THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY - Date: GAIN Report Number: Post: Report Categories: Approved By: Prepared By: Report Highlights: The Japanese organic food market was estimated at approximately $1.4 billion as of 2009 with slow but steady growth to that point. Nonetheless the Japanese organic market is still limited in scope with significant challenges to expansion; including limited domestic supply; underdeveloped distribution channels; and a low level of consumer understanding of organics. Organic industry insiders believe that consumer interest in organics is increasing and that the growth potential of the market is significant. With the U.S. - Japan organic equivalency arrangement in place, ATO Japan can offer U.S. organic suppliers assistance with following market movements in Japan and taking advantage of opportunities that the Japanese organic market may present. Chika Motomura, marketing specialist at ATO Osaka Mr. Morgan Perkins, ATO Japan Director Market Development Reports Special Certification - Organic/Kosher/Halal Japanese Organic Market Osaka ATO Japan JA7705 12/27/2017 Public Voluntary

Transcript

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY

USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT

POLICY

-

Date:

GAIN Report Number:

Post:

Report Categories:

Approved By:

Prepared By:

Report Highlights:

The Japanese organic food market was estimated at approximately $1.4 billion as of 2009 with slow but

steady growth to that point. Nonetheless the Japanese organic market is still limited in scope with

significant challenges to expansion; including limited domestic supply; underdeveloped distribution

channels; and a low level of consumer understanding of organics. Organic industry insiders believe that

consumer interest in organics is increasing and that the growth potential of the market is

significant. With the U.S. - Japan organic equivalency arrangement in place, ATO Japan can offer U.S.

organic suppliers assistance with following market movements in Japan and taking advantage of

opportunities that the Japanese organic market may present.

Chika Motomura, marketing specialist at ATO Osaka

Mr. Morgan Perkins, ATO Japan Director

Market Development Reports

Special Certification - Organic/Kosher/Halal

Japanese Organic Market

Osaka ATO

Japan

JA7705

12/27/2017

Public Voluntary

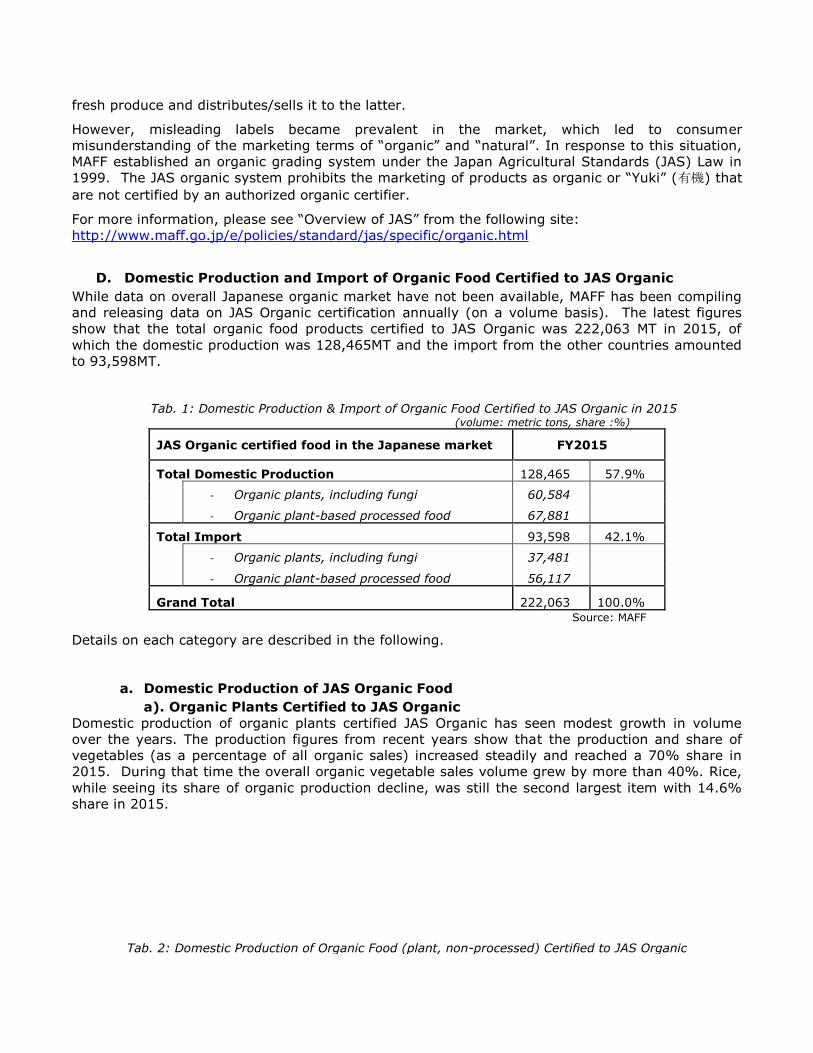

I. Market Overview

A. Japanese Organic Market

According to the Research Institute of Organic Agriculture (FiBL) and the International Federation

of Organic Agricultural Movements (IFOAM), the world organic food market had a value of $81.6

billion in 2015. Data released by the Organic Trade Association (OTA) reveals that the U.S. organic

food market recorded sales of $43.09 billion in 2016, with an annual growth rate of 8.4%,

accounting for 5.3% of total food sales.

This is in stark contrast to the Japanese organic food market. To begin with, there has not been a

comprehensive survey of the overall Japanese organic market other than the “Organic Market

Research Project (OMRP),” conducted by a team led by IFOAM Japan in 2010. That study estimated

the value of the Japanese organic food market at around $ 1.3 to $1.4 billion* as of 2009. The

Japanese Ministry of Agriculture, Forestry and Fisheries (MAFF) as well as the Japanese organic

industry has been quoting this figure to refer to the Japanese organic market.

According to MAFF, the share of organic in the domestic production of plants, including fungi, was a

mere 0.24% in 2015.

This comparison makes clear that the Japanese organic market has not expanded to the extent

seen in other markets. This is partly due to limited supply of domestic organic products and

undeveloped distribution channels for organic products, limiting the availability of organic products

in the market. In addition, many consumers lack a clear understanding of what is meant by the

word “organic” and confuse the term with “natural.” Industry contacts believe that tendency

hampers growth of the organic market. * The exchange rate used in this report is $1=100 yen, unless otherwise mentioned.

B. Selling as Organic in Japan

The production and distribution of organic food in Japan are regulated by JAS

(Japan Agricultural Standards) Law. JAS Organic certification and placement

of the JAS Organic seal (Figure 1) on each product is required for food

products to be labeled and sold as organic in Japan.

It should be noted, however, that this requirement applies only to what are

defined as “specified products.” The JAS law defines plants, including fungi, and plant-based

processed foods as “specified products” and requires them to be JAS Organic certified and affixed

with JAS Organic seal in order to be sold as organic.

According to the JAS law, the “plant” category includes, but is not limited to, fresh fruit &

vegetables, grains, and soybeans. The “plant-based processed food” category, limited to processed

foods made from at least 95% plant-based ingredients, includes a wide range of processed foods

such as canned fruit & vegetables, fruit & vegetable juice, sugar and processed soybean products.

On the other hand, the law defines all the other foods—including, e.g., meat, fish and dairy

products—as “non-specified products,” and exempts them from the JAS requirements. At present

these non-specified organic products can be sold as ‘organic’ without being certified to JAS Organic

standards and without affixing JAS Organic seals. Also exempted are organic processed foods

containing more than 5% non-plant-based ingredients; such as a frozen pizza in which the cheese

might exceed 5% of product weight.

C. History and Background

The Japanese organic/natural food market developed from what is called “teikei-saibai” or

“keiyaku-saibai” in Japanese, which can be translated as contract-base production and distribution,

in which farmers and consumers establish a partnership and the former produces organic/natural

Fig. 1

fresh produce and distributes/sells it to the latter.

However, misleading labels became prevalent in the market, which led to consumer

misunderstanding of the marketing terms of “organic” and “natural”. In response to this situation,

MAFF established an organic grading system under the Japan Agricultural Standards (JAS) Law in

1999. The JAS organic system prohibits the marketing of products as organic or “Yuki” (有機) that

are not certified by an authorized organic certifier.

For more information, please see “Overview of JAS” from the following site:

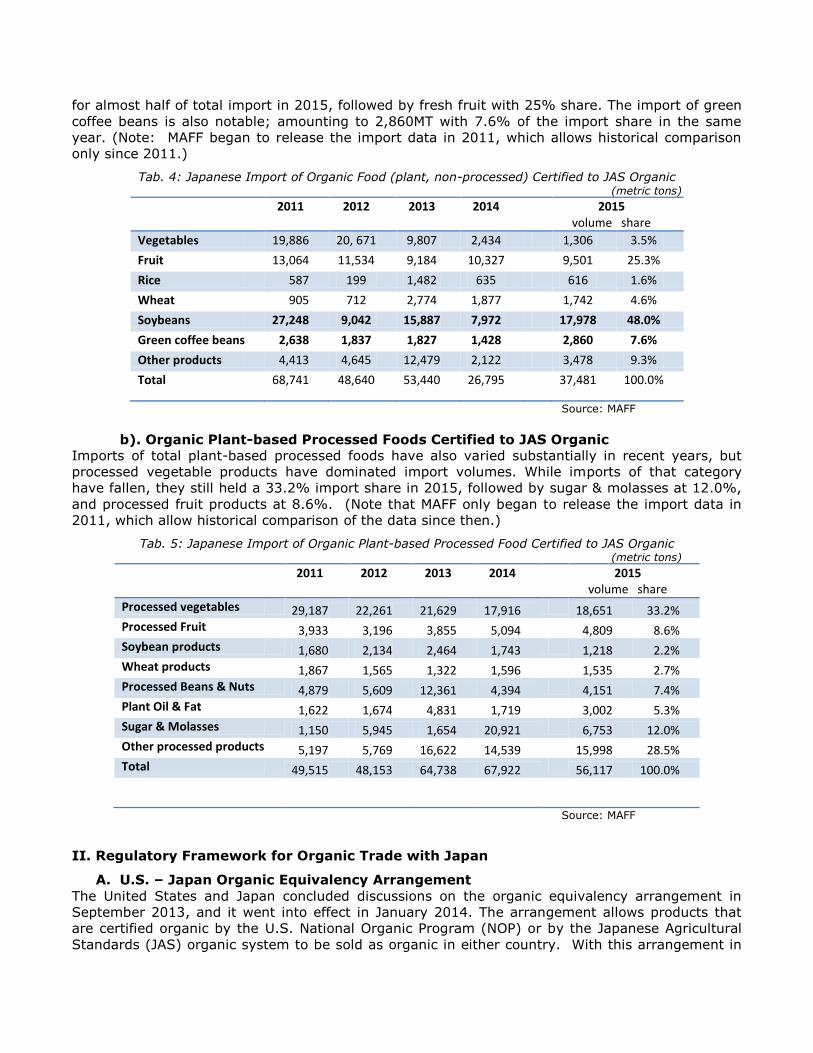

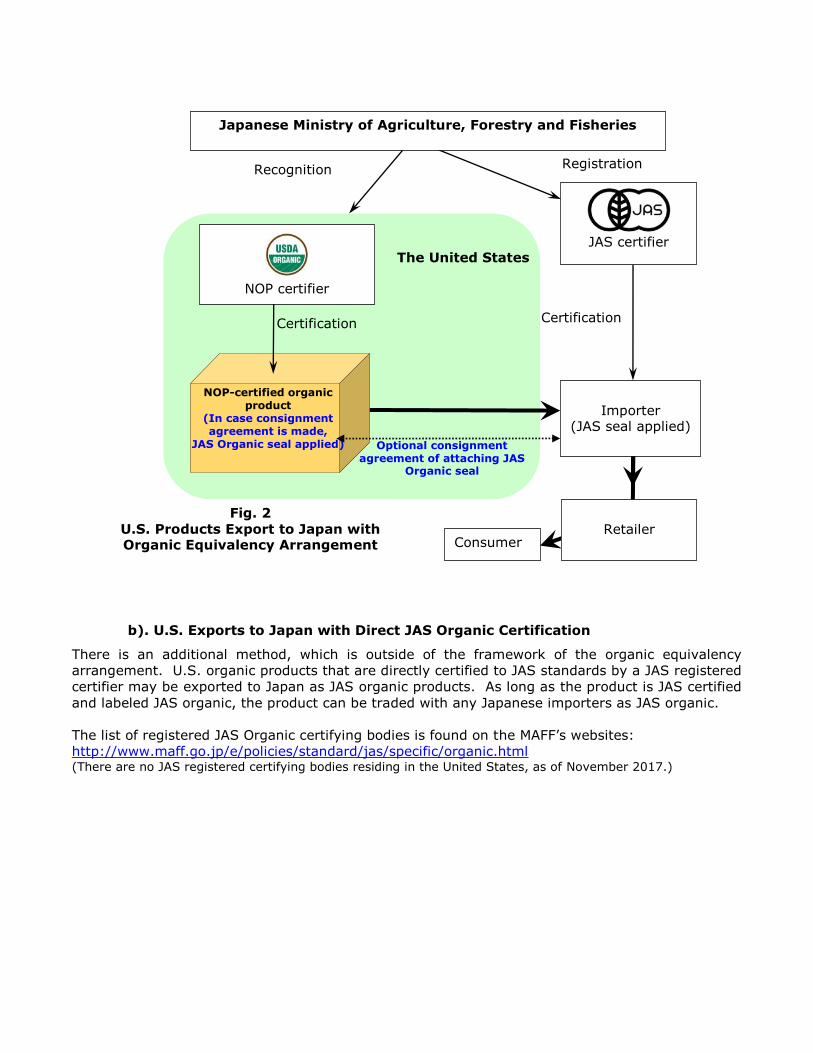

b). U.S. Exports to Japan with Direct JAS Organic Certification

There is an additional method, which is outside of the framework of the organic equivalency

arrangement. U.S. organic products that are directly certified to JAS standards by a JAS registered

certifier may be exported to Japan as JAS organic products. As long as the product is JAS certified

and labeled JAS organic, the product can be traded with any Japanese importers as JAS organic.

The list of registered JAS Organic certifying bodies is found on the MAFF’s websites:

http://www.maff.go.jp/e/policies/standard/jas/specific/organic.html (There are no JAS registered certifying bodies residing in the United States, as of November 2017.)

Importer (JAS seal applied)

JAS certifier

The United States

Recognition

NOP-certified organic product

(In case consignment agreement is made,

JAS Organic seal applied)

Certification

NOP certifier

Registration

Japanese Ministry of Agriculture, Forestry and Fisheries

Certification

Consumer

Retailer

Optional consignment agreement of attaching JAS

Organic seal

Fig. 2

U.S. Products Export to Japan with Organic Equivalency Arrangement