104

Competitive Brazil Challenges and strategies for the manufacturing industry

| Date post: | 16-Jul-2015 |

| Category: |

Documents |

| Upload: | dr-lendy-spires |

| View: | 128 times |

| Download: | 1 times |

Competitive Brazil Challenges and strategies for the manufacturing industry

I I

I I I

IV

Competitive Brazil Challenges and strategies for the manufacturing industry

•• The statistics mentioned in this book reflect the latest available information at the closing of this publication. The disclosure of data by the press or any other market sources updating the statistics exposed herein does not annul the informative purpose of this material, which is to analyze the changes and essential trends established and developed throughout the years, despite one-off changes or shortterm economic and business cycles.

•• The contents of articles written by the guest authors in this collection do not necessarily reflect the opinion of Deloitte.

•• All rights reserved to Deloitte. No parts of this book may be reproduced, including citations of information, except if prior authorization from Deloitte and guest authors, upon request, is granted in writing and commitment to source credit is binding.

Affiliated to the BrazilianAssociation for BusinessCommunication (ABERJE)

Contact for readers: [email protected]

About DeloitteDeloitte provides services in audit, consulting, tax avisory, corporate finance, outsourcing, to clients spanning multiple industries. With a global network of member firms in more than 150 countries, Deloitte brings world class capabilities and deep local expertise to help clients succeed the best performance, wherever they operate. Deloitte’s 186,000 professionals are committed to becoming the standard of excellence and they are unified by a collaborative culture that fosters integrity, outstanding value to markets and clients, commitment to each other, and strength from diversity. Deloitte has been in Brazil since 1911. Nowadays, the Firm is one of the market leaders and its over 4,500 professionals are recognized by integrity, competence and capability to turn their knowledge out in the best solutions for their clients. Deloitte’s operations cover throughout the Brazilian territory, with offices in São Paulo, Belo Horizonte, Brasília, Campinas, Curitiba, Fortaleza, Joinville, Porto Alegre, Rio de Janeiro, Recife and Salvador.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

© 2012 Deloitte Touche Tohmatsu. All rights reserved.

Project directionJosé Othon Tavares de Almeida

Editorial boardJuarez Lopes de AraújoAltair RossatoHeloisa Helena MontesJosé Othon Tavares de Almeida

Editorial coordinationRenato de Souza (Mtb 26.563)

EditionJulio Meneghini (Mtb 52.308)

Editorial productionSthefani Tironi (Mtb 43.533)

Graphic production and image selectionElisa PaulilloOtavio Sarsano

Production supportEster RossiKarina SousaLi Ying Yu

Promotion supportAndrea BragaDébora CostaNadia Ikeda

Further economics informationFernando RuizGiovanni CordeiroGabriel Nickolas Cazotto

ProofreadingMiriam Moreira SoaresSonia Hagemann

English versionUnitrad – Profissionais em tradução

LayoutMare Magnum

PhotographsWalter Craveiro (project official photographer)Bruno Carvalho (Eduardo Raffaini)Izilda França (Pedro Suarez) Régis Filho (Carlos Fadigas)

Collaboration (pictures)FiatMonsanto

PressIntergraf Ind. Gráfica Ltda.

Print run2,500 copies in Portuguese version500 copies in English version

Collaborating companies and entitiesAlstom BrazilBASF Braskem CNI Cummins BrazilDow EcoverdiFiat/Chrysler GM BrazilICC BrazilJacto Monsanto BrazilPositivo Rhodia Sanofi Group Brazil

The manufacturing industry in Brazil attracts both companies and investors from all over the world, particularly at this historical time of our development. More than ever, our country is a market of great opportunities. No multinational industry today can afford to ignore Brazil in its strategies of growth for the next years.

Nevertheless, domestic industry experiences today a series of major challenges as a result of both foreign competition and historical internal restraints. Deloitte believes that to meet these challenges, it is necessary to understand them deeply.

This collection of articles organized with contributions from some of the main executives in this market offers us a panoramic view of these exciting, stimulating and complex times we are experiencing, and that helps us to build new paths.

Starting its second century of operation in Brazil in 2012, Deloitte has a privileged vision to help business leaders define the most appropriate strategies to compete and prosper in the country.

We wish everyone an enjoyable read.

Juarez Lopes de AraújoPresident of Deloitte – Brazil

New paths for national industry

“Domestic industry experiences today a series of major challenges as a result of both foreign competition and historical internal restraints.Deloitte believes that to meet these challenges, it is necessary to understand them deeply.”

Guest authors

José Othon Tavares de AlmeidaDeloitte leader in Brazil for manufacturing industry

André DiasPresident of Monsanto Brazil

Deloitte•–•local•and•global•leadership

Craig Giffi Consumer and industrial products leader, Deloitte United States (Deloitte LLP)

André Luis RodriguesFormer Chief Financial Officer (CFO) of Rhodia and presently Financial Officer of JHSF

Alfred HackenbergerPresident of BASF for South America

Carlos FadigasPresident of Braskem

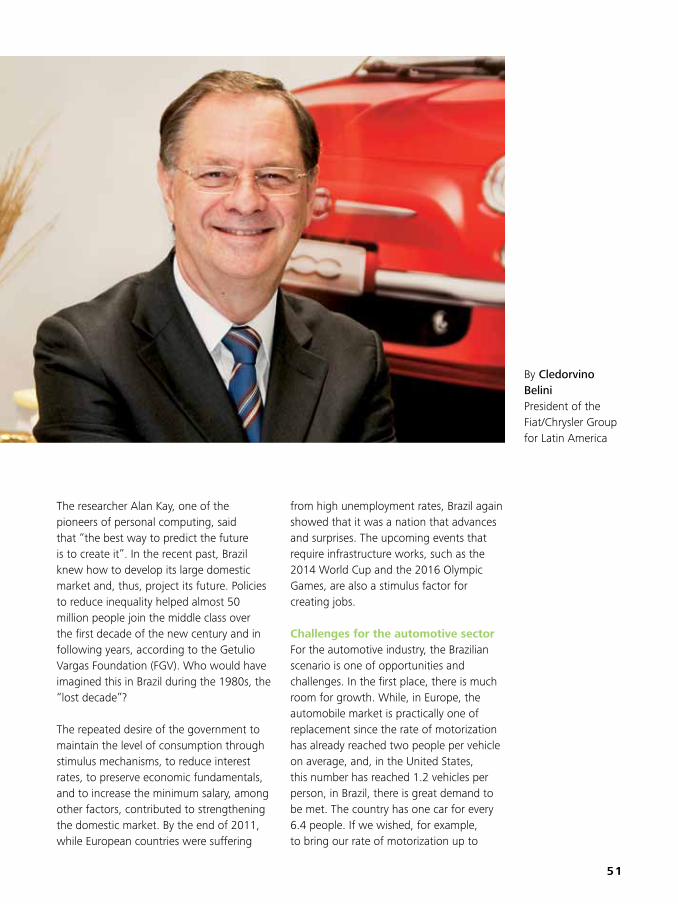

Cledorvino Belini President of the Fiat/Chrysler Group for Latin America

Hélio Bruck RotenbergCEO of Positivo Informática

Heraldo MarcheziniGeneral director of Sanofi Group – Brazil

José Augusto Coelho FernandesExecutive director of the National Confederation of Industry (CNI)

Joe VitaleGlobal automotive sector leader, Deloitte Touche Tohmatsu Limited (DTTL)

Eduardo Tavares RaffainiDeloitte leader in Brazil for mining segment

Luc BurtonFormer Chief Financial Officer (CFO) of Alstom Brazil and presently Financial Officer of Puma Energy

Luiz Eduardo TalibertiCEO of the Ecoverdi Group

Marcos da Cunha RibeiroAdministrative director of the Jacto Group

Sandra MarianiFormer CFO of GM Brazil

Tadashi YamashitaLatin America treasury director for Cummins Brazil

Pedro SuarezPresident of Dow for Latin America

Marcelo Drügg Barreto ViannaVice president of the International Chamber of Commerce (ICC Brazil)

Douglas Nogueira LopesPartner of Deloitte Brazil’s Tax area

Deloitte•–•industry•and•business•expertise

6

For a greater BrazilOvercoming the current challenges of the manufacturing industry in the country will require a broad pact of all market agents. Initiatives such as the “Bigger Brazil Plan” signal some alternatives and invite us to build joint solutions to benefit our competitiveness, with innovation and sustainability.

The manufacturing industry’s current agenda in Brazil reflects opportunities that result from the special position

the country has been gaining in the international scenario. With one of the largest and most dynamic domestic markets in the world, with solid economic fundamentals and a perspective of sustainable long-term expansion, it would be natural for Brazil to become one of the most important destinations attracting investment from multinational companies in the most diverse industries.

At the same time, however, our ever increasing intense connection with an economy that has reached unprecedented levels of globalization also has its troublesome side, which presents a number of large challenges for local

production activities. Recent sluggishness in the more mature economies and the rise of other emerging nations intensify the competition Brazilian companies face, making their operation within and outside our market difficult. In addition, we are facing dilemmas that are now common to almost all countries, such as relative deceleration of industrial production, a reduced share of total generated wealth and, even, the risk of deindustrialization in important sectors.

Neither can we forget the historical obstacles that harm operation of national industry, such as the “Brazil Cost”, infrastructure deficiencies and low-skilled labor. Our industry’s current challenges lead to a simple question: how do we ensure conditions so that it can be competitive and sustainable in the new global reality?

Introduction

7

By José Othon Tavares de AlmeidaDeloitte leader in Brazil for manufacturing industry

Times of great challenges usually awaken the Brazilian people’s creativity and determination. This, more than ever, is a time to rethink models, reinvent practices and, primarily, for private initiative, the government and all of civil society to unite to promote the development of industry. All market agents need to unite around this pact.

The“Bigger Brazil Plan” (PBM in Portuguese), instituted by the federal government in 2011 and expanded in 2012 with the objective of stimulating the economy and, in particular, national industry, is one of the initiatives that today try to express the changes needed for the resumption of growth in the productive sectors. The participation of private initiative in the program, by means of representatives of the so-called Competitiveness Councils, legitimates its

purpose and offers the business community another way to position itself to face a situation that seriously affects its business. With the motto “innovate to compete; compete to grow”, the PBM, to the extent it is supported by modern Brazilian corporate leadership, has full conditions to generate practical results to benefit its own development.

Therefore, it is evident that to meet the complexity of our challenges, Brazil needs structural reforms in the most diverse fields. Tax exemptions, foreign trade stimulus, expansion of corporate credit, trade protection measures and incentives for significant sectors are some of the timely measures established by the PBM that need to be incorporated into the essence of a national development strategy. Today, Brazil has the responsibility to preserve and promote one of its most significant

8

Colonial•BrazilThe Portuguese metropolis used to prohibit the establishment of factories in the territory from 1500 to 1822.

economic frontiers: one of the largest and most diversified industrial parks in the world.

In the same way, it is up to the business community to continue its efforts to adopt better business practices and continuously foster innovation, within a social and economic environment increasingly based on the values of sustainability – of the planet, its relations with society and the business itself.

The collection of articles “Competitive Brazil – Challenges and strategies for the manufacturing industry” has the merit of comprehensively addressing a broad set of issues that characterize the dynamics of productive activity in the country. Deloitte, which with its clients daily builds solutions to address the challenges presented here, had the honor to put together in this book

End•of•the••19th•centuryIndustrial development begins in Brazil, with coffee growers starting to invest part of their profits to create factories of textiles, footwear and other manufactured goods.

The•decades•of•the•1930s•and•1940sIndustrialization gains strength during the Getúlio Vargas presidency, with protectionist measures, infrastructure investments and regulation of the labor market.

Periods and moments that mark the history of productive activity in Brazil

1956-1960The president Juscelino Kubitschek opens the economy to foreign capital, attracting multinational companies, and establishes measures to support local industry.

1962Electrobras is created during the João Goulart presidency, supporting the generation and distribution of electric power that significantly benefits some industrial sectors.

1969Embraer is created, raising the global status of Brazilian industry. Its first challenge was line production of the Bandeirante airplane.

A development trajectory

“Our industry’s current challenges lead to a simple question: how do we ensure conditions so that it can be competitive and sustainable in the new global reality?”

Sources: The National Confederation of Industry (CNI) and Deloitte (consolidation of public information)

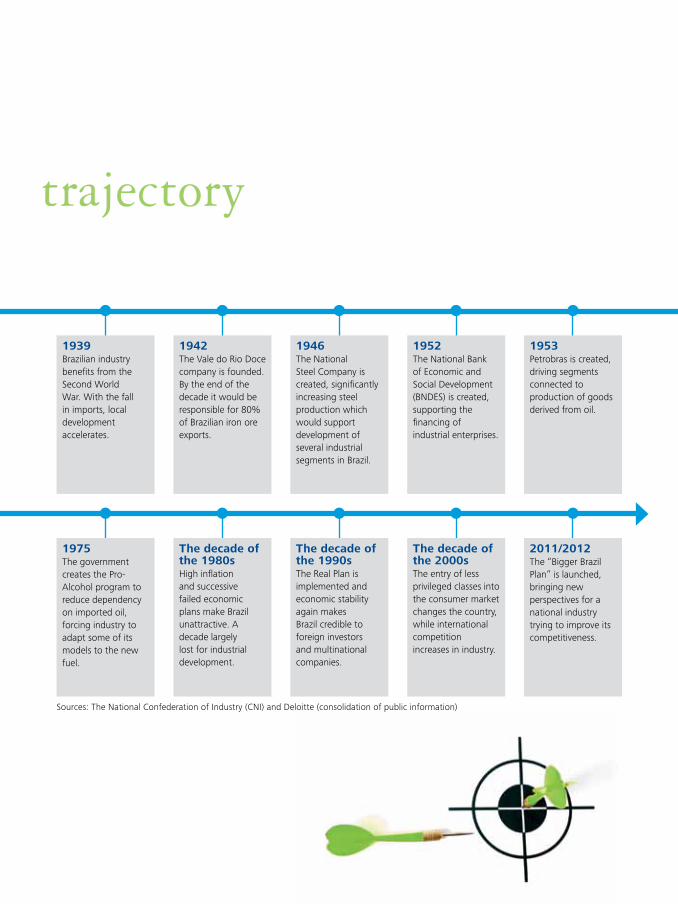

1939Brazilian industry benefits from the Second World War. With the fall in imports, local development accelerates.

1942The Vale do Rio Doce company is founded. By the end of the decade it would be responsible for 80% of Brazilian iron ore exports.

1946The National Steel Company is created, significantly increasing steel production which would support development of several industrial segments in Brazil.

1952The National Bank of Economic and Social Development (BNDES) is created, supporting the financing of industrial enterprises.

1953Petrobras is created, driving segments connected to production of goods derived from oil.

1975The government creates the Pro-Alcohol program to reduce dependency on imported oil, forcing industry to adapt some of its models to the new fuel.

The•decade•of•the•1980sHigh inflation and successive failed economic plans make Brazil unattractive. A decade largely lost for industrial development.

The•decade•of•the•1990sThe Real Plan is implemented and economic stability again makes Brazil credible to foreign investors and multinational companies.

The•decade•of•the•2000sThe entry of less privileged classes into the consumer market changes the country, while international competition increases in industry.

2011/2012The “Bigger Brazil Plan” is launched, bringing new perspectives for a national industry trying to improve its competitiveness.

A development trajectory

10

a group of exceptional business leaders and experts around the major issues that impact Brazilian industry today.

The articles presented in this publication are grouped around two large areas: the first, emphasizes competitiveness, examining the country’s historical dilemmas and current

“The collection of articles ‘Competitive Brazil – Challenges and strategies for the manufacturing industry’ has the merit of comprehensively addressing a broad set of issues that characterize the dynamics of productive activity in the country.”

opportunities; and the second, addresses the issues of innovation and sustainability, taking into account the role of industry in the construction of new development models. From the views expressed here, the reader can tap into reflections at the highest level to help in developing strategies to benefit Brazilian industry.

11

The challenges faced by global manufacturers have no boundaries. Global economic uncertainty has become the new normal. Resource scarcity, new patterns of consumption, climate change, new patterns of mobility, and the convergence of new technologies are among the global megatrends reshaping the global manufacturing industry landscape.

These megatrends and challenges at the same time also provide opportunities for manufacturers. Staying competitive is about not being afraid to reinvent your company to adapt to new situations. Leading manufacturers achieve profitable growth by driving excellence in areas such as product development. They also harness the power of collaborative innovation and master the art of managing the complexities of their global value chain.

We hope that you enjoy this special collection of articles organized by Deloitte. The articles offer valuable insights on what it takes to compete in Brazil and how manufacturers can be successful in an ever-evolving global landscape.

Tim HanleyGlobal Leader, ManufacturingDeloitte Touche Tohmatsu Limited (DTTL)

Competing in an evolving landscape

12

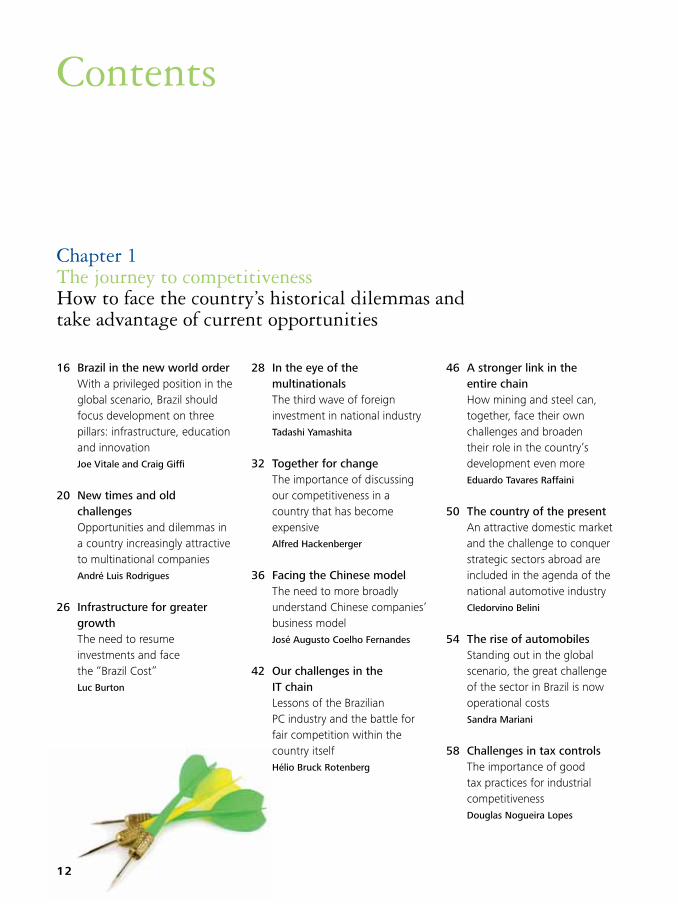

Contents

16 Brazil in the new world orderWith a privileged position in the global scenario, Brazil should focus development on three pillars: infrastructure, education and innovationJoe Vitale and Craig Giffi

20 New times and old challengesOpportunities and dilemmas in a country increasingly attractive to multinational companiesAndré Luis Rodrigues

26 Infrastructure for greater growthThe need to resume investments and face the “Brazil Cost”Luc Burton

28 In the eye of the multinationalsThe third wave of foreign investment in national industry Tadashi Yamashita

32 Together for changeThe importance of discussing our competitiveness in a country that has become expensiveAlfred Hackenberger

36 Facing the Chinese modelThe need to more broadly understand Chinese companies’ business model José Augusto Coelho Fernandes

42 Our challenges in the IT chainLessons of the Brazilian PC industry and the battle for fair competition within the country itselfHélio Bruck Rotenberg

46 A stronger link in the entire chainHow mining and steel can, together, face their own challenges and broaden their role in the country’s development even more Eduardo Tavares Raffaini

50 The country of the presentAn attractive domestic market and the challenge to conquer strategic sectors abroad are included in the agenda of the national automotive industryCledorvino Belini

54 The rise of automobilesStanding out in the global scenario, the great challenge of the sector in Brazil is now operational costsSandra Mariani

58 Challenges in tax controls The importance of good tax practices for industrial competitivenessDouglas Nogueira Lopes

Chapter 1The journey to competitivenessHow to face the country’s historical dilemmas and take advantage of current opportunities

13

64 Limits and expectationsNew needs awaken a transformation in the essence of industry in the worldLuiz Eduardo Taliberti

68 Produce and conserve more Technology as a fundamental ally in the search for efficiency and sustainable practicesAndré Dias

72 Part of the solutionInnovation and collaboration as determinants of sustainable development of businessCarlos Fadigas

76 The role of life’s industryDialogue with stakeholders and the strengthening of corporative responsibility as essential for social and economic growthHeraldo Marchezini

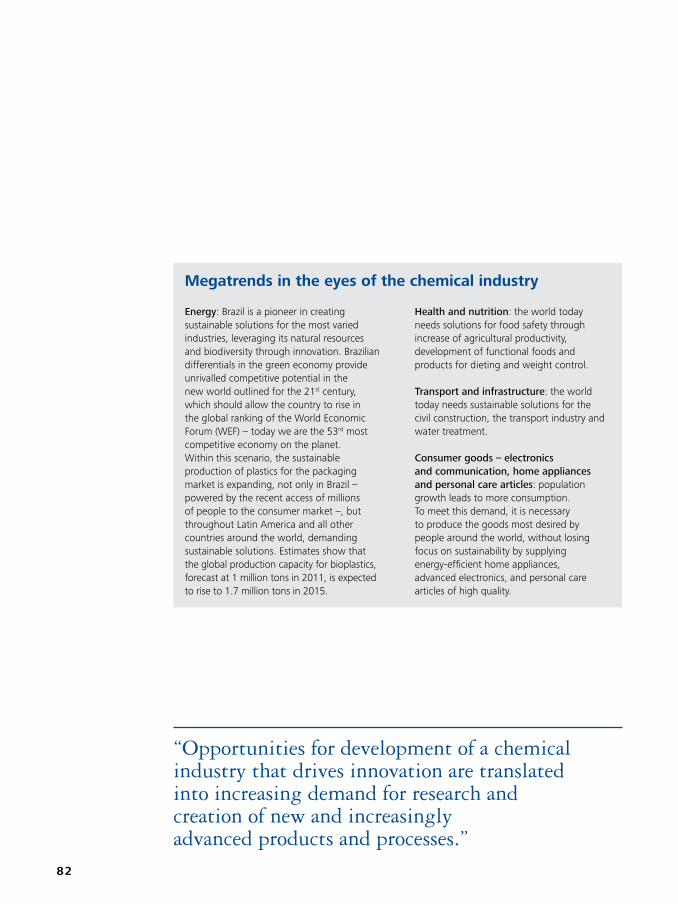

80 The chemistry of innovationThe importance of the chemical industry for innovation and progress based on principles of sustainabilityPedro Suarez

84 Construction of a new futureAdoption of innovative and sustainable practices to influence operational and strategic business models Marcos da Cunha Ribeiro

90 Sustainability and social responsibilityNew challenges in managing the integration of organizational systems in search of industrial competitivenessMarcelo Drügg Barreto Vianna

Chapter 2For an innovative and sustainable futureThe role of the industry in a new model of development

14

“Brazil Cost” • Infrastructure • Multinational presence • Manpower qualification • Foreign competition • Impacts of China • Internationalization • “Bigger Brazil Plan” • Cost management • Tax management • Basic industry

The journey to competitivenessHow to face the country’s historical dilemmas and take advantage of current opportunities

Chapter 1

16

Brazil in the new world order

As a rising competitor, the country today has a strong position in the global scenario. To achieve its competitive potential viable in the new world order of the industry, Brazil needs to broaden its focus on the development of physical infrastructure and education, in addition to encouraging innovation.

For several years, Deloitte has collaborated with a number of organizations committed to manufacturing competitiveness at both a country and

international level. This past year, Deloitte served as Project Advisor to the World Economic Forum (the Forum) on a “Future of Manufacturing” project chartered to generate insights and a platform for informed dialogue between senior business leaders and policymakers about the pivotal drivers of change in the industry, today and in the future. Following the anticipated release of the Future of Manufacturing report in April 2012, the Forum with Deloitte will embark on the next phase of research on the topic of Manufacturing for Growth. The project is expected to provide CEO insights on how manufacturers are driving economic growth worldwide. Highlighting some of the perspectives from

these projects, this article provides a brief look at Brazil’s potential in a new world order of manufacturing competitiveness.

The manufacturing industry plays a vital role in the economic health of every country and has become increasingly more dynamic and competitive globally. As a resource rich nation with an attractive market for investment, Brazil has an opportunity to significantly increase its global manufacturing competitiveness by focusing efforts on developing the nation’s physical infrastructure and education system. Despite slowing growth figures, Brazil is seen as a strong competitor globally and is in a great position to create sustainable growth and prosperity.

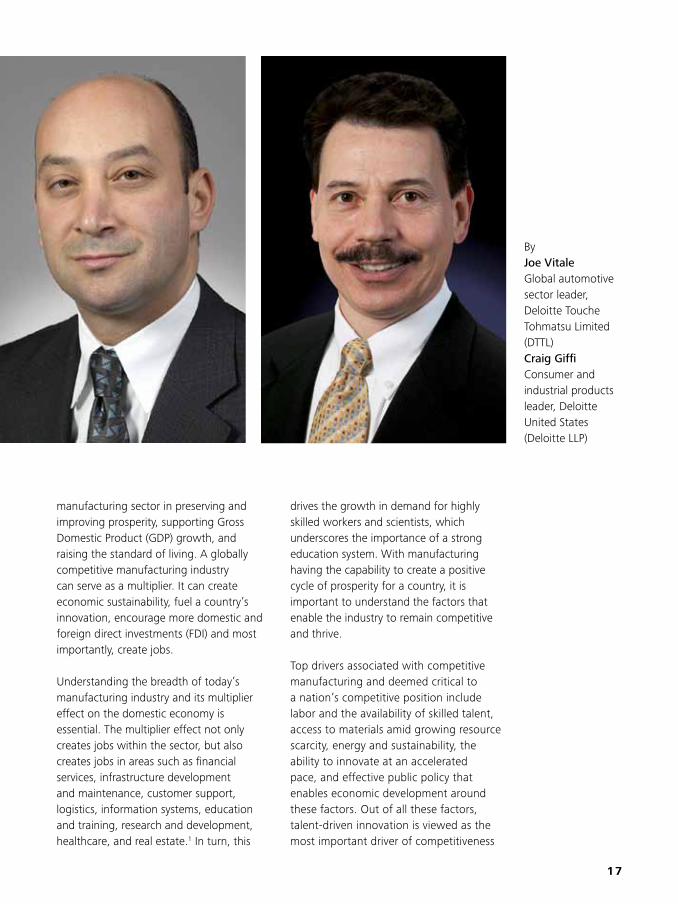

Manufacturing•as•a•multiplierThe recent global economic downturn revealed the true value of the

17

manufacturing sector in preserving and improving prosperity, supporting Gross Domestic Product (GDP) growth, and raising the standard of living. A globally competitive manufacturing industry can serve as a multiplier. It can create economic sustainability, fuel a country’s innovation, encourage more domestic and foreign direct investments (FDI) and most importantly, create jobs.

Understanding the breadth of today’s manufacturing industry and its multiplier effect on the domestic economy is essential. The multiplier effect not only creates jobs within the sector, but also creates jobs in areas such as financial services, infrastructure development and maintenance, customer support, logistics, information systems, education and training, research and development, healthcare, and real estate.1 In turn, this

drives the growth in demand for highly skilled workers and scientists, which underscores the importance of a strong education system. With manufacturing having the capability to create a positive cycle of prosperity for a country, it is important to understand the factors that enable the industry to remain competitive and thrive.

Top drivers associated with competitive manufacturing and deemed critical to a nation’s competitive position include labor and the availability of skilled talent, access to materials amid growing resource scarcity, energy and sustainability, the ability to innovate at an accelerated pace, and effective public policy that enables economic development around these factors. Out of all these factors, talent-driven innovation is viewed as the most important driver of competitiveness

By Joe VitaleGlobal automotive sector leader, Deloitte Touche Tohmatsu Limited (DTTL) Craig Giffi Consumer and industrial products leader, Deloitte United States (Deloitte LLP)

18

Brazil’s•manufacturing•competitiveness•Three factors are likely to influence Brazil’s manufacturing industry competitiveness over the next several years1:

Physical infrastructure: the productivity of an industry in any country is directly related to the quality of its physical infrastructure for commerce. Reliable and efficient physical infrastructure such as roads, ports, electricity grids, and telecommunication networks play a vital role in logistics, moving raw materials and finished products on time and with minimum costs. Investing in effective infrastructure is essential. As host to the World Cup in 2014 and the Olympics in 2016, Brazil is expected to improve infrastructure and bring in foreign investment, which will likely also have a positive influence on improving the country’s manufacturing industry and competitive position.

Talent: the need to rapidly innovate and develop new products and processes has led to a growing skills gap. Shortages in skilled production jobs are taking their toll on manufacturers’ ability to expand operations, drive innovation, and improve productivity.3 In order for Brazil to sustain its competitive position and create a positive cycle of prosperity, the country will be as challenged as other nations to be a global leader in attracting, developing and retaining top science and engineering talent to drive world-class innovation, research and development, and close the skills gap.

Energy costs: clean, reliable energy directly influences production costs and is an increasingly important factor in determining global manufacturing competitiveness. Fortunately, Brazil is one of the few countries with a sufficiently large natural resource base coupled with a relatively advanced research infrastructure. This places the country in a unique position to capture more profitable stages of the value chain through alternative energies that are ecologically sustainable.

and is top-of-mind with manufacturing executives across the world.1

Talent-driven innovation comprises both the quality and availability of a country’s brain trust. This includes its skilled workers, such as scientists, researchers, engineers, and teachers, who collectively have the capacity to continuously innovate and, simultaneously, improve production efficiency. Talent has been described as both the key differentiator of a country’s competitive

edge in the 20th century and the most critical determinant of success in the 21st century.2

Competitive•positionBrazil continues to be viewed by manufacturing executives as a rising contender in the global manufacturing competitiveness race. Not unexpectedly, Asian giants like China, India, and the Republic of Korea are projected to dominate the scene over the next few years, out-positioning dominant

19

manufacturing super powers of the late 20th century – the United States (U.S.), Japan, and Germany.

In order to remain competitive, Brazil will need to carefully navigate its position on foreign trade, exchange controls, and investments. Brazil’s pursuit of an industrialization policy centered on replacing imported manufactured products with domestically produced goods has yielded a highly diversified manufacturing sector.1 Although export promotion remains a policy priority, the current account deficit is expected to rise to an annual average of 4.0 percent in 2012 to 2016 as import growth exceeds that of exports.4 Concerns over a surge of Chinese imports has already led to some non-tariff barriers and protectionist measures particularly in the automotive and light manufacturing sectors.

With tax incentives for foreign and domestic investors, Brazil proves to be an attractive market for companies considering the country as an export base. Many manufacturers have already announced plans to expand operations, including Asian manufacturing newcomers who are installing facilities and/or distribution network channels in Brazil. An increase in foreign direct investment will likely create greater domestic competition and encourage government policy modifications to positively influence the state of Brazil’s manufacturing competitiveness.

The global manufacturing landscape continues to evolve and with this comes a shift in the drivers that enable manufacturers and nations to remain globally competitive. In less than a decade, a new world order for manufacturing competitiveness has emerged. Countries are placing greater emphasis on creating manufacturing- based economies that produce higher-value jobs, leveraging the multiplier effect, and rapidly growing their economic middle classes.3 As a rising global contender, Brazil has several factors that support a strong manufacturing competitive position. Building on the nation’s strengths while continuing to focus on developing physical infrastructure and education will enable Brazil to sustain manufacturing competitiveness and prosperity.

“As a resource rich nation with an attractive market for investment, Brazil has an opportunity to significantly increase its global manufacturing competitiveness by focusing efforts on developing the nation’s physical infrastructure and education system.”

1 “Global Manufacturing Competitiveness Index” (Deloitte Touche Tohmatsu Limited and the U.S. Council on Competitiveness, June 2010)2 “Ignite 2.0: Voices of American University Presidents and National Lab Directors on Manufacturing Competitiveness” (Deloitte Touche Tohmatsu Limited and the U.S. Council on Competitiveness, July 2011)3 “Boiling point? The skills gap in U.S. manufacturing” (Deloitte United States – Deloitte Consulting LLP – and the Manufacturing Institute, October 2011) 4 Economist Intelligence Unit (www.eiu.com)

20

Since the term “emerging country” was defined, it has been associated with the word “opportunity”. It wasn’t long before a new acronym, BRIC1,

was created to designate the main players included in the group at the beginning: Brazil, Russia, India and China. Any novelty is bound to draw attention. From that point on, many companies and investors started a new adventure towards a future of enormous possibilities offered by each of these economies.

After working for a multinational operating in Brazil for 93 years, it was not difficult to sell our country during this exhilarating time. No one remembers any longer some words of the past that posed true ordeals for both Brazilian executives and foreign entrepreneurs, such as “hyperinflation” or “lost decade.”

New times and old challenges

Brazil offers great opportunities to multinational corporations today. Predictability, social mobility and cultural qualities justify the attractiveness. Some dilemmas, however, if not faced in time, may puzzle those that see us from outside.

The prognosis that this nation would someday be successful has proven true. The feeling that the right time and moment have arrived is a fact. Certainly, some investors on other continents regret not having believed that the prophecy would come true, since even with difficulties and complexities in the business environment, our future is quite different from the past.

Multinational•strategiesWhy Brazil should have already been, and today is and will definitely continue to be strategic for foreign multinationals? Being the sixth economy in the world, in and of itself, already makes this a country that deserves to be included, in a detailed way, in any strategic plan of successful enterprises. A new rhythm has started some years ago and we have perhaps arrived at the best economic moment of our history.

21

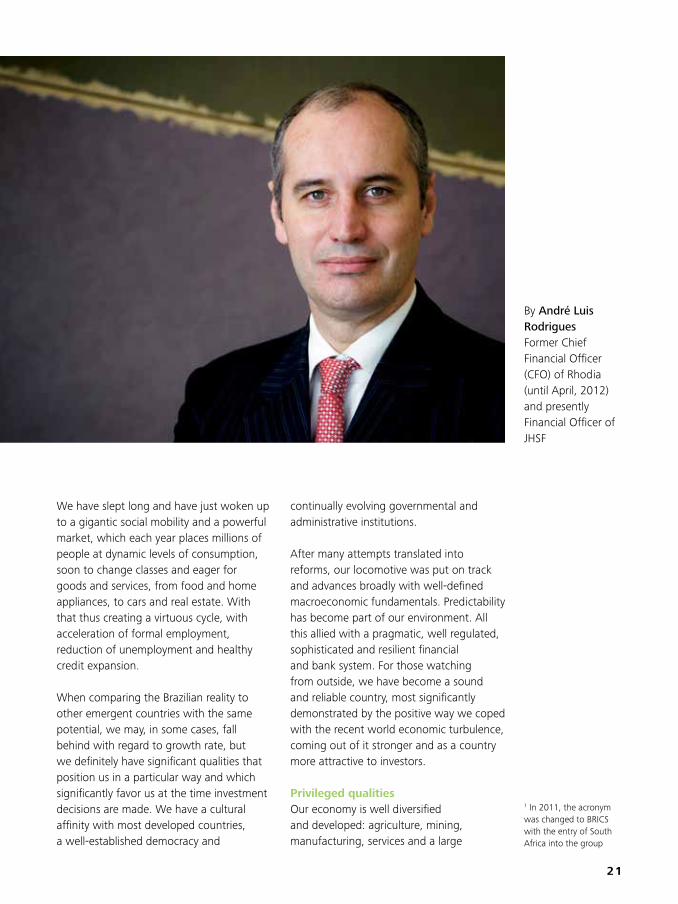

By André Luis RodriguesFormer Chief Financial Officer (CFO) of Rhodia (until April, 2012) and presently Financial Officer of JHSF

We have slept long and have just woken up to a gigantic social mobility and a powerful market, which each year places millions of people at dynamic levels of consumption, soon to change classes and eager for goods and services, from food and home appliances, to cars and real estate. With that thus creating a virtuous cycle, with acceleration of formal employment, reduction of unemployment and healthy credit expansion.

When comparing the Brazilian reality to other emergent countries with the same potential, we may, in some cases, fall behind with regard to growth rate, but we definitely have significant qualities that position us in a particular way and which significantly favor us at the time investment decisions are made. We have a cultural affinity with most developed countries, a well-established democracy and

continually evolving governmental and administrative institutions.

After many attempts translated into reforms, our locomotive was put on track and advances broadly with well-defined macroeconomic fundamentals. Predictability has become part of our environment. All this allied with a pragmatic, well regulated, sophisticated and resilient financial and bank system. For those watching from outside, we have become a sound and reliable country, most significantly demonstrated by the positive way we coped with the recent world economic turbulence, coming out of it stronger and as a country more attractive to investors.

Privileged•qualitiesOur economy is well diversified and developed: agriculture, mining, manufacturing, services and a large

1 In 2011, the acronym was changed to BRICS with the entry of South Africa into the group

22

industrial base. Brazil produces all that emerging nations need to grow. With the exportation of these products and the possibility to import what, in most of cases, the developed countries produce at low prices, our trade balance is attractive.

Our supply chain is also very privileged, due to our massive energy reserves, particularly those from renewable sources and minerals. We are practically self-sufficient in oil and world leaders in the development and production of biofuels. That is, sustainable development is a priority for any serious company and, in Brazil, we have countless conditions to develop these opportunities.

Equally, a multinational company is also attracted by the cultural qualities of our people. Brazilians have a strong enterprising spirit, are creative and skilled at working in teams – key components for innovation. They are open minded and can rapidly make changes, precisely correcting course when necessary, besides being strong as a result of the mixture of races and cultures, which creates an environment of respect for opinions, religions and beliefs.

In a country where it is possible to find the main global business megatrends, it is also possible to try all the growth processes: organic, given our economy’s growth rate; through innovation, given the rich raw materials base and trained teams; and through acquisitions, due to

23

“After many attempts, translated into reforms, our locomotive was put on track and advances broadly with well-defined macroeconomic fundamentals. Predictability has become part of our environment. All this, allied with a pragmatic, well regulated, sophisticated and resilient financial and bank system.”

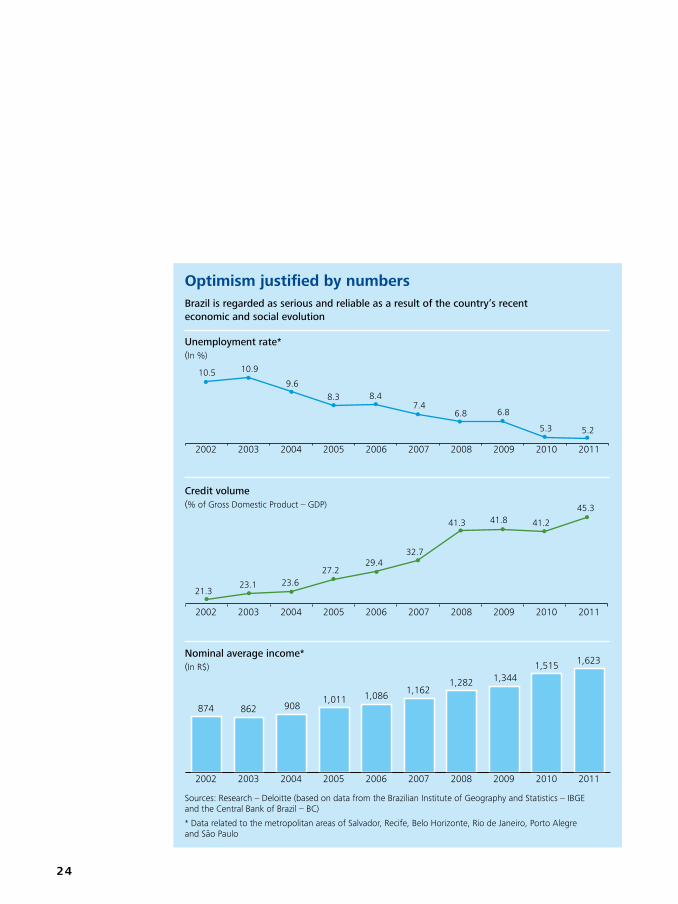

the varied conditions for consolidation of some sectors and other opportunities. The exploitation of oil in the pre-salt layer, the World Cup in 2014, the Rio de Janeiro Olympic Games in 2016, as well as important energy generation projects, already represent billions in investment and ensure continuity in the development of our economy.

To•compete•head-to-head•Since there is no easy competition, we face some challenges that may reduce our speed and raise some questions for those looking from outside. Our infrastructure, in some cases, is somewhat precarious, with a high number of blackouts in some regions, conservation of public highways far below that of private ones, airports that cannot handle the increasing number of passengers, and an incipient metro and railroad network, when compared to developed countries.

In the education field, we are unable to cover the demand for professionals that the expanding economy requires. Our education level is still lower than that of the majority of the emerging competition and, even with advancement in some of the rankings, we graduate doctors at a rate five times lower than developed countries, and we are still in the 24th position in volume of patents registered, according to the most recent findings available on these topics.

Actions are being taken and the solutions will come with time. Consequently, more companies will be attracted by these opportunities. What may really dissuade foreign companies are the factors that place us in a difficult competitive situation. We came in at a poor 53rd in the ranking of 142 countries released by the World Economic Forum in 2011. What is remarkable is the excessive bureaucracy in our business

24

21.323.1 23.6

27.229.4

32.7

41.3 41.8 41.2

45.3

Credit volume(% of Gross Domestic Product – GDP)

Sources: Research – Deloitte (based on data from the Brazilian Institute of Geography and Statistics – IBGE and the Central Bank of Brazil – BC)

* Data related to the metropolitan areas of Salvador, Recife, Belo Horizonte, Rio de Janeiro, Porto Alegre and São Paulo

Optimism•justified•by•numbersBrazil is regarded as serious and reliable as a result of the country’s recent economic and social evolution

10.5 10.9

9.68.3 8.4

7.46.8 6.8

5.3 5.2

Unemployment rate* (In %)

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Nominal average income*(In R$)

874 862 9081,011 1,086 1,162

1,282 1,3441,515 1,623

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

25

“Actions are being taken and the solutions will come with time. Consequently, more companies will be attracted by these opportunities. What may really dissuade foreign companies are the factors that place us in a difficult competitive situation.”

environment, an inefficient and complex system, with close to one hundred taxes, resulting in a very high tax proportion in relation to company profits. The two issues make it difficult for private initiative to decide to play a role in solving these dilemmas.

We cannot miss the opportunity available at this time. To ensure a successful future, it is now time to have a State program addressed to the bottlenecks that undermine our competitiveness, having in mind that, if with so many difficulties we were able to attract the largest companies in the world, with implementation of the reforms already understood as necessary, Brazil would soon occupy a better position among the largest world economies.

26

Infrastructure for greater growth

To realize its potential for economic expansion, the country needs to confront its “Brazil Cost” and invest strongly in infrastructure, ensuring the global competitiveness of its domestic industry.

The last 60 years of Alstom’s and Brazil’s shared history are witness to a stable and mutually beneficial collaboration. Alstom has

been active – and continues to be – in all the large Brazilian projects, bringing the country innovative and cutting-edge technology in the energy and transportation sectors. Its financial partners – French and those of other countries – contribute equally to make a large number of these projects possible. During this process, Alstom has learned much from its activity in Brazil and has a clear vision of what the country strategically represents today.

Brazil is an important country today whose weight should grow. This trend is strengthened by the growth potential of the so-called “emerging” countries. In addition, due to its cultural characteristics – openness

to new initiatives, a dynamics of sustainable implementation and creativity – Brazil should increasingly confirm its role as a “laboratory of good practices,” whether of a technical or managerial nature.

The country’s growth path is wide and the infrastructure area is one of the great drivers of this expansion. We are experiencing a decisive moment in this environment and the investment possibilities are limitless. The infrastructure bottlenecks must be overcome so that we can reach all the potential of a country of continental dimensions. The economy is growing and Brazil is becoming a power of the 21st century, attracting direct investment and intensifying local sales.

Invest•to•competeThis picture is only clouded by the “Brazil Cost”, this set of obstacles of a fiscal, legal,

27

financial and logistic nature that undermines the competitiveness of Brazilian companies, as well as, certainly, the competitiveness of the entire domestic market in relation to the ability of importers and exporters to deal with international competition.

Therefore, even more investment in local industry is needed in order to create significant turnover in the domestic economy. It is important to recognize that attracting new technologies or importing solutions is not enough. Increasing investment is needed to generate jobs, income and demand.

We have a wealth of natural resources and growing manpower. With the correct public and private initiatives it is possible to guarantee the high expectations placed on us, and infrastructure is an essential aspect of the development of all this potential.

By Luc BurtonFormer Chief Financial Officer (CFO) of Alstom Brazil and presently Financial Officer of Puma Energy

Investment•lower•than•growthReturning to the 1970s levels of investment in infrastructure is essential to lowering the “Brazil Cost” for companies that operate in the country.

0

1

2

3

4

5

6

1970 1980 1990

Water and sanitation Telecommunications Transportation Electricity

Investments in large areas of infrastructure made in recent decades (% of GDP)

Sources: consolidated using numbers from the World Bank, the Institute of Applied Economic Research (IPEA) and the National Bank of Social and Economic Develop-ment (BNDES)

2000

28

In the eye of the multinationals

The growth of direct foreign investment entering Brazil shows its significance in the revenues generated by subsidiaries established in the country. In its third major wave of attracting international capital at the moment, the country should make efforts to gradually reduce the “Brazil Cost”.

The first wave of foreign investment in Brazil occurred during President Juscelino Kubitschek’s Financial Plan in the second half of

the 1950s, led primarily by companies in the automotive sector. At the time, multinational subsidiaries established in Brazil represented little in the global sales and profits of their companies.

Cummins, the largest independent manufacturer of diesel engines in the world, entered the country at that time through an independent distributor. The first factory was launched in 1971 attracted by the low-cost labor and abundance of raw material. Its production was directed basically to the foreign market. It was during the 1980s that the company’s business took form, driven by tax incentives such as the Befiex Program through which export companies

were immediately credited 14% of their transactions value. It was an incentive that could not be passed up. With it, Brazil significantly raised its exports, contributing to the trade balance.

The end of the Befiex Program in 1989 caused companies to turn back to the domestic market, gradually reducing exports and increasing domestic sales. In the first years of the 1990s, despite the opening of markets by the Collor administration, foreign capital continued to arrive as Foreign Direct Investment (FDI), however, at a historical average of around US$ 2 billion per year (current value), according to Brazilian Central Bank sources..

Many foreign companies were hesitant to making large investments in the country, mainly as a result of the high inflation level, which reached 3% per day at the

29

time. The inflationary environment and the exchange rate volatility kept many businessmen and financial executives up at night, spending hours on end reasoning on how to explain their effects on the subsidiaries’ results. Many of them prepared feasibility studies to decide whether to stay in the country. It was then that multinationals started to invest heavily in systems of total quality, employing tools unknown at the time in the country, such as Kaizen, the Total Quality System, and the Failure Model and Effect Analysis (FMEA), among others.

The second wave of foreign investments, from my perspective, occurred at the end of the 1990s, more precisely in 1997, with Foreign Direct Investment (FDI) reaching US$ 18.9 billion. With the maxi-devaluation of the real during this period, foreign investments surpassed US$ 30 billion.

By Tadashi YamashitaLatin America treasury director for Cummins Brazil

With a devalued exchange rate, there was an opportunity to raise international capital to increase investments in Brazil. Privatization of companies in the energy and telecommunications sectors also attracted new interest. However, although the exchange rate favored investment, uncertainties caused at the time by the 2002 presidential election ended up driving away foreign investors and significantly reducing FDI from 2001 on.

With the continuation of the prior administration’s economic policy and the promotion of political stability by president Luiz Inácio Lula da Silva, foreign multinationals and investors saw that the new administration was not the threat that had been imagined before the elections and they resumed investment in the country. Starting in 2004, multinational companies also began to consolidate their operations

30

in Brazil. Many of them made the country their regional headquarters for Latin America.

Modern•practicesIn addition to these facts, still at the end of the 1990s, many multinational companies brought their model of quality management, known as Six Sigma, to Brazil. Its concept is the reduction of variations in the process, increasing productivity and raising companies’ profits. All the companies that adopted the model were successful, both in the

international and domestic environments. Another important fact worth mentioning is that the products manufactured in Brazil started to strictly follow the international quality standards practiced by their parent companies. In addition, the companies modernized their industrial parks, globalizing products and using cutting-edge technology. With the globalization of products, the Brazilian subsidiaries were able to supply foreign customers, particularly in the case of production stoppages of units in other countries.

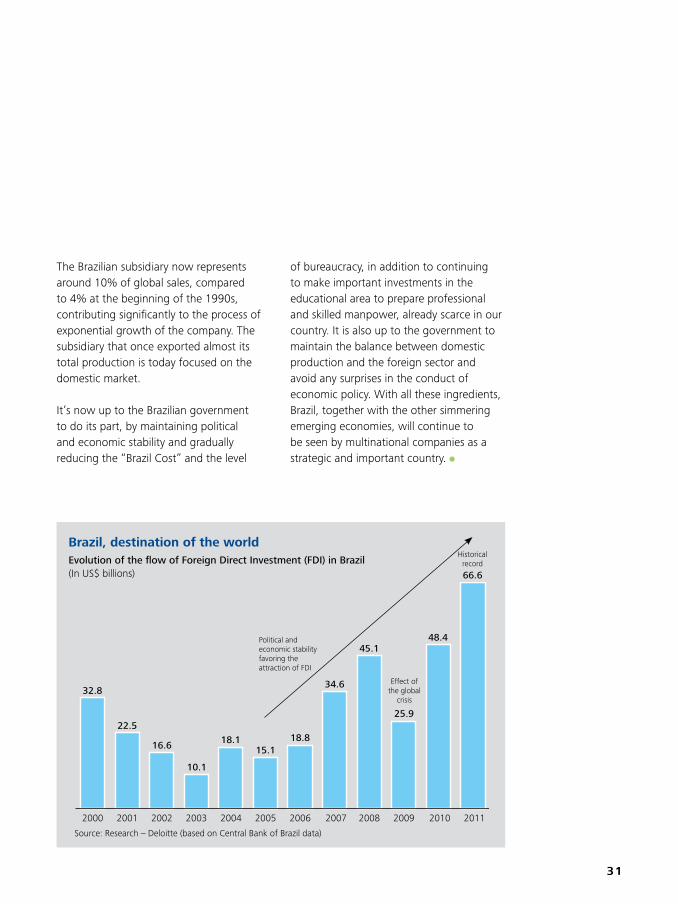

Given that Brazil has great mineral reserves and suppliers of primary products, the majority of multinational companies make the country an important base for supply of raw materials. Many of them continue to invest heavily and open new factories throughout the country. Chinese, Korean and North American companies, particularly in the automotive and construction machinery sectors, are arriving and establishing new factories, mainly because of the 2014 World Cup and the 2016 Olympic Games, events that are attracting the third wave of productive capital. US$ 66.6 billion were invested in Brazil in 2011 alone (see chart on page 31).

The revenues of subsidiaries established in the country are significant today in the global context of multinationals. In the case of Cummins, for instance, sales outside the United States have already reached 60%.

“It is now up to the Brazilian government to do its part, by maintaining political and economic stability and gradually reducing the “Brazil Cost” and the level of bureaucracy, in addition to continuing to make important investments in the educational area to prepare professional and skilled manpower.”

31

The Brazilian subsidiary now represents around 10% of global sales, compared to 4% at the beginning of the 1990s, contributing significantly to the process of exponential growth of the company. The subsidiary that once exported almost its total production is today focused on the domestic market.

It’s now up to the Brazilian government to do its part, by maintaining political and economic stability and gradually reducing the “Brazil Cost” and the level

of bureaucracy, in addition to continuing to make important investments in the educational area to prepare professional and skilled manpower, already scarce in our country. It is also up to the government to maintain the balance between domestic production and the foreign sector and avoid any surprises in the conduct of economic policy. With all these ingredients, Brazil, together with the other simmering emerging economies, will continue to be seen by multinational companies as a strategic and important country.

Brazil,•destination•of•the•worldEvolution of the flow of Foreign Direct Investment (FDI) in Brazil (In US$ billions)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

32.8

22.5

16.6

10.1

18.115.1

18.8

45.1

25.9

48.4

66.6

Political and economic stability favoring the attraction of FDI

Effect of the global

crisis

Historical record

Source: Research – Deloitte (based on Central Bank of Brazil data)

34.6

32

Together for changeToday Brazil presents opportunities for local and foreign companies, but it has become an expensive country. The solution requires initiatives like the Competitiveness Council, part of the “Bigger Brazil Plan”, which enables the discussion and development of material actions to deal with loss of competitiveness in the industrial sector.

Close to fifty years ago, a BASF professional in Germany came to Brazil to help select a site for construction of a plant in Guaratinguetá

(SP) – still our largest industrial complex in the country. Upon his return to Europe, he noted: “Brazil is and will continue to be the country of the future”. Today, however, I must correct this: Brazil is already the country of the present.

This observation is not just the view of a foreigner seeing the wealth of natural resources and enterprising people. One can say Brazil is one of the main global markets based on the positive results of recent decades. The nation is experiencing an auspicious moment. It attained economic stability and is a power in agribusiness – the second largest exporter of grains after only the United States – with the potential to

expand its agricultural production without damaging the environment, thanks to the technology applied and the natural resources available.

In recent years it has also seen rapid growth in the mobility of the social classes, increasing the number of consumers with considerable purchasing power. Over the last 20 years, it has further benefitted from another competitive advantage: the demographic bonus – the country already has, and should continue to have over the next two decades, two workers for each retiree or child. This provides a favorable environment for economic development.

This scenario provides opportunities for both domestic and foreign companies. The country is considered one of the levers of the emerging markets, which are showing

33

greater growth than the developed nations. In 2020, the emerging countries will be responsible for more than a third of the global Gross Domestic Product and will contribute with close to 60% of all global chemical production. In Brazil, data released by the Brazilian Chemical Industry Association (ABIQUIM) indicate that market growth in 2011 was close to 10%.

The chemical industry will play a particularly important role in market growth by driving innovation and contributing to sustainability in aspects related to natural resources, the environment, the climate, the area of food and nutrition and the quality of life.

In this context, BASF has defined seven strategic sectors in which it intends to contribute with solutions, helping the country capture value from the opportunities linked to global megatrends:

Together for change

transportation, construction, consumer goods, health and nutrition, electronics, agriculture, energy and natural resources.

A•more•expensive•countryThe promising portrait for the next years, however, is compromised by the structural challenges that over many decades have been slowing the full development of Brazilian industry, undermining the competitiveness of domestic production and threatening the sustainable growth of the economy.

The high tax load that burdens the purchase of machinery and equipment and the contracting of engineering services has been a constant inhibitor of productive investments. The tax incentives granted by the government are almost always short-term and they deter broader planning by businessmen. The high social

By Alfred HackenbergerPresident of BASF for South America

34

Stimulus•to•competitiveness

With the “Bigger Brazil Plan”, started in 2011 and expected to run through 2014, the federal government intends to promote measures that bring more efficiency to the productive environment of the country. In the first half of 2012, a new package of goals and measures was announced to achieve the program objectives.

Goals• Encourage public and private investment;

• Increase competitiveness in Brazilian industry through productivity and innovation;

• Reduce tax, economic and financial costs.

Measures• Exchange rate: continuity of timely actions

on the exchange rate;

• Taxing: a continuous process of relaxation;

• Production: promote domestic production;

• Development: foreign trade financing;

• Trade protection: respond to international competition;

• Technological: incentives to the information and communications industry;

• Credit: Investment Support Program (PSI in Portuguese);

• Automotive: expand procurement of domestic components and ensure investment in research and development (R&D).

Source: Research – Deloitte (from consolidation of public data of April 5, 2012)

35

“The chemical industry will play a particularly important role in market growth by driving innovation and contributing to sustainability in aspects related to natural resources, the environment, the climate, the area of food and nutrition and the quality of life.”

to more openly and constructively discuss the problems that affect each segment.

In the chemicals area, we expect that critical questions, as the cost of raw materials and energy, will be raised and addressed, in addition to effective and ongoing support for research and development (R&D). Bringing academia, the government and industry together is an initiative essential for improving Brazilian competitiveness.

We are optimistic that this joining of forces will result in effective changes and concrete actions to confront the loss of competitiveness in the industrial sector. And, the confidence of entrepreneurs and investors under a sustainable “Bigger Brazil” scenario will result in even more investment, compatible with the country’s potential, ensuring that this prosperity will be maintained today and always.

charges, that burden production, and the precarious logistical structure, that makes exports difficult, are other obstacles to development. Energy costs are the fourth highest in the world, seriously harming some industrial sectors, such as chemicals. Brazil has become expensive, very expensive.

Faced with these and other factors, it is not surprising that the Brazilian industrial GDP has shown only modest growth – the worst result among the BRICS. Some analysts have already begun talking about a process of deindustrialization. It is necessary to reverse the situation. We believe that the Competitiveness Council, which is part of the “Bigger Brazil Plan” (see chart on page 34) and whose purpose is to analyze the factors affecting the efficiency of Brazilian industry and propose measures to counteract them, will allow the government, workers and businessmen

36

Facing the Chinese model

To deal with the challenges presented by the Asian giant, Brazilian industry needs a strategy on two levels: that of the country and that of companies. Understanding the government policies is not enough. It is necessary to understand the Chinese company, its business model and the process of globalizing its production chains.

The emergence of China presents new challenges for Brazilian industry and the country as a whole. The oriental megapower’s

process of growth and diversification of its industrial production has brought opportunities and, on a larger scale, challenges for practically all elements of Brazil’s productive sectors, which have seen their positions in the foreign and domestic markets affected.

Brazil’s ability to deal with the challenges presented by China requires strategy changes on two levels: that of companies and that of the country. Research by the National Confederation of Industry (CNI) has monitored China’s impact on Brazilian companies and how the local industry has reacted (see chart on page 40). In general, the conclusions of this research show that the companies

that intend to survive these generalized impacts have to evaluate their weaknesses and strengths with regard to Chinese competition. This requires identification of competitive advantages, both in their operation as well as in relation to the institutional and market environments in which they operate, including an evaluation of where China closes or opens possibilities for insertion in global production chains.

For formation of a strategy, it is important to understand the connections between insertion patterns in global chains, engineering and business models. The risk of focusing all our attention to the “Brazil Cost” issue and unfair competition lies in that we can lose sight of the size of the challenges that must be faced.

The case of the United States is illustrative. There are many explanations for North

37

American loss of manufacturing leadership in many industries, but the fact is that some countries now have more efficient production. This can be objectively verified: the number of hours to produce a product, the number of years to move from the research phase to production and the accuracy of machinery, for example.

The lessons of demobilization of manufacturing in the United States and of manufacturing growth in other countries relates to productivity, innovation and the understanding of the involvement of different industries in global production chains. This agenda will determine Brazil’s ability to develop its new industrial base. The center of reaction policy is in the companies. It is their reaction that will, in fact, provide support.

Understanding•local•companiesTo understand China, it is important to understand its companies’ business model and how they integrate with global production chains. They take advantage of the fragmentation of production on a global scale, stimulated by gains in economies of scale and helped by the development of the container in transporting cargos and its corresponding logistics infrastructure, as well as by the significant drop in the cost of data transmission networks and by industrial policies consistent with this environment of fragmented production.

China was a major beneficiary of the process of globalization that occurred at the end of the 20th century and start of the 21st. The ability to connect to this new environment explains one important source of its growth and its transformation

By José Augusto Coelho FernandesExecutive Director of the National Confederation of Industry (CNI)

38

rapidly into new niches after having a clear vision of the profitability of the original invention.”1

Beyond•the•public•policiesChina as an industrial platform benefits from a geographic advantage: its location in an area favored by a network of super ports that connect different countries – Japan, South Korea, Malaysia, Singapore and Thailand, among others – in a strong productive integration of a wide base of suppliers located in the various markets of the region. This productive base, a true industrial ecosystem, has also developed an extraordinary capacity to produce with flexibility and reconfigure processes to supply large quantities and a varied mix of products.

The key issue is that, to build a Brazilian industrial strategy with respect to China, the understanding of its public policies is not enough. The starting point for developing a long-lasting strategy is to understand the Chinese company, its business model and the evolution of the process of globalization of production chains.

in the center of the production networks of practically all industrial sectors.

As it captures portions of the fragmentation of production on a global scale, China is gaining basic advantages associated with economies of scale and of scope, and learning born from specialization. These economies lead to a system that operates with margins much lower than those of more vertical industrial systems. This is the primary source of Chinese competitiveness.

Specialization strengthens this movement by encouraging focus, efficiency and the development of specific knowledge, more difficult to achieve in less specialized industrial structures. In one of their books, the authors Dan Breznitz and Michael Murphree, academics from the Georgia Institute of Technology, synthesize the Chinese model: “China’s capacity for innovation is not only in the process (or increase) of innovation, but also in the organization of production, manufacturing techniques, technologies, delivery, design and in the second innovation cycle. This structure allows China to move more

“The risk of looking only for the problems of ‘Brazil Cost’ and unfair competition is to lose perspective on the scale of the challenges that must be faced.”

39

Production chains are not static. They evolve due to changes in relative prices, technological transformations, logistics, evaluations of risk, the profile of demand, societal values – such as sustainability – and management models.

Production chains may be entering a new phase: from a focus on uniting multiple links of low cost to one of shorter chains structured in regional manufacturing networks. If this trend continues, the chances increase for Brazil to capture manufacturing opportunities. This potential will be greater and better if the country is prepared to offer efficient logistics, adequate communication systems, and business models open to integration and information sharing. No less important, to create a point-to-point strategy, the existence of innovative manufacturing companies with the ability to adapt will always be essential in our country.

Strategic•initiativesIn structuring a strategy for Brazilian industry to adapt to the impacts generated by China, the company is the starting point. However, there is a set of equally important actions that require joint public and private action. To better position national manufacturing with respect to the Chinese model:•• Increase the competitiveness of companies in the country: regardless of the scenario, Brazil needs to raise its competitiveness. China increases the

sense of urgency. Brazil today has an economy of high costs: taxation, logistics, infrastructure, wages, energy and credit. And all within an environment with an overvalued exchange rate. ••Strengthen the opening of the Chinese market: through its tariff schedule and non-tariff barriers, China makes import of Brazilian industrial products difficult. Brazil should have a strategy and action plan to deal with those problems identified. This is particularly important for agribusiness products, for which Brazil has clear competitive advantages. The action developed in favor of pork is an example of initiative that should be repeated.••Consolidate the strategy for natural resource intensive products: Brazil needs to build a strategy that exploits China’s dependency on natural products in order to maximize the benefits of this relationship. This approach involves actions in infrastructure, logistics and research and development (R&D).••Educate the market to identify niches and opportunities: the size of the Chinese market and its development perspectives require systematic work of prospecting, identification of opportunities and business promotion actions. ••Consider the opportunities for integrating with value chains: in fragmented chains, Brazil needs to identify the links in which the country can sustain competitive positions by means of economies of scope and scale,

1 “Run of the Red Queen: government, innovation, globalization, and economic growth in China”

40

and the ability to innovate. Multinational companies have taken steps to avoid concentrating their inputs and raw materials in a few suppliers due to the risk of being without supplies in the event of natural disasters or political crises. This strategy represents an opportunity

for Brazilian companies to capture investment and integrate with global production chains. In other cases, due to China’s high level of competitiveness, the best strategy for Brazil is to maintain competitiveness by integrating with parts of the Chinese supply value chain. This is a step that is being taken by several Brazilian companies, both in connection with importation and investment in China.••Facilitate the structural transformation of Brazilian industry: China and Asia as a whole impose structural modifications on Brazilian industry. The critical question is whether the country has the capacity to develop new sectors and products that take advantage of good competitive conditions and meet the challenges of change, both global and of its industries. The size of the Brazilian market and its area of influence, as well as the opportunities related to pre-salt, renewable energy, products derived from ethanol and exploitation of biodiversity are vectors of this process of transformation.••Attract Chinese direct investment: China has become an important global investor. It is up to Brazil to develop strategies to capture Chinese Foreign Direct Investment (FDI). One area has become especially promising: infrastructure. Funds recently created for the sector, currently in the regulation phase, should be a powerful instrument

Action•and•reactionHow China impacts Brazilian industry and how it positions itself

Research conducted by the National Confederation of Industry (CNI) on the impact of the Chinese competition model on Brazilian companies points to a number of findings:

• Competition from Chinese products in the domestic market affects one in every four industrial companies and the exposure to competition increases in accordance with the size of the organization;

• The intensity of the competition varies by industry – those most affected are electronic and communication material, textiles, hospital and precision equipment, footwear and machinery and equipment;

• Competition with the Chinese is even more intense in the international market than it is in the domestic market;

• The number of companies that import raw material, final products or machinery and equipment has increased over time.

In reviewing Brazilian companies’ strategies to deal with this competition, the following patterns of reaction stand out:

• Half of the companies have already developed a strategy to deal with the competition (the rate varies in accordance with the size of the organization);

• The main actions involve investment in the quality and/or design of products and reduction of costs and/or gains in productivity;

• The portion of large companies that already have their own production facilities in China is 10%, concentrated in four industries: automotive vehicles, machinery and equipment, electrical machinery and materials and electronic and communication material.

41

for achieving this objective. Note that Chinese investment has increased in Brazil and, more recently, it has also begun competing in the manufacturing industry.••Develop a trade strategy focused on the interests of industry: one of the paths toward confronting the Chinese challenge is to develop a network of trade agreements in markets significant for Brazilian industry. Free trade agreements result in the establishment of preferences. To the extent that Brazil can succeed in developing these agreements and China has difficulty doing so, our competitive capacity increases. For Brazil, it is especially important to maintain preferential margins in the Americas, where Mexico is the primary priority, and consolidate the penetration of Africa.••Coordinate international actions: undervaluation of the Chinese currency and the problems associated with China’s

trade and industrial policy – considering its conformance with the World Trade Organization (WTO) –, depend on coordinated actions in international forums.••Strengthen the trade protection system: it should be ready to use the mechanisms provided for by the WTO efficiently, competently and in a timely manner.••Monitor China’s economic evolution: Brazilian corporate and public policies in relation to China cannot be based on ignorance. Monitoring is important to identify how China will adapt to the challenges of strengthening its domestic economy and increasing its role in the international financial system. The probable increase in domestic consumption, the process of capital liberalization and appreciation of the yuan, the evolution of domestic costs and industrial policies deserve special attention.

“The lessons of demobilization of manufacturing in the United States and of manufacturing growth in other countries relates to productivity, innovation and the understanding of the involvement of different industries in global production chains. This agenda will determine Brazil’s ability to develop its new industrial base.”

42

Our challenges in the IT chain

The success of the Brazilian PC industry, with the introduction of good public policies, has been supporting the growth of the official market. To ensure the ability to compete with large international groups, Brazil will now need increased surveillance to prevent unfair competition and to enforce clear rules to be applied to all.

The Brazilian personal computer industry can be considered a success case for the introduction of public policies focused on economic

and social development. The framework of incentives for personal computer (PC) production encompasses not only local manufacture of computers but also the development of a chain of inputs, such as motherboards, monitors, memory and hard disks, in addition to investments in research and development, nationally.

Consequently, the information technology sector generates jobs and fosters researches, creating a virtuous cycle for the country in terms of income and technology. Above all, the Brazilian model is fair, since it grants similar incentives to all manufactures, independently of their origins. This is

the reason why practically all significant multinational groups have a Brazilian production, providing consumers with access to a large range of brands.

The success of the Brazilian model has contributed to the growth of the official market in recent years. Before 2005, approximately 80% of the PCs sold in the country were offered by the so called “grey market” (those with some level of illegality in their chain). Currently, it is the official market that accounts for close to 80% of the amount sold in Brazil, according to International Data Corporation (IDC). In an increasing legalized manner, the Brazilian market has been expanding at a rapid pace, surpassing more mature economies such as those of the United Kingdom and Japan, to become the third largest global market for PCs. This is an irrefutable proof

43

that the local production model does not pose any obstacle to market development.

The•international•competitionOne of the consequences of the successful development of the domestic market is that the good opportunities have encouraged multinationals – both North American and Asian companies – to increase their focus on our territory in recent years. As a result, the increased competition in Brazil has changed the industry’s levels of profitability, contributing to a convergence with levels close to those realized by developed countries. Although accelerated by the weak demand in the more mature economies, it can be understood as a natural process.

The episodes of unfair competition related to imported notebooks, a recurrent

problem in the country, are worrisome. Large volumes of PCs manufactures in Asia have entered the local market at quite reduced prices. This process has occurred with signs of under invoicing, since there is a tax burden of over 40% over imports of this kind, which theoretically would be sufficient to make the entry of finished computers into Brazil inviable. Deficiencies in our customs inspection system have allowed such imports, harming the domestic industry as a whole. The impacts have continued to the present, even after the implementation of inspection improvements by the government, since it is hard for computer prices to return to their previous level after having been strongly reduced in the market. The lesson serves as a warning to the government, that it should ensure equal competitive conditions in the official computer industry.

By Hélio Bruck RotenbergCEO of Positivo Informática

44

Besides greater market oversight efforts, another point that deserves attention from development policymakers is the exemption of taxes on revenue (PIS) and contributions for social security funding (COFINS) levied on imported PCs. It does not make sense to maintain such a benefit to foreign manufactures when we have already developed a local industry with production capacity well

matched to demand. This would not be protectionism, given the increasing participation of foreign companies with local production in the Brazilian PC market.

Market data support this thesis. Presently, the sales ranking of the five largest manufacturers already includes four multinational groups. Two years ago, Brazilian companies dominated this list. Positivo Informática is the only domestic manufacturer that has maintained a solid position in the Brazilian market, a sales leader for the past six years according to International Data Corporation (IDC).

It is possible to operate in this market and compete with large international groups. Our leadership in the market evidences that, a natural consequence of a formula that generates value for customers, nimble management, and a rigorous search for competitive costs. It is fundamental to have clear rules applied to all to enable the Brazilian market to maintain its growth trajectory, contributing to the technological development of the country.

“Above all, the Brazilian model is fair, since it grants similar incentives to all manufactures, independently of their origins. This is the reason why practically all significant multinational groups have a Brazilian production.”

45

“It is fundamental to have clear rules applied to all to enable the Brazilian market to maintain its growth trajectory, contributing to the technological development of the country.”

46

A stronger link in the entire chain

As essential bases of the manufacturing industry chain, mining and steel can, together, starting with more cooperative actions between them, better meet their own challenges and expand their role in the country’s development even more.

The mining and steel sectors are at the base that supports the industrial development of the country. By

understanding the challenges that both currently face and evaluating the ways to meet them, in reality we are actually discussing ways to expand competitiveness in all sectors of the manufacturing industry. And this is exactly what we need at this time.

In analyzing the proximity and interconnection between these two sectors, greater collaboration between their respective agents can be seen as a trend, both emerging and necessary. In spite of the numerous challenges the mining sector faces – new sources of financing, increased costs and competition for resources from the energy

and infrastructure sectors – and in the steel sector – always looking for ways to protect itself from commodity price volatility, starting, for example, with hedge operations by participating directly in financing the mining sector –, there is still room to make progress in the two areas. The growing number of joint ventures between companies in the two sectors to optimize their operations already shows this movement of greater cooperation, which can only grow.

Volatility•and•other•issuesIn mining, the main issues that affect the sector should continue practically unchanged over the next years. However, from a macroeconomic and geopolitical viewpoint, it becomes clear that the difficulties that plague the industry are rapidly reaching an extreme and unprecedented level.

47

By Eduardo Tavares RaffainiDeloitte leader in Brazil for mining segment

Cost increases are not new, but they are larger. Changes in fiscal and government policies have been taking place for years, but the associated costs and their unpredictability have increased. The price volatility of commodities is greater than ever, in part, due to market uncertainty and the unprecedented demand from governments and companies in Asia. Issues related to sustainability, which involve conservation of the environment and the guarantee of human rights in work practices, have frequently been transformed into cases of community activism and social unrest.

The shortage of labor, on the other hand, continues to increase. Companies’ cash on hand has increased, resulting in growing expectations on the part of shareholders. Investment project portfolios have assumed an increasingly significant

role. And, in addition to all this, the regulatory environment continues to be restrictive.

Events that normally occur every 100 years are also taking place with an alarming regularity. In addition to the long-term effects of the global financial crisis that continue to reverberate, primarily in Europe, destructive weather phenomena are taking a toll.

To the extent that these global forces converge, the leaders of mining companies must look beyond the traditional scenarios used in their planning. To prepare themselves for the risks not previously predicted, companies must begin to incorporate more complex scenarios into their strategic planning. They must also be ready to look for nonconventional solutions to conventional

48

challenges if they really expect to resolve some of the sector’s most endemic issues.

Steel•and•synergyIn steel, global competition is even stronger. The steel produced in countries such as China and India is able to enter the country at competitive prices, strongly affecting local suppliers. In the largest