PRIME ACADEMY 31st SESSION MODEL EXAM - IPCC – ACCOUNTING QUESTION PAPER ACTG No. of Pages: 5 Total Marks: 100 No of Questions: 6 Time Allowed: 3 Hrs All are compulsory 1. (i) Shiv Ram Ltd.issued 1,500 ,16%debentures of Rs.100 each at a discount of 5%.on Jan 1st ,2009 repayable by equal drawings in four years. Show discount on issue of debentures account over the period. (ii) Mr.X and Mr.Y are partners sharing profits in the ratio of 5:3 with capital of Rs.2,50,000 and RS.2,00,000 respectively .Mr.Z was admitted on the terms that he would payRs.50,000 as capital and Rs.16,000 as goodwill for 1/5 th share of profits. Find the balance of capital accounts after admission of Mr.Z (iii) List the items of inflows from financing activity. (iv) Mention the two categories of investments defined by AS-13 and also state their valuation principles. (v) What is covered as inventory by AS-2. (vi) What is contract revenue as defined by AS-7? (vii) During the current year 2009-2010,X limited made the following expenditure relating to plant building: Routine Repairs Rs.1,00,000 Repairing Rs.4,00,000 Partial replacement of roof tiles Rs. 50,000 Substantial improvements to the electrical wiring system which will increase efficiency Rs.10,00,000. What is the amount to be capitalized. (viii) Suppose salaries paid during 2009 was Rs.23,000.Find out the amount to be debited to the profit and loss account if Salaries unpaid on 31 st Dec 2008 was Rs.1,400 Salaries prepaid on 31 st Dec.was Rs , 400 Salaries unpaid on Dec 2008 was RS.1,800 And Salaries prepaid on Dec.2009 was RS. 600. (ix) Mr.Ganesh purchased a truck on hire purchase system .As per the terms he is required to pay Rs.70,000 down ,Rs.53,000 at the end of first year ,Rs.49,000 at the end of second year and Rs.55,000 at the end of the third year. Interest is charges at 10% p.a..Calculate the total cash price of the truck. (x) What is purchase consideration as defined by AS-14. (2 x10 = 20 Marks) PRIME / ME31 / IPCC 1

Transcript

PRIME ACADEMY 31st SESSION MODEL EXAM - IPCC – ACCOUNTING

QUESTION PAPER

ACTG No. of Pages: 5 Total Marks: 100 No of Questions: 6 Time Allowed: 3 Hrs

All are compulsory

1.

(i) Shiv Ram Ltd.issued 1,500 ,16%debentures of Rs.100 each at a discount of 5%.on Jan 1st ,2009 repayable by equal drawings in four years. Show discount on issue of debentures account over the period.

(ii) Mr.X and Mr.Y are partners sharing profits in the ratio of 5:3 with capital of Rs.2,50,000 and RS.2,00,000 respectively .Mr.Z was admitted on the terms that he would payRs.50,000 as capital and Rs.16,000 as goodwill for 1/5th share of profits. Find the balance of capital accounts after admission of Mr.Z

(iii) List the items of inflows from financing activity. (iv) Mention the two categories of investments defined by AS-13 and also state their valuation

principles. (v) What is covered as inventory by AS-2. (vi) What is contract revenue as defined by AS-7? (vii) During the current year 2009-2010,X limited made the following expenditure relating to plant

building: Routine Repairs Rs.1,00,000 Repairing Rs.4,00,000 Partial replacement of roof tiles Rs. 50,000 Substantial improvements to the electrical wiring system which will increase efficiency

Rs.10,00,000. What is the amount to be capitalized.

(viii) Suppose salaries paid during 2009 was Rs.23,000.Find out the amount to be debited to the profit and loss account if

Salaries unpaid on 31st Dec 2008 was Rs.1,400 Salaries prepaid on 31st Dec.was Rs , 400 Salaries unpaid on Dec 2008 was RS.1,800 And Salaries prepaid on Dec.2009 was RS. 600.

(ix) Mr.Ganesh purchased a truck on hire purchase system .As per the terms he is required to pay Rs.70,000 down ,Rs.53,000 at the end of first year ,Rs.49,000 at the end of second year and Rs.55,000 at the end of the third year. Interest is charges at 10% p.a..Calculate the total cash price of the truck.

(x) What is purchase consideration as defined by AS-14. (2 x10 = 20 Marks)

PRIME / ME31 / IPCC 1

2. Zed Ltd. presents to you the following balance sheet and income statement:

Balance Sheet

As on 31st March 2009 As on 31st March 2010 Rs Rs Equity Share Capital 10,00,000 10,00,000 Retained Earnings 8,30,000 9,46,000 12% Debentures 6,00,000 5,00,000 Trade Creditors 1,02,500 1,21,700 Outstanding Expenses 21,800 27,400 25,54,300 25,95,100Fixed Asset at cost 24,00,000 26,00,000 Provision for Depreciation (8,00,000) (9,80,000) Investments 2,50,000 1,00,000 Inventories 4,13,300 5,07,100 Trade Debtors 1,60,000 1,80,000 Provision for bad debts (8,000) (9,000) Cash in hand and at Bank 1,34,200 1,93,400 Underwriting commission 4,800 3,600 25,54,300 25,95,100

Profit and loss Account for the year ended 31st March, 2010

Rs Sales 36,40,200 Cost of Goods sold (18,60,000) Compensation received in Lawsuit 55,000 Interest received on Investments 21,000 Profit on sale of investments 7,500 Sundry operating expenses (7,83,500) Interest on Debentures (66,000) Provision for Bad Debts (1,000) Provision for Depreciation (1,80,000) Underwriting Commission, Written off (1,200) Net profit before tax 8,32,000 Tax for the year paid 4,16,000 Net Profit after Tax 4,16,000 Prepare Zed Ltd’s cash flow statement for the year ended 31st March, 2010 using (1)the direct method and (2)the indirect method. Zed Ltd. Informs you that debentures have been redeemed at par.

(16 Marks)

PRIME / ME31 / IPCC 2

3. The following are the balance sheet of Strong Limited and Small Limited as at 31st December, 2009

Liabilities Strong Ltd Rs

Small Ltd Rs Assets Strong Ltd

Rs Small Ltd

Rs Share Capital Fixed Assets at cost

less depreciation 1,40,000 75,000

Equity sh. Of the face value of Rs 10 each

1,50,000 1,20,000 Current Assets

Reserves 95,000 10,000 Stock 42,000 47,000 Secured loans Trade Debtors 30,000 50,000 10% Debentures 20,000 Balance at Bank 80,000 10,000 Current Liabilities Trade Creditors 47,000 32,000 2,92,000 1,82,000 2,92,000 1,82,000

Strong Limited agreed to absorb Small Limited as on 31st December 2009 on the following terms:

(1) Strong Limited agreed to repay 10% Debentures of Small Limited (2) Strong Limited to revalue its Fixed Assets at Rs 1,95,000 to be incorporated in the books (3) Shares of both companies to be valued on net Assets Basis after considering Rs 50,000 towards

value of goodwill of Small Limited. (4) The cost of absorption of Rs 3,000 are met by Strong Limited.

You are required to : (a)Calculate the ratio of exchange of shares (b)Give Journal Entries in the books of Strong Limited and, (c)Construct the Bank Account to arrive at the balance on absorption.

(16 marks)

4. (a) From the following information, you are required to work out the claim under the Loss of Profits Insurance Policy.

1) Cover-Gross Profit-Rs 75,000 2) Indemnity period-6 months 3) Damage-due to fire accident on 28th December-Accounting year ends on 31st December. 4) Net profit plus all standing charges in the prior accounting year Rs 1,12,500. 5) Standing charges uninsured Rs 18,750. 6) Turnover of the last accounting year was Rs 3,75,000.The rate of gross profit being 25%. 7) The annual turnover ,namely the turnover for 12 months immediately preceding the fire

Rs 3,90,000. 8) As a consequence of fire there was a reduction in certain insured standing charges at the rate of

Rs 18,750 per annum. 9) The standard turnover Rs 1,95,000 10) Increased cost of working during the period of indemnity was Rs 15,000 11) Turnover during the period of indemnity was Rs 75,000 and out of this turnover of Rs 60,000 was

maintained due to increased cost of working. (10 Marks)

PRIME / ME31 / IPCC 3

(b) Prepare total accounts from the following particulars in the three ledgers:

Rs Jan 1, 2009 Balance on bought ledger(Dr) 1,740

Balance on bought ledger(Cr) 23,880 Balance on sales ledger(Dr) 29,240 Balance on sales ledger(Cr) 480

5. (a) On 1st April, 2009 Anand held 20,000 fully paid equity shares of Rs 10 each in P Ltd. appearing in Anand’s books at Rs 3,05,500. On 1stjune, 2009 he acquired 5,000 more equity shares in the company at an all inclusive cost of Rs 17 per share. On 30thjune, 2009 P Ltd. announced a bonus issue at the rate of one fully paid equity share of Rs 10 for every five shares held. Anand received the bonus shares on 4thAugust, 2009.

P Ltd. Also made the right issue the terms being as follows:

(1) The issue would entitle the shareholders to subscribe to one equity shares of Rs 10 in the company for every three share held as on 9th august, 2009;the new shares would be issued as premium of Rs 5 per share, the whole amount being payable by 30th September, 2009.

(2) The share holders would be entitled to renounce their entitlement either wholly or in part to outsiders. Anand exercised his option under the issue for 50%of his entitlements and sold the balance of his rights to another person @ Rs 1.50 per share. P Ltd. Declared a dividend at the rate of 20% for the year ended 31st March , 2009. Anand received the dividend on 3rd October 2009. On 1st December 2009 Anand sold 15,000 equity shares and received a net sum of Rs 2,62,500. Prepare Investment Account in Anand’s ledger for the year ended 31st March, 2010.Usage cost method.

(8 Marks)

PRIME / ME31 / IPCC 4

(b) A, B and C are partners sharing profits and losses in the ratio of 2 : 3 : 5. On 31st March 2010 their Balance sheet was as follows:

Balance Sheet

Liabilities Rs Assets Rs Capitals: Cash 22,000 A 40,000 Bills receivable 20,000 B 42,000 Furniture 28,000 C 50,000 1,32,000 Stock 44,000 Creditors 68,000 Debtors 46,000 Bills Payable 32,000 Investments 32,000 Profit and Loss A/c 14,000 Machinery 34,000 Goodwill 20,000 2,46,000 2,46,000 They admit D into partnership on the following terms:

1) Furniture, investments and machinery to be deprecated by 15%. 2) Stock is revalued at Rs 48,000. 3) Goodwill to be valued at Rs 26,000. 4) Outstanding rent amounted to Rs1,800. 5) Prepaid salaries Rs 800. 6) D to bring Rs 32,000 towards capital for 1/6 share and other partners to re-adjust their capital

accounts on the basis of their profit sharing ratio. 7) Adjustments of capitals to be made by cash.

Prepare Revaluation Account, Partner’s Capital Accounts, Cash Accounts and Balance Sheet of the new firm.

(8 Marks)

6. Answer the following:

a) What are the advantages of using an ERP. b) Explain the procedures to be adopted for charging depreciation in cases where additions or

extensions are made to a capital asset. c) Show The Profit &Loss extract in the books of a contractor in respect of the following data:

Rs.000’s

Contract price (fixed) 600 Cost incurred to date 390 Estimated cost to complete 260

d) What are the major considerations that should be kept in mind in determination and selection of accounting policies. (4 x 4=16 Marks)

PRIME / ME31 / IPCC 5

PRIME ACADEMY 31st SESSION MODEL EXAM - IPCC – ACCOUNTING

SUGGESTED ANSWERS

1.

(i) Total amount of discount on issue of debentures = Rs (1,50,000 / 100) * 5 = Rs 7,500

The total discount of Rs 7,500 is to be written off in proportion to the debentures outstanding at the beginning of each year. This outstanding balance will be as follows:

(iii) Financing activities are activities that result in changes in the size and composition of the owners’ capital (including preferences share capital in the case of company) and borrowings of the enterprise. Examples include issues of shares / Debentures, redemption of Debentures / preferences shares, Payment of dividends and payment of interest (other than interests paid by financial institutions).

(iv) Current investment-valued at cost or fair value which ever is lower.

Long term investments-valued at cost

(v) Inventories as Assets held

a. For sale in the ordinary course of business or

b. In the process of production for such sale or

c. In the form of materials or supplies to be consumed in the production process or in rendering of services.

PRIME / ME31 / IPCC 6

(vi) Contract revenue should comprise:

a. The initial amount of revenue agreed in the contract; and

b. Variations in contract work, claims and incentive payments to the extent that it is probable that they will result in revenue and they are capable of being reliably measured.

(vii) Expenditure that increases the future benefits from the existing asset beyond its previously assessed standard of performance is included in the gross book value, e. g., an increase in capacity. Hence in the given case repairs amounting Rs. 5Lakhs and partial replacement of roof tiles should be charged to profit and loss statement. Rs. 10Lakhs incurred for substantial improvement to be electrical writing system which will increase efficiency should be capitalized.

(viii) Rs.23,200 is to be transferred to profit and loss account

(ix) Ratio of interest and amount due = Rate of interest / 100 + Rate of interest = 10 / 110 = 1/11

Calculation of interest and cash price

No. of installments

Amount due at the time of installment

Interest Cast price Rs.

3rd 55,000 1/11 of Rs 55,000 = Rs 5,000 50,000 2nd *99,000 1/11 of Rs 99,000 = Rs 9,000 90,000 1st **1,43,000 1/11 of Rs 1,43,000 = Rs 13,000 1,30,000

*Rs50,000 + 2nd instalment of Rs49,000 = Rs 99,000

**Rs90,000 + 1st instalment of Rs 53,000 = Rs 1,43,000.

(x) The term purchase consideration is the aggregate of the shares and other securities issued and the payment made in the form of cash or other assets by the transferee company to the shareholders of the transferor company.

2. Direct Method:

Zed Ltd.

Cash Flow Statement for the year ended 31st March, 2010

Rs Rs Cash Flows from Operating Activities Cash receipts from customers 36,20,200 Cash paid to suppliers and employees (27,12,500) Cash inflow from operations 9,07,700 Income Tax paid (4,16,000) 4,91,700 Cash flow from extraordinary item: Compensation received in law suit 55,000 Net cash from operating activities 5,46,700

PRIME / ME31 / IPCC 7

Cash Flow from investing Activities Purchase of fixed assets (2,00,000) Sale proceeds of investments 1,57,500 Interest received on investments* 21,000 Net cash used in investing activities (21,500) Cash flows from Financing Activities Redemption of debentures at par (1,00,000) Interest on debentures paid* (66,000) Dividends paid (3,00,000) Net cash used in financing activities (4,66,000) Net increase in cash and cash equivalents 59,200 Cash and cash equivalents as on 31st March, 2009 (Opening Balance) 1,34,200 Cash and cash equivalents as on 31st March, 2010 (Closing Balance) 1,93,400

Working Notes

(1)

Rs Calculation of cash receipts from customers: Sales 36,40,200 Add: Trade debtors as on 31st march, 2009 1,60,000 38,00,200 Less: Trade debtors as on 31st march, 2010 1,80,000 36,20,200

(2)Calculation of cash paid to suppliers and employees: Cost of goods sold 18,60,000 Add: sundry operating expenses 7,83,500 26,43,500 Add: Inventory as on 31st March, 2010 5,07,100 Trade creditors as on 31st March 2009 1,02,500 Outstanding Expenses as on 31st March 2009 21,800 32,74,900 Less: Inventory as on 31st March 2009 4,13,300 Trade creditors as on 31st March 2010 1,12,700 Outstanding Expenses as on 31st March 2010 27,400 5,62,400 27,12,500 (3) Fixed Assets purchased during the year: Fixed Assets at cost on 31st March 2010 26,00,000 Less: Fixed Assets at cost on 31st March 2009 24,00,000 2,00,000 (4)Sale proceeds of Investments Cost of investments sold(Rs 2,50,000 – Rs 1,00,000) 1,50,000 Add: Profit on sale of investment 7,500

PRIME / ME31 / IPCC 8

1,57,500 (5)Calculation of dividends paid: Retained earnings as on 31st March 2009 8,30,000 Add: Net profit for the year ended 31st March 2010 4,16,000 12,46,000 Less: Retained earnings as on 31st March 2010 9,46,000 Dividends paid 3,00,000 (2)INDIRECT METHOD Rs Rs Cash flow from operating activities Net profit before income tax and extra-ordinary item 7,77,000 Adjustments for: Depreciation 1,80,000 Provision for bad debts 1,000 Under writing commission amortised 1,200 Profit on sale of investments (7,500) Income from investments (21,000) Interest on debentures 66,000 Operating profit before working capital changes 9,96,700 Adjustments for: Increase in inventory (93,800) Increase in trade debtors (20,000) Increase in trade creditors 19,200 Increase in outstanding expenses 5,600 Cash inflow from operations 9,07,700 Income tax paid (4,16,000) 4,91,700 Cash flow from extra-ordinary item: Compensation received in lawsuit 55,000 Net cash from operating activities 5,46,700 Cash flows from investing activities Purchase of fixed assets (2,00,000) Sale proceeds of investments 1,57,500 Interest received on investments 21,000 Net cash used in investing activities (21,500) Cash flows from financing activities Redemption of debentures at par (1,00,000) Interest on debentures paid (66,000) Dividends paid (3,00,000) Net cash used if financing activities (4,66,000) Net increase in cash and cash equivalents 59,200 cash and cash equivalents as on 31st March 2009(opening balance) 1,34,200 cash and cash equivalents as on 31st March 2010(closing balance) 1,93,400

PRIME / ME31 / IPCC 9

Working Notes (1) Net profit before income tax and extra-ordinary item: Rs Net profit before income tax 8,32,000 Less: Compensation received in lawsuit 55,000 7,77,000

3. Computation of ratio of exchange of shares

Strong Ltd Rs Small Ltd Rs (A)Assets: Fixed asset (at cost less depreciation) 1,95,000 75,000 Goodwill 50,000 Stock 42,000 47,000 Trade debtors 30,000 50,000 Bank Balance 80,000 10,000

A 3,47,000 2,32,000 Liabilities: 10% Debentures 20,000 Trade creditors 47,000 32,000 B

47,000 52,000

Net Worth(A – B) 3,00,000 1,80,000 Number of shares 15,000 12,000 Intrinsic value of share Rs 20 Rs 15

Number of shares to be issued by Strong Ltd to Small Ltd is equal to Rs 1,80,000 / Rs 20 = 9,000 shares.

Therefore exchange ratio = 9,000 / 12,000 = 3:4.

Date Particulars LF Dr. Rs Cr. Rs 2009 Fixed assets A/C 75,000 Dec31 Goodwill A/C 50,000 Stock A/C 47,000 Trade debtors A/C 50,000 Bank A/C 10,000 To 10% Debenture holders A/C (Note 1) 20,000 To trade creditors A/C 32,000 Liquidator of Small Ltd A/C 1,80,000 To Equity share capital A/C 90,000 (Being the different asset and liabilities taken over from small

Ltd as per the agreement dated…)

Liquidator of Small Ltd A/C 1,80,000 To Equity share capital 90,000 To Share premium A/C 90,000

PRIME / ME31 / IPCC 10

(Being purchase consideration discharged by issue of 9,000 Equity share of Rs10 each at a premium of Rs 10 per share)

Goodwill A/C 3,000 To bank A/C 3,000 (Being payment of cost of absorption)

Cash Account

Dr Cr Date Particulars Rs Date Particulars Rs 2009 To balance b/d 80,000 2009 By Goodwill A/C (cost of

absorption) 3,000

Dec31 To sundries- taken over from small Ltd

10,000 Dec31 By balance c/d 87,000

90,000 90,000 Working note: (1)it is assumed that strong Ltd will pay debenture holder on a subsequent date.

4.

a) Calculation of short sales:

Rs.

Standard turnover 1,95,000

Turnover during the indemnity period 75,000

Short sales 1,20,000

Calculation of Rate of gross profit

= Net profit + all standing charges – uninsured standing charges / Sales of last accounting year

=(Rs. 1,12,500 –Rs. 18,750) / Rs 3,75,000 * 100

=25%

Amount of claim:

Rs

Loss of profit on short sales of Rs 1,20,000 @ 25% 30,000 Add: Increased cost of working: Actual amount of increased cost 15,000 Gross profit @ 25% on turnover for 12 months Immediately preceding the date of fire (3,90,000 * 25%)

97,500

Gross profit as above plus uninsured standing charges(97,500 + 18,750) 1,16,250

PRIME / ME31 / IPCC 11

Claim for increased cost of working(15,000 * 97,500/1,16,250) 12,580 (Gross profit @ 25% on additional sales of Rs 60,000 due to increased Cost 60,000 * 25% =15000 is more than Rs 12,580, so claim admissible is Rs 12,580)

42,580 Less: Saving in standing charges for ½ year(18,750 * ½) 9,375 33,205

Application of average clause:

Uninsured / Gross profit on preceding 12 month sales * Amount of claim

= Rs 75,000 / 25% of 3,90,000 * 33,205

=Rs 75,000 / Rs 97,500 * 33,205

=Rs 25,542.

Therefore claim for loss of profit to be lodged is Rs 25,542.

b) General Ledger

Debtors Ledger Adjustment A/C

Date Particulars Rs Date Particulars Rs 2009 2009 Jan 1 To balance b/d 29,240 Jan 1 By balance b/d 480 Jan 31 To General Ledger Adjustment

Date Particulars Rs Date Particulars Rs 2009 2009 Jan 1 To balance b/d 1,740 Jan 1 By balance b/d 23,880 Jan 31 To General Ledger Adjustment A/C Jan 31 By General Ledger

Date Particulars Rs Date Particulars Rs 2009 2009 Jan 1 To balance b/d 23,880 Jan 1 By balance b/d 1,740 Jan 31 To Creditors Ledger

Adjustment A/C Jan 31 By Creditors Ledger

Adjustment A/C

Purchases 1,32,260 Purchase Returns 5,120 Cash 1,16,860 Discount 3,320 Bills Payable 4,500 To Balance c/d 1,540 To Balance c/d (Balancing

figure) 26,240

1,57,780 1,57,780

PRIME / ME31 / IPCC 13

5.

a)

Investment Account Equity Shares in P. Ltd.

Dr Cr Date Particulars No. Income Principal

Account Date Particulars No. Income Principal

Account 2009 Rs Rs 2009 Rs Rs Apr 1 To Balance

b/fd 20,000 3,05,500 ? By Bank-

Sale of rights

7,500

June 1 To Bank 5,000 85,000 Aug 4 To Bonus

Shares 5,000 --- Oct 3 By Bank-

Dividend for 1996-97

40,000 10,000

Sept 30 To Bank- Subscription to 50% of rights shares

5,000 75,000 Dec 1

By Bank- Sale

15,000

2,62,500

Dec 1 To Profit & Loss A/C- Profit on sale

70,500

2010 Mar 31

To Profit & Loss Account

40,000 2010 Mar 31

By Balance c/d

20,000

2,56,000

35,000 40,000 5,36,000 35,000

40,000 5,36,000

2010 Apr 1

Balance b/d 20,000 2,56,000

Working Notes:

(1) Calculation of profit on sale of 15,000 shares:

Amount paid for 35,000 shares: Rs Rs (305500+85000+75000) Less: Amount received on sale of rights Dividend for 2008-09 on shares purchased on 1st June 2009

7,500

10,000

4,65,500

17,500 Cost of 35,000 shares 4,48,000 Sale proceeds of 15,000 shares 2,62,500 Less: Cost of 15,000 shares= Rs 4,48,000 * 15,000 / 35,000 1,92,000 Profit 70,500

PRIME / ME31 / IPCC 14

(2) Calculation of value of closing stock of 20,000 shares: Cost of 35,000 shares as calculated in (1)above=Rs 4,48,000 Hence cost of 2,000 shares= Rs 4,48,000 * 20,000/35,000=Rs 2,56,000 Cost per share = Rs 2,56,000 / 20,000 = Rs 12,809. Assuming that the market price of the shares is higher than the cost closing stock will be shown at cost price I e., Rs 2,56,000.

b) Revaluation Account

Particulars Amount

Rs. Particulars Amount

Rs. To Outstanding Rent 1,800 By Stock 4,000 To Furniture 4,200 By Prepaid Salaries 800 To investments 4,800 By Loss transferred to: To Machinery 5,100 A’s Capital A/C 2,220 B’s Capital A/C 3,330 C’s Capital A/C 5,550 11,100 15,900 15,900

Partners’ Capital Account (A, B, C)

Particulars A Rs. B Rs. C Rs. Particulars A Rs. B Rs. C Rs. To Revaluation A/C 2,220 3,330 5,550 By balance b/d 40,000 42,000 50,000 To cash A/C 9,780 - - By P & L A/c

(Profit) 2,800 4,200 7,000

To Balance c/d 32,000 48,000 80,000 By Goodwill A/C 1,200 1,800 3,000 By cash A/C - 3,330 25,550 44,000 51,330 85,550 44,000 51,330 85,550

D’s Capital Account

Particulars Amount Rs.

Particulars Amount Rs.

To Balance c/d 32,000 By Cash A/C 32,000 32,000 32,000

Cash Account Particulars Amount

Rs. Particulars Amount

Rs. To Balance b/d 22,000 By A’s Capital A/C 9,780 To B’s Capital A/C 3,330 By balance c/d 73,100 To C’s Capital A/C 25,550 To D’s Capital A/C 32,000 82,880 82,880

PRIME / ME31 / IPCC 15

Balance sheet of the new firm as on 31st March 2010 Liabilities Amount

Rs. Assets Amount

Rs. Creditors 68,000 Cash 73,100 Bills Payable 32,000 Bills Receivable 20,000 Outstanding Rent 1,800 Debtors 46,000 Capitals: Stock 48,000 A 32,000 Prepaid Salaries 800 B 48,000 Investments 27,200 C 80,000 Furniture 23,800 D 32,000 1,92,000 Machinery 28,900 Goodwill 26,000 2,93,800 2,93,800 Working Notes: (1)Calculation of new profit sharing ratio Old ratio= 2:3:5 D’s share= 1/6 Remaining share= 1 – 1/6 = 5/6 New profit sharing ratio of A= 5/6 * 2/10 = 2/12 B= 5/6 * 3/10 = 3/12 C= 5/6 * 5/10 = 5/12 D= 1/6 or 2/12 New Profit sharing Ratio = 2:3:5:2

(2)Increase in the value of Goodwill by Rs 6,000 is divided among the old partners in their old ratios

(3) The full value of Goodwill is shown in the balance sheet (4) On the basis of D’s capital contribution for 1/6th share the total capital of the reconstituted firm

should be Rs 32,000 * 6 = Rs 1,92,000. This is divided among the partners in their new profit sharing ratio of 2:3:5:2.

A=1,92,000 * 2/12 = 32,000

B=1,92,000 * 3/12 = 48,000

C=1,92,000 * 5/12 = 80,000

D=1,92,000 * 2/12 = 32,000

6.

a) Advantages of using an ERP

The Advantages of using an ERP for maintaining accounts are as follows

PRIME / ME31 / IPCC 16

(1) Standardized process and procedures: An ERP is a generalized package which covers most of the common functionalities of any specific module.

(2) Standardized Reporting: Majority of the desired reports are available in an ERP package. These reports are Standardized across industry and are generally acceptable to the users,

(3) Duplication of data entry is avoided as it is an integrated package

(4) .Greater information is available through the package.

b) Additions or extensions

The procedures to be adopted for charging depreciation in cases where additions or extensions are made to a capital asset, are

Where extension or addition becomes an integral part of an existing asset

Where extension or addition results is an asset with (1)a separate identity and (2)can be used even after the original asset is disposed of

a)ascertain remaining amortised amount including incremental cost (say x)

a)determine the incremental amortized amount (say y)

b)Depreciate x over the remaining useful life b)determine useful life c)For, practical consideration apply identical rate of depreciation as applicable to original asset

c)Amortise y over useful life.

c)

Rs 000 A. Cost incurred to date 390 B. Estimate of cost to completion 260 C. Estimated total cost 650 D. Degree of completion A/C 60% E. Revenue Recognised (60% of 600) 360 Total foreseeable loss(650 – 600) 50 Less: Loss for current year(E – A) 30 Expected loss to be recognized immediately 20 Profit and Loss A/C

Rs Rs To construction cost 390 By contract price 360 To provision for loss 20 By Net Loss 50 410 410

d) An enterprise has therefore to exercise scruples care in selection and application of accounting principles and methods such a selection is guided by three major considerations.

(a) Prudence

Prudence is the inclusion of a degree of calculation in the exercise of judgements needed in making estimates required under conditions of uncertainity.

PRIME / ME31 / IPCC 17

By exercising prudence an enterprise does not recognized only when realised though not necessarily in cash. However all known losses are anticipated and provided.

(b) Substance over form

If information is to represent faithfully the transactions or events, it is essential that they are accounted for and presented in accordance with their substance and economic reality and not merely their legal form.

(C) Materiality

The relevance of information is affected by its materiality.Information is material if its misstatement i. e, omission of erroneous statement, could influence the economic decisions taken by the user based on such financial statements should disclose all material items i. e. knowledge of which might influence the decision of the user of financial statements.

Other qualitative characteristics of accounting information such as (1)relevance (2)neutrality (3) Completeness (4)reliability are equally critical to users in order that financial statements are meaningful in the selection and adoption of accounting policies these aspects should also be kept in view.

PRIME / ME31 / IPCC 18

PRIME / ME31 / IPCC 1

1

PRIME ACADEMY 31st SESSION MODEL EXAM - IPCC – LAW ETHICS AND COMMUNICATIONS

QUESTION PAPER

LWEN No. of Pages: 4 Total Marks: 100 No of Questions: 16 Time Allowed: 3 Hrs

All are compulsory

PART – I

1.

a) M agreed on Monday to sell his property to N by a written agreement which stated “that this offer to be left open until Saturday 10 a.m.” In the meantime on Wednesday, M enters into a contract to sell the property to O. N, who was sitting in the next room, hears about the deal between M and O. On Friday, N accepts the offer and delivers to M the letter of acceptance. Is N’s acceptance valid? Give reason.

(5 Marks)

b) State With reasons whether the following statements are correct or incorrect i. A person is deemed to have accepted the special terms / conditions in a contract, if they

are communicated to him in some reasonable manner. ii. A hires a carriage of B and agrees to pay Rs. 500 as hire charges. The carriage is unsafe,

though B is unaware of it. A is injured and claims compensation for injuries suffered by him. B is not liable to compensate.

(2 Marks)

c) Examine whether the following constitute a contract of “Bailment” under the provisions of the Indian Contract Act, 1872. C, D and E 1 mark each

i. A parks his car at a parking lot, locks it and keeps the keys with himself.

ii. Seizure of goods by Customs Authorities

(1 Mark)

d) “A” intending to deceive “B” falsely represents that five hundred maunds of indigo are made annually at A’s factory and thereby induced ‘B’ to buy the factory:

a. This agreement is valid b. This Contract is voidable at the option of ‘A’ c. This Contract is voidable at the option of ‘B’ d. This contract is void

(1 Mark)

PRIME / ME31 / IPCC 2

2

e) A draws a bill on B, who accepts it without consideration. He endorses the bill to C for valuable consideration. On due date when C presents the bill to B for payment, B contends absence of consideration. Decide the case.

(1 Mark)

2. a) A Company was incorporated on 6th October, 2003. The certificate of incorporation of the

Company was issued by the Registrar on 12thOctober, 2003. The Company on 10thOctober, 2003 entered into a contract which created its contractual liability. The Company denies from the said liability on the ground that the Company is not bound by the contract entered into prior to issuing certificate of incorporation. Decide whether the Company can be exempted from the said contractual liability.

(5 Marks) b) Though six out of seven signatures to the Memorandum of Association of a company were

forged, the company was registered and the Certificate of Incorporation issued. Can the registration of the company be challenged subsequently on the ground of forged signatures?

(5 Marks)

3. In an accounting year, a Company to which the Payment of Bonus Act, 1965 applies, suffered heavy losses. The Board of Directors of the said Company decided not to give Bonus to the employees. The employees of the Company move to the Court for relief. Decide whether the employees will get relief.

(5 Marks) 4. ‘A’ Signs as a maker the blank Stamp paper and gives it to ‘B’ and authorizes to fill it as a

note for Rs. 500, to secure an advance which ‘C’ is to make to ‘B’. ‘B’ fraudulently fills it as a note for Rs. 2,000 payable to ‘C’ who has in good faith advance Rs. 2,000. Decide whether ‘C’ is entitled to recover the amount, and if so, up to what extent?

(5 Marks) 5. Under the provisions of the payment of Gratuity Act, 1972 an employee in his nomination

distribute the amount of gratuity payable to him amongst more than one nominee. Is it permissible under the payment of Gratuity Act.? Explain.

(5 Marks)

6. An Executive Committee is to be constituted to assist the Central Board under the provisions of the Employees Provident Funds and Miscellaneous Provisions Act, 1952. State the composition of such Executive Committee.

(5 Marks) 7. The object clause of the Memorandum of RSP Private Ltd., Bangalore authorized to do

trading in fruits and vegetables. The Company, however, entered into a Partnership with Mr. A and traded in steel and incurred liabilities to Mr. A. The Company, subsequently, refused to admit the liability to A on the ground that the deal was ‘Ultra Vires’ the company. Examine the validity of the company’s refusal to admit the liability to A. Give reasons in support of your answer.

(5 Marks)

PRIME / ME31 / IPCC 3

3

8. DSC Ltd. holds 40% of the total equity shares in Goodluck Ltd. The Board of Directors of Goodluck Ltd. (incorporated on 1.1.2005) decided to raise the paid up Equity Share Capital by issuing further shares and also decided not to offer any shares to DSC Ltd. on the ground that it was already holding a high percentage of shares in Goodluck Ltd. Articles of Association of Goodluck Ltd. provides that the new shares be offered to the existing shareholders of the company. On 1.3. 2009 new shares were offered to all the shareholders excepting DSC Ltd. Examine the validity of decision of the Board of Directors of Goodluck Ltd.

(5 Marks) 9. M/s. Maxima Limited ows Mr. Suresh Rs. 1,000. On becoming this debt payable, the

Company offered Mr. Suresh 10 shares of Rs. 100/- each in full settlement of the debt. The said shares were fully paid and were allotted to Mr. Suresh. Examine the validity of allotment in the light of the provisions of the Companies Act, 1956.

(5 Marks)

10. M/s. Narmadha Ltd. issued a notice for holding of its Annual General Meeting on 7th November, 2009. Notice was posted to Members on 16th October, 2009. Some of the Members alleged that Company had not complied with the Act as regards period of Notice and as such Meeting was not validly called. Decide:

a) Whether the meeting has been validly called? b) If there is a shortfall in the number of days by which Notice falls short of Statutory

Requirement, state and explain by how many days Notice fall short of Statutory Requirement?

c) Can the shortfall, if any, be condoned? (5 Marks)

PART – II 11.

a) Explain the importance of ethical behaviour at the workplace. (5 Marks)

b) Explain the meaning of Ethical Dilemmas. (5 Marks)

12. What are the aspects to be considered in creating an ethical accounting

environment in the business house? (5 Marks)

13. State with reasons whether the following statements are correct or incorrect: a) Fairness and honesty are the pillars of success in the business. b) There is no difference between ethics and morals.

(5 Marks)

PART – III 14.

a) What are the merits and demerits of grape-vine form of Communication? (5 Marks)

PRIME / ME31 / IPCC 4

4

b) M/s. SQR Pvt. Limited wants to hold Annual General Meeting on 20th September, 2010 to discuss the matter only relating to ordinary business. Draft a Notice for the Annual General Meeting.

(5 Marks) 15. Prepare Chairman’s speech to be given at Annual General Meeting. For this purpose, take

some facts on notional basis. (5 Marks)

16. A Partnership firm was constituted by X, Y and Z. X, the partner of the firm expressed his desire to retire from the partnership firm by mutual consent. Draft a “Partnership Retirement Deed”.

(5 Marks)

PRIME / ME31 / IPCC 5

5

PRIME ACADEMY 31st SESSION MODEL EXAM - IPCC – LAW ETHICS AND COMMUNICATIONS

SUGGESTED ANSWERS

1.

a) (i) Acceptance is made before revocation of the offer by M and well (ii) The time specified by M in his letter of offer. (iii)Overhearing by N does not amount to a valid revocation by M. (iv) Hence N’s acceptance is valid. (v) The treatment would be difference if, before acceptance by N, M had formally

communicated his revocation to him.

b) (i) Correct (ii) Incorrect

c)

(i) No. Mere custody of goods does not mean possession. Leading case: Kaliaperumal pillai vs Visalakshmi (ii) Yes. The possession of goods is transferred to the Customs authorities. (Section 148 is applicable)

d) (c) e) B is liable to pay to C who is holder in due course.

2.

a) The Company came into existence on the date of incorporation stated on the certificate. The contract entered into by the Company before the issue of certificate of incorporation shall be binding up on the Company. The date of issue of certificate is immaterial. The Company cannot be exempted from the contractual liability in this case.

b) As per Section 35, Certificate of Incorporation is a conclusive evidence. So, in the given

case, Registration cannot be challenged. 3.

i. Minimum Bonus shall be paid to the employees irrespective of losses of the Establishment.

ii. Where the Bonus liability is negligible as compared to the losses suffered, then the Company should not be relieved of its liability to pay minimum Bonus u/s 10.

iii. It is only the appropriate Government that is authorized to exempt any Establishment or class of Establishment from the payment of minimum Bonus.

iv. Hence, the Company has to pay minimum Bonus irrespective of its Huge losses, unless having regard to its financial position and

PRIME / ME31 / IPCC 6

6

Other circumstances, the appropriate Government exempts it from the payment of minimum Bonus.

4.

i. Estoppel: The given case constitutes an Inchoate Stamped Instrument. As per Sec.20 a person who gives another person, possession of his signature on blank stamped paper prima facie authorizes the latter as his agent to fill it up and give to the world the instrument as accepted by him. The principle is one of estoppel.

ii. Analysis: In the given case, ‘A’ is estopped from setting up B’s fraud since ‘A’ has effectively authorized ‘B’ to fill up any amount covered by the stamp, on that instrument. Thus ‘C’ is entitled to recover Rs. 2,000 from ‘A’ because ‘C’ has obtained it as a Holder in due course.

5. Gratuity is paid to the employee. But, if the services of the employee is terminated due to the death of employee, this amount is to be paid to his successors. To avoid any type of complications and controversies in such payment, the employee can made nomination.

Every employee, who has completed 1 year of service, shall make nomination for the purpose of the second proviso to Sec. 4(1). Such nomination shall be made within such time in such form and in such manner, as may be prescribed. An employee may in his nomination, distribute the amount of gratuity payable to him under this Act amongst more than one nominee.

If an employee has a family at the time of making a nomination, the nomination shall be made in favour of one or more members of his family, and any nomination made by such employee in favour of a person, who is not a member of his family shall be void.

If at the time of making a nomination the employee has no family, the nomination may be made in favour of any person(s). But if the employee subsequently acquire a family, such nomination shall forthwith become invalid and the employee shall made within such time as may be prescribed, a fresh nomination in favour of one or more members of his family.

Subject to the provision of Sec. 6(3) or 6(4), A nomination may be modified by an employee at any time, after giving to his employer a written notice in such form and in such a manner as may be prescribed.

If a nominee predeceases the employee, the interest of the nominee shall revert to the employee, who shall a fresh nomination, in the prescribed form, in respect of such interest.

Every nomination, fresh nomination or alteration of nomination, as the case may be, shall be sent by the employee to his employer, who shall keep the same in his safe custody.

6. Composition of the Committee

a) The Central Government has the power to constitute an Executive Committee. b) Executive Committee shall consist of 13 members.

PRIME / ME31 / IPCC 7

7

c) The members of the Executive Committee are selected out of the members of the Central Board. i. Chairman - appointed by the Central Government ii. 2 persons - representatives of the Central Government iii. 3 persons - representatives of the State Government iv. 3 persons - representatives of the employers v. 3 persons - representatives of the employees vi. Central Provident Fund Commissioner as a member.

7. A company has power to do the following acts:

a) The act is authorized by the memorandum (i.e. Express Power) b) The act is incidental for the attainment of its objects (i.e. Implied Power)

If the company does some another act, then it is ultra vires the company. According to the doctrine of ultra vires, such acts are void ab-initio. (Leading case: Ashbury Railway Carriage Company v Riche) In the given case M/s. RSP Pvt. Ltd. is authorized to trade directly on fruits and vegetables. It has no power to enter into a partnership for Iron and Steel with Mr. A. Such act can never be treated as ‘express’ or ‘implied’ powers to the company. As per ‘Doctrine of Constructive Notice’, Mr. A is deemed to be aware of the lack of powers of M/s. RSP Pvt. Ltd. So, Mr. A cannot enforce liability against M/s. RSP Pvt. Ltd. This conclusion is supported by the decision reported in the case of ‘The Ganga Mata Refinery Company (Pvt.) Ltd. v CIT)

8.

1. Provisions of Companies Act: i. Right of Pre-Emption: Existing shareholders have the right of pre-emption

u/s 81 i.e. any further issue of shares after a specified period should be first offered to them.

ii. Issue to Outsiders: Shares can be issued to outsiders only if they are issued within the specified period or when issued after the time limit, by way of Resolution passed at the General Meeting.

2. Court Ruling: A Company can be restrained from not offering any shares to its existing shareholders, when the Articles of Association provides for offer of new issue to them. Gas Meter Co. Ltd. vs. Diaphragm and General Leather Ltd.

3. Analysis and Conclusion: (a) Since the issue is made after 4 years of incorporation, provisions of Section

81 is attracted and therefore DSC Ltd. is entitled to be offered to subscribe for the shares.

(b) Goodluck Ltd. by not offering to DSC Ltd. has violated the provisions of Companies Act, 1956 and also the requirement contained in its Articles of Association. Therefore, decision of the Board is invalid.

(c) Also, Goodluck Ltd. cannot take a decision not to allot shares to DSC Ltd. unless the same is approved in the General Meeting.

PRIME / ME31 / IPCC 8

8

9. As per the Section 75 of the Companies Act, 1956 when shares are allotted to a person by a company, payment may be made (i) in cash, or (ii) in kind (with the consent of company). CASH here does not necessarily mean the current coin of the country. It means such transaction as would in an action at law for calls, support a plea of payment. So, such allotment is valid.

10.

Issue Discussion Conclusion Validity of Meeting a.) 21 clear days Notice of an Annual

General Meeting must be given b) If Notice is sent by post, it shall be deemed to have been received on expiry of 48 hours from the time of its posting. c) For working out clear 21 days, day of Notice and day of Meeting shall be excluded.

21 clear days notice has not been served and the meeting is, therefore, NOT validly convened.

Shortfall in Notice a)Where Notice is sent by post, it must have been sent at least 25 days before the date of Meeting b) Notice should have been posted on 14.10.2009; while actually it is posted on 16.10.2009.

Notice falls short by 2 days.

Condonation of delay

a)An Annual General Meeting called at a Notice shorter than 21 clear days shall be valid if consent is accorded thereto by all the Members entitled to vote thereat. b) Hence, if all the Members of the Company approve to shorter notice, shortfall may be condoned.

Shortfall can be condoned by the Members.

11.

a) An organization, whether a business or a government agency, is first and foremost a human society. If an employer does not take steps to create a work place where the employees have a clear and common understanding of what is right and wrong, and feels free to discuss and ask question about ethical issues and report violations, significant problems could arise, including:

i. Increased risk of employees making unethical decisions. ii. Increased tendency of employees to report violation to outside regulatory

authorities (whistle blowing) because they lack internal forum. iii. Inability to recruit and retain top people. iv. Diminished reputation in the industry and the community. v. Significant legal exposure and loss of competitive advantage in the market place.

And thus from the above problems, it is clear that how important is ethical behavior at work place.

PRIME / ME31 / IPCC 9

9

b) In many cases, Business interests come into conflict with moral values. Businessmen are faced with moral and ethical dilemmas while making a choice from various alternatives. The ethical dilemmas are highly complex and there are no clear guidelines to resolve the conflict.

Ethical behaviour creates goodwill and reputation that expand opportunities for profit. While competing for customers and workers, the company with a reputation for ethical behaviour has an edge over others which are considered unethical.

12. A sound ethical environment is necessary for ensuring ethical behaviour on the part of

members of the organization The following actions can be helpful for creating an ethical environment.

1. Awareness of Responsibilities:

All employees should be made aware of their legal and ethical responsibilities. Top Management should initiate policies to train and motivate employees towards ethical behaviour Employees should be encouraged to report cases of frauds, manipulations, misappropriations, etc.

2. Open Communication System:

There must be an open communication system in the organization. This communication system help the Employees to communicate frauds, mismanagement or any other form of non-routine detrimental behaviour, without the fear of being fired. This may be in the form of a helpline comprising of senior members of the Company, who are available for guidance on any moral, legal or ethical issues that an employee of the company may face.

3. Fair Treatment to Whistle Blowers:

A Whistle Blower is an employee / person who reports fraud, mismanagement or unethical practices to the appropriate level of management. Fair treatment and appreciation of Whistle Blowers is necessary to check fraud.

People in an organization hesitate to blow whistle due to fear of victimization. Top Management must ensure fair treatment to whistle blowers to assure and encourage them. This would help to check fraud and other unethical practices.

13.

a) Correct. Fairness and honesty are at the heart of business ethics. Businessperson are expected not harm customer, employees, clients or competitors knowingly through deception, misrepresentation, coercion or discrimination. One aspect of fairness and honesty is related to disclosure or potential harm caused by the product use. Another aspect of fairness relates to competition, sometimes gain control over market by using questionable practices that harm competition and business too. So, we can conclude that the fairness and honesty are pillars of success in the business.

PRIME / ME31 / IPCC 10

10

b) Incorrect. The root word for ethics is the Greek “ethos” meaning character while the root word of moral is latin “Mos” meaning “custom”. Character and custom, however, provide two very different standards for defining what is right and wrong. Character is personal attribute, while custom is defined by a group overtime. People have character societies have customs. Another way to look at the distinction is to say that morals are accepted from an authority (culture, religion etc.) while ethics are accepted because they follow from personally accepted principles. So there is a vast distinction between ethics and moral and hence the statement is FALSE.

14.

a) The network or pathway in informal communication is known as grapeline. In the context of an organization the flow of information in informal communication is called, ‘grapevine’ because of the origin and direction of the flow of these messages cannot be easily fraud.

The merits and demerits of grapevine form of communication are as follows: Merits:

i. Speed: Speed in the most removable fast since there is no formed barriers and no stopping.

ii. Support System: A grapevine is an informal support system development by employees within an organization. It ways them closer and gives man immense satisfaction.

iii. Feedback: The managers get to income the reason of must subordinate. Thus feedback is quick. Employees attitudes and reactions to plans and policies can be ascertained by managers through informal and interactions.

iv. Psychological Satisfaction: The grapevine gives immense psychological to the workers and strengthens their solidarity. It drawn them nearly to each other and thus keeps the organization intact as a social entity. It builts team spirit among the employees.

Demerits:

i. Less credible: A grapevine is less credible than a formal channel of communication. It cannot be taken seriously as involves only a mouth.

ii. Leakage: Information may get leaked at the wrong time the word ‘open secret’ in an organization can often be attributable to such take.

iii. Incomplete and distorted information: The information passed through the grapevine does not carry complete information nor does it reveal the complete picture. The reason for this is that information transmitted through the grapevine carry rumors and distorted facts.

iv. Adverse effect on reputation: The grapevine often gives a distorted picture of the actual situation and spread rumors, loose talks about responsible people leaving an adverse effect on the image of the organization.

PRIME / ME31 / IPCC 11

11

b) SQR PRIVATE LIMITED

NOTICE

NOTICE is hereby given that the TWENTY-SEVENTH ANNUAL GENERAL MEETING of the members of the Company will be held on Monday, the 20th September, 2010 at 1.00 a.m. at the Registered Office of the Company at………. to transact the following business:- 1. To consider and adopt the Profit & Loss Account for the Corporate Financial Year

ended 31st March, 2010 and the Balance Sheet as at that date and the Reports of the Directors and Auditors thereon.

2. To declare a dividend on equity shares. 3. To appoint a Director in place of Mr. ‘X’, who retires by rotation and being

eligible, offers himself for re-appointment. 4. To appoint M/s. ‘Y’ , retiring Auditors as Auditors of the Company, to hold office

from the conclusion of this meeting until the conclusion of the next Annual General Meeting of the Company and to fix their remuneration.

By Order of the Board of Directors

Sd/-

Place: Company Secretary Date: NOTES: A MEMBER ENTITLED TO ATTEND AND VOTE IS ENTITLED TO APPOINT A PROXY TO ATTEND AND VOTE INSTEAD OF HIMSELF AND THE PROXY NEED NOT BE A MEMBER. PROXIES IN ORDER TO BE VALID MUST BE RECEIVED BY THE COMPANY NOT LESS THAN 48 HOURS BEFORE THE MEETING. 15. CHAIRMAN SPEECH

Ladies and Gentlemen,

I am very thankful to get the privilege to welcome you to 28th Annual General Meeting of your Company. I am feeling pleasure to say that the performance of your company is beyond the expectations, like –

1. Gross Turnover for the year 2009-10 grew by 25% to Rs. 5050

crores, besides a cut through competition in the market. 2. Government increased the rate of excise duty on our products,

but even then the pre-tax profit increased by 20% and post-tax profit by 18%

3. Earnings Per Share for the year is Rs.8 (increased by 50%) 4. During the last five years, the net worth of company is increased

by 10% amounting to Rs. 6580 Billion.

PRIME / ME31 / IPCC 12

12

You will be very happy to know that on the basis of turnover, your company is now among the top ten companies of India.

I am sure that the strategic progress of the businesses in your Company’s portfolio is a source of satisfaction to shareholders. Your Company has made substantial investments in technology and innovation. Brand building at the national and international level was the main target of the year.

It is due to your continued trust in your Company that your Company’s brands today account for three of the top five brands in the country.

The progress made in strategy implementation and the resultant financial performance have further aspired us to make a larger contribution to the Indian society.

Corporate Social Responsibilities: The Indian business is integrating with the global market. So, there is a great need for responsible business conduct for global competitiveness. In line with this thought, your Company is engaged to involve its consumers as partners in progress by bundling CSR. Other Social Initiatives Your Company’s social initiatives in the vicinity of its operating locations are centered around three main areas---

a) natural resource management, which includes wasteland, watershed and agriculture development;

b) sustainable livelihoods, comprising genetic improvement in livestock and women’s economic empowerment; and

c) community development, with focus on primary education and health and sanitation. Conclusion The journey of the past decade has been most rewarding for your Company’s world-class employees and for me personally. The real transformation lies in their capabilities, their commitment to stay the course of a challenging strategic path, and their willingness to go the distance in their quest for enduring value for the nation and for shareholders. In the unfolding era of new opportunities and new challenges, I seek your support on their behalf, as always. Thanks for your attention. CHAIRMAN

PRIME / ME31 / IPCC 13

13

16. Any partner may, at any time during the subsistence of the partnership, retire from the firm giving at least one month notice of his intension of doing so.

Partnership Retirement Deed

This must be executed on a stamp paper of appropriate value and copy sent to registrar of firms along with the prescribed form duly completed. The execution of retirement deed results in a reconstitution of the firm.

X, Y and Z were carrying on business in partnership and whereas X having expressed his desire to retire the partnership firm by mutual consent., the terms of retirement are hereby agreed as follows:

i. X will retire from the partnership effective from close of business on 31st March 09 ii. The firm is free to continue the business with all the assets and liabilities and use the

same firm name with the remaining partners. iii. The continuing partners (Y, Z) release X of all the debts and allegation including taxes

due from the firm on the date of this deed to third parties. iv. The parties hereby agree to execute even other document that may be necessary to

give effect to the partnership retirement agreement.

PRIME ACADEMY 31st SESSION MODEL EXAM

IPCC – COST ACCOUNTING AND FINANCIAL MANAGEMENT QUESTION PAPER

CGLT

No. of Pages: 5 Total Marks: 100 No of Questions: 7 Time Allowed: 3 Hrs

All are compulsory

Working notes should form part of the answers

1. Answer any five of the following:

(i) What are the objectives of cost accounting. (ii) Calculate efficiency, and activity ratio from the following data :

Capacity ratio = 75% Budgeted output = 6000 units Actual output = 5000 units Standard Time per unit = 4 hours

(iii) Distinguish between cost control and cost reduction. (iv) What are the main advantage of cost plus contracts. (v) A Company sells two products, J and K. The sales mix is 4 units of J and 3 units of K. The

contribution margins per unit are Rs. 40 for J and Rs. 20 for K. Fixed costs are Rs. 6,16,000 per month. Compute the break-even point.

(vi) What are three major essentials of a good cost accounting system. (5x3=15 Marks)

2. Mega Company has just completed its first year of operations. The unit costs on a normal

costing basis are as under : Rs.

Direct material 4 kg @ Rs. 4 = 16.00 Direct labour 3 hrs @ Rs. 18 = 54.00 Variable overhead 3 hrs @ Rs. 4 = 12.00 Fixed overhead 3 hrs @ Rs. 6 = 18.00

100.00 Selling and administrative costs:

Variable Rs. 20 per unit Fixed Rs. 7,60,000 During the year the company has the following activity : Units produced = 24,000

PRIME / ME31 / IPCC 1

Units sold = 21,500 Unit selling price = Rs. 168 Direct labour hours worked = 72,000 Actual fixed overhead was Rs. 48,000 less than the budgeted fixed overhead. Budgeted variable overhead was Rs. 20,000 less than the actual variable overhead. The company used an expected actual activity level of 72,000 direct labour hours to compute the predetermine overhead rates. Required: (i) Compute the unit cost and total income under :

(a) Absorption costing (b) Marginal costing.

(ii) Under or over absorption of overhead. (iii) Reconcile the difference between the total income under absorption and marginal costing.

(18 Marks)

3. a) XP Ltd. furnishes you the following information relating to process II.

(i) Opening work-in-progress—NIL (ii) Units introduced 42,000 units @ Rs. 12 (iii) Expenses debited to the process :

Rs. Direct material 61,530 Labour 88,820 Overheads 1,76,400

(iv) Normal loss in the process = 2% of input. (v) Closing work-in-progress—1200 units

Degree of completion — Materials 100% Labour 50% Overhead 40%

(vi) Finished output—39500 units (vii) Degree of completion of abnormal loss :

Material 100% Labour 80% Overhead 60%

(viii) Units scraped as normal loss were sold at Rs. 4.50 per unit, (ix) All the units of abnormal loss were sold at Rs. 9 per unit.

Prepare: a) Statement of equivalent production. b) Statement showing the cost of finished goods, abnormal loss and closing work-in-progress. c) Process II account and abnormal loss account.

(10 Marks) b) The following information is available from the cost records of Vatika & Co. For the month of

August, 2009 : Material purchased 24,000 kg Rs. 1,05,600

PRIME / ME31 / IPCC 2

Material consumed 22,800 kg Actual wages paid for 5,940 hours Rs. 29,700 Unit produced 2160 units. Standard rates and prices are : Direct material rate is Rs. 4.00 per unit Direct labour rate is Rs. 4.00 per hour Standard input is 10 kg. for one unit. Standard requirement is 2.5 hours per unit. Calculate all material and labour variances for the month of August-2009.

(9 Marks) 4. Answer any three of the following :

(i) Standard Time for a job is 90 hours. The hourly rate of Guaranteed wages is Rs. 50. Because of the saving in time a worker a gets an effective hourly rate of wages of Rs. 60 under Rowan premium bonus system. For the same saving in time, calculate the hourly rate of wages a worker B will get under Halsey premium bonus system assuring 40% to worker.

(ii) Explain briefly, what do you understand by Operating Costing. How are composite units computed ?

(iii) The following information relating to a type of Raw material is available : Annual demand 2000 units Unit price Rs. 20.00 Ordering cost per order Rs. 20.00 Storage cost 2% p.a. Interest rate 8% p.a. Lead time Half-month Calculate economic order quantity and total annual inventory cost of the raw material.

(iv) List the eight functional budgets prepared by a business. (3x3=9 marks)

5. Answer any five of the following :

(i) What are the limitations of Financial ratios. (ii) What do you understand by Business Risk and Financial Risk ? (iii) Differentiate between Factoring and Bills discounting. (iv) Distinguish Financial Management and Financial Accounting. (v) Y Ltd. retains Rs. 7,50,000 out of its current earning. The expected rate of return to the

shareholders. If they had invested the funds elsewhere is 10%. The brokerage is 3% and the shareholders came in 30% tax bracket. Calculate the cost of retained earning.

(vi) From the informations given below calculate the amount of Fixed assets and Proprietor's fund. Ratio of fixed assets to proprietors fund = 0.75 Net working capital = Rs. 6,00,000

(5x2=10 Marks)

PRIME / ME31 / IPCC 3

6. Y’s profit and loss statement for the year ended 31 March 2010 and balance sheet as at 31

March 2010 and 31 March 2009 were as follows: Y – profit and loss statement for the year ended 31st March 2010

Rs.’000 Rs.’000 Sales revenue 360 Raw materials consumed (35) Staff costs (47) Depreciation (59) Loss on disposal (9)

(150) Operating profit 210 Interest payable (14) Profit before tax 196 Income tax expense (62) Profit after tax 134

639 668 Current assets Inventory 12 10 Trade receivables 33 25 Bank 24 28

69 63 708 731

Capital and reserves Share capital 180 170 Share premium 18 12 Retained earnings 358 257

556 439 Non-current Liabilities Long-term loans 100 250 Current liabilities Trade payables 6 3 Income tax 46 39

52 42 708 731

During the year, the entity paid Rs. 45,000 for a new piece of machinery. A dividend of Rs. 33,000 was paid during the year.

PRIME / ME31 / IPCC 4

Requirement Prepare a statement of cash flows for Y for the year ended 31 March 2010 in accordance with the requirements.

(20 Marks)

7. Answer any three of the following:

(i) Explain the two basic functions of Financial Management. (ii) Explain the following terms:

a) Ploughing back of profits b) Desirability factor.

(iii) What do you understand by Weighted average cost of Capital? (iv) There are two firms P and Q which are identical except P does not use any debt in its

capital structure while Q has Rs. 8,00,000, 9% debentures in its capital structure. Both the firms have earning before interest and tax of Rs. 2,60,000 p. a. and the capitalisation rate is 10%. Assuming the corporate tax of 30%, calculate the value of these firms according to MM Hypothesis.

(3x3=9 Marks)

PRIME / ME31 / IPCC 5

PRIME ACADEMY 31st SESSION MODEL EXAM

IPCC – COST ACCOUNTING AND FINANCIAL MANAGEMENT SUGGESTED ANSWERS

1.

(I) OBJECTIVES OF COST ACCOUNTING The main objectives of Cost Accounting are as follows:

i. Ascertainment of cost. ii. Determination of selling price. iii. Cost control and cost reduction. iv. Ascertaining the profit of each activity. v. Assisting management in decision-making.

(II)

AT w Capacity ratio = -------

BT ATw

75% = ---------- 6000 x 4

ATw = 24000 x 75% = 18000 hrs

ST 5000 X 4

Efficiency ratio = ---- = ---------- x 100 = 111.11% ATw 18000

ST 20000

Activity ratio = ---- = -------- x 100 = 83.33% BT 24000

Here ST = Standard time for actual output

ATw = Actual time worked BT = Budgeted time.

PRIME / ME31 / IPCC 6

(III) Cost Reduction, may be defined "as the achievement of real and permanent reduction in the unit cost of goods manufactured or services rendered without impairing their suitability for the use intended or diminution in the quality of the product." Cost reduction should not be confused with Cost control. Cost saving could be a temporary affair and may be at the cost of quality. Cost reduction implies the retention of the essential characteristics and quality of the product and thus it must be confined to permanent and genuine savings in the cost of manufacture, administration, distribution and selling, brought about by elimination of wasteful and inessential elements from the design of the product and from the techniques carried out in connection therewith. In other words, the essential characteristics and quality of the products are retained through improved methods and techniques and thereby a permanent reduction in unit cost is achieved. The definition of cost reduction does not, however, include reduction in expenditure arising from reduction in taxation or similar Government action or the effect of price agreements.

(IV) Advantages of Cost-plus Contracts: Such contracts have number of advantages for the

contractor and the contractee.

Advantages to Contractor i. All costs are fully covered. There is no risk of loss due to price changes and under

estimation of costs, ii. There are no bargaining hassles. iii. There is an automatic escalation clause so that cost increases are recovered, iv. Profit is known in advance, v. Work of preparing tenders and quotations gets simplified.

Advantages of Contractee i. Contractee pays only the reasonable price based on actual cost incurred, ii. No bargaining hassles, iii. Contractee gets the benefit of fall in price of materials and wage rates, etc.

(V) Break up point in case of multi product firm

Fixed Cost 616000 BEP = ----------------------------------- = ------------------------------

Overall Contribution per unit 31.428571/- (W.N.1)

= 19600 Units per month

W.N. (1) Overall contribution per unit

Product Contribution per unit

Sales Mix

Contribution X Sales Mix

J K

40/- 20/-

4 units 3 units

7

160 60

220

PRIME / ME31 / IPCC 7

Σ Contribution x Sales Mix Overall Contribution per unit = --------------------------------

Σ Sales Mix 220

= ----- = 31.428571 /- 7

(VI) Essentials of a good Cost Accounting System: The essential features, which a good Cost Accounting System should possess, are as follows:

i. Cost Accounting System should be tailor-made, practical, simple and capable of meeting the requirements of a business concern.

ii. The data to be used by the Cost Accounting System should be accurate; otherwise it may distort the output of the system.

iii. Necessary cooperation and participation of executives from various departments of the concern is essential for developing a good system of Cost Accounting.

iv. The Cost of installing and operating the system should justify the results. v. The system of costing should not sacrifice the utility by introducing meticulous and

unnecessary details.

2. (i) Profit & Loss A/c under absorption costing Rs. Rs.

To D. Material (24000 units @ 16/- per unit) ” D. Labour (24000 units @ 54/- per unit) ” Variable overhead absorbed ” Fixed overhead absorbed ” Selling & Admn. Overhead Variable (21500 units @ 20/- p.u.) Fixed ” Under recovery of variable overhead ” Net Income

3,84,000

12,96,000

2,88,000 4,32,000

4,30,000

7,60,000

20,000

3,00,000 39,10,000

By Sales (215000 units @ 168/- p.u.) ” Over recovery of fixed overhead ” Closing Stock (100/- x 2500 units)

36,12,000

48,000

2,50,000

39,10,000 Profit & Loss A/c under marginal costing Rs. Rs. To D. Material ” D. Labour ” Variable overhead (Actual) ” Fixed overhead (Actual) ” Selling & Admn. OH Variable

3,84,000 12,96,000 3,08,000 3,84,000

4,30,000

By Sales ” Closing Stock (82.8333/- x 2500 units)

36,12,000 2,07,083

PRIME / ME31 / IPCC 8

Fixed ” Net Income

7,60,000 2,57,083

38,19,083

38,19,083

Budgeted Fixed overhead = 72000 labours hours x 6/- per hour = 432000/- Actual Fixed overhead = 432000/- - 48000 /- = 383000/- Fixed overhead absorbed = units produced x fixed oh per unit = 24000 x 18/- = 432000 /- Budgeted variable overhead = 72000 labour hours @ 4/- per hour = 288000 /- Actual variable overhead = 288000/- + 20000 /- = 308000 /- Cost per unit under absorption costing Rs.D. Material 16.00 D. Labour 54.00 Variable Overhead 12.00 Fixed Overhead 18.00 Total Cost 100.00 Cost per unit under Marginal costing Rs. D. Material 16.00 D. Labour 54.00 Variable overhead 12.83 308000/- -------------- 2400 units Total Cost 82.83 (ii) Under or over absorption of overhead (a) Variable Overhead (Actual) 308000/- ” ” (Absorbed) 288000/- Under recovery = 20000/- (b) Fixed overhead (Actual) = 384000/- ” ” (Absorbed) = 432000/- Over recovery = 48000/- (iii) Reconciliation statement between profit under absorption costing & marginal costing Profit as per marginal costing 257083 /- Add : under valuation of Clo. Stock in marginal costing 42917/- Profit as per absorption costing ---------- 300000 /-

PRIME / ME31 / IPCC 9

3. (a) Statement showing equivalent production Particulars Total

Rs. Material

% Qty Rs.

Labour % Qty Rs.

Overhead % Qty Rs.

(i) Opening WIP (ii) Units in produced, completed & transferred process III (iii) Normal Loss (iv) Abnormal Loss (v) Closing WIP Equivalent Production

NIL

39500

840 460 1200

42000

--

100%

-- 100% 100%

--

39500

-- 460 1200

41160

--

100%

-- 80% 50%

--

39500

-- 368 600

40468

--

100% --

60% 40%

--

39500 --

276 480

40256

Statement showing cost per unit of each element of material, labour & overhead

Material Labour Rs. Rs.

Overhead Rs.

Total Material Cost including additional material (Rs.) Less : Scrap value of Normal Loss [840 units @ 4.5/- per unit] Equivalent Production Cost per unit

565530

3780 561750 41160

13.647959/-

88820

-- 88820 40468

2.1948205/-

176400

-- 176400 40256

4.3819554/- Statement showing cost of finished goods, abnormal loss closing WIP Particulars Finished Goods

Rs. Abnormal Loss

Rs. Closing WIP

Rs. D. Material D. Labour Overhead

539094/- (39500 x 13.647959)

86695/- (39500 x 2.1948)

173087/- (39500 x 4.3819/-)

798876/-

6278/- (460 x 13.6479)

807/- (368 x 2.1948/-)

1210/- (276 x 4.3819/-)

8295/-

16378/- (1200 x 13.6479/-)

1318/- (600 x 2.1948/-)

2103/- (480 x 4.3819/-

19799/- Process II account Particulars Qty Amount

Rs. Particulars Qty Amount

Rs. To D. Material ” Other Material ” D. Labour ” Overhead

42000 -- -- --

42000

504000 61530 88820

176400 830750

By Normal Loss ” Abnormal Loss ” Finished Goods a/c ” Closing WIP

840 460

39500 1200

42000

3780 8295

798876 19799

830750

PRIME / ME31 / IPCC 10

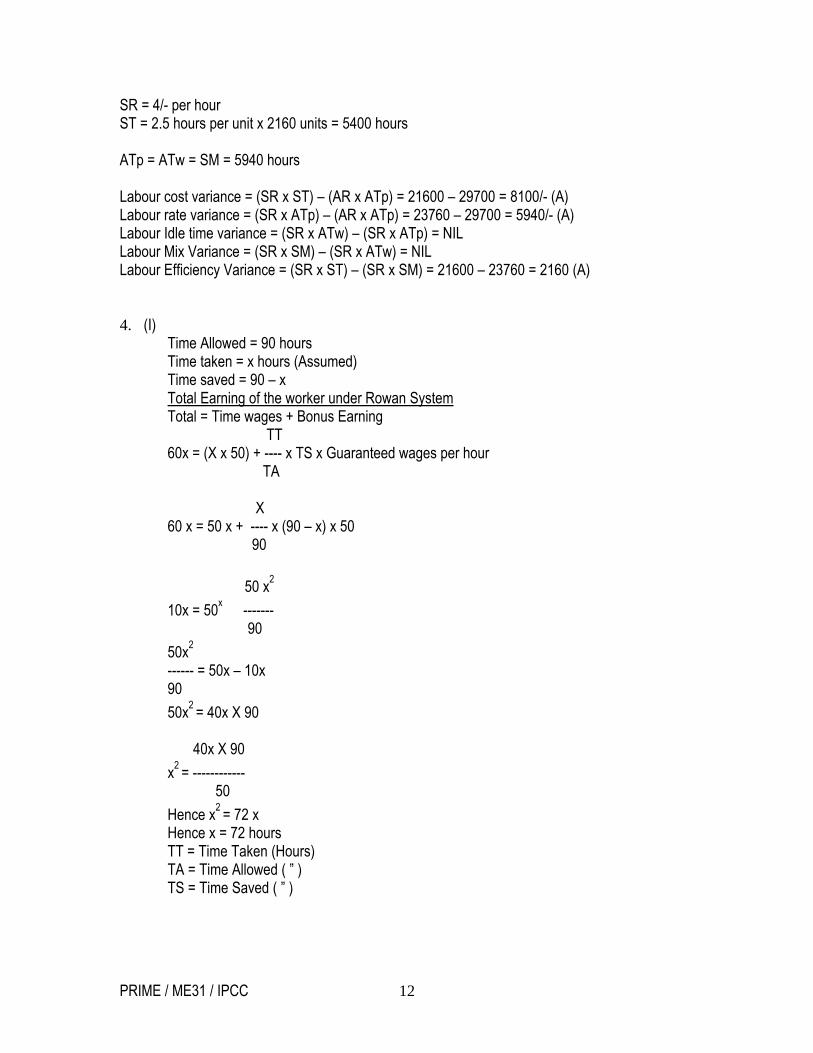

Abnormal Loss account Rs. Rs. To Process II a/c 8295 By Cash a/c (460 units @ 9/- p.u.) 4140 ” Profit & Loss a/c (B/F) 4155 ------- -------- 8295 8295 ------- ------- 3 (b) Material Variances (Assuming Partial plan)

SP x SQ Rs.

SP x SM Rs.

SP x AQ used Rs.

AP x AQ used Rs.

4 x (10 x 2160) = 86400/-

4 x 22800 = 91200/-

4 x 22800 = 91200/-

4.4 x 22800 = 100320

SP = Standard Price of material per kg = 4/- SQ = Standard Quantity for actual output = 10 kg x 2160 units = 21600 k.g. AQ used = Actual Quantity used = 22800 k.g.

Rs. 105600 AP = Actual Price of Material per K.g. = --------------

24000 k.g. = 4.4/- per k.g. SM=Total Actual quantity used in standard mix ratio= 22800 k.g. (because there is only one material given in the question) Material Cost variance = (SP x SQ) – (AP x AX used) = 86400/- - 100320/- = 13920 /- (A) Material Price variance = (SP x AX used) – (AP x AQ used) = 91200/- - 100320/- = 9120/- (A) Material usage variance = (SP x SQ) – (SP x AQ used) = 86400 – 91200 = 4800/- (A) Material Mix Variance = (SP x SM) - (SP X AQ used) = 91200 – 91200 = NIL Material yield variance = (SP X SQ) – (SP X SM) = 86400 – 91200 = 4800 /- (A) Labour varianceSR X ST SR X SM SR X ATW SR X ATP AR X ATP 4 x (2.5 x 2160) 4 x 5940 4 x 5940 4 x 5940 29700/- = 21600/- = 23760/- = 23760/- = 23760/- Here, SR = Standard rate of labour per hour AT = Actual rate of labour per hour ST = Standard time for actual output ATw = Actual time worked. ATp = Actual time paid for SM = Total Actual time worked in standard mix ratio. Note : - (1) It is assumed that ATp = ATw (2) In this question only one type of labour is there therefore SM = ATw.

PRIME / ME31 / IPCC 11

SR = 4/- per hour ST = 2.5 hours per unit x 2160 units = 5400 hours ATp = ATw = SM = 5940 hours Labour cost variance = (SR x ST) – (AR x ATp) = 21600 – 29700 = 8100/- (A) Labour rate variance = (SR x ATp) – (AR x ATp) = 23760 – 29700 = 5940/- (A) Labour Idle time variance = (SR x ATw) – (SR x ATp) = NIL Labour Mix Variance = (SR x SM) – (SR x ATw) = NIL Labour Efficiency Variance = (SR x ST) – (SR x SM) = 21600 – 23760 = 2160 (A) 4. (I)

Time Allowed = 90 hours Time taken = x hours (Assumed) Time saved = 90 – x Total Earning of the worker under Rowan SystemTotal = Time wages + Bonus Earning

TT 60x = (X x 50) + ---- x TS x Guaranteed wages per hour

TA X

60 x = 50 x + ---- x (90 – x) x 50 90

50 x2

10x = 50x ------- 90 50x2

------ = 50x – 10x 90 50x2 = 40x X 90

40x X 90

x2 = ------------ 50 Hence x2 = 72 x Hence x = 72 hours TT = Time Taken (Hours) TA = Time Allowed ( ” ) TS = Time Saved ( ” )

PRIME / ME31 / IPCC 12

Total earning of the worker under halsey scheme (40%) For the same savings in time Total Earning = Time wages + Bonus = Time wages + 50% of time saved x Guaranteed wages = (50% x 72 hours) + 50% [18 hours x 50/-] = 3600/- + 450/- = 4050 /- Total Earning Hourly Earning of worker B = ----------------- TT 4050 /- = --------- = 56.25/- 72 hrs

(I) MEANING OF OPERATING COSTING : It is a method of ascertaining costs of providing

or operating a service. This method of costing is applied by those undertakings which provide services rather than production of commodities. The emphasis under operating costing is on the ascertainment of cost of services rather than on the cost of manufacturing a product. This costing method is usually made use of by transport companies; gas and water works departments, electricity supply companies, canteens, hospitals, theatres, schools, etc. Composite units i.e, tonnes Kms, quintal Kms. etc may be computed in two ways -

i. Absolute (Weighted average) tonnes-kms., quintal kms., etc: Absolute (weighted) tonnes kms, are the sum total of tonnes kms., arrived at by multiplying various distances by respective load quantities carried.

ii. Commercial (simple average) tonnes Kms., quintal Kms etc: Commercial (simple average) tonnes Kms., are arrived at by multiplying total distance kms., average load quantity.

(II) 2AB

Economic order quantity = Whole Root of ------ C A = Annual Consumption = 2000 units assuming consumption ratio of finished goods & Raw material is 1:1 B= Ordering Cost per order = 20/- C = Carrying cost per unit per annum = (2% + 8%) of Purchase price = 10% of Rs. 20/- = 2/- per unit p.a. 2AB 2 X 2000 x 20

(III) EOQ = Whole Root ------ = Whole root ---------------- = 200 units C 2 Total Annual Inventory cost of Raw Material = Inventory Purchase cost + Inventory Holding Cost + Inventory Carrying Cost = 40000/- + 200/- +200/- = 40400/- Inventory Purchase Cost = 2000 units @ 20/- p.u. = 40000/-

PRIME / ME31 / IPCC 13

AB 2000 X 20 ” ” Holding Cost = --------- = --------------- EOQ 200 = 200/-

EOQ x C 200 units x 2/- ” ” Carrying Cost = ---------- = ----------------- 2 2 = 200/-

(IV) List of eight functional budgets prepared by a business are –

1. Sales Budget 2. Production Budget 3. Production Cost Budget 4. Raw Material Consumption Budget 5. Raw Material Purchase Budget 6. Direct Labour Budget 7. Factory/Manufacturing Overheads Budget 8. Administration Overheads Budget etc.

5.

(I) Limitations of Financial ratios

a) Financial statements do not represent a complete picture of the business, but merely a collection of facts which can be expressed in monetary terms. These may not refer to other factors which affect performance.

b) Over use of ratios as controls on managers could be dangerous, in that management might concentrate more on simply improving the ratios than on dealing with the significant issues. For example, the return on capital employed can be improved by reducing assets rather than increasing profits.

c) Ratios are interconnected. They should not be treated in isolation. The effective use of ratios, therefore, depends on being aware of all these limitations and ensuring that, following comparative analysis, they are used as a trigger point for investigation and corrective action rather than being treated as meaningful in themselves.

(II) Business Risk: It is concerned with the operation of any firm. The cost structure of the any

firm gives rises to business risks because of the existence of fixed nature of costs. Financial Risk: It indicates the effects on earnings by rise of fixed cost funds. It refers to the use of debt in the capital structure. Financial risk arises when a firm deploys debt funds with fixed charge.

PRIME / ME31 / IPCC 14

(III) Factoring Bills discounting

1. It is also called ‘Invoice factoring’. 2. In this, the parties are viz., client, factor and debtor. 3. It is broad in scope. 4. It is management of book debts. 5. Maximum time is 6 months. 6. Grace time is not given. 7. Bad debts protection is given for extra commission. 8. There is no specific Act. 9. Settlement : No such provision. 10. Provision of advance payment on book debts is available.

1. It is also called ‘Invoice discounting’. 2. In this, the parties are : drawer, drawee and payee. 3. It is narrow in its scope. 4. It is a sort of borrowing from commercial banks. 5. Maximum time is 3 months. 6. Grace time is 3 days. 7. Protection is allowed for del credre commission. 8. Negotiable Instruments Act applies. 9. Settlement : Notary public. 10. No such provision is available.

(IV) Difference between Financial Management and Financial Accounting :