51

Macro Economic and Industry Analysis Dr. Himanshu Joshi

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | evan-mcdaniel |

| View: | 228 times |

| Download: | 1 times |

Macro Economic and Industry Analysis

Dr. Himanshu Joshi

• Fundamental Analysis• Approach to Fundamental Analysis:– Domestic and global economic analysis– Industry analysis– Company analysis

• Why use the top-down approach?

Framework of Analysis

• Performance in countries and regions is highly variable

• Political risk• Exchange rate risk– Sales– Profits– Stock returns

Global Economic Considerations

Table 17.1 Economic Performance in Selected Emerging Markets

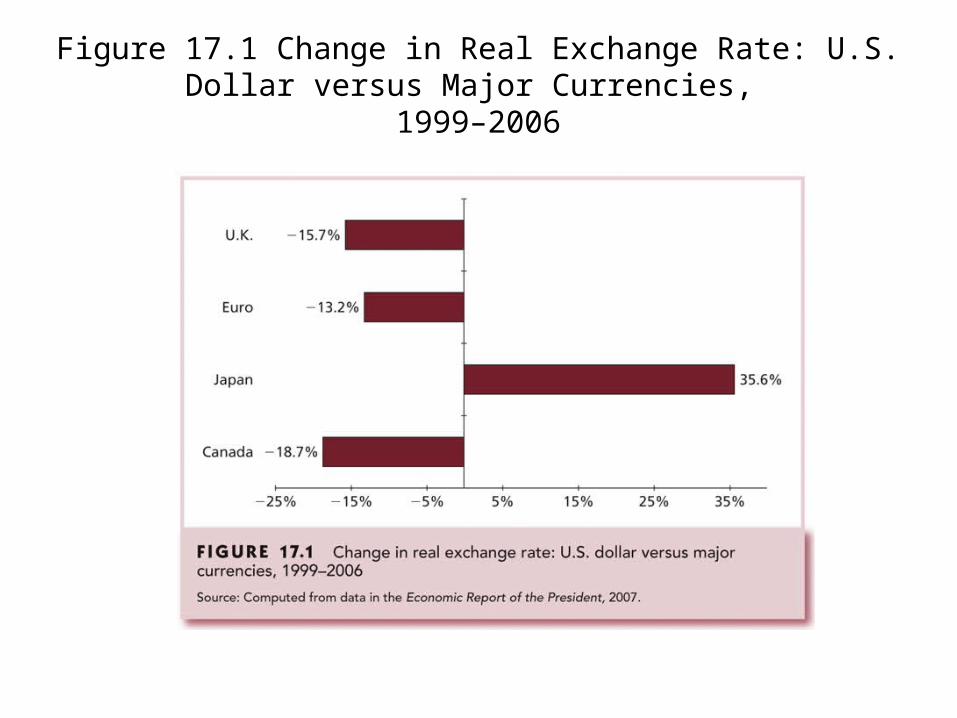

Figure 17.1 Change in Real Exchange Rate: U.S. Dollar versus Major Currencies, 1999–2006

• Gross domestic product• Unemployment rates• Interest rates & inflation• Budget deficit• Consumer sentiment

Key Economic Variables

• Demand shock - an event that affects demand for goods and services in the economy

Demand Shocks

• Supply shock - an event that influences production capacity or production costs

Supply Shocks

Federal Government Policy

• Fiscal Policy: Demand-side management– Tax rate cut– Increases in government spending

Federal Government Policy Continued

• Monetary Policy - Demand-side management–Manipulation of the money supply to influence

economic activity• Initial & feedback effects• Tools of monetary policy–Open market operations–Discount rate–Reserve requirements

11

Definition “Groupthink” - a type of thought exhibited by group members who try to minimize conflict and reach consensus without critically testing, analyzing, and evaluating ideas.

Individual creativity, uniqueness, and independent thinking are lost in the pursuit of group cohesiveness, as are the advantages of reasonable balance in choice and thought that might normally be obtained by making decisions as a group.

Groupthink may cause groups to make hasty, irrational decisions, where individual doubts are set aside, for fear of upsetting the group’s balance.

12

Action Learning: Contrarian Thinking. Ask yourself, at the present time:

·What are the prevailing common assumptions about local and world markets?

What are the implications, if some or all of these assumptions are wrong by 180 degrees (i.e. if the precise opposite is true)?

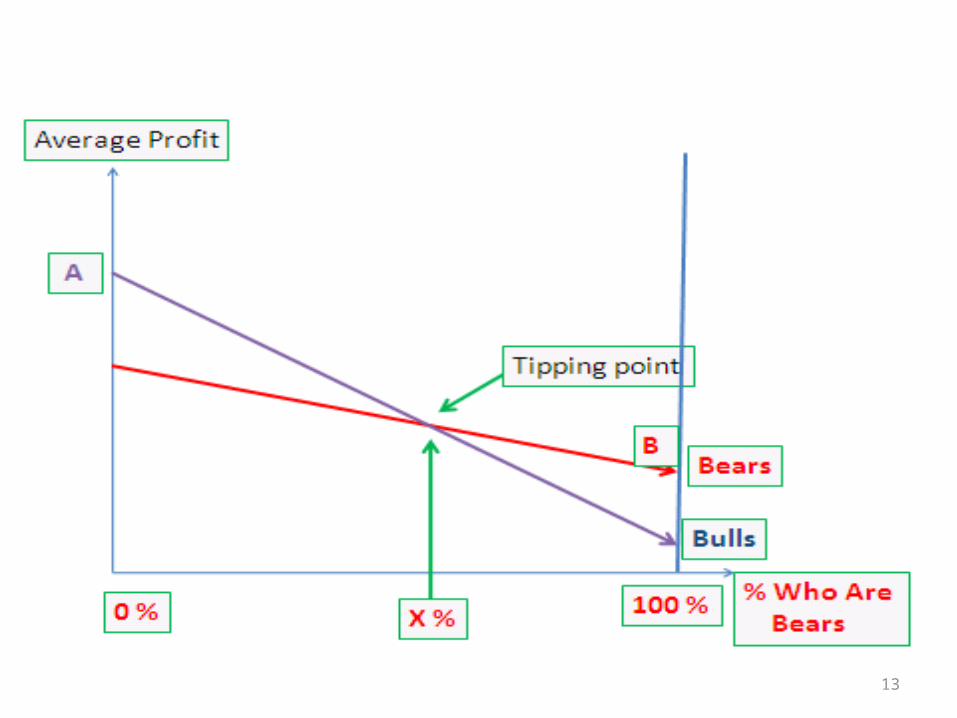

13

Tipping Point (critical mass): When More than X% Become ‘Bears’

14

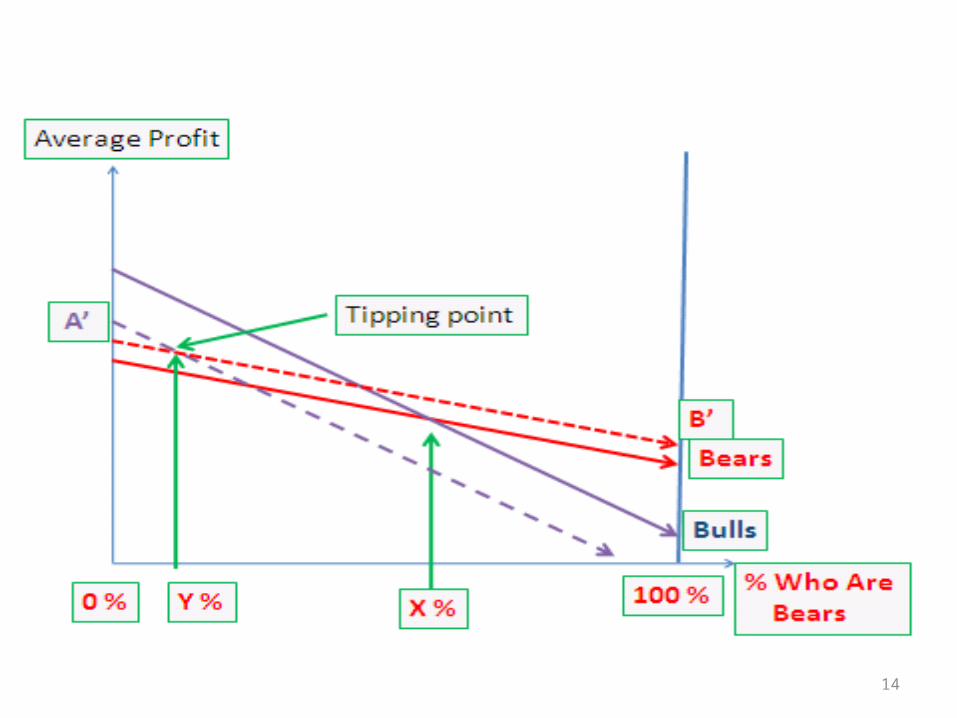

Tipping Point (critical mass): Pessimism is Self-Fulfilling

15

Analyst? Or Strategist?

Ask yourself, are you primarily an analyst? Or a strategist?

Definition: Analyst: An employee of a brokerage or fund management firm who studies companies and makes buy and sell recommendations on stocks of these companies. Strategist: Those who weigh broad market sentiment and macroeconomic factors in order to assess the overall business environment , as an aid to those building buy and sell recommendations.

Action Learning..

• Chicken, Cow and Grass• Which of the three does not belong?• Western thinking: logical, seeks causal links

and categories.• Eastern Thinking: holistic, systematic and seek

relationships.

Case..• In US, the recession has reduced consumer spending on toys.

Many of the world’s toys are made in china. So Chinese factories have greatly slashed their production.

• Cardboard is major component of toys. So china’s import of recycled paper has declined.

• Britain is a major world supplier of recycled paper. The reason is that Britain is the world’s largest consumer of paper products, importing 7.6 million tons out of its 12.5 million tons of paper consumption in 2005.

• Britain has therefore lots of paper to recycle, and has a well organized recycling system.

• The price of recycled paper once as high as USD 144/ton, dropped drastically in 2008, falling to USD 22/ton. At that price, it does not pay to collect the waste paper.

• A profitable business model was shredded.

18

The Teleology That Created A Market Leader

Jorma Olilla, while vacationing in southern France in Nov. 1989, observed the Fall of the Berlin Wall.He reasoned:· the fall of the Wall will quickly cause the two Germany’s to unite, · this, in turn, will hasten European unification, and the single European Market in turn, the European Single Market will need, above, all, communication, communication will require mobile phones, because of difficulties in integrating national land-line systems.

19

Fall of the Berlin Wall9.11.1989

Unification of East and West Germany

Creation of EuropeanSingle Market

Need for Europe-wide communication

EstablishNokia Mobile

Mobile speedsSingle Market

20

GELT – Geopolitics, Economics, Lifestyle, Technology.

G - Geopolitics: Instabilities and changes resulting from political trends, in various regions and countries in the world.

E - Economics: Economic trends, including exchange rates, economic growth, trade, exports, finance, interest rates, capital flows.

L - Lifestyle: Sociology, the way people live, social trends, cohort effects (differing values across age groups.

T – technology: Technology trends, new technologies, new basic science that can lead to new technologies.

21

Impact

Timing (years)

0 1 2 3 4 5

GBerlin Wall Falls;Germany reunited

EEuropean Single Markethastened

LNeed for Europe-wideCommunication

TBuild CellularTechnology

22

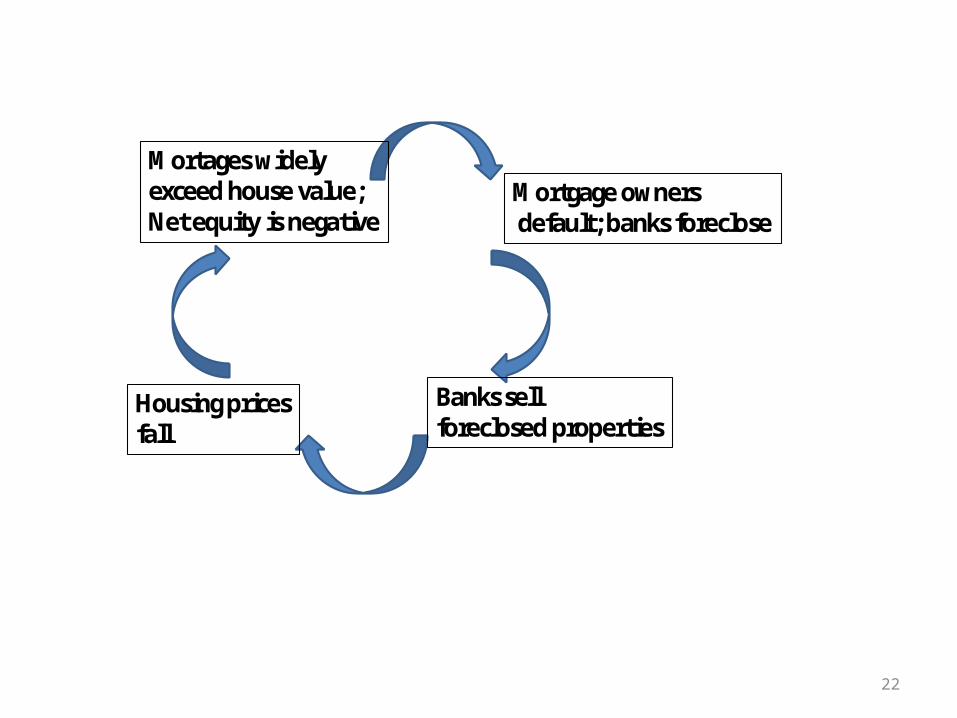

Housing pricesfall

Mortages widelyexceed house value;Net equity is negative

Mortgage ownersdefault; banks foreclose

Banks sellforeclosed properties

23

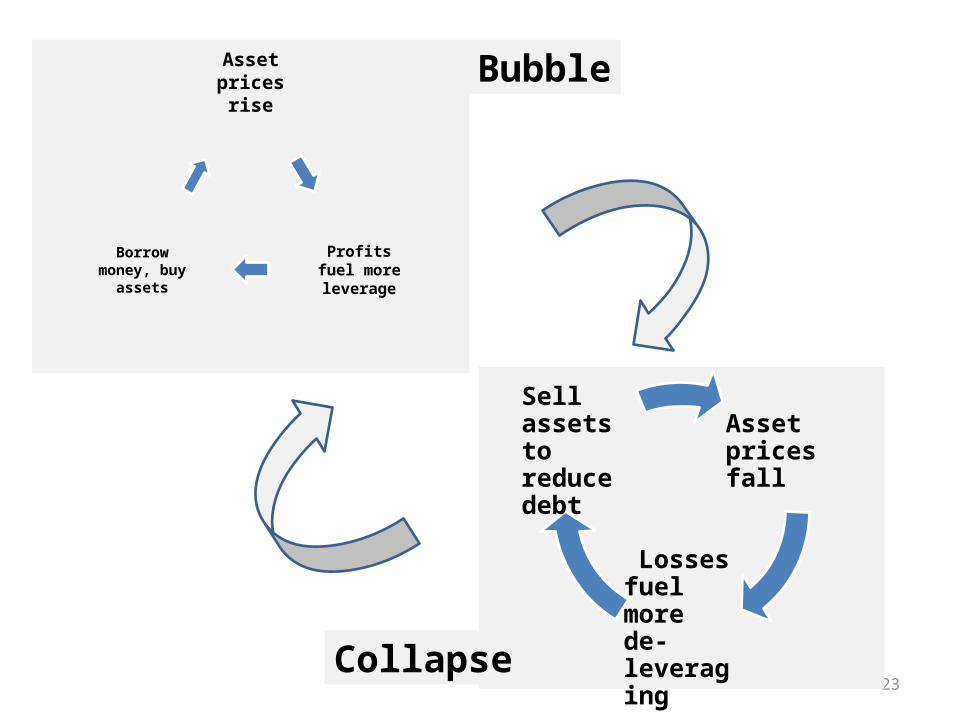

Asset prices rise

Profits fuel more leverage

Borrow money,

buy assets

Asset prices fall

Losses fuel more de-leveraging

Sell assets to reduce debt

Bubble

Collapse

Action Learing:Linking two events..

• 2000 dot.com burst.• 2007-09 subprime Crisis.• Can you explain the two events?• Can you link the two events?

25

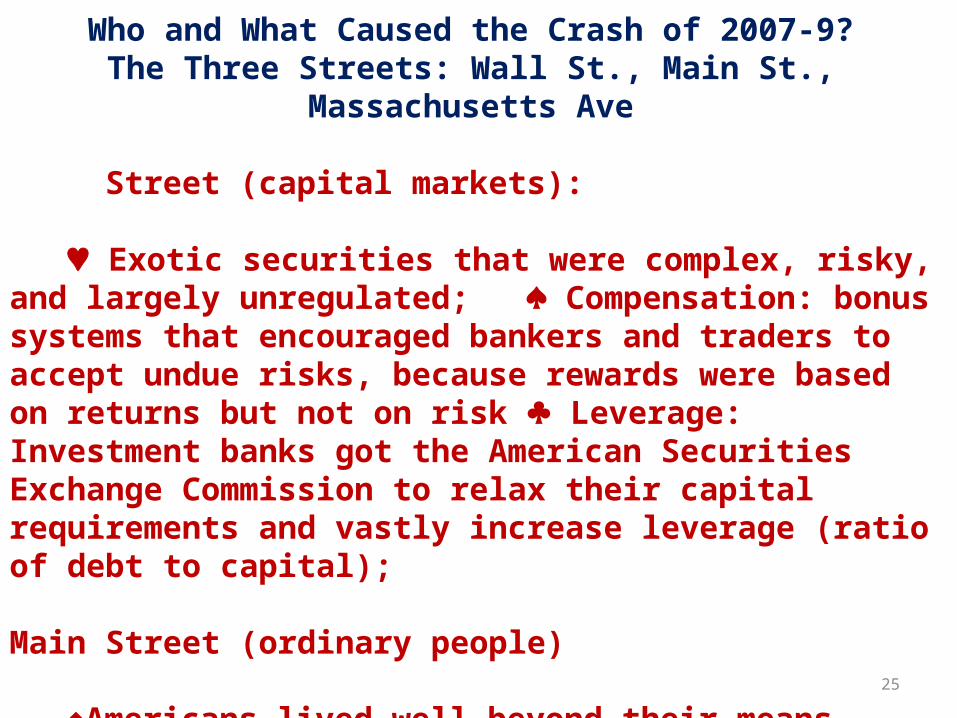

Who and What Caused the Crash of 2007-9?The Three Streets: Wall St., Main St., Massachusetts Ave

Wall Street (capital markets):

Exotic securities that were complex, risky, and largely unregulated; ♠ Compensation: bonus systems that encouraged bankers and traders to accept undue risks, because rewards were based on returns but not on risk ♣ Leverage: Investment banks got the American Securities Exchange Commission to relax their capital requirements and vastly increase leverage (ratio of debt to capital); Main Street (ordinary people)

Americans lived well beyond their means, overspent and overborrowed; ♣ small and midsized banks overlent to builders; ♠ greedy homeowners used inflated home prices to borrow and spend;

26

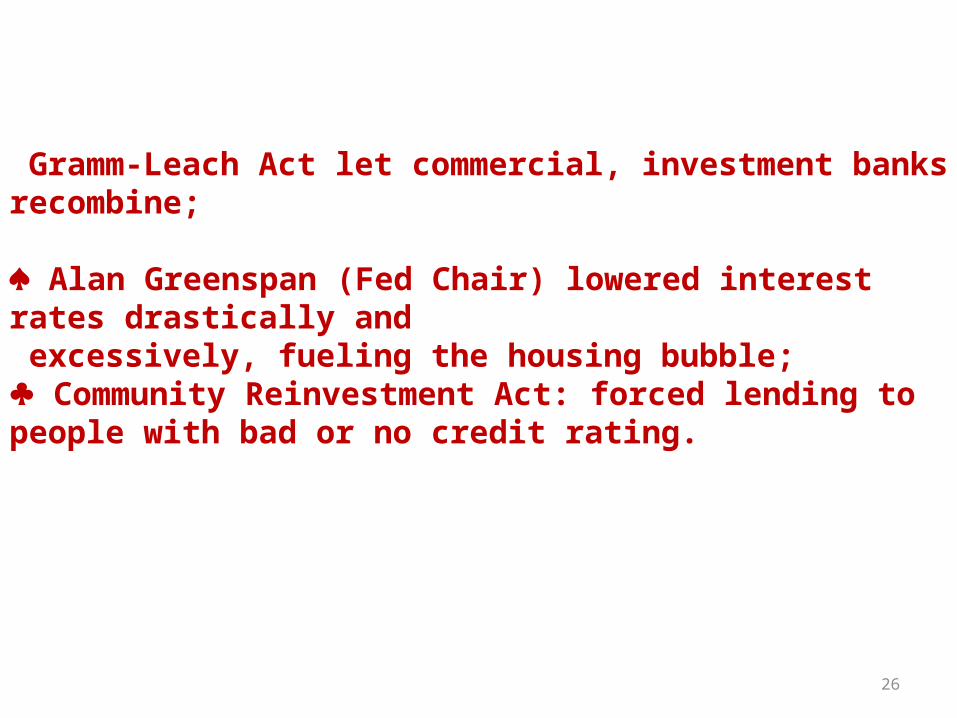

Massachusetts Ave. (Federal government)

Gramm-Leach Act let commercial, investment banks recombine;

♠ Alan Greenspan (Fed Chair) lowered interest rates drastically and excessively, fueling the housing bubble;

♣ Community Reinvestment Act: forced lending to people with bad or no credit rating.

Business Cycles

• The transition points across cycles are called peaks and troughs– A peak is the transition from the end of an

expansion to the start of a contraction– A trough occurs at the bottom of a recession

just as the economy enters a recovery

It is worthwhile to remark that a product is no sooner created than it, from that instant, affords a market for other products to the full extent of its own value. When the producer has put the finishing hand to his product, he is most anxious to sell it immediately, lest its value should diminish in his hands. Nor is he less anxious to dispose of the money he may get for it; for the value of money is also perishable. But the only way of getting rid of money is in the purchase of some product or other. Thus the mere circumstance of creation of one product immediately opens a vent for other products.

J.B. Say, 1803. A Treatise on Political Economy, or the production, distribution and consumption of wealth, 1803 (Engl. transl.) p.138-9)

J.B. Say’s “Law of Markets”

28

Definitions: Business cycles are short-term fluctuations in GDP and unemployment—cycles of recession, recovery, growth and again recession, around a long-term growth trend, over periods of about four to eight years. They involve shifts between periods of relatively rapid growth (expansion, or boom) and periods of relative stagnation or decline (contraction, recession, or bust). Trends are long-term movements in GDP, prices, income and employment, with consistent direction and nature, over the course of a decade or more. Recession: Once defined as "two consecutive quarters of decline in real GDP", the most recent authoritative definition is: "a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales". Source: National Bureau of Economic Research, www.nber.org Downturn: Loosely-used phrase referring to the contraction phase of the boom-bust cycle. A downturn can mean either an actual decline in real GDP (as occurred in the U.S., Europe and Japan, in 2009) or a significant slowdown in the rate of growth of GDP (as occurred in China, in 2009). Depression: A prolonged severe economic contraction that lasts longer than a typical recession and that afflicts economies in many parts of the world; a global economic contraction. Inflation: a general and progressive increase in prices, often occurring during the 'boom' part of the business cycle. Deflation: a general and progressive decrease in prices, often occurring during the 'bust' part of the cycle. 29

Figure 17.3 Cyclical Indicators

• Leading indicators tend to rise and fall in advance of the economy

• Examples:– Avg. weekly hours of production workers– Stock Prices

Leading Indicators

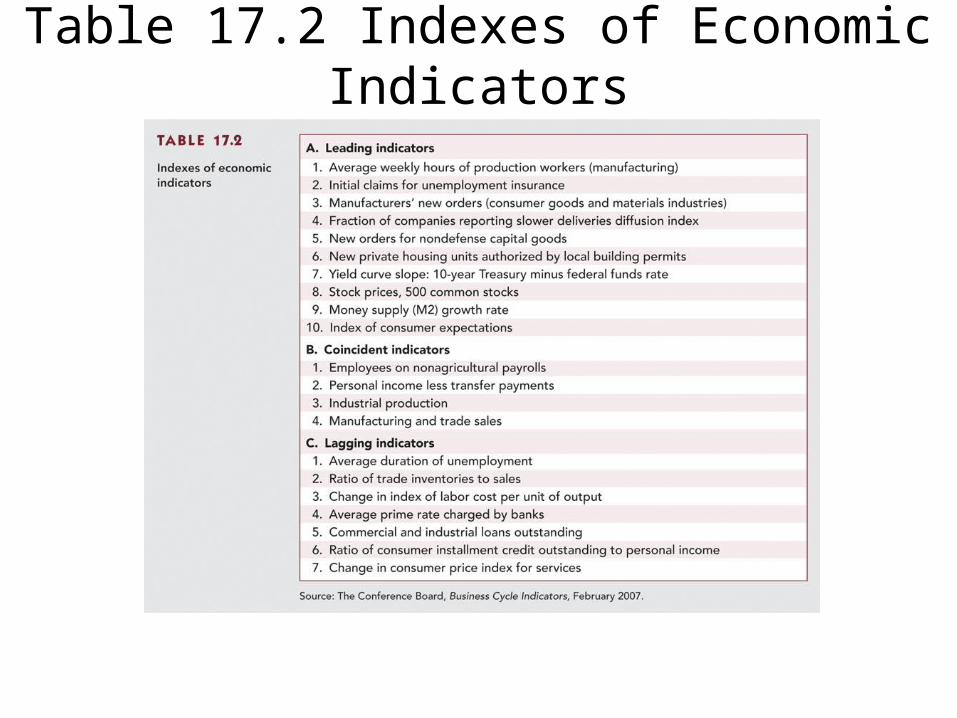

Table 17.2 Indexes of Economic Indicators

• Coincident Indicators - indicators that tend to change directly with the economy

• Examples:– Industrial production–Manufacturing and trade sales

Coincident Indicators

• Lagging Indicators - indicators that tend to follow the lag economic performance

• Examples:– Ratio of trade inventories to sales– Ratio of consumer installment credit

outstanding to personal income

Lagging Indicators

Figure 17.4 Indexes of Leading, Coincident, and Lagging Indicators

Business cycle Theories Government policy: It is sometimes argued that government policy itself exacerbates, or even causes, rather than mitigates, business cycles. Politics: Related to stop-go is the so-called 'political cycle'. Democracies have elections every four years or so. In the two years prior to the election governments stimulate the economy, creating a boom, in order to be elected or re-elected. In the two years after it, they brake the economy, creating a bust, to resolve the problems created during the boom. Cyclical responses to initial shocks: This theory, due to J.M. Keynes and expanded by M.I.T. Professor Paul Samuelson, shows how the complex interaction between consumers (personal consumption) and businesses (investment) can create cycles. "Real business cycles": External 'innovation' shocks occur, as new technologies replace old ones, and economies decline, then boom, as investment pauses and then accelerates. In this theory, business cycles are not a sign of inefficiency or market failure but rather a sign of rejuvenation, implying that governments should not try to intervene or 'smooth' the cycle. Marx: Capital accumulation causes profit rates to fall, leading businesses to merge and create monopolies, to reduce wages, leading to economic crisis. Credit cycles: In boom times, banks overlend, businesses and people overborrow, as interest rates fall and real (inflation-adjusted) rates may become negative. When borrowing halts, as a result of over-leverage, investment slows, asset prices decline and the economy dives into recession. 36

Action learning: Four Question Framework

* Do people have money and are they optimistic and keen to spend it? Or are they concerned about debt and pessimistic about losing their jobs?

* Are businesses making profits and are they keen to reinvest them, in creating new assets (buildings, machineries, equipment, software)?

* Do governments have money and are they keen to spend it, beyond what they absorb in tax revenues?

* Are businesses selling more abroad to other nations than is being bought from abroad, i.e. do exports exceed (or fall short of) imports, and is the gap widening or shrinking?

37

Animal Spirits as a Cause of Business Cycles

In Keynes' landmark 1936 book The General Theory, which struggled to explain the Great Depression then afflicting the major economies of the world, there is the following passage:

…There is instability due to the characteristic of human nature that a large proportion of our positive activities depend on spontaneous optimism rather than mathematical expectations… Our decisions to do something positive…can only be taken as the result of animal spirits - a spontaneous urge to action rather than inaction…

J.M. Keynes. The General Theory of Employment, Interest and Money. London: Macmillan, 1936, pp. 161-2.

38

39

Action Learning: Gauging Animal Spirits

Do you regularly engage in informal

conversations? Do you cross-check by matching survey data with your own observations? Can you acquire a sense of 'animal spirits' through these conversations? Some excellent sources of such data are: taxi drivers (taxis are sensitive to the business cycle, because people walk or take public transportation when their incomes decline); restaurants (also sensitive to business conditions); shopping malls (are they crowded, and are people carrying packages, or simply window-shopping?).

Industry Analysis

• Sensitivity to business cycles• Factors affecting sensitivity of earnings to

business cycles:– Sensitivity of sales of the firm’s product to the

business cycles– Operating leverage– Financial leverage

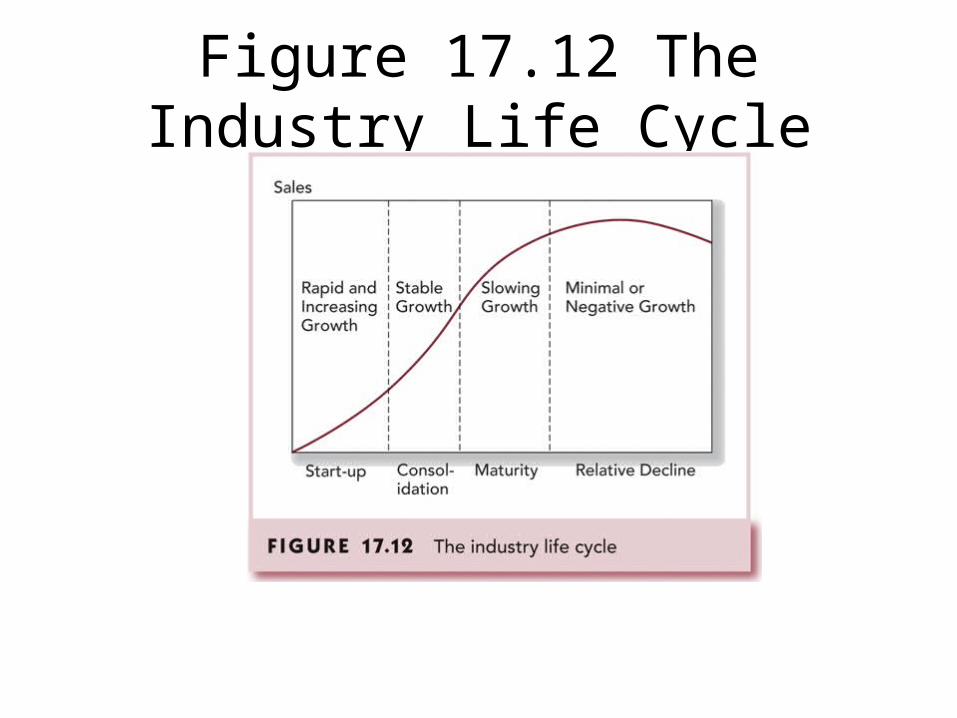

• Industry life cycles

Figure 17.6 Return on Equity, 2007

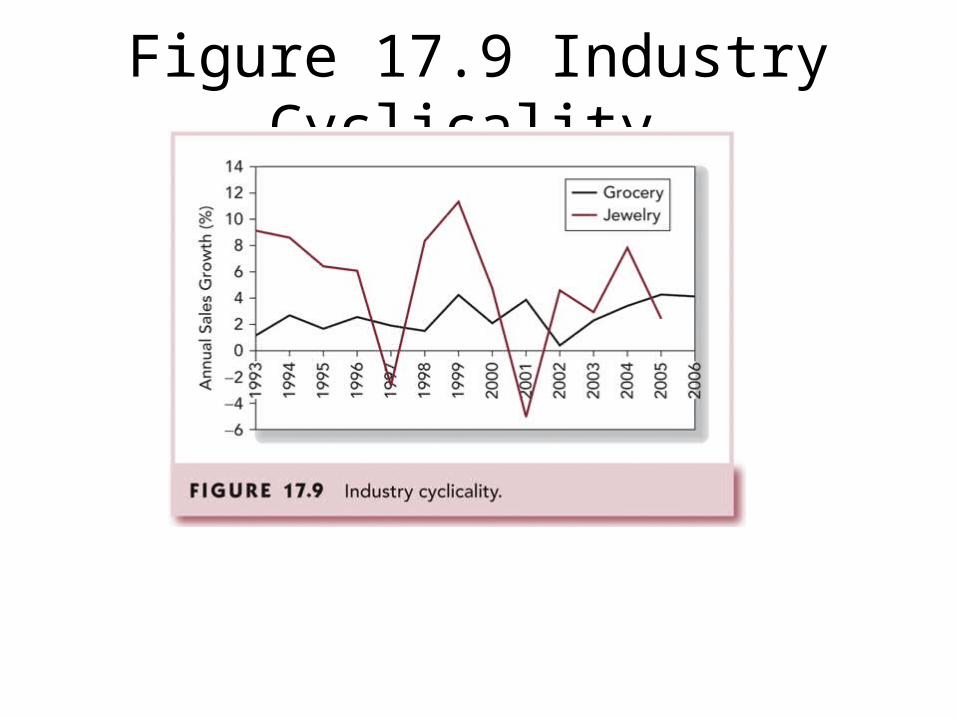

Figure 17.9 Industry Cyclicality

Table 17.6 Operating Leverage of Firms A and B Throughout the Business Cycle

Figure 17.10 A Stylized Depiction of the Business Cycle

Sector Rotation

• Portfolio is adjusted by selecting companies that should perform well for the stage of the business cycle– Peaks – natural resource extraction firms– Contraction – defensive industries such as

pharmaceuticals and food– Trough – capital goods industries– Expansion – cyclical industries such as consumer

durables

Figure 17.11 Sector Rotation

Stage Sales GrowthStart-up Rapid & IncreasingConsolidation StableMaturity SlowingRelative Decline Minimal or Negative

Industry Life Cycles

Figure 17.12 The Industry Life Cycle

Industry Structure and Performance

• Threat of entry• Rivalry between existing competitors• Pressure from substitute products• Bargaining power of buyers• Bargaining power of suppliers

50

Figure 7.6. Price – Earnings Ratio for Standard & Poor 500 Index (U.S.) 1900 - 2009

51

Fig. 7.6. Company value (1994 = 100%): Fundamental value andExpectation premium, 1994 and 2000