No part of it may be circulated, quoted, or reproduced for distribution outside the organization without prior written approval from Fullerton India Home Finance Co. Ltd. Fullerton India Home Finance Co. Ltd. Investor Presentation Quarter ended March 31 st 2020

Transcript

No part of it may be circulated, quoted, or reproduced for distribution outside the organization without prior written approval from

Fullerton India Home Finance Co. Ltd.

Fullerton India Home Finance Co. Ltd.

Investor Presentation

Quarter ended March 31st 2020

AGENDA

Industry Landscape

About Grihashakti

Business Highlights

Risk Management

Liquidity Management

Financial Performance

2

Industry Landscape

3

4

‘We always over-estimate the Change that will occur in the next two years & underestimate the Change that will occur in the nextten.’ – Bill Gates

36%

48%51%

64%69%

2015 2019 2020 2025 2027

India's Millennial as % of Workforce**

Incremental demand

198

164 150 137

56

-

50

100

150

200

1980 1990 2000 2010 2015 2019

Credit-to-GDP ratio*

KR UK US MY IN

Underpenetrated Market

Source –** Morgan Stanley ^PwC – GDP at purchasing power parity (PPP) adjusts for price level differences providing a better measure of the volume of goods and services produced. *BIS (KR: Korea UK: United Kingdom US: United States MY: Malaysia IN: India)

India's economy is poised to become third-largest by 2027 with $6 trillion GDP**

8.7

11.8

15.7

2016 2020 2025

GDP in PPP^ (US$ trillion)

Growth potential

Housing FinanceBuoyed by demographics, unmet demand

Segment Opportunity

Total Household Population

~110 Mio

~140 Mio

~1,100 Mio

Per Capita Income

$ 8,800

$ 3,000

$ 1,200

• Indian mortgage market is significantly

underpenetrated. Mortgage to GDP Ratio at 10%

• Rising trend of urbanization (at 34%) resulting in

increasing GDP per capital ($) 2019 at US$ 2,242

• Improving affordability, nuclearisation of families,

emergence of tier-II and tier-III cities, ease of

financing, tax incentives to support growth

• Government measures continue to help the sector.

Extending Small Ticket Loans in Tier 1 peripherals, Tier 2 & 3 towns

NHB Refinance Diversifies funding mix and

supplements bank borrowings

Risk Weighted Assets

Lower risk weightage for Home Loans

SARFAESI Applicable across ticket sizes for

Housing Finance Cos.

Valuation premium

100% secured business enhances valuation multiplier of the group

Consumer Benefit

Tax incentives

Government subsidies & schemes

HFCs’ average loan life is ~7-8 years

Annuity Income

Consumer

• Housing for all (Pradhan Mantri Awas Yojana) scheme to address urban housing shortage, CLSS to push affordable housing extended till Mar-21

• Home buyers recognized as financial creditors under IBC

• RERA implementation – protecting interests of buyers

• Union Budget 2020 has continued its focus on affordable housing segment. It has favoured both home buyers and developers in terms of tax incentives

Developer • Tax holiday for real estate cos. involved in affordable projects

• GST rates slashed for under-construction flats to 5% and affordable homes to 1%, effective from April 1, 2019

• Smart City Project - plan to build 100 smart cities

• RERA regulation to enhance developer performance & transparency

Regulatory / Government Support

• Relaxation in LTV norms and risk weight guidelines

• Grant of infrastructure status to affordable housing

• Better access to funds with revised ECB regulation

• Enhanced Home Loan limit under Priority Sector Lending (PSL)

• NHB refinancing limit for HFCs increased to INR 300 billion

• Reduction in the minimum holding period for assets to be securitised

• Asset purchase under government guarantee scheme

HFC vs. NBFCs

The HFC Advantage

Impetus for Long-term growth

6

About Us – The Group

7

8

Fullerton Financial Holdings, Singapore (FFH) is a wholly

owned subsidiary of Temasek Holdings

• Temasek is a global investment company, headquartered in

Singapore

• FFH invests in and operates financial institutions in

emerging markets

Fullerton India Credit Co. Ltd. (FICCL) is a wholly-owned

subsidiary of FFH

• FICCL was acquired by FFH in December 2005

• Launched Commercial Operations in January 2007

• Pan-India presence established across 22 states and 3

union territories

• Retail finance products for urban and rural households as

well as SMEs

Grihashakti, Fullerton India Home Finance Co. Ltd. is a

wholly-owned subsidiary of FICCL

• Commenced operations in December 2015

About UsHousing Finance arm of Fullerton India

Temasek Holdings (Private) Ltd.

Fullerton Financial Holdings Pte Ltd

Fullerton India Credit Company Ltd.

Fullerton India Home Finance Company Ltd.

Wholly owned subsidiary

Wholly owned subsidiary

Wholly owned subsidiary

Fullerton Management Pte Ltd

Angelica Investments Pte Ltd

Wholly owned subsidiary

96.15%

3.85%

DUBAI, UAE6 outlets34k Cust

INDIA648 Branches3,200k Cust

Central CHINA4 Provinces,41 Outlets100k Cust

CHINA127 Community Banks2400k Customers

MYANMAR51 Branches223k Cust

CAMBODIA POST BANK103 Branches129k Cust

MALAYSIA82 Branches957 k Cust

Fullerton Financial Holdings (FFH) has 8 operating financial services entities located across 6countries.

9

INDIADigital MSME

55K Cust

FFH operates financial institutions in emerging marketsFocused on SME and mass market customer segments

*FFH is a wholly owned subsidiary of Temasek ^Fullerton Home Finance is a wholly owned subsidiary of Fullerton India

Fullerton Home Finance^

Multi-product offerings support a range of customer needs

Consumer

Urban MSME

Rural

Cross-Sell

Personal Loans, Loans Against Property

Commercial Vehicle Loans, Business Loans, Loans Against Property

Personal / Group Loans, Loans Against Property, Vehicle Loans

Life / General Insurance

Established Customer Connect across Urban and Rural India

24,805 Cr

AUM (INR)

> 3.6 MioCustomers

648

Branches

14,264Employees

58,000

Villages

AAARating*

Data as at FY 20. *Rating CRISIL, ICRA, CARE. (Temasek rated 'AAA/Stable' by S&P Global)

Fullerton India Credit CompanyA wholly-owned subsidiary of Fullerton Financial Holdings

Digital Tapping expanded (newer & wider) segment of customers

10

The Foundation For our Strategy and Culture

VisionBe the Company of choice in financial services for our customers, employees, communities and

stakeholders, recognized for innovation and high ethical standards.

Values

Agility

Diversity

Collaboration

Integrity

Innovation

Excellence

11

Board & Management TeamStrong Oversight and Guidance

12

Anindo MukherjeeChairman – Grihashakti,

Non-Executive Director - Fullerton India Credit Co. Ltd

Rakesh MakkarCEO - Grihashakti,

Whole-time Director

Milan ShusterIndependent Director

Rajashree NambiarNon-Executive Director,

MD & CEO – Fullerton India Credit Co, Ltd

Board of Directors

Management Team

Pankaj MalikChief Financial Officer

Parag ShahChief Risk Officer

Ram KolliGM – Head Business & Product

Rakesh MakkarCEO - Grihashakti,

Whole-time Director

FFH has senior level representation on the Board and various committees of Board

Sudha PillaiIndependent Director

About Us - Our Journey

13

14

Jul-15

Dec-15

Nov-16

Sep-17

Mar-19

Jan-18Rated AA+ by CARE

Received HFC license with equity infusion of INR 1

Bio

Started operations with 20

branches

Sep-16

Crossed AUM of INR 10 Bio

Team size of 425

Nov-17SARFAESI Approval

Crossed AUM of INR 15 Bio

Crossed AUM of INR 30 Bio

Expanded – Added 20 more branches

Expanded network to 60 Branches Jun-19

Crossed AUM of INR 35 Bio

Enhanced network of 78 branches

Jul-19

Equity infusion of INR 2 Bio

Aug-19

CRISIL ‘AAA’ Rated

Closed securitization deal worth INR 2 Bio

Mar-20

Rated ‘AAA’ by CARE

Our Journey So FarSteady asset growth, geographical expansion

Nov-19 Crossed AUM of INR 43 Bio

Grihashakti Overview Deepening presence in underserved segments

15

AUM

INR 43,016 Mio

Customer Acc.

~23,000

Average Yield

12.7%

Avg. Ticket Size

2.0 Mio

Home Loan AUM

58%

Salaried (Units)

38%

Sales: Credit

3:1

No. of branches

78

Net Revenue

INR 2,369 Mio

Working Profit

INR 1,065 Mio

Net NPA

2.0%

C/I

55.1%

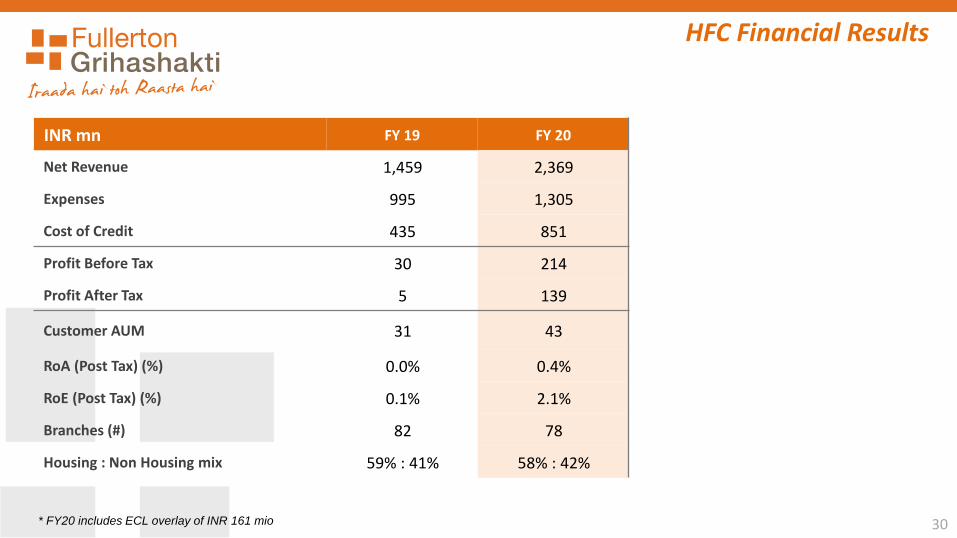

Financial Performance as of Mar-20

16

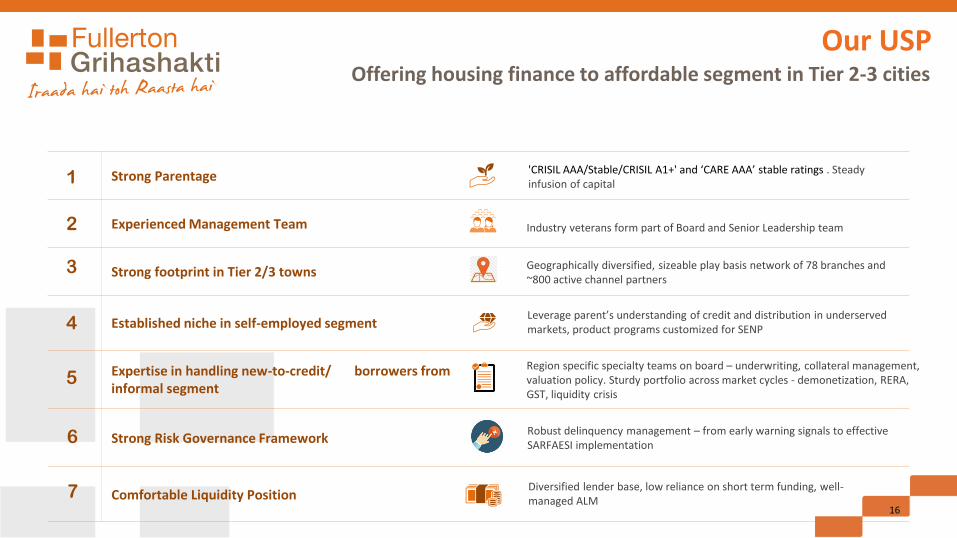

Strong Parentage

Experienced Management Team

Strong footprint in Tier 2/3 towns

Established niche in self-employed segment

Expertise in handling new-to-credit/ borrowers from informal segment

Strong Risk Governance Framework

Comfortable Liquidity Position

'CRISIL AAA/Stable/CRISIL A1+' and ‘CARE AAA’ stable ratings . Steady infusion of capital

Industry veterans form part of Board and Senior Leadership team

1

2

3

4

5

6

Geographically diversified, sizeable play basis network of 78 branches and ~800 active channel partners

Leverage parent’s understanding of credit and distribution in underserved markets, product programs customized for SENP

Robust delinquency management – from early warning signals to effective SARFAESI implementation

7 Diversified lender base, low reliance on short term funding, well-managed ALM

Region specific specialty teams on board – underwriting, collateral management, valuation policy. Sturdy portfolio across market cycles - demonetization, RERA, GST, liquidity crisis

Offering housing finance to affordable segment in Tier 2-3 cities

Our USP

Business Highlights

17

311.7%

141.1%

68.1% 68.2% 55.1%

FY16 FY17 FY18 FY19 FY20

Cost/Income Ratio

-49 -74

246465

1,065

FY16 FY17 FY18 FY19 FY20

Operating Profit (INR Mio)

23 180

770

1,459

2,369

FY16 FY17 FY18 FY19 FY20

Net Revenue(INR Mio)

137267

517774 805

FY16 FY17 FY18 FY19 FY20

People strength

18

Building Strong FranchiseSince inception performance

Note - FY16 and FY17 nos. are as per IGAAP while, FY18 and FY19 are as per IndAS

2424,735

19,022

30,654

43,016

FY16 FY17 FY18 FY19 FY20

AUM (INR Mio)

1472,348

9,664

16,519

22,892

FY16 FY17 FY18 FY19 FY20

Customer Base

19

Meeting Diverse Customer NeedsTrusted partner for customers, DSA channels

Product ShareProduct Suite

Fulfil dream of owning a home

• Home Loans (HL) –Purchase of New and Resale

• Home Improvement• Home Construction • Residential Plot and

Home Construction Loans

• Home Extension Loans

Expand Business /Working Capital

• Loan against Property (LAP)

• Lease Rental Discounting

• Loans for commercial property - New and Resale

• Loans for construction of commercial property

Access to developers• Approved Project

Financing• Construction

Finance (CF)

Programs customized for self-employed segment

• Liquid Income Program

• Gross Turnover Program

• Income Multiplier Program

• Banking Product• High Equity Program• EMI Equalizer

Program

59%

40%

1%

Closing AUM (March-20)

HL LAP CF

Geographic reach

• Major share of business from Tier 2-3-4 locations in FY20 with ATS of 2 Mio

• Expansion of Rural business to 5 states in FY21 for additional yield kicker

• Deepening presence in markets with healthy book and potential catchments

Collections Management

Strengthen footprint in Tier 2-3 towns

Fair-mix of Salaried and Self Employed

Managing New-To-Credit customers

Process Improvisation

Healthy Customer Mix

• Leverage parent’s understanding of credit and

distribution in underserved markets

• Product programs customized for SENP

• Geography specific rates for Salaried customers

• More products per customer; run cross-sell and up-

sell programs

New-To-Credit

• Drive Government schemes – PMAY, CLSS

• Region specific specialty teams on board – underwriting, collateral management, valuation policy

• Separate verticals for legal and technical team to have better control over collateral

Improvements in Operating Model

• Digitally enabled customer acquisition and

collection process

• Sales App acts as an single interface for on-

boarding and performance monitoring

• Centralised underwriting - cheque salaried / SE

affordable cases under income to help

standardise underwriting across geographies

Robust Collections Management

• Investments into data & analytics for risk

monitoring and service

• Pro-active monitoring based on external

environment, customer data, bureau trends

• Targeted collections process

20

Establishing Our NicheLeveraging our parent expertise in mortgage space

21

Build local scale; depth over breadth

Smart Usage of Analytics

AnalyticsProductivity

• Build business rule engine for reducing human

bias and faster processing

• Scorecard-based underwriting for HL

• Analytics driven up-sell and cross-sell program

• Usage of bureau data and analytics to identify

low-risk target segments

• Early allocation of high risk accounts through risk

segmentation of customers (based on bounce

and off us) on field to improve customer contact

ratio and conversion

Systems• Leveraging on-ground expertise and resources

sharing with FICC branches

• Policy trainings for frontline team

• Maintain healthy mix of DSA and Direct sourcing

• Enhance partnerships with banks, MFIs, fintech

firms, online alliances and developers

• Considering tough conditions for real estate, no

new cases for developer funding

• Less 10% portfolio is under-construction

• Focus on building a low cost, scalable operating model

• Reduce operating expenses through process enhancements

• Usage of digital assets – customer portal and mobile app for

loan origination

• Digital payment infrastructure for collections

Robust Housing Finance PlatformBuilding strong business franchise on the foundation of risk governance

Covid related activities

Portfolio Protection and Risk Mitigation

Process and Cost Re-engineering

Process improvement and digitization, Rationalizing expenses, Data mining and analysis, Workflows for

new ways of underwriting and risk mitigation

One TEAM approach for Sales, Credit & Collection verticals

Product Policy and Technical Valuation trainings conducted for frontline teams

Up-skilling, team activities to keep team engaged and motivated

This presentation has been prepared by Fullerton India Home Finance Company Limited (the “Company”) solely for your information. This presentation is for information purposes only and should not be deemed to

constitute or form part of any offer or invitation or inducement to sell or issue any securities, or any solicitation of any offer to purchase or subscribe for, any securities of the Company, nor shall it or any part of it or the

fact of its distribution form the basis of, or be relied upon in connection with, any contract or commitment therefor. The financial information in this presentation may have been re-classified and reformatted for the

purposes of this presentation. You may also refer to the financial statements of the Company available at https://www.grihashakti.com/home.aspx, before making any decision on the basis of this information.

This presentation contains statements that may not be based on historical information or facts but that may constitute forward-looking statements. These forward looking statements include descriptions regarding the

intent, belief or current expectations of the Company or its directors and officers with respect to the results of operations and financial condition of the Company. Such forward-looking statements are not guarantees of

future performance and involve risks and uncertainties, and actual results may differ from those in such forward-looking statements as a result of various factors and assumptions which the Company presently believes to

be reasonable in light of its operating experience in recent years but these assumptions may prove to be incorrect. Any opinion, estimate or projection constitutes a judgment as of the date of this presentation, and there

can be no assurance that future results or events will be consistent with any such opinion, estimate or projection. The Company does not undertake to revise any forward-looking statement that may be made from time to

time by or on behalf of the Company.

No representation, warranty, guarantee or undertaking, express or implied, is or will be made as to, and no reliance should be placed on, the accuracy, completeness, correctness or fairness of the information, estimates,

projections and opinions contained in this presentation. Potential investors must make their own assessment of the relevance, accuracy and adequacy of the information contained in this presentation and must make such

independent investigation as they may consider necessary or appropriate for such purpose. This presentation does not constitute and should not be considered as a recommendation by the Company that any investor

should subscribe for, purchase or sell any of Company's securities. By viewing this presentation you acknowledge that you will be solely responsible for your own assessment of the market and the market position of the

Company and that you will conduct your own analysis and be solely responsible for forming your own view of the potential future performance of the business of the Company. None of the Company, book running lead

managers, their affiliates, agents or advisors, the placement agents, promoters or any other persons that may participate in any offering of any securities of the Company shall have any responsibility or liability whatsoever

for any loss howsoever arising from this presentation or its contents or otherwise arising in connection therewith. This presentation and its contents are confidential and should not be distributed, published or reproduced,

in whole or part, or disclosed by recipients directly or indirectly to any other person. Viewing this information may not be lawful in certain jurisdictions. In other jurisdictions only certain categories of person may be

allowed to view this information. Any person who wishes to view this site must first satisfy themselves that they are not subject to any local requirements which prohibit or restrict them from doing so. Please exit this

webpage if you are not permitted to view this presentation on this website or are in any doubt as to whether you are permitted to view these materials.

This presentation has been prepared by the Company based on information and data which the Company considers reliable, but the Company makes no representation or warranty, express or implied, whatsoever, and noreliance shall be placed on, the truth, accuracy, completeness, fairness and reasonableness of the contents of this presentation. This presentation may not be all inclusive and may not contain all of the information that youmay consider material. Any liability in respect of the contents of, or any omission from, this presentation is expressly excluded.