Bankinter Group Statutory report prepared pursuant to the Corporations Law and the Commercial Code. Consolidated financial statements prepared by the Board of Directors of Bankinter, S.A. on 14 March 2007.

Transcript

Bankinter Group

Statutory report prepared pursuant to the Corporations

Law and the Commercial Code. Consolidated financial

statements prepared by the Board of Directors of

Bankinter, S.A. on 14 March 2007.

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 1

B

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 2

Bankinter Group

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 3

Consolidated balance sheets at 31 December 2006 and 2005

Consolidated income statements for the years ended 31 December 2006 and 2005

(1) Group description and activities

(2) Accounting standards and criteria applied

(3) Distribution of profit

(4) Deposit Guarantee Fund

(5) Accounting policies and measurement bases

(6) Cash and balances with central banks

(7) Financial assets and liabilities held for trading/Other financial assets at fair value through

profit or loss

(8) Available-for-sale financial assets

(9) Loans and receivables

(10) Held-to-maturity investments

(11) Hedging derivatives (assets and liabilities)

(12) Non-current assets held for sale

(13) Investments

(14) Tangible assets

(15) Intangible assets

(16) Tax assets and liabilities

(17) Prepayments and accrued income and Accrued expenses and deferred income

(18) Other assets and liabilities

(19) Financial liabilities at amortised cost

(20) Liabilities under insurance contracts

(21) Provisions

(22) Equity having the substance of a financial liability

(23) Own funds

(24) Valuation adjustments (equity)

(25) Contingent liabilities and commitments

(26) Transfers of financial assets

(27) Other memorandum items - Financial derivatives

(28) Personnel expenses

(29) Fee and commission income and expense

(30) Interest and similar income/Interest expense and similar charges

BBankinter Group 4

Contents

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 4

(31) Gains/losses on financial assets and liabilities

(32) Net exchange differences

(33) Other general administrative expenses

(34) Other operating income and expenses

(35) Other gains/Other losses

(36) Transactions and balances with related parties

(37) Remuneration of and balances with the members of the Board of Directors

(38) Information on the environment

(39) Customer Care Service

(40) Branches, centres and financial agents

(41) Trust and investment services

(42) Fees paid to auditors

(43) Tax matters

(44) Assets and liabilities measured at other than fair value

(45) Risk management policies

(46) Segment reporting

(47) Events after the balance sheet date

(48) Explanation added for translation to English

Directors' report

AppendixesI. Consolidated statements of changes in equity (Consolidated statements of recognised

income and expense)

II. Consolidated cash flow statements

III. Segment reporting

IV. Transactions and balances with related parties

V. Balance sheets for the distribution of 2006 dividends

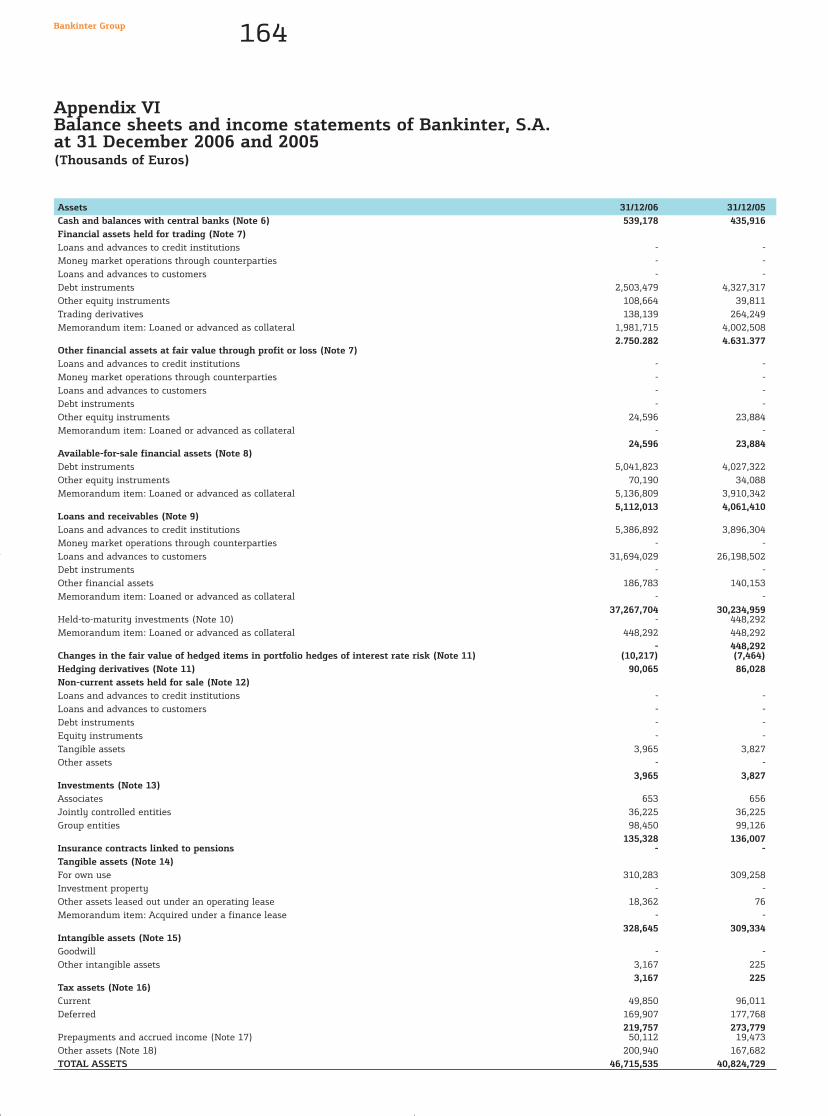

VI. Balance sheets and income statements of Bankinter, S.A.

at 31 December 2006 and 2005

5Bankinter Group

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 5

B

Consolidated Balance Sheets at 31 December 2006 and 2005

Bankinter Group 6

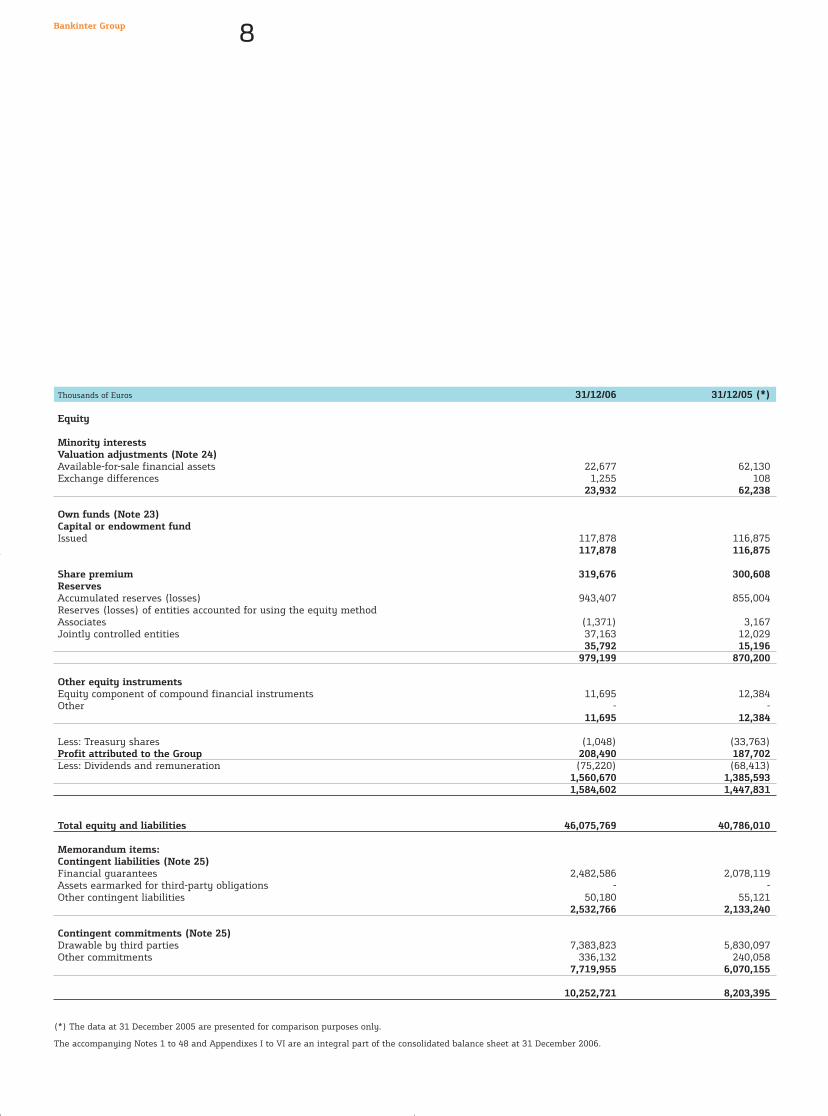

Thousands of Euros 31/12/06 31/12/05 (*)

Assets

Cash and balances with central banks (Note 6) 539,178 435,916

Financial assets held for trading (Note 7)Debt instruments 2,503,479 4,327,317 Other equity instruments 108,664 39,811 Trading derivatives 148,059 267,274 Memorandum item: Loaned or advanced as collateral 1,981,715 4,002,508

2,760,202 4,634,402 Other financial assets at fair value through profit or loss (Note 7)Other equity instruments 24,596 23,884 Memorandum item: Loaned or advanced as collateral - -

24,596 23,884 Available-for-sale financial assets (Note 8)Debt instruments 4,251,163 3,473,735 Other equity instruments 240,399 307,846 Memorandum item: Loaned or advanced as collateral 3,804,929 3,210,431

4,491,562 3,781,581 Loans and receivables (Note 9)Loans and advances to credit institutions 5,387,117 4,205,236 Loans and advances to customers 31,653,807 26,139,388 Other financial assets 186,783 140,153 Memorandum item: Loaned or advanced as collateral - -

37,227,707 30,484,777 Held-to-maturity investments (Note 10) - 448,292 Memorandum item: Loaned or advanced as collateral - 448,292 Changes in the fair value of the hedged items in portfolio hedges of interest rate risk (10,217) (7,464) Hedging derivatives (Note 11) 90,065 86,028 Non-current assets held for sale (Note 12)Tangible assets 3,965 3,827 Other assets - -

106,539 79,396 Tangible assets (Note 14)Property, plant and equipment for own use 319,970 320,666 Investment property 5,300 5,421 Other assets leased out under an operating lease 18,362 76 Memorandum item: Acquired under a finance lease - -

Liabilities under insurance contracts (Note 20) 488,271 622,843

Provisions (Note 21)Provisions for pensions and similar obligations 1,390 10 Provisions for contingent liabilities and commitments 32,040 25,271 Other provisions 131,181 137,294

Contingent commitments (Note 25)Drawable by third parties 7,383,823 5,830,097 Other commitments 336,132 240,058

7,719,955 6,070,155

10,252,721 8,203,395

(*) The data at 31 December 2005 are presented for comparison purposes only.

The accompanying Notes 1 to 48 and Appendixes I to VI are an integral part of the consolidated balance sheet at 31 December 2006.

(

T

C3

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 8

9Bankinter Group

Thousands of Euros 31/12/06 31/12/05 (*)

Interest and similar income (Note 30) 1,455,871 1,076,615 Interest expense and similar charges (Note 30) (998,591) (655,656) Return on equity having the substance of a financial liability (11,139) (7,255)Other 987,452 648,401 Income from equity instruments 16,354 9,308 Net interest income 473,634 430,267 Share of results of entities accounted for using the equity method 29,623 24,645

Fee and commission income (Note 29) 286,965 249,677 Fee and commission expense (Note 29) (69,846) (59,978) Insurance activity income 1,694 (75)Insurance and reinsurance premium income 32,960 45,612 Reinsurance premiums paid (6,392) (1,119)Claims paid and other insurance-related expenses (184,271) (185,730)Reinsurance income 2,216 1,242 Net provisions for insurance contract liabilities (135,737) (107,381)Finance income 101,944 102,149 Finance expense (80,500) (69,610)Gains on financial assets and liabilities (net) (Note 31) 49,776 30,684 Held for trading 1,903 3,367 Other financial instruments at fair value through profit or loss 2,767 5,223 Available-for-sale financial assets (27,273) 42,647 Loans and receivables - - Other 72,379 (20,553)Exchange differences (net) (Note 32) 47,756 36,634 Gross income 819,602 711,854 Sales and income from the provision of non-financial services - - Cost of sales - - Other operating income (Note 34) 24,003 18,763 Personnel expenses (Note 28) (227,336) (192,398)Other general administrative expenses (Note 33) (174,940) (160,703) Depreciation and amortisation (24,151) (21,031) Tangible assets (Note 14) (24,034) (21,031) Intangible assets (Note 15) (117) - Other operating expenses (Note 34) (5,532) (4,902) Net operating income 411,646 351,583 Impairment losses (net) 96,898 80,143 Available-for-sale financial assets 1 187 Loans and receivables (Note 9) 97,295 80,340 Held-to-maturity investments - - Non-current assets held for sale (399) (384)Investments 1 - Tangible assets - - Goodwill - - Other intangible assets - - Other assets - - Provisions (net) 5,892 7,035 Finance income from non-financial activities - - Finance expenses of non-financial activities - - Other gains (Note 35) 15,231 7,214 Gains on disposal of tangible assets 886 642 Gains on disposal of investments 20 15 Other 14,325 6,557 Other losses (Note 35) (7,751) (6,174) Losses on disposal of tangible assets 344 35 Losses on disposal of investments 666 124 Other 6,741 6,015 Profit before tax 316,336 265,445 Income tax (Note 43) (107,846) (77,743) Profit from ordinary activities 208,490 187,702 Profit/Loss from discontinued operations - - Consolidated profit for the year 208,490 187,702 Profit/Loss attributed to minority interests - - Profit attributed to the Group (Note 23) 208,490 187,702 Earnings per share (euros) 2.68 2.44Diluted earnings per share (euros) 2.58 2.34

(*) The data at 31 December 2005 are presented for comparison purposes only.

The accompanying Notes 1 to 48 and Appendixes I to VI are an integral part of the consolidated income statement for the year ended 31 December 2006.

Consolidated income statements of the Bankinter Group for the years ended31 December 2006 and 2005

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 9

B

Explanatory notes to the consolidated financial statementsfor the year ended 31 December 2006(Amounts in thousands of euros)

(1) Group description and activities

Bankinter, S.A. (“the Bank” or “the Entity”) engages in banking activities and is subject to the rules

and regulations applicable to banks operating in Spain.

In addition to the operations carried on directly by it, the Bank is the head of a group of

subsidiaries that engage in various business activities and which compose, together with it, the

Bankinter Group (“the Group” or “the Bankinter Group”). Therefore, the Bank is obliged to prepare,

in addition to its own individual financial statements, the Group's consolidated financial

statements, which also include the interests in joint ventures and investments in associates.

The Bank’s assets accounted for 99% of the Group’s total assets at 31 December 2006 and 2005.

The Group's consolidated financial statements for 2005 were approved by the shareholders at the

Annual General Meeting of the Bank on 20 April 2006. The 2006 consolidated financial statements

of the Group and the 2006 financial statements of the Bank and substantially all the Group entities

have not yet been approved by their shareholders at the respective Annual General Meetings.

However, the Bank's Board of Directors considers that the aforementioned financial statements will

be approved without any changes.

Bankinter, S.A. was incorporated by public deed executed in Madrid on 4 June 1965 under the

name of Banco Intercontinental Español, S.A. and adopted its present name on 4 May 2004.

The Bank is registered with number 30 at the Special Registry of Banks and Bankers. Its employer

identification number is A-28157360 and it is a member of the Deposit Guarantee Fund with code

number 0128.

Its registered office is located at Paseo de la Castellana 29, 28046 Madrid (Spain). The subsidiaries

composing the Bankinter Group are listed in Note 13, “Investments”. The Group's consolidated

financial statements were prepared in accordance with the accounting policies set forth in the

“Accounting Policies and Measurement Bases” section.

The balance sheets of Bankinter, S.A. at 31 December 2006 and 2005 and the income statements

for the years then ended are presented in Appendix VI.

The securitisation special purpose vehicles Bankinter 12 Fondo de Titulización Hipotecaria,

Bankinter 13 Fondo de Titulización de Hipotecaria and Bankinter 2 Pyme Fondo de Titulización de

Activos were fully consolidated in 2006 for the first time.

Bankinter Internacional, B.V. was dissolved and Bankinter Netherlands B.V. and Prota, S.A. were

sold in 2006.

Bankinter Group 10

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 10

(2) Accounting standards and criteria applied

a) Basis of presentation of the consolidated financial statements Under Regulation (EC) no. 1606/2002 of the European Parliament and of the Council of 19 July

2002, all companies governed by the law of an EU Member State and whose securities are admitted

to trading on a regulated market of any Member State must prepare their consolidated financial

statements for the years beginning on or after 1 January 2005 in conformity with the International

Financial Reporting Standards (IFRSs) previously adopted by the European Union.

In order to adapt the accounting system of Spanish credit institutions to the new standards, the

Bank of Spain issued Circular 4/2004, of 22 December, on Public and Financial Reporting Rules and

Formats.

The Group's consolidated financial statements for 2006 were prepared by the Bank's directors

(at the Board meeting on 14 March 2007) in accordance with International Financial Reporting

Standards as adopted by the European Union and taking into account Bank of Spain Circular

4/2004, using the basis of consolidation, accounting policies and measurement bases set forth in

Note 5 and, accordingly, they present fairly the Group's equity and financial position at 31

December 2006, and the consolidated results of its operations, the changes in consolidated equity

(statement of recognised income and expense) and the consolidated cash flows in 2006. These

consolidated financial statements were prepared from the individual accounting records of the

Bank and of each of the companies composing the Group, and include certain adjustments and

reclassifications required to unify the accounting policies and measurement bases applied by the

Group.

At the date of preparation of these consolidated financial statements various Standards and

Interpretations had been adopted by the European Union but had not yet come into force. The

directors consider that the entry into force of these Standards and Interpretations will not have a

material effect on the Group’s consolidated financial statements.

The notes to the consolidated financial statements contain supplementary information to that

presented in the consolidated balance sheet, consolidated income statement, consolidated

statement of changes in equity (statement of recognised income and expense) and consolidated

cash flow statement. The notes provide, in a clear, relevant, reliable and comparable manner,

narrative descriptions and breakdowns of these financial statements.

All accounting policies and measurement bases with a material effect on the consolidated financial

statements were applied in their preparation.

11Bankinter Group

s

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 11

B

b) Accounting policies and measurement basesThe consolidated financial statements were prepared in accordance with the generally accepted

accounting policies and measurement bases described in Note 5, “Accounting Policies and

Measurement Bases”.

Unless stated otherwise, these consolidated financial statements are presented in thousands of

euros.

c) Use of judgment and estimatesThe information included in these consolidated financial statements is the responsibility of the

Bank’s directors. In this connection certain estimates were used, where appropriate, in order to

measure certain assets, liabilities, income, expenses and commitments. These estimates, which

were made by the Group's senior management and were ratified by its directors, relate basically

to the following:

• the impairment losses on certain assets

• the useful life of the tangible and intangible assets

• the fair value of certain unquoted assets

• the actuarial assumptions used in the calculation of the post-employment benefit liabilities and

obligations

• the calculation of the provisions made

Although these estimates were made on the basis of the best information available at 31 December

2006 about the items analysed, events that might take place in the future might make it necessary

to change these estimates (upwards or downwards) in coming years. Changes in accounting

estimates, if appropriate, will be applied prospectively, recognising the effects of the change in esti-

mates in the related consolidated income statement.

d) Basis of consolidation The Group was defined as provided for by current accounting standards and rules. Investees

include subsidiaries, jointly controlled entities and associates.

“Subsidiaries” are defined as entities which form a decision-making unit with the Parent, i.e.

entities over which the Parent has, directly or indirectly through other investee(s), the capacity to

exercise control. Control is, in general but not exclusively, presumed to exist when the Parent owns

directly or indirectly through other investees half or more of the voting power of the investee.

Control is the power to govern the financial and operating policies of an investee so as to obtain

benefits from its activities and may be exercised even if the aforementioned ownership interest is

not held.

Bankinter Group 12

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 12

Note 13 contains significant information on the investments in subsidiaries at 31 December 2006

and 2005.

The financial statements of the subsidiaries were fully consolidated with those of the Bank.

Accordingly, all material balances and transactions between consolidated entities were eliminated

on consolidation. Also, the share of third parties of the Group's equity is presented under Minority

Interests in the consolidated balance sheet and the share of the profit for the year attributed to

minority interests is presented under Profit Attributed to Minority Interests in the consolidated

income statement.

The results of subsidiaries acquired by the Group during the year are included in the consolidated

income statement from the date of acquisition to year-end. Similarly, the results of subsidiaries

disposed of during the year are included in the consolidated income statement from the beginning

of the year to the date of disposal.

Jointly controlled entities are investees that are not subsidiaries and are jointly controlled by the

Group and by one or more unrelated entities not related to the Group or the joint ventures. A joint

venture is a contractual arrangement whereby two or more entities (“venturers”) undertake

operations or hold assets so that strategic financial and operating decisions affecting the joint

venture require the unanimous consent of the venturers, provided that these operations or assets

are not integrated in financial structures other than those of the venturers.

The financial statements of jointly controlled entities are accounted for using the equity method

and the exceptions provided for by current accounting standards and rules were applied.

Note 13 contains significant information on the interests in jointly controlled entities at 31

December 2006 and 2005.

Associates are entities over which the Group exercises significant influence. Significant influence is

generally, although not exclusively, deemed to be exercised when the Group holds -directly or

indirectly through other investees- 20% or more of the voting power of the investee.

In the consolidated financial statements, investments in associates are accounted for using the

equity method, i.e. at the Group's share of net assets of the investee, after taking into account the

dividends received therefrom and other equity eliminations. The profits and losses arising from

transactions with an associate are eliminated to the extent of the Group's interest in the associate.

If as a result of losses incurred by an associate its equity were negative, the investment should be

presented in the Group's consolidated balance sheet with a zero value, unless the Group is obliged

to give it financial support.

13Bankinter Group

r

-

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 13

B

Note 13 contains significant information on the investments in associates at 31 December 2006

and 2005.

Note 13 contains information on the most significant acquisitions and disposals of subsidiaries,

jointly controlled entities and associates in 2006.

A business combination is the bringing together of two or more separate entities or economic units

into one single entity or group of entities.

Business combinations performed on or after 1 January 2004 whereby the Group obtains control

over an entity are recognised for accounting purposes as follows:

• The Group measures the cost of the business combination, defined as the fair value of the assets

given, the liabilities incurred and the equity instruments issued, if any, by the acquirer.

• The net fair values of the assets, liabilities and contingent liabilities of the acquiree, including

any intangible assets which might not have been recognised by the acquiree, are measured and

recognised in the consolidated balance sheet.

• Any negative difference between the net fair value of the assets, liabilities and contingent

liabilities of the acquiree and the business combination cost is recognised as discussed in Note 2-m;

any positive difference is recognised in “Other Gains” in the consolidated income statement.

e) Comparative informationThe information relating to 2005 contained in these notes to the consolidated financial statements

is presented with the information relating to 2006 for comparison purposes only and, accordingly,

it does not constitute the Group's statutory consolidated financial statements for 2005.

f) EquityThe publication of Law 13/1992, of 1 June, and of Bank of Spain Circular 5/1993 and subsequent

amendments thereto brought into force the regulations governing the minimum capital

requirements for credit institutions both at entity level and at consolidated group level.

At 31 December 2006, the Group's eligible capital exceeded the minimum requirements by

EUR 511,958 thousand (31 December 2005: EUR 481,090 thousand).

Bankinter Group 14

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 14

(3) Distribution of profit for the year

The distribution of Bankinter, S.A.’s net profit for the year ended 31 December 2006 that the

directors will propose for approval by the shareholders at the Annual General Meeting is, and the

approved distribution of 2005 profit was, as follows:

The distribution of the net profit for the year ended 31 December 2006 of Bankinter, S.A.'s

subsidiaries that their respective directors will propose for approval by the shareholders at their

respective Annual General Meetings is as follows:

15Bankinter Group

;

Thousands of Euros 2006 2005

Distribution:

Voluntary reserves 64,482 66,809

Canary Islands investment reserve - 1,200

Interim dividend 102,056 92,728

Distributed profit 166,538 160,737

Profit for the year 166,538 160,737

Thousands of Euros Net Profit Provision for Dividend Reserves AllocationsIncome Tax

Bankinter Capital Riesgo, S.G.E.C.R., S.A. 663 230 - 359 74

Bankinter Seguros de Vida, S.A. de Seguros y Reaseguros 19,581 6,840 6,294 6,447 -

Aircraft, S.A. (384) (134) - - -

Bankinter Netherlands BV (18) - - - -

Bankinter Sociedad de Financiación, S.A. 1 - - - 1

Bankinter Emisiones, S.A. 28 10 - - 18

Bankinter Capital Riesgo I, Fondo Capital (665) (233) - - -

Helena Activos Líquidos, S.L. (6) - - - -

Arroyo Business Consulting Development, S.L. - - - - -

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 16

(a) Going concernThe consolidated financial statements were prepared under the assumption that the Group entities

will continue as a going concern for the foreseeable future and hence the accounting policies were

not applied to determine the consolidated net asset value for the purpose of total or partial transfer

or the amount that would result from liquidation.

(b) Accrual basis of accountingExcept for cash flow information, these consolidated financial statements were prepared on the

basis of the actual flow of goods and services, regardless of when the related payment or collection

is made.

Income and expenses are recognised using the accrual basis of accounting rather than the cash

basis, except for interest on loans and receivables and other non-investment loans to borrowers

classified as impaired, which is credited to the income statement when it is collected.

Interest on asset and liability transactions with settlement terms exceeding twelve months is

accrued by the interest method and that on shorter-term transactions is accrued by either the

interest or the straight-line method.

In accordance with general banking practice, transactions are recognised on the date they are

performed, which may differ from the related value date on the basis of which interest income and

expense are calculated.

(c) Foreign currency transactions and balancesForeign currency balances and transactions were translated to euros using the following methods:

- Monetary assets and liabilities: at the average spot exchange rate ruling on the foreign currency

market at the reporting date.

- Non-monetary items measured at historical cost: at the exchange rates prevailing on the date of

acquisition.

- Non-monetary items measured at fair value: at the exchange rates on the date when the fair

value was determined.

- Income and expense items: at the exchange rates at the transaction date (average exchange rates

for the year were used for all the transactions performed during the year). Depreciation and

amortisation were translated to euros at the exchange rates applied to the related asset.

Exchange differences were recognised in the consolidated income statement, except for those

differences arising in non-monetary items measured at fair value whose adjustment to fair value

is recognised in equity.

17Bankinter Group

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 17

B

(d) Recognition, measurement and classification of financial instrumentsFinancial assets and liabilities are recognised when the Group becomes a party to the contract in

accordance with the provisions thereof.

Financial assetsRegular way purchases or sales of financial assets, defined as those in which the parties' reciprocal

obligations must be discharged within a time frame established by regulation or convention in the

marketplace and that may not be settled net, such as stock market and spot currency purchase and

sale contracts, are recognised as an asset by the purchaser and derecognised by the seller on the

date from which the rewards, risks, rights and duties attaching to all owners are for the purchaser,

which, depending on the type of asset or type of market, may be the trade date or the settlement

or delivery date.

Debt instruments are recognised from the date on which a legal right to receive or a legal

obligation to pay cash arises. Derivatives are recognised from the trade date. The Group generally

derecognises financial instruments on the date from which the related rewards, risks, rights and

duties or control thereon are transferred to the purchaser.

Financial assets are classified in the consolidated balance sheet as follows:

i) Cash and balances with central banks: this category includes cash balances and balances with

the Bank of Spain and other central banks.

ii) Financial assets held for trading: this category includes financial assets acquired for the purpose

of selling them in the near term. They are part of a portfolio of identified financial instruments

that are managed together and for which there is evidence of a recent actual pattern of short-term

profit taking or they are derivative instruments that are not designated as hedging instruments.

The changes in the fair value of financial assets held for trading are recognised directly in the

income statement.

iii) Other financial assets at fair value through profit or loss: this category includes (1) hybrid

financial assets not held for trading that are measured entirely at fair value and (2) financial

assets not held for trading that are managed jointly with liabilities under insurance contracts

measured at fair value or with derivative financial instruments whose purpose and effect is to

significantly reduce exposure to variations in fair value, or that are managed jointly with financial

liabilities and derivatives for the purpose of significantly reducing overall exposure to interest rate

risk.

Bankinter Group 18

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 18

iv) Available-for-sale financial assets: this category includes debt instruments not classified as held-

to-maturity investments, as other financial assets at fair value through profit or loss, as loans and

receivables or as financial assets held for trading and equity instruments issued by entities other

than subsidiaries, associates and jointly controlled entities, provided that such instruments have

not been classified as financial assets held for trading or as other financial assets at fair value

through profit or loss. The changes in the fair value of available-for-sale financial assets are

recognised directly in equity until the financial asset is derecognised.

v) Loans and receivables: this category includes financial assets that are not quoted in an active

market, that do not have to be measured at fair value and that have fixed or determinable cash

flows in which the Group will recover all of its investment, other than losses because of credit

deterioration. This category includes the investment arising from ordinary lending activities, such

as the cash amounts of loans drawn down and not yet repaid by customers, the deposits placed

with other institutions, whatever the legal instrument, unquoted debt securities and the debt

incurred by the purchasers of goods, or the users of services, constituting part of the Group's

business.

vi) Held-to-maturity investments: this category includes debt securities with fixed maturity and

fixed cash flows which the Group has decided to hold to maturity, basically because it has the

financial ability to do so or because it has related financing. The entity shall not classify as held-to-

maturity, or hold any financial asset in this category if during the current year or the two

preceding years it has sold or reclassified assets in this portfolio for more than an insignificant

amount relative to the total amount of the assets in this category.

vii) Changes in the fair value of hedged items in portfolio hedges of interest rate risk: this item

is the balancing entry for the amounts credited to the consolidated income statement in respect of

the measurement of the portfolios of financial instruments which are efficiently hedged against

interest rate risk through fair value hedging derivatives.

viii) Hedging derivatives: this category includes the financial derivatives acquired or issued by the

Group which qualify for hedge accounting.

ix) Investments: this item includes the equity instruments of jointly controlled entities and

associates.

19Bankinter Group

d

e

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 19

B

In general, financial assets are initially recognised at acquisition cost and are subsequently

measured at each period-end as follows:

i) Financial assets are measured at fair value, except for loans and receivables, held-to-maturity

investments, equity instruments whose fair value cannot be determined in a sufficiently objective

manner, investments in subsidiaries, jointly controlled entities and associates and financial

derivatives that have such equity instruments as their underlying asset and are settled by delivery

of those instruments.

ii) The fair value of a financial asset on a given date is taken to be the amount for which it could

be exchanged by two knowledgeable, willing parties in an arm's length transaction. The best

evidence of fair value is the market price on an active, transparent and deep market.

If there is no market price for a given financial asset, its fair value is estimated on the basis of the

price established in recent transactions involving similar instruments and, in the absence thereof,

of sufficiently proven valuation techniques, taking into account the specific features of the financial

asset to be measured and, particularly, the various types of risk associated with it.

iii) The fair value of financial derivatives with a quoted price on an active market is deemed to be

their daily quoted price and if, for exceptional reasons, the quoted price at a given date cannot

be determined, these financial derivatives are measured using methods similar to those used to

measure derivatives not arranged in organised markets.

The fair value of OTC derivatives is taken to be the sum of the future cash flows arising from the

instrument, discounted to present value at the date of measurement using valuation techniques

commonly used by the financial markets.

iv) Loans and Receivables and Held-to-Maturity Investments are measured at amortised cost using

the effective interest method. Amortised cost is understood to be the acquisition cost of a financial

asset plus or minus, as appropriate, the principal repayments and the portion recognised in the

consolidated income statement by the effective interest method of the difference between the

initial cost and the maturity amount, less any impairment loss recognised directly as a reduction of

the amount of the asset or through an allowance account. In the case of loans and receivables

hedged in fair value hedges, the changes in the fair value of these assets related to the risk or

risks being hedged are recognised.

Bankinter Group 20

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 20

The effective interest rate is the discount rate that exactly matches the initial amount of a financial

instrument to its estimated cash flows during its expected life based on the related contractual

conditions, such as early redemption options, but disregarding future credit losses. For fixed rate

financial instruments, the effective interest rate coincides with the contractual interest rate

established on the acquisition date plus, where applicable, the fees that, because of their nature,

can be equated with a rate of interest. In the case of floating rate financial instruments, the

effective interest rate coincides with the rate of return prevailing in all connections until the next

benchmark interest reset date.

v) Equity instruments of other entities whose fair value cannot be determined in a sufficiently

objective manner and financial derivatives that have those instruments as their underlying asset

and are settled by delivery of those instruments are measured at acquisition cost adjusted, where

appropriate, by any related impairment loss.

As a general rule, changes in the carrying amount of financial assets are recognised in the

consolidated income statement, distinguishing between those arising from the accrual of interest

and similar items -which are recognised under “Interest and Similar Income”- and those arising for

other reasons, which are recognised at their net amount under “Gains/Losses on Financial Assets

and Liabilities” in the consolidated income statement.

However, changes in the carrying amount of instruments included under “Available-for-Sale

Financial Assets” are recognised temporarily in equity under “Valuation Adjustments”, unless they

relate to exchange differences. The amounts included in “Valuation Adjustments” remain in equity

until the related assets are derecognised, whereupon they are charged to the consolidated income

statement.

In fair value hedges, the gains and losses arising on the financial assets designated as hedging

instruments and hedged items attributable to the type of risk being hedged are recognised

directly in the consolidated income statement.

In fair value portfolio hedges of interest rate risk, the gains or losses that arise on measuring the

hedging instruments are recognised directly in the consolidated income statement, whereas the

gains or losses due to changes in the fair value of the hedged amount -attributable to the hedged

risk- are recognised in the consolidated income statement with a balancing entry under “Changes

in the Fair Value of Hedged Items in Portfolio Hedges of Interest Rate Risk”.

21Bankinter Group

l

f

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 21

B

Financial liabilitiesFinancial liabilities are classified in the consolidated balance sheet as follows:

i) Financial liabilities held for trading: this category includes the financial liabilities acquired for

the purpose of realising them in the near term. They form part of a portfolio of identified financial

instruments that are managed together and for which there is evidence of a recent pattern of

short-term profit taking, they are financial derivatives not designated as hedging instruments and

financial liabilities arising from the outright sale of financial assets purchased under reverse

repurchase agreements or borrowed.

ii) Financial liabilities at amortised cost: this category relates to financial liabilities not included in

any of the other balance sheet categories which arise from the ordinary deposit-taking activities

carried on by financial institutions, irrespective of their instrumentation and maturity.

iii) Hedging derivatives: this category includes the financial derivatives acquired or issued by the

Group which qualify for hedge accounting.

iv) Equity having the substance of a financial liability: amount of the financial instruments issued by

the Entity that, although equity for legal purposes, do not meet the requirements for classification as

equity. These instruments relate basically to issued shares that do not carry voting rights and whose

yield is established on the basis of a fixed or floating interest rate. These instruments are measured

as financial liabilities at amortised cost unless the Group has designated them as financial liabilities

at fair value provided that the required conditions are met.

Financial liabilities are measured at amortised cost, as defined for financial assets, except in the

following cases:

i) The financial liabilities included under “Financial Liabilities Held for Trading” are measured at

fair value, as defined for financial assets. Financial liabilities hedged in fair value hedges are

adjusted and changes in fair value with respect to the risk being hedged are recognised.

ii) Financial derivatives that have as their underlying asset equity instruments whose fair value

cannot be determined in a sufficiently objective manner and are settled by delivery of those

instruments, are measured at cost.

As a general rule, changes in the carrying amount of financial liabilities are recognised in the

consolidated income statement. A distinction is made between the changes resulting from the accrual

of interest and similar items -which are recognised under “Interest Expense and Similar Charges”- and

those arising for other reasons -which are recorded at their net amount under “Gains or Losses on

Financial Assets and Liabilities” in the consolidated income statement.

Bankinter Group 22

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 22

The gains or losses arising on financial liabilities designated as hedged items or as hedging

instruments are recognised as stated for financial assets.

(e) Recognition of income and expensesAs a general rule, interest income, interest expenses and similar items are recognised on the basis

of their period of accrual using the effective interest method. Dividends received from other

companies are recognised as income when the right to receive them arises.

Fees and commissions paid or received for financial services, however denominated contractually,

are classified in the following categories, which determine their recognition in the consolidated

income statement:

i) Financial fees and commissions, which are those that are an integral part of the effective yield or

cost of a financial transaction and are recognised in the income statement over the expected life of

the financing as an adjustment to the effective yield or cost of the transaction. They include loan

origination and analysis fees, fees on credit overlimits and fees on deposit overdrafts.

ii) Non-financial fees and commissions, which are those arising from the provision of services and

may arise from the provision of a service over a period of time and from the rendering of a service

in a single act.

Fee and commission income and expenses are generally recognised in the consolidated income

statement as follows:

i) Those relating to financial assets and financial liabilities measured at fair value through profit or

loss are recognised when paid.

ii) Those arising from transactions or services that are provided over a period of time are

recognised over the life of these transactions or services.

iii) Those relating to a transaction or service performed in a single act are recognised when the

single act is carried out.

Non-finance income and expenses are recognised for accounting purposes on an accrual basis.

Deferred collections and payments (over periods longer than a year) are recognised for accounting

purposes at the amount resulting from discounting the expected cash flows at market rates.

23Bankinter Group

l

d

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 23

B

(f) Impairment of financial assetsThe carrying amount of a financial asset is generally adjusted with a charge to the income

statement when there is objective evidence of an impairment loss, which occurs when:

i) In the case of debt instruments, i.e. loans and debt securities, after their initial recognition a

single event or the combined effect of several events causes a negative impact on their future cash

flows

ii) In the case of equity instruments, after their initial recognition a single event or the combined

effect of several events means that their carrying amount cannot be fully recovered.

As a general rule, the carrying amount of impaired financial instruments is adjusted with a charge

to the consolidated income statement for the period in which the impairment becomes evident,

and the reversal of previously recognised impairment losses, if any, is recognised in the

consolidated income statement for the period in which the impairment is reversed or reduced.

When the recovery of any recognised impairment is considered unlikely, the amount of the

impairment is derecognised, without prejudice to any actions that the Group may initiate to seek

collection of the amount receivable until their contractual rights are extinguished by expiry of the

statute-of-limitations period, forgiveness or any other cause.

The amount of an impairment loss incurred on a debt instrument measured at amortised cost is

equal to the difference between its carrying amount and the present value of its estimated future

cash flows. For quoted instruments, instead of the present value of future cash flows, market value

may be used provided that it is sufficiently reliable to consider it as representative of the amount

that might be recovered by the Group.

The estimated future cash flows of a debt instrument are all the principal and interest amounts

that the Group considers will flow to it over the life of the instrument. Its estimate takes into

account all relevant information available on the date when the financial statements are

authorised for issue about the likelihood of collecting the contractual cash flows in the future.

The future cash flows of a collateralised instrument are estimated by taking into account the flows

that would result from foreclosure less costs for obtaining and subsequently selling the collateral,

whether or not foreclosure is probable.

The discount rate used to calculate the present value of the estimated future cash flows is the

instrument's original effective interest rate, if its contractual rate is fixed, or the effective interest

rate at the reporting date determined under the contract, if it is floating.

Bankinter Group 24

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 24

Debt instrument portfolios, contingent liabilities and contingent commitments, irrespective of the

holder, instrumentation or guarantee, are reviewed so as to determine the credit risk to which the

Group is exposed and to consider whether an impairment allowance is required. In the preparation

of the consolidated financial statements, the Group classified its transactions on the basis of the

inherent credit risk and assessed separately the insolvency risk attributable to customers and the

country risk to which the transactions are exposed.

The objective evidence of impairment is determined individually for all debt instruments that are

individually significant, and individually or collectively for the groups of debt instruments which

are not individually significant. When a specific instrument cannot be included in any group of

assets with similar credit risk characteristics, it is analysed solely on an individual basis to

determine whether it is impaired and, if so, to estimate the impairment loss.

Collective assessment of a group of financial assets to estimate impairment losses is carried out as

follows:

i) Debt instruments are included in groups with similar credit risk characteristics that are indicative

of the debtors' ability to pay all amounts due, both principal and interest, according to the

contractual terms. The credit risk characteristics to be taken into account for grouping assets are,

among others: instrument type, debtor's industry, geographical location, type of guarantee or

collateral, age of past-due amounts and any other factor relevant to the estimation of future cash

flows.

ii) The future cash flows from each group of debt instruments are estimated for instruments with

similar credit risk characteristics to those in the respective group, after making the necessary

adjustments to adapt the historical data to current market conditions.

iii) The impairment loss of each group is the difference between the carrying amount of all the

debt instruments in the group and the present value of the estimated future cash flows.

Debt instruments not measured at fair value through profit or loss, and contingent liabilities and

contingent commitments are classified, on the basis of insolvency risk attributable to the customer

or to the transaction, in one of the following categories: standard, substandard, doubtful due to

customer arrears, doubtful for reasons other than customer arrears and write-off. The specific

impairment allowances are estimated for debt instruments not classified as standard risk, taking

into account the age of past-due amounts, the guarantees provided and the economic situation of

the customer and, where appropriate, of the guarantors. This estimate is generally performed on the

basis of the default schedules.

25Bankinter Group

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 25

B

In addition to the specific impairment allowances mentioned above, the Group recognised an

overall impairment allowance for inherent losses on debt instruments not measured at fair value

through profit or loss and on contingent liabilities classified as standard risk.

In this connection, the Bank of Spain determines the parameters, methods and amounts to be used

to cover the inherent impairment losses incurred in debt instruments and contingent liabilities

classified as standard risk.

The calculation method established in Annex IX of Bank of Spain Circular 4/2004 is divided into

two stages.

At the first stage, balances are classified into the six risk classes defined in the Circular, namely

negligible risk, low risk, medium-low risk, medium risk, medium-high risk and high risk.

The impaired charge is the sum of

a) the products of the change during the period in the balance of each risk class and the related

regulatory α parameter, plus

b) the sum of the products of the total balance of the transactions included in each risk class at the

end of the period and the related regulatory β parameter, less

c) the amount of the overall net impairment charges for the relevant specific allowances or

provisions made in the period.

The overall balance of this general allowance or provision must at all times be between 33% and

125% of the sum of the products obtained by multiplying the amount of each risk class by its

related α parameter. The balance at the Group at 31 December 2006 and 2005 related to the

maximum ratio.

Parameters α and β, for each risk class, are as follows:

Bankinter Group 26

α β

Negligible risk 0% 0%

Low risk 0.6% 0.11%

Medium-low risk 1.5% 0.44%

Medium risk 1.8% 0.65%

Medium-high risk 2.0% 1.10%

High risk 2.5% 1.64%

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 26

The recognition of interest accrual under the contractual terms in the consolidated income

statement is suspended for debt instruments individually classified as impaired and for the

instruments for which impairment losses have been assessed collectively because they have

payments more than three months past due.

The amount of the impairment losses on debt instruments and equity instruments included under

“Available-for-Sale Financial Assets” is the positive difference between their acquisition cost, net of

any principal repayment or amortisation, and their fair value less any impairment loss previously

recognised in the consolidated income statement.

When there is objective evidence that the decline in fair value is due to impairment, the unrealised

losses recognised directly in consolidated equity under “Valuation Adjustments” are recognised

immediately in the consolidated income statement. If all or part of the impairment losses are

subsequently reversed, the reversed amount is recognised in the consolidated income statement for

the year in which the reversal occurred, in the case of debt instruments, and under “Valuation

Adjustments” in consolidated equity in the case of equity instruments.

The impairment loss on equity instruments measured at cost is the difference between the carrying

amount and the present value of the expected future cash flows discounted at the market rate of

return for similar securities. Impairment losses are recognised in the consolidated income

statement for the period in which they arise as a direct reduction of the cost of the financial asset.

These losses can only be reversed subsequently in the case of the sale of the related asset.

The impairment losses on investments in jointly controlled entities and associates are estimated by

comparing their recoverable amount with their carrying amount. Impairment losses are recognised

in the income statement for the period in which they occur; subsequent reversals are recognised in

the income statement for the period in which the impairment losses are reversed.

(g) Financial derivativesFinancial derivatives are instruments which, in addition to providing a profit or loss, may permit

the offset, under certain conditions, of all or a portion of the credit and/or market risks associated

with balances and transactions, using interest rates, certain indices, equity prices, cross-currency

exchange rates or other similar benchmarks as underlyings. The Group uses financial derivatives

traded on organised markets or traded bilaterally with the counterparty outside organised markets

(OTC derivatives) both for proprietary transactions and for transactions with the wholesale or retail

customer segment.

27Bankinter Group

d

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 27

B

The Group takes positions in derivatives for the purpose of arranging hedges, actively managing

other financial assets and liabilities or benefiting from price changes. Financial derivatives that do

not qualify for hedge accounting are classified as trading derivatives.

Derivatives with an active market are measured at the quoted prices in such markets.

Derivatives with no market or with an inactive market are measured using the most consistent and

appropriate economic methods, maximising the use of observable data and other factors that

market participants would take into account, such as: a) recent transactions involving other

instruments that are substantially equal, b) discounting of cash flows and c) market option pricing

models. The valuation techniques are preferably those used by market participants and have been

demonstrated to provide the most realistic estimate of the instrument's price.

All financial derivatives are initially recognised at fair value. In the case of financial swaps the fair

value is assumed to be zero, unless the Group demonstrates otherwise using appropriate valuation

techniques. In this case, the initial recognition of fair value generates a profit or loss that must be

recognised in the income statement when all the variables of the model stem exclusively from

observable market data, giving rise to the so-called “day-one profits”. Based on a prudential

supervisory ruling issued by the Bank of Spain at the request of the Bank, the Board of Directors

decided to apply an alternative criteria consisting of the recognition of the aforementioned “day-

one profits” on a straight-line basis over the life of the swaps giving rise to them.

A derivative may be designated as a hedging instrument only if it meets the following criteria:

i) It qualifies in its entirety as a hedging instrument, even when only a percentage of its total

amount is such, except that in the case of options it is permitted to designate as the hedging

instrument the change in their intrinsic value, excluding changes in their time value, and in the

case of forward contracts it is permitted to designate as the hedging instrument the difference

between the spot and forward prices of the underlying asset.

ii) It is designated as a hedge for its total remaining term to maturity.

iii) If more than one risk is hedged, the different hedged risks can be clearly identified, each part

of the instrument can be designated as a hedge of specific hedged items and the effectiveness of

the various hedges can be demonstrated.

Bankinter Group 28

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 28

The hedge effectiveness of hedging derivatives is duly documented through effectiveness analysis,

which is the tool that evidences that the differences arising from changes in market prices between

the hedged item and the hedging instrument remain at reasonable parameters over the term of the

transactions, in line with the estimates made at the trade date.

If this is not the case at any time, the associated transactions in the hedging group would be

treated as trading derivatives and would be duly reclassified in the balance sheet.

The hedges entered into by the Group are classified as fair value hedges:

� Micro-hedges or individual hedges (in which hedged items and hedging instruments are

specifically identified) hedge the exposure to changes in the fair value of the hedged item.

The profit or loss arising in measuring the hedging instruments and the hedged items is

recognised immediately in the consolidated income statement.

� Portfolio hedges (hedges of interest rate risk in a portfolio of financial instruments) hedge

the exposure to changes in the fair value of the hedged amount in response to changes in the

hedged interest rate. The profit or loss arising from measuring hedging instruments is

recognised immediately in the consolidated income statement. In the case of the hedged

amount, the profit or loss arising on measurement is recognised directly in the income

statement with a charge or credit, as appropriate, to the asset or liability item “Changes in the

Fair Value of Hedged Items in Portfolio Hedges of Interest Rate Risk” depending on whether the

hedged amount relates to financial assets or financial liabilities, respectively.

(h) Transfers and derecognition of financial instrumentsThe accounting treatment of transfers of financial instruments depends on the extent to which the

risks and rewards associated with the transferred financial instruments are transferred:

i) If the Group transfers substantially all the risks and rewards to third parties -unconditional sale,

sale under an agreement to repurchase at fair value at the repurchase date, sale of financial assets

with a purchased call option or written put option that is deeply out of the money, securitisation of

assets in which the transferor does not retain a subordinated debt or grant any credit

enhancement to new holders, etc.-, the transferred financial instrument is derecognised and any

right or obligation retained or created in the transfer is recognised simultaneously.

29Bankinter Group

d

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 29

B

ii) If the Group retains substantially all the risks and rewards associated with the transferred

financial instrument -sale of financial assets under an agreement to repurchase them for a fixed

price or the sale price plus interest, a securities lending agreement in which the borrower

undertakes to return the same or similar assets, etc.-, the transferred financial instrument is not

derecognised and continues to be measured by the same criteria used before the transfer. However,

an associated financial liability is recognised for an amount equal to the consideration received.

This liability is subsequently measured at amortised cost. The income from the transferred

financial asset not derecognised and any expense incurred on the new financial liability are

recognised in the consolidated income statement.

iii) If the Group neither transfers nor retains substantially all the risks and rewards associated with

the transferred financial asset -sale of financial assets with a purchased call option or written put

option that is not deeply in or out of the money, securitisation of assets in which the transferor

retains a subordinated debt or other type of credit enhancement for a portion of the transferred

asset, etc.-, the following distinction must be made:

� If the Group does not retain control, the transferred financial instrument is derecognised and

any right or obligation retained or created in the transfer is recognised.

� If the Group retains control, it continues to recognise the transferred financial instrument in

the balance sheet for an amount equal to its exposure to changes in value and recognises a

financial liability associated with the transferred financial asset. The net carrying amount of

the transferred asset and of the associated liability is the amortised cost of the rights and

obligations retained, if the transferred asset is measured at amortised cost, or the fair value of

the rights and obligations retained, if the transferred asset is measured at fair value.

Accordingly, financial assets are only derecognised when the rights on the cash flows they

generate have expired or when substantially all the inherent risks and rewards have been

transferred to third parties. Similarly, financial liabilities are only derecognised when the

obligations they generate have expired or when they are acquired with the intention either to

cancel them or to re-place them.

(i) Tangible assetsTangible assets are presented at acquisition cost, revalued pursuant to certain legal provisions and

also as permitted in the transition to the new accounting standards, less the related accumulated

depreciation and any impairment losses.

The acquisition cost of foreclosed assets is the carrying amount of the financial assets settled

through foreclosure.

Bankinter Group 30

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 30

Depreciation is calculated by the straight-line or the sum-of-the-years'-digits method by applying

the years of estimated useful life of the various items to the acquisition cost of the assets less their

residual value. The land on which the buildings and other structures stand has an indefinite life

and, therefore, is not depreciated. The tangible asset depreciation charge is recognised in the

consolidated income statement and is calculated on the basis of the years of estimated useful life,

which are basically the same as the minimum legal periods:

Depreciation Method

Buildings Straight-line over 50 years

Furniture, fixtures and other Straight-line over 6 to 12 years

Computer hardware Sum-of-the-years'-digits or shifts

The Group reviews the depreciation period and method of each tangible asset at least at the end of

the reporting period.

Upkeep and maintenance expenses that do not enhance the utilisation or lengthen the useful life

of the respective assets are charged to the consolidated income statement when and as they are

incurred.

At the reporting date the Group assesses whether there is any internal or external indication that

an asset may be impaired (i.e. its carrying amount exceeds its recoverable amount). If this is the

case, the Group reduces the carrying amount of the asset to its recoverable amount and adjusts

future depreciation charges in proportion to the revised carrying amount and to the new remaining

useful life (if the useful life has to be re-estimated). Similarly, if there is an indication of a recovery

in the value of a tangible asset, the Group recognises the reversal of the impairment loss

recognised in prior periods and adjusts the future depreciation charges accordingly. In no

circumstances may the reversal of an impairment loss on an asset raise its carrying amount above

that which it would have if no impairment losses had been recognised in prior years.

(j) Intangible assetsIntangible assets are identifiable non-monetary assets without physical substance. Intangible

assets are deemed to be identifiable when they are separable from other assets because they can

be sold, rented or otherwise disposed of individually, or when they arise from contractual or other

legal rights. An intangible asset is recognised when, in addition to meeting the above definition,

the Group considers it probable that economic benefits will flow from the asset and the cost of the

asset can be measured reliably.

31Bankinter Group

,

h

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 31

B

Intangible assets are recognised initially at acquisition or production cost and are subsequently

measured at cost less any accumulated amortisation and any impairment losses.

The Group recognises any impairment loss on the carrying amount of these assets with a charge to

the consolidated income statement. The criteria used to recognise the impairment losses on these

assets and, where applicable, the reversal of impairment losses recognised in prior years are

similar to those used for tangible assets.

(k) LeasesLease contracts are presented in the consolidated financial statements on the basis of the economic

substance of the transaction regardless of its legal form and are classified from inception as

finance or operating leases.

i) A lease is classified as a finance lease when it transfers substantially all the risks and rewards

incidental to ownership of the asset forming the subject-matter of the contract.

When the Group acts as lessor of an asset, the sum of the present value of the lease payments

receivable from the lessee plus the guaranteed residual value -which is generally the exercise price

of the purchase option of the lessee at the end of the lease term- is recognised as lending to third

parties and is therefore included, based on the type of lessee, under “Loans and Receivables” in the

consolidated balance sheet.

When the Group acts as lessee, it presents the cost of the leased assets in the consolidated balance

sheet according to the nature of the asset forming the subject-matter of the contract and,

simultaneously, recognises a liability for the same amount (which is the lower of the fair value of

the leased asset and the sum of the present value of the lease payments to be made to the lessor

plus, if appropriate, the exercise price of the purchase option). The depreciation policy for these

assets is consistent with that for property, plant and equipment for own use.

The finance income and finance expense arising from these contracts is credited or debited,

respectively, to the consolidated income statement so as to achieve a constant rate of return over

the life of the lease contracts.

ii) Leases other than finance leases are classified as operating leases.

When the Group acts as lessor, it presents the acquisition cost of the leased assets under “Tangible

Assets”. The depreciation policy for these assets is consistent with that for similar tangible assets

for own use and income from operating leases is recognised on a straight-line basis in the

consolidated income statement.

Bankinter Group 32

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 32

When the Group acts as lessee, the lease expenses, including any incentives granted by the lessor,

are recognised on a straight-line basis in the consolidated income statement.

(l) Non-current assets held for saleNon-current assets held for sale are assets whose carrying amount is expected to be recovered

mainly through sale and that are available for immediate sale and their sale is considered to be

highly probable.

Non-current assets held for sale are measured at the lower of fair value less costs to sell and their

carrying amount. These assets are not depreciated.

Impairment losses are recognised under “Impairment Losses - Non-Current Assets Held for Sale” in

the consolidated income statement. The reversals of impairment losses are recognised in the

consolidated income statement up to an amount equal to the impairment losses previously

recognised.

Foreclosed assets are measured at the lower of their fair value less costs to sell and their carrying

amount. Impairment losses, which are calculated individually for assets that remain on the balance

sheet for a period longer than initially envisaged for their sale, are recognised under “Impairment

Losses - Non-Current Assets Held for Sale” in the consolidated income statement.

(m) OffsettingAsset and liability balances arising from transactions which, contractually or as a result of a legally

enforceable right, envisage the possibility of offsetting and the Group intends to settle them on a

net basis, or to realise the asset and pay the liability simultaneously, are recognised in the

consolidated balance sheet at their net amount.

(n) Securities lent or pledged as collateralSecurities lending is defined as a transaction in which the borrower receives full title to securities

without making any payment except fees and commissions, with the commitment to return to the

lender others of the same class as those received.

Securities lending agreements in which the borrower undertakes to return the same or

substantially the same assets or other similar ones having the same fair value are deemed to be

transactions in which the lender retains substantially all the risks and rewards incidental to

ownership.

(o) Financial guaranteesFinancial guarantees are defined as contracts whereby the Group undertakes to make specific

payments for a third party if the latter does not do so, irrespective of the various legal forms they may

have, such as guarantees, irrevocable documentary credits issued or confirmed by the Group, etc.

33Bankinter Group

c

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 33

B

Financial guarantees are recognised under “Accrued Expenses and Deferred Income” at their fair

value which, on initial recognition and in the absence of evidence to the contrary, is the present

value of the cash flows to be received, using an interest rate similar to that of the financial assets

granted by the entity with a similar term and risk. Simultaneously, the present value of the future

cash flows receivable using the aforementioned interest rate is recognised under “Other Financial

Assets”.

Subsequently, the value of contracts recognised under “Other Financial Assets” is discounted by

recording the differences in the consolidated income statement as interest income. The fair value

of guarantees recognised under “Accrued Expenses and Deferred Income” is allocated to the

consolidated income statement as income from commissions received, on a straight-line basis over

the expected life of the guarantee, or by another method provided that it more adequately

reflects the economic risks and rewards of the guarantee.

Financial guarantees are classified on the basis of the insolvency risk allocable to the customer or

to the transactions and, if appropriate, the need for provisions is assessed by application of criteria

similar to those indicated in Note 5-f) for debt instruments measured at amortised cost.

If a provision for financial guarantees is required, the unearned commissions recognised under

“Accrued Expenses and Deferred Income” on the liability side of the consolidated balance sheet are

reclassified to the appropriate provision.

(p) Personnel expenses

Post-employment benefitsPost-employment benefits are employee compensation that is payable after completion of

employment. All post-employment obligations, including those covered by internal or external

pension funds are classified as defined contribution plans or defined benefit plans based on the

terms and conditions of those obligations, taking into account all commitments made, whether

within or outside the terms formally agreed with employees.

The Group recognises the contribution to be made to insurance entities at the amount of the

insurance premiums paid under “Personnel Expenses” in the consolidated income statement.

Irrevocable post-employment commitments to senior management are recognised over the

estimated total period of service by senior management to the Entity.

Equity-instrument-based employee remunerationThe accrued portion of the market value of the implicit options at the grant date relating to

outstanding issues of convertible debentures for Group employees (Note 19-e) is recognised as a

personnel expense with a credit to “Other Equity Instruments” in consolidated equity until the

options expire or are cancelled early.

Bankinter Group 34

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 34

As the Group carries out capital increases to cater for the conversion of debentures into shares over

the term of the convertible debenture issues, the item “Other Equity Instruments” is converted into

“Share Premium”.

In the event of non-compliance with the internal conditions established by the Group for the

conversion of debentures into shares, the accumulated amount recognised in equity in this

connection is reversed with a credit to the consolidated income statement.

The personnel expenses referred to in this section do not entail the receipt of any remuneration

or right by employees, since convertible debenture issues are financial transactions in which

employees can participate voluntarily, bear the risks of the transaction and forfeit the conversion

right if they leave the Group for any reason.

Multi-year incentive plansThe amount of the payments under the multi-year executive incentive plans is recognised under

“Personnel Expenses” on an accrual basis.

(q) Other provisions and contingenciesThe Group recognises provisions for the estimated amount required to meet present obligations

arising from past events whose nature is clearly specified but whose amount or settlement date is

uncertain and that the Group expects to settle through an outflow of resources embodying

economic benefits. These obligations may arise from:

� A legal or contractual requirement.

� An implicit or tacit obligation arising from valid expectations created by the Group to third

parties regarding the assumption of certain types of responsibilities. Such expectations are

created when the Group publicly accepts responsibilities, or derive from past practice or from

publicly known business policies.

� Virtual certainty as to the future course of regulation in particular respects, especially

proposed new legislation that the Group cannot avoid.

Contingent liabilities are possible obligations of the Group that arise from past events and whose

existence is conditional on the occurrence or non-occurrence of one or more future events beyond

the control of the Group. They include the present obligations of the Group when it is not probable

that an outflow of resources embodying economic benefits will be required to settle them or when,

in extremely rare cases, their amount cannot be measured with sufficient reliability.

35Bankinter Group

LEGAL GRUPO ingles.qxd 13/6/07 08:44 Página 35

B

Provisions and contingent liabilities are classified as probable when it is more likely than not that

they will occur; as possible when it is more likely than not that they will not occur; and as remote

when it is extremely rare that they should occur.

The Group's consolidated financial statements include all the material provisions with respect to

which it is considered that it is more likely than not that the obligation will have to be settled.

Contingent liabilities are not recognised in the consolidated financial statements, but rather

information thereon is disclosed unless the possibility of an outflow of resources embodying

economic benefits is remote.

Provisions are quantified on the basis of the best information available on the consequences of the

event giving rise to them and are estimated at each reporting date taking into account the

financial effect, if it is material. Provisions are used to cater for the specific obligations for which

they were originally recognised and are fully or partially reversed when such obligations cease to

exist.

At 31 December 2006 and 2005, certain litigation and claims were in process against the Group

arising from the ordinary course of its operations. The Group's legal advisers and the directors of

the Bank consider that the outcome of such litigation and claims will not have a material effect, in

addition to that included as a provision, on the consolidated financial statements.

(r) Insurance contractsIn accordance with standard accounting practice in the insurance sector, insurance entities credit to

the income statement the amounts of the premiums written and charge to income the cost of the

claims incurred on final settlement thereof. Also, insurance entities are required to accrue at year-

end the unearned premiums written credited to their income statements and the expected costs for

claims not charged to the income statement.

The most significant liabilities recorded by insurance entities in relation to direct insurance

contracts arranged by them relate to the following technical provisions: provisions for unearned

premiums, provisions for unexpired risks, provisions for claims outstanding, mathematical

provisions, provisions for life assurance policies where the investment risk is borne by the

policyholders and provisions for bonuses and rebates. The technical provisions to cater for claims

arising from direct insurance contracts are recognised in the accompanying consolidated balance

sheets under “Liabilities under Insurance Contracts”.

“Reinsurance Assets” includes the amounts that the entities are entitled to receive for reinsurance

contracts with third parties. They are calculated on the basis of the reinsurance contracts entered