site and surrounding area / buildings / supporting infrastructure / services, etc

� confirming the criteria for site selection, and assessing the high-level viability of a few sites against these criteria. The approach has involved:

o working with members of the consulting team to review, update, modify and confirm the site selection criteria, including weightings of criteria

o obtaining approval from client on the selection criteria and weightings

o undertaking an independent assessment of scoring the different sites against each criterion with supporting rationale for scoring each criterion

o providing results of site assessment and conduct discussions with the client prior to including into the feasibility study

� identifying examples of successful ownership models that could be applicable for Auckland, including analysis of the governance arrangements, management and operational arrangements and upfront and ongoing finance and funding arrangements. This has included utilising our networks to identify:

o the most relevant “best practice” examples of convention centre developments and operations (to the New Zealand context) in Australia, UK, Europe, USA, South America and Asia

o relevant information in relation to the most relevant examples, from an owner operator perspective.

In the short time available we have undertaken the following key steps to achieving the scope of work:

� reviewed existing available research regarding conference demand in New Zealand and the need for / opportunity for new conference facilities, including a review of Committee for Auckland’s previous research

International Convention and Exhibition Centre – Feasibility Study Page 6 Auckland City Council July 2009

� interviewed key conference industry stakeholder representatives including:

o Conventions and Incentives New Zealand (“CINZ”)

o THE EDGE®

o SKYCITY Entertainment Group

o Tourism Auckland

o The Conference Company Ltd

� contacted a conference industry consultant in Australia to assist in information about trends in international conferences

� additional research as required to address the objectives outlined above, including:

o updated general trends in the global convention market, from the ICCA conventions database

o assessed the exhibition space requirements of international conventions

o reviewed the business case submissions made to the Christchurch City Council regarding the proposed significant expansion of the Christchurch Convention Centre.

1.3 DISCLAIMER This report and the projections included in it have been prepared on the specific instruction of the reference group. Neither the report nor its contents, nor any reference to our firm may be included or quoted in any document without the prior written consent of Horwath HTL Ltd. This report is based on estimates, assumptions and other information available to us, the sources of which are stated in the appropriate sections of the report. We did not carry out an audit or verification of the information supplied to us during the engagement, except to the extent stated in this report. We advise that the projections and forward looking statements presented in this report are based on estimates and assumptions which are inherently subject to uncertainty and variation depending upon certain evolving events. Accordingly, we do not present the projections as results which actually will be achieved. Actual results achieved may vary from the projections and the variation may be material. Horwath HTL Ltd assumes no responsibility whatsoever in respect or, or arising out of, or in connection with the contents of this report to parties other than the reference group. If any other parties choose to rely in any way on any advice provided by Horwath HTL Ltd to you, even with our approval, they do so entirely at their own risk.

International Convention and Exhibition Centre – Feasibility Study Page 7 Auckland City Council July 2009

1.4 EXECUTIVE SUMMARY

The primary rationale for developing a new international convention and exhibition centre for Auckland is to substantially improve New Zealand’s capability for hosting medium to large-scale international conferences and related exhibitions / tradeshows. This involves winning such conferences over competing countries (especially Australia) and hosting them with the minimum of compromises. New Zealand has some capability for hosting small to medium sized international conferences at present, and New Zealand has hosted some reasonably large international conferences in the past. However, we are facing increasingly significant constraints and competitive disadvantages when compared to international facilities and locations, especially when compared to our closest competitor, Australia. The key target conferences where New Zealand does not currently have good competitiveness is in international association (ie: non-corporate entity) conferences of over 1,000 delegates. Historical Conference Activity There has been substantial growth reported in the number of larger international association conferences held annually in the period 1999 – 2008, with the strongest growth being in meetings of 1,000 – 2,000 delegates (6.7% per annum Compound Annual Growth Rate (CAGR)), where New Zealand currently does not have strong capability. The rate of growth has also been strong in the largest conferences, although the total number of such conferences is smaller. There has been no trend of reduction in the number of conferences in any size category during the period. There has been stronger growth in international association conferences hosted in the Asia / Middle East / Pacific region during the period 1999 – 2008, only interrupted by the outbreak of SARS in the region in 2003. The data shows that New Zealand achieved a CAGR (between 1999 and 2008) of 6.3% (above Australia at 2.9%). Figure 1.1 summarises the performance of New Zealand in the context of Australasia, Asia / Middle East / Pacific region and the World. The 38 conferences held in New Zealand in 2008 represent a share of 0.5% of total conferences. These conferences had an average size of 467 delegates compared to the world average of 638 delegates.1

1 The average size of conferences reported has fallen mainly as a result of in increase in the number of smaller conferences reported by new / additional hotel venues.

International Convention and Exhibition Centre – Feasibility Study Page 8 Auckland City Council July 2009

Figure 1.1: New Zealand’s Share of International Association Conferences – 1999, 2008

The data indicates that New Zealand has “punched above its weight” in terms of winning international association conferences within the Australasian and world markets over the past decade, even with limitations of facilities. This can partly be attributed to the Christchurch Convention Centre (which opened in 1997) and SKYCITY Auckland Convention Centre (which opened in 2004) becoming established in the international market, and improved marketing and targeting of international conventions by Conventions and Incentives New Zealand in conjunction with the leading venues and regional convention beaureus. In addition to these regional and international conferences, New Zealand taps into the Australian ‘domestic’ market for association conferences – ie: those conferences normally hosted only in Australia but which come to New Zealand on occasion. These conferences do not meet the ICCA criteria of international association conferences. Australian corporate conferences (as well as corporate conferences from further afield, to a lesser extent) are also a target for the New Zealand conference industry.

The strong growth in international conference activity in the Asia / Middle East / Pacific region has partly been stimulated by the substantial growth in large-scale convention and exhibition centre developed in Asia and Australia during the past 10 – 15 years. The schedule identifies the date of opening, and (where applicable) expansion of the facilities. This confirms a significant expansion in convention centre supply, and an even greater expansion in exhibition space. Many of the Asian facilities have been developed as icons of national pride for hosting regional and international inter-governmental meetings and conferences. Hosting large-scale regular trade shows has also been a significant driver of the expansion of exhibition facilities.

New Zealand (not to scale)

Australasia (not to scale)

Asia / ME / Pacific (not to scale)

1999 2008 Number 22 38 % of Australasia 13.5% 17.3% Growth (10 yrs) +73% Average Size 269 467 (Refer to Table 2.1 for annual growth)

1999 2008 Number 857 1,612 % of World 19.4% 21.6% Growth (10 yrs) +88% Average Length 4.5 4.0 Average Size 659 599 (Refer to Table 2.1 for annual growth)

1999 2008 Number 163 220 % of Asia/ME/Pac 19.0% 13.6% Growth (10 yrs) +35% Average Size 665 521 (Refer to Table 2.1 for annual growth)

World

1999 2008 Number 4,424 7,475 Growth (10 yrs) +69% Average Length 4.4 3.9 Average Size 722 638

International Convention and Exhibition Centre – Feasibility Study Page 9 Auckland City Council July 2009

In the case of Australia, a significant factor in the development and expansion of facilities has been driving economic impact at a state level. Therefore, winning national conferences and exhibitions (which attract inter-state conference delegates) is important, as well as winning international conferences and exhibitions, for many of the Australian venues. Current and Expected Future Market Trends Sustainability has become a key focus in the international (and local) conference industry largely because of increased awareness and concern of consumers regarding the ‘carbon footprint’ of travel. This may become an increasingly significant factor in conference buyers considering the choice of destination for international conferences in the future, responding to the views and perceptions of conference delegates. This presents a risk to New Zealand (and Australia) in terms of marketing to and winning international conventions, assuming environmental concerns continue to be ‘top of mind’ to the consumer, although the risk is less in relation to domestic, Australasian and Asia / Pacific conferences. Australasian destinations may become proportionately less favourable over time than if there were no environmental concerns. It is unlikely, however, that distance will become the critical decision factor in the choice of location, even if it is still one factor, for most international conferences, although it may become a critical decision factor in the choice of location for international conferences2. There is no particular reason why convention delegate arrivals to New Zealand would be worse affected than leisure visits from international visitors. Arguably, leisure travel is more of a ‘luxury’ and discretionary nature and therefore less ‘justifiable’ than international conference attendance. For example, it will always be important for professional training and development for doctors to attend medical conferences, the largest international association conference segment.

Improved video conferencing technology provides both risks and benefits for the conference industry. The risks are around the potential for substitution of video conferencing for travel to meetings and conferences. To the extent that this risk is real, it is more significant in relation to corporate meetings of short duration (eg: part or full day meetings) rather than multi-day conferences, and generally in relation to smaller groups rather than larger groups. It is unlikely that video conferencing is a practical alternative to multi-day international association meetings and conferences. The benefits of improving communication and video conferencing relate to the increased ability to have expert input from a wider range of presenters (including

2 Alan Trotter, CEO, Conventions and Incentives New Zealand

International Convention and Exhibition Centre – Feasibility Study Page 10 Auckland City Council July 2009

keynote presenters) by video link as a substitute to their attendance in person. This allows greater flexibility, richness and depth in conference content, and greater cost efficiency.

Evolving communication technologies provide both risks and opportunities for the conference industry. The risks involve increasing use of the internet and other on-line forums for communicating and sharing information and ideas globally. There is the potential that increased sharing of information, ideas and thought leadership through increasingly effective and cost-effective technology solutions could reduce the degree of reliance of some organisations (both corporate entities and associations) on face-to-face meetings and conferences, and therefore result in fewer conferences than might otherwise be the case. Similarly, such communication channels may mean that conference delegates could be more challenging to attract, and delegate numbers be more difficult to achieve than previously. The benefits of evolving communication technology for international conferences relate to marketing opportunities. New Zealand’s Competitive Position New Zealand’s competitive position is currently compromised by the fact that three of our largest venues (THE EDGE®, Wellington Convention Centre and Christchurch Convention Centre) are all multi-purpose venues that rely on arts-focused spaces to provide them with the critical scale. Furthermore, for conferences of any significant size (eg: 600 delegates plus) that require exhibition space, it is necessary to have delegates moving between multiple buildings. These current arrangements mean that from a pure physical facility perspective, New Zealand is becoming an increasingly uncompetitive destination, particularly as cities in Australia and Asia continue to upgrade and expand their facilities. Despite this, New Zealand is continuing to attract a small number of international conferences. This can partly be attributed to the increased marketing effort that is being applied (eg: the Ministry of Tourism-funded Conference Assistance Programme operated by Conventions and Incentives New Zealand). In a general sense, therefore, New Zealand’s key current weaknesses relate to venue scale, quality, and functionality while the country’s key strengths relate to its destination appeal and support infrastructure. There are a number of specific opportunities that New Zealand can leverage in order to optimise the outcomes from developing an international standard convention centre. Key opportunities include:

International Convention and Exhibition Centre – Feasibility Study Page 11 Auckland City Council July 2009

� 100% Pure New Zealand marketing campaign and brand recognition

� targeting international conferences hosted in Australia

� development of a distinctive venue that showcases New Zealand In seeking to increase New Zealand’s share of the international conference market, it is important to acknowledge key challenges that New Zealand will need to overcome, including:

� New Zealand is a long-haul destination – “carbon miles” implications, “wash down” factor

� the emerging tendency for conference venues and / or destinations to “buy” conferences.

Site selection criteria and location analysis Proximity to a critical mass of appropriate standard hotel rooms is regarded as the single most important attribute due to the convenience this provides conference organisers and delegates. Based on the location attributes identified above, a CBD location is the most obvious and advantageous option for an international convention centre. This is primarily because the CBD is the only precinct that provides the critical mass of appropriate accommodation to support the centre’s operation. Furthermore, existing transport links and infrastructure have been designed to primarily service the CBD area, and the CBD has the greatest concentration of existing meetings infrastructure and entertainment facilities. Scale We have undertaken interviews with key “buyer” and “seller” representatives in New Zealand and the leading Auckland venues3 regarding the optimal scale of convention centre. The clear view is that the larger of three facility size scenarios (27,000 m2 GFA) should be regarded as the optimum on the basis that:

� it provides much clearer incremental capability to any existing or planned conference facilities in New Zealand

� it is more clearly competitive with the ever-expanding capacities and capabilities of the Australian and Asian venues

� it provides the highest degree of flexibility and convenient and effective ‘flow’ while minimising compromises

� it provides the highest degree of ‘future proofing’

3 Conventions & Incentives New Zealand (including IAEG-funded CAP programme); Tourism Auckland (including Business Events team); SkyCity Entertainment Group; THE EDGE

®

International Convention and Exhibition Centre – Feasibility Study Page 12 Auckland City Council July 2009

� it provides the greatest future potential for generating maximum venue operational cashflows through maximising event numbers and utilisation.

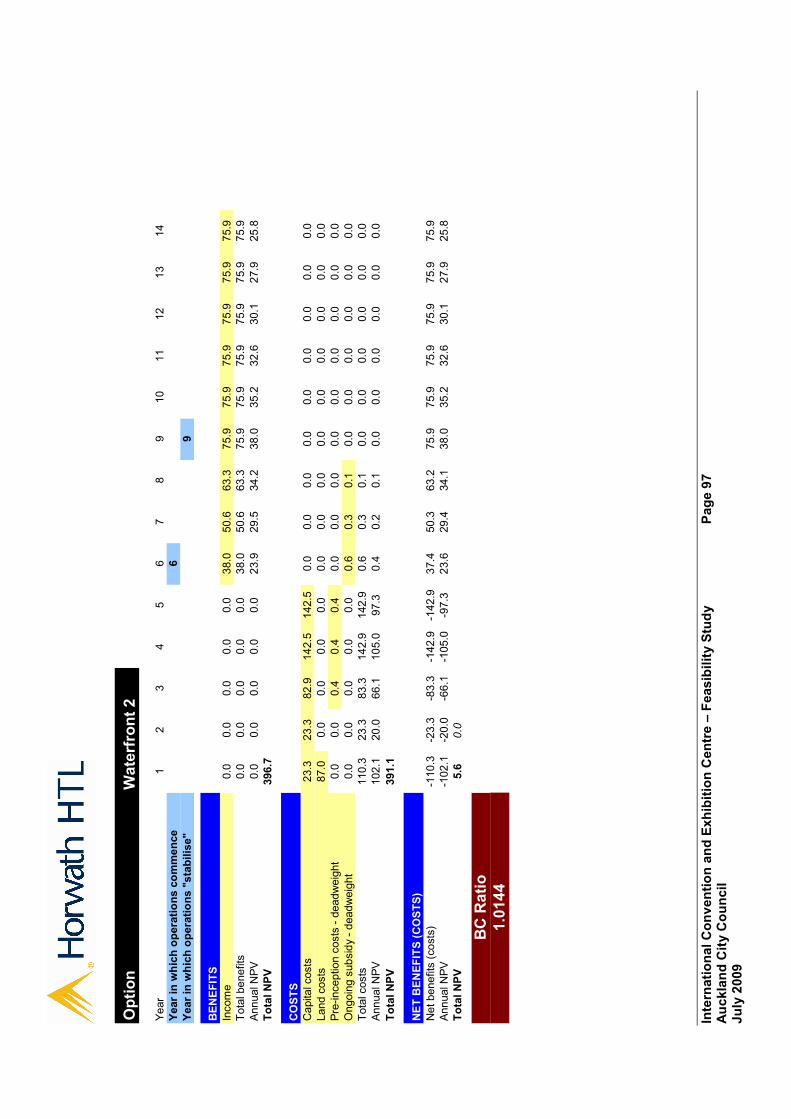

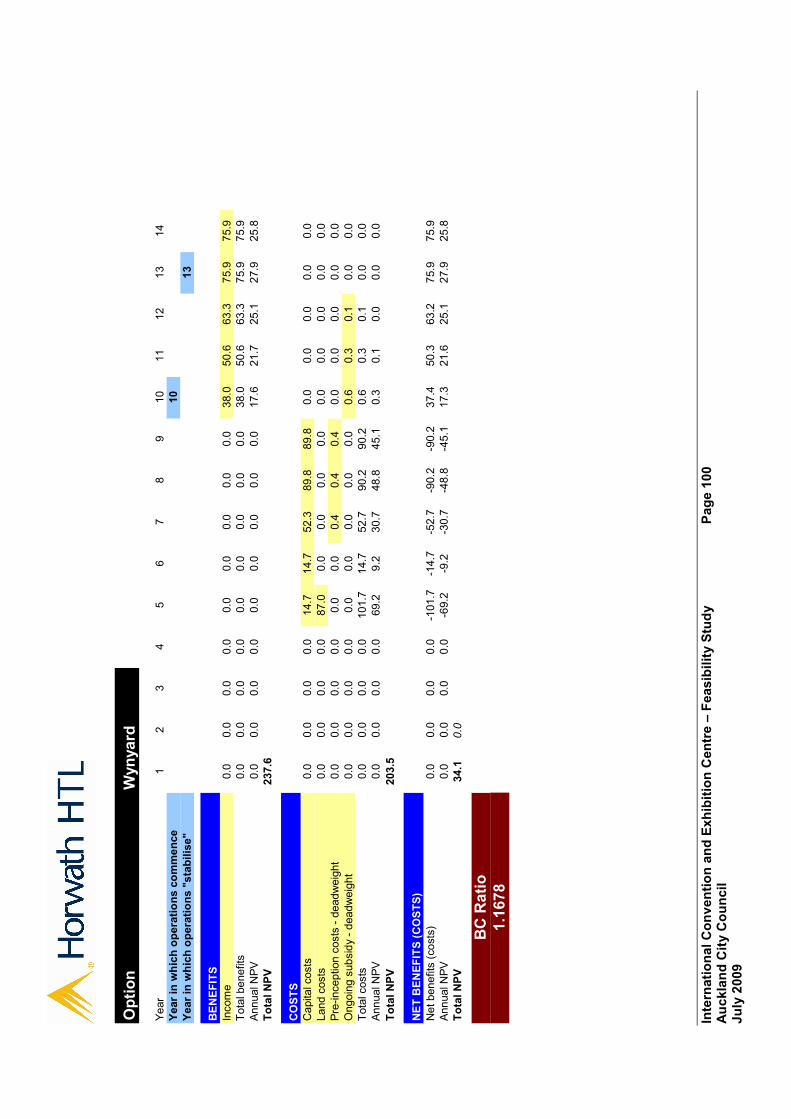

The rationale for developing an international convention centre for New Zealand is not predicated on developing an exhibition centre for stand-alone tradeshows and exhibitions, or replicating or competing with the ASB Auckland Showgrounds. Such an expansion could only be contemplated if it was planned to close down the recently expanded ASB Auckland Showgrounds. We have not assumed that the proposed convention and exhibition centre will win any exhibition business at the expense of the ASB Auckland Showgrounds. The substantial expansion of facilities in the Asia / Pacific region (especially in Asia, and in Australia) to cater for such shows and exhibitions is, in our view, not justified in New Zealand. Capital Expenditure Analysis WT Partnership have prepared capital cost estimates of alternative convention centre scenarios. Three scenarios assume a waterfront location, one a location at Wynyard Point and one a CBD location. Land purchase costs are excluded. A summary of the cost estimates follows:

Bledisloe

(Full)

($m)

Bledisloe

(Half)

($m)

Other

Wharf

($m)

Wynyard

Point

($m)

CBD

Site

($m)

Convention Centre (excl. land) 191,700 191,700 191,700 191,700 191,700

Fees, consents, other 43,612 53,219 62,827 33,548 33,548

Base cost (pre-escalation) 292,822 357,329 421,837 225,247 225,247

Escalation (4 years, except Wynyard option: 9 years)

37,178 44,671 53,163 82,753 28,753

Total cost (incl. escalation) 330,000 402,000 475,000 308,000 254,000

(Source: WT Partnership)

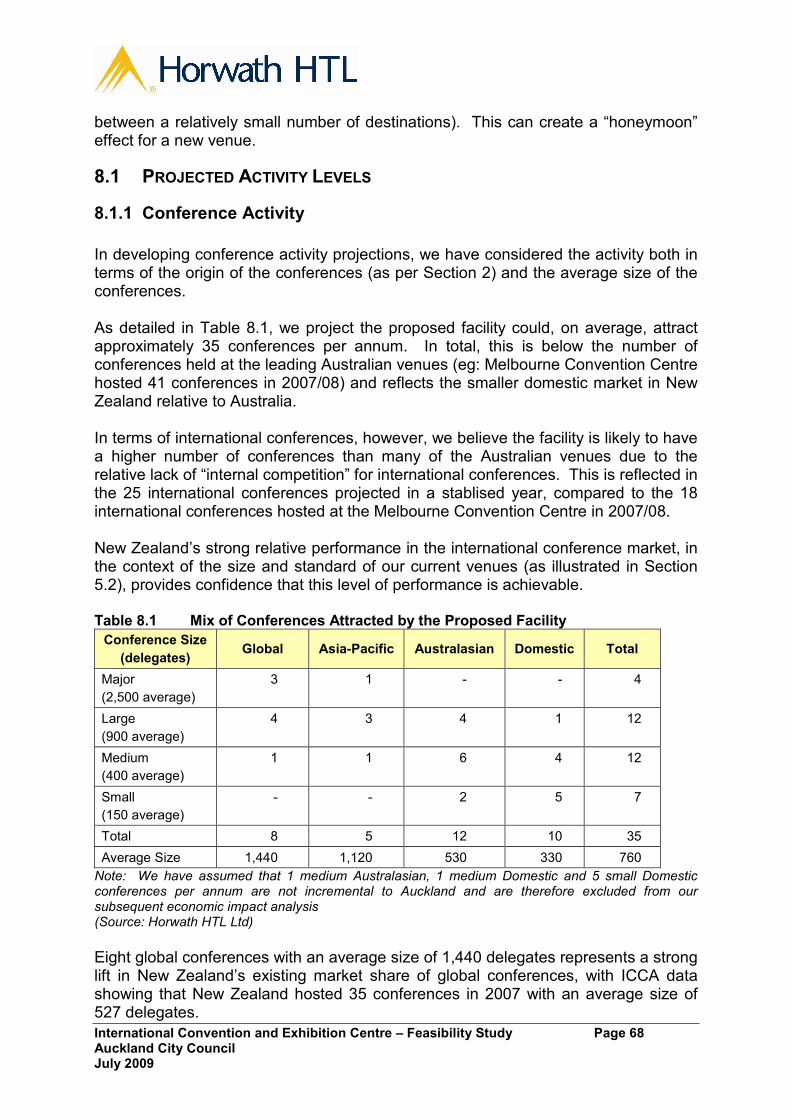

Operating Projections In developing conference activity projections, we have considered the activity both in terms of the origin of the conferences and the average size of the conferences. We project the proposed facility could, on average, attract approximately 35 conferences per annum. In total, this is below the number of conferences held at the leading Australian venues (eg: Melbourne Convention Centre hosted 41 conferences

International Convention and Exhibition Centre – Feasibility Study Page 13 Auckland City Council July 2009

in 2007/08) and reflects the smaller domestic market in New Zealand relative to Australia.) In terms of international conferences, we believe the facility is likely to have a higher number of conferences than many of the Australian venues due to the relative lack of “internal competition” for international conferences such as exisits between the various Australian facilities. This is reflected in the 25 international conferences projected in a stablised year, compared to the 18 international conferences hosted at the Melbourne Convention Centre in 2007/08. The 25 conferences with an average size of 939 delegates represents a strong lift in New Zealand’s existing market share of international conferences, with ICCA data showing that New Zealand hosted 35 conferences in 2007 with an average size of 527 delegates. Based on our financial projections, we anticipate the facility will operate broadly on a break-even cash flow basis. This level of cash flow performance is consistent with that achieved by the major Australian venues including Melbourne and Adelaide. Economic Impact Analysis / Benefit-Cost Analysis It is estimated that, when fully operational, events at the proposed facility will generate and increase of $85.4 million in tourism-related expenditure per annum (almost 22,000 additional international visitors who would not otherwise visit New Zealand, and more than 200,000 extra visitor days). 84% of the incremental visitor expenditure is associated with people who participate in conferences. There is a significant spin-off from associated visitor activity which account for over half of the visitor days and 39% of visitor expenditure. Approximately 95% of the incremental expenditure is attributable to conferences. Assuming 80% of capital costs will be funded from the public sector, the estimated capital costs have been increased by 16% (a 20% increase on the public sector contribution) to recognise the effect of deadweight loss. Land costs have been included, on the basis that these represent an opportunity cost, at an assumed $75 million for each site option. The CBD option has the lowest total Net Present Value (NPV) of costs (except Wynyard) as its capital costs are purely for construction of the convention centre. The addition of an “iconic” structure for the waterfront options, and the varying costs of wharf strengthening, raises the NPV of their costs. The Wynyard option differes from the others primarily in terms of its timing, with no additional site costs or “iconic” enhancements. The NPV of benefits is $396.7 million for all site options (except Wynyard Point) as all options assume the same income stream. The CBD option has the highest Benefit Cost Ratio (BCR). The lowest-cost waterfront option and the Wynyard option have similar BCRs. The effect of additional costs of wharf strengtheneing is to reduce the BCRs of other waterfront options

International Convention and Exhibition Centre – Feasibility Study Page 14 Auckland City Council July 2009

further. In the case of the most expensive waterfront option, its NPV costs exceed NPV benefits. If the assumptions are considered realistic, a CBD option would be favoured as it delivers the benefits from increased tourism at the earliest date and the least capital costs. In comparison, the waterfront options incur additional capital costs but secure no additional benefits. They provide additional amenity values from “iconic” structures in a “signature” location. The Wynyard option assumes the same costs and benefits as the CBD option, but with a four year delay. Given the fact that the options generally deliver net benefits, the impact of deferring these is to reduce the value of this project option. The relativity of benefits to costs between the options could change if there were significant differences in land values between the options. The above results have been applied through the NZIER Computable General Equilibrium (CGE) model of the New Zealand economy to estimate the total effects from the initial impacts of capital and tourism expenditure. The effect of the additional $85.4 million per annum in tourism expenditure is an increase in national GDP value added of $40.3 million per annum. The CGE model assumes all tourism expenditure is generated equally throughout the year, and that there is limited surplus capacity in the economy throughout the year to absorb the incremental demand. However this assumption does not reflect the underlying reality of conference demand, which occurs generally during the shoulder and low season of the international and domestic visitor industry, therefore increasing demand at times when there is usually significant excess capacity. Therefore the GDP estimates produced by the CGE analysis are likely to be significantly understated. Other potential non-quantified and intangible effects of the convention centre include:

� savings of offshore expenditure: New Zealanders attending events at the home-based convention centre rather than travelling overseas to the conferences held elsewhere

� reputational effects: hosting major conventions reinforces the perception of Auckland and New Zealand as a destination of international standing, especially in fields in which New Zealand wishes to establish its international standing (eg: emerging technologies)

� learning and relationships effects: the personal contacts that New Zealand conference delagtes make at international conferences, and the subsequent exchange of information, collaborative activities, business venture, etc, contributes to New Zealand’s “global connectedness”

� local networking: local planning and preparation for major international conventions may provide a catalyst for local networking, including business, academia and / or the public sector, and may lead to ongoing collaboration.

These effects are potentially significant but are regarded as non-quantifiable.

International Convention and Exhibition Centre – Feasibility Study Page 15 Auckland City Council July 2009

Public / Private Ownership, Governance, Operations Convention and Exhibition (Convex) Centres are substantial real estate investments (in terms of capital cost) and are not generally run on a “commercial” basis. The key reasons for developing international standard convention centres revolve around their ability to generate substantial economic impact and facilitate the transfer of valuable knowledge and contacts to the benefit of the local economy. It is because of these “public good” aspects and the large capital costs that large convention centres tend to predominantly be funded by the public sector. In order to optimise private sector funding contributions it is likely that a range of funding mechanisms will need to be pursued. There are three broad ownership options available for an international standard convention centre:

� private ownership through a BOOT scheme

� direct ownership by the public sector

� the creation of special purpose entities that are accountable to the public sector. These entities take a diverse range of forms.

The benefit of these entities is that they are fully accountable to the public sector but are able to operate at arms length to ensure the public sector’s objectives are met in the most efficient and effective manner. We note that the Royal Commission on Auckland Governance has recommended the establishment of a Council Controlled Organisation to own all regionally significant event venues, which would logically include the proposed international convention centre. The on-going governance model for the proposed centre will be a product of the ownership model that is adopted. There may be merit in establishing an interim governance structure to oversee the development of the facility. This could be akin to the Redevelopment Board that has been established at Eden Park and have specific responsibility for ensuring key stakeholder requirements are met in the development of the physical building. The skill-sets of the representatives on this governance structure are likely to differ significantly from the skill-sets sought for those on the governance structure of the ownership entity although some continuity of representation would be highly desirable. In Australasia there is a reasonably even split between in-house venue management and out-sourced venue management. The primary advantages of contracting out venue management include realising “key money” in return for the commercial opportunity and the potential to obtain specialist operational expertise to improve performance levels, particularly during the establishment phase.

International Convention and Exhibition Centre – Feasibility Study Page 16 Auckland City Council July 2009

The key risks of contracting out the venue management is the potential for mis-alignment of objectives and the potential that revenue performance may not be improved to the extent necessary to off-set the associated management fees. Historically, there has been a tendency for venue managers to out-source food and beverage services to specialist caterers. However, in recent years there has been a trend towards venue managers bringing these services back in-house to assist their profitability and ensure greater control over service standards. Conclusion The rationale for development of an internationally competitive venue for hosting international and national conferences, exhibitions and other business events is centred on:

� generating incremental economic impact for the New Zealand economy as a result of hosting such events

� providing the opportunity to ‘showcase’ New Zealand to international delegates in an internationally competitive venue

� generating other tangible and intangible benefits which are not directly measurable in economic terms.

The Cost Benefit ratios of all but one scenario analysed in this study are positive. The economic impact analysis is based on a General Equilibrium model of the New Zealand economy and is conservative because it assumes that:

� demand will occur for the conference and exhibition centre evenly throughout the year – whereas international (and national) conference demand will tend to peak during the months March – October (nine months)

� New Zealand’s capacity to host such events will face capacity constraints throughout the year – whereas the period of peak demand will coincide with the shoulder and low season demand for the required infrastructure (most importantly hotel accommodation, but also other commercial accommodation, airline and airport infrastructure, coach and other public transport, etc) when capacity is generally available and under-utilised.

Because the demand and capacity constraint assumptions inherent with General Equilibrium modelling do not reflect the underlying reality of the shape of convention activity and the highly seasonal nature of international and domestic visitor activity demand on infrastructure in New Zealand, the actual incremental contribution to GDP is likely to be significantly higher than indicated in the analysis contained in this report. In addition to the conservative economic impact assumptions adopted in the analysis contained in this report, the employment and financial benefits to the visitor industry (especially in terms of the owners of tourism industry infrastructure) are likely to be incrementally substantial.

International Convention and Exhibition Centre – Feasibility Study Page 17 Auckland City Council July 2009

For example, incremental hotel room demand in Auckland (and elsewhere around New Zealand) as a result of incremental conference demand (including pre- and post-conference travel in New Zealand) will have a high ‘flow-through’ to net profit during a period of the year when profitability is under significant and increasing pressure as peak season visitor demand grows (ie: November – February). If, on an indicative basis, total revenue in a typical ‘conference’ hotel grew by 2 – 3 percent on an annual basis as a result of incremental conference industry demand, it is possible that net profit before tax could grow by 4 – 6 percent or even 8 – 12 percent on an annual basis. Incremental off-season demand combined with improved overall industry profitability will result in more sustainable businesses in the tourism industry, and increased full-time year-round employment for New Zealanders to replace seasonal / casual labour, much of which is provided by short-term migrants.

International Convention and Exhibition Centre – Feasibility Study Page 18 Auckland City Council July 2009

2. HISTORICAL CONFERENCE ACTIVITY The primary rationale for developing a new international convention and exhibition centre for Auckland is to substantially improve New Zealand’s capability for hosting medium to large-scale international conferences and related exhibitions / tradeshows. This involves winning such conferences over competing countries (especially Australia) and hosting them with the minimum of compromises. New Zealand has some capability for hosting small to medium sized international conferences at present, and New Zealand has hosted some reasonably large international conferences in the past. However, we are facing increasingly significant constraints and competitive disadvantages when compared to international facilities and locations, especially when compared to our closest competitor, Australia. The key target conferences where New Zealand does not currently have good competitiveness is in international association (ie: non-corporate entity) conferences of over 1,000 delegates.

2.1 INTERNATIONAL ASSOCIATION CONFERENCE ACTIVITY

The main data source relating to this conference activity is the International Congress and Convention Association (“ICCA”) database of conference activity.

The ICCA database does not cover governmental / ‘quango’ organisation conferences (eg: World Bank, United Nations, Commonwealth Heads of Government, etc).

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

According to ICCA, the association market covers a wide range of event types and categories: medical meetings (the largest segment); scientific; other academic; trade organisations; professional bodies; social groupings. In terms of size, budget, duration and complexity there are significant variations between and also within categories. However, some similarities can be identified:

���� almost every ‘specialty’ has an association which holds one or more meetings

���� most associations have meetings that are repeated at regular intervals; these can be annual, biennial, etc

International Convention and Exhibition Centre – Feasibility Study Page 19 Auckland City Council July 2009

���� the destinations rotate, and they rarely return to the same destination within a very short time-span

���� the initiative to host a meeting often comes from the local counterpart, eg: the national association; if that body is difficult to motivate to organise the meeting, the chances are high that the meeting will be scheduled elsewhere

���� Association meetings have a very long lead-time; it is not unusual to find lead times of 5 years or more.

���� it is estimated that a growing minority of about 25-30% of the decision-making processes no longer include an official bidding procedure, but have a “central initiator” who selects the location and venues based on pre-determined and strict criteria.

2.1.1 International Congress and Convention Association Database

The ICCA database is the primary source of published quantitative information regarding non-governmental international association conferences. It is estimated that there are approximately 15,000 such association meetings organised in the world on a regular basis.4 The ICCA Association Database has collected information on approximately 80% of them (approximately 12,000). The 15,000 association meetings include non-annual meetings, meetings which do not rotate between countries (including USA-based associations that rotate principally within the USA), and association meetings of less than 50 participants. In order to be included in the ICCA database, association meetings must meet the following criteria:

���� be attended by at least 50 participants

���� be organised on a regular basis (ie: one-off events are not included)

���� move between at least three different countries. In 2009, ICCA identified 7,475 international Association conferences that were reported as being held in 2008 which met these criteria5. The difference between the 13,000 association meetings in the ICCA database and the 7,475 meetings reported in 2008 relates to the proportion of Associations which do not hold annual meetings, non-reporting by ICCA members by the reporting deadline of 1 February 2009, conferences held at non-ICCA member venues, and meetings of less than 50 delegates in the 2008 year.

4 ICCA: International Association Meeting Market Statistics Report 1999 to 2008 5 Subsequent top-line ICCA data for 2008 indicates 7,475 conferences, an 11.9% increase on 2007

International Convention and Exhibition Centre – Feasibility Study Page 20 Auckland City Council July 2009

2.1.2 International Association Conference Market Trends – Global

Figure 2.1 illustrates the global growth in the association conference market by number of participants (over 500 delegates) between 1999 and 2008. This segmentation is based only on a subset of the ICCA database where participant numbers are stored. Reporting of delegate numbers appears to be more complete in the larger conferences (over 500 delegates); however it is probable that the data in Figure 2.1 understates that actual number of larger international association conferences. Figure 2.1: International Association Conferences (> 500 delegates) – Global (1999 – 2008)

0

100

200

300

400

500

600

700

800

500 to 999 1,000 to 1,999 2,000 to 2,999 >3,000

Number of Participants

Number of Association Conferences

1999 2008

CAGR = Compound Annual Growth Rate (Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

As shown in Figure 2.1, there has been substantial growth reported in the number of larger international association conferences. There has been strong in meetings of 1,000 delegates and over where New Zealand currently does not have strong capability. There has been no trend of reduction in the number of conferences in any size category during the period. Figure 2.2 shows the growth trend in the association conference market by number of participants (over 500 delegates) including in the intermediary years between 1999 and 2008.

CAGR – 4.5%

CAGR – 6.7%

CAGR – 6.2% CAGR – 5.1%

International Convention and Exhibition Centre – Feasibility Study Page 21 Auckland City Council July 2009

Figure 2.2: Global Growth Trend – International Association Conferences by Size

y = 25.794x + 387.53

y = 14.824x + 196.47

0

100

200

300

400

500

600

700

800

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

Number of Conferences by Size

500 to 999 1000 to 1999 2000 to 2999

3000 to 4000 5000 to 10000 10000+

Linear (500 to 999) Linear (1000 to 1999)

(Source: ICCA: International Association Meeting Market Statistics Report 199-2008)

The international association conference market is highly seasonal, as illustrated in Figure 2.3. The number of international association conferences peaks in June and September, and bottoms out in December – February.

International Convention and Exhibition Centre – Feasibility Study Page 22 Auckland City Council July 2009

Figure 2.3: Seasonality of International Association Conferences – Global (1999 and 2008)

0

200

400

600

800

1000

1200

1400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Number of Meetings

1999 2008

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

ICCA also compiles statistics (where the data is available) on the venues used by association conferences. As shown in Figure 2.4, the most popular conference venues, particularly for smaller conferences, are hotels with meeting facilities (42%), followed by dedicated conference / exhibition centres (30%) and universities (19%). Figure 2.4: Conference Venues Used – Global (2008)

Hotels

42%

Conference /

Exhibition Centres

30%

Universities

19%

Other Venues

9%

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

International Convention and Exhibition Centre – Feasibility Study Page 23 Auckland City Council July 2009

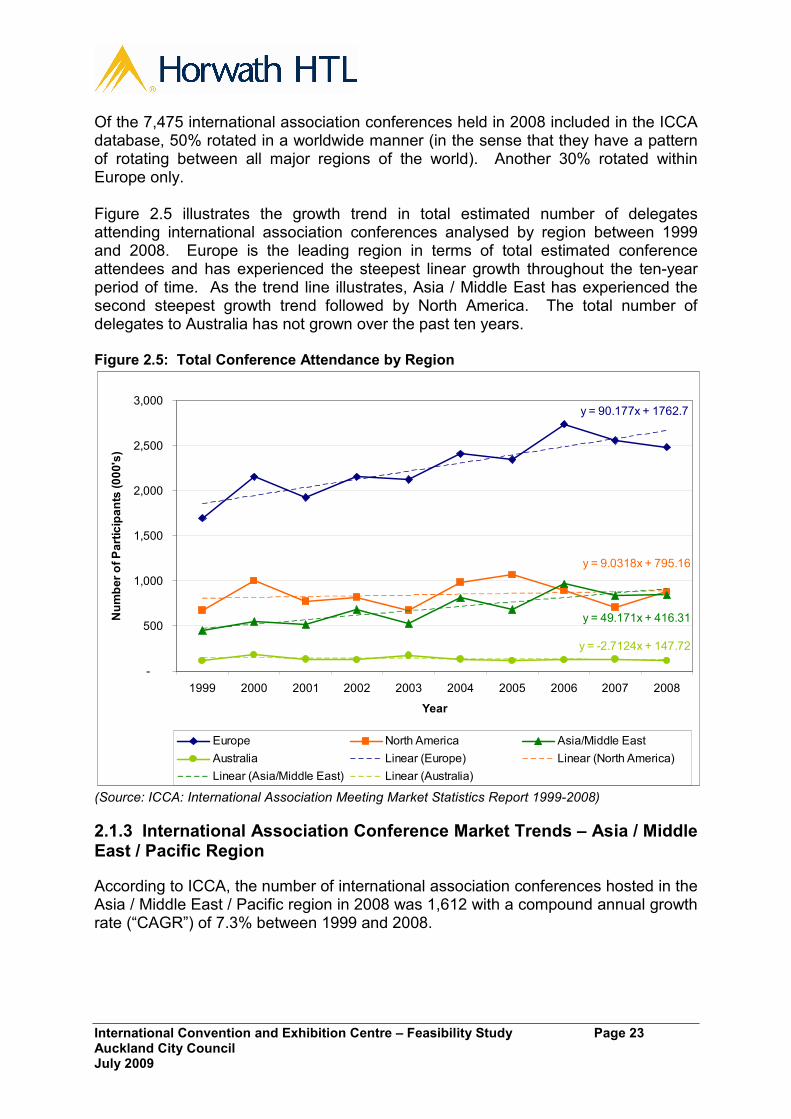

Of the 7,475 international association conferences held in 2008 included in the ICCA database, 50% rotated in a worldwide manner (in the sense that they have a pattern of rotating between all major regions of the world). Another 30% rotated within Europe only. Figure 2.5 illustrates the growth trend in total estimated number of delegates attending international association conferences analysed by region between 1999 and 2008. Europe is the leading region in terms of total estimated conference attendees and has experienced the steepest linear growth throughout the ten-year period of time. As the trend line illustrates, Asia / Middle East has experienced the second steepest growth trend followed by North America. The total number of delegates to Australia has not grown over the past ten years. Figure 2.5: Total Conference Attendance by Region

y = 90.177x + 1762.7

y = 9.0318x + 795.16

y = 49.171x + 416.31

y = -2.7124x + 147.72

-

500

1,000

1,500

2,000

2,500

3,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

Number of Participants (000's)

Europe North America Asia/Middle East

Australia Linear (Europe) Linear (North America)

Linear (Asia/Middle East) Linear (Australia)

(Source: ICCA: International Association Meeting Market Statistics Report 1999-2008)

2.1.3 International Association Conference Market Trends – Asia / Middle East / Pacific Region

According to ICCA, the number of international association conferences hosted in the Asia / Middle East / Pacific region in 2008 was 1,612 with a compound annual growth rate (“CAGR”) of 7.3% between 1999 and 2008.

International Convention and Exhibition Centre – Feasibility Study Page 24 Auckland City Council July 2009

This rate of growth is 21% higher than the rate of growth reported for the world over the same period (with CAGR of 6.0%).6

The higher regional rate of growth reflects the number of major new convention centres which opened in Asia during the period.

Figure 2.6 demonstrates the consistent growth in international association conferences hosted in the Asia / Middle East / Pacific region during the period 1999 – 2008, only interrupted by the outbreak of SARS in the region in 2003.

Figure 2.6: Number of International Association Conferences – Asia / ME / Pacific (1999 - 2008)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Calendar Years

Number of Association Conferences

Other Asia / ME / Pacific Australia New Zealand

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

Table 2.1 shows a further analysis of the conferences held in the region in 1999 and 2008. This highlights the dramatic growth in conference activity within Asia, especially in China, Korea and Singapore, which countries have invested heavily in new and expanded convention and exhibition centres.

6 The ICCA database includes new venues reporting conference activity, as well as ‘actual’ growth in total conference activity, although it is not possible to identify what the underlying ‘actual’ growth is.

Impact of SARS: postponements followed by ‘bounce back’

International Convention and Exhibition Centre – Feasibility Study Page 25 Auckland City Council July 2009

Table 2.1: Number of Conferences Hosted within Asia / Middle East / Pacific Region

Number of International Association Conferences Held Country

1999 2008

Percentage Change

1999 - 2008

CAGR

Change

1999 - 2008

Japan 154 247 60.4% 5.4%

China 69 223 223.2% 13.9%

Korea 67 169 152.2% 10.8%

Singapore 46 118 156.5% 11.0%

Other Asia 277 539 94.6% 7.7%

Total Asia 613 1,296 111.4% 8.7%

Sydney 56 64 14.3% 1.5%

Melbourne 35 38 8.6% 0.9%

Brisbane 18 18 0.0% 0.0%

Other Australia 32 62 93.8% 7.6%

Total Australia 141 182 29.1% 2.9%

Auckland 8 17 112.5% 8.7%

Christchurch 1 8 700.0% 26.0%

Other New Zealand 13 13 0.0% 0.0%

Total New Zealand 22 38 72.7% 6.3%

Other ME / Pacific 81 96 18.5% 1.9%

Total Asia / ME / Pacific 857 1,612 88.1% 7.3%

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

The data shows that New Zealand achieved a CAGR (between 1999 and 2008) of 6.3% (above Australia). The New Zealand growth has been influenced by additional venues (including hotels and universities) reporting relatively smaller conferences other than in Auckland and Christchurch.

Other Asian countries that experienced high volume growth in the 1999 – 2008 period included China (CAGR of 13.9%), Korea (10.8%) and Singapore (11.0%).

The ICCA database shows that, of the 1,612 international conferences hosted in the region in 2008, 680 of these (42% of total) rotated only within the region (ie: not on a worldwide basis). This was up from 328 conferences (38% of total) in 1999.

The number of conferences in Australasia (ie: New Zealand and Australia combined) grew from 163 in 1999 to 220 in 2008, consistent with the overall world growth, but significantly less than the overall Asia / Middle East (“ME”) / Pacific region. This resulted in a reduction in market share of Australasia within the region, and reflects the rapid growth in conference activity in Asia, and particularly China, Korea and Singapore.

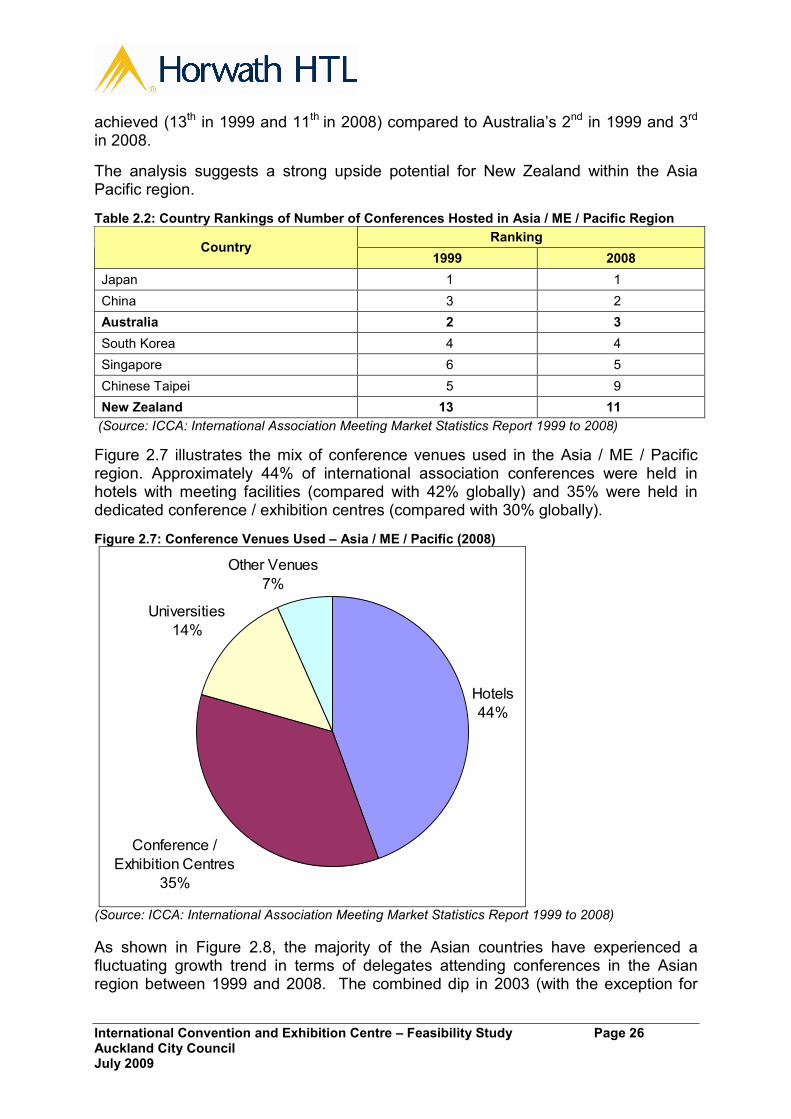

Table 2.2 summarises the relative rankings in terms of number of conferences hosted by country within the region. This highlights the low New Zealand share

International Convention and Exhibition Centre – Feasibility Study Page 26 Auckland City Council July 2009

achieved (13th in 1999 and 11th in 2008) compared to Australia’s 2nd in 1999 and 3rd in 2008.

The analysis suggests a strong upside potential for New Zealand within the Asia Pacific region.

Table 2.2: Country Rankings of Number of Conferences Hosted in Asia / ME / Pacific Region

Ranking Country

1999 2008

Japan 1 1

China 3 2

Australia 2 3

South Korea 4 4

Singapore 6 5

Chinese Taipei 5 9

New Zealand 13 11

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

Figure 2.7 illustrates the mix of conference venues used in the Asia / ME / Pacific region. Approximately 44% of international association conferences were held in hotels with meeting facilities (compared with 42% globally) and 35% were held in dedicated conference / exhibition centres (compared with 30% globally).

Figure 2.7: Conference Venues Used – Asia / ME / Pacific (2008)

Hotels

44%

Conference /

Exhibition Centres

35%

Universities

14%

Other Venues

7%

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

As shown in Figure 2.8, the majority of the Asian countries have experienced a fluctuating growth trend in terms of delegates attending conferences in the Asian region between 1999 and 2008. The combined dip in 2003 (with the exception for

International Convention and Exhibition Centre – Feasibility Study Page 27 Auckland City Council July 2009

Singapore) may be related to the bird flu resulting in fewer participants willing to travel to conferences. Figure 2.8: Delegates per County in Asia

-

50

100

150

200

250

300

350

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

Number of Participants per Country (000's)

Republic of Korea Japan China-P.R. Thailand Singapore Other Asia

2.1.4 International Association Conference Market Trends – New Zealand

Figure 2.6 summarises the performance of New Zealand in the context of Australasia, Asia / ME / Pacific region and the World. The 38 conferences held in New Zealand in 2008 represent a share of 0.5% of total conferences. These conferences had an average size of 467 delegates, compared to the world average of 638 delegates.7

7 The average size of conferences reported has fallen mainly as a result of in increase in the number of smaller conferences reported by new / additional hotel venues.

International Convention and Exhibition Centre – Feasibility Study Page 28 Auckland City Council July 2009

Figure 2.9: New Zealand’s Share of International Association Conferences – 1999, 2008

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

The data indicates that New Zealand has “punched above its weight” in terms of winning international association conferences within the Australasian and world markets over the past decade, even with limitations of facilities. This can partly be attributed to the Christchurch Convention Centre (which opened in 1997) and SKYCITY Auckland Convention Centre (which opened in 2004) becoming established in the international market, and improved marketing and targeting of international conventions by Conventions and Incentives New Zealand in conjunction with the leading venues and regional convention bureaus.

In addition to these regional and international conferences, New Zealand taps into the Australian ‘domestic’ market for association conferences – ie: those conferences normally hosted only in Australia but which come to New Zealand on occasion. These conferences do not meet the ICCA criteria of international association conferences.

Australian corporate conferences (as well as corporate conferences from further afield, to a lesser extent) are also a target for the New Zealand conference industry. Conventions and Incentives New Zealand is active in marketing New Zealand in the Australian market with full-time representation in Sydney, as are several of the Convention Bureaux and major venues in New Zealand.

Meetings, the annual New Zealand conference industry trade show, also heavily targets Australian buyers. As a result of these initiatives New Zealand has an increasingly high profile in Australia as a destination for conferences.

There are currently almost 670 conferences in the ICCA database that include within their organisation some connection to New Zealand (eg: a committee member of=n the international organisation). Figures 2.10 to 2.14 refer to this sub-set of the ICCA conference database.

New Zealand (not to scale)

Australasia (not to scale)

Asia / ME / Pacific (not to scale)

1999 2008 Number 22 38 % of Australasia 13.5% 17.3% Growth (10 yrs) +73% Average Size 269 467 (Refer to Table 2.1 for annual growth)

1999 2008 Number 857 1,612 % of World 19.4% 21.6% Growth (10 yrs) +88% Average Length 4.5 4.0 Average Size 659 599 (Refer to Table 2.1 for annual growth)

1999 2008 Number 163 220 % of Asia/ME/Pac 19.0% 13.6% Growth (10 yrs) +35% Average Size 665 521 (Refer to Table 2.1 for annual growth)

World

1999 2008 Number 4,424 7,475 Growth (10 yrs) +69% Average Length 4.4 3.9 Average Size 722 638

International Convention and Exhibition Centre – Feasibility Study Page 29 Auckland City Council July 2009

Figure 2.10 shows the proportion of the main country base of the organisation. The largest proportion of the organisations (57%) is Europe based followed by the Americas (22%). Asia-Pacific represents a combined 19% of the organisations.

Figure 2.10: Main Country Base of Organisation (with some NZ contact)

Main Country Base of Organisation

Not Identified

2%

Americas

22%

Oceania

5%

Asia

14%Europe

57%

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

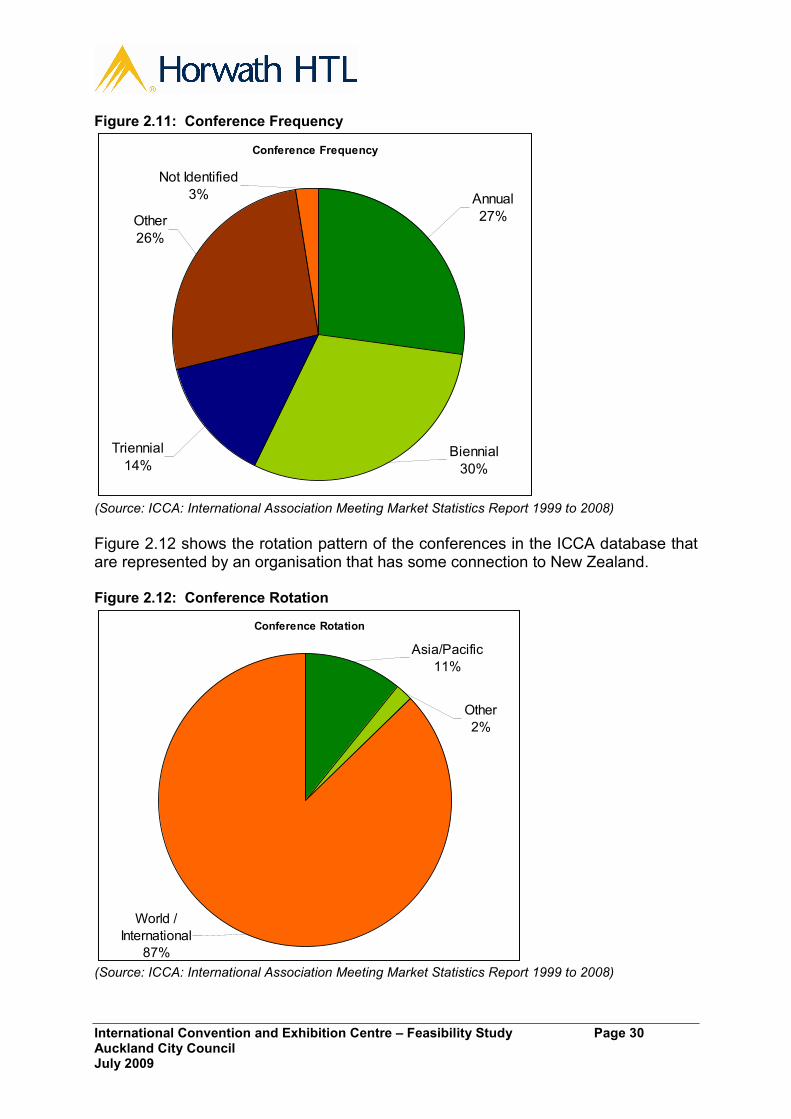

Figure 2.11 illustrates the frequency of the conferences (ie: how often they are held). The 25% of ‘other’ conferences represents conferences that have a different kind of frequency (eg: several times a year, only each tenth year, by no particular frequency schedule, etc).

International Convention and Exhibition Centre – Feasibility Study Page 30 Auckland City Council July 2009

Figure 2.11: Conference Frequency

Conference Frequency

Annual

27%

Not Identified

3%

Other

26%

Triennial

14%Biennial

30%

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

Figure 2.12 shows the rotation pattern of the conferences in the ICCA database that are represented by an organisation that has some connection to New Zealand. Figure 2.12: Conference Rotation

Conference Rotation

Asia/Pacific

11%

Other

2%

World /

International

87% (Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

International Convention and Exhibition Centre – Feasibility Study Page 31 Auckland City Council July 2009

Figure 2.13 illustrates the conference activity in terms of time of the year. 79% of the conferences (for which the timing is known) occur during the New Zealand winter and shoulder period of the year compared with only 21% that occur during the New Zealand summer. Figure 2.13: Conference Activity throughout the Year

Conference Activity throughout the Year

Not Identified

53%

April-

September

37%

October-

March

10%

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

As illustrated in Figure 2.14, for those conferences where the usual type of conference venue is identified, 76% of the conferences, are hosted either at a Congress Centre (or Conference Centre) only or a Congress Centre in conjunction with one or more venues.

International Convention and Exhibition Centre – Feasibility Study Page 32 Auckland City Council July 2009

Figure 2.14: Venue Type

Venue Type

Congress

Centre or

Shared

29%

Other

(Including

Hotel only,

University,

etc)

9%

Not Identified

62%

(Source: ICCA: International Association Meeting Market Statistics Report 1999 to 2008)

In addition to these 667 international association conferences where there is some New Zealand contact / representation in relation to the organisation responsible for the conference, approximately 20 of these organisations are either based in New Zealand or are led by a person based in New Zealand. A list of these conferences is attached as Appendix 7. These organisations and conferences potentially may have a higher probability of being hosted in New Zealand, and are a higher priority for targeting for conference bids by CINZ (where the expected conference size within New Zealand’s current capability to host.

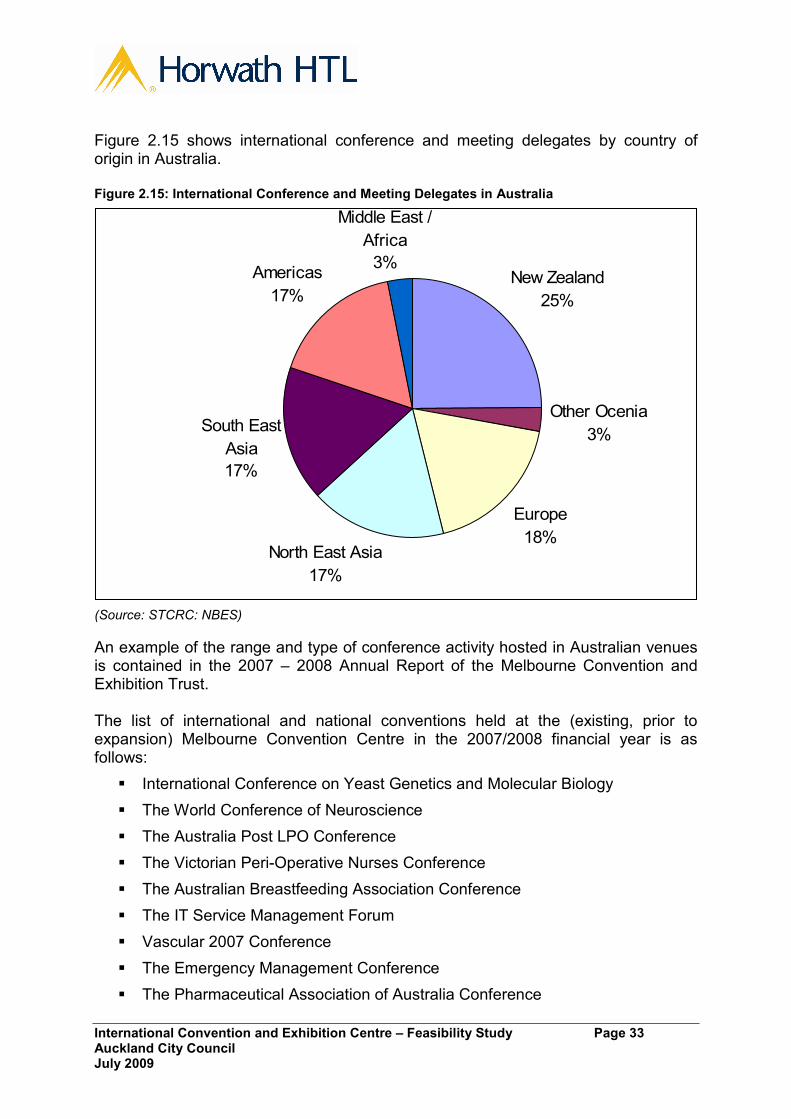

2.2 AUSTRALIAN CONVENTION ACTIVITY The National Business Events Study8 (“NBES”) produced by the Sustainable Tourism Cooperative Research Centre (“STCRC”) recorded a total of 20 million meeting and conference delegates in 2003, of which approximately 1% or approximately 200,000 visitors were of international origin9. According to the study, New Zealand was Australia’s largest international market representing nearly 25% of total international conference and meeting delegates. The next largest market was Europe, generating nearly 18% of total international conference and meeting delegates.

8 Latest version published in 2005 and based on 2003 data 9 According to Tourism Australia visitor arrival statistics, there were 280,300 international conference arrivals in 2004.

International Convention and Exhibition Centre – Feasibility Study Page 33 Auckland City Council July 2009

Figure 2.15 shows international conference and meeting delegates by country of origin in Australia. Figure 2.15: International Conference and Meeting Delegates in Australia

New Zealand

25%

Other Ocenia

3%

Europe

18%North East Asia

17%

South East

Asia

17%

Americas

17%

Middle East /

Africa

3%

(Source: STCRC: NBES)

An example of the range and type of conference activity hosted in Australian venues is contained in the 2007 – 2008 Annual Report of the Melbourne Convention and Exhibition Trust. The list of international and national conventions held at the (existing, prior to expansion) Melbourne Convention Centre in the 2007/2008 financial year is as follows:

� International Conference on Yeast Genetics and Molecular Biology

� The World Conference of Neuroscience

� The Australia Post LPO Conference

� The Victorian Peri-Operative Nurses Conference

� The Australian Breastfeeding Association Conference

� The IT Service Management Forum

� Vascular 2007 Conference

� The Emergency Management Conference

� The Pharmaceutical Association of Australia Conference

International Convention and Exhibition Centre – Feasibility Study Page 34 Auckland City Council July 2009

� The 9th Australian Palliative Care Conference

� The Australia and New Zealand Mental Health Services Conference

� Apimondia

� Aged Community Services Conference Australia

� The Australasian Association of Clinical Research Conference

� Australian Market and Social Research Society Conference

� Financial Planning Association National Conference

� Australian Health and Medical Research Conference

� Asia Pacific Congress of Heart Failure

� International Society of Aesthetic Plastic Surgery Conference

� Ottawa International Conference on Clinical Competence

� World Congress on Endometriosis

� Enviro 2008

� Irrigation Australia 2008

� Annual Meeting of Organisation of Human Brain Mapping

� World Mental Health Conference

� International Symposium on Forensic Science

� Australian Human Resource Institute Conference

� Scientific Meeting on Medical Imaging and Radiation Therapy.

2.3 GROWTH IN CONVENTION AND EXHIBITION CENTRES – ASIA PACIFIC The strong growth in international conference activity in the Asia / Middle East / Pacific region (refer Section 2.1) has partly been stimulated by the substantial growth in large-scale convention and exhibition centre developed in Asia and Australia during the past 10 – 15 years. Figure 2.16 illustrates the growth in conference / exhibition floor space capacity by country and venue in the Asia-Pacific Region over the past 12 years. Japan had the largest exhibition floor space until 2005 when Singapore Expo undertook a major expansion and Hong Kong opened Asia World-Expo. Australia has for this period of time dropped from third place to seventh in the Asia-Pacific Region in terms exhibition floor space capacity despite their expansions.

International Convention and Exhibition Centre – Feasibility Study

Page 35

Auckland City Council

July 2009

Figure 2.16: Exhibition Floor Space Capacity by Country and Venue in Asia / Pacific

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

M LH

Singapore

Australia

China

Malaysia

Thailand

South Korea

Philippines

Hong Kong

Singapore Expo

Singapore Expo

MATRADE, Kuala Lumpur

Kuala Lumpur

Convention Centre

Putra, Kuala Lumpur

Indonesia

Shanghai

Bangkok

Queen Sirikit, Bangkok Japan

Tokyo

Philippine, Manilla

SMX, Manilla

Hong Kong

Asia W

orld-Expo, Hong Kong

Gold Coast

Perth

Sydney

Cairns

Brisbane

Melbourne

Jakarta

Suntec, Singapore

IntexOsaka

Pattaya

MakuhariMesse, Chiba

Adelaide

ICC Jeju, Siogwipo

COEX, Seoul

Nagoya

CNCC, Beijing

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

M LH

Singapore

Australia

China

Malaysia

Thailand

South Korea

Philippines

Hong Kong

Singapore Expo

Singapore Expo

MATRADE, Kuala Lumpur

Kuala Lumpur

Convention Centre

Putra, Kuala Lumpur

Indonesia

Shanghai

Bangkok

Queen Sirikit, Bangkok Japan

Tokyo

Philippine, Manilla

SMX, Manilla

Hong Kong

Asia W

orld-Expo, Hong Kong

Gold Coast

Perth

Sydney

Cairns

Brisbane

Melbourne

Jakarta

Suntec, Singapore

IntexOsaka

Pattaya

MakuhariMesse, Chiba

Adelaide

ICC Jeju, Siogwipo

COEX, Seoul

Nagoya

CNCC, Beijing

(Source: Venues web sites)

Note: 1. Left arrows illustrates venues that were built before 1997 and or venues that have been expanded since their original building year

2. Dashed lines illustrates venues of smaller exhibition floor space capacity than the venue with largest exhibition floor space capacity in the country

3. Solid lines illustrates the venue with the largest exhibition floor space capacity within the country

International Convention and Exhibition Centre – Feasibility Study Page 36 Auckland City Council July 2009

Appendix 6 contains a schedule of the major convention and exhibition centres in New Zealand, Australia and Asia.

The schedule identifies the date of opening, and (where applicable) expansion of the facilities. This confirms a significant expansion in convention centre supply, and an even greater expansion in exhibition space. Many of the Asian facilities have been developed as icons of national pride for hosting regional and international inter-governmental meetings and conferences. Hosting large-scale regular trade shows has also been a significant driver of the expansion of exhibition facilities. In the case of Australia, a significant factor in the development and expansion of facilities has been driving economic impact at a state level. Therefore, winning national conferences and exhibitions (which attract inter-state conference delegates) is important, as well as winning international conferences and exhibitions, for many of the Australian venues.

2.4 NEW ZEALAND INTERNATIONAL CONFERENCE ACTIVITY International visitor arrivals to New Zealand for the year ended December 2008 amounted to 2.46 million, of which 2.3% (or approximately 57,000 visitors) indicated their main reason to visit was to attend a conference in New Zealand.10 Figure 2.17 shows the growth in conference-related international visitor arrivals between YE December 2000 and 2008. Figure 2.17: Growth in Conference-related International Visitor Arrivals

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

YE December

Conference Related Visitor Arrivals

(Source: International Visitor Arrival Statistics, Statistics New Zealand)

10 International Visitor Arrival Statistics, Statistics New Zealand

International Convention and Exhibition Centre – Feasibility Study Page 37 Auckland City Council July 2009

The international conference market has experienced a compound average growth rate (“CAGR”) between 2000 and 2008 of 6.6%, despite a plateauing of arrivals since 2005 at approximately 60,000 per annum. Factors contributing to the growth in international delegate arrivals include:

���� New Zealand’s reputation as a ‘safe’ country, building on the success of Tourism New Zealand’s 100% Pure marketing campaign

���� dedicated resourcing and focus of international conference marketing by Conventions and Incentives New Zealand and regional convention bureaus, especially in the Australian market

���� competitive airfares, especially on the trans-Tasman routes

���� new and refurbished convention facilities becoming established in the market (eg: Christchurch Convention Centre, SKYCITY Auckland Convention Centre, Auckland Convention Centre at THE EDGE®) thereby improving New Zealand’s competitiveness in the international conference market, and particularly in relation to Australian corporate and association conference markets.

As shown in Figure 2.18, New Zealand’s key source markets for conference-related visitors in 2008 were Australia (59%), Asia (15%) and the Americas (10%). Figure 2.18: Source Markets of Conference-related Visitors (2008)

Australia

59%Asia

15%

Americas

10%

Other

8%

Europe

8%

(Source: International Visitor Arrival Statistics, Statistics New Zealand)

As illustrated in Figure 2.19, between 2000 and 2008, the source markets with the highest CAGRs were Asia (9.9%) followed by Australia (7.1%).

International Convention and Exhibition Centre – Feasibility Study Page 38 Auckland City Council July 2009

Figure 2.19: Growth in Source Markets of Conference-related Visitors

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2000 2001 2002 2003 2004 2005 2006 2007 2008

YE December

Conference-related Visitor Arrivals

Australia Asia Americas Europe Other

(Source: International Visitor Arrival Statistics, Statistics New Zealand)

2.4 CONFERENCE ACTIVITY IN NEW ZEALAND MAIN CENTRES

Based on the National Convention Activity Survey11, Auckland, Wellington and Canterbury (mainly Christchurch) hosted approximately 3,500 multi-day conferences between them in the year ended June 2008.

Auckland is dominant in terms of the numbers of conferences held in New Zealand. This reflects:

� the dominance of corporate meetings and conferences over association meetings12, supported by Auckland’s position as New Zealand’s leading commercial centre

� the dominance of major hotels, and hotel conference venues, in Auckland13 (eg: The Langham, Hyatt Regency, Stamford Plaza, Rendezvous and Hilton hotels)

� the opening of the new SKYCITY Auckland Convention Centre in 2003, and the expansion / refurbishment of conference facilities at THE EDGE® at the same time.

Figure 2.20 provides a summary of the number of multi-day conferences (both corporate and association) in the three main centres between YE June 2004 and 2008.

11 Convention Activity Survey, Angus & Associates

12 Approximately

2/3 of New Zealand conferences are corporate conferences

13 Approximately 40% of New Zealand’s major hotel room supply is in Auckland

International Convention and Exhibition Centre – Feasibility Study Page 39 Auckland City Council July 2009

Figure 2.20: Total Multi-day Conferences in New Zealand Main Centres

International Convention and Exhibition Centre – Feasibility Study Page 40 Auckland City Council July 2009

3. CURRENT AND EXPECTED FUTURE MARKET TRENDS

A number of current and expected future trends are addressed in this section including trends in convention centre design and capability and trends in international conference buyer demand.

Appendix 2 contains the results of a survey of leading international Professional Conference Organisers (“PCOs”).

3.1 SUSTAINABILITY Sustainability has become a key focus in the international (and local) conference industry largely because of increased awareness and concern of consumers regarding the ‘carbon footprint’ of travel. This may become an increasingly significant factor in conference buyers considering the choice of destination for international conferences in the future, responding to the views and perceptions of conference delegates. This presents a risk to New Zealand (and Australia) in terms of marketing to and winning international conventions, assuming environmental concerns continue to be ‘top of mind’ to the consumer, although the risk is less in relation to domestic, Australasian and Asia / Pacific conferences. Australasian destinations may become proportionately less favourable over time than if there were no environmental concerns. It is unlikely, however, that distance will become the critical decision factor in the choice of location, even if it is still one factor, for most international conferences, although it may become a critical decision factor in the choice of location for international conferences14. There is no particular reason why convention delegate arrivals to New Zealand would be worse affected than leisure visits from international visitors. Arguably, leisure travel is more of a ‘luxury’ and discretionary nature and therefore less ‘justifiable’ than international conference attendance. For example, it will always be important for professional training and development for doctors to attend medical conferences, the largest international association conference segment. Appendix 2(I) contains responses from international PCO’s to the following questions:

� If NZ was to demonstrate an outstanding commitment to sustainability in its approach to its convention centre facilities and marketing, what might that look like?

� Do you believe that the distances involved in travelling to NZ have a negative impact on NZ as a convention destination. If ‘yes’, please describe those impacts and how long-term you think they may be.

14 Alan Trotter, CEO, Conventions and Incentives New Zealand

International Convention and Exhibition Centre – Feasibility Study Page 41 Auckland City Council July 2009

The focus of the conference industry is on how to mitigate these potential impacts / risks. The industry response is still emerging, and is being pro-actively integrated into forward planning, and involves:

� new convention centres being developed to rigorous environmental standards (eg: the new ‘6 star’ Melbourne Convention and Exhibition Centre)

� accreditation / certification of existing and new venues, organisers, suppliers, etc.

There is an opportunity for the New Zealand conference industry to present a ‘leading edge’ industry-wide approach to environmental sustainability. Such an industry-wide approach should be led by the ‘flagship’ national convention centre. Other leading venues in New Zealand are already Green Globe certified15 or ISO accredited16. Green Globe is a worldwide Benchmarking, Certification and Performance Improvement programme developed specifically for industry. Green Globe assists organisations improve their economic, social and environmental sustainability while being rewarded and recognised for it. These achievements are underpinned by the Green Globe Company Standard, which sets out the guidelines, procedures and Self-Assessment Checklist organisations must follow to achieve sustainability. The Green Globe Company Standard provides organisations with a framework to conduct a comprehensive assessment of their environmental sustainability performance, through which they can monitor improvements and achieve certification. The focus is not just on ‘green’ venues but on wider ‘sustainability’ issues. This incorporates ‘green’ and Corporate Social Responsibility (“CSR”). The international event management company MCI17 has produced Sustainable Event Standards which includes the following extracts: