24

1 Investor Presentation March 2007

1

Investor PresentationMarch 2007

2

Forward-Looking Statement

Certain statements in this presentation constitute “forward-looking statements”within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known risks, uncertainties and other factors that may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Such factors include, among other things, (1) general economic and business conditions; (2) interest rate changes and the availability of mortgage financing; (3) the relative stability of debt and equity markets; (4) competition; (5) the availability and cost of land and other raw materials used by the Company in its homebuilding operations; (6) the availability and cost of insurance covering risks associated with the Company’s business; (7) shortages and the cost of labor; (8) weather related slowdowns; (9) slow growth initiatives and/or local building moratoria; (10) governmental regulation, including the interpretation of tax, labor and environmental laws; (11) changes in consumer confidence and preferences; (12) required accounting changes; (13) terrorist acts and other acts of war; and (14) other factors over which the Company has little or no control. See the Company’s Annual Report on Form 10-K/A and Annual Report to Shareholders for the year ended December 31, 2005 and other public filings with the Securities and Exchange Commission for a further discussion of these and other risks and uncertainties applicable to Pulte’s business. Pulte undertakes no duty to update any forward-looking statement whether as a result of new information, future events or changes in Pulte's expectations.

3

Challenging Homebuilding Environment Continues

• Navigating Through a Challenging Environment– Facts and figures

• Pulte Maintains its Core Strategy– Short-term: Keep a balanced approach

– Slowing the business

– Financial discipline, segmenting the business, and operational excellence

• Long-Term drivers remain positive

4

ChallengingHomebuilding

Environment Continues

5

Market Conditions 2004 - 2005

•Characteristics of the U.S. housing market in 2004 and 2005– Exceptional buyer demand– Limited inventory of new and existing homes– Rapid price appreciation in many major markets– Cancellation rates at historical lows– High levels of investor demand for real estate

6

Market Conditions Changed Rapidly in 2006

•In March 2006, buyer demand began to pull back; in many markets, significantly– Home inventories (new and existing) increased sharply– Real estate investors stopped buying and began selling – Cancellation rates accelerated– Markets with rapid price appreciation in ’04 and ’05

were hit hardest – Incentives and price concessions escalated

•Change occurred while the economy is strong, job growth was positive and interest rates were moderate

7

Pullback in Buyer Demand

New Home Sales (Units 000)

0

200

400

600

800

1,000

1,200

1,400

Dec

'03

Jun

'04

Dec

'04

Jun

'05

Dec

'05

Jun

'06

Dec

'06

• Low buyer confidence

• Affordability stretched in key markets

• Demand became supply as “investor” buyers became sellers

• Selling incentives offered to buyers increased

• A meaningful decline in gross margins were realized

Source: U.S. Census Bureau SAAR Data

8

Supply of New Homes Remains High

0

100,000

200,000

300,000

400,000

500,000

600,000

Dec'03

Mar'04

Jun'04

Sep'04

Dec'04

Mar'05

Jun'05

Sep'05

Dec'05

Mar'06

Jun'06

Sept'06

Dec'06

Hom

es fo

r Sal

e

0

1

2

3

4

5

6

7

Mon

ths

Supp

ly

New Homes For SaleMonths Supply

New Homes For Sale

Source: U.S. Census Bureau SAAR Data

9

Pulte Homes Cancellation Rate

0%

5%

10%

15%

20%

25%

30%

35%

40%

Q1 Q2 Q3 Q4

2004 2005 2006

Historical “can” rate

Cancellation Rates Still Higher Than Historical Periods

10

Pulte Maintains ItsCore Strategy

11

Short-term Tactics: Land

• Over $6 billion of new land investment planned for 2006 thru 2008 has been cut

• Lots under control at year-end reduced 36% from 3rd quarter 2006 level

Capital allocation focused on development of “owned” lot positions, and lot takedowns related to ongoing projects

Lots Under Control

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

'03 '04 '05 '06

Owned Approved Pending

12

Short-term Tactics – Land & Other (cont’d)

• Continue to review / renegotiate deals currently under option– Renegotiate if possible; walk away if not

• Slowed pace of new home production– Spec units under production reduced by 44% at year-end

from its 2nd quarter 2006 peak; goal is to start future specs on a very limited basis

– Cancellations could potentially result in new specs, but overall number of homes under production will continue to trend down

• Engaged in active discussions with suppliers and contractors regarding pricing

• Meaningful workforce reductions in 2006 (approx 25%)• Focus on running a balanced business to help deliver the

best short- and long-term results

13

Strategy: Maintain Financial Discipline

• Strong financial position• Long-standing strategy

of 40% debt-to-cap or lower

• Increased cancellation rates and rapid slowdown in sales resulted in higher house inventory and working capital– Working down spec-

inventory position will free-up additional capital

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2002 2003 2004 2005 2006

Debt to Capitalization

14

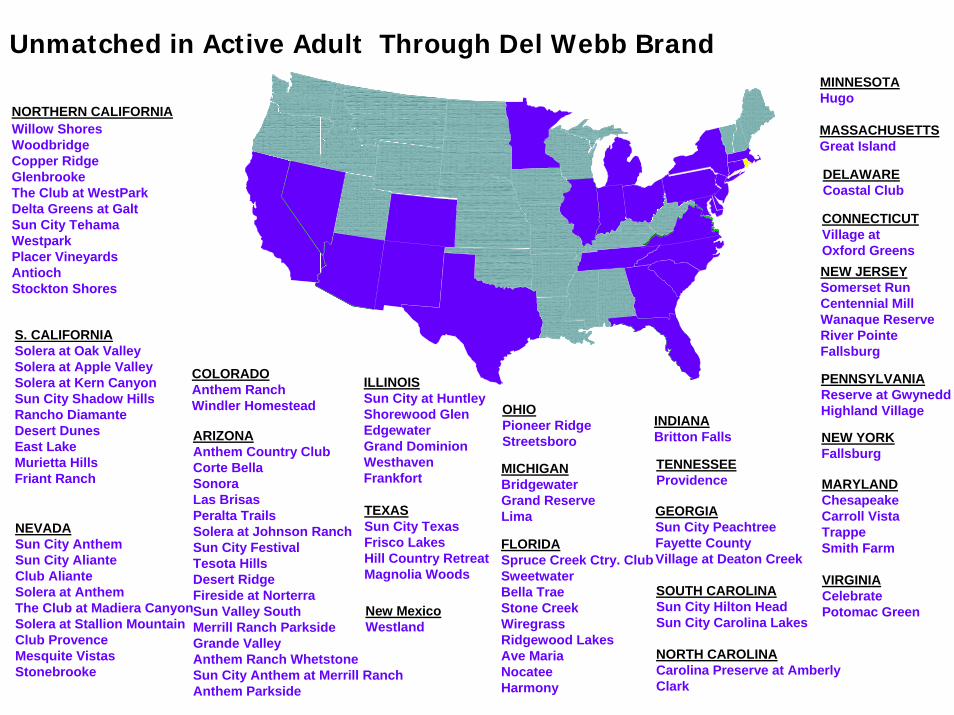

Pulte HomesDel Webb

DiVosta

Strategy: Segmenting Our Business

2006 Closings By Buyer Profile

1st Time Buyer 17%

1st Move Up Buyer 24%

2nd Move Up Buyer 15%

Active Adult 44%

FLORIDASpruce Creek Ctry. ClubSweetwaterBella TraeStone CreekWiregrassRidgewood LakesAve MariaNocateeHarmony

NEVADASun City AnthemSun City AlianteClub AlianteSolera at AnthemThe Club at Madiera CanyonSolera at Stallion MountainClub ProvenceMesquite VistasStonebrooke

ILLINOISSun City at HuntleyShorewood GlenEdgewaterGrand DominionWesthavenFrankfort

ARIZONAAnthem Country ClubCorte BellaSonoraLas BrisasPeralta Trails Solera at Johnson RanchSun City FestivalTesota HillsDesert RidgeFireside at NorterraSun Valley SouthMerrill Ranch ParksideGrande ValleyAnthem Ranch WhetstoneSun City Anthem at Merrill RanchAnthem Parkside

SOUTH CAROLINASun City Hilton HeadSun City Carolina Lakes

MASSACHUSETTSGreat Island

MARYLANDChesapeakeCarroll VistaTrappeSmith Farm

NEW JERSEYSomerset RunCentennial Mill Wanaque ReserveRiver PointeFallsburg

PENNSYLVANIAReserve at GwyneddHighland Village

DELAWARECoastal Club

TEXASSun City TexasFrisco LakesHill Country RetreatMagnolia Woods VIRGINIA

CelebratePotomac Green

MICHIGANBridgewaterGrand ReserveLima

NORTH CAROLINACarolina Preserve at AmberlyClark

OHIOPioneer RidgeStreetsboro

GEORGIASun City PeachtreeFayette CountyVillage at Deaton Creek

COLORADOAnthem RanchWindler Homestead

S. CALIFORNIASolera at Oak ValleySolera at Apple ValleySolera at Kern CanyonSun City Shadow HillsRancho DiamanteDesert DunesEast LakeMurietta HillsFriant Ranch

NORTHERN CALIFORNIAWillow ShoresWoodbridgeCopper RidgeGlenbrookeThe Club at WestParkDelta Greens at GaltSun City TehamaWestparkPlacer VineyardsAntiochStockton Shores

INDIANABritton Falls

New MexicoWestland

MINNESOTAHugo

NEW YORKFallsburg

TENNESSEEProvidence

CONNECTICUTVillage at Oxford Greens

Unmatched in Active Adult Through Del Webb Brand

16

Strategy: Operational Excellence

•Short-term cost reduction efforts– Some reductions realized from supplier base

•Long-term construction efficiency; reduce labor and material costs – Simplify design, engineering, specification and build

processes• Initiative to standardize specifications to drive lower costs and/or

increased customer value

– Better coordination of material purchases regionally and nationally

– Better supply chain management

– Vertical integration where it makes sense (Pulte Building Systems, DiVosta)

17

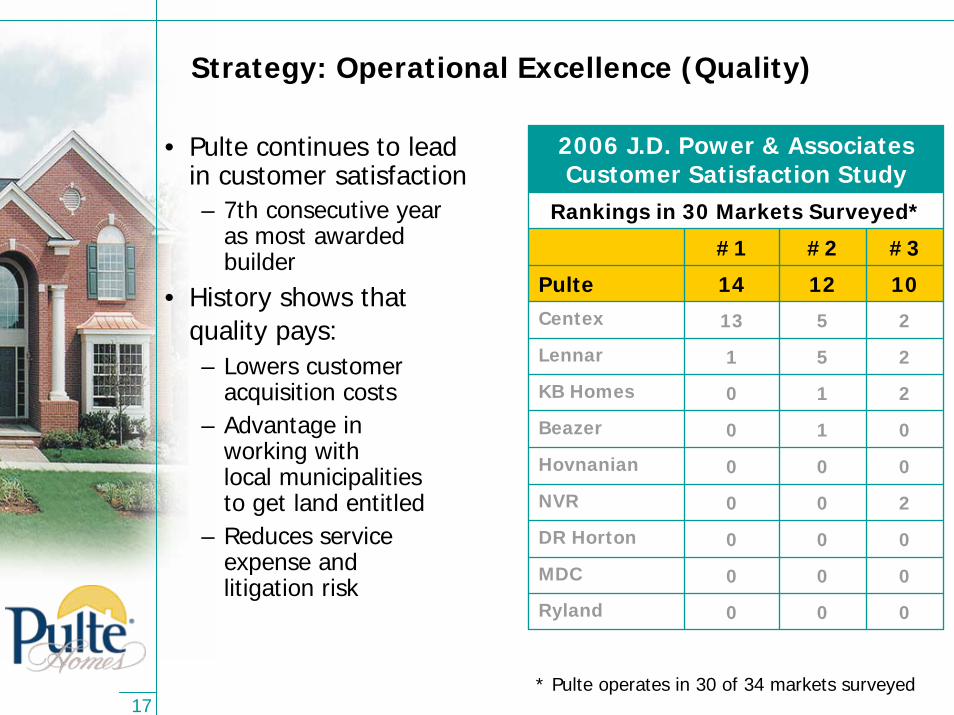

2006 J.D. Power & Associates Customer Satisfaction Study

Rankings in 30 Markets Surveyed*

#1 #2 #3

Pulte 14 12 10Centex 13 5 2

Lennar 1 5 2

KB Homes 0 1 2

Beazer 0 1 0

Hovnanian 0 0 0

NVR 0 0 2

DR Horton 0 0 0

MDC 0 0 0

Ryland 0 0 0

Strategy: Operational Excellence (Quality)

• Pulte continues to lead in customer satisfaction – 7th consecutive year

as most awarded builder

• History shows that quality pays:– Lowers customer

acquisition costs– Advantage in

working with local municipalities to get land entitled

– Reduces service expense andlitigation risk

* Pulte operates in 30 of 34 markets surveyed

18

Long-term Business Drivers Remain Positive

19

Macro Factors Remain Favorable

U.S. Population Estimates(millions)

0

50

100

150

200

250

300

350

400

450

'00 '05 '10 '15 '20 '25 '30 '40

• Recent data suggest U.S. population passed 300 million people in 2006

• Rate of growth accelerating, with population expected to top 400 million by 2040

20

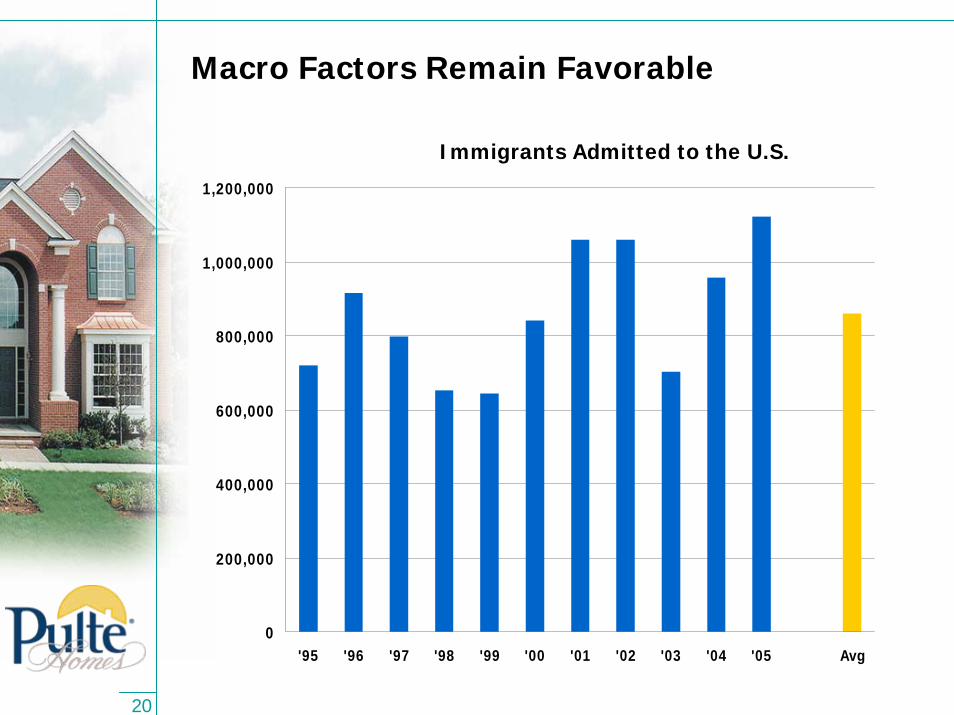

Macro Factors Remain Favorable

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 Avg

Immigrants Admitted to the U.S.

21

Macro Factors Remain Favorable

• According to the Joint Center for Housing Studies:– total household growth

in the next decade could surpass the prior 10 years by 2 million households.

– Immigration will be a key driver of the increase

Household Growth (millions)

0

2

4

6

8

10

12

14

16

1995 to 2005 2005 to 2015

Source: Joint Center for Housing Studies 2006

Entitlement 2006 The Future Will Be Tougher

More competitive 18-24 months

Limited availability 36 months or moreMore competitive 24-36 months

Nothing is easyEasier 6-12 monthsEasier 12-18 monthsMore competitive 18-24 months

Limited availability 36 months or moreMore competitive 24-36 months

Estimated Time to Entitle Land

Entitled Land Remains in Short Supply

Based on Company estimates

23

Competitive Advantages remain withBig Builders

• Better able to control land resources

• Better management of contractor resources

• Access to lower cost capital– Availability of capital

• Higher volume capability long-term makes simplification a real advantage

24

Summary

• Cyclical downturn continues– Buyers moved to the sideline, as supply increased– Too early to say a bottom has been found– Need sustained signs of:

• Home inventory levels stabilizing/contracting• Cancellation rates retreating toward historical levels

• Pulte adjusted short-term tactics in 2006– Shortened land pipeline– Lowered house production / spec volumes– Scaled back overheads appropriately

• Long-term drivers remain supportive of future demand