30

Introduction

Introduction

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 1

Blackstone: Leaving the pack behind

FAST LANE

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 2

What you may not know about Blackstone

Our funds created $33 billion of value in the past year

In the past year investors entrusted us with $52 billion in additional funds

We invest for over half of all U.S. pensioners

Innovation has driven $122 billion in AUM from new products since our IPO

We are the most profitable asset manager in the world

We have a greater presence on social media than any of our peers

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 3

2007 Today

$165

$84

$357

BX Alternatives

$38 $19 $6

$40 $41

$100

BX Alternatives

2007 Today

# of Public Companies

Market Cap and Free Float ($ in billions)

# of Institutions with >1mm Shares of BX

Average Daily Trading Volume ($ in millions)

The “Alternatives” have evolved

3

8

IPO Today

14

65

________________________________________________

Note: As of June 10, 2014. Alternatives include: APO, ARES, BX, CG, FIG, KKR, OAK and OZM.

Float Mkt Cap

2007 Today

Float Mkt Cap

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 4

Where would Blackstone rank today in the S&P 500?

________________________________________________

Note: As of June 10, 2014.

Market

Market

Cap / LTM

Avg. Daily

Trading

Cap Employees Employee Earnings Volume ’13A ’14E

Blackstone $38,014 2,016 $18.9 $3,700 $165 4.3% 5.4%

Median for Asset Managers in S&P 500 22,149 7,523 3.3 1,255 97 2.0% 2.0%

S&P 500 Financials Median 19,498 10,991 1.1 1,004 108 2.0% 2.1%

S&P 500 Median 17,983 17,800 1.0 796 124 1.6% 1.7%

In which quartile would

Blackstone rank?1 4 1 1 2 1 1

Dividend Yield

($ in millions)

Blackstone 5

2014 Blackstone Investor Day

Blackstone’s earnings are not closely linked to the stock market

R² = 0.22

-300%

-200%

-100%

0%

100%

200%

300%

-20% -15% -10% -5% 0% 5% 10% 15% 20%BX

EN

I

S&P 500

Blackstone Earnings vs. S&P 500

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 6

$0.4bn

$6.9bn

’98 ’00 ’02 ’04 ’06 ’08 ’10 ’12 1Q’14 LTM

The market values growth

31%

26%

10x

10%

24%

16x

15%

26%

23x

11%

39%

19x

9%

30%

23x

BX Asset Managers Advisory Firms Biotech Software

Earnings Growth(1)

Stock Volatility(2)

’14E P/E(3)

________________________________________________

Note: Asset managers include: AB, AMG, BEN, BLK, EV, FII, IVZ, JNS, LM, TROW and WDR. Advisory firms include: LAZ, GHL, EVR, and MC. Biotech and Software based on the Global Industry Classification Standard. (1) As of December, 31, 2013. Trailing 3-year CAGR. (2) Based on the average of the implied volatility (6M, 100 strike) for the companies within the industries. (3) Based on 2014 consensus estimates.

From peak to peak the growth was 120%

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 7

LTM 1 2 3 4 5 6 7 8 9 10Years

Current 1 2 3 4 5 6 7 8 9 10

Years

What’s it all worth?

________________________________________________

Note: Presentation of hypothetical growth in Fee-Earning AUM and Distributable Earnings not intended to project future performance. Calculation of hypothetical Distributable Earnings per unit is intended to be illustrative and for that purpose contains a number of assumptions including, among others, constant management and performance fee rates and margins over the ten-year period, a 2x realized multiple of invested capital over an average hold period of 4.5 years for our draw-down funds and an effective tax rate of 15%–20% on taxable income for the ten-year period. Cumulative distributions paid assumes 100% payout of Distributable Earnings. Analysis assumes no reinvestment of distributions paid.

Average Cash Earnings: $2.70

$4.15

$610

$204

Yield in Year 10

Year 10 excluding

Distributions

Cumulative Distributions

Paid Total

6% $69 $27 $96

5% $83 $27 $110

4% $104 $27 $131

+ + +

= = =

Hypothetical Fee-Earning AUM ($ in billions)

Hypothetical Distributable Earnings ($ per diluted unit) Implied Stock Price

If:

12% AUM growth

2x multiple on invested capital

7%–10% liquid fund returns

60% below our historic rate

Stocks price 10-yr CAGR @96 – 11.0%

@110 – 12.5% @131 – 14.5%

Welcome Remarks

Blackstone 1

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Welcome to Blackstone’s fourth Investor Day

Private Equity

Joe Baratta

Dave Calhoun Real Estate

Jon Gray

Tactical Opportunities

David Blitzer

Hedge Fund Solutions

Tom Hill

Private Wealth

Brendan Boyle Finance & Technology

Laurence Tosi

Secondaries

Verdun Perry

Credit

Bennett Goodman

Blackstone 2

2014 Blackstone Investor Day

Leading market positions across all our businesses

People have been trying to imitate Blackstone for years…

Blackstone 3

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Not easy to replicate

One of the best brands in all financial services

Most extensive network of institutional LP relationships

Deepest and broadest management team

Scale to handle large, complex transactions that others can’t

Better information; seamless sharing of knowledge and ideas

Unique culture

Tradition of winning

The only firm with leadership positions across multiple businesses

Blackstone 4

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

What makes Blackstone different?

Small Firm Feel

each person makes a difference

An enduring culture that is

unique and compelling

Engaged Leaders

shaping and guiding people daily

Flat Organization

no bureaucracy; move quickly

Talent

deep; broad; driven

Innovation

entrepreneurial spirit

Camaraderie

cohesive teams; common mission

Passion

drive to win

Blackstone 5

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

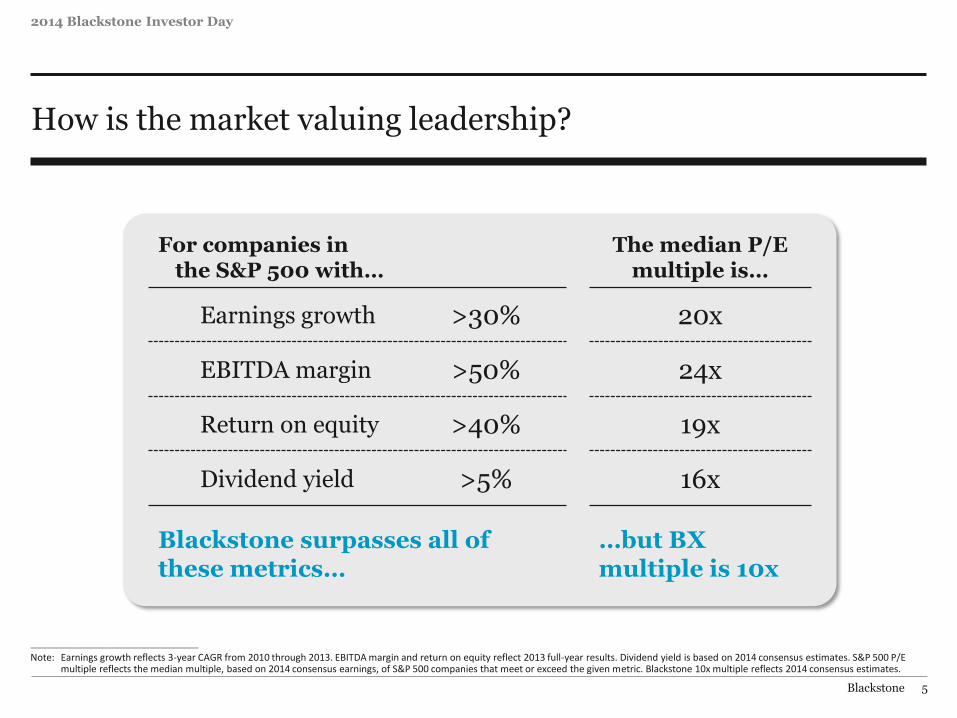

How is the market valuing leadership?

________________________________________________

Note: Earnings growth reflects 3-year CAGR from 2010 through 2013. EBITDA margin and return on equity reflect 2013 full-year results. Dividend yield is based on 2014 consensus estimates. S&P 500 P/E multiple reflects the median multiple, based on 2014 consensus earnings, of S&P 500 companies that meet or exceed the given metric. Blackstone 10x multiple reflects 2014 consensus estimates.

For companies in the S&P 500 with…

The median P/E multiple is…

Earnings growth >30% 20x

EBITDA margin >50% 24x

Return on equity >40% 19x

Dividend yield >5% 16x

Blackstone surpasses all of these metrics…

…but BX multiple is 10x

GSO

GSO’s Business Today

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 2

Global footprint with over 250 employees in New York, London, Dublin and Houston

GSO Capital Partners

$66.0 billion

Mezzanine Funds

$7.8 billion

Rescue Lending Funds

$8.8 billion

BDCs (Small Cap

Direct Lending)

$11.0 billion

CLOs

$20.3 billion

Closed End & Commingled

Funds, ETF and SMAs

$10.5 billion

Hedge Fund Strategies

$7.6 billion

Private Market Strategies Public Market Strategies

Total Assets Under Management

GSO question – can we change color of dotted lines and text color of bottom labels

Alternative Investment Funds

$35.2 billion

Customized Credit Strategies – Long Only

$30.8 billion

________________________________________________

Note: The AUM for Blackstone, GSO or any specific fund, account or investment strategy presented in this Presentation may differ from any comparable AUM disclosure in other non-public or public sources. Certain of these differences are in some cases required by applicable regulation.

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 3

Our Mission: Strong investment results across our strategies

________________________________________________

Note: Past Performance is not necessarily indicative of future results. See “Important Disclosures” section at the front of the presentation book. (1) Rescue Lending Flagship funds and Mezzanine Flagship funds returns shown from inception of the first flagship fund of each strategy (September 2009 and June 2007, respectively) through March 31,

2014. BDCs shown from inception of first fund in January 2009 through March 31, 2014. Hedge Fund Strategies Flagship Funds shown from inception (August 2005) through March 31, 2014. Leveraged Loans shown from December 2000 through March 31, 2014.

(2) Indices, in order, are as follows: DJ CS Event Driven Distressed, CS High Yield Index + 200bps, 80% CS LLI / 20% CS HYI, HFRI Fund Weighted Composite and CS Leveraged Loan Index. (3) U.S. Leveraged Loans Composite includes U.S. CLO and other vehicles where at least 80% of the invested assets are senior secured bank loans. Performance is presented gross of fees. Estimated net

returns for this composite are 3.8% and 4.5% for 2013 and ITD, respectively, assuming a 1.25% management fee. The performance of CLO portfolios included in this composite is calculated based on the unlevered underlying portfolio assets within the CLO structure. Actual management fees for accounts within this composite vary. CLOs within this composite also have an incentive fee specific to the fund, subject to an IRR hurdle, which is not included here.

2013 Results Inception to Date(1)

Strategy AUM Net Returns Net Returns Index(2)

Private Market Strategies

Rescue Lending Flagship Funds $8.6 24.3% 17.6% 9.2%

Mezzanine Flagship Funds 5.4 17.9% 19.0% 10.4%

Small Cap Direct Lending (BDCs) 11.0 16.5% 15.8% 14.1%

Public Market Strategies

Hedge Fund Strategies Flagship Funds $4.5 18.2% 9.4% 4.8%

U.S. Leveraged Loans Composite(3) 7.8 5.1% 5.7% 5.0%

($ in billions)

GSO’s Evolution

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 5

71% of our AUM and 34% of LPs are invested in products that did not exist five years ago

Evolution of the GSO platform

________________________________________________

(1) Alternative assets only.

December 31, 2008 March 31, 2014

Total AUM: $22.4 $66.0

Alternatives 5.9 35.2

Customized Credit Strategies 16.5 30.8

% of AUM from products that didn’t exist in 2008(1) – 71%

% of LPs invested in products that didn’t exist in 2008(1) – 34%

($ in billions)

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 6

Where have we grown?

Over the past five years, $25 billion of our AUM growth has come from new products and strategies

As of December 31, 2008 As of March 31, 2014

Hedge Fund Strategies Flagship funds $2.7 $4.5

Mezzanine Flagship funds 2.0 5.4

Rescue Lending Flagship funds – 8.6

Strategic SMAs(1) – 5.3

BDCs – 11.0

Other Credit Funds(2) 3.6 0.3

Customized Credit Strategies 14.1 30.8

Total AUM $22.4 $66.0

________________________________________________

(1) Includes various SMAs, co-investments and opportunistic funds managed by GSO. (2) Includes legacy funds currently in wind down.

($ in billions)

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 7

How have we achieved this growth?

Raise new pools of capital based on key industry themes developed within GSO and Blackstone

Examples: energy and residential housing

Rescue Lending Funds

Business Development Corps (BDCs)

CLO consolidation

Created over $5 billion in separate accounts with large LPs over past few years

Capitalizes on LP trend to consolidate GP relationships

Allows LPs to invest more capital quickly with better fees and greater transparency

Products that capitalize on strong demand for yield by retail investors: Closed-End Funds, ETF, BDCs

Tapping into private banks for distribution: Rescue Lending, Mezzanine and Hedge Funds

Leverage Industry Themes

Capitalize on Market Dislocations and

Regulatory Changes

Strategic Partnerships with Large LPs

Retail Channels

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 8

Capitalizing on industry themes: Energy and Power

GSO has invested over $15 billion in the Energy sector since 2005

Dedicated Energy team of 16 people with unique sector expertise and long-standing management relationships

Energy fits extremely well within GSO’s investment approach

• Deal flow driven by significant capital needs and fragmented nature of the industry

• Hard asset value coupled with commodity exposure should allow for downside protection

and upside participation

We have leveraged our Energy capability across the GSO platform

• $1 billion of Energy separate accounts

• Energy-focused BDC (~$3 billion)

• GSO believes high exposure to Energy investments has driven strong investment results across funds and has enabled us to raise larger sized funds

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 9

Select GSO Energy and Power investments

________________________________________________

Sub Sector / Theme Privately Originated Public Investments

Upstream

Midstream

Service and Equipment

Power Generation

Pecos

Lake Road Generating Calpeak

________________________________________________

All rights to the trademarks listed herein belong to their respective owners, and GSO’s use hereof does not imply any affiliation with, or endorsement by, the owners of these trademarks.

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 10

GSO’s Energy investments touch the major U.S. oil & gas plays

________________________________________________

Note: Green shading represents key U.S. oil & gas production area.

Exploration & Production

Midstream

Power

Services

Utica

Bakken

Exploration & Production

Midstream

Power

Services

Utica

Bakken

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 11

Capitalizing on industry themes: residential housing

Opportunistically invested $4 billion of capital across public and private strategies as our view on the housing recovery evolved(1)

________________________________________________

(1) Includes long investments made in GSO’s Hedge Fund Strategies funds, Rescue Lending funds, Mezzanine funds, total commitments for GSO’s dedicated Land Bank Fund and investments made by alternative investment SMAs managed by GSO since GSO’s inception within the Homebuilder, Building Materials and Real Estate sectors.

2006 2007 2008 2009 2010 2011 2012 2013

2006–2007

Bearish view

Short positions

2009

GSO provides capital to mid cap homebuilders: • Beazer Homes • Plygem • KB Homes

2013–2014

Rescue financings for Morris Homes, KP1

Hedge fund positions in Beazer, iStar, Quinn Group

GSO forms dedicated $500 million Land Bank Fund

2008

Cautious but turning constructive

Investment in Standard Pacific

2011–2012

Positive view on homebuilding recovery GSO deploys capital across public and private funds Invested in Hovnanian, City Ventures, Miller Homes,

CEMEX, Giant Cement, Cementos Portland and Realogy Land bank strategy initially deployed in hedge and

mezzanine funds

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 12

Select GSO homebuilder and building products investments

________________________________________________

All rights to the trademarks listed herein belong to their respective owners, and GSO’s use hereof does not imply any affiliation with, or endorsement by, the owners of these trademarks.

Sub Sector / Theme Privately Originated Public Investments

Homebuilders / Realtor

Building Products

REITs

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 13

Market dislocation and regulatory changes

GSO’s views on market opportunity

Significant structural and regulatory changes in financial markets create opportunity for GSO

Global investment banking model moved to “Capital Lite”

Volcker Rule / Dodd-Frank / OCC Leverage Guidelines

Basel III

CLO “skin in the game” requirements / limited new issuance

GSO Activities Rescue Lending Flagship Funds BDCs CLO Acquisitions

Launch: September 2009 January 2009 April 2010

New AUM(1): $8.6 billion $11 billion $15 billion

Strategy: Rescue lending Small cap direct

lending Consolidation of the

CLO industry ________________________________________________

(1) Rescue Lending Flagship Funds New AUM reflects AUM of GSO’s flagship Rescue Lending funds as of March 31, 2014. BDCs New AUM reflects AUM of GSO’s Small Cap Direct Lending funds as of March 31, 2014. CLO Acquisitions New AUM reflects the dollar amount of CLOs acquired by GSO following April 2010.

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 14

What’s next?

GSO’s views:

Credit markets remain frothy

• Yields and spreads at record lows

• Public market deals have more aggressive leverage, weaker covenants and lower credit quality

• Sets up well for next distressed cycle

Activity in Europe picking up significantly

Areas of Focus:

• European direct lending fund – $2.5 billion

• Expand into emerging market corporate debt

• Additional capital for energy activities

• Forge new strategic partnerships with large LPs

184 0 92 102 0 70 0 152 195 99 206 202 201 221 3 0 103 120

2014 Blackstone Investor Day

Blackstone 15

Why are we well positioned for the future?

Investment Performance

Superior results generated across the platform

Believe we’re top quartile performer in all of our major strategies

Unique Competitive Advantages

Ubiquitous presence in below investment grade corporate credit

Scale enables us to do deals that others can’t

“Blackstone / GSO” brand globally recognized by companies and boards

Tradition of Innovation

Long track record of providing creative solutions

Market volatility and dislocations are our opportunity to grow

Culture

Entrepreneurial group of 15 SMDs

Strong cooperation across Blackstone and GSO

Excellent alignment with our LPs